Abstract

This article takes a comparative qualitative approach to explore the intertwined external accountability and legitimacy attempts of independently wealthy philanthropists. By comparing accountability forums and institutional logics stated by philanthropists, it is investigated to whom they are externally accountable and how they legitimate their controversial funding of public goods. The study compares the external accountability and legitimacy attempts of philanthropists with that of public agencies, corporations, and fundraising-dependent nonprofits. Empirically, this is a cross-sectional study of funders supporting human embryonic stem cell research in either California or Sweden. The study shows that it is through local isomorphism, rather than any specific accountability forum or institutional logic, that philanthropists are accountable and thus legitimate their giving. This is in contrast to other types of funders, which are more similar within each form when comparing accountability forums across societies, and more similar within societies in their usage of institutional logics, with certain patterned statements. In addition, philanthropists in both societies are more detached than any other type of funder as regards both specific patient populations and the general electorate. This finding raises questions on what philanthropists’ private funding for public purposes actually entails.

Keywords

Introduction

Philanthropy is often described as an obligation to take from one’s abundant private funds and contribute to the public sphere, such as in Carnegie’s (1901) wealth essay or in the more recent Giving Pledge (Buffett, 2011). Yet the use of private wealth for public purposes may be criticized, as it entails essentially unchecked private entities being allowed to dictate the organization of the public sphere (Arnove, 1984; Roelofs, 2003). This stipulation poses challenges to some of the fundamental notions of a liberal democracy (Ostrander, 2007; Prewitt, 2006; Reich, 2016). Already the creators of the first major philanthropic foundations understood that to ensure long-term survival, philanthropists needed to gain legitimacy both by legislators and in the public eye (Hall, 2006; Karl & Katz, 1981; Nielsen, 2001). As an important building block in that strive for legitimacy, accountability has been put forth as a means to stifle debates questioning philanthropists’ activities and threatening their existence (Hammack & Anheier, 2013). As Heydemann and Toepler (2006) write, “accountability has in many respects become the dominant language through which concerns about the legitimacy of foundation practices is expressed” (p. 5).

A central path toward legitimacy has thus been various attempts to demonstrate accountability to external stakeholders (Frumkin, 2006a; Nielsen, 2001). When surveying the broader field of social science, accountability is often stated as a basis for legitimacy (Black, 2008; Kersbergen & Waarden, 2004). However, we know very little about the relationship between philanthropists’ external accountability relationships and their legitimacy attempts. Although Frumkin (2006b) writes, “At the core of the angst within philanthropy are three complex and intertwined issues that have long confronted donors of all kinds: effectiveness, accountability, and legitimacy” (p. 55), little empirical work has been conducted to learn more about these complex interactions. While effectiveness of philanthropy is beyond the scope of this article, I will here attempt to empirically explore the two other intertwined issues—accountability and legitimacy. Philanthropists are here defined as those practicing “private giving for public purposes” (Ostrower, 1997, p. 4), with a focus on elite donors who define themselves as independently wealthy.

Previous research on the accountability and legitimacy of philanthropists is inconclusive, showing both that philanthropists are essentially free to act as they please, that is, unchecked by accountability forums, and that they adhere to different forms of accountability, potentially based on their need to garner legitimacy. On one hand, philanthropists are thus portrayed as barely externally accountable at all given the freedom derived from their wealth (Fleishman, 2009; Frumkin, 2006b; Jung & Harrow, 2015). Philanthropists demonstrate a meager amount of external accountability mainly pertaining to simple legislative adherence (Cordery & Sim, 2018; McIlnay, 1995; Williamson et al., 2017), despite its potential relevance in rendering legitimacy (Prewitt, 2006).

On the other hand, philanthropists are described as drawing on specific institutional norms to account for and legitimize their actions. Philanthropists are here portrayed as equally externally accountable as other funders, as they are dependent on being perceived as legitimate by a broad set of constituents as regards their funding of public goods (Tomei, 2013). These institutionalized norms may be locally contingent, and there may exist local specificities in nonprofit self-regulation, especially on a national basis (Bies, 2010; Marquis & Battilana, 2009).

Previous research has also shown that the comparative contextualization of philanthropists is important when exploring their accountability (Cordery & Sim, 2018). For example, in the United States, studies emphasize how philanthropic foundations strive to demonstrate independence to be legitimate (Ostrander, 2007; Quinn et al., 2014; Whitman, 2009). Others indicate that rather than independence, a more conservative alignment with elite institutions takes precedence as foundations strive for legitimacy (Aksartova, 2003; Eisenberg, 2007). These somewhat contradictory ways to demonstrate legitimacy—independence versus alignment with elite institutions—combined with the potentially local variation in accountability relationships—indicate that the role of accountability in the legitimacy of philanthropists is far from self-evident and needs to be empirically examined and theorized.

Given this background, the aim of this article is to comparatively explore the relationship between the external accountability and legitimacy attempts of philanthropists. This will be done by comparing independently wealthy philanthropists with three other types of funders—corporations, public agencies, and fundraising-dependent nonprofits, in one funding area, and across two types of welfare regimes. I find that external accountability is rather bound to organizational form, being more similar across the two societies, whereas legitimacy attempts are more societally determined. However, philanthropists stand out in the comparison, being more isomorphic within their society and more diverse across societies, both as regards prevalence of accountability forums and type of legitimacy attempts.

Theoretical Operationalization

To operationalize the aim of the article, I leaned on two well-established theoretical models to code and analyze external accountability forums and legitimacy attempts.

External accountability is operationalized by using Bovens’s (2007) model of public accountability, stemming from the public administration literature. Accountability is here defined as “a relationship between an actor and a forum, in which the actor has an obligation to explain and to justify his or her conduct, the forum can pose questions and pass judgement, and the actor may face consequences” (Bovens, 2007, p. 450). This model is an appropriate choice as Bovens addresses different fora of external public accountability, rather than focusing on internal accountability as in many nonprofit studies (cf. Ebrahim, 2003; Kearns, 1994; Najam, 1996). Bovens (2007) lists five types of external forums that may be of relevance. Given the proliferation of new public management (Hood, 1991; Pollitt & Bouckaert, 2004) in the production of public goods, I have added a sixth category of market accountability to Bovens’s taxonomy, breaking it out of the very broad category “other stakeholders” in his concept of social accountability. The types of accountability forums are thus the following:

Political accountability—directed toward elected representatives, political parties, voters, and the media

Legal accountability—directed toward the courts and legislated auditing functions of various other public agencies

Administrative accountability—directed toward auditors, inspectors, and controllers, here defined as pertaining to private auditing actors such as, for example, standard setters

Professional accountability—directed toward professional norms, standards, and peers

Social accountability—directed toward interest groups, charities, and other stakeholders

Market accountability—those “other stakeholders” who as beneficiaries of public goods are cast as clients in the age of new public management (Hood, 1991; Pollitt & Bouckaert, 2000) with the option to exercise the exit/voice strategy (see Meijer, 2004, cited in Bovens, 2007, as well as Hirschman, 1970)

To operationalize legitimacy attempts, I turn to the neo-institutional literature in organization studies (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). In comparison with the specific relationships in focus when studying accountability forums, legitimacy relates to more subtle adherence to social norms and values, legitimizing the actions of philanthropists, especially in contentious situations. Legitimacy may be defined as “a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions” (Suchman, 1995, p. 574). Such legitimacy may be operationalized as institutional logics, guiding actors as they account for their actions (Friedland & Alford, 1991; Thornton et al., 2012). In addition, such institutional pressures may also vary across different geographical locations (Bies, 2010; Marquis & Battilana, 2009).

