Abstract

Radiology is among the most capital-intensive specialities in healthcare, relying on high-cost imaging equipment, complex information technology infrastructure, long-term vendor contracts, and increasingly, artificial intelligence systems. Decisions about these resources shape patient access, diagnostic quality, workforce sustainability, and the long-term resilience of imaging services. Despite this, most radiologists receive little formal training in key financial concepts, and financial decision-making is often perceived as external to clinical practice. This article positions foundational financial reasoning as a core competency for radiologists, introducing key concepts from financial management, including: liquidity, leverage, efficiency, profitability, risk, and capital budgeting, and translating them into clinically meaningful frameworks relevant to radiology. Using practical examples and mini-cases, this article demonstrates how commonly used financial ratios and investment appraisal tools can be interpreted as diagnostic tools for organisational health rather than abstract accounting exercises. Interpreting financial metrics as an integrated system rather than as isolated indicators is important in demonstrating how short-term resilience, long-term commitments, operational efficiency, and sustainability interact in real-world radiology decision-making. Extending this framework to the measurement of value beyond volume and revenue, highlighting the potential role of patient-reported outcome measures (PROMs), as well as the relevance of implementation science and change management, is important in ensuring that financially sound investments deliver meaningful clinical impact. By equipping radiologists with a shared language and conceptual toolkit for engaging with financial decisions, this article aims to strengthen clinical leadership, support transparent resource allocation, and promote resilient, high-value imaging services aligned with patient-centred care.

Introduction

Radiology is among the most capital-intensive specialities in modern medicine. The delivery of imaging services depends on high-cost diagnostic equipment, sophisticated information technology (IT) infrastructure, long-term vendor and maintenance contracts, and increasingly, artificial intelligence (AI) systems that promise improvements in efficiency, quality, and safety. 1 These financial commitments fundamentally shape how radiology is practiced, who has access to imaging, how work is distributed, and how sustainable departments are over time. Despite this, radiology literature has largely focused on operational efficiency, technological innovation, and clinical outcomes, with comparatively little attention paid to financial reasoning and decision-making among radiologists themselves.

Financial decision-making is often discussed implicitly, through debates about productivity, backlog, or AI adoption, with relatively less attention invested in explicitly equipping radiologists with the conceptual tools needed to engage meaningfully with these decisions. As a result, many of the most consequential choices affecting radiology practice are often experienced by clinicians as externally imposed constraints rather than as strategic decisions in which they have informed agency. This separation between clinical expertise and financial reasoning is increasingly challenging in modern radiology practice. Financial decisions directly influence patient access to imaging, turnaround times, diagnostic quality, radiologist workload, and professional autonomy. When radiologists lack the language and frameworks to interrogate these decisions, they risk being excluded from discussions that shape the future of the speciality. This review offers a framework for bridging clinical expertise and financial reasoning, outlining foundational concepts in finance that can strengthen radiology leadership and advance patient-centred care.

Limitations of Traditional Radiology Metrics

Radiology performance is commonly evaluated using operational metrics such as imaging volume, relative value units (RVUs), turnaround time, and report counts. 2 These measures are familiar, intuitive, and closely tied to day-to-day clinical work. However, they provide only a partial picture of departmental health and sustainability. A department may demonstrate impressive throughput and still struggle to justify new hires, replace ageing equipment, or invest in innovation. Conversely, periods of apparent inefficiency may coexist with long-term financial resilience.

The limitation of traditional metrics lies in their focus on activity rather than sustainability. Volume and productivity capture how much work is done, but not whether that work creates sufficient value to support future investment, absorb risk, or respond to unexpected shocks. Financial frameworks complement operational metrics by focusing on relationships between resources, obligations, and outcomes over time. They help answer questions such as whether a department can withstand short-term disruptions, whether its long-term commitments are manageable, and whether current practices are eroding or strengthening future capacity. For radiologists, understanding these frameworks can help to contextualise clinical metrics. Understanding key concepts in finance can allow radiologists to interpret operational data within a broader strategic landscape and to engage more effectively in discussions about resource allocation, innovation, and system-level change.

