Abstract

This paper presents a strategy for scaling climate change adaptation within urban areas. The strategy specifically focuses on the requirements for mobilizing large amounts of capital for adaptation and other urban risk reduction above and beyond the amounts that will likely be mobilized through new international adaptation funds. The paper, based on a report published by ICLEI–Local Governments for Sustainability,(1) proposes a re-framing of the urban adaptation and disaster reduction challenge. The approach shifts the adaptation focus from risk reduction as a primary end in itself to a broader development focus on financing

I. Introduction

Urban reformers have long wrestled with the awkward reality that the riskiest urban places – so-called “slums”,(2) flood zones, polluted industrial areas – are, for many, tremendous sites of opportunity, attracting increasing residence and investment. Regulating risky development and relying solely upon public expenditure to mitigate risks in poorly developed urban areas does not appear to be an adequate response in a world of very opportunistic, rapid urbanization.

Consider the growing conflict between urban growth and risk exposure in even the most manageable and fiscally prosperous circumstances. California’s highly urbanized coastal region is exposed to some of the world’s most extreme seismic risk. In the twentieth century, the region suffered several costly 7.0 magnitude earthquakes. Yet between 1906, when an earthquake destroyed San Francisco, and 1994, when an earthquake killed 61 and caused US$ 15 billion in damage in the Los Angeles area, metro San Francisco’s population grew by nearly six million; and 15 million new residents, rich and poor, sought their opportunities in vulnerable metro Los Angeles. The first steps towards a state-wide, advanced seismic early warning system were only taken in 1998 despite the region’s wealth and technological sophistication;(3) and Silicon Valley’s municipal and corporate leadership only recently started work on a regional disaster preparedness and response plan.

Urban agglomeration clearly offers compelling locational economic advantages, even when factoring in the intensification of risks in urban areas as populations concentrate. The fact that coastal California faces a scientifically validated 99 per cent chance of another major earthquake over the next decades seems to have little bearing on urban location and investment decisions.(4) Billions of people and trillions of investment dollars continue to flow into urban areas that are vulnerable to tropical storms, flooding, earthquake and sea-level rise.

It is not coincidental that disaster incidence – reported disasters increased by 60 per cent, from 4,241 to 6,806, between 1997 and 2006(5) – correlates with continued rapid urbanization of high risk geographies. Dominant approaches to urban land use and watershed management, urban design, building regulation and materials and infrastructure exacerbate vulnerabilities to weather, seismic activity, disease, crime, resource shortages and industrial risks, causing some experts to re-frame the whole disaster reduction discussion from one of “natural disaster” to “unnatural disaster”(6) or “disaster by design”.(7) Urbanization in vulnerable areas exposes a growing inventory of expensive urban assets and infrastructure to damage and disruption, such that disaster-related losses during the 1990–1999 period were more than 15 times higher in constant dollars than in the 1950–1959 period.(8)

The relationship between urban development, disaster events and disaster costs is clearly evident in the area of climate change. In spite of wide variances in cost estimates for climate adaptation,(9) most agree that future adaptation costs will be concentrated in urban areas and infrastructure. The UNFCCC attributes up to 76 per cent of its cost estimate to the infrastructure adaptation category, which by its calculation

Although there are no full assessments of annual, global fixed investment in urban development, some compelling estimates have been made. The McKinsey Global Institute, for instance, has estimated that there will be US$ 46 trillion in fixed asset expenditure in Chinese cities between 2005 and 2025.(11) In other words, just one year’s worth of Chinese expenditure on fixed urban assets – an estimated US$ two trillion, excluding expenditure on planning, governance and operations – is approximately 67 times the total adaptation fund pledges made to date for the three-year period 2010–2012. If the estimated Chinese rate of urban asset expenditure is extrapolated on a per capita basis for each new urban dweller globally during this 20-year period, then a rough global estimate of urban fixed asset expenditure between 2005 and 2025 would be in the region of US$ 200 trillion – or US$ 10 trillion per annum.(12) In other words, investment in urban fixed assets could well be 300 times the available adaptation funds.

At this magnitude, even the most ambitious estimates for climate adaptation funding – assuming a substantial re-allocation of the funds from rural to urban projects – would have a negligible impact on urban climate risk reduction. An effective adaptation finance strategy would seem to require a substantial leveraging of public and international development resources to change the way in which private investment and expenditure in urban areas is made. Climate funds would need to be used to support relevant planning, design, institutional development and technical assistance efforts rather than direct investment in a very small percentage of urban areas and assets. Providing support to these capacity-building activities would enable local authorities, utilities and other development institutions to substantially leverage conventional urban development investments in favour of risk reduction.

Within this context, the premise of this paper is that the economic “downsides” associated with investments in risky urban locations need to be internalized into investment schemes for those particular locations. For instance, the downside risk of increased tropical storm damage in a highly urbanized coastal area needs to be factored along with the conventional “upside” returns from investments, for example rental incomes, utility fees, appreciation of asset values. This is particularly important in a time of significant fiscal constraint, when public resources for proactively managing growing risks or for responding to increasing disasters will be quite limited. Urban risk reduction itself needs to be re-framed as an

This internalization of the lifecycle cost of disaster risk extends well beyond increases in insurance premiums associated with high risk urban locations. It requires the establishment of an investment logic for risk reduction. Simply put, this logic is that assets and locations with low exposure to climatic and other disasters will produce more stable net revenue streams and maintain more stable asset values. In other words, through efforts to define and factor locational risk into urban investment decisions, an investor’s front-end (and thereby lower cost) measures to reduce risk could increase the financial performance of the property, urban area or infrastructure system from a net present value (NPV) or internal rate of return (IRR) perspective. This re-emphasis on urban asset or locational performance can be expressed in terms of “resilience”.

