Abstract

By building on foundations from psychology, we aim to enhance academic understanding of the advising process in family businesses. We find evidence, based on rich qualitative data, suggesting that trust serves as a key construct in the relationship between family businesses and their advisors. In particular, we empirically show and theorize that trusting relationships evolve via a nonlinear process characterized by a constant interplay between cognitive and—increasingly important—affective assessments of family business trustors. The following types of trust emerge from these internal assessments: an intention to trust, which develops into perceived trust and finally results in behavioral trust.

Introduction

Compared with other types of firms, family businesses, which are characterized by an overlap between the business and the family, typically consider a wider range of goals, including noneconomic goals that are strongly affected by socioemotional wealth (SEW) considerations (Berrone et al., 2010; Gómez-Mejía et al., 2007). In family businesses, pursuing goals related to SEW leads to idiosyncratic judgments, for example, regarding external collaborations (De Massis et al., 2016; Duran et al., 2016; Gagné et al., 2014; Holt et al., 2017). That results in the establishment and maintenance of unique interpersonal relationships with family business external stakeholders (Sharma, 2004).

Third-party advisors represent an important group of family business external stakeholders and have been found to highly affect cognitive and affective processes within family businesses. On a cognitive basis, which is broadly defined as the internal processing of information related to observable actions (McAllister, 1995), advisors provide knowledge, recommendations (Hiebl, 2013; Reay et al., 2013) and missing information (Michel & Kammerlander, 2015); serve as facilitators in important transitions, such as intergenerational succession (Salvato & Corbetta, 2013); and influence processes, such as facilitating adaptive sensemaking (Strike & Rerup, 2016). On an affective basis, which is defined as the internal processing of emotions related to subtle feelings (McAllister, 1995), third-party advisors use their own feelings and empathy to become attuned to family business members to capture, influence, and facilitate attention (Strike, 2013). For example, advisors reduce feelings of uncertainty (W. D. Davis et al., 2013) by engaging in mediating activities, including unearthing and alleviating latent negative emotions (Bertschi-Michel et al., 2020). In such contexts, third-party advisors are often identified as the most trusted advisor that largely influences individual- and firm-level outcomes (e.g., Bertschi-Michel et al., 2019; Distelberg & Schwarz, 2015; Naldi et al., 2015).

However, while prior research has revealed the importance of third-party advisors, academic knowledge regarding the family business’s actual decision process concerning how advisors enter and build a relationship to become trusted advisors is surprisingly limited (Strike, 2013). Hence, family business research needs to increase its knowledge of the internal, microlevel processes (De Massis & Foss, 2018) and underlying mechanisms resulting in relationships promoting advice taking (Strike et al., 2018). Therefore, we pose the following research question: How does the relationship between family businesses and their third-party advisors evolve during advice seeking, advice giving and advice taking?

As relationship building is a phenomenon essentially driven by both cognitive and affective processes, we conducted our investigation by viewing the relationship building between family businesses and their trusted advisors through a psychological lens. We adopted a qualitative approach by conducting 36 semistructured interviews with both family business owner managers and family business advisors. The synthesis of our data with foundations from psychology leads to a nuanced process model that contributes to the current family business literature in at least two important ways.

First, our study contributes to a more nuanced understanding of the underlying processes of how third-party individuals actually become the most trusted advisors in family businesses (Strike et al., 2018). We thereby add to the frequent call to increase understanding of family businesses’ idiosyncratic microlevel processes determining the relationship of these businesses with external parties (De Massis & Foss, 2018; Sharma et al., 2020). Psychological foundations serve as a way to disentangle the interplay between family businesses and external parties (Sharma et al., 2020), such as the emergence of specific subtle biases and heuristics when deciding whom to rely on when seeking advice (e.g., Strike, 2012, 2013; Strike et al., 2018). Throughout the different stages of the advising process, three types of interpersonal trust emerged as main drivers that promote the evolution of increasingly deeper levels of trust: an initial intention to trust, which further develops into perceived trust and is finally manifested and displayed as behavioral trust. For all three types of trust, we observed that family business trustors’ internal appraisals were largely driven by aspects related to the trustors’ individual personality (C. Davis et al., 2007), which can be expected to have a particularly strong influence in family businesses (Carney, 2005)—for better or worse (Judge et al., 2009)—and by the pursuit of goals related to SEW such as sharing of similar values or key stakeholders’ agreement (Berrone et al., 2012). Hence, family business idiosyncrasies are crucial in developing a trusted advisor relationship at different levels.

Second, by integrating and contrasting our findings with for the field of family business research novel concepts from psychology, we increase understanding of the implications of psychological foundations for the management of family businesses in the context of advising. Our data show that when initially establishing a relationship with an advisor as a trustee, family business trustors reduce uncertainty by judging and weighting observable characteristics to create cognitive assessments of the advisors’ perceived trustworthiness (Mayer et al., 1995). Such behavior can be explained by the psychological concepts of the “judge-advisor system” (JAS) or “weight of advice” (WOA) (Bonaccio & Dalal, 2006; Budescu & Yu, 2007); These concepts suggest that family business trustors internally assess certain weights to different attributes of the advisor. Furthermore, we provide evidence of a constant interplay between cognitive and affective appraisals (e.g., Chowdhury, 2005) and find that during the process, increasing levels of interpersonal trust typically go along with affect-driven heuristics to decide whether trust is perceived or displayed. Such internal judging processes have not, until now, been conceptually distinguished or theoretically explained in the family business literature.

Theoretical Background

Family Businesses and Trust Building

There are various definitions of family businesses from multiple perspectives (Sharma, 2004). First, the current literature emphasizes the importance of family control over the business through ownership (Calabrò & Mussolino, 2013) and its generational transfer, meaning that the family business is in at least its second generation with the intention of continuing as a family business (Astrachan et al., 2002). Second, the family must be actively managing the business; active management of the business by the family is typically defined as one family member being active in a leading role within the firm (Fernández & Nieto, 2006). Third, there is a self-perception of the business as a family business (Kellermanns et al., 2012). Based on these considerations and the seminal work by J. H. Chua et al. (1999), in this study, we define a firm as a family business if at least 50% of the business is family owned, the firm is at least in the second generation and at least one family member is a member of top management.

According to this definition, particularly in this type of firm, the business and its ownership are closely interrelated with the family (Tagiuri & Davis, 1996). Consequently, multidimensional goals related to SEW involving family, business, and ownership reference points (Berrone et al., 2012) strongly affect the establishment and maintenance of relationships between family businesses and nonfamily actors (Hauswald & Hack, 2013). As goals related to SEW are driven mainly by affective elements, such as the identification of family members with the firm, emotional attachment and family control (Berrone et al., 2012), interpersonal trust between a family business and an external actor is the key connecting factor (Sundaramurthy, 2008). Previous family business research has found that trust serves as a governance mechanism (Eddleston et al., 2010), reduces transaction costs (Steier, 2001), fosters cooperation (Kudlats et al., 2019), increases a family business’s social capital (Cabrera-Suárez et al., 2015; Pearson & Carr, 2011) and, thus, constitutes a competitive advantage (Steier, 2001; Sundaramurthy, 2008). Surprisingly, to date, how trust building processes in family businesses evolve remains a black box (Sundaramurthy, 2008); thus, a clear understanding of the internal psychological processes affecting family business’s assessments of the risk (uncertainty) associated with trusting a nonfamily actor is lacking (Jiang et al., 2018; Sundaramurthy, 2008).

Interpersonal trust is defined as an expectation held by an individual about the perceived behavior of another individual (Rotter, 1967) and further developed as the willingness to be vulnerable to the actions or advice of another party (J. H. Davis et al., 2000). Interpersonal trust can be summarized as “a psychological state comprising the intention to accept vulnerability based upon positive expectations or behavior of another” (Rousseau et al., 1998, p. 395). To build trust, individuals must initially be willing to test or enter a trust situation. Then, trust can be built through similar motives that lead to perceptions of trust and felt security (Simpson, 2007). This phase leads to the willingness to take risks and, thus, place trust in another party (Mayer et al., 1995). Trust building between a trustor and a trustee results from social interactions and the individual characteristics of the two parties. On the one hand, a trustor’s individual willingness to trust others or likelihood of trusting others is a prerequisite for trust building. The literature assumes that this willingness is a stable factor in individuals; this willingness is referred to as the propensity to trust. On the other hand, factors, such as the trustee’s individual ability (skills and competencies), benevolence (caring for others) and integrity (principled acting) determine trust building. These factors lead to perceptions of predictable, dependable behavior; these perceptions are referred to as the perceived trustworthiness of a trustee (Mayer et al., 1995).