Financial Ratios: Interpreting the Financial Health of Radiology Departments

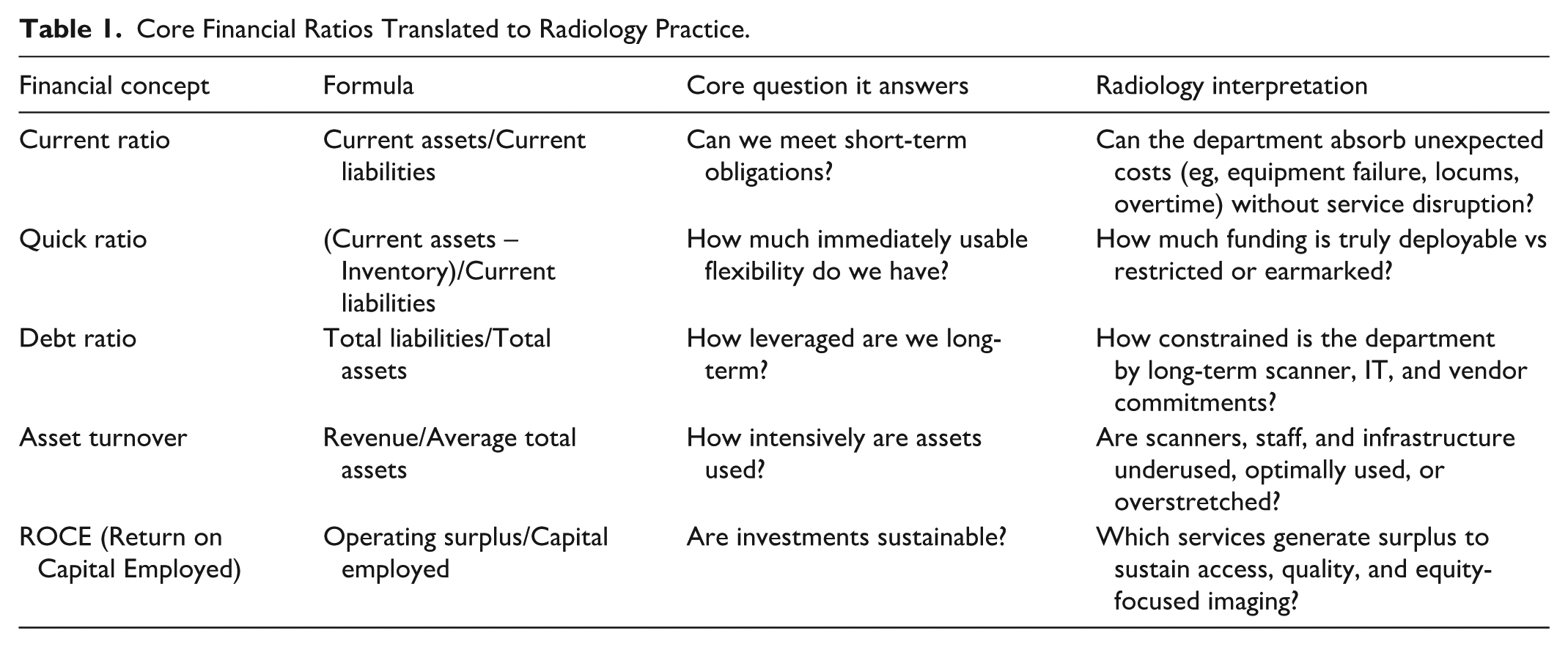

Financial ratios describe relationships between different elements of an organisation’s finances and allow complex financial statements to be interpreted in a structured, comparative way. 3 Although these ratios originate in corporate finance, they are directly applicable to radiology departments when appropriately translated. Importantly, these ratios are tools for asking practical questions about resilience, risk, efficiency, and sustainability. Table 1 highlights key financial ratios and the lenses through which they can be used to examine clinical and operational questions.

Core Financial Ratios Translated to Radiology Practice.

Liquidity Ratios: Can the Department Absorb Short-Term Shock?

