Abstract

Prior literature establishes a link between family involvement and the firm financial performance. However, the mechanisms through which family involvement in a firm affects its financial performance in different institutional settings are largely unknown. Using an unbalanced panel of 3,322 listed firms from 32 countries over a 9-year period, we find that family involvement in ownership and management on average has negative effects on financial performance. Moreover, the negative effect of family ownership is less profound in countries with good institutional quality. We further find that R&D intensity partially mediates the negative relationship between family involvement and the firm financial performance, but the mediation effect is conditional on the degree of institutional quality in a country. These findings advance the family business, innovation, and institutional literature, and offer important implications for theory and practice.

Introduction

A number of studies highlight the prevalence of firms with family involvement worldwide and view this form of business organization as an important component of capital markets (Burkart et al., 2003; De Massis, Frattini, et al., 2018). Listed firms with family involvement are particularly interesting because managers, often family members and sometimes professional managers, need to deal with very different forces in place, namely the firm’s prosperity, family interests, and public investors’ objectives (Anderson & Reeb, 2004; Chua et al., 2018). These different interests and motivations might be quite diverse or even paradoxical (Kastanakis et al., 2024; Kotlar et al., 2014, 2018), impacting corporate R&D strategies with subsequent implications for financial performance.

Family business’ impact on financial performance occurs through its involvement in ownership and in management (e.g., Chua et al., 2018; Lee, 2006; Poutziouris et al., 2015; Sciascia & Mazzola, 2008) and is largely dependent on the extent to which country-level institutions provide a reliable framework to protect shareholder and minority interests (Berrone et al., 2020; La Porta et al., 2000). In particular, firms with higher family involvement typically have higher market valuations in countries with better institutional quality, where the ability of the controlling family to expropriate nonfamily shareholders and minority investors is rather small (Bozzi et al., 2017; La Porta et al., 2000; Maury, 2006). Although recent studies urge to explain the mechanisms through which the controlling family affects financial performance in countries with different levels of institutional quality (Gedajlovic et al., 2012; Kotlar et al., 2018; Mazzi, 2011; Miller & Le Breton-Miller, 2006; Pinelli et al., 2024; Wagner et al., 2015), little research has been performed, to our best knowledge, to address this research gap. Prior research further suggests that R&D intensity is at the heart of innovative activities for many family firms and represents one of the core drivers of their economic viability (Chrisman et al., 2015; Muñoz-Bullón et al., 2020; Schmid et al., 2014). However, most of existing studies did not consider a direct link between financial performance of family firms and their R&D intensity (Honoré et al., 2015; Muñoz-Bullón & Sanchez-Bueno, 2011; Muñoz-Bullón et al., 2020; Schmid et al., 2014). Therefore, our study aims to answer the aforementioned questions by drawing from the agency and socioemotional wealth (SEW) perspectives to offer a more holistic model that considers how internal and external factors (family involvement, innovation, and institutional context) shape firm financial performance. Specifically, we propose that R&D intensity constitutes a channel through which the degree of family involvement can affect the financial performance of a firm. As there are notable differences in the propensity to invest in R&D between family-owned and family-managed firms in existing literature (Calabrò et al., 2018; Chrisman et al., 2015; De Massis et al., 2012), we pay specific attention to capturing different types of family involvement in a firm (ownership and management) in our study. Moreover, as family firms’ ability to invest in R&D varies substantially between good and weak institutional environments (Hillier et al., 2011; Pindado et al., 2015), we further disentangle the mediating effect of R&D intensity across different institutional environments.

To test our hypotheses, we constructed a unique multi-country panel data set of publicly traded firms across 32 countries over a 9-year period (2007–2015). Using this data set, we analyzed the financial performance of firms with and without family involvement, with a special focus on the R&D intensity as a mechanism through which family involvement in ownership (using the percentage of shares held by a family member and other alternative definitions) and management (in presence of family CEO) affect financial performance in countries with varying degrees of institutional development. In so doing, we contribute to a more nuanced theoretical understanding of potential mediators of the cross-country family business performance (Berrone et al., 2020; Duran et al., 2019).

We also pay attention to family business heterogeneity, an inspirational theme that has a prominent role within family business research (Salvato & Aldrich, 2012; Sharma, 2002; Voordeckers et al., 2014), and institutional heterogeneity, a prominent theme within the international business research (Peng & Jiang, 2010; Torres de Oliveira et al., 2022), through the analysis of the financial performance levels of family-owned firms and family-managed firms in the different institutional contexts where they operate. To mitigate the potential endogeneity of family involvement (Sacristán-Navarro et al., 2011) and survivorship bias (Elton et al., 1996), we exploit the longitudinal nature of our data and use the Heckman’s two-step estimator. In addition, several robustness tests were carried out to rule out possible alternative explanations related to alternative variable definitions and estimation techniques.

We make at least three contributions to the literature. First, while previous research on the determinants of family business performance has studied separately internal (Chua et al., 2018; M. González et al., 2012; Lee, 2006) and external factors (Berrone et al., 2020; Duran et al., 2017, 2019), our study provides a better and more integrated understanding of firm financial performance through the joint consideration of family involvement in the firm, R&D intensity, and institutional context as important internal and external factors driving the firm financial performance. Specifically, our work extends this logic by demonstrating the importance of R&D intensity in understanding why firms with different degrees of family involvement differ in their firm financial performance across countries with varying degrees of institutional quality. To the best of our knowledge, this is the first study to do so.

Second, we contribute to research on innovation management (Calabrò et al., 2018; Kurzhals et al., 2020; Röd, 2016) by providing theoretical and empirical insights about R&D intensity as an antecedent of financial performance of family firms and a more nuanced explanation of the mechanism leading to inferior family business performance internationally. While this stream of literature has largely analyzed the R&D intensity of family and nonfamily firms (Honoré et al., 2015; Muñoz-Bullón & Sanchez-Bueno, 2011; Muñoz-Bullón et al., 2020; Schmid et al., 2014), it has not yet explored how the R&D intensity can alter firm financial performance of listed family and nonfamily firms in countries with varying degrees of institutional quality.

Third, we provide insights into the role of institutional quality for financial performance, thus contributing to research on institutional theory (North, 1991; Peng et al., 2009) and R&D intensity in countries with varying levels of institutional quality (Hillier et al., 2011; Seifert & Gonenc, 2011). By revealing the significant mechanism that drives the financial performance of different types of firms with family involvement across countries with varying degrees of institutional quality, we also provide relevant insights for owners, managers, advisors of firms with family involvement, and for policymakers.

Theory and Hypotheses

Family goals and vision (Chua et al., 1999) are highly correlated with the extent of family involvement in ownership and management (Chrisman et al., 2012; Patel & Chrisman, 2014). We present two opposing sets of arguments concerning the financial performance of firms with family involvement in ownership and management drawn from two popular perspectives—namely agency and SEW perspectives. We refer to these theoretical perspectives as they surface negative and also positive views of firms with family involvement that tie in closely with both principal–principal agency and nonfinancial wealth (Gómez-Mejía, et al., 2007; Le Breton-Miller & Miller, 2018).

Inferior Financial Performance of Firms With Family Involvement: The Negative View

Firms with higher family involvement are usually considered to be risk-averse and less willing to break away from their old ways of doing business, thus limiting organizational resources and capabilities available for achieving extraordinary financial performance (Chrisman et al., 2015; De Massis, Frattini, & Lichtenthaler, 2013). When the controlling family is increasingly involved either via ownership or management in publicly listed firms, there may be a set of negative forces at work that limit these firms’ potential to outperform their nonfamily counterparts. First, prior research shows that family firms experience significant principal–principal agency costs, as family members, particularly in listed firms, extract private benefits from the business (Morck & Yeung, 2003; Schulze et al., 2002; Schulze et al., 2001; Singla et al., 2014; Villalonga & Amit, 2006). Private benefits take various forms, including paying special dividends to the controlling family, favoring family members for managerial positions over nonfamily candidates, creating highly remunerated jobs for the offspring, and using control-enhancing mechanisms (Bertrand & Schoar, 2006; Masulis et al., 2011; Pérez-González, 2006).

Moreover, having several family members at the helm of a family business can be particularly harmful as they may keep their jobs despite incompetence (Claessens et al., 2002). In firms with a higher degree of family ownership, control may be diluted through ownership dispersion among family members (De Massis, Kotlar, et al., 2013), making relational conflicts even more likely (Eddleston et al., 2008; Gersick et al., 1997). The aforementioned principal–principal agency costs demolish the organizational resources available to the firm to achieve extraordinary financial performance.

Second, poor management and incentive practices become more pronounced as family involvement increases (Bloom et al., 2011), which reduces productivity and growth. Thus, financial performance can be destroyed when an increasing number of family members are in charge, particularly in multigenerational firms (Bennedsen et al., 2007; Cucculelli & Micucci, 2008; Villalonga & Amit, 2006). Third, in multigenerational firms with increasing family involvement, varying preferences among family branches or relatives may fuel conflicting or self-serving goals (Kammerlander & Ganter, 2014; Kotlar & De Massis, 2013). Again, this can impede financial performance. Finally, next to their financial goals, family owners and managers have strong family-centered nonfinancial goals that lead them to value business survival over the firm’s wealth maximization and that they see their firm as a precious asset to be handed over to the next generation (Chrisman & Patel, 2012; Gómez-Mejía et al., 2007).

By following their nonfinancial goals, which stem from the emotional ties between the family and the business, firms with higher family involvement accumulate socioemotional wealth (SEW) that, in turn, can have detrimental consequences for financial performance (Cruz et al., 2012). As a result, as the level of family involvement increases, firms often place greater emphasis on pursuing their nonfinancial goals and thus aim to preserve their SEW rather than achieve financial gains (Berrone et al., 2012; Chrisman et al., 2012; Sciascia et al., 2015). This tricky goal trade-off might become even more relevant when we turn our attention to how financial performance is perceived by investors on the stock market.

Superior Financial Performance of Firms With Family Involvement: The Positive View

Some research argues that firms with higher levels of family involvement are characterized by a close connection between the controlling family and the business as well as intimate social relationships, particularly within their owning family (Carr et al., 2010; Zellweger et al., 2018). Given that learning arises in the interactions in social relationships where (tacit) knowledge can be shared and leveraged, firms with higher family involvement are thus particularly receptive to extraordinary organizational learning (Chirico & Salvato, 2016; Patel & Fiet, 2011) that can potentially lead to the above-average financial performance. In addition, as the degree of family involvement increases, the family often has a higher incentive to contribute their knowledge to the continuation of their company because their economic and noneconomic wealth is concentrated therein (Zellweger et al., 2012, 2013). If its business fails in a changed environment and if the aim to engage in transgenerational entrepreneurship cannot be pursued further, there is much more to lose for the owning family than other (nonfamily) shareholders or managers (Chrisman et al., 2015; Kammerlander & Ganter, 2014).

A Quandary

Clearly, the principal–principal agency and SEW perspectives lead to opposite conclusions regarding the financial performance of firms with varying degrees of family involvement. Moreover, the empirical findings to date are mixed. While a number of studies find that financial value is destroyed by increasing family involvement in ownership and management (Claessens et al., 2002; King & Santor, 2008; Lins, 2003; Oswald et al., 2009; Pérez-González, 2006), some others find the opposite (Anderson & Reeb, 2003; Lee, 2006), and others report no differences between financial performance of nonfamily and firms with family involvement (Martínez et al., 2007; Singal & Singal, 2011).

