Abstract

Despite the central role that landlords, or residential rental property owners (RRPOs), play in housing, important areas of RRPO decision making are not well understood. Because of the importance of RRPOs in the housing system, gaps in our knowledge leave planners at a disadvantage when creating policies to improve housing stability for tenants. This article is a comprehensive, interdisciplinary literature review of RRPO characteristics and behavior framed around three decision points: career lifecycle, portfolio maintenance and development, and property operations. This review ends with suggestions for an RRPO-focused research agenda that supports urban resiliency and housing stability for renters.

Introduction

In the American housing system, the private market is the primary source for the provision and distribution of housing (Marcuse and Keating 2006). This means that first a property is developed, then a succession of owners decides who lives in the building, the terms of that tenure, and the extent to which the building is managed and maintained. Although the proportion of owner-occupied and rental units varies widely from city to city, residential rental property owners (RRPOs) remain central to the stability and resilience of local housing systems. Despite their importance, RRPOs’ decision making and motivations rarely serve as a focus of planning research.

In this article, we use the term “RRPO” to describe individuals and entities who own residential rental properties. We believe this term has several advantages over “landlord” or other common terms. Its primary strength is that it clearly specifies the topics of concern. Other terms can be more generally applied to a range of real estate assets, but we are interested in residential rental property. Being a landlord is a multidimensional social and economic role which can be studied from a variety of perspectives. Where others have incorporated property managers or examined the perspective of “investors,” for example, we are approaching this work focused on key decision points under the unique authority conferred to owners. The term also helps bridge some traditional divisions that are commonly used when discussing landlords. RRPO is a classification for owners that can be inclusive of different portfolio sizes, organizational structures, and building types. We believe this shift is an important step in developing typologies of rental ownership that provide insight into today's pressing problems of housing resilience, stability, and affordability. It also invites planners and other governmental actors to consider new possibilities for partnering with, incentivizing, or more effectively regulating these vital stakeholders.

Planners today must address local needs for rental housing stability and affordability within a regulatory and market context that differs significantly from earlier periods. The meaning and impacts of rental market dynamics and how researchers have made sense of them have changed over time. For example, during the upheaval of the 1960s when the urban housing crisis took center stage in national politics (Taylor 2019), Sternlieb's groundbreaking work, The Tenement Landlord, investigated the role of RRPOs in rehabilitating urban neighborhoods in Newark and found that declining real estate markets were responsible for lowering maintenance standards (Sternlieb 1969). A decade later Sternlieb and Hughes found that the city contained two distinct markets: one where low-income people sought affordable shelter and one where elites sought housing as an investment (Sternlieb and Hughes 1983). Within a short time, Sternlieb's concern had shifted from abandonment to gentrification.

Sternlieb's work suggests that changing markets and the decisions that RRPOs make over time related to the development and management of their portfolio are important areas of research. Questions regarding investment trends emerged again during the mortgage crisis. For example, following the passage of the 2008 Housing and Economic Recovery Act, the federal government sold millions of real estate-owned (REO) properties to investors through government-sponsored enterprises, leading to increases in single-family rentals and distinct shifts in ownership trends, particularly in Sunbelt housing markets (Immergluck 2010; Molina 2016; Molloy and Zarutskie 2013). The crisis changed the array of owners operating in the rental market and the distribution of owners and renters. This was especially true in places with heated rental markets where families who lost their homes to foreclosure became renters (Mallach 2010). As the financial crisis waned, demand for real estate investments remained high, driven in part by high returns (especially in supply-constrained markets) and the entry of new types of investors (Colburn, Walter and Pfeiffer 2021; Fields 2015, 2018; Ganduri, Xiao and Xiao 2022; Li and Gao 2012).

Since the financial crisis, researchers have increasingly focused on the behaviors of institutional investors (Fields 2018; Garboden 2021; Immergluck and Law 2014a, 2014b; Mallach 2010; Mills, Molloy and Zarutskie 2019; Molina 2016; Molloy and Zarutskie 2013; Pfeiffer and Lucio 2016; Raymond et al. 2016). Ongoing trends related to the financialization and commodification of housing have caused concern about institutional RRPOs dominating markets and creating barriers that prevent owner-occupants or noninstitutional RRPOs from purchasing homes, particularly in predominantly nonwhite neighborhoods (An 2023; Chilton et al. 2018; McMillan and Chakraborty 2016; Seymour et al. 2023; Tapp and Peiser 2022). We define “institutional” as a legal entity or fiduciary that is investing in real estate on behalf of clients or shareholders. This can include banks, REITs, private equity companies, and large development corporations. Alternatively, “noninstitutional” owners usually invest using their own capital and personal debt. They may be sole proprietors or have their business structured as a Limited Liability Company (LLC), trust, or other entity. Typically, noninstitutional owners are knowledgeable about specific properties in their portfolio and directly involved in the business of property ownership and management. While individual RRPOs using LLCs can be described as corporatized, they are not necessarily corporations (Travis 2019).

The reasons that individuals come to own rental properties are more complex than generating returns for investors and can include a range of circumstances and motivations like accidental ownership through inheritance, planning for retirement, or seeking independence as a small business owner. Likewise, how individual owners select properties, manage units, relate with tenants, and interact with local governments are informed by any number of social, personal, political, and entrepreneurial beliefs. Discussions that generalize the diverse behaviors of individual rental property owners risk obfuscating the complexity of this group. As a result, planning practitioners may be missing opportunities for productive, long-term collaboration where business and public interests align.

We organize the relevant literature around three key areas of RRPO decision making:

Career: Why does someone enter or exit the RRPO field? Who is likely to own rental property? What factors affect the trajectories of the professional lifecycle of a rental property owner? Strategy: What factors influence decisions to buy and sell properties within a portfolio? What variables influence the composition of portfolios of RRPOs and the places where they decide to invest? Operations: How do RRPOs approach the operation of their rental property businesses including tenant relationships, rent setting, and property maintenance? How does professional management and technology impact operational decisions? How do RRPOs react to fair housing laws, restrictions on evictions, and other local policies?

