Abstract

Children’s FinTech apps are digital mobile platforms that incorporate features for managing children’s financial activities ranging from the setting and tracking of chores, the payment of allowances or pocket money, the capacity for saving and spending, and the facilitation of investment options. As we show in this paper, a key aspect of these child money and finance apps is the inclusion of playful affordances such as gamified interface designs and elements that aim to make financial activities fun and appealing to younger users. In doing so, we build on emerging research on children’s FinTech to identify and discuss key implications of playful finance in children’s app environments. Methodologically, the paper draws on established app walkthrough and interface design feature analysis methods, as well as a case study approach from app studies, which are applied to children’s financial app platforms. We identify various playful affordances such as gamified designs and app features in three case study examples where children are incentivised to complete chores, document their savings goals, embrace debit cards and digital consumption, or learn about money and finances through digital rewards such as points, tokens, or levels. Through the interface design analysis, we find that children’s finance apps encourage regular input and collection of their economic activity and information, build attachments to platforms through personalised branding and the accrual of valued in-app assets and status, and instruct children in norms of both digital finance and data surveillance.

Introduction

Children’s FinTech apps are mobile digital platforms that incorporate features for managing children’s financial activities ranging from the setting and tracking of chores, the payment of allowances or pocket money, the management of saving and spending and even the facilitation of investment portfolios. A key aspect of these child money and finance apps is the inclusion of playful affordances such as gamified design interfaces and elements that aim to make financial activities fun and appealing to younger users. These design affordances intensify what has more broadly been described in adult FinTech economies as ‘playful finance’ (Lai and Langley, 2023), by directing them at children’s financial lives. Thus, identifying and discussing the implications of playfulness in children’s Fintech app platforms is an important contribution to the emerging research area of children’s FinTech.

This paper draws on established app walkthrough and interface design feature analysis methods (Hasinoff and Bivens, 2021; Light et al., 2018), as well as a case study approach from app studies (Flyvbjerg, 2001), which are applied to children’s financial app platforms. This study is significant in bringing concepts of playfulness, affordances, and gamification from digital platform and games studies and applying these to children’s FinTech research. Specifically, we explore how playful affordances in children’s FinTech apps are mediating children’s household labour, consumer socialisation, and financial literacy (Goyal and Kumar, 2021; Gudmunson and Danes, 2011; OECD, 2014). We identify various playful affordances such as gamified designs and app features in three case study examples where children are incentivised to complete chores, document their savings goals, embrace debit cards and digital consumption, or learn about money and finances through digital rewards such as points, tokens, or levels. The three case studies analysed are S’mores tokens within the S’moresUp app, personalised debit cards within the FLX app, and “money mission” learning levels in the GoHenry app.

Through the interface design analysis, we find that children’s finance apps encourage regular input and collection of their economic activity and information, build attachments to platforms through personalised branding and the accrual of valued in-app assets and status, and instruct children in norms of both digital finance and data surveillance. In this way, these FinTech apps incorporate playful elements to both shape and quantify children’s economic behaviour, while also establishing financial technology platforms as essential in children’s lives. Nevertheless, we do not argue against children’s access to digital savings or payment technologies per se. Rather, we approach children’s FinTech apps as ambivalent socio-technical systems that enable more extensive forms of financial participation and literacy, whilst also introducing new and more intensive forms of commercial influence, behavioural shaping, and surveillance as part of data-generating infrastructures within commercialised financial ecosystems.

Background: Understanding playful affordances in children’s finance platforms

Children’s financial socialisation and Fintech apps

Child consumer socialisation literature has historically explored a range of questions associated with children’s financial development, learning, and wellbeing (Levison, 2000; Zelizer, 2002). This field has not, however, extended these topics to consider the more recent developments in children’s digital finance or FinTech platforms in mediating these financial dynamics and relationships. Instead, this literature has tended to focus on more traditional aspects of children’s finances, such as the importance of allowances or pocket money for shaping children as economic agents in consumer societies (Levison, 2000; Marshall, 2010). Here, allowances are usually regarded as the key means of financial socialisation in children (Le Baron and Kelley, 2021). As such, they have been normatively understood to ensure the development of financial literacy (Gudmunson and Danes, 2011), and as a form of compensation for household labour (Zelizer, 2002). In these contexts, parents are viewed as important intermediaries in empowering the financial socialisation of children (Yexin et al., 2019). Thus, children’s financial socialisation is typically assumed to be contained within families and driven by their reception of parental financial knowledge (Levison, 2000). Financial literacy is the development of knowledge and skills to make effective personal financial decisions across varied contexts and to participate as an individual in economic life (Goyal and Kumar, 2021; OECD, 2014).

Research has highlighted how inconsistencies or gaps in financial education within formal schooling systems have in the past been filled by financial institutions like banks, who promote children’s banking products to create brand awareness and consumer loyalty under the guise of developing a desired responsible financial subject (Maman and Rosenhek, 2023; Sawatzki, 2018). Research on children’s financial socialisation has long shown that tools such as piggy banks, school banking programs, and parental rewards functioned not only to teach money management, but also to cultivate habits of saving, spending, and financial responsibility (e.g., Bonke, 2013; Hermann et al., 2017; Teachers Mutual Bank, 2016). These practices framed money as both a pedagogical and affective object, often linking financial behaviour to ideas of effort and reward. More recently, children’s FinTech platforms are emerging as a pervasive aspect of children’s financial experience and learning. Contemporary FinTech apps build on financial socialisation traditions, but extend them through digital interfaces and features, including gamified designs and data tracking infrastructures, marking a shift from families, schools, and banking systems of financial education to computational and digital platform-mediated ones.

To date, however, there is little research into the increasingly popular use of child financial management apps, and the role of FinTech in the economic lives of children. Apps for managing children’s finances can be located within broader research on digital money (Lovink et al., 2015; Kozinets et al., 2021; O’Dwyer, 2023), or FinTech, which is defined as the intersection of finance and technology within an emergent and diverse sector of digital retail monetary and financial services (Langley and Leyshon, 2021). FinTech plays an important role in how financial products and services are now produced, delivered, and consumed, with FinTech research covering a broad range of topics including financial data and investment, new technologies such as blockchain and peer-to-peer (P2P) lending, as well as digital payment systems and transactions services such as mobile wallets, mobile payments applications, and social payment platforms such as Venmo (e.g., Acker and Murthy, 2020; Maurer 2015; Swartz 2020). This intersection of technology and finance is characterised by the transformation of economic transactions into information, the creation of detailed consumer data records, and the development of FinTech platform economies (Dieter and Tkacz, 2020; Langley and Leyshon, 2021; Lai and Langley, 2023; O’Dwyer, 2023).