Such trust building based on cognitive reasoning regarding observable criteria, including professionalism or role performance, is called cognition-based trust (Chowdhury, 2005). Cognition-based trust is positively associated with tangible resources (such as the provision of task advice (R. Y. J. Chua et al., 2008) and, consequently, is present in professional relationships (Chowdhury, 2005). Interestingly, cognitive processes of assessment do not seem to be entirely rational, as cognitive biases (i.e., trustors tend to confirm their initial beliefs and attitudes about a trustee) frequently occur (McKnight et al., 1998).

One reason for such bias is that trust frequently involves a highly affective component. Thus, trust building is based primarily on shared values, the citizenship behaviors of the trustee, frequent informal interactions, and resulting feelings of intimacy and emotional ties (Chowdhury, 2005). Hence, trust building also involves empathy, rapport, and self-disclosure and can be referred to as affect-based trust, which is associated with friendship ties or personal guidance (R. Y. J. Chua et al., 2008) and, therefore, is present in personal relationships (Chowdhury, 2005). The literature widely agrees that affect-based trust based on care and concern is associated with deeper levels of trust (McAllister, 1995) and that close interplay occurs between cognitive- and affect-based trust (Williams, 2001). For example, the feelings-as-information model states that trustors use their affective states as a basis for cognitive assessments of a trustee’s ability, benevolence, and integrity; therefore, a trustee’s perceived trustworthiness depends on affective states (Schwarz, 1990; Williams, 2001). Moreover, affective states influence the trustor’s motivation to trust and whether a trustor engages in cooperative behavior toward the trustee. Hence, increasing our understanding of the combined influences of cognition and affect among different social groups (i.e., family businesses and advisors) on trust is important (Williams, 2001).

Most Trusted Advisors in Family Businesses

Advisors constitute an important group of external nonfamily actors on whom family businesses frequently rely (Reay et al., 2013; Strike, 2012; Strike et al., 2018). Particularly, when initiating fundamental strategic changes, such as succession (in which the firm and knowledge of how to lead the business are transferred from an older to a younger generation) (Shepherd & Zacharakis, 2000), family businesses frequently seek external advice. Thus, advisors can reduce information asymmetries and agency costs between the two generations (Michel & Kammerlander, 2015) and help in developing the competencies of the future leader (Salvato & Corbetta, 2013). During this intense process, both generations must trust their advisor when seeking answers regarding how to relinquish control of the business, how to transfer responsibility or what their future role will be after the transfer (Sharma et al., 2003).

An external advisor can provide crucial support in unearthing the often-hidden fears and uncertainties and subsequently engaging in emotion-alleviating activities (Bertschi-Michel et al., 2020). Additionally, during such processes, interpersonal conflicts frequently arise. Thus, an advisor can positively influence the relationship between the incumbent and successor by mentoring (Distelberg & Schwarz, 2015; Salvato & Corbetta, 2013) and acting as a troubleshooter who moderates between the two parties (Lane et al., 2006; Michel & Kammerlander, 2015). Another study adopting both psychological and management-related perspectives found that an external advisor can facilitate the adaptive sensemaking processes that unfold when a family business begins to doubt the initial assessments (Strike & Rerup, 2016). Specifically, an advisor can mediate individual sensemaking processes by inducing pause, slowing action and facilitating doubt that produces critical rethinking (Strike & Rerup, 2016).

In her seminal literature review, Strike (2012) distinguishes among the following three types of advisors: (1) formal, externally hired advisors; (2) informal advisors, such as spouses, close friends, or mentors (Boyd et al., 1999); and (3) advisory boards, which have legal standing and often provide advice regarding strategic, long-term-oriented questions (Strike, 2012). In the following discussion, we focus on formal advisors (such as accountants, lawyers, bankers, family therapists, and psychologists) who provide either expert knowledge or process guidelines (Kaye & Hamilton, 2004). Such skilled, professional individuals advising family businesses regarding complex questions at the interface of family, business, and owners (Dyer & Hilburt Davis, 2003) can be considered a firm’s most trusted advisor (Strike, 2013).

Often, the family is highly dependent on the trusted advisor, who is deeply embedded within the family and, in many cases, remains lifelong with the family business (Strike, 2013). With increasing age, family businesses more strongly emphasize emotional goals and retain their well-known most trusted advisor (Perry et al., 2015). However, to date, in the family business literature, knowledge regarding how such sources of advice become the most trusted advisor, that is, how an external individual gains the trust of a family business and how such a trust base ultimately affects whether advice is taken, is lacking (Strike et al., 2018; Sundaramurthy, 2008).

Method

Empirical Setting

To answer our research question, which evolves around why and how questions oriented toward understanding a process in a real-world context, we apply an inductive, qualitative case study approach based on Eisenhardt (1989) and Yin (1994). Thus, a multiple case study design was chosen to analyze the research focus in different contexts (Baxter & Jack, 2008) and to increase the validity and generalizability of the findings (Galloway & Sheridan, 1994).

Our sample consisted of 20 family businesses in Switzerland; these businesses fulfilled the following selection criteria: all firms had to be family firms according to our definition (i.e., at least 50% of the business had to be family owned, the firm had to be at least in the second generation, the top management team had to include at least one family member, and the firm had to consider itself a family firm); the firm needed to have experience in taking advice from external advisors; and the key informants had to be in a position where they could take advice from external advisors (typically family–internal chief executive officers (CEOs) or family owners).

We supplemented the interviews with the family firms with 16 interviews with family business advisors to triangulate the interview statements of the family businesses. To become part of our sample of advisors, the person or company had to self-identify as an advisor of family businesses. Furthermore, the firms and individuals were required to have past experience in advising at least one family business, and they had to have been paid for their advice. The advisors were required to provide an external perspective on the family business and not be directly involved (e.g., by being employed) in the family business.

