Abstract

Charitable giving is a socially desirable behavior, and therefore prone to misreporting. In this article, we survey two decades of published research to understand the extent to which objective measures, capturing observed behavior, are used in philanthropy research. A systematic review of 437 articles found that 73% included at least one subjective (i.e., self-reported) measure and only 33% included at least one objective (i.e., observed behavior) measure. Objective measurement was more common in economics journals, research conducted in Western Europe, and studies using archival or experimental methods; and especially uncommon in nonprofit studies journals and survey research. We also generate an inventory of the diverse ways that charitable giving has been measured, both subjectively and objectively, as a resource for philanthropy scholars. Finally, we close with recommendations for future research detailing when and how we can include more objective measurement of charitable giving.

Charitable giving, or voluntary financial donations, are the lifeblood of many nonprofits. Without funding, nonprofits would be unable to deliver their essential work across a range of social and environmental issues. Whether searching for a cure for cancer, supporting vulnerable people and animals, or addressing climate change, nonprofits rely on funding to achieve their missions. The amount of nonprofit funding that comes through charitable giving from community members is significant: in the United States, for example, private donations exceeded $557 billion in 2023 (Giving USA, 2024).

Generosity is commonly considered to be socially desirable: people generally like others who are generous and want others to think of them as generous too (Lee & Woodliffe, 2010). One drawback of studying socially desirable behavior is that people may be prone to misrepresenting their actions to be seen in a positive light. This appears to be the case with charitable giving. Although self-reports and actual behavior are typically positively correlated (r = .24; see Chapman, McKay, et al., 2025 for a meta-analysis), self-reported measures remain imperfect proxies for real-world charitable behavior. Lee and Sargeant (2011), for example, asked U.K. donors how much they had given in the previous 12 months and matched their responses to their actual donation history. Two-thirds (65%) of those donors over-reported their generosity. Bekkers and Wiepking (2011) did the same with donors in the Netherlands and found that 57% of donors overestimated their generosity. Furthermore, a recent meta-analysis of 242 effect sizes drawn from 143 independent studies found that only 6% of the variance in observed prosocial behavior (including, for example, charitable giving, blood donation, and recycling) could be explained by self-reports drawn from the very same sample (Chapman, McKay, et al., 2025). This leaves a substantial 94% of prosocial behavior unexplained by what people self-report.

Despite being imperfect proxies for charitable behavior and prone to social desirability biases, self-reports may still be valid for measuring giving if they return similar conclusions to more ecologically valid measures (i.e., measures that are closer to the real-world behavior being studied; Kihlstrom, 2021). Early evidence, however, suggests this is not the case: studies that have included both types of measure have often returned substantially different effects (either in direction, significance, or size) on self-reported versus objective measures (e.g., Lichtenstein et al., 2004; Shang et al., 2020; Zhou et al., 2021).

If self-reports about giving are imperfect proxies for actual giving behavior, and if subjective and objective measures return different conclusions, then relying primarily on self-reported giving measures may undermine confidence in research conclusions. The reduced external validity with self-reports could have significant downstream consequences because these measures are often used to build theories, test interventions, and make recommendations for practice.

There are a range of pragmatic reasons that self-reported measures are widely used. Subjective measures are arguably the easiest way to capture information relevant to giving, as they can easily be embedded into surveys and lab experiments (Connors et al., 2016); although, as we shall see, there are a range of objective measures that can also be embedded as easily. Subjective measures also do not require additional funding or partnerships with nonprofits, as some objective measures do. In certain contexts, subjective measures have also been shown to have superior psychometric properties than equivalent objective measures (Corneille & Gawronski, 2024; Dang et al., 2020). As we shall see, subjective measurement is also widespread, which likely gives researchers confidence that their work will be publishable without objective measurement. Finally, it is possible that many researchers are not aware that conclusions may vary depending on the measure chosen.

Criticisms of and discussions around best practices in survey research on charitable giving are not new (see, e.g., Bekkers & Wiepking, 2006; Cnaan et al., 2011; Hall, 2001; Lee & Woodliffe, 2010; Rooney et al., 2004; Wilhelm, 2007). However, to date, there has been no broad survey of the field to understand what our collective practices are. Neither, to our knowledge, have there been any systematic discussions around the use of subjective and objective measurement in philanthropy research. Given the rapid expansion of the field, with approximately 50% of all research published in the last 6 years alone (Chapman, Louis, Masser, & Thomas, 2022), the time is ripe to assess the state of charitable giving measurement practices.

In this article, we distinguish between two broad orientations in measurement: subjective and objective. We use the term subjective measurement to refer to forms of measurement where the participant self-reports their giving intentions, willingness, or behavior. Such subjective measures may include, for example, self-reported giving intentions and self-reported past donations. By objective measurement, on the other hand, we mean verifiable records of actual behavior. Examples of objective giving measures include consequential donations (i.e., those involving real money) captured within research studies, where participants can donate some of their participation fee or a bonus payment, as well as transactional records and behavior observed by a third party.

Given the observed discrepancies between subjective and objective measures of charitable giving and the rapid growth in this field of study, the purpose of this paper is to understand the current state of scholarship on charitable giving and provide recommendations for the future. Specifically, this article has three goals. First, we systematically review the literature to understand how charitable giving is currently measured and how measurement practices have varied over time, and across different geographic regions, disciplines, and methods. Second, we provide an inventory of both subjective and objective measures of charitable giving. This is intended to be a resource for the growing number of scholars who wish to study charitable giving. Third, we outline recommendations for how to increase the use of objective measurement and suggestions for when subjective measurement may be appropriate. In doing so, we hope to generate a practical resource for scholars of charitable giving while also suggesting directions for future scholarship in this rapidly growing field.