Emerging research on children and digital money points to dynamics of financial literacy emerging outside of homes or banking institutions through new formations and relations with FinTech platforms (Chowdhury, 2019; Nansen and Bliss, 2024). Children’s economic participation is increasingly influenced by the widespread use of child finance apps. It is unclear, however, how the digitisation of children’s finances is influencing children’s financial learning and consumer agency, as well as creating economic value for banking institutions and digital platforms. Children’s finance apps ostensibly seek to promote financial literacy and ensure children’s savings habits or purchasing power through features such as chore or allowance payments and budgeting features. Yet, when the development of children’s financial literacy is shaped by finance apps with management and monitoring features questions arise about the kinds of child financial knowledge, socialisation, or capacities being privileged or produced, as well as the privacy costs of handing over this financial data. Recent research examining how children’s FinTech apps operate to influence the financial conditions of contemporary childhood has detailed five key design functions of child finance apps: chore management; child savings; payment and spending systems; parental control features; and banking and finance features (Nansen and Bliss, 2024). Further, this research identifies key dynamics of surveillance, datafication, and gamification in the operation of these apps mediating children’s consumer participation and financial lives. Yet, the diversity and implications of playful affordances and gamified design features require further research to understand how they attract and retain child users.

Playful features and gamified designs in children’s finance apps

Playful affordances can be understood as technology-mediated arrangements of experience that promote enjoyable experiences for purposes such as increasing engagement or guiding specific outcomes. Affordances, which have attracted much theoretical attention in design, media and technology studies fields, can be broadly understood as the possibilities and constraints enabled through the interaction of users with technology features. They are not predetermined by features alone, but instead constructed through the range of options features create in combination with how users adopt and appropriate them. They can include quite direct or individual level impacts, along with broader shaping of social norms or cultural ideologies (Bucher and Helmond, 2018; Evans et al., 2017; Nagy and Neff, 2015), as well as more economically oriented ‘transactional affordances’ such as platform payment systems like ‘checkout’ features on social media apps that normalise online financial cultures (Manzerolle and Daubs, 2021).

Gamification is one key form of playfulness, which has been developed as a concept and applied as a design approach in the use of gamified elements and logics in non-game contexts (Deterding et al., 2011). Gamification has for example been applied by researchers, app developers and educators to understand how children might achieve positive educational outcomes with gamified designs seen as reducing the sense of ‘effort’ (or ‘learning’) which is sometimes considered to disengage children. In this respect, it is a concept that has been widely applied, such as in classroom environments and public libraries, as well as on digital apps used by children (Barata et al., 2015; Downie and Proulx, 2022). However, the effects of gamification on children’s financial socialisation remain unclear and contested (Sailer and Homner, 2020). We build on this emerging area by focusing specifically on gamification as a mode of playfulness in children’s Fintech platforms.

Gamification is translated from its origins in video games to finance apps when children are rewarded or compensated with virtual badges, stickers and digital tokens that contain no direct financial value. Some key types of gamification elements include: rewards and incentives such as virtual points awarded for completing tasks, badges that work as virtual tokens for reaching milestones, and in-app currencies that can be earnt to purchase in-game items; levels and progress tracking that provide visual indicators of progress toward goals, unlock new content to encourage continued activity, and give reinforcement through feedback; challenges and quests that encourage engagement and a sense of purpose or direction through the promotion and attainment of specific goals; and leaderboards, avatars, and personalisation, which are used to customise accounts, display identity preferences identity and rank to create a sense of identity and ownership, and to foster connection, competition and community.

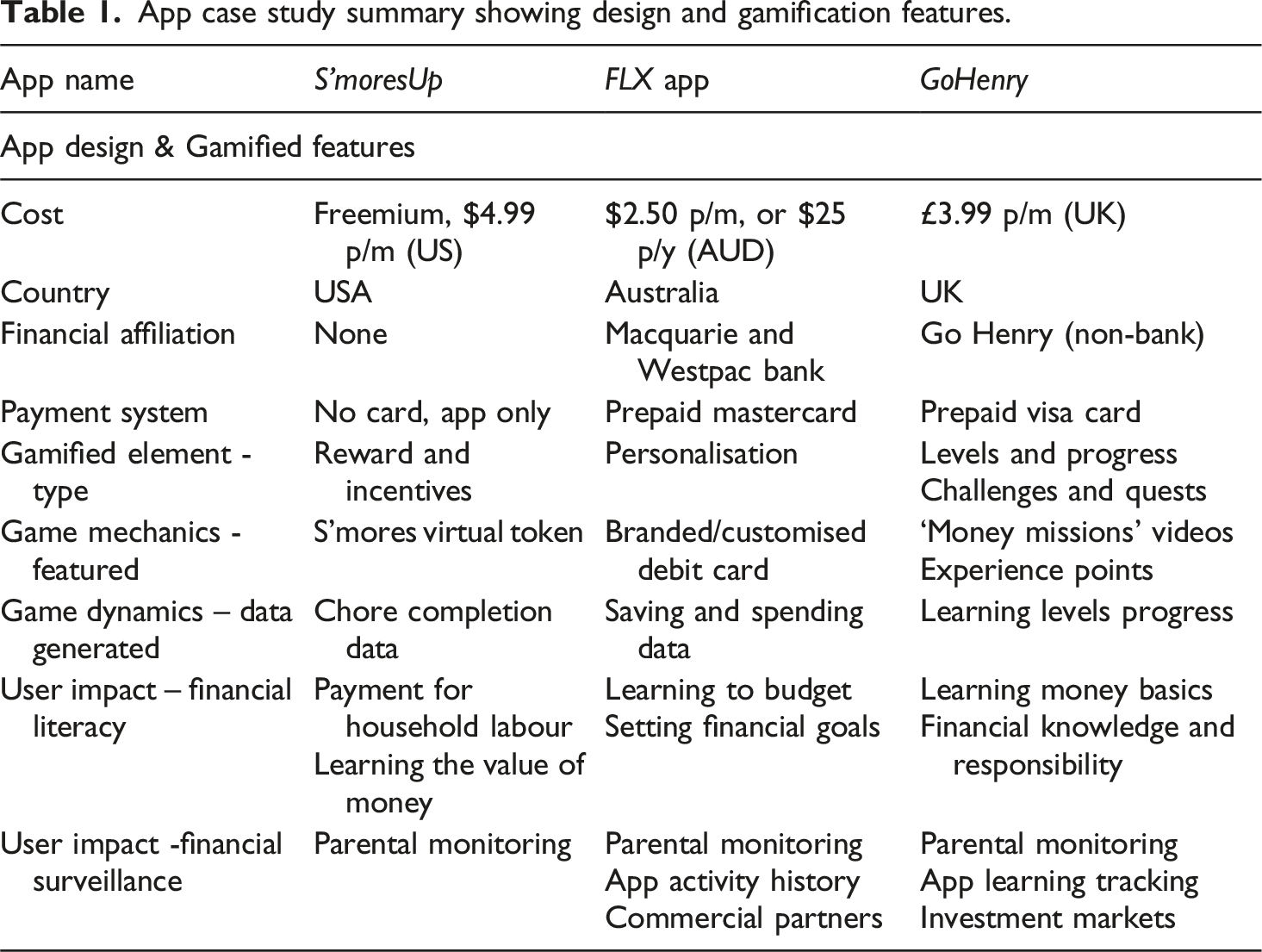

App case study summary showing design and gamification features.

