Abstract

Continued employment in later life is important for economic well-being and health, and is a key policy issue. However, existing models of the determinants of extended working life do not provide a detailed account of coupled women’s early retirement patterns in the United Kingdom. This article uses data from the English Longitudinal Study of Ageing to show that partnered women aged between 50 and 59 do not adjust the timing of their labour force exit according to the level of pension wealth the couple has accrued. A retired or inactive spouse, caring obligations and poor health accelerate employment exit. Moreover, the odds of an involuntary exit from the labour force, where women have limited control or choice over the timing, are higher for women in lower pension wealth households than those in high wealth families, and among women with inactive rather than retired partners.

Keywords

Introduction

The United Kingdom government and wider society are underprepared for the implications of a rapidly ageing population (House of Lords: Select Committee on Public Service and Demographic Change, 2013). Public welfare expenditure may be strained as the proportion of retirees and inactive older people in the population increases, and state financial support may be inadequate for sustaining a good standard of living in later life. Increasing employment rates of people aged 50 to state pension age is important for reducing the state welfare bill, increasing tax receipts and improving economic growth (Foster, 2018). Retaining older people in employment has therefore become a key policy concern.

Older women are currently under-represented in the workforce (Edge et al., 2017) compared to their male counterparts. Female employment rates are highest between the ages of 50 and 59 (Office for National Statistics, 2015a), and retaining women of this age in work has advantages for their own economic and physical well-being, in addition to benefits for the state. Women who leave work in their fifties are not yet eligible for the state pension, can become dependent on welfare payments, which are increasingly difficult to access (Phillipson et al., 2016), or may need to rely on family support as many have limited or no assets in their own right (Warren et al., 2001). They have difficulties in maintaining living standards throughout retirement (Foster, 2018) and are at greater risk of poverty than their male counterparts (Edge et al., 2017; Mann, 2001). Furthermore, older women who leave work face significant barriers to re-entering well-paid employment should it be necessary or desirable to do so. Available jobs are often low wage with poor prospects (Lain, 2012; Loretto and Vickerstaff, 2015), and they encounter both sexism and age discrimination with competition for roles from both men and younger women (Atkinson et al., 2015; Cabrera, 2007; Moore, 2009). Labour market exit prior to state pension age among women tends to be involuntary (Phillipson et al., 2016) and characterized by a low level of choice and control over the timing. Transitions of this nature are associated with poorer mental and physical health outcomes as well as financial strain (Fisher et al., 2016).

Recent initiatives aimed at retaining older workers in the labour force include raising the state pension age. Women’s former entitlement age of 60 increased to the men’s age of 65 in 2018, and pensionable age for both genders will rise to 68 by 2046. The effectiveness of this policy for women’s continued employment, however, depends on how influential pension wealth is for their work exit. If transitions out of work prior to pensionable age are highly responsive to other non-pension factors and circumstances, including those in the wider family domain (Phillipson et al., 2016), then raising the age of entitlement may have limited influence on their employment patterns. The relationship between pension wealth and women’s continued employment, and how any effect compares in magnitude to other individual, partner and family effects, has not been estimated in the UK context. Improving understanding of the determinants of women’s work exit is important for evaluating the effectiveness of pension-related policy, and for devising new initiatives aimed at encouraging continued employment of older workers.

Women tend to follow diverse routes to retirement defined by partner circumstances, domestic responsibilities and financial need (Duberley and Carmichael, 2016; Duberley et al., 2014; Loretto and Vickerstaff, 2013). The role of these household and family circumstances is often under-theorized and under-analysed in quantitative analyses of women’s retirement processes. Moreover, the meaning and process of retirement is not the same for all, especially among women. Part-time employment, provision of informal care, responsibility for domestic chores and involvement in volunteer activities can mean there is no clear transition or demarcation between women’s working and non-working lives, and many are confused and uncertain about whether and when they can consider themselves retired (Duberley et al., 2014; Everingham et al., 2007; Loretto and Vickerstaff, 2013). Available research examining women’s retirement, however, is either based on small-scale qualitative studies and therefore not generalizable (Duberley et al., 2014; Everingham et al., 2007; Loretto and Vickerstaff, 2013), does not focus on women who leave work prior to state pension age (Carr et al., 2016a, 2016b; Clark et al., 2017; Stafford et al., 2017; Wellbeing, Health, Retirement and the Lifecourse (WHERL), 2017), or does not adequately account for partner and family circumstances (Edge et al., 2017).

The aim of this article is to determine the impact of household and family circumstances on employment exit of women aged 50 to 59 in the UK, using a quantitative approach. The focus is on women residing with a spouse or partner. Single women households are excluded because they form a minority in this age group (Office for National Statistics, 2018), and non-coupled women are more likely to work beyond state pension age than those married due to greater financial vulnerability and limited opportunities for social interaction in the home environment (Dingemans et al., 2017). The employment patterns and caring obligations of women living without a partner are different from those of coupled women, and the financial situation of non-coupled women varies according to whether they are never married, divorced, or widowed (Price, 2006; Radl and Himmelreicher, 2015; Warren et al., 2001). This diversity cannot be adequately captured in one analytic framework.

Our theoretical approach is presented next, and subsequent sections review relevant literature and articulate the research hypotheses. Details of methods, results and discussion follow that.

