Abstract

The ways in which partners manage their money provide important clues to gender inequality in and the nature of couple relationships. Analyzing data from nationally representative surveys (N = 11,730 couples), I examine changes across British cohorts born between the 1920s and 1990s in their household financial management, and how the changes vary across individuals and couples occupying differential income positions. The results show divergent, nuanced cohort trends toward gender equality in couples’ money management. Across successive cohorts of low-earning women, there has been a subtle relaxation in the form of male control, reflected in a decrease in the proportion of men adopting “back-seat” management by retaining the majority of the couple’s money while delegating the chore of managing daily expenses to their partners. By contrast, the empowerment of high-earning women is reflected primarily in an individualization of financial management, evident in a cohort decrease in joint financial management and an increase in independent management. The trend of individualization is particularly prominent among couples in which both partners have equally high earnings. The findings provide new insights into and important extensions of the theorization of gender relations in and the individualization of couple relationships.

Over the past decades, there has been a long march toward gender equality in the public sphere, which is reflected in a long-term increase in women’s education and labor force participation, a decrease in the gender wage gap, and a rise in women’s economic status (England 2010; England, Levine, and Mishel 2020; Gerson 2009; Goldscheider, Bernhardt, and Lappegård 2015). By contrast, however, progress toward gender equality lags far behind in the domestic sphere (Sullivan, Gershuny, and Robinson 2018). While much research has focused on care and housework as the “last bastion” in the gender revolution (e.g., Few-Demo and Allen 2020; Geist and Cohen 2011), relatively less attention has been paid to what happens to earnings after they enter the household and to gender inequality in how partners manage their money. 1

Household financial management contains crucial clues to the nature of and inequality in couple relationships (Anderson 2017; Bennett 2013; Burgoyne 2004; Pahl 1990; Treas 1993). Partners’ decision to pool their money or keep separate purses indicates whether their union is built on the foundation of unitary collectivism or represents an association of two autonomous individuals (Bennett 2013). Thus, examining household financial management puts to the test Beck and Beck-Gernsheim’s (2002) individualization thesis, Giddens’ (1992) prediction of the decline of the material foundation of late-modern intimacy, and Cherlin’s (2010, 2020) theorization of the deinstitutionalization of marriage. Partners’ unequal access to money has far-reaching consequences for intra-household inequalities in living standards, life satisfaction, and housework division (Hu 2019; Kulic, Minello, and Zella 2020; Lersch 2017). Because such inequalities are often gendered, contestation over money and power in couple relationships is a key focus of gender research (Anderson 2017; Kenney 2006; Pepin 2019).

Despite increasing scholarly interest in intra-household economy and its gender inequalities (see Bennett 2013 and Kulic and Dotti Sani 2017 for comprehensive reviews), the cohort dynamics of household financial management and its relationship with earnings remain insufficiently studied. This raises two important questions, which I address in this research:

How have the ways in which partners manage their money changed across distinct birth cohorts?

How do the cohort trends vary over the distributions of partners’ individual, relative, and total earnings?

Answering these questions promises to provide crucial insights into the interplay between the gender revolution and the transformation of intimate relationships (Goldscheider, Bernhardt, and Lappegård 2015; Sullivan, Gershuny, and Robinson 2018). Has the gender revolution fashioned a cohort increase in gender equality in financial management as reflected in women’s enhanced access to or autonomy over money in the household? If so, what have been the inter-cohort pathways toward gender equality? Across successive cohorts, have women’s earnings come to play a more prominent role in bolstering their bargaining power and thus control of the couple’s money; or have they given rise to women’s financial autonomy and helped individualize household financial management (cf. Beck and Beck-Gernsheim 2002; Cherlin 2010; Giddens 1992)? Looking through an intersectional lens (Collins and Bilge 2020), how do the pathways of cohort change differ between women with low and high earnings, and how do they vary with partners’ total earnings?

To answer these questions, I analyze nationally representative data (N = 11,730 couples) from the British Household Panel Survey (BHPS) and the United Kingdom Household Longitudinal Study (UKHLS). The results uncover divergent cohort trends toward gender equality in household financial management across individuals and couples occupying differential income positions. While the form of male control has undergone a subtle relaxation across successive cohorts of women with low earnings, there has been a cohort increase in the proportion of high-earning women who manage their money independently rather than control the couple’s money. The individualization of partners’ money management—for example, a cohort decrease in joint financial management and an increase in independent management—is more prominent among high-income individuals and couples than among their low-income counterparts. The findings provide new insights into and important extensions of the theorization of gender relations in and the individualization of couple relationships.

Theoretical Considerations and Literature Review

Theorizing Systems of Household Financial Management

My research focuses on couples’ everyday money management. Previous research has examined other aspects of household finances, such as savings, debts, and investments (Burgoyne 2004; Kan and Laurie 2014; Lersch 2017; Tisch and Lersch 2021; Treas, 1993). I do not focus on these aspects because they are susceptible to diverse mechanisms of selection into having savings, debts, and investments (Kan and Laurie 2014). Arguably, all couples manage their money on a daily basis (Bennett 2013). Although managing the household’s finances does not necessarily equate with absolute control of money (Himmelweit et al. 2013; Pahl 1995), financial management plays a crucial role in providing partners with the essential access to money and thereby enhancing their financial satisfaction and well-being (Elizabeth 2001; Kulic, Minello, and Zella 2020; Lersch 2017). What makes money management distinctive, complex, and interesting is its duality—as a means of seizing power and as a housekeeping chore (Burgoyne et al. 2007; Hu 2019).

Existing research has identified four major systems of household financial management (Pahl 1995; Pepin 2019; Vogler 1998), which distribute power and responsibilities between partners in distinct ways. First, in the joint system, partners pool most or all of their money (Kenney 2006; Pahl 1990), which implies that partners not only have equal access to their money but also share the chore of money management (Pahl 1995). Second, in the independent system, partners manage most or all of their money separately (Burgoyne 2004; Pahl 1995). Third, in the allowance system, one partner, usually the male, manages the couple’s money and gives the other a housekeeping allowance (Vogler 1998). Because a housekeeping allowance has a designated use, its recipient has little power over the household’s finances (Pahl 1995). Finally, in the whole-wage system, one partner manages the couple’s money and the other hands over his or her money, retaining a small amount of personal spending money (Bisdee, Daly, and Price 2013). Here, a further distinction can be made between male whole-wage (i.e., the male partner manages the couple’s money) and female whole-wage (i.e., the female partner manages the couple’s money) systems. Because personal spending money is less restrictive than housekeeping allowance, the partner who does not manage the couple’s money has greater power and financial autonomy in the whole-wage than in the allowance system.

Underlying the different systems are distinct allocative principles, which are theorized along two lines. The first line of principles—unity and autonomy—focuses on whether partners pool their money or keep separate purses. Conceptualizing partners as cooperative social actors in a collectivist couple unit (Becker 1991), the norm of unity obliges partners to pool their money to foster a sense of solidarity (Pepin 2019; Tisch and Lersch 2021). Money pooling is reinforced by the marital institution, as joint management is more common in first marriage as opposed to remarriage or unmarried cohabitation, when partners have children, and as the duration of a relationship increases (Burgoyne and Morison 1997; Lott 2017; Treas 1993). Pooling also reduces the transaction cost of transferring money between partners (Treas 1993). By contrast, the autonomy principle conceptualizes couplehood as an association of two autonomous individuals who retain ownership of their respective money (Elizabeth 2001; Pepin 2019).