Research has highlighted that in broader or adult FinTech spaces, the use of playful or game-like design elements is a common feature. O’Dwyer (2023), for example, highlights how tokens (or digital reward and payment systems) operate specifically within such gamified intersections of technology and finance to transform transactions into digital information, create detailed consumer records that datafy life, and drive the development of platform economies. Tokens, then represent, the wider gamification or use of game design elements in non-game contexts such as finance. Lai and Langley (2023) use the phrase ‘playful finance’ to understand such affordances in finance platforms, noting that ‘playful finance’ is deployed by platforms with the aim of making the technology more enjoyable to use by rewarding engagement, which in turn captures user attention and valuable economic behavioural data (Lai and Langley, 2023; Langley and Leyshon, 2021).

There is however, much less research on playfulness or gamification in the contexts of children’s FinTech platforms. Where gamification has been studied is in the specific use of apps to manage children’s household chores (Bjering et al., 2015; Nansen and Bliss, 2024). This limited research on gamification in children’s FinTech highlights the use of in-app rewards in children’s chore apps to compensate children for their household labour. Bjering et al. (2015), for example, found that these chore apps tended to focus on external rather than intrinsic motivation or incentives, and they targeted children’s chores individually rather than treating housework as a collective family dynamic. Nansen and Bliss (2024), also identified gamification elements in the chore functionality of the child finance app marketplace, highlighting how incentives via in-app rewards or penalties blurred conceptual distinctions between work and play, with children’s domestic labour promoted as fun when gamified features are utilised. Yet they also found that some of these apps also have the potential to redistribute family power relations and labour through features that make household work more transparent by allowing all family members including parents to record their household work.

We seek to extend the analysis of gamification in children’s finance apps by considering wider applications and contexts of playfulness and gamification in children’s Fintech platforms. These platforms do not only mediate chores but also have various combinations of features that enable the payment of allowances or pocket money, the management of children’s saving and spending, and the facilitation of financial learning and investment options. Our paper develops this area by focusing directly on the specific elements and impacts of playful affordances and gamified designs applied across a range of children’s Fintech products. As we explore, children’s finance apps use playfulness to create value to different constituents or stakeholders including children, parents, educators, and the finance industry. As we show below, children gain symbolic, virtual, and material rewards through gamified features and play around their chores, saving, and spending. Parents gain access to tracking and management features that provide for financial surveillance and regulation of their children. Educators and schools draw on and direct families to the resources developed by these child finance apps to assist in the broader financial education of children. Whilst digital finance platforms build children’s brand loyalty and platform attachment to extract valuable data about children’s consumer and financial lives.

In this paper, we identify playful affordances and gamified design features through three case study examples in which children are incentivised to complete chores, save and spend money, or learn about finances through digital rewards. The three case study examples are S’mores virtual tokens for incentivising household chore task completion within the S’moresUp app, “cool card designs” that use familiar brand franchises or personalised debit cards to attract children to the FLX app, and “money missions” that use points and levels to make financial learning appealing for children within the GoHenry app. These playful and gamified affordances encourage regular input and collection of children’s financial activity, information and transactions, build attachments to platforms through personalised branding and the accrual of valued in-app assets and status, and instruct children in norms of both digital finance and data surveillance.

Methods: Researching children’s finance apps

The study draws on app interface design methods from both feature and walkthrough analysis techniques (Hasinoff and Bivens, 2021; Light et al., 2018). These are well-established methodological approaches in platform studies, software studies, and critical UX research (e.g. Burgess, 2021; Dieter et al., 2019; Poell et al., 2019). Here, these approaches are adapted and applied through a case study analysis of specific examples of gamification features within different key child finance app platforms. Feature and walkthrough methods are evolving qualitative interface-based research approaches that seek to understand both individual app products and features incorporated across groups of app designs. The feature analysis approach is underpinned by the idea that app designers make assumptions about ideal users and focuses on common sets of features as they operate across a category of app types (Hassinoff and Bivens, 2021). A feature is defined as “any function that the user executes in the app, including anything the user can access, modify, or control” (Hassinoff and Bivens, 2021: 96–97). Feature analysis builds on the close attention other scholars pay to app interfaces and the ways culture is embedded in app design by specifically concentrating on documenting key app features and applying an analysis of the mechanisms and conditions of those features, as well as the ways they construct affordances around “cultural norms, assumptions, and ideologies” (Hasinoff and Bivens, 2021: 90). Walkthrough methods focus on how interface elements, affordances, visual rhetorics, and interaction flows organise user action and meaning, regardless of whether these effects were explicitly intended by designers. This makes them particularly well suited to analysing gamified systems, where motivation, reward, and behavioural nudging are embedded in interface design through icons, feedback, and progress indicators rather than solely through explicit instructions or content. By treating children’s FinTech apps as socio-technical artefacts, this approach enables systematic examination of how financial practices, values, and expectations are configured through design. Rather than seeking to reconstruct designers’ intentions, the analysis attends to how interfaces function as persuasive and pedagogical environments that actively shape how users are invited to understand saving, spending, and finance. These developer and user perspectives are addressed as a limitation and a direction for future research below.

We applied this app interface and feature approach to key case studies of children’s Fintech apps. The case study approach is informed by the app “walkthrough” approach (Light et al., 2018), which asks researchers to review and document the interface and operation of a specific app by downloading, onboarding, and spending time using the app in order to investigate design from the perspective of an app user, including the features “that mandate or enable an activity,” and the symbolic aspects of apps, including “the look and feel of the app and its likely connotations and cultural associations” (Light et al., 2018: 891–892). This approach, too, informs an understanding of affordances as shaped through the ways users appropriate the symbolic and material possibilities available within app environments. A case study approach was applied due to its capacity to provide a more focused, in-depth, and contextual understanding of an emerging or embedded phenomena (Flyvbjerg, 2001), such as the use and impact of playful affordances and gamification designs in children’s Fintech platforms. This approach offers qualitative and exploratory insights by integrating the app walkthrough of downloading, creating an account, exploring screens and features, and then taking a more targeted investigation by experimenting with the gamification elements and their operation within the app environment to allow for a detailed, contextual analysis.