Systematic Review

To understand how charitable giving is currently being measured, we conducted a systematic review to identify empirical research articles that measured charitable giving and had been published since 2004. Our review methodology was informed by the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) protocols (Moher et al., 2015).

Search Strategy

We ran searches in July 2024 across the two largest multidisciplinary academic journal databases: Scopus and Web of Science. Rather than to identify every study ever conducted, our goal was to generate a large corpus of research on charitable giving and ensure a comprehensive snapshot of the field. This approach allowed us to identify a wide range of studies with varying measures to illustrate the diversity of measurement in the field, while also facilitating the timely dissemination of findings that is needed in a rapidly expanding field.

Search terms were nested around the concepts of nonprofits (not for profit*, not-for-profit*, non profit*, non-profit*, nonprofit*, NGO*, non governmental, non-governmental, third sector) and charitable giving (charitable giving, charitable gift*, donat*, philanthrop*, bequest*, fundrais*, prosocial*). We used these terms to search titles, abstracts, and keywords and restricted searches to articles written in English, published in peer-reviewed journals since 2004, and indexed under relevant subject categories in the database (e.g., psychology, business, social sciences, economics). Further details of the search and screening process are outlined in the preregistered PRISMA-P document available on the Open Science Framework (OSF; https://osf.io/rz9vf/). Searches identified 3,182 unique articles.

Screening

The first author screened all identified articles in three rounds: based on title, abstract, and full text, respectively. To assess the reliability of the screening, the fifth author independently screened a random 10% selection of records (n = 318) using the preregistered PRISMA protocol. The two screeners agreed on 89% of decisions (Cohen’s κ = .68), indicating “substantial” level of inter-rater agreement (Gisev et al., 2013).

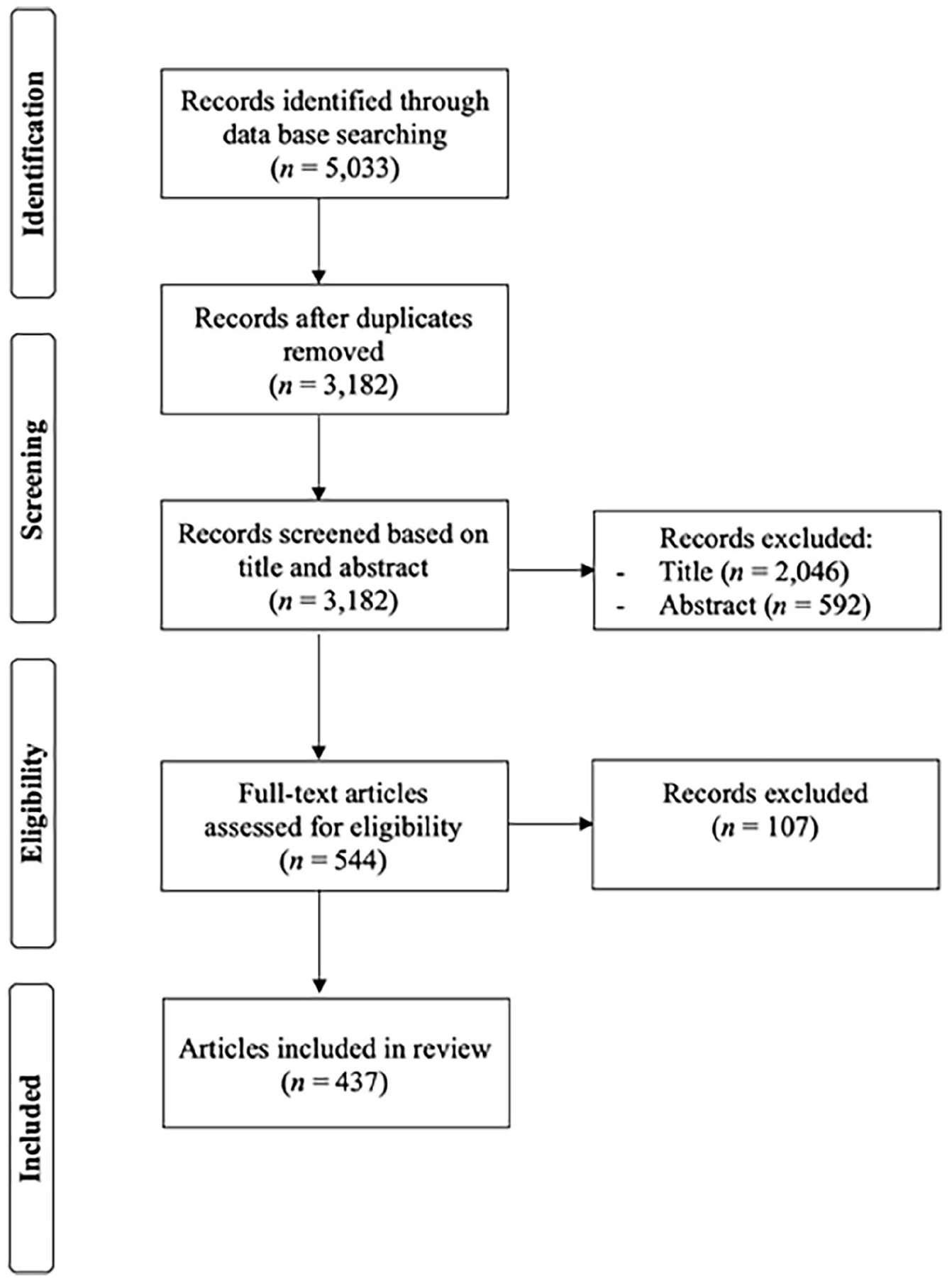

To be included, articles must have been empirical in nature, specifically measured charitable giving, and been published in a peer-reviewed journal. Conceptual articles, review articles, conference abstracts, dissertations and theses, articles published in languages other than English, and those published before 2004 were all excluded. Following our preregistered protocol, we also excluded articles that examined non-financial donations (e.g., time, blood, goods, body parts), organizational giving (e.g., corporate giving, foundations), or giving occurring in exchange relationships (e.g., cause-related marketing, charity auctions), and studies considering the recipient-level (e.g., what the charity receives) rather than donor-level (i.e., what the donor gives). The screening process is summarized in the PRISMA flowchart (Figure 1). Following screening, a final corpus of 437 relevant articles was identified.

