Abstract

Despite the prevalence of publicly listed family-controlled firms (FCFs) in high-technology sectors, the impact of family control on their corporate venture capital (CVC) strategy remains largely unexplored. Using socioemotional wealth (SEW) theory, we posit that FCFs in high-technology sectors are less likely to invest in CVC and, when they do, make fewer but larger CVC investments to enhance influence over startups and reduce risk. However, board independence can limit FCFs’ SEW-driven CVC investment behavior. Empirical evidence from a sample of U.S. publicly listed firms in three high-technology sectors supports most of our hypotheses.

Keywords

Introduction

Corporate venture capital (CVC) is a systematic practice employed by established corporations to make equity investments in startup companies, and it has undergone drastic expansion in recent decades (Eckblad et al., 2019). Researchers have shown increasing interest in understanding the reasons why some firms pursue CVC more proactively, specifically, which investment strategies are followed (e.g., Basu et al., 2011; Dushnitsky & Lenox, 2005a; Gaba & Meyer, 2008; Tong & Li, 2011). However, despite extensive literature on the organizational and market antecedents of CVC, the question of how ownership structure can affect both the decision to implement CVC programs and the investment strategy followed remains largely unexplored (Amore et al., 2021; Prügl & Spitzley, 2021). We address this question by examining the distinction between publicly traded family-controlled and non-family-controlled firms operating in high-technology sectors. Our focus on large firms in these sectors stems from the fact that, although CVC activity has been increasing overall, it remains predominantly concentrated among such firms (Balachandran & Eklund, 2024; Ryu et al., 2025). CVC is particularly relevant in industries that depend on continuous innovation and frequently seek breakthrough products or technologies through collaborations with entrepreneurial ventures (Basu et al., 2011; Dushnitsky & Lenox, 2006; Dushnitsky & Yu, 2022).

Publicly listed family-controlled firms (hereafter referred to as family-controlled firms or FCFs) are enterprises where members of the same family group enjoy substantial ownership and are involved in top decision-making (i.e., a firm’s board or top management), which allows them to influence the firm’s strategic decision-making (Anderson & Reeb, 2003; Le Breton-Miller et al., 2011; Villalonga & Amit, 2006). 1 FCFs are highly prevalent worldwide (La Porta et al., 1998), accounting for nearly 41% of listed firms in developed and emerging markets (Berrone et al., 2022). In the United States, FCFs represent approximately 33 percent of publicly traded corporations (Berrone et al., 2022). Given the importance and ubiquity of FCFs, as well as their increasing participation in CVC deals (Amore et al., 2021), it is crucial to improve our understanding of how family control and influence can impact a firm’s CVC investment strategy.

This study relies on the socioemotional wealth (SEW) theory (Berrone et al., 2012; Gómez-Mejía et al., 2007) to outline the theoretical mechanisms linking FCF and CVC strategy. As the literature discusses, CVC creates tensions within firms (Jeon & Maula, 2022). For example, in non-FCFs, some executives may view CVC investments as a means of exploring new opportunities, such as learning about new technologies. Others may see such investments in terms of financial outcomes, emphasizing CVC’s return on investment. In contrast, the FCFs’ SEW generates additional tensions between economic and non-economic goals. Conversely, FCFs may be heterogeneous in governing such tensions (Van Aaken et al., 2017).

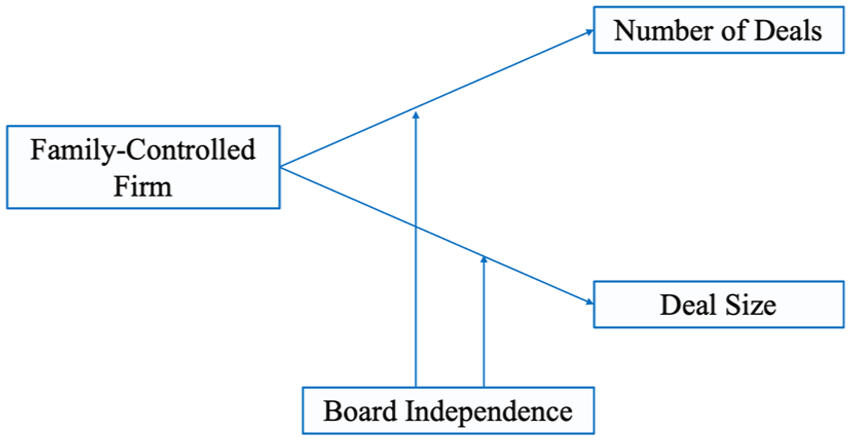

We suggest that FCFs in high-technology sectors are less prone to participate in CVC programs than their non-FCF counterparts due to the complexity and downside risks associated with CVC that might affect the family’s socioemotional endowments. If the FCF indeed pursues CVC programs, we expect the family’s SEW concerns to induce the firm to make fewer but larger CVC investments than non-FCFs. Such a targeted investment approach would enable FCFs to strengthen their family influence over the startups and focus on less risky ventures at later stages of their development. However, FCFs differ in their approach to appointing independent directors to their boards. We thus suggest that board composition is a relevant governance practice for constraining family-centric behavior concerning CVC. Specifically, by exercising their monitoring role, independent directors—those the firm does not directly or indirectly employ—lessen the possibility that FCFs’ managers act only on behalf of the controlling family, thus reducing FCFs’ SEW-driven CVC behavior.

We test our hypotheses using a sample of firms listed on the U.S. stock market from three high-technology sectors—information technology, health care, and communication services. We collected detailed information about these corporations’ CVC investments between 2007 and 2018, and then we combined this information with yearly data about these firms’ ownership structures and corporate governance.

Our research contributes to the literature on CVC and family firms in two significant ways. First, we extend the literature on CVC (Basu et al., 2011; Jeon & Maula, 2022; Ma, 2020; Tong & Li, 2011) by demonstrating that family control influences CVC investment strategies in high-technology sectors. Previous studies have explored factors, such as a firm’s industry or technological resources, as predictors of CVC involvement (Drover et al., 2017). However, research linking firm control to CVC investment behavior is sparse (for exceptions, see Amore et al., 2021; Anokhin et al., 2016; Theisen et al., 2024). In this study, we generate insights into the role of the firm’s control structure as a critical factor explaining differences in CVC involvement and investment behavior and the role of board governance as a contingency in FCFs’ strategic decisions. Second, we add to the literature on corporate entrepreneurship in family firms. Whereas most of this literature studies family businesses as recipients of venture capital (VC) (e.g., Croce & Martí, 2016; Ljungkvist & Boers, 2017; Marchisio et al., 2010), we analyze FCFs as investors of VC. This is important for researchers because corporate entrepreneurship and venturing can play a crucial role in the survival and growth of FCFs, especially in high-technology sectors (Kellermanns & Eddleston, 2006; Phan et al., 2009).

Theory and Hypotheses

SEW Theory

The literature on family firms has extensively highlighted the importance of family-centric objectives in the FCFs’ decision-making process (Berrone et al., 2010). The SEW perspective, in particular, has been one of the most relevant theories to capture the role of non-economic goals in family owners’ behavior and the impact of family control on the overall business system (Davila et al., 2023; Nason et al., 2019). SEW theory draws on the behavioral agency model (BAM), which combines prospect and agency theory (Gómez-Mejía et al., 2019). SEW theory’s central argument is that socioemotional goals—defined as the “non-financial aspects of the firm that meet the family’s affective needs, such as identity, the ability to exercise influence, and the perpetuation of the family dynasty” (Gómez-Mejía et al., 2007: 106)—might constitute the family owners’ primary reference point for their risk perception (Gómez-Mejía et al., 2007). In this sense, family owners who prioritize SEW may frame decision-making regarding loss aversion, favoring the avoidance of potential losses to their non-economic goals over the pursuit of economic gains (Gómez-Mejía et al., 2007). As a result, they might avoid strategic business options that could threaten family owners’ SEW, even if such options increase the risk of poor performance (Gómez-Mejía et al., 2007) or are considered “economically irrational” (Gómez-Mejía et al., 2011, p. 661).

According to SEW, maintaining managerial control and influence is among the most critical concerns for some family owners (Berrone et al., 2012; Davila et al., 2023). Such control allows the family to obtain the required legitimacy, liberty, and power to pursue business initiatives that satisfy, protect, and enhance family-centric needs (Carney, 2005; Miller et al., 2013; Zellweger et al., 2012). As a result, FCFs that prioritize SEW may shun investments or strategic initiatives that could dilute such control (Berrone et al., 2022; Miller & Le Breton-Miller, 2014). For example, studies show the reluctance of FCFs to pursue innovation (Duran et al., 2016), acquisitions (Cuevas-Rodríguez et al., 2023; Gómez-Mejía et al., 2018), diversification (Gómez-Mejía et al., 2010), and internationalization (Arregle et al., 2017). The reasoning is that the pursuit of risky strategies requires external financial resources and managerial capabilities that family businesses are unwilling to obtain due to potential financial distress, changes in management style, and reduced discretionary family power over the business (Souder et al., 2017).

In sum, SEW theory, with its focus on the tension between the double utility of family principals (financial and socioemotional) as opposed to the single focus on financial risk-bearing of non-family principals, represents a suitable lens to explain differences in FCFs’ strategic behaviors—such as CVC investments—relative to non-FCFs (Gómez-Mejía et al., 2019).

Family-Controlled Firm and CVC Program Participation

CVC is an innovation vehicle valued by financial analysts and potential investors (Guo et al., 2019), as CVC programs allow firms to improve their innovation strategy and adapt to market needs faster than in-house R&D (Basu et al., 2011; Dushnitsky & Lenox, 2005a; Ma, 2020). CVC can also reduce the information asymmetry between managers and investors, facilitating assessing a firm’s innovative performance (Guo et al., 2019). These investments can also improve the connection of firms to high-technology ecosystems (Danneels & Miller, 2023). However, CVC programs can pose a substantial risk of failure to firms. This can be partially explained by difficulties in designing and operating CVC programs (Gaba & Meyer, 2006), lack of internal expertise to manage investments (Dushnitsky & Shapira, 2010), lack of fit between ventures’ innovations and the overall corporation’s strategy (Alvarez-Garrido & Dushnitsky, 2016; Pahnke et al., 2015), and lack of managerial attention to effectively monitor startups (Keil et al., 2016). In addition, the business model viability, market demand, and expected returns of new ventures are typically beyond managerial control (Dushnitsky & Shapira, 2010; Tong & Li, 2011). As a result, although a new venture’s success can boost corporate financial performance (Huang & Madhavan, 2021), the risk of corporate shareholders’ value destruction exists. For example, Benson and Ziedonis (2010) estimate that the average return to acquisitions of CVC portfolio companies is more than 1.5% lower than the average return to non-CVC investments.

As mentioned earlier, FCFs tend to avoid strategies with uncertain upsides to reduce the risk of failure (Gómez-Mejía et al., 2018). The family SEW suffers if the family business performs poorly or fails (Block et al., 2019). Unlike other corporate restructuring strategies (e.g., M&A), CVC initiatives typically require substantial internal funding commitments (Dushnitsky & Lenox, 2005b), making them more financially demanding and potentially leading to reliance on external financing. Research suggests that FCFs are less prone to rely on external sources of capital (Hansen & Block, 2021), given the potential threat to the family’s control and decision-making autonomy (Gómez-Mejía et al., 2010), core SEW priorities for these firms. Moreover, increasing business risk can create obstacles to intrafamily succession intentions (Clinton et al., 2025; Ireland et al., 2025; Ortiz et al., 2021), another central SEW objective for many FCFs.

To help new ventures succeed, VC investors typically pool their resources into syndicates and exchange knowledge about management and technology with the portfolio companies (Lerner, 1994). This collaborative effort can involve disclosing core expertise with other parties who share ownership in the startup (Park & Steensma, 2012). FCFs may be overly protective regarding their independence (Carney, 2005) and more reluctant to share proprietary information with outsiders (Schulze et al., 2001). Consequently, due to SEW concerns, FCFs may have a lower incentive and willingness to invest with external stakeholders (Le Breton-Miller, & Miller, 2013).

Among the multiple objectives, corporations invest in new ventures to upgrade their technology (Dushnitsky & Lenox, 2005a). CVC becomes especially attractive when the firm’s marginal innovative output obtained through startup acquisitions surpasses its internal innovation performance (Dushnitsky & Lenox, 2005b) and when the corporation experiences a deterioration in its capability to develop in-house innovations (Ma, 2020). In some FCFs, tendencies toward controlling and prioritizing SEW may contribute to a higher internal innovation input-innovation output conversion rate (Duran et al., 2016). When this is the case, FCFs might find it more beneficial to leverage internal capabilities and resources for developing new technologies rather than relying on CVC investments.