We build on recent finance app feature analysis research, which has documented the range of features and their commercial operating models (Nansen and Bliss, 2024). We identified three key case studies, which we subjected to close analysis by downloading and using each of the three apps: S’moresUp, FLX, and GoHenry. We analysed the prevalence of playful and gamified features in which children are incentivised to save money, complete chores, or learn about finances through digital rewards such as points, tokens, badges, or levels. The three apps analysed originate from the United States, Australia, and the United Kingdom. Rather than offering a cross-cultural comparison, this selection reflects the prominence of English-language children’s FinTech platforms within Global North markets. Our aim is to identify shared design logics and commercial strategies across these settings, while recognising that regulatory, cultural, and educational differences may shape how these apps are produced and used. These contextual variations are addressed as a limitation and a direction for future research below.

Across the case studies, the units of analysis were gamification elements, and how these are operationalised and encoded through specific game mechanics, dynamics, and impacts (see Table 1). We documented the playful or gamified app features by reviewing information in App Store descriptions, company websites, and product reviews, as well as through the walkthrough and feature analysis methods described above. The gamifying elements identified in the three case studies analysed were rewards and incentives in S’mores tokens within the S’moresUp app, personalisation of debit cards within the FLX app, and levels, progress tracking, and challenges in the “money mission” learning levels in the GoHenry app. We then applied a gamification analysis framework to these elements to investigate game mechanics, game dynamics and user impacts in our discussion of the case studies below. Game mechanics include structural elements such as points, badges, leaderboards, tokens or progress bars as described above. Game dynamics focus on the data produced by these mechanics, and how this data encourages certain behaviours and actions. User impacts of gamification highlight individual outcomes in forms of financial literacy, as well as broader social or economic impacts of datafication or financial surveillance generated through these features. Table 1 below provides an overview of the gamification analytical categories studied – elements, mechanics, dynamics, and impacts – and their specific instances mapped onto the three financial app case studies.

Our analysis of gamified interface elements should be understood as analyses of design rhetoric – that is, how visual and symbolic elements are used to communicate values, expectations, and norms. We do not claim that children necessarily experience or interpret these elements in the same way; rather, we examine how such imagery is mobilised by the interface to frame financial labour, reward, and responsibility. Understanding children’s lived meanings requires empirical engagement, which we identify as an important direction for future research. Moreover, there is no reliable data on the volume of app usage for children’s use of FinTech apps based on commercial constraints and proprietary nature of these apps, which reflects the limited transparency surrounding children’s financial technologies.

Analysing examples of playful affordances in child finance apps

Tokens in S’moresUp app

S’moresUp app is a US-based chore management financial app recommended for children aged 6 and older, which involves the setting, monitoring, and management of children’s household chores. Chore tasks can be either ad hoc or scheduled, nominated as completed by children, and checked and approved by parents. Payment for completion of chore tasks is organised around digital tokens, which are disconnected from actual money payments, although they can be exchanged for money if parents set up an exchange price for the value of S’mores tokens. In S’moresUp, the app uses the symbol of a S’more as the reward token (see Figure 1). This symbol is based on the popular S’mores treat, which is made from toasted marshmallow and chocolate held between two graham crackers. They are popular camping and holiday treats, typically using a campfire to toast the marshmallow. And so, they signify ideas of family, enjoyment, and harmony, which the app token seeks to leverage. Screenshot of S’moresUp app reward token and tagline.

S’mores then are a representative example of gamification in children’s FinTech, with S’Mores tokens used for rewarding chore task completion to compensate children for their household labour. Prior research on chore apps suggests that such in-app rewards promote extrinsic rather than intrinsic incentives (Bjering et al., 2015). Here, we can see this extrinsic reward embodied by the playful symbol of a S’more, which is designed to incentivise children’s willingness to do chores without necessarily any actual monetary equivalence or payment. In turn, we can see how the visual illustrated image of the S’more represents a playful appropriation of a fun treat to represent a reward for completion of household chores and work. In doing so, this token blurs the distinct values inherent to play versus work through gamified features that attempt to make housework fun (Nansen and Bliss, 2024).

Because of these extrinsic and playful dimensions, gamification in child finance apps may promote ambiguous, contradictory, or even conflicting financial values in children. These contradictions position children as simultaneously working and playing for economic incentives via in-app rewards, potentially undermining traditional values associated with work ethic and the value of money. By extension, the playfulness of children’s FinTech apps within their gamified features is arguably designed to reduce children’s sense of chores as ‘work’, and displace the traditional link between children’s household labour and earned allowances (i.e. work and income) in favour of allowances as a form of ‘play’.

Moreover, the taglines of this app, “it’s a family thing” and “your partner in parenting” (S’moresUp app), appear to confuse the intended user or beneficiary of the app, suggesting it is an app for all the family, whilst simultaneously implying the app is there to serve and support parental authority in implementing and managing children’s household work. Such ambiguities in the distribution of work and responsibility are further compounded by the symbol of the playful S’more token operating across a spectrum of monetary value from none (symbolic reward only) through to varied rates of exchange for actual cash based on what monetary exchange rates parents decide to set the S’more at. Finally, to gain rewards, the app normalises parental surveillance through chore completion features that require children to take photos of completed tasks, or ‘tick off’ each chore as it’s finished (see Figure 2). Thus, work also becomes intimately linked to digital surveillance. Screenshot of S’moresUp completion monitoring settings.

This reward token then encourages regular input, as well as automated data collection about children’s labour, their chores, and the financial value placed on those transactions by families. And so, they also operate to datafy children’s economic activity, turning these playful digital transactions into data points of information that over time create detailed records of children’s financial lives, helping to drive the development of finance platform economies (O’Dwyer, 2023). This surveillance, whilst visibly enacted within families, becomes largely invisible in the wider finance platform economy as child finance data is collected through both playful and automated features that collect child data. Whilst practices of rewarding children for chores have long been part of family life, whether through pocket money, treats, or shared activities. What distinguishes their incorporation into FinTech apps is not the existence of incentives per se, but their formalisation within gamified, data-driven systems that track performance, allocate rewards, and visualise progress through persistent digital interfaces. In this way, affective and moral economies of effort and reward become embedded within platform logics of playful optimisation, parental monitoring, and behavioural design.