The second line of principles—entitlement, equity, and equality—focuses on who manages the couple’s money. The entitlement principle allocates the right to money based on ascribed characteristics such as gender (Deutsch 1975). Traditional gender ideologies prioritize “men’s ‘natural’ right to money” and women’s responsibility in making money (i.e., housekeeping allowance) stretch (Nyman 2003, 92). The equity principle allocates rewards (i.e., access to money) in proportion to input (i.e., earnings) (Deutsch 1975; Tisch and Lersch 2021). Reinforcing this principle, the resource-bargaining theory posits that partners’ greater contribution to the couple’s earnings enhances their bargaining position in household finances (Becker 1991). Under the male-breadwinner norm, however, high-earning women—particularly those who out-earn their partners—may not benefit from the equity principle; rather, they may “perform gender” by relinquishing money management to protect their partners’ masculinity (Pahl 1995; West and Zimmerman 1987). The equality principle emphasizes “partnership of equals” and, as a result, equal access to the couple’s money regardless of input (Tisch and Lersch 2021; Vogler 2005).

Theorizing and Contextualizing Cohort Changes in Household Financial Management

The above principles are not immutable but are susceptible to social changes. While previous research has provided illuminating snapshots of how couples manage their money (e.g., see Bennett 2013 and Kulic and Dotti Sani 2017 for comprehensive reviews; see Anderson 2017; Kulic, Minello, and Zella 2020; Lersch 2017; Lott 2017; Pepin 2019; and Tisch and Lersch 2021 for research published since the reviews), scholars are yet to establish a systematic understanding of how, if at all, the systems of household financial management have evolved alongside sweeping social changes that demarcate distinct birth cohorts. In this section, I provide a theoretical and contextual account of why we might expect the systems and underlying principles of household financial management to vary across cohorts in the UK.

The last few decades have witnessed dramatic changes in gender ideologies, relations, and structures. With the decline of gender essentialism and the rise of gender egalitarianism (Cotter, Hermsen, and Vanneman 2011; Scarborough, Sin, and Risman 2019; Scott, Crompton, and Lyonette 2010), the entitlement principle may have become less relevant and the equality principle may have become more salient in determining how couples manage their money. Meanwhile, the progress toward gender equality in the UK, at least in education and employment, has outpaced the average progress across the Organization for Economic Co-operation and Development (OECD) countries, which may have helped enhance women’s bargaining power in household financial management across cohorts. The gender gap in education has reversed in the UK (Klesment and van Bavel 2017), driven by an increase in women’s tertiary education participation rate from 24.9 to 55.1 percent between 1998 and 2019, compared with 24.3 to 51.3 percent across the OECD countries (OECD 2021a). The employment rate of the UK women ages 16–64 years increased from 52.8 percent in 1971 to 72.1 percent in 2020 (Office for National Statistics [ONS] 2021), at a speed that far exceeded the OECD average. The gender gap in gross hourly wage decreased from 46.4 to 16.0 percent between 1974 and 2019, compared with 38.1 to 18.5 percent in the US (OECD 2021b).

The ideological underpinnings and forms of couple relationships have also changed considerably. Proponents of the individualization thesis have cast doubt on the economic foundation of unitary couple units, arguing that as partners seek to produce their individual biographies, intimate relationships have become individualized (Beck and Beck-Gernsheim 2002). In theorizing the rise of “pure relationships,” Giddens (1992) predicted the waning importance of economic interdependence between intimate partners. Cherlin (2010, 2020) described a shift in the force that binds intimate partners together: from functional exchange to equal companionship, and then to the individualized pursuit of self-growth. Alongside these ideological changes, couple relationships have become more diverse. As in the US (Cherlin 2020), there has been a long-term rise of unmarried cohabitation and a decline of marriage in the UK; and the divorce rate increased from 2.8 to more than 14 per 1,000 married people between 1971 and 1993, and then decreased continuously since 1993, due partly to plummeting marriage rates (ONS 2018). These trends may have undermined the foundation of unitary couplehood and conferred greater marital power upon women (Lewis 2001).

In the UK, legal, policy, and technological changes may have also helped “individualize” couples’ financial management. The UK Family Law builds on an ideology of unitary collectivism, holding spouses and civil partners financially liable for each other (Gilmore and Glennon 2020). Although assets accumulated during marriage or civil partnership are equally divided upon union dissolution, the division of assets in unmarried cohabitation, which has become more prevalent across cohorts, is determined by each partner’s contribution (Gilmore and Glennon 2020). Meanwhile, the UK’s taxation and welfare systems—such as calculation and deduction of income tax and welfare payments—have become individualized since the 1980s (Daly and Scheiwe 2010). Compared with conservative and democratic welfare regimes (e.g., Germany and the Scandinavian countries), the liberal welfare regime in the UK, as in the US, places a greater emphasis on the individual rather than the family collective (Castles et al. 2010). Moreover, an increase in the adoption of internet and mobile banking has reduced the transaction costs of independent financial management. In 2019, more than 90 percent of people ages 16–34 years in Great Britain used internet banking, as opposed to 38 and 18 percent of people ages 75–79 years and 80 years and older, respectively (ONS 2019).

The above trends may have promulgated new norms that valorize autonomy and equality in couple relationships, while undermining men’s entitlement to money. The cohort increases in women’s education, employment, and earnings may have given recent cohorts of women greater power in household finances and created a favorable condition of economic self-sufficiency for them to keep separate purses (Pahl 2005; Pepin 2019). Thus, these trends may have helped individualize household financial management across cohorts, as specified in Hypothesis 1A. Moreover, if partners view managing the couple’s money, through the whole-wage or allowance system, as a means to seize power (Kenney 2006), a cohort increase in women’s power in financial management may be reflected in an increase in women’s and a decrease in men’s management of the couple’s money, as specified in Hypothesis 1B. However, if partners view managing the couple’s money as an onerous chore (Pahl 1995), then, opposite to Hypothesis 1B, there may be a cohort decrease in the female whole-wage system and an increase in the male whole-wage system, as the division of domestic labor becomes more gender-egalitarian and more men undertake the chore of managing the couple’s money across cohorts (Few-Demo and Allen 2020).

Hypothesis 1: There has been a cohort decrease in joint financial management and an increase in independent management (1A); while the female allowance and male whole-wage systems have diminished across cohorts, the female whole-wage system has become more prevalent (1B).

Theorizing Differential Cohort Changes across Income Gradients

To further nuance our understanding of cohort changes in household financial management through an intersectional lens (Collins and Blige 2020), it is important to consider that the changes may have spread unevenly across individuals and couples occupying distinct income positions. Partners with differential resources have different opportunities and constraints to enact the ideals of gender egalitarianism and individualism in daily money management (Nyman 1999; Sung and Bennett 2007).

Women with low individual earnings are unlikely to be economically self-sufficient to adopt independent financial management, according to the autonomy principle (Pahl 2005; Sung and Bennett 2007). Low-income women tend to have low relative earnings vis-à-vis their partners. 2 According to the equity principle (Deutsch 1975), women with low relative earnings are unlikely to develop the bargaining power required to control the couple’s money through the female whole-wage system (Tisch and Lersch 2021). Despite these constraints, the equality principle provides a viable means for recent cohorts of low-income women to access power through joint financial management. As gender equality increasingly extends to the division of domestic labor (Few-Demo and Allen 2020) in encouraging men to undertake the chore of everyday money management, the female allowance system, which is often associated with female housekeeping (Pahl 1995), may have diminished across cohorts of low-income women, while the male whole-wage system may have become more prevalent.

