Abstract

This paper explores the impact of the growth in e-commerce and the landmark Wayfair ruling on the politics of land fiscalization in California. Through analysis of city revenue data, the author demonstrates that sales tax revenue for cities with a concentration of e-commerce distribution warehouses has increased substantially since the Wayfair ruling. In California, online retailers, such as Amazon, are required to pay sales tax to a local jurisdiction based on the location of the fulfillment center. Several cities in California have utilized tax incentives to attract e-commerce companies to their jurisdiction. Tension between cities that benefit from these new sales tax regulations and those that feel disadvantaged by it has emerged, raising broader questions regarding regional inequality. Achieving an equitable distribution of sales tax revenue remains a challenge for states with an origin-based local sales tax (such as California) as well as states with a destination-based local sales tax.

The growth of e-commerce has reshaped the spatial geography of retail. The proportion of retail sales that are conducted online was accelerated by the Covid-19 pandemic, growing from 10.6% of all retail sales in 2019 to 15.4% in 2023 (U.S. Census Bureau, 2024). This growth in e-commerce has had implications for the sourcing of sales tax and the distribution of sales tax revenue between states and cities across the United States. Sourcing is a term used to determine the physical location of a sale, and thus which local tax rates apply to a purchase and which jurisdiction receives the sales and use tax revenue (Coleman, 2018). Under an origin-based system, sales taxes are collected based on the location of the retailer, while under a destination-based system, sales taxes are collected based on the location where the consumer first receives their purchase. Across the United States, 45 states and the District of Columbia collect a state sales tax (Coleman, 2018), and over 35 of these states also allow local jurisdictions to collect a local sales tax (Agrawal & Shybalkina, 2024). Most states have a destination-based system; only 12 states have an origin-based system (Afonso, 2019).

For bricks-and-mortar sales, the origin (location of the retailer) and destination (location where the customer receives the purchase) are typically the same. However, with online purchases, the origin and destination are often different locations. Until recently, online retailers without a physical presence in a state were considered “out-of-state” retailers and states could typically only collect a use tax for purchases made outside but delivered into their state. In 2018, a landmark ruling by the U.S. Supreme Court, (South Dakota v. Wayfair, Inc., 2018) (the Wayfair ruling), expanded the ability of states to collect sales tax from out-of-state sellers if the seller has an “economic presence” in the state (Agrawal & Shybalkina, 2024; Mikesell et al., 2023). The economic presence, or nexus, is defined by each state based on a threshold number of transactions or value of total sales within the destination state (Agrawal & Shybalkina, 2024). Forty-three states have implemented regulations regarding sales taxes for out-of-state sellers. For example, in California, the threshold for economic nexus is $500,000 in total sales; in Illinois the threshold is $100,000 (Afonso, 2019).

The sourcing rule adopted by a state with a local sales tax will impact which local jurisdictions receive sales tax revenue for online purchases. For destination-based states, the sales tax will typically be collected by the local jurisdiction in which the customer lives. For origin-based states, the point-of-sales for online transactions are not always clear cut. Only three states have origin sourcing for remote sales—Arizona, California, and New Mexico (Afonso, 2019). Several studies have investigated the impact of the Wayfair ruling on sales tax revenue at the local level for states with destination-based systems. Agrawal and Shybalkina (2024) found that destination-based states have seen an increase in sales tax revenues for small, rural jurisdictions at the expense of larger, urban retail centers, which were previously the destination for in-person sales. In a study at the county level in Tennessee, Bruce et al. (2023) similarly found that rural counties have experienced rapid growth in sales tax revenue.

This paper discusses how e-commerce has reshaped city competition for sales tax revenue and the politics of land fiscalization. It uses California as a case study of an origin-based sales tax system. Through this paper, I explore competition for sales tax revenue associated with e-commerce distribution warehouses between cities in California as well as the tension between cities who have benefited from the changes to sales tax regulation and the growth of online shopping, and those cities that feel disadvantaged by it. This paper illustrates the ongoing unintended consequences of property tax limits in the e-commerce era and raises important questions regarding the equitable distribution of sales tax revenue, which has implications for destination-based and origin-based local sales tax systems across the United States.

In the next section, I summarize the existing literature on the fiscalization of land use, city competition for jobs and sales tax revenue, and the pros and cons of destination-based and origin-based sales tax systems. Following an overview of my research approach, I present my analysis of city revenue data that illustrates the growth of sales tax revenue for metropolitan fringe cities in the e-commerce era, and their reliance on sales tax revenue (as opposed to property tax revenue). Drawing on a review of policy proposals to regulate city competition for jobs and sales tax, I outline ongoing debates regarding the distribution of sales tax revenue and the use of sales tax incentives as an economic development tool. I conclude the paper with a discussion of the politics of land fiscalization in California in the e-commerce era whereby cities are not just competing for sales tax revenue with neighboring cities but cities across their region and California writ large and outline potential policy solutions to move toward an equitable distribution of sales tax revenue.

Theoretical Context

Fiscalization of Land use

Fiscal austerity policies during the 1970s promoted a transition in local government away from the provision of local services and toward attracting economic activity, particularly footloose capital, referred to as the shift from urban managerialism to urban entrepreneurialism (Harvey, 1989). Peterson (1981, p. 69) suggested that “to maintain their local economic health,” cities are required to concentrate on developmental rather than redistributive policies – to do otherwise, would “precipitate the flight of mobile taxpayers to other jurisdictions” (Schragger, 2016, p. 137). Many scholars have argued that urban entrepreneurialism has created a zero-sum game of city competition for jobs and investment (Harvey, 1989).

Federal fiscal austerity policies placed several restrictions on local taxation, and placed pressure on local governments to find alternative ways to increase local revenue streams (Schragger, 2016). According to Lewis (2001), Misczynski (1986) pioneered the concept of the fiscalization of land use, which refers to “local efforts to employ land-use regulation so as to increase local revenue streams” (p. 24), or as LeRoy (2005) put it, “cities let budget issues dictate how land will be used” (p. 144). Several studies have provided evidence of the pervasiveness of the fiscalization of land use and its links to sprawl (see Chapple, 2018; Lewis, 2001; Wassmer, 2002), with many of these studies focusing on California—particularly in light of Proposition 13.

Proposition 13 was introduced in California in 1978. It capped property tax rates at 1% and annual property value adjustments at 2%, with property value reassessment only occurring after the sale of a property (Innes & Booher, 1999). Due to these restrictions, which still exist today, property taxes remain low for properties that do not turn over, regardless of shifts in their market value. Following the introduction of Proposition 13, sales tax became an important discretionary source of local revenue for cities in California (Innes & Booher, 1999; Wassmer, 2002).

Studies on the fiscalization of land use have highlighted the desirability of retail uses— particularly shopping centers, car dealerships, and big-box retail—because, in addition to generating property tax revenue, retail generates sales and payroll taxes and has lower service demands compared to residential development. Hoene (2004) found that, between 1972 and 2002, there was little change in the reliance of California cities on sales tax revenues; however, there was an increase in reliance on user charges and fees. Regardless, Hoene (2004) emphasized that there is substantial incentive for cities to pursue sales tax revenues.