In sum, this study argues that CVC programs carry significant risks to FCFs’ SEW, which reduces these firms’ incentives to adopt them. Consequently, we hypothesize that:

Family-Controlled Firm and CVC Investment Strategy

In addition to an FCF’s decision to implement a CVC program, it is important to understand the investment behavior of those FCFs that do become involved in CVC. In the following hypotheses, we continue applying the above SEW arguments to predict the behavior of FCFs that pursue CVC investment. We would like to emphasize that the theoretical arguments presented in the following hypotheses are specific to firms participating in CVC programs. The theory below does not aim to predict the behavior of firms not involved in these programs. In other words, the following hypotheses are conditional on participation in a CVC program. This study focuses on two important strategic aspects of CVC investment behavior: (a) the number of investment transaction deals to pursue and (b) the average size—in terms of monetary value—of these transactions.

We first argue that FCFs who decide to implement CVC programs tend to participate in a lower number of deals relative to non-FCFs for several reasons. First, managing an extended portfolio of new ventures requires distinctive expertise that corporations often lack (Dushnitsky & Shapira, 2010). Although corporations can fill this need by participating in syndicates (Theisen et al., 2024) or hiring CVC managers with career experience in VC firms (Dokko & Gaba, 2012; Lerner, 1994), FCFs tend to be more reluctant to rely upon outside expertise, as it may threaten family control (Arregle et al., 2017). Second, CVC programs can be challenging to operate (Gaba & Meyer, 2006). CVC managers must overcome the complexity of the deal selection process and information overload about external technologies to avoid selecting poor-quality deals that may hamper the corporation’s performance (Wadhwa & Kotha, 2006). In addition, managers must ensure that ventures’ innovations align with the corporation’s strategy and products (Pahnke et al., 2015) and that CVC-backed ventures can leverage corporate assets to enhance innovation (Alvarez-Garrido & Dushnitsky, 2016). However, resource constraints and limited managerial attention reduce the capacity to effectively manage an extensive venture portfolio (Keil et al. 2016). FCFs are often particularly attentive in avoiding the situations described above (McConaughy et al., 1998), as their financial resources and future family wealth may be at stake (Carney, 2005). Given that FCFs are more inclined to close oversight of their CVC strategy and performance, FCFs are likely to adopt a more conservative and selective approach to the number of CVC deals they engage in. Therefore, we propose the following hypothesis:

The monetary value or size of a venture capital investment transaction is a crucial strategic decision that any VC firm must make (Gompers & Lerner, 1999). For example, some VC firms may choose to participate in many smaller investment deals, while others may prefer to become involved in fewer deals of larger size. Two crucial factors that drive this decision relate to (a) the willingness to participate with other investors through syndicates (Sorenson & Stuart, 2008) and (b) the development and risk profile of the portfolio companies that the investor finds acceptable (Lerner, 1994).

Even though the strategy of co-investing with other firms allows for decreased risk exposure, the VC firm will reduce its influence on the startup company receiving the funds (Mingo, 2013). Typically, corporations making CVC investments take a minority equity stake in their portfolio companies through syndication, allowing private VC firms to lead the investments and take board seats on startup ventures (De Clercq et al., 2006). It is uncommon to find CVC investors occupying board seats as part of their investment relationship (Hallen et al., 2014). Corporations often maintain distance from their portfolio companies to avoid scaring off startups with threats of corporate dominance (Diestre & Rajagopalan, 2012). However, the typical minority status that corporations hold over portfolio companies may conflict with an FCF’s SEW desire to influence business activities (Berrone et al., 2012). To address this concern, we propose that FCFs will likely invest more capital in CVC deals than other organizational forms, aiming to secure greater influence over their portfolio companies.

To extract the performance and strategic benefits of investing in startups, venture capitalists monitor the progress of their portfolio companies (Wadhwa & Kotha, 2006). Greater influence over the portfolio company enables FCF executives to participate more actively in the new venture’s governance (Keil et al., 2008) and exercise their monitoring capabilities (Carney, 2005; Duran et al., 2016). Moreover, by allocating more capital to specific startups, FCFs can pursue their SEW interests in the entrepreneurial venture (Dushnitsky & Shaver, 2009) while acting more independently. This approach reduces scrutiny from other investors (Miller et al., 2013) and minimizes potential conflicts of interest (Paik & Woo, 2017). Finally, a more predominant role for an FCF within the portfolio company would foster a closer relationship with the venture’s experts, facilitating the acquisition of crucial knowledge about startup operations (Keil et al., 2008; Wadhwa & Kotha, 2006). Acquiring expertise and technological competencies from ventures helps reduce uncertainty for FCFs (Ceccagnoli et al., 2018) and alleviates the potential SEW concerns of families regarding overreliance on external expertise from VC co-investors.

We also argue that FCFs will likely commit more resources to CVC investment deals to access portfolio companies with a lower-risk profile. Startups financed by VC firms typically raise capital in rounds (Gompers & Lerner, 1999). In accounting for the agency problem in VC, VCs invest incrementally—early-stage ventures typically raise smaller amounts of capital than those at later stages of development (Fitza et al., 2009). In other words, the size of a VC investment transaction rises as the venture’s development level increases, and its risk of failure decreases (Khoury et al., 2015). As discussed earlier, to protect SEW, FCFs have a higher tendency to avoid the risk of failure (Block et al., 2019; Gómez-Mejía et al., 2014, 2018). Therefore, focusing CVC investments on startups in later stages of development—with higher valuations—would help achieve this goal. Moreover, FCF executives are less likely to have compensation incentives that favor risky behavior in exchange for the “security blanket” provided by the controlling family (Gómez-Mejía et al., 2011). Thus, FCF managers may lack upside incentives to target earlier-stage rounds, resulting in a focus on later-stage startups (Dushnitsky & Shapira, 2010). Since the amount of VC funds raised in an investment round is generally higher for more mature and valuable ventures, FCFs are likely to be required to make, on average, larger investment deals.

In short, we argue that the FCFs’ preference for more influence and a lower risk of failure will translate into larger CVC investment deals. Hence, we hypothesize that:

The Moderating Effect of Independent Directors on the Family Control-CVC Investment Strategy Relationship

We reason that FCFs will vary in their ability to address the tension between economic and SEW non-economic goals. The controlling family may recognize that FCFs’ executives may overemphasize socioemotional goals to the detriment of the firm’s financial performance. FCFs may adopt specific governance mechanisms to alleviate the downsides of this tension (Van Aaken et al., 2017). We focus on the role of independent directors. The board of directors plays a crucial role in approving funding and overseeing the strategy of corporations, including CVC (Anokhin et al., 2016). Given that FCFs pursuing SEW-driven strategic decisions may create agency conflicts between family controllers and minority shareholders (Luo & Chung, 2013), it is both theoretically and empirically important to investigate how governance mechanisms, such as board independence, influence the ability of FCFs to foster SEW-driven CVC investment behavior (Berrone et al., 2022; Duran & Ortiz, 2020; Miller et al., 2013).

Generally, two groups of shareholders with different risk orientations coexist in FCFs: the controlling family and minority shareholders. As discussed earlier, the controlling family is risk-averse in their strategic choices because they invest a significant portion of their wealth in the firm (Duran et al., 2016), and family wealth would suffer if high-risk strategies fail (Mishra & McConaughy, 1999). In addition, the controlling family is often loss-averse concerning their SEW (Gómez-Mejía et al., 2007), leading FCFs to avoid risky strategic choices for non-economic endowment (Patel & Chrisman, 2014). On the contrary, scholars assume minority shareholders to be risk-neutral agents (Eisenhardt, 1989; Souder & Bromiley, 2017), prompting managers to undertake riskier projects with potentially higher returns, as they can mitigate their risk exposure through investment diversification (Jensen & Meckling, 1976). We suggest that these diverse attitudes toward risk and tolerance for failure affect how each shareholder group understands the optimal investment strategy regarding CVC. More specifically, FCFs participating in CVC programs would opt for an SEW-driven approach by reducing the number of CVC deals made by the firm (see H2a) but increasing the average size of each CVC deal to protect SEW (see H2b). However, the opposite tendency should be observed in minority shareholders. Non-family shareholders are likely to favor an investment strategy that emphasizes a higher number of CVC deals of a smaller size each to optimize investment performance (Yang et al., 2014). Since the controlling family is the most influential shareholder group in FCFs, the family logic to handle CVC investments should prevail in these firms. However, we argue that the board’s composition, specifically the proportion of independent directors, may influence FCFs’ discretion in advancing particular CVC investment strategies. Appointing independent directors to the board is a variable governance solution among FCFs. It is a form of voluntary self-binding where foresightful families recognize a need to alleviate their tendency to pursue socioemotional goals by introducing actors into their governance structure to check FCFs’ socioemotional propensities.

Independent directors mean their directorship is their only affiliation with the firm. Directors currently employed by the firm (or retired from it), their immediate family members, and those with existing or potential business relationships with the firm are not classified as independent directors (Anderson & Reeb, 2003). Independent directors are assumed to better represent the interests of all firm shareholders due to their greater objectivity in decision-making (Mutlu et al., 2018), thereby effectively balancing the interests of the controlling family and minority owners (Kuo & Hung, 2012). One of the independent directors’ primary functions concerns monitoring the firm’s management (Adams et al., 2010; Hasija et al., 2025). The higher the presence of independent directors on a firm’s board, the higher the oversight over executive actions (Hermalin, 2005). This is particularly relevant for minority shareholders investing in FCFs, as family members often hold leadership positions, or their non-family executives are heavily influenced by the controlling family’s desires. By exercising their monitoring role, independent directors may reduce the likelihood that managers prioritize the controlling family’s SEW needs over acting in the best interest of all shareholders (Anderson & Reeb, 2004; Miller & Le Breton-Miller, 2006). In other words, independent directors will induce FCFs to behave more like dispersed-owned organizations regarding CVC strategy.

Moreover, several studies have documented how board independence affects the risk-taking of FCFs (e.g., Chen & Hsu, 2009; Majocchi & Strange, 2012). By bringing critical business expertise, FCF’s independent directors can encourage strategic risk-taking without threatening the family’s socioemotional goals (Jones et al., 2008). Indeed, since CVC deal activity is sensitive to executives’ prior experience (Souitaris et al., 2012), independent directors may expand the knowledge base in CVC investment, thereby reducing family concerns about relying on external expertise to manage an extended portfolio of startups. Finally, another critical function of independent board members is to design an appropriate managerial compensation system that aligns managerial actions with shareholders’ expectations. Independent directors may rely on this function to advocate for executive incentive schemes that favor a more balanced composition of the firm’s portfolio of ventures in their development stage, rather than focusing on late-stage startups (Dushnitsky & Shapira, 2010), which better aligns with FCFs’ minority shareholders’ risk orientation. Hence, we propose the following hypotheses:

Figure 1 summarizes our theoretical framework.

Theoretical Framework (Firms that Participate in CVC Programs).

Methodology and Data

We built our database in several steps. First, we relied on NRG metrics to identify a list of corporations traded on the U.S. stock market. NRG Metrics provides yearly data about the corporate governance of listed companies in the United States. The database considers information from annual reports, U.S. securities and exchange commission (SEC) filings, corporate governance reports, firm presentations, and press releases. NRG metrics data have been used in previous finance and management research (e.g., Duran et al., 2025), including studies on family firms (e.g., Miroshnychenko et al., 2021). We then built a sample of the 100 largest firms from three industrial sectors—information technology, health care, and communication services—based on the firms’ 2018 total revenues. In the case of communication services, we include all 56 firms that are included in NRG Metrics. We chose these industries because their technological nature makes them more prone to CVC activity (Basu et al., 2011; Dushnitsky & Lenox, 2006). This “focused” sample ensures the reliability and completeness of the information. In addition, a focused sample reduces the likelihood of including firms that make random, one-time opportunistic CVC investments without a clear strategy (Banholzer et al., 2022).

Next, we obtained detailed information on CVC investment transactions for the firms in the sample during 2007–2018 from VentureXpert (Refinitiv® Eikon). The firms in our panel data set were involved in 3,978 CVC deals during the period under study. All the information at the investment-transaction level was then aggregated by firm each year, obtaining the yearly number of deals made by every firm and the total annual investment in CVC. Financial data for the firms come from COMPUSTAT. In addition, we used variables from the NRG Metrics data set 2 to obtain the yearly information that allows us to identify FCFs, measure the percentage of family members on the board of directors, and determine board independence. Finally, we merged the CVC, financial, and NRG Metrics data, generating the firm-year observations used in the empirical analyses. Information related to the control variables comes from the same data sources.

Dependent Variables

Our empirical work considers three dependent variables. The first is CVC Program, a dummy variable equal to 1 if a firm has ever participated in a CVC program during the period under study, that is, made at least one CVC investment deal during that period. We use this variable to test H1.

We use the following two dependent variables to assess H2 and H3, respectively. The variable Number of Deals measures the number of deals a firm makes during a particular year. The variable Deal Size is the natural logarithm of the average size, 3 in USD, of the CVC investment deals made by a firm during a year plus 1. We applied a logarithmic transformation to handle skewness.