Women with high individual earnings, regardless of cohort, are unlikely to receive a housekeeping allowance (Pahl 1990). Due partly to their high education, recent cohorts of high-income women are more likely to endorse the ideology of individualism than their low-income counterparts (Beck and Beck-Gernsheim 2002); and they are also economically self-sufficient to be able to afford independent financial management (Himmelweit et al. 2013; Pahl 2005). Given a decline of the male-breadwinner norm (Klesment and van Bavel 2017), the pressure may have eased for successive cohorts of high-income women, particularly those who out-earn their partners, to “perform gender” by relinquishing control of financial management to protect their partners’ manhood (Kulic, Minello, and Zella 2020; West and Zimmerman 1987). Thus, there might be a decrease in the male whole-wage system across cohorts of high-income women. However, there may not be a cohort increase in the female whole-wage system among high-income women, because they have the better alternative of deriving power from managing their own money independently than undertaking the more onerous chore of managing the couple’s money. The decline of the male-breadwinner norm also means that recent cohorts of men may have become less obliged to share their earnings with their partners and thus more likely to manage their money independently (Pepin 2019), when they have sufficient earnings to support themselves.

Hypothesis 2: The cohort decrease in joint financial management and increase in independent management are greater among high-income than low-income women and men (2A); the cohort decrease in the female allowance system and increase in the male whole-wage system are greater among low-income than high-income women (2B).

Furthermore, cohort changes in financial management may vary with partners’ total earnings. The economic resources available to a couple affect their ability to individualize their finances. Although income pooling helps low-income couples to coordinate their consumption (Sung and Bennett 2007), high-income couples can afford not to pool (Treas 1993), partly because the latter tend to have two self-sufficient partners. Compared with low-income couples, high-income couples are more likely to be free from material concerns to prioritize the postmaterialist pursuit of individualism and “pure relationships” (Beck and Beck-Gernsheim 2002; Giddens 1992), and they are also better able to afford the transaction costs arising from independent management (Treas 1993). Existing research shows that income pooling is less likely in households with higher income in the US and Sweden (Heimdal and Houseknecht 2003) but not in Denmark (Bonke and Uldall-Pulsen 2007).

Hypothesis 3: The cohort decrease in joint financial management and increase in independent management are greater among couples with higher total income than those with lower total income.

We may not expect cohort trends of women’s and men’s management of the couple’s money to vary with couple total earnings. On the one hand, gender egalitarianism tends to be more closely endorsed by highly educated, affluent couples (Scarborough, Sin, and Risman 2019; Scott, Crompton, and Lyonette 2010), which predicts a cohort increase in women’s power in financial management among high-income couples. On the other hand, as economic necessity increasingly compelled recent cohorts of women in low-income families to undertake paid work (Scott, Crompton, and Lyonette 2010), there may have been a cohort increase in women’s power in financial management among low-income couples as well.

Data and Methods

Data and Sample

I analyzed data from the BHPS and the UKHLS. The BHPS began in 1991 with a nationally representative sample of 10,000 individuals ages 16 years and older from 5,500 households, and the respondents were re-interviewed annually until 2008 (Taylor et al. 2010). Extra households from Scotland and Wales were added to the panel in 1999, and more from Northern Ireland in 2001. The UKHLS was initiated in 2009 as a successor to the BHPS. In the first wave, a nationally representative sample of more than 50,000 individuals 16 years and older from 30,000 households were interviewed (Platt et al. 2020). They have been re-interviewed each year since. The BHPS respondents were absorbed into the UKHLS in its second wave. To ensure data comparability over time, I did not use the Northern Ireland panel, because the BHPS was originally designed to represent Great Britain.

The analytical sample was first limited to survey waves with information on household financial management: BHPS waves 1–5 (1991–1995) and 15 (2005) and UKHLS waves four (2012–2014) and eight (2016–2018). I then limited the sample to working-age (25–64 years) respondents who had participated in the main interviews and lived with their partners (N = 65,317 person-years). As I analyzed information from both partners of a heterosexual couple, I deleted 16,760 person-years with no matching partner records, one person-year with missing information on gender, and 246 person-years in a same-sex relationship (N = 48,310 person-years) and reshaped the data into couple dyads (N = 24,155 couple-years). Then I listwise deleted 1,610 couple-years with invalid or missing information for the variables analyzed (N = 22,545 couple-years). Because the longitudinal data may overrepresent couples who stayed together for longer, I kept one random couple-year observation for each couple, yielding a final analytical sample of 11,730 couples. See Online Appendix A1 for detailed information on sample construction.

Dependent Variable: Household Financial Management

Individual respondents were asked to describe the management of the household’s finances by the two partners. The response categories were as follows: (a) “we share and manage our household finances jointly”; (b) “I look after the household’s money except my partner’s spending money”; (c) “my partner is given a housekeeping allowance; I look after the rest of the money”; (d) “my partner looks after all of the household’s money except my personal spending money”; (e) “I am given a housekeeping allowance; my partner looks after the rest of the money”; (f) “we pool some of the money and keep the rest separate”; (g) “we keep our finances completely separate”; and (h) “I have some other arrangement.” Less than 1 percent of couples in which one or both partners had other financial arrangements were deleted during data cleaning.

I recoded the original categories into five systems: joint (category [a] for both genders), independent (categories [f] and [g] for both genders), female allowance (category [e] for women, [c] for men), male whole-wage (category [d] for women, [b] for men), and female whole-wage (categories [b] and [c] for women, [d] and [e] for men). I combined couples who managed part (f) or all (g) of their money separately into one system, because only a small number of the couples kept their finances completely separate in the earlier cohorts. When partial independence was reported (category [f]), it was not clear what exact proportion of their earnings each partner contributed to the joint pool. However, previous research has found that the item measuring partial independence is likely to be understood as denoting an essential individualism (Hu 2019). Because only 97 couples in the sample adopted the male allowance system (category [c] for women, [e] for men), I merged this system into the female whole-wage category, in which female partners manage the couple’s money (Pahl 1995). The findings were robust to the exclusion of couples who adopted the male allowance system.

For the vast majority of couples, both partners provided valid information on their financial management, and following Lott (2017), a random response from one partner was used to represent a couple. In cases in which one partner failed to provide valid information on the measure (N = 354), I used the corresponding valid response from the other partner. Because partners may provide discrepant information on their financial management, I conducted robustness checks using the responses from the female partner, male partner, and both partners (i.e., using multilevel models clustering partners’ responses in a couple dyad). These alternative specifications yielded substantively consistent results.

Key Predictors

Birth cohort. I created five dummy variables based on the female partner’s year of birth to identify five birth cohorts: ≤1949 (1927–1949), 1950–1959, 1960–1969, 1970–1979, and ≥1980 (1980–1993). Due to cell size considerations, I was unable to further disaggregate the first and last cohorts. An alternative cohort measure based on the male partner’s birth year yielded consistent findings.

Partners’ individual, relative, and total earnings. The survey measured individuals’ monthly gross earnings in British pounds. Whereas net earnings may vary with welfare and tax arrangements, gross earnings comprehensively measure individuals’ earning power. To account for inflation, I adjusted individual earnings to the 2018 value of the pound sterling. I top-coded the measure at the 99th percentile to minimize the influence of outlier cases. I calculated relative earnings as the proportion of the couple’s total earnings represented by the female partner’s earnings. A couple’s total earnings were calculated by adding up both partners’ individual earnings.

Covariates

As presented in Table 1, I controlled for a range of variables that may confound the role played by earnings in moderating cohort changes in financial management. At the individual level, I controlled for both partners’ ages and ethnic minority status. I took account of whether each partner had obtained a higher education degree. In line with the reversal of the gender gap in education (Klesment and van Bavel 2017), a larger proportion of the women (37 percent) than the men (33 percent) were degree holders. Time spent on paid work may constrain the time available for financial management. The survey captured the normal number of weekly hours respondents spent on paid work, using a continuous variable. On average, the women spent fewer hours (M = 19.98) than the men (M = 27.76) on paid work. The average work hours are relatively low because the survey explicitly instructed respondents to exclude non-routine overtime and meal breaks and the sample includes respondents with diverse employment status and arrangements. I controlled for whether each partner was in a remarriage (Burgoyne and Morison 1997) and whether each partner’s parent(s) co-resided in the household.