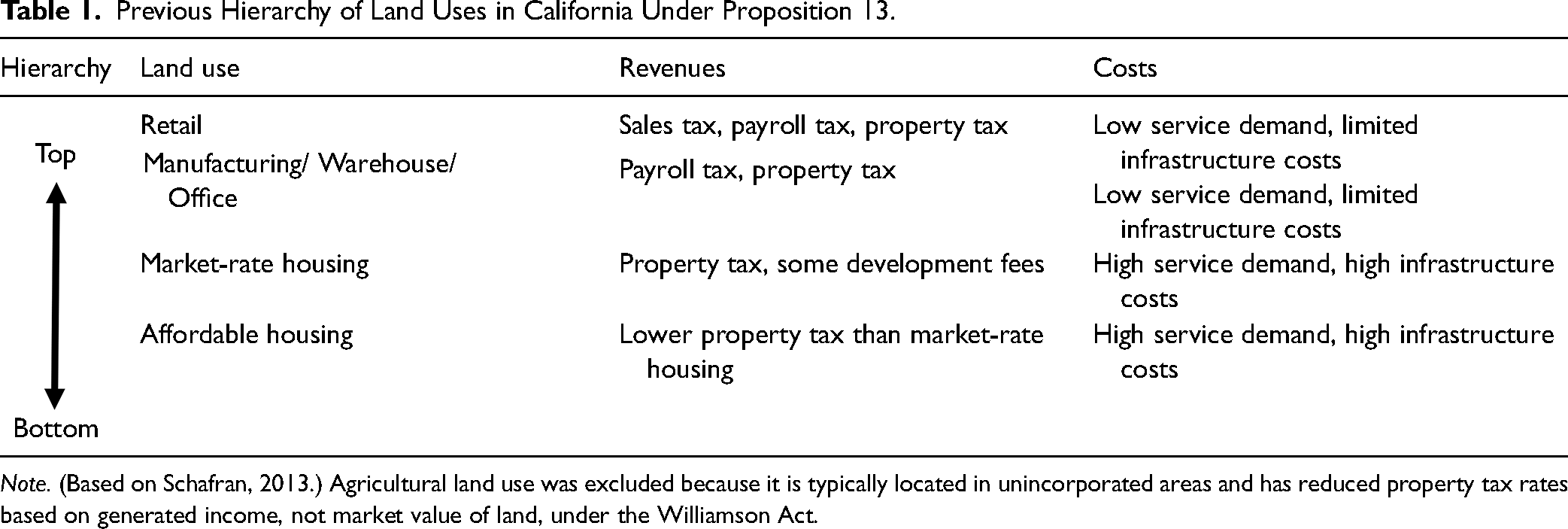

The hierarchy of land uses under Proposition 13 is illustrated in Table 1. Retail uses are at the top of the hierarchy and are the most attractive because they generate multiple sources of tax revenue and have lower infrastructure demands compared to residential development. Innes and Booher (1999) noted that employee-intensive uses can be “fiscally unattractive because income taxes go to state government and most property taxes go to school districts” (p.144). Thus, retail uses are more desirable for cities because of the sales tax revenue.

Previous Hierarchy of Land Uses in California Under Proposition 13.

Note. (Based on Schafran, 2013.) Agricultural land use was excluded because it is typically located in unincorporated areas and has reduced property tax rates based on generated income, not market value of land, under the Williamson Act.

There are several unintended consequences of the fiscalization of land use. Schragger (2016) emphasized that the fiscalization of land use encourages local governments to zone land in ways that “distort regional property markets,” which generates “unequal provision of public services” (p. 222). By focusing on retail, cities are trading high tax revenues for low wage (and low quality) jobs (Chapple, 2018). While the suburbanization of retail was occurring prior to the introduction of Proposition 13—fueled by population growth in the suburbs (Lewis, 2001)—existing studies highlighted that Proposition 13 further promotes the approval of large shopping centers in locations outside town centers, which has not only impacted the viability of retail in town centers, but has also contributed to sprawl (Chapple, 2018; Innes & Booher, 1999; LeRoy, 2005; Lewis, 2001; Wassmer, 2002).

City Competition

Both the dependence on sales tax revenue as a discretionary source and the broader shift toward a developmental state have promoted competition between cities to attract businesses that will increase jobs and tax revenue, and thus the use of subsidies and tax incentives. Cities compete to attract mobile capital including export-oriented industries and retail development. An increase in capital mobility, which refers to “the ability of owners of capital to place it in a variety of locations” (Thomas, 2007, p. 45), has led to an intensification of competition among cities, and over a greater distance. Cities that have a more desirable market position for capital relative to their competitors are in a better position to negotiate with the private sector (Weber, 2007). As Weber noted, cities are “handicapped” because they are “embedded in space and not footloose like businesses” (p. 145).

The effectiveness of subsidies and tax incentives is mixed. According to Markusen and Nesse (2007), competition for jobs and tax revenue through incentives is “costly, generally inefficient and often ineffective even for the winning regions” (p. 1). Schwartz (1997) argued that the pursuit of retail uses prioritizes short-term gains at the expense of long-term economic development goals, particularly because retail jobs have lower wages than, for example, manufacturing. In a study of the use of financial incentives for business expansion and relocation in Kansas, Jensen (2017) found that incentive programs have “no discernable impact” (p. 85) on job creation or the relocation decisions of firms. Schragger (2016) noted that competition can be positive where it encourages investment in services, infrastructure, and innovation to attract economic resources, and competition can be negative “to the extent that it leads to races to the bottom – the lowering of taxes or regulation below an optimum, the poaching of neighbors’ productive enterprises, the intra-metropolitan fight for tax base” (p. 32). Bartik (2019a, 2019b, 2020) similarly concluded that city and state officials can promote local job creation more effectively by focusing on customized business services, infrastructure, land development policies, local education, and job training, rather than tax incentives. More broadly, there is a concern that corporations are not held accountable to the jobs and revenues that they promise.

Destination-Based Versus Origin-Based Sales Tax Systems

There are several considerations for states when implementing either a destination-based or origin-based sales tax system. An origin-based system encourages retailers to locate in the lowest tax jurisdiction (Fox, 2012). Under such a system, states and cities can compete for retailers by reducing their sales tax rates or providing incentives to retailers. The use of sales tax incentives creates an uneven playing field for retailers, favoring large retailers at the expense of small businesses (Frenkel, 2017; Propheter, 2011), and as noted above, the effectiveness of tax incentives is mixed. There are several costs for implementing a tax system including operation, auditing, and enforcement (Fisher, 2022). An origin-based sales tax system is considered to be “more efficient and less costly to implement and enforce” (Frenkel, 2017, p. 137) compared to a destination-based sales tax system.

A destination-based system may induce consumers to make purchases (online or in-person) in jurisdictions with lower taxes or no taxes. When consumers travel further to reduce or avoid sales taxes, there is an efficiency cost associated with the purchase (Fisher, 2022). Although use taxes were introduced to address tax avoidance, (Fisher, 2022; Fox, 2012; Mikesell et al., 2023), many consumers are not aware that they owe a use tax and it is often costly or infeasible to collect or enforce (Fisher, 2022).

The rise of e-commerce presents an opportunity to understand how changes to sales tax regulation that allow cities to collect sales tax from e-commerce companies, impacts the spatial distribution of sales tax revenue and the politics of land fiscalization. By focusing on California, I consider how these changes impact an origin-based sales tax system and the policy implications for regional equality.

Research Approach

Method

Through analysis of city revenue data, I compare trends in sales and property tax revenue between 2005 and 2022. Cities are required to submit a Financial Transactions Report to the California State Controller each fiscal year. The raw data have been made publicly available by the California State Controller for each year from 2004–2005 to 2021–2022. I extracted, cleaned, and analyzed general revenue data for all cities in California and grouped the tax revenue data into categories that are typically reported in the Annual Comprehensive Financial Reports (ACFR 1 ) released by Californian cities (property tax, 2 sales tax, 3 utility users’ tax, transient occupancy tax, and others). General revenues can be utilized by a city for any public purpose as they are not tied to a specific function or program (California State Controller, 2022). I calculated property tax as a proportion of total general revenues and sales tax as a proportion of total general revenues using “Total General Revenue” from the data sets. I utilized population data from the U.S. Census Bureau to calculate sales and property tax rates per person for each city.