Although some firms with higher family involvement can potentially demonstrate extraordinary financial performance thanks to their unique organizational learning, we argue that, on average, as family involvement in ownership or management increases, is likely to deteriorate financial performance of a listed firm due to the prioritization of nonfinancial goals (Gómez-Mejía et al., 2007), lack of appropriate business skills (Cruz et al., 2012; Pérez-González, 2006), possible incompetence (Bennedsen et al., 2007; Villalonga & Amit, 2006), presence of conflicts (Pérez-González, 2006), or weak management and incentive practices (Bloom et al., 2011), associated with the family’s involvement stake. Furthermore, in the context of listed family versus nonfamily firms, the controlling families often adopt the control-enhancing mechanisms including dual-class stock, pyramidal structure, or disproportionate board representation, among others, to exercise stronger control over a firm (Amit & Villalonga, 2020). These control-enhancing mechanisms, in turn, have been shown to negatively affect firm financial performance (Heitor & Daniel, 2006; Masulis et al., 2011). Therefore,

Institutional Quality, Family Involvement, and Firm Financial Performance

Whereas H1a and Hb predict negative effects of the degree of family involvement in ownership and management on firm financial performance globally, the institutional quality may have an important moderating effect in line with the institution-based view of firm financial performance (Peng & Jiang, 2010; Peng et al., 2009).

Like other firms, firms with higher family involvement do not operate in a vacuum but are embedded in, and influenced by, the institutions (North, 1991). Such institutions are commonly associated with being the formal and informal rule-makers, which provide structures (Scott, 2013) and limit opportunism behavior (North, 1991). Firms within a specific formal institutions tend to behave similarly because they comply with like structures and rules (DiMaggio & Powell, 1983), whereas distinct institutions foster diverse arrangements, namely their business systems, which impact organizations (C. González & González-Galindo, 2022; Torres de Oliveira & Figueira, 2019; Whitley, 1999). Furthermore, the effect of higher family involvement in ownership and management on firm financial performance can vary as a function of the country’s institutional quality (Pindado & Requejo, 2015). Specifically, higher family involvement can bring higher financial value in countries with better institutional quality, where the controlling family has lower opportunities for extracting private benefits of control (Barontini & Caprio, 2006; Maury, 2006), protection of minority shareholders is high (Bozzi et al., 2017; La Porta et al., 2000) and strong exercise of public power to prevent corruption is in place (Amore & Bennedsen, 2013). In fact, a systematic review of more than 300 empirical papers on family business performance by Pindado and Requejo (2015) suggests that drawbacks of higher family involvement for firm financial performance can be substantially lower in countries with better institutional quality, as compared to countries with weak institutional quality.

Family firms may have to share part of the uncertainty and associated risks of weak institutional quality with family members and their employees to operate profitably in that environment or just to remain viable as a going concern. This is likely to translate into lower SEW for the controlling family, as operating costs may have to be adjusted as needed to compensate for unexpected changes in the country-level institutional environment (for instance, a sudden political instability or a drop in the speed of pro-market reforms). When top government officials are not bound by publicly recognized procedures or laws, the controlling family cannot be confident that their investment will not be expropriated or rendered valueless through abrupt changes in economic policy. The financial performance disadvantages of firms with family involvement versus nonfamily firms could be magnified in weak institutional environments. In contrast, countries with more effective public and economic policies, and long-term government commitments to their policy promises, are likely to be more conducive to family investments in their business prosperity (Crouzet, 1999).

Our core thesis is that country-level institutional quality including government effectiveness, regulatory quality, rule of law, and financial system may have a profound effect on the financial performance of firms with varying degrees of family involvement. In particular, it can limit the tendency of controlling family owners and executives to extract private resources to the disadvantage of other shareholders due to weak law enforcement, making higher financial gains more likely. Moreover, countries with better institutional quality have more sophisticated financial markets (La Porta et al., 2000) and financial intermediaries (Levine et al., 2000), as they promote better monitoring and mitigate information asymmetries between firms and investors (Dittmar et al., 2003; Giannetti, 2003). Investments of family business owners and managers are also less likely to be expropriated or rendered valueless in countries with sound institutional quality. In such countries, we expect that firms with higher family involvement, that frequently prioritize nonfinancial goals and principal–principal, will be less subject to such disadvantages, and thus the negative impact of higher family involvement on financial performance will be lower, as compared to countries with weak institutional quality.

The Mediation Effect of R&D Intensity

R&D intensity is an important driver of durable competitive advantage (Lengnick-Hall, 1992; Sirmon et al., 2007), and of extraordinary firm financial performance (Artz et al., 2010; Pindado et al., 2015). According to the seminal argument of Schumpeter (1934), the process of creative destruction is driven by large firms that possess excess financial resources for R&D activities (Alonso-Borrego & Forcadell, 2010). It is a prerequisite for a listed firm for the creation of new knowledge and to meet the ever-changing technological demands of customers (Chan et al., 2001; Del Monte & Papagni, 2003). However, at the same time, these are also risky investments as their outcomes are largely uncertain and can pay off only in the long term (Hall, 2002).

In contrast to nonfamily firms, as the family involvement increases, the family ties their financial wealth solely to their most precious asset, namely the family business itself (Anderson & Reeb, 2003), leading mostly to the pursuit of family-centered nonfinancial goals undermining their R&D activities (De Massis et al., 2016; König et al., 2013). Their goals are less focused on firm financial performance and growth via the development of new products and services as frequently they do not want to lose control (Gómez-Mejía et al., 2007). Some research further suggests that R&D intensity is low in firms with higher family involvement because their tolerable risks are lower when compared with nonfamily firms as their main strategy—which is to survive—plays out over multiple generations (Kotlar & De Massis, 2013). Family owners and managers are very concerned and cautious when it comes to their financial wealth aiming to survive in the long run without any substantive changes (Chang et al., 2010; Naldi et al., 2007), particularly neglecting risky and uncertain investments in R&D. In addition, family owners and managers often block costly and resource-intensive R&D projects as they are reluctant when it comes to attracting external financial resources (Gallo et al., 2004).

We argue that R&D intensity represents one of the potential mechanisms that can explain the lower financial performance of listed firms with higher family involvement, as compared with the financial performance of listed nonfamily firms. This is particularly the case because higher family involvement in the firm translates into under-investment in R&D (“innovation reluctance”; Muñoz-Bullón & Sanchez-Bueno, 2011), a channel through which higher family involvement hampers firm financial performance. As family owners and managers are concerned with protecting not only their financial wealth but also their SEW (Gómez-Mejía et al., 2007; Kempers et al., 2019), they are more likely to use their discretion to avoid excessive investment risks and uncertain payoffs, and one way to accomplish this is to aggressively cut corporate R&D projects at will. R&D costs are typically one of the largest single operating expenses in a firm, and reducing these costs as needed is a financial shield to counter uncertainty. Accordingly, drawing on the previously theorized links between family involvement and R&D intensity, on one hand, and R&D intensity and firm financial performance, on the other, we argue that R&D intensity—in particular, the amount of financial resources spent by a firm on R&D over its revenue—is a mechanism through which higher family involvement in ownership and management negatively affects firm financial performance. Thus, we expect R&D intensity to act as a mediator in the relationship between family involvement and firm financial performance.

The Mediation Effect of R&D Intensity in Countries With Varying Degrees of Institutional Quality

We further theorize that firms with higher family involvement will conduct more effective R&D in countries with good institutional quality and, thereby, the negative impact of higher family involvement on firm financial performance will be lower in those countries, as compared with firms operating in countries with weak institutional quality. Specifically, institutional quality, “the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development” (Kaufmann et al., 2011, p. 223), positively impacts how family involvement in a firm perceives and is willing to invest in R&D. For instance, countries with good institutional quality have better intellectual property protection and such institutional environment incentivizes firms with higher family involvement to invest more in R&D compared with the same firm in countries with weak institutional quality. In addition, countries with better institutional quality foster the emergence of business networks (Oxley, 1999) and the use of open (H. W. Chesbrough, 2003) and collaborative (Feranita et al., 2017) innovation approaches, which are likely to have positive implications for R&D intensity-firm financial performance of firms with higher family involvement. As value creation is a consequence of innovation that emerges from R&D in firms with higher family involvement (Hillier et al., 2011), good institutional quality represents a critical factor for these firms’ improved financial performance. The classic examples are firms like Bosch, a German family firm that has large and highly intensive R&D centers in high-institutional-quality countries, such as the United States and Germany, but only minor (and mainly focused on local adaptation) R&D centers in low-institutionalized-quality countries (Bosch, 2020).

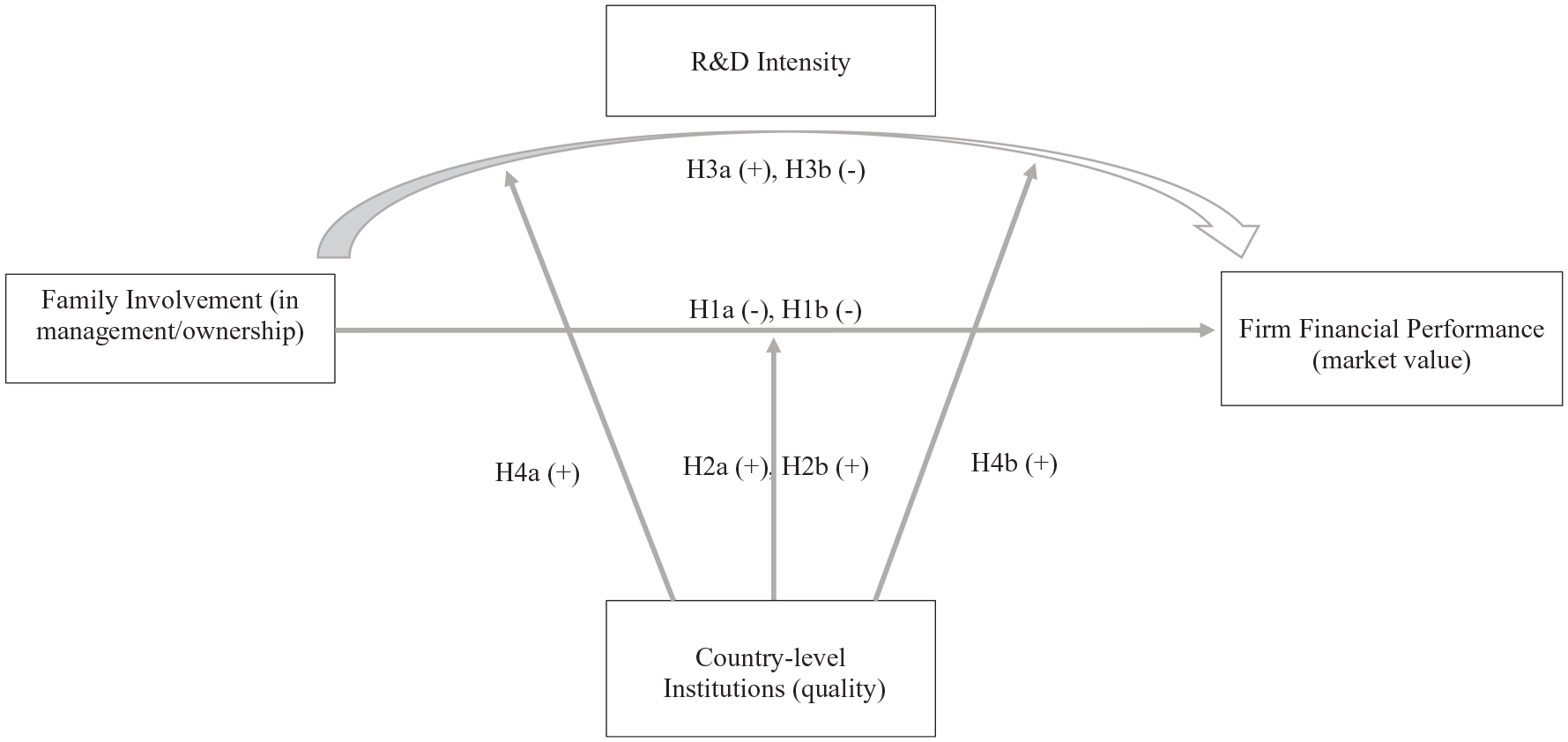

The hypothesized relationships are illustrated in Figure 1.

