Abstract

Professional planners working in the private sector intersect with a complex sphere of business interests. Management consultants have a growing influence in many organizations, including private sector planning firms. Using a mixed-method approach to examine the strategies and priorities of management consultants, I find that management consultants view the “value” of planning as opening the door to future contracts and selling firm services. This has implications for understanding how practitioners reconcile professional values (such as autonomy, neutrality, and protection of the public interest) with market imperatives, and for the profession as one driven by societal, rather than entrepreneurial goals.

Introduction

Research on planning practice has often understood it from the perspective of planners themselves (e.g., Lauria and Long 2017; Read and Leland 2011; Schön 1983) or the impact on the communities they serve. Yet for planners working in the private sector, the business realm introduces a more complex range of influences on their work, such as firm executives, management consultants, and shareholders. Private sector planning has experienced significant changes, both as an industry and in its relationship with public sector clients. At the firm level, increasing consolidation through mergers and acquisitions (M&A) has resulted in very large, diverse companies, as firms seek to capitalize on the opportunity to expand market shares (Linovski 2019; Raco 2018). Public sector clients of planning have also experienced significant changes in the face of austerity measures, leading to increasing reliance on private sector firms in many jurisdictions (Parker, Street, and Wargent 2018; Steele 2009; Wargent, Parker, and Street 2020).

Alongside these changes in private sector planning, there has been outsized growth in the management consultant industry, influencing a wide variety of both public and private sector organizations, and creating implications for society as a whole (Canato and Giangreco 2011; Hurl 2018; Kipping and Clark 2012; Vogelpohl and Klemp 2018). While planning consultant firms provide advice on planning issues, management consultants provide advice on the business of firms, such as organizational strategy, firm valuation, and ownership models. The large management consultant firms (such as McKinsey, Deloitte, and Boston Consulting Group) are widely known, but there are also specialists that focus exclusively on architecture, engineering, and construction services (AEC) firms, marketing a “deep understanding of built environment” companies. 1 These consultants provide management strategies, advising on metrics and benchmarking, corporate re-organization, and business development to a variety of firm types. 2 While they have received little attention in planning scholarship, management consultants are influential in shaping the goals and strategies of both public and private sector organizations (Canato and Giangreco 2011; Cerruti, Tavoletti, and Grieco 2019), and particularly in diffusing discourses of value (Froud et al. 2000). The changing institutional context for private sector planning points to a need to understand the wider range of actors that intersect with the work of practitioners, especially given the potential for corporate strategies to re-shape professional practices (Allan, Faulconbridge, and Thomas 2019; Cushen 2013). The literature on the role and influence of management consultants raises important questions for understanding contemporary planning practice. This research fills that gap by addressing the following questions:

Through analyzing the perspectives, strategies, and expectations of AEC management consultants, I demonstrate that this industry has the potential to redefine planning practices in significant ways. As in other fields (Allan, Faulconbridge, and Thomas 2019; Alvehus and Spicer 2012; Cushen 2013), the focus on financial metrics—and assessing “success” by these fine-grained measures—can alter the work of professionals. Despite the widespread promotion of these metrics, management consultants themselves acknowledge that these can affect the work of planners in negative ways. Management consultants also promote tactics and strategies that not only are in conflict with professional codes of conduct but also raise new ethical issues for practitioners. The perspectives of management consultants on the “value” of planning offers insight into how the field could shift under both their influence and broader market changes. I find that as AEC firms are increasingly diverse in their service offerings, planning is largely valued for the potential to lead to other types of work. While planning contracts were described as relatively low value and low margin, planners were seen as particularly well-positioned to sell other firm services, such as high-value engineering and design services. Critically, the tactics suggested by consultants can be seen as at odds with long-held values in the planning field (such autonomy, neutrality, and protection of the public interest) and as a profession driven by public values, rather than entrepreneurial goals.