My analysis of city revenue data is supported by a review of sales tax rebate agreements and state policy proposals to regulate local sales tax revenues. I identified the cities that have sales tax rebate agreements through a review of ACFRs for a select number of case study cities. Cities typically report the agreements that they have signed in their ACFR, although the name of the retailer remains anonymous. I reviewed state bills proposed since 2015 to regulate local sales tax revenues utilizing the California Legislative Information website. My review focused on the bill analysis reports, including who was identified as a supporter or opponent of each bill. These bills provided me with insight on the core economic development issues raised in relation to the distribution of sales tax revenues over the past 5 years.

Throughout this paper, I draw on the perspectives of interest groups that I interviewed as part of a broader study on the political economy of warehouse development. I conducted 27 semistructured interviews with representatives from city, county, and state government; business advocacy organizations; warehouse developers and investors; real estate advisory firms; labor organizations; environmental justice groups; and community groups (environmental and resident action groups). Interviews were conducted both in-person (in San Bernardino, Riverside, and San Joaquin counties) and using Zoom. Interviewees were identified and recruited based on their professional position and organization. The open-ended interviews focused on topics such as the history of warehouse development, the pros and cons of warehouse development, the economic role of the regions, and broader economic development issues and opportunities. I highlight comments made by interviewees relating to the role that sales tax revenue plays in incentivizing warehouse development and broader debates regarding redistribution.

Case Study Cities

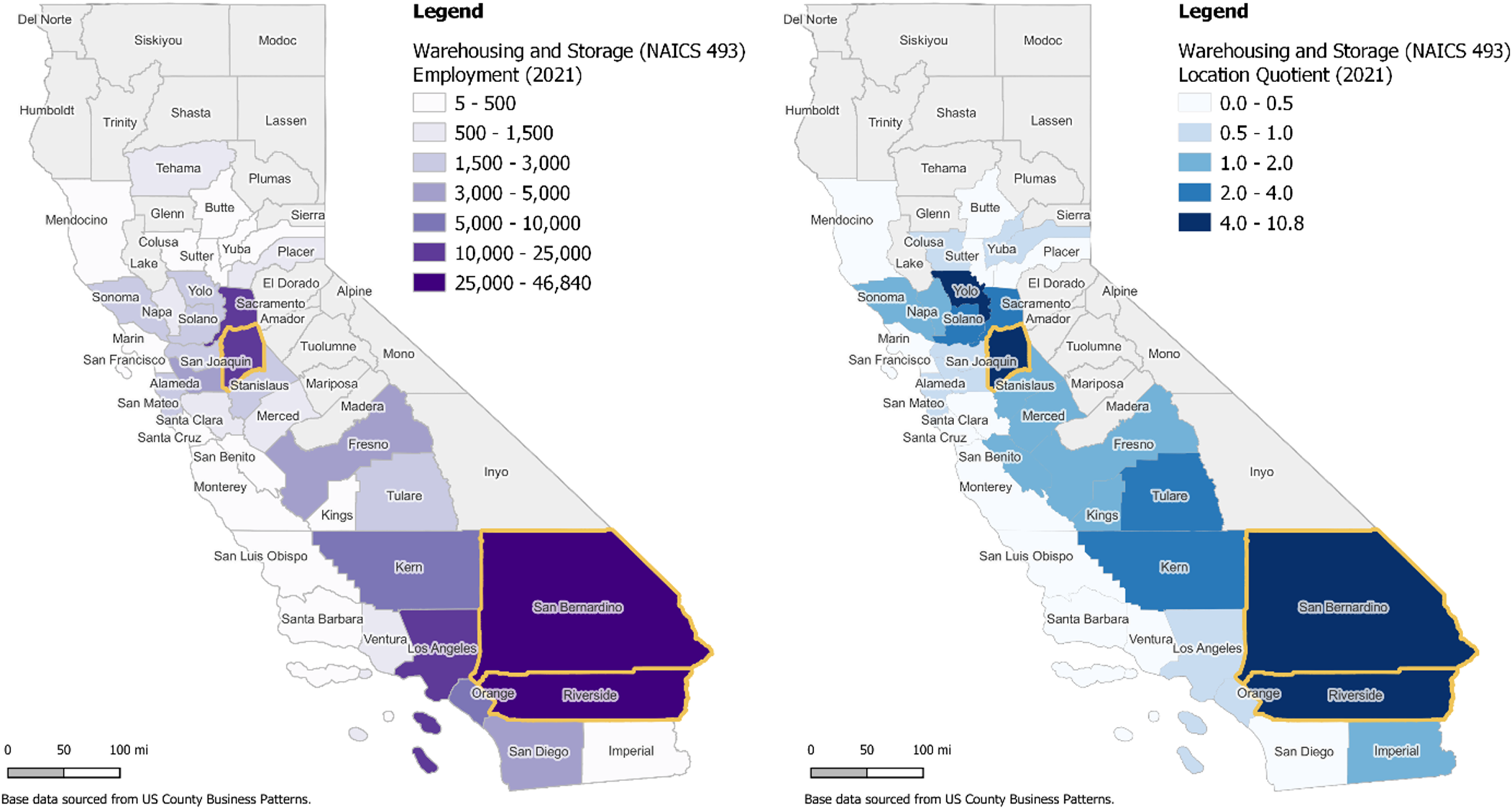

This paper focuses on cities within three counties that have a concentration of warehouse development in California: San Bernardino, Riverside, and San Joaquin. San Bernardino and Riverside counties form the Inland Empire that sits adjacent to the Los Angeles Metropolitan Area in Southern California. The scale of development in Inland Empire has been described as one of “the world's largest warehouse hubs” (Alimahomed-Wilson, 2019, p. 106). San Joaquin County sits adjacent to the San Francisco Bay Area. Walker and Schafran (2015) have referred to San Joaquin County (and its neighboring Stanislaus and Merced counties) as the Bay Area's “Inland Empire.”

Over the two decades between 2001 and 2021, employment in warehousing and storage 4 (warehousing) in California grew from just over 15,500 jobs in 2001 to over 170,000 jobs in 2021. 5 In 2021, more than 50% of California's employment in warehousing was concentrated in San Bernardino, Riverside, and San Joaquin counties. These three counties not only have high employment in warehousing measured by absolute jobs, but they also have high location quotients, 6 which illustrates that they have a higher concentration of employment in warehousing compared to the national average (Figure 1). For example, in San Bernardino County, warehousing comprises 7.4% of all employment, compared to 1.2% for California and 0.93% for the United States. Warehousing is only one component of the logistics industry 7 and these numbers do not account for employment across the broader retail supply chain (e.g., manufacturing of goods, truck transportation, and retail).

Warehousing and storage (NAICS 493) employment and location quotient by county, 2021.

My analysis focuses on a select number of cities located in three counties that have a concentration of e-commerce warehouses: Moreno Valley, Perris, and Riverside in Riverside County; Fontana, Ontario, Rialto, and San Bernardino in San Bernardino County; and Stockton and Tracy in San Joaquin County. I also refer to several cities outside of these regions as benchmarks for comparison including urban cities that have suffered from declines in downtown retail expenditure since the onset of the Covid-19 pandemic, such as San Francisco and Los Angeles, cities that used sales tax incentives to attract e-commerce warehouse companies such as the cities of Dinuba and Fresno, and cities on the urban periphery that have not benefited from the growth in e-commerce like Reedley and Manteca. I also utilize an average for all cities in California as a baseline comparison. The cities mentioned in this study are illustrated in Figure 2.

Case study cities across California.