Theoretical framework

It is assumed that the timing of an older woman’s transition from employment can be explained by both family and individual circumstances, as furthered by Loretto and Vickerstaff (2013). Underpinning this assumption is sociological theory that argues individual behaviour is influenced by the wider situational context (Fisher et al., 2016; Madero-Cabib et al., 2016; Szinovacz, 2013; Szinovacz et al., 2001). Considering contextual factors is important for understanding how the retirement process unfolds (Szinovacz, 2013), and the family environment is of interest as it gives rise to ‘opportunities and constraints’ that guide individual behaviour and key life transitions, including those in the work domain (Dingemans et al., 2017: 974). The economic prerequisites for retirement, and individuals’ preferences for work or leisure, are influenced by family circumstances (Radl and Himmelreicher, 2015).

Fisher et al. (2016: 230) identify family-related and personal antecedents of retirement timing, using a definition of the time of retirement as ‘the age or relative point at which workers exit from their position or career path’. Based on that, a transition from work in this study is defined as a change from self-reported employment to a reported state of retirement, caring, illness or unemployment. The three states of caring, illness and unemployment are collectively referred to as inactive, non-retired positions. The distinction between work and non-work is not completely clear-cut, however, in that some individuals reporting as retired, a carer, or ill may continue with part-time or intermittent employment (Loretto and Vickerstaff, 2013).

Fisher et al. (2016) identify marital factors, care-giving responsibilities, and spousal employment and support for retirement as family characteristics that influence retirement timing. In addition, they recognize the following individual characteristics as important: physical, cognitive and mental health; economic status including pensions and wealth; demographic characteristics; and psychological factors. However, Fisher et al. arguably under-theorize the role of gender in early retirement processes, failing to adequately account for its impact in shaping heterogeneous routes out of the labour market. For example, there are gender inequalities in involuntary retirement in the UK: men are more likely to exit via employer-provided pre-retirement schemes, while women frequently retire for personal reasons (Hofacker et al., 2016).

In this study, we distinguish between two main types of early retirement processes: voluntary and involuntary retirement. Models of retirement timing emphasize the importance of involuntariness in the retirement decision for moderating health outcomes (Fisher et al., 2016; Szinovacz and Davey, 2005). Involuntary exit occurs where individuals perceive they have limited control or choice over the timing of their transition out of work, such as in cases of deteriorating health, the need to provide care, or job displacement (Foster, 2018; Szinovacz and Davey, 2005; Van Solinge and Henkens, 2007). Work exit is more likely to be considered voluntary where women have a greater degree of choice and control, and might happen where there are sufficient financial resources or where retirement timing is coordinated with that of a spouse, with the incentive of shared leisure time. We define an involuntary transition when a woman has moved from employment into a reported state of illness, unemployment or caring for home and family. A voluntary transition is defined as entry into reported retirement prior to pensionable age. Based on our review of the literature below, we argue that the factors that predict women’s involuntary retirement are different from factors that predict their voluntary retirement. This distinction is not made clear by Fisher et al. (2016) due to their lack of theorization on the role of gender in relation to different processes of early retirement.

The distribution of pension resources within families is not necessarily even across men and women within couples. In Fisher et al.’s (2016) model, pension wealth is considered an individual asset. However, women’s difficulty in accumulating personal pension wealth and dependence on family resources in retirement is well documented (Foster, 2012; Ginn and Arber, 1993, 1996; Phillipson et al., 2016; Price, 2006, 2007; Warren et al., 2001). Their provision of family care throughout the life course can result in disrupted employment trajectories, reduced ability to accumulate occupational and state pension rights, and reliance on a couple’s joint funds rather than individual wealth in retirement (Banks et al., 2005; Dingemans et al., 2017; Foster, 2018; Ginn and Arber, 1993, 1996; Warren et al., 2001). Thus, we depart from Fisher et al.’s model by analysing the role of pension wealth on a household, rather than individual, basis.

Family pension wealth

In Fisher et al.’s (2016) model of retirement timing, more generous pension provision is associated with earlier retirement, and people with lower pension provision have an economic incentive to stay on at work and accumulate greater pensions savings. Hence, our first hypothesis is that women from high pension wealth households are expected to have a higher probability of leaving work between the ages of 50 and 59 than their peers with lower levels of pension resources (Hypothesis 1). The influence of family pension wealth has not yet been examined within a model of women’s early retirement timing, yet accumulated pension resources are crucial for determining future income after paid work ends. Women tend to come ‘in and out of the labour market depending upon childcare and other caring responsibilities and to support the family income’ (Loretto and Vickerstaff, 2013: 69). If having sufficient family income in retirement is dependent on pension provision, then the likelihood of a woman’s early retirement and her age of labour market exit might be influenced by the level of pension wealth accrued in the household. Existing quantitative studies of women’s retirement measure the effect of individual rather than joint pension benefits (Blau and Riphahn, 1999; Rice et al., 2011; Szinovacz and DeViney, 2000), examine the effect of pension eligibility or membership on labour supply and retirement timing (Kubicek et al., 2010; Lalive and Parrotta, 2017; Madero-Cabib et al., 2016); evaluate different aspects of pension reform (Engels et al., 2017); or analyse household income but not pension assets (Drobnič, 2002).