Liquidity ratios assess whether an organisation can meet short-term obligations using resources that are readily available. The most commonly used liquidity measure is the current ratio, 4 calculated as:

Each variable in this formula warrants careful interpretation in a radiology context. Current assets refer to resources that can realistically be accessed within approximately 1 year. At a departmental level, this may include allocated operating cash, short-term receivables linked to imaging activity, or discretionary reserves held within a service line budget. Importantly, not all nominal “assets” are equally usable; funds that are earmarked for specific programs or locked into institutional budgets may not be truly liquid. Current liabilities represent obligations that must be met within the same time horizon. For radiology departments, these commonly include equipment servicing contracts, maintenance fees, software licensing costs, overtime payments, locum coverage, and other short-term staffing expenses.

Conceptually, the current ratio answers a simple question: if the department were faced with an unexpected disruption over the next year, could it meet its obligations without emergency intervention? A ratio greater than 1 suggests that short-term resources exceed short-term commitments, while a ratio below 1 signals potential vulnerability.

Consider an example of a radiology department operating at high clinical volume but with a low current ratio. If a CT scanner fails unexpectedly and requires urgent servicing, the department may be forced into reactive decisions such as delaying elective studies, restricting overtime, or diverting cases to external providers. In this way, weak liquidity can translate directly into access and workflow challenges, despite strong apparent productivity.

A more conservative liquidity measure is the quick ratio, 4 calculated as:

Although radiology departments do not hold physical inventory in the traditional sense, the conceptual value of this ratio remains important. It encourages leaders to exclude resources that are not immediately deployable. In practice, departments can approximate a “quick” measure by subtracting restricted or earmarked funds that cannot be rapidly reallocated. From an implementation standpoint, liquidity analysis is most useful when tracked longitudinally. Quarterly review of departmental-level liquidity trends, in collaboration with hospital finance teams, can help identify emerging fragility before it manifests as service disruption.

Leverage Ratios: Understanding Long-Term Commitments

Leverage ratios describe the extent to which an organisation relies on long-term obligations to finance its assets. A commonly used measure is the debt ratio, 5 calculated as:

Here, total liabilities include both short- and long-term obligations. In radiology, this often encompasses financed scanners, long-term leasing arrangements, PACS and RIS licensing agreements, extended service contracts, and IT infrastructure commitments. Total assets include physical imaging equipment, digital systems, and other resources required to deliver imaging services. The debt ratio, therefore, reflects how much of a department’s asset base is financed through obligations rather than owned outright. A higher ratio indicates greater leverage and, consequently, greater sensitivity to changes in demand, reimbursement structures, or institutional policy.

High leverage is not uncommon in radiology and is not inherently problematic. It often reflects strategic investment in advanced technology. 6 However, leverage can reduce flexibility. For example, a department that has recently expanded its scanner fleet through long-term leases may find itself constrained if referral patterns shift or if staffing shortages limit utilisation. Fixed obligations remain even when clinical demand fluctuates. Understanding leverage allows radiologists to engage more thoughtfully in capital planning discussions. Rather than viewing equipment acquisitions as isolated decisions, radiologists can consider how cumulative obligations affect long-term resilience and risk tolerance, and how contract structure (duration, escalation clauses, service guarantees) influences the department’s ability to adapt.

Efficiency Ratios: Are Assets Being Used Well?

Efficiency ratios assess how effectively assets are used to generate output. One commonly used measure is the asset turnover ratio, 7 calculated as:

In this formula, revenue represents income generated by imaging services over a defined period, while average total assets reflect the mean value of the equipment, infrastructure, and systems employed during that same period. The ratio, therefore, describes how intensively assets are being used to produce clinical and financial output.

In radiology, asset turnover encourages a shift away from raw volume towards utilisation quality. A low ratio may reflect underutilised scanners, inefficient scheduling, excessive downtime, or workflow bottlenecks. Conversely, an unusually high ratio may indicate overuse of assets, with downstream consequences such as accelerated equipment wear, increased maintenance costs, and staff burnout.

Operational metrics such as scanner utilisation rate, calculated as actual operating hours divided by available operating hours, provide essential context. Used together, financial and operational measures help distinguish between true capacity limitations and inefficiencies that could be addressed through workflow redesign rather than capital expansion.