Resilience, therefore, creates a clearer linkage with the area’s or infrastructure system’s overall investment attractiveness and potential. Rather than just being a risk reduction cost, “resilience upgrading” investments aim to create a development premium through a set of financially justified risk reduction measures that increase the reliability of investment returns and asset values under a wider range of circumstances. The challenge of climate adaptation, and of other risk reduction strategies, is to create the institutional, planning and policy frameworks, business practices, information systems and financing instruments to establish a market basis for resilience upgrading of vulnerable urban areas and systems as private investments flow into these assets and areas over the coming decades.

There are numerous examples of resilience upgrading from the urban best practices literature, but they have not yet been widely applied to the disaster risk reduction challenge. For instance, Barcelona increased the economic resilience of its Poblenou district when it created a network of underground conduits for the installation of future forms of infrastructure as part of the district’s redevelopment scheme. This kind of state-of-the-art infrastructure was used to attract private investment flows into the deteriorated old industrial–residential area. The incremental investment in the conduits makes the district more resilient than competing districts in the face of unpredictable technology changes. It reduces the risk that the district will not be able to cost-effectively adapt in a timely way to new business infrastructure requirements.

To take another example, Toronto’s establishment of a district heating and cooling system and specialized utility for its central business district (CBD) has allowed the provision of 20-year fixed price contracts for heating and cooling for major employers and property owners in the district. This makes Toronto’s CBD more resilient than competing CBDs to future energy supply and price shocks. It reduces the risk that the district will lose its competitive advantage under future energy scenarios. The reduction of risk and the greater quality (i.e. performance) of services should be reflected in asset values and rents.

The “resilient cities” investment strategy outlined below applies similar investment logic to addressing climate and other disaster risks in areas of established and/or accumulating risks. The strategy was first presented at the 2011 Resilient Cities congress in the form of an ICLEI report entitled “Financing the resilient city: a demand-driven approach to development, disaster reduction and climate adaptation”.(13)

II. Resilience Upgrading: A Description

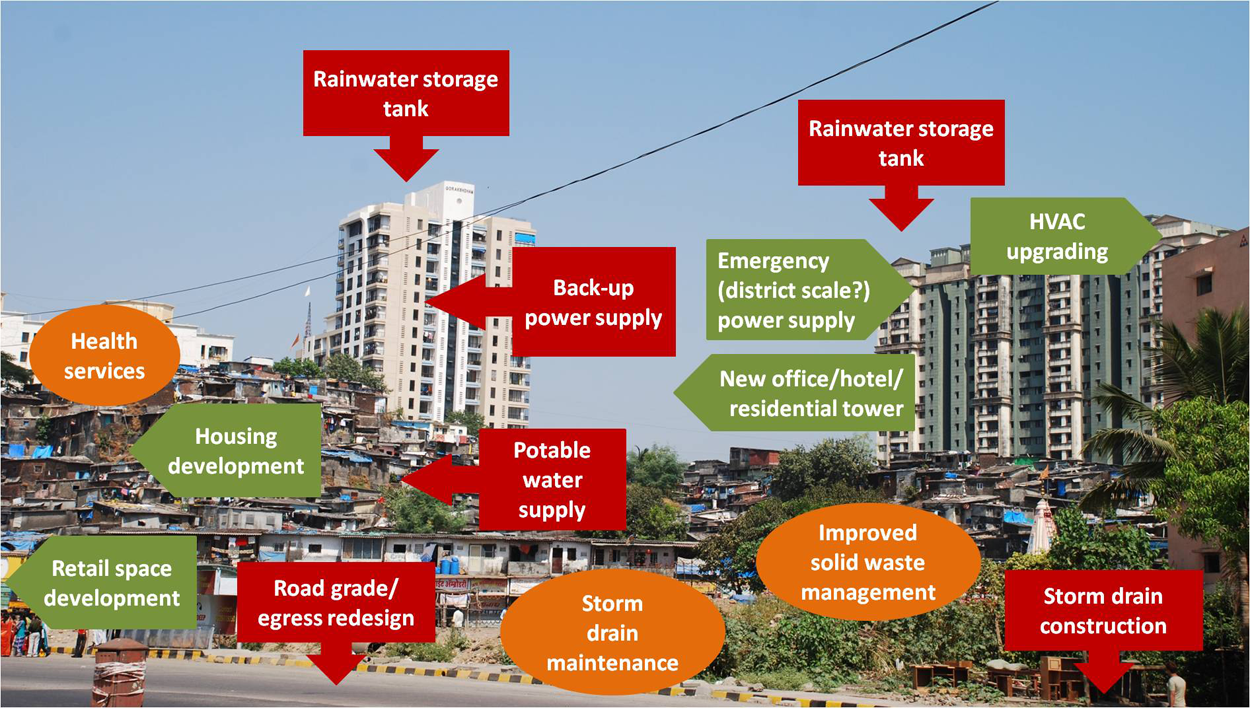

Consider the typical “infill” development scene in one of Mumbai’s sprawling suburbs (Photo 1). Considerable investment – formal, quasi-formal and informal – is being made in this area, intensifying land use and commercial life and opportunity. As the area’s population and utilization increase, so do the area’s risks in terms of performance and crisis. During the monsoon season, the pressures on an increasingly under-capacity storm drain system and the clogging of drains due to inadequate waste management exacerbate the frequency and scale of flooding. Associated transportation problems can make the area temporarily inoperable, undermining commercial vitality. Flooding and poor waste management also exacerbate the vectors and incidence of communicable diseases. During the dry season, insufficient water and electricity supply also constrain the productivity of the area. As a result, the area underperforms in terms of revenues, NPV and IRR. Three different performance gaps need to be closed in the development of this area, and these are illustrated in Photo 2.