Sample Characteristics

NOTE: N = 11,730 couples. For dummy variables, 0 = No and 1 = Yes. SD = standard deviation. Mean values are reported for continuous variables and proportions reported for dummy variables. Column proportions may not add up to 1 due to rounding. All earnings measures are adjusted to the 2018 value of British pounds to account for inflation; and 1 British pound ≈ 1.35 U.S. dollars in 2018. Birth cohorts are classified based on the female partner’s year of birth, and alternative classification based on the male partner’s year of birth yielded consistent results.

Gender difference significant at the 1‰ level and below, based on chi-square test for categorical variables and two-tailed t-test for continuous variables.

Top-coded at the 99th percentiles to reduce the influence of outlier cases.

Calculated based on couples with at least one child in the household.

At the couple level, I distinguished between unmarried cohabiting and married couples and controlled for the duration of the current relationship, because household finances tend to become more integrated with marriage (Lott 2017) and over time (Treas 1993). Having non-adult children in the household affects couples’ resource allocation (Burgoyne et al. 2007), so I also controlled for the number of children who were younger than 16 years using a categorical variable—none, one, two, and three and above—and the age of the youngest child in the household. Because the systems of financial management may differ between small and large households, I controlled for household size. Finally, because people’s housing situation impinges on their financial strategies, I also distinguished between homeowners (owned outright or with a mortgage), social renters, and private renters.

Analytic Strategy

The analysis was conducted in two steps. I first conducted descriptive analyses to chart cohort changes in how partners manage their money. Then I fitted logit regression models to explore how partners’ individual, relative, and total earnings, respectively, moderated cohort changes in household financial management. In the models, I used birth cohort, earnings (i.e., both partners’ individual earnings, women’s relative earnings and its quadratic term, and couple total earnings, respectively), and the interaction of cohort and earnings as the key predictors, while controlling for all covariates. In modeling how women’s relative earnings moderated the cohort trends, I controlled for couple total earnings; and in modeling the moderating role of couple total earnings, I controlled for women’s relative earnings and its quadratic term. The difficulty of distinguishing age-period-cohort effects is well documented in existing literature (Yang and Land 2013). Following Mishel et al. (2020), I included respondents’ birth cohort and age, but not survey year (i.e., period), in all models. 3 This means the cohort trends reported here may partly reflect period effects.

I used multiple binary logit regression models for different systems of financial management instead of multinomial logistic regression models, due to smaller cell sizes in the latter (Mishel et al. 2020). Nonetheless, alternative multinomial models yielded substantively consistent results. Although my analytical sample contained nonworking individuals to capture the full range of partners’ income positions, the results were robust to limiting the sample to couples in which both partners were in work. The results were also robust to a more limited sample of couples ages 25–54 years. A variance inflation factor (VIF) test showed that all VIFs, apart from those for quadratic terms, were below the threshold of 2.5 (Li 2013). To provide an intuitive illustration of the results, I graph the conditional probabilities of outcome-category membership against the key predictors. The results for the full regression models are available in the Online Appendices, and those for the robustness checks are available upon request from the author.

Descriptive Findings

Cohort Changes in Household Financial Management

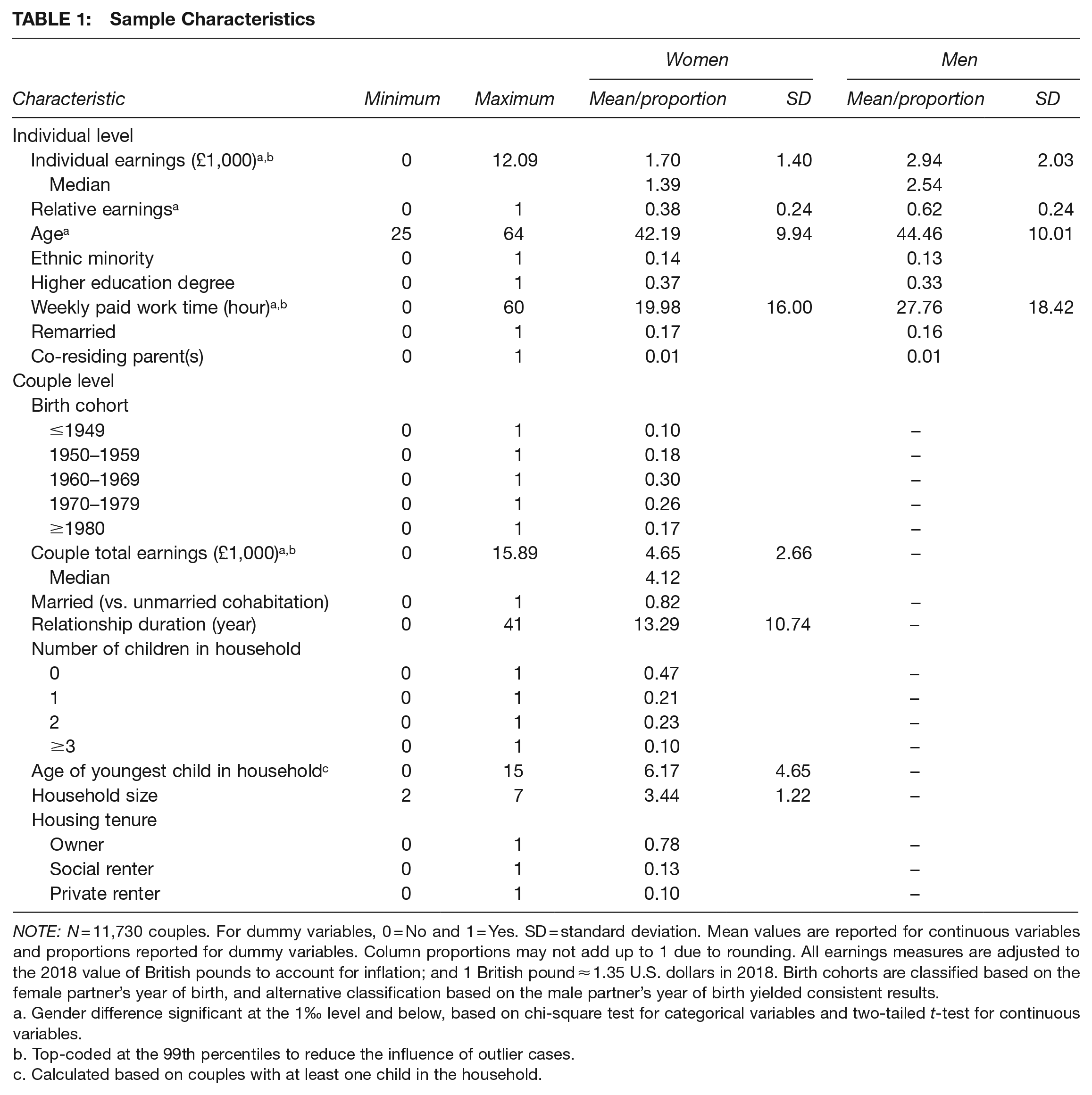

Figure 1 presents changes across British cohorts in their household financial management. The results partly support Hypothesis 1A, derived from the individualization thesis, in showing a gradient cohort increase in the adoption of independent management from 2.8 (born ≤1949) to 14.6 percent (born ≥1980). However, the proportion of couples managing their money jointly stayed relatively stable across the cohorts. In line with Hypothesis 1B predicting a cohort increase in women’s empowerment in household finances, male control through the highly restrictive female allowance system diminished from 12.4 to 1.8 percent between the first and last cohorts. However, when it comes to the male and female whole-wage systems, the opposite of Hypothesis 1B is observed: While there has been a cohort increase in the prevalence of the male whole-wage system from 9.4 to 16.4 percent, the prevalence of the female whole-wage system underwent a gradient decrease across the cohorts from 27.9 to 18.8 percent. This may have occurred because a cohort trend toward a more gender-egalitarian division of domestic labor has encouraged men in recent cohorts to undertake the chore of managing the couple’s money.