Institutional logics may be defined as “both supraorganizational patterns of activity through which humans conduct their material life in time and space, and symbolic systems through which they categorize that activity and infuse it with meaning” (Friedland & Alford, 1991, p. 232). The originally conceptualized logics were the capitalist market, the bureaucratic state, democracy, family, and religion. As has been shown by recent research, different logics may be drawn on to externally account for various types of potentially contentious actions (McPherson & Sauder, 2013). Friedland and Alfords’s (1991) logics system was eventually developed and elaborated on by Thornton et al. (2012), who added two pertinent categories, the logics of professions and of community. In combining the two logics systems, I get a robust taxonomy of seven institutional logics for classifying and interpreting legitimacy attempts:

Logic of the capitalist market—relating to profit and economic growth

Logic of the bureaucratic state—relating to organizational standards as well as regulation

Logic of democracy—relating to democratic norms and practices

Logic of family—relating to the personal sphere

Logic of religion—relating to theological convictions

Logic of professions—relating to professional norms and standards

Logic of community—relating to the well-being and shared responsibility of a specific community

In sum, by combining Bovens (2007), Friedland and Alford (1991), and Thornton et al. (2012), I have a taxonomy of external accountability forums and institutional logics guiding legitimacy attempts, that may be used as a basis to interpret the relationship between philanthropists’ external accountability and legitimacy. Given this taxonomy, my research question is as follows:

Comparing philanthropists with other funders and across societies, to which forums do philanthropists experience accountability, and which institutional logics do they draw on to legitimize their funding of public goods?

Research Context and Design

To study the relationship between philanthropists’ external accountability and their legitimacy attempts, I selected a comparative case study design (Eisenhardt, 1989; Yin, 2003). For comparative purposes, it was important to select an empirical field where not only philanthropists but also other types of organizational forms were engaged in funding public goods in different societies at the same point in time. In addition, I wanted to find an area in which funding of the public good was contested, allowing me to draw out legitimacy attempts. Human embryonic stem cell (hESC) research funding is such a public good, and it is also a contested topic, making it more likely that all research funders involved will be able to elucidate their funding decisions. By combining two ideal-type classifications based on nonprofit status and manner of resource provision (Blau & Scott, 1962; Wamsley & Zald, 1973), I selected four categories as the study’s comparative basis: (a) independently wealthy philanthropist (PHIL), (b) fundraising-dependent nonprofit (NP), (c) public agency (PA), and (d) corporation (C).

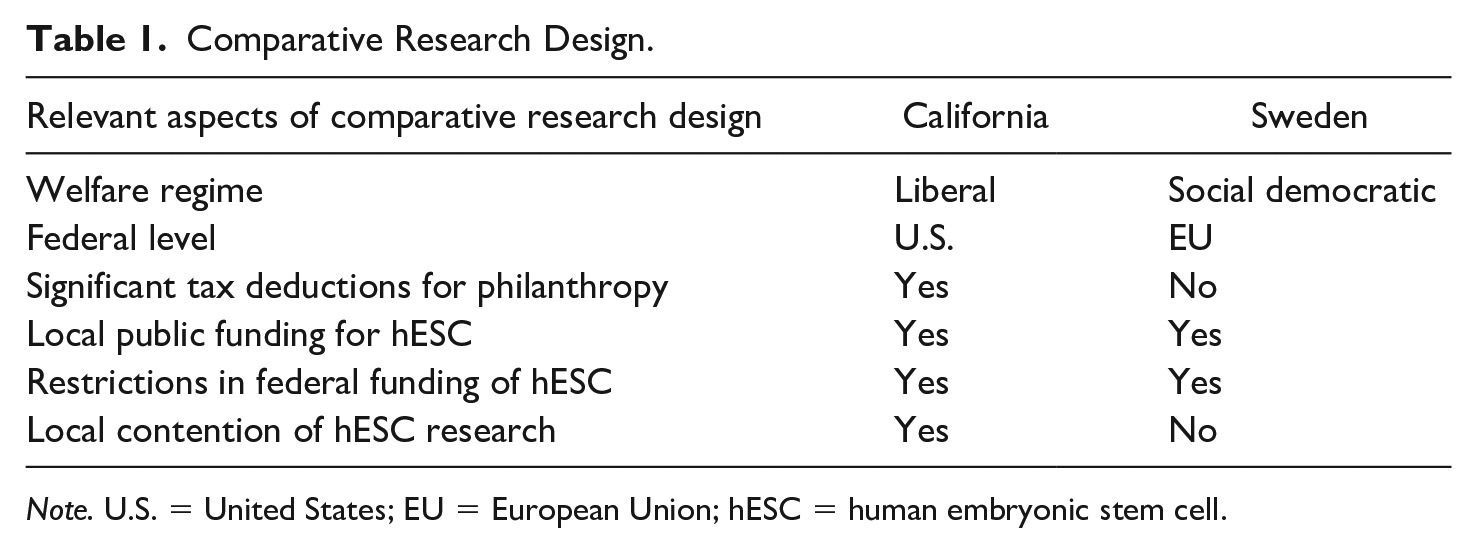

For the societal comparison, I sampled California and Sweden using Esping-Andersen’s (1990) welfare-regime classification, building on previous nonprofit sector research (Salamon & Anheier, 1998). The welfare-regime model is based on the idea that the way social policy, and by extension public utilities such as research funding, is organized varies systematically across different welfare regimes (Esping-Andersen, 1990). California is classified as a liberal welfare regime, and Sweden as social democratic. In California, philanthropic foundations as well as individual donations are primarily regulated by tax law, and there are significant possibilities for tax deduction through philanthropic engagement (Brody, 2006), thus distributing public funds through private allocation. The practice of philanthropy in California has been described as an expression of democratic engagement (Prewitt, 2006).

In California, hESC research policy can be traced back to historical controversies related to abortion and research on human embryos (Gottweis, 2010). In 2001, George W. Bush put a halt to most federal hESC research funding (Korobkin & Munzer, 2007). Private funders, many of them philanthropists, stepped in to enable the research. However, the legislation was subsequently counteracted on a state level (Karmali et al., 2010), most importantly by the Proposition 71 vote in California in 2004, resulting in state bonds of US$3 billion to be spent on hESC (Hayden, 2008). When Barack Obama was elected, the previous federal ban on hESC research was partially lifted, but legal contestations of the research in the courts continued (Levine, 2011) at the time when this study was conducted.

In Sweden, at the time of the study, only very small individual donations were tax deductible (the cap was approximately US$200), and this deduction was eventually abandoned altogether (Vamstad, 2018). However, there are a few large philanthropic foundations in the country, primarily focused on research funding and often controlled by wealthy families, sometimes as a way of circumventing corporate taxes and retaining family control over corporations (Turunen & Weinryb, 2018). In Sweden, philanthropic engagement has traditionally primarily concerned research funding, essentially complementing, and largely coordinating the funding work with public research funders (Wijkström & Einarsson, 2004).

In terms of hESC research, Sweden has experienced virtually no controversies (Bjuresten & Hovatta, 2003). Free abortion has not been a contentious issue in Sweden in the same way as in the United States (Linders, 2004), and hESC research is considered on a par with other types of biomedical research (Svensk författningssamling, 2003:460). Being part of the European Union (EU), however, Swedish researchers have had to face restrictions in public funding on a federal level, as pro-life activists and the fear of eugenics have influenced EU funding policy (Salter, 2005).