A typical suburban area in Mumbai that is attracting private investment

The elements of a “resilience upgrading” project

The red rectangles (with arrows) in Photo 2 highlight the area’s

The orange ovals and green arrows in Photo 2 suggest that further investment is necessary to develop the resilience and overall performance of this area. The ovals highlight the

Finally, the green arrows highlight the potential, if not the need, to further optimize the performance of the area as a place in which to live and generate wealth. Investments in fixed assets for revenue generation and asset appreciation purposes have their own development function and investment logic. They close an

Considering the numerous implicit interdependencies between the three types of indicated projects, the example simply highlights the advantages of applying incremental investment for climate adaptation within the context of a comprehensive effort to reduce risks and increase the overall performance of the urban location. The three highlighted types of investment, jointly designed and implemented, enhance not only the area’s performance for today’s residents and users but also the resilience of its performance – the range of circumstances under which the area will function at a higher performance level. In principle, this increases the returns on the large and small investments being made in the district and thereby attracts new forms of investment to the area.

Cities are dense, complex systems. They are characterized by intense, regular interactions that are structured in identifiable activity areas such as a district like this one, or in key resource management or mobility sub-systems, for example urban drainage or energy systems. The character of urban districts as complex place-based systems is very different to that of lower-density rural areas where activities are more spatially separated and interactions are less intense. In the urban environment in particular, the resilience of a place-based system is only as great as its weakest part. The density of interactions and the intensity of interdependencies amplify and accelerate feedback and cascading effects, starting in spatial proximity and spreading through system networks that extend to other locations across the city. As a result, urban function or performance during stress events is as much determined by the relationships and interactions between the many different individual fixed assets (e.g. buildings, roads, pipes)

This spatial understanding of the requirements for effective adaptation at the district scale – and the inseparability of environmental, development and locational performance – is a key technical insight underlying the resilience upgrading concept. Risks are reduced and investment value increased when a place or whole system is being transformed, not only a single building, facility or infrastructure intervention. This differentiates resilience upgrading from conventional development project design, which often does not distinguish between the supply-side definition of an attractive unit of investment (e.g. a sewerage treatment plant or new ring road) and the integrated functioning of the total area and its interdependent sub-systems.

Lessons derived from the still-limited body of international development assistance (IDA) financed urban adaptation projects point towards this conclusion.(14) The largest urban adaptation project financed by the Global Environmental Facility (GEF), “Adaptation to Climate Change in Ho Chi Minh City”, involves nearly US$ one billion in pledged resources. It quickly showed the need to spatially calibrate and customize adaptation interventions. This topic has been explored at length in a series of papers by Professors K Moon and H Storch, with N Downes and H Rujner, based on their planning experience in the Ho Chi Minh City (HCMC) project. Moon et al. conclude that effective intervention requires a spatial definition of “urban structure typologies” that are associated with distinct vulnerabilities and risks, requiring distinctive mixes of adaptation and disaster risk management (DRM) measures. They call the process of factoring local structural typologies when developing portfolios of development and risk reduction measures “downscaling”. To quote Moon et al.:

“Vulnerability to climate change varies considerably from settlement to settlement and even within settlements. The location, urban structure, dominant building type, socioeconomic characteristics and institutional capacity are key factors that affect vulnerability and adaptive capacity of a settlement in the mega-urban region […] Climate change-related urban adaptation decisions require a rational characterization of urban structural landscapes according to risk relevant features. Urban structure types, block size and form are dependent upon the transportation or surface water networks that frame the block, as well as the formal or informal nature of the building typologies, their individual forms, their connections as well as their interconnections to adjacent structures […] Other differentiations are made based upon land uses, orientation, structure density and building and sealing material. Furthermore, at the street level, via valuable local knowledge, photography and site visits, the climate change relevant indicators and parameters for each urban structure type can be surveyed…”(15)

Resilience upgrading differs in two fundamental respects from the conventional strategy for development and adaptation finance. First, the purpose of the adaptation project shifts from a singular focus on specific climate-affected infrastructures and interventions towards a more integrated focus on overall environmental risks, development conditions and local area performance. And second, the investment strategy shifts from a top-down, international development project finance approach to a bottom-up, diversified and leveraged finance approach that reflects the more decentralized and market-oriented character of twenty-first century societies. Adaptation projects are currently understood as a response to an “additional” policy agenda, being established through international climate negotiations. The framework parameters and rules for fund-worthy projects are defined by the established international climate funds and are negotiated first with national ministries and international organizations. Substantial terms of the projects are therefore originated by supra-national finance suppliers and supra-local institutions.

In contrast, the resilience upgrading approach is inherently “downscaled” and mainstream. The starting point is the unique, overall development requirements and investment opportunities of each vulnerable place and its stakeholders. Project preparation involves bundling a set of mutually supportive investments in the area into a comprehensive upgrading project. The most appropriate financing for the project (and its different components) is then sourced from local government, private investors and international funds. The international climate funds can be critical partners and contributors, but the nature of their contribution is integrated within a more comprehensive development plan. To the extent that the international climate funds can organize themselves to be responsive to such bottom-up demand, resilience upgrading can substantially add to the achievements of their project portfolios.