FLX app personalised debit cards

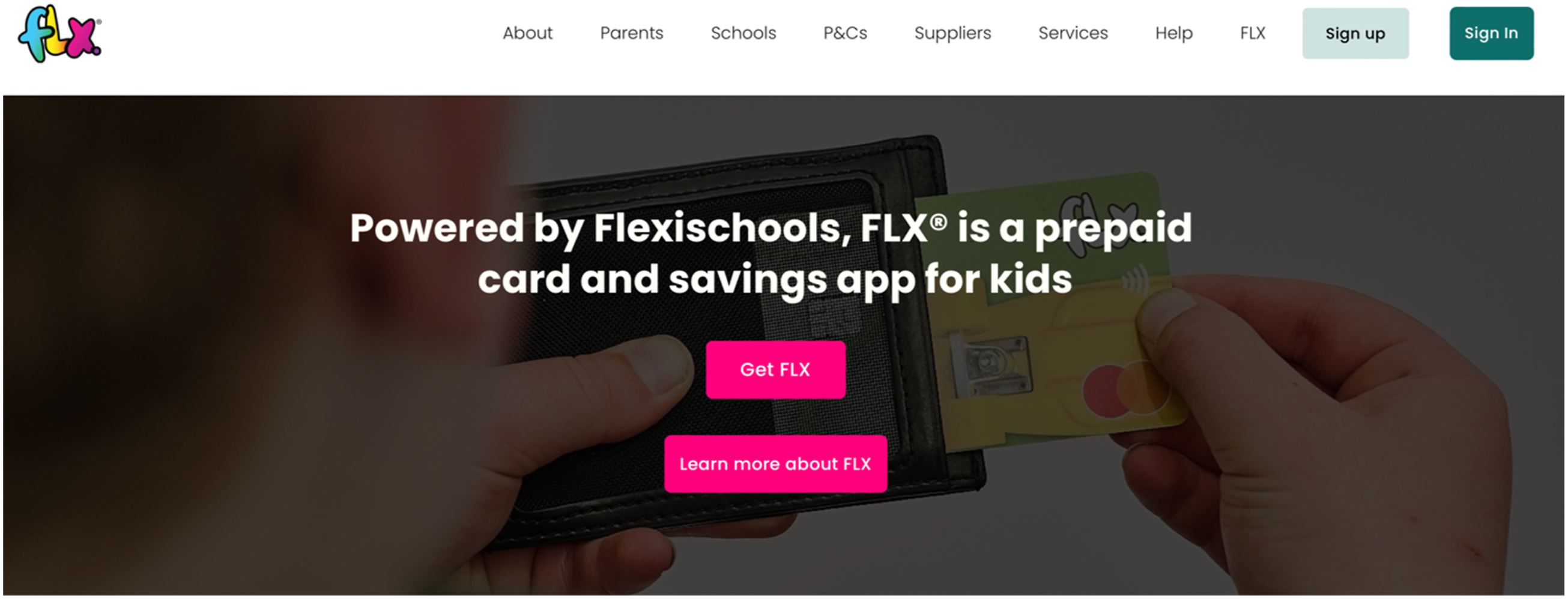

The next case study example is FLX app, an Australian finance app connected to a prepaid debit card for children, which is listed as appropriate for children aged 4 and older. Unlike the chore app described above, this is an example of a dedicated child finance app, which mediates children’s financial agency via banking and spending features (see Figure 3). In this and similar finance apps, key features are centred on payment and spending systems such as setting savings goals and child budgeting, parental money deposits and transfers, automated and scheduled money payments, mobile payments, and spending capacity with prepaid debit cards tied to platform accounts. Screenshot of FLX finance app with debit card website.

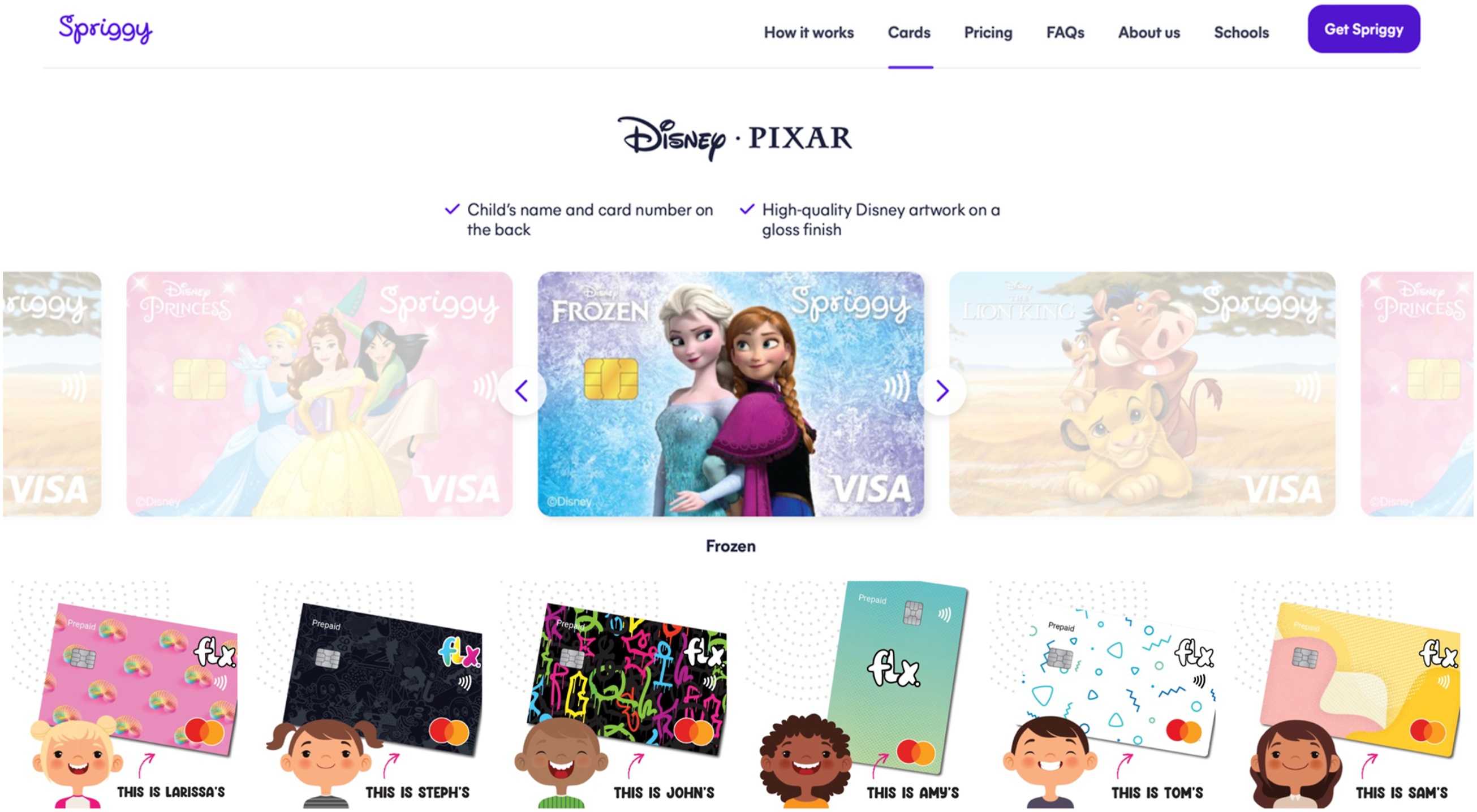

In addition, children are encouraged to choose from a range of “‘cool’ prepaid card designs”. Other examples of finance apps with customised debit cards include an app called Spriggy, which also offers branded collaborations with entertainment franchises such as Marvel and Disney for personalising debit cards (see Figure 4). Screenshots of personalised and branded debit card options.