PRISMA Flowchart Summarizing the Screening Process.

Data Extraction

To summarize the existing corpus, the first and second authors extracted the basic attributes of the articles: year of publication, discipline, country where the data were collected, study design, type of measure, and item wording. A coding spreadsheet summarizing these data is available on the OSF.

How Charitable Giving Is Being Measured

Before zeroing in on our focal project—to summarize the relative use of objective and subjective measurement in the field—we first briefly overview the corpus of research. The primary objective in doing so is to provide a snapshot of the last two decades of charitable giving measurement. Next, we summarize the field in terms of the relative use of objective and subjective measurement. Finally, we identify and test possible moderators to explain when objective measurement has been more, or less, prevalent.

Summary of the Corpus

The corpus of research on charitable giving covered a period of over 20 years and reported studies conducted in 49 different countries. Most of this research was done in countries in North America (50%), Western Europe (18%), and to a lesser extent Asia (13%). Comparatively few studies were drawn from samples in the Middle East (4%), Australasia (3%), Eastern Europe (2%), Latin America (2%), and Africa (1%). Although not focal to the current study, this suggests that philanthropy research has been conducted primarily in countries that can be described as WEIRD (i.e., Western, Educated, Industrialized, Rich, and Democratic; Henrich et al., 2010). Wiepking (2021) argues that we need to expand our understanding of generosity behaviors by considering how they may manifest in different cultural contexts so that theorizing and empirics represent a truly global perspective. Because the current corpus of studies contains largely WEIRD data, we suggest that there is still a way to go before we have an inclusive and representative body of knowledge on charitable giving.

Charitable giving is an interdisciplinary research topic. Within the current corpus of studies, outlets for publication included journals dedicated to the disciplines of marketing (n = 162), nonprofit studies (n = 151), management (n = 45), and economics (n = 36), as well as a broad range of other disciplines. Articles could be coded into more than one category if the journal was interdisciplinary in nature. For example, 66 articles were published in journals straddling the disciplines of nonprofit studies and marketing (i.e., those dedicated to nonprofit marketing), which are particularly common outlets for publishing charitable giving research.

Various methods have been employed to study charitable giving. The most common approach is through surveys, with 53% of all identified articles including survey data. Experimental methods were also common: 38% of articles reported lab experiments, which were conducted in controlled environments (whether offline or online) where participants knew they are taking part in a study (Cockrill & Parsonage, 2016). A further 7% reported field experiments, which were conducted in real-world settings with participants who did not know they were involved in research. Archival studies—where existing data like supporter databases or website records are analyzed—were reported in 9% of articles. Less common methods included dictator games (3%), conjoint models and choice studies (2%), and interviews (1%).

Finally, as discussed above, there has been a noticeable uptick in the rate at which new articles on charitable giving have been published. Indeed, half (50%) of all the identified research has been published since 2019. Only four new articles were published in 2004 (the first full year in our sample), compared with 42 in 2023 (the last full year). This represents a 10-fold increase in the rate of research in our field over the last two decades and further motivates the value of the current project to audit how giving is measured and orient the field toward the future.

Subjective and Objective Measurement

Across the corpus, subjective measures were more common than objective measures. Overall, 73% of articles reported at least one subjective measure and 33% reported at least one objective measure. Two-thirds of articles (67%) only measured giving subjectively, just over a quarter (27%) only measured it objectively, and only 6% of articles included at least one subjective and at least one objective measure.

Throughout this article, we also identify two broad orientations in the way that charitable giving can be assessed: donation likelihood and donation value. Measures assessing donation likelihood consider whether a donation will be made at all and relate to the decision to donate (or not). Measures assessing donation value consider how much will be given and relate to the value or amount donated. Both donation likelihood and donation value can be assessed either subjectively or objectively.

Subjective Measures

Among subjective measures, the most common approaches were to ask about giving intentions (34% of the studies using subjective measures), self-reported past giving (24%), or willingness to donate (19%). A third (36%) of studies using subjective measures considered the donation value, and only 6% considered the frequency of giving. The majority considered the likelihood of any gift being made.

Objective Measures

Among objective measures, assessing donation value was more common (86% of the studies with objective measures). Frequency of donations was still rarely considered (7%). The kind of objective measure also varied. Less than half (42%) of studies with objective measures examined people’s choices to donate their personal money, which they had earned independent of the study. A third (35%) considered the choice to give away some or all of their earnings from participating in the study. Finally, almost another third (29%) examined giving choices in the context of either a bonus (i.e., extra money the participant had not anticipated receiving) or a lottery (i.e., low odds of winning extra money). Lotteries were more commonly employed than bonuses, at a ratio of 3:2. There are psychological and practical differences in these different measures that may affect their validity, which will be discussed in more detail below.

Comparisons in the Use of Objective Measurement

We considered whether the rate of objective measurement use varied across different disciplines, countries, methodological approaches, or time periods. For statistical comparisons, we retained only categories that contained at least 30 observations. Chi squared tests for independence were run to determine whether the rate of subjective and objective measurement use was dependent on various possible moderating factors (see Figure 2). Where the moderation was found to be significant, we used chi squared goodness-of-fit tests to identify whether the rate of “objective only” versus “subjective only” versus “both objective and subjective” measurement use within the category differed significantly from the overall rate observed across the corpus.