A practical case is a department requesting a new MRI scanner because waitlists are increasing. An efficiency analysis might reveal that the existing scanner is idle during certain blocks due to staffing gaps, that cancellations are high due to scheduling practices, or that protocol variability creates avoidable delays. In such instances, improving utilisation may create “virtual capacity” without immediate capital expenditure.

Departments can implement efficiency analysis by combining financial data with operational metrics, such as scanner hours, cancellation rates, maintenance downtime, protocol turnaround, and the distribution of case complexity across the day. This integrated view helps identify whether perceived capacity constraints are financial, operational, or both, and whether the most value-generating intervention is new equipment or better system design.

Profitability Ratios: Understanding Sustainability and Cross-Subsidisation

Profitability ratios examine how revenues relate to costs and capital employed, providing insight into sustainability rather than profit maximisation. One widely used measure is return on capital employed (ROCE) 8 :

In this formula, operating surplus represents the excess of operating income over operating costs before financing considerations. In practice, this is the amount available to reinvest in service improvement, workforce support, equipment replacement, and quality initiatives. Capital employed includes long-term assets such as scanners and IT systems, as well as working capital required to run the service. ROCE therefore describes how effectively invested resources are generating surplus that can be reinvested to sustain or improve services. In radiology, ROCE is particularly valuable for understanding cross-subsidisation. Some modalities or service lines may generate a surplus that supports lower-margin but clinically essential activities.

A practical case is a department considering expansion of a lower-margin imaging pathway to improve access (eg, community outreach imaging or service coverage for underserved populations). Understanding ROCE allows leaders to make such decisions transparently, recognising that surplus from other areas may be required to sustain the expansion, and that the rationale may be equity, quality, or system stewardship rather than short-term margin. In publicly funded systems, such as Canada’s, this framing is especially important. Profitability metrics should not be used to justify “only” high-margin imaging; instead, they can illuminate how to preserve comprehensive access while remaining financially sustainable.

Risk, Return, and Portfolio Thinking in Radiology

Many strategic choices in radiology resemble investment decisions, even if they are not explicitly framed as such. Decisions to adopt AI tools, expand subspeciality services, or enter teleradiology arrangements all involve trade-offs between expected benefit and uncertainty. In finance, expected return is often calculated as the average of possible outcomes weighted by their probability. While radiologists rarely calculate expected returns numerically, the concept remains important. For example, an AI triage tool may be expected to reduce reporting time by an average of 10%, but actual outcomes may vary widely depending on case mix and workflow integration. Risk can be quantified using measures such as variance or standard deviation, which describe how widely outcomes vary around the average. Greater variability implies greater uncertainty. In radiology, high variability may manifest as unpredictable effects on workload, downstream imaging, or diagnostic confidence.

Portfolio thinking emphasises that combining activities with different risk profiles can reduce overall volatility. 9 For example, a department might pilot a high-risk AI innovation while maintaining stable core services that generate predictable value. Radiologists who understand these principles can advocate for staged adoption and diversification rather than all-or-nothing investment decisions.