Independent Variables

Family-Controlled Firm

Research suggests that family owners’ SEW objectives are particularly salient when the family enjoys substantial influence in setting the firm’s primary goals and strategic decisions (Arregle et al., 2017; Berrone et al., 2010, 2022; Davila et al., 2023; Duran et al., 2016; Gómez-Mejía et al., 2007; Kim et al., 2019; Zellweger et al., 2012). Based on previous work, we operationalize Family-Controlled Firm as a dummy variable that is equal to 1 if, during a particular year, the firm’s largest shareholder is a member of the owning family (founder, descendant, or family member) who holds an executive management position (CEO, Chairman, or Vice Chairman) or serves on the firm’s board of directors (Anderson & Reeb, 2003, 2004; Feldman et al., 2019; Gómez-Mejía et al., 2024; Le Breton-Miller et al., 2011; Villalonga & Amit, 2006, 2009, 2010). 4

Family Board Percentage

In addition to the Family-Controlled Firm variable, we use the alternative variable Family Board Percentage. We define this variable as the percentage of family members on the board of directors (including executive and non-executive family members). This alternative non-binary variable captures the level of influence that the family has in continuously controlling strategic decisions. Based on this measure, we provide complementary analyses that mirror the models with the Family-Controlled Firm dummy.

Board Independence

We measure Board Independence as the ratio of outside directors to board size during a particular year, expressed as percentage (i.e., multiplied by 100). Outside directors are board members who have not been “directly or indirectly employed by the firm, either as an employee or as a manager” (Randøy & Jenssen, 2004, p. 283). Directors who are currently employed by the firm (or have retired from it), their immediate family members, and individuals with existing or potential business ties to the firm are not considered independent directors (Anderson & Reeb, 2003). Members of the founding or owning family are not considered independent directors.

Control Variables

Depending on the models, we consider different types of control variables. We include the control variables CEO Tenure and Family Generation. Another relevant control variable is the Number of Investors, which we define as the average number of investors involved in the deals made by a firm (size of the syndicate) during a particular year. We also control for the firm’s total revenues in billions of USD using the variable Sales. We include the variable Age to control for the years since the firm’s inception—a logarithmic transformation was applied to avoid convergence problems with the fixed- and time-effects structure (due to the temporal nature of age). Next, we include a set of key financial metrics: return on assets (ROA), capital expenditures (CAPEX), long-term debt to total assets (Debt), and R&D expenses (R&D). Table 1 offers a detailed description of each variable.

Description of Variables.

CVC investment experience and activity can affect the likelihood of future CVC transactions. To control this issue, we include the variable Deals in Previous 5 Years, which represents the total CVC deals made by the firm during the previous 5 years. Prior studies on VC and private equity typically control for investment experience (Mingo et al., 2018). Finally, depending on the specification and statistical methodology, we include industry, firm, and time (year) fixed effects.

Statistical Methodology

We employ various statistical models, depending on the hypothesis being analyzed. Due to the nature of H1, we must conduct the analysis at the firm level. To avoid spurious results, the analyses assessing this firm-level hypothesis consider only firms that remained either family-controlled or non-family-controlled throughout the entire period under study (209 firms). Due to the lower number of observations and the cross-sectional nature of this particular analysis, we use a more conservative approach through the application of Welch’s t-test to compare the group of firms controlled by families and the group of firms not controlled by families (Ganco et al., 2020; Toh & Miller, 2017). 5 In addition to this test, we run a cross-sectional probit model that includes the Family-Controlled Firm and the basic financial and industry control variables collapsed at the firm level. We replicate this probit regression using the Family Board Percentage variable too.

Consistent with our theoretical framework, we tested H2 and 3, which involve firm-year-level analysis conditional on CVC participation, using the subsample of firms that engaged in at least one CVC deal during the period. Focusing on this subsample of firms maintains consistency with our theoretical development (we discussed more details about this issue in the section “Theory and Hypotheses”). In this case, the data were longitudinal, and the analysis was at the firm-year level. It is important to note that family control, the percentage of family members on the board, and board independence can experience changes over time.

The models that predict the number of CVC deals are fixed-effects negative binomial regressions. Negative binomial regressions are instrumental when the dependent variable is a count variable (e.g., the number of investment deals in a year) and there is evidence of overdispersion (the variance in the count data is larger than the mean). Also, since we have a panel of firms, we can apply fixed effects to control for time-invariant, unobserved characteristics of the firms in our sample.

Finally, we ran feasible generalized least squares (FGLS) models to examine average deal size. Unlike traditional fixed-effects estimation, which requires substantial within-panel variation of the independent variable(s) to generate consistent and efficient estimates (Desender et al., 2016), FGLS models are appropriate for handling a panel data set with independent variables that change infrequently. As is typical in empirical family business research, the variable Family-Controlled Firm remains relatively stable over time within the usual time frames used. For more details about using FGLS in family business research, please refer to Dinh et al. (2022). To maintain consistency, our analyses using the percentage of family members on the board are based on the same methodology.

Results

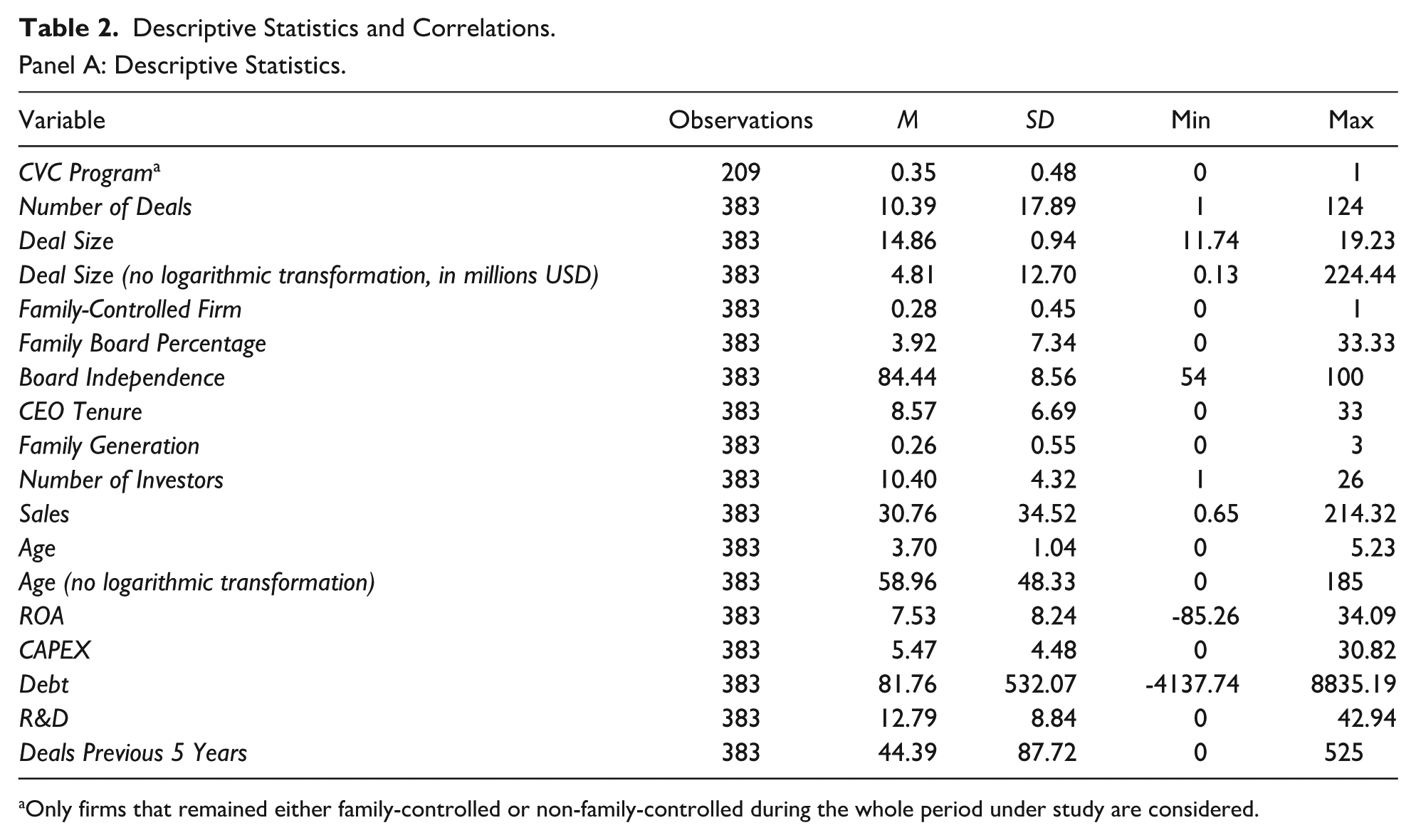

Table 2 (Panels A and B) presents the descriptive statistics and correlations between the variables. The information indicates that 35% of the 209 firms included in the analyses to test H1 participated in a CVC program during the study period.

Descriptive Statistics and Correlations.Panel A: Descriptive Statistics.

Only firms that remained either family-controlled or non-family-controlled during the whole period under study are considered.

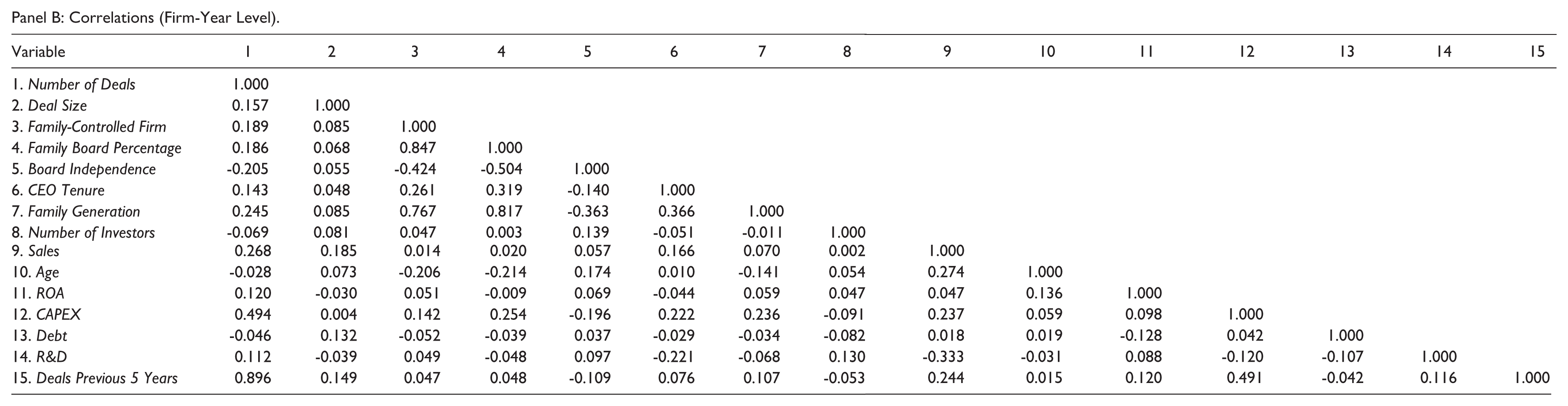

Panel B: Correlations (Firm-Year Level).

Table 2 (Panel A) also shows that the average for the variable Number of Deals is 10.4. Considering the logarithmic transformation, the average size of a CVC investment deal is 14.86 (approximately $ 4.81 million for the original variable). Finally, it is interesting to note that 28% of the firm-year observations are FCFs, with an average of 3.9 for the variable Family Board Percentage, and a percentage of board independence of 84.4% for all these observations. This percentage of board independence, albeit high, is aligned with other studies on U.S. corporate governance (e.g., Joseph et al., 2014).

Main Results

As mentioned earlier, to examine H1, we consider the 209 firms that remained either family-controlled or non-family-controlled during the whole period under study. There are 68 FCFs (Group 1) and 141 non-FCFs (Group 2). According to the data, 26% of the firms in Group 1 and 40% in Group 2 have participated in CVC programs. We ran a Welch’s t-test to assess the significance of this difference. Our findings indicate that the average participation in CVC programs for firms in Group 1 is significantly lower than for those in Group 2, with a p-value of .03.