Analysis of Sales Tax Revenue

Local Sales Tax Regulations in California

California primarily has an origin-based sales tax system (state and local sales taxes are collected at the location of the sale), as well as a destination-based use tax system for special-district taxes that may be introduced by cities or counties. In California, the base local sales and use tax of 7.25% is levied, which comprises a 6% tax that the California government receives, 1% that is distributed to the local jurisdiction (city and/or county), and 0.25% that is distributed to the transportation fund for the local county (California Department of Tax and Fee Administration, 2023b). Chapple (2018, p. 295) noted that the additional benefit of the 1% local jurisdiction tax is that it is a general tax that can be used at the city's discretion. 8 For traditional bricks-and-mortar retail sales, the local jurisdiction (or Bradley-Burns) sales tax—the 1% tax— is allocated to the jurisdiction where the sale occurs and is referred to as the “situs rule” (Chapple, 2018; Lewis, 2001; Sankus, 2020). Herein lies the incentive for local municipalities to zone land for retail uses: A large retail sector will increase sales tax revenues (Lewis, 2001), and as illustrated earlier, retail generates more revenue than other commercial development, and has a smaller demand on infrastructure and services than residential development.

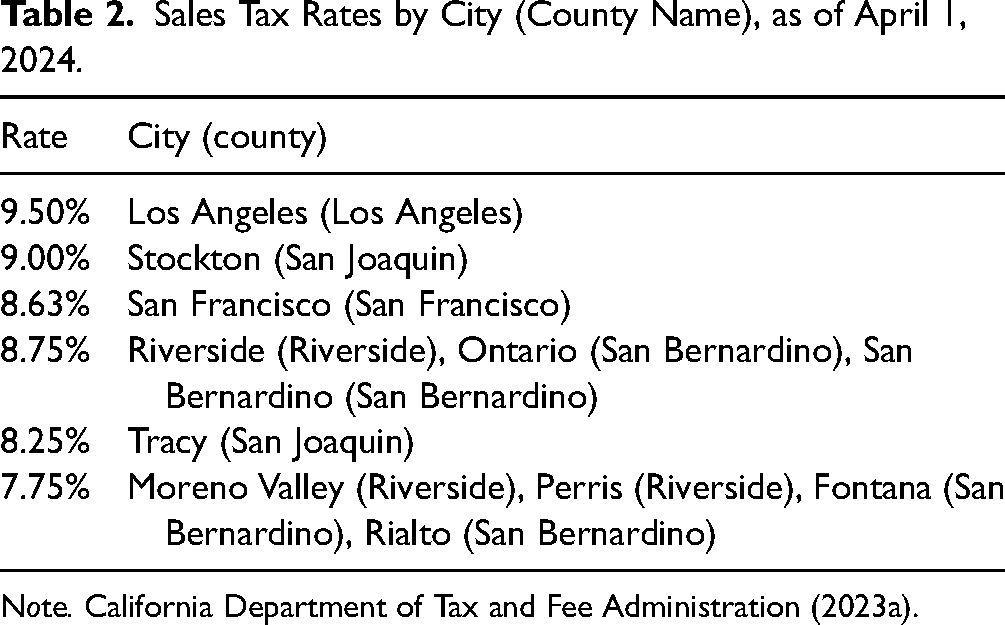

The sales tax rates for the case study cities are provided in Table 2. A city or county may increase its sales tax rate by introducing special tax measures. For example, the City of Stockton has a 9% sales tax that includes several additional tax measures that are distributed to the city as well as to San Joaquin County. These special tax measures are often collected as a destination-based use tax.

Sales Tax Rates by City (County Name), as of April 1, 2024.

In 2019, new regulations were introduced in California following the Wayfair ruling that require out-of-state online retailers to pay sales tax based on the location of the fulfillment center (California Department of Tax and Fee Administration, 2023c). Typically, industrial land uses do not generate sales tax; however, with the rise of e-commerce and changes to sales tax regulation, industrially zoned land can generate sales tax where it contains a warehouse that is designated as a point-of-sale facility (where an order is fulfilled).

