Abstract

The private rented sector (PRS) recently enjoyed a revival, in particular in the years before and after the Great Financial Crisis (GFC). At the same time however, affordability concerns have come to the fore. The main aim of this paper is to explain trends in housing affordability for lower-income households in the PRS across Western European countries, from a supply versus demand perspective. To this end we: (1) related trends in housing affordability to wider changes in housing systems, welfare regimes, demographic indicators and housing market financialisation; and (2) decomposed affordability trends in terms of rents and incomes, controlling for compositional shifts. We incorporated the spatial dimension by distinguishing between urban and rural regions. Although we could not explicitly test for the more fine-grained mechanisms relating housing market financialisation to increased ‘unaffordability’ of PRS-housing, our findings nevertheless warrant future research into this topic. In particular in countries with strong financialisation (Ireland, the Netherlands, Spain and Portugal) decreasing affordability arises from the fact that during the period 1995–2007 private rent increases were not compensated for sufficiently by income growth. We furthermore found that across urban regions, between 1995 and 2007, affordability worsened through demand pressure arising from in-migration. Changes after the GFC (up to 2013) were more limited and diverse.

Introduction

The private rented sector (PRS) recently enjoyed a revival: across Western Europe a century-long decline has either stalled or turned into significant increases, in particular in the years before and after the Great Financial Crisis (GFC). At the same time and somewhat counter-intuitive given increased supply, affordability concerns – particularly in the PRS – have come to the fore (The Foundation Abbé Pierre and FEANTSA, 2017; Pittini et al., 2015; Salvi del Pero et al., 2016). Declining affordability was already apparent in the years before the GFC, and has been linked to trends increasing demand for PRS-housing: house price inflation (limiting access to homeownership for younger and poorer households); 1 the shift of public support for lower-income households away from social housing to housing allowances; and societal changes (e.g. demographic trends, labour market flexibilisation, income inequality) restricting households’ access to mortgages and/or increasing attractiveness of more flexible housing arrangements. These problems are likely to have intensified following the GFC, given increases in unemployment and employment insecurity, combined with austerity measures and welfare reform. In many countries, housing affordability problems in the PRS are (far) more severe compared with other tenures (e.g. Dewilde and De Decker, 2016).

Comparative research into the PRS is hampered by differences in meanings and practices, rooted in diverse regulatory and policy environments. Definitions of ‘private renting’ and characteristics of private renters are influenced by a range of interrelated dimensions, such as ownership (individuals, companies, other organisations), owners’ objectives (profit-making through rental income streams or capital gains) and financing and governance (e.g. subsidies and taxation; rent regulation) (for an overview, see Crook and Kemp, 2014). For instance, in countries with (residual) small social housing sectors, the PRS houses more lower-income and disadvantaged households (e.g. immigrants). PRS-dynamics – the mobility of dwellings and households in and out of the sector – are furthermore affected by developments in the wider housing market and political economy (Kemp, 2015). The secular increase in homeownership before the GFC was partly realised by the ‘filtering up’ of (private) rental dwellings and renters into owner-occupied houses and homeowners. In some countries, e.g. the United Kingdom (UK) and Ireland, this trend reversed as homeownership rates declined and wealthy (outright, older) homeowners started to actively invest in additional rental property in order to safeguard retirement income (Kemp, 2010; Ronald et al., 2015). Most of this ‘new’ PRS-stock however originates from the homeownership segment, e.g. through inheritance or buy-to-let (Crook and Kemp, 2014). In Germany, strong increases in PRS-stock since the 1990s arose from the privatisation of public housing associated with the termination of subsidy arrangements (e.g. Kemp and Kofner, 2010; Wijburg and Aalbers, 2017). Notwithstanding the difficulties of comparative research, many scholars implicitly or explicitly analyse PRS-dynamics, in particular affordability, from a supply versus demand perspective.

Changes in the PRS are not only shaped by local trends, but also by broader, international changes (Crook and Kemp, 2014; Kemp, 2015). An emerging body of research explores the potential impact of the ‘financialisation’ of housing and (urban) real estate on the PRS and its inhabitants across different contexts and through various mechanisms and dynamics (e.g. Albrecht and Van Hoofstat, 2011; Desmond, 2012; Fields and Uffer, 2016; Hulse and Yates, 2017; Kemp, 2015; Kitzmann, 2017; Rogers and Koh, 2017; Wijburg and Aalbers, 2017). ‘Financialisation’ is linked with economic globalisation, deregulation and the rise of neo-liberalism, 2 and refers to the transformation of local, tangible assets into liquid, globally tradeable financial commodities, resulting in an increasingly autonomous realm of ‘global finance’ in which profits accrue through financial transactions, rather than trade and commodity production (Fainstein, 2016; van der Zwan, 2014: 103, citing Krippner, 2005). The concept has been broadened to incorporate housing and other real estate (Aalbers and Christophers, 2014; Fernandez and Aalbers, 2016). The ‘financialisation of housing’ refers to ‘structural changes in housing and financial markets and global investment whereby housing is treated as a commodity, a means of accumulating wealth and often as security for financial instruments that are traded and sold on global markets’ (United Nations (UN), 2017: 3).

Empirical research on (housing market) financialisation has so far been mainly concerned with demonstrating its diverse origins and existence as a geographically uneven process (Engelen et al., 2010; Fernandez and Aalbers, 2016; Rogers and Koh, 2017; Wijburg and Aalbers, 2017). Housing market financialisation has also been linked to stratification and inequality. As property is foundational to power and wealth, preferences and incentives for institutions and households are thought to have altered and opportunities for rent extraction increased (Aalbers and Christophers, 2014; Forrest and Hirayama, 2015). Rolnik (2013: 1059) argues that the intensified use of housing as an investment asset ‘has profoundly affected the enjoyment of the right to adequate housing around the world’, resulting in: unaffordability; displacement; evictions; and dwindling housing provision for low-income households by public and private providers (also see UN, 2017). These mostly theoretical claims are supported by qualitative case studies and circumstantial evidence. In this paper, we contribute to the literature by integrating housing market financialisation into the broader explanatory ‘supply versus demand’-framework for PRS-housing, focusing on affordability.

This brings us to the aim of this paper. Notwithstanding the ‘uniqueness’ of each country and differences in meanings and practices, declining affordability of housing for private renters is a common trend across Western European countries. Therefore, the focus of this paper lies not so much with the qualitative ‘reconstruction’ of within-country narratives (even though such studies informed the current research), but rather with a more systematic exploration of between-country variation over time. Our main research question hence concerns the explanation of trends in housing affordability for lower-income households in the PRS across Western European countries. To this end we: (1) relate trends in housing affordability to wider changes in housing systems, welfare regimes, demographic indicators and housing market financialisation; and (2) decompose affordability trends in terms of rents and incomes, controlling for changes in the social composition of lower-income private renters, in order to evaluate the plausibility of empirical associations. We focus on low-income households, as these lack economic and political power and are therefore most vulnerable for changes in housing systems, exogenous changes (e.g. declining wages, unemployment, benefit cuts, immigration), or pressures arising from housing market dynamics caused by such wider trends (Dewilde and Lancee, 2013; Leishman and Rowley, 2012; Rothenberg et al., 1991). We distinguish between urban and rural regions, as: (1) in many countries private renting is an urban affair (Crook and Kemp, 2014); and (2) drivers of demand versus supply, e.g. immigration, often have an urban–rural dimension.