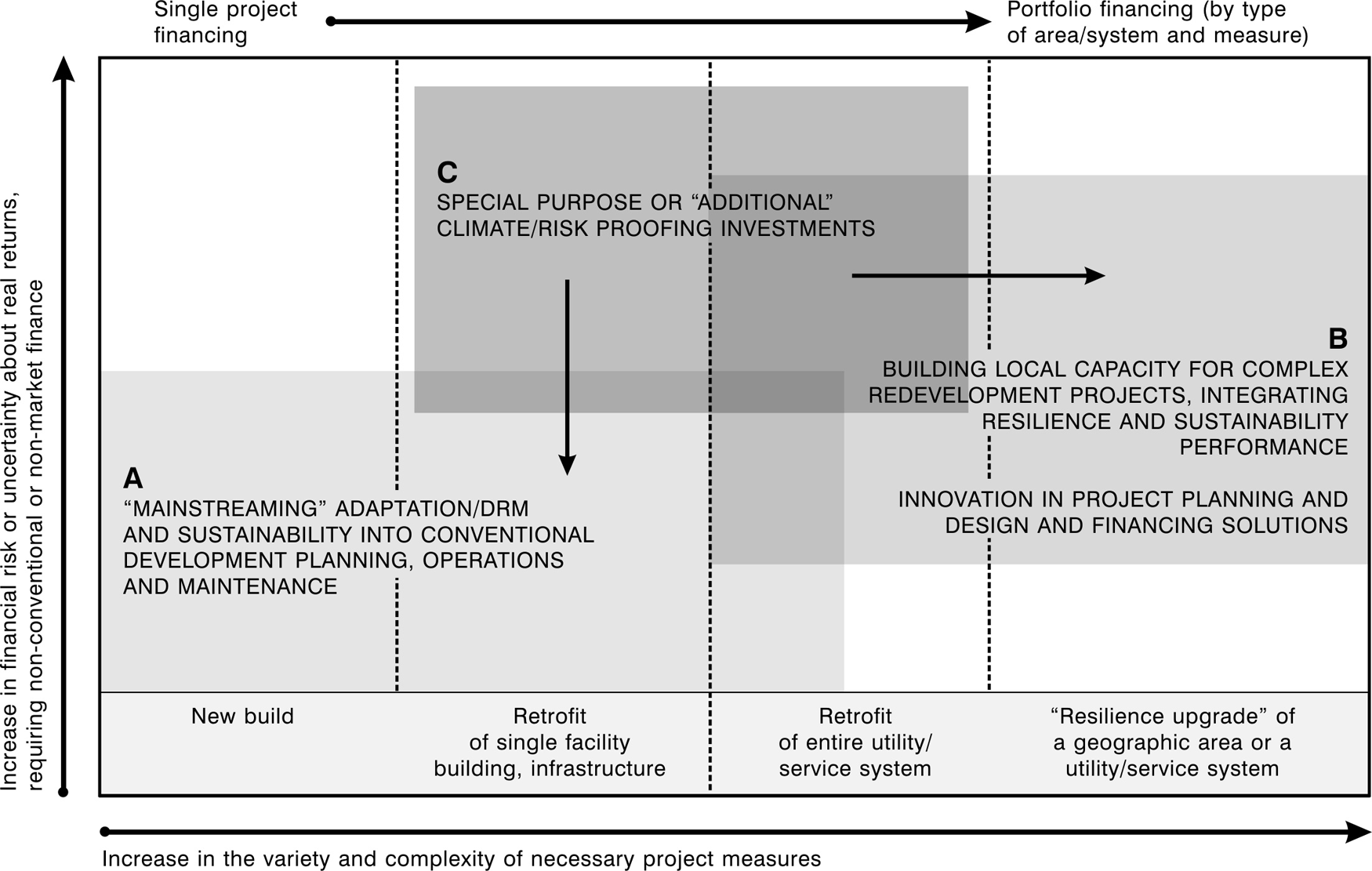

Within the context of resilience upgrading projects, we propose that international adaptation funds can achieve their greatest impact through two main strategies, illustrated in Figure 1 below. The first strategy is to shift the use of limited adaptation fund resources from direct investment in specific climate-proofing measures (type-C expenditures) to policy and programme initiatives that integrate risk reduction and sustainability into the local, sub-national and national design and development approval requirements for “mainstream” urban construction and infrastructure (type-A investments). This “mainstreaming” shift, as indicated in Figure 1, re-focuses resources from high-risk/low-return type-C expenditures towards the attraction and support of lower risk, market-based investments in revenue-generating type-A urban development projects. The role of the climate funds would be to finance the scaling of effective standards, resilience metrics and technical assistance for risk reduction across the construction and infrastructure industries.

Leveraging climate adaptation funds

Drawing upon these efforts, the second approach focuses on leveraging adaptation funds together with other public and private finance for type-B urban upgrading investments within existing, highly complex urban areas and infrastructure/service systems. The “resilience upgrading” approach shifts resources from stand-alone climate-proofing measures to coordinated public and private investments to improve the conditions and performance in priority areas. The approach allows alignment of the adaptation agenda with the agendas of slum upgrading, green building, urban regeneration and profit-seeking private real estate development generally.

The remainder of this article focuses on two challenges of the resilience upgrading shift: the development of new local institutional capacities for large-scale, integrated upgrading projects; and the development of complementary new financial instruments to attract private capital to these projects.

III. Demand-Driven Investment: Creating Market Conditions for Resilient City Building

Comprehensive upgrading of vulnerable urban areas only becomes possible if effective, bottom-up demand for improved district level performance can be matched with responsive, sufficient sources of finance, i.e. forms of financing that are responsive to local performance requirements. This demand-side investment challenge requires the establishment of three distinct local capacities for resilience upgrading. These are:

bottom-up

bottom-up

bottom-up

The establishment of effective planning processes for vulnerability and risk assessment is addressed in the source report for this paper. Numerous local adaptation planning exercises have been completed or are underway. This paper only addresses the local institutional capacity required to implement such plans through resilience upgrading.

The difficulties of transforming existing built areas and infrastructure/service systems are widely recognized in the urban planning and property development industries. The difficulties include, but are not limited to, problems of land consolidation, liens and rights of way, historical liabilities and ex-post facto legal recognition of semi-formal and informal claims and tenure rights. Further complexities include the challenges of different building types and conditions, varieties of economic activities with sensitive place-based dependencies, and the claims and preferences of organized communities. Such difficulties are a primary reason why the property development industry and the financial industry that supports it show preference for new-build or “greenfield” projects, which in turn result in the sprawl of under-utilized urban assets and infrastructure that is a worldwide urban growth phenomenon. These difficulties are also a primary reason why local governments establish special planning districts for existing built areas that require thorough upgrading, as well as special development companies or other special purpose vehicles to manage upgrading comprehensively within these zones.