Capital Budgeting: Making Sense of Major Radiology Investments

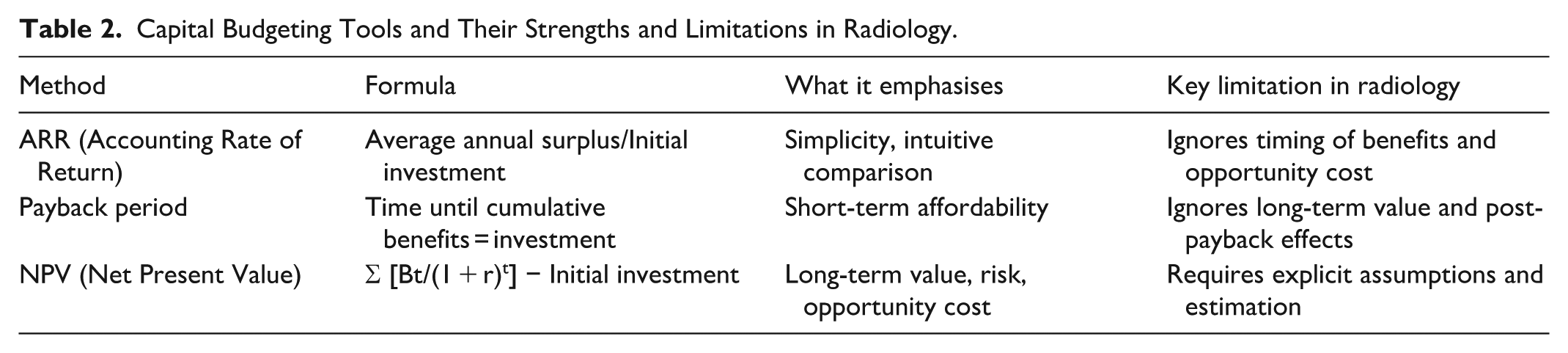

Capital budgeting refers to methods used to evaluate long-term investments by comparing their costs and benefits over time. 10 These tools are particularly relevant in radiology, where decisions about scanners, AI systems, and digital infrastructure shape clinical practice for many years. Capital budgeting frameworks are intended to make assumptions explicit, compare alternatives transparently, and understand the consequences of uncertainty versus produce exact predictions. Table 2 compares commonly used capital budgeting methods, illustrating how each emphasises different dimensions of value and risk. In radiology, these tools are most informative when used comparatively rather than as standalone decision rules.

Capital Budgeting Tools and Their Strengths and Limitations in Radiology.

The accounting rate of return (ARR) 11 is calculated as:

In this formula, average annual accounting surplus refers to the expected yearly excess of revenues over operating costs attributable to the investment, while initial investment includes purchase price, installation, training, and any upfront integration costs. ARR is intuitive and easy to compute, which explains its frequent use in healthcare settings. However, ARR treats all future surpluses as equivalent regardless of when they occur, and ignores opportunity cost. In radiology, this can bias decisions towards projects with early but modest gains while undervaluing investments whose benefits accrue more gradually, such as workflow redesign or staff development.

The payback period measures how long it takes for cumulative net benefits to equal the initial investment. 12 It is calculated by summing expected annual net benefits until the original cost is recovered. Payback is often appealing in resource-constrained systems because it emphasises short-term affordability. However, it assumes that benefits beyond the payback point are irrelevant and provides no insight into what happens after cost recovery. A technology that pays for itself quickly but generates limited long-term value may therefore appear preferable to one that delivers sustained clinical and operational benefits over a longer horizon.

The net present value (NPV) framework 13 addresses these limitations by explicitly incorporating time and uncertainty. NPV is calculated as:

In this formula, Bt represents the net benefit generated in year t, t represents the year in which the benefit occurs, and r is the discount rate, which reflects opportunity cost and risk. In practical terms, the discount rate reflects opportunity cost, recognising that resources committed to one project cannot be used elsewhere and that benefits realised in the future are inherently less certain than those realised today. Even when exact numbers are debated, the structure of NPV encourages transparency about assumptions and trade-offs.

For radiology departments, Bt may include increased throughput, reduced overtime costs, avoided outsourcing, improved diagnostic confidence, or reduced downstream testing. Importantly, it may also include non-financial benefits, such as improved patient outcomes/experience or reduced clinician burnout, if these are explicitly recognised, even if they are not monetised directly. NPV forces assumptions to be stated clearly. For example, it requires explicit estimates of utilisation, adoption rates, staffing impact, and durability of benefits. Sensitivity analysis can then test how robust conclusions are to changes in these assumptions, aligning financial reasoning with implementation realities.