From our analysis of the existing literature, we suggest that researchers should construct new typologies of RRPOs that consider how owners differ within and across these decision-making areas. New knowledge related to the careers, strategies, and operations of noninstitutional RRPOs will help planners better understand the unique composition of their local housing market and collaborate with or regulate RRPOs in ways that consider tenant needs and owner constraints, anticipate RRPO responses to interventions, mitigate unintended consequences at the point of implementation, and meet policy objectives. In the remainder of this article we briefly describe our methods for the literature review then present our findings organized within the decision-making framework. Finally, based on the existing literature we identified some RRPO variables that can serve as a starting place for decision-based typologies and propose a research agenda that can be used to develop the types of typologies that we believe can provide actionable insights and inform planning practice.

Methods

We began our review using the methodology outlined by Xiao and Watson in their article, “Guidance on Conducting a Systematic Literature Review” (2019). We restricted our search to English-language articles from 2008 or later with primarily US-focused research, and we developed a method using decoy articles to verify the comprehensiveness and validity of our findings. Since no database catalogs all potentially relevant articles across disciplines, some publications were not captured. However, we are confident that this review identified more than 90% of the relevant articles that fell within our search parameters. 1

First, we brainstormed a list of terms related to rental property businesses and conducted a round of test searches to identify additional keywords. We combined these terms with synonyms for “landlord” and then conducted searches in two databases: Google Scholar and JSTOR. Next, we identified the decoy articles. Decoys are a method used in human and ecological censuses to minimize undercounting and indicate the adequacy of an enumeration effort (Wright and Devine 1992). In this review, decoys served a similar purpose: if the decoy articles were not identified, we could estimate the degree to which the search process was incomplete. The 15 decoy articles were all in peer-reviewed planning journals, fit the same parameters as the searches, and had been cited an average of 54 times. After checking our initial searches against the decoy list, we refined our search terms and re-ran the expanded list of search terms through EBSCOHost.

Finally, we organized the articles and selected three for each decision category. We used these articles for forward and backward searches to identify articles we missed in the initial searches. Our final list for the review included 196 articles. Because 93% of the decoy articles appeared in the searches, we are confident that we found most of the relevant articles in peer-reviewed and gray literature in and outside of planning. 2

This review investigates the complexity within the field of noninstitutional RRPOs. Our methodology was not structured to distinguish between institutional and noninstitutional owners because the existing literature often does not distinguish between the two. However, many of the studies discussed in this review focus specifically on behaviors or characteristics of individuals who own rental properties. These individual RRPOs are by definition noninstitutional. When a study explicitly focuses on institutional RRPOs, that will be identified in the text.

Findings

This section discusses the themes among the RRPO-focused articles that align with our three decision-making categories: Career, Strategy, and Operations. At the end of each subsection, we discuss the implications of the diversity of RRPOs revealed in this review. The findings are followed by a discussion of why planners need a more nuanced understanding of rental property owners and a set of factors that could form the foundation of new typologies for categorizing RRPOs. The paper ends with recommendations for an RRPO-focused research agenda that could address existing gaps and further develop new typologies.

Career

RRPO decisions to enter the business are influenced by social, economic, and personal factors. However, conventional wisdom about RRPO career decisions is largely based on stereotypes or knowledge that merits reexamination (Roberts and Satsangi 2021). We found that the career-based considerations in the literature include the fundamental decision to enter or exit the market and individual, economic, and cultural factors associated with these decisions. Some research considers how geographic trends and market expectations affect new investors. There is also research on how taxation policies affect RRPO career decisions and how RRPOs decide on the corporate structure of their business.

The desire to generate revenue from real estate is consistent with “America's broader aspirations for self-sufficiency and autonomy” (Garboden 2021, 2–3). For aspiring entrepreneurs, the rental business is reputed to have low barriers to entry relative to other small businesses and to require a skill set that can be gained through the self-help industry. This attracts people without significant savings because assets can be leveraged, meaning “real estate represents an opportunity for poorly capitalized individuals to generate investment portfolios far beyond what would be possible with stocks or bonds” (Garboden 2021, 2). For owners with small portfolios, real estate opportunities typically crowd-out stock market participation (D’Lima and Schultz 2021); and economically marginalized groups show a growing preference for investment over savings to create financial security (Garboden 2021).

Individuals often become RRPOs at the urging of a friend, family member, or professional mentor (Garboden 2021). There are books, courses, and online communities that can influence someone's decision to enter the business. These popular sources promote rental property ownership by touting it as “exceptionally profitable and fun” (Turner 2021) and promising annual returns between eight and ten percent (Tyson and Griswold 2009). Garboden cites Fridman's book Freedom from Work to say that “investment techniques pedaled by self-help gurus … are utilized by economically insecure individuals not only for financial ends but as a broader project of self-help” (Garboden 2021, 3).

Timing matters with real estate investment, and new RRPOs often mistime their market entry. Individuals who were initially motivated by flipping or speculation are more likely to purchase properties when the market is nearing its peak (Bayer, Mangum and Roberts 2016). This increases the probability that they will overpay, earn lower returns, and default on a mortgage (Bayer, Mangum and Roberts 2016). Leading up to the mortgage crisis, the decisions of many RRPOs repeated these dynamics. When purchasing properties in other cities, they gravitated to areas where prices had already risen sharply, exacerbating the inevitable bust (Chinco and Mayer 2016).

Age also affects the career decisions of individual RRPOs. Research on pre-2008 data found “investment in rental real estate increases with age through midlife and then decreases thereafter” (Seay et al. 2018). Baby boomers may be defying these expectations as they tend to maintain “bridge employment” in retirement compared to older generations (Gobeski and Beehr 2009). Decker found that 30% of RRPOs are retired and 46% think of their rental properties as part of their retirement plan (Decker 2021c). Garboden found that retirement without a pension leads some to seek passive income even if they have retirement savings (2021). Older RRPOs with mortgaged property faced additional pressures to sell during the pandemic (Choi and Goodman 2020), which could hold true for other market shocks.