Conceptual Model

Method and Data

Data and Sample

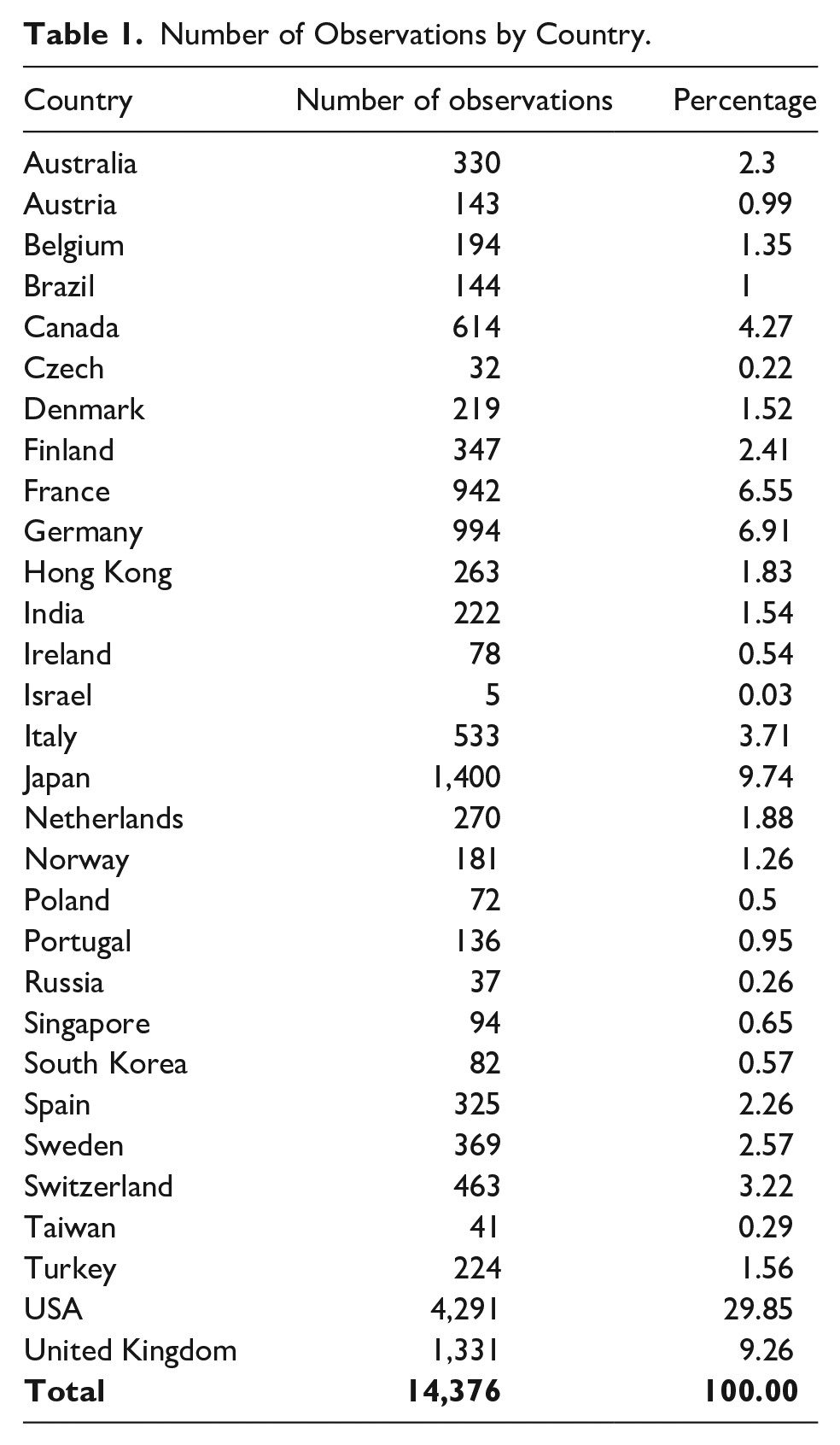

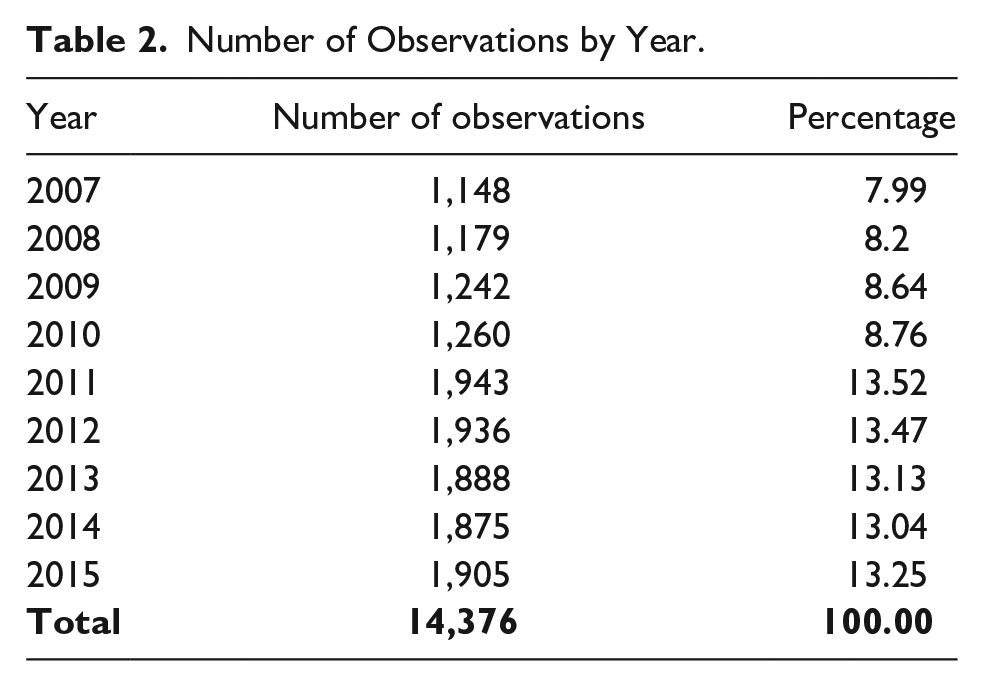

We tested our hypotheses using a comprehensive firm- and country-level data set of publicly traded firms, including both firms with family involvement and those without such involvement. We collected data from multiple sources, including NRG Metrics, Thomson Reuters Eikon, the World Bank, and the Worldwide Governance Indicators (WGI). While the first two databases provided us with firm-level information, such as financial performance, family involvement, and operating industries, we extracted country-level data, including institutional quality and gross domestic product (GDP) per capita from the latter two. Finally, our sample covers 23,141 observations of publicly traded firms with and without family involvement in 32 OECD (Organisation for Economic Co-operation and Development) countries over a 9-year period (2007–2015). Tables 1 and 2 illustrate the number of observations per country and year. That said, our final analysis only had 14,376 observations because the information on variables was not available for all businesses.

Number of Observations by Country.

Number of Observations by Year.

In our sample, the majority of firms were located in the United States (26.35%), followed by the United Kingdom (9.04%), Germany (6.94%), Japan (6.8%), and France (5.07%). There were only a few firms in the Czech Republic, Croatia, and Israel. With regard to yearly distribution, our sample showed an increase in recent waves from around 8% prior to 2010 to nearly 14% in the 2015 round.

Our sample provides us with a good research laboratory in several ways. First, we cover 32 OECD countries (out of 38 country members of the OECD) capturing a large concentration of wealth globally, thus offering strong sample representativeness and high cross-country variation in institutional quality. Second, our sample has an unbalanced structure allowing us to mitigate the survivorship bias problem (Elton et al., 1996). Moreover, its focus on listed firms allows us to analyze a homogeneous cluster of firms because private firms have different strategic goals and financial performance outcomes (Carney et al., 2015). Third, we cover the period of the global financial crisis (2007–2009) and the period of macroeconomic stability (2010–2015) during our study period allowing us to trace the financial performance of our sampled firms across different business cycles.

Measures

Dependent Variable

The financial performance variable was measured using Tobin’s Q. These data were collected from the Thomson Reuters Eikon database. Tobin’s Q represents a firm’s market value to the replacement cost of its assets (Morck et al., 1988). It is a market indicator of financial performance that has the advantage of being less vulnerable to accounting misrepresentations because it relies on stock market values instead of potentially accounting-based measures (such as return on assets, which managers may be able to manipulate; Srivastava et al., 1998), and by incorporating not only current but also future profitability—market valuation of future cash flow (Montgomery & Wernerfelt, 1988). Thus, Tobin’s Q captures a firm’s market value that incorporates not only tangible but also unmeasured intangible assets (Bharadwaj et al., 1999; E. Fang et al., 2008). This market value approach is appropriate to measure the financial performance of our listed firms in correlation with R&D intensity (Hussinger & Pacher, 2019; Sandner & Block, 2011).

Independent Variable

We investigated two types of family involvement. First, we measured the variable family management with a dummy variable that received the value 1 if the CEO is either the founder or a member of the founder’s family, such as a CEO-descendant (Schmid et al., 2014; Scholes et al., 2021). Second, we measured the variable family ownership as the percentage of shares held by a family member (Matzler et al., 2015; Memili et al., 2018). Both variables, family management and family ownership, were drawn from the NRG Dataset. 1

Mediation Variable

We measured R&D intensity, the mediator variable in our model, as the ratio of R&D expenditures over total revenue (Coad, 2019). This variable was drawn from the Thomson Reuters Eikon database.

Moderation Variable

To assess the institutional quality in our cross-country study, we focused on country differences in regulatory quality, reflecting “the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development” (Kaufmann et al., 2011, p. 223). The data were collected from the WGI; the World Bank aggregates six dimensions, for example, government effectiveness, regulatory quality, rule of law, and control of corruption, and uses diverse respondents (enterprises, citizens, and experts in a country), thus representing the quality of regulatory mechanisms in that country (Schneider et al., 2010).

Control Variables

We included various firm-level control variables: size, age, industry, and state ownership as controls in our model. Firm size was integrated as large firms have more resources to invest in profit-generating business activities such as R&D and thereby are more likely to gain better returns (Jiménez-Jiménez & Sanz-Valle, 2011). According to the literature, firm age can have a positive impact on financial performance as firms increase their experience as they mature (H. C. Fang et al., 2021). With regard to industry, we included this commonly used control variable as the literature shows a variance in financial performance across the industries in which firms operate (Belderbos et al., 2004). We also control for state ownership given its negative impact on firm financial performance (Wei & Varela, 2003).

In our study, firm size was measured using the number of employees (Tojeiro-Rivero & Moreno, 2019), whereas firm age was measured using years of trading since the establishment (Di Cintio et al., 2017). We coded the industry variable with nine dummies—basic materials, consumer goods, consumer services, health care, industrials, oil and gas, technology, telecommunication, and utilities—following the Global Industry Classification Standard (Arouri & Nguyen, 2010). The state ownership variable was measured using the share of the state owner (Sami et al., 2011). We collected information on these variables from the Thomson Reuters Eikon database.