Table 1 summarizes the relevant aspects of the comparative research design.

Comparative Research Design.

Note. U.S. = United States; EU = European Union; hESC = human embryonic stem cell.

Data and Method

The population of the study consists of funders who have funded hESC research in California and Sweden. To create my sample, in late 2011 to early 2012, I listed all donors thanked in peer-reviewed articles published by hESC research groups in California and Sweden. Using PubMed, I subsequently coded all hESC research publications coming out of the two societies. After finding 93 articles in California and 37 in Sweden, I had a list of 109 funders in California, and 62 in Sweden. By searching news articles and funder homepages, I selected the hESC research funders in each society that had in some way been vocal about their funding of this type of research, and thus somehow made attempts to legitimize this research funding. In each society, I double-checked the relevance of my final sample of funders with a leading local stem cell researcher.

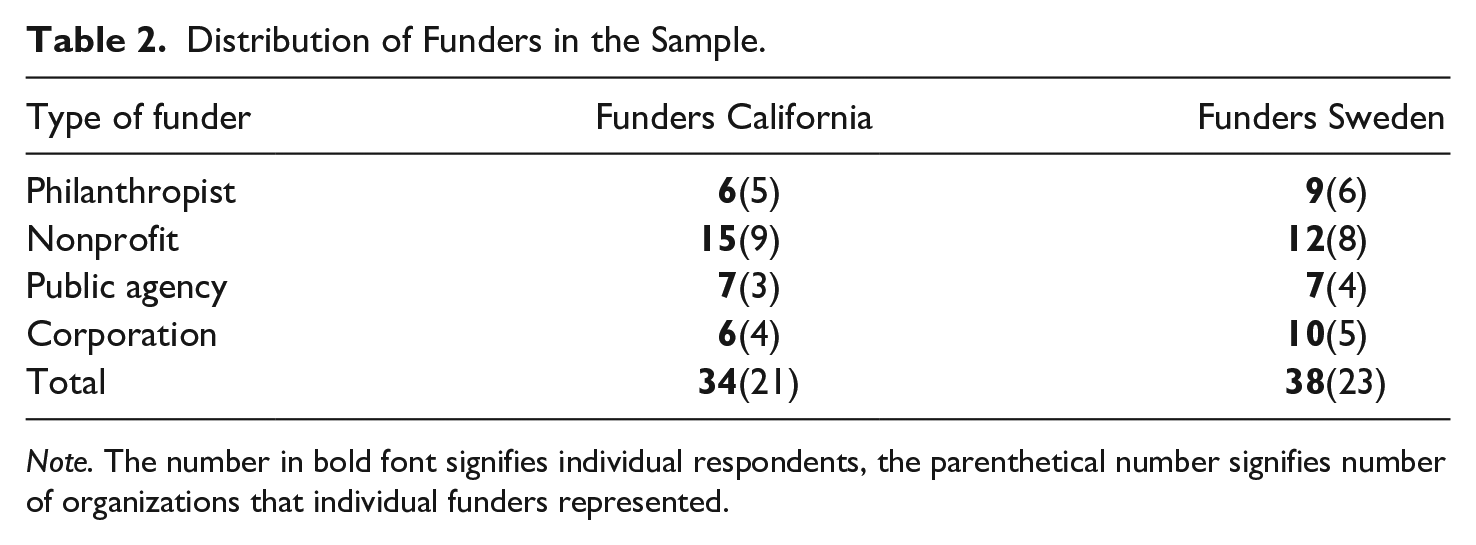

Funders were sampled based on their funding of research in the two societies, although their locations were sometimes outside Sweden and California. However, all Swedish philanthropists were based in Sweden, and all Californian philanthropists were based in the United States. In the end, the study comprised 72 interviews covering 44 funding organizations in California and Sweden. Table 2 shows the distribution of the funders in the sample.

Distribution of Funders in the Sample.

Note. The number in bold font signifies individual respondents, the parenthetical number signifies number of organizations that individual funders represented.

To learn about the external accountability and legitimacy attempts of philanthropists, it is appropriate to explore how they justify their “views to others” (Tetlock, 1983, p. 74). I therefore used semi-structured qualitative interviews to gather information on each funder in each society. The Swedish interviews were conducted between October 2011 and January 2012, and the Californian interviews were conducted between January and May 2012. All interviews were transcribed verbatim. When scheduling the interviews, I explicitly requested to talk to persons in the highest possible managerial positions who felt they could represent the funder and who were also knowledgeable about the relevant research funding practices. Five interviews in Sweden and nine in California were conducted on the phone, one interview in California was conducted in writing, and the rest of the interviews were conducted in person.

In each interview, I probed into two central themes: (a) to whom the funder experienced accountability and (b) why the funder had chosen to fund hESC research. To substantiate the first theme, respondents were provided with a simplified version of Bovens’s (2007) definition of accountability. As regards the second theme, I as a researcher became the “other” to whom they legitimated their conduct. I coded the first theme as external accountability to a specific forum, and the second theme as legitimacy attempts in the form of institutional logics. Given my systematic comparative approach, I did not work in a strictly grounded inductive manner. Following similar empirical papers examining accountability in the nonprofit sphere (Bies, 2010; Williamson et al., 2017), I coded the data through a combination of inductive and deductive approaches (Fereday & Muir-Cochrane, 2006; Saldaña, 2012). This resulted in a pattern matching, as described by Reay and Jones (2016) when discussing the coding of institutional logics. All coding was first done per each individual respondent, and then aggregated for each organizational funder, in case of multiple respondents representing the same funder.