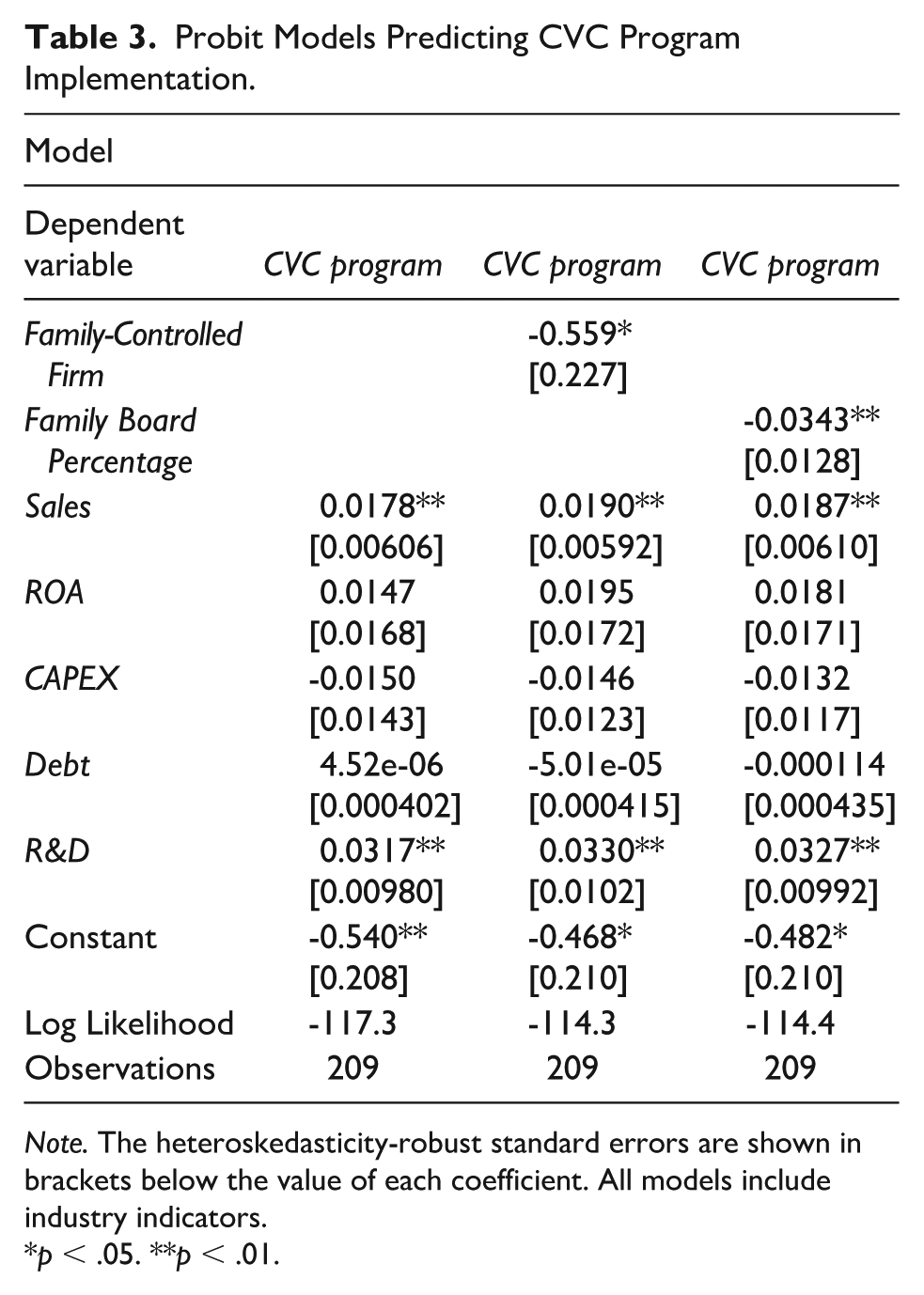

In addition, we present the results of a probit regression predicting CVC program implementation (Table 3). The second column shows a significantly negative coefficient on the variable Family-Controlled Firm. Therefore, the evidence in both the Welch t-test and the probit regression is consistent with H1, that is, FCFs are less likely to participate in CVC programs than non-FCFs. Finally, the third column in Table 3 shows that a higher level of family members on the board of directors is associated with a lower likelihood of implementing a CVC program. Although these results are consistent with H1, we interpret them cautiously due to the cross-sectional nature of these analyses.

Probit Models Predicting CVC Program Implementation.

Note. The heteroskedasticity-robust standard errors are shown in brackets below the value of each coefficient. All models include industry indicators.

p < .05. **p < .01.

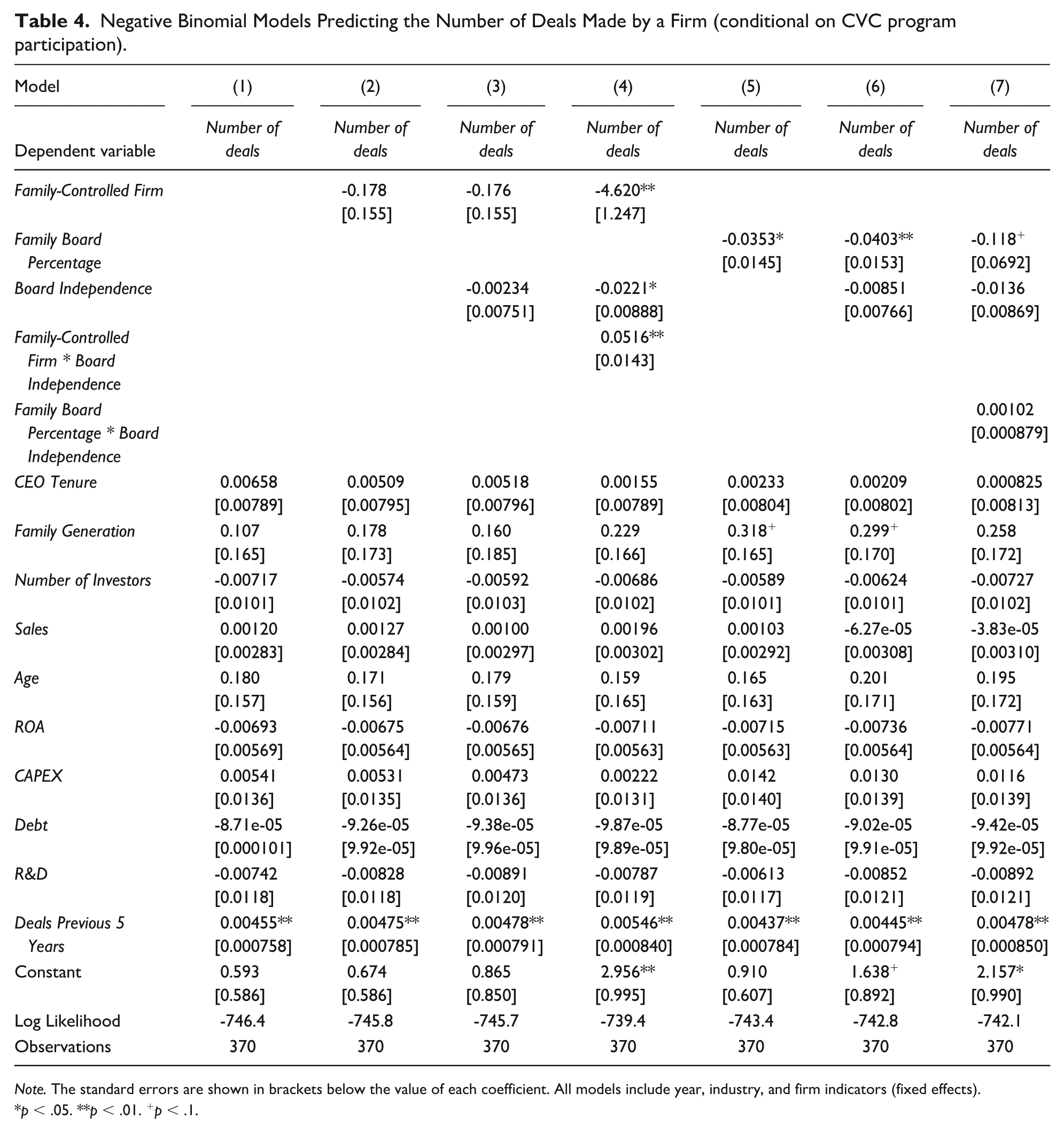

From this point on, we follow a firm-year level of analysis. To test H2a, we consider the information from Model 3 (Table 4). Model 3 includes the direct effect of the variable Family-Controlled Firm on the Number of Deals. The results show that the coefficient on Family-Controlled Firm is negative but not significantly different from zero, with a p-value of 0.26. H2a is not supported.

Negative Binomial Models Predicting the Number of Deals Made by a Firm (conditional on CVC program participation).

Note. The standard errors are shown in brackets below the value of each coefficient. All models include year, industry, and firm indicators (fixed effects).

p < .05. **p < .01. +p < .1.

On the contrary, Model 6 (Table 4) shows a significantly negative coefficient on the variable Family Board Percentage with a p-value of .01. Regarding the effect size, Model 6 predicts that a 1 SD increase in the percentage of family board members over the average value is associated with a 24% decrease in the number of deals.

Summarizing, although we verify that a higher percentage of family members on the board is associated with a significantly lower number of deals, we are unable to establish that the number of CVC deals made by an FCF is significantly lower than those made by a non-FCF.