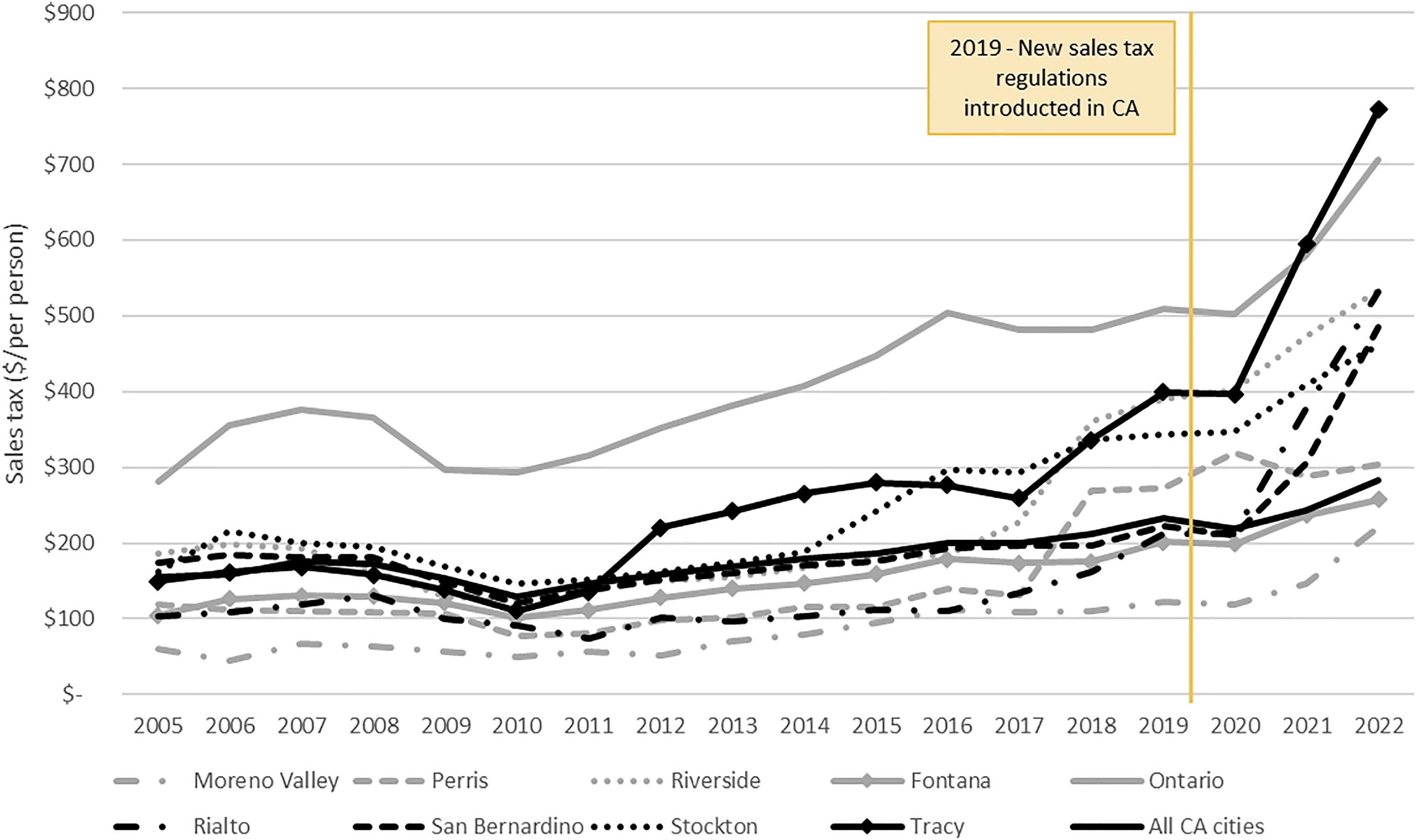

Sales tax revenue for cities with a concentration of warehouses has increased substantially since the changes to sales tax for online retail transactions were introduced in 2019 and 2020. The rapid increase also coincided with the rapid increase in e-commerce sales over the same period, fueled by the Covid-19 pandemic. As illustrated in Figure 3, per capita local sales tax revenues are no longer stagnant. Sales tax revenue per person for the City of Tracy has more than doubled over the last 5 years, increasing from $336 in 2018 to $772 in 2022. Over the same period, the sales tax revenue per person for all cities in California increased from $212 in 2018 to $282 in 2022. In its ACFR for 2021–2022, the City of Tracy (2023) noted that the increase in sales tax revenue is due to growth in e-commerce and specifically emphasized “a recent change in tax reporting by a predominant e-commerce business located within Tracy” that “shifted the tax allocation directly to Tracy as the point-of-sale jurisdiction” (p. xiii). This statement highlights the impact that a change in the point-of-sale allocation can have on sales tax revenues for a city, which did not necessarily require the construction of a new warehouse. While these data also include destination-based use taxes (where the city has a special measure in place and the revenue is collected as general revenue), the revenue from these special measures has remained relatively stable; the growth in sales tax revenue is primarily from the 1% origin-based sales tax.

Sales tax revenue per person by city, select cities, 2005–2022.

Reliance on Sales Tax Revenue Versus Property Tax Revenue

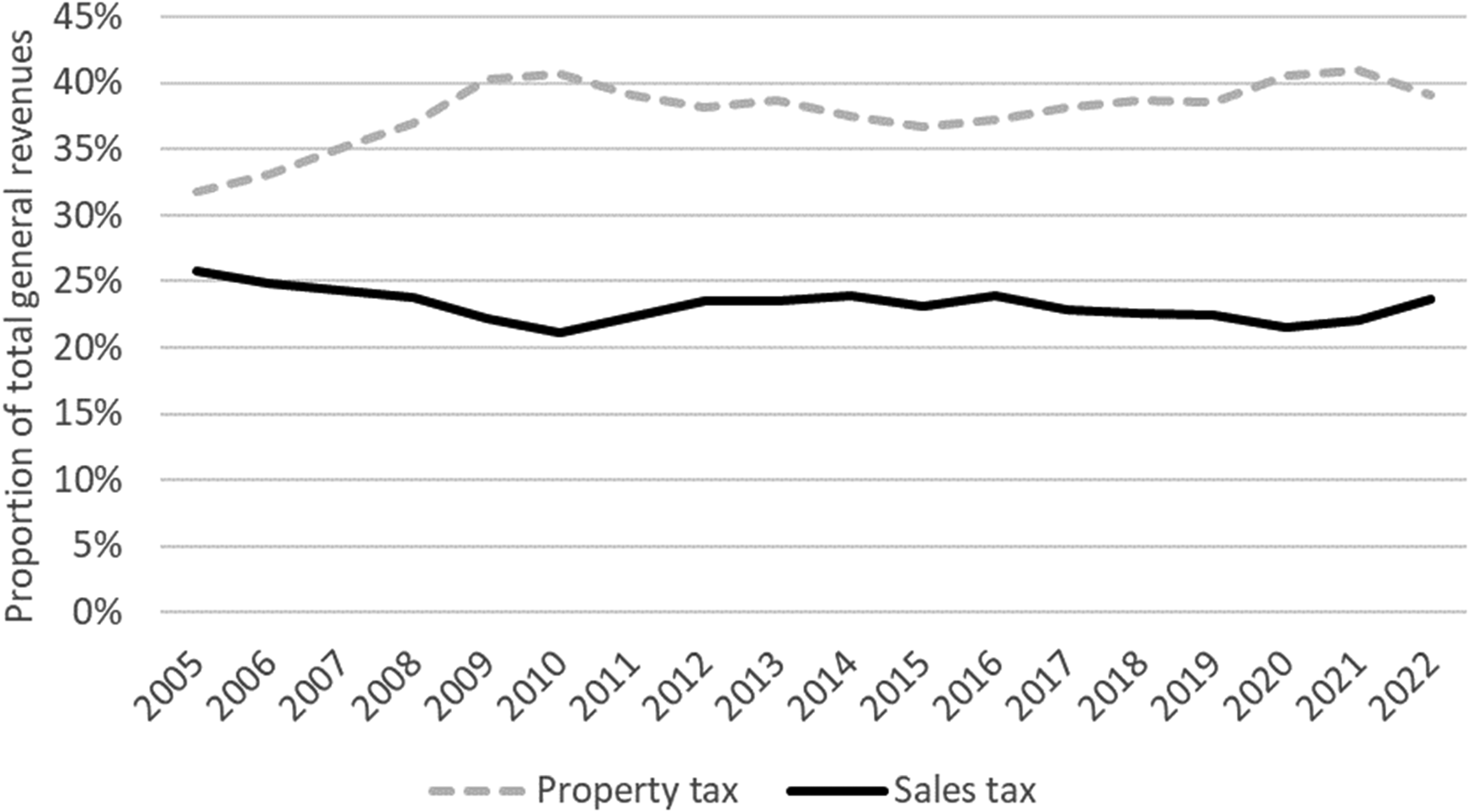

Comparing property tax and sales tax revenue as a proportion of total general revenue provides insight into the extent to which warehouse cities are reliant on sales tax as their predominant source of general revenue and how their reliance varies over time. Despite Proposition 13, property tax revenue remains the primary source of tax revenue across all of California's cities (Figure 4); however, this pattern varies from city to city.

Property tax and sales tax revenue as a proportion o of total general revenue, all California cities, 2005–2022.