Cohort Changes in Systems of Household Financial Management

Cohort Differences in Earnings

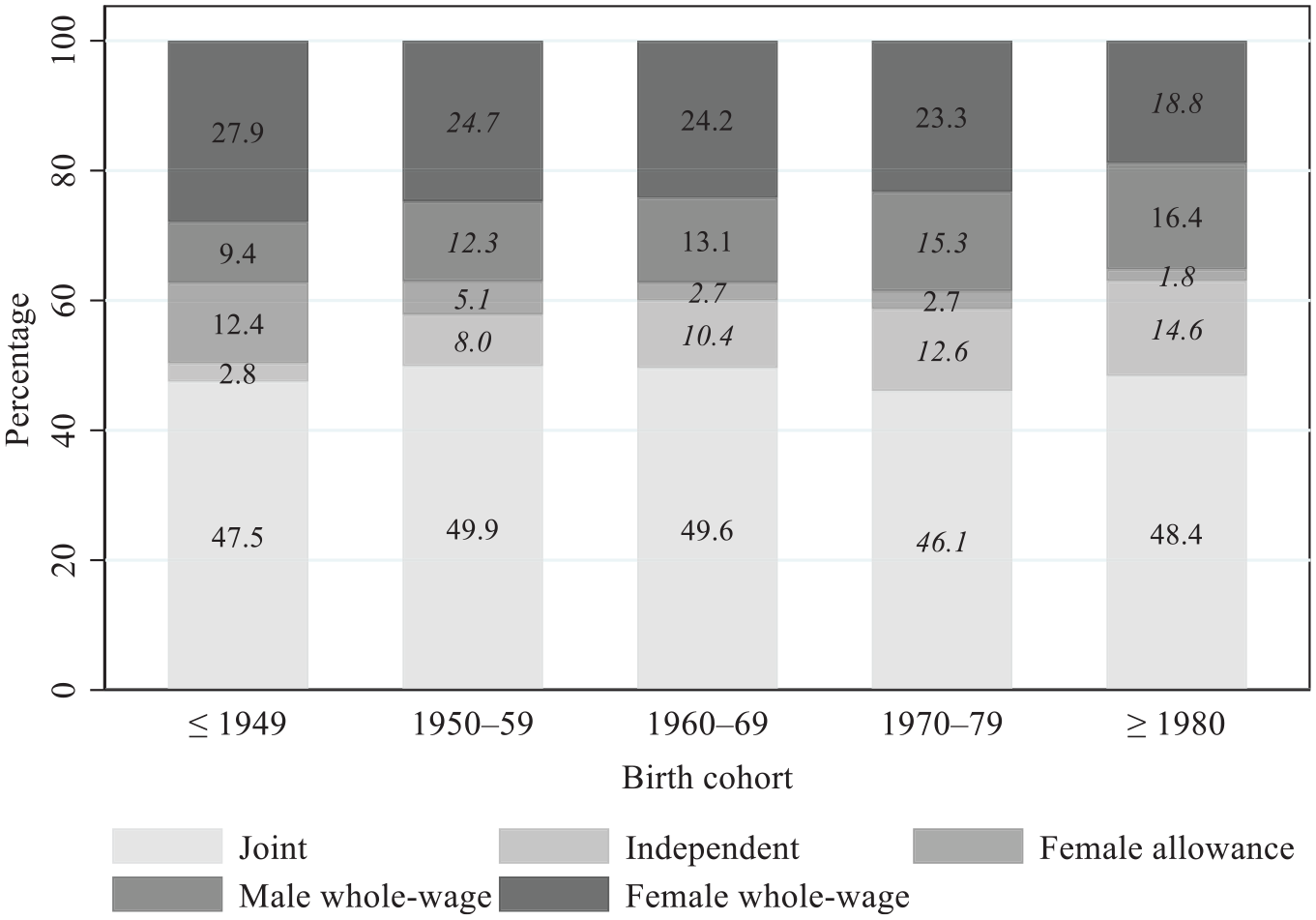

Figure 2 describes cohort differences in partners’ individual and relative earnings. The individual earnings of both women and men increased across the cohorts, except for the post-1980 cohort. Compared with their predecessors born 1960–1979, the post-1980 cohort had lower individual earnings, partly because respondents in this cohort were at an earlier stage in their career. As the cohort increase in women’s earnings outpaced that of men, women’s relative contribution to the couple’s earnings increased from 31.2 percent (born ≤1949), through 35.6 percent (born 1950–1959), to 38.6 percent (born 1960–1969), and then the increase slowed down in the last two cohorts. These patterns concur with the over-time increase in women’s labor force participation and economic standing, as well as the slow-down of the gender revolution over the past three decades (England, Levine, and Mishel 2020; Scott, Crompton, and Lyonette 2010).