Many people become RRPOs unintentionally. One study found that nationally, for RRPOs who owned only 1 or 2 units, 16% had inherited the property, 43% were renting out units that had once been their primary residence, and 26% were renting out properties that they intended as a future home for themselves or a family member (Decker 2021c). Circumstantial ownership can be associated with life changes like divorce or having children (Wood and Ong 2013). Owners obtaining property circumstantially may focus less on profit maximization than those purchasing primarily for investment revenue (Shiffer–Sebba 2020).

Rental housing is an attractive investment option for higher-income households since property tax, maintenance costs, and depreciation are deductible (Bourassa et al. 2013). The mortgage interest deduction further decreases tax liability for debt-financed ownership with significant implications for the rental market (Hudson 2010). Research in the United States and abroad suggests that removing the mortgage interest tax deduction would decrease demand for rental homes, lower housing prices generally, and increase homeownership by 5.2% (Bourassa et al. 2013). Similarly, researchers predict that without deductions, RRPOs would exit markets because of “the higher tax obligations created by the elimination of the mortgage interest deduction” (Sommer and Sullivan 2018). The 1031 exchange tax provision also makes it possible for an owner to defer capital gains tax on a property sale as long as they continue to invest in real estate (Mühlhofer 2013) and investing across multiple countries helps the wealthy further minimize tax liabilities (Fernandez, Hofman and Aalbers 2016). The cumulative effect of these tax benefits is that real estate investing is sticky, particularly for high-income owners. The tax benefits (and appreciation) associated with rental property ownership mean that an RRPO's decision to sell is often based on more than just cash flow — ultimately an empty property may still be a money maker.

The conditions under which someone embarks on their RRPO career will influence how they operate their business going forward. Someone persuaded to become an RRPO by their friends or family is likely to continue to seek their input. Someone responding strictly to market trends might be more sensitive to changing forecasts, competing opportunities, or regulations. There may be specific social or cultural influences related to becoming an RRPO that provide planners with insight into the behaviors and objectives of some RRPOs and opportunities to build shared goals. Based on the available literature, an understanding of career-related variables could be useful to identify potential barriers and opportunities related to housing policy goals.

Strategy

Once in the business, RRPOs must decide how to manage their portfolio and whether to grow their holdings over time. Owners have different strategies for purchasing property that align with their career goals, desired returns, and risk calculations. Their business strategies shape the class, size, and location of the properties they select, and these strategies evolve in response to changes in their needs and market conditions. Decisions about buying, holding, or selling a particular property can be influenced by an RRPO's perceptions of a neighborhood and the people who live there, often with class and racial implications.

RRPOs’ must navigate potentially conflicting goals “including risk reduction on one side, and leveraging risk to seize market opportunities on the other” (Fusch 2019, 90). An RRPO's position along this spectrum may result in decisions to scale up and acquire new assets, to forgo expansion and focus on operations, or to sell properties. Mallach coined the terms “rehabber,” “milker,” “flipper,” and “holder” to explain the strategies of buyers participating in the market during the 2008 housing crisis. Flippers and rehabbers buy properties in poor condition and sell them quickly to make a profit with (rehabbers) or without (flippers) improvements (2010). They like tight markets and are arbitraging “intermediaries who survive based on superior information, or momentum traders blindly chasing the market trend” (Leung and Tse 2017, 255). Flippers’ and rehabbers’ strategies may not involve rental revenue at all.

Milkers buy cheap properties in poor condition and “rent them out in as-is or similar condition with minimal maintenance often to problem tenants” (Mallach 2010, 10). Their cash-flow comes from exploiting the difference between a low purchase price with minimal renovation and relatively high rents. This may be reinforced by “a lack of competitive traditional mortgage financing and a resulting reliance on … high-yield [single-family rental] and hard money lending” (Morrison 2021, 75). Milkers are motivated by rental properties that generate short-term profit. These RRPOs are more likely to be successful if they buy properties with cash, already own real estate, or have local knowledge of the area (D’Lima and Schultz 2021).

Holders are motivated by cash flow and long-term appreciation. They buy and lease properties in fair to good condition, generally maintain the properties, and carefully select tenants. Since holders consider increased equity in their strategy, it is not “necessarily a sign of financial distress” if RRPOs are not profitable, as such owners plan for a period of marginal cash flow and use rents to pay their mortgage (Decker 2021b, 6). The ability of well capitalized holders to adjust their strategy between cash flow and appreciation has led to the suggestion of an additional subcategory of “buy and hold institutional investors” to account for long-term institutional RRPOs, though the long term strategies of institutional RRPOs, particularly in the single-family rental market, have yet to manifest (Colburn, Walter and Pfeiffer 2021, 1619).

Changing land values may also change how investors see their assets and potential returns over time (Christophers 2016). Owners may start as milkers or holders, then become something akin to large-scale rehabbers who redevelop the land they own to increase returns. Owner occupants and RRPOs who eventually redevelop a property to increase profitability are a relatively unexplored group but merit examination in relation to upzoning efforts around the country. Research shows that properties that were intended for demolition are more likely to be the sites of eviction and displacement (Ramiller 2022). As a owner's vision for a property or parcel changes, so do their revenue expectations and their image of a desirable tenant.

RRPOs also consider property attributes in their business strategies and resulting portfolio decisions. Small rental properties are associated with lower rents and more resident owners (Ellen, Been and Hayashi 2013). Immergluck and Law (2014b) found that smaller, older homes require a low up-front investment which attracts certain buyers, while other owners want more durable property that, as a result, is also more expensive. The housing stock in these smaller properties is highly diverse and RRPOs’ strategies consider demand for housing in different submarkets (Mallach 2007).

Local conditions affect real estate investment patterns. In high-price cities, RRPOs are motivated by potential capital gains, while those in low-price areas anticipate higher rental returns (Demers and Eisfeldt 2022). Sociological research before 2008 showed that RRPOs were investing in places with laissez-faire principles, greater residential instability, and a lack of local economic headquarters (Goldstein 2018). The foreclosure crisis affected RRPO strategies differently depending on the rental market. Foreclosure rates were high for rental properties in majority Black neighborhoods where high-priced loans were concentrated (Gilderbloom et al. 2012; Rosenblatt and Sacco 2018), and after the crisis, institutional investors showed a preference for these distressed properties (Cohen and Harding 2020; Fields 2015; Molina 2016; Treuhaft, Rose and Black 2011). Sunbelt cities showed distinct trends during this time. In Phoenix, RRPOs who purchased foreclosures were more likely to accept housing vouchers than previous RRPOs, and the volume of single-family home foreclosures increased the ability of voucher holders to rent in more affluent areas (Pfeiffer and Lucio 2016, 2017). In Atlanta, single-family home rentals increased substantially, particularly in Latino and Asian neighborhoods with older housing stock (Immergluck et al. 2020).

