Abstract

Drawing on (mostly) medium-sized and unlisted Polish firms, this study explores the influence of the interaction between founder-controlled family firms and managerial overconfidence on corporate social responsibility (CSR). We demonstrate that founder-controlled family firms show low levels of CSR engagement. This suggests that families try to limit CSR activities that could challenge their control and thus their socioemotional endowment. Moreover, overconfident executives in these firms tend to exhibit superior CSR performance. Consequently, the family’s preference for control can be mitigated by overconfident executives who underestimate the family’s control risk and focus on building reputation by acting socially responsible.

Introduction

Due to increasing public awareness, corporate social responsibility (CSR) has received considerable attention among many firms and their stakeholders. The distinct nonfinancial aspects of family firms (FFs) in general and founder-controlled FFs (FCFFs) in particular that are emphasized by the socioemotional wealth (SEW) concept (Gómez-Mejía et al., 2007) raise doubts regarding whether those firms show the same CSR engagement exhibited by nonfamily firms (NFFs). Although the value systems of many (FC)FFs seem to be characterized by an ethical orientation (García-Álvarez & López-Sintas, 2001), previous evidence regarding the CSR performance of (FC)FFs compared to their nonfamily counterparts is rather mixed (e.g., Berrone et al., 2010; Dyer & Whetten, 2006; El Ghoul et al., 2016; Litz & Stewart, 2000). This evidence rules out the conclusion that (FC)FFs are unambiguously more socially responsible than NFFs. Therefore, (FC)FFs might not constitute a homogeneous group in terms of their CSR orientation (de la Cruz Déniz Déniz & Suárez, 2005). Indeed, recent research (e.g., Cruz et al., 2014) indicates that different SEW reference points of family actors might be able to explain these mixed results. On one hand, if family members focus on the family identification dimension of the SEW framework as their primary reference point, they want to ensure a positive family image. As a damaged firm reputation could endanger their family image, they might put a special emphasis on acting socially responsible. On the other hand, if they use the family control dimension as a key reference point, they will focus on maintaining control over their firm to protect their socioemotional endowment. Consequently, they might avoid CSR activities that could threaten the family’s control. Although previous studies (Bingham et al., 2011; Ding & Wu, 2014) suggest that the CSR engagement of FFs varies depending on the generation in control of the business, to the best of our knowledge, evidence regarding how these different SEW reference points shape the CSR engagement of (nonlisted) FFs in the founder stage is (still) missing.

Moreover, even though the concept of SEW is rooted in Kahneman and Tversky’s (1979) prospect theory, and the SEW itself is “anchored at a deep psychological level among family owners” (Berrone et al., 2010, p. 87), much of the extant literature has not shed light on the SEW concept from a psychological perspective (Jiang et al., 2018). Such a perspective, however, might be particularly fruitful when analyzing the CSR engagement of (FC)FFs, as a few recent studies indicate that psychological traits such as overconfidence influence CSR activities (e.g., McCarthy et al., 2017; Tang et al., 2018; Tang, Qian, et al., 2015). In this regard, previous research argues that overconfidence (or the closely related trait of hubris) can induce CEOs to underestimate firm risk or their dependence on stakeholders (McCarthy et al., 2017; Tang et al., 2018; Tang, Qian, et al., 2015), suggesting a negative impact of overconfidence on the CSR engagement. This evidence for firms in general, however, may not hold true for FCFFs, as overconfidence might alter the perception of different SEW dimensions or reference points. To the best of our knowledge, no one has analyzed whether this trait has a different effect in FCFFs than in NFFs.

Thus, drawing on the SEW concept and behavioral economics as theoretical frameworks, we aim to explore (1) how SEW dimensions and reference points shape the CSR engagement of FCFFs and (2) how the psychological trait of overconfidence can alter the perception of different SEW dimensions. To answer these questions, we provide survey evidence from mostly medium-sized firms based in Poland. This sample allows us to analyze a unique and homogeneous group of FCFFs, as Poland is not only a country with a homogenous cultural and religious background but also a relatively young free-market economy wherein almost all FFs exhibit a founder presence.

We argue that in shaping their CSR engagement, FCFFs might attach greater importance to maintaining control (family control dimension of SEW) than image and reputation enhancement (family identification dimension). The trait of overconfidence, however, is expected to shift the SEW reference point in FCFFs from the family control dimension to the family identification dimension, suggesting a positive influence of overconfidence on CSR. Thereby, this study contributes to and extends the concept of SEW, as we demonstrate not only how different SEW dimensions are perceived by family actors in the founder stage but also how psychological traits such as overconfidence can alter the frame of reference in FCFFs.

Literature Review and Theoretical Framework

CSR

Based on the European Commission’s (2001) definition, CSR is “a concept whereby companies integrate social and environmental concerns in their firm operations and in their interaction with their stakeholders on a voluntary basis.” CSR therefore reflects the extent to which a firm actively engages in social initiatives in response to a wide range of stakeholder interests (McWilliams & Siegel, 2001; Tang, Qian, et al., 2015), and distinct elements of CSR are embedded in corporate governance (Matten & Moon, 2008); CSR overlaps with the concept of ESG (environmental, social, and governance; European Commission, 2018), but the latter term is used mainly in the finance-oriented literature as well as in the finance industry (e.g., Amel-Zadeh & Serafeim, 2018). Empirically, CSR consists of clearly articulated and communicated policies and practices of firms that reflect business responsibility for some of the wider societal good (Matten & Moon, 2008). The range of CSR engagements is broad: Examples include activities that are directed toward employee safety, social security, community or regional charitable activities, supplier ethics, environmental protection, consumer protection, investor protection, and anti-corruption measures (European Commission, 2001).

Over the past few decades, a substantial theoretical and empirical literature on CSR has emerged. Opposing views stretch from Friedman’s (1970) perspective on CSR as a waste of scarce resources to the counter viewpoint of Freeman’s (1984) famous stakeholder theory. According to the latter theory, CSR can improve a firm’s relationships with stakeholders and can be interpreted as a signal of good management (Waddock & Graves, 1997). A significant strand of research focuses on the benefits of CSR engagement, its link to financial performance, and its risk-reducing role (Deng et al., 2013; Edmans, 2011; El Ghoul et al., 2011; Ferrell et al., 2016; Goss & Roberts, 2011; Jiao, 2010; Margolis et al., 2009). Moreover, the literature shows that CSR is remarkably driven by institutional and legal determinants (e.g., J. L. Campbell, 2007; Ferrell et al., 2016; Matten & Moon, 2008). In addition, there is some evidence that CSR is determined by CEO characteristics (e.g., Di Giuli & Kostovetsky, 2014; Tang et al., 2018; Tang, Qian, et al., 2015). The extant research predominantly focuses on large listed firms; CSR policies in smaller firms, which are often dominated by families, could differ substantially. This article contributes to the literature by investigating how ownership characteristics in unlisted firms, such as family influence in the founder stage, are linked to CSR performance.

SEW

Behavioral theories of the firm suggest that a company’s (nonfinancial) goals are shaped by the values, attitudes, and intentions of its dominant decision makers (e.g., Chrisman et al., 2012). In (FC)FFs, families control the dominant coalition (Chua et al., 1999). Therefore, (FC)FFs will purse specific family-centered (nonfinancial) goals that do not (or rarely) exist in NFFs (e.g., Chrisman et al., 2012; Chua et al., 2015; De Massis et al., 2019; Miller & Le Breton-Miller, 2014; Tagiuri & Davis, 1992). Many scholars agree that the (substantially greater) emphasis on nonfinancial goals might be even a defining characteristic of (FC)FFs (e.g., Chrisman et al., 2012; Chua et al., 2015; Gomez-Mejia et al., 2011). Gómez-Mejía et al. (2007) summarize the nonfinancial aspects that favor a family’s affective needs under the term socioemotional wealth. Building on behavioral agency theory (Wiseman & Gomez-Mejia, 1998), which itself extends and modifies classical agency theory and its assumptions by the insights of Kahneman and Tversky’s (1979) prospect theory, such as loss aversion, 1 they emphasize that families do not exclusively want to maximize their financial returns or shareholder wealth but rather that their primary reference point is to avoid the loss of their SEW. The authors theorize and find empirical evidence that family actors are loss averse toward their socioemotional endowment and thus might even accept significant threats to the financial situation of their firm to protect their SEW. Since its introduction, the SEW concept has played an important role in the family business literature (e.g., Chua et al., 2015; Jiang et al., 2018).

Berrone et al. (2012) indicate that SEW can be seen as a multidimensional concept manifesting itself in the dimensions of “family control and influence” (family control), “identification of family members with the firm” (family identification), “binding social ties”, “emotional attachment of family members”, and “renewal of family bonds to the firm through dynastic succession”. Previous work suggests that these different dimensions might explain not only the different reference points among family principals but also distinct (FC)FF policies, depending on the prioritization of one dimension or the other(s) (e.g., Berrone et al., 2012; Cennamo et al., 2012; Cruz et al., 2014; Gomez-Mejia et al., 2014; Martin et al., 2016). Thus, we aim to analyze how different SEW dimensions and reference points might affect the CSR engagement of FCFFs.

