Abstract

Different public-private partnerships may exhibit various characteristics, yet we understand little about the impact of imbalanced power dynamics among partners on the success or failure of partnerships. This study focuses on the private actor, an incumbent bank coerced into a collaborative governance configuration aimed at addressing the wicked problem of fighting financial crime. We investigate the response strategies of organizational members to examine the impact of when hybridity is enforced, meaning that organizations are driven by a multiplicity of values and objectives. We organize these strategies in two narratives: first, organizational members respond with a strategy of separation in resisting the integration of public values; second, organizational members respond with a strategy of transcendence by aiming to resistors to adopt their belief system. The ongoing struggle with the enforced hybridity reveals the dark side of public-private partnerships as members grapple with involuntary changes that threaten the private and commercial objectives of the bank. Our key message is that when private and public actors are involved in forced collaborations, the guise of a reputable, collaborative relationship may be used to conceal negative aspects and power imbalances, which helps to overcome resistance and elicit compliance.

Keywords

Introduction

The growing complexity and competing demands of public tasks necessitate the development of modified forms of governance (Lienhard, 2018), including public-private partnerships (PPPs). Despite debates surrounding the definition of a PPP (Hodge and Greve, 2007), it is generally understood as a voluntary and mutually beneficial collaboration aimed at creating social or economic value through the combination of public and private actors’ complementary skills (Quélin et al., 2017; Villani et al., 2017). Effective collaborative governance is contingent upon aligning individual and collective perspectives into shared understandings (Bevir and Rhodes, 2016) and fostering relationships of mutual trust, understanding, commitment and reciprocity, which require considerable time, effort, and skill (Bartels and Turnbull, 2020; Head and Alford, 2015). Collaborative relationships are critical for addressing wicked problems as multiple parties can leverage a broad and diverse knowledge base, interests, and values (Head and Alford, 2015). PPPs are therefore often viewed as a panacea for the crisis-ridden world (Nayak, 2019) by providing more efficient and effective structures for achieving public tasks and goals (Takano, 2017).

However, not all partnerships are the same. The usage of the term PPP may lead to a false sense of commonality between public-private cooperative efforts that have significant differences in characteristics affecting their success or failure (Schaeffer and Loveridge, 2002). In fact, not all PPPs are voluntary and based on mutual trust and understanding, as is the case with the efforts aimed at addressing the wicked problem of fighting financial crime, where banks are required to participate through government-imposed legislation and the threat of substantial fines for noncompliance (Favarel-Garrigues et al., 2011). Unlike the private sector, which mostly relies on persuasion and the directional power of capital, the public sector has the power to enforce compliance with its plans (Schaeffer and Loveridge, 2002). Yet, the impact of power dynamics among actors on the efficacy of public-private collaborations is not well understood.

One of the challenges banks face during the transition to being a compliant partner in the PPP is reconciling the private objective of profitability with the public objective of safeguarding society. However, the public objective entails a cost-compliance burden that paradoxically interferes with banks’ private goal of maximizing returns (Balani, 2019). These conflicting objectives reflect the status of banks as hybrid organizations. Hybridity refers to organizations driven by a multiplicity of logics, identities, forms, or other core elements within the organization that are often incompatible and paradoxical (Skelcher and Smith, 2015; Smith and Besharov, 2019). The general consensus is that organizations benefit from sustaining hybridity by striking a balance or creating synergy between the multiple tensions, identities, forms, or logics (Pratt and Foreman, 2000; Smith and Besharov, 2019). Response strategies, such as separation, connection, and transcendence, have been proposed as ways to do so, with the latter being less explored (Andriopoulos and Lewis, 2009; Bednarek et al., 2017; Smith and Lewis, 2011).

The main objective of this paper is to gain a better understanding of organizational members’ response strategies to paradoxical tensions resulting from hybridity enforced by the public actor, in order to provide insights into the success and failure of public-private collaborations aimed at addressing wicked problems. In this single case study, we collected data from semi-structured interviews, observations, and archival sources at an incumbent bank in the Netherlands. Adopting a ‘decentered’ approach to governance, which assumes that governance arises from the bottom-up and “actions arise from the beliefs that individuals adopt” (Bevir and Rhodes, 2016: p. 5), we examine the perspective of the private actor in a PPP addressing a wicked problem to gain further insight into the actor-positioning process. Our research question is as follows: “How do organizational members of the private actor in a public-private partnership cope with and respond to enforced hybridity by the public actor?”

Our findings reveal two response strategies to enforced hybridity, which we describe in narratives – the typical form through which organizational members engage in sensemaking (Maitlis and Sonenshein, 2010). In the first narrative, organizational members produce separation responses as they resist the integration of public values. According to them, the paradox of private and public objectives cannot coexist in the bank. In the second narrative, organizational members respond with a strategy of transcendence, aiming to inspire the members of the first narrative to adopt their belief system. These members argue that the private actor must accept the hybrid status of banks and move towards a future in which they may regain a level of autonomy and agency over the bank’s actions. The ongoing struggle of the private actor with enforced hybridity reveals the dark side of public-private partnerships, underscoring previous findings that PPPs are no panacea to addressing wicked problems. We argue that when private and public actors are involved in forced collaborations, they may use the guise of a reputable, collaborative relationship to conceal the negative aspects and power imbalances of the collaboration. This concealment helps to overcome resistance and elicit compliance from organizational members of the private actor, as is demonstrated by the interplay between the first and second narrative. Ultimately, this study underscores the complexities of collaborative governance, where the exchange between various interests is not always straightforward.