Local governments have significant control over urban development. Planners can use research on how RRPOs develop their portfolios to incentivize certain kinds of investment in the places where that investment is needed. Most planners concerned with housing stability want to discourage conditions that lead RRPOs to a flipping, milking, or short-term rental strategy, instead finding incentives that support the pursuit of gradual appreciation. The literature related to RRPO strategies also includes considerations for neighborhoods susceptible to speculation and gentrification. This should be a concern for planners interested in promoting rental housing stability, and it is essential to recognize these conditions early and act quickly to prevent mass displacement (Way, Mueller and Wegmann 2018).

Operations

The research on RRPO operational decisions covers various topics, including tenant selection, rent setting, maintenance, capital improvements, and disaster response. RRPOs demonstrate different levels of flexibility regarding tenant management, and a large body of research has explored how owners use evictions in their business strategies. Innovations in property management technology have improved processes for RRPOs and promises of profit maximization and the ongoing stream of tenant data make the development of new products likely. The variable landscape of tenant protections and rental policies means operations-related practices function differently in different communities, often with racialized and gendered implications.

RRPOs in most parts of the country have significant discretion in screening prospective tenants. Tenant selection has particularly high stakes for those less able to withstand the costs of late rent or damages. As a result, individual RRPOs might be more selective, more aggressively screen tenants, and make more subjective decisions than institutional RRPOs (Decker 2021b). Rosen and Garboden found that individual RRPOs use “culture of poverty” stereotypes and moral evaluations when screening tenants. They are particularly wary of “professional tenants” who take “advantage of tenant-friendly eviction laws to live rent-free for months” (Rosen and Garboden 2022, 482). Institutional RRPOs often use objective, standardized tenant selection processes that protect them from discrimination charges (Decker 2021b). However, such standards do not eliminate bias; discrimination is simply automated in software that relies on biased eviction and criminal records to guide decisions (So 2022).

The tenant selection process is one step in what Korver-Glenn describes as a series of “serial stereotyped interactions” that compound inequality across the housing market (2018). RRPOs show preference to white renters in subtle ways including quicker response times, more detailed correspondence, and the use of positive language when replying to inquiries (Hanson, Hawley and Taylor 2011). Direct Fair Housing violations also persist. Faber and Mercier (2022) found that family structure is subject to racialized discrimination in rental applications with Black women and Latinas penalized for having children or being single mothers and married Latinas accepted more than unmarried white women.

A few states have antidiscrimination protections beyond the federally identified protected classes. These regulations may prohibit discrimination based on marital status, sexual orientation, nonrelated households, and source of income (Hatch 2021), but harassment and discrimination from RRPOs and managers remains common and difficult to regulate (Rosen 2020; Rosen and Garboden 2022; Tester 2008). Despite HUD's decision to add sexual orientation to Fair Housing rules, protected classes beyond a strict legal interpretation may be increasingly fragile. D’Amato (2016) brought up a hypothetical claim based on the Burwell v Hobby Lobby Stores Inc. decision that religious liberty arguments could be used to justify discrimination against LGBT people. Given the 303 Creative v. Elenis decision, it seems even more likely that courts may hear cases aimed at challenging expanded Fair Housing protections (Wellhausen 2023).

Understanding how owners view their tenants and what motivates flexibility when problems arise is important. Rosen and Garboden found that owners may take time to educate tenants, “molding them into a profitable ideal,” using paternalistic reformist and punitive strategies (Rosen and Garboden 2022, 470). Garboden et al. studied RRPO perception of voucher-holding tenants and found that some perceive them as more grateful and respectful of their property while others worried about an increased risk for property damage, evictions, citations, and other headaches (2018). They, along with Rosen (2020), found that owners focused on low-income renters often accepted vouchers to ensure predictable income, especially in cities with low rents.

Setting rents is another significant operational decision. Researchers have shown that RRPOs impose higher rent burdens in low-income neighborhoods. Desmond and Wilmers point out that “perceived market risk and consumer exploitation have long gone hand in hand,” with redlining justified “by claiming that insuring mortgages in [B]lack communities was too risky” (2019, 1117). Decker found that noninstitutional RRPOs “provide substantial discounts to good tenants” but cautioned that these decisions may not be equitable, socially beneficial, or legal (2021a, 71). Alternatively, institutional owners have standardized processes and rent increases that are “consistently higher than in comparable units in the same market” (Clarke 2017, 18). Slowly changing rents are associated with small and detached units (Verbrugge and Gallin 2017). This points to divergent rent-setting strategies of institutional and noninstitutional RRPOs, perhaps a result of a desire by the latter to avoid turnover and vacancy costs.

Property maintenance behaviors vary according to investment strategy and owner type. Studies show that large owners are less likely to rehabilitate properties and more likely to incur code violations (Ellen, Been and Hayashi 2013; Fisher and Lambie-Hanson 2012; Hwang 2019), using corporate liability protections and shielding from management companies to evade accountability (Horner 2018). Among noninstitutional RRPOs, Rose and Harris found that small properties with absentee-owners had the most code violations, owner-occupied had the least, and local RRPOs fell in the middle. Absentee RRPOs with LLCs did better, but properties that relied on managers were worse (2022). Other research has associated LLCs with property neglect and abusive practices toward tenants (Horner 2018; Huq and Harwood 2019; Travis 2019). These discrepancies align with the ambiguous relationship between LLC status and ownership size. However, public programs like the federal Neighborhood Stabilization Program and Housing Choice Vouchers (which require inspections) may encourage maintenance (Cossyleon, Garboden and DeLuca 2020; Holtzen et al. 2016; Immergluck and Law 2014a).