Local development corporations, focused on upgrading specific areas or infrastructure systems, have been at the forefront of innovation in urban development, including its financial aspects.(16) Some of the financial innovations developed and widely used to support comprehensive redevelopment of specific areas include the creative use of land leases, land swaps, “bonusing” incentives, value capture schemes, tax increment debt financing, revolving loan funds, property-assessed clean energy financing and project guarantees.

The development of local institutions with special planning controls, financing powers, financial instruments and other redevelopment capabilities is a critical capacity-building requirement in societies wishing to rapidly and effectively reduce the very specialized climate and other disaster risks facing very different local areas. This kind of local institutional capacity is also essential to leverage the limited resources of international development banks and special climate funds, along with private and local public investment. Supporting the development of such institutions, particularly for high vulnerability urban regions, may be the most important capacity-building investment that the adaptation community can make.

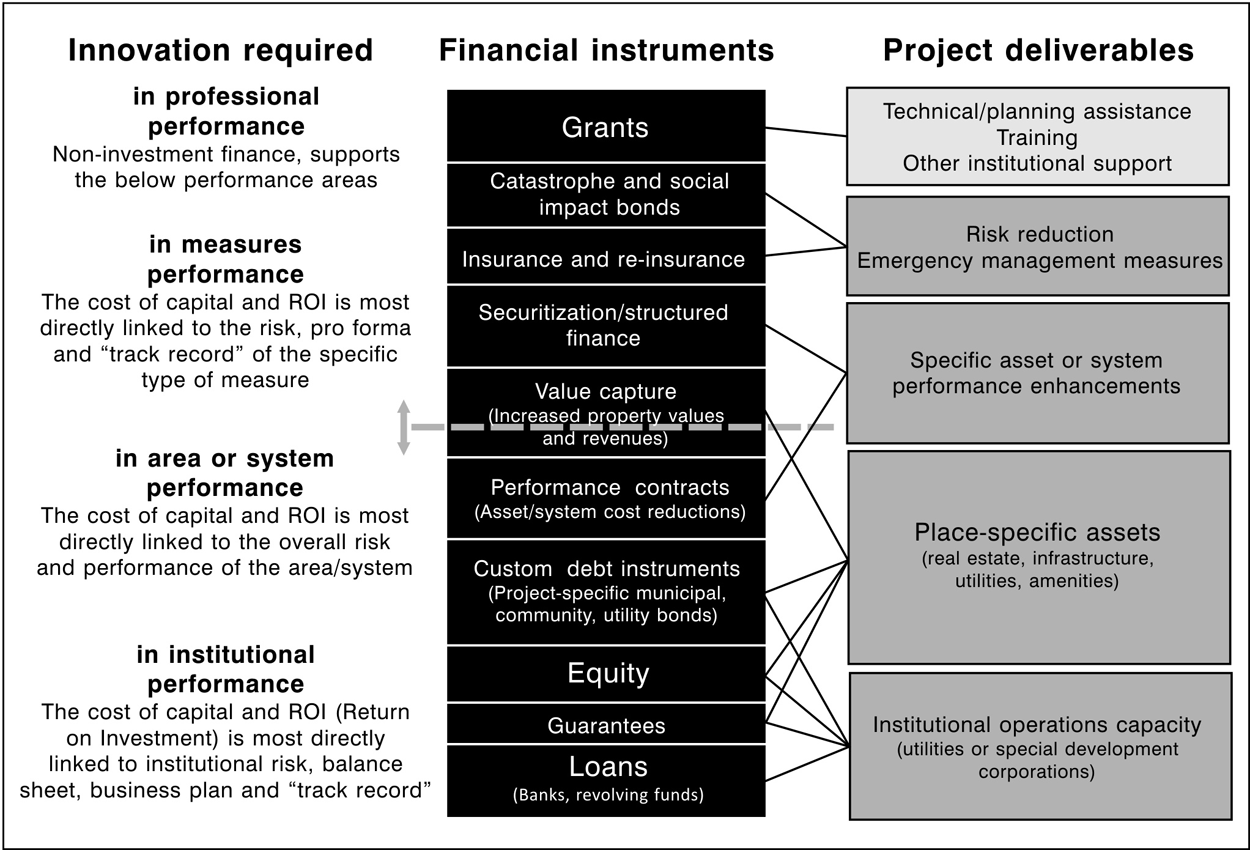

The proposed local development institutions must have the technical capabilities to source different forms of finance for the different types of measures and to structure optimal financing for each comprehensive upgrading project. An indication of the components of a redevelopment or upgrading project is provided in Figure 2. A comprehensive project bundles and coordinates multiple types of public and private project deliverables (right hand column). Each component is matched with different financing mechanisms and instruments, which in turn are linked to different development innovations required to build resilient urban areas (left hand column). This results in the use of a mix of financial instruments in each upgrading project.

Investment structuring for complex urban upgrading projects

This bundling together of measures and their matching with different financing mechanisms is complex and cannot be achieved without a special purpose vehicle (SPV) that is dedicated to the task. When upgrading an individual asset the benefits and risks rest with the individual asset owner(s). But risks at the scale of an entire district, neighbourhood or transportation corridor do not rest with a clear investor, even if the district is a valued functioning economic unit of a city. Without an SPV as a lead investment agent, the district suffers the classic “tragedy of the commons”. Increases in revenues and asset values from district-wide upgrading measures will accrue to local businesses and households, but no entity views the district as its main unit of investment, so the investments will not be made. The district itself is not organized and does not function as an investment unit to create a return that can be captured by a single entity, excepting the local tax authorities.