Addressing wicked problems in PPPs

Rittel and Webber (1973) introduced the concept of wicked problems to describe a type of social problem that is ambiguous, continuously evolving, and characterized by multiple actors with conflicting values. Problems become ‘more wicked’ when complex and diverse situations trigger higher levels of uncertainty and ambiguity (Head and Alford, 2015). Although there is no clear criterion for resolving wicked problems, policy actors must assess their strategies to improve them, leading to the evaluation paradox (Termeer and Dewulf, 2019). To influence the private actor’s behavior in a public-private partnership, public actors may employ sanctions when the contractual obligations are not met, although formal contracts may not always influence the private actor’s operations (Klijn & Koppenjan, 2016). A recent study on collaborative governance in healthcare by Van Duijn et al. (2022) suggests that central policymakers have limited influence on shaping the private actor’s local landscape due to the various coping strategies that local actors employ. These findings suggest that the organizational members of the private actor maintain some degree of autonomy and agency within PPPs.

Research on PPPs has primarily focused on identifying the factors that contribute to the success or failure of partnerships, including drivers, lessons, experiences, best practices, challenges, obstacles, and barriers (Xiong et al., 2019). The majority of PPP research has concentrated on contractual issues in the infrastructure and construction sector (e.g., Van Marrewijk et al., 2008), the energy sector (e.g., Jay, 2013) and the health care sector (e.g., Villani et al., 2017). There has been comparatively little attention given to institutional issues concerning authority, regulation, and legislation in PPPs (Xiong et al., 2019). While PPPs are often viewed as a solution for achieving public goals and addressing crises (Nayak, 2019; Takano, 2017), they have also faced criticism for their inequitable allocation of risks, prolonged negotiation processes, and project accountability concerns (Chan et al., 2010).

Furthermore, while some scholars consider the public-private distinction a truism, others denounce the distinction and argue that public and private organizations are more alike than different (Rainey and Bozeman, 2000). Although some studies have found similar value systems between public and private organizations, such as accountability, expertise, and reliability (Van Der Wal et al., 2008), other studies have found that they operate on different institutional logics (Saz-Carranza and Longo, 2012). Although there are nuances to the public-private distinction in various ways, this paper focuses on the conflict of values, goals, and logics between private and public actors in PPPs.

Responding to paradox and hybridity

Wicked problems and grand challenges present a fertile ground for the emergence of paradoxes and hybrid configurations due to their complexity involving multiple disciplines, interests, and organizational actors (Jarzabkowski et al., 2019). Paradoxes are defined as persistent contradictions that can create seemingly irrational or absurd situations over time, as their continuity presents options as mutually exclusive and makes it difficult to choose among them (Putnam et al., 2016). Hybrid organizations are called “arenas of contradiction” by nature (Pache and Santos, 2013: p. 972) and are driven by a multiplicity of logics, identities, forms, or other core elements that may be to some degree incompatible within the organization (Skelcher and Smith, 2015; Smith and Besharov, 2019; Villani et al., 2017). Similarly, PPPs, as a form of hybrid organizing, give rise to ambiguities, subcultures, conflicts, and power struggles because they bring together competing partners, interests, values, and modes of rationality (Van Marrewijk et al., 2008). Generally, organizations are assumed to benefit from striking a balance or creating synergy between the various core elements, which requires active management and corporate governance (e.g., Denis et al., 2015).

Quélin et al. (2017) distinguish between hybridity in terms of governance and hybridity in logics. The first refers to public-private and cross-sector collaborations where assets, resources or competences are pooled, while the second refers to single organizations embedding multiple institutional logics. In our case, however, the collaboration with public parties has coerced the private organization of interest to internalize public logics; thus, we argue that taking the perspective of hybridity in logics is more appropriate while placing it in the context of a public-private collaboration.

As a response to hybridity, separation or differentiation concentrates efforts on one of the two poles of the paradox. Connection or integration, on the other hand, emphasizes the interdependence between the two seemingly opposing elements (Andriopoulos and Lewis, 2009). Transcendence, however, involves moving to a higher level of comprehension, in which paradoxical components are perceived as complex interdependencies instead of competing interests (Jarzabkowski et al., 2013; Lüscher and Lewis, 2008; Smith and Lewis, 2011). Through transcendence, paradoxes can be transformed into something more adaptable and practical by utilizing rhetorical practices (Bednarek et al., 2017). This practice of transcendence involves a constantly evolving dynamic balance of dualities, where the two poles are no longer separate but interdependent, mutually enabling and constituents of each other (Bednarek et al., 2017; Farjoun, 2010). However, the actual unfolding of transcendence and the generative mechanisms leading to such practices are relatively undertheorized (Bednarek et al., 2017).

In summary, the existing theoretical framework lacks clarity on how transcendence occurs in practice. Moreover, we have limited understanding of how response strategies to hybridity relate to resisting or accepting forced public-private partnerships aimed at addressing wicked problems, which could provide insight into the success or failure of such collaborations. Our study takes up this critical question, revealing how organizational members of the private actor respond differently to the need to balance paradoxical tensions created by enforced hybridity resulting from a forced collaboration.

Method

Case description

We ground our theoretical insights at ‘North Bank’ 1 , an incumbent bank in the Netherlands. As a result of the global financial crisis of 2007/08, the Dutch government saved the bank and still holds a small majority of the shares today. While this may suggest that the state holds more discretionary power in North Bank compared to other banks where the state is not a major shareholder, we consider the state’s power in North Bank to be equal to other banks on this specific topic. This is because the state, through legislation and regulatory reform following the financial crisis, has required all banks operating in the Netherlands to take the same measures. The law in question is the ‘Wwft’ (in Dutch: ‘wet ter voorkoming van witwassen en terrorisme financiering’), which outlines the expectations that the lawmaker has of financial institutions in preventing financial crime, also known as ‘the gatekeeper’s role’. This includes a list of requirements regarding client research, reporting suspicious transactions and transaction patterns, and taking proportional measures to estimate the institution’s risk of involvement with money-laundering and terrorism financing based on the institution’s nature and size. The Wwft also specifies the public parties responsible for overseeing the implementation, regulation, and enforcement of the collaboration, such as the Dutch Central Bank (DNB), the Authority Financial Markets (AFM), and the Minister of Finance. In recent years, the implementation of Wwft has led to a new ecosystem of initiatives and forms of collaboration between various parties and stakeholders concerned with undermining crime. All public and private actors involved consistently refer to the collaboration against financial crime as a public-private partnership in their official communication.