Context: Management Consultants and the Planning Profession

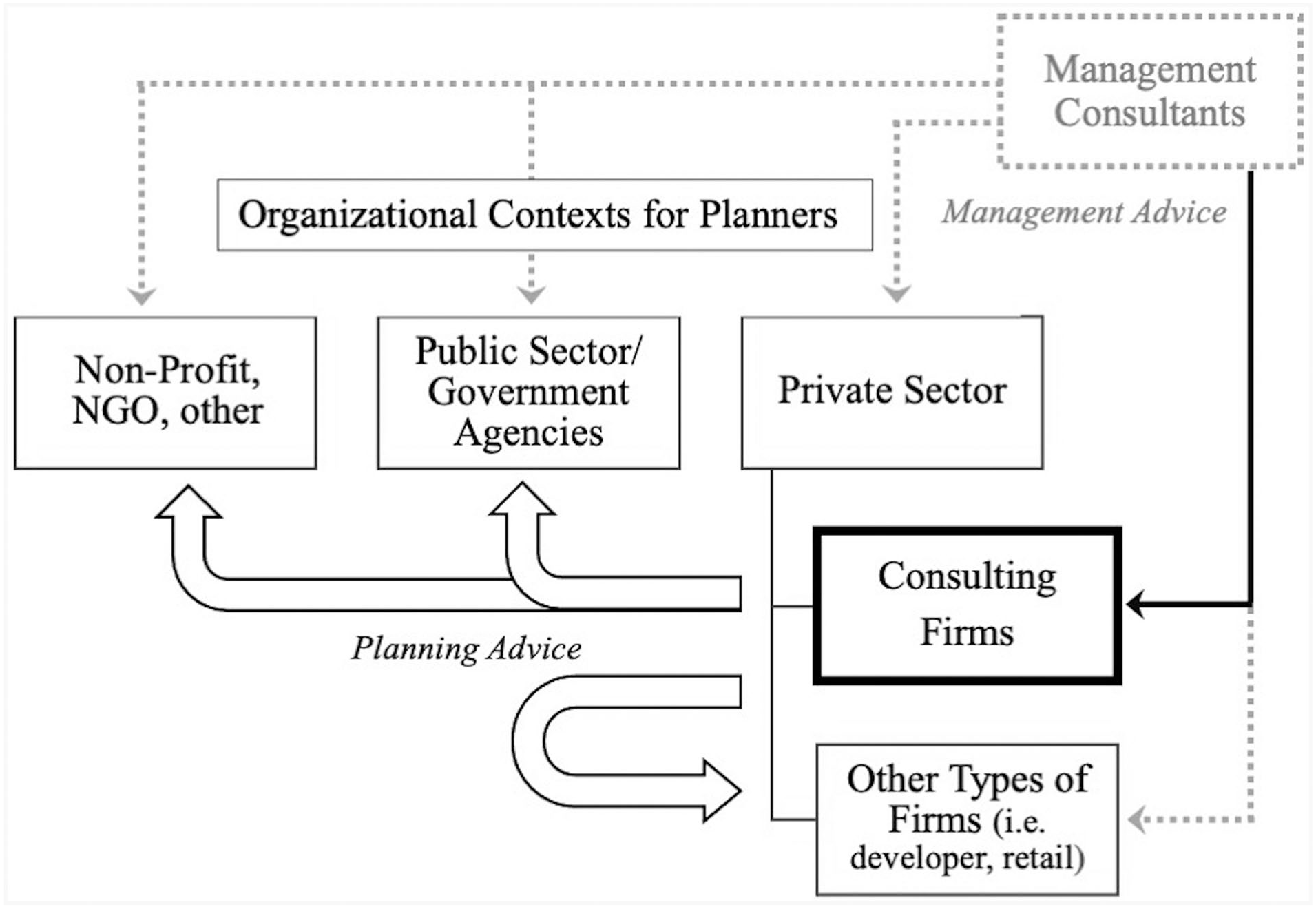

The focus of this research is on the interactions between management consultants and planning consultant firms. Planners work in a variety of organizational contexts (see Figure 1)—broadly broken down here as private sector, public sector/government, and non-profit/non-governmental organization (NGO). 3 Planners in the private sector may work for firms as “in house” planners—such as for housing developers or retailers—or for firms that provide planning advice to other agencies, referred to here as planning consultants. Planning consultant firms include large firms that offer a variety of services (such as AECOM, Stantec, and WSP, which all operate globally) and smaller ones with practice or regional specializations. I use the term planning consultant firm to refer to any private firm that includes planning services, although they may include other services (commonly engineering, architecture, and allied fields). Planning consultant firms provide advice to public sector, private sector, or other types of organizations, in a variety of forms. For example, planning consultants may develop a long-range plan for a municipality, provide advice on zoning and site planning for a housing developer, or create ridership projections for a transit agency. For firms that do not focus exclusively on planning work, services may be related. For example, firms may provide site planning for a new housing development, and then undertake the detailed engineering for roads and sewers if it is approved. Similarly, transportation planners may provide alternatives analysis for a new transportation project, and if the project proceeds, the firm may then do detailed engineering work.

Organizational contexts for planners and management consultants.

In contrast, management consultant firms provide advice on improving business functions, such as increasing efficiency, improving financial outcomes, or developing better leadership, also to a variety of organization types. Management consultants can be broad in their focus (such as KPMG, Deloitte, and McKinsey, which provide advice to both governments and firms) or focus on industries such as AEC (e.g., Zweig Group, Morrissey Goodale, AEC Advisors). The focus here is on the advice that these specialized management consultants provide to planning consulting firms. The management consulting firms studied here vary in scope, areas of expertise, and size but provide similar services in three main areas: (1) firm operations, (2) valuation and ownership transition (including for M&A), and (3) benchmarking and surveys. The first area is the broadest and includes advice on areas such as business development; proposal development, staff recruitment, and retention; project management; leadership skills; tax strategies; and marketing. The second area provides firm appraisals, assessing the value of companies for changes in ownership, including internal changes or for sale to external buyers, with a significant focus on mergers. Last, the benchmarking area is the creation of “state of the industry” surveys and reports, that include financial profiles, key performance indicators (KPIs), M&A activity, and analysis of industry trends. Some firms also provide assessments of major clients—primarily public sector—such as tailored guides on winning state and federal Department of Transportation contracts.