Summary of the Relative Frequency of Subjective and Objective Measures of Charitable Giving Across Different Disciplines, Geographic Regions, and Methods (n = 437 articles).

Discipline

Measurement use varied across journal discipline, χ2(4) = 37.51, p < .001, Cramér’s V = .15 (a medium effect size, following Cohen, 1992). While rates of measurement use within marketing and management journals were not significantly different from the overall corpus, ps ≥ .248, significant differences were observed for the other disciplines. Articles published in nonprofit studies had higher than expected rates of subjective measurement and lower than expected rates of objective measurement, χ2(2) = 17.92, p < .001, whereas the reverse pattern was observed for articles published in economics journals, χ2(2) = 25.20, p < .001.

Geographic Region

Measurement use also varied across different geographic regions, χ2(3) = 14.10, p = .003, V = .10 (small effect size). Research conducted in Western Europe employed objective measures at higher rates than expected, χ2(2) = 13.31, p = .001, whereas the measurement use in North America and Europe did not differ statistically from the overall corpus, ps ≥ .074.

Method

Measurement use varied substantially across method of research, χ2(3) = 172.84, p < .001, V = .36 (large effect size). Articles reporting survey research disproportionally relied on subjective measures and used fewer objective measures, χ2(2) = 62.19, p < .001. Archival research, χ2(2) = 64.99, p < .001, field experiments, χ2(2) = 67.60, p < .001, and experiments conducted in the lab or online, χ2(2) = 18.83, p < .001, all used objective measures at disproportionately higher and subjective measures at disproportionately lower rates.

Time Period

Comparing measurement use over 5-year time blocks (i.e., 2004–2008, 2009–2013, 2014–2018, 2019–2024), we found that measurement use did not vary across time block, χ2(3) = 3.05, p = .384. In other words, the relative frequency of objective and subjective measurement use has not changed significantly over the two decades that we have considered.

Inventory of Charitable Giving Measures

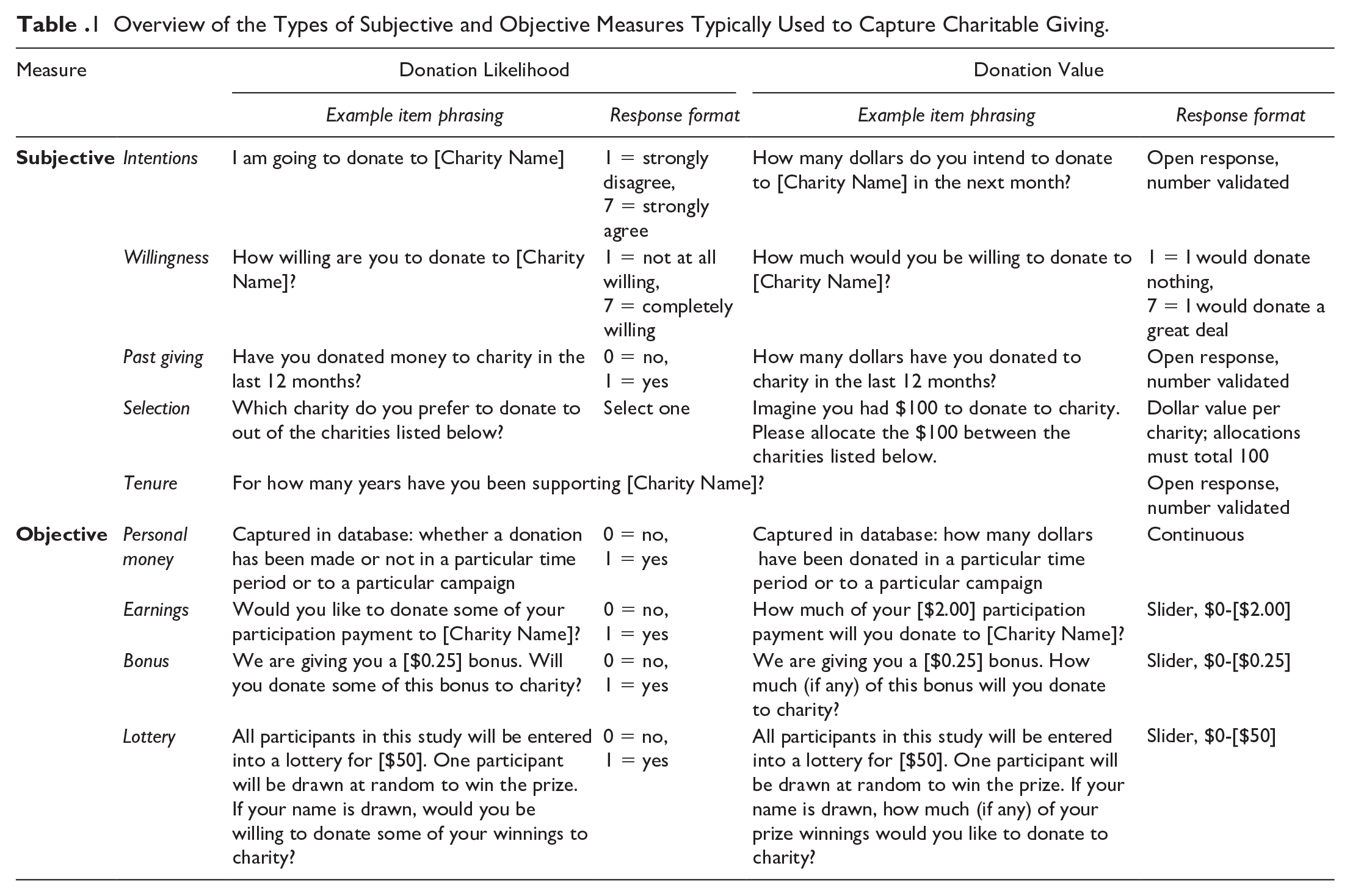

For both incumbent and emerging scholars in the field, in this section we provide an inventory of the different ways that charitable giving has typically been measured (summarized also in Table 1). We summarize approaches to both subjective and objective measurement. For each measurement approach, we provide a few examples of articles that have employed it. Details of every article that was identified in our systematic review and the approach they used for measurement can also be found in the coding spreadsheet that is available on the OSF.