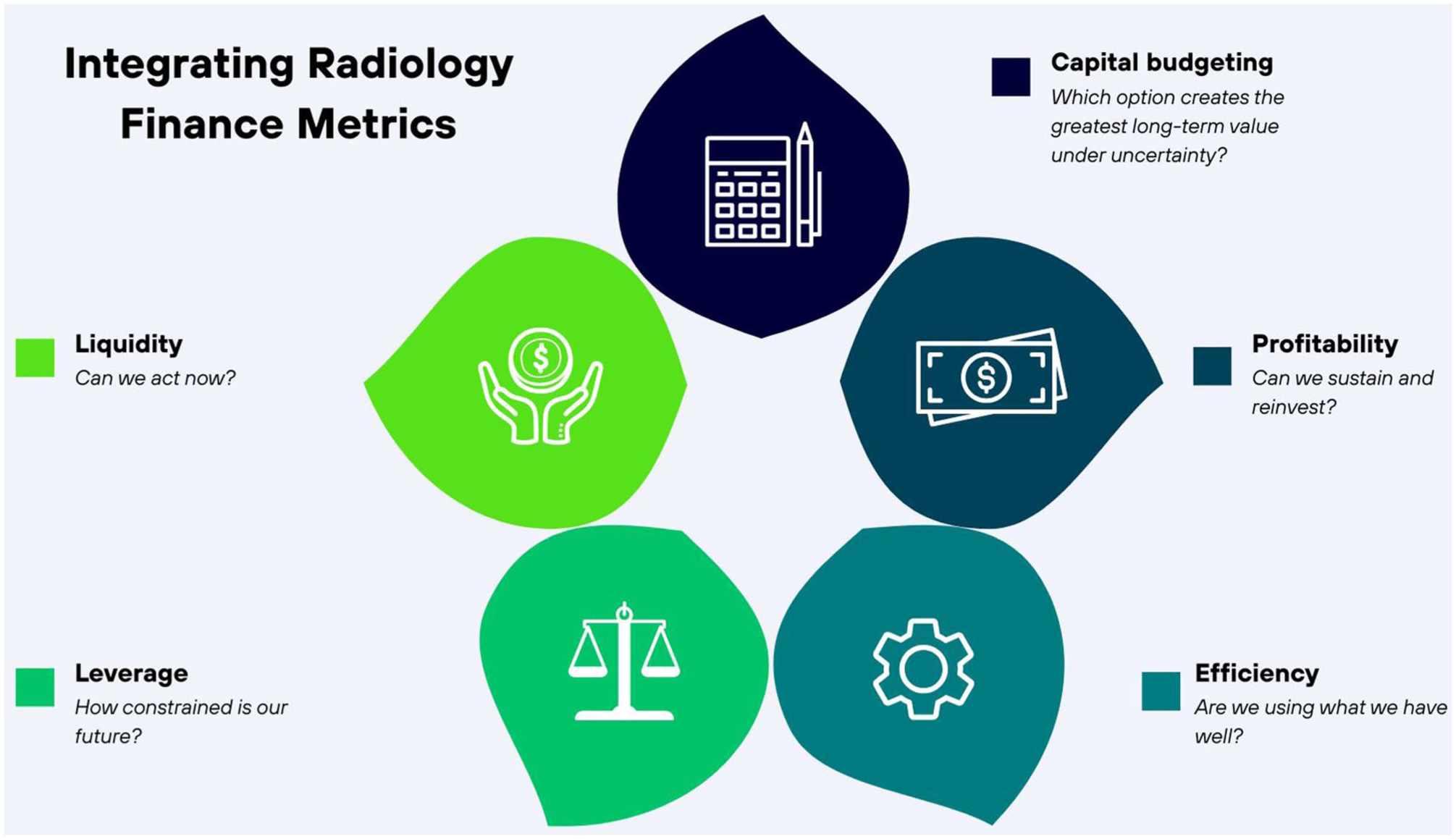

Interpreting Financial Metrics Together: From Ratios to Decisions

A critical limitation of financial analysis is the tendency to interpret ratios in isolation. In practice, financial metrics are most informative when considered together, as they describe different dimensions of the same underlying system. Interpreted as a set, these ratios enable radiologists and leaders distinguish between short-term fragility and long-term risk, between capacity problems and efficiency problems, and between apparent growth and sustainable growth. One useful way to think about the ratios is that they ask different versions of the same question: what can we commit to, and what can we sustain? Liquidity ratios indicate the department’s short-term resilience, whether the department can absorb disruptions without immediately compromising service delivery. Leverage ratios describe long-term commitments and the degree to which future flexibility has been traded for present capability. Efficiency ratios examine whether existing resources are being used well enough to justify additional investment. Profitability ratios describe whether the department is generating sufficient surplus to maintain and improve services over time. Rather than sequential steps, these dimensions interact continuously (Figure 1) and should be interpreted together when evaluating strategic decisions.