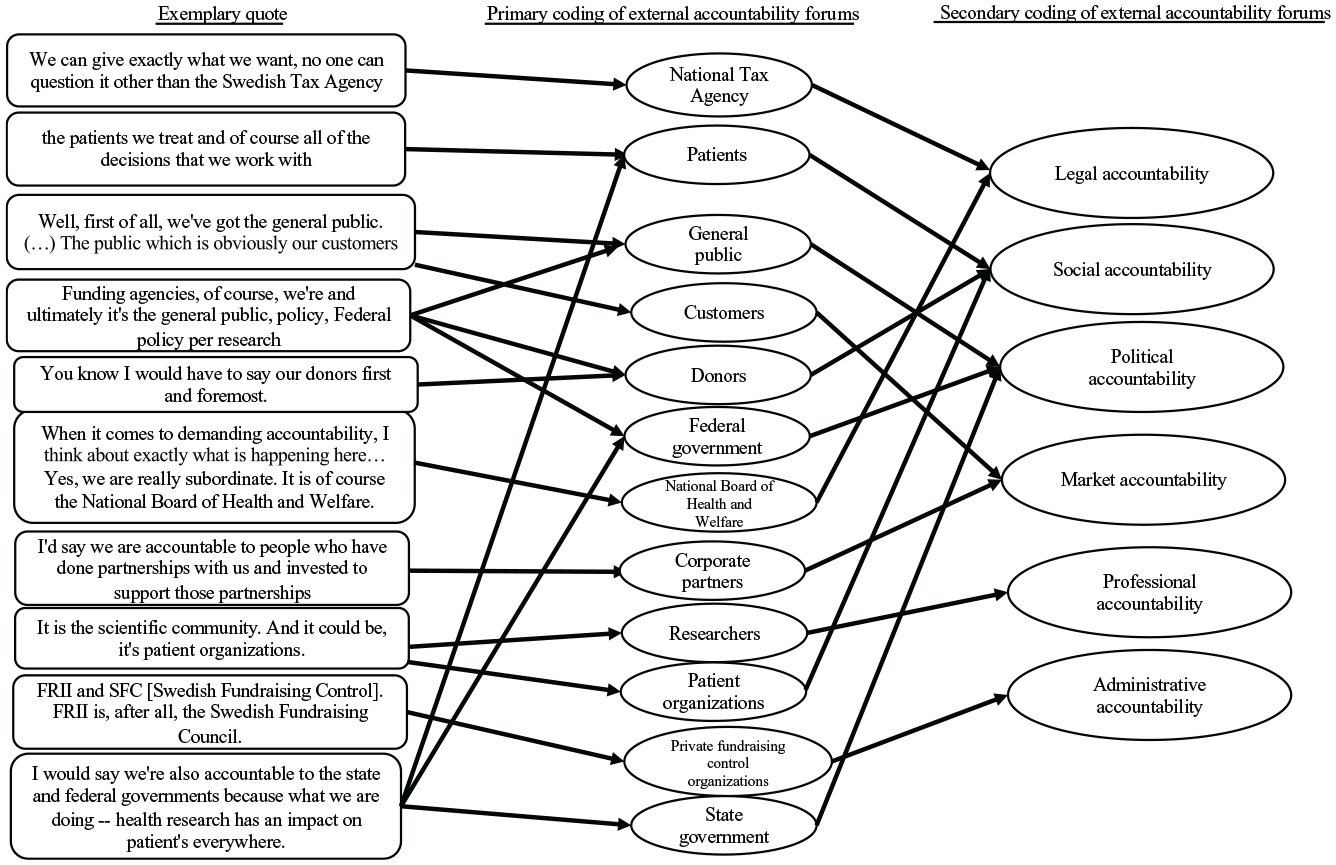

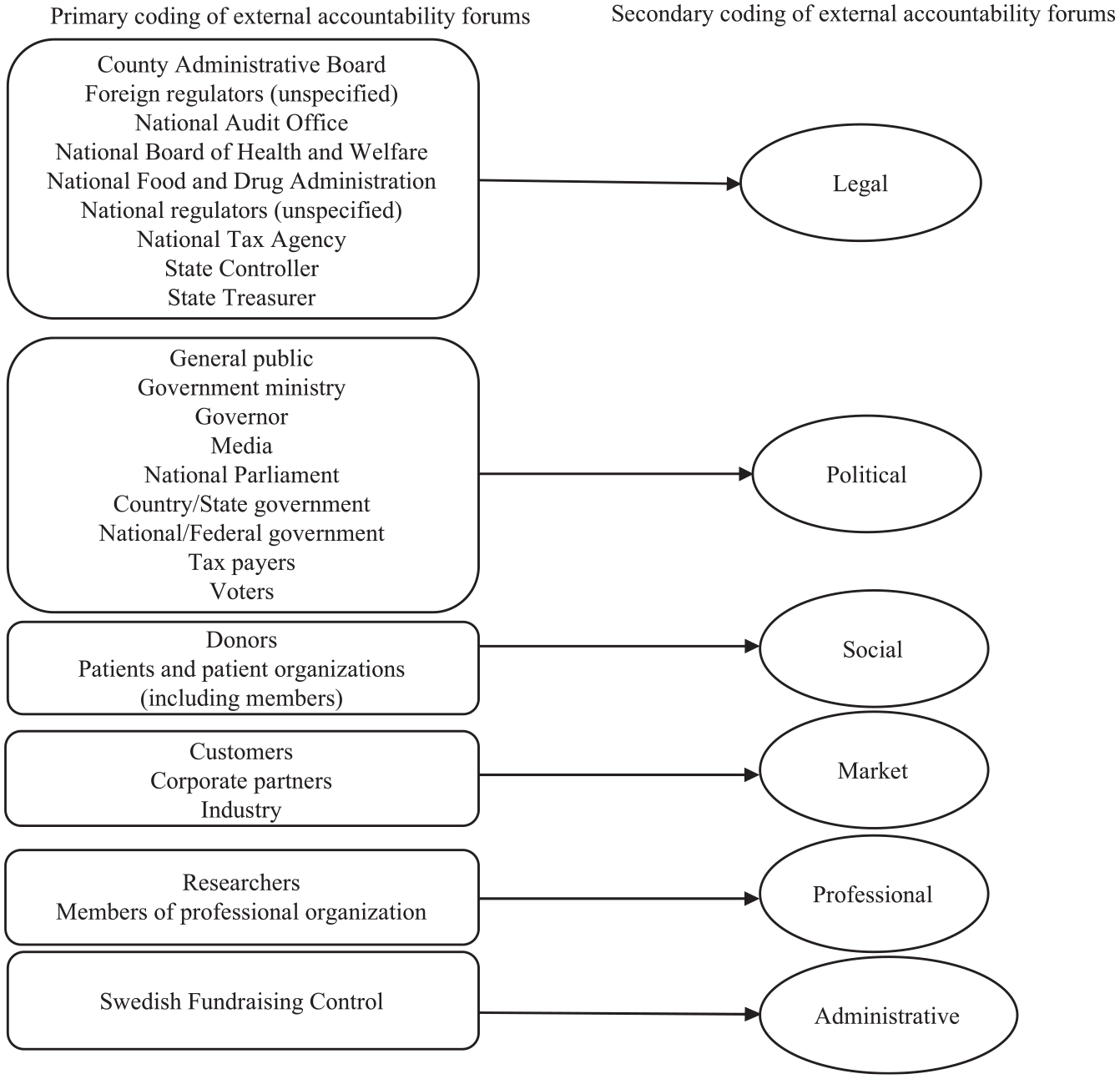

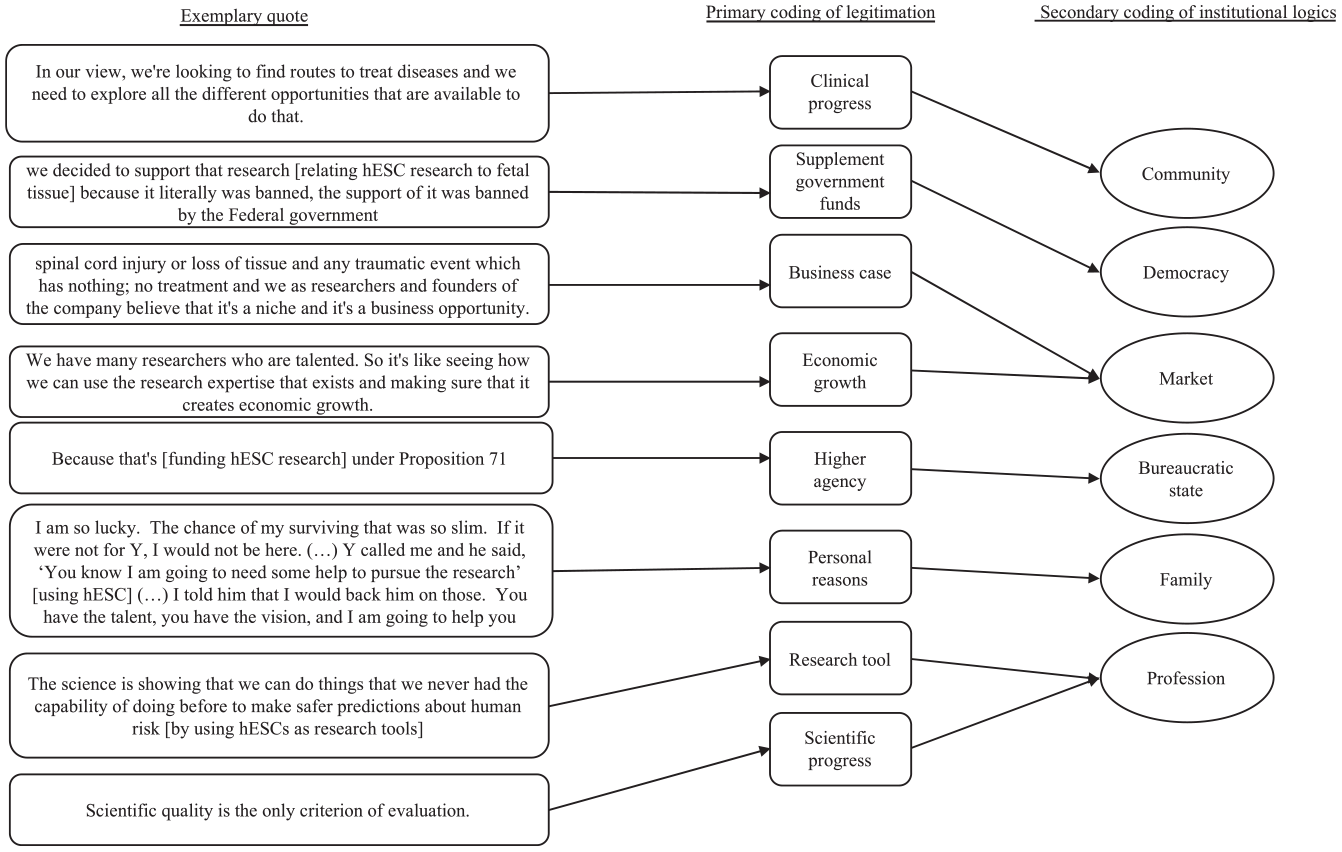

The first theme elicited rather direct lists of accountability forums emerging inductively from the data, as can be seen in the exemplary quotes in Figure 1. As a second-order coding, I then matched the stated accountability forums onto Bovens’s (2007) typology, as can be seen in Figures 1 and 2. When coding legitimacy attempts, I proceeded along the same route. As a first-order coding, I inductively coded patterns emerging from the data, and matching these categories onto the institutional logics’ typology. This coding process can be seen in Figure 3. The second theme elicited a more complex set of responses than the accountability forums. This is in line with the institutional idea of norm adherence often being demonstrated in rather subtle ways, in comparison with the more direct notion of an accountability relationship to a specific forum. I therefore include quotes of institutional logics in the empirical section of the article, and only show exemplary coding quotes for the accountability forums in Figure 1. As in all qualitative analysis, the entirety of the interview informed the coding process. For example, funders’ description of supplementing federal funds was discerned in numerous places in the interviews, as was the focus on patients. Whereas political motivations often explicitly overrode other possible lines of interpretation, the patient focus was more subtle, as clinical applications in and of themselves of course also have commercial implications, especially for corporations. In each individual case, the predominant reasoning of the interviewees determined the interpretation of ambiguous quotes.

Coding of external accountability forums—from quote to forum.

Overview of coding of external accountability forums—primary and secondary coding.

Coding of institutional logics—from quote to logic.

After I had done the second-order coding of both themes, I used pivot tables to tabulate coded data and facilitate a search for patterns (Eisenhardt, 1989; Silverman, 2015). Figures 4 to 7 in the empirical section show graphs of these cross-tabulations on the frequency of external accountability forums and institutional logics mentioned per type of funder in each society. As my research approach was qualitative in its nature, the purpose of these pivot analyses was to get a comparative overview of the themes, rather than analyze exact numbers. These comparisons were thus corroborated and analyzed with the help of the full interview transcripts.

External accountability forums—California.

External accountability forums—Sweden.

Institutional logics—California.

Institutional logics—Sweden.

The study was conducted in accordance with the research ethics legislation in Sweden, and its scope and content were examined and approved by the appropriate collegial bodies at Uppsala University where the research was conducted. All respondents were informed about the scope and purpose of the study, and consented to their participation. Respondents were also able to review interview transcripts and confirm their informed consent.