Data collection and data analysis

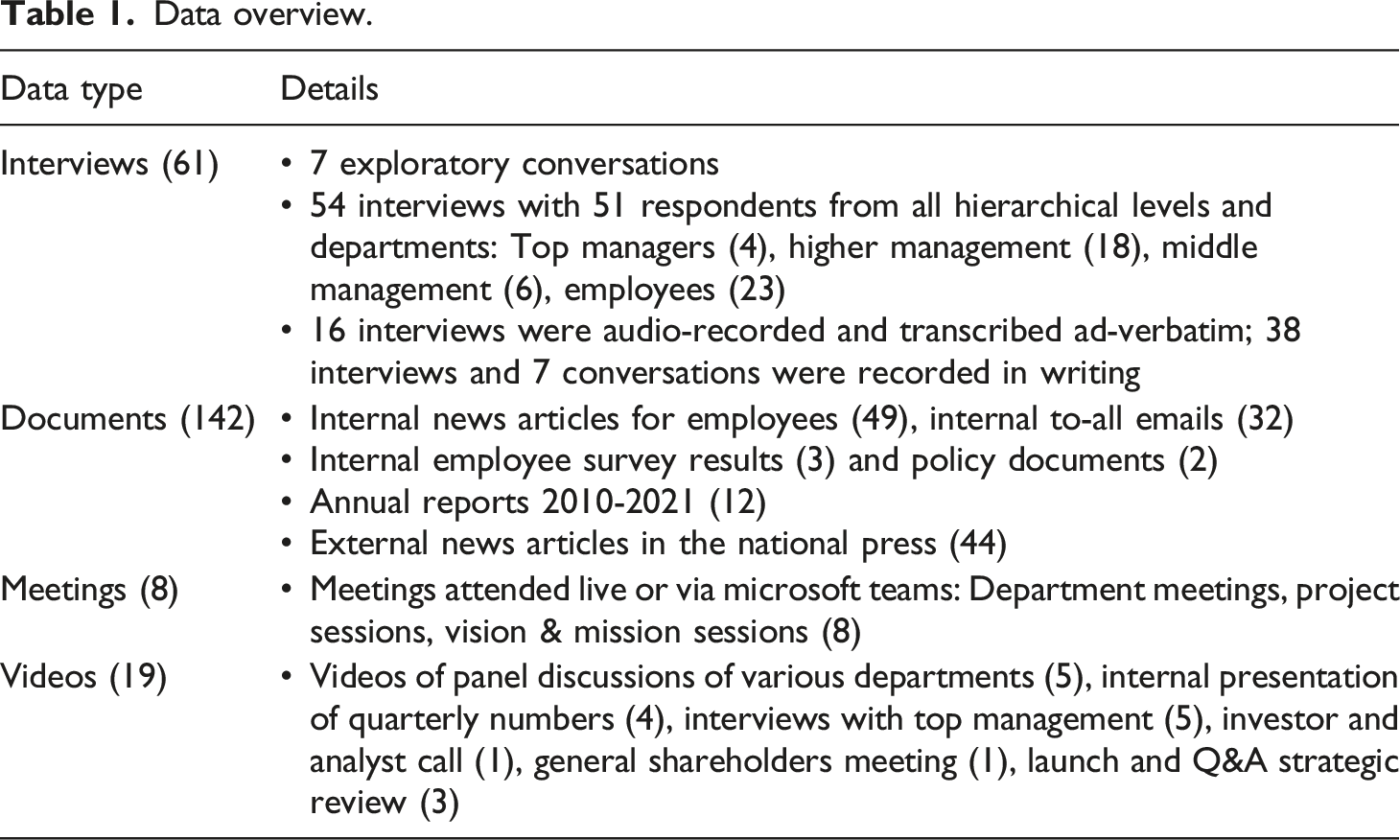

Data overview.

Given the persistent nature of interdependent contradictions inherent in paradox, it is crucial to incorporate a longitudinal element in data collection (Jarzabkowski et al., 2019). In line with this perspective, we draw on secondary data and included retrospective elements in our interviews, such as discussions about the genesis and evolution of the gatekeeper’s role over several years. Our main body of data was collected between October 2019 and September 2021, which was when we gathered interview and observational data.

For the selection of interview respondents, we employed various methods that corresponded to the different stages of our research project. Initially, we followed warm leads provided by an internal supervisor, engaging in exploratory and informal conversations to gain familiarity with the sensitizing concepts. Subsequently, respondents were selected using theoretical sampling, by searching the internal database of employees to ensure a diverse group of participants from different hierarchical layers and departments within the bank. Insights gleaned from earlier interviews informed subsequent ones, helping us to narrow down the topics of interest and explore the emerging theoretical puzzle. Out of the total database of 54 semi-structured interviews, we have directly cited eight interviews for this article.

Coding scheme.