These services are marketed to firms of all sizes, including smaller (1–50 employees), mid-sized (50–500 employees), and large firms (500+) with national and international practices. While the costs for private consulting services are not known, the majority of firms studied here include relatively low-cost services such as training sessions ($40–$1,500), survey results ($400–$1,000), and conferences ($300–$1,400), as well as free documents, webinars, and podcasts, making them potentially accessible to even the smallest firms and disseminated widely.

Literature Review: Competing Logics for Private Sector Professionals

Professions have long been differentiated by the motivation to serve the public interest, rather than a focus on profit (Freidson 2001; Larson 1977). While there are debates as to how the public interest is defined and put into practice, it remains a cornerstone of the planning profession (Campbell and Marshall 2002; Johnson 2010; Lennon 2016), such as through professional codes of conduct (e.g., American Institute of Certified Planners 2016; Canadian Institute of Planners 2016). Although previous work on professional practice has often assumed planners as public employees, there has been a recent and substantial interest in the work of private sector planners and their interactions with the public interest (Loh and Norton 2015; Parker, Street, and Wargent 2018; Wargent, Parker, and Street 2020). Unlike public employees, planners in the private sector are responsible for the financial health of their firm, leading to different values, attitudes, and ethical concerns (Loh and Arroyo 2017; Read and Leland 2011). Complex flows between public and private sectors—exacerbated by public sector austerity and outsourcing—can introduce different concerns as planners attempt to balance entrepreneurial concerns and public interests (Parker et al. 2014; Raco 2018; Steele 2009). As Steele (2009, 200) notes, “the task of steering competitive market aspirations to work for the public interest appears to be an increasingly compromised and uncertain endeavour.” Conflicts between professional and corporate values may result in tensions for planners in practice. Planners in private practice face different ethical concerns than those in the public sector (Loh and Arroyo 2017), including ones not addressed by professional codes of conduct (Lauria and Long 2019; Linovski 2017).

Institutional contexts are important for how professionals approach and balance competing values and beliefs, often referred to as conflicts between professional logics and corporate, managerial, or entrepreneurial ones (Suddaby, Gendron, and Lam 2009). While professional logics traditionally rely on values such expertise and public service, practitioners must negotiate conflicting market logics that prioritize shareholder value, profitability, and efficiency (Adams 2020; Freidson 2001). The influence of profit-motivated demands on practitioners can operate through a variety of mechanisms, such as the corporate budgeting processes, which allow for financial narratives and capital interests to dominate the work of knowledge workers (Cushen 2013). These measures can have a direct impact on professional practices, through work intensification, job insecurity, discounting of professional expertise, and as a form of employee control, transforming how professionals spend their time and prioritize projects (Alvehus and Spicer 2012; Cushen 2013). The prioritization of financial metrics, leading to competition and job insecurity, can be seen as undermining professional logics or values in favor of career protection (Allan, Faulconbridge, and Thomas 2019). The influence of financial demands on professional practice should not be underestimated, as in some fields “professional work and careers in financialized organizations have been fundamentally reconfigured by the disciplinary effects of financial technologies deployed” (Allan, Faulconbridge, and Thomas 2019).

History and Role of Management Consultants

The management consultant industry, providing strategic and business advice to a wide variety of public and private sector organizations, has significantly expanded both in geography and scope (Canato and Giangreco 2011; Cerruti, Tavoletti, and Grieco 2019), affecting both greater numbers and types of organizations (Kipping and Clark 2012). The earliest forms of management consulting emerged in the late nineteenth century, and addressed industrial efficiency, led by engineers with experience on the “shop floor.” Management consultancy as an industry that focused on corporate organization emerged during the inter- and post-war period (Kipping 2002) with significant growth since the early 1990s (Canato and Giangreco 2011; Kipping and Clark 2012). The rise of management consulting has been tied to broader trends—such as the growth of capital mobility, increasing competitiveness, and turbulence of markets—and for public sector organizations, privatization and de-regulation (Fincham 1999). For firms, the use of consultants has also been linked to the increasing power of stakeholders, with pressures on managers to demonstrate the legitimacy of their business strategies (Engwall and Kipping 2013). Management consultants have also been associated with larger trends of financialization, having a role in codifying and promulgating many of the strategies associated with financialization and the “shareholder value revolution” (Froud et al. 2000; Knafo and Dutta 2020). Although there is an extensive literature on the evolution of management consulting—including the interactions with specific industries such as manufacturing, and the development of major firms such as McKinsey and Deloitte (Bryson 2002; Engwall and Kipping 2013; O’Mahoney and Sturdy 2016)—there is little analysis tracing its historical impact on planning firms or related policy. A notable exception is the work by Weber and O’Neill-Kohl (2013) exploring the role of real estate consultants as “bridging agents,” with significant impacts on redevelopment policy. 4

A key question for scholars has been how management consultants demonstrate their value to clients, and establish their legitimacy and expertise. Clients have different reasons for engaging management consultants, but the dominant discourse has been as providers of expertise that is lacking in organizations, or in some cases to legitimate preferred options (Sturdy, Werr, and Buono 2009). This has been viewed as a process of “problematization” (Bryson 2002), with management consultants successful not only in constructing their expertise but also in establishing the range of problems for clients, that they can then “solve” (Fincham 1999). Although consultant services may be portrayed as impartial or neutral, these discourses are used to establish a market for services, as consultants have an “explicit interest in exercising power and try to convince clients of the indispensable nature of the solutions they propose” (Canato and Giangreco 2011, 234).