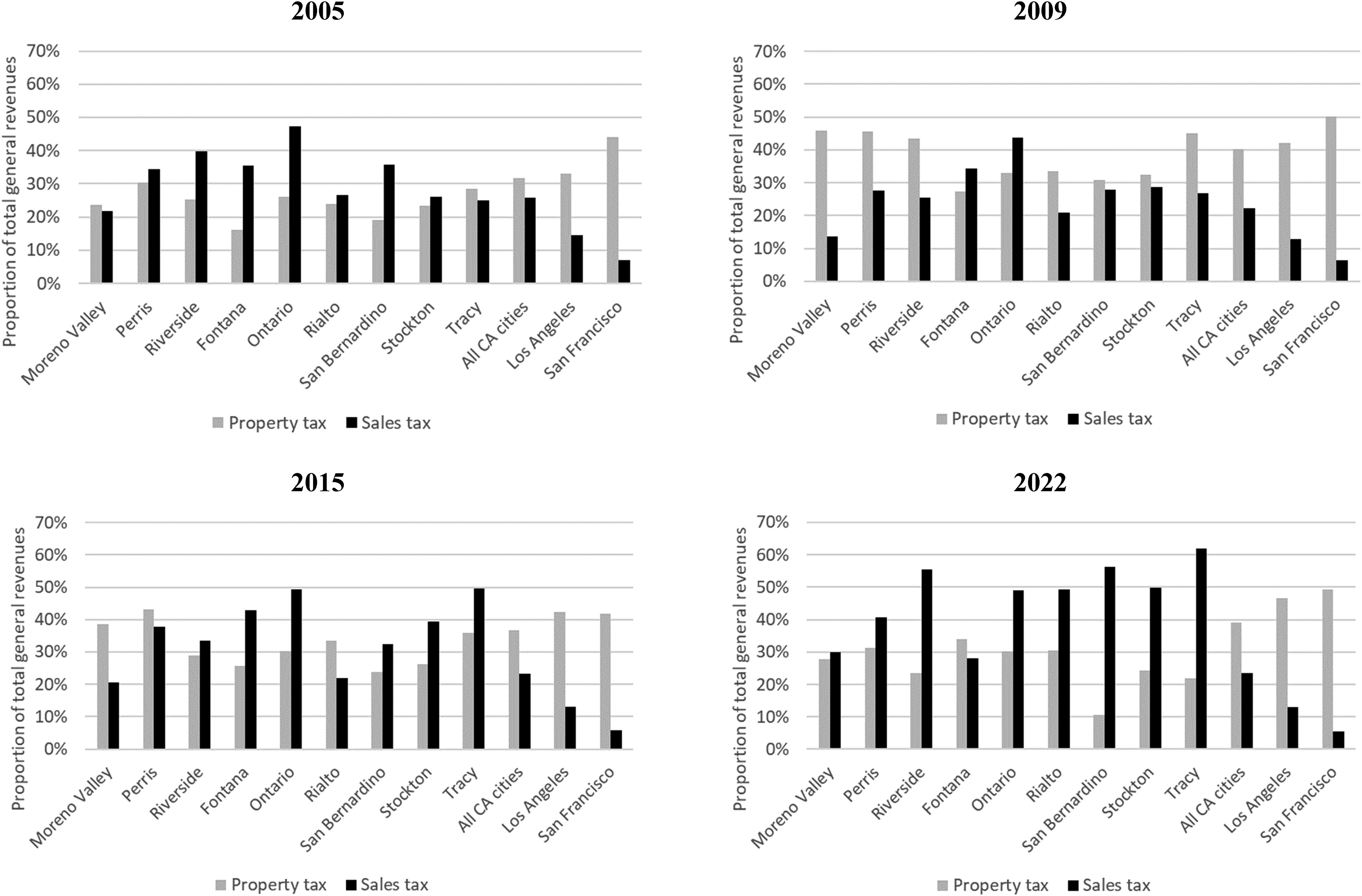

In 2005, during the housing market boom, sales tax was the dominant source of general revenue across all case study cities, except Tracy, Moreno Valley, San Francisco, and Los Angeles (Figure 5). In 2009, during the global financial crisis, property tax was the dominant source of general revenue in all of California's cities except Fontana and Ontario. The reliance on property tax in 2009 reflects both the responsiveness of sales tax revenue to economic downturns and the inelasticity of the housing market that is “less responsive to economic changes” due to property assessment processes (Hoene & Pagano, 2010, p. 256). In 2015, sales tax reemerged as the predominant source of general revenue for Riverside, San Bernardino, Stockton, and Tracy. By 2022, the warehouse boom was visible: Sales tax represented over 50% of total general revenues for several cities, compared to an average of almost 25% for all cities in California, which is unprecedented in the last 20 years.

Property tax and sales tax revenue as a proportion oof total general revenue, 2005, 2009, 2015, and 2022.

Cities with e-commerce warehouses are experiencing windfall gains in sales tax revenues. While this may impact cities that rely on bricks-and-mortar retail as a source of sales tax revenue, the larger urban cities are typically more reliant on property tax as their primary source of general revenue—a pattern that has remained steady over the last 20 years. These patterns also reflect a path dependency associated with the implementation of Proposition 13. The legislature used “pre-1978 ratios to determine the formula that allocates property tax revenues among governments” (Lewis, 2001, p. 22), which means that older cities that had higher property taxes and revenues have retained their allocation, while newer cities, which had lower property taxes, received a lower share. Newer inland cities have had to rely on sales tax revenue because their property tax shares have always been low. An interviewee from a local city noted that the need to balance budgets has shaped not only their perception of the benefits of warehouse development, but also their decisions around land use (personal interview, August 8, 2023). Such comments highlight the broader fiscal challenges faced by inland cities.

City Competition for Jobs and Sales Tax

Sales Tax Rebate Agreements

Cities compete for jobs and tax revenue, and this includes jobs in warehousing. Several cities within the case study counties have utilized sales tax rebate agreements as an incentive to attract warehouses to their city, including Ontario, Perris, and Tracy. Ontario has 14 agreements in place, which provided a rebate of $9.4 million to retailers in 2021–2022 (7% of the city's sales tax revenue). Perris had two agreements in place, which provided a rebate of $3 million to retailers in 2021–2022 (12%). Tracy had three agreements in place, which provided a rebate of $6.9 million in 2022–2023 (9%). 9 While these rebate agreements covered a range of retail businesses, the newer agreements that generate the largest rebates are primarily with e-commerce retailers. As an example, Ontario provided a sales tax subsidy to Nike that will waive $17.25 million over the 11.5-year term of the agreement in exchange for Nike agreeing to construct a 580,000 square foot distribution center that it “would not consider locating” in Ontario without the subsidy and “possibly not in the State of California” either (City of Ontario, 2020). Ontario (2020) expected the agreement to “generate substantial revenue” including sales taxes, property taxes, and 325 full-time jobs (at an average base salary of $36,197). More broadly, Ontario (2020, Section 5-Statement of Public Purposes) noted that the agreement is aligned with its policy to be “business friendly and support economic growth including the creation of new job opportunities and new sources of revenue that support residents and city services.” In 2021–2022, Nike received a rebate of $983,728 (City of Ontario, 2023).

The cities of Dinuba and Fresno, located in the Central Valley of California between the Inland Empire and North San Joaquin Valley, have been utilizing sales tax rebate agreements to attract warehouse companies. Dinuba entered into an agreement with Best Buy, which reportedly returns 50% of sales tax revenue back to Best Buy, 10% to the lawyer who executed the agreement, and 40% to the city (California Senate Committee on Revenue and Taxation, 2024). The City of Fresno has entered agreements with Amazon, Nordstrom, and Gap. In addition to offering sales tax rebates to e-commerce companies, Fresno also offered property tax rebates and invested in infrastructure to support warehouse development (Hinkley & Weber, 2021).

The focus of these sales tax rebate agreements is not only attracting the development of the warehouse itself and the associated jobs, but also the designation of the warehouse as a “sales office” or “point-of-sale.” E-commerce companies are reportedly able to play cities against each other because they have the power to choose where they establish their warehouses and to determine the point-of-sale location for sales in California, regardless of where the order is fulfilled. For example, Best Buy has allocated all its California sales to its location in Dinuba (Mahoney, 2023a), despite having several distribution warehouses located elsewhere in the state. The California Department of Tax and Fee Administration is challenging several cities that contain warehouses that have been established as the primary point-of-sale for online retailers. For example, it is engaged in legal action with San Bruno regarding its establishment as a point-of-sale facility for Walmart.com online sales (Mahoney, 2023b; Rusch, 2024). There is a lack of transparency by retailers regarding the allocation of the point-of-sale and the proportion of sales that are fulfilled at these locations.

Sales tax rebate agreements are typically justified by cities based on the jobs that will be generated by the agreement. Policies that promote job creation are politically attractive because they are rewarded by voters (Bartik, 2019a). There is a significant opportunity cost associated with rebate agreements as they pull public dollars away from local expenditures and promote city competition, which can lead to a race to the bottom (Propheter, 2011; Wassmer, 2009). There is also a broader equity issue in the selective use of rebate agreements because they typically favor larger retailers at the expense of smaller businesses (Propheter, 2011). While the agreements may lead to an increase in jobs and tax revenue for the cities who enter into them, increasing automation in warehouses means these jobs have the potential to disappear. Several studies have emphasized the poor quality of warehouse work (see Alimahomed-Wilson, 2021; De Lara, 2018; Delfanti & Frey, 2021; Loewen, 2018; Struna & Reese, 2021), which raises broader questions about the implications of cities becoming locked into long-term sales tax rebate agreements with large e-commerce corporations.