Method, data and indicators

Given the explorative nature of this paper, theory and mechanisms will be discussed throughout the different sections in which trends over time are ‘deconstructed’. As we combine macro-level indicators (see notes to the tables for definitions and sources) with aggregated micro-level data, in particular to analyse trends in affordability problems for low-income private renters over time, we first discuss data and indicators.

We use representative and cross-nationally comparable micro-level data from the European Community Household Panel (ECHP, 1994–2001) and the EU-Statistics on Income and Living Conditions (EU-SILC, 2004–2013) (Dewilde, 2015; Haffner, 2015), for 12 Western European countries: Belgium (BE), Finland (FIN), France (FR), United Kingdom (UK), Ireland (IE), Austria (AT), Germany (DE), the Netherlands (NL), Spain (ES), Greece (GR), Italy (IT) and Portugal (PT). Our focus is on adults and children living in households with a reference person ≤ 60 years of age, as in most countries elderly households – who are more often in social housing or long-term protected tenancies – have remained more shielded from rent increases or income declines. We also exclude individuals in a household with a reference person still at school. While in housing studies the unit of analysis is the dwelling or the household, in research on poverty and inequality the analytical focus is on the individual within the context of her household (e.g. Atkinson et al., 2002). Unless otherwise stated, ‘own calculations’ are based on this sample selection.

Households with an equivalent 3 disposable income 4 in the two bottom quintiles are considered ‘lower income’ (e.g. Milligan, 2003). As the poor are more often living in social housing, the more pressing problems may be located higher up in the income distribution. The 30/40 rule, for instance, is based on the observation that housing affordability problems (defined as housing costs ≥ 30% of disposable income) mainly affect households in the lower 40% (Leishman and Rowley, 2012). Affordability in this paper is defined in terms of the ratio of housing costs to income, but we apply a variable threshold. A fixed threshold (e.g. 30% or 40%) makes the unjustified assumption that the residual income a household needs to cover non-shelter needs is lower as household income decreases. On the other hand, richer households often spend a much higher percentage of their income on housing, while still having sufficient income left (Stone, 2006). When compared with the residual income approach, the ratio-approach defines the situation of lower-income households as too rosy (Heylen and Haffner, 2013). By using a variable threshold, we better accommodate both criticisms. We use a 25% threshold for quintile 1 and a 30% threshold for quintile 2. Housing cost ratios equal to or above the threshold indicate affordability problems.

Differences between ECHP and EU-SILC pertain to the definition of housing costs, and to the measurement of social/private renting in countries with a so-called integrated rental market, where state subsidies are available to all types of providers and strict regulation ensures comparable rents and quality in the public and private sectors. While housing costs in ECHP refer to payable rent for renters and total mortgage costs (principal repayment + interest) for owners, in EU-SILC the main focus is on a concept called ‘total housing costs’, 5 of which the components are not separately available. Utility costs are also included. Because energy is a separate market, driven by other factors such as liberalisation and volatility in world prices, we exclude utility costs. Instead, we use the ‘original’ ECHP-rental cost variable, which is also available in EU-SILC. Amounts are gross of housing allowances (i.e. including housing allowances), but the latter are also included in disposable income. This approach is not equivalent to comparing net housing costs to disposable income net of housing allowances, as it will make affordability outcomes worse in countries that rely more on housing allowances. It does, however, accommodate better for the situation in which housing allowances form a non-identifiable part of other social transfers, e.g. in Germany and Belgium (Haffner, 2015). Our approach is defensible since our main focus is not on comparing ‘absolute’ affordability outcomes between countries, but on decomposing housing affordability trends over time within countries, with a focus on between-country variation in these trends. Our theoretical arguments furthermore pertain to payable rent rather than to net rent.

A second comparability issue concerns the measurement of tenure. Rather than distinguishing between social/public renting and private renting as in ECHP, in EU-SILC ‘renting at market rate’ is distinguished from ‘renting at reduced rate’ (social housing, renting from employer, actual rent fixed by law). Private renters rent their accommodation ‘at prevailing or market rate’, even when the rent is recovered from housing benefits or other sources. However, in some countries with an integrated rental market (Denmark and the Netherlands), where there is no clear distinction between a ‘market rent’ sector and a ‘reduced rent’ sector, all renters are classified in the former category. As our analysis concerns only those in private renting (ECHP) or renting at market rent (EU-SILC), we exclude Denmark. For the Netherlands, private renting in EU-SILC is approximated by reported rents higher than the so-called ‘liberalisation threshold’.

Information on the regional location of households in both data sources is scarce and comparability is problematic. In ECHP, only NUTS1-regions have been recorded. We classified respondents as ‘urban’ (as opposed to ‘rural’) when living in a region with at least 250 inhabitants per km2 or when living in the capital region. In EU-SILC, NUTS2-regions are available, but not for each country. There is however information on the degree of urbanisation. ‘Densely populated’ (at least 1500 inhabitants per km2) and ‘intermediate areas’ (at least 300 inhabitants) are classified as ‘urban’, while ‘thinly populated areas’ are classified as ‘rural’. Different thresholds for both surveys are justified by the fact that NUTS1-regions in ECHP are much larger than areas in EU-SILC (Local Administrative Units). Because of these differences, there is no guarantee that respondents in identical localities will be classified in the same category in ECHP as in EU-SILC. Nevertheless, with our approach we achieve fairly similar per cent of respondents in urban/rural environments in the last wave of ECHP (2001) compared with the first used wave of EU-SILC (2005) (results available). There is no information on regional/spatial location for the Netherlands. For all other countries, we decompose affordability trends of lower-income private renters for ‘urban’ versus ‘rural’ regions.

Our time frame captures the period in which the financialisation of housing markets intensified. For clarity of presentation and because of ‘reversing’ trends in some of our macro-level indicators following the GFC, we focus on three years: 1995 (about 10 years before the culmination of house price inflation), 2007 (right before the GFC) and 2013 (latest available).