Finance apps promote their utility as resources for teaching children how to save, budget, set financial goals and understand the value of money, as discursively positioned in tagline descriptions. Apps with financial features promote themselves as empowering children to develop their financial literacy, socialisation, and ultimately consumer agency: “FLX is a safe and secure way to teach your kids how to earn, save, and spend. Teach your child financial literacy within a safe and secure platform” (FLX app). Here, FinTech platforms discursively position themselves as remedying gaps in financial literacy education, either at home or in schools. Indeed, in Australia, public schools promote this private application, with FLX part of the flexischools system, which is mandatory for use in many schools for children to access and use school canteens and uniform services, creating a potentially closed economic system where third-party services privilege or imply the need for families to purchase and adopt these commercial FinTech products. This financial education occurs through the child savings and spending features in which children are encouraged and supported to achieve savings goals and learn about budgeting. Complementing savings features are payment systems and spending functionality for children, which ostensibly develop children’s consumer understanding, activity, and agency, and particularly in the use of prepaid debit cards.

A more critical view of these features, however, suggests the use of playful affordances such as personalised and branded debit cards are designed to appeal to and create a market of young users by enabling them to display aspects of their identity, aesthetic preferences, and cultural taste. In addition, these personalised or branded debit cards are designed to build children’s consumer identification, brand loyalty and attachment to the finance platform by creating a sense of identity and ownership, and thus by extension an attachment to the FinTech digital finance industry more broadly through the personal data these cards help to capture and record. Several consequences flow from this attachment. One, finance apps ensure children’s purchasing power and thus regular consumption and participation in consumer capitalism (De La Rosa and Tully 2022). Two, their displacement of physical cash for digital money in the lives of children plays a crucial role in aligning children’s financial socialisation with digitally driven finance. And three, child financial agency is enabled by the same surveillance features that exploit their data.

In terms of compelling regular consumer participation, the digital money provided in children’s FinTech apps can be seen to limit the risks of children carrying physical cash and facilitating child consumer purchasing power transacted both in stores and online (Chowdhury, 2019). Clearly, these apps play a crucial role in the displacement of physical cash for digital money in the lives of children. Our analysis does not imply that children should be restricted to cash, nor that debit cards are inherently inappropriate. Rather, our focus highlights how children’s personalised debit cards function within platform ecosystems that link financial activity to branding, data generation, and behavioural nudging. These dynamics warrant critical attention because they shape how children come to understand money, identity, and participation in digital economies from an early age.

In doing so, these apps may mediate children’s financial socialisation in ways that align with increasingly digitally driven consumer cultures and markets. This agency may, however, be challenged by the digital surveillance and control features of children’s finance apps. On one hand, surveillance works for purposes of child security and parental care, whilst on the other, fostering an intensive datafied surveillance of family life (Lupton and Williamson, 2017; Mascheroni and Siibak, 2021). We can see that the economic data collected could be of value to children and parents. For example, the financial data produced within these apps might have personal and family value, such as creating a history of children’s spending that shows their consumer identity and changing lifestyle preferences and interests as they grow. Parental control features enable monitoring and management of children’s financial safety by temporary blocking spending, blocking age-inappropriate merchant categories, or restricting or preventing cash withdrawals. These embedded and remote modes of parental financial control then enhance parental modes of surveillance for children’s spending. Or in some cases, facilitate other forms of tracking, with notifications of child purchases showing parents the real-time geo-location of their child. Indeed, apps keep all transactions digitally recorded and tracked, limiting children’s financial independence. And by limiting access to cash, children have reduced opportunities to spend on items privately without a record of the transaction. Such dynamics can reduce children’s financial privacy, potentially fostering mistrust and a lack of financial development, agency and independence. So, whilst these apps are promoted as building children’s financial safety, support, and independence, the financial lives of children become datafied in ways that further entrench norms of parental monitoring, decreasing their privacy and independence (Mavoa et al., 2023; Page Jeffrey, 2021).

More invasively, this datafication serves commercial and financial institutions that may be less visible than those between parents and children but are much more widely pronounced with children’s financial activity. This activity is translated through digitisation into valuable data points, which can be aggregated and analysed to produce economic value for FinTech platforms and the finance industry. This institutional datafication is largely invisible but also traded off for personalisation features such as branded debit cards. These personalised cards are designed to encourage brand loyalty that entangles child finance data collection with extended networks of third-party commercial partners, data brokers and finance markets, enabling detailed financial data analysis and profiling of children through their spending patterns and histories.