Findings

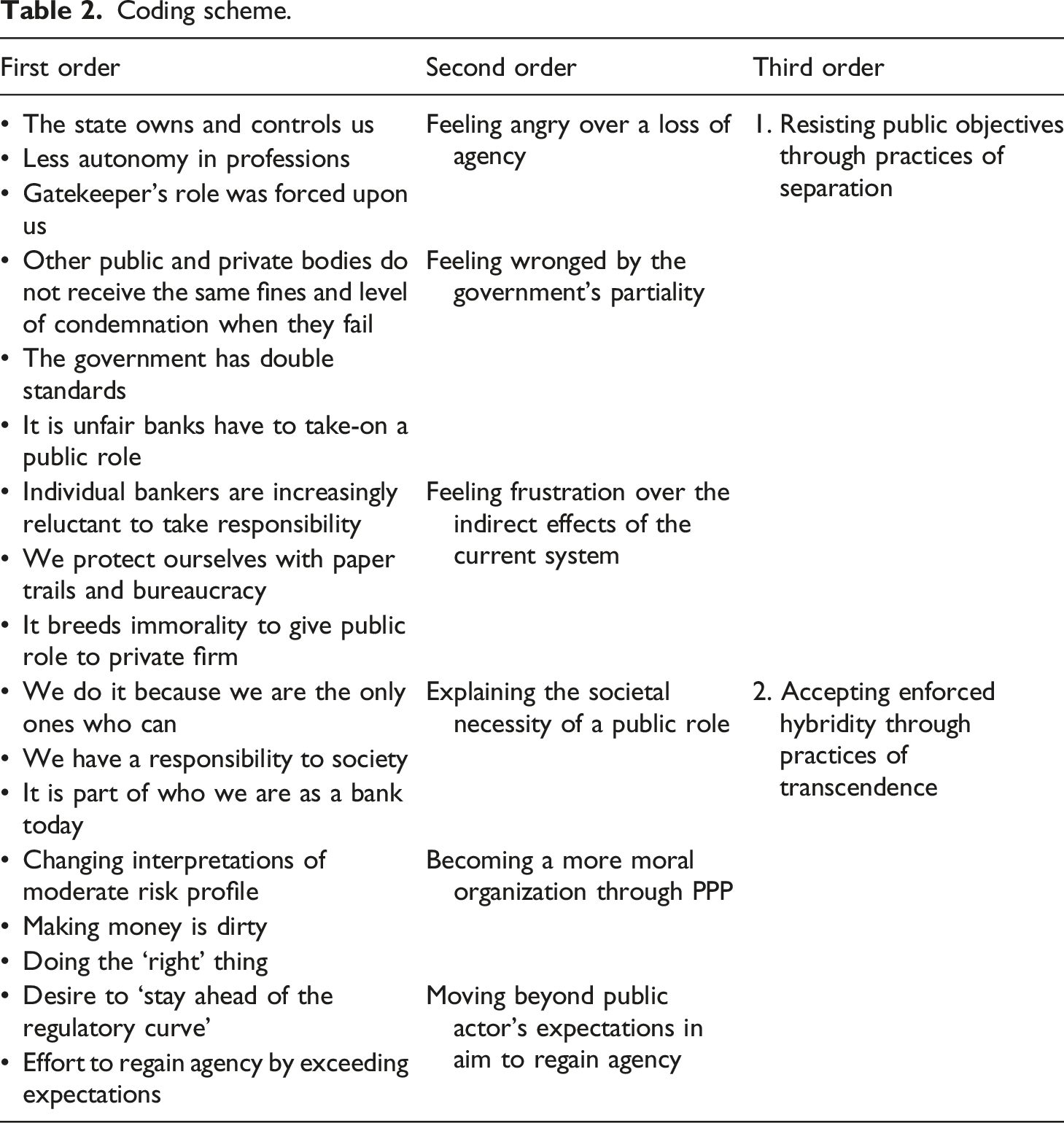

Resisting public objectives through practices of separation

In this section, we undertake an exploration of the range of discursive responses expressed by organizational members of North Bank as the organization grapples with the challenge of coerced hybridity, specifically, the increasing state regulation that raises expectations of the bank’s role in addressing the wicked issue of financial crime. Organizational members are found to be experiencing anger as a result of the loss of agency over the content of their professions, as well as the liberty to decide over the organization’s objectives which have been impacted by the imposition of the gatekeeper’s role on banks. Second, members are feeling wronged over the perceived maltreatment and injustice of the government’s partiality since public parties with a control task are not held to the same standards as private banks. Lastly, members express frustration over the ineffectiveness of the current system and PPP collaboration. To protect themselves from possible blame and punishment, bankers resort to employing paper trails and bureaucracy. Furthermore, private and public objectives are seen as conflicting and challenging, if not impossible, to merge. The separation of the two poles of the hybrid configuration is instigated by resistance against the integration of public logics and objectives enforced by the public actor in the PPP.

Feeling angry over a loss of agency

Stricter legislation and regulation concerning anti-money laundering and counter-terrorism financing have brought about various consequences for organizational members’ daily work. One such consequence is that the nature of some members’ job nature has changed due to stricter control, as expressed by one employee: “Since the crisis, the legislation increased to such a degree that my job has become much less about the core business and instead it’s all about the rules and demands. Before, I was able to make a free and subjective judgement about a client’s application, but now I merely have to judge whether it’s within the boundaries of the set policy. I don’t have as much intellectual freedom anymore. […] We don’t have any hard targets anymore either, because these are considered perverse incentives that led to too much risk-taking leading up to the crisis.” (R25, employee, commercial banking)

The strict adherence to rules and regulations has limited the freedom of some members to execute their profession as they see fit, leading to a sense of loss of agency. The perception of checks and controls on the tasks of financing specialists creates the illusion that personal judgement is no longer necessary, as everything has already been decided in policy or will be decided in commissions. Another reason for members’ experience of a loss of agency is the state takeover and the fact that the majority of stakes are still in the state’s hands today, as expressed by a middle manager: “I mean, really, we still belong to the state. […] It’s more about ‘minding the shop’ as senior management than—. The ECB is in control of the decisions. If you do a project, it will be passed along the executive board first, but it always has to be tested by the ECB. Every year, the bank gets a letter from the ECB with a supervisory summary of how they’ve been performing. The interference of the state and the supervisor is very profound. It’s really… They decide everything.” (R46, middle manager, private banking)

The pervasive role of the supervisor is emphasized, and with the recent history of being levied hundreds of millions of euros in fines, organizational members have become afraid of making mistakes in their personal name as well as in the organization’s name. One employee from commercial banking expresses resentment against the bank’s decision to fully take on the public role of catching criminals and the inability to turn this imposed gatekeeper’s role into something that is commercial and more aligned with the bank’s private objectives: “It seems as if KYC has become our core business. The supervisor forced this role on us through all sorts of fines. And then we announce we not only want to comply to the regulatory demands, but we actively want to hunt down criminals! Well, then I think to myself: you should get a job with the police. And no one is even challenging the government on this. We just do it, even though it costs us loads of money. Then at least think of a business model around this. Maybe we can offer clients a passport that says: I have been approved by North Bank so I can be onboarded more easily at other financial institutions. Where is the creativity?” (R36, employee, commercial banking)

This respondent shows resentment against members of the bank who want to fully take-on the public role of catching criminals, as well as resentment against the inability of the bank to turn this imposed gatekeeper’s role into something that is commercial and therefore more in line with the private objective of the bank.