Proposals to Redistribute Sales Tax Revenue

With the growth of e-commerce over the last decade, several proposals to alter sales tax regulations in California that focus on either the redistribution of sales tax revenue or banning sales tax agreements have been raised. Changes to the Bradley-Burns Uniform Local Sales and Use Tax Law have been floated in the past in response to competition between cities for sales tax revenue. For example, in 1993, the California Legislative Analyst Office (1993) proposed changes to local sales and use taxes that would have removed the existing Bradley-Burns local 1% sales tax and replaced it with an increase in the state sales tax rate to “eliminate unproductive competition between local agencies over the siting of retail operations” (p. 123). At the time, Schwartz (1997) suggested that the proposal would reduce the incentive for cities to pursue retail land use and instead encouraged cities to promote uses that “create higher property values and better paying jobs” (p. 216).

In recent years, there have been two unsuccessful proposals to shift from an origin-based to a destination-based sales tax system (SCA-20 and ACA-13). These proposals were opposed by cities that have sales tax rebate agreements with retailers (for example, Dinuba, Fresno, and Ontario). In its opposition letter to SCA 20, Ontario noted that land use decisions are made “based on the expectation that Bradley-Burns tax revenues will mitigate any consequential burdens to the surrounding community,” and that eliminating the revenue would leave cities with these burdens (California Senate Committee on Elections and Constitutional Amendments, 2018, p. 9). Ontario also noted that e-commerce is “an economic catalyst that has benefited many cities and counties” in California, particularly in the Inland Empire (California Senate Committee on Elections and Constitutional Amendments, 2018, p. 9). Focusing on the allocation of sales tax to county transport funds, the California State Auditor (2017) released a report recommending a change from an origin-based to a destination-based sales tax system because it would result in “a more equitable distribution” of local transport funding and remove the incentive for cities to compete to attract sales tax revenue. However, in the report, the California State Auditor did not explain how a destination-based system is more equitable.

The ongoing possibility of a redistribution of sales tax revenue was mentioned in several interviews. An interviewee from a local city emphasized that there is always a possibility that the state could change the process for allocating sales tax revenue and as a result “we can't rest on the idea that [sales tax is] going to be the reason why all this stuff is ok” (personal interview, August 8, 2023). The League of California Cities (2023), a statewide advocacy organization representing all cities, has formed a City Managers Sales Tax Working Group to consider policies to facilitate a more equitable distribution of sales tax revenue between the cities that facilitate the delivery of the goods and cities that are the destinations for the goods: The equitable allocation of remote revenues from e-commerce recognizes both sides of the transaction and their contribution to sales tax generation. Allocation of the Bradley Burns 1 percent local sales tax revenue from in-state online purchases should proportionately benefit those communities that provide the infrastructure and incentives that facilitate the transaction and delivery of those goods and those communities that are the destinations for the goods. The regional impacts to infrastructure, land use, environmental quality, and public health stemming from e-commerce as well as the financial dependence of communities on the resulting revenues must be recognized. Changes to consumer behavior, which consists of more online shopping, must also be considered as to the fiscal sustainability of all cities. City officials should account for these factors in the evolving marketplace and continuously strive for prospective fair and equitable revenue sharing based on data, as available. City officials should also employ their best judgement to support policies that benefit the sustainability of all cities (League of California Cities, 2023, p. 10).

The League of California Cities refers to the above statement as an equity statement. However, an equal allocation of e-commerce sales tax revenues to the locations of warehouses and the consumers is likely to benefit cities that contain a concentration of consumers—wealthy urban cities like San Francisco. Arguably, the fiscal sustainability of cities that are reliant on sales tax revenues is more at risk, particularly in economic downturns. In fact, Stockton and San Bernardino both declared bankruptcy in the wake of the Global Financial Crisis (Walsh, 2012), exiting bankruptcy in 2015 and 2017, respectively.

Proposals to Regulate Sales Tax Rebate Agreements

Several bills have been proposed to rein in the use of sales tax rebate agreements in relation to warehouses over the past 5 years. In 2015, SB 533, which prohibits cities from entering into sales tax rebate agreements that would result in a reduction in the sales tax revenue received by the city where the retailer maintains a presence, was approved by California Governor Gavin Newsom.

Despite being approved by the Assembly Floor in October, 2019, SB 531, which would have prohibited sales tax rebate agreements, was vetoed by Governor Newsom because he believes that the use of the agreements is “limited” and is “an important local tool that captures additional economic activity, particularly in rural and inland California cities that continue to face significant economic challenges like high unemployment rates” (California Office of Senate Floor Analyses, 2019, p. 5). Newsom determined that “removing these tax options from local decision makers is the wrong approach” (California Office of Senate Floor Analyses, 2019, p. 5). Instead, Newsom approved AB 485, which requires cities to publicly report the details of economic development subsidies of $100,000 or more provided to warehouse distribution centers.

In 2024, two bills were proposed relating to sales tax rebate agreements. The first bill, AB 2854, requires local agencies to publish sales tax agreements on their websites and imposes monetary penalties for local agencies who fail to do so. In September 2024, Governor Newsom signed AB 2854. The second bill, SB 1494, proposed to ban sales tax agreements. SB 1494 was opposed by several cities including Beaumont, Dinuba, Eastvale, Fresno, Ontario, Perris, and Tracy, as well as the League of California Cities and various retail and business chambers. In its letter of opposition, the League of California Cities noted that it wants to preserve sales tax rebate agreements as “an economic incentive tool” while considering opportunities to “reduce competition and create a fairer environment” through a redistribution of sales tax revenues (League of California Cities, 2024, p. 2). When SB 1494 was discussed on the Senate Floor in June 2024, the debate focused on the role of sales tax rebate agreements as an economic development tool for disadvantaged cities, and the distribution of local sales tax revenue. Senators from Stockton and Riverside highlighted the environmental and health costs of warehouses that their communities sustain. SB 1494 failed to receive sufficient votes to progress and is now inactive. Cities may continue to negotiate sales tax rebate agreements with e-commerce corporations.

Discussion: Politics of Land Fiscalization and Equity Considerations

The rise of e-commerce and the origin-based sales tax system in California has created a new politics of land fiscalization characterized by a growing tension between what the California Assembly Revenue and Taxation Committee described as “cities that benefit” and “cities that feel disadvantaged” by the current e-sales tax revenue system (California Senate Committee on Revenue and Taxation, 2024, p. 5). Prior to the Covid-19 pandemic, downtown retailers were largely supported by high-wage office workers. Office vacancies associated with remote work and tech layoffs continue to impact retail expenditure in downtowns, particularly in San Francisco (Li & Stiefel, 2024). While the vulnerability of retail employment to economic downtowns is not new, the rise of e-commerce has reshaped the geography of retail employment, affecting suburban and downtown shopping centers, which has flow-on impacts for retail employment and also sales tax revenue for cities. For states with a local sales tax and a destination-based sales tax system, sales tax revenue has increased in rural localities at the expense of urban downtowns, which typically have large retail agglomerations (Agrawal & Shybalkina, 2024). However, for states with an origin-based sales tax system for e-commerce transactions, like California, localities on the urban periphery with warehouses have experienced an increase in sales tax revenue, at the expense of urban downtowns. For example, the City and County of San Francisco (2023) noted that while its sales tax revenue has recovered somewhat since the Covid-19 pandemic, the recovery has been “slightly offset” by a decrease in sales tax revenue from e-commerce because “a major online merchant began to deliver goods to San Franciscans through in-state fulfillment centers, resulting in shifting sales tax revenue from San Francisco to the jurisdictions in which the centers are located” (p. 13).