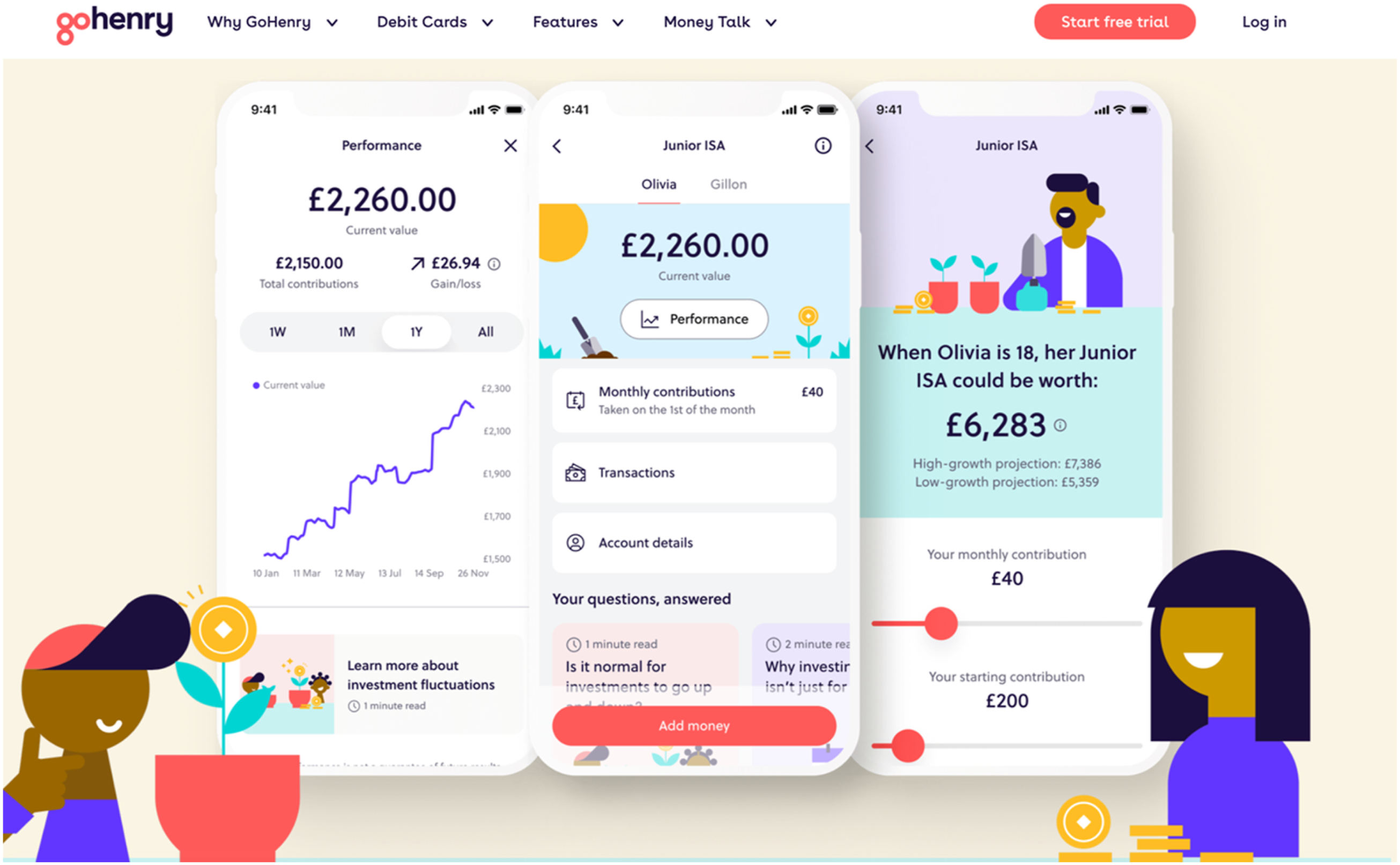

Challenges and levels in GoHenry app “money missions”

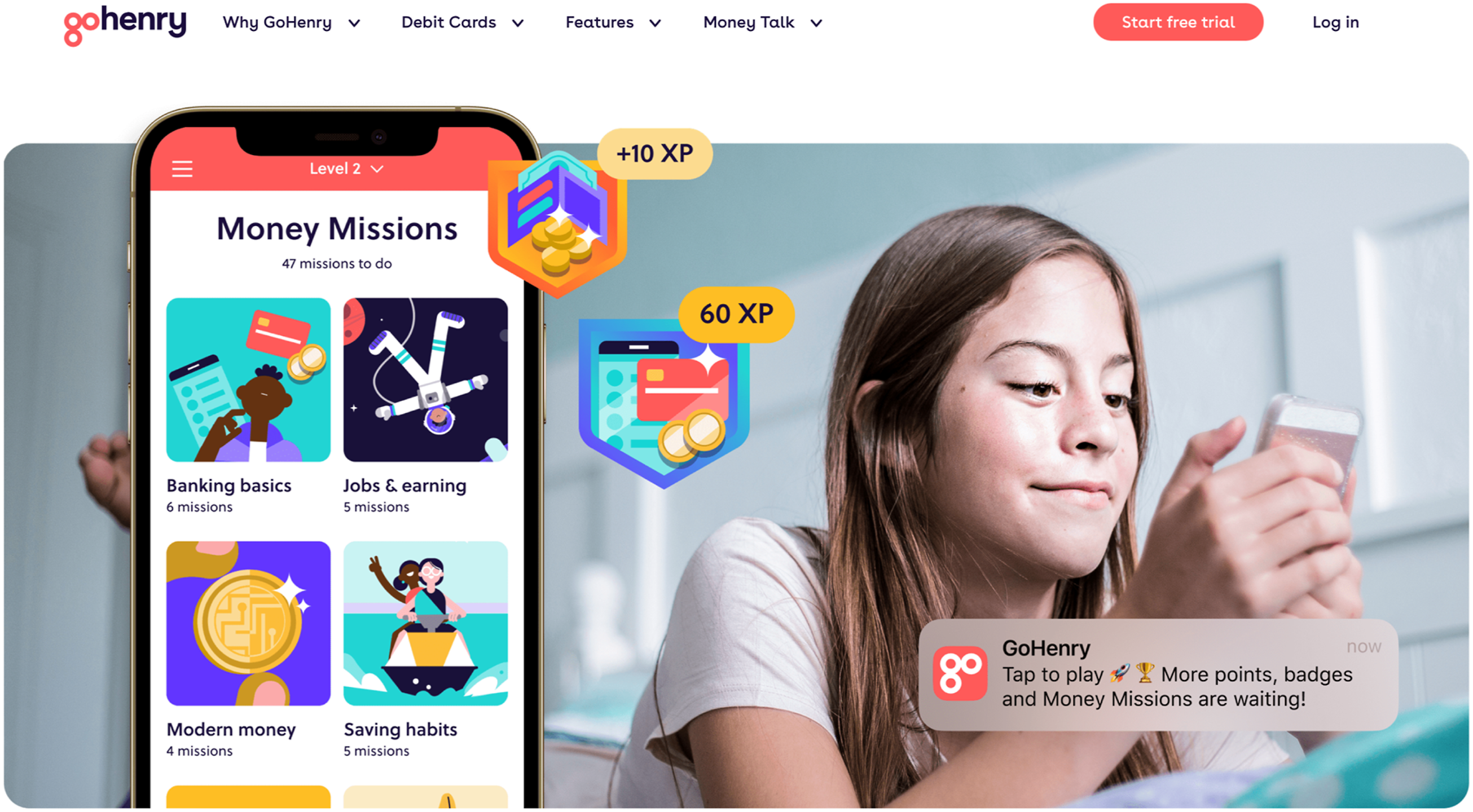

The final case study is GoHenry, a UK-based banking and finance app designed for children aged 6–18, which includes both chore and finance features noted in the previous app examples. In addition, and more importantly for the analysis here, GoHenry also includes a gamified education program comprised of animated videos and interactive quizzes designed to teach children about money and finances, called ‘Money Missions’. Money Missions cover a range of topics such as money basics, saving, budgeting, investing, credit, money safety and so on (see Figure 5). Screenshot of GoHenry app advert for money Missions and reward points.