Impact of Management Consultants

There has been little consensus on the direct impacts of management consultants (Kipping and Clark 2012). While management consultants may be seen as providing innovative and high-value services, they have been critiqued as exploiting client vulnerabilities (such as fear of “lagging behind”) and manipulating institutional contexts to sell their services (Cerruti, Tavoletti, and Grieco 2019, 916). Research from fields outside of management have been more critical of the role of consultants, such as in their impact on public sector organizations (Saint-Martin 2000; Vogelpohl and Klemp 2018), partly attributed to increasing models of marketization and privatization in the public sector (Fincham 1999). For example, management consultants have been key in undertaking “municipal delivery service reviews” that use benchmarking and metrics to promote reductions in public services (Hurl 2018).

Management consultants are instrumental in the widespread adoption of specific financial metrics (Bryson 2002; Froud et al. 2000), both in traded and privately held firms (Muzio and Faulconbridge 2009). While management consultants can have a variety of roles, as “standard setters,” their locus of experience includes developing and promoting standards (Canato and Giangreco 2011). In tracing the financial measures and league tables established by consultants, Froud et al. (2000) point to the impact of these discourses of competition and ranking: The excellent can serve as exemplars of what is possible while the rest identify their task of improvement and status as clients in need of assistance through necessary measures including “surgery.” (Froud et al. 2000, 90)

Promised strategies to increase shareholder value may be unrealistic or ineffective, driving significant re-organization within firms, especially as the “persistent gap between expectations and outcomes can drive a whole series of behaviours which do change the world” (Froud et al. 2000, 108).

The impact of the financial metrics and strategies on professionals and organizations has received increasing attention. 5 In professional services firms, the imposition of financial metrics and measures can clash with long-standing conceptualizations of professional practices, such as autonomy and “good citizenship” (Cushen 2013; Faulconbridge and Muzio 2009). Financial demands can be direct in transforming how professionals spend their time and prioritize projects, and seen overall as a form of employee control (Alvehus and Spicer 2012). The use of specific metrics and benchmarking of firm success has led to the re-organization of firms to better meet these targets, despite the negative impact on working conditions and long-term stability of firms (Allan, Faulconbridge, and Thomas 2019; Faulconbridge and Muzio 2009).

Beyond diffusing measures and standards, the influence of management consultants is more equivocal, especially given methodological issues in understanding their impact on clients (Sturdy, Werr, and Buono 2009); the diffuse nature of their influence (such as through “thought leadership”; Sturdy 2011); and differing responses from clients in accepting or contesting consultant advice (Engwall and Kipping 2013). Consultant influence on firms has frequently been assessed in terms of measurable indicators, such as layoffs, share price, or in the diffusion of key ideas in management (Canato and Giangreco 2011). In contrast, assessments of management consultants’ influence on government agencies address broader societal and public interest issues such as policy convergence, changes in public service provisions, and democratic processes (Saint-Martin 2000; Vogelpohl 2019; Vogelpohl and Klemp 2018; Weber and O’Neill-Kohl 2013). Ethnographic accounts have shown that that the profit motivations of management consultants have led to their ignorance of the broader socio-economic impacts of their advice (Stein 2020). Importantly, the clients of consultant services are not just limited to the firm itself, but can include “unwitting” or “ultimate” clients, such as the client organizations’ customers (Schein 1997). 6 This distinction between public and private sector organizations in understanding consultant influence is problematic for planning practice, as both are involved in shaping public policy (Linovski 2018; Steele 2009) and as the “ultimate” clients for planning firms often includes public agencies. While there has been extensive research on management consultants, their influence on planning firms and practitioners is largely unknown, despite evidence of their integral role in shifting the values and work of other types of professionals. This research addresses this gap by exploring how management consultants view planning practices, the strategies used to improve business function, and how this may affect planners.