Pension wealth is not evenly distributed across UK households. Coverage of the state pension is close to complete, with minimal variation in the amount received, but the same is not observed for privately accrued resources, with an estimated 24% of households holding no private pension funds (Office for National Statistics, 2015b). Of households with private resources, the wealthiest 10% hold 47% of the total private pension wealth (Office for National Statistics, 2015b). Banks et al. (2005) examine the association between family pension wealth and couples’ labour market status. They find that households where both members are retired have the highest median accumulated wealth, pointing to a possible association between high pension wealth and retirement of the female partner. In a small-scale qualitative study, Loretto and Vickerstaff (2013) identify a distinct group of relatively financially comfortable couples where labour force exit of the female partner occurred at a similar time to the voluntary retirement of her male spouse. However, the authors point out such transitions might not be solely driven by finances, with other factors including health and job loss also possibly influential.

Banks et al. (2005) find couples with both members not working but in an inactive, non-retired state had the lowest median accumulated pension wealth. This household type might have originated as either single or dual earner couples in which job displacement, illness or caring responsibilities led to labour force withdrawal of either the female partner or both couple members. Women who leave work due to such involuntary events are often in constrained financial circumstances (Foster, 2018; Price and Nesteruk, 2010). Hence, this evidence suggests women from low pension wealth households may take an involuntary pathway out of the labour market, rather than remain in work for economic reasons as predicted by Fisher’s model. We hypothesize that women from low pension households are more likely to report their transition as an involuntary early retirement than their higher wealth peers (Hypothesis 2). Despite their low levels of pension savings, the economic incentives to remain in work are constrained by household processes that lead to involuntary retirement by household members.

Spousal circumstances: health and employment status

Banks et al. (2005) show in descriptive analysis that poor health is the most common reason for involuntary early retirement in the UK. Among people who report forced retirement, 56% of men and 45.5% of women give their own ill health as the main cause. Additionally, 17.6% of women state others’ poor health as the primary reason, compared to only 3.8% of men. Different theories attempt to explain the impact of poor partner health on older women’s work. The female spouse may leave work to provide care (Phillipson et al., 2016) or alternatively remain in the labour market because she is adept at managing both caring needs and paid employment from earlier life course experiences (Dingemans et al., 2017; Szinovacz and DeViney, 2000). The likelihood of the female partner’s continued employment may be contingent on the male partner’s status; Blau and Riphahn (1999) find that women with partners in poor health are more likely to remain in work if the partner also stays in employment.

International research suggests the effect of poor partner health on women’s continued employment may be moderated by financial status, with women expected to stay working where pension funds are inadequate (Szinovacz and DeViney, 2000) or due to the high costs of the partner’s disability (Kubicek et al., 2010). This is not necessarily the case in the UK context, however, because of the availability of disability benefits. Health constraints are more prevalent among individuals from low wealth households, but disability payments replace a high proportion of lost income should they leave the workforce (Banks and Smith, 2006) and this increases the likelihood of the female partner also leaving to provide care. Women in wealthier households are also expected to transition from work to care in the advent of poor partner health, due to having accumulated sufficient resources to ensure financial well-being. Poor spousal health, therefore, is expected to accelerate women’s labour market exit (Hypothesis 3) and increase women’s risk of an involuntary rather than voluntary transition (Hypothesis 4).

Quantitative research of retirement patterns in the UK does not differentiate between the non-working states of partners (Carr et al., 2016a, 2016b). Women have a reduced likelihood of working where partners are also not working (Phillipson et al., 2016; Rice et al., 2011), but non-working spouses vary in their reasons for labour market exit, and in the extent to which they had choice over the timing of their transition (Foster, 2018). Early retirement among men is associated with a higher degree of voluntariness and financial resources, while the majority of men who left for reasons other than retirement are likely to have done so because of poor health (Banks and Smith, 2006). A higher transition rate is thus expected among women in households where the male partner retired voluntarily (Hypothesis 5). Households where the male partner is not working but in an inactive, non-retired state may be under greater economic pressure for the female member to remain in work, but as we argued for Hypothesis 2, such households usually originate as either single or dual earner couples in which involuntary events led to the labour force withdrawal of either the female partner or both couple members (Banks et al., 2005). Hence, we expect women with male partners who are inactive but not retired are themselves more likely to report an involuntary transition into retirement (Hypothesis 6).

Data and methods

Data

The English Longitudinal Study of Ageing (ELSA; Marmot et al., 2011) is a biannual study of people aged 50 and over living in private residences. Measures include individual and household demographics, health, employment, income, and pensions and assets. The first five waves of data were analysed, covering the period 2002–2011. The first wave contained 12,099 individuals, with 9432 in the second, 9771 in the third, 11,050 in the fourth and 10,275 in the fifth.

Married or cohabiting couples were eligible for the analytic sample if they contained a woman aged between 50 and 59 years old inclusive, who had been observed in two or more consecutive waves. Her labour market status needed to be reported as ‘employed’ on at least the first of these. Based on these criteria, 2238 couples were initially selected. The sample was then restricted to respondents that had full data available for all necessary individual, household and partner measures. This gave a final sample of 1569 households.

Dependent variables

Transition from employment

A self-reported employment status was used, in which participants were asked to select the best description of their current situation from one of employed, self-employed, retired, unemployed, permanently sick or disabled, or looking after home and family. Employed and self-employed respondents were amalgamated to form one common state of employment. A transition was defined as a change in status from employment to a non-working state in consecutively observed waves. Of the 1569 sampled women, 287 (18.3%) had an observed transition. This figure was commensurate with statistics from the Department for Work and Pensions (2014), which showed 78% of 52-year-old women, but only 62% of those aged 59, were in work in 2014. This was a 16 percentage point difference in the proportion of women working at those ages. Justification for treating employment transitions as labour market withdrawal, rather than the beginning of a temporary spell out of work, came from Banks and Smith (2006), who concluded that retirement in the UK is an absorbing state for most. In line with this, analysis of the sample data showed few incidents of women reporting a return to an employed state following their transition.