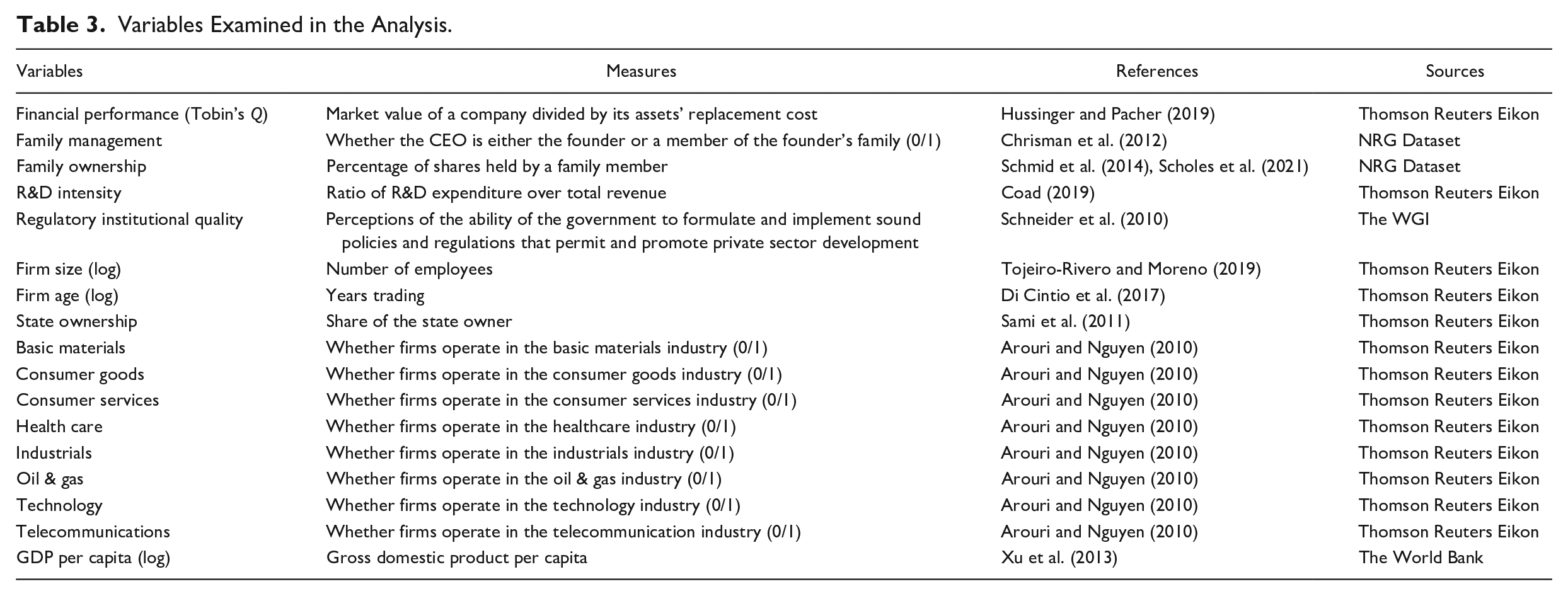

Following Xu et al. (2013), we also included various country-level control variables. In our study, we have 23,141 observations spreading across 32 OECD countries over a 9-year period. The observations mostly come from the big five countries (the United States, the United Kingdom, Germany, Japan, and France), whereas others such as the Czech Republic, Croatia, and Israel only have a few firms in the sample. Using dummy variables for all countries would not be statistically sufficient with those small observations and, more importantly, would not capture the dynamics of the business environment in these countries. Consequently, with regard to the country-level control variables, the GDP per capita was integrated into the estimation model to control for the dynamic difference between countries in our analysis. We extracted the information about GDP per capita from the World Bank database (World Bank, 2019). We included the GDP per capita because firms operating in high-income countries seem to have fewer constraints in accessing financial resources than those in lower-income countries, which influences firm financial performance (Xu et al., 2013). Consequently, it enabled us to better control for the differences among countries rather than using country dummy variables. For analysis purposes, we used log-transformed variables to deal with the skewness of Tobin’s Q, firm size, age, R&D intensity, GDP per capita, and regulatory score (Feng et al., 2014). Table 3 summarizes the variables used in the analyses.

Variables Examined in the Analysis.

Econometric Model

Given that our data were organized in a hierarchical structure which consists of firm and time (year) levels, we tested whether there was a presence of multilevel effect in our data by first calculating the intraclass correlation (ICC; Hox, 2010). The ICC value showed that 78% of the variation in firm financial performance is attributable to the difference between firms. This is significant, as shown by the chi-square test (p < .01), which also means that 22% of the variation is due to change over time. We then run a likelihood ratio test, and the test statistic is 495 with one degree of freedom, indicating a statistical significance. Taken together, we can say there is between-time variance; in other words, the presence of a multilevel effect (Goldstein, 2011).

The presence of a multilevel effect suggested that we needed to apply multilevel regression to test our hypotheses. In addition, the number of firms per year (time level) in the data is at least 375 in the year 2007, which is much higher than the suggested number of 30 (Hox, 2010), ensuring the robustness of the multilevel analysis. We used a mixed command in Stata 16.0 to run the regression. The moderated mediation model was tested using the bootstrapping technique with 500 replications (Preacher & Hayes, 2008) and the ml_mediation command in Stata 16.0 (Sieweke & Zhao, 2015) following the guidelines of MacKinnon et al. (2007) and Muller et al. (2005).

Bias Testing

In the study, we only included firms with information about all variables used; thus, we excluded firms that had missing values, raising concerns about selection bias. We dealt with this issue by including the inverse Mills ratio as a selection parameter in our estimation (Certo et al., 2016). The inverse Mills ratio was calculated from an equation estimating the probability of an observation entering our sample.

Firm performance is attributed not only to family involvement, R&D intensity, and institutional quality but also to other factors that were not captured in this study, such as managerial capabilities, customers, and market segment. This, together with the reverse causality problem, might lead to an estimation bias. We applied several approaches to deal with this endogeneity problem. First, we included widely used control variables in the estimation, namely firm size, age, and industry (Reeb et al., 2012). Second, we employed a time-lagged effect on the dependent and mediation variables (Triana et al., 2019) that family involvement variables were collected on time t-2, the R&D intensity variable on time t-1, and the remaining variables on time t. Third, we applied Heckman’s two-step selection multilevel modeling (Heckman, 1979).