The association between professional property management and property conditions is unclear. The role of managers has evolved from caretaker to a profession aimed at helping maximize profits and compliance with local, state, and federal regulations (Carucci Goss and Campbell 2008). A variety of technology products also help maximize RRPO returns. Both professional property managers and self-managing RRPOs may use automated systems to support repeatable business processes including advertising, screening, leasing, tenant move-in, property maintenance, retention/lease renewals, and tenant move-out; but the technology is likely to be more fragmented for small and mid-sized managers (Bassett and Pisano 2022). Researchers have also shown that technologically enabled management has even made it possible for institutional RRPOs to own and operate a property without a physical presence in the market (Fields 2022). While technology can lower management costs and generate additional value for RRPOs, Fields argues that systems that benefit from the extraction of tenant data constitute a second form of rent and “entangles tenants with largely unaccountable systems of information extraction and commodification” (Fields 2017, 19).

RRPOs vary in their use of evictions. Evictions may be strategic, the cost of doing business, or an onerous chore to be avoided. RRPOs with large holdings or property managers are likely to follow standardized processes for nonpayment, lease violations, and eviction (Garboden and Rosen 2019; Immergluck et al. 2020; Raymond et al. 2016). In Boston, such RRPOs file two to three times more evictions than small RRPOs and are more likely to file repeatedly over small amounts (Gomory 2022). Leung, Hepburn, and Desmond found that almost one-third of evictions are serial evictions, meaning evictions that are filed repeatedly against the same household, sometimes only months apart, and intended to force tenants to vacate or to repeatedly pay monetary sanctions (2021). The Leung study demonstrated that these evictions were concentrated in neighborhoods where institutional owners were responsible for a large share of the eviction filings.

Garboden and Rosen found that RRPOs used evictions to levy additional fees for late payments and keep “poor tenants [living] in a constant state of housing insecurity” (2019, 657). In Atlanta, serial filings were highest in large buildings owned by RRPOs with multiple properties. However, nonserial filings were more likely to result in displacement and take place in predominantly Black neighborhoods (Gomory 2022; Immergluck et al. 2020). Foreclosure sales are often linked to future eviction filings (Seymour and Akers 2021), a pattern that is especially stark in communities like Detroit where, since 2008, more than a third of properties have gone into foreclosure. Anderson (2016) argues that the influence, access, and political capture of local governments by institutional and wealthy individual RRPOs is just starting to unfold in cities around the country and may increasingly impede tenant protections and eviction policy.

Personality also plays a role. Individuals prone to ad hoc decisions may be more likely to pursue negotiations or informal means of removing a tenant. Balzarini and Boyd found that the need for security motivated small-scale RRPOs in Philadelphia to communicate and work with tenants to avoid evictions (2021). Instead, they waived fees, created payment plans, accepted services in lieu of rent, and referred tenants to service providers. Such strategies helped build long-term tenants and avoid turnover costs (like repairs) that are particularly high in cities with older housing stock. Sometimes owners pay tenants to leave — cash for keys — to avoid an eviction. Because small RRPOs have more agency to use informal practices, the loss of this tier of owner could make low-income tenants more vulnerable to eviction and housing insecurity (Balzarini and Boyd 2021; Garboden and Rosen 2019).

Scholars have investigated the effectiveness of eviction-prevention programs. Mediation, legal clinics, and conflict resolution might encourage RRPOs to work with tenants to remedy nonpayment disputes outside of eviction proceedings. Yet the voluntary nature, time, and expense of mediation may not appeal to owners who know they can leverage their relative power in court (Bieretz, Burrowes and Bramhall 2020; Eisenberg and Ebner 2020). Mediation requirements also increase procedural formalism, which some argue causes RRPOs to increase rents and become more selective, thus harming prospective tenants (Bonleu 2019). Right to cure and pay-to-stay ordinances may exacerbate tensions with owners and support their perception that these “encourage tenants to be tardy with their rent, turning them into ‘deadbeats’ who habitually and deliberately delay payment … [and] breeds delinquency and irresponsibility” (Purser 2016, 401).

Eviction and the threat of eviction can be powerful coercive tools in the hands of unscrupulous managers and owners. Sexual harassment of tenants is under-reported because of fear of retaliation, embarrassment, and safety. “Landlords used their institutional authority … and racialized gender stereotypes to exploit tenants’ economic vulnerabilities and sexually coerce them” (Tester 2008, 349). In one study, 10% of women reported sexual harassment severe enough to justify legal action (Oliveri 2019).

Eviction regulations vary widely across the country (Nelson et al. 2021). Serial evictions are more common where the process is fast, inexpensive, and allows the RRPO to easily collect rent and late fees (Leung, Hepburn and Desmond 2021). State protections for tenants are effective in lowering eviction rates. However, even with such protections, predominantly Black neighborhoods show higher rates of evictions, patterns which some researchers suggest align with the racial geography of financialized rental housing (Fields and Raymond 2021; Merritt and Farnworth 2021). RRPOs factor risks associated with tenant-friendly regulation into their rents and increase their investment in tenant screening (Ambrose and Diop 2021).

Tsai et al. (2022) surveyed low and middle-income tenants during the eviction moratorium and found that 4.3% still experienced an eviction. They also found that tenants who delayed rental payments reported worsening relations with their property owner. Large RRPOs exhibited the most adaptability in response to the pandemic, but this adaptability came at the expense of deferred maintenance (De La Campa, Reina and Herbert 2021; Reina et al. 2020). Housing supply often decreases after a disaster, which may tempt RRPOs to raise rents at the same time tenants are experiencing a reduced ability to pay (Notaft et al. 2019). Researchers found that in pro-business jurisdictions, eviction rates increase significantly after a disaster (Raymond et al. 2016), and some owners refuse to make necessary repairs, forcing tenants to move (Ayala 2018).

