Abstract

This study investigates the effect of nonfamily chief executive officers (CEOs) on family firms’ propensity to form political connections. We combine research on corporate political activity and family business and draw from the bounded reliability theory to analyze how the presence of a nonfamily CEO is related to the hiring of politically connected managers and board members. We further examine how our base hypothesis is contingent upon the organizational and environmental factors influencing nonfamily CEOs’ bounded reliability. Using the data from publicly listed Chinese family firms, support for our model was found. The study advances the understanding of family firms’ political activity.

Introduction

Political connections are essential to corporate political activity in developed and emerging economies (Burt & Opper, 2020; Faccio, 2006; Hillman et al., 1999). The traditional literature documented extensively the benefits of political connections, such as granting firms access to valuable resources and information, nurturing capabilities and competitive advantage, and ultimately enhancing market performance (see Lawton et al., 2013; Lux et al., 2011; Mellahi et al., 2016, for reviews). However, lately, there has been a growing concern about the downside, warning that politically connected firms are prone to “political liabilities” including government intervention and reputational damage (Boubakri et al., 2012; Dieleman & Boddewyn, 2012; Faccio, 2006; Frye & Shleifer, 1996; Okhmatovskiy, 2010).

The abovementioned paradox urges scholars to reconsider why firms form political connections (Ge et al., 2019). It is striking for family firms because, on one hand, given their inherent weakness in resources, capital, and market recognition (Dinh & Calabrò, 2019; Sirmon & Hitt, 2003), these firms can benefit greatly from political connections in terms of accomplishing the economic or financial goals (Dinh et al., 2021; T. Lee, 2019; D. Wang et al., 2016; Yang et al., 2020). On the other hand, family firms are known for their distinct focus on preserving noneconomic endowments or socioemotional wealth (SEW), even at the cost of economic gains (Gómez-Mejía et al., 2007, 2011). Political connections are likely to pose a threat in this respect, undermining, for example, family firms’ control, autonomy, identity, and long-term survival (Combs et al., 2020; Ge et al., 2019).

However, our review of the literature suggests that research on family firms’ political activities is lacking in general (Soleimanof et al., 2018). Of the limited studies (Combs et al., 2020; Ge et al., 2019; Hadani, 2007; Muntean, 2016), there are two issues. First, scholars failed to fully recognize the advantages and disadvantages of political activities, which often leads to contradictory views. For example, biased toward the benefits, Hadani (2007) and Muntean (2016) expected family firms to be more politically active than nonfamily firms, whereas Combs et al. (2020) contended that family firms are politically avoidant due to the fear of social attacks potentially triggered by political involvement. Second, influenced by the predominant family firm versus nonfamily firm paradigm (Chua et al., 2012), scholars chose to focus on mainly how family owners or managers influence firms’ political strategy. As a result, we know little about the role of nonfamily executives. For example, do they drive or deter family firms’ political engagement? Such question is meaningful because hiring outsiders to be top managers (Tabor et al., 2018), including the chief executive officer (CEO; Waldkirch, 2020), is common among family firms. Specifically, research has underlined the CEO’s affiliation with the owner’s family as a critical attribute of family firms. It shows that firms managed by nonfamily CEOs tend to display different practices and strategies than those by family CEOs (Cui et al., 2018; Huybrechts et al., 2013; Lardon et al., 2017).

In light of this, the present study will explore the relationship between the presence of a nonfamily CEO and the family firm’s likelihood of forming political connections. Our analysis seeks to unveil how these CEOs perceive the paradox of political connections differently than their family counterparts. Previous scholars comparing the two types of CEOs drew heavily on the agency theory and stewardship theory. However, due to the competing nature of these two theories, this literature strand is impeded by the ongoing debate about nonfamily CEOs’ opportunism (Madison et al., 2016; Waldkirch, 2020). Hence, we build our work upon the newly formed theory of bounded reliability (Kano & Verbeke, 2015; Verbeke & Greidanus, 2009, 2012; Verbeke & Kano, 2010, 2012). The theory is intended to reconcile the agency–stewardship dialectic. It contends that managers are not necessarily opportunistic; rather, their behaviors are influenced by a set of systematic individual attributes or “less-than-ideal logics,” including time-discounting bias, overcommitment, and identity discordance.

Combining the theory with family business literature, we propose that nonfamily CEOs demonstrate greater bounded reliability than their family counterparts, which further leads to these CEOs’ more substantial attention to the benefits of political connections yet lower awareness of and alertness to the downside. Based on this, we argue that family firms managed by a nonfamily CEO are more likely to form political connections than those by a family CEO. Next, we examine how the impact of nonfamily CEOs may vary. Kotlar and Sieger (2019) noted that the materialization of bounded reliability can be subject to task complexity. Via this lens, we investigate organizational and environmental factors that shape the task complexity perceived by nonfamily CEOs. The task of nonfamily CEOs is to meet the family’s economic and noneconomic goals (Tabor et al., 2018; Waldkirch, 2020). Specifically, we begin with family involvement (Chua et al., 1999; Kammerlander et al., 2020) and argue that a high family board ratio further induces nonfamily CEOs’ bounded reliability by growing their pressure on the task. In contrast, the incoming generation has the opposite effect because it signals nonfamily CEOs to prioritize the noneconomic aspect which underpins family succession. We further consider how organizational slack alleviates nonfamily CEOs’ bounded reliability by offering them relief and flexibility (Bradley et al., 2011; Martin et al., 2016; Singh, 1986) in juggling the two different goals. Likewise, we cast light on firms’ surrounding institutions because nonfamily CEOs may perceive lower task complexity in well-developed institutions. Considering the reduced paradoxical effect of political connections in such an environment (Ge et al., 2019), we hypothesize the difference between the two types of CEOs would diminish.

We test our model using a large sample of publicly listed family firms in China between 2010 and 2016. China offers an ideal setting for the study because it consists of many family firms (X. C. Li et al., 2015), and building political connections is a widely adopted strategy (Burt & Opper, 2020; Shi et al., 2014). Meanwhile, as a transitional economy, the Chinese context heightens the paradoxical effect of political connections for firms (Zhang et al., 2016). Following recent research (H. Jiang et al., 2021), we examine family firms’ political connections by their appointment of upper echelons (including the top managers and board directors) with prior government working experience. This measurement helps capture firms’ efforts to acquire relationships with the authorities, especially in emerging markets (Deng et al., 2018). It also aligns with the scholarly works that reveal the CEOs’ power and direct involvement in selecting managers and nominating board members (Cohen et al., 2012).

Overall, the study produces insight into the circumstance under which family firms are more likely to form political connections. As for the contributions, it first advances the under-developed literature of family firms’ political activity (Soleimanof et al., 2018). Specifically, by explicating the paradox, we add to the scholarly work that recognizes increasingly the negative consequences of political connections on family firms (Combs et al., 2020; Ge et al., 2019; Lee, 2019). Our finding regarding the CEO’s family affiliation also answers the call to unfold the link between family firms’ idiosyncratic characteristics and political activity (Dinh & Calabrò, 2019). Second, the study enriches the nonfamily CEO research. Consistent with Kotlar and Sieger (2019), it showcases how scholars could compare family and nonfamily CEOs through a novel theoretical perspective. Third, in so doing, the study contributes directly to the theory of bounded reliability by extending it to the new fields of family business and corporate political activity. Through the moderators, the study further provides insight into economizing bounded reliability, which is a critical but under-researched area.

Theoretical Background

In this section, we describe the complex effects of political connections and then relate them to family firms. Next, we explain the theory of bounded reliability on which the study relies.

The Complex Effects of Political Connections and Family Firms

Political connections refer to the “boundary-spanning personal and institutional linkages between firms and the constituent parts of public authorities” (P. Sun et al., 2012, p. 68). They are an essential component of corporate political strategy and represent a relational approach to engage with the government (Hillman et al., 2004; Hillman & Hitt, 1999). For many years, scholars have associated the value of political connections closely with firms’ economic or financial goals. They claimed that through connecting with politicians or government officials, firms gain access to critical resources and information, reduce uncertainty and transaction costs, enhance competitive advantage, and ultimately achieve excellent market performance (Hillman et al., 1999; Lawton et al., 2013; Lux et al., 2011; Mellahi et al., 2016). Not surprisingly, these benefits are documented in the family business literature (Dinh et al., 2021; Francis et al., 2009; Muttakin et al., 2015; Yang et al., 2020). Such effect is further said to be prominent in emerging markets where the government retains strong power and influence in the market and society (Deng et al., 2018). It matters also particularly to family firms because, as private businesses, they experience disadvantages compared with the state-owned enterprises (SOEs) that share the “blood line” with the government (Dinh & Calabrò, 2019; Haveman et al., 2017; X. C. Li et al., 2015).

On the other hand, recent literature has begun to recognize the downside of political connections. Concerned about the exchange nature of political strategy (Hillman et al., 1999), Frye and Shleifer (1996) and Faccio (2006) pointed out that sometimes political actors attempt to extract rents generated by the connections; in other words, looking for obligated “paybacks” from firms. Note that although the form and scale of rents vary considerably in practice, with some being “affordable,” scholars have warned the situation of the government imposing tight constraints on firms’ strategic choices, manipulating their business operations and forcing disclosure of sensitive business information (Boubakri et al., 2012; Dieleman & Boddewyn, 2012; Okhmatovskiy, 2010). With these excessive interventions, the “helping hand” of the government turns into the “grabbing hand” (J. P. Fan et al., 2007). For example, Dieleman and Widjaja (2019) described the case of an Indonesian company experiencing resource appropriation by the government via political ties. Tian et al. (2009) found that in China, the pressure to follow a new policy or a “national priority” is extreme for politically connected firms because they are expected to help the government set up the standard or benchmark for others in the market, as the way of returning the favor. Firms must respond to such demands, and those unwilling or unable to comply with them could face serious consequences or penalties.

Another scenario of political connections backfiring on firms is concerned with the strong bonding effect between firms and connected politicians (Lebedev et al., 2021). Specifically, due to power change in the political system, especially following unexpected political shocks or regime shifts (Siegel, 2007), a firm’s “friends” in the government could lose power, and consequently, the firm may no longer be entitled to those benefits such as access to resources, information, and political protection (Holburn & Vanden Bergh, 2008). The situation could be worsened if the successor has different interests and priorities (Zhong et al., 2019) or comes from a rival political group (Siegel, 2007). In China, for example, the danger of being the “red-hat” entreprenuers (referring to those engaging closely with the government) is always acknowledged (Chen, 2007). Over the past two decades, it was not uncommon to see wealthy Chinese private business owners being even prosecuted because of their tight link with highly ranked officials who lost their power within the Communist Party. 1 Furthermore, research shows that the depreciated value of political connections sometimes trigger adverse social and market reactions toward the firms. For example, during China’s widespread anti-corruption campaign, research found that firms associated with the ousting officials were losing public confidence and legitimacy (F. Liu et al., 2018; Zhou, 2017) and consequently, fell out of favor with investors (L. X. Liu et al., 2017; Y. Xu, 2018). It echoes Combs et al.’s (2020) claim that association with politics could potentially endanger firms’ reputation and identity.