This is why we propose that the institution most closely associated with the local tax authority be supported to establish SPVs with authority and interest in the overall performance of vulnerable districts. The SPV can function as an investor that optimizes the revenue and asset value potential of all assets located in the district, i.e. of the district as a whole. The increasing value of the district’s assets can be captured in part by the SPV or local government in the form of fees and special charges, special property taxes or the improvement and sale of its own property holdings. These revenues can be re-invested in further upgrading activities. In other words, the establishment of an upgrading “zone”, with special development standards, and an SPV to invest in location-wide resilience and value creation establishes a proxy “investor” with a financial interest in district-wide performance. The SPV plans, sources, coordinates and integrates the scores of investments that will take place in the course of upgrading. Such an entity can successfully manage such complexity because of its specialized focus on the unique challenges and opportunities of the particular district or zone and its unique risks and opportunities.

IV. Creating Greater Financial Flows for Resilient City Building

Even with an SPV to oversee the upgrading of a particular “risk zone”, the evaluation, establishment and maintenance of resilience in urban districts and their fixed assets will likely involve measures that have not historically been associated with the development industry’s creation of value or revenue streams. Until industry learns how to integrate resilience as a value proposition into the front-end of project planning and product design – this being the practical definition of “mainstreaming” in the urban context – there will likely be a need for new, non-conventional financing instruments to support certain aspects of resilience upgrading. As argued above, the international adaptation funds will not offer sufficient funds for these measures.

In Figure 2, the hatched line indicated by ↕ suggests the existence of a threshold for new financial instrument innovation. The financial instruments indicated below the line are structured to secure returns for investors on the basis of institutional (e.g. utility) or individual fixed asset performance, or on the basis of cost savings arising from customized efficiency measures such as energy efficiency retrofits in buildings. The use of these conventional financing instruments for resilience upgrading requires the mainstreaming of risk performance criteria into the investment propositions and project deliverables associated with these instruments. But it only secondarily involves innovations in the instruments themselves.

Take the example of “green building” as a new value proposition in the building industry internationally. Not long ago, achieving very high levels of energy, water and materials lifecycle efficiency in buildings did not attract investment. Individual building owners were left to finance these kinds of improvements from their internal resources. Then in the 1990s the energy service company (ESCo) model emerged, using the financial innovation of performance contracting to mobilize external sources of finance for these kinds of performance improvements in client properties. But even large ESCos such as GE Capital had a hard time breaking into key markets such as commercial or local government buildings. In due time, however, pioneering cities and architectural and engineering firms demonstrated that “green building” measures actually attracted higher rents, higher asset values and more stable tenancies. In very short order, “green building” was mainstreamed as a core element into the value proposition of the conventional building industry, and conventional financing instruments like debt and equity were deployed to support projects.

Conventional instruments will not be available to finance all required measures for district level adaptation and disaster reduction. The investments and instruments indicated above the ↕ line in Figure 2 highlight some of the key areas for innovation to create value and financial returns in particular from

The new instruments will initially need to be developed and prototyped in specific local project contexts. The general design of new instruments, and the policy and business model changes required to support them, will need to be extracted from lessons in these individual, bespoke projects. This learning will support diffusion of the innovations to projects in other cities. As resilience upgrading begins to scale across larger numbers of cities, opportunities can be identified to bundle portfolios of specific types of measures from different cities and to pool associated investment demand by creating secondary financial instruments such as catastrophe bonds or structured finance instruments.

We can notionally identify the types of instruments that might be most suited to support the non-conventional resilience measures indicated in Figure 2.

a. Value capture instruments

The existence of a local tax assessment authority over geographic areas offers a unique opportunity to finance comprehensive resilience upgrades. Local governments have widely used value capture mechanisms and borrowing against future tax revenues, such as tax increment financing, to incentivize if not finance investments in blighted areas, i.e. areas with high private investment risk. Value capture mechanisms use special district level taxes and community improvement fees to capture part of the value created for private owners and developers as a result of district-wide improvements by local government. In principle, the same mechanisms used to capture part of the value accruing to private owners from public investment in district level infrastructure could be applied when public investments are made to reduce disaster or insurance risks to private landowners.

Tax increment financing is a form of value capture based on borrowing, i.e. the issuance of a bond against future increases in tax revenues arising from increases in the district’s property values due to the upgrading investments. If it can be established that climate or disaster risks are directly lowering property values, then value capture mechanisms should in principle be available to finance the measures to reduce these risks, and thereby increase those values.

b. Securitization and structured finance

Financial instruments such as mortgages, automobile loans or credit card debt create relatively predictable revenue streams. Similar instruments can be structured into large portfolios, and shares in these portfolios can be sold to investors at a price that is below the anticipated total discounted cash flows from the portfolio. The investors’ share purchases generate an advance payment of a portion of the bundled instruments’ future cash flows to the original issuers of the loans. The issuers thereby secure immediate access to capital, which they can use for their priority expenditures or investments.

The use of securitization to generate immediate capital from predictable, regulated long-term revenue streams such as credit, utility or tax bills provides a possible way of bringing private capital into resilience investment activities. A municipality, a local development corporation or utility company might offer loans to thousands of building owners to retrofit their buildings against known risks. In exchange, the utility would secure the right to charge building owners a monthly loan repayment on regular utility bills, or the municipality could apply surcharges on property tax bills to recover their loan. In both instances, they would likely charge interest to the building owners on the loaned balances.

If the utility or municipality would like to immediately access a large part of the future revenue stream from these loans to invest in a resilience upgrade of the whole system or district, then it might structure the pool of loans into a secondary financial instrument. Private investors could take ownership of the secondary or “structured” instrument and provide the utility or SPV with an immediate payment that is equivalent to part of the total discounted revenue stream predicted over the term of the pool of loans. This advance payment on the loans could be used for resilience upgrade investments.

c. Insurance, re-insurance and catastrophe bonds

Insurance provides an important instrument for reducing the extent of possible losses to those who would otherwise want to invest and hold assets in a risky city district or urban infrastructure system. In this sense, insurance is a very important financial instrument when seeking to mobilize additional capital for any kind of city building.