Describing trends in housing markets and the PRS

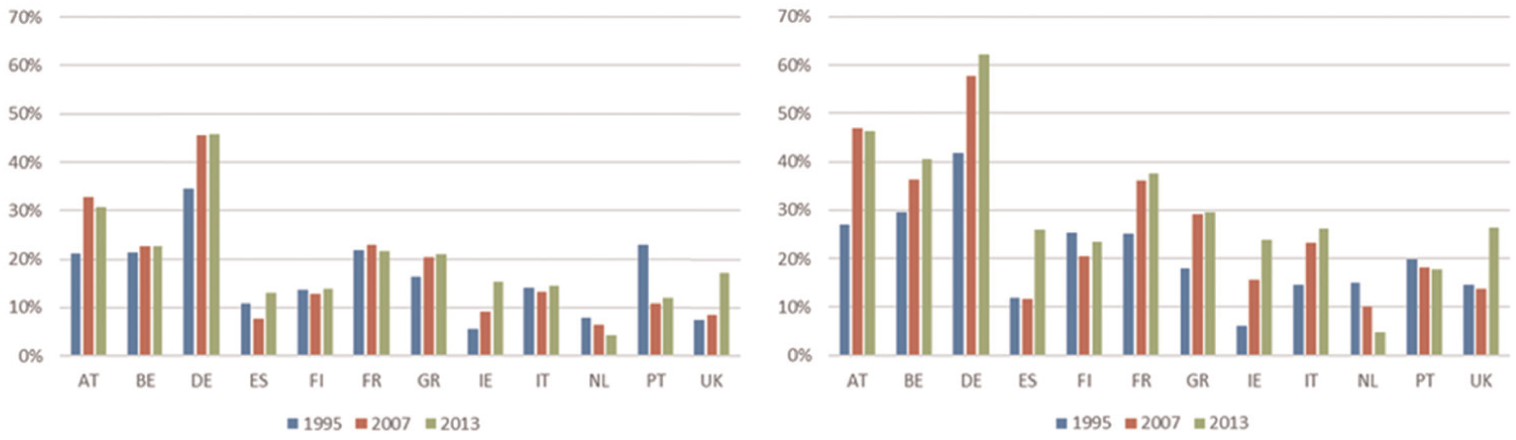

Figure 1 shows the trend in PRS size (see Table 1 for alternative data sources), for all households (left panel) and low-income households (sample selection, right panel). For most countries, PRS growth was already evident in the period 1995–2007, but increases were largest in Germany (11.0%) and Austria (11.7%). The increase in Germany can be explained by a sustained conversion of social into private rentals, although the distinction between both sectors is less clear-cut. 6 Declines were largest in Spain (−3.3%) and especially Portugal (−12.1%), and reflect the expansion of debt-financed homeownership. Trends for low-income households were more outspoken though not identical: increases seem more strongly associated with increasing difficulties of accessing homeownership (e.g. in Greece, France, Ireland, Italy, Belgium). Sector growth continued during the years 2007–2013, but is now larger in countries that were hit harder by the GFC (Whitehead et al., 2014): Ireland, Spain and the UK – with similar but more pronounced trends for low-income households. Overall, a pattern of PRS-growth seems evident.

Per cent of all households (left) and per cent of low-income households (right) in PRS, (ECHP and EU-SILC, own calculations).

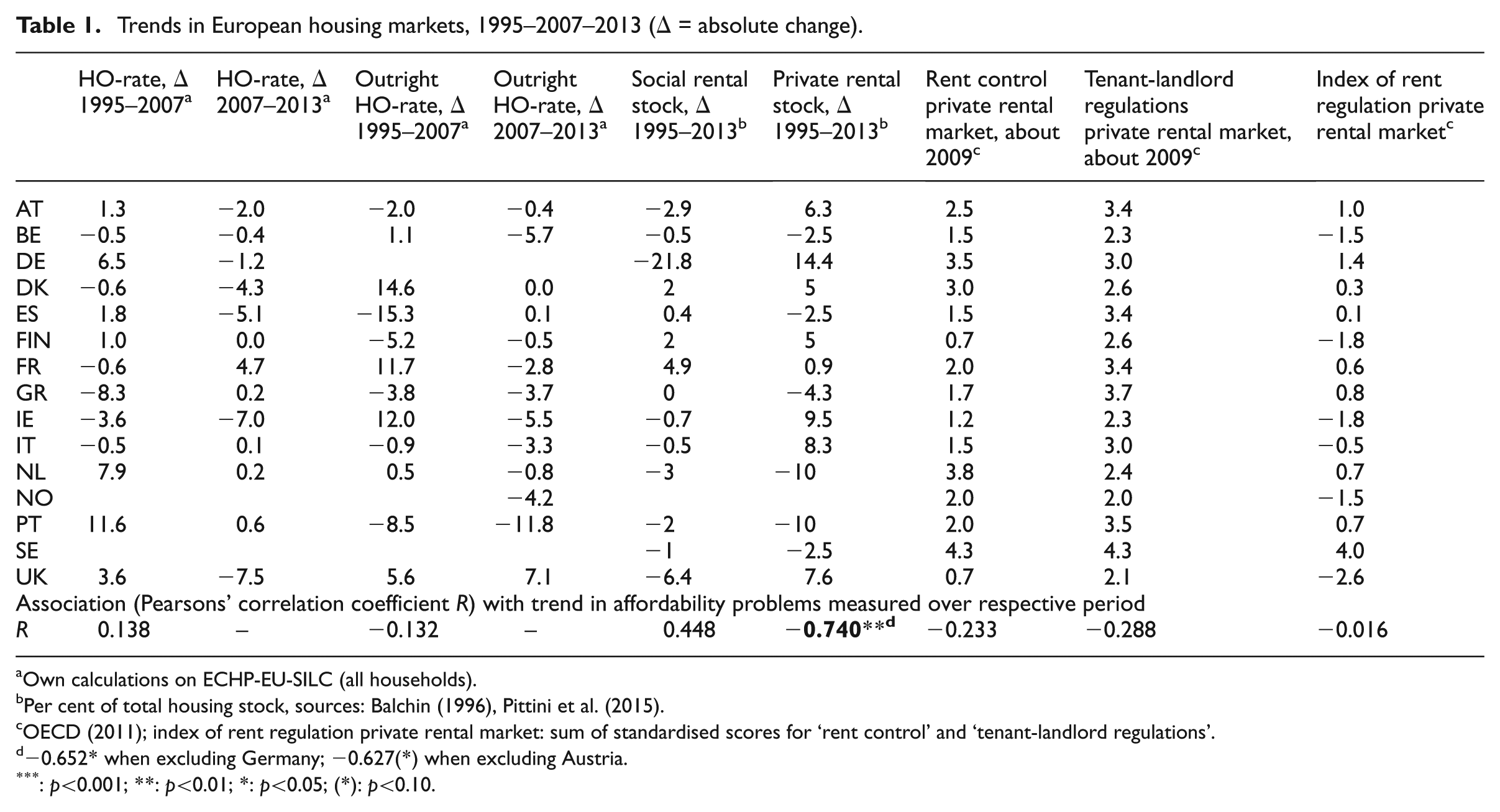

Trends in European housing markets, 1995–2007–2013 (Δ = absolute change).

Own calculations on ECHP-EU-SILC (all households).

Per cent of total housing stock, sources: Balchin (1996), Pittini et al. (2015).

OECD (2011); index of rent regulation private rental market: sum of standardised scores for ‘rent control’ and ‘tenant-landlord regulations’.

−0.652* when excluding Germany; −0.627(*) when excluding Austria.

: p<0.001; **: p<0.01; *: p<0.05; (*): p<0.10.

In Table 1 some further housing market characteristics are presented. From 1995 to 2007, homeownership rates increased in seven countries, but decreased in six; although declines were mostly minimal, except for Ireland (−3.6%) and Greece (−8.3%). After the GFC, there was stabilisation or decline, except for France (+4.7%). There were strong increases in outright homeownership before the crisis in Denmark, France, Ireland and also the UK, and strong decreases in Spain, Portugal and also Finland. Again, there was more stability or decline afterwards, though not in the UK (+7.1%). Except for Germany (−21.8%), the social rental stock has remained fairly stable, but there was an increase in France (+4.9%) and a decrease in the UK (−6.4%).