Results

Descriptive Analysis

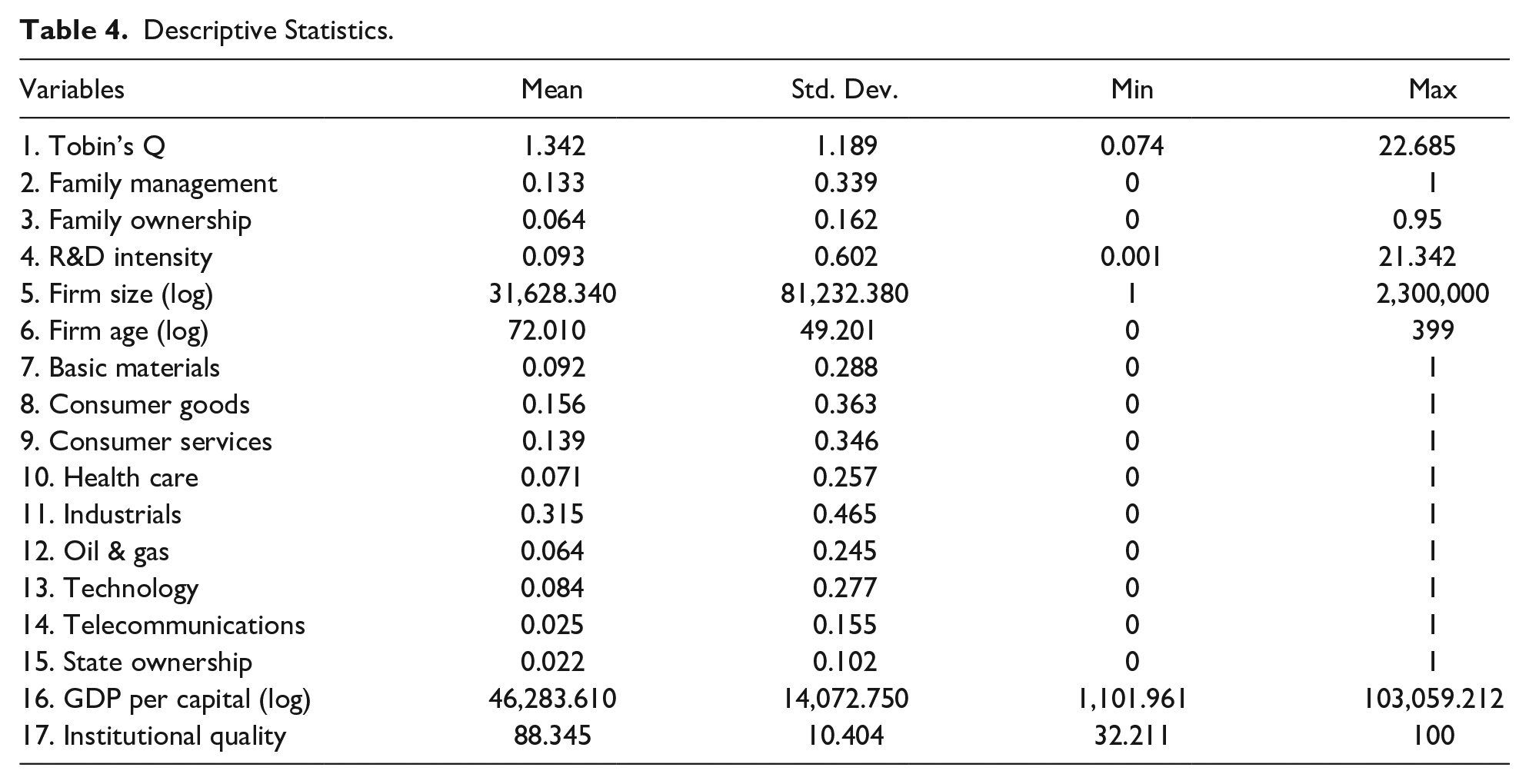

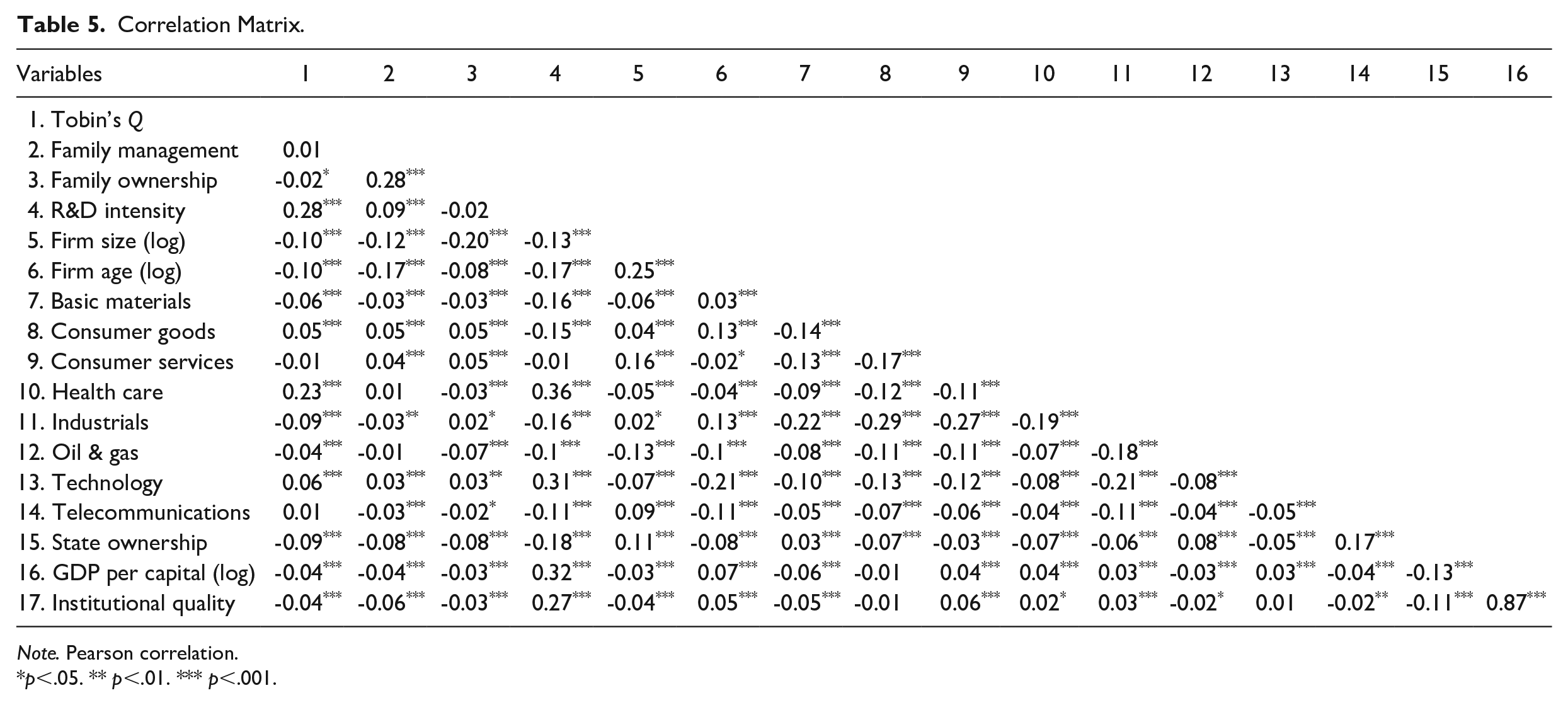

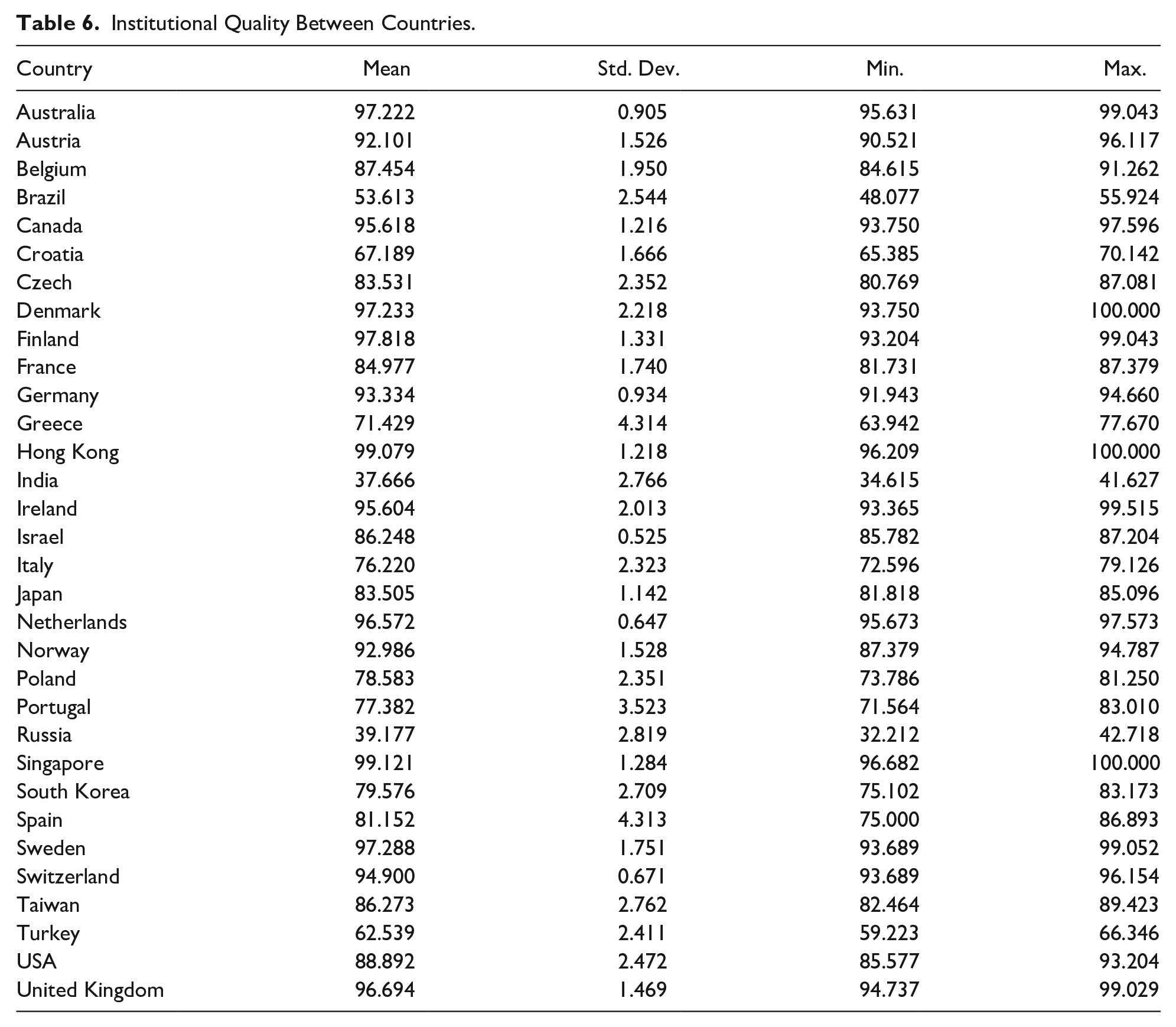

Tables 4 and 5 summarize the descriptive statistics of the variables used in the analysis. The typical firm in our sample is quite large and mature (sample average of 31,600 employees and 72 years of firm age). The firms operate in a diverse range of industries, with the majority of firms operating in manufacturing industrial products (31.5%), consumer goods (15.6%), consumer services (13.9%), basic materials (9.2%), and technology (8.4%). The involvement of the state in the ownership of these firms, as shown in the share of this owner type, is quite low at only 2.2% on average. Thirteen percent of firms in our sample have a CEO who is either the founder or a member of the founder’s family, and the family share accounts for more than 10% in around 31% of firms. The R&D intensity is at 9.3% on average—similar to other studies on OECD firms (Science, 2017). The institutional quality is good, with a mean score of 88 out of 100 (see more detail in Table 6). As expected, there are significant correlations between dependent, independent, mediation, moderating, and control variables, indicating the statistical rationale of our study. We also performed a simple comparative analysis between regions, and we found that family business in the European Union and the like (the United Kingdom, Germany, France, Italy, etc.) had lower performance compared with their U.S. counterparts. On the other hand, family business in Asia countries (Japan, Singapore, South Korea, etc.) outperformed the U.S. family business.

Descriptive Statistics.

Correlation Matrix.

Note. Pearson correlation.

p<.05. ** p<.01. *** p<.001.

Institutional Quality Between Countries.

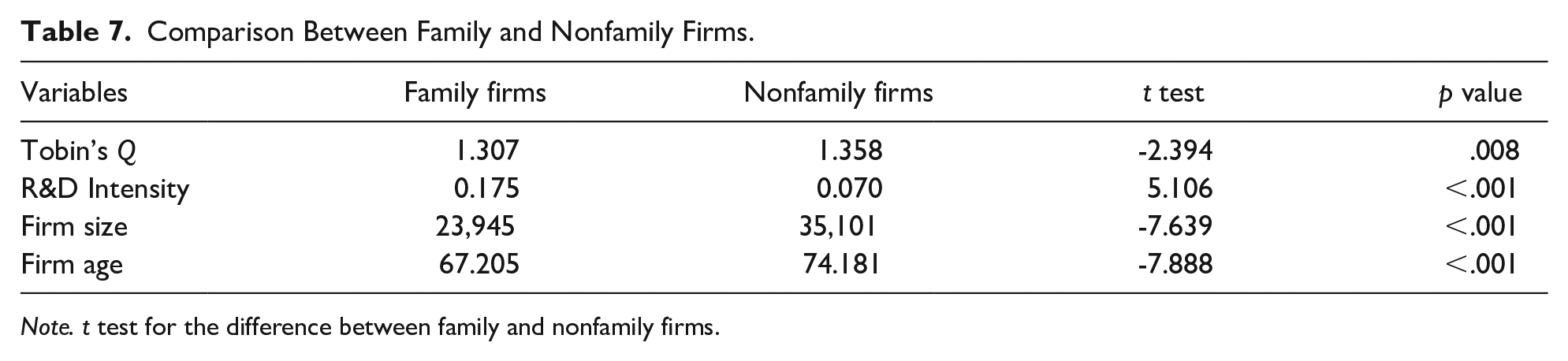

We also explored whether there are significant differences between firms with and without family involvement in our main variables. The results in Table 7 confirm that firms with family involvement have significantly smaller size in terms of number of employees (23,945 employees versus 35,101) and younger (67 years compared with 74 years). However, they tend to invest more in R&D activity but do not financial performance as well as their nonfamily counterparts.

Comparison Between Family and Nonfamily Firms.

Note. t test for the difference between family and nonfamily firms.