CSR in Founder-Controlled Family Firms

Empirical Evidence

Studies on the CSR performance of (FC)FFs compared to that of NFFs provide mixed evidence. Whereas some studies of listed firms document a higher performance of FFs (Berrone et al., 2010; Dyer & Whetten, 2006), other scholars find lower performance (El Ghoul et al., 2016; Rees & Rodionova, 2015) or a mixed picture, depending on the type of CSR activity (Block & Wagner, 2014; Cruz et al., 2014; Hirigoyen & Poulain-Rehm, 2014). The evidence for nonlisted or founder-controlled FFs is scarce. According to Campopiano and De Massis (2015), a sample of listed and nonlisted large- and medium-sized Italian FFs differ in their CSR reporting practices from NFFs, depending on the topic of reporting. In addition, the interaction of family involvement in ownership and management matters in determining the firm philanthropy of small- and medium-sized Italian FFs (Campopiano et al., 2014). Regarding small U.S. FFs, Litz and Stewart (2000) report that they show greater levels of community involvement, whereas Ding and Wu (2014) indicate that they are less likely to engage in corporate misconduct than are NFFs. This evidence, however, does not hold true for younger FFs. Similarly, Bingham et al. (2011) find some evidence that being an FF or having a higher family involvement positively affects the CSR performance of U.S. listed companies (more initiatives and fewer concerns in different areas of CSR engagement). These findings indicating a positive “family effect” on CSR, however, receive only limited support when looking at the impact of a higher founder involvement (no significant differences for CSR initiatives and fewer CSR concerns only in the area of “product” engagement). Given these mixed and/or limited findings, the CSR performance of FFs, especially those that are nonlisted or founder-controlled, remains an open research question.

SEW and CSR Engagement

Family business scholars regularly refer to the pursuance of distinct (nonfinancial) family goals and therefore different SEW dimensions to delineate the CSR engagement of (FC)FFs from that of NFFs. In this regard, above all, the family control and family identification dimensions of the SEW are supposed to shape the CSR engagement of (FC)FFs. With reference to the family identification dimension, family members want to ensure a positive family image and reputation (e.g., Berrone et al., 2010; Berrone et al., 2012; Cruz et al., 2014; Martin et al., 2016). Consequently, (FC)FFs could focus more on social responsibility than could NFFs (e.g., Berrone et al., 2010; Cennamo et al., 2012; Cruz et al., 2014; Dyer & Whetten, 2006), as a negative image of their business would also spill over to the family’s image and thus could endanger their SEW (e.g., Berrone et al., 2010; Cennamo et al., 2012; Cruz et al., 2014). Moreover, by acting socially responsible, (FC)FFs can maintain a good reputation with stakeholders (Dyer & Whetten, 2006) and gain legitimacy as good corporate citizens (Campopiano & De Massis, 2015).

Shedding light on the family control dimension of SEW, families want to maintain control over their business to protect their socioemotional endowment (e.g., Berrone et al., 2012; Cruz et al., 2014; Gómez-Mejía et al., 2007; Jones et al., 2008; Martin et al., 2016). The family’s intention to exert control is considered to be one of the key determinants of the behavior of (FC)FFs (e.g., Astrachan Binz et al., 2017; Chrisman et al., 2012; Cruz et al., 2014; Gómez-Mejía et al., 2007), which is even used by scholars to define these companies (e.g., Chrisman et al., 2004; Chrisman et al., 2012; Chua et al., 1999), as only through control can families influence the firm’s decisions (e.g., Astrachan Binz et al., 2017; Berrone et al., 2012; Chrisman et al., 2012) and pursue (other) family-centered nonfinancial goals (e.g., Berrone et al., 2012; Chrisman et al., 2012). Thus, families might engage in strategies that help them retain or even extend their influence and control over their business (Cruz et al., 2014). This might include employing family members or promoting career opportunities for these family members for altruistic reasons 2 and probably without regard to their qualification (e.g., Anderson & Reeb, 2003; Cruz et al., 2014; Haynes et al., 2015; Lubatkin et al., 2005; Schulze et al., 2001), refraining from performance-based compensation for family employees and managers (e.g., Cruz et al., 2010; Cruz et al., 2014; McConaughy, 2000), or insulating their compensation from risk (Gomez-Mejia et al., 2003). Such strategies aiming to maintain family control and to protect the position of family employees contradict CSR efforts to provide equal career opportunities and equal pay for all employees (European Commission, 2001). Contrary to good corporate governance, families were found to limit the number of independent board members to increase their discretion and control over firm resources (Anderson & Reeb, 2004), whereas affiliate directors might pose less of a threat to family control (Jones et al., 2008). To be able to fill board positions without interference from nonfamily shareholders, FFs were found to make less voluntary disclosure about their corporate governance practices in their regulatory filings (Ali et al., 2007). Moreover, (FC)FFs could violate good corporate governance practices by relying on dual-class shares or other control-enhancing mechanisms to protect their share of voting rights and thus control over the firm (e.g., Martin et al., 2016; Villalonga & Amit, 2006). Consequently, Cruz et al. (2014) conclude that SEW can be a “double-edged sword” that leads to both socially responsible and irresponsible practices, as certain CSR activities, for example, those ensuring fair treatment of and providing equal opportunities for (family and nonfamily) employees or mechanisms regarded as good corporate governance, could threaten family control or the position of family employees in the firm. In addition, to guarantee the family’s control over the firm, FFs were also found to be less compliant with CSR standards, as such strictly formalized and bureaucratic regulations might constrain the family’s managerial authority, autonomy, and opportunity to pursue their goals and priorities in the firm (Campopiano & De Massis, 2015).

Hypotheses Development

Gómez-Mejía et al. (2007) show that the family’s desire to maintain control is particularly pronounced in the founder generation and declines in later stages, which is also supported by later studies (e.g., Keasey et al., 2015; Stockmans et al., 2010; Vandemaele & Vancauteren, 2015). In addition, Ding and Wu (2014) document that the reputational considerations of the family lead to a lower level of corporate misconduct only in mature but not in younger FFs. Similarly, Bingham’s et al. (2011) evidence for a positive “family effect” on CSR engagement receives only limited support for the founder stage. Therefore, younger FFs or those with founder presence might put less emphasis on building their reputation (e.g., Ding & Wu, 2014; Sageder et al., 2018), as they are usually occupied with their struggle for survival (Ding & Wu, 2014) or pursuing growth strategies (e.g., Miller et al., 2011; Sageder et al., 2018). Thus, we suppose that the family control dimension of SEW might arguably play a more crucial role than do reputational considerations and therefore the family identification dimension for FCFFs, whereas in later generations, that is, nonfounder-controlled FFs (NFCFF), reputational concerns might dominate over control. Maintaining control (and pursuing growth strategies) seems to be an omnipresent goal for family actors in FCFFs, exerting immediate pressure on them and constituting the “default script” when shaping their CSR engagement, while reputational concerns are considerably less present on a day-to-day basis, until an unanticipated reputational threat—such as a scandal caused by the unethical behavior of (e.g., altruistically hired) family actors—calls for immediate attention (Vardaman & Gondo, 2014). Similarly, loss-averse family actors in FCFFs might prefer avoiding the (straightforward) loss of control that is associated with a high CSR engagement to achieving a gain in reputation until immediate reputational threats change their frame of reference. To summarize, we expect that FCFFs, which dominate the relatively young free-market economy of Poland, show lower CSR engagement than NFFs, as they (1) exhibit a particularly strong desire to maintain control by keeping down their CSR engagement and (2) tend to put building their reputation last and, consequently, might neglect the reputational benefits of CSR activities. Consequently, we postulate the following hypothesis:

Previous studies (Campopiano & De Massis, 2015; Cruz et al., 2014; McCarthy et al., 2017) indicate that reputational and/or control concerns of (FC)FFs and thus their CSR engagement might vary depending upon the type of CSR activity. Cruz et al. (2014), for example, show that FFs are less likely to adopt CSR measures that are related to internal stakeholders (employees or corporate governance) to ensure continued family control, whereas they exhibit the same level of CSR engagement entailing reputational benefits with external stakeholders as do NFFs. Other research hints at a differentiated attitude of (FC)FFs toward CSR activities targeted at external stakeholders. On one hand, FFs were found to focus on external CSR engagement entailing particularly high reputational benefits, such as (local) community, charitable, or environmental activities, as this engagement allows them to be recognized as good corporate citizens (e.g., Campopiano & De Massis, 2015; Cruz et al., 2014; McCarthy et al., 2017). On the other hand, FFs seem to put less emphasis on certain (powerful) external stakeholders (e.g., customers; Campopiano & De Massis, 2015), suggesting that external stakeholders might also endanger their control over the firm. Reinforcing this argument, FFs were found to avoid complying with CSR standards, as such bureaucratic constraints might limit their managerial autonomy (Campopiano & De Massis, 2015).

Thus, we expect that, compared to NFFs, FCFFs will show a lower level of CSR activities that might endanger family control—those that limit the family’s authority, discretion, and autonomy by bringing along a commitment to powerful nonfamily stakeholders and/or an adherence to bureaucratic regulations (e.g., CSR engagement targeted toward corporate governance, employees, or customers, compliance with CSR standards or certifications). The same, however, should not hold true for CSR activities that bring along particularly high reputational benefits for the family—those that promise the greatest reputation gains and thus allow family actors to prove themselves to be responsible corporate citizens while entailing the lowest level of commitment to nonfamily stakeholders or the limitation of discretion that could endanger family control at the same time (e.g., CSR engagement targeted toward the (local) community, charitable, or environmental activities). Regarding the latter, FCFFs are expected to exhibit higher or at least the same CSR performance as NFFs. Thus, we hypothesize the following:

Overconfidence in Founder-Controlled Family Firms and CSR

Introduction

The extant research indicates that next to ownership characteristics such as founder control or family ownership, executives’ characteristics have a distinct influence on the CSR engagement of firms. These personal characteristics include, among others, personal values such as political ideologies (Chin et al., 2013; Di Giuli & Kostovetsky, 2014) and psychological traits such as overconfidence, confidence, hubris, or narcissism (McCarthy et al., 2017; Petrenko et al., 2016; Tang et al., 2018; Tang, Qian, et al., 2015). These findings for firms in general, however, cannot be directly transferred to FCFFs, as the family’s SEW is supposed to represent a crucial factor for the executives’ decision making in these firms. In this study, we concentrate primarily on executives’ “overconfidence”, a concept that was found to be associated with a wide range of firm policies (e.g., Hirshleifer et al., 2012; Malmendier et al., 2011; Malmendier & Tate, 2005, 2008; McCarthy et al., 2017; Schrand & Zechman, 2012), and argue that this personality trait might alter the perception of different SEW reference points and thus the CSR engagement of FCFFs.