Voluntary/involuntary work exit

The sample of 287 transitioned women was divided into voluntary and involuntary groups, according to stated reasons for retirement and reported labour market position (Radl and Himmelreicher, 2015). Women who reported illness, unemployment or caring were placed into the involuntary category, as they were most likely to have had a low level of control over the timing of their transition. This group was comprised of 153 members, which was 9.8% of the full sample of 1569 women. The remaining 134 women who reported as retired formed the voluntary category; this was 8.5% of the full sample. The validity of this categorization was assessed using ELSA job history data on stated reasons for retirement and found to be sufficiently accurate, with reasons stated by the majority of respondents correlating with their voluntary or involuntary classification. The online Supplemental Appendix 1 contains further details.

Independent variables

Family characteristics

All variables described here were time-varying, with the exception of tenure. Household pension wealth was a quintile measure, calculated using the total of a couple’s accumulated wealth from state and private pension sources at the time of each ELSA interview. Each individual member’s contribution was their pension entitlement if they were to retire at that point and accumulate no further rights. The wealthiest quintile was the designated reference category. Further details on the construction of this variable are in online Supplemental Appendix 2. A self-reported measure of partner employment categorized men as either employed, retired, or in a non-working but non-retired state of unemployment, illness or caring. Partner functional health constraints were indicated by a measure of limiting long-term health (Manor et al., 2001).

Additional family-related variables included caring responsibilities, which were indicated where women had provided care to a spouse or partner, child, grandchild, parent, other relative, friend or neighbour in the past week; and a dependent child was defined as a resident aged 17 or under who earns less than £5000 per year. Women were also allocated into quintile groups for household non-pension wealth, which included property and business assets. There was a low level of correspondence between pension and non-pension wealth quintiles, with over two-thirds of women in any given quintile for pension wealth placed in a different non-pension wealth category. The tenure variable denoted outright ownership, having an outstanding mortgage, and renting. Constraints in the ELSA dataset preclude the inclusion of measures of marital quality.

Individual characteristics

Women’s health was measured first using the same limiting health indicator as for their partners, and secondly using a time-varying indicator of general self-reported health. This had a ‘good or better’ category formed from responses of excellent, very good or good, and a ‘poor’ health group formed from responses of fair or poor. Educational attainment was measured as either post-secondary education, secondary school level qualifications, or no qualification. Socioeconomic status was a three-category variable of higher managerial, administrative and professional occupations; intermediate workers; and routine and manual workers. These variables were time invariant and measured at the time of the first ELSA interview. Income was a time-dependent continuous measure of the gross weekly total earnings from employment and self-employment, pension payments, benefits and any other sources. Part-time working was defined as less than 35 hours per week. Limitations of the available data mean job-related variables are not included.

Analytical strategy

A two-stage modelling strategy was followed (Allison, 1982). In the first stage, a discrete time event history model (Singer and Willett, 2003) for predicting the probability of a transition occurring at a given age was estimated from the full sample of 1569 women. A cloglog link function was used to account for the underlying continuous time process, and estimation was performed under a conditional likelihood assumption to account for left truncated observations (Guo, 1993). The baseline hazard function was fitted first and captured change in women’s transition probabilities over time. Following that, women’s demographic, health, income, housing and non-pension wealth variables were incorporated. Pension, partner employment and partner health measures were tested separately in subsequent models.

In the second phase, the sample was restricted to the 287 women with an observed transition. A binary logistic model was fitted to this subsample to determine predictors of voluntary and involuntary exit. The dependent variable was the log odds of an individual experiencing an involuntary versus voluntary transition. Statistical significance in both the first and second modelling stages was determined using log likelihood ratio tests. Analysis was done in the R software environment (R Foundation for Statistical Computing, Vienna, Austria) using the lme4 package for multilevel models.