While Fair Housing laws and eviction protections fall short of their goals, researchers have found that other laws and regulations impact RRPO operational practices, just not in the ways intended. Nuisance property ordinances gained popularity after public housing began excluding people with criminal convictions and local governments sought ways to make RRPOs responsible for public costs related to these “problem” tenants (Mead et al. 2018). Nuisance ordinances are disproportionately used to police nonwhite and low-income residents (Kurwa 2020) and may apply to subjective problems such as bullying (Swan 2015). These ordinances have furthered carceral logics, social control, and third-party policing (Desmond and Valdez 2013; Thatcher and Dalton 2022). Women are often targeted with evictions when owners are contacted by the police following 911 calls, even calls about domestic violence (Desmond and Valdez 2013; Fais 2008). Ordinances can encourage RRPOs to engage in excessive screening, increase rents, and divest from inexpensive housing stock (Greif 2022).

Operational decisions affect the conditions under which renters obtain, reside in, and depart a rental unit. As such, it is the area of RRPO decision making where local policy is most likely to focus efforts to improve habitability and stability for tenants. However, research shows that policies that attempt to directly regulate or incentivize operational decisions face wide-spread noncompliance, are difficult to enforce, and run the substantial risk of exacerbating other issues and creating unintended consequences. To improve the efficacy of local regulations, planners should consider designing policies and implementation strategies with different types of RRPOs in mind and with a greater degree of flexibility, like multi-tiered codes (Mallach 2007). A better understanding of what leads RRPOs to offend could also help cities target limited enforcement capabilities on the most discriminatory, dangerous, and exploitative RRPOs.

Building More Nuanced Typologies of RRPOs and an RRPO Research Agenda

Rental housing matters to planners because local governments and planners need strategies that promote urban resiliency and help tenants who are renting in the private market attain and maintain housing stability. We argue that reaching these objectives requires a better understanding of who owns rental properties and a more nuanced set of typologies that look beyond the institutional dichotomy or small holder/mid-level/large-scale investor. Cities require research-based typologies of RRPOs grounded in observed behavioral differences and empirical studies that are connected to tenant outcomes with actionable implications for practice. In our review of the existing literature on RRPOs, we have identified a substantial body of research on their characteristics and decision-making processes, and the literature makes it clear that this is a richly complex group that can be understood from a multitude of perspectives. However, these perspectives lose their applicability when RRPOs are reduced to overly simplified groups that are assumed to be homogenous. Planners don’t have a way to think about, then plan for, the diversity of RRPOs and the various ways they are likely to respond to changes and different situations. We thus urge the formation of new typologies that start to account for, rather than obfuscate, the diversity of these actors. A fuller and more nuanced understanding of RRPOs career, strategy, and operational decisions. A fuller more nuanced understanding of RRPOs’ career, strategy, and operational decisions would give planners a more effective framework to develop policy, guide effective implementation, and manage housing outcomes.

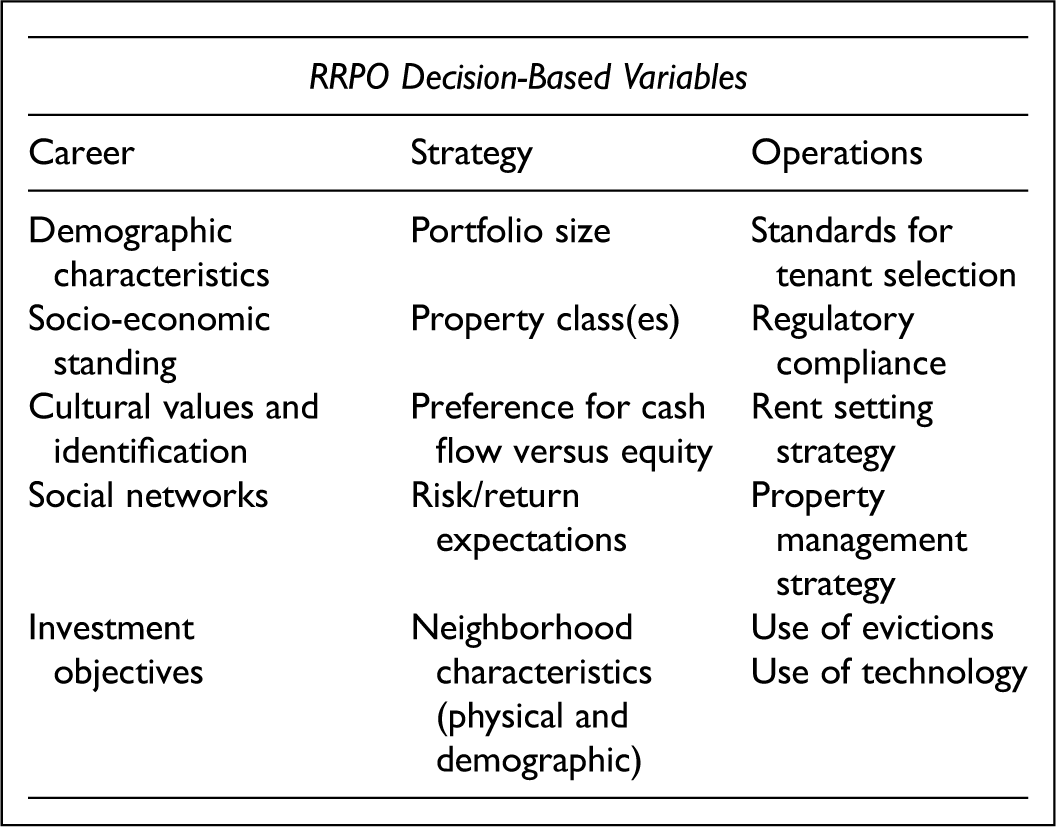

The field of noninstitutional investors is complex. Typologies intended to influence practice require evidence and testing. Although our goal with this paper was not to develop a typology ourselves, we have identified the following factors that we suggest as a starting point for developing new RRPO typologies:

Developing useful typologies requires a research agenda that will generate this to target desired outcomes and consider consequences, intended and otherwise, within the interrelated web of decisions that an RRPO may pursue. In the remainder of this section we propose research agendas for each of the decision-making areas that can contribute to the development of RRPO typologies.