Methods

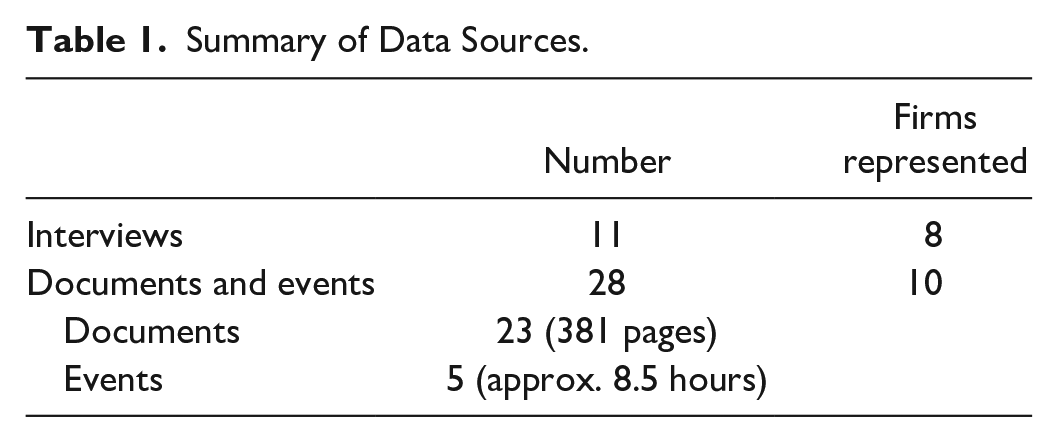

As Kipping and Clark (2012, 17) note, management consultancy can be a particularly difficult area to research, due to concerns about client confidentiality. Despite this, there is value in analyzing self-reported and public data to understand management discourses and strategies. This research uses a mixed-method approach that draws on (1) interviews with management consultants and (2) content analysis of management firm research reports and events (see Table 1). I used Internet searches to identify management firms that specialize in built environment or AEC companies (using AEC and planning, in combination with terms such as management consultant, advisor, business strategy, mergers, acquisitions), as well as snowball sampling through the interviews. I identified fourteen management consultancy firms, and collected interview or documents for analysis from ten of these firms. Given the small number of management firms specifically focusing on AEC companies, this purposive strategy was used to target relevant subjects, and the positive response rate was 68 percent. The services provided by management consulting firms include advice on M&A, strategic planning, ownership transition, valuation, and business development. I conducted interviews with eleven management consultants, who specialize in services for AEC firms, and had experience with planning as a practice area. Interviews lasted between thirty minutes and one hour, and included questions on their experience with planning practices, how they evaluate and value planning services, strategies to increase firm success, and their views on planning as part of firm offerings.

Summary of Data Sources.

The majority of interviewees had a background in finance or business, although four of the interviewees had training or previous careers in an allied professional field (primarily engineering). Documents and events were selected for analysis if they specifically addressed issues related to professional practice, such as engaging professional staff in business development or benchmarks for evaluating staff performance. 7 For both interview transcripts and firm reports, I used directive coding strategies (Hsieh and Shannon 2005), drawing on concepts and themes identified in the existing literature, such as the impact of metrics on professionals and financial priorities in firms. The documents were then coded again with an inductive strategy, allowing for emergent themes that were not previously covered (the appendix). For conferences and webinars where transcripts or presentation materials were not available, I took detailed notes, which were then coded.

Limitations

Given the relatively small sample size and number of interviews, there is the potential for selection bias, if management consultants with strong views on planning services were more likely to agree to interviews. While the response rate was relatively high (68%), and document analysis was used to corroborate interview data, these biases may influence the findings. Due to the competitive and proprietary nature of management consultancies, there is only scattered information on the firms they advise, although all those interviewed had direct experience with planning as a business line. 8 I did not explicitly ask management consultants questions related to professional ethics as most would not have familiarity with professional codes of conduct, although this may be an area for future research. A limitation of the research is that it is based on the perspectives of management consultants, pointing to the need for further research that explores the planning firms that receive advice and understands the use of management consultants through planners’ experiences.

Findings: Management Consultant Priorities and Perceptions of Planning

As others have noted, management consultants increasingly have influence in a wide range of policy, governance, and professional practice forums (Canato and Giangreco 2011; Froud et al. 2000; Kipping and Clark 2012). The management consultants studied here work exclusively with AEC firms, marketing their expertise as specific to these types of companies. As one firm states, “our intimate knowledge of the AEC industry separates us from others . . . who are unfamiliar with the intricacies of AEC firms and how they ‘tick’” (Firm 7). While the absolute number of management consultancies focusing on the AEC field may be small compared with more generalist firms, their exclusive focus on the built environment fields, as well as the nature and uniformity of their advice, has significant implications for planning practice.