The negative effects outlined here are worrying for family firms from the SEW perspective. SEW highlights family firms’ distinctive emphasis on preserving the “affect-related value” or noneconomic utilities (Berrone et al., 2012; Gómez-Mejía et al., 2007, 2011). As research shows, it is often used by family firms as a key noneconomic reference point for decision-making (Berrone et al., 2012; Cennamo et al., 2012; Chirico et al., 2020; Gómez-Mejía et al., 2011, 2019). From this perspective, we argue that political connections could threaten family firms in several ways. For example, a critical dimension of SEW is family control and influence (Berrone et al., 2012), whereas the possible government rent-seeking and interventions arising from political connections will undermine firms’ autonomy and challenge the family’s ownership and controlling position in the firm (Ge et al., 2019). Furthermore, SEW emphasizes stability and long-term survival (Berrone et al., 2012; Cennamo et al., 2012). Nevertheless, politically connected family firms are prone to substantial risks and uncertainties in this regard when becoming the victims of political changes. Plus, SEW highlights the desire to bind with stakeholders and create a sense of legacy. It could be endangered once family firms face negative sentiment and lose public interest. While political connections sometimes help obtain legitimacy (W. Li et al., 2016; Y. Wang et al., 2019), such an effect can be fragile and becomes even opposite with political change or social movement. As Combs et al. (2020) reiterated, in many countries, “the society still long held negative views of businesses engaging in politics” (p. 153).

In summary, although political connections can enhance family firms’ economic or financial outcomes, they may also put these firms’ noneconomic endowments at stake. Comparatively, the former benefit appears promising and imminent, whereas the latter downside seems to be uncertain and ambiguous in terms of whether, when, and to what extent it may happen. Very little research has explained family firms’ propensity to form political connections by considering these opposing effects and their distinct nature. The current study addresses this gap through the lens of the CEOs whose perception of a strategy can directly affect the firms’ decisions (De Massis & Foss, 2018; Hambrick & Mason, 1984; Huybrechts et al., 2013). As the literature suggests, family firms increasingly hire outsiders to compensate for their shortage of talent (Klein & Bell, 2007; Tabor et al., 2018), and it has become prevalent for nonfamily CEOs to navigate firms’ development (Waldkirch, 2020). Accordingly, we shed light on nonfamily CEOs and analyze how the presence of a nonfamily CEO is related to the formation of political connections in comparsion with having a family CEO at the apex of the family firm.

Boundedly Reliability

To explain and predict managers’ behaviors within organizations, agency theory is the most widely used. The theory views individuals as fundamentally opportunistic, or “self-interest seeking with guile” (Williamson, 1991), and that they experience bounded rationality, that is, make decisions in the situation of lacking complete information and the ability to evoke relevant knowledge (Simon, 2000). While agency theory is highly influential, it has met the challenge from the stewardship theory (Davis et al., 1997; Donaldson & Preston, 1995). Much of the debate is centered at opportunism. Scholars who support stewardship theory criticized the assumption of opportunism for the limited conceptual grounding and the absence of empirical analysis (Wathne & Heide, 2000). They argued that individuals are indeed loyal and trustworthy by nature, hence, always committed to the firm’s success through which they can also realize self-actualization.

Against this background, Verbeke, Kano, and colleagues developed the theory of bounded reliability (Kano & Verbeke, 2015; Verbeke & Greidanus, 2009; Verbeke & Kano, 2010, 2012). They attempted to relax the overly rigid assumption of opportunism by promoting a nonideological view of human nature. According to them, managers do not need to be assumed intrinsically trustworthy or nontrustworthy or strongly inclined to do good or bad. Instead, they are all pro-organizational and make decisions in good faith. Although managers sometimes fail and their decisions turn out to be wrong, it is not because of their “intentional deceit” (Verbeke & Kano, 2012) but rather the influence of several “less-than-ideal” logics which make them boundedly reliable.

To explain this further, Verbeke and Greidanus (2009) highlighted two logics of “benevolent preference reversal.” First, managers can have a time-discounting bias, meaning they often care less about a future consequence and prefer immediate utility over delayed utility. It is rooted in human nature that individuals place a lower value on future events than on more proximate ones. According to Verbeke and Greidanus, such bias causes managers to reprioritize or procrastinate certain commitments to the point where they can no longer fulfill them. Second, managers can be overcommitted. Driven by dysfunctional impulsivity and overconfidence (i.e., unrealistic belief in one’s abilities, predictions, or chances of success), they select to fulfill multiple commitments and commit too highly. Having to scale back on those commitments eventually results in the loss of resources and is often deemed a failure. Later, Kano and Verbeke (2015) added the notion of identity-based discordance. This logic concerns the scenario that “in spite of individuals’ stated or assumed commitments, they maintain contradictory behavior but in line with their personal identity or with past, prevailing practices they identify with” (p. 98). For example, managers identify with and pursue the goals that they believe appropriate (in good faith) but are misaligned or in conflict with those of others in a way that ultimately diminishes achieving firm-level goals.

The theory of bounded reliability was developed originally in the context of firms’ international strategies (Verbeke & Greidanus, 2009). It was then applied in family firms about family managers (Verbeke & Kano, 2010, 2012) and, more recently, nonfamily managers (Kotlar & Sieger, 2019). We continue this trend by focusing on nonfamily CEOs’ bounded reliability relative to their family counterparts. Previous research comparing these two types of CEOs draws heavily on the agency and stewardship theories (Waldkirch, 2020). According to Madison et al. (2016), it remains controversial whether the outsiders are self-serving and will undermine the family/firm deliberately, or they have natural incentives to act in the best interest of the firm and its owners just like family CEOs (Huybrechts et al., 2013; Karra et al., 2006; Lardon et al., 2017). We consider bounded reliability as a novel perspective to reconcile the issue.

Hypotheses

Bounded Reliability and Political Connection

Our central premise is that nonfamily CEOs experience greater bounded reliability than family CEOs, which explains their stronger intent to form political connections. First, it is because nonfamily CEOs have a more substantial time-discounting bias. Studies reveal that they are often impatient and truncate time horizons in decision-making due to their little or no stake in the firm (Le et al., 2009) and the fixed-term contract offered to them (Hackbarth et al., 2021). On the contrary, family CEOs hold a long-run interest in the company because of their ownership of the firm and the desire to preserve SEW (Le Breton-Miller et al., 2011; Lumpkin & Brigham, 2011; Miller et al., 2005; Strike et al., 2015). As Lumpkin et al. (2010) stated, decision-making by family members has “the tendency to prioritize the long-range implications and impact of decisions and actions that come to fruition after an extended time period” (p. 241).

Regarding political connections, the “present-focused” nonfamily CEOs (Desjardine & Shi, 2021) are naturally drawn to the promising and imminent benefits (e.g., resources and information acquisition, and special treatment) of this strategy which can enhance firms’ competitive advantages and market performance for the foreseeable future. They may, for example, consider hiring someone with political background and experience as an efficient and effective approach for the firm to access the political network. Meanwhile, these CEOs could be less aware of the downside of political connections because of its uncertainty and remote possibility (Hackbarth et al., 2021). After all, the government does not always ask for rents from firms (only when needed), and excessive government interventions do not necessarily accompany rent-seeking. Besides, the chance for disruptive political changes usually feels rather slim and ambiguous as they do not happen regularly. Comparatively, those “future-focused” family CEOs (Desjardine & Shi, 2021) are known to form strategies based on an extended timeline (Alessandri et al., 2018) and always look out for probable losses (Gómez-Mejía et al., 2014). They will be more mindful of the downside of political connections, hence, showing reluctance or a weaker motive to pursue the strategy.

Second, nonfamily CEOs are more likely to experience the issue of overcommitment. It is because in family firms, there is asymmetric altruism or bifurcation bias (Kano & Verbeke, 2018; Verbeke & Kano, 2010), referring to the de facto differential treatment of family versus nonfamily assets, including personnel. Nonfamily CEOs, as research shows, are subject to not only monitoring, evaluations, or disciplines much more strictly than their family counterpart (Dyer, 2006), but also the “colored” evaluation of their performance by the owning family (Samara et al., 2019; Verbeke & Kano, 2010). Under this circumstance, these CEOs face greater pressure to meet expectations and prove themselves to the family, which can induce overcommitment. Note that some research suggests family CEOs’ overconfidence (Dick et al., 2021; J. M. Lee et al., 2017). However, nonfamily CEOs are also overconfident based on their abilities and career achievements (Tabor et al., 2018). Considering the additional pressure from the owner family, we suspect they in general should exhibit overcommitment more strongly than family CEOs.

Importantly, nonfamily CEOs’ overcommitment will be associated closely with the firm’s economic goals. It is because the family members often feel challenged to explain their complex and diverse goals to outsiders from both the business and family perspectives (Visintin et al., 2017), so they prefer communicating with a stronger sensitivity to performance regarding reward and penalty (Hillier & McColgan, 2009; Rizzotti et al., 2017). As such, economic overcommitment drives nonfamily CEOs to emphasize obtaining the benefits of political connections. Even if they become aware of some drawbacks, they may choose to tolerate them as the “reasonable cost” for desirable organizational outcomes, such as sacrificing certain degree of control.

Third, nonfamily CEOs are prone to identity discordance. Research shows that they usually feel part of the firm but not necessarily of the family system because of their outsider background and natural inclination to draw on the success or experience before joining the family firm (Kano & Verbeke, 2015; Kotlar & Sieger, 2019). Accordingly, these CEOs have a strong tendency to embrace the identity of professionalism, which results in them acting mostly from an economic logic other than the family logic (Kelleci et al., 2019). Based on this, we argue that nonfamily CEOs would emphasize the desirable effects of political connections on firm’s performance but are less concerned about the potential negative impact relating to SEW. On the contrary, family CEOs who share identity with the family maintain a strong interest in nurturing and safeguarding the noneconomic utilities. They would stay vigilant to any threat toward the respect, so that the trade-off of political connections becomes more visible to them, which, in turn, makes these CEOs feel cautious in adopting this strategy.

In summary, we argue that nonfamily CEOs display stronger bounded reliability than family CEOs, which can be translated to their greater inclination of forming political connections. Considering the CEO’s influence on firms (Huybrechts et al., 2013), we propose the following:

The salience of bounded reliability, however, could be altered by the task complexity managers face—the more complex task, the more salient bounded reliability. For nonfamily CEOs, the complexity of their task lies in the pursuit of the competing economic and noneconomic goals simultaneously (Tabor et al., 2018; Waldkirch, 2020). For example, Mr. Hongbo Fang, the nonfamily CEO at the Midea Group (a family-owned large home appliance manufacturing company in China) once said in an interview that the biggest challenge for him was to manage the family and firm/business at the same time. 2 Dr. Van Schaik who was the first nonfamily CEO hired by Heineken also shared the similar view. 3 In this context, we consider how the impact of nonfamily CEOs on political connections may change according to the contextual factors that shape the CEOs’ task complexity (Kotlar & Sieger, 2019). Specifically, we discuss how family involvement, organizational slack, and institutional environment influence these CEOs’ overcommitment, time orientation, and identity discordance.

Moderation Effect of Family Board Ratio

The board of directors is a common governance mechanism adopted by family firms (Bammens et al., 2011). It consists of nonfamily and family members (Brenes et al., 2011; Kotlar & Sieger, 2019). While the former is expected to provide complementary knowledge and resources (Anderson & Reeb, 2004; Bammens et al., 2011), the latter represents the family to exert control and influence on the top executives, especially the outside CEO (Audretsch et al., 2013; Minichilli et al., 2014). We argue that the family board ratio, defined as the proportion of family members sitting on the board of directors (Calabrò et al., 2021), can have a positive moderation effect on the base hypothesis.