Empirical Analysis

External Accountability Forums

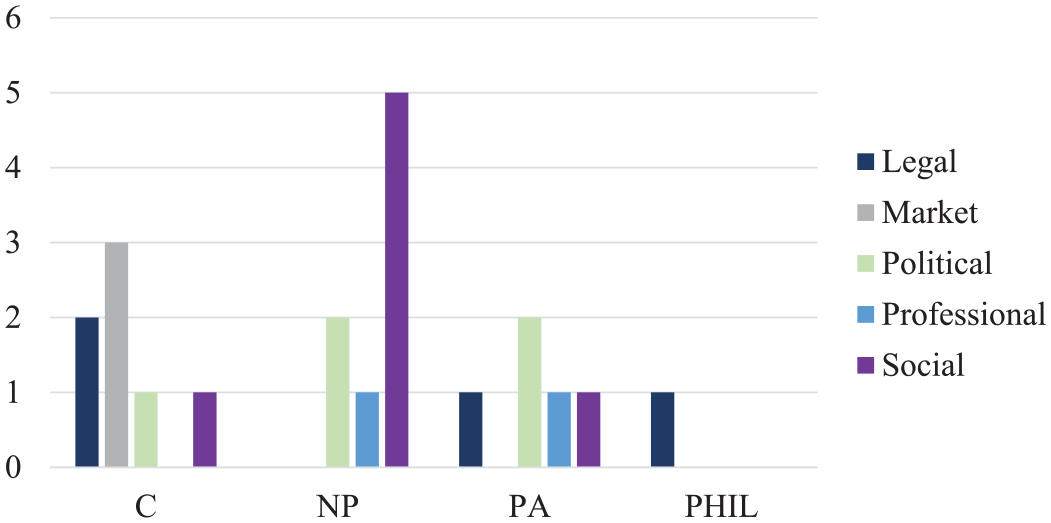

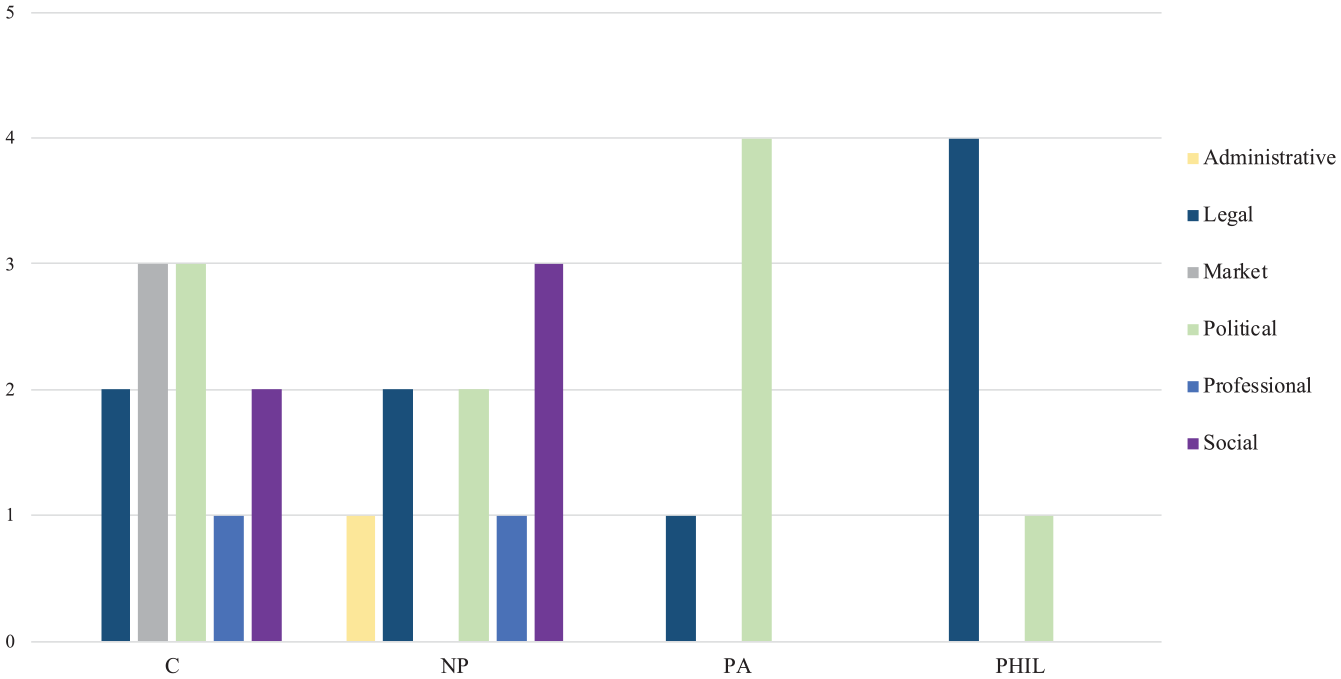

Figures 4 and 5 summarize the type of accountability forums stated per type of funder in California and Sweden. In all figures in the article, C signifies corporation, NP fundraising-dependent nonprofit, PA public agency, and PHIL independently wealthy philanthropist.

Among corporations, quite intuitively, market accountability was prevalent in both societies. For corporations, also legal accountability was important in both societies, which is not surprising as they were assessed and aspired to work on an international market, where demonstrated legal accountability is a baseline for engagement. In both societies, corporations also mentioned political and social (to patients) accountability forums. Yet in Sweden, there seemed to be more attention paid among corporations to political and social accountability than in California. This difference potentially reflected Californian corporations prioritizing legal adherence (legal accountability) to fend off contention, rather than focusing primarily on patients and the general public. In Sweden, also professional accountability (within the realm of medical research) was mentioned by one corporation.

Among fundraising-dependent nonprofits in California, political, professional, and social forms of accountability were mentioned. Yet among these types of accountability, it was clear that in California, the category of social accountability was most prevalent, putting the patients center-stage in their role as targeted beneficiaries of hESC research. This social accountability was not surprising, given that the long-term financial stability of the nonprofit organizations hinged on their ultimate relevance to patients benefiting from hESC research to elicit donations for the nonprofits’ work. In both societies, professional accountability was quite rare among fundraising-dependent nonprofits, being relevant only for one nonprofit in each society, both being professional medical associations. In Sweden, the same categories of accountability forums as in California were mentioned by the fundraising-dependent nonprofits, with the same focus on social accountability. Yet, in Sweden, there was also a focus on legal and administrative accountability, the latter in relation to a private third-sector auditing body. In contrast to Sweden, nonprofits in California mentioned only other forms of accountability (social/political/professional) perhaps related to the contentious nature of the hESC research, prioritizing to signal its relevance for patients, professionals, and the general public. This differed from Sweden, where the third sector in itself may be more controversial given the social democratic nature of the society, rather than hESC research, making it more relevant to also demonstrate legal adherence.

As regards the external accountability of public agencies, a broader variety of categories were mentioned in California, including legal, political, professional, and social accountability, than in Sweden. In Sweden, only legal and political accountability was mentioned, with political accountability being absolutely most prevalent. Yet, overall, both Californian and Swedish public funders stated that the most common external form of accountability was to a variety of political forums. For public agencies in both societies, legal accountability was a mentioned although not a common category. This may be explained by these agencies’ explicit political governance, where elected officials set the legal boundaries for the activities of these organizations, and the accountability categories legal/political may be interpreted as overlapping. One Californian public agency stated professional and social accountability, being a researcher-led institution with a medical focus.

Finally, among philanthropists, I found the strongest differences between the two societies. Overall, accountability forums were barely mentioned by philanthropists in California, save for one respondent mentioning legal accountability. This is in sharp contrast to Sweden, where legal accountability was stated as highly relevant to philanthropists, although they, similarly to Californian philanthropists, did neither prioritize social accountability (patients) nor professional accountability (researchers, medical professionals), and only one Swedish philanthropist mentioned political accountability. This particular foundation had the interest of the general public inscribed in its bylaws, which may be interpreted as a form of legal accountability, rather than any direct assessment of political contentiousness of the research at hand, or financial dependence on the government. Other than this foundation, there was no political accountability mentioned by the philanthropists.

Institutional Logics

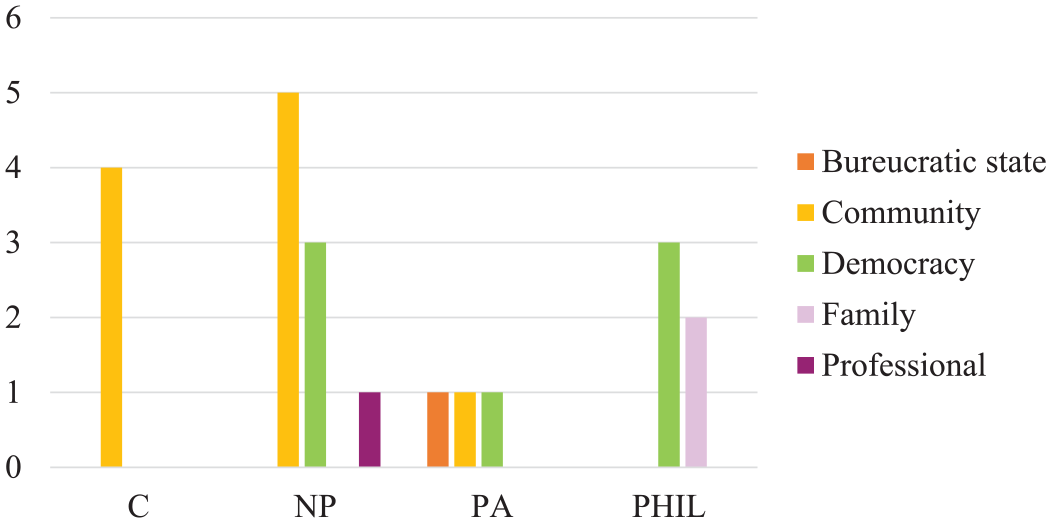

Figures 6 and 7 summarize the types of institutional logics per type of funder in California and Sweden.