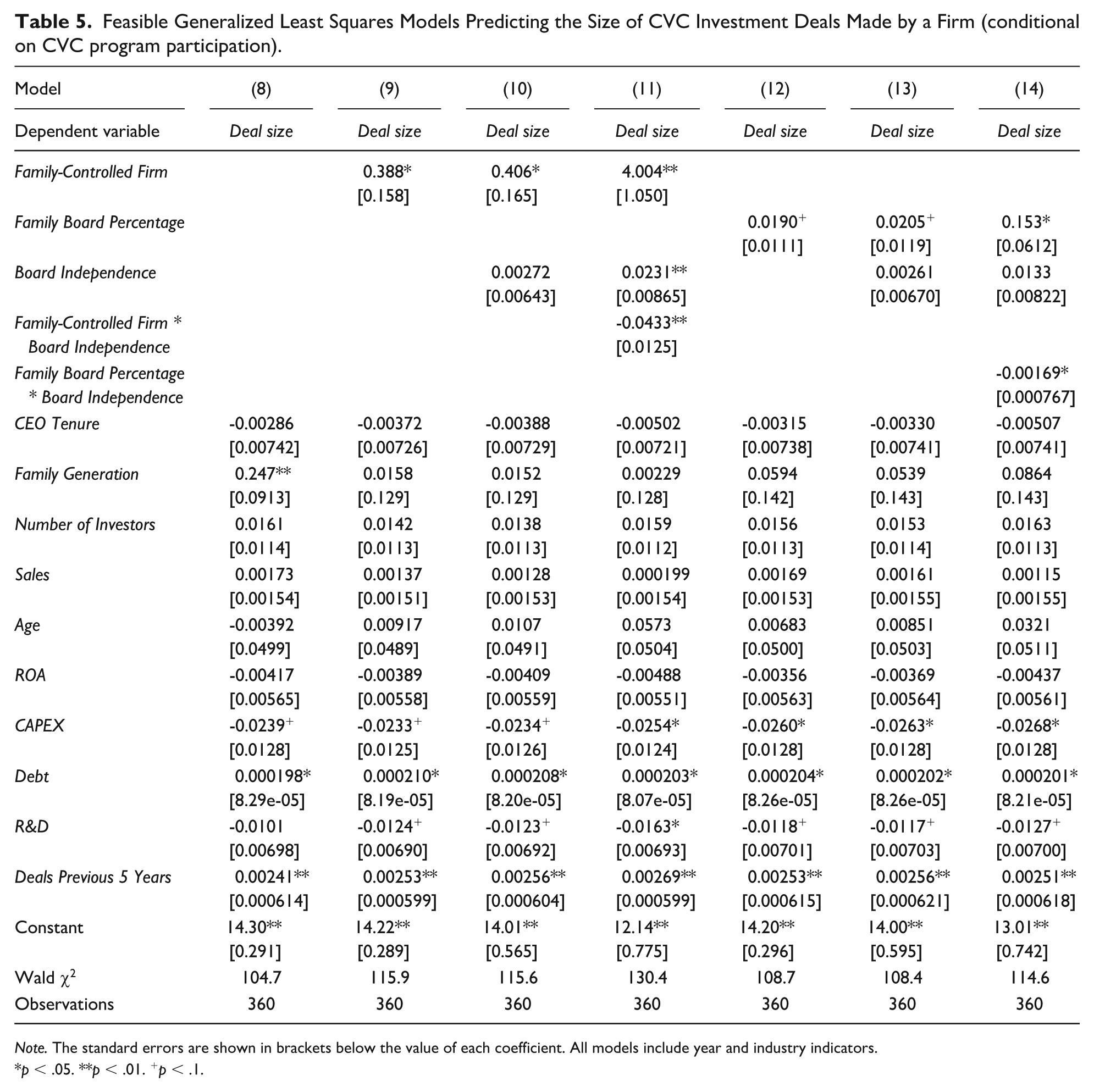

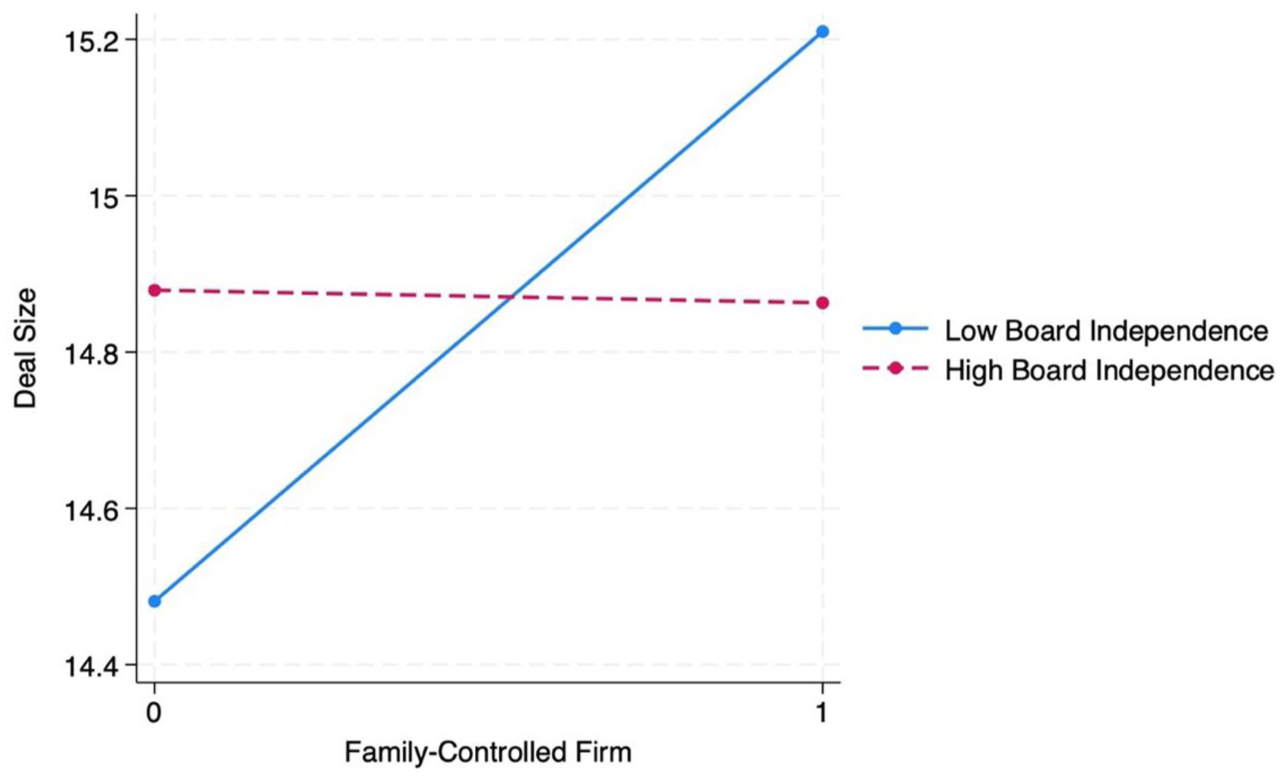

We use Model 10 (Table 5) to test H2b. Model 10 includes the direct effect of the variable Family-Controlled Firm on Deal Size. The results show that the coefficient on Family-Controlled Firm is positive and significant. The p-value of the coefficient is .014. Regarding the effect size, the model predicts that FCFs make investment deals that are, on average, 50% larger in dollar terms than those made by non-FCFs. These results support H2b.

Feasible Generalized Least Squares Models Predicting the Size of CVC Investment Deals Made by a Firm (conditional on CVC program participation).

Note. The standard errors are shown in brackets below the value of each coefficient. All models include year and industry indicators.

p < .05. **p < .01. +p < .1.

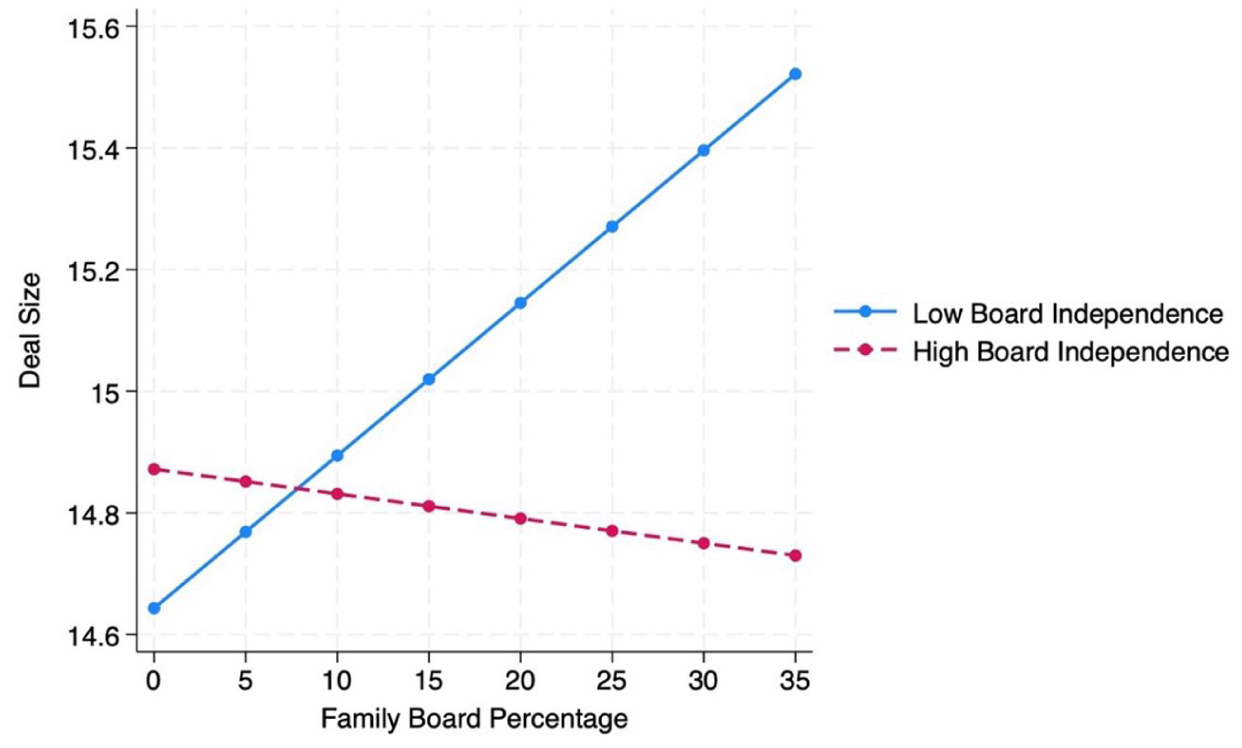

Model 13 (Table 5) also shows a positive coefficient on the variable Family Board Percentage with a p-value of .08. Regarding the effect size, a 1 SD increase in the percentage of family board members over the average value is associated with a 15% increase in deal size (measured in dollar terms).

Therefore, the empirical evidence shows that, conditional on CVC program participation, an FCF’s average investment deal size is significantly higher than that of a non-FCF. The analysis using the Family Board Percentage variable also reveals a positive association with deal size, although the effect is comparatively weaker.

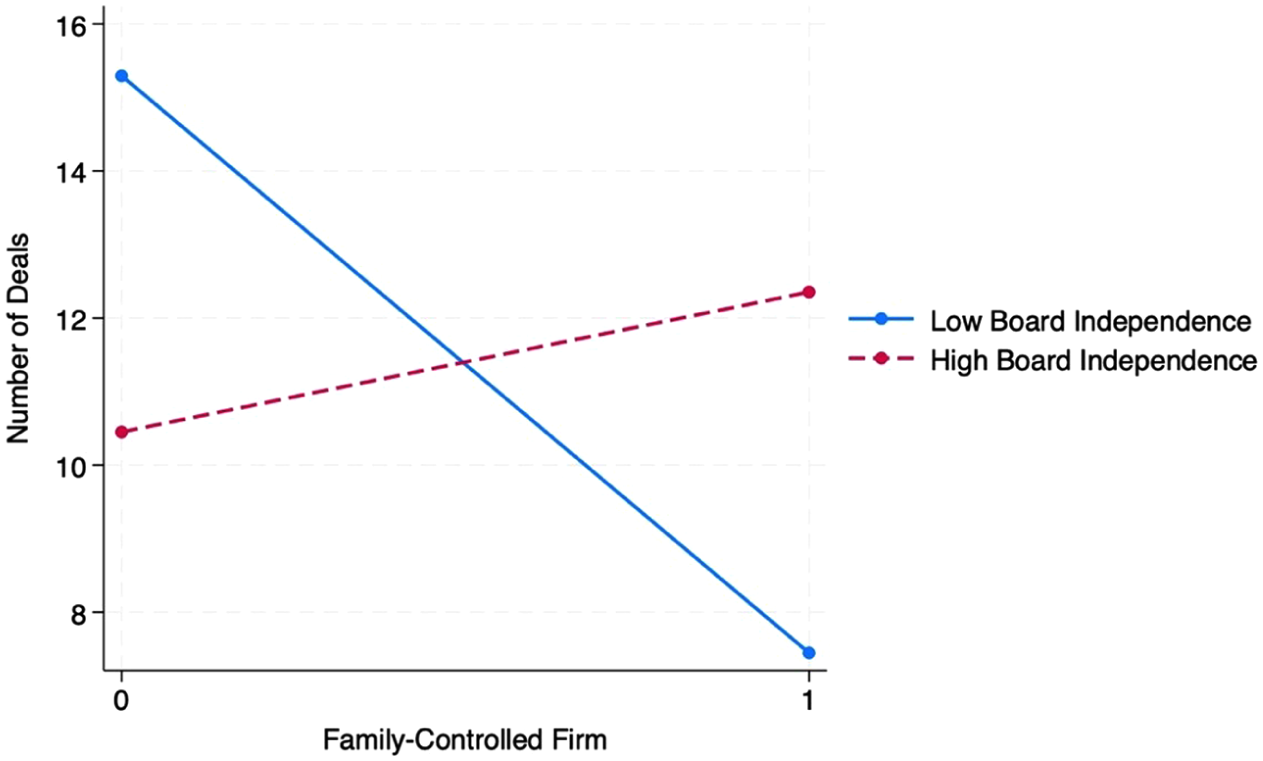

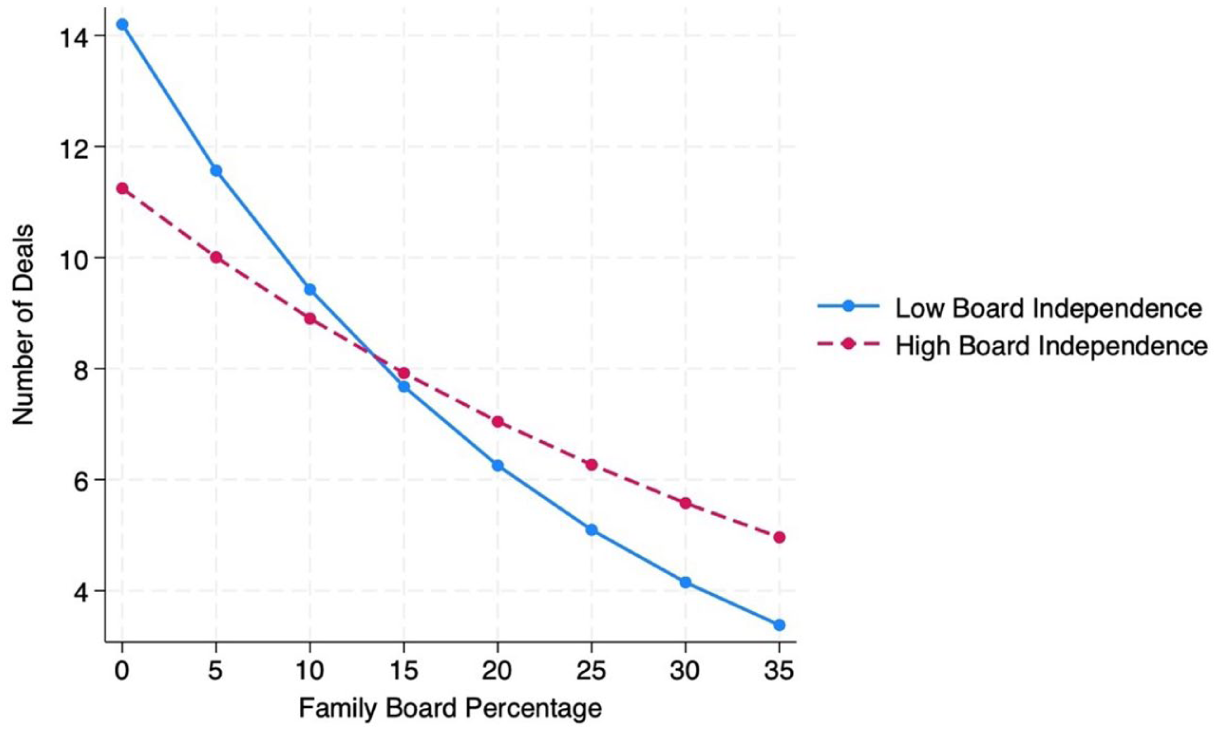

Model 4 includes the interaction terms used to analyze H3a (Table 4). The coefficient on the interaction between Family-Controlled Firm and Board Independence is positive and significantly different from zero, with a p-value of less than .01. Following Hayes and Montoya (2017), Figure 2 shows a strong negative relationship between family control and the number of CVC deals when board independence is low. This negative relationship disappears, and even turns slightly positive, when board independence is high. Therefore, conditional on CVC program participation during the period, a higher proportion of independent directors on the firm’s board significantly weakens the negative relationship between family control and the number of CVC deals. This evidence supports H3a. On the contrary, in Model 7 (Table 4), the coefficient on the interaction between Family Board Percentage and Board Independence is not significantly different from zero. Figure 3 shows these results graphically.