Integrating radiology finance metrics.

Forecasting and Sensitivity Analysis: Planning for an Uncertain Future

Radiology operates in an environment characterised by demand volatility, workforce shortages, 14 technological change, and evolving policy. 15 Financial planning tools, such as forecasting and sensitivity analysis, provide structured ways to navigate this uncertainty. Forecasting involves projecting future activity based on historical trends and anticipated changes. 16 In radiology, this includes imaging demand, referral patterns, and staffing requirements. Inaccurate forecasting can lead to overcapacity, underinvestment, or chronic backlog. Radiologists who understand forecasting principles can contribute clinical insight that improves the realism of projections and highlights emerging risks.

Sensitivity analysis examines how outcomes change when assumptions vary. 17 Rather than relying on single “best-case” projections, sensitivity analysis asks what happens if key assumptions are wrong. For example, what are the consequences if imaging demand increases faster than anticipated, or if an AI tool delivers smaller efficiency gains than promised? These questions transform abstract uncertainty into concrete scenarios, improving the quality of strategic decision-making.

Consequences of Financial Blind Spots in Radiology

In many settings, radiologists are not always present in the forums where key financial decisions are made that impact the medical imaging department. When financial reasoning is conducted primarily outside clinical spaces, decisions can be experienced by radiologists as opaque or externally imposed, even when they have the expertise to engage meaningfully. This structural separation can erode trust, reduce morale, and constrain clinicians’ ability to advocate effectively for patients, colleagues, and service quality. 18 It also increases the risk that innovative initiatives, incentive structures, or workload models are designed without sufficient clinical insight, leading to misalignment between financial objectives and day-to-day practice. Conversely, when radiologists are meaningfully included in financial discussions alongside healthcare administrators and system leaders, clinical and financial perspectives can be integrated rather than siloed. Radiologists bring contextual understanding of workflow, diagnostic complexity, and patient impact that helps surface implicit assumptions, clarify trade-offs, and anticipate unintended consequences of financial decisions. This shared deliberation supports investments that are operationally feasible, clinically appropriate, and aligned with patient-centred care. In this setting, financial decision-making becomes a form of collaborative stewardship, strengthening professional agency and shared governance rather than placing clinical values in tension with administrative priorities.

Measuring Value in Radiology: Beyond Volume and Revenue

A central limitation of many financial discussions in radiology is the assumption that value can be inferred from volume, revenue, or cost containment alone. While these metrics are important, they fail to capture whether imaging services meaningfully improve patient outcomes, experience, or downstream care. In finance, value is commonly defined as the difference between benefits generated and resources consumed over time. Translating this concept to healthcare requires expanding the definition of benefit. In radiology, benefits include financial returns, alongside diagnostic confidence, reduced uncertainty, avoidance of unnecessary testing, and patient-centred outcomes such as reassurance or functional improvement. Patient-reported outcome measures (PROMs) offer a structured way to capture these benefits directly from patients. 19 Although PROMs are more commonly associated with therapeutic interventions, they are increasingly relevant to diagnostic pathways. For example, timely imaging that reduces diagnostic delay may substantially improve patient-reported anxiety, quality of life, and influence treatment decisions. When such outcomes are excluded from financial evaluation, radiology investments that generate substantial patient value risk being systematically undervalued. Financial tools such as net present value can, in principle, accommodate broader definitions of benefit if these outcomes are explicitly recognised. While not all benefits can be monetised, acknowledging their existence changes the framing of investment decisions from narrow cost recovery to holistic value creation.

Implementation Science and Change Management: Why Financially Sound Ideas Still Fail

Even when a radiology investment appears clinically and financially attractive on paper, successful implementation is not guaranteed. Implementation science examines the factors that influence whether evidence-based interventions are adopted, integrated, and sustained in real-world settings. 20 From a financial perspective, failed or partial implementation represents value leakage: resources are expended without the anticipated return.