Feeling wronged by the government’s partiality

Organizational members deflect their responsibility for the gatekeeper’s role in highlighting public organizations with a control task who fail to take protective measures for civilians: “[The government] has double standards. I used to work for the tax authorities in Rotterdam which included customs, the control of all incoming goods in the port of Rotterdam. And, you know—don’t think for a second it’s waterproof. The system is as leaky as a sieve. Now and then they catch something, so just imagine what passes through on a given day. And that’s a gatekeeper’s role, a governmental one. Then consider their negligence and it not having any serious consequences, no personal ones either, and you compare it to the manhunt at South Bank. They must pay hundreds of millions of euros in fines and a top manager has to fall. Well… It’s just exorbitant. So yes, I see a discrepancy in the highest order. I think we as banks currently employ more people to stop money laundering than the number of people the tax authorities employ altogether. That’s pretty absurd.” (R40, higher manager, finance)

The notion of double standards is evident in the perception of a higher manager in the finance sector, who suggests that the government is biased in punishing private entities for their failures while exempting public agencies from such consequences. The manager draws a comparison between the gatekeeping role of the tax authorities and the financial institutions, emphasizing that while the latter are penalized heavily for any slip-ups, the former is spared of any repercussions despite their failure to discharge their duties efficiently.

This bias is further evident in the public-private collaboration to fight financial crime, where public parties are not held to the same standards as banks. During a roundtable discussion held at North Bank in September 2020, high-placed members in the detecting financial crime department, the CEO of North Bank, the head of the department of supervision integrity risk at DNB, and a host, discussed challenges related to the PPP. When presented with the fact that Dutch banks reported 39,900 unusual transactions to the Financial Intelligence Unit (FIU), but only a small portion of these reports were processed, the head of the DNB attributed this to a shortage of resources in the detection and prosecution chain: Head DNB: “Well, it’s a chain. Three to five years ago, the issues were at the beginning of that chain. That is: the financial institutions that weren’t fulfilling their obligation to report. Now, the problem has shifted to the FIU that has trouble handling the number or reports. Detection capacity is also falling short.” Host: “How many people work there [at FIU]?” Head: “Hundreds.” Host: “So the banks hired thousands of people to make detections, but only a few hundred people are available to follow up on them?” Head: “Yes. […]” Host: “[…] I’m a layman, but I think it’s strange that we’re rallying up everyone at the banks without having people on the back end to actually catch the criminals.” Head: “Too few people, yes. Just this week, the Noordanus committee published the advice to the government to spend 400 million more on undermining financial crime and to direct most of it to detection and prosecution. There is just not enough money there.” Host: “Isn’t that a little discouraging? […]” Head: “I don’t think so because this is not the only reason that banks do this work. It should be gratifying in itself to have detected a questionable client. A client whose actions are unusual, dubious, or downright criminal and whom the bank will no longer serve. Or to detect such a client at the gate and choose not to do business with them. There’s a sense of pride in that.” (Observation panel discussion, 26/09/2020)

The head’s explanation suggests that banks are coerced to hire more employees to improve their gatekeeper’s role while public parties responsible for further processing the reports are unable to handle them due to a lack of monetary resources. However, the head of the DNB argues that the mere detection of a questionable client should be gratifying in itself, despite the lack of follow-up. The costs associated with the improvement of the detection system are borne by the banks themselves. Overall, this situation highlights the double standards in the treatment of private and public entities with a control task.

Feeling frustration over the indirect effects of the current system

Moreover, the efforts of banks to combat money laundering and terrorist financing can have unintended consequences and cause frustration among organizational members. One such consequence is the increased inefficiency and laboriousness of the client onboarding process: “With our mortgage label we do the screening of new clients. We created an entire apparatus to help us with that. It’s costing a lot of effort without actually detecting any number of clients worth mentioning that are overstepping the law. So, it’s an extremely drastic remedy. In our line of business, certainly, there are very few clients that do anything wrong.” (R41, higher manager, mortgages)

This higher manager expresses concern about the cumbersome screening process, which, despite its efforts, is not detecting any significant number of clients breaking the law. Another source of frustration is the disciplinary laws in place at the bank to ensure that organizational members adhere to the expected standards, which also have an indirect effect: “What you see happening is that bankers are growing reluctant to take responsibility for clients. […] We have disciplinary laws, so many people are afraid to make decisions by themselves out of fear to break the rules and, since there are so many rules, it is easy to break one. So, we created a risk assessment form that has 321 questions for the client. What you see in an organization like ours, is that nobody wants to be accountable anymore. That leads us to make these extensive forms and that we record every single thing we do.” (R50, higher manager, risk and ethics)

The strict penalties imposed to comply with new regulations result in organizational members being more hesitant to take responsibility and be accountable for their actions. Furthermore, the lack of clarity regarding the expectations from banks is also cited as a reason for this hesitance: “It is precisely because of the large volume of legislation and the fact that there is not enough clarity about what do we accept, what does the supervisor accept, what do politics accept from us, that we are afraid to take any accountability at all and that we completely detach” (R50, higher manager, risk and ethics).