Results

Descriptive statistics

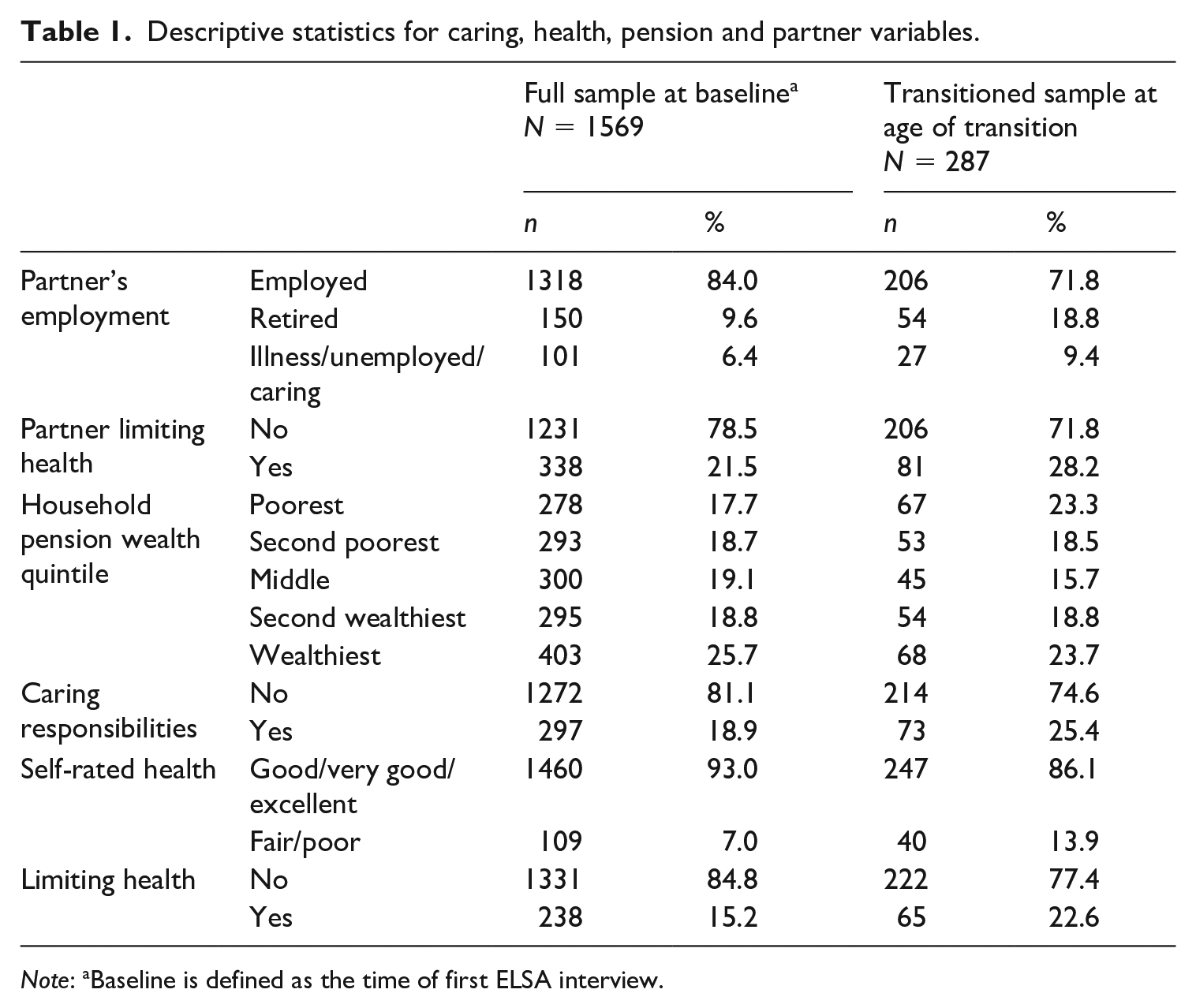

Table 1 contains descriptive statistics relating to selected variables of interest for the full sample of 1569 women, and for the subsample of 287 transitioned women. Results for other covariates are available in online Supplemental Appendix 3. Statistics for the full sample were calculated from baseline measures taken at the time of women’s first ELSA observation. Those for the subsample used values recorded at the time of last known employment prior to transitioning. The mean baseline age of women in the full sample was 53.2 years, slightly younger than that for the male partners of 55.8 years, and the mean age of women’s transition was 55.9. The baseline sample was skewed towards couples in the richest quintile for household pension wealth, with 25.7% in this group compared to 17.7% in the poorest quintile. Poor health and partners with limiting conditions were more common among women who left work than in the full sample, and caring obligations were also more prevalent. Employed partners were less frequently observed among transitioned women (71.8% compared to 78.5% in the full sample), while the incidence of retired spouses was notably higher (18.8% compared to 9.6%). Just over 9% of transitioned women were coupled to men not working but non-retired.

Descriptive statistics for caring, health, pension and partner variables.

Note: aBaseline is defined as the time of first ELSA interview.