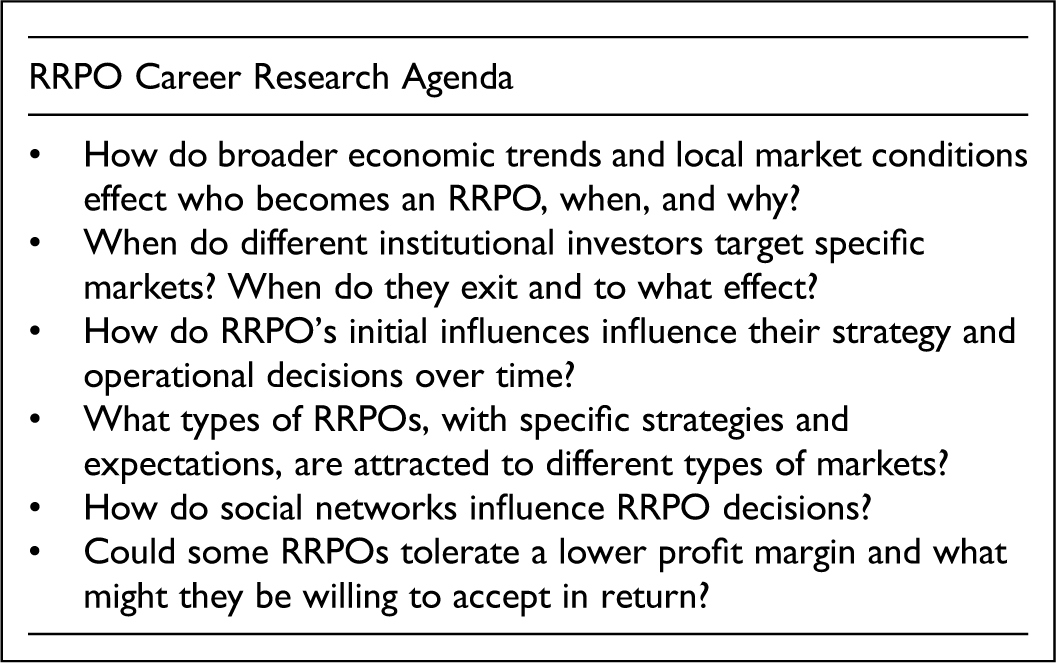

Research Agenda: RRPO Careers

The proposed research agenda for RRPO Career decisions is fundamentally about who, how, and when people and organizations become interested in rental property ownership. There has been significant foundational research in this area, but the next step is to put that research in the context of different markets. A more specific and granular understanding of RRPO types has the potential to help planners incentivize and partner with socially responsible RRPOs, which could fundamentally change the relationship between cities and RRPOs and redefine what is possible in a local housing system. Similarly, knowing more about RRPOs can help cities proactively regulate to protect communities against RRPOs with exploitative propensities through targeted policies that minimize unintended consequences.

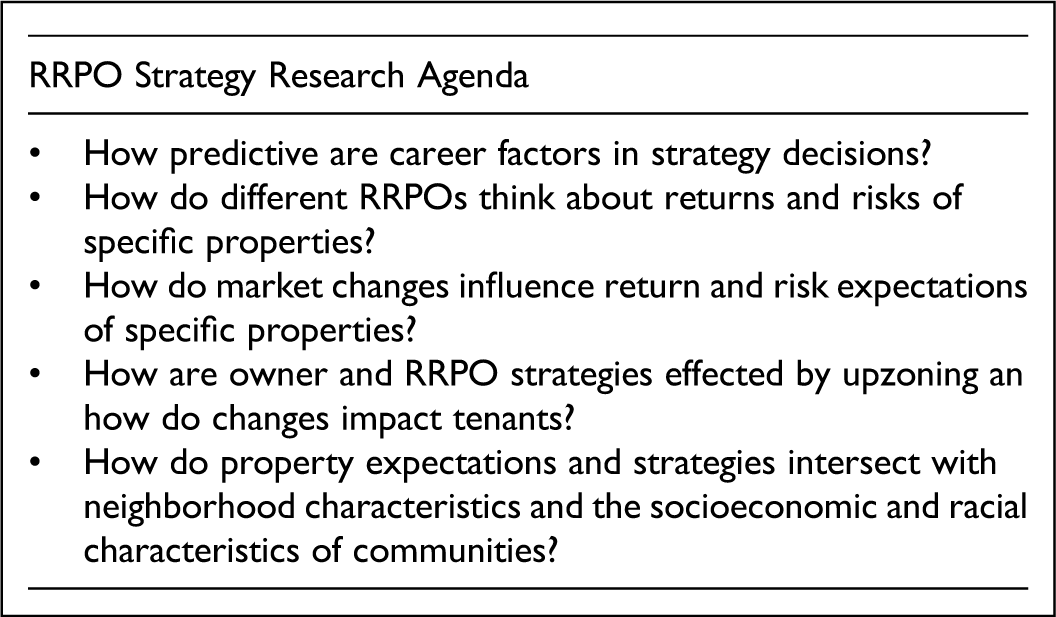

Research Agenda: RRPO Strategy

An RRPO research agenda organized around owners’ portfolio strategies can be especially helpful for planners to develop policies and programs that reflect an understanding of how RRPOs view their businesses, differentiate between categories of RRPOs, and more effectively manage dynamic local markets. This will be particularly useful for policymakers responding to economic shocks and natural disasters, which can have uneven impacts across neighborhoods (Dewar, Seymour and Druță 2015; Immergluck 2010) and drive opportunistic speculation (Brand 2015; Woods 2017). Local distressed property remediation programs must deal with complex ownership issues that require coordination between multiple levels of government and a diverse private sector (Bacher and Williams 2014). Prospective RRPOs can be incentivized to invest, but as Immergluck (2010) observed with the Neighborhood Stabilization Program, investors and speculators move faster than government programs. Ideally, governments should predetermine the RRPOs they would like to incentivize to pursue these opportunities when the time arises and prepare agile policies that can move closer to the speed of markets.