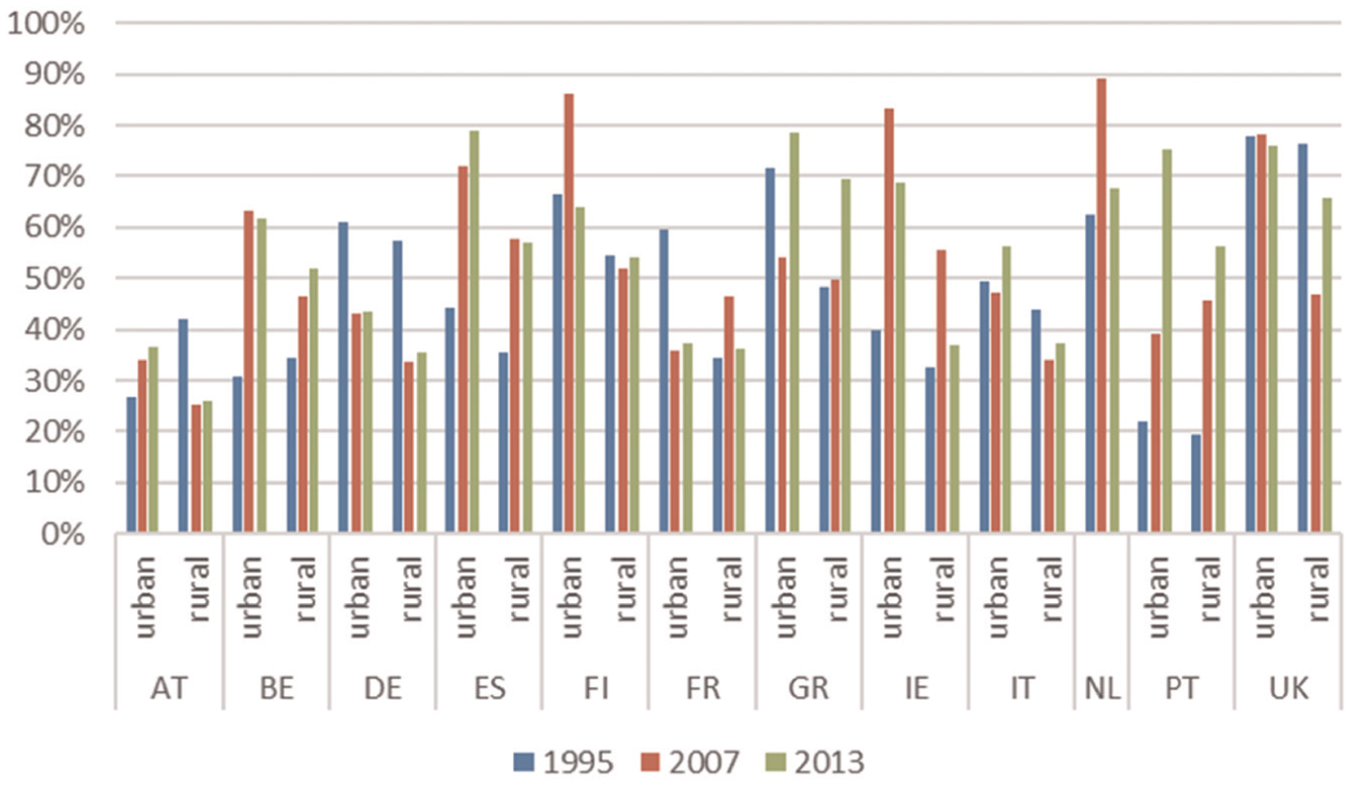

Figure 2 displays the per cent of low-income private renters with housing affordability problems in 1995, 2007 and 2013. In most countries (seven out of 11), trends in housing affordability are fairly comparable for urban versus rural regions. Although experiences before and after the GFC were mixed, in two-thirds of country-regions housing affordability has worsened between 1995 and 2013. Increases were more common in urban settings, while decreases were more common in rural settings. A clear exception is Germany, where housing affordability in both urban and rural regions improved between 1995 and 2007. A tentative explanation is that the ‘added’ private rentals converted from public housing (see earlier) have comparatively lower rents. Also, according to Kitzmann (2017) investment strategies of private equity funds in ownership of portfolios of rental housing (in Berlin) have since the GFC concentrated on rental income streams from low-income households, with rent payments guaranteed by social services. In some countries or regions, lower-income private renters experience a more or less steady increase of housing cost unaffordability over time: this is the case for Belgium, Portugal, Spain, urban Austria and rural Greece. In other settings (rural Finland, Italy, rural UK, urban Greece), housing affordability improved between 1995 and 2007, but suffered following the GFC. Finally, there are some instances whereby housing affordability worsened between 1995 and 2007, but improved after the GFC (urban Finland, rural France, the Netherlands, Ireland).

Per cent of low-income private renters with housing affordability problems (ECHP and EU-SILC, own calculations).

Judging by statistical significance, worsening housing affordability over time is not associated with trends in (outright) homeownership, social rental stock or rent regulation. We do find that – for the whole period 1995–2013 – increases in the private rental stock are significantly associated with decreased affordability problems, also when excluding Germany and Austria. We come back to this later.

Housing systems, welfare regimes and demographic drivers of PRS supply and demand

Although PRS growth seems associated with better affordability ‘across the board’, a number of exceptions necessitate additional explanations. A first explanation is that in many countries, sector growth has been surpassed by increasing demand for PRS housing. Across countries, ‘long-term’ demand for private renting has grown as socio-demographic changes entail an increasing number of lower-income households looking for (temporary) housing (i.e. immigrants, singles, divorced or separated people) (see country chapters in the volume edited by Hulse and Yates, 2017; Crook and Kemp, 2014). Economic and labour market change, combined with welfare state restructuring/retrenchment, resulted in increased income insecurity/decline (in particular at the lower end), compromising long-binding financial contracts such as mortgages. These difficulties were partly overcome by (housing market) financialisation and in particular the liberalisation of mortgage finance, allowing more lower-income households to enter homeownership through easier access to credit and product innovation aimed at lowering the cost of housing finance (Andrews et al., 2011; Crouch, 2009; OECD, 2011; Scanlon et al., 2008) – homeownership rates between 1995 and 2007 were mostly stable or increasing (see Table 1). Following demand pressure and house price inflation however, inequality with regard to access to affordable homeownership increased, affecting those at the fringes. In some countries (e.g. the Netherlands), innovative use of tax subsidisation of homeownership capitalised into real house prices, and because of its regressive nature favoured high-income households to the detriment of housing affordability for young and lower-income entrants (e.g. Salvi del Pero et al., 2016). Research across 11 Western European countries (Dewilde and De Decker, 2016) found that housing market financialisation (measured in terms of increased Residential Mortgage Debt (RMD) to Gross Domestic Product (GDP) ratios) during the years before the GFC was strongly and positively associated with a worsening of affordability for low-income homeowners (without concomitant improvement in other housing conditions). As credit and mortgage requirements tightened following the GFC, demand of lower-income households for PRS housing further increased. This is compounded by welfare reform and housing policy changes inspired by austerity. In some countries (e.g. the UK, Ireland), these factors seem to combine in a ‘perfect storm’ (e.g. Coulter, 2017; Kennett et al., 2013), with PRS growth potentially outpaced by demand.