From the governance perspective, family board members are essentially the “monitoring device” deployed by the owner family (Audretsch et al., 2013; Visintin et al., 2017). Monitoring is concerned with the “measurement of the performance of decision agents and implementation of rewards” (Fama & Jensen, 1983, p. 303). For nonfamily CEOs, such monitoring, on one hand, is materialized regarding the firm’s market success (Audretsch et al., 2013; Chrisman et al., 2007; Rizzotti et al., 2017). As Visintin et al. (2017) reported, with a higher family board ratio, nonfamily CEOs are more likely to be dismissed or penalized for poor performance. On the other hand, the monitoring conveys an important message from the family to emphasize noneconomic utilities within the firm (Gómez-Mejía et al., 2007). The higher the family board presence, the greater pressure nonfamily CEOs feel about pursuing family goals.

Therefore, the family board ratio complicates the task situation perceived by nonfamily CEOs by adding more control to them and increasing their pressure to achieve high-economic and noneconomic outcomes simultaneously. Under the circumstance of higher ratio, nonfamily CEOs, first, are likely to demonstrate a more substantial time-discounting bias. As research shows, monitoring, especially regarding tight financial control, is associated with the increased frequency of performance evaluations, hence, inducing shortened time horizon behavior of managers (Goranova et al., 2017). Second, nonfamily CEOs could further suffer from overcommitment. It is because handling the two competing goal sets is challenging. Individuals encountering great challenges are inclined to overestimate their abilities and outcomes (Galasso & Simcoe, 2011; Picone et al., 2014) and adopt risky gambles and strategies (Ordóñez et al., 2009; Sitkin et al., 2011). Third, in response to their difficult situation, nonfamily CEOs may show a stronger tendency to rely on their own experience and knowledge in searching for the “right ways” (Zhu & Chen, 2015). While this is driven by good faith, according to Kano and Verbeke (2015), it leads to a pronounced identity discordance between these CEOs and the family.

On the contrary, family CEOs would not view family board members as a monitoring device. Instead, they may consider a high family board ratio to be a source of great support and protection from “own people” and a clear indicator of further emphasizing family values (Kano & Verbeke, 2018; Verbeke & Kano, 2012). As such, the higher the ratio, the more family CEOs’ direct attention toward noneconomic goals yet feel anxious about firm performance.

Based on the above, we suggest that the family board ratio augments nonfamily CEOs’ bounded reliability relative to family CEOs, further dividing these two types of CEOs regarding political connections.

Moderation Effect of Generational Involvement

Generational involvement refers to family firms’ deliberate involvement of children in the business and signals the owner’s intent to transit his or her power in the near future (Handler, 1994; LeCounte, 2020; Sharma & Irving, 2005). We argue that it has a negative moderation effect on the base hypothesis.

During the so-called “pre-succession phase” (Nordqvist et al., 2013), the family’s priority is to increase the level of preparedness of its young generation (Daspit et al., 2016; Sharma, 2004). The family will convey this message to nonfamily CEOs and urges them to nurture and mentor the successor candidates (Waldkirch et al., 2018). As such, the most critical mission for nonfamily CEOs is to care for succession. It suggests reduced task complexity, manifested by an explicit focus on SEW and less strict demand on the financial aspect. Accordingly, nonfamily CEOs will display less (economic) overcommitment. They may begin to also opt for a relatively long-term orientation to accommodate the upcoming changes within the firm, which offsets their inherent time-discounting bias. Besides, to support succession, nonfamily CEOs are expected to engage with the family more frequently and closely. Provided this allows these CEOs to learn about the family’s interests and principles or the “family logic,” their identity discordance could be alleviated.

While nonfamily CEOs show less bounded reliability, the opposite may be true for their family counterparts. It is because the family must convince other shareholders and top executives of their intended succession by demonstrating the successor’s competence and ability to protect the firm’s financial interest (Basco & Calabrò, 2017; Cater et al., 2016; McMullen & Warnick, 2015). Specifically, the family needs to showcase that the next generation’s involvement enhances other than undermines firms’ financial outcomes or performance. This mainly concerns family CEOs because of their usually weaker economic orientation or lower performance aspiration than nonfamily CEOs (Waldkirch, 2020). Hence, generational involvement should increase the task complexity for family CEOs, who will then respond with a noticeable surge of emphasis on firm performance. This gives rise to their (economic) overcommitment. Time-discounting bias may also emerge because the financial measures these CEOs aim for would be associated closely with the current pre-succession timeframe.

Overall, we propose that the next generation’s involvement in family firms mitigates nonfamily CEOs’ bounded reliability relative to family CEOs, thus, lessening the difference between these two types of CEOs regarding political connections.

Moderation Effect of Organizational Slack

Slack refers to the spare resources or the pool of resources in an organization that is more than what the organization needs for current operations or to produce a given level of organizational outputs (Cyert & March, 1963; Nohria & Gulati, 1996). Scholars have long identified slack as an essential organizational attribute influencing managerial goal-setting and decision-making (Cheng & Kesner, 1997; George, 2005; Martin et al., 2016; Tan & Peng, 2003). Drawing from this line of literature, we propose slack can have a negative moderation effect on the base hypothesis.

First, slack is considered to be a crucial indicator of firm’s success (Singh, 1986); therefore, plentiful slack can make managers feel accomplished and then relieved from meeting high-performance targets (You & Du, 2012). In family firms, while this effect may be seen for both family and nonfamily CEOs, it would be more pronounced for the latter because of the distinctive high-performance expectation placed on them. Hence, we regard that slack could reduce nonfamily CEOs’ pressure on the financial aspect. It suggests less task complexity for these CEOs and further their curtailed economic overcommitment. In addition, recent study found that when outsider managers experience less financial pressure, they may begin to restructure their goal system and values to align more closely with the family (Randolph et al., 2019). Based on this, we expect slack to potentially also minimize identity discordance between the two types of CEOs.

Second, scholars pointed out that an important function of slack is to offer a “safety net” for mistakes in practice and act as a “shock absorber” for firms (Bourgeois, 1981; Latham & Braun, 2009). Therefore, those having access to slack resources, according to Martin et al. (2016), often enjoy the privilege and flexibility to “allocate resources across different time horizons within their firm while also satisfying the short-term performance demands” (p. 2467). Applying this view to nonfamily CEOs, we regard that slack can relax the time constraints on them. It eases these CEOs’ task complexity and should alleviate their time-discounting bias. Such an effect, however, could be less apparent for family CEOs because of their inherent long-term orientation.

In summary, we argue that slack decreases nonfamily CEOs’ bounded reliability relative to family counterparts, thus negatively moderating the base hypothesis.

Moderation Effect of Regional Institutions

Our fourth boundary condition pertains to firms’ institutional environment. While early research examined institutional environment at a country level (Ahmadjian, 2016; Hitt et al., 2004; Wan & Hoskisson, 2003), recent studies suggest a subnational or regional focus because of the more direct impact on firms and the uneven development of institutions, especially in geographically vast emerging economies (Chan et al., 2010; Y. Liu & Yu, 2018; Ma et al., 2013, 2016). We argue that regional institutions have a negative moderation effect on the base hypothesis.

More specifically, scholars describe that in advanced institutions, laws and regulations are in place and enforced, the government imposes fewer market restrictions, and valuable resources are no longer unevenly allocated by authorities, such as between SOEs and private firms (Luo, 2007). It means less complexity for nonfamily CEOs in respect to pursuing the economic goals because they can compete on market-based strategy without relying heavily on political strategy (Ma et al., 2016). Under this circumstance, these CEOs’ strong commitment to firm performance no longer necessarily leads to the choice of forming political connections.

Likewise, advanced institutions reduce the concerns about government rent-seeking and intervention because the authorities are less likely to abuse their administrative power and impose discretion over firms (Khanna et al., 2005). Such institutions are also characterized with low political uncertainty or instability (Ma et al., 2013; S. L. Sun et al., 2015), suggesting minimal probability for firms to encounter drastic political changes. Even if the changes did happen, the impact on firms might not be frightening because of the open and fair regulatory system. Objectively, these features point toward the diminished costs and risks of political connections. Hence, nonfamily CEOs and their family counterparts, despite the former’s time-discounting bias and identity discordance, will differ less noticeably in terms of foreseeing the downside of political connections and taking precautions.

Furthermore, family CEOs may actually grow their intention to form political connections in advanced institutions. It is because the economic benefits of political connections in a well-developed institutional environment, although decreasing, do not vanish entirely (Burt & Opper, 2020). Meanwhile, provided there is a highly appraised government and little political uncertainty, political connections could help firms improve their social legitimacy and recognition (W. Li et al., 2016; Y. Wang et al., 2019), which relates to SEW. Hence, we regard that in an advanced institutional environment, family CEOs tend to feel more comfortable with political connections or “safe” to reap the benefits of this strategy.

In summary, we propose that the difference between nonfamily CEOs and their family counterparts in forming political connections becomes less prominent in better-developed institutions, thus a negative moderation effect for regional institutions.

Method

Data and Sample

We tested our hypotheses based on a sample of publicly listed family firms in China. We extracted all Chinese publicly listed family firms in the Shanghai and Shenzhen stock market from 2010 to 2016 from China Stock Market and Accounting Research (CSMAR), which is one of the most popular data sources of Chinese public firms used by scholars (Xia et al., 2014). Following prior studies (Pan et al., 2018 D. Xu et al., 2019), we selected our sample firms from the dataset using two main criteria: the founder and his or her family are the largest shareholder and hold at least 10% firm ownership, and at least one family member is involved in the firm management. Such identification standard aligns with the broad definition of a family firm where a family controls the firm and participates in the management (Astrachan et al., 2002; Chua et al., 2004). 4

The CSMAR database provides detailed information on family firms’ executives’ backgrounds, such as the family background of the CEOs and board members, whether there is any next generation involved in the management, and relevant accounting and financial data of the firms. Next, we collected data on family firms’ political connections from their annual reports published on the Shanghai and Shenzhen stock exchange websites. We extracted the personal information of firms’ top managers and board directors, including their work experience, specifically their employment history at government agencies. It allowed us to identify whether the person had a historical political linkage. Furthermore, we obtained the subnational institutional development from the National Economic Research Institute of China (P. Sun et al., 2016; S. L. Sun et al., 2015).

After dropping the missing values, we finally have 922 family firms and 3,816 firm-year observations. According to the sample, on average, the controlling family dominates the family firm through 41% of ownership and more than two family managers; about 60% of CEO positions are taken by the family members.

Measurements

Dependent Variable

Because many political activities seen in Western countries are not allowed in China, such as political lobby and party campaign donation/support (Shi et al., 2014; Zhang et al., 2016), Chinese private firms, including family firms, typically seek to form political connections by hiring the upper echelons, defied as the top management team (TMT) and board members, who have prior government working experience (Haveman et al., 2017; H. Jiang et al., 2021). These upper echelons maintain their ties with former colleagues and enjoy the advantage of developing relationships with government officials even after they left the government agencies; therefore, hiring them allows the firm to quickly become connected with the authorities and access the political network for resources and special treatment (Burt & Opper, 2020). As a matter of fact, during the 2010s, there was reportedly even a wave of government officials resigning from their current roles to join private firms (Ren et al., 2020). A rather high-profile case, for example, was that Mr. Mingqi Dong, who was once the Secretary of the Party Committee and Deputy Governor of the Hainan Province, became an independent board director of a large publicly listed family company (Goldlok Holdings) in 2015.