Overconfidence refers to an overestimation of a particular outcome occurring (W. K. Campbell et al., 2004; Hiller & Hambrick, 2005). Specifically, “overconfidence is defined as a positive difference between average confidence and average accuracy” (W. K. Campbell et al., 2004, p. 299). In this regard, executive overconfidence and closely related behavioral anomalies, such as (over)optimism and hubris, share “the tendency for individuals to overestimate their abilities and chances for success” (Hiller & Hambrick, 2005, p. 302). 3 Previous literature suggests that overconfidence is significantly associated not only with (1) corporate policies and risk-taking decisions, including the decision to invest in CSR as a risk-reducing mechanism (McCarthy et al., 2017), but also with (2) the founder status and (3) the SEW dimensions “family identification” and “family control.” Findings indicate that overconfident managers accept greater risks and achieve higher innovation (Hirshleifer et al., 2012; Li & Tang, 2010; Tang, Li, & Yang, 2015). Overconfidence (hubris) can influence corporate policies in unfavorable ways, such as overinvestment, value-destroying acquisitions, suboptimal capital structures (e.g., Hayward & Hambrick, 1997; Malmendier et al., 2011; Malmendier & Tate, 2005, 2008), or a greater likelihood of earnings management and even financial misreporting and fraud (Schrand & Zechman, 2012). We believe that managers’ psychological biases, such as overconfidence, should have an even greater influence on CSR policies in smaller firms than in large, listed corporations. 4

Overconfidence in Founder-Controlled Family Firms

Concerning overconfidence in (FC)FFs, the evidence is scarce. Miller and Le Breton-Miller (2006) argue that if left unchecked, family management can promote overconfidence (hubris). Dissecting case studies, they (Miller & Le Breton-Miller, 2005) identify overconfidence as one of the main causes of business failure in (FC)FFs. Landier and Thesmar (2009) show that entrepreneurs who have founded (and not inherited or purchased) a business tend to have overoptimistic expectations, thereby suggesting higher overconfidence of founders. Similarly, Lee et al. (2017) provide evidence that founder CEOs are more overconfident than their nonfounder counterparts. Thus, FCFFs constitute an ideal research area for analyzing the trait of overconfidence.

In these companies, overconfidence will affect the perception of the family’s SEW, as SEW considerations are supposed to represent a crucial factor in the executives’ decision making. This may hold true not only for the founder or members of their family holding executive positions but also for professional executives from outside the family. Founders select these professional executives to overcome the limited pool of managerial resources in the family (e.g., Burkart et al., 2003; Waldkirch, 2019). Thus, they not only are expected to support the founder and their family as counselors, confidants, or management trainers (Blumentritt et al., 2007), for example, by providing advice in maintaining and enhancing SEW but also might be selected, retained, rewarded, and promoted for their efforts and success in preserving SEW (Deephouse & Jaskiewicz, 2013) or for acting as the founder’s steward (Y. M. Chen et al., 2016). In addition, through interactions with the family, professional executives get to know the firm’s culture over time and might internalize its goals and values. This socialization process may take place especially in smaller FFs, where owners and the firm’s culture are difficult to separate, (Garcés-Galdeano et al., 2017), or in FCFFs, where the firm’s culture is inextricably tied to the founder’s personality (Eddleston, 2008), and might even result in a sense of psychological ownership toward the firm (Huybrechts et al., 2013). To summarize, not only family but also professional executives might care strongly for the family, its firm, its legacy, and thus its SEW (Huybrechts et al., 2013; Waldkirch, 2019). Moreover, family and professional executives shape the perception of SEW reference points in FCFFs and consequently the CSR engagement through their role as counselors to nonexecutive family owners.

Hypothesis Development

Previous evidence indicates that CEO overconfidence (or related concepts such as confidence and hubris) tends to induce a lower level of CSR (McCarthy et al., 2017; Tang et al., 2018; Tang, Qian, et al., 2015). This evidence for firms in general, however, may not hold true for FCFFs, as this personality trait is expected to alter the perception of different SEW reference points.

Overconfident (hubristic) CEOs were found to underestimate firm risk and thus the risk-reducing role of CSR (McCarthy et al., 2017) or their dependence on others, such as stakeholders (Tang et al., 2018; Tang, Qian, et al., 2015), suggesting a negative impact of overconfidence on the CSR level of firms in general. Although we cannot completely rule out that these factors—as Haynes et al. (2015) hint—might also limit the CSR engagement of (FC)FFs, overconfidence can induce executives in FFs and particularly in FCFFs to underestimate the family’s risk of losing control over the business. The financing choices of overconfident (FCFF) executives provide evidence for this; Landier and Thesmar (2009) show that (over)optimistic French entrepreneurs—among whom entrepreneurs who founded their business are overrepresented—prefer (cheaper) short-term debt over long-term debt, as they underestimate the risk of not being able to repay their short-term debt obligations and therefore losing control over their firm. Similarly, Huang et al. (2016) show that for large, listed U.S. firms, overconfident CEOs underestimate the liquidity risk that is associated with short-term debt, as they hope they can refinance short-term loans with lower costs when positive news arrives in the future, which is empirical evidence that was also supported by Graham et al. (2013). Finally, Hackbarth (2008) presents a formal proof that overconfident managers’ tendency to underestimate bankruptcy risk will lead to higher debt levels. Therefore, overconfidence might induce executives in (FC)FFs to underestimate the control risk that is associated with high CSR engagement and thus might attenuate the impact of the family control dimension of SEW on CSR, which is considered to play a crucial role in shaping firm policies, especially for FCFFs. Conversely, overconfident (FC)FF executives could assign a higher priority to the reputational benefits of CSR and therefore the family identification dimension to strengthen the family’s SEW.

In summary, whereas overconfident executives of firms in general were found to underestimate their firm risk or dependence on others, implying a negative effect of overconfidence on CSR, executives of (FC)FFs might underestimate the control risk associated with CSR activities and thus consider the corresponding reputational benefits as (relatively) more valuable, suggesting a positive impact of overconfidence on CSR. Consequently, overconfidence is supposed to shift the focus of the family’s SEW to maintaining and enhancing its image and reputation and therefore to the family identification dimension of SEW. As discussed above, overconfidence could be more present in FCFFs, thereby suggesting a (particularly) strong effect of overconfidence in these companies compared to FFs in later generations. Thus, we postulate the following hypothesis:

Research Design and Data

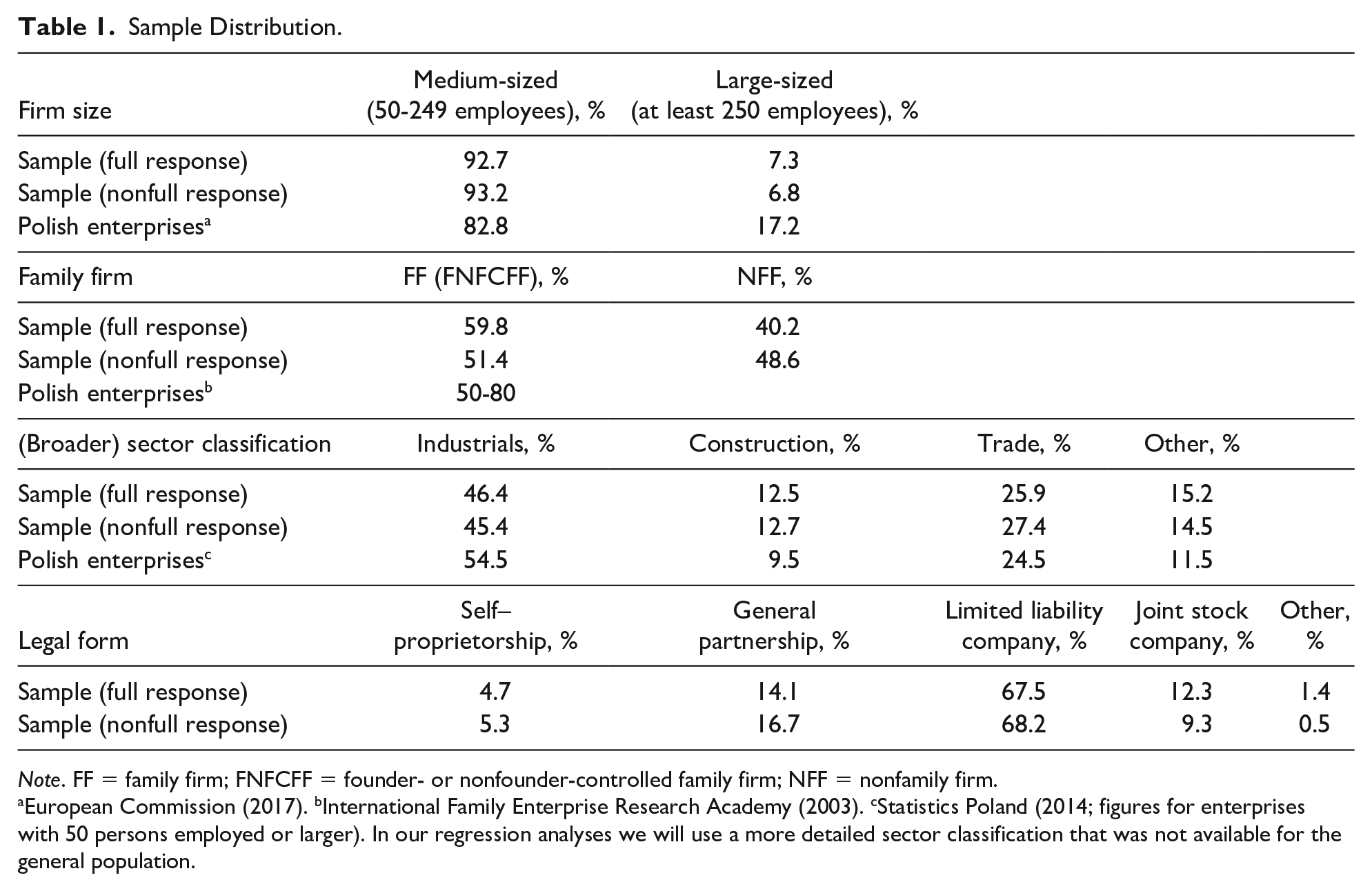

In 2014, the executives of 12,215 Polish companies with at least 50 employees were contacted using computer-assisted telephone interviewing as part of a larger research project on the firm policies of FFs. A total of 758 executives agreed to participate in the survey. After excluding 400 enterprises with missing data and 15 financial firms, 343 companies—most of which were medium-sized firms and nearly all of which were nonlisted—were included in our study (“full respondents”). In line with other studies on (private) FFs (e.g., Amore et al., 2011; Garcés-Galdeano et al., 2016; Gulbrandsen, 2005), in this study, FFs were identified as companies where a family owns at least 50% of the shares. A total of 191 FFs showed a founder presence in management or ownership (FCFF), whereas only 14 FFs without founder presence could be identified (NFCFF). Therefore, our sample includes 205 FFs with and without founder presence (founder- or nonfounder-controlled FFs [FNFCFFs]).

To ensure representativeness and to address nonresponse bias, we first compared the characteristics of the sample with those of the general population of enterprises in Poland (see Table 1). This comparison suggests that despite minor differences (e.g., medium-sized firms are over- and industrials are underrepresented), the characteristics of our sample are by and large similar to the national averages. Second, we compared 343 full respondents with 400 nonfull respondent firms. As Table 1 shows, firm size, sector, and legal form are highly comparable (chi-square tests reveal no significant differences between the two groups), thereby indicating that our final sample does not suffer from nonresponse bias. Nevertheless, NFFs are overrepresented among the nonfull respondents. Most likely, their executives may be less willing to complete a time-consuming telephone interview, as all respondents were informed that the survey focused on the firm policies of FFs.

Sample Distribution.

Note. FF = family firm; FNFCFF = founder- or nonfounder-controlled family firm; NFF = nonfamily firm.

European Commission (2017). bInternational Family Enterprise Research Academy (2003). cStatistics Poland (2014; figures for enterprises with 50 persons employed or larger). In our regression analyses we will use a more detailed sector classification that was not available for the general population.

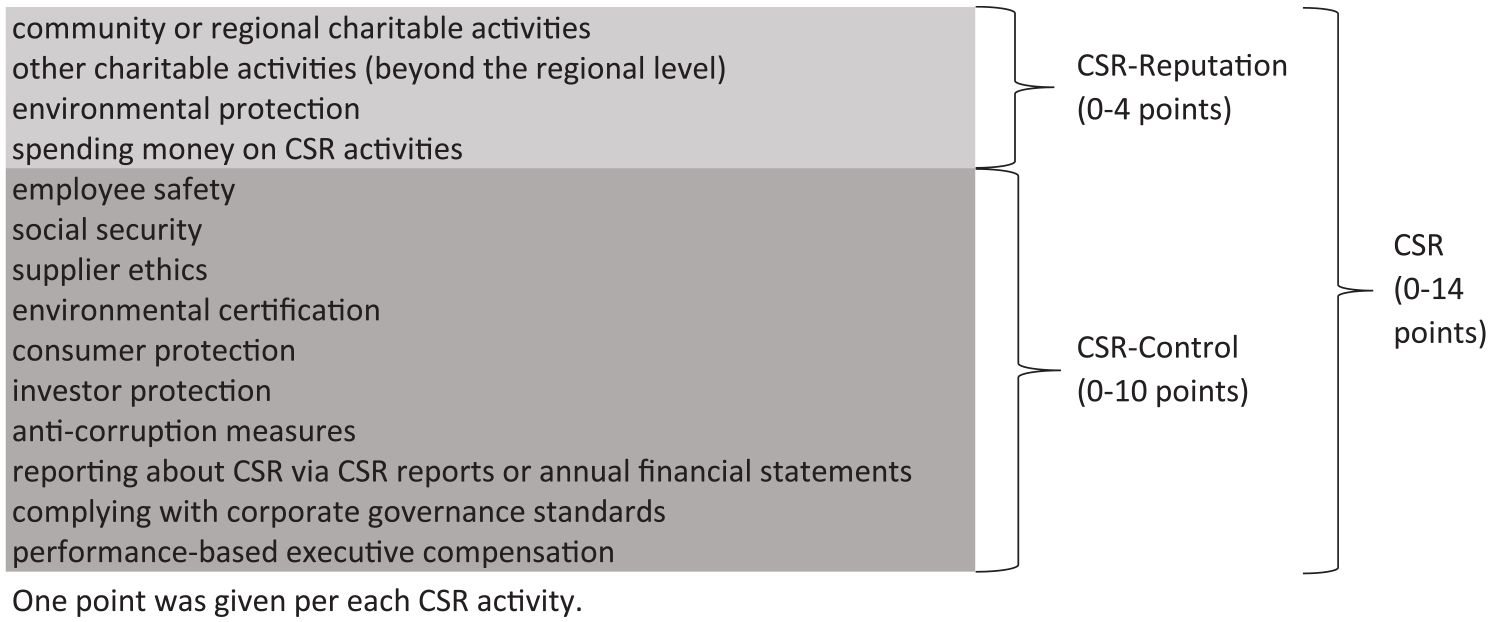

We use a novel survey-based measure of CSR commitment. In line with our understanding of CSR (see the definition above), respondents were asked whether their firms voluntarily engage in activities that are directed toward employee safety, social security, community or regional charitable activities, other charitable activities (beyond the regional level), supplier ethics, environmental protection, environmental certification, consumer protection, investor protection, and anti-corruption measures. Based on the answers, we construct an index ranging from 0 to 10. Additional points (1 each) can be acquired for spending money on CSR activities, reporting to the public about CSR via dedicated CSR reports or annual financial statements, complying with corporate governance standards, and relying on performance-based executive compensation. Consequently, the final index ranges from 0 to 14 (see Figure 1).

Survey-based indices of CSR engagement.

Following previous survey-based studies (Li & Tang, 2010; Tang, Li, & Yang, 2015), we operationalize (managerial) overconfidence as the (positive) deviation of an executive’s subjective evaluation of their firm’s situation from its objective economic condition. In this regard, we draw on the overestimation of profitability (e.g., Li & Tang, 2010; Malmendier et al., 2011; Tang, Li, & Yang, 2015) and the underestimation of the firm’s risk (e.g., Ben-David et al., 2007) and add to this the overestimation of liquidity, degree of innovation, and growth opportunities. Executives were asked how they estimate these variables compared to their industry using a Likert-type scale (5 = far above average, 3 = average, 1 = far below average). The executives were supposed to overestimate their situation if they thought that the position of their firm was far (5) or rather (4) above (below for firm risk) their industry average and if their actual profitability or liquidity was below (above for sales risk) the respective industry median. Likewise, concerning the degree of innovation and growth opportunities, executives were to overestimate these variables if they thought they scored far or rather above their industry average and if they lacked positive sales growth or research and development expenses. Finally, our index of overconfidence (OVERC) ranges from 0 (no overestimation) to 5 (overestimation of profitability, liquidity, degree of innovation, and growth opportunities and underestimation of firm risk). Using linear regression models, we measure the effect of family influence and overconfidence on our CSR index.