Predicted Values for the Number of Deals Made by a Firm (Interaction Effect).

Predicted Values for the Number of Deals Made by a Firm (Interaction Effect).

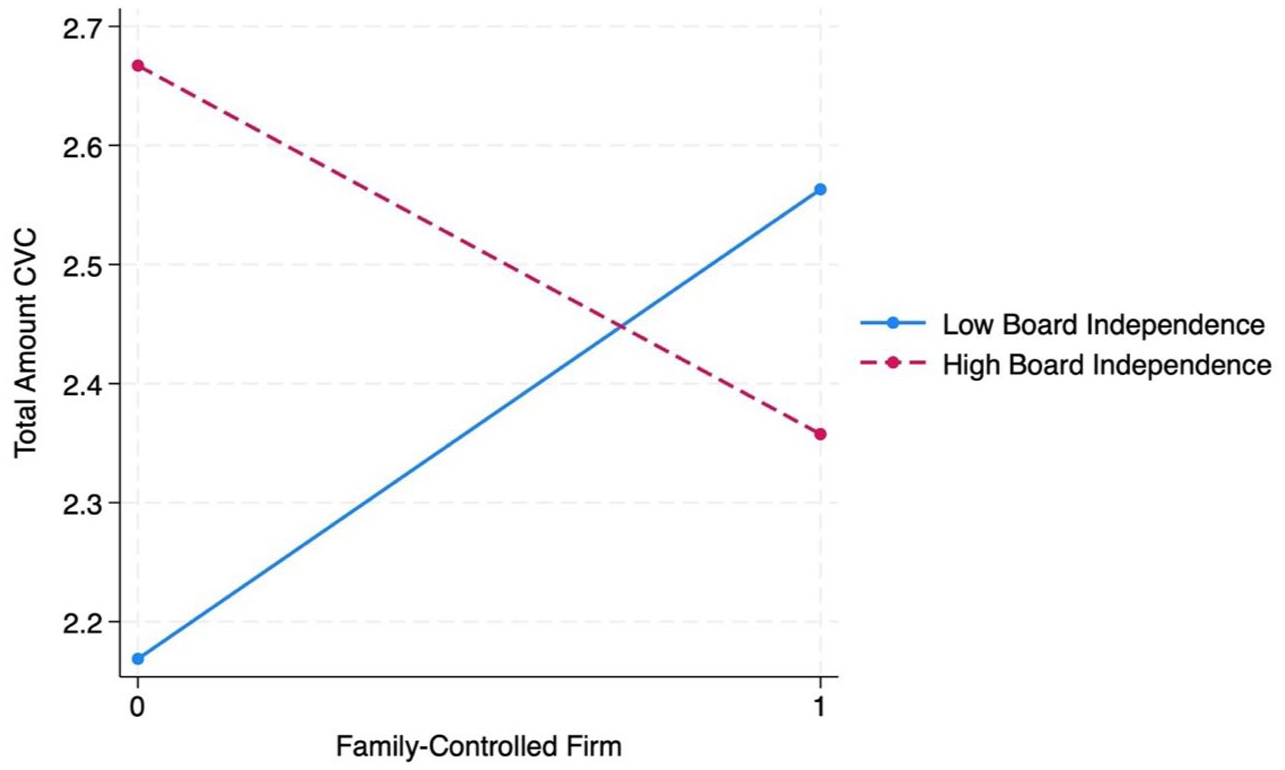

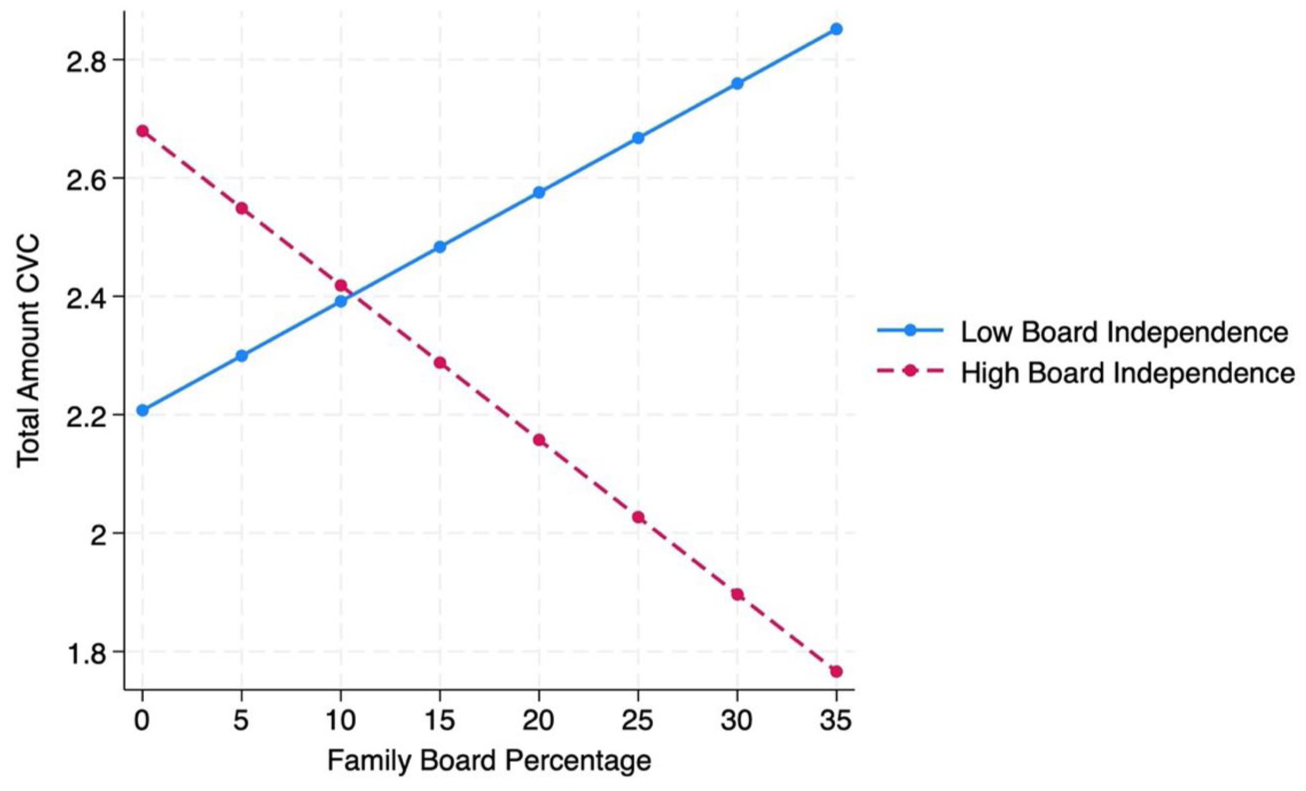

Finally, in Model 11 (Table 5), the coefficient on the interaction between Family-Controlled Firm and Board Independence is negative and significantly different from zero, with a p-value below 0.01. Figure 4 presents these results graphically (Hayes & Montoya, 2017). We can observe that the positive relationship between family control and average deal size disappears when board independence is high. Thus, conditional on CVC program participation during the period, a higher proportion of independent directors on the firm’s board significantly weakens the positive relationship between family control and average investment deal size. H3b is supported. In the case of Family Board Percentage, Model 14 shows a similar effect (Table 5 and Figure 5).

Predicted Values for the Size of CVC Investment Deals Made by a Firm (Interaction Effect).

Predicted Values for the Size of CVC Investment Deals Made by a Firm (Interaction Effect).

Post Hoc Analyses

Total Amount of CVC Investments

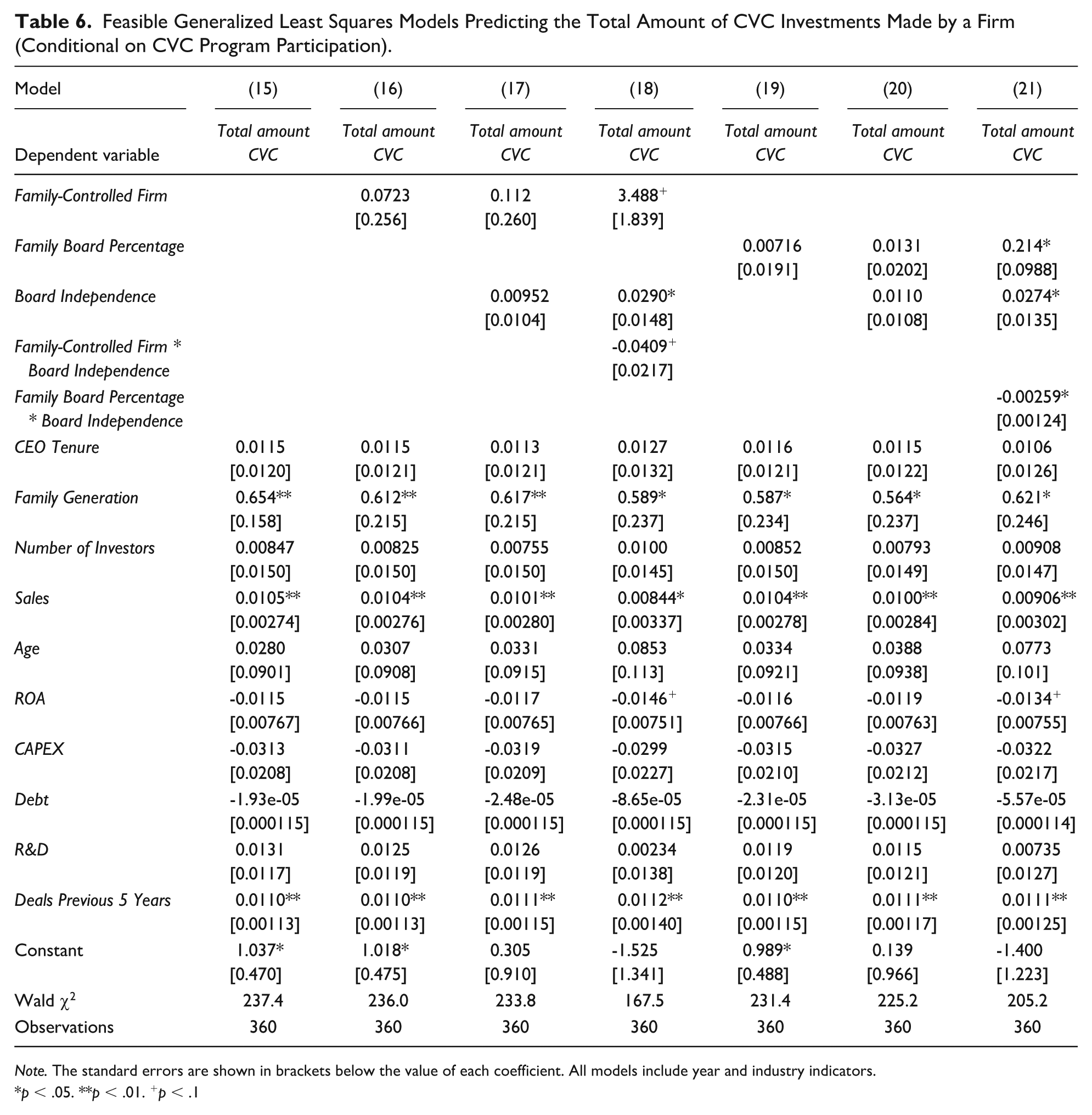

Our hypotheses focus on the number of investments and the average size of each deal. This post hoc analysis examines the total CVC funds invested in a given year. We created the variable Total Amount CVC, which corresponds to the logarithm of the sum of all the funds (in millions of USD) invested by the firm during a year. First, there is no significant impact of being a Family-Controlled Firm on the total amount of CVC funds invested yearly (Model 17, Table 6). Similarly, we found no association between Family Board Percentage and Total Amount CVC (Model 20, Table 6).