Data Collection

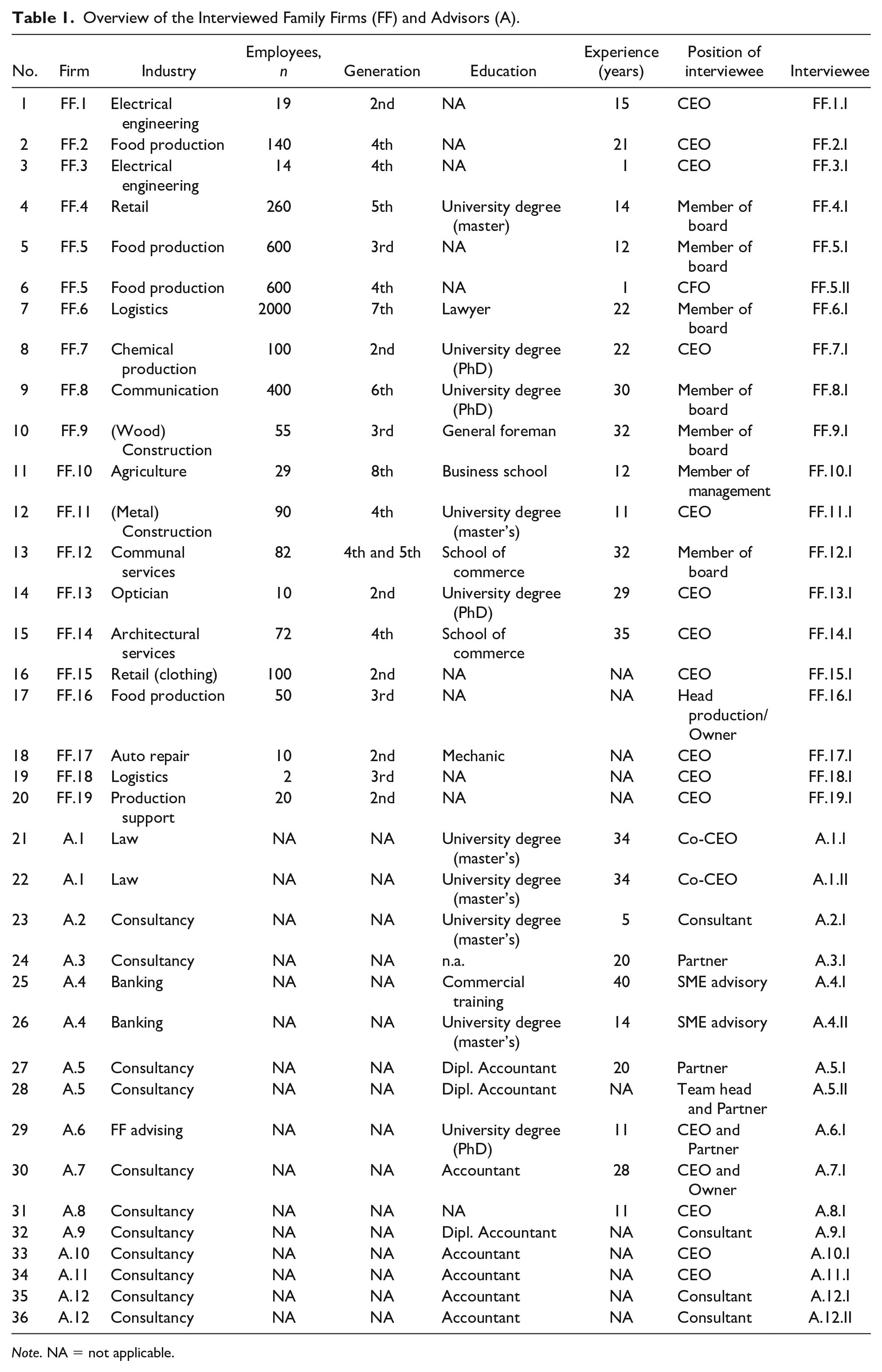

The main database for the present study consists of 36 semistructured interviews with family businesses and family business advisors. Table 1 presents an overview of the interviews conducted for the study. We collected data on the family businesses until saturation had been reached when comparing the interview statements. Especially in smaller family businesses, the (family) CEO is the person who ultimately decides whether to take advice. Therefore, we found a saturation point; that is, the themes in the interviews reoccurred and only marginally new information was added (Moser & Korstjens, 2018).

Overview of the Interviewed Family Firms (FF) and Advisors (A).

Note. NA = not applicable.

We found the key informant sampling strategy adequate and, hence, conducted one interview per family business (except for FF.5). We found the perspective of the individual advisor to be the most relevant to our research question. Other studies addressing research questions concerning advisors in family businesses have referred to the advisor as the unit of analysis (e.g., Strike, 2013).

Most interviews were conducted face-to-face and on the property of the family business or advisory firm. The interviews lasted between 19 and 117 minutes and led to 422 pages of transcripts. MaxQDA (VERBI GmbH, Berlin, Germany) was the coding software used. Whenever possible, the interviews were conducted by two researchers. To triangulate the findings from the interviews, we further collected secondary data and additional material about the companies with which the interviewees were associated. For all firms, we visited the company website and searched for general information about the company (e.g., main field of activity, company history, facts, and figures). When available, we downloaded and screened annual reports for useful information and systematically searched for press coverage that referred to activities related to interactions between the family businesses and their advisors. However, for most of the family businesses in the sample, such material was unavailable and kept private. Reports were available for eight of the companies, and press coverage related to the topic of our research was available for seven firms in the sample.

Data Analysis

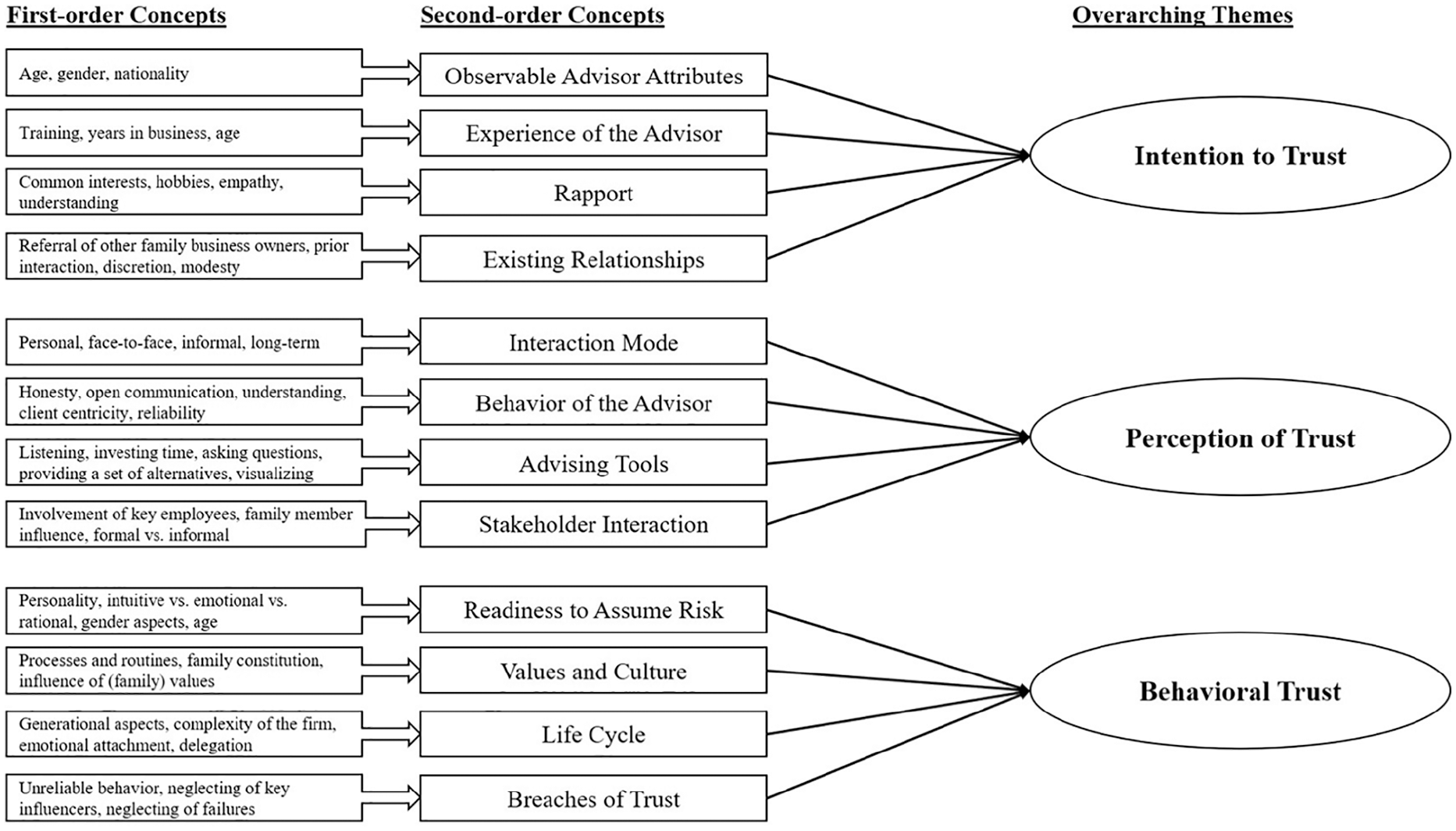

To analyze our data, we used inductive measures (Langley & Abdallah, 2016). To compare and recognize repeating patterns and to understand in depth the process of advising family businesses within and across cases by using a multiple case study (Eisenhardt, 1989), we inductively coded our material (interviews, emails, reports, and websites) (Glaser & Strauss, 1967). First, we extracted first-order concepts from the interviews (e.g., advisor communicates openly, “open communication”). In a subsequent step, we interpreted these concepts in the study context and aggregated them into second-order concepts (e.g., “advisor behavior”). This aggregation was an iterative process and undertaken by both authors’ alternating between the data and the literature. In the final step, we subsumed the second-order concepts in three overarching themes (e.g., “perceived trust”). The data structure is visualized in Figure 1, and a table providing an overview of categories and related quotes is presented in the appendix. The data structure comprises three levels of analysis, which is frequently applied in inductive qualitative research (Gioia et al., 2013).

Data structure.

To identify common patterns and themes across the cases (Eisenhardt & Graebner, 2007), we iteratively analyzed the data while contrasting the current literature (Eisenhardt, 1989), and we steadily refined emerging themes and patterns by revisiting single cases. Much of our efforts was dedicated to ensuring the reliability of our analysis. In keeping with Lincoln and Guba’s (1990) suggestions, we triangulated our data whenever possible by comparing the assessments of the family businesses with those of their respective advisors. Additionally, we followed up with emails to our informants to obtain missing details. Disagreements among the authors about interpretations of data were debated until consensus was reached. As soon as we identified a strong match between theory and data, we recommunicated with our informants and experts to validate our observations and to discuss alternative explanations. According to our discussions, we further refined our data structure several times. We drew visual maps (Langley & Truax, 1994), which, during data discussions and interpretations, were later condensed into the more general final model presented in this article. Finally, to provide high levels of transparency and replicability of our study, we followed the recommendations of Aguinis and Solarino (2019), who recently provided a set of 12 criteria to evaluate studies based on interviews with key informants.

Findings

In the following discussion, we describe our findings that emerged from the data in relation to the three overarching themes we inductively identified. These themes refer to different types of trust, as shown by the family business (trustor) toward its advisor (trustee), that evolve during the advising process and are as follows: intention to trust, perceived trust, and behavioral trust.