However, it is not just cities in the urban core that are disadvantaged under the current sales tax regulations in California. Cities on the urban periphery without point-of-sale warehouses may also be losers under the current system. For example, Manteca and Tracy are both located in San Joaquin County and have comparable population sizes (87,000 residents versus 97,000 residents), the same sales tax rate (8.25%), and comparable property tax revenues. In 2022, Manteca had a sales tax revenue of $184 per person compared to $772 per person in Tracy. Similarly, in 2022, Reedley had a sales tax revenue of $89 per person, compared to $575 per person for neighboring Dinuba. (Both cities had approximately 25,000 residents in 2022, and Reedley had a higher sales tax rate at 9.225% compared to 8.5% for Dinuba.) Cities such as Manteca and Reedley, which have not benefited from the growth in e-commerce from a sales tax revenue perspective, are at more of a disadvantage than cities such as San Franciso because they do not have a substantial property tax revenue base.

For bricks-and-mortar retail, the ability of cities to “steal” sales tax revenue from other cities is largely constrained by the retailer's physical proximity to consumers, particularly for day-to-day shopping needs. With e-commerce, retail catchments are no longer confined to the distance that consumers are willing or able to travel to purchase goods. The distance between the consumer and the point-of-sale has increased, and retail capital has become more mobile. In addition, retailers determine the point-of-sale location, giving them additional leverage with cities. Cities are not just competing to attract warehouse development because of the potential jobs, development fees, and property tax revenue, they are also competing and negotiating with e-commerce retailers for their warehouses to become point-of-sale locations to increase their sales tax revenue. The pool of sales tax revenues that can be allocated to a city as the point-of-sale is also much larger than for bricks-and-mortar retail because it is not constrained by local retail catchments either. There is a lack of transparency regarding whether the warehouses that are designated as point-of-sale facilities are where orders are actually being fulfilled. The California Department of Tax and Fee Administration is currently investigating some of these agreements.

Sales tax is an important general revenue source for many cities, particularly cities that have lower property values. As a county official stated, “warehousing is where the money is… it's hard for a lot of jurisdictions to look at other options, when the sales tax base coming in from warehousing can mean they can pay for public safety, that they can pay for parks” (personal interview, July 11, 2023). The development of a warehouse does not guarantee sales tax revenue if the warehouse is not a fulfillment center and is not designated as a point-of-sale facility. Many cities have become fiscally dependent on e-commerce warehouses as a source of sales tax revenue and employment, meaning that the local economy and fiscal position of cities remains vulnerable to economic downturns.

A core issue in California is the use of sales tax rebate agreements and the lack of transparency regarding the point-of-sale location. The League of California Cities is leading a statewide proposal for a more equitable distribution of sales tax revenues, which could see a redistribution of sales tax revenues from the location of e-commerce warehouses to the location of e-commerce consumers. The California Department of Tax and Fee Administration (2023a) has undertaken analysis of the impact of a destination-based system on the sales tax revenue of cities in California using retail transaction data for large retailers. The analysis concluded that of the 482 cities studied, 313 will experience an increase and 28 will experience a decline in revenue. The cities expected to experience a decline in revenue are primarily warehouse cities like Tracy, Eastvale, Rialto, Perris, and Dinuba; the cities expected to experience the most gains are those with a lack of retail shopfronts or warehouses. This analysis, however, did not assess the impact of a destination-based system on local jurisdictions in California compared to the origin-based system before the Wayfair ruling; that is, the impact on cities that have experienced declines in sales tax revenue due to the decline in bricks-and-mortar sales. The winners and losers are likely to differ depending on the base case for comparison.

The momentum for a destination-based system may be building, given the decline of in-person retail expenditure driven by remote work and increasing use of e-commerce was spurred by the Covid-19 pandemic. Some politicians continue to advocate for bans on sales tax rebate agreements. However, previous proposals to redistribute sales tax revenue and ban sales tax rebate agreements have received insufficient support to progress. A destination-based system would address the issue of competition for point-of-sale facilities and the use of sales tax rebate agreements. However, a destination-based system would result in a concentration of sales tax revenues in jurisdictions with higher incomes and higher population densities, which are typically jurisdictions with higher property tax revenues. Concentrating sales tax revenues in cities with wealthy consumers under a destination-based system would not address equity. Focusing on reducing sales tax competition between states (rather than between cities), Bruce et al. (2023) suggested that “policy options to further reduce sales tax competition should go beyond rates, bases, and sourcing rules to include consideration of voting thresholds for policy changes, equalization grants or other mechanisms to offset competition” (p. 22). Considering the constraints that California cities face in raising revenue, particularly property tax revenue, a more equitable distribution will likely require the redistribution of sales tax revenues (and even property tax revenues) to address fiscal disparities. Other states have implemented revenue redistribution programs such as Minnesota (Fiscal Disparities Program). Through Minnesota's property tax revenue sharing program, local jurisdictions are required to provide 40% of the growth in their commercial and industrial property tax base since 1971 to an areawide pool, which is then distributed to local jurisdictions based on relative fiscal capacity 10 (Swanson & Hinze, 2020). Alternatively, California could replace its local Bradley-Burns sales tax with an increased state sales tax, which has been proposed in the past, and distribute the increased state sales tax to local jurisdictions based on fiscal capacity. In addition, as highlighted by the League of California Cities (2023), consideration could also be given to the cost borne by cities with e-commerce warehouses, particularly wear and tear on roads due to the high number of trucks on local streets and the financial costs required to maintain these roads.

Conclusion

The rise of e-commerce and the Wayfair ruling have altered the allocation of local sales tax revenues across the United States. Existing studies demonstrated that in states with a destination-based local sales tax, rural localities have experienced increases in sales tax revenues at the expense of urban cores with retail agglomerations. For states with an origin-based local sales tax system, such as California, cities on the urban periphery with a concentration of warehouses have experienced substantial increases in sales tax revenues. The changes to how local sales tax is allocated in California have also created a perverse incentive for cities to negotiate sales tax rebates with retailers in exchange for the designation of their warehouse as a point-of-sale location. Cities now compete at the regional or state level with other cities to attract e-commerce point-of-sale warehouses. E-commerce warehouses are somewhat more mobile than bricks-and-mortar retail because they are not constrained by proximity to local retail catchment. These e-commerce point-of-sale warehouses service a much wider area than a local store, which means that a warehouse brings more jobs, more sales, and thus, more sales tax revenue. Additional transparency is required regarding the catchment that these point-of-sale warehouses serve and the number of sales that are being processed within them to inform policy changes.

Implementing a destination-based local sales tax system will address the issues associated with city competition for sales tax revenue; however, it will not necessarily achieve an equitable distribution of sales tax revenue. The e-commerce revolution has redistributed sales tax revenue to cities with limited economic leverage, but the fiscal position of these cities remains vulnerable to economic downturns. The cities that have benefited from an increase in sales tax revenue are dependent on sales tax as a core general revenue source, while some cities that are disadvantaged under this current system are able to lean on property tax as a core revenue source to fund infrastructure and services. They are likely to be in a more stable fiscal position during economic downturns than metropolitan fringe cities without warehouses. Policy changes should also take into consideration the role that cities with a concentration of warehouses play in the retail supply chain, specifically, the fiscal burden that cities face in maintaining roads impacted by truck traffic, as well as the long-term fiscal sustainability of all cities, and equality in service provision. Implementing an equitable sales tax system may require a movement away from the local collection of sales taxes and require states to distribute sales taxes to cities based on fiscal capacity. Achieving a more equitable allocation of sales tax revenue at the local level remains a challenge for origin-based states as well as destination-based states that have also seen a shift in the distribution of sales tax revenue.

Footnotes

Acknowledgements

I would like to extend my gratitude to Karen Chapple, Carolina Reid, Sai Balakrishnan, Maximilian Buchholz, the three anonymous reviewers, and the associate editor for their thoughtful comments and constructive feedback on earlier drafts of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.