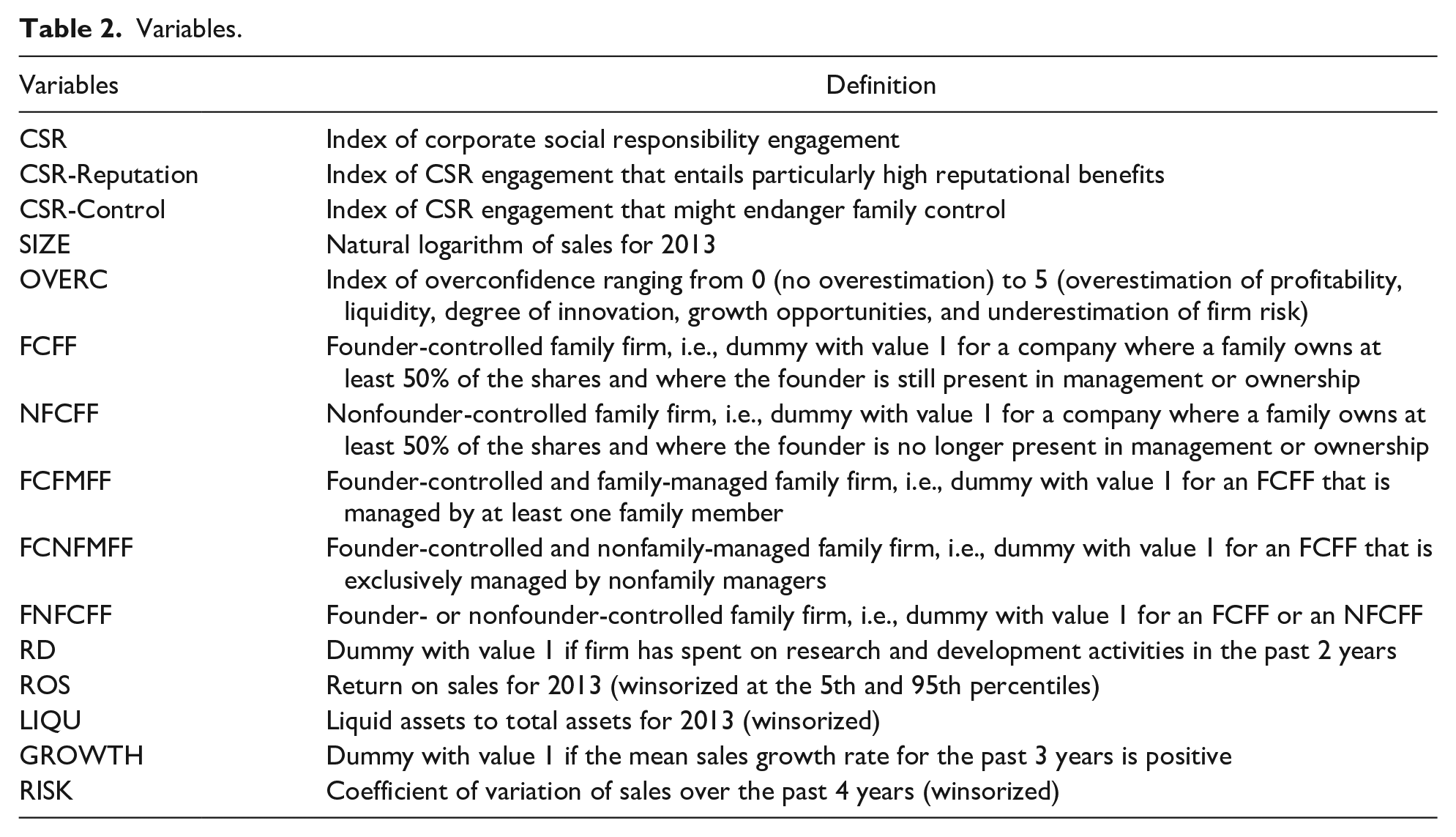

We follow the literature on the determinants of CSR (e.g., El Ghoul et al., 2016; McCarthy et al., 2017) and control for firm-specific variables (see Table 2 for the respective definitions). We expect a positive relationship between firm size (SIZE) and CSR, as larger firms, among others, may have more resources for CSR investments (Margolis et al., 2009), and a negative link between firm risk (RISK) and CSR (e.g., El Ghoul et al., 2011; Margolis et al., 2009). We include research and development expenses (RD), return on sales (ROS), and sales growth (GROWTH) to proxy for innovation and (future) profitability. A positive association is expected because CSR is positively linked to corporate innovation, performance, and growth opportunities in the literature (C. Chen et al., 2016; Margolis et al., 2009; McWilliams & Siegel, 2000). Moreover, financially constrained firms should have fewer resources to invest in CSR (Di Giuli & Kostovetsky, 2014; Hong et al., 2012). Thus, we include proxies for liquidity (LIQU) and expect a positive relationship between liquidity and CSR. Furthermore, we control for industry effects in all our regressions (see Table 3 for the respective sectors used in the regressions).

Variables.

Descriptive Statistics.

Note. CSR = corporate social responsibility. Description of the variables can be seen in Table 2.

Table 2 summarizes all variables we use.

Results

Descriptive Statistics

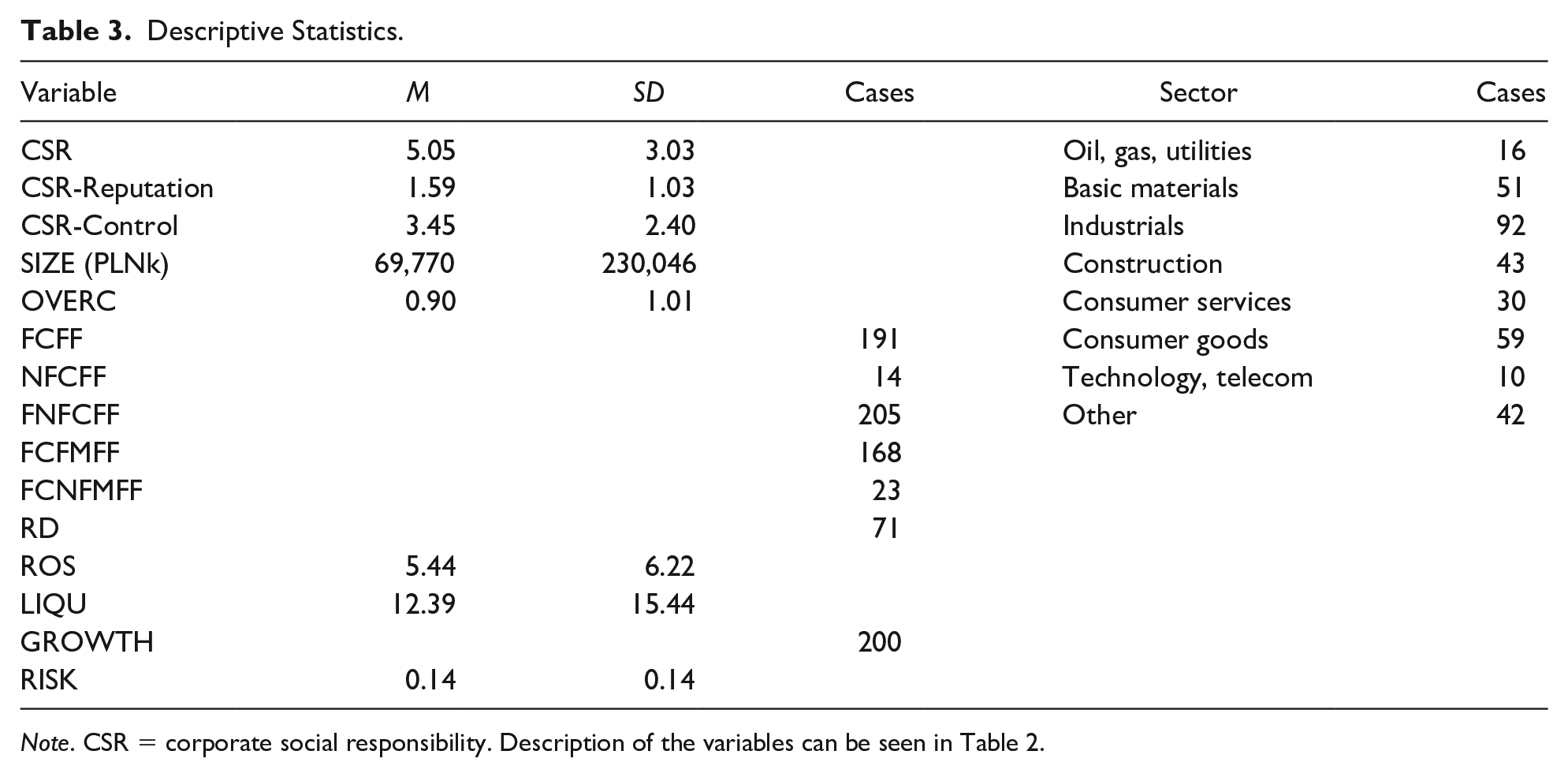

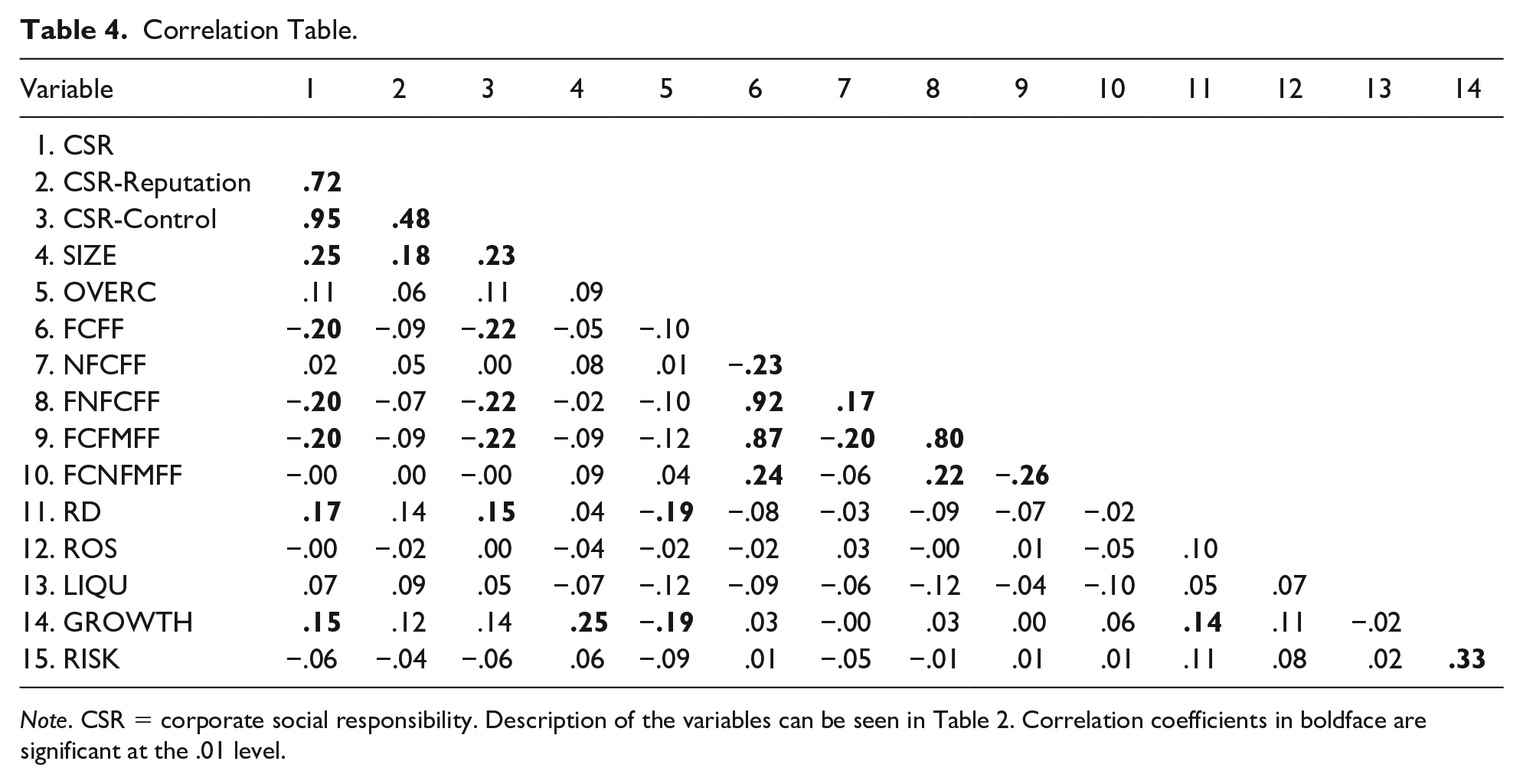

Table 3 lists the mean values and standard deviations for the metric variables and the numbers of cases for the dummy variables, whereas Table 4 shows the correlations between the variables. We could not identify signs of (severe) multicollinearity because all correlation coefficients between the independent variables used in the respective models are (far) less than .8 (e.g., Argyrous, 2011) and the single variance inflation factors are far less than 5 (Studenmund, 2017).