Partners’ Individual and Relative Earnings, by Birth Cohort

Multivariate Findings

Variations in Cohort Changes with Partners’ Individual Earnings

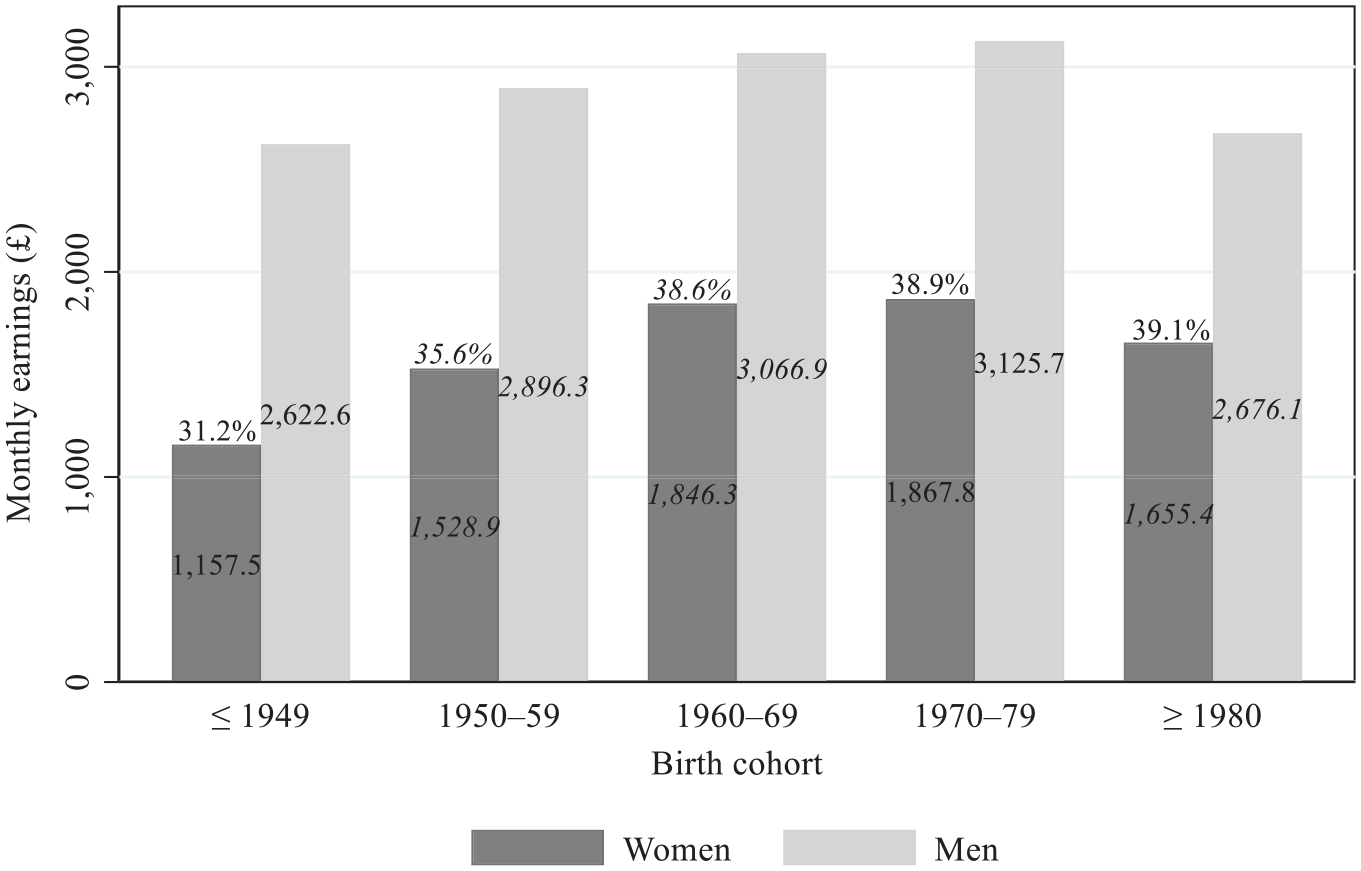

Figure 3 shows how cohort changes in financial management vary with partners’ individual earnings. The results partly support Hypothesis 2A that there has been a steeper cohort decrease in joint management among women and men with high rather than low earnings. As shown in the first row of Figure 3, there has hardly been any cohort change in the prevalence of joint management at the 5th and 25th percentiles of partners’ individual earnings. As we move across to partners with high individual earnings, the more recent cohorts have become far less likely to manage their money jointly. For women and men at the 95th percentile of individual earnings for their respective gender, joint management decreased by 17.9 and 12.8 percentage points, respectively, between the first and last cohorts. However, the trend of cohort increase in independent management did not vary significantly with partners’ individual earnings.

Predicted Cohort Changes in Household Financial Management, by Percentile Rank of Women’s and Men’s Individual Earnings

The results support Hypothesis 2B that the cohort decrease in the female allowance system and cohort increase in the male whole-wage system have both been greater among women with lower individual earnings. The prevalence of the female allowance system diminished from 24.2 to 2.1 percent across cohorts of women at the 5th percentile of individual earnings, compared with a trend of 2.6 to 0.3 percent for women at the 95th percentile. Meanwhile, the male whole-wage system trended from 8.4 to 26.6 percent among women at the 5th percentile of individual earnings, compared with a trend of 7.1 to 12.0 percent among women at the 95th percentile. These results are reverse mirrored by a steeper cohort decrease in the female allowance system and a greater increase in the male whole-wage system among men with higher individual earnings.

In line with my earlier theoretical discussion, the cohort trend of the female whole-wage system did not vary with partners’ individual earnings, perhaps because women with low individual earnings across cohorts are consistently hindered by a lack of bargaining power to control the couple’s money, whereas women with high individual earnings have resorted to alternative means (i.e., independent management) of accessing power in money management.

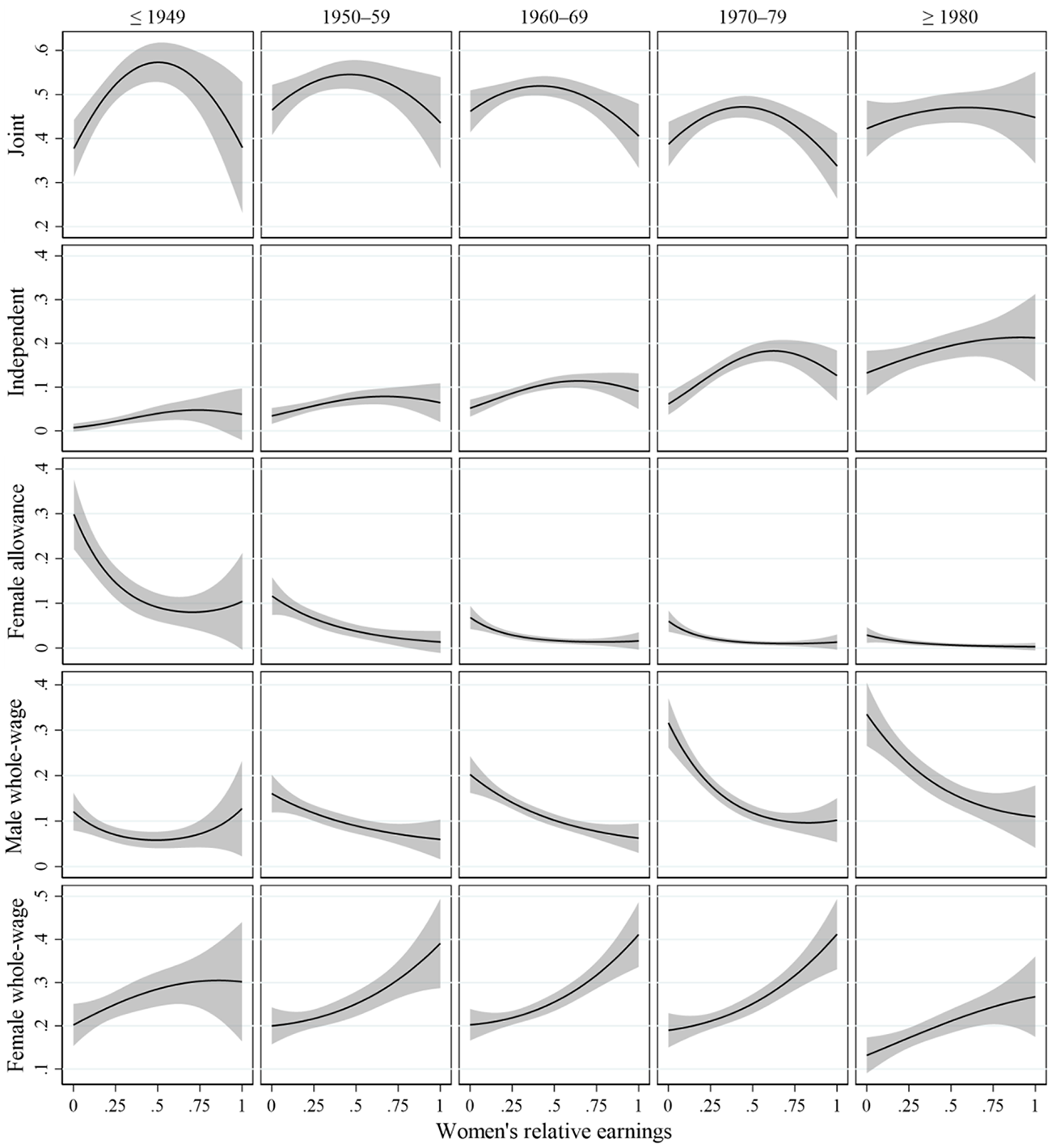

Variations in Cohort Changes with Women’s Relative Earnings

Figure 4 depicts the cohort trends of distinct systems of financial management over the distribution of women’s relative earnings. In addition to the results for partners’ individual earnings, Figure 4 further fleshes out nuanced nonlinear relationships between partners’ relative earnings and financial management.

Predicted Probability of Household Financial Management over the Distribution of Women’s Relative Earnings, by Birth Cohort

Hypothesis 2A is not supported by the results for joint management: A statistically significant (at the 5% level) cohort decrease in the prevalence of joint management is noted among neither women nor men with high relative earnings (i.e., the two ends of the relative income distribution). Rather, as the first row of Figure 4 shows, the cohort decrease is observed mainly among partners who contributed more or less equally to the couple’s earnings. Combined with the results that women and men with high individual earnings trended away from joint financial management across cohorts, the results for relative earnings suggest that the cohort decline of unitary couplehood has been most prominent among couples formed of two equally high-earning partners. The result also suggests a cohort shift from the equity to the equality principle in joint financial management (Deutsch 1975). In the pre-1950 cohort, joint management was most likely when partners make more or less equal contributions to the couple’s earnings. By contrast, as we move across to the post-1980 cohort, joint management has become equally likely across the full distribution of partners’ relative earnings, regardless of input.