Intention to Trust

The first theme identified was the family businesses’ intention to enter an advising relationship and, thus, potentially trust a certain advisor (intention to trust). This overarching theme is based on factors influencing the relationship and trust building in the very beginning. We aggregated the observed factors into the following second-order concepts: observable advisor attributes, advisor’s experience, rapport, and existing relationships (including recommendations).

Observable Advisor Attributes

Our data show that when family business trustors assess an advisor, observable demographic attributes were the most frequently mentioned factors. However, many interviewees generally stated that age, gender, and nationality play only a minor role, as follows: “I would really think that age, gender, and nationality do not matter at all” (FF.11.I); some interviewees agreed that an advisor’s age influenced the perceived similarity between the parties; this perceived similarity fostered trust. Thus, an advisor “has a slightly better connection” (A.7.I) with family business actors who are of approximately the same age. However, many interviewees agreed that after having cleared the first hurdle, a younger advisor can also be perceived as competent, as shown in the following quote: Sometimes, it is an advantage to be a little older. A twenty-five-year-old advisor may be perceived as less competent than a fifty-year-old who has been around longer. It is easier, at least at the beginning. I think that once the younger one has convinced the family business actor, then you certainly believe them as well. (A.11.I)

In addition, the interviewees reported mixed effects regarding the advisors’ region of origin. The region from which an advisor originates can be both an advantage and a disadvantage. Differences have been noted between urban and rural areas. Family businesses in rural areas tend to consider the origin of an advisor, while the origin of an advisor is somewhat unimportant for family businesses from cities: “I would not care where he came from. Of course, you have to be able to communicate, but whether he is German or Austrian does not matter” (FF.16.I).

Advisor Experience

An advisor’s education is mentioned by most interviewees as a factor that they simply take as given, as shown in the following quote: “I simply take the specialist knowledge for granted” (FF.19.I); an advisor’s experience is perceived as crucial in creating an intention to enter a trusting relationship. Most interviewees stated that education and training alone are no guarantee of the quality of advice; instead, it is rather important to the interviewees that an advisor has already been active and successful in the industry in which they are advising a firm. If the advisor has already conducted many successful consultations, the interviewees are rather inclined to evaluate the advisor as competent. Some interviewees further mention that examples of successful consulting serve as proof of an advisor’s experience. Interestingly, this view also applies for examples of failure when a company did not follow the advisors’ advice.

Rapport

Regarding aspects of an advisor that create affection among family business trustors, some interviewees stated that they consider their feelings (such as liking the advisor as a person due to his or her specific nature or disposition) more important than observable criteria (such as experience). In particular, one interviewee stated that he needs to sense that “this advisor is a nice person” (A.4.II). He even perceived this aspect as the most important factor when choosing an advisor, as shown in the following quote: “Basically, I am sure it is about liking each other. If you don’t have this feeling and do not like to talk and work with this person, then trust is never built” (A.4.II).

Some interviewees further stated that having interests in common with an advisor in their private lives can facilitate the beginning of a professional relationship because having common interests creates a feeling of similarity and, thus, of liking each other. Advisor A.4.II, for example, attends the games of FF.14.I’s hockey club, thereby creating a close personal connection: “That is also certainly an important point, that you are at the games and show them something like that, that you share his passion with him.” (A.4.II). In turn, FF.14 spoke positively of the advisor: “With this guy [A.4.II], that is almost something [like] a friend, he also comes to watch games.”

Existing Relationships

Moreover, many of our interviewees stated that to assess an advisor, they evaluate the personal references of the advisor’s prior cases and reputation for discretion and integrity. In this context, the interviewees emphasized that advisors should be discreet, meaning that what the family business tells the advisor remains with the advisor. Almost all interviewees stated that integrity behavior is required for every advisor.

Several interviewees also mentioned that it is important that the advisor and advisee initially get to know each other in a rather informal personal conversation. Thus, a sense of a common history and the sharing of values are decisive for a successful relationship. Hence, how an advisor initially contacts the family business also considerably influences building the relationship and gaining trust. Advisors who were recommended by a close confidant of the family business have higher acceptance rates than advisors who were not.

Perceived Trust

We identified perceived trust as the second main theme. The intention to trust builds the basis for subsequently establishing a perception of trust that interacts with advisor actions fostering or hindering trust building. We aggregated the aspects of perceived trust into the following second-order concepts: interaction mode, advisor behavior, advising tools, and stakeholder interaction.

Interaction Mode

Family business trustors attach great importance to personal contact with their advisors and prefer face-to-face meetings, as noted by FF.13.I, who says that they initially attempted to conduct meetings via telephone conferencing, video calls, or similar communication channels. However, they realized that there were more misunderstandings when meetings occurred at a distance than when meetings were conducted in person. In contrast, the preferences regarding the closeness of the relationship between the advisor and the advisee are very subjective. Some family businesses seem to prefer a relationship that is purely businesslike, “that is sporadic, and that maintains a certain distance” (A.5.II), whereas others prefer to have a more “intimate relationship with the advisor” (FF.14).

The frequency of interaction does not seem to influence trust building. However, many of our interviewees stated that they often also appreciate a mostly informal and quite spontaneous interaction. For example, with more project-based issues, the family business may also contact the advisor briefly and directly to ask for help, for example, by making a phone call without always setting a formal meeting. In such interactions, the relationship is usually already perceived as quite strong and trustful. Similarly, many family businesses told us that they seek a long-term relationship with their advisor: If you have a new advisor every two years and you have to tell him from A to Z what you [the company] are actually doing, then the [owner/family business trustor] will say after the third change, ‘you know, there are other banks. There, I have had the same advisor for 10 years now. (A.4.II)

Advisor Behavior

Concerning advisor behavior, our interviews revealed that certain advisors, especially bankers, are subject to the prejudice that they may simply be salespeople; therefore, such advisors must prove themselves to be open and reliable before being able to establish a perception of trust. In particular, honesty was mentioned by all family businesses as a prerequisite for future advising. The family businesses, thus, told us that to perceive an advisor as honest, they require open communication without fear of potential conflicts. External advisors are often the only people who openly address problems in the company and who directly point them out to the family business: “What is also much appreciated is openness. An external advisor can actually tell a client that he is the problem. Others cannot, and there are actually people [clients] who appreciate that because they are not used to this feedback” (A.8.I). Additionally, the advisor “must also spend time getting to know the family’s circumstances” (A.1.I; FF.4.I).

Furthermore, many interviewees mentioned the ability to be understanding, meaning that being people oriented and making the advisee’s needs central is of utmost importance for advisors, as shown in the following quote: I say you must like people when advising them, and you sometimes see that this is not the case. That someone is a top expert, but if he does not find access to people, he will never be perceived as an advisor. [Advising] needs a lot of empathy. (A.4.II)

Hence, the advisor’s ability to understand the position of the advised family business and show such an understanding of their concerns requires a holistic perspective of the company. In contrast, if the advisor labels the problem small and aims to quickly sell a standard solution without truly addressing the company, the probability of advice taking decreases. Additionally, proposals for radical changes are often rejected; however, “the more actively the family business seeks advice, the greater the likelihood that it will accept the advice received” (A.4.I; FF.8.I)

Similarly, “reliability is one of the crucial factors” for building a trusted relationship (A.4.II). However, this aspect does not necessarily mean that a failure or that wrong advice will immediately lead to a loss of trust. Instead, many interviewees told us that “bad advice” can also be an opportunity to strengthen the relationship of trust, given that the advisor admits the mistake and continues to support the family business in solving the issue: “You can make mistakes, but it will be forgiven if you stand by them and admit them. That can always also be a chance for a corrective approach” (A.7.I).

Advising Tools

According to our interviewees, advisors use different strategies and techniques to achieve perceptions of trust in the family business. An essential element that is repeatedly mentioned is “to be able to listen” (A.5.II) and to take time to actually understand the needs of a family business and to become familiar with the firm. In general, open conversations are a central tool of advice giving. However, the key is not only to listen but also to ask questions, question solutions, and discuss alternatives. Nevertheless, this process can lead to heated discussions and conflicts. Ultimately, the advisor’s ability to listen and ask questions is needed to achieve successful solutions and build trust in the family business.

Presentations and visualizations are supporting tools used to show different possibilities and scenarios and make them understandable to the family business. The more comprehensible and descriptive a solution is, the greater the likelihood that it will be accepted. Thus, an advisor’s central task is to gain the confidence of the responsible family members. This task is particularly successful when family members are guided such that they themselves develop the solution.