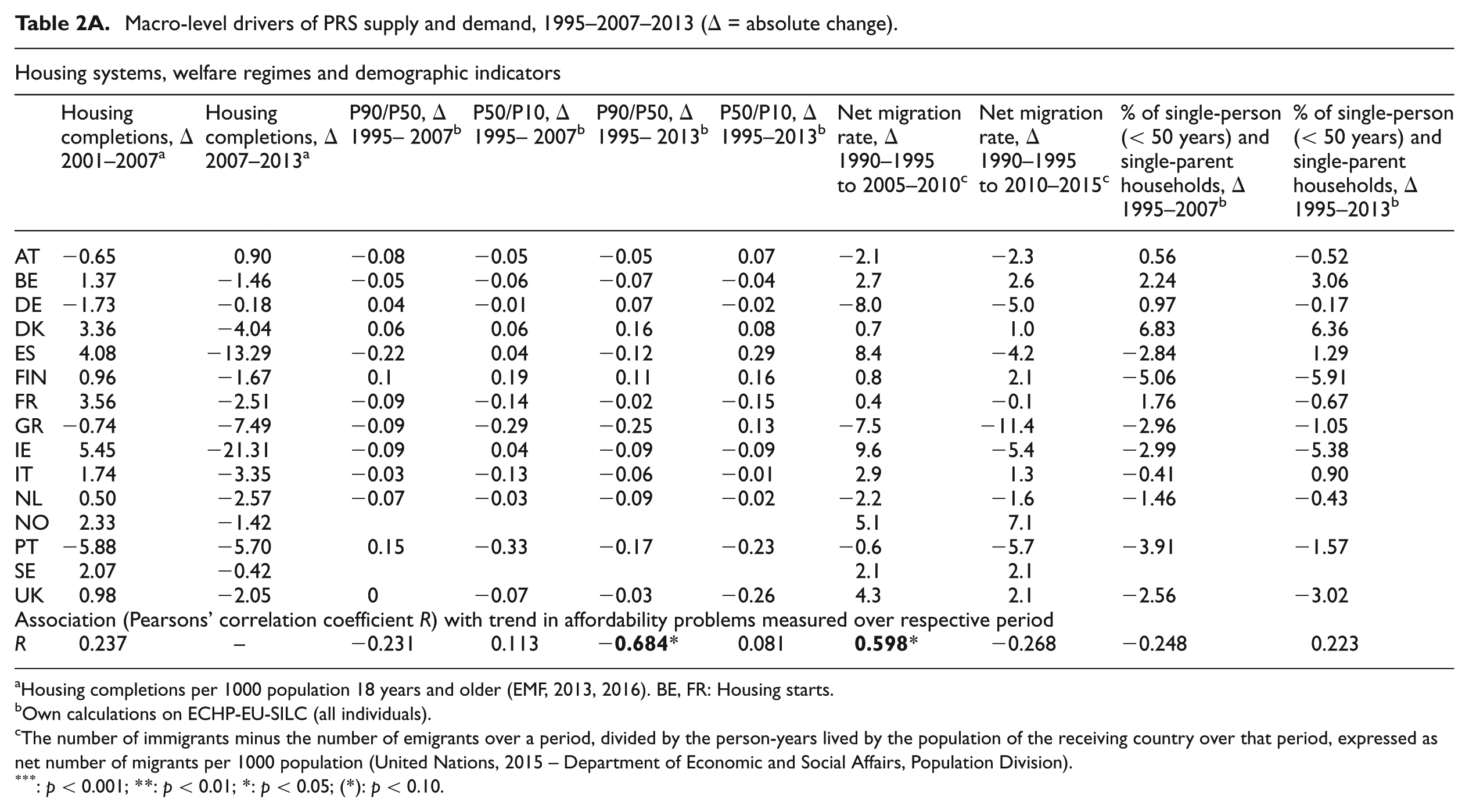

Table 2A presents a number of housing system, welfare regime and demographic indicators for the period 1995–2007–2013 and their associations with trends in housing affordability problems. Income inequality as ‘catch-all’ indicator of welfare regimes is measured by means of the P90/P50 and P50/P10 ratios. There is however no clear ‘overall’ increase in income inequality since 1995 and after the crisis, and there is no association with housing affordability trends – apart from the counter-intuitive finding that housing affordability problems among low-income households increased as income inequality in the top half of the distribution declined (1995–2013). This correlation can be considered as spurious, arising from the fact that in the countries that were hit hardest by the GFC (Spain, Greece and Portugal) richer households became relatively poorer. Changes in the per cent of single-person (< 50 years) and lone-parent households are not associated with trends in housing affordability problems of low-income private renters. For the period 1995–2007, the net migration rate is however positively and significantly associated with declined affordability. We also looked at housing completions as a general indicator of housing supply, which was severely affected by housing market financialisation and the GFC (Whitehead et al., 2014), but found no association with affordability trends in the PRS.

Macro-level drivers of PRS supply and demand, 1995–2007–2013 (Δ = absolute change).

Housing completions per 1000 population 18 years and older (EMF, 2013, 2016). BE, FR: Housing starts.

Own calculations on ECHP-EU-SILC (all individuals).

The number of immigrants minus the number of emigrants over a period, divided by the person-years lived by the population of the receiving country over that period, expressed as net number of migrants per 1000 population (United Nations, 2015 – Department of Economic and Social Affairs, Population Division).

: p < 0.001; **: p < 0.01; *: p < 0.05; (*): p < 0.10.

Financialisation and housing affordability for private renters

We next integrate the emerging literature on the ‘financialisation of housing’ into the previously outlined framework of demand versus supply. To this end, we distinguish between different sets of mechanisms and how these may affect housings costs and therefore affordability for low-income private renters. These mechanisms evidently may occur to varying degrees and with varying effects across contexts as global processes are refracted when passing through institutional prisms.

A first set of mechanisms focuses on the financialisation of (home)ownership through mortgage market liberalisation associated with house price inflation, which potentially resulted in housing market dynamics affecting the cost of housing at the lower end, not only for low-income owners but also for renters, particular in the period 1995–2007. It can, for instance, be argued that increased demand for owner-occupation, in a context of inelastic supply of new housing and rising unaffordability of the existing stock, resulted in the ‘filtering up’ of properties from the PRS into the ownership segment. Housing stock affordable to lower-income groups is then converted into more expensive housing. House price increases, particularly in the ‘cheaper’ segment of the market, raise the potential for capital yield to outpace rental yield. When house prices are high, private landlords – in particular in the low-quality segment – are financially better off selling their property to middle- and lower-income households aspiring to homeownership and willing to buy less attractive but more affordable properties. Lower-income renters usually do not have the financial means to allow landlords to upgrade their rents in line with house prices. The result is an ‘impoverishment’ of the supply of affordable private rental accommodation for a more selective group of lower-income households, as the best properties flow into the ownership segment. Such dynamics have been reported for several countries, often with tight housing markets, e.g. Belgium (Albrecht and Van Hoofstat, 2011; Heylen and Winters, 2008) and the UK (Izuhara and Heywood, 2003). House price inflation did however not only spur demand for owner-occupation, but also for buy-to-let housing, giving rise to ‘investor landlords’ looking for capital gains (Kemp, 2015; Ronald et al., 2015). Hulse and Yates (2017) argue, for Australia, that such changes in the type and scale of investment, in a context of urban restructuring and increased land values in inner areas of large cities, have resulted in a ‘private rental paradox’: while demand of both higher- 7 and lower-income households for PRS-housing increased, supply increases have concentrated on mid-market segments with the safest investment prospects. High land/house values resulted in more limited ‘filtering down’ of older stock to the PRS (next to a process of ‘filtering up’ as discussed above), and also to the demolishment of low-quality housing in attractive locations in order to free land for investment housing. Although buy-to-let mortgages have dwindled, in the post-GFC context the procurement of buy-to-let housing remained a popular investment strategy among equity-rich and older households, given the lack of investment alternatives (e.g. Ronald et al., 2015). In line with the mechanisms outlined above, Quigley and Raphael (2004) find for the USA that decreasing affordability of rental housing since the 1990s is mainly attributable to higher rents, not to lower incomes. The stock available to low-income renters has declined. Quality increases are an important explanatory factor, as are process of gentrification and urban renewal (which are linked to housing market financialisation), that tend to remove lower-income housing from the dwelling stock, while adding stock for middle- and high-income households.