Consider a department that adopts an AI decision-support tool with strong evidence of efficacy. If radiologists do not trust the tool, if workflows are disrupted, or if training is inadequate, utilisation may remain low. In such cases, financial projections based on full adoption will overestimate realised value. Change management frameworks emphasise the importance of engagement, alignment, and culture in mitigating these risks. 15

Financial reasoning strengthens implementation by encouraging realistic assumptions and contingency planning. Sensitivity analysis can be used to model how delays, partial uptake, or workflow friction affect projected outcomes. For example, explicitly examining how net present value changes if adoption reaches only 50% rather than 100% helps align financial planning with implementation realities. Radiologists who understand these dynamics are better positioned to advocate for staged rollouts, pilot evaluations, and iterative refinement. Such approaches reduce downside risk, support learning, and increase the likelihood that investments deliver meaningful and sustained value.

Mini-Case 1: Scanner Replacement Versus Workflow Redesign

A radiology department is experiencing prolonged CT wait times and is considering purchasing a new scanner. Efficiency analysis reveals that asset turnover is high, suggesting heavy utilisation, but a closer operational review shows that scanner downtime due to staffing gaps and protocol variability is significant. Liquidity analysis indicates limited short-term flexibility, while leverage ratios show substantial existing long-term commitments from prior equipment leases. Interpreted together, these metrics suggest that immediate capital expansion may exacerbate financial risk without addressing the underlying problem. A workflow redesign: standardising protocols, adjusting staffing patterns, and reducing cancellations, may improve utilisation and access without increasing leverage. In this case, integrated ratio analysis supports a decision to defer capital expenditure and invest instead in operational improvement.

Mini-Case 2: AI Decision Support Adoption

A radiology department is evaluating an AI decision-support tool intended to reduce reporting time. Projected ARR appears favourable, driven by expected efficiency gains. However, liquidity analysis shows that upfront implementation costs would strain short-term resources, while leverage ratios indicate limited tolerance for additional long-term commitments. Sensitivity analysis reveals that if adoption reaches only 50% rather than the projected 90%, the NPV becomes marginal. Considering these metrics together reframes the decision. Rather than full-scale adoption, a staged pilot with defined evaluation milestones may reduce downside risk, preserve liquidity, and generate real-world data to refine assumptions. Here, integrated financial reasoning aligns with implementation science principles, supporting cautious adoption rather than binary approval or rejection.

These mini-cases illustrate how financial ratios, capital budgeting tools, and operational insight work together to inform decisions. No single metric determines the correct course of action. Instead, value emerges from understanding how short-term resilience, long-term commitment, efficiency, and sustainability interact within the clinical and organisational context.

Interpreting financial metrics as an integrated system allows radiologists to move beyond binary judgements of “good” or “bad” performance. It supports nuanced discussion about trade-offs, priorities, and alignment with institutional values such as access, safety, quality, and equity. Viewed collectively, these tools support strategic sense-making rather than narrow, calculation-driven decision-making.

A Call to Action

Radiology as a speciality is fortunate to have many clinicians with substantial financial knowledge, particularly among those involved in leadership, practice management, and system-level work. At the same time, exposure to formal financial frameworks remains variable across training pathways and practice settings, and opportunities to apply this expertise consistently in strategic decision-making are uneven. As a result, financial considerations that shape radiology services are often discussed using fragmented assumptions or discipline-specific language rather than shared conceptual models. This article focuses on articulating a common framework that can support clearer interpretation, dialogue, and collaboration across clinical and administrative domains. When radiologists share accessible tools for reasoning about liquidity, risk, efficiency, and value, they are better positioned to engage meaningfully in decisions about resource allocation, innovation, and service design, regardless of their prior financial experience. Embedding these concepts within radiology education, mentorship, and continuing professional development can help normalise their use and ensure that financial reasoning is integrated with outcome measurement, implementation science, and change management. Such integration allows investments to be evaluated based on feasibility, equity, and real-world clinical impact, in addition to projected financial performance. In contemporary radiology practice, financial and clinical decisions are inseparable. Radiologists who can situate financial considerations within broader discussions of value, outcomes, and system design are better equipped to advocate for patients, support their colleagues, and contribute constructively to the future direction of the speciality.

Footnotes

Author Contributions

RK was involved with conceptualising the study. RK led the writing of the manuscript. MP was involved with critical revision of the manuscript. All co-authors approve the submission.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.