Overview of the Types of Subjective and Objective Measures Typically Used to Capture Charitable Giving.

Subjective Measures

Donation Intentions

One common approach is to ask participants whether they intend to donate to charity in the future. Donation intention measures are sometimes single items but more commonly multi-item scales. Most intention measures consider the intention for any donation to be made. Example items for donation intention scales include: “If I can, I intend to make charitable donations in the near future” (Lee & Kim, 2023), “I will definitely donate to the charity in question in the future” (Merchant et al., 2010), “I will donate money to charities or community service organizations in the next 4 weeks” (Millán et al., 2024), and “I intend to donate to this NPO [Nonprofit Organization] in the near future” (Tao et al., 2021). Occasionally, measured intentions related instead to the intended value of donations (e.g., “If you were asked to donate to [Charity Name], how much money would you donate right now?”; Aghakhani et al., 2019) or the intended frequency of future donations (Hou et al., 2017; Kinsky et al., 2015).

Donation Willingness

A person’s willingness to donate was often called donation intentions in the articles we analyzed (e.g., Cho et al., 2019; Harrison et al., 2022; Kim, 2014; Li & Feng, 2021), although we propose that these two constructs are subtly different. Willingness is more about openness, whereas intentions tap into commitment or plans. Various measures of willingness have been employed, both with single items and multi-item scales. Example scale items include: “I am willing to make a donation to [Charity Name]” (Cao & Jia, 2017) and “To what extent would you be willing to donate money to this organization?” (Goh et al., 2021). Willingness measures typically assess how willing the participant is to donate at all rather than the value they would be willing to donate. Occasionally, however, the frequency with which they would be willing to donate has been considered. For example, Choi and colleagues (2019) asked participants how often they would be willing to donate in the future, with response options ranging from “no plan to donate in the future” to “once every month or more frequently.”

Self-Reported Past Giving

Another common way to capture charitable giving subjectively has been to ask people to report what, if anything, they have given in the past. This approach was sometimes labeled “behavior” in the studies we reviewed, implying an objective approach (e.g., Alhidari et al., 2018; Kashif et al., 2015; Konrath et al., 2023; Osili et al., 2011). However, as we have discussed, self-reported past giving is subjective and can be prone to distortion (Bekkers & Wiepking, 2011; Lee & Sargeant, 2011).

The most common approach used was to ask people if (and how much) they have donated in a recent timeframe, generally 12 months. For example, “How high was the total amount of money you have donated last year?” (Boenigk & Mayr, 2016), “In the past 2 years, have you donated money to any environmental organization?” (Greenspan et al., 2012), or “How much did you donate to the nonprofit organization in the last year?” (Dogan et al., 2021). Sometimes, to ensure a greater portion of past gifts are captured (see Bekkers & Wiepking, 2006), this approach has been used to consider not only overall giving but rates of giving to different charity categories or fundraising methods (e.g., Bekkers & Wiepking, 2006; Hager & Hedberg, 2016; James & Sharpe, 2007).

Not all measurement of giving is as granulated, however. Some studies capture a general orientation toward past giving rather than asking about specific donation values. For example, Kashif and colleagues (2015) asked participants to respond to the statement, “Over the past 4 weeks, I did not donate money to charities or community service organizations,” with response options ranging from “not at all true” to “absolutely true.” This more general approach can also be applied to assessing the value of past donations: for example, “When you make a donation to a non-profit organization, how small or large is your typical contribution?,” with response options from “very small” to “very large” (Bullard & Penner, 2017). Others capture the value of past giving in predetermined categories, such as “Approximately how much have you donated, in U.S. dollars, in the past 12 months?”: “less than $100,” “$100 or more but less than $500,” “$500 or more but less than $1,000,” “$1,000 or more but less than $5,000,” and “$5000 or more” (Ki & Oh, 2018).

These more general types of questions introduce additional noise because of the relative crudeness or subjectivity of response options. We instead propose that subjective measures of past giving should use questions about the specific values donated (in the relevant currency). This approach is optimal because response options are continuous, allowing capture of exact values, and can still be easily converted into a binary category to understand donation likelihood: with participants returning $0 donation values being treated as non-donors.

Finally, subjective measures of past giving sometimes captured the relative frequency of donations. For example, Alhidari and colleagues (2018) asked people to report their donation behavior in the previous month with response options ranging from “not at all” to “frequently.” Another option is to ask how many donations have been made (e.g., “How many times have you donated to the nonprofit organization in the last year?”; Dogan et al., 2021).