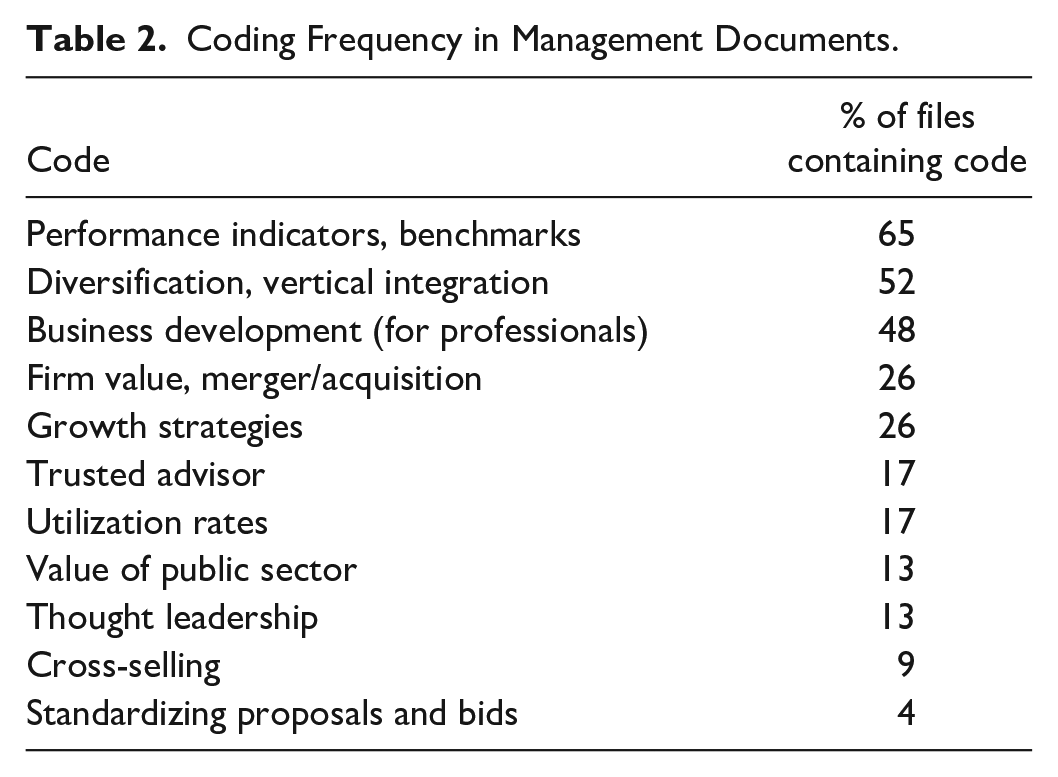

Analysis of management consultant discourses provides insight into the strategies and priorities espoused by these advisors, as well as key areas where firms align in their guidance. Regardless of specific focus, the majority of firm materials included references to standardized performance indicators, diversifying firm services and the role of professional staff in business development (see Table 2). Other themes were less frequently mentioned, such as firms acting as a “trusted advisor” to clients, but have potentially important implications for planning professionals.

Coding Frequency in Management Documents.

Financial Metrics and KPIs

Unsurprising given the financial focus of management consultants, the majority of documents included some reference to performance indicators.

9

Despite the focus of these firms on AEC firms, none of them included measures that address the outputs of these firms, such as how many plans or buildings completed per year, or ones that focus on reputation such as awards. The benchmarks commonly included were measures such as billable/non-billable staff ratios, EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization), revenue per billable hour, net multipliers, and days in accounts receivable. Many AEC management consulting firms have concentrated on increasing the “business sophistication” of companies (Interview 11), focusing on standardized benchmarks or KPIs. Although KPIs have largely been associated with publicly traded firms as part of regulated quarterly reporting, the AEC management consultants studied here push for their adoption by all types of firms, approaching the “financialization by proxy” observed in other fields (Muzio and Faulconbridge 2009). In some instances, consultants emphasize that the value of a firm is not related to reputation, quality of work, or even commercial measures like revenue, but rather reduced to the single metric of EBITDA: Valuation is not driven by awards, revenue, headcount, fancy offices, backlog. It is all about Adjusted EBITDA!!! (File F2_D3)

10

For professional service firms—where staff are the primary resource—there is a significant focus on staff productivity and utilization, broadly measured as the proportion of employee time that can be billed to clients. As seen in other fields, this translates into fine-grained measures related to productivity and profit: [It is] possible to improve utilization with management focus. Each 1% increase in utilization tends to lead to a ~0.5+ percentage point increase in profit margins, so small improvements can have a huge impact on the bottom line. (File F7_D1)

Similar to other fields (Froud et al. 2000; Muzio and Faulconbridge 2009), the ranking of firms—with many of the consultants studied here producing “state of the industry” reports and benchmark surveys—works to promote business metrics above all else. The reports largely focus on these markers of success, but they also increase competition between firms and promote a fear of “lagging behind.” As one survey states, Don’t allow near-term economic concerns to prevent you from stretching your team’s expectations toward the upper quartile of these survey results. Don’t target the median results—strive for excellence. (File F2_D1)

Given the task of comparing hundreds of firms (as consultants promise the broadest surveys of peer firms), measures focus on measurable financial data, such as utilization and overhead rates. These benchmarking reports reinforce the financial measures of success promoted by management consultants.

Although the use of financial metrics is not problematic in itself, their translation to professional practices raises questions. Some strategies suggested to improve utilization have clear implications for professional planners and their clients, such as reducing the time professional staff spend on proposal documents by standardizing elements or having them completed by sales staff (File F2_D2). Other common metrics relate to time in accounts receivable (such as “days sales outstanding”) which can affect planning processes, such as public engagement, that are more fluid or difficult to predict in timing. Relatedly, firms have often used sub-consultants as a way to involve companies that may have more local or specialized knowledge, but this is discouraged because it can increase collection times. Interestingly, one management consultant, who was a strong proponent of standardized metrics, acknowledged that these measures have a negative impact on professional practice: It definitely filters down [to staff]. Connecting the dots . . . investors are unhappy about stock prices. Why is our stock price low? Our profits are low. We’ve got to increase profits. How do we do that? Well, we’ve got to increase our utilization. How do we do that? We put pressure down the organization to increase utilization, so if you’re 60% utilized, that’s no longer good enough. You’ve got to be 65% utilized. So, that puts pressure on the planner to do that, which is not fun. So that’s a simple example of how this sort of trickles down to the rank-and-file planners when we get pressure for higher performance. (Interview 11)

As noted by management consultants themselves, an oversized focus on these measures has the potential to shift planning practices in substantial ways.