Predictors of older women’s transitions out of employment

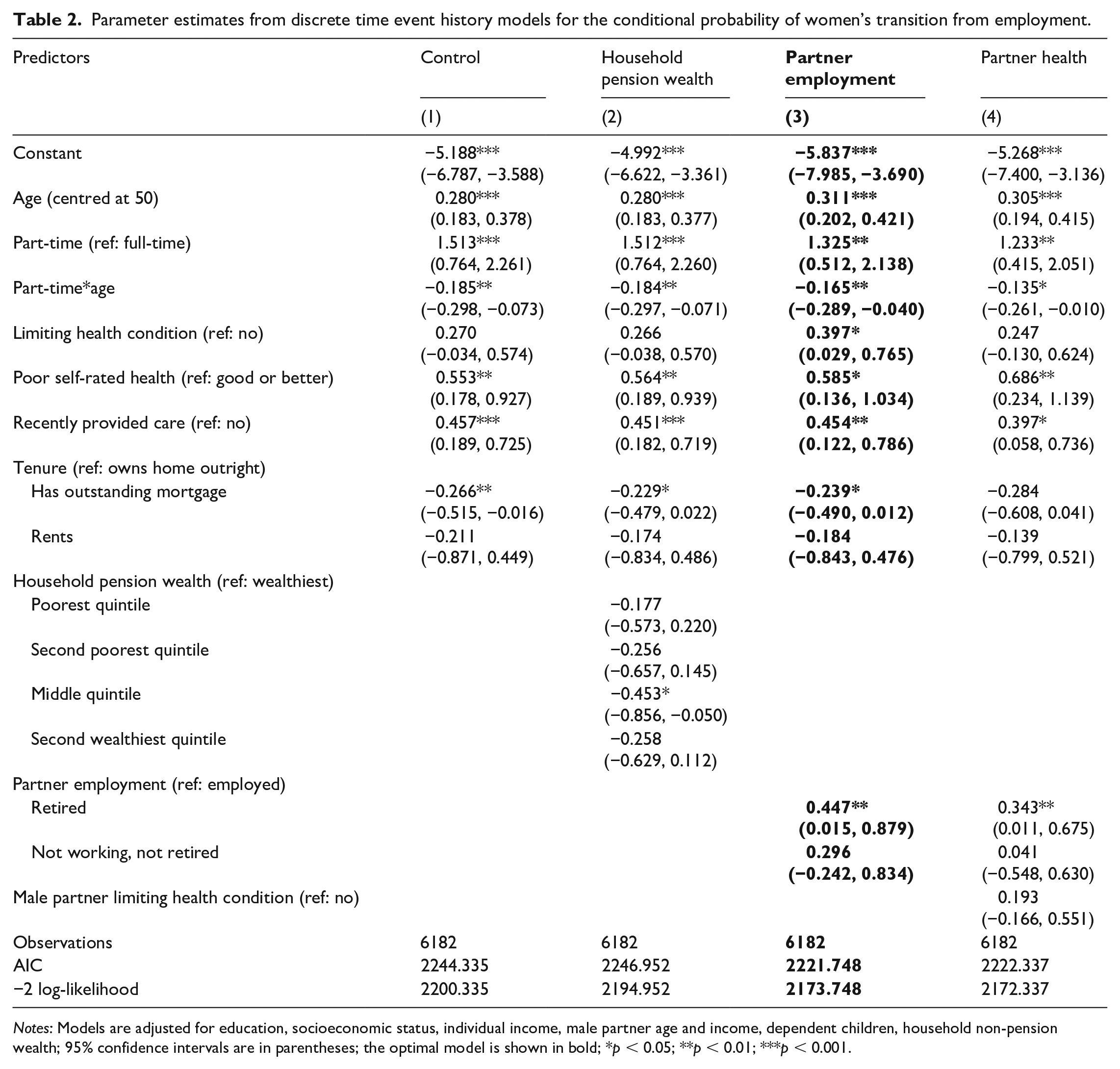

Results from the fitted event history model are in Table 2. A linear baseline hazard, which is a function of age, was established as the optimal baseline form. Added to this were main effects for demographic variables, part-time working, health, caring, non-pension wealth, tenure, partner income and age, and dependent children. This model also contained a statistically significant interaction term between age and part-time working, but interaction terms between each of age and limiting health, self-rated health, and caring responsibilities were not significant and therefore not retained. Model 1 shows estimated coefficients and fit statistics for this specification. Further details of the analysis summarized here are in online Supplemental Appendix 4.

Parameter estimates from discrete time event history models for the conditional probability of women’s transition from employment.

Notes: Models are adjusted for education, socioeconomic status, individual income, male partner age and income, dependent children, household non-pension wealth; 95% confidence intervals are in parentheses; the optimal model is shown in bold; *p < 0.05; **p < 0.01; ***p < 0.001.

Model 2 tested the effect of household pension wealth. No evidence of a statistically significant association was found