Regression Analysis

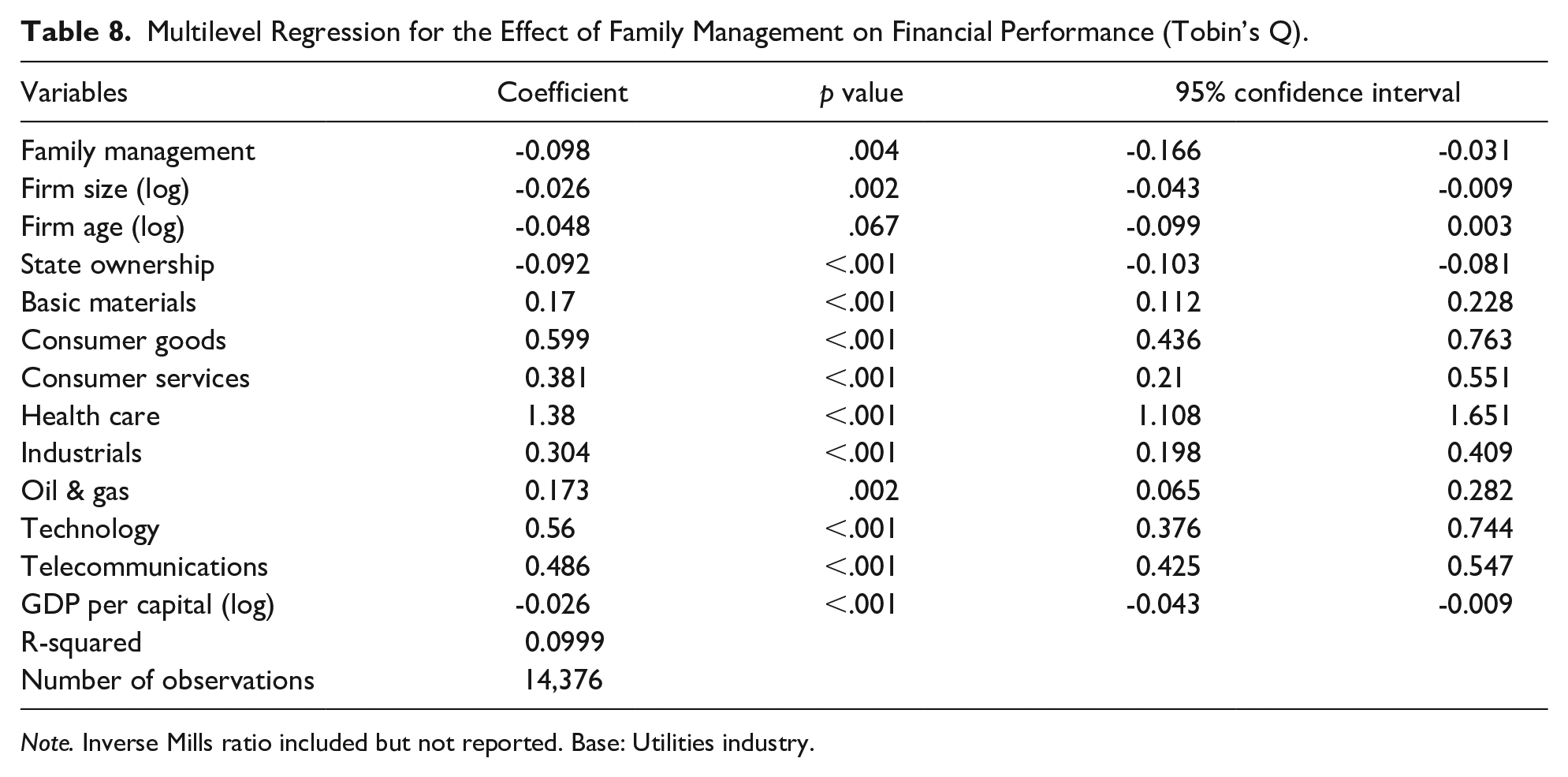

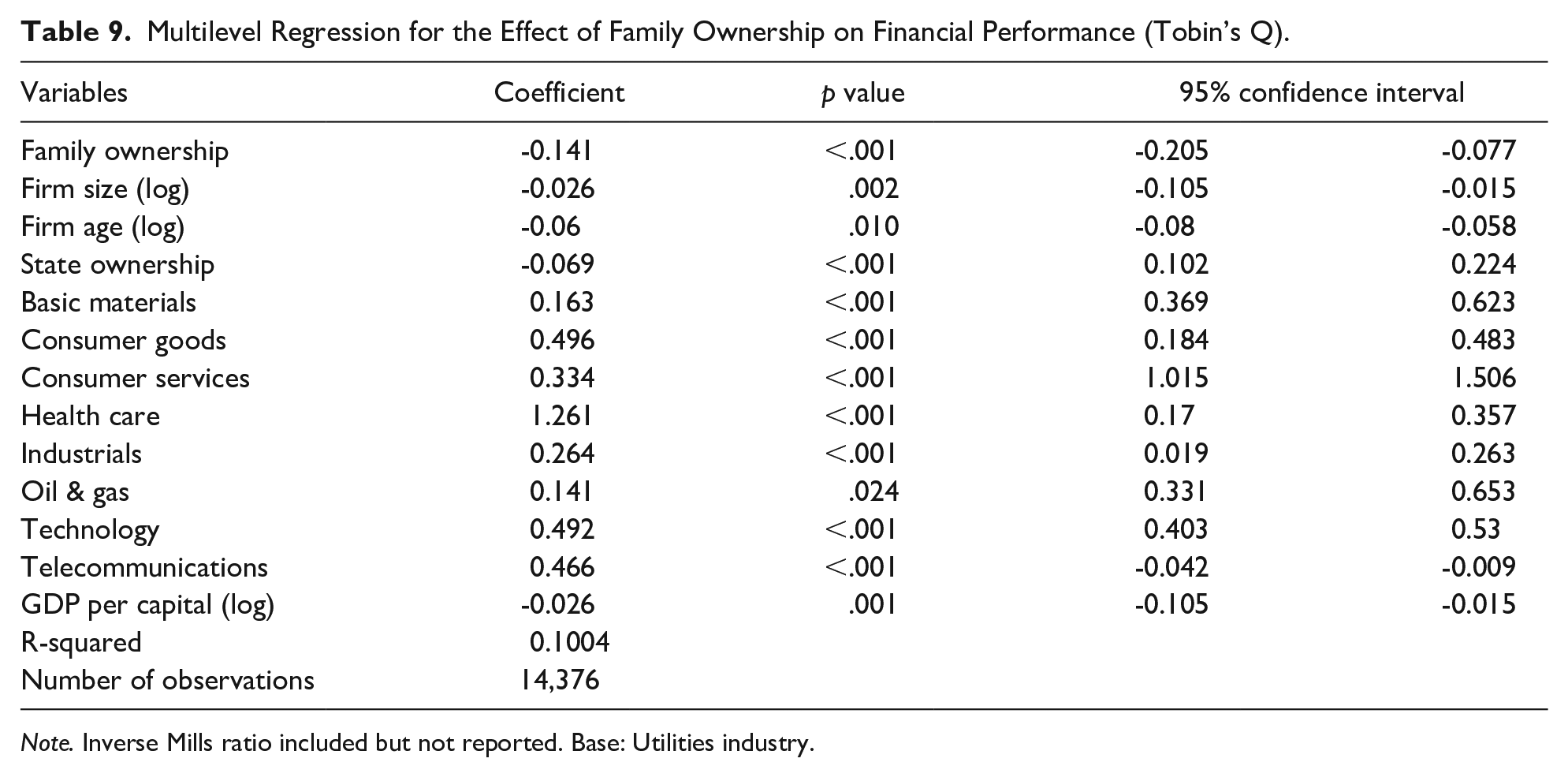

Tables 8 and 9 summarize the estimation results of the direct relationship between family involvement in a firm and financial performance. As shown, family involvement in the form of management—if the CEO is either the founder or a member of the founder’s family, such as a CEO-descendant (Schmid et al., 2014; Scholes et al., 2021)—and ownership—as percentage of shares held by a family member (Matzler et al., 2015; Memili et al., 2018)—was negatively correlated with financial performance; these relationships are statistically significant (p<.01). In terms of effect, a 1% increase in family involvement in ownership or management decreases the value of Tobin’s Q by 14.1% and 9.8%, respectively. Therefore, H1a and H1b are supported.

Multilevel Regression for the Effect of Family Management on Financial Performance (Tobin’s Q).

Note. Inverse Mills ratio included but not reported. Base: Utilities industry.

Multilevel Regression for the Effect of Family Ownership on Financial Performance (Tobin’s Q).

Note. Inverse Mills ratio included but not reported. Base: Utilities industry.