Other Subjective Measures

Although rarer, subjective measures can sometimes be used to capture charity selection or giving tenure. Charity selection, for example, may be assessed by asking people to directly report the nonprofits they support (e.g., Clerkin et al., 2013; Horne et al., 2005). For example, Chapman and colleagues (2018) asked, “What is the main, or most recent, charity you supported through workplace giving?” Alternatively, charity selection may be assessed by asking people to either choose between two or more charities or charity categories (e.g., “If you were approached by the following two nonprofit organizations after a natural disaster, to which organization would you donate $100?”; Qu & Daniel, 2021), or divide a hypothetical donation between different options (Fleming et al., 2023; Kim & Van Ryzin, 2014). Giving tenure can be captured, for example, by asking how many years they have been donating to the cause, either with a free response format (Barnes, 2011; Kim et al., 2024) or with designated response categories (e.g., only this year, 1–5 years, more than 5 years; Halvorsen et al., 2024).

Objective Measures

Personal Money

Some studies using objective measures analyzed donations of the participants’ personal money, which they had earned independently of the study in question. These studies typically involved archival analyses of transactional database information (Agypt et al., 2012; Fang et al., 2020; Goswami & Urminsky, 2020; Karlan & List, 2020; Shang et al., 2020; Waites et al., 2023), although sometimes used other information sources such as probate records (James & Baker, 2015) or data scraped from crowdfunding websites (Jang & Chu, 2022). Very rarely studies observed people making donations with their own money in person (e.g., Fajardo et al., 2018). The primary advantage of examining people’s donations of their personal money is that it is the most ecologically valid approach. In other words, the measurement closely aligns with the behavior being studied.

Earnings

Another common way to examine objective giving has been to ask people to donate some of what they earned through participating in the study. Study payments vary considerably. Some in person studies pay as much as $10 to $20 (e.g., Chao & Fisher, 2022; Exley, 2020; Helms et al., 2013; Shang et al., 2008), but most online studies pay only a dollar or two (Jin et al., 2021; Kamijo et al., 2020), or even a matter of cents (Chan & Septianto, 2022; Rai et al., 2017; Septianto et al., 2022). Thus, although these studies include objective measures of giving, there are constraints on the amount people can elect to donate. Furthermore, people may behave differently when (a) they are currently working to earn the very money they have been asked to donate and (b) they know that their decisions are being observed as part of the study. In addition, people’s motivations for participating vary across individual participants: some are focused on assisting researchers, whereas others are more motivated by earning potential. Differences in these underlying motivations may also affect donation responses with study earnings.

Bonus or Lottery

Some studies examine consequential giving choices by giving participants an unexpected bonus payment or lottery entrance. In the former, participants can either keep or choose to donate all, or part of, their bonus. In the latter, participants are told they are being entered into a lottery to win a bonus and are asked how much (if any) they will donate of that prize if they win. Bonus payments and lottery payments can be viewed as psychologically similar to one another because they both involve windfall money (i.e., money the participant never expected to have). The benefit of lotteries is that the value in question can be higher. Lottery prizes are generally cash or gift cards worth between $50 and $100 (Becker, 2018; Ugur & Heermans, 2024), although occasionally higher (e.g., Adena et al., 2019). However, the donation decision associated with a lottery is largely hypothetical because it is unlikely that the person will win. Bonus payments are typically very small (e.g., 15c, Chao, 2017; or 25c, Leclercq et al., 2024), meaning donation decisions may not be seen as very consequential; but at least people know the money is theirs.

Recommendations

Our systematic review has uncovered many ways that charitable giving has been measured over the last two decades, identifying a range of subjective and objective measures. We have also summarized these diverse approaches into an inventory that we hope will prove valuable for both new and incumbent scholars in the field. From this historical snapshot we now turn to the future. In this section, we outline five key recommendations for approaching measurement in future research, which we hope will help elevate the scholarship of charitable giving and therefore the value and practicality of our field’s research learnings.

More Objective Measurement of Giving

Only a third of the articles we identified that measured charitable giving over the last two decades had included at least one objective measure of giving. As we have elaborated, charitable giving is a socially desirable behavior that is prone to being overrepresented in self-reported measures (Bekkers & Wiepking, 2011; Lee & Sargeant, 2011) and recent evidence suggests that only a small amount of the variance observed in prosocial behavior can be explained by people’s self-reports of that behavior (Chapman, McKay, et al., 2025). To the extent that a primary objective of scholarship on charitable giving is to understand real-world charitable behavior and provide practical guidance to nonprofits about the approaches and interventions that may help them raise money, this relative lack of objective measurement may therefore give our field pause.

A key finding of the current research is that the rate of objective measure use varies significantly across disciplines, geographic regions, and methods. Nonprofit studies have historically relied on subjective measures (Qu & Mason, 2023), as our data confirm. This could be motivated by financial or logistical barriers or simply convenience, as self-report measures can sometimes be administered faster and at less cost to researchers (Connors et al., 2016). Our data also show that lab experiments are much more likely to include objective measures than survey studies are, even though both typically use questionnaire formats, suggesting feasibility is not the barrier.

We speculate that the current imbalance—with subjective measures being typically favored over objective ones—may at least partially be explained by a combination of disciplinary norms, perceptions that objective measurement is not feasible, and a lack of awareness of how divergent findings can be on objective versus subjective measures. Regarding norms, researchers in some disciplines (i.e., economics) and parts of the world (i.e., Western Europe) are already using objective measures at higher rates, which suggests that different contexts may have different expectations for objective measurement. Regarding feasibility, we have highlighted a broad range of options for incorporating objective measurement into various research designs, many of which do not require significant funding or institutional partnerships and should therefore be feasible for most researchers. Regarding awareness, we hope that this article has drawn attention to the consequences of measurement choice and therefore encourages new scholars to the field to consider their options carefully.