Consistent with previous studies in China (e.g., Shi et al., 2014; Zhang et al., 2016), our measurement of the dependent variable is intended to capture the sample firms’ practice of hiring politically connected upper echelons. The Chinese government mandate publicly listed firms to disclose the resumes of upper echelons in their annual financial reports (H. Jiang et al., 2021). It allows us to identify all TMT and board members’ personal background information, including prior career experience. Our panel data contain the information for each CEO in the given family firm during the given year (t). We first check whether there were politically connected upper echelons newly hired in the next year (t + 1). If yes, then we calculate the count number of how many. Based on this, we measure the formation of political connections by a count number of politically connected TMT and board members hired by the focal family firm.

In the robustness analysis, we measured the dependent variable in two alternative ways. First, we used the ratio of politically connected upper echelons divided by the total number of TMT and board members to control the scale effect that firms with a larger executive team could have a higher possibility of hiring politically connected ones. Second, although the CEO usually plays a role in designing the board of directors (Cohen et al., 2012), there is a possibility that in family firms whereby the family retains much control, nonfamily CEOs are more powerful and influential in hiring managers than appointing board members. Thus, we used the hiring of TMT managers with government background (excluding the board members) in the analysis.

Independent Variable

Following prior family business literature (Pan et al., 2018; D. Xu et al., 2019), we define a family CEO as possessing the family blood or marital relations with the owner’s family. We code nonfamily CEO as 1 and family CEO as 0.

Moderating Variables

We measure the family board ratio as the number of family members on the board divided by the total number of board members. Next-generation involvement is coded as 1 if family members of the next generation have taken a senior management role in the company, 0 otherwise. As scholars noted, many Chinese family firms now face the issue of succession because those founders who started their businesses in the 1980s and 1990s are near retirement (X. C. Li et al., 2015).

Organizational slack. Following previous literature (Bradley et al., 2011; Paeleman & Vanacker, 2015), we use firm’s cash reserves scaled by total assets as the measurement of firm slack.

For regional institutions, we derive our measurement from the provincial-level the National Economic Research Institue (NERI) index of marketization (G. Fan et al., 2003). This index is developed based on four elements: regulatory separation (separation of the regulatory authority from the executive branch), liberalization (of most product markets), depoliticization (reduced political influence on the regulatory authority), and privatization of SOEs (Shi et al., 2012). Scholars have used it extensively to measure the degree of institutional development in regions across China (Y. Liu & Yu, 2018; P. Sun et al., 2016; H. Wang & Qian, 2011). We match the index with the province and year of each focal firm. A higher index indicates that the focal firm is located in a more developed institution in the given year.

Control Variables

We control carefully for the CEO, family-level, and firm-level variables. First, we include the CEO’s age and CEO tenure as control variables because they can be associated with the CEO’s time orientation in strategy (J. M. Lee et al., 2018; Strike et al., 2015). CEO age is measured as the logarithm transformed value of the years since the CEO was born, and CEO tenure is measured as the logarithm transformed value of the number of months the CEO has served in the position. Second, we control the firm’s degree of family ownership, indicated by the total share percentage held by the controlling family (Berrone et al., 2012). Likewise, we control family management by the number of family members in the TMT (H. Fang et al., 2018). Third, we control for firm characteristics, including firm age and size, which are important indicators of the firm’s accessible external resources (Tsai, 2000). Firm age is measured as the logarithm of the number of years since establishment; firm size refers to the natural logarithm transformed value of the firm’s total asset.

Furthermore, the literature suggests that firms’ tendency toward political involvement may be dependent upon their market-oriented capabilities (Du et al., 2019). Therefore, we include a few critical dimensions of these capabilities. Intangible asset ratio is measured as the intangible assets over total assets. As per China’s accounting standards, intangible asset includes trademarks, copyrights, patents, franchises, and so on (He et al., 2022). R&D ratio, which indicates firms’ innovation efforts, is measured by the ratio of R&D expenses scaled by total revenue. We also include factors that could potentially affect the firm’s capability to obtain external resources. Financial performance will increase the firm’s ability to accumulate resources from an internal aspect (Paeleman & Vanacker, 2015) or decrease its tendency to obtain resources from external aspects through debt (Fama & French, 2002; Shyam-Sunder & Myers, 1999). We, therefore, control for the ROA, the net income scaled by the total asset, to measure the firm’s financial performance, a commonly used accounting-based measurement of firm financial performance (Chang et al., 2013; Marquis & Qian, 2014; H. Wang & Qian, 2011).

Moreover, the literature suggests that a family firm’s decision-making, unless 100% owned by the family, can be influenced by the nonfamily owners (Arregle et al., 2012; Calabrò et al., 2017). To control for the influence of nonfamily investors on firm strategy, we include ownership concentration in our analysis. Following the Herfindahl–Hirschman index, it is measured by the total of squares of the shareholding percentage of the top five largest shareholders (we combined all family shareholder percentages as a whole). As such, the higher ownership concentration indicates lower ownership concentrated in the hand of nonfamily investors and lower influence in family firm decision-making. We use TMT size, the logarithm of the total number of TMT members, to examine the involvement of nonfamily managers. Finally, we control industry, year, and province dummy variables.

Estimation Methods

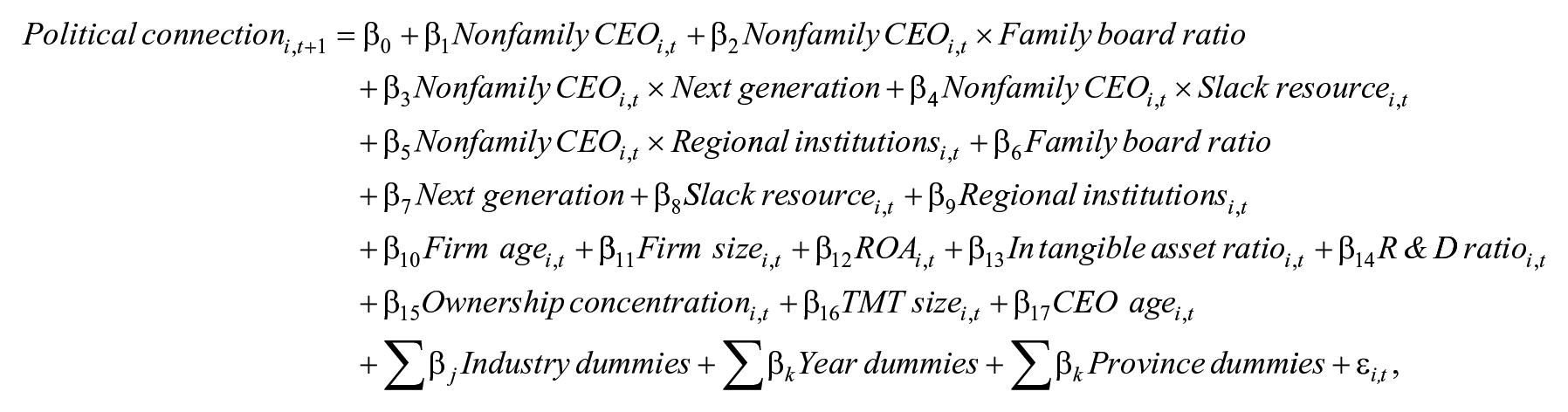

The use of the firm’s political connection as the dependent variable indicates the use of the count model, like a Poisson or negative binomial (NB) model. As many family firms may not have political connections, in which case the value of zero is overdistributed in independent variable-political involvement, we choose to use zero-inflated negative binomial regression model (ZINB) with Stata’s zinb command. Because it may take time to recruit executives and build political connections, we lagged our independent variables by 1 year.

We use the following regression to estimate our hypothesized relationship between nonfamily CEO and political connection.

where

Results

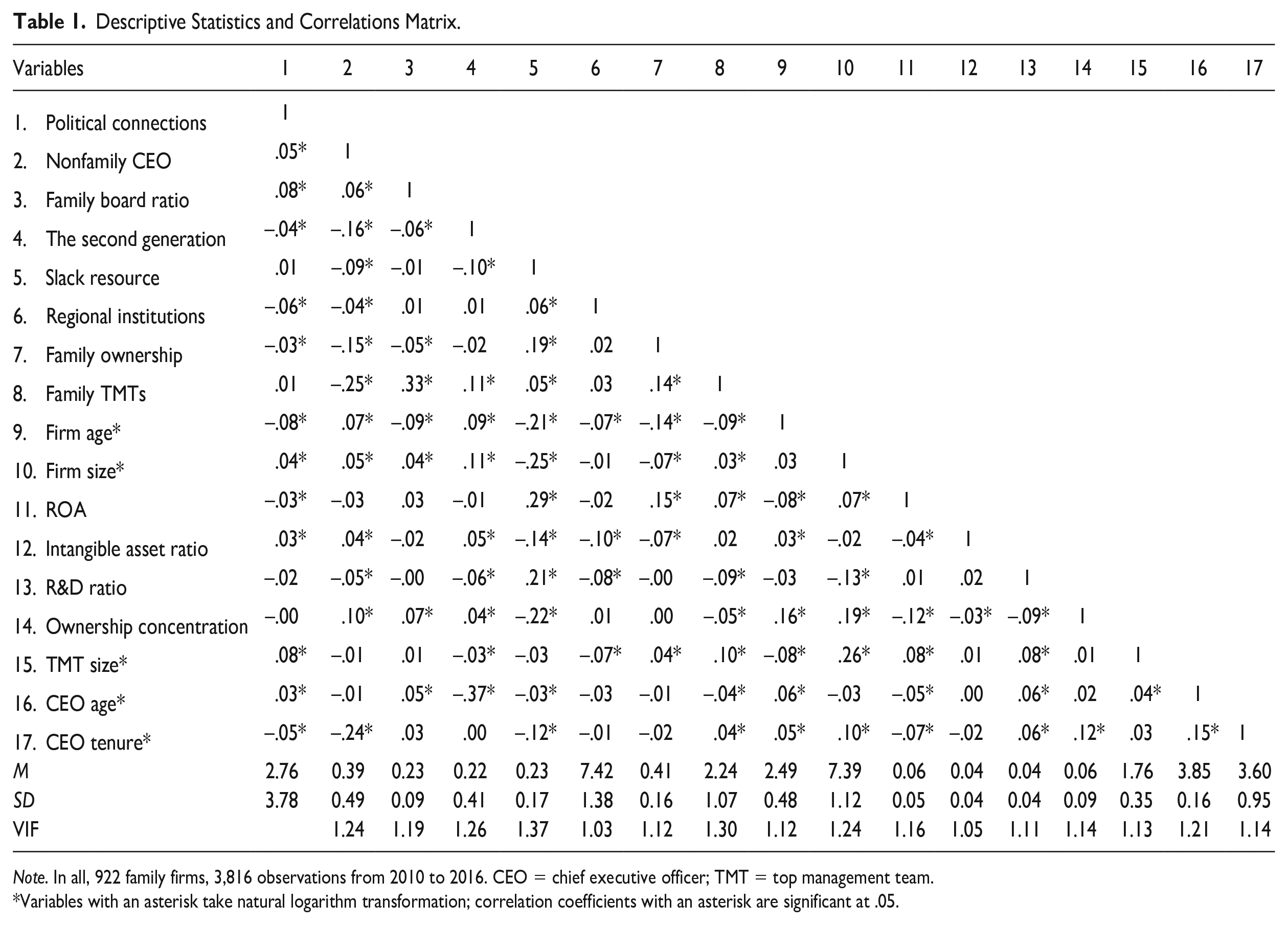

Table 1 shows the descriptive statistics and correlation matrix. There are no large correlations between variables. We further calculate variance inflation factor (VIF) statistics, and the largest VIF is 1.37 for slack resource, which is significantly lower than the rule-of-thumb value of 10 (Ryan, 2008). Therefore, our data are safe from the problem of multicollinearity. The descriptive statistics also show the average family firm age in our sample (13.43) with a standard deviation of 5.59, and the average firm size by staff number (3,429). The mean of CEO age is 47.6, with a standard deviation of 7.25.