Determinants of voluntary and involuntary transitions

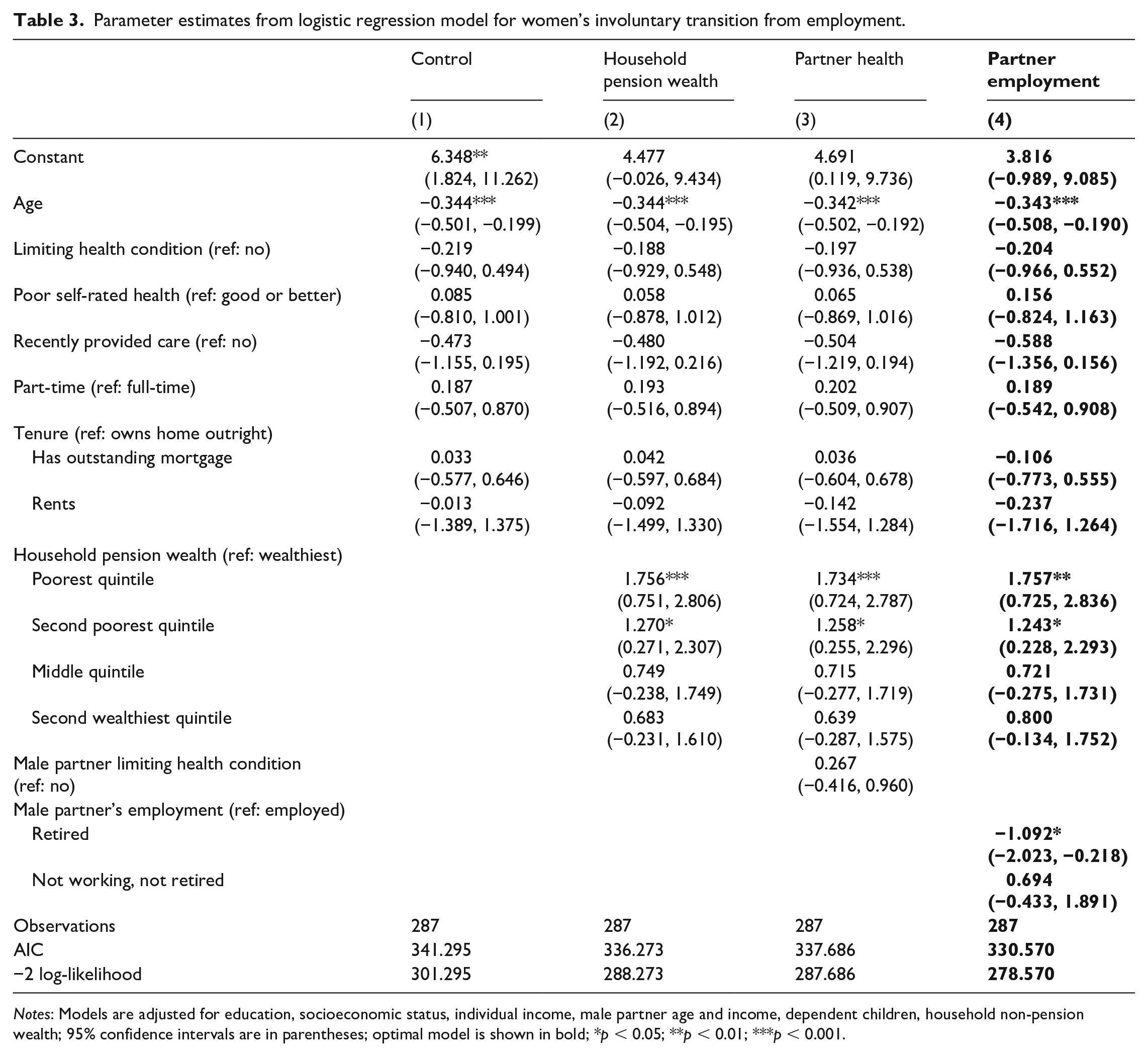

Table 3 shows parameter estimates for a series of logistic regression models fitted to the subsample of 287 transitioned women. Exponentiated coefficients give the odds of an involuntary transition compared to voluntary retirement. Model 1 contains measures of age, dependent children, income, health, non-pension wealth, tenure and male partner’s age and income. Model 2 incorporates the household pension wealth covariate, which was statistically significant

Parameter estimates from logistic regression model for women’s involuntary transition from employment.

Notes: Models are adjusted for education, socioeconomic status, individual income, male partner age and income, dependent children, household non-pension wealth; 95% confidence intervals are in parentheses; optimal model is shown in bold; *p < 0.05; **p < 0.01; ***p < 0.001.

Discussion

This study shows that there are differences among coupled women regarding the risk of employment exit and early retirement between the ages of 50 and 59. There is also heterogeneity in the level of voluntariness women might have over that transition, with some experiencing a greater degree of control and choice over the timing of their work exit than others. To explain this diversity, we expanded on an existing model of women’s retirement timing and analysed factors relating to the family environment and partner circumstances, while accounting for women’s own attributes.

Results show women’s labour market exit prior to state pension age is precipitated by that of her spouse. Retirement among male spouses encourages earlier and voluntary withdrawal of female partners (Hypothesis 5), whereas men leaving work for non-retirement reasons is associated with women’s involuntary exit (Hypothesis 6) that on average occurs later than for women with retired partners. Early voluntary retirement among couples is associated with high wealth and preferences for shared leisure (Banks and Smith, 2006; Radl and Himmelreicher, 2015), whereas the most probable reason for non-retirement work exit of male partners is poor health (Banks and Smith, 2006). Thus, while no evidence is found of a direct effect of poor spousal health on the timing or nature of women’s early employment exit, as postulated in Hypotheses 3 and 4, poor spousal health could indirectly lead to a woman leaving work if the male partner transitions out of the workforce himself or needs care (Blau and Riphahn, 1999; Phillipson et al., 2016). Later transitions out of work among these women may be explained by her remaining in work until his caring needs necessitate her work exit, or until such time disability support payments are received and the couple can forgo her income.

Contrary to the first research hypothesis, after accounting for income and non-pension assets, there is no evidence that partnered women in their fifties adjust the timing of their work exit according to the family’s level of pension wealth (Hypothesis 1). Their transitions are more likely explained by their own health, caring obligations and partner’s work status. However, women from low pension wealth families who transition prior to pensionable age tend to have less choice and control over the timing of their work exit than those from families with greater levels of pension wealth (Hypothesis 2). This may place them at higher risk of poor health outcomes, as well as the financial strain, that is associated with involuntary work transitions (Fisher et al., 2016). Phillipson et al. (2016) suggest that many women who leave the labour market prior to state pension age tend to do so involuntarily, but this study has identified a group of women, who are partnered and from higher pension wealth families, that have a greater degree of voluntariness over the timing of their transition

The significant impact of a partner’s employment for women’s age of exit, and pension wealth for determining the level of control and choice over any transition that occurs, is commensurate with sociological theory, assuming individual behaviour is influenced by the wider situational context (Fisher et al., 2016). This study provides empirical support to the argument that retirement patterns need to be examined within the context of the wider family unit and from a gendered perspective (Loretto and Vickerstaff, 2013). Existing models of retirement timing under-theorize the role of a partner’s employment status by not differentiating between retired and other economically inactive states (Carr et al., 2016b; Szinovacz and DeViney, 2000), and we extended Fisher et al.’s (2016) model by distinguishing between women’s voluntary and involuntary retirement. These are details that previous models of retirement patterns have not shown, contributing to a fuller understanding of early labour market exit among coupled older women. The lack of evidence found for a relationship between pension wealth and partner health factors and the timing of women’s retirement might be explained by the hypotheses not fully accounting for the heterogeneous routes older women take out of the labour market, which can include a phased exit from employment rather than an abrupt exit, or intermittent periods of paid work (Fisher et al., 2016; Loretto and Vickerstaff, 2013).