Finally, an additional indirect consequence of how banks perform their gatekeeper role is the risk of “unbankables” – individuals who are unable to open a bank account anywhere. This is caused by a conflict of interest arising from the dual nature of the bank: “In its core, the bank is a commercial firm, so that gives rise to a conflict of interest. Because high-risk clients, but also all the related costs to high-risk clients that you make in order to fulfil the gatekeeper’s role, comes at the price of the bank’s profitability. The biggest risk, if you ask me, is when you have these high-risk clients that may be completely honest people, but they are trading with Sudan or Afghanistan, and we exclude them even though they may be doing great things. You get the risk of the unbankables. And with that you lay a lot of responsibility at the hands of a commercial party that has another interest as well. Additionally, for us, efficiency is key. We can use AI to screen our entire customer base for suspicious transactions (...). I would personally have more faith in a public party or independent body to give shape to these processes than when you give it to banks.” (R50, higher manager, risk and ethics)

As a private institution, banks prioritize low costs and efficiency, which may mean that they sacrifice their public objective of acting in the best interests of every citizen. Instead, they aim to serve the interests of most civilians while remaining cost-effective, efficient, and compliant with the law. The higher manager suggests that the responsibility of shaping these gatekeeping processes should be entrusted to a public entity or an independent body rather than to banks.

2. Accepting enforced hybridity through practices of transcendence

In this section, the transcendence practices expressed by top management and higher management of the compliance and financial crime detection departments are presented. The first practice involves reordering the bank’s priorities and objectives to make the public objective of protecting society from financial crime an integral part of the bank’s identity. The second practice aims to align the bank’s logics with public logics, which emphasize moderation and morality, in contrast to the private logics of profitability and commerciality that have historically driven the bank. The final practice aims to provide organizational members with a vision of the future where the bank’s activities are no longer dictated by external regulators, as the bank will fully comply with all regulations and thus regain a level of freedom and agency. These practices work towards a process of incorporating public values and objectives alongside private ones. In the absence of alternatives, the CEO of North Bank presents a narrative that transcends the either/or dichotomy of public and private logics and objectives, resulting in a both/and duality.

Explaining the societal necessity of a public role

In this passage, the importance of banks embracing the gatekeeper’s role is discussed. The primary rationale for doing so is the bank’s responsibility to society, as described by the CEO: “Another key aspect to the work we do is not just sticking to the law but knowing your social responsibility. The law is the foundation and the framework. But ever since the inception of the banking system, we as banks have had—in the past, we still have it now and we will always keep it—a responsibility to society. That’s why the law was drawn up the way it is. That touches on the core of who you are and what you stand for, and it serves to protect yourself, society, and your clients. It’s extremely important.” (CEO, observation panel discussion, 26/09/2020)

Here, the CEO posits that adherence to the law is only the starting point, and that the bank’s social responsibility is a fundamental aspect of its identity. As a result, adapting to evolving expectations of the gatekeeper’s role is a logical next step. The CEO notes that rather than apportioning blame, there is still much to be learned by all parties in the collaboration, and finding the right balance will remain a focal point.

The CEO provides a response to organizational members who express concern about the potential for ongoing increases in demands from the state on banks for detecting financial crime. The CEO takes the opportunity to explain the necessity of the bank’s work, stating that while it may not be possible to fully prevent financial crime, the bank’s oversight of its clients’ financial streams provides an opportunity to report suspicious transactions: “And some of you [employees] may wonder, will it ever be enough? Let me tell you. We, as a bank, will never be able to fully prevent financial crime. But the fight does start with us. If the bank has oversight over the financial streams of our clients, it is our duty to report suspicious transactions. Organizations such as the FIOD [fiscal information and investigation service], the OM [public prosecutor] and the police don’t have that information. But we do. If we perform well on our gatekeeper’s role, the investigative services are more capable of tracking down criminals. […] That’s how we work together towards a common goal: a trustworthy financial system and a safe society. […] The most important task of the bank, our bank, is to live up to the trust that our clients give us.” (CEO, quarterly meeting, 19/04/2021)

By reporting suspicious transactions, the bank can work together with public investigative services to track down criminals and contribute to the shared goal of a trustworthy financial system and safe society. Moreover, the CEO notes that public parties are unable to access transaction data due to privacy legislation, underscoring the critical role that the bank plays in detecting financial crime. The CEO further justifies the bank’s involvement in detecting financial crime by emphasizing its importance and necessity: “I think it is only reasonable we do it. We are in the middle of attuning the various processes now, and we hope it doesn’t just feel like an administrative burden but that we realize it’s part of being a banker in this day and age. It is a part of what we do and who we are. And that is the essence of the gatekeeper’s system. And with that, you fight financial crime.” (CEO, quarterly meeting, 19/04/2021)

The CEO emphasizes the importance of being compliant with regulations while acknowledging that the process can be burdensome. By presenting the bank's gatekeeper role as an essential part of its identity, the CEO aims to persuade employees to see it as a crucial aspect of their work.

Becoming a more moral organization through PPP

The bank’s integration of the gatekeeper’s role and its incremental integration of public objectives are reflected in various ethical initiatives. One of these initiatives is a revised interpretation of the bank’s moderate risk profile: “After the financial crisis, the bank decided to take on a moderate risk profile. That hasn’t changed in recent years. But what has changed is the interpretation of that profile over time. Sometimes business lines may combine low-risk activities with high-risk activities, so overall, the average will be moderate-risk. And now you can see that the bank is now stepping away from that practice and no longer wants activities that are high-risk or that don’t comply to the principle of moderate-risk.” (R48, higher manager, regulatory execution team)

The bank’s decision to refrain from engaging in high-risk activities, as opposed to offsetting them with low-risk ones, is an adaptation of its business practices to a model that aligns better with public values, such as stability and safety.