Feasible Generalized Least Squares Models Predicting the Total Amount of CVC Investments Made by a Firm (Conditional on CVC Program Participation).

Note. The standard errors are shown in brackets below the value of each coefficient. All models include year and industry indicators.

p < .05. **p < .01. +p < .1

Regarding the moderation effect, the coefficient on the interaction between Family-Controlled Firm and Board Independence is negative, with a p-value of .059 (Model 18, Table 6). Also, as shown in Model 21 (Table 6), the coefficient on the interaction between Family Board Percentage and Board Independence is negative, with a p-value of .037. Figures 6 and 7 show these results graphically. It is interesting to observe that the positive relationship between the variables when board independence is low turns negative when board independence is high. These findings highlight a complex moderating effect of board independence. Future research should explore the underlying drivers of this interaction in greater depth.

Predicted Values for the Total Amount of CVC Investments Made by a Firm (Interaction Effect).

Predicted Values for the Total Amount of CVC Investments Made by a Firm (Interaction Effect).

Investment Stage

As discussed in the Theory and Hypotheses section, H2b—FCFs involved in CVC make, on average, larger CVC deals than non-FCFs—involves two mechanisms. First, FCFs invest larger sums of money per deal to gain greater influence over investees. Second, FCFs prefer to invest in later-stage startups, which typically require larger amounts of funding, to lower the financial risk of their CVC portfolios.

In this post hoc analysis, we more directly assess the second mechanism—FCFs’ preference for later-stage startups. Specifically, we created the dependent variable Investment Stage to measure the average development stage of all firm’s investees in a year. Each investment is scored using the VentureXpert categories: Seed investment (1), Early-stage investment (2), Expansion investment (3), Late-stage investment (4), and Advanced investment (5). This approach allowed us to capture the venture stage preference of the CVC firm.

We do not observe the hypothesized results when using Investment Stage as the dependent variable. Therefore, FCFs’ preference for larger deal sizes appears to be driven by the stronger influence they can exert over investees through large investments, rather than a focus on later-stage startups to mitigate financial risk. We observe a similar situation when we use Family Board Percentage as the independent variable. The corresponding regression results are available in Appendix A.

We conclude that (a) the average deal size and the average development stage of investees should be treated as separate constructs with distinct theoretical implications and (b) the findings associated with H2b appear to be primarily driven by FCFs’ need to exert influence over their investees rather than by a preference for later-stage investments with lower financial risk. Future studies should delve deeper into this line of inquiry.

Lone-Founder Firms

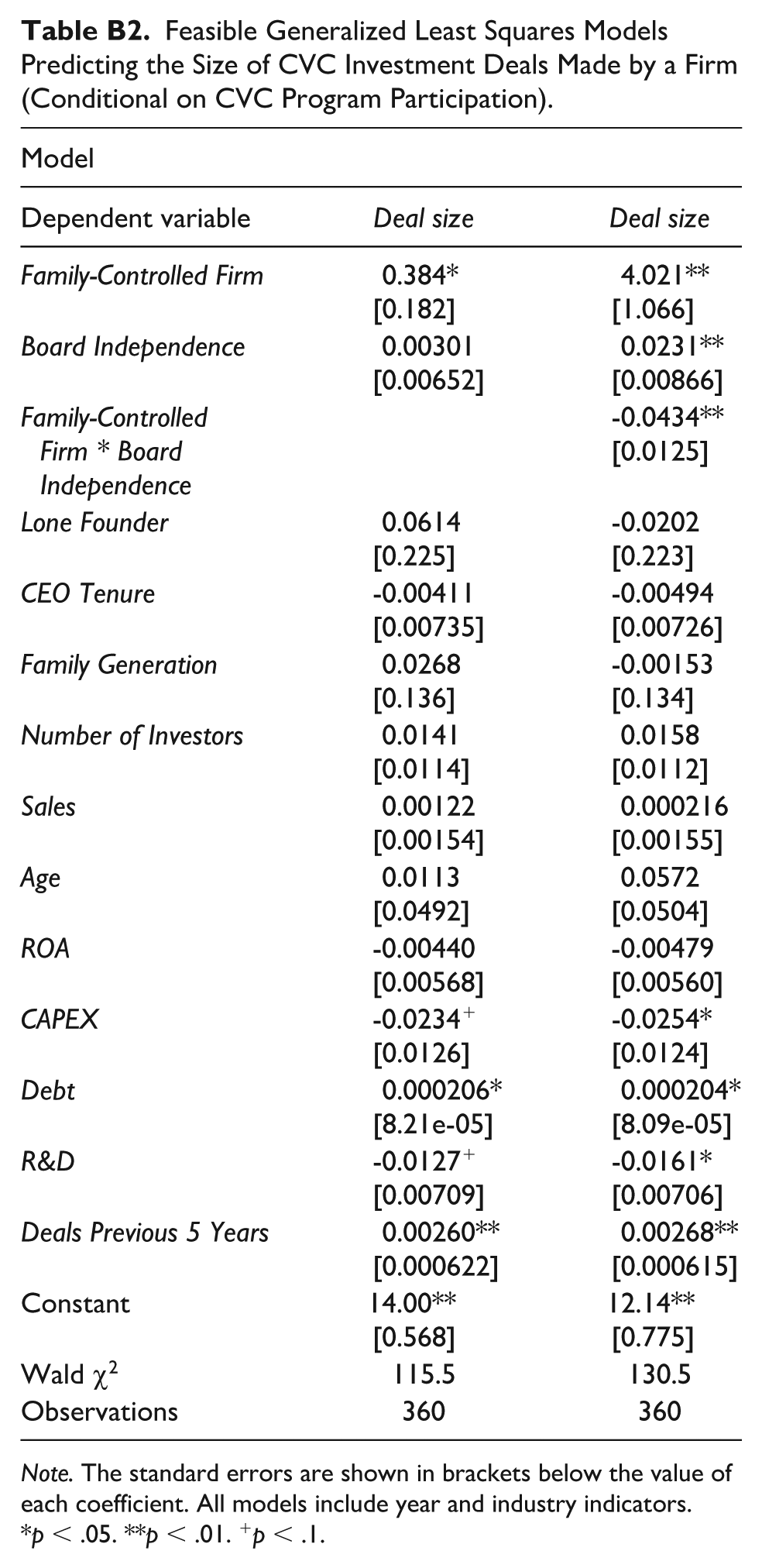

Our definition of FCFs includes lone-founder firms (LFFs). LFFs are those FCFs where the company’s founders are the only family members involved in the firm (Block, 2012; Cannella et al., 2015; Miller et al., 2011). In this post hoc analysis, we replicate the main results while including a variable for the “lone-founder effect.” Adding a variable for this effect separates the lone-founder effect from the main independent variable (Gómez-Mejía et al., 2024). We define Lone Founder as a dummy variable equal to 1 if the FCF is also an LFF and zero otherwise. Our analyses show that when we separate the lone-founder effect, the results are consistent with the main results. Therefore, it seems that FCFs of the lone-founder type are not driving the results we observe. Future research should explore how the CVC investment behavior of FCFs may differ depending on the type of FCF (e.g., multi-family firms; Duran & Ortiz, 2020). The corresponding regression results are available in Tables B1 and B2 (Appendix B).

Family Ownership Stake

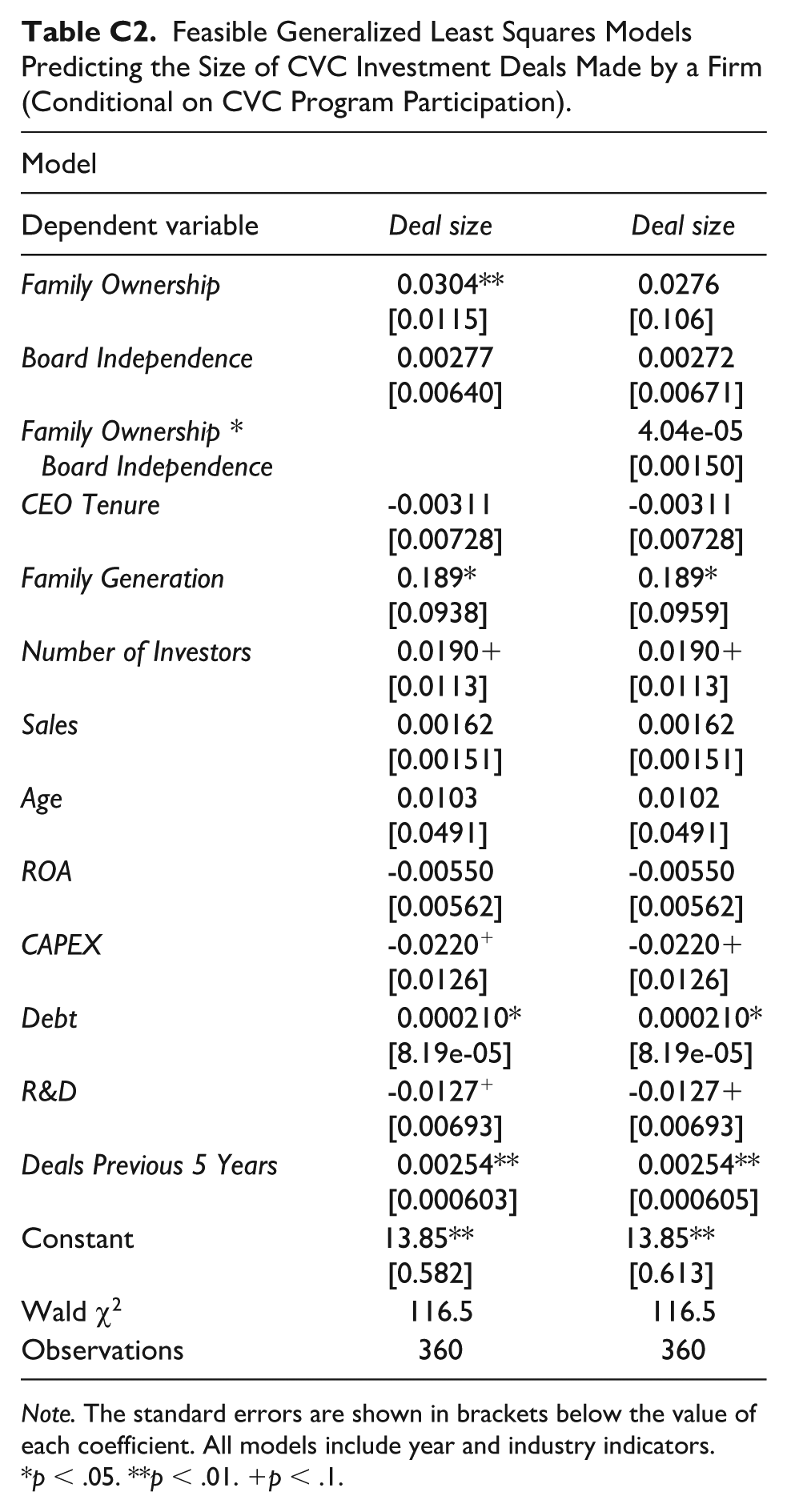

Finally, we conducted a post hoc analysis using the percentage of family ownership as the independent variable. Although our theoretical emphasis is on strategic control and influence over decisions rather than ownership per se, this alternative variable provides a complementary analysis. We do find that higher family ownership levels are associated with fewer CVC deals and larger average deal sizes. However, the moderating role of board independence is not significant. The corresponding regression results are available in Tables C1 and C2 (Appendix C). Although our study focuses on governance-based measures of family influence as independent variables, future work could explore in greater depth the specific role of family ownership in CVC investments. Considering data from smaller firms would be recommended since family ownership percentages can achieve higher levels than in large publicly listed firms, but this will require the development of a theory that is tailored to family ownership.

Discussion

CVC can be an effective and transparent innovation strategy for adopting cutting-edge technologies quickly and efficiently (Guo et al., 2019), and it represents a lower-risk option compared to other strategies with similar goals (Basu et al., 2011). Consequently, there has been an increasing popularity of CVC programs over the last few decades (Eckblad et al., 2019), particularly in large firms competing in technology-intensive sectors (Basu et al., 2011; Dushnitsky & Lenox, 2006). However, not all firms may be equally willing to participate in CVC programs, and those that do may follow different investment strategies. Understanding the underlying reasons that explain such differences is crucial. Although previous literature has examined CVC’s economic and behavioral drivers, ownership structure and control insights have been largely neglected (Drover et al., 2017).