Stakeholder Interaction

Interviewees stated that the hierarchy in family businesses is typically flat, the communication channels are short and informal, and there is a high degree of transparency between the management of the firm and its employees. Therefore, most family businesses also involve their employees, particularly if the employees are directly affected by the advice. However, employees are also involved if they hold key positions or are opinion leaders among the other employees. Thus, to avoid resistance and to strengthen the support of the project within the workforce, the following holds true: The [employees] still have a certain power, whether something is implemented or not. I think it is also crucial that we can resolve this problem. We have tried that now, that you simply include them. Above all, it involves minds that are very critical. They are essential for implementation. There is no point in us agreeing, finding everything good, and not implementing it in the end. My lesson from this is that they should be included as early as possible. (FF.11.I)

When identifying the key stakeholders who influence the advising process, it is also important to identify the core families. Advisors must, therefore, identify who belongs to the family: How far does the family go? Is the illegitimate child of the stepbrother somehow also there or not? What about married couples and children? First, you have to clean up the field: Who belongs to the family? Who is in this circle? (A.5.II)

The interviewees repeatedly mentioned that a close family circle is crucial, as without its support, it is impossible to achieve perceived trust: “For him [FF.14.I], it is simply important that they [the family] stand behind him when he makes a decision [. . .]. So, he does not decide until he realizes he has the support of the family” (A.4.II). As an important part of the inner circle, although no longer formally active in the firm, the previous generation was frequently mentioned as interfering and acting gatekeepers: “But, I know the circumstances. I do not know the senior; he is 85, but he is a gatekeeper” (A.5.II). Furthermore, the interviewees mentioned the involvement of children, particularly if succession is concerned. Above all, however, spouses were mentioned to serve as key enablers of trusting relationships because spouses often act as a link between the company and the family. Spouses integrate into both worlds and adopt both the family perspective and the company perspective: “With him [FF.14.I], it is certainly also important to get to know them with their spouse. And, really, to have good contact with the wife because she then says yes or no at the end” (A.4.II).

Behavioral Trust

Behavioral trust, which is our third main theme, is built on perceived trust and shown when the family business trustor is willing to take the risk associated with acting on and adopting the trusted advisor’s advice. We identified second-order concepts that are directly linked to the display and sustainment of behavioral trust. We present our data along the following second-order themes: a family business trustor’s readiness to assume risk, the family business’s values and culture, the family business’s life cycle, and occurring breaches of trust.

Readiness to Assume Risk

In the interviews, the respondents mentioned various characteristics and personality traits (such as the tolerance of the family business trustor of uncertainty) that build the basis for the display of behavioral trust by the respondents toward the advisor as the trustee, as shown in the following quotes: “It is more about the personality, whether one is open or not” (A.5.I). “It is really very type dependent” (A.3.I). For example, whether decisions “are made intuitively, rationally, or emotionally” (A.6.I) depends on personality traits. Hence, personality strongly affects how family business trustors judge and eventually accept advice, as illustrated by the following quotes: “I am quite strong as a head person. Thus, I like to analyze situations and establish a construct out of them. I am less the emotional decision maker from the gut” (FF.7.I); “I very often make intuitive and emotional decisions, all of us, me in particular” (FF.8.1); and “I am perhaps more the structured one, and he decides perhaps more with intuition and perhaps also more emotionally” (FF.5.I). Thus, the interviewees also indicated that such interindividual differences in personality traits are stable over time.

Values and Culture

The interviewees stated that in addition to personal tolerance of uncertainty, the behavior of the family business as an organization under uncertainty also determines whether advice is taken. Therefore, the requirements for showing behavioral trust by family businesses are frequently also based on “fixed processes and routines that are anchored in the company” (A.6.I; FF.6.I; FF.5.I). The written documented processes, values, norms, or structures of family businesses provide advisors important information regarding a firm’s culture.

Corporate culture, including the family’s values, also plays a role in determining whether and to “what extent employees’ risk assessments influence decision-making” (FF.7.I). In summary, family businesses are more likely to accept advice when it corresponds with their values and habits, such as being actively involved in solving the problem and “making decisions themselves” (FF.6.I).

Life Cycle

In principle, the duration of a family business on the market is not decisive for its openness to external advice (A.3.I). However, family businesses grow—whether in terms of size or geographical orientation—over time and generations; this growth, in turn, contributes to the way in which topics become more diverse, complex, and specific. Thus, “to obtain necessary knowledge, external advice is increasingly required” (FF.6.I; FF.5.I) in later generations. In addition, as founders, the first generation tends “to be much more emotionally connected than subsequent generations” (A.4.I), who prefer to delegate important tasks to a family-external party, as shown in the following quote: “There is a saying. The first generation founds and builds, the second generation administers, and the third generation studies art history” (A.6.I). Moreover, the second and third generations may have to assume control earlier than planned and then find themselves in a situation where they are overburdened and lack experience. Such situations increase the likelihood “that they trust an external advisor” (A.3.I).

Breaches of Trust

Some interviewees stated that low-quality advice or failure by the advisor as the trustee can immediately destroy the level of trust achieved and, perhaps, even the relationship. Hence, when the family business trustor is disappointed by receiving bad advice, breaches of trust may abruptly end the advising relationship. The interviewees emphasized that while trust building is long and continuous, breaches of trust lead to make-or-break decisions and occur very quickly.

If the advisor shows dishonest or unreliable behavior, the family business will immediately lose the trust that has thus far been built and mistrust every further step taken by the advisor, whether this mistrust is justified or not. In these cases, such a loss of trust is often irreversible: “I simply notice that I have had companies where things have not been good, where you have had a lot of trust and then something that may not have been good on our side has happened . . . And then, the trust is gone . . . If the trust is really broken, for whatever reason, whether justified or unjustified, then you have lost” (A.4.II).

Discussion

Our study responds to the frequent calls to build family business research on foundations from psychology (Holt et al., 2018; Sharma et al., 2020; Zahra & Sharma, 2004) to gain deeper insights and theoretically explain crucial processes within family businesses. With our qualitative study, we seek and find answers regarding how the interaction and evolvement of the relationship between family businesses as trustors and their advisors as trustees affect advising during different phases. Trust building between the family business and the advisor inductively emerged as a core concept from our data. Building and, later, testing trust thus appears to be the driver of all phases of advising.