Consider the likelihood that a resilience upgrading project would not be able to economically reduce some of the area’s catastrophic risks. Prospective investors, whether in conventional projects or in special risk reduction measures, may not be willing to invest if the catastrophic risk cannot be mitigated. In this instance, a customized insurance policy could provide the prospective investors with a way to manage those extreme risks, thereby making their other investments attractive.

Re-insurance further spreads the risk of major losses by sharing parts of the insurer’s risk portfolio with the secondary insurer. Re-insurance allows an insurer who holds thousands of policies to select the exact portfolio of risks that it wishes to manage and those losses for which it will be directly liable, passing on the remaining risks to the re-insurer for a contracted premium.

It is important to note that insurance instruments are not conventionally used to generate revenues for mitigation of the insured risks. In other words, the proceeds of insurance policy sales are not reinvested in risk reduction measures associated with the policy, but are instead invested in more conventional instruments that generate profits for the insurer while maintaining liquid assets to cover possible policy losses. However, a proven quasi-insurance instrument – the catastrophe bond – could conceivably be used to create a pool of capital for direct investment in risk reduction measures.

Catastrophe bonds were first developed by insurers in the early 1990s in response to the increasing strength of hurricanes striking highly urbanized southern Florida, causing losses significantly above the levels that insurers were willing to bear. A catastrophe bond passes the insurer’s extreme risks onto a variety of private investors who are willing to assume the risk of losing all investment principal (in the instance of a defined catastrophic condition) in exchange for the opportunity to earn substantial interest on their investment if no catastrophe occurs.

Following the introduction of catastrophe bonds by the insurance industry, governments started issuing their own catastrophe bonds to cover losses from extreme national crises. For instance, in 2006 Mexico issued catastrophe bonds to establish a pool of funds to respond to and recover from major earthquakes. In 2009, the World Bank established a Multi-Catastrophe or “MultiCat” programme to help governments structure “coverage” against multiple kinds of catastrophe risk, or to pool the risks of multiple governments through the issuance of a special bond. Mexico was the first government to issue a bond to cover extreme losses due to earthquake, flooding and tropical storms.

A major innovation in the MultiCat approach is the pooling of specific classes of risk or risks across a number of countries. In 2007, the insurer Allianz issued a US$ 150 million “flood bond” to insure property owners in London against losses associated with an extreme flood event. The bond was viewed as a specific response to the increased flood risks associated with climate change.(17) A further innovation might be to use the catastrophe bond instrument to cover a portfolio of

The current uses of catastrophe bonds are passive; that is, proceeds are held in managed funds for a “rainy day” event against which catastrophic losses could be claimed. In the meantime, the funds invest the proceeds to generate a return. Interest is paid from the funds to investors for each year that a catastrophe, of specified severity and conditions, does not occur. In this sense, the bonds do not serve to reduce risks or prevent catastrophe.

An actively structured catastrophe bond would use part of the proceeds from sales of the bond to implement measures for which there is a record of reliable risk reduction effect at a predictable range of cost. By using proceeds from the bond to reduce the risk of triggered payouts to the covered cities, the interest payments demanded by investors could also be reduced, and the issuer of the bond could maintain a balance of funds to generate its own financial returns and to cover future claims against the bond.

d. Social impact bonds

Social impact bonds are a particular kind of “active” bond, which is structured to generate proceeds to finance specific measures intended to reduce a social ill, cost or risk. For instance, in the United Kingdom a social impact bond was issued to generate funds to finance social agency efforts to reduce recidivism by convicted criminals of specific types of crimes. The bond was structured in such a way that the relevant government department would pay proceeds to the bond issuer for each offender who was prevented from re-offending. The proceeds were calculated as part of the cost that would be borne by the government should there be a re-offence.

Such a bond only works when there is considerable predictability that a group of agencies has established the capacity to implement reliable measures to reduce the risk, and to do so at a cost that is less than the cost of the risk event. The cost savings can thereby be predicted, and the investor, the issuer and the government department can negotiate the sharing of the savings. There is no reason why the same kind of instrument could not be used to mobilize resources for climate risk reduction measures should the above conditions be met.

e. Climate adaptation funds

Finally, we argue that government-secured debt and grants from the international adaptation funds will be necessary for three main purposes. The first is to finance technical support and development of the local institutional infrastructure for upgrading – such as SPVs and national development banks – and to support the mainstreaming of resilience as a new and core value proposition in the property development process. The second purpose is to finance early resilience upgrading demonstration projects in carefully selected zones of representative cities, thereby assuming risk from the early pioneers of resilience upgrading and of associated new financial instruments. Finally, once these pioneers’ innovations begin to diffuse to other cities and into industry, there may be particular types of risk reduction measures for which no market-based investment proposition can be established. The funds could be used to finance these particular measures within the context of comprehensive resilience upgrading projects.

v. Conclusions and Next Steps

The strategic framework offered in this paper provides a way to map key areas for innovation and programmatic action to scale local climate and disaster risk reduction. When it comes to new-build and facility-specific retrofits, the development assistance community, local governments and NGO and private sector partners need to focus resources on mainstreaming climate and disaster risk reduction as factors in conventional development planning, project design and development regulation. When it comes to comprehensive redevelopment of urban areas or systems, the development community and its partners might focus resources on developing local institutional capacity to prepare, structure and manage comprehensive redevelopment projects. At the same time, further support could be provided to develop and demonstrate specialized financial instruments for the riskier components of these projects, to which finance cannot be attracted via mainstreaming measures.

The proposed focus on establishing sufficient local mainstreaming efforts, as well as a pipeline of quality resilience upgrades and associated demand for new financial offerings, suggests the need for a major programmatic initiative. This initiative, akin to global efforts such as Local Agenda 21, City Development Strategies, Cities for Climate Protection or major disease eradication programmes, could initially be constituted in the form of an “alliance for resilient cities” consisting of local governments and their support institutions, to develop the project pipelines, corporate partnerships and financial service providers to develop new financing solutions.