Our research contributes to the literature by offering new insights into FCFs’ CVC strategies. We are unaware of any published study analyzing how FCFs invest in CVC, particularly regarding the quantity and size of the investments. This study draws upon SEW theory to build our arguments, which has been critical in capturing the unique impact of family firms on strategic actions (Davila et al., 2023; Hussinger & Issah, 2019; Nason et al., 2019). SEW theory posits that although adopting risky strategic choices may allow the firm to capitalize on business opportunities (Davila et al., 2023), FCFs generally avoid such initiatives to preserve SEW. Following this perspective, we hypothesized that FCFs in high-technology sectors would be less willing to participate in CVC programs than non-FCFs. More interestingly, we argue that in FCFs involved in CVC programs, the potential fear of losing SEW would make them incur fewer but larger CVC investment deals than their non-FCF counterparts. We suggest that the particular CVC investment behavior of FCFs enables them to maintain their independence from external stakeholders and increase influence and monitoring over their portfolio companies. However, this family-centric behavior may conflict with the interests of non-family shareholders; thus, principal-principal (or secondary agency) conflicts arise (Morck et al., 1988). Finally, we suggest that independent board members can temper the SEW-oriented behavior of FCFs’ decision-makers (Anderson & Reeb, 2003), helping to balance the different perspectives of family and non-family owners on CVC investment strategies.

Our study also contributes to the existing literature on M&As in family firms (e.g., Fuad et al., 2021). In alignment with this work (e.g., Cuevas-Rodríguez et al., 2023; Gómez-Mejía et al., 2018; Schierstedt et al., 2020), our findings indicate that, within the context of CVC, FCFs exhibit a lower likelihood of engaging in investments. Furthermore, FCFs seem to be more discerning in selecting their investment targets than non-FCFs. This underscores the significance of investigating FCFs’ CVC investments as a different strategic avenue for acquiring new technologies (Van de Vrande et al., 2009).

Empirically, we test our arguments using a novel data set of firms listed on the U.S. stock market from three high-technology sectors. First, our results confirm that FCFs (vs. non-FCFs) are less likely to participate in CVC programs. Second, conditional on CVC program participation during the period, even though we find partial support for our prediction of fewer CVC investments by FCFs, we verify that the average size of the CVC deals by FCFs is significantly larger. In addition, when we examine the moderating effect of board independence, we empirically confirm a strong negative relationship between FCFs and the number of CVC deals when board independence is low. Finally, the positive relationship between FCFs-CVC deal size and board independence is particularly strong when board independence is low, and weak when board independence is high.

Our results have significant implications for SEW theory. First, we challenge the notion that SEW theory has limited power to explain FCFs’ behavior in contexts such as the United States (Berrone et al., 2022; Miller et al., 2013). According to Miller and colleagues (2013), U.S.-based FCFs are subject to pressure to avoid SEW objectives and, therefore, are likely to conform to the strategic decisions of non-FCFs. However, our study shows that despite the increasing popularity of CVC programs associated with large firms competing in technology-intensive sectors (Basu et al., 2011; Dushnitsky & Lenox, 2006), FCFs are less likely than non-FCFs to implement CVC programs, and when they do, FCFs pursue a differentiated CVC strategy relative to non-FCFs. Second, we demonstrate how adopting higher levels of board independence can serve as an effective corporate governance mechanism to alleviate FCFs’ SEW-driven CVC behavior. As a result, our study identifies important boundary conditions to the prioritization of SEW that underlie FCFs’ CVC strategy.

Limitations and Directions for Future Research

The first limitation concerns capturing FCFs’ SEW objectives. Berrone et al. (2012) propose the FIBER scale, which reflects five SEW dimensions: (1) family control, (2) identification with the firm, (3) social ties, (4) emotional attachment, and (5) dynastic succession. As in prior research (e.g., Kotlar et al., 2018; Leitterstorf & Rau, 2014; Souder et al., 2017), we proxied SEW using family control in the main models through a dummy variable and the percentage of family members on the board. However, other SEW dimensions may also shape FCFs’ CVC behavior. For instance, FCFs might be more selective on CVC deals due to reputational concerns or value misalignment (Gómez-Mejía et al., 2011). Future research would benefit from directly measuring SEW dimensions using validated scales (e.g., Debicki et al., 2016; Hauck et al., 2016; Naldi et al., 2024) through primary data collection from family firm leaders (e.g., Vandekerkhof et al., 2018). Doing so would allow for a more nuanced assessment of how specific SEW motives (e.g., legacy preservation vs. emotional attachment) influence CVC behavior. In addition, experimental methods (e.g., Lude & Prügl, 2019, 2021) offer a promising approach to explore FCFs’ decision-making under conditions of tradeoffs between economic and SEW goals. These methods can help isolate causality and assess how SEW concerns influence FCFs’ strategic choices, such as VC investment. Finally, alternative proxies from archival data to measure the level of family control over strategic decisions could also be explored in future research. For example, in addition to the percentage of family members on the board, the proportion of family members who are part of the top management team could be a relevant dimension.

As discussed in the post hoc analyses above, we do not find support for H2b when using Investment Stage as the dependent variable, suggesting that FCFs’ preference for larger deal sizes is not motivated by a preference for later-stage startups. Building on this, future research should explore which other target-side characteristics make startups more appealing to FCFs. Drover et al. (2017) note that “the influence of similarity biases is important for understanding how venture capitalists decide whether to invest in specific deals” (p. 1829). Future work could then examine whether FCFs favor startups that share family-related narratives, relational proximity, or geographic closeness (Colombo et al., 2024). Perceived similarity in founding values, management style, or industry background may also foster trust and reduce relational risk (Bruns et al., 2008; Murnieks et al., 2011), potentially increasing the likelihood of investment. Given that FCFs are often guided by SEW considerations, future studies could examine how such non-financial relational cues influence their CVC investment decisions.

Although we include a control variable for family generation using data from NRG, we cannot observe the number of family generations simultaneously active in a firm on a yearly basis. This is an important distinction because the coexistence of multiple generations may influence innovation and strategic risk-taking in family firms. We encourage future research to examine the implications of overlapping generational involvement more directly for CVC investment behavior.

Moreover, several contextual factors may impact the scope of our findings. While our focus is on publicly listed high-tech firms, this approach allows for a more precise observation of governance contingencies. Given their greater agency issues (Miller & Le Breton-Miller, 2006), examining how FCF board independence shapes SEW-driven behavior is theoretically relevant. Another potential extension is to examine CEO duality as another boundary condition (Gove et al., 2017). Empirically, publicly listed firms’ disclosure requirements provide high-quality data to compare CVC behavior across FCFs and non-FCFs while controlling for other influences. Still, we should not overgeneralize our results to all family firms (Duran & Ortiz, 2020). SEW priorities vary across family firm types (e.g., private vs. public, single- vs. multi-family), likely leading to different effects of family control on CVC behavior (Amore et al., 2021; Chua et al., 2012; Duran & Ortiz, 2020; Gómez-Mejía & Herrero, 2022).

Furthermore, in the specific context of innovation in high-tech industries, FCFs may exhibit a greater scientific and procedural rationality, which may curtail the impact of SEW influence on decision-making. Research on FCFs reveals financial parsimony in the context of innovation, particularly through the practice of lean innovation (Carney et al., 2019; Duran et al., 2016). Indeed, in the United States, the prevailing culture of bold, high-tech entrepreneurship may shift FCFs’ reference points (Nason et al., 2019) toward non-FCFs and high-profile entrepreneurs who inspire greater risk-taking. Moreover, our empirical approach overlooks that families may pursue VC through family offices rather than firms (Block et al., 2019). Future research should examine how our findings apply across family firm types and governance structures.

Thus, our findings should be interpreted cautiously, as U.S.-based FCFs may not reflect global contexts. FCFs’ discretion in SEW-based decisions varies with national institutions and societal support for family businesses (Berrone et al., 2022; Duran et al., 2016; Duran et al., 2019). Since institutions also influence VC investments (Bustamante et al., 2021; Mingo et al., 2018), future research should replicate and extend our study using multi-country data. In addition, our study shows that ownership structure shapes CVC strategies, with FCFs and non-FCFs taking distinct approaches to startup investment. Future research could examine other ownership types, such as state-owned enterprises. Like FCFs, state owners pursue financial and non-economic objectives, including social and political goals (Tihanyi et al., 2019). Future work could examine how these goals affect CVC investment strategies.

We show that FCFs follow a distinct CVC strategy, with smaller portfolios and higher resource commitments, aiming to protect SEW through closer oversight and influence over investees. Fulfilling this objective requires higher resource commitments per portfolio company. Going forward, researchers should explore how FCFs monitor startups and transfer “family logic” to them. In addition, scholars could investigate how receptive startups are to receiving investments from FCFs, considering these firms’ desire to influence investee decision-making. These questions can enrich the limited literature on VC governance by highlighting how FCF investments affect monitoring and venture governance (Drover et al., 2017).

Finally, as an empirical limitation, our data set includes three specific industries—information technology, health care, and communication services—and only large firms listed on the U.S. stock market. Even though these industries and firms contribute significantly to CVC investment activity, future studies could examine other economic sectors and non-listed firms. Moreover, it is important to point out that the empirical measures of this study do not assess specific characteristics of the startups receiving CVC investments. Future studies could consider more detailed information about the investees to focus on phenomena at the startup level.

Practical Implications

This study provides practical implications for FCFs, non-family investors, and new ventures in high-technology sectors. First, FCFs’ owners and decision-makers should know how the pursuit of SEW goals impacts their CVC investment strategies. This work can inform family firms’ executives about reconciling the need to invest in CVC with SEW loss aversion. Following the CVC investment behavior of publicly traded firms competing in three technological sectors, we showed that, conditional on CVC program participation, FCFs tend to invest in a relatively smaller number of CVC deals but with a higher resource commitment per deal. This strategy seems to allow FCFs involved in CVC to increase their influence over portfolio companies. Second, our study suggests that non-family shareholders must be aware that FCFs tend to pursue a unique CVC investment approach, which may go against their preferred investment strategy. A higher presence of independent directors on the board can reduce non-family shareholders’ concerns about FCFs’ CVC investment behavior. Finally, this study also offers insights for startups. New ventures that aim to obtain VC financing from established corporations must be aware that not all corporations behave similarly regarding CVC—FCFs may monitor and exert a stronger influence over the venture at levels that may exceed those of non-FCFs.

Footnotes

Appendix A

Feasible Generalized Least Squares Models Predicting the Investment Stage of Deals Made by a Firm (Conditional on CVC Program Participation)

Appendix B

Feasible Generalized Least Squares Models Predicting the Size of CVC Investment Deals Made by a Firm (Conditional on CVC Program Participation).

| Model | ||

|---|---|---|

| Dependent variable | Deal size | Deal size |

| Family-Controlled Firm | 0.384*

[0.182] |

4.021**

[1.066] |

| Board Independence | 0.00301 [0.00652] |

0.0231**

[0.00866] |

| Family-Controlled Firm * Board Independence | -0.0434**

|

|

| Lone Founder | 0.0614 |

-0.0202 |

| CEO Tenure | -0.00411 |

-0.00494 |

| Family Generation | 0.0268 |

-0.00153 |

| Number of Investors | 0.0141 |

0.0158 |

| Sales | 0.00122 |

0.000216 |

| Age | 0.0113 |

0.0572 |

| ROA | -0.00440 |

-0.00479 |

| CAPEX | -0.0234+

|

-0.0254*

|

| Debt | 0.000206*

|

0.000204*

|

| R&D | -0.0127+

|

-0.0161*

|

| Deals Previous 5 Years | 0.00260**

|

0.00268**

|

| Constant | 14.00**

|

12.14**

|

| Wald χ2 | 115.5 | 130.5 |

| Observations | 360 | 360 |

Note. The standard errors are shown in brackets below the value of each coefficient. All models include year and industry indicators.

p < .05. **p < .01. +p < .1.

Appendix C

Feasible Generalized Least Squares Models Predicting the Size of CVC Investment Deals Made by a Firm (Conditional on CVC Program Participation).

| Model | ||

|---|---|---|

| Dependent variable | Deal size | Deal size |

| Family Ownership | 0.0304**

[0.0115] |

0.0276 [0.106] |

| Board Independence | 0.00277 [0.00640] |

0.00272 [0.00671] |

| Family Ownership * Board Independence | 4.04e-05 |

|

| CEO Tenure | -0.00311 |

-0.00311 |

| Family Generation | 0.189*

|

0.189*

|

| Number of Investors | 0.0190+

|

0.0190+

|

| Sales | 0.00162 |

0.00162 |

| Age | 0.0103 |

0.0102 |

| ROA | -0.00550 |

-0.00550 |

| CAPEX | -0.0220+

|

-0.0220+

|

| Debt | 0.000210*

|

0.000210*

|

| R&D | -0.0127+

|

-0.0127+

|

| Deals Previous 5 Years | 0.00254**

|

0.00254**

|

| Constant | 13.85**

|

13.85**

|

| Wald χ2 | 116.5 | 116.5 |

| Observations | 360 | 360 |

Note. The standard errors are shown in brackets below the value of each coefficient. All models include year and industry indicators.

p < .05. **p < .01. +p < .1.

Author Contributions

All authors contributed equally.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding for this work was provided by ANID FONDECYT Regular Folio 1221195.