The developers advertise that “Money Missions are designed to make financial education fun, building confidence, literacy, and curiosity in 6–18-year-olds” (GoHenry app). Visually, these missions use thumbnails with playful, colourful images of scenes, such as astronauts or jet skiing, to appeal to young people. And they deploy a range of gamified elements including experience points (XP) as a reward token system, as well as levels and progress tracking of missions, which get progressively more advanced. These levels, then, provide a visual indication of financial learning progress and unlock more sophisticated financial content to encourage continued activity and give reinforcement through feedback. These gamified systems reward in-app behaviours such as financial learning activity completion, with the accrual of experience points (XP) able to be exchanged as an in-app currency for purchasing other virtual goods such as virtual badges that visually signify skills or accomplishments achieved. These missions also operate as gamified challenges through a ladder of levels that encourage engagement and a sense of purpose or direction through the promotion and attainment of specific financial learning goals in each level.

The developers further claim that this FinTech platform was not developed purely by the finance or start-up industries, but in collaboration with educators to build pedagogically appropriate financial content for children of different ages. They state that the money missions were “developed with teachers and financial experts and mapped to age-appropriate education guidelines in the UK and US” (GoHenry app). And so, their marketing suggests that the app developers developed the content of their money missions in partnership with pedagogical experts to complement school financial education curriculum, and that educators and policy makers endorse the use of this app to assist in the broader financial education of children. Clearly, they aim to teach financial literacy to children, filling in pedagogical gaps for financial literacy skills not taught in schools (Sawatzki, 2018). Yet in doing so, these apps also promote digital finance products to create brand awareness and consumer loyalty and dependence under the guise of developing a desired responsible financial citizen or subject (Maman and Rosenhek, 2023). Money missions then, can also be seen to train norms of family responsibility for securing the financial safety and literacy required of this subject.

More niche topics covered by GoHenry “money missions” include stock market investing, along with in-app tools for parents to establish and manage children’s personal stocks and shares individual savings accounts (see Figure 6). These are ostensibly designed to encourage more advanced financial literacy or activity, yet can also be seen to reinforce the dominance of financial markets and speculation in children’s economic participation. So, whilst child FinTech platforms may disrupt traditional banking institutions or services, they nevertheless actively partner with financial payment services and financial trading and investment companies to reinforce the dominance of financial ideologies of labour, speculation, and profit. The type of financial literacy privileged through digital transactions, education, and niche investment features can be seen as serving to establish and entangle child consumers as dependent upon FinTech platforms and as lifelong customers of the finance industry. And thus, such apps enrol children as active participants with agency and responsibility in the development of their own financial socialisation. Screenshot of GoHenry app stock investment performance.

Conclusion

In conclusion, we find that these child finance apps leverage playful affordances to both shape and quantify children’s economic behaviour, while also creating an early presence of FinTech platforms in children’s lives. In this study, we identified the prevalence of numerous gamified features and designs in which children are incentivised to complete chores, document their savings goals, embrace debit cards and digital consumption, or learn about money and finances through digital rewards. This study is significant in developing the emerging field of child FinTech studies, and specifically by bringing concepts of playfulness, affordances, and gamification from digital platform and games studies to this field. We find that these playful affordances and gamified design features in children’s finance apps encourage regular input and collection of children’s economic activity and information, build attachments to platforms through personalised branding or valued in-app tokens, assets and status, and instruct children in norms of both digital finance and data surveillance. The study shows that, on the one hand, these playful affordances facilitate forms of datafication that confer agency to both parents and children in setting, tracking, completing, and documenting saving, spending and finances. Yet they also work as data points to be aggregated and analysed to produce economic value for finance platforms and the FinTech industry.

Together, these findings highlight how children’s FinTech apps function not only as financial tools but as pedagogical and commercial platforms that shape how young users learn to understand money, work, and responsibility. By foregrounding design, gamification, and datafication, this study opens pathways for future research that combines interface analysis with interviews, ethnography, and regulatory study to better understand how these systems are designed, experienced, and governed. We do not argue that children’s FinTech apps should not exist, nor that children should be excluded from digital financial participation. Instead, our findings point to the need for more transparent, ethically grounded, and developmentally sensitive approaches to the design and governance of children’s financial technologies. We call for greater attention to how commercial, pedagogical, and data-driven logics intersect in shaping children’s financial futures.

This study focused on playful gamification features in children’s FinTech apps and so has clear limitations in its scope and analysis, which is focused on the technology rather than the wider social, economic, or political contexts around child finance products. A key limitation of this study is that it focuses on the analysis of interface design rather than on the perspectives of designers or users. This study is grounded in a design-centred analysis of children’s FinTech apps, using app walkthrough and feature-based methods to examine how interface elements, gamification, and visual rhetorics structure financial practices and meanings. While this approach provides robust insight into how platforms organise behaviour through design, it does not capture how these systems are produced by developers or experienced by children and families in everyday life. Future research would therefore benefit from combining interface analysis with interviews and participatory methods involving both app designers and child and family users, to better understand how design intentions, commercial priorities, and lived experiences intersect with the logics embedded in these platforms. The study is also limited by the availability of empirical data on children’s engagement with FinTech apps. Greater transparency from regulators and companies, as well as independent empirical research, would be crucial for assessing the scale, distribution, and social implications of children’s participation in digital finance. Moreover, comparative and locally grounded studies would be an important direction for future work, as our selection of apps from the United States, Australia, and the United Kingdom limits the scope of research. Our intention, however, was to identify shared design logics within English-language, Global North markets rather than to offer a systematic cross-cultural comparison.

Finally, while practices such as rewarding children for chores, encouraging saving, or using visual prompts to motivate financial behaviour have long histories in family and educational settings, their incorporation into data-driven, gamified platforms introduces new forms of tracking, automation, and commercial mediation. Further research is needed to examine how these historical continuities and digital transformations intersect in children’s everyday financial lives, and to explore how alternative design and governance models might better support children’s financial learning without embedding them so deeply within commercial and surveillance-oriented infrastructures. For example, while we cannot explore the impact of wider trends in FinTech here, such positioning is potentially reflective of the “financialization of everyday life”, in which households embrace financial cultures that value self-sufficiency, entrepreneurship, and self-management of risk within a global financial framework (Fligstein and Goldstein, 2015). Clearly, there are new and emerging children’s investment apps too, such as Pigzy, Raiz Kids and Spriggy Invest, which offer children the chance to open accounts and trade in shares, and so have the potential to radically reconfigure the financialisation of childhood by intensifying demands on children’s financial rather than consumer knowledge and participation, and we note these demand greater research attention. Following from these limitations, future work will investigate family and child experience, perceptions, and use of these apps, extend the focus to investigate financial investment apps more thoroughly, and examine issues of child data privacy through data governance, terms of service policies, and data markets.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Australian Research Council; FT250100270.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.