A second instance in which the integration of public logic is visible is the CEO's discussion of the bank’s moral responsibility to detect financial crime and doing ‘the right thing’, particularly in light of the hundreds of millions of euros in fines imposed on the bank: “The total sum of the fine reflects the severity of our shortcomings. We failed dramatically in our role to combat money laundering. As a bank, we have an important role to protect our financial system from crime. And as we often say, we don’t just do that because it is our legal obligation. It is, above all, our moral responsibility to keep society safe. It hurts us that we, as a bank, have fallen short in our gatekeeper’s role. We haven’t lived up to society’s expectations. And yes, that is unacceptable, it shouldn’t have happened and therefore we offer our sincerest apologies today to our clients and to society.” (CEO, quarterly meeting, 19/04/2021)

The CEO’s apology to clients and society demonstrates the bank’s embracement of the need to become a more moral organization. By acknowledging its failures and apologizing to clients and society, the bank is taking responsibility for its actions and committing to doing better in the future. Another example that reflects a shift in morality within the bank is the declining emphasis on making revenue, as noted by a middle manager: “We have to make money, but actually you don’t really hear anyone talk about that anymore. It is more about, oh, oh, we planted these trees in Flevoland, instead of, we just landed three big corporates and we have a three million revenue on each of them. You hear no one about that.” (R46, middle manager, private banking)

This change in focus from maximizing revenue to acting in the best interests of society is indicative of a broader shift in organizational values. As one compliance manager notes: “Ten, fifteen years ago, we were condemned for only having financial interests at heart, so now we are looking for a different purpose that may not immediately bring money to the bank. We are longing for a positive story or a positive narrative in the sense that we don’t only want to be on the news for the fines we have received et cetera, but we would also like to reach the news once in a while for things that we actually did do right.” (R01, middle manager, compliance)

By prioritizing their gatekeeper’s role and emphasizing their contribution to society, the bank can rebuild its reputation and gain a renewed appreciation from the public.

Moving beyond public actor’s expectations in aim to regain agency

The eagerness of some members in North Bank’s detecting financial crime department to exceed the current expectations of banks in fulfilling the gatekeeper’s role is noteworthy. This is illustrated in the following account of how members communicate with their supervisor: “During our conversations [with the supervisor], we sometimes discuss the dilemma’s that we face. But you can tell there is little space to… to negotiate whether we’re going to comply to the legislation yes or no. What we can do is to be transparent about the maturity level that we want to achieve in order to comply. So, we can implement a certain type of legislation, and we can either do the least that is necessary in order to comply, or we can say as a bank: no, we want to be the best at what we do. […] The supervisor also demands that we come up with our own plan. In practice, however, we often end up in a situation of ‘over-promising’ and ‘under-delivering’, because we place the bar too high for ourselves.” (R48, higher manager, regulatory execution team)

By exceeding expectations, members seek agency by determining the level of maturity they will deliver, given that they have no say in other aspects of compliance. An additional instance of incorporating public logic regarding detecting financial crime becomes evident in a panel discussion where the bank’s head of detecting financial crime is asked by the host whether the primary aim is compliance and avoiding penalties or actually catching criminals. The head responds: “I want the latter, and we must also do the former. I can’t promise to do the latter without abiding to the law in a transparent way. We have to do both. It’s hard, but it’s a great challenge for me as a professional. I have to do the right thing for the bank in all those arenas. And we’re doing well.” (Observation panel discussion, 26/09/2020)

This citation illustrates that the bank not only aims to comply with regulations and avoid penalties, but also strive to assist in tracking down financial criminals. By adopting a proactive approach to detecting financial crime, the bank is demonstrating a commitment to fulfilling its gatekeeper’s role.

A similar ambition is reflected in the pursuit of a so-called ‘license to operate’ from the supervisor, which is contingent upon the bank’s effectiveness in fulfilling the gatekeeper’s role while remaining compliant with regulations. As one higher manager explains: “Our ‘license to operate’ means to do as much as we are ordered to do to comply to the legislation and at the same time satisfy the expectations that our stakeholders have of us. […] And in the core of that is really to comply to legislation and regulations” (R50, higher manager, risk and ethics). If banks can meet the expectations set by regulators, they may be granted a degree of autonomy, referred to as moving from a ‘license to operate’ to a ‘license to grow’: “At the moment we comply entirely with what is expected of us, […] if we have that license to operate, and we do well, then some of the limitations that the DNB has put on us will be removed. You have to imagine that because of that license to grow, and because we don’t have all of our files in order and we don’t fully comply yet, the DNB requests that we maintain a higher capital buffer for the risks that we are taking for our ‘bad policy’. Because not complying could mean we have to pay a fine at some point or we may need to invest in correcting our files in the future and so on. And that buffer means we cannot use that money to invest in better products, efficiency, or better systems to service our clients.” (R50, higher manager, risk and ethics)

When the bank is deemed fully compliant by the supervisor, some of the current limitations on banks can be relaxed, allowing the bank to regain its lost agency. It is perceived to be the only way forward: “It is not going to go away; it is going to stay with us. That’s why I hope that our license to operate will be our license to grow. Because when we do that right, we can actually get there” (CEO, observation investor & analyst call, 11/11/20). Achieving full compliance with regulatory standards will ultimately enable private actors to refocus on private objectives again.

Discussion and conclusion

Our research investigated how the private actor in collaborative governance navigate the challenges and opportunities presented by the bank’s transition towards becoming a hybrid organization enforced by the public actor. This transition requires the bank to balance the private goal of profit maximization with the public objective of contributing to societal protection in the context of combating financial crime. By examining the experiences and response strategies of these actors, we shed light on the dynamic and complex nature of collaborative governance in the context of addressing wicked problems.

The first narrative highlights a paradoxical tension that organizational members experience between integrating public objectives while maintaining their private objectives, which they feel cannot coexist. Those who adhere to this narrative respond to the enforced hybridity with practices of separation: feeling compelled to choose between either their public goals as a police-like gatekeeper or their private goals as a commercial bank. The impact of the public actor’s enforcement of the hybridity becomes evident in this narrative. Organizational members feel that their agency has been diminished, they perceive bias towards the functioning of public parties, as well as experience frustration over the indirect and bureaucratic effects of the current system. As a result, they engage in practices of deflection similar to the behavior of healthcare workers observed by Van Duijn et al. (2022). However, unlike the healthcare workers, the members in our study have limited to no capacity to navigate between competing demands, to reframe tensions to their advantage, or to work around the rules backstage, leading to further frustration. Therefore, if organizational members of the bank engage in more active protests against the enforcement, their resistance to collaborating in fighting financial crime has the potential to obstruct the success of the PPP’s mission.