Financialisation however not only influenced dynamics in the ownership segment – with a knock-on effect on the PRS – but also rental housing itself. Institutional investors in particular may not be interested in rental yield and tenants, but in the value of the underlying land or of portfolios of rental properties as security for other financial transactions (e.g. Fields and Uffer, 2016; Kemp and Kofner, 2014; Rolnik, 2013; UN, 2017). In urban regions, particularly in world cities (e.g. New York, London, Amsterdam, Berlin), financialisation has entailed increased investment in private rental housing by global institutional investors and equity traders. Their investment strategies however negatively impact on security of tenure, housing quality and housing affordability. Comparing New York City and Berlin, Fields and Uffer (2016) identify different strategies, depending on the type and location of properties. The ‘upgrading’ strategy entails speculation on a rising market, exploiting opportunities to extract higher rents through renovation and modernisation – resulting in displacement of lower-income renters. In New York, systematic harassment through exploitation of the legal system was deployed as a means of achieving (lower-income) tenant attrition in order to secure deregulation and vacancy bonuses. Less attractive housing portfolios are subject to a ‘capital leveraging strategy’, whereby investors speculate on the potential to rapidly flip the property or use it as a collateral. The housing and tenants themselves are neglected, and suffer from disrepair and increasing segregation (also see Kemp and Kofner, 2014). A third ‘post-GFC’ strategy (mentioned previously) singles out low-income households as ‘preferred’ tenants guaranteeing a secured rental income stream (e.g Kitzmann, 2017: 6, for Berlin; Lind and Blomé, 2012: on ‘slumlords’ in Sweden). Again, investors’ motives are ‘far from altruistic’ and their business model might evolve as global markets improve.

We conclude that for lower-income PRS households, house price inflation and housing market dynamics related to financialisation may have reduced the supply of affordable rental housing, which consequently compromised housing costs. Next to the two sets of mechanisms outlined above, a third mechanism links housing market financialisation to declined affordability in the PRS. Countries that were more involved in these processes were hit harder by the GFC. The costs of the economic downturn were however socialised through austerity measures and broader (housing) policy changes (Rolnik, 2013; UN, 2017). Kennett et al. (2013) for instance argue that in the UK policy responses to the GFC focus on the ‘easy’ target of lower-income renters. Reforms include flexible social housing tenancies, curtailing of housing allowances (an important tool for poverty prevention), and reduced security of tenure. According to this third mechanism, increased housing costs combine with reduced incomes to produce affordability problems.

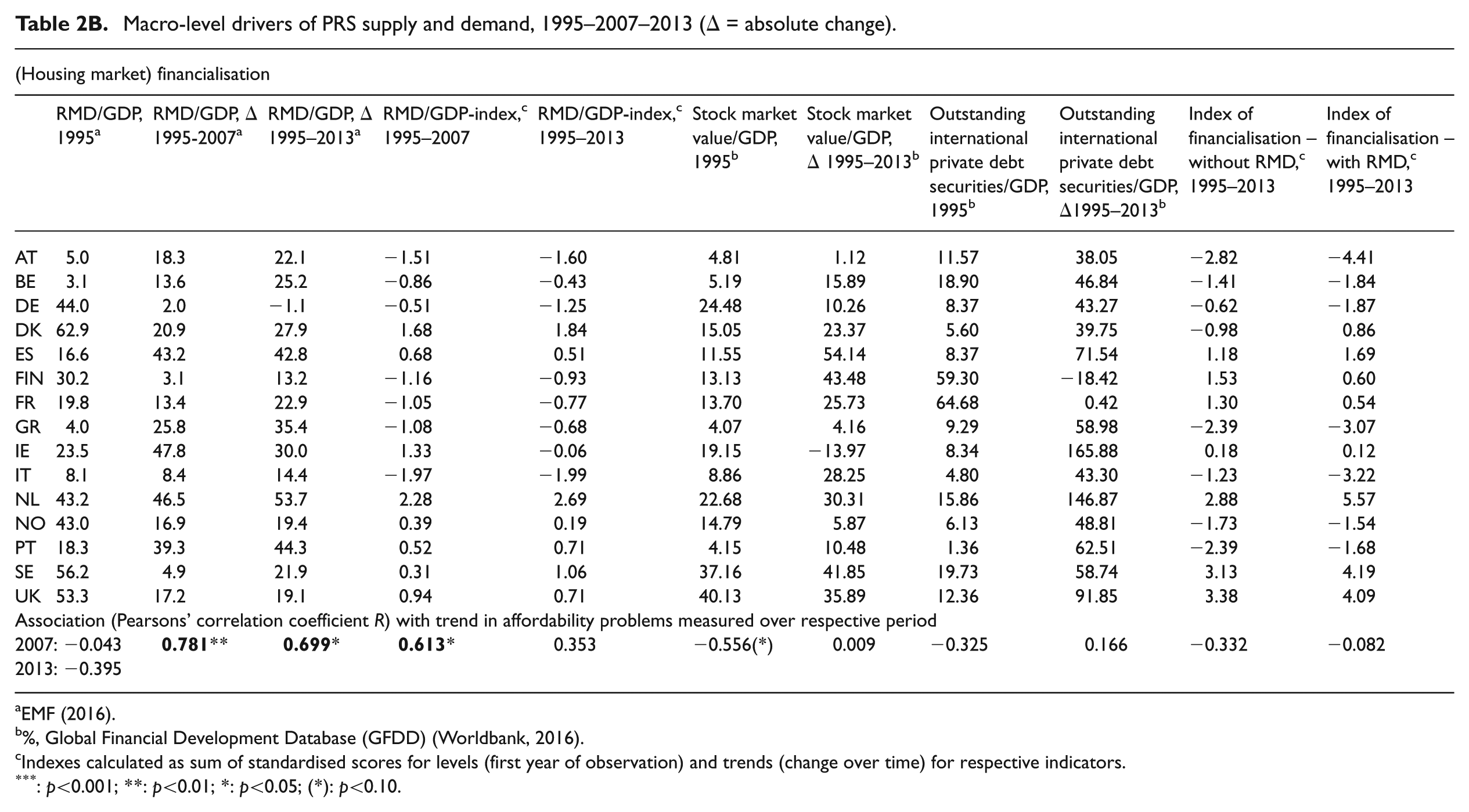

Table 2B presents selected indicators of financialisation, taking account of ‘starting’ 1995-levels and trends over time. Housing market financialisation is measured in terms of RMD to GDP ratios, 8 as other indicators (e.g. share and type of institutional landlords, cross-border foreign direct investment in residential real estate) are not readily available across time for all countries. ‘General’ indicators of financialisation (stock market value/GDP; outstanding international private debt securities/GDP) are not associated with trends in housing affordability for low-income private renters. Increasing housing market financialisation over time (rather than the cross-national variation in 1995 ‘starting levels’) – is however positively and significantly associated with increasing affordability problems. This association is furthermore somewhat stronger for the period 1995–2007, hence before the GFC.

Macro-level drivers of PRS supply and demand, 1995–2007–2013 (Δ = absolute change).

EMF (2016).

%, Global Financial Development Database (GFDD) (Worldbank, 2016).