Correlation Table.

Note. CSR = corporate social responsibility. Description of the variables can be seen in Table 2. Correlation coefficients in boldface are significant at the .01 level.

Results for Base Models

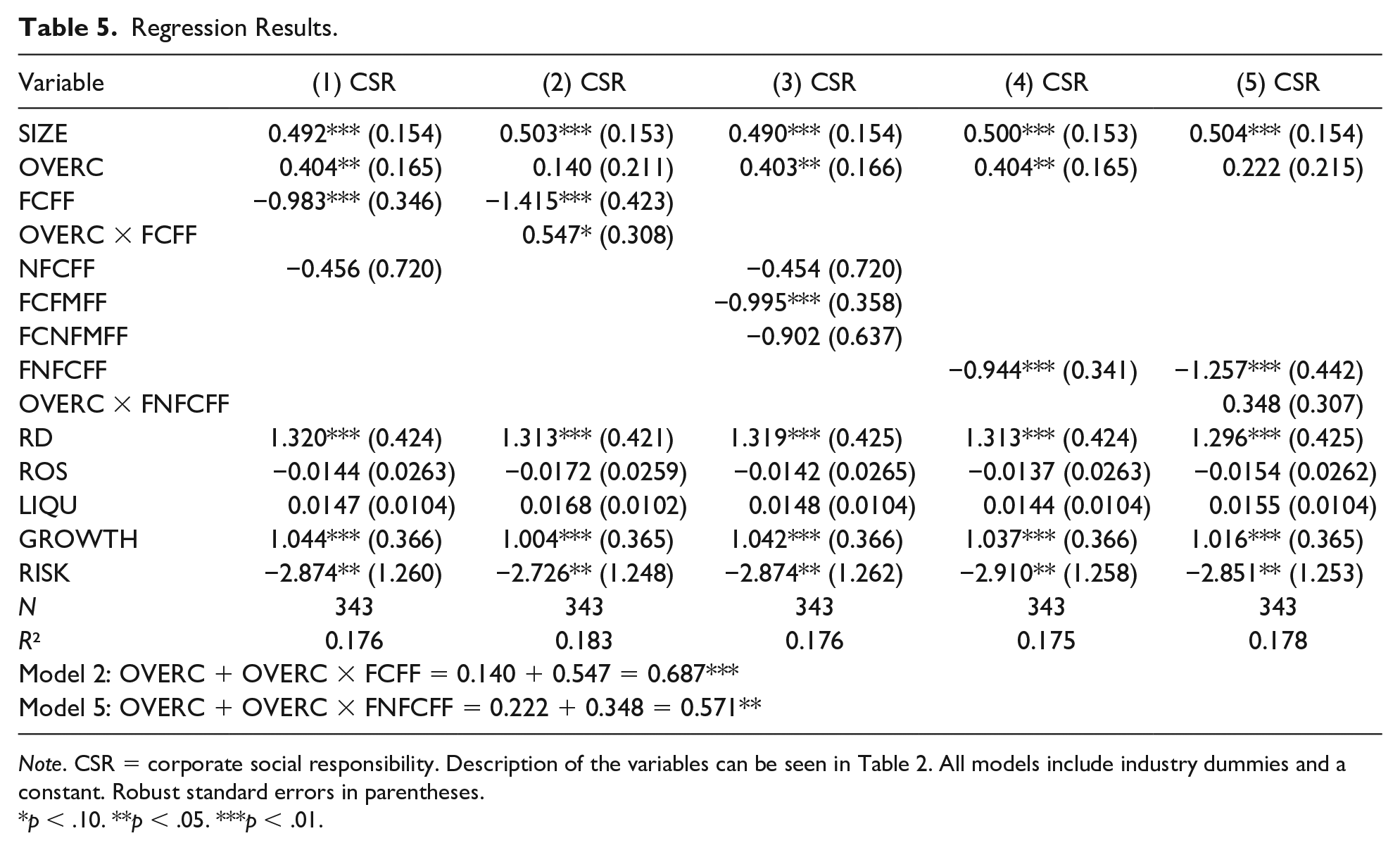

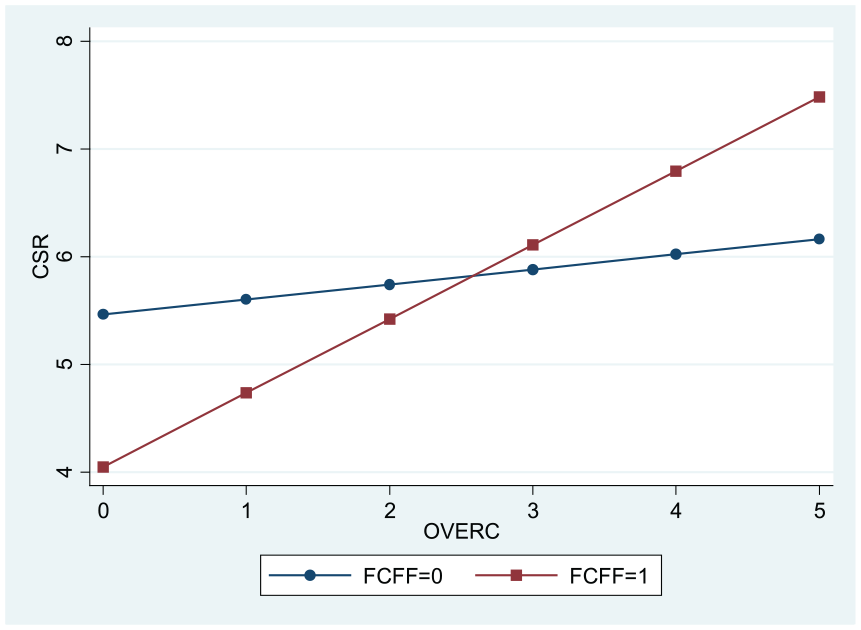

Table 5 reports our results. Model 1 shows that a respondents’ overconfidence (OVERC) entails a higher CSR engagement, whereas the CSR level of FFs with founder presence (FCFF) is significantly lower. As FCFFs are reluctant to engage in CSR, the family control dimension of SEW seems to play a more crucial role than do reputational considerations and, therefore, the family identification dimension, which supports Hypothesis 1a. In Model 2, we test the interaction between FCFF status and overconfidence. The interaction variable OVERC × FCFF indicates that the effect of overconfidence is significantly higher in FFs with founder presence than in other firms. Correspondingly, if we sum up OVERC and OVERC × FCFF, we find a significantly positive effect of overconfidence on CSR in FCFFs, thereby supporting Hypothesis 2, whereas the insignificant effect for OVERC shows that in other businesses, overconfidence does not lead to a higher CSR level. Figure 2 illustrates the interaction effect graphically and documents a (much) steeper slope of OVERC for FCFF compared to other firms. In summary, we find evidence that FCFFs exhibit a lower level of CSR and that overconfidence has a positive impact on CSR exclusively in FCFFs, suggesting that this trait shifts the SEW reference point in FCFFs from maintaining family control (family control dimension) to enhancing image and reputation (family identification dimension).

Regression Results.

Note. CSR = corporate social responsibility. Description of the variables can be seen in Table 2. All models include industry dummies and a constant. Robust standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

Interaction effect between OVERC and FCFF on a firm’s CSR engagement.

The very limited number (14) of FFs without founder presence (NFCFF) makes it difficult to draw conclusions for this group. Nevertheless, the nonsignificant coefficient for NFCFF in Model 1 suggests that the lower CSR engagement of FFs is probably solely driven by those with founder presence, which corresponds to previous evidence that the family’s control concerns are particularly pronounced in the founder stage (e.g., Gómez-Mejía et al., 2007; Keasey et al., 2015; Stockmans et al., 2010; Vandemaele & Vancauteren, 2015), whereas reputational considerations play only a minor role for these firms (Bingham et al., 2011; Ding & Wu, 2014). Moreover, we control for family management as a determinant of (FC)FF heterogeneity (e.g., Chirico & Bau, 2014). As previous studies suggest that control intentions of owner families diminish as they hand over the management to external nonfamily managers (e.g., Gómez-Mejía et al., 2007; Vandemaele & Vancauteren, 2015), we expect that control concerns of the family will particularly lead to a lower CSR engagement if their firm is (still) managed by the family. Model 3 provides evidence for this, as only FFs with founder presence that are managed by at least one family member (founder-controlled and family-managed FFs —FCFMFF) show a lower level of CSR, whereas the same does not hold true for those that are exclusively managed by nonfamily managers (founder-controlled and nonfamily-managed FFs —FCNFMFF). Nevertheless, this result should also be considered with care, as only a rather limited number (23) of FCFFs are exclusively managed by nonfamily managers. For robustness reasons, we reran our models by adding both FFs with and without founder presence into a single variable (FNFCFF). These Models 4 and 5 provide similar results when compared to the base models. Although in Model 5, OVERC × FNFCFF is not significant, overconfidence (only) has a positive effect on CSR in FNFCFF (OVERC + OVERC × FNFCFF). Finally, although profitability (ROS) and liquidity (LIQU) do not affect CSR in Models 1 to 5, all the remaining control variables are significant and show the expected signs, that is, larger (SIZE), more innovative (RD), and higher growth (GROWTH) firms show a higher CSR engagement, whereas firm risk (RISK) affects CSR negatively.