Descriptive Statistics and Correlations Matrix.

Note. In all, 922 family firms, 3,816 observations from 2010 to 2016. CEO = chief executive officer; TMT = top management team.

Variables with an asterisk take natural logarithm transformation; correlation coefficients with an asterisk are significant at .05.

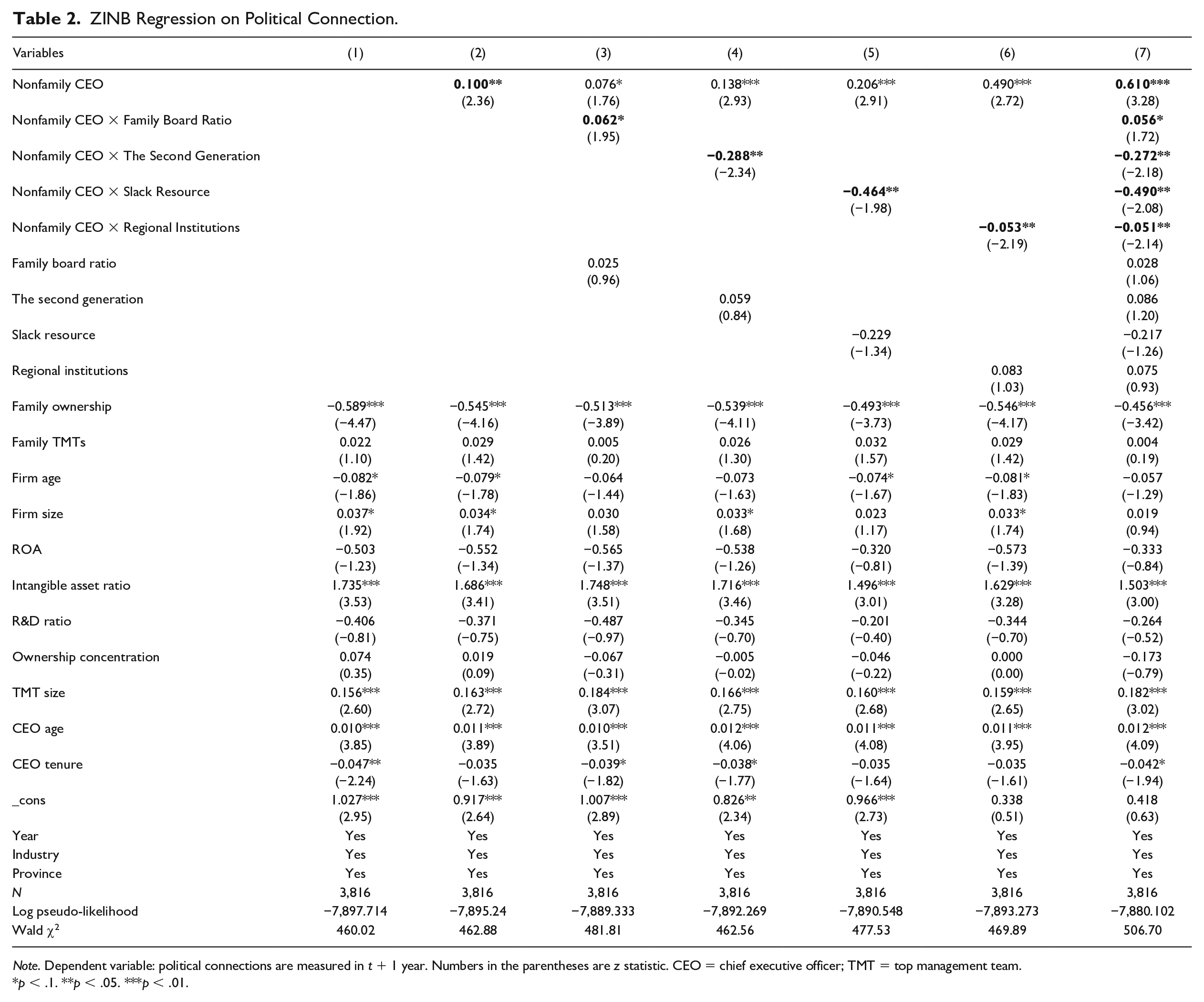

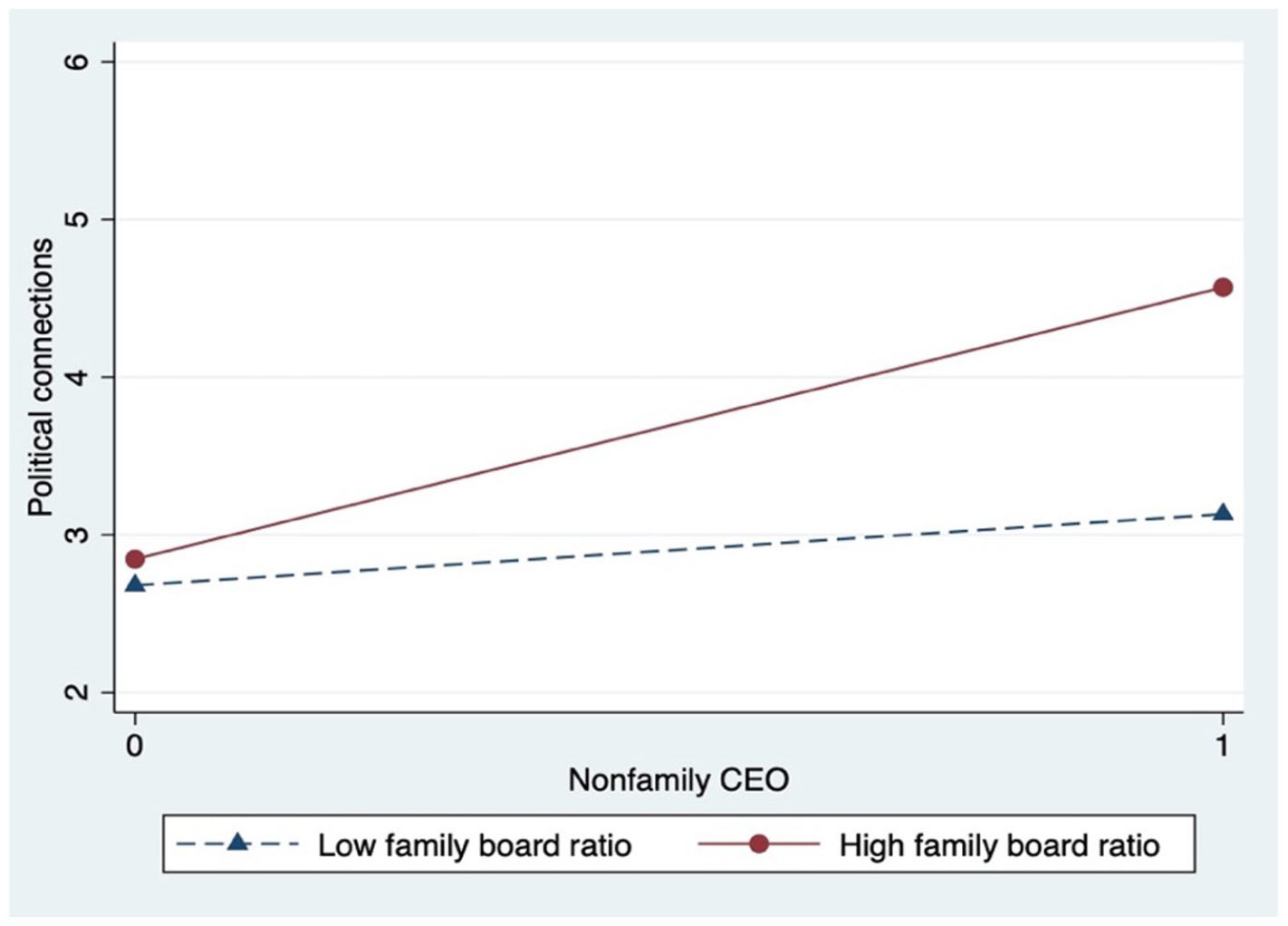

Table 2 presents the results of ZINB regression. In Model (1), we include only the control variables. In Model (2), we add the independent variable and find that it is positively correlated with the dependent variable (coefficient = 0.100, p < .05), which suggests that family firms led by nonfamily CEOs are more likely to form political connections, hence supporting Hypothesis 1. In Model (3) and Model (4), we test the moderating effects of the family board ratio and next generation, respectively. Results in Model (3) show that the interaction term of family board ratio has positively significant coefficient (coefficient = 0.062, p < .1). It means that the relationship between the nonfamily CEO and political connections becomes stronger for family firms with a higher family board ratio, thus supporting Hypothesis 2. This moderating effect is visualized in Figure 1, which shows that nonfamily CEO has a positive effect on political connection and the slope becomes steeper when the family members are involved in the board.

ZINB Regression on Political Connection.

Note. Dependent variable: political connections are measured in t + 1 year. Numbers in the parentheses are z statistic. CEO = chief executive officer; TMT = top management team.

p < .1. **p < .05. ***p < .01.