Ginn and MacIntyre (2013: 100) assert that under an increased state pension age ‘many older workers in the future will be left in limbo, too old, sick or occupied with caring to undertake paid work and too young to receive a state pension’. Results of this study are commensurate with that, as they show that employment exit among coupled women in their fifties is driven by caring obligations, health, and their spouse’s work rather than the amount of pension wealth accrued by the family. There is limited support for allowing early access to state pension funds for carers or those with poor health (Cridland, 2017), meaning financial assistance for women who leave work in their fifties may come from alternative public welfare schemes, if disability and unemployment benefits are substituted for lost pension income (Cribb et al., 2014). The raising of men’s state pension age, in contrast, may impact on older women’s retirement patterns. If working men react to the raising of their pension age by remaining in work for longer, then a rise in the labour market retention of their partners would be expected, with the length of their employment spells also increased (Lalive and Parrotta, 2017). Alternatively, the increase in men’s pension age may not extend men’s working lives; rather, they may leave employment and claim disability or unemployment benefits as an alternative to retiring on the state pension. If this were the case, there could be a flow-on effect and a rise in claims from the female partners. Policies aimed at retaining older women in the workforce need to look beyond pension provision and address the barriers to continued employment associated with care provision, poor health and non-working spouses.

Study limitations

The results and interpretation of this work come with limitations and caveats. Firstly, for reasons explained in the introduction, the focus was narrowed to married or partnered women, and findings may not extend to those in non-coupled situations. A fuller understanding of single women’s retirement trajectories is better achieved in a separate study. Secondly, the event history models are fitted under a conditional likelihood approach, which assumes the first transition observed is the first that occurred. This assumption may not hold for all women, as the retirement process can be characterized by spells in and out of paid employment (Loretto and Vickerstaff, 2013). ELSA data are collected bi-annually, and may not be granular enough to detect all such spells. If the probability of leaving work at a given age is dependent upon the number of previous transitions made, then the fitted models may underestimate the risk of transition for women with prior unobserved job changes. This, along with limits to the number of potential predictors and interaction effects that can be tested in any model, limits the extent to which heterogeneity in women’s retirement pathways can be adequately captured. This limitation is exacerbated by constraints in the dataset which preclude the inclusion of some family-related factors known to impact on women’s retirement trajectories. Indicators of marital quality are one note-worthy omission (Szinovacz and DeViney, 2000). Antecedents of women’s retirement timing also arise from other contexts, such as the work environment (Fisher et al., 2016). Job satisfaction is an important element in women’s retirement decisions (Loretto and Vickerstaff, 2013), but this and other job quality measures could not be included in this study. Lastly, there is the possibility of misclassification of women placed into either the voluntary or involuntary retirement categories in the analysis. Women may have more or less control or choice over their work exit than what has been assumed. Their perceived level of choice in the decision-making process may be lower if they experience pressure to leave work from their partner (Loretto and Vickerstaff, 2013), and caring obligations will not necessarily restrict all affected women’s employment options to the same degree (Carr et al., 2016b).

Conclusion

In this study, an existing model of retirement timing (Fisher et al., 2016) is extended to account for the role of gender in distinguishing between voluntary and involuntary early retirement transitions among coupled women in the UK. Results show heterogeneity in the timing and voluntariness of work exit among women aged in their fifties is explained by selected partner and domestic circumstances, providing empirical support to recommendations that studies of women’s retirement need to be contextualized within the family environment (Loretto and Vickerstaff, 2013). Partner’s labour market status is a particularly strong influence on different aspects of women’s retirement trajectories: those with retired partners have shorter working lives on average and are more likely to experience a voluntary transition, characterized by high feelings of control and choice, compared to their peers who have economically inactive but not retired partners. These findings contribute a more detailed understanding of the influence of spousal labour market position than what is known from existing studies (Carr et al., 2016b; Szinovacz and DeViney, 2000). There is no evidence to support the hypothesis that low levels of household pension wealth are an economic incentive for coupled women’s continued employment, or that poor partner health has a direct effect on women’s age of transition; however, their risk of work exit may increase should partners develop additional caring needs, or leave employment themselves. In such cases, women from low pension wealth families would be at risk of economic hardship as they forgo paid work yet are ineligible for the state pension. This research highlights the need for a holistic approach to initiatives aimed at retaining older women in the workforce that account for caring demands and the labour market position of the male partner in addition to the accrual of pension assets.

Supplemental Material

SDI906358_Appendices – Supplemental material for The Influence of Household Pension Wealth, Partner’s Health and Spousal Employment Status on Heterogeneous Early Retirement Transitions among Women in England

Supplemental material, SDI906358_Appendices for The Influence of Household Pension Wealth, Partner’s Health and Spousal Employment Status on Heterogeneous Early Retirement Transitions among Women in England by Jennifer Prattley and Tarani Chandola in Work, Employment and Society

Footnotes

Acknowledgements

We would like to thank Johan Koskinen and Bram Vanhoutte for advice given throughout the doctoral research programme that led to this article. We would also like to thank the anonymous reviewers of this journal for their constructive comments on earlier versions.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: this work was supported by the Economic and Social Research Council (grant numbers 1227745 and S/J019119/1).

Supplementary material

The supplementary material is available online with the article. Data will be made available on request.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.