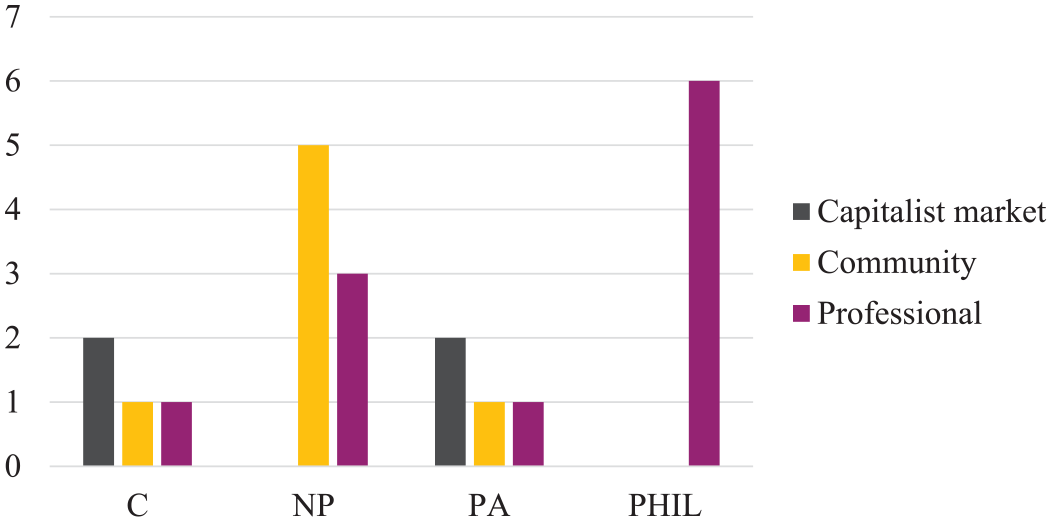

Among corporations in California, the community logic was dominant, focusing primarily on patients: Because we think it’s the best possible way to get some major results in clinical applications. (Community logic—Corporation, California)

For corporations in Sweden, the community logic was stated, along with the capitalist logic (most common) and the professional logic. It seems like in Sweden it was more legitimate for corporations to state hESCs as an actual business opportunity, which in theory every corporation should have as its goal, whereas this was not legitimate in California, perhaps given the contentious nature of the research.

The answer is simple, we don’t fund for any other reason than wanting a return on our investments (. . .) when we make big breakthroughs and have really well-selling products we will earn back this money by far. (Market logic—Corporation, Sweden)

Fundraising-dependent nonprofit was the organizational form with most similarities when comparing between the two societies. Both in California and in Sweden, the community logic was most common, in line with the patient focus among these funders. For nonprofits in both societies, the community logic was used to emphasize the suffering and challenges of specific patient groups, also with the hope of a cure, not “just” a treatment: For us, the motivation is that we have both the causes and the consequences, so we can find some kind of cure. (Community logic—Fundraising-dependent nonprofit, Sweden)

Yet, in California, nonprofits also had a focus on the logic of democracy, specifically focusing on how these funders practiced democracy through their funding by supplementing the state and thereby contributing to society at large. The logic of democracy was only employed in California and was not mentioned at all by any funder in Sweden.

About the time when all of the Bush and NIH [federal public funding agency restricting hESC research] stuff was going on. So, we were one of the few funders that actually went out in public and said that we think the world needs more stem cell lines and we’ll put the money behind it. (Democracy logic—Fundraising-dependent nonprofit, California)

The professional logic was only used in a few instances among fundraising-dependent nonprofits in both societies, but with slightly different foci. In California, the professional logic primarily referred to the utility of hESCs as research tools: Largely what we fund, using these cells, is projects where they’re used as research tools. And that’s what everybody’s excited about. (Professional logic—Fundraising-dependent nonprofit, California)

In Sweden, the professional logic was also employed to demonstrate that the hESC research funding was on par with any other type of research funding, selected only by virtue of its scientific excellence, regardless of any controversial status of the research. This type of method neutrality as regards hESC research was common in Sweden among several types of funders and did not occur at all in California.

We fund research that is good. We always have the quality requirement so that once funding has gone there [to hESC research], as it has done in some cases, it’s because it’s good and effective research. (Fundraising-dependent nonprofit, Sweden)

As regards public agencies in the two societies, there was barely any overlap, except a minor usage of the logic of community: We believe it’s important for future research and the future treatment options for patients. (Community logic—Public agency, Sweden)

Yet, in California, public agencies primarily emphasized either the logic of democracy (the will of the voters) or the logic of the bureaucratic state (just following orders from a higher level public agency).

Well, the people of California voted, 59% of the voters, 7 million people in this state said we want this research to continue [despite federal restrictions] (Logic of democracy—Public agency, California)

In contrast, public agencies in Sweden focused on the capitalist market (hESC research having the potential to spur economic growth), as well as the professional importance of the research (from a medical research perspective). The market logic among public agencies in Sweden was very explicit: In order for it [hESC research] to support economic growth in Sweden. (Market logic—Public agency, Sweden)

The Swedish public agencies’ usage of the professional logic was similar to the one used by the Swedish fundraising nonprofits. Here, hESC research was funded in open competition with other research funding applications, where the specific status of these cells was not taken into account: Because it is of high quality. We fund all research if it’s of high quality, regardless of what it contains or what it focuses on. (Professional logic—Public agency, Sweden)

Although there were large disparities between public agencies in the two societies, the most extreme differences in logic usage may be found among philanthropists. In California, philanthropists legitimized their funding by drawing on the logics of democracy and family. The logic of democracy was seen in the argument that philanthropists could supplement the federal government, precisely because of their independence: We pretty much have our own ideas to what we would like to fund (. . .) We were interested in doing so [funding hESC research] at the time where the federal government was restricting and not willing to fund this kind of research. (Democracy logic—Philanthropist, California)

In the family logic, funding was justified on personal grounds. These arguments were only used by philanthropists, and only in California. Legitimacy attempts drawing on the family logic were extremely personal and emphasized the sometimes very subjective nature of philanthropy: I was contacted (. . .) to meet a young doctor by the name of Y who was a neurosurgeon and doing incredible work as it relates to a condition called [the Disease] (. . .) My sister ended up with [the Disease]. (. . .) we consider Y family by the way (. . .). The operation was obviously successful (. . .) And he applied for a grant for my—if my number is correct, for $1 million and he received it. (. . .) Y came at us again and he had a new project (. . .) And Y received, my recollection is $1 million more. So, the bottom line is, if Y comes to us with a project, we look at these projects. (Philanthropist, California)

In contrast to the logics of democracy and family used in California, Swedish philanthropists relied solely on the professional logic. This indicates that in Sweden, the choice of funding of hESC research was viewed as a strictly scientific decision, whereas in California it was a personal and political statement: It simply hasn’t been in any particular special position of either, whether in terms of supporting or not supporting, but it’s there as interesting research if it’s done in a good way. (Professional logic—Philanthropist, Sweden)

As can be seen from these quotes, the argument of scientific progress was almost identical among Swedish public, nonprofit, and philanthropic funders. However, philanthropists were much more homogeneous as a group within each society in comparison with other funders, as all philanthropists in Sweden drew on this logic, and none in California.

Finally, it is interesting to note that religion has been a central argument against the research on a federal level in both societies. Yet no funder, neither in California, nor in Sweden, used the logic of religion in legitimating their funding decisions of hESC research.

Combining Data on External Accountability Forums and Institutional Logics

When comparing accountability forums and institutional logics used by funders in the two societies, there are stronger differences between institutional logics than there is between accountability forums. Most accountability forums were shared between the organizational forms in the two societies (albeit to different degrees). In contrast, although funders in both societies related to the community logic, and one fundraising-dependent nonprofit in California (medical professional association) employed the professional logic, there was no other overlap between logic usage in the two societies. This indicates that accountability forums are more related to organizational form, whereas institutional logics are more societally determined. Yet there were also variations between types of funders, philanthropists being the most extreme case, with no overlap whatsoever in institutional logics’ usage when comparing between the two societies, and very strong differences as to the prevalence of accountability forums stated.