Moderating Effect of Family Board Ratio

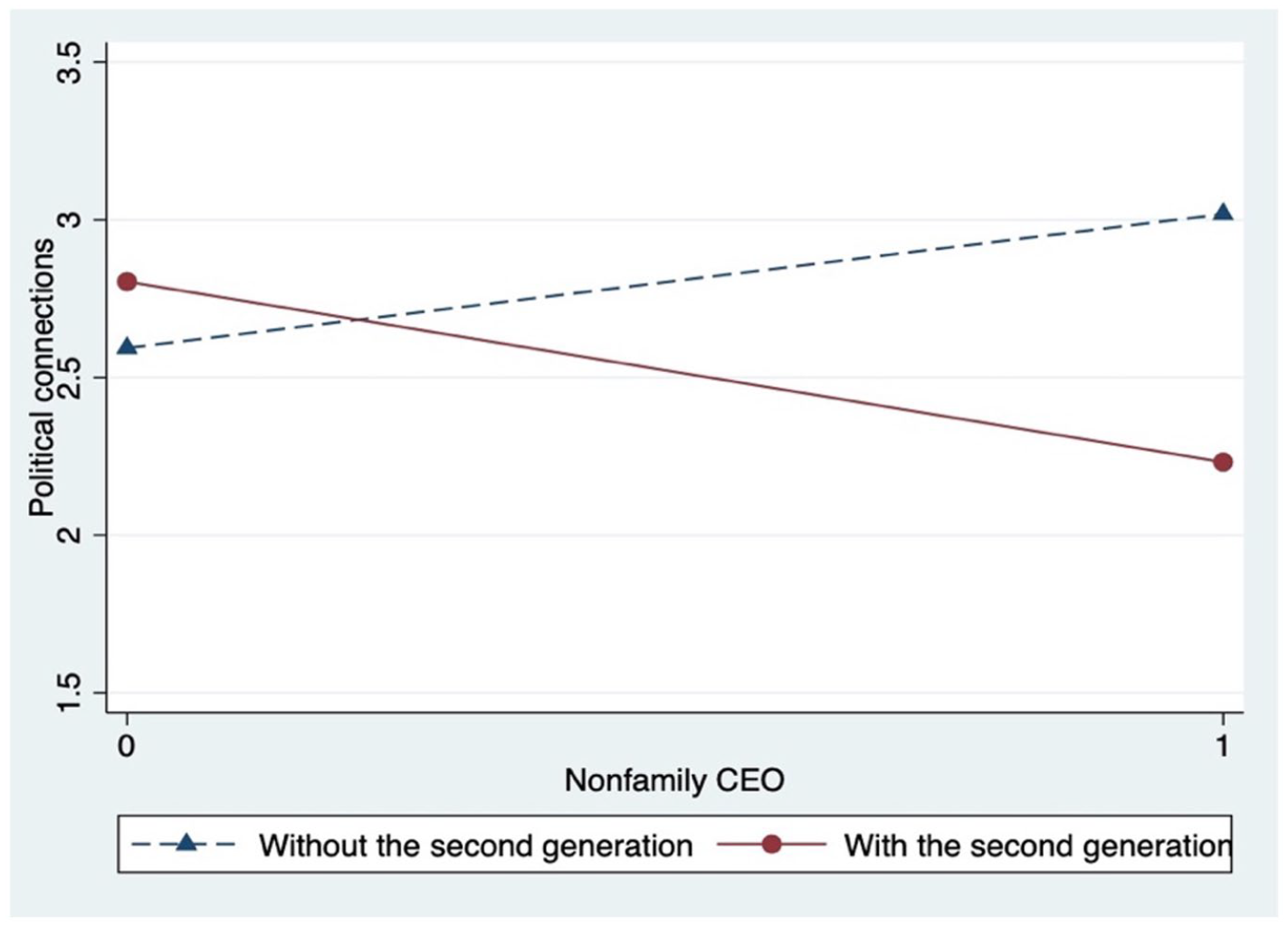

Results in Model (4) show that the next generation negatively moderates the nonfamily CEO and political connection relationship (coefficient = −0.288, p < .05). In other words, when family firms involve the next generation in management, the positive relationship between nonfamily CEO and political connections turns to be weaker. This supports Hypothesis 3. Figure 2 further illustrates that the positive relationship between nonfamily CEO and political connections becomes flatter for family firms that involve next-generation family members.

Moderating Effect of the Next Generation

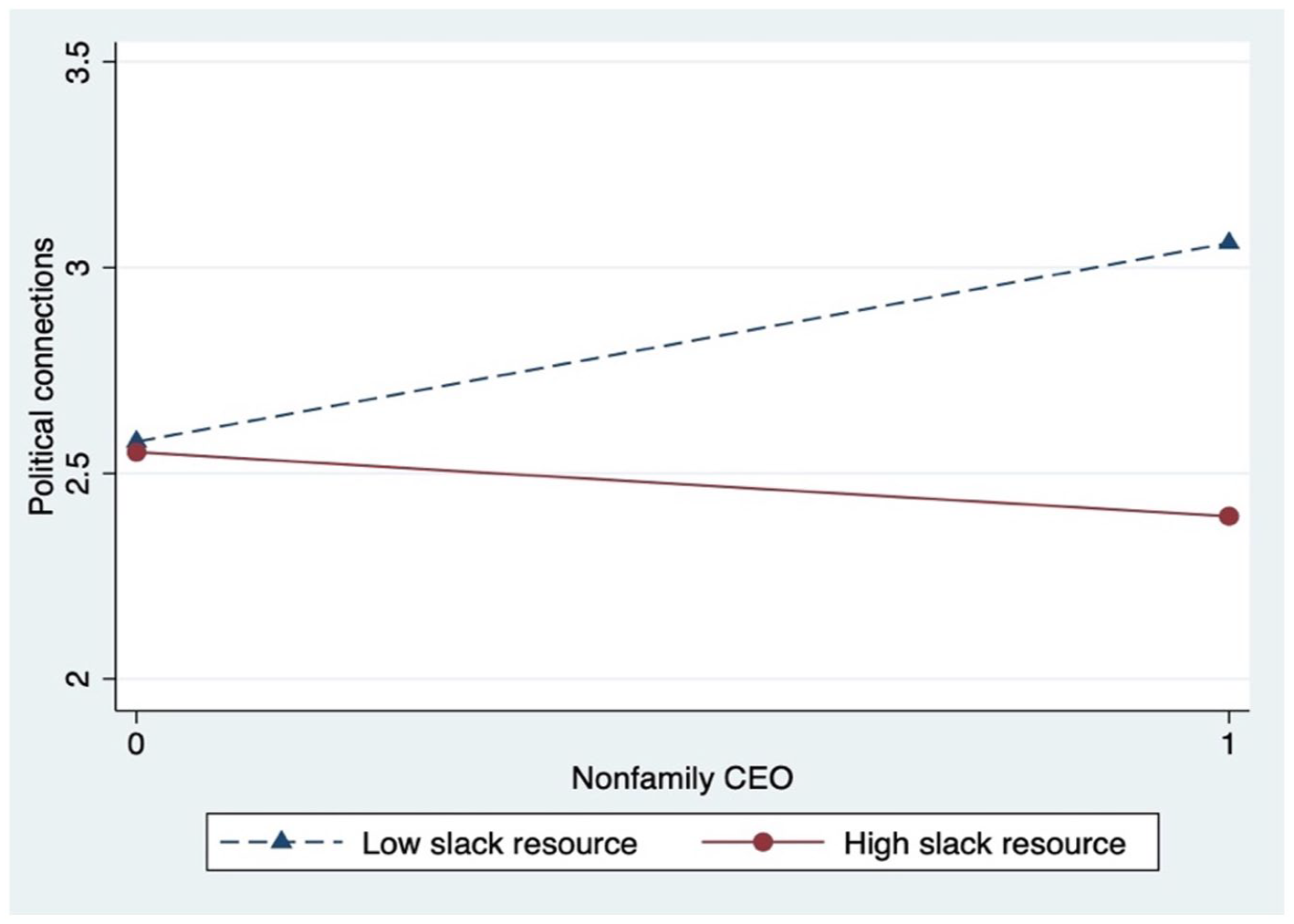

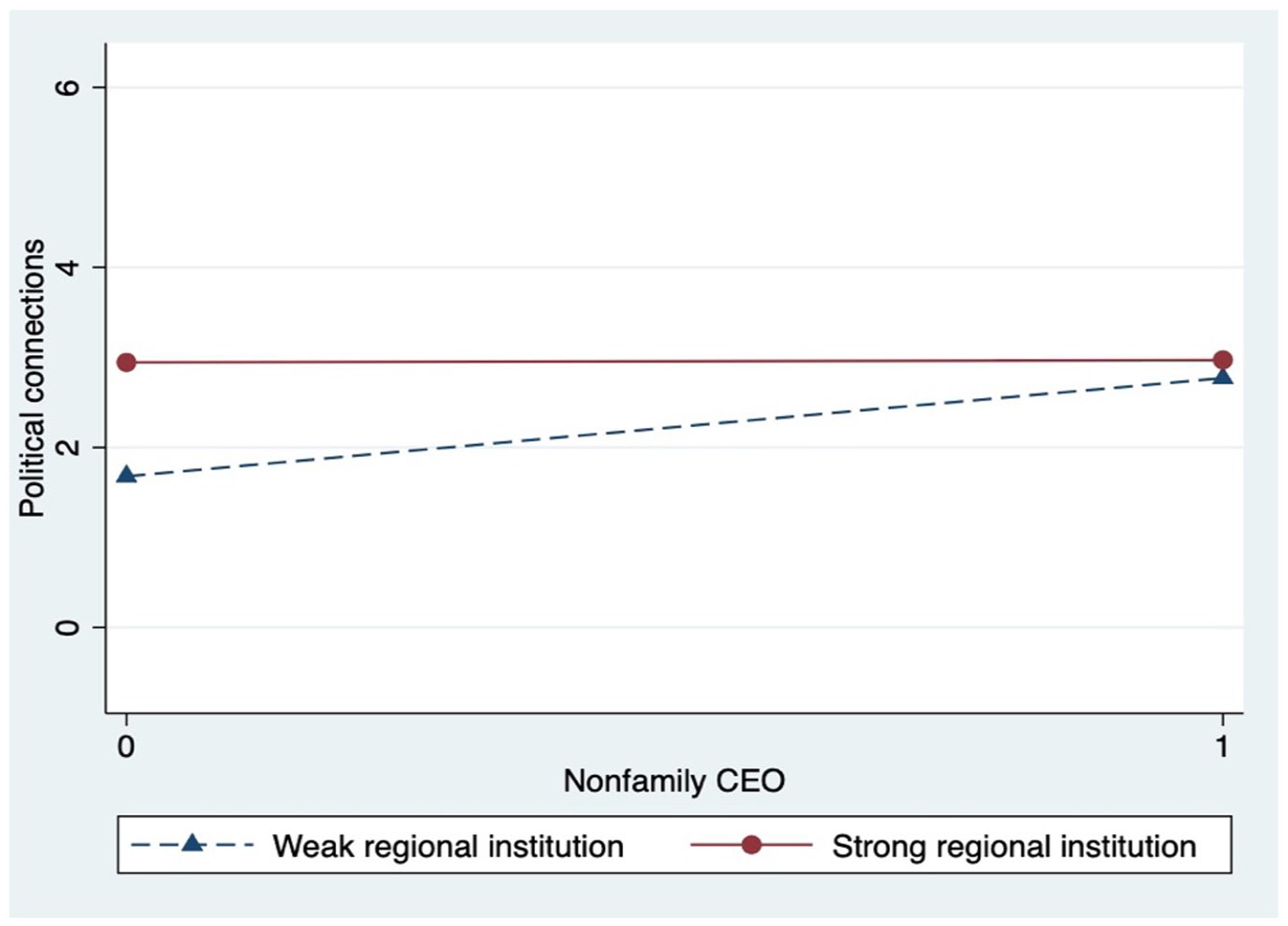

In Models (5) and (6), we test the moderation effects of slack resources and regional institutions. Our results support Hypothesis 3, by showing that slack can weaken the positive relationship between nonfamily CEO and political connections (coefficient = −0.464, p < .05). It is illustrated in Figure 3 that nonfamily CEO has a positive effect on political connection, and the slope is flatter when the family firm has more slack resources. Results also suggest that institutional development has a negative moderation effect (coefficient = −0.053, p < .05), supporting Hypothesis 4. As Figure 4 shows, the positive relationship slope between the nonfamily CEO and political connection is steeper in regions with less developed institutions. On the contrary, the slope appears flat in regions with well-developed institutions, meaning there is little difference in forming political connections between firms led by family and nonfamily CEOs. It is consistent with our prediction that the two types of CEOs may no longer have distinctive attitudes toward building political connections, given the declining benefits and costs in such an institutional environment.

Moderating Effect of Slack Resources

Moderating Effect of Regional Institution

Model (7) shows our full model, where we find all consistent results supporting our hypotheses.