Turning Your “Doers” into “Sellers”

As management consultants work to increase firm value, a common theme is the role of professionals in business development. Firms discuss how business development can no longer be seen as only the domain of firm executives or dedicated sales staff, but rather needs to involve professionals in the firm. Management consultants often used the phrase “turning your doers into sellers” (or the doer-seller model) to refer to this expansion of business development, with almost 50 percent of the data studied including some reference to the role of professionals in driving new business. This emphasis on involving all firm staff in business development is depicted as necessary to drive firm growth, and meet performance indicators. Some firms provide guidance as to how professionals should undertake business development, contrasting the role of executives who “establish a vision or strategic direction” with professionals who have a role in “open[ing] the door” with clients (File F4_D1). To illustrate the importance of including professional staff in business development, one consultant provided an example of a successful firm in this respect: Soon, they began cultivating existing staff and hiring new staff to transition to a Seller-Doer culture. “Seller-doers are our golden geese who lay the golden eggs for us” [firm executive] says. (File F3_D5)

Despite the promotion of seller-doer models, some consultants acknowledged inherent conflicts with professional values. One interviewee noted that there is a tension between professional staff values and the profit-seeking direction that management consultants suggest: I will still say a lot of architects, engineers and planners are not business people. They don’t really have training to think economically from a business perspective. Profit is a dirty word for many of them. They didn’t get into the business to become rich. (Interview 11)

While all private sector firms must be profitable, the focus on technical staff in driving new growth, along with the increased reliance on standardized metrics, can affect professional practices and create conflicts.

Emphasizing the role of professional staff in business development has further implications when combined with other common strategies advocated by management firms, such as diversification and firms acting as a “trusted advisor” to clients. Firm diversification (or vertical integration) was referred to in over 50 percent of the documents studied, with many management consultants advising firms move into new sectors, markets, or geographies. This was seen not only as a safeguard against changing market cycles or recessions, but as a way of changing client perceptions of the firm. Offering multiple services to the same client was depicted as a way to build trust, as in this firm profile presented by a management consultant: . . . “the more services we offer, the more trust we build,” says [firm executive]. “If we do just structural engineering, we won’t be unique. Now, we’re often dealing with decision-makers beyond those who would hire us for straight engineering.” (File F3_D3)

This emphasis on firms or staff acting as a “trusted advisor” to clients was present in 17 percent of the studied documents, along with 13 percent that referred to “thought leadership” or influencing broader discussions about related issues. Multiple management consultants used this term or related ones: Seller-doers are the lifeblood of A/E/C firms and the best ones . . . are viewed as a “trusted advisor” by their clients. (File F3_D1)

While this was common in the management consultant discourse, the idea of a trusted advisor to a client runs contrary to traditional conceptions of professional planning practice which see planners as neutral parties, providing advice that best protects the public interest.

Last, some business development approaches suggested by management consultants would likely conflict with planners’ codes of conduct or professional ethics, particularly with public sector clients. For example, one firm lists reasons why competitors may be more successful in business development: Did they get known to the political entities through volunteering for committee assignments, sponsoring local charity events, etc.? Did [they] hire a recent retiree from the client sector who was well known and respected? Did they . . . work assiduously to be visible to key decision-makers who procure those services by working in professional and local organizations . . .? (File F2_D2)

Some of these suggestions may already be regulated, such as policies that prevent public sector staff from accepting positions in private firms for a specified time. However, for firms with public sector clients, business development strategies that focus on influencing decision-making processes blur the line for acceptable professional behavior.

Planning as Low Value and Low Margin

Understanding the perspectives of management consultants on planning as a business service offers insight into the shifting context of professional practice. The framework established by the analysis of management consultant documents and events was expanded through interviews with consultants working for these firms, who were able to comment specifically on their experiences with planning practices (either as standalone firms or as a service area of a diverse firm). Critically, management consultants pointed to two contradictory yet related perceptions of planning practice: (1) planning contracts are relatively low value and low margin and (2) the value of planning work is in leading to other types of work. These views of planning work are in contrast to traditional conceptions of planning as motivated by public service, rather than entrepreneurial goals.

Most management consultants viewed planning as a relatively low value service, both in terms of contract sizes and margins. With many firms undertaking large-scale engineering projects, consultants largely felt that “the dollars are in the design and execution side, the dollars are not really in the planning side” (Interview 11). Similarly, some interviewees felt that planning projects were not a major concern for large firms. One interviewee who had experience as both a professional engineer and management consultant noted, In urban planning, the projects are relatively small. They’re not the kinds of projects that these big publicly-traded firms are really going after. Those guys are going after the Toronto subway and the Second Avenue Subway in New York, that’s the kind of thing that they’re looking for. They’re not looking for a $30,000 urban planning study. So, the urban planning work is really shunned by those publicly-traded firms. (Interview 6)

Overall, none of the management consultants interviewed felt that planning projects—as independent business lines—were important revenue sources for diverse firms, despite their inclusion as an offering.