In line with Hypothesis 2A, a cohort increase in independent management is observed among both women and men with high relative earnings. Notably, the increase has been greater for women with high relative earnings than for their male counterparts. Among women who were the sole earner (i.e., relative earnings = 1), the prevalence of independent management increased from 3.8 to 21.3 percent between the first and last cohorts, compared with an increase from 0.1 to 13.2 percent among male sole earners (i.e., relative earnings = 0). This may have occurred because, compared with female sole earners, men who contribute the lion’s share to the couple’s earnings are still more likely to be viewed as the breadwinner, despite the decline of the male breadwinner norm (Klesment and van Bavel 2017).

Hypothesis 2B is supported by the results that the cohort decrease in the female allowance system and cohort increase in the male whole-wage system are observed primarily among women with low rather than high relative earnings. There has hardly been any cohort change in the two systems among women with high relative earnings. By contrast, among women who did not make a contribution to the couple’s earnings (i.e., relative earnings = 0), the prevalence of the female allowance system decreased from 29.9 to 2.9 percent and that of the male-whole wage system increased from 12.1 to 33.5 percent between the first and last cohorts.

The results for the female whole-wage system provide some evidence for the cohort decline of “gender performance” in financial management. 4 In the pre-1950 cohort, when women out-earned their partners, an increase in their relative earnings did not translate into an increase in their likelihood of managing the couple’s money. By comparison, in the cohorts born 1950–1979, there was a notable positive association between the women’s relative earnings and the adoption of the female whole-wage system. In the post-1980 cohort, the strength of the positive association decreased slightly, in part because women with high relative earnings in this cohort have turned to independent financial management.

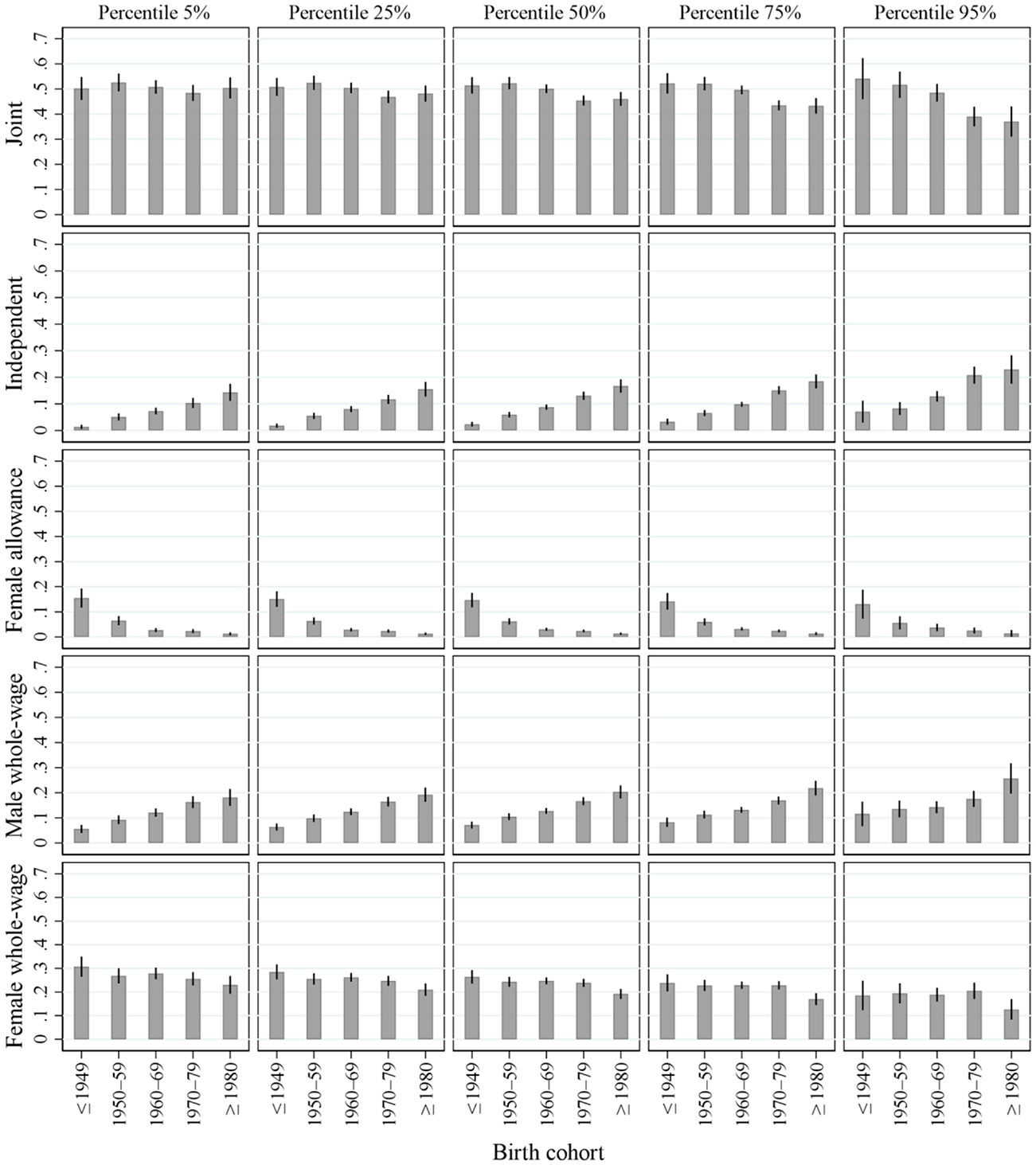

Variations in Cohort Changes with Couple Total Earnings

Figure 5 presents how cohort changes in household financial management vary with couple total earnings. The results partly support Hypothesis 3 that the cohort decrease in joint management has been steeper among high-earning than low-earning couples, though the cohort trends of independent management varied little with couples’ earnings. Among couples at the 95th percentile of partners’ total earnings, the prevalence of joint management decreased from 54.1 to 37.0 percent between the first and last cohorts, compared with hardly any cohort change among couples at the 5th percentile. This is consistent with the theoretical expectation that compared with low-income couples, high-income couples are more likely to enact the ideology of individualism because they are better able to afford not pooling their earnings as well as the transaction costs of transferring funds between partners who keep separate purses (Sung and Bennett 2007; Treas 1993). In line with the theoretical discussion, couple total earnings do not seem to moderate the cohort trends of the female allowance and whole-wage systems.

Predicted Cohort Changes in Household Financial Management, by Percentile Rank of Couple Total Earnings

Before discussing the contributions and implications of the findings, it is important to briefly consider the limitations of my analysis, which suggest some potential directions for future research. First, whereas I focused on couples’ everyday money management, future research could focus on other dimensions of household finances, such as consumption, savings, debts, and investments (Burgoyne 2004; Kan and Laurie 2014; Lersch 2017; Pepin 2019; Tisch and Lersch 2021; Treas 1993). Second, due to the small number of same-sex couples in the data set, I focused on heterosexual couples only; and it remains unclear how same-sex couples manage their money. Third, although I analyzed financial unity and autonomy as discrete categories, because the survey captured couples’ financial management as such, future research could examine financial unity–autonomy using a continuous spectrum to distinguish different levels of financial integration and independence between partners. Fourth, although this research focused on Great Britain, it is worth extending the approach and theoretical insights developed here to other contexts. Finally, future research could consider further dimensions of intersectionality such as race and ethnicity.