Robustness Checks

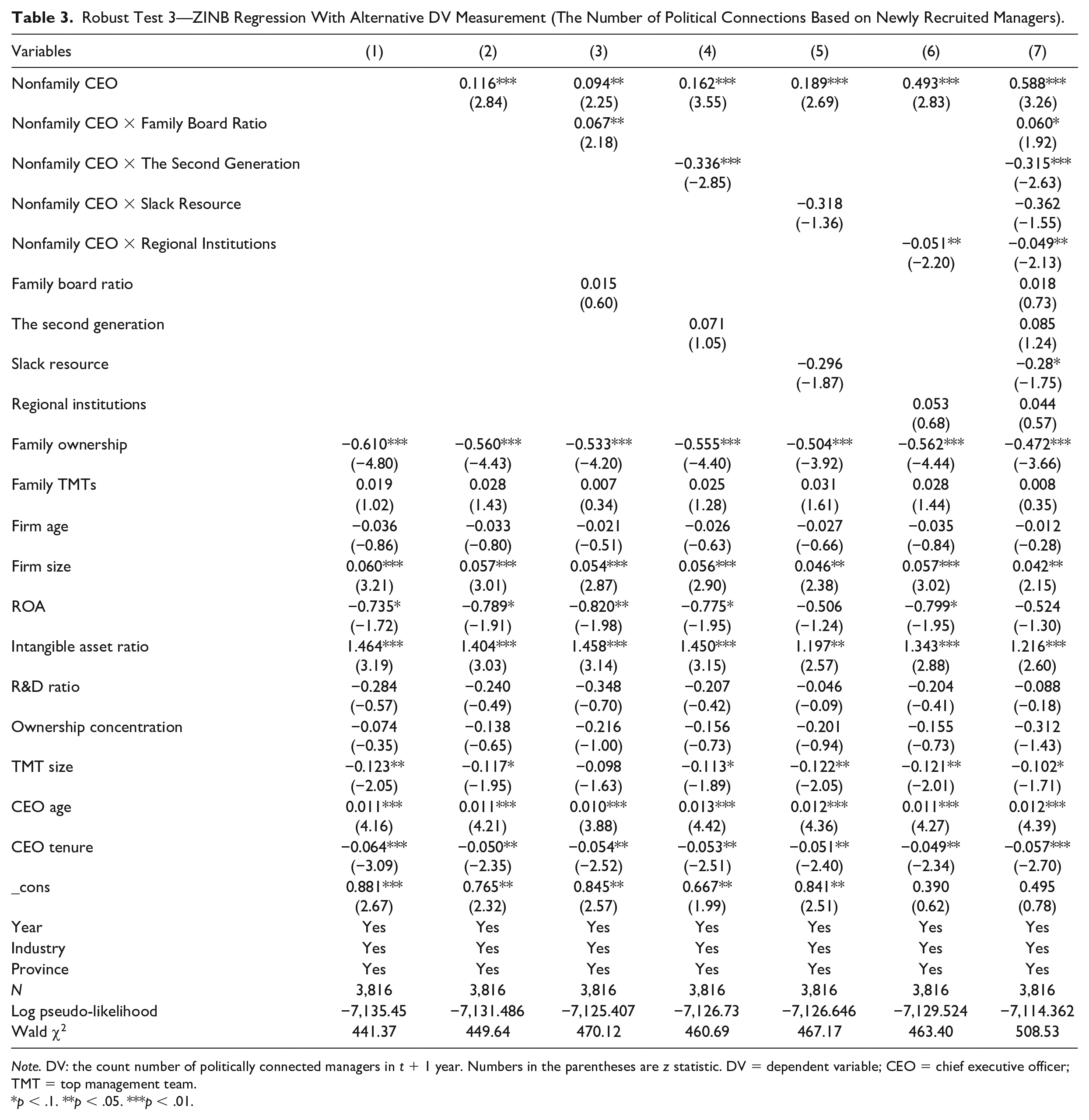

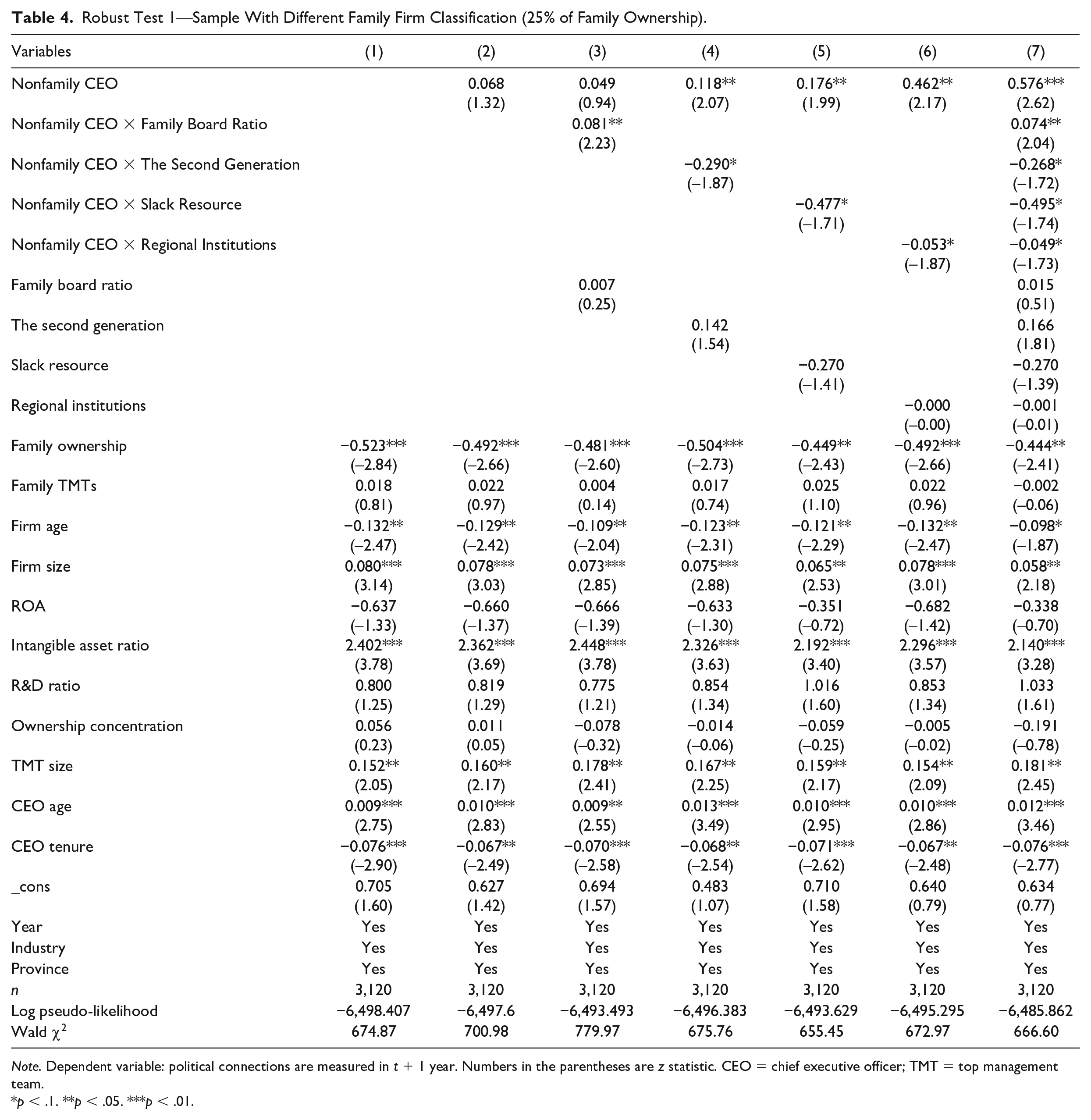

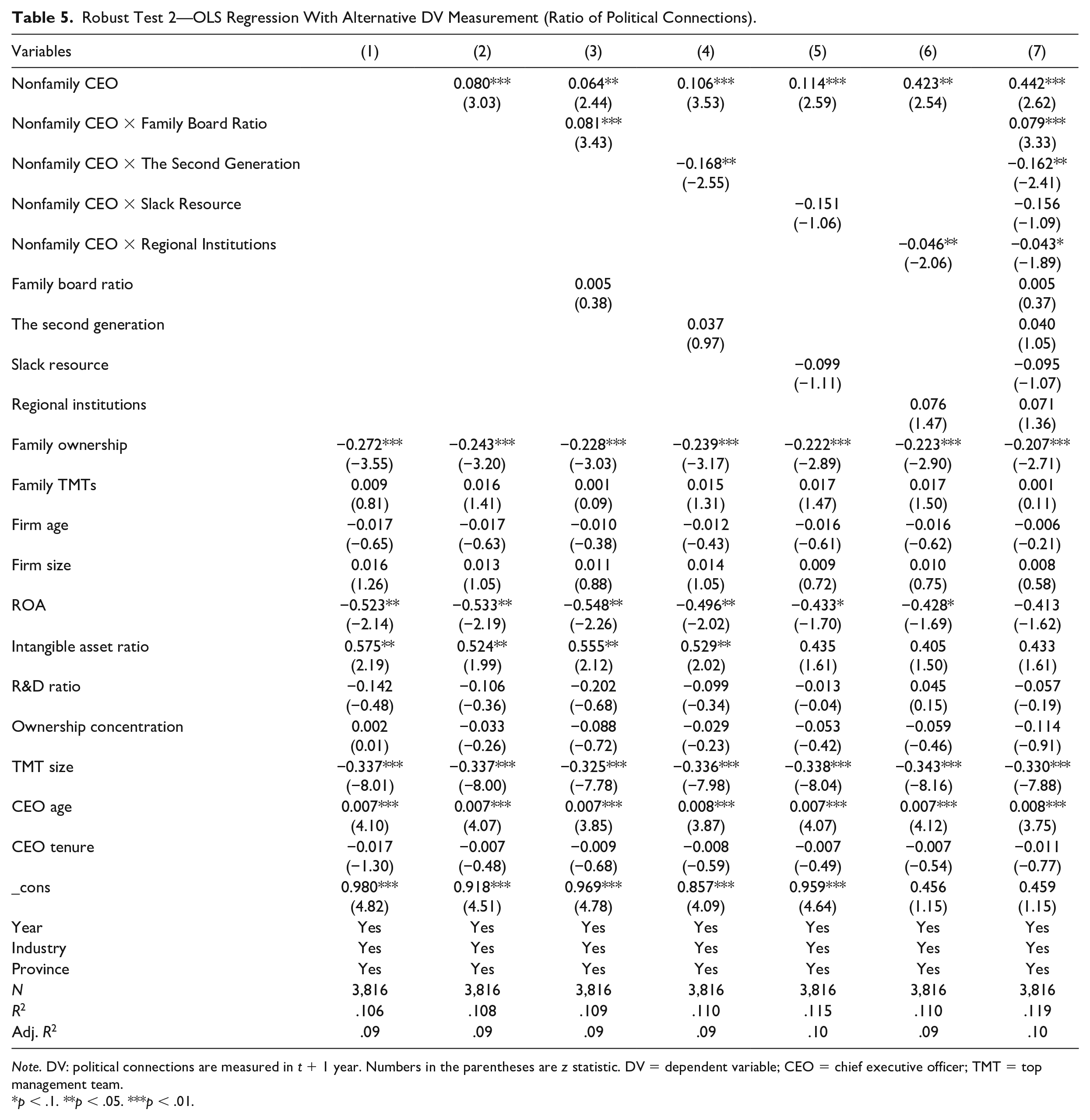

We conducted several robustness checks based on alternative samples, measurements, and alternative analysis methods. First, although the CEO usually plays a role in designing the board of directors (Cohen et al., 2012), we are concerned with the potential power constraint on them in family firms. For example, it is possible that nonfamily CEOs have more authority in recruiting managers than appointing board members. Thus, we adopt an alternative measure for the dependent variable, that is, the hiring of politically connected managers (excluding board members) to test our hypotheses (shown in Table 3). We found largely consistent results, which lends further support for our model. The only exception is that the negative moderating effect of slack resource becomes insignificant. Provided the alternative measure reflects nonfamily CEOs’ power in family firms more closely, this finding could indicate that slack might not be very effective in alleviating nonfamily CEOs’ bounded reliability in juggling the economic and SEW goals. Second, due to the high ownership concentration in Chinese firms compared with Western firms (Xu et al., 2019), we used a sample of family firms with more than 25% of family ownership as the family firm threshold and reran our models (shown in Table 4). We found very consistent results. Third, we used the ratio of political connections as the alternative dependent variable to test our hypotheses and found consistent results (shown in Table 5). Last, we conducted a Poisson fixed analysis and consistent results were found. Due to space limits, we do not show the results here. The details are available upon request.