There remains an important place for subjective measurement alongside an increased use of objective measurement. There may be times when subjective measurement is more feasible or may generate more reliable findings. For example, when running early exploratory studies of new concepts or in new contexts, administering pilot surveys with established subjective measures may be a valuable starting point. Furthermore, there are projects that are more interested in understanding subjective outcomes or that wish to compare the relative influence of different constructs or theories and may select to examine their relative impact on subjective measures as a starting point. As we discuss below, we encourage a move toward more objective measurement in the field, wherever possible selecting the approach that is most ecologically valid within the particular constraints of the project.

Improving Ecological Validity in Giving Research

There are various ways that charitable giving can be measured objectively. In this article, we have distinguished between (a) the participant donating their personal money, which is not connected with the research study, (b) the participant donating some of the money they have earned by taking part in the study, and (c) the participant donating some of either a bonus payment they did not expect to receive or potential lottery winnings that they have low odds of receiving. We propose that these three approaches vary meaningfully in terms of their ecological validity, or how representative they are of real-world charitable giving. Scholars are encouraged to select the most ecologically valid measure that is feasible given their research objectives and circumstances.

The best way to measure charitable giving is to capture data on people’s donation choices when they do not know that their behavior is being observed, and when they are making donations with their personal money. Studies that use such objective measures are providing insight into real giving behavior. Consequently, we can be most confident that the conclusions drawn from these studies will translate into the real world. A range of methods have employed measures of people donating their personal money, including archival studies analyzing transactional or web scraped data, surveys matched to database information, and field experiments.

Considering people’s actual charitable giving, independent of the study, design, or demand characteristics, could perhaps be considered the gold standard of objective measurement. There can nevertheless also be disadvantages. In those studies that focus mostly on aggregate behavior (e.g., Chapman, Louis, Masser, Hornsey, et al., 2022), there are limits to prediction as only observed behavior is analyzed and no information is provided by participants. Therefore, factors like donor attributes, motivations, and underlying psychology generally cannot be considered. These studies still add important insights to the overarching body of knowledge about charitable giving by testing whether predicted patterns of behavior play out in the real world (see also Chapman et al., 2024). Even better, however, are studies that have paired transactional data capturing participants’ donations of their personal money with survey data from the same participant, to gain a richer understanding of the underlying mechanisms promoting giving behavior in the real world (e.g., Croson et al., 2009; Sargeant et al., 2006). We recommend more studies of this latter type in the future.

A benefit of using objective measures to capture people giving their personal money is that these are often included when scholars collaborate with industry partners. Partnerships with industry not only enhance the ecological validity of our research, they also substantially increase the odds that our learnings will be used by practitioners. More philanthropy research being conducted with and for nonprofits will only benefit our field. Nevertheless, we acknowledge that forming industry partnerships for research may be out of reach for some PhD students, junior scholars, and researchers in some developing research environments.

In our view, if it is not possible to study people’s giving independent of the study, then the next best option is to give them an opportunity to donate some of their earnings from participating in the study and observe what they do. Because the participants have earned this money themselves, and were not expecting to give it away, they are more likely to make decisions that reflect their real-world charitable behavior. However, participation payments are typically quite small, meaning the donation value range will be artificially restricted. Also, when this approach is employed, participants will be aware that their donation behavior is being observed and this may change their honest response, in line with the social desirability bias discussed above. Nevertheless, offering people the chance to donate their earnings is a simple and relatively cost-effective approach to measuring charitable giving objectively, and one that does not rely on the researchers having professional networks in industry or large research budgets.

Finally, although bonuses and lotteries are perhaps not the ideal ways to examine real-world charitable giving, they offer improved ecological validity over purely subjective measures. There is evidence that people donate more with windfall money than with money they have earned (Carlsson et al., 2013; Li et al., 2019). Learnings from studies using windfall methods like bonuses and lotteries may therefore not translate perfectly to understanding real-world charitable behavior. Bonuses at least represent real money that, although unexpected, the participant can now possess. In this way, decisions made with bonus payments are still consequential. A limitation, however, is that bonus payments are typically very small. With lotteries, although the participant is deciding about a donation that may translate into actual differences of money in their pocket, the odds of winning the lottery are generally low and participants know that. On one hand, this may lead some people to over-represent their giving, as they know the money is unlikely to eventuate anyhow. On the other hand, some people may under-represent their giving, as the ambiguity of the situation provides them with an excuse to be less generous (Garcia et al., 2020; Mesa-Vázquez et al., 2021). Lottery measures are therefore lower in ecological validity than the other objective measures discussed above. For future research, we recommend scholars select more ecologically valid objective measures (i.e., donations of study earnings or personal money) over bonuses and lotteries when possible. However, when resource constraints mean that lotteries or bonuses are the only financially viable approach, we encourage this kind of objective measurement as an improvement over purely subjective measurement.

Where Possible, Use Both Objective and Subjective Measures

Our review identified various approaches to measuring charitable giving, each subject to different sources of bias and limitation. Subjective measures like donation intentions or willingness may be particularly vulnerable to social desirability bias, whereas self-reported past giving may be prone to distortions based on poor memory or recall: participants may find it easier to remember particularly large or meaningful donations and may forget smaller contributions (Tourangeau et al., 2000). Even objective measures are not without limitations. Research has shown, for example, that economic games and observed donations in laboratory settings may suffer from demand characteristics, where participants’ awareness of being observed alters their behavior (Levitt & List, 2007). Understanding and recognizing the influence of different biases is therefore an important endeavor for philanthropy scholars, and one that requires comparative research.

Only 6% of the corpus of articles published over the last 20 years reported both a subjective and an objective measure of charitable giving. This further complicates the confidence we can have in the overarching body of knowledge. With relatively few studies that allow direct comparisons of predictors of subjective and objective giving, it remains hard to conclude whether the dominant subjective measures are appropriate proxies for actual charitable behavior. We therefore recommend that, whenever feasible, researchers should include both subjective and objective measures and directly compare their relationship with one another and evaluate the underlying drivers of each.