The initial focus of such an alliance could be to implement some comprehensive resilience upgrade pilots, including investment and financial planning, to better understand the financial aspects of these projects. The initiative would also identify instruments that could offer the necessary mix of financing solutions required to implement a truly comprehensive upgrade. On the basis of such pilots, the associated planning process could be more widely diffused and applied. The alliance could then focus – presumably with solid international adaptation fund support – on scaling resilience upgrading across the world’s vulnerable urban areas.

Footnotes

1.

Brugmann, J (2011), Financing the Resilient City: A Demand-driven Approach to Development, Disaster Reduction and Climate Adaptation – An ICLEI White Paper, ICLEI Global Report, Bonn, 48 pages.

2.

The term “slum” usually has derogatory connotations and can suggest that a settlement needs replacement or can legitimate the eviction of its residents. However, it is a difficult term to avoid for at least three reasons. First, some networks of neighbourhood organizations choose to identify themselves with a positive use of the term, partly to neutralize these negative connotations; one of the most successful is the National Slum Dwellers Federation in India. Second, the only global estimates for housing deficiencies, collected by the United Nations, are for what they term “slums”. And third, in some nations, there are advantages for residents of informal settlements if their settlement is recognized officially as a “slum”; indeed, the residents may lobby to get their settlement classified as a “notified slum”. Where the term is used in this journal, it refers to settlements characterized by at least some of the following features: a lack of formal recognition on the part of local government of the settlement and its residents; the absence of secure tenure for residents; inadequacies in provision for infrastructure and services; overcrowded and sub-standard dwellings; and location on land less than suitable for occupation. For a discussion of more precise ways to classify the range of housing sub-markets through which those with limited incomes buy, rent or build accommodation, see Environment and Urbanization Vol 1, No 2 available at ![]() .

.

3.

Sipkin, S A, J R Filson, H M Benz, D J Wald and P S Earle (2006), “Advanced national seismic system delivers improved information”, Eos Trans. AGU Vol 87, No 36, page 365.

4.

Science Daily (2008), “California has more than 99 per cent chance of a big earthquake within 30 years, report shows”, 14 April, accessed 1 November 2010 at ![]() . The report concludes that California faces a 99 per cent chance of a 6.7 magnitude earthquake and a 46 per cent chance of a 7.5 magnitude or greater earthquake by 2040.

. The report concludes that California faces a 99 per cent chance of a 6.7 magnitude earthquake and a 46 per cent chance of a 7.5 magnitude or greater earthquake by 2040.

5.

Burton, C et al. (2009), Building Resilient Communities: Risk Management and Response to Natural Disasters through Social Funds and Community-driven Development Operations, The World Bank, Washington DC, page 9.

6.

Abramovitz, J (2001), “Unnatural disaster”, Worldwatch Paper No 158, Worldwatch Institute, Washington DC, 31 pages.

7.

Mileti, D (1999), Disasters by Design: A Reassessment of Natural Hazards in the United States, Joseph Henry Press, Washington DC, 335 pages.

8.

See reference 5. The Hurricane Katrina disaster caused nearly 800 deaths, a loss of more than 90,000 jobs and US$ three billion in lost wages in New Orleans alone during the first 10 months following the disaster. Floods and landslides in Rio de Janeiro and São Paulo in early 2011 left more than 800 dead and 20,000 homeless. That same year, Cyclone Yasi created more than US$ 20 billion in losses in Australia due to flooding alone, a large percentage of this in urban areas. See Neligan, M (2011), “Australian flood loss could total US$ 20 billion: Aon”, Thomson-Reuters, 6 February.

9.

Estimated costs of managing climate-related risks vary by a factor of two to three from the UNFCCC’s own wide-ranging 2007 global estimate of US$ 49–171 billion per annum by 2030.

10.

World Bank representatives cited this figure extensively in their public statements during the COP 16 in Cancún. The figure is further cited on the World Bank website at http://climatechange.worldbank.org/content/new-report-sees-cities-central-climate-action, referencing the report by Hoornweg, Daniel et al. (2010), Cities and Climate Change: An Urgent Agenda, The World Bank, Washington DC.

11.

Woetzel, Jonathan, Lenny Mendonca et al. (2009), Preparing for China’s Urban Billion, McKinsey Global Institute, accessed 21 March 2011 at ![]() , pages 16 and 115. Note that the report defines urban fixed investment as primarily “…construction and purchases of fixed assets in cities.”

, pages 16 and 115. Note that the report defines urban fixed investment as primarily “…construction and purchases of fixed assets in cities.”

12.

China will account for an estimated 23 per cent of the global urban population growth during 2005–2025. The cited figures on urban population growth are drawn from United Nations, Department of Economic and Social Affairs, Population Division (2010), World Urbanization Prospects, the 2009 Revision, accessed 26 April 2011 at ![]() .

.

14.

The Global Environmental Facility (n.d.), Financing Adaptation, accessed 6 October 2010 at ![]() .

.

15.

Moon, K, N Downes, H Rujner and H Storch (2009), “Adaptation of the urban structure type approach for vulnerability assessment of climate change risks in Ho Chi Minh City”, E-Proceedings: 45th ISOCARP Congress 2009 on Low Carbon Cities, The Hague, pages 2–4, accessed 9 December 2010 at ![]() .

.

16.

It is important to note that where these special purpose companies are given both very broad authority and a long-term operating licence, their record has been more mixed due to governance issues related to their greater independence and reduced accountability to the public. There are many stories of bureaucratic inefficiency, land speculation and poor execution associated with such broadly defined, permanent entities.

17.

Tett, G and A Felsted (2007), “Insurers launch ‘London flood’ bond”, The Financial Times, 10 April, accessible at ![]() .

.