Robust Test 3—ZINB Regression With Alternative DV Measurement (The Number of Political Connections Based on Newly Recruited Managers).

Note. DV: the count number of politically connected managers in t + 1 year. Numbers in the parentheses are z statistic. DV = dependent variable; CEO = chief executive officer; TMT = top management team.

p < .1. **p < .05. ***p < .01.

Robust Test 1—Sample With Different Family Firm Classification (25% of Family Ownership).

Note. Dependent variable: political connections are measured in t + 1 year. Numbers in the parentheses are z statistic. CEO = chief executive officer; TMT = top management team.

p < .1. **p < .05. ***p < .01.

Robust Test 2—OLS Regression With Alternative DV Measurement (Ratio of Political Connections).

Note. DV: political connections are measured in t + 1 year. Numbers in the parentheses are z statistic. DV = dependent variable; CEO = chief executive officer; TMT = top management team.

p < .1. **p < .05. ***p < .01.

Discussion

Our study explores how family firms’ propensity to form political connections varies according to the CEOs’ family affiliation. It answers the call to bridge the family business literature and corporate political activity (CPA) literature, which are both fast-growing but little intersected (Soleimanof et al., 2018). Using the data from China, we found that firms led by nonfamily CEOs are more likely to build political connections and that such difference is contingent upon family involvement, organizational slack, and institutional environment, which shape these CEOs’ task complexity. Based on this, the study contributes to the literature as follows.

First, the study advances the understanding of family firms’ political activity in several ways. The CPA literature recognizes the downside of political connections, but little work has analyzed it alongside the well-documented benefits (Lebedev et al., 2021). Likewise, family business scholars began to caution against the detrimental outcomes of political activity (Combs et al., 2020), but few attempt to capture the “dual effects” in the analysis (Ge et al., 2019). We address the gap by highlighting the paradox of political connections and further delineating it in the family business context. It lays a solid conceptual basis for scholars to continue investigating the dilemma family firms would face regarding political connections or activities.

The paradox we describe is relevant to family firms worldwide because building political connections is a common nonmarket strategy (Mellahi et al., 2016). However, it would be more salient in emerging markets than developed countries. Taking China as an example, there is still considerable economic value attached to political connections (Burt & Opper, 2020; Haveman et al., 2017). Meanwhile, these connections have a high chance of inducing risk for politically linked firms (Y. Xu, 2018; You & Du, 2012) because the government may intend to manage the economy and businesses directly (Fligstein & Zhang, 2011). It is also challenging to forecast political turnovers and changes in China due to its centralized power and opaque political system (H. Li & Zhou, 2005; Zhong et al., 2019). Although China has only one ruling party, internal power conflicts and drastic incidents within the political regime are not uncommon (L. X. Liu et al., 2017).

Thus, we suggest family firms in emerging markets or transition economies should be extra vigilant about handling political connections. A crucial issue for scholars to consider is that, can these firms obtain the benefits while safeguarding from the negative consequences at the same time? For example, what might be the optimal “political proximity” for firms? Likewise, would family firms be able to “buffer” political liabilities by, as Dieleman and Boddewyn (2012) recommended, using their governance structure as a mechanism? Answers to these questions could have important practical implications for family firms.

Furthermore, the study helps to reconcile the mixed views on whether family firms are more active politically than nonfamily firms (Combs et al., 2020; Dinh & Calabrò, 2019; Hadani, 2007). Specifically, it reveals that not all family firms are the same, and those led by family and nonfamily CEOs display distinct levels of forming political connections. This directs attention to family firm heterogeneity (Daspit et al., 2021; Jaskiewicz & Dyer, 2017). Our approach corresponds with Chua et al. (2012), who attributed the inconsistent findings in previous research to treating family firms as a whole and overlooking their internal variance. Future scholars should continue looking into this aspect because family firm heterogeneity in political activities remains largely uninvestigated. They may explore, for example, other than the CEO’s family status, what factors could also act as the source of family firms’ variance in political connections (Chua et al., 2012). Such efforts will advance the current literature. After all, as Neubaum and Micelotta (2021) reiterated lately, comparative studies of family and nonfamily firms “no longer provide the same level of theoretical novelty that similar studies once did” (p. 243).

Second, the study contributes to the literature on nonfamily CEOs. Although research presents ample evidence of the difference between these top outsider executives and their family counterparts (Tabor et al., 2018), the reason for the phenomenon is still controversial, primarily owing to the debate on opportunism (Huybrechts et al., 2013; Madison et al., 2016). For example, do nonfamily CEOs care more about individual interests like financial income and job security but less about SEW? The study reconciles this issue by introducing a novel perspective. Based on the theory of bounded reliability, we regard nonfamily CEOs as pro-organizational, which challenges the agency theory; yet we do not take for granted that these CEOs will behave like family members, as the stewardship theory may assume. As such, the study intends to move beyond the agent–stewardship dialectics.

The study further proposes nonfamily CEOs’ bounded reliability by explicating their cognitive and behavioral logics. Such application of the theory is rare in literature (Kotlar & Sieger, 2019). Importantly, we demonstrate that these logics present a compelling framework to synthesize and explain many of these CEOs’ distinct traits compared with their family counterparts. Future scholars may draw from our work to interpret their findings from an alternative theoretical lens. For example, in recent studies, Kelleci et al. (2019) claimed nonfamily CEOs have “less worrying” personalities than risk-averse family CEOs. H. C. Fang et al. (2021) asserted that nonfamily managers are “narrow-framed” while considering risky strategies compared with the “broadly framed” family decision-makers. According to these authors, narrow-framing refers to the tendency of people to emphasize short-term and tangible gains and losses but underestimate future problems. These notions echo nonfamily CEOs’ bounded reliability, such as time-discounting bias and identity discordance.

Third, based on the above, the study contributes to the theory of bounded reliability. While Verbeke and colleagues introduced bounded reliability originally to explain “why firms fail,” we demonstrate it can enhance the understanding of managerial decision-making in much broader contexts. This is meaningful given the theory is still at the early stage of development. Particularly, we show the theory offers much to family business research. Based on our work, scholars could, for example, continue probing nonfamily CEOs’ bounded reliability and its impact on firm strategies, especially those with complex effects like political connections and risky entrepreneurial behaviors (Kotlar & Sieger, 2019). They could also combine bounded reliability with other influential theories in the family business field. For example, how does bounded reliability play a role for nonfamily CEOs in mixed gambling (Fuad et al., 2021; Gómez-Mejía et al., 2014)? Such efforts will deepen our understanding of how and why family firms make critical strategic choices that have distinct effects on their financial wealth and SEW. Indeed, considering bounded reliability as a vital micro-foundation construct relating to the cognitive aspect of managers (Verbeke et al., 2021; Verbeke & Greidanus, 2012, 2015), our view echoes De Massis and Foss (2018) recommendation of extending, enriching, and refining the current knowledge on family firms with a microfoundational focus.

Moreover, how to economize bounded reliability is a critical inquiry but little researched (Kano & Verbeke, 2015; Verbeke & Greidanus, 2012). The study contributes by examining a set of organizational and environmental moderators. First, these moderators are derived via the lens of task complexity. Although the study does not examine task complexity directly, our findings offer preliminary support for the link between this construct and bounded reliability, which remains somewhat intuitive in the literature. Second, the study implies that while firms may curb bounded reliability through certain activities (e.g., family involvement), some factors that induce bounded reliability are external and thus beyond firms’ control (e.g., institutional environment). It underlines the challenge of dealing with bounded reliability in practice. The study also suggests distinct impacts of family board ratio and generational involvement on nonfamily CEOs’ bounded reliability. This is novel because although scholars have widely discussed the role of family involvement in influencing nonfamily members’ behavior (Chua et al., 1999; Kammerlander et al., 2020; Yang et al., 2020), they pay little attention to whether and how those different ways of involvement may have opposite effects.

The study has limitations, and future research can investigate our findings and extend the study in several directions. First, we measure political connections by the hiring of individuals with a political background, such as former government officials. There could be other ways of connecting with the authorities (Deng et al., 2018). Further research can, for instance, examine the connections cultivated through intimate personal relationships (Zhang et al., 2016) or expand our study more broadly by capturing firms’ other political activities, such as lobbying and political donations (Combs et al., 2020). The latter requires the researcher to look beyond China where the activities are legally allowed and prevalent. These efforts should help endorse our study as we anticipate similar results to ours.

Second, the study presumes the influence of CEOs on family firms’ strategic decisions. While it is common in research, how and to what extent the influence may occur is complicated, given that family members often retain senior management roles, such as the Chair of the company. We regard this as an important limitation and urge future research to investigate how nonfamily CEOs’ choice of political strategy, as a result of bounded reliability, may be approved or declined by the controlling family. Answering such questions demands a close look into family firms’ governance and decision-making dynamics (Daspit et al., 2018). For example, scholarly works on faultlines (Minichilli et al., 2010; Vandebeek et al., 2016) could offer valuable insight into this respect.

Third, we used bounded reliability to explain the difference between family and nonfamily CEOs. However, our study could not examine directly the underlying theoretical mechanism due to the archive data limitation. Future studies may address this by observing these CEOs’ bounded reliability more closely and how it shapes their perceptions of the paradox of political connections, and further the intention to hire politically connected upper echelons. For such detailed and complementary findings, we encourage researchers to employ qualitative research designs like a case study.

Fourth, while the study examines the impact of nonfamily CEOs on political activity, future research can extend it toward firm performance. Given the complex effects of political connections, we suspect the result to be consistent with previous findings that the impact of nonfamily CEOs on firm performance is positive in the short term but might turn negative in the long term (Waldkirch, 2020).

Finally, we used a sample of publicly listed family firms in China to test hypotheses. Although it is a suitable context, there are some unique characteristics of these firms. For example, these listed family firms in China are relatively young and mostly under control of the first and second generation, so that the family dominance in firm management is relatively high (S. Jiang & Min, 2022; Yu et al., 2020), which could make the bounded reliability issue more salient. To reduce such bias, future research could choose different contexts to investigate nonfamily CEOs’ bounded reliability.

Research Questions

Our study examines in family firms how the presence of a nonfamily CEO affects the firm’s likelihood of forming political connections. To do so,

Our study attempts to unravel the complex effects of political connections regarding family firms.

Our study seeks to develop a novel perspective on the difference between family CEOs and nonfamily CEOs by drawing on the theory of bounded reliability.

Practical Implications

Our study highlights the benefits and risks of forming political connections. Therefore, family firms need to take a more balanced view of undertaking political strategy.

Our finding shows when it comes to political strategy decisions, nonfamily CEOs tend to focus more on the short-term benefits while overlooking the long-term risks. Family owners, therefore, should pay more attention to this and moderate nonfamily CEOs’ decisions if necessary.

Our results suggest that it could be more important for family owners to monitor nonfamily CEOs’ decisions in political strategy when the firms have more family members on the board, fewer slack resources, and are located in less developed institutional environments.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.