Discussion

In this research, I have shown considerable changes across British cohorts born between the 1920s and 1990s in how partners managed their money in couple relationships. Highlighting the intersectional configuration of the changes (Collins and Bilge 2020), I have also shown the nuanced ways in which the cohort trends varied with partners’ individual, relative, and total earnings. In doing so, I have scrutinized two major, intertwining trends regarding the transformation of couple relationships: namely, the gender revolution (England, Levine, and Mishel 2020; Gerson 2009; Goldscheider, Bernhardt, and Lappegård 2015) and individualization (Beck and Beck-Gernsheim 2002; Giddens 1992). Bringing together these two trends, my findings provide new insights into the role of the gender revolution in constituting and shaping the transformation of couplehood.

Divergent Gender Revolutions in Household Financial Management

Over the past decades, there has been much progress toward gender equality in women’s labor force participation, education, and economic standing (England 2010; England, Levine, and Mishel 2020). Propelled by several waves of feminist movements, the gender revolution has also fashioned a rising tide of gender egalitarianism (Cotter, Hermsen, and Vanneman 2011; Gerson 2009; Scarborough, Sin, and Risman 2019). Have these trends parlayed into a rise of gender equality in household financial management? While my findings show an overall cohort progress toward gender equality in how couples manage their money, they also reveal divergent and nuanced gender revolutions in household financial management across cohorts of women and couples occupying differential income positions.

The cohort progress toward gender equality in couples’ money management differed considerably between women with low and high individual and relative earnings. Across successive cohorts of low-income women, their empowerment in household financial management is characterized by a subtle shift in the form of male control from the female allowance system to the male whole-wage system. As one has greater freedom in the use of personal spending money in the whole-wage system than housekeeping money in the allowance system (Pahl 1995), the findings show a nuanced relaxation of financial restrictions imposed on low-income women. This trend is accompanied by a cohort decrease in the proportion of men who have adopted “back-seat” financial management through the female allowance system, which allows men to retain the lion’s share of the couple’s money and derive power from the money while delegating the onerous chore of managing day-to-day expenses to their partners. Rather, there has been a cohort increase in the proportion of men with low-income partners who have stepped up to embrace the chore of everyday money management through the male whole-wage system.

By contrast, the findings show a considerably different cohort trend of gender empowerment in financial management among women with high earnings. This trend is characterized by a shift in the women’s role from partaking in household finances through joint management (i.e., the pre-1950 cohort) to controlling the couple’s money through the female whole-wage system (i.e., cohorts born 1950–1979), and then to controlling their own earnings through independent financial management (i.e., the post-1980 cohort). Whereas financial management had provided a site at which earlier cohorts of partners construct and perform their gender identities (Kulic, Minello, and Zella 2020; Pahl 1995; West and Zimmerman 1987), the “gender performance” predicated on the gender essentialist ideal of men’s entitlement to money has diminished across cohorts. Compared with their pre-1950 predecessors, women born between 1950 and 1979 who out-earned their partners have become far less likely to “perform femininity” in money management to protect their partners’ sense of masculinity. Rather, they have become better able to translate their high relative earnings into bargaining power in controlling the couple’s money. With the rise of individualism in the post-1980 cohort, however, managing their own money independently rather than the couple’s money seems to have provided a more attractive option for high-earning women. The decline of the male breadwinner norm has also helped fashion a cohort increase in the proportion of high-earning men who kept separate purses, as they have become less obliged to share their earnings in the family (Pepin 2019).

In sum, these findings suggest that there have been plural, divergent, and subtle gender revolutions in household financial management. A broad-sweeping cohort trend toward gender equality notwithstanding, it is crucial to adopt an intersectional lens to understand the ways in which women with differential resources have different opportunities and constraints to seek gender empowerment in everyday financial management across cohorts (Collins and Bilge 2020).

The Individualization of Household Financial Management

Eminent social theorists, such as Giddens (1992) and Beck and Beck-Gernsheim (2002), have predicted a rise of “individualized” and “pure” relationships in late modernity, due partly to the spread of gender egalitarianism and postmaterialism, a long-term increase in women’s education and labor force participation, and a resulting increase in the sense of autonomy women derive from their earnings. Cherlin (2010, 2020) similarly argued that modern couplehood is increasingly predicated on an association of equal, autonomous individuals in pursuit of self-growth rather than economic interdependence. How accurate are these arguments, seeing through the lens of money in couple relationships?

My findings show a cohort trend of individualization in household financial management in that the proportion of couples keeping separate purses increased more than five times between the pre-1950 and post-1980 cohorts. My findings also show that the cohort decrease in joint financial management is most prominent when both partners have equally high earnings. While joint financial management was most likely when partners contributed equally to the couple’s earnings in earlier cohorts (according to the equity principle), partners’ relative contribution to the couple’s earnings has become less relevant in predicting the probability of joint management in more recent cohorts (in line with the equality principle). Thus, the results suggest a cohort replacement of the equity principle with the equality principle. Moreover, given the economic imperative for low-income couples to coordinate their consumption carefully and the transaction costs of transferring funds between partners who keep separate purses (Treas 1993), it is not surprising that the cohort decrease in joint financial management is observed among high-income rather than low-income couples.

Despite the ideals of individualism, autonomy, and “pure relationships” (Beck and Beck-Gernsheim 2002; Cherlin 2020; Giddens 1992), my findings underline the very material and intersectional conditions required for couples to put these ideals to practice. As a result of individual partners’ and couples’ differential economic positions, the cohort trend of individualization in household financial management is segmented along socioeconomic lines. The decline of unitary collectivism and resource bargaining, as well as the rise of the ideal of equality in couples’ money management, thus invites scholars to reconsider and revise the conceptualization of the family and couplehood as a site of economic exchange, cooperation, and contestation (cf. Becker 1991).

Conclusion

Taken together, my findings indicate that household financial management contains crucial and rich clues to changing gender relations in couple relationships. Scholars, policy makers, and the general public are gravely concerned about the uneven, stalled, and incomplete nature of the gender revolution in the domestic sphere in aspects such as household and care work (England, Levine, and Mishel 2020; Gerson 2009; Scarborough, Sin, and Risman 2019; Scott, Crompton, and Lyonette 2010). My findings reveal some room for optimism, showing some progress toward, but not yet the achievement of, gender equality in how couples manage their money. The findings also highlight the importance of an intersectional lens in understanding the divergent trajectories of the gender revolution in household finances and the individualization of couple relationships.

Supplemental Material

sj-docx-1-gas-10.1177_08912432211036912 – Supplemental material for Divergent Gender Revolutions: Cohort Changes in Household Financial Management across Income Gradients

Supplemental material, sj-docx-1-gas-10.1177_08912432211036912 for Divergent Gender Revolutions: Cohort Changes in Household Financial Management across Income Gradients by Yang Hu in Gender & Society

Footnotes

Author’s Note:

The author is grateful to the editors Barbara J. Risman and Irma Mooi-Reci and the anonymous reviewers for their constructive feedback. The data used in this research were made available through the UK Data Archive. The British Household Panel Survey data were originally collected by the Economic and Social Research Council (ESRC) Research Centre on Micro-Social Change, University of Essex. The United Kingdom Household Longitudinal Study is an initiative funded by the ESRC and various Government Departments, with scientific leadership by the Institute of Social and Economic Research, University of Essex, and survey delivery by NatCen Social Research and Kantar Public. Neither the original collectors of the data nor the Archive bears any responsibility for the analyses or interpretations presented here.

Notes

Yang Hu is a Senior Lecturer in Sociology at Lancaster University, UK. His research focuses on changing work–family and gender relations, as well as their intersections with population mobility in a global context. He is the author of the book Chinese-British Intermarriage–Disentangling Gender and Ethnicity. His recent research has been published in journals such as the Journal of Marriage and Family, European Sociological Review, and Gender, Work & Organization.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.