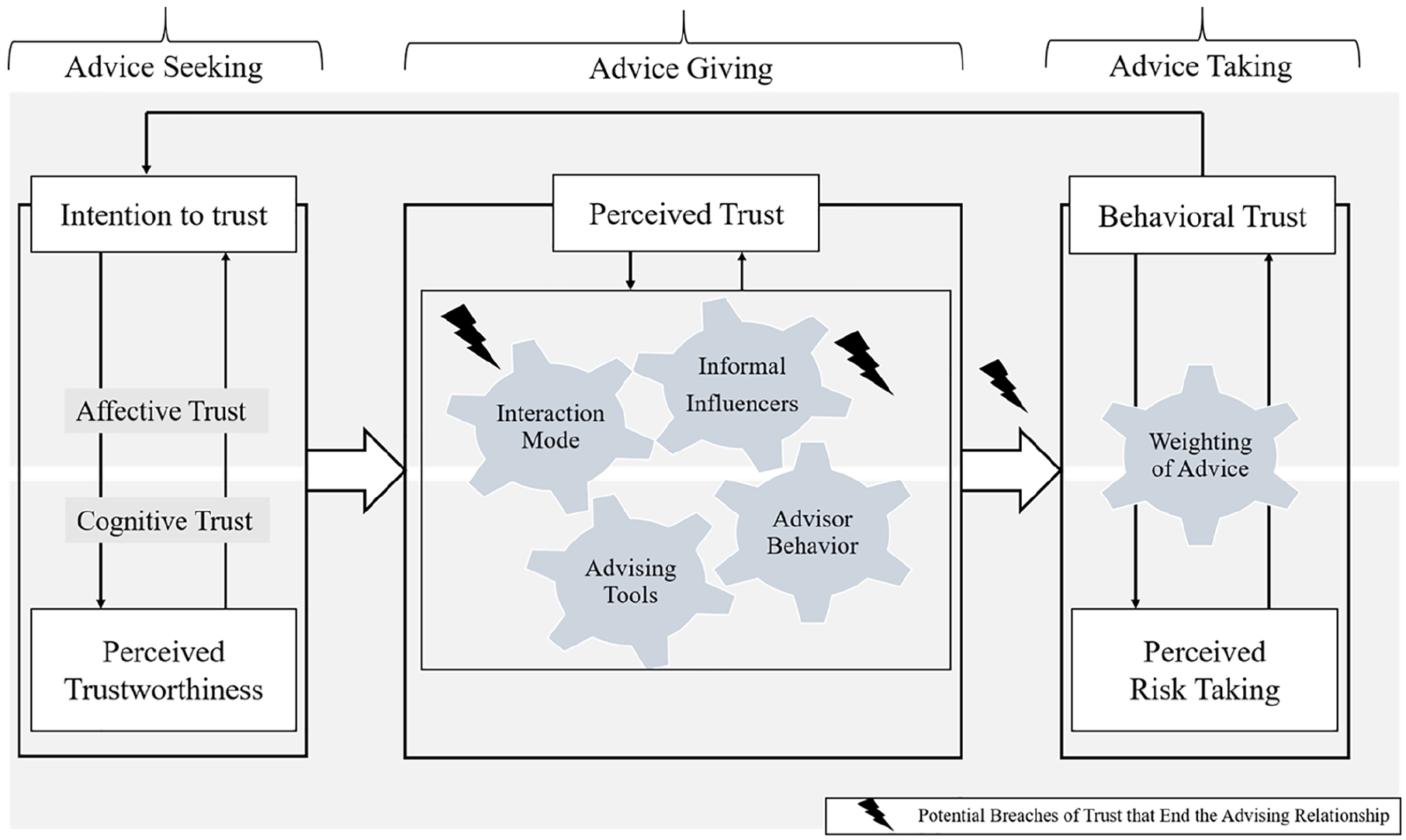

A Process Model of Trust Building in Family Businesses

Based on our findings, we developed an emergent process model. This model follows the three phases of the advising process, that is, advice seeking, advice giving, and advice taking, that result in three major types of trust, namely, the intention to trust, perceived trust, and behavioral trust. This model allows us to profoundly explain the evolution of organizational trust (Mayer et al., 1995) and the internal processing of weighting and evaluating the characteristics of the trustee (Gino & Moore, 2007) in a family business–specific context. Our model is shown in Figure 2.

The process of building trust in family business–advisor relationships.

In our model, we define family businesses as the trustors and advisors as the trustees. Consistent with the definition of trust applied above (as voluntary vulnerability toward another party; J. H. Davis et al., 2000), to initiate the advising process by seeking advice, family businesses must be willing to test collaborations with an outside party (i.e., an advisor) to begin building a trusting relationship (Simpson, 2007). According to the psychology literature, such a willingness or intention to trust represents an affective state, also called trusting beliefs (Mayer et al., 1995). However, our data also show the influence of various cognitive assessments about an advisor. Therefore, the trustor’s intention to trust is not static but is rather the outcome of the trustor’s constantly weighting and judging cognitive and affective information about an advisor’s capabilities.

Most interviewees stated that they make cognitive assessments of the advisor’s attributes, experience, and existing relationships as proxies for evaluating the advisor’s trustworthiness. Some interviewees mentioned observable similarities between them and the advisor in terms of demographic attributes (such as age or geographic origin), which they call “icebreakers,” thereby indicating that these aspects can facilitate the first contact; however, these attributes do not seem to be determining factors in creating trustworthiness. Similarly, most interviewees cognitively assessed education and expertise as important factors signaling information that creates feelings of having a competent advisor (or not, if the signals are undetected).

More important, many interviewees stated that affective assessments, such as rapport in terms of a feeling of liking the advisor or the belief that the advisor is a good person, support the intention of these interviewees to trust, particularly at the very beginning. Furthermore, many interviewees emphasized that subtle advisor characteristics, such as discretion and modesty, are of utmost importance. Thus, cognitive aspects seemingly related to ability, benevolence and integrity affect the perceived trustworthiness (Mayer et al., 1995) of an advisor and serve as a necessary condition for a general willingness to begin trust building. However, family business trustors, particularly, seem to more strongly weigh advisor aspects related to affective attributes, such as rapport, liking and perceived similarity; these affective attributes can be considered a sufficient condition for the intention to trust. Concerning trust in general, this finding contradicts the literature, which states that both components of trust are equally important (Chowdhury, 2005). According to this finding, in the unique family business context, although the components are interrelated, affective trust is more strongly emphasized; in turn, this stronger emphasis on affective trust resonates well with considerations of SEW (Berrone et al., 2010), which emphasize the importance of affective goals in family businesses.

After a specific advisor has been chosen and hired, the advice-giving phase begins. During this phase, the selected advisor interacts with the family business trustor to provide advice (Strike et al., 2018). Our data show that, during ongoing interactions with the advisor (trustee), the family business trustor’s intention to trust further develops toward a sense of trust. By relying on the psychology literature, this evolution of trust can be explained as the trustor’s (the family business’s) establishing certain perceptions of the trustee’s (advisor) behavior during repeated interaction (Simpson, 2007; Zak et al., 1998). Such perceived trust, which is not yet “real” trust, constantly interplay with the trustee’s actions and serve as a precondition for building deeper levels of trust.

Hence, perceived trust is also a dynamic construct closely interrelated with an advisor’s activities when giving advice to the family business. During advice giving, the advisor prepares and uses different strategies to present advice to the family business. The interviewees stated that throughout this phase, they assessed the advising tools used by the advisor (these tools include active listening, investing time, asking questions, providing alternative solutions and visualizing potential paths) and reported that these tools cognitively affected the interviewees’ perception of trust. Our data further revealed that the advisor’s behavior (such as making the advisee central, communicating openly, analyzing the situation as rationally as possible, identifying advantages and disadvantages, and proposing options and recommendations to the family business trustors) mostly cognitively but also affectively influenced the interviewees’ perception of trust. The psychology literature explains such behaviors as the creation of cognitive assessments of mutually beneficial outcomes, thereby indicating that both parties are increasingly convinced that the other party seeks outcomes that benefit both parties (Simpson, 2007).

In contrast, an advisor’s interaction mode generally seems to intensify the relationship on an affective basis since most family businesses prefer informal and personal interactions and direct communication. In addition, long-term, almost friendship-like, relationships support the perception of trust, whereas the intensity of the interactions does not seem to have an influence. Additionally, including informal influencers is of utmost importance for achieving perceived trust. Particularly, in family businesses, trustors are influenced by daily informal discussions with family members (such as spouses), the older generation or key employees, all of whom express opinions in subtle ways and frequently have a significant, albeit informal, influence on the trustor. Informal influences are often underestimated, and if an advisor neglects such key influencers, breaches of trust occur, and the prior perceived trust may be destroyed in a negative, affective reaction very abruptly and surprisingly for the advisor.

Hence, advisor actions involving trust building strengthen the perceived trust of the family business if this trust is not destroyed through inappropriate interaction modes or the neglect of key influencers; in turn, strengthening this perceived trust increases the motivation to repeatedly interact and, thus, support further trust building. During this phase, in contrast to the prior advice-seeking phase, the advisor can actively influence trust building by his or her actions. While an advisor’s pure actions, such as using tools and adopting certain behaviors, are mostly related to cognitive trust building, actual interactions with the family business trustor and his or her informal influencers lead to outcomes that are seemingly strongly linked to affective trust.

During the final phase of the advising process, that is, the advice-taking phase, the family business trustor evaluates the advice received by the trustee and either accepts or rejects it. Family business decision makers emphasize that even in situations where they accept an advisor’s advice, these decision makers never leave the decision to the advisor. Hence, consistent with theory regarding the trust building process, the assumption of this ultimate decision by the family business constitutes a willingness for risk taking and, thus, an actual display of trust (Mayer et al., 1995). We refer to such a display of trusting behavior as behavioral trust; that is, the family business trustor is willing to perform an action by adopting the advisor’s advice.

According to our data, such behavioral trust is affected by a family business trustor’s personality, which determines the individual readiness to assume risk; readiness to assume risk seems to be generally lower in family businesses, according to our interviewees; this observation is consistent with SEW considerations resulting in a lower willingness to take risks (Berrone et al., 2012). Theoretically, the evaluation of such willingness can be explained by the psychological concept of weighting of advice, which assesses an advisor’s influence on the trustor’s advice taking. This concept states that the weight of an advice measures the effect of advice by dividing the difference between an advisee’s final and initial estimate by the difference between the advice and the initial estimate (Gino, 2008; Yaniv & Kleinberger, 2000). The advice provided by an advisor who has been able to build a trusting relationship will be weighted more strongly than the advice of a less trusted advisor; this finding is further theoretically supported by the concept of the judge-advisor system in psychology (Budescu & Yu, 2007). A positive outcome of such advice or advisor judgment results in an increased probability of advice taking and, thus, risk taking. Hence, the display of behavioral trust is influenced by the prior steps (including the initial assessments of the advisor) in the process related to the intention to trust and perceived trust, both of which result from the interplay between the cognitive and affective components of trust and are subsequently affected by ongoing interactions between the trustor and the trustee.