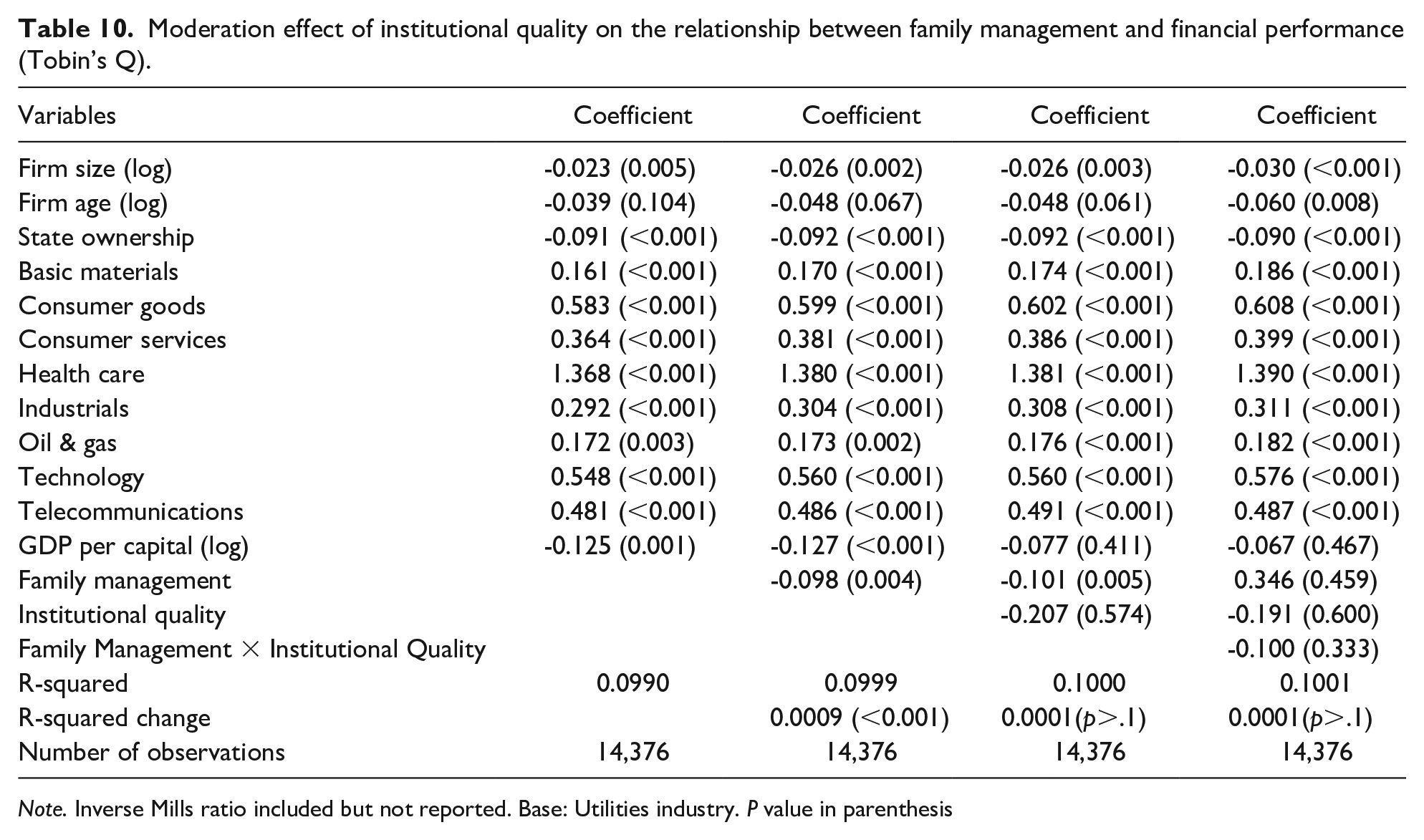

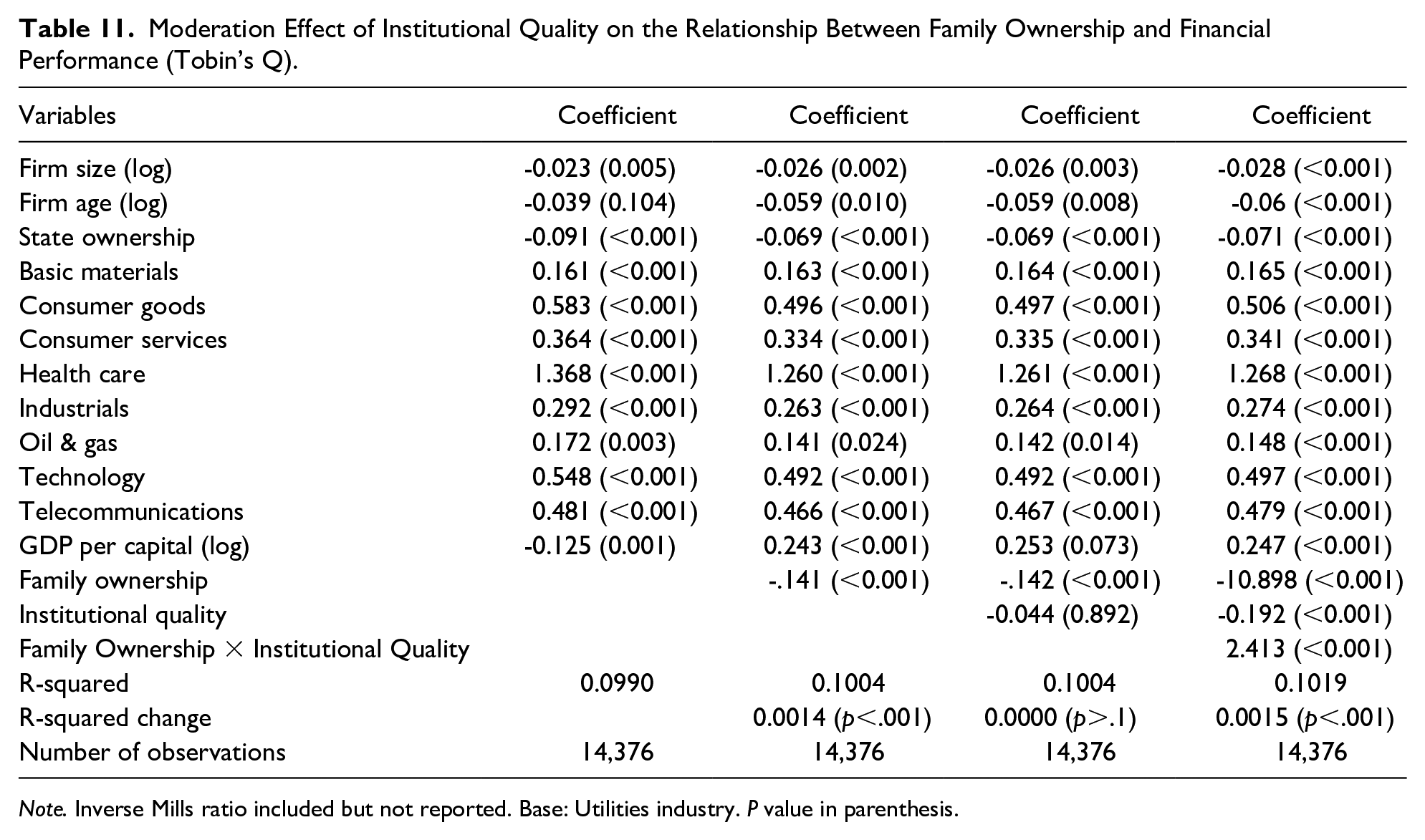

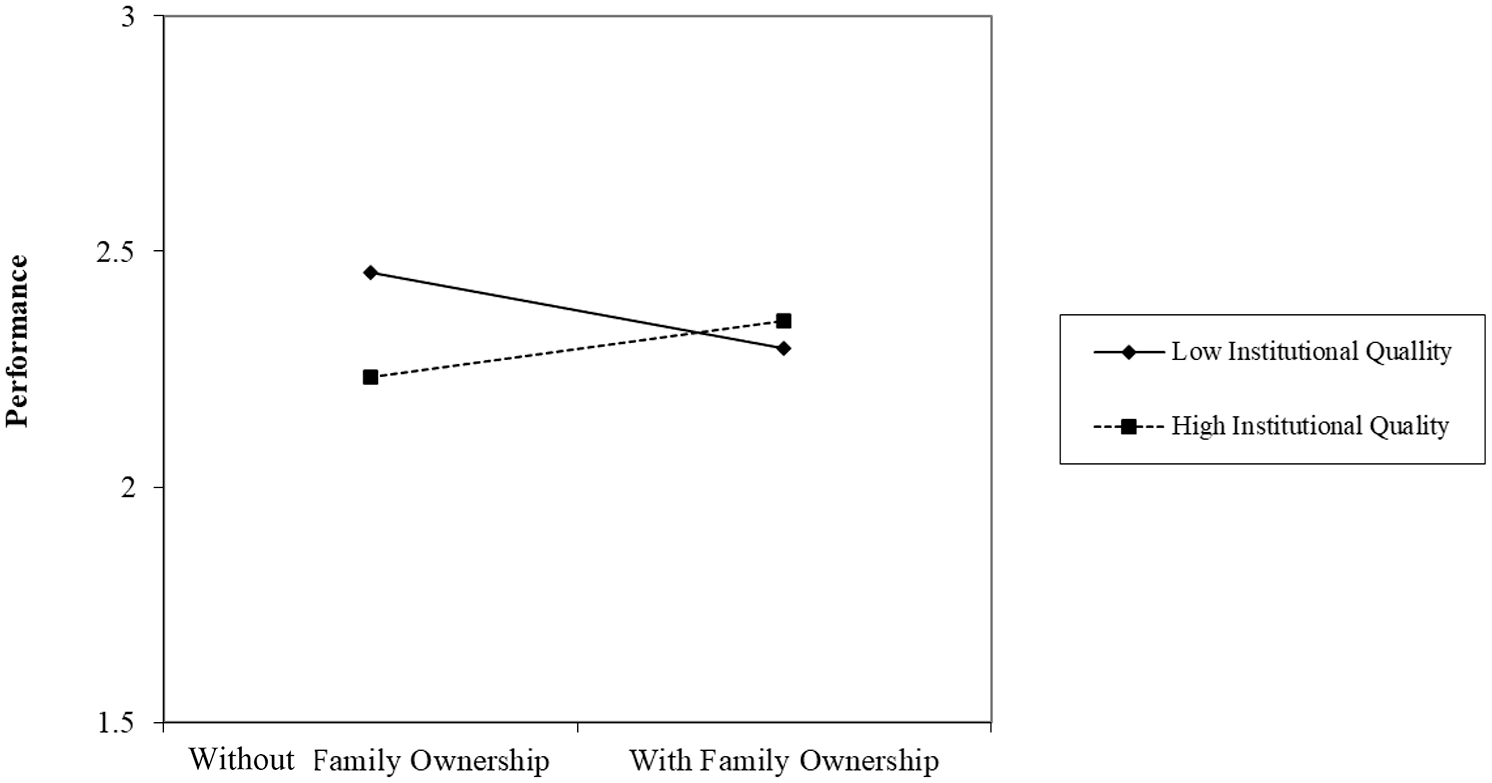

Tables 10 and 11 show the moderation effect of institutional quality on the relationship between family management and financial performance, and family ownership and financial performance. Looking at the interaction between Family management and Institutional quality variables, we see that it is not statistically different from zero. This suggests that the institutional quality does not seem to moderate the negative effect of family management on firm financial performance, rejecting our H2a. The coefficient of the interaction term of Institutional quality and Family ownership variables is positive and significant (β = 2.412; p < .001). This suggests that the negative impact of family ownership on firm financial performance in countries with good institutional quality is lower than in countries with weak institutional quality. Specifically, a 1% increase in the institutional quality means that family ownership decreases Tobin’s Q by some -8.5% (β = −10.898+ 2.412 = −8.486, p<.001) in countries with good institutional quality, as compared to a decrease in Tobin’s Q of around -10.9% (β = −10.898, p < .001) in countries with weak institutional quality. We plotted this result in Figure 2 using the Dawson template (Dawson, 2020). Thus, we find empirical support for our H2b.

Moderation effect of institutional quality on the relationship between family management and financial performance (Tobin’s Q).

Note. Inverse Mills ratio included but not reported. Base: Utilities industry. P value in parenthesis

Moderation Effect of Institutional Quality on the Relationship Between Family Ownership and Financial Performance (Tobin’s Q).

Note. Inverse Mills ratio included but not reported. Base: Utilities industry. P value in parenthesis.

The Moderation Effect of Institutional Quality on the Relationship Between Family Ownership and Financial Performance (Tobin’s Q).

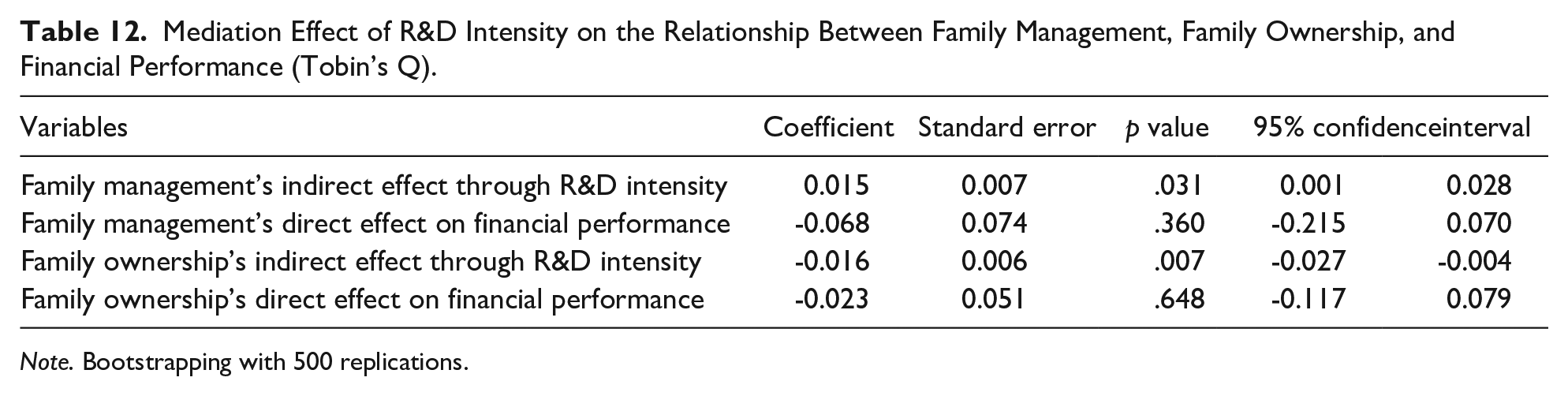

Table 12 reveals the mediation impact of R&D intensity on the relationship between family involvement and the firm financial performance. We applied the ml_mediation command in Stata 16.0 using bootstrapping methods with 500 resamples. The results were bias-corrected with 95% confidence intervals. We found partial mediation impacts for family management and family ownership through R&D intensity. We found that R&D intensity acts as a suppressor variable in the relationship between family management and financial performance, and partially diminishes the total direct negative effect of family involvement. The proportion of indirect effect to the total effect of family management is 41.1% (β = 0.015; standard error = 0.005; lower level of the 95% confidence interval = 0.001 and upper level of the 95% confidence interval = 0.028). We further found that R&D intensity partially mediates the link between family involvement and the firm financial performance(β = -0.016; standard error = 0.006; lower level of the 95% confidence interval = -0.027 and upper level of the 95% confidence interval = -0.004 for family ownership), and 37.0% impact of family ownership on financial performance is transferred through R&D intensity. Therefore, H3a and H3b were supported.

Mediation Effect of R&D Intensity on the Relationship Between Family Management, Family Ownership, and Financial Performance (Tobin’s Q).

Note. Bootstrapping with 500 replications.

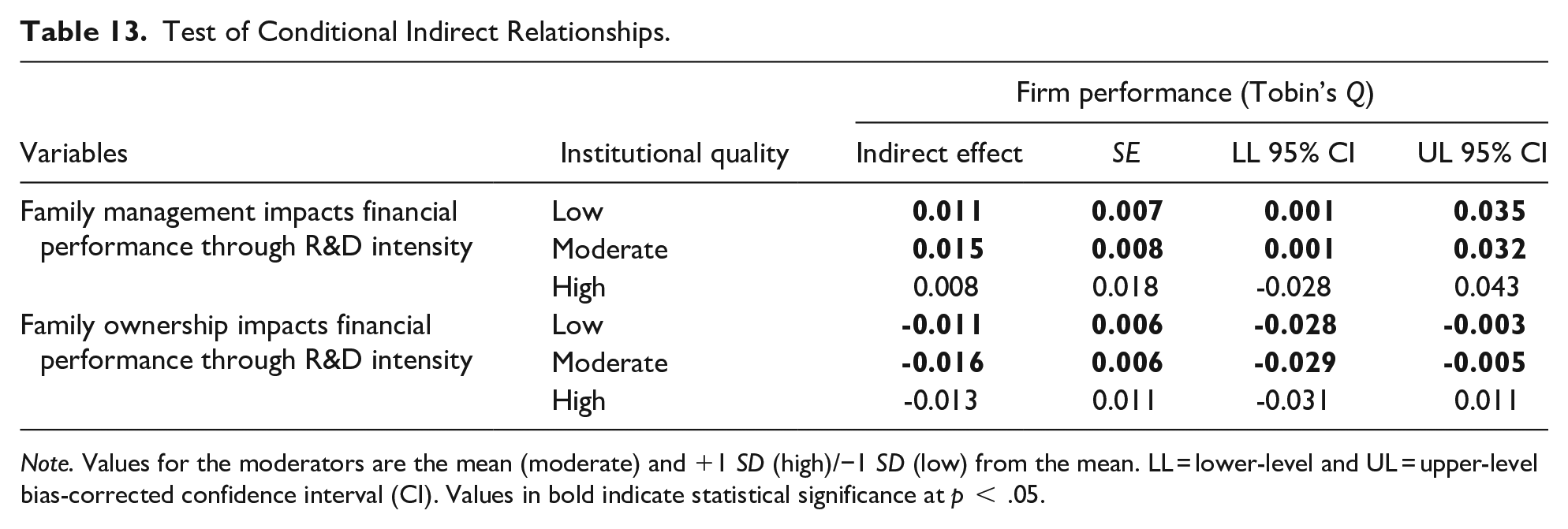

To examine the moderated mediation effects, we built a path model combining the mediation and moderation impact and then estimated the conditional indirect effects tested by a bootstrapping approach using Stata 16.0 (Preacher et al., 2007) in Table 13. We found that institutional quality, on average, significantly moderated the mediation impact of R&D intensity on the relationship between family management and financial performance (conditional indirect effect = .015, p < .05), and between family ownership and financial performance (conditional indirect effect = −.016, p < .01). Furthermore, the magnitude of the conditional indirect relationships was stronger when firms were operating in a country with better institutional quality, confirming our H4a and H4b.