Indexes calculated as sum of standardised scores for levels (first year of observation) and trends (change over time) for respective indicators.

: p<0.001; **: p<0.01; *: p<0.05; (*): p<0.10.

Decomposing housing affordability trends

From the previous sections, we concluded that declined affordability of housing for low-income PRS-renters across Western Europe is associated with net immigration (1995–2007) and housing market financialisation in terms of RMD/GDP growth, while supply-increase (1995–2013) is associated with improved affordability. Before addressing the potential relationships between these macro-level trends with regard our outcome of interest, we tease out how trends in affordability problems of lower-income private renters came about before and after the GFC – this provides additional information regarding the plausibility of macro-level associations.

Declining housing unaffordability arises in different ways: (1) rents can increase, (2) household incomes can deteriorate (assuming constant socio-economic profiles of private renters), (3) or the composition of the group of lower-income private renters may change over time. In 1970–1980s housing affordability in the PRS decreased as the better-off renters and dwellings were drawn into homeownership, leaving those with a weaker socio-economic profile behind in the least attractive properties. Private renting and renters were ‘residualised’ (Allen et al., 2004: Southern Europe; De Decker and Geurts, 2005: Belgium; Kemp, 2010: UK). However, in the previous sections we discussed an opposite trend, as in recent decades the PRS increasingly started to cater for more and/or a wider range of people. We should thus expect a reverse tendency, i.e. influx of younger people with a more diverse, potentially higher socio-economic profile. Such a trend may improve overall affordability (or not, depending on supply constraints), while outcomes for lower-income households traditionally in the sector may be develop differently.

Figure 3 illustrates first and foremost how trends in unaffordable housing came about. For both time periods 1995–2007 and 2007–2013, we calculated the ratio for the different indicators, distinguishing between urban and rural regions (Moore and Skaburskis, 2004). 9 A first conclusion is that trends in housing affordability are most outspoken for the period 1995–2007, whilst experiences after the GFC are varied and changes are smaller. Particularly in those countries characterised by a strong upward trend in housing affordability problems (Ireland, the Netherlands, Belgium, Spain and Portugal), this can be explained by the fact that growth in real private rents is stronger than real income growth (overall, real incomes of low-income private renters increased during this period of economic growth). This is the case for each country in this group, and across urban and rural regions. After the GFC, rents declined more than incomes in Ireland and the Netherlands, leading to improved affordability. In Spain and Belgium there was not much change. Rents further increased in Portugal, while incomes declined – this resulted in worsening housing affordability.

Trends in housing affordability problems, private rents and household incomes across countries (low-income private renters, ECHP and EU-SILC, own calculations).

In the countries where housing affordability trends remained more or less stable (Finland, Austria and France), the country-level findings are a bit deceptive because of opposite trends in urban versus rural regions. Absolute changes however remain smaller, and trends are diverse. For instance, we note increased affordability problems between 1995 and 2007 across Finnish and Austrian urban regions (again rent growth outpaced income growth), while in rural regions there is an opposite trend. Affordability in French urban regions improved as rents declined while incomes grew, while the opposite was true for rural regions. Finally, in the countries where housing affordability for low-income private renters improved ‘overall’, this is due to a combination of declines in real rents and/or income improvements. Between 1995 and 2007, housing affordability across the UK (not shown) improved somewhat (be it from a very high level of unaffordability), as incomes rose stronger than rents. This is in line with policy changes by the New Labour government during this period, which were aimed at combatting child poverty (i.e. increased Income Support) and making work pay. Rural regions clearly profited more from this trend, as housing costs increased only marginally. In urban settings, the income-effect was dampened by rent increases. After the GFC, we note income declines for the UK and also Greece, which – except for urban UK regions – are not (fully) compensated for by rent declines. During the period 1995–2007, affordability across Italy (not shown) improved as incomes increased more than rents (particularly in rural regions), the opposite is true for the period 2007–2013. In Germany, housing affordability improved before the GFC as private rents for lower-income households declined. Earlier we noted that a potential explanation might the influx of former public housing (with lower rents) into the PRS.

Changes in the socio-economic profile of lower-income private renters

To control for the possibility that decreasing housing affordability for lower-income private renters over time arises from a changing socio-economic profile rather than ‘real’ trends (mainly rent increases), we performed a so-called shift-share analysis (e.g. Fritzell and Ritakallio, 2010): For each country we reweighed our calculations for 2007 (2013) in such a way that the socio-economic profile of lower-income private renters in 2007 (2013) matches that for 1995 (2007) exactly. Because the absolute number of low-income private renters is not that high in many countries, we constructed a variable that captures the following characteristics: the household reference person is in work (yes/no); number of children < 16 years; number of persons ≥ 16 years. The combination of these variables results in the following weight-variable: (1) single person in work; (2) single person not in work; (3) single-parent household; (4) couple no children reference person in work; (5) couple no children reference person not in work; (6) couple with children reference person not in work; (7) couple with 1–2 children reference person in work; (8) couple with 3 or more children reference person in work. Reweighting our data however leaves our findings largely unaffected (results available).

We also checked whether our results are confounded by a possible influx of younger people – who experienced increasing difficulties to enter homeownership – into the group of lower-income private renters. Young people have comparatively low incomes compared with the population, but at the same time they may be able to afford higher rents than the ‘traditional’ disadvantaged PRS tenants, which would explain our over-time trend of increasing rents and incomes. This is not the case: in many countries the share of young people among lower-income private renters has actually decreased (somewhat) over time. The share of households with an older reference person (45+) has increased somewhat (results available).

We thus conclude that the general trend towards greater unaffordability of housing for low-income PRS households – mostly evident in the period 1995–2007 – can be explained by rent increases. Affordability problems thus arise from housing market changes, rather than from income declines or compositional shifts – although of course, compositional shifts may still have indirectly resulted in demand pressure for those traditionally in the sector.