Additionally, it is not only the family business trustor’s attitude toward uncertainty but also the family business’s idiosyncratic values and firm culture (which is usually largely affected by family values) that determine whether advice is adopted and, thus, whether trust is displayed. According to our data, established processes and routines, the family constitution, and the involvement of the family in problem solving appear to increase a firm’s willingness to take the risk of trusting a third party. Moreover, during the firm’s life cycle, the firm becomes characterized by increased complexity and less emotional attachment in later generations (Le Breton-Miller & Miller, 2013); these changes affect a family businesses’ risk-taking behavior. Thus, we assume that the theoretical construct of the readiness to assume risk and engage in risk taking (Mayer et al., 1995) is not valid only on the individual level but also on the familial and organizational level.

In our interviews, the family businesses frequently stated that if the above activities are not carried out carefully and the family business begins to doubt an advisor’s integrity, trust building can end abruptly; we refer to such advisor behavior as breaches of trust. Such breaches of trust do not even have to be intended by the advisor. Family business trustors may perceive certain behaviors by the advisor as a breach of trust even though the advisor was attempting only to perform his or her job. To avoid breaches of trust, many interviewees stated that it is very important for advisors not only to engage in trust-building activities with the family business trustor but also to include informal influencers. Our data further indicate that once trust is lost, it cannot be restored, even if the situation that led to the breach of trust proves to be a misunderstanding.

Hence, our data again reveal a close interplay regarding the cognitive decision to take a risk; this decision manifests in the affective state of behavioral trust. However, displaying vulnerability by taking a risk and, thus, showing trusting behavior may lead to mixed experiences. Positive experiences can result in a feedback loop that leads to an increased intention to trust in future advising processes, thereby accelerating future advising processes and vice versa in cases of negative experiences. In contrast, we found that even if the outcome of the taken advice was negative for the business, family businesses remained loyal to their advisors if the advisors could address such situations while maintaining their level of trust.

Implications

The syntheses of the described findings with foundations from psychology result in the derived model of trust building between family businesses and their external advisors; based on these syntheses, we provide at least two important implications for family business research that are also of high practical relevance. First, we contribute to the academic literature concerning the currently understudied process of trust building between family businesses and external parties, such as advisors, by using insights from psychology to further explain the underlying mechanisms of trust building. In prior literature, trust is frequently mentioned as a precondition for advice taking (Strike et al., 2018) because trust reduces transaction costs and functions as a governance mechanism (Steier, 2001) or a catalyst that “serve[s] as reminders of the family glue” (Kaye & Hamilton, 2004, p. 152). Our interviews revealed that, initially, no “real” trust exists; this lack of real trust explains why family business trustors search for observable attributes (e.g., experience, formal qualification, and appearance) to create a sense of trustworthiness (Mayer et al., 1995), whereas, during subsequent trust building, the advisor’s activities, behaviors and relationship-oriented aspects serve to establish interpersonal trust. During the advising process, different types of trust emerged from the data, namely, initially an intention to trust, which, after interactions between the family business and the advisor, further develops into perceived trust and, finally, is manifested and displayed as behavioral trust.

Trust building, therefore, does not appear to be a linear process but consists of constantly testing the relationship, thereby gradually promoting deeper levels of trust but also creating feedback loops that can not only accelerate but also decelerate trust building. Theoretically, such dynamic processes of building and testing between individuals influence progress across the different stages of interpersonal trust building (Kaye & Hamilton, 2004; Sundaramurthy, 2008). Our interviewees indicated that family business trustors’ internal appraisals were largely driven by judgments related to individual preferences of the family decision maker (Carney, 2005) and pursuing goals of SEW (Berrone et al., 2012).

For example, the intention to trust an advisor seems to be affected more by personal recommendations, perceived similarity, common interests and thus, a feeling of liking each other than by criteria that are typically mentioned in the advising literature as being relevant, such as education and experience (Strike, 2012). Similarly, the perception of trust seems to be highly influenced by an advisors’ ability to interact in a personal way that strongly accords with SEW considerations (Berrone et al., 2012) and to equally involve key employees and informal family decision makers. Finally, the display of behavioral trust, again, seems to be highly dependent on owner managers’ personal traits affecting their willingness to take risks and on the family business’s unique aspects, such as routines, culture and their emotional ownership depending on the generation (Björnberg & Nicholson, 2012).

Second, insights from our data synthesized with foundations from psychology contribute to a better understanding of the idiosyncratic processes of managing family businesses (Chrisman & Patel, 2012; De Massis et al., 2016; Duran et al., 2016) in the context of building relationships with external parties, such as advisors. Our findings highlight how these unique processes can be explained by psychological mechanisms and theories to show in what way family businesses are different from a theoretical perspective and to provide answers to open questions regarding how family business trustors process the information they receive while pursuing multiple goals (Berrone et al., 2012). Foundations from psychology inform us that during the advising process, the family business trustor constantly weighs and judges facets about an advisor by comparing current and initial estimates and how potential differences in assessments are influenced by the information received in between (Bonaccio & Dalal, 2006; Gino, 2008; Gino & Moore, 2007).

Our data further reveal an interplay between cognitive and affective assessment processes (e.g., Chowdhury, 2005; McAllister, 1995); this interplay suggests that family business owner managers internally weight cognitive and affective information regarding an advisor. It seems that family businesses, particularly, over time increasingly interact with their advisors in a very personal, friendship-like way; in contrast, other types of businesses commonly have business-like cognitively oriented advisor–principal relationships. As a consequence, our data show that with increasing levels of interpersonal trust, family business trustors more strongly base their advisor appraisals on internal heuristics largely driven by affective aspects to determine whether the advisor evolves from initially being trustworthy to becoming a trusted advisor (McAllister, 1995; Strike, 2012, 2013). In other words, during the advising process, family business trustors increasingly seem to put greater weight on affective relationship-oriented and SEW-driven aspects (Berrone et al., 2012) when deciding toward whom they display behavioral trust. This finding resonates well with current studies highlighting the particular importance of long-lasting relationships that family businesses seek to establish with external parties (Hauswald & Hack, 2013; Kotlar & De Massis, 2013).

Interestingly, this specific emphasis by family businesses on affective trust persisted even when some advice was wrong or led to a negative outcome. According to our data, such events do not necessarily end the trusting relationship if the perceived integrity of the trustee remains intact, for example, if the advisor admits and openly communicates about the mistake. Psychological foundations explain such behavior through cognitive dissonance reduction theory. This theory states that if the trustor’s attitude toward the trustee is generally affectively positive and trustful, in cases of failures, cognition is adapted to confirm the initial affective attitude to reduce dissonance (Shultz & Lepper, 1996). Hence, we theorize that, in their judgments of an advisor, family businesses increasingly rely more strongly on aspects related to affective trust than on aspects related to cognitive trust (Mayer et al., 1995), and in cases of an advisor’s unexpected failures, family businesses even seek to cognitively confirm their initial attitudes toward the advisor. However, our data further reveal that if a failure is not admitted, such dissonance reduction is not applied, and the trusting relationship is immediately destroyed, thereby leading to breaches of trust; this finding represents an important extension to the established model of the sustaining cycle of trust in family businesses (Sundaramurthy, 2008).

Finally, our results provide guidance to advisors of family businesses by highlighting the importance of investing time in building trust while carefully avoiding negative feedback loops or even breaches of trust caused, for example, by unreliable behavior often resulting in bad feelings. Moreover, it is crucial to identify the family business’s key influencers and the criteria or goals mostly related to the socioemotional aspects that these influencers weight and judge in relation to the information received.

Limitations and Future Research

The present study has several limitations that show potential areas for future research. First, our model does not consider contextual and institutional factors. Therefore, whether our findings hold true across different sectors and economies or whether our findings depend, for instance, on the cultural context and on economic welfare remains unclear. The data were all collected on Swiss family businesses; therefore, the applicability of our findings to other contexts might be limited. While we believe that most of our findings can also be applied to other (Western) settings, some aspects of Swiss culture might have biased some of our findings. For example, in Switzerland, there is the concept of Swissness, which refers to a person being Swiss in a particular way. Especially in rural areas, this Swissness is likely to influence important relationships (e.g., in the building of trust) within our process model. We, therefore, encourage researchers to conduct additional studies in different cultural contexts. Furthermore, regarding the intention to trust, the background of the advisor seems to be unimportant for family businesses. However, in our sample, the interviewees all referred to advising relationships among Swiss firms and Swiss advisors or advising relationships between Swiss firms and advisors with a background in other German-speaking countries (i.e., Germany or Austria) possibly because advisors with more diverse backgrounds do not even make it to the evoked set of the family businesses. Therefore, we encourage future research to investigate how the effects of differences in nationality or cultural background unfold in a more diverse setting and affect the choice for or against an advisor.