When Using Subjective Measures, Be Consistent and Precise

Significant variability was found in the way charitable giving has been measured, even when ostensibly tapping the same construct. There were almost as many ways to measure giving intentions, for example, as there were studies including an intention measure. We recommend consistency, with validated scales and items that are demonstrated to be robust and appropriate for capturing charitable giving. The inventory of measures we include here may serve as a starting point for thinking about measurement options. However, significant development and refinement will be needed in the future to consolidate measurement practices in the field.

Conceptual clarity could also be improved. We found instances, for example, of self-reports of past giving being labeled with phrases like “actual behavior” or “donation behavior” (e.g., Alhidari et al., 2018; Kashif et al., 2015; Konrath et al., 2023; Osili et al., 2011) and of people’s willingness to give being labeled as “donation intentions” (e.g., Cho et al., 2019; Harrison et al., 2022; Kim, 2014; Li & Feng, 2021). Some studies also provided construct labels but no information about how the construct was actually measured (e.g., Chang, 2005; Jones et al., 2019; Lee et al., 2017; Peterson et al., 2018). As researchers and scientists, we collectively understand the importance of precision, yet conceptual slippage is still present in some of our research articles. Following existing best practices for research, we recommend that scholars be vigilant when labeling constructs in their own research to ensure that conceptual labels align with operationalization. Researchers are also encouraged to explicitly discuss why they selected the measure based on their specific research question, theoretical approach, or even pragmatic considerations.

Consider a Two-Step Approach to Understanding Giving

Throughout this article we have discussed how there are two broad orientations in the way that charitable giving can be considered: donation likelihood and donation value. Previous research has shown that the psychological antecedents of donation likelihood and value may vary (Chapman et al., 2021; Chapman, Spence, et al., 2025), suggesting that measures of likelihood and value are not interchangeable.

In the real world, donation values may be constrained by a range of practical factors. How much one gives may depend, for example, on the person’s disposable income, other financial commitments, and how much they are asked to give. Someone with limited means could make a very small donation but not a very large one: therefore, the relationship between psychological antecedents and giving at all should contain less external noise than the relationship between those antecedents and giving value.

Explicit consideration of when and why to measure donation likelihood versus value was largely absent in the articles we considered. Sometimes one was used, sometimes the other, and sometimes both, with little explicit discussion of how donation likelihood and value may be psychologically and practically different constructs. There was also divergence in whether consideration of donation value was contingent on a gift being made at all or not: in some studies $0 values were included (e.g., Heiser, 2006; Yang & Hsee, 2022) and in others only values greater than $0 were included when predicting donation value (e.g., James, 2009; Shaker et al., 2016).

One recommended approach is called the double-hurdle method (see, for example, James, 2009; Shaker et al., 2016). Following this approach, donation likelihood is modeled first to understand the probability of any donation being made. Next, conditional donation value is modeled to understand what promotes heightened generosity among people who do choose to give. Whether using subjective or objective measurement, we believe the double-hurdle approach should be systematically employed to effectively build up a body of knowledge about the relative drivers of giving at all (i.e., donation likelihood) and relative generosity (i.e., donation value). To this end, we recommend that scholars include measures capturing both likelihood and value in future research.

Strengths, Limitations, and Future Directions

We employ a systematic review method, which introduces transparency and replicability to the review, and helps to minimize subjectivity by including all articles that meet the specific, preregistered requirements. This approach allows us to identify a large corpus of research on charitable giving published across disciplines, countries, and years, and therefore to provide an empirical basis for our conclusions and recommendations.

Our research is limited to the published corpus and information that previous scholars have included in their articles. While we identify a broad array of measurement approaches, which vary systematically across disciplines, geographies, and research methods, we cannot speak to the reasons that these patterns are observed. Future research may wish to survey scholars to explore how disciplinary norms, institutional contexts, or practical constraints shape measurement decisions. Another opportunity for future scholarship would be to explore the relative efficacy of measures for different populations. Dictator games, for example, have been used with success for research involving children (Harbaugh & Krause, 2000; Ugur, 2021).

More broadly, scholars may wish study topics related to the five propositions we have outlined. In particular, future work is needed to identify and validate consistent measurement approaches, potentially building on the inventory of options provided in this article to support greater consistency and conceptual precision in measurement practices. Finally, our article focuses on how charitable giving is measured. Other study design decisions beyond the selection of measures can affect giving decisions, including the method employed, whether an experimenter is present, if the flow of the study introduces demand effects, and if there are flaws and biases in the design of the interventions being tested. Although beyond the scope of the current project, we encourage scholars to systematically consider other methodological factors relevant to philanthropy research.

Conclusion

In this article, we review 437 research articles that measured charitable giving and have been published over a period of two decades. Overall, we find much higher rates of subjective than objective measurement, although this varied across disciplines, geographic locations, and the research methods employed. Self-reports about charitable giving are prone to distortion because giving is widely considered to be a socially desirable behavior. For that reason, we make five recommendations for how, as a field, we can collectively improve our measurement practices. First, introduce more objective measurement. Second, select the most ecologically valid measure that is feasible and appropriate. Third, include and compare subjective and objective giving measures within the same study. Fourth, improve consistency and precision in how charitable giving is measured and reported. Fifth, consider a two-step approach to understanding both donation likelihood and value, in turn. By summarizing the existing state of the field, and making recommendations for future research, we hope this article will be of value to both established and emerging philanthropy scholars and serve as a resource to orient our field toward the future.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Cassandra Chapman is the recipient of an Australian Research Council Discovery Early Career Researcher Award (project number DE220100903) funded by the Australian Government.