Results for CSR Subindices

To analyze the effect of family influence and overconfidence on different CSR activities, we identified activities that seem to have the greatest reputational benefits while showing the lowest level of commitment to nonfamily stakeholders or the limitation of discretion that could endanger family control at the same time. On one hand, community or charitable activities seem to entail high (Cruz et al., 2014) or even the highest reputational benefits (McCarthy et al., 2017). These findings seem to hold especially true for CSR engagement targeted at the local community, as it allows family actors to be recognized as good corporate citizens (Campopiano & De Massis, 2015). Similar arguments can be made for environmental activities (Campopiano & De Massis, 2015; Cruz et al., 2014; McCarthy et al., 2017). On the other hand, especially activities directed toward internal stakeholders (e.g., employees or in the area of governance) seem to restrict the family’s control over their (listed) firm (Cruz et al., 2014). In line with this, (FC)FFs, for example, were found to refrain from performance-based compensation for family employees and managers (e.g., Cruz et al., 2010; Cruz et al., 2014; McConaughy, 2000) or to make less voluntary disclosure about corporate governance practices (Ali et al., 2007). Moreover, Campopiano and De Massis (2015) show that (large- and medium-sized) FFs not only place less emphasis on the stakeholder groups shareholders, employees, and customers in CSR reports but also seem to be less compliant with CSR standards, as formalized and bureaucratic constraints might limit their managerial authority and autonomy. We think that in our sample of mostly medium-sized and (almost exclusively) nonlisted FCFFs, activities entailing a commitment toward (powerful) internal (shareholders and employees) and external stakeholders (e.g., customers or suppliers) might limit the family control or the discretion of family actors to an even higher extent than in listed or larger companies. The same should hold true for CSR activities requiring adherence to regulations (e.g., anti-corruption regulations, environmental certification). In this regard, we constructed an “CSR-Reputation” index ranging from 0 to 4 representing CSR engagement that entails particularly high reputational benefits, wherein points can be acquired for voluntary engagement in the areas of community or regional charitable activities, other charitable activities (beyond the regional level), environmental protection, or spending money on CSR. The remaining CSR activities—voluntarily engaging in the fields of employee safety, social security, supplier ethics, environmental certification, consumer protection, investor protection, and anti-corruption measures; reporting about CSR via CSR reports or annual financial statements; complying with corporate governance standards and performance-based executive compensation—are considered to be CSR engagement that might endanger family control and were assigned to an “CSR-Control” index ranging from 0 to 10 (see Figure 1). They not only seem to have lower reputational benefits but also might limit the family’s authority, discretion, and autonomy by bringing along a higher commitment to (powerful) nonfamily stakeholders and/or an adherence to bureaucratic regulations.

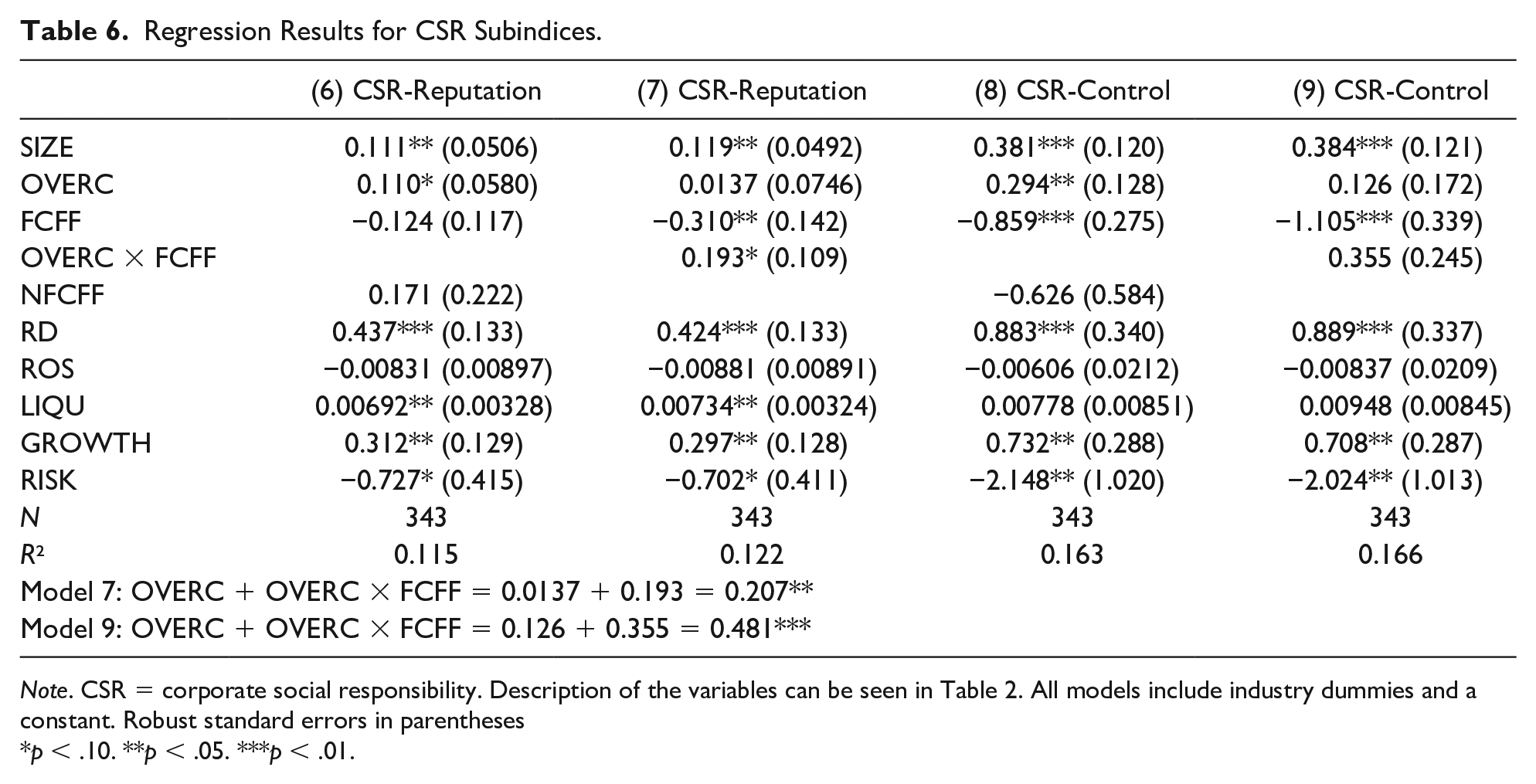

Table 6 reports the results for our two CSR subindices. FCFFs exhibit a similar level of CSR activities that entail particularly high reputational benefits (CSR-Reputation) as do NFFs in Model 6, which supports Hypothesis 1c; however, in line with Hypothesis 1b, we notice a significantly lower level of CSR activity that might endanger family control (CSR-Control) in Model 8. The results confirm that concerns emphasized by the family control dimension of SEW induce FCFFs to avoid CSR activities that might challenge family control. Although reputational concerns (family identification dimension of SEW) do not induce them to show a higher CSR engagement than do NFFs, they show at least the same level of CSR activities that entail high reputational benefits as do other firms.

Regression Results for CSR Subindices.

Note. CSR = corporate social responsibility. Description of the variables can be seen in Table 2. All models include industry dummies and a constant. Robust standard errors in parentheses

p < .10. **p < .05. ***p < .01.

Robustness Tests

Our results seem to be quite robust, as alternative specifications for FCFF—apart from replacing FCFF by FNFCFF, we recalculated FCFF using a lower threshold of family ownership (25% instead of 50%)—and OVERC—we modified our overconfidence index by dropping one of the five variables estimated by our respondents, respectively, and, in addition, replaced the index by dummy variables indicating overconfidence toward at least one or two of the five variables—yield (qualitatively) similar results. The same holds true for different specifications of CSR engagement. These alternative CSR measures range, among others, from a weighted CSR index—respondents were asked to estimate their voluntary CSR engagement in activities that are directed toward employee safety, social security, community or regional charitable activities, other charitable activities (beyond the regional level), supplier ethics, environmental protection, environmental certification, consumer protection, investor protection, and anti-corruption measures using a Likert-type scale (5 = very high engagement, 1 = very low engagement)—to a very basic CSR measure, where respondents just indicated whether they report to the public about CSR via dedicated CSR reports or annual financial statements or not. Since our study builds on self-reported data, these different measures and response formats may also alleviate a potential common method bias by allowing a methodical separation of measurement. In addition, we control for this potential bias by guaranteeing response anonymity (Podsakoff et al., 2003) and, following Podsakoff and Organ (1986) and other studies in the FF context (e.g., Kellermanns & Eddleston, 2006; Liang et al., 2014; Zahra et al., 2004), by applying Harman’s one-factor test. As neither a single factor nor a general factor that accounts for the majority of the covariance among our variables emerges, the test confirms that common method bias is not a serious concern in our study. Moreover, including firm age as additional (yet insignificant) control variable did not change our results.