Second, our study explicitly focuses on external advisors who are paid for their services. Other research and our own results show that this type of advising is not the only type used in family businesses. Beyond internal types of advisors, such as supervisory boards (e.g., Bammens et al., 2011), there are external types of advisors, such as mentors (Distelberg & Schwarz, 2015) and family therapists (Castaños & Welsh, 2013; Distelberg & Castanos, 2012). In our sample, for example, no family therapists were included. In contrast, our sample mostly included bankers and accountants. It could be interesting to investigate whether trust building and, thus, advice-taking processes evolve similarly when other aspects (in addition to the business) of the owner family are the focus. Similarly, future studies are encouraged to illuminate whether our findings depend on the number of advisors involved and whether the advisor is hired for the short or long term.

Third, our study does not consider the potential influence of further aspects, such as the family’s perceptions or time pressure. Regarding the advice-seeking phase, future research should investigate whether family businesses’ advice-seeking behavior differs depending on the families’ perception of whether they need advice, as some families might not realize that they even need external support. Similarly, the severity of the issues associated with increased time pressure can tremendously affect advice-seeking behavior. Moreover, during the subsequent phase of trust building, it could be interesting for future research to investigate how time aspects affect trust building, such as whether a longer trust-building phase is more sustainable than a shorter phase.

Footnotes

Appendix

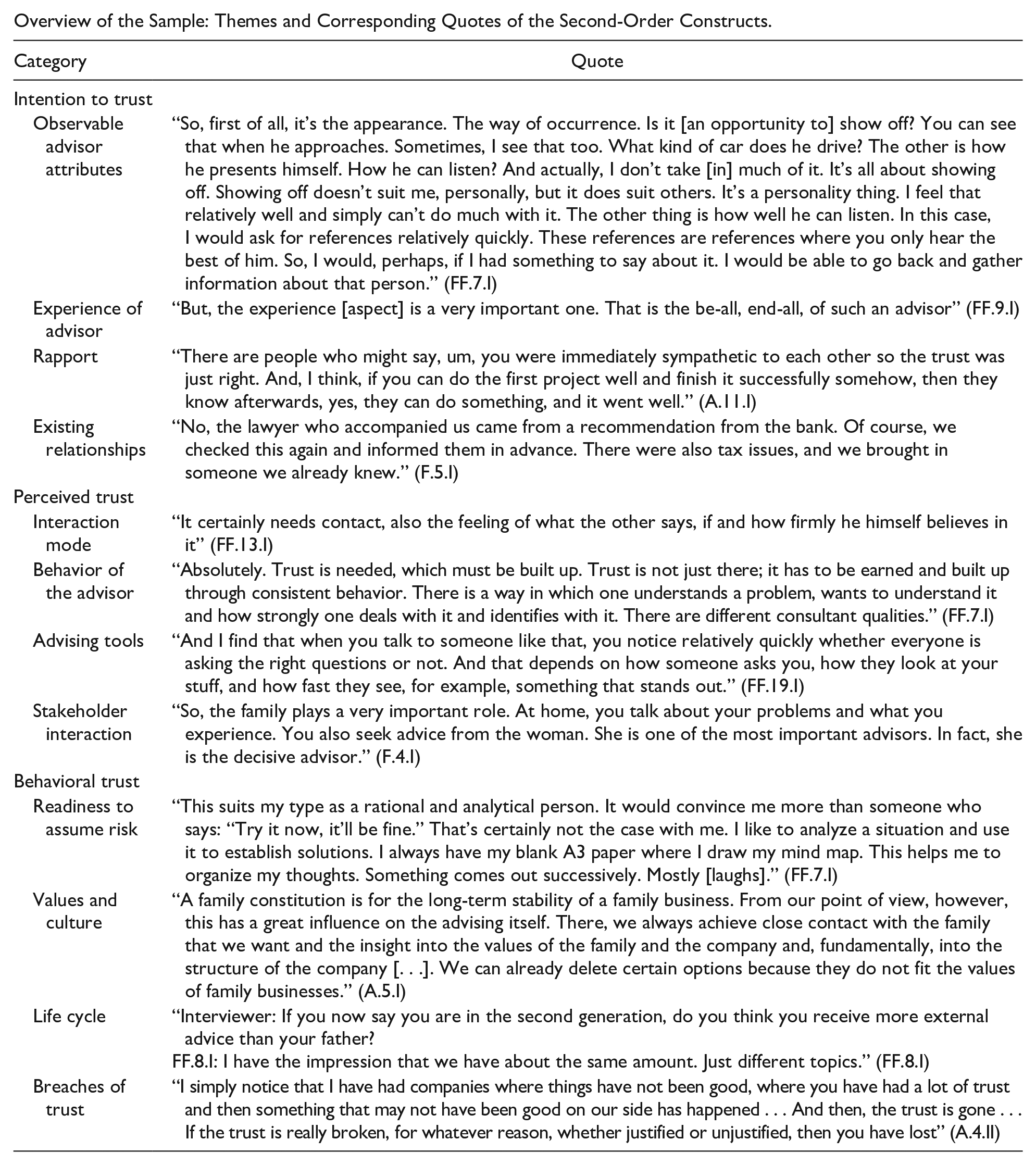

Overview of the Sample: Themes and Corresponding Quotes of the Second-Order Constructs.

| Category | Quote |

|---|---|

| Intention to trust | |

| Observable advisor attributes | “So, first of all, it’s the appearance. The way of occurrence. Is it [an opportunity to] show off? You can see that when he approaches. Sometimes, I see that too. What kind of car does he drive? The other is how he presents himself. How he can listen? And actually, I don’t take [in] much of it. It’s all about showing off. Showing off doesn’t suit me, personally, but it does suit others. It’s a personality thing. I feel that relatively well and simply can’t do much with it. The other thing is how well he can listen. In this case, I would ask for references relatively quickly. These references are references where you only hear the best of him. So, I would, perhaps, if I had something to say about it. I would be able to go back and gather information about that person.” (FF.7.I) |

| Experience of advisor | “But, the experience [aspect] is a very important one. That is the be-all, end-all, of such an advisor” (FF.9.I) |

| Rapport | “There are people who might say, um, you were immediately sympathetic to each other so the trust was just right. And, I think, if you can do the first project well and finish it successfully somehow, then they know afterwards, yes, they can do something, and it went well.” (A.11.I) |

| Existing relationships | “No, the lawyer who accompanied us came from a recommendation from the bank. Of course, we checked this again and informed them in advance. There were also tax issues, and we brought in someone we already knew.” (F.5.I) |

| Perceived trust | |

| Interaction mode | “It certainly needs contact, also the feeling of what the other says, if and how firmly he himself believes in it” (FF.13.I) |

| Behavior of the advisor | “Absolutely. Trust is needed, which must be built up. Trust is not just there; it has to be earned and built up through consistent behavior. There is a way in which one understands a problem, wants to understand it and how strongly one deals with it and identifies with it. There are different consultant qualities.” (FF.7.I) |

| Advising tools | “And I find that when you talk to someone like that, you notice relatively quickly whether everyone is asking the right questions or not. And that depends on how someone asks you, how they look at your stuff, and how fast they see, for example, something that stands out.” (FF.19.I) |

| Stakeholder interaction | “So, the family plays a very important role. At home, you talk about your problems and what you experience. You also seek advice from the woman. She is one of the most important advisors. In fact, she is the decisive advisor.” (F.4.I) |

| Behavioral trust | |

| Readiness to assume risk | “This suits my type as a rational and analytical person. It would convince me more than someone who says: “Try it now, it’ll be fine.” That’s certainly not the case with me. I like to analyze a situation and use it to establish solutions. I always have my blank A3 paper where I draw my mind map. This helps me to organize my thoughts. Something comes out successively. Mostly [laughs].” (FF.7.I) |

| Values and culture | “A family constitution is for the long-term stability of a family business. From our point of view, however, this has a great influence on the advising itself. There, we always achieve close contact with the family that we want and the insight into the values of the family and the company and, fundamentally, into the structure of the company [. . .]. We can already delete certain options because they do not fit the values of family businesses.” (A.5.I) |

| Life cycle | “Interviewer: If you now say you are in the second generation, do you think you receive more external advice than your father? FF.8.I: I have the impression that we have about the same amount. Just different topics.” (FF.8.I) |

| Breaches of trust | “I simply notice that I have had companies where things have not been good, where you have had a lot of trust and then something that may not have been good on our side has happened . . . And then, the trust is gone . . . If the trust is really broken, for whatever reason, whether justified or unjustified, then you have lost” (A.4.II) |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.