Test of Conditional Indirect Relationships.

Note. Values for the moderators are the mean (moderate) and +1 SD (high)/−1 SD (low) from the mean. LL = lower-level and UL = upper-level bias-corrected confidence interval (CI). Values in bold indicate statistical significance at p < .05.

Robustness Testing

We conducted several ad hoc tests to check the robustness of our findings. First, we replaced Tobin’s Q with return on asset as a measure of financial performance as an alternative proxy of financial performance. Furthermore, we substituted our proxy of family management with several other NRG family management definitions. For instance, we captured it as the dummy that equals 1 if the CEO is the founder or descendant, or family founder-controlled, and one or more family members are officers, directors, or blockholders, otherwise 0. In doing so, the results stay unchanged. The same applies to the alternative operationalization of the family ownership variable, where we used different cut-off points of family ownership: 5%, 10%, and 15%. Again, the results remain equal. We also substituted our proxy of the institutional quality with another measure extracted from the WGI called “rule of law” that captures the perceptions on the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence; we obtained the same pattern consistent with our main findings. Thus, the results of the robustness checks confirm our principal findings.

Discussion

Combining insights from the SEW and agency perspectives, our study proposes and tests a holistic model that considers how internal and external factors (family involvement, innovation and institutional context) shape firm financial performance of listed firms around the world. Specifically, our model posits that the effect of family involvement on financial performance is mediated by R&D intensity, while the relationship between this intensity and financial performance is moderated by the level of institutional quality. Based on a longitudinal analysis of thousands of firms across dozens of diverse countries, we find that higher family involvement in ownership and management hampers firm financial performance in line with prior studies (Claessens et al., 2002; King & Santor, 2008; Lins, 2003; Oswald et al., 2009; Pérez-González, 2006). However, the negative effect of higher family ownership on firm financial performance is mitigated by the presence of a good institutional environment in a country—government effectiveness, rule of law, regulatory system, and financial system. In such countries, the negative financial performance of family-owned firms, as compared to nonfamily-owned firms, is substantially lower. The literature has provided institutional arguments to explain cross-country differences in family business prevalence, R&D, and internationalization, suggesting that legal and regulatory institutions (Hillier et al., 2011; Peng & Jiang, 2010), and institutional imperfections or “voids” (Luo & Chung, 2013; Torres de Oliveira & Rottig, 2018) are important contingencies affecting family ownership and control, the ensuing firm strategies, and R&D (dis)advantages. Here we advance the current conversation by examining the financial performance of firms with varying degrees of family involvement with an explicit focus on institutional quality variations across different contexts. At the same time, we find that the presence of a family CEO in a family business hampers firm financial performance regardless of the quality of the national institutional environment. A possible explanation for this finding is the fact that family managers, who are often assigned via kinship (Pérez-González, 2006), exercise poor management and incentive practices (Bloom et al., 2011) that cannot be mitigated by the presence of a good institutional environment in a country. We further find that R&D intensity constitutes the channel through which family involvement in ownership and management affects firm financial performance. Further, our results suggest that the magnitude of the mediation impact of R&D intensity on the relationship between family involvement and financial performance was stronger in countries with better institutional quality. Our results remain robust in correcting for the endogeneity of family involvement, accounting for potential survivorship bias, and alternative variable definitions and estimation techniques.

In short, our empirical results are compelling and highlight a stronger need to further search for the potential mechanisms through which family involvement affects financial performance in countries with varying degrees of institutional development.

Theoretical and Practical Implications

With our study, we make several important contributions to the firm financial performance, family business, innovation management, and institutional literatures. First, we substantially extend prior mixed research on the determinants of family business performance, which investigated separately internal (Chua et al., 2018; M. González et al., 2012; Lee, 2006) and external factors (Berrone et al., 2020; Duran et al., 2017, 2019) through the joint consideration of family involvement, R&D intensity and institutional context as important internal and external factors driving the firm financial performance in a cross-country sample of listed firms. By jointly examining the roles of family involvement, R&D intensity, and institutional context, we bridge the gap between previously fragmented research streams, providing a more comprehensive and nuanced view of the factors influencing firm financial performance. In so doing, we develop a better and more integrated understanding of firm financial performance. Specifically, we offer a rich theoretical model that proposes the mechanisms behind changes in family vs. nonfamily firms’ financial performance across countries with varying degrees of institutional quality and provide longitudinal empirical evidence on this research topic Put differently, our theoretical model not only illuminates the complex interplay between internal and external determinants but also offers new insights into how these dynamics vary across different institutional environments. Moreover, our empirical findings, grounded in a cross-country longitudinal data set, contribute robust evidence that enhances the validity and generalizability of our theoretical propositions. Specifically, we explicitly account for the potential endogeneity problem of family involvement and survivorship bias in our study following the call of Evert et al. (2016), and Pindado and Requejo (2015). A battery of robustness tests is also performed to rule out possible alternative explanations for our findings. By addressing potential endogeneity and survivorship biases, we ensure that our results are both methodologically sound and theoretically significant. Overall, we hope that this study can serve as a springboard for future research aiming to better understand the mechanisms behind firm financial performance of publicly traded firms with family involvement in different institutional contexts.

Furthermore, by bridging SEW and agency research, we argue that family involvement in ownership or management of a firm are less likely to be associated with above-average financial performance due to the SEW losses and agency costs. This would involve family-centered nonfinancial goals and principal–principal conflicts, and thus, according to the SEW and agency theorizations (Gómez-Mejía et al., 2007; Le Breton-Miller & Miller, 2018), family firms would be willing to incur financial losses (maintaining current control even at the expense of firm financial performance) to avoid those SEW losses and to not exacerbate existing principal–principal conflicts. Nonfamily firms, on the other hand, are more likely to excel financially, as they are not burdened by SEW considerations and principal–principal agency costs, in essence not incurring those losses as needed for delivering extraordinary financial performance (who are driven only by financial goals). Based on our data, family involvement in ownership and management does seem to play detrimental roles in a firm’s financial performance. As such we contribute to the growing stream of literature distinguishing a combination of theoretical explanations (SEW and agency theories) within the black box of “financial performance of family business,” each with important business performance implications.

Then, we enhance the current understanding of the financial performance of firms with family involvement by arguing and finding empirical support for the notion that family involvement is detrimental to financial performance, but country-level institutional quality partially alleviates such a detrimental effect. Firms with higher family involvement in ownership do better financially in countries with good institutional quality, and thus, company shareholders are primary beneficiaries of this in these countries. Thus, a combination of higher family ownership in a firm together with good institutional quality in a country can help to partially improve the inferior financial performance of listed firms with family involvement, as compared to firms without such involvement. Hence, our analysis documents the important role of country-level institutional quality in the family ownership-financial performance nexus thereby addressing the research calls of Pindado and Requejo (2015); Le Breton-Miller and Miller (2018).

Next, our study provides new insights into the mechanisms explaining the financial performance of listed firms with family involvement in different parts of the world. We find that higher family involvement in ownership negatively affects firm financial performance through R&D intensity; however, this negative effect is lower in countries with good institutional quality. Thus, our analysis contributes to understanding the role of dominant owners in a firm’s financial performance (de Miguel et al., 2004; Hamadi, 2010; Thomsen & Pedersen, 2000), by identifying the mechanisms through which family involvement in ownership translates into inferior firm financial performance. We also find that R&D intensity acts as a suppressor in the family management-firm financial performance relationship. In this relationship, R&D intensity substantially decreases the negative effect of family management on firm financial performance, particularly in countries with good institutional quality. Thus, we show that family-managed firms not only have lower financial performance around the world thanks to their R&D intensity, but importantly that this negative performance effect is most salient in noxious institutional contexts where shareholders are at the mercy of unpredictable actions of the controlling family. In brief, our results expand the family business literature into a new domain, as we show a considerable variation in the financial performance of firms with varying degrees of family involvement as an outcome of their ability to invest in R&D and reveal that such firms modify their performance as the level of country-level institutional quality changes.

We also contribute to the broader discussion on the influence of contextual factors on firms with family involvement. Our results explain that family business strategies and motivations are not only about the family’s inner-circle context logic but also dependent on broader, institutional logics. These multiple, lower- and higher-level institutional logics coexist (Greenwood et al., 2011) and are critical when analyzing family businesses. With our findings, we draw attention to the fluid nature of institutional logics and tensions between the family business context in both developed and developing economies. When various ownership forms are subject to fewer institutional constraints, they are more likely to use their own interpretive lens to frame the gains and losses associated with major decisions, and as a result, their business actions diverge even more. Transposing these arguments to our specific case in relation to decisions pertaining to R&D intensity, firms with family involvement are more likely to frame investments in R&D as a loss (due to SEW interests) more than nonfamily firms, and thus, when the institutional context readily accommodates a variety of behavioral responses (i.e., in a more volatile institutional field characterized by weak institutional quality), this should increase the negative impact of family involvement on financial performance.

Finally, this study has direct practical and policy implications. Given the ongoing debates in regulatory and business circles on policies to secure economic growth in a sustainable manner, our study reveals that family involvement in ownership and management has important detrimental effects on firm financial performance through R&D intensity, particularly in countries with weak institutional quality. Thus, our study cautions policymakers and potential investors to pay regard to the prevalence of firms with family involvement in a country and its institutional quality when evaluating plausible economic scenarios. What is more, our work underscores the importance for a firm’s owners, managers, and consultants to consider the mutual influence between the external environment and R&D intensity to understand the potential financial performance outcomes of firms with family involvement.

Limitations and Future Research

Our study has some limitations that offer ample opportunities for future research. We have considered family involvement in ownership and management using several definitional constructs following prior studies in the field (Claessens et al., 2002; King & Santor, 2008; Lins, 2003; Oswald et al., 2009; Pérez-González, 2006), but future research could extend our work by using alternative measures of family involvement in a firm, for instance, measuring the SEW and the strategic reference points of the controlling family (Debicki et al., 2016; Gómez-Mejía et al., 2018; Shinkle, 2011), or family involvement in a board or family guardianship in terms of the existence of a family council or trustee (Scholes et al., 2021), or accounting for different board models in firms with family involvement (Bettinelli, 2011; Vandebeek et al., 2016). We regard these further explorations as particularly promising.

Even though different innovation proxies are highly correlated with each other (Hagedoorn & Cloodt, 2003), it will be interesting to further distinguish between internal and external R&D efforts of a firm when studying the effect of family involvement on financial performance. In addition, different types of innovation outcomes including open innovation (H. Chesbrough et al., 2006), disruptive innovation (Kammerlander et al., 2018), radical innovation (Medina et al., 2006), social innovation (Cajaiba-Santana, 2014), and frugal innovation (Hossain, 2018) deserve further attention as potential mechanisms through which financial performance of firms with family involvement are affected.

The companies covered in our sample were only publicly traded. However, private firms with family involvement are known to have quite different family goals (Chua et al., 2018; De Massis, Kotlar, et al., 2018) and time horizons (Carney et al., 2015; Kappes & Schmid, 2013), as compared to listed firms with family involvement. Thus, future studies could further scrutinize the results of our work in the context of private family firms. We also hope that others will study the financial performance of firms with family involvement during even longer time periods than the period covered in our work (2007–2015) to better understand the role of the organizational life cycle in family business performance. Finally, although our results did not distinguish between developed and developing economies, such a comparative examination could open new perspectives and we welcome future research to do so.

Conclusion

In summary, our study bridges the family business, innovation management, and institutional literatures. We proposed and found that family involvement directly affects financial performance and indirectly shapes it through R&D intensity. Both the direct and indirect effects of family involvement are dependent on the level of institutional quality in a country. Taken together, our findings support the notion that an identification of the mechanisms through which family involvement affects financial performance can allow us to capture the complexity of this phenomenon.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.