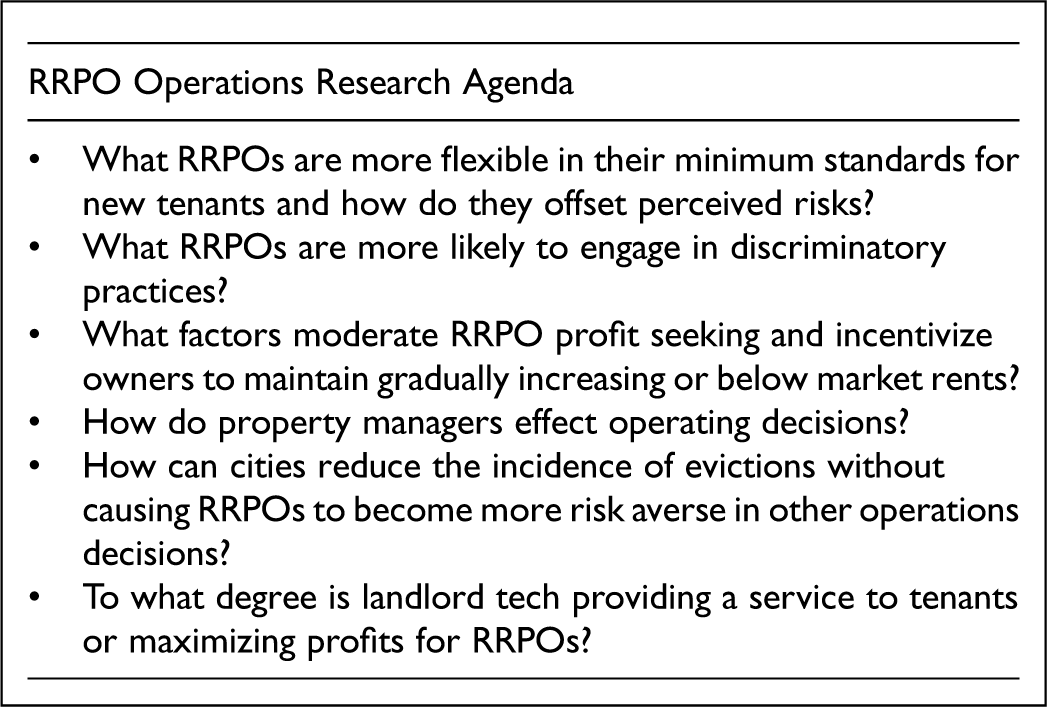

Research Agenda: RRPO Operations

An RRPO research agenda supporting an operations-decision taxonomy may provide the most immediately actionable information for planners and programs that connect people facing housing barriers to flexible, but responsible RRPOs, and ensure that those tenants maintain their access to long-term, stable housing. This can be done through carefully designed incentives and support programs tailored to the RRPO and tenant. Knowing more about RRPO decisions around tenant selection and how those decisions serve their goals would be invaluable insights for such incentive programs.

Operations decisions may also result in tenant discrimination. Without resources and political will to enforce housing protections, instances of discrimination and harassment will persist, particularly for those with the least power in the tightest markets. Experts have criticized HUD's failure to address fair housing concerns (Taylor 2019), but state and local governments also have the capacity to enforce fair housing laws. But such enforcement requires knowledge of the types of RRPOs that are most likely to offend (Bullock, Lamb and Wilk 2018). The information needed to develop decision-based typologies and, potentially, predictive models highlights the opportunity for more interdisciplinary collaboration between planning and fields such as economics, finance, and data science.

Scholars could also use these improved RRPO typologies to examine how RRPO behavior changes over time. Technology will continue to present new opportunities and challenges that planners may need to manage, particularly as some individual RRPOs are influenced by aggressive investment advice, are rapidly “formalizing” their business practices, and may come to closely mirror the depersonalized behaviors of institutional owners (Messamore 2023). Disasters can reveal deeply rooted structural issues, and such inequities may manifest in the operations-related decisions that RRPOs make postdisaster. For example, Latinos experienced unique discrimination after hurricane Katrina (Weil 2009; Woods 2017), immigrants have been excluded from postdisaster housing and shelter (Weil 2009), and tenants not listed on leases may be excluded from recovery assistance (Mueller et al. 2011). The foreclosure crisis compounded inequality and segregation (Rugh and Massey 2010), while the COVID-19 pandemic resulted in differences in rental market trends based on neighborhoods’ racial characteristics (Kuk et al. 2021). Understanding these patterns and their sources gives planners the best chance to improve stability for the most frequently exploited and marginalized residents.

In the development of new typologies, it is important for planning scholars to carefully consider how and if they will use existing typologies. For example, researchers should be deliberate when treating institutional and noninstitutional owners as clearly delineated groups and not assume that they have wholly distinct patterns of behavior when it comes to operational decisions. Unexamined assumptions and oversimplifications can lead planning scholars miss significant variables and risk undermining efforts to foster rental housing stability. Institutional RRPOs are not a monolithic group either (Nethercote 2020), and factors like ownership structure, dependence on local intermediaries, and general and local economic conditions may lead some types of institutional owners to pursue long-term strategies that depend on reputation just as much if not more than a “mom-and-pop” operation does. Similarly, galvanized by aggressive investment advice and enabled with advertising, screening, and management technologies, noninstitutional owners may be as likely as institutional RRPOs to make decisions based on aggressive financial strategies, risk calculations, and opportunity costs. Researchers should help provide valuable insights that address relevant questions for practitioners; the problems practitioners need to address are probably determent by factors other than RRPO size and ownership.

Conclusion

Planners must work with RRPOs. However, the relationship between public entities and owners, particularly individual RRPOs, is often difficult and adversarial. The possibility of creating more productive relationships depends on a very practical question: How well do planners know the RRPOs operating within their jurisdictions? RRPOs are a diffuse and diverse group and may have little reason or motivation to interact with local governments beyond necessary tax payments, licensing fees, or inspections. Research on effective strategies to identify RRPOs most likely to benefit from local partnerships, foster communication, and develop tools like rental registries that support housing goals would have immediate implications for local planners and others involved in managing local rental housing markets (Greenlee 2014; Mallach 2007). Local governments and planners need new strategies that promote urban resiliency within the current economic and political context and that help tenants who are renting in the private market attain and maintain stable housing. We argue that reaching those objectives begins with a better understanding of who owns rental properties. A fuller understanding of RRPOs’ career, strategy, and operational decisions would give planners a more effective framework to develop policy, guide effective implementation, and manage housing outcomes.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Science Foundation (grant number NSF 2139816, RAPID NSF 2050264).