The second narrative highlights how members of the detecting financial crime department and top management approach fostering acceptance of the enforced hybridity within the bank. They engage in practices of transcendence by creating a future vision of a fully compliant bank that retains agency and autonomy through a series of argumentations. These practices range from explaining the societal necessity of banks to take up this public role to becoming a more moral organization that relates more closely to public values. Rather than focusing on the legal obligation to be a gatekeeper, these members emphasize the moral obligation. By reframing the previously perceived either/or dichotomy as a both/and duality, where the two poles of the hybrid configuration are enabling and constituent of one another, top management aims to inspire the members who adhere to the first narrative to adopt their belief system. In doing so, the organizational members that adhere to the second narrative make being a gatekeeper a central and core aspect of what it means to ‘be’ a bank in today’s day and age, in all likelihood contributing to the success of the PPP’s mission.

Our study provides valuable insights into the complexities of PPPs and their effects on organizational behavior. Since various characteristics impact the success or failure of public-private collaborations (Schaeffer and Loveridge, 2002), we set out to explore the impact of the public actor’s power to enforce compliance with their plans on the experiences of the private actor’s organizational members. Our analysis challenges the conventional understanding of PPPs as mutually beneficial and voluntary partnerships (Quélin et al., 2017; Villani et al., 2017) characterized by relationships of trust, understanding, and reciprocity among multiple actors (Bartels and Turnbull, 2020; Head and Alford, 2015) as not all partnerships operate in the same way. In the case of the PPP for detecting financial crime, the private actor, i.e., the bank, does not benefit from the costs and efforts involved in crime detection, despite the societal benefits of a safer society. This creates a paradoxical tension for organizational members of the private actor, who now have to cope with enforced hybridity as a bank with public-private values and objectives. If this resistance is left unaddressed, it may lead to a failure of the private actor’s participance in the collaboration which will result in renewed penalties and fines for the private actor. This is in nobody’s interest, because failing this PPP also means failing to address the wicked problem of fighting financial crime. Our case reveals that a second group of organizational members, including top management, may seek to address the resistance to enforced hybridity by formulating a persuasive narrative that emphasizes the need to adopt the belief system imposed by the public actor. This group of members recognize that the bank does not benefit from incurring heavy fines for non-compliance with the public actor’s requirements, and therefore they see no alternative but to accept the changes and strive to make the most of them. In this way, the characteristic of being in an enforced collaboration strongly influences the behavior of the private actor as well as the internal sensemaking processes of organizational members. Despite not being a relationship built on voluntariness, understanding and reciprocity among various actors, it may still lead to a successful collaboration aimed at addressing wicked problems, provided that the private actor can overcome internal resistance and envision a future in which they can regain agency and autonomy.

Although the private actor in our case does not benefit from the high costs and efforts related to fighting financial crime, the nature of the mutually beneficial exchange in this PPP is more nuanced. On one hand, banks provide crucial client and transaction information that public parties cannot obtain due to privacy legislation. On the other hand, public parties provide banks with legitimacy, some degree of reputation protection, and, when compliant, enable them to avoid fines while also providing them a “license to grow” since the public actor determines the level of capital buffers banks must maintain. Thus, while a mutually beneficial relationship exists between the parties, banks are not motivated solely by potential gains, but rather by the consequences of noncompliance, such as hefty fines and reputational damage. This means that banks must consider the potential losses of not collaborating with public actors in the fight against financial crime.

This nuance further plays into the question of why public and private actors would continue to refer to their enforced collaboration as a “partnership,” which implies equality among partners. The public actor’s motivation for concealing the problematic aspects of its partnership with banks in fighting financial crime is perhaps more straightforward than the private actor’s motivation. The legitimacy of governments is dependent on the support they enjoy from their citizens, and public actors therefore strive to avoid actions that could diminish citizens’ sympathy toward them. This includes the use of top-down relationships, which may be perceived as unfair and thus jeopardize public support. Ultimately, once the private actor becomes fully compliant with the public actor’s expectations, the parties involved may reach a stage where their collaboration is indeed based on equality and reciprocity. This legitimizes the use of the term “partnership” and aligns with the discourse around well-established public-private partnerships in sectors such as infrastructure where equal relationships are common.

The private actor’s motivation to use a reputable and collaborative relationship as a guise to conceal the negative aspects and power imbalances of the collaboration is slightly more complex. The adherents to the second narrative recognize the legal obligation of the bank’s public-private hybridity, but they do not acknowledge the coercion and power imbalance underlying the partnership. Doing so could result in active protests and resistance among organizational members of the bank who adhere to the first narrative. This, in turn, could lead to non-compliance with legislation, further fines from the public prosecutor, and a general uproar in society. Therefore, we contend that the partnership’s facade helps maintain peace and elicit compliance among the private actor’s organizational members.

Our research examined the paradoxical tensions related to power imbalances and enforced hybridity in public-private partnerships (PPPs) aimed at addressing the wicked problem of fighting financial crime. While our findings shed light on this specific case, they have broader implications for other PPPs with similar power dynamics. Future research could identify objective boundary conditions for the emergence of enforced hybridity in PPPs based on larger data sets. The banking sector provides a suitable context for exploring the effects of power asymmetry in PPPs, but other sectors in which compliance with legislation is the foundation of the collaboration could also offer new perspectives. Our study also raises the question of whether the belief system of the members adhering to the second narrative has been successfully adopted by the members of the first narrative over time, and if so, how and why. Ongoing research into collaborative governance is necessary for a nuanced understanding of the impact of power dynamics and paradox in public-private collaborations. After all, more successful partnerships are likely to lead to more success in addressing wicked problems.

Footnotes

Declaration of conflicting interests

The authors declare no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by a consortium of public and private organisations known to the Editors as part of a broader research program.