Disentangling macro-level drivers of trends in housing affordability, 1995–2007

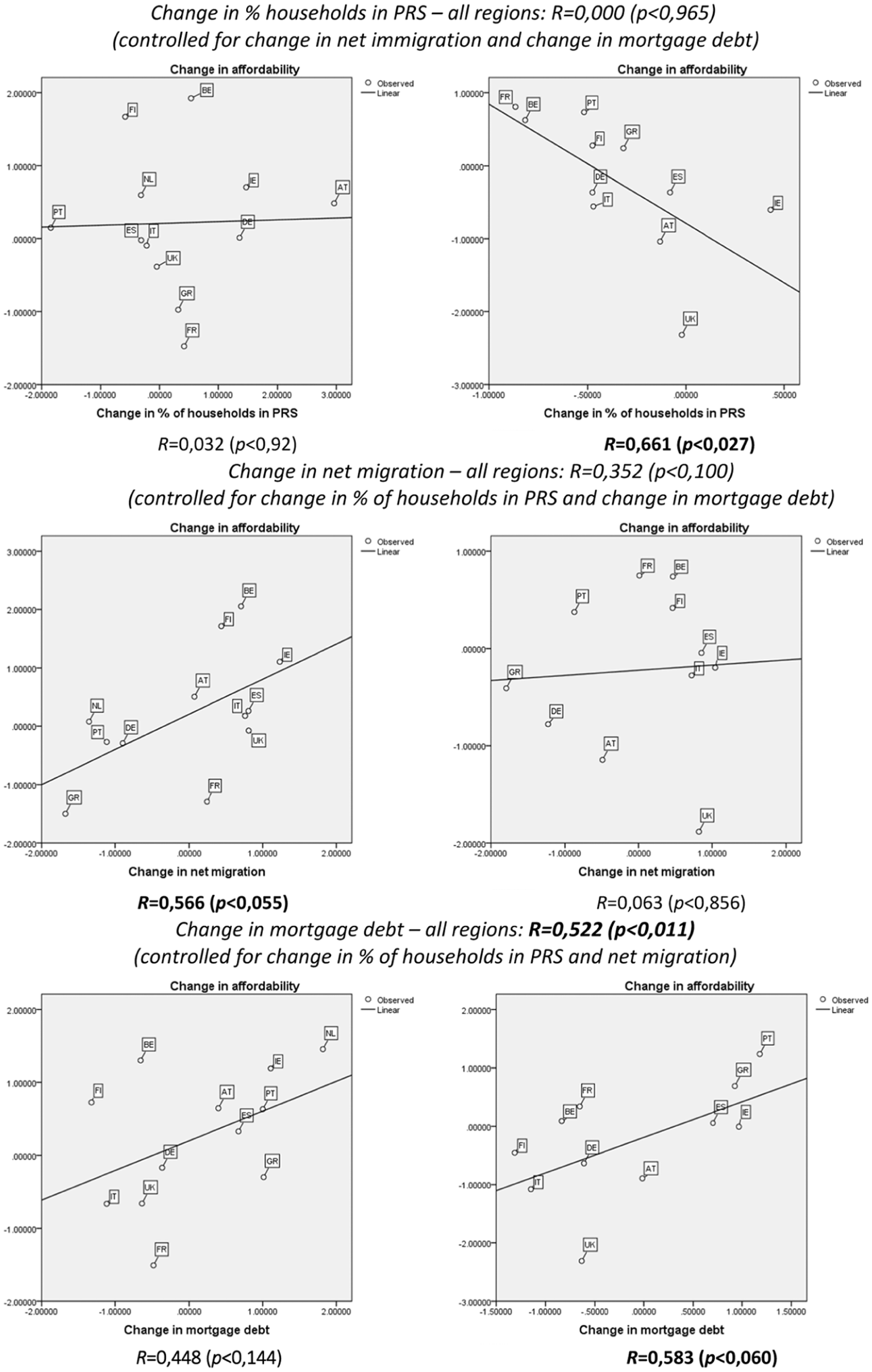

Earlier we noted that increased affordability problems over time (1995–2007) are associated with higher in-migration and mortgage market financialisation, while supply-increases improve affordability. In this final section, we control for possible associations between these ‘drivers’ of affordability trends (which may lead to spurious effects), while also taking the regional level into account. 10 Results are summarised in Figure 4: although ‘net’ associations are weaker, we find support for all ‘drivers’ of demand versus supply. Increases in the number of households in the PRS (as a proxy for increased supply) are associated with improved affordability (and vice versa), but only in rural regions. Increased net migration is associated with declined affordability, but only in urban regions. This is in line with the preference of immigrants to establish themselves in larger cities. We also find evidence for an effect of housing market financialisation, for all country-regions taken together and for rural regions; the ‘net’ association for urban regions only does not reach statistical significance. Stepwise regression analysis however indicates that the ‘uncontrolled’ positive and significant effect (p < 0.05) for urban regions is mediated by the number of (low-income) households in the PRS. More financialised countries however also experienced higher in-migration. Nevertheless, our findings are in line with emerging evidence on the negative impact of housing market financialisation on low-income households – through reduced supply of (affordable) PRS housing but also through other mechanisms; in particular given that a ‘net’ association remains in rural regions.

Partial regression plots for change in affordability problems of low-income private renters (ECHP and EU-SILC, own calculations), for urban (left) and rural (right) regions, 1997–2005.

Conclusion and discussion

The private rented sector (PRS) recently enjoyed a revival, in particular in the years before and after the Great Financial Crisis (GFC). At the same time and somewhat counter-intuitive given increased supply, affordability concerns – particularly for PRS-tenants – became a social issue. The main aim of this paper was to explain trends in housing affordability for lower-income households in the PRS across Western European countries, from a supply versus demand perspective. To this end we: (1) related trends in housing affordability to wider changes in housing systems, welfare regimes, demographic indicators and housing market financialisation; and (2) decomposed affordability trends in terms of rents and incomes, controlling for changes in the social composition of lower-income private renters. We focused on low-income households, as these lack economic and political power and are therefore most vulnerable for changes in housing systems, exogenous changes (e.g. declining wages, unemployment, benefit cuts, immigration), or pressures arising from housing market dynamics related to such wider trends. We incorporated the spatial dimension by distinguishing between urban and rural regions.

We contributed by integrating the ‘financialisation of housing markets’ into our explanatory framework. An emerging body of research explores the potential impact of such a process on the PRS and its inhabitants across different contexts and through various mechanisms and dynamics. Although financialisation is a ‘diffuse’ concept, with varying effects across contexts as global processes are refracted when passing through institutional prisms, we distinguished between three ‘sets’ of mechanisms – housing market dynamics resulting from the financialisation of (home)ownership; the financialisation of rental housing; and welfare reforms resulting from the GFC – all leading to the expectation of a positive association between housing market financialisation and a worsening of housing affordability for low-income private renters. Although we found the strongest increases in affordability problems to occur before the GFC, between 2007 and 2013 worsening affordability for low-income private renters indeed occurred in some countries that have been affected harder by the crisis – Portugal, Greece and Italy. Two of these countries however did not experience strong housing market financialisation. We hence did not find much support for our third mechanism. Given that welfare reform does not happen overnight, this mechanism might however be of future relevance.

Although we could not explicitly test for the more fine-grained mechanisms relating housing market financialisation to increased ‘unaffordability’ of PRS-housing, our findings nevertheless warrant future research. Keeping the socio-economic profile of lower-income private renters constant, in particular in countries with strong financialisation (Ireland, the Netherlands, Spain and Portugal) decreasing affordability arises from the fact that during the period 1995–2007 private rent increases were not compensated for sufficiently by income growth. For urban regions, this association is mediated by a declining number of (low-income) households in the PRS – which is in line with our underlying mechanisms. We furthermore found that for these regions, between 1995 and 2007, affordability worsened through demand pressure arising from in-migration.

Given our shorter time frame, changes after the GFC are more limited. Housing market financialisation will however likely remain a relevant trend to watch. In the post-GFC context of low interest rates, real estate remains valued as an asset class in the investment portfolios of equity firms and ‘high-net-worth individuals’ operating on a global scale (Rogers and Koh, 2017). The process has however become more direct: in terms of the actual procurement of (residential) real estate rather than investment in securities (Ronald and Dewilde, 2017). According to Savills (2016), cross-border residential property investment increased 334% between 2009 and 2015. Although motives and uses differ (e.g. for actual use by oneself or one’s family members, as a ‘storage’ for excess wealth, to rent out or leave vacant, as security for financial transactions), housing opportunities of local (low-income) households are likely affected.

Footnotes

Acknowledgements

ECHP and EU-SILC data were provided by Tilburg University. The author thanks the reviewers, as well as participants of the ENHR Housing Finance and Private Rental Housing Working Groups (joint session, ENHR-Conference Belfast, 2016) for their useful suggestions.

Funding

Funding was received from European Commission > European Research Council ERC Starting Grant HOWCOME 283615.