Finally, we address to what extent our results for overconfidence might be influenced by narcissism. Narcissists exhibit an inflated positive view of the self and want to affirm this self-view (W. K. Campbell et al., 2004; Morf & Rhodewalt, 2001; Tang et al., 2018). Thus, they may fail in realistically appraising their abilities and likelihood of success, thereby resulting in overconfidence (W. K. Campbell et al., 2004). Indeed, overconfidence has been found to be more pronounced in narcissistic personalities (e.g., W. K. Campbell et al., 2004; Schaefer et al., 2004); Schrand and Zechman (2012) even argue that “extreme” overconfidence is consistent with narcissism. Narcissism could lead to a higher CSR engagement because CSR can be a response to a narcissistic CEO’s high need for image reinforcement, attention, social praise, and admiration by stakeholders (McCarthy et al., 2017; Petrenko et al., 2016; Tang et al., 2018). We think that this effect should be especially pronounced in (FC)FFs because of the very close link between firm and family image (e.g., Berrone et al., 2010; Cennamo et al., 2012). Narcissistic (family and nonfamily) executives gain praise and admiration for promoting CSR not only from the public but also from the (other) members of the family because their image is strengthened by corporate CSR activities. Tang et al. (2018) found evidence that the key difference between narcissistic and hubristic (overconfident) CEOs’ attitudes toward CSR lies in the fact that narcissists want to strengthen their inflated positive self-view through these activities, whereas hubristic personalities care comparatively less about external recognition. Hence, if FCFF executives’ overconfidence is related to narcissism, their overconfidence might have a positive effect on CSR activities entailing high reputational benefits (CSR-Reputation) but not necessarily on those endangering family control (CSR-Control). If (mere) overconfidence affects their behavior, we expect a positive effect on CSR-Control—overconfidence may induce them to underestimate the family’s control risk—but not necessarily on CSR-Reputation. In Models 7 and 9 (Table 6), we find significantly positive (and qualitatively similar) effects of FCFF executives’ overconfidence (OVERC + OVERC × FCFF) on both CSR-Reputation and CSR-Control. Thus, we cannot conclude whether (mere) overconfidence or overconfidence related to narcissism predominantly drives our results, but rather we suppose that both overlapping cognitive biases (Capalbo et al., 2018) might favor CSR activities in FCFFs.

Discussion and Conclusions

Contributions to Research

Whereas previous evidence on the CSR policies of FFs compared to those of NFFs is almost exclusively limited to listed companies, we provide survey evidence for mostly medium-sized, nonlisted firms from Poland. This relatively young free-market economy allows us to analyze a unique and homogeneous set of FFs controlled by founders, a group that could be particularly susceptible to psychological traits such as overconfidence (e.g., Landier & Thesmar, 2009; Lee et al., 2017). Moreover, Poland features a very strong Catholic influence (e.g., Gasparski, 2005). This characteristic helps us to isolate the effect of different SEW dimensions or reference points and psychological traits on the CSR policies of FCFFs while assuming that the surveyed executives share similar values with regard to their homogeneous cultural and religious background.

We show that FCFFs exhibit lower CSR engagement, yet this evidence holds true only for activities that might endanger family control. Moreover, overconfidence promotes CSR activities solely in FCFFs but not in other firms. Therefore, at first sight, our study seems to confirm previous evidence indicating a lower level of CSR in FFs (e.g., El Ghoul et al., 2016; Rees & Rodionova, 2015) in the context of FCFFs. Families in the founder stage seem to restrict the CSR efforts of their firms, as they want to ensure control over their company to protect their socioemotional endowment. This finding suggests that at least in FCFFs the family control dimension of the SEW dominates over reputational considerations and, therefore, the family identification dimension when shaping their CSR engagement. Accordingly, we can confirm previous studies that indicate a stronger reluctance to give up control in the founder stage (e.g., Gómez-Mejía et al., 2007; Keasey et al., 2015; Stockmans et al., 2010; Vandemaele & Vancauteren, 2015) or the diminished reputational concerns and thus lower CSR performance of younger FFs (Ding & Wu, 2014) as well as those with founder presence (Bingham et al., 2011).

Our results, however, should not be interpreted as evidence for socially irresponsible behavior by FCFFs in general. Rather, we confirm the results of Cruz et al. (2014) for listed firms that FFs avoid CSR engagements that endanger family control but exhibit the same level of CSR activities that entail particularly high reputational benefits as do NFFs and thus can be both “socially responsible and irresponsible at the same time” (Cruz et al., 2014, p. 1295) for smaller and nonlisted FCFFs. This picture is reinforced by our result that overconfident FCFF executives tend to show higher CSR engagement. Thus, corroborating previous evidence (e.g., Huang et al., 2016; Landier & Thesmar, 2009) in the context of FCFFs, overconfidence may induce executives to underestimate the family’s risk of losing control over the business. Consequently, not only unanticipated reputational “shocks”, such as scandals (Vardaman & Gondo, 2014), but also personality traits, such as overconfidence, seem to shift the reference point in FCFFs from maintaining family control (family control dimension of SEW) to image and reputation enhancement (family identification dimension). Thus, the analyzed psychological trait might entail a stronger adherence of FCFF executives to ethical and moral values. Consequently, we add evidence to the previous literature (e.g., Hirshleifer et al., 2012; Judge et al., 2009; Tang, Li, & Yang, 2015) that “dark side” leader traits such as hubris could also bring along positive effects.

Contributions to Practice

Our evidence is highly relevant for practice. Stakeholders who want to build relationships with FCFFs based on CSR principles must be aware that this might arouse opposition from family actors. They, however, should realize that the reluctance of FCFFs to engage in CSR might not be a sign of social irresponsibility but rather an attempt of the family to protect its influence and control. Moreover, owner families and FCFF executives should take into account that CSR activities might not necessarily endanger family control but could entail numerous advantages, such as promoting image and reputation, fostering stakeholder relations, and gaining legitimacy as good corporate citizens. Finally, both stakeholders and families should know that the psychological traits of FCFF executives play a decisive role in their attitude toward CSR.

Limitations

Finally, some (methodological) limitations should be acknowledged. First, our overconfidence index does not delineate (mere) overconfidence from overconfidence related to narcissism. Although we have found some evidence that both of them might drive our results, future studies should try to overcome this shortcoming by developing distinctive measures for these traits in the context of not only listed firms (as Tang et al., 2018, did) but also private firms. Second, although we addressed nonresponse bias and representativeness, our final sample is not necessarily representative of all FCFFs. Thus, care should be taken in applying our results to larger/listed firms or enterprises based outside of Poland or Europe. Particularly, as it consists almost exclusively of founder-controlled and family-managed FFs, the study does not allow a well-grounded analysis of the effects of different family generations or of nonfamily management. Further studies involving more mature markets could overcome these issues. Third, our study relying on cross-sectional survey data may suffer from a potential reverse causality issue, that is, that the CSR engagement of a firm might affect its ownership structure and/or its executive overconfidence. Nevertheless, we believe this is not a major issue. (1) The family’s intention to maintain control, which is particularly pronounced in the founder stage (e.g., Gómez-Mejía et al., 2007), and thus the stable ownership structure of (FC)FFs makes a reverse causality problem for family ownership rather unlikely (e.g., Andres, 2011; Isakov & Weisskopf, 2015). In line with this argument, previous research could even document an exogenous impact of the largest shareholder on the firm performance of listed firms, a question that was considered especially susceptible to reverse causality issues (Gugler & Weigand, 2003). (2) Similarly, although we cannot rule out completely that overconfident executives might choose to work in firms with a specific level of CSR engagement, we suppose that such exceptional cases are not a major issue in FCFFs. Finally, qualitative research could address in detail the questions of under what circumstances FCFF actors attach greater importance to reputational considerations than control concerns and how psychological traits affect these decisions.

Concluding Comments

In summary, our results contribute to and extend the concept of SEW, as we demonstrate not only how different SEW dimensions affect the CSR engagement of FCFFs but also how psychological traits such as overconfidence can alter the perception of these different dimensions and thus the frame of reference, which is an issue that, to the best of our knowledge, has not been analyzed until now. Our research takes up the calls to examine the effect of cognitive biases on SEW decisions (Jiang et al., 2018) and to analyze the conflicts between SEW dimensions (e.g., Chua et al., 2015; Kellermanns et al., 2012; Vardaman & Gondo, 2014). In addition, we respond to proposals to distinguish the positive outcomes from the negative outcomes of different SEW priorities (Miller & Le Breton-Miller, 2014) or—as Kellermanns et al. (2012, p. 1175) call it—to look at the “dark side” of SEW. At first glance, FCFFs seem to follow family-centric and/or self-serving SEW priorities—in the form of a lower CSR engagement to ensure continued family control—that might run counter to the interests of nonfamily stakeholders. However, detailed analyses reveal that FCFFs show the same level of community, charitable, or environmental activities as their nonfamily counterparts and therefore might also promote reputation and sustainability. Moreover, the analyzed psychological trait also seems to lead to positive outcomes, with a stronger emphasis on sustainability and nonfamily stakeholders.

Footnotes

Acknowledgements

This study was carried out within a larger research project on firm policies of Polish family firms. We are grateful to Jerzy Węcławski and Robert Zajkowski (Maria Curie Skłodowska University, Lublin, Poland) for their cooperation in the project (e.g., in designing the questionnaire). Moreover, we would like to thank our guest editor, Yi Tang, and the two anonymous reviewers for their very insightful and constructive comments and suggestions. Finally, we appreciate the helpful feedback from participants and reviewers of the IFERA (International Family Enterprise Research Academy) Annual Conference 2018 in Zwolle (Netherlands) and the EMFAIC (Emerging Markets Finance and Accounting International Conference) 2018 in Linz (Austria).

Declaration of Conflicting Interest

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Markus Dick and Helmut Pernsteiner have received research grants from Narodowe Centrum Nauki (Krakow, Poland: NCN Project No. 2012/07/B/HS4/00455).