Compared with other types of funders, philanthropists in both societies were not accountable to patients, researchers, the general public, elected politicians, or the media. This is in line with previous research stating that philanthropists are less accountable than other funders (Fleishman, 2009; Frumkin, 2006b). However, there were also stark differences between the stated accountability forums mentioned by philanthropists in the two societies. In California, philanthropists barely stated any forums at all to which they experienced external accountability (except for one funder), whereas it was common among Swedish philanthropists to stress that they experienced accountability (primarily legal).

In terms of institutional logics, all Swedish philanthropists drew on the professional logic when legitimating hESC research funding, whereas in California philanthropists drew on the logics of democracy and family. In a Californian context, it was thus the personal stance against the government, and in favor of a specific doctor to whom the funder had a personal almost family-like relationship, that was considered an appropriate legitimacy attempt. In Sweden, it was quite the opposite—the impersonal argument being central with philanthropists stating explicitly that hESC research was regarded and assessed as any other type of research.

Philanthropists had some affinities to fundraising-dependent nonprofits in their respective society in terms of the institutional logics they drew on when legitimating their hESC research funding. Fundraising-dependent nonprofits and philanthropists in California drew on the logic of democracy, and fundraising-dependent nonprofits in Sweden, like philanthropists, drew on the professional logic. Yet, in both societies, fundraising-dependent nonprofits also drew on the logic of community, relating to the well-being of the patients. This type of logic was also prevalent among public agencies and corporations in both societies. It was only philanthropists, in both societies, who entirely disregarded patient communities. In addition, unlike other types of funders, philanthropists barely experienced any political accountability, other than one case of it being inscribed in the bylaws of a foundation.

Discussion

What do these findings say about the relationship between the external accountability and legitimacy attempts of philanthropists? Intuitively, some external accountability forums may seem closely related to the usage of certain institutional logics and may be interpreted as material instantiations of these logics (Friedland & Alford, 1991). The empirical analysis does imply that there is some overlap between social accountability and legitimation by the community logic, especially among fundraising-dependent nonprofits. Similarly, there exists, although barely, an overlap between usage of the market logic and accountability to market forums. As regards professional accountability and professional logics, there is also a tiny overlap. This is also the case for political accountability and the logic of democracy and the bureaucratic state. The analysis thus indicates a weak intuitive relationship among related forms of external accountability and legitimacy attempts. Yet these overlaps do not seem very common. For example, the mentioning of a professional accountability forum was not directly translated into the relevance of a professional logic. There was thus no indication of a generalizable and direct translation mechanism (Sahlin & Wedlin, 2008) between institutional logics and accountability forums. Instead, the usage of institutional logics and external accountability forums seemed to function more as complements, addressing a large number of stakeholders (Mitchell et al., 1997) rather than a strictly defined target group. Yet there were patterns in this usage, as forums of external accountability and institutional logics seemed to complement each other, rather than supplement, however in complex ways. This lack of overlap points to a potentially complementary symbolic use of accountability forums to render institutional legitimacy. Another explanation may be that accountability forums essentially provide checks and balances for the daily operations of the funders, which are largely decoupled (cf. Meyer & Rowan, 1977) from the formal organization that relates to a whole different set of legitimacy demands through the usage of institutional logics.

It is, however, interesting to note that among philanthropists, none of the intuitive overlaps between institutional logics and accountability forums were found. Philanthropists in California, who were barely accountable at all, legitimized their funding by referring to the logic of democracy and family. In contrast, in Sweden, philanthropists experienced mostly legal accountability, yet they legitimized their funding by referring to the professional logic. In their usage of logics, both in their stated partiality (the logic of democracy and family in California) and stated impartiality (the professional logic in Sweden), philanthropists were more uniform as a group than other types of funders, indicating isomorphism (DiMaggio & Powell, 1983). These results are both in line with previous research stating that philanthropists strive to demonstrate independence (Ostrander, 2007; Quinn et al., 2014; Whitman, 2009), as in the Californian case, and that philanthropists align with elite institutions (Aksartova, 2003; Eisenberg, 2007), as in the Swedish case, where philanthropists were most similar to the public agencies holding preeminent authority in the Swedish context. As regards accountability forums, philanthropists’ extreme lack of forums stated (California) and extreme uniformity of forums stated (Sweden) also indicate isomorphism. Within each society, both in terms of accountability forums and legitimacy attempts, philanthropists were thus more alike as a group within each society than other funders, and yet more different across societies. This indicates that it may be through local isomorphism, rather than any specific accountability mechanism, that philanthropists demonstrate accountability and legitimate their giving.

The findings on philanthropists challenge the notion of accountability forums serving purposes of complementary legitimacy or effectiveness in a decoupled capacity. Rather it seems like philanthropists in some instances do not need accountability to be isomorphic (California), but it is rather the conformity to the local philanthropic field itself that renders legitimacy, regardless of accountability forums. The role of forums in relation to logics is thus far from intuitive, neither in a complementary nor a decoupled sense.

Conclusions, Limitations, and Future Research

This study has shown, in line with previous research (Cordery & Sim, 2018; McIlnay, 1995; Williamson et al., 2017), that philanthropists are both less accountable and primarily legally accountable. However, this accountability varies between societies. In addition, the analysis indicates, similar to other studies (Quinn et al., 2014; Tomei, 2013), that philanthropists attempt to legitimate actions by demonstrating adherence to various institutionalized norms (logics), although this legitimation is locally contingent.

The stark differences between the societies in terms of institutional logics used by philanthropists thus support research on the local contingencies of institutionalized arguments (Bies, 2010; Marquis & Battilana, 2009). However, the results on accountability forums also indicate that the organizational form of philanthropists matters, as philanthropists within each society are more isomorphic (DiMaggio & Powell, 1983; Meyer & Rowan, 1977) than other types of funders.

It is important to learn more about the implications of these findings regarding philanthropists’ legitimacy and accountability. Philanthropists were essentially detached from both the general public (political accountability) and specific concerns about patient communities (social accountability) in both societies in terms of accountability forums, which raises questions about their legitimate engagement for public purposes at the expense of elite interests, as has been raised by previous research (Arnove, 1984; Roelofs, 2003). This study indicates that the type of public sphere legitimacy that philanthropists may strive for by demonstrating accountability is locally contingent, albeit elitist and somewhat insular, being primarily related to their independence (California) and scientific prowess (Sweden), rather than patients or the broader general electorate. These findings strengthen the notion of philanthropy being an elite institution, posing challenges in terms of its legitimate role in a liberal democracy (Ostrander, 2007; Prewitt, 2006; Reich, 2016).

The findings of this study are limited given the comparative qualitative nature of the research. Generalizations have been made to allow for comparative elements, which more in-depth qualitative studies could contribute more nuance to. Future research drawing on quantitative data may fully explore and test the findings indicated, especially the complex relationship between institutional logics and external accountability forums may be further elucidated. This may also be done by moving beyond the extreme case of hESC research funding and explore whether the results presented here are valid also in other policy areas.

Footnotes

Acknowledgements

The author wishes to thank Maria Blomgren for believing in this study from the outset, as well as Jona Stössel for unwavering support.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study had not been possible without the grants that were generously contributed by the Ryoichi Sasakawa Young Leaders Fellowship Fund, the Kjell and Märta Beijer Foundation, the Jan Wallander and Tom Hedelius Foundation, the PhD Fellowship of ARNOVA, Stiftelsen Clas Groschinskys Minnesfond for Behavioral and Social Research, and the Foundation for Economics and Law.