In addition to the lower value of planning contracts, they may also rank lower according to the KPIs which affect business lines differently. For example, consultants pointed to the selling effort required to get different types of work. One interviewee mentioned that they are interested in the “cost to win” business, as it may be more expensive to win contracts in some sectors, if more staff time is required to produce bid documents (Interview 10). The perceived lower value of planning work is also related to the types of metrics used to evaluate success. For example, utilization rates can be poor for planning practice: The philosophy of the big firms to focus so much on utilization really puts the people who do the smaller, specialty projects like urban design, urban planning . . . it really puts them in the background of the firm’s priorities and they just don’t give them a lot of value. (Interview 6)

Projects that are relatively lower value, such as planning work, not only provide less revenue for the firm, but can also skew KPIs such as utilization, if they require more non-billable time. While management consultants felt that overall planning services were low value, both in terms of absolute revenue and relative margins, many diverse firms not only provide planning services, but have actively sought to acquire planning firms. The following section examines a contrasting view of the value of planning practices for diverse firms that offer multiple service lines.

Planning as an “Entrée”: The Value of Planning

While planning was largely described as a low value and low margin service, it remains a part of many AEC firms, with multiple notable M&As focusing on planning service firms (Linovski 2019; Raco 2018; WSP 2019). Interviews with management consultants gave insight into why planning was seen as a benefit to AEC firms, despite the lower revenues. The majority of consultants interviewed felt that planning’s potentially foundational role in larger projects offered benefit to firms beyond the dollar amount of contracts.

Firms have profitability pressures, including the need to show continual growth and meet KPIs. For firms that are project-based—with few long-term contracts—this increases the pressure to sell. As one consultant noted, for these types of firms, this involves significant, and continual, business development efforts: [For these firms] there’s a profitability pressure. The challenge with all these businesses from a financial perspective is that they start the year with zero revenues. They’ve got some longer-term contracts, but basically there’s a huge amount of selling that has to happen to get the new projects. (Interview 1)

In light of these pressures, management consultants saw planning as having larger benefits than just related to absolute revenues. Cross-selling—or the ability to provide multiple services to the same client—is a common strategy for firms in driving growth, and this was identified by management consultants as one of the benefits of providing planning services. With a focus on increasing sales, selling multiple services to the same client is seen as easier than developing new clients, so there is an advantage in offering related services: I know that there’s a lot of firms that might view planning as something they can add as a means of diversification. It only makes more sense that it’s easier to cross-sell—it’s cheaper to acquire a client that you already have and sell them more services than it is to go out and find new clients. (Interview 9)

Planning was seen as particularly attractive for cross-selling because it may form the basis for future work. For example, preliminary transportation planning (such as alternatives analyses) or land development plans may lead to large engineering or design contracts if projects proceed further. Although this does not apply to all types of planning, and some jurisdictions may limit this through procurement policies, consultants still felt that this was a significant benefit of planning.

11

While two of the consultants described planning services as just part of offering a full range of services, or providing a “one-stop shop” for clients (Interview 4), the majority discussed specific value for planning being “early in processes.” For example, this consultant saw planning as particularly well-positioned for selling other firm services: Planners are in a good position to cross-sell or to up-sell, or at least to notify the other divisions that “hey, there’s this project coming or this part of the region is going to develop, they will need road, rails, sewer, water, schools, etc.” It doesn’t have to come from planning, but the planning people are there early. (Interview 5)

The value of planning as leading to other types of work was also noted as related to the recent trend of M&A in the AEC field. As one consultant noted, acquiring firms that offer planning services can drive growth through earlier knowledge about projects: To gobble up a firm that does urban planning is really a smart move because it moves them up the value chain so they can have earlier entrée into knowing about projects or even potentially positioning themselves to get some of the projects that would come about from their planning. (Interview 2)

Critically, as this consultant remarked, the value of planning is seen as not only knowing about what future work may arise, but also in allowing the firm to position itself to win these contracts.

There were two issues raised by management consultants that questioned the value of planning for cross-selling strategies. First, one consultant noted that very large firms would be less likely to push planning bids that could potentially lead to future contracts because of the need to demonstrate value immediately: I think [cross-selling] practices are viable for smaller design firms. But for the mega-firms, unless there’s a really obvious way to connect the dots from the planning study to the bigger design and construction study projects, they tend not to really go after that very much, it’s not a priority. (Interview 6)

This management consultant felt that for very large firms, particularly publicly traded firms, every bid needed to meet margin or value criteria, potentially limiting the emphasis on cross-selling. Second, another consultant felt that cross-selling strategies may be perceived negatively by planning clients, who may prefer specialized firms that do not attempt to sell multiple services: One of our clients, a major billion-dollar firm, is looking to acquire [specialized planning] businesses because they have found that they lose to them in competitions when it comes to urban planning and economic development in particular, even with their expertise in that area. Some of their clients actually prefer to work with smaller firms that are not trying to cross-sell them other services, which makes them more biased in terms of their advice. (Interview 11)

This consultant noted that cross-selling could result not only in reduced client interest, but also conflicts of interest. Paradoxically, client concerns about the independence of advice in diverse firms was seen as motivation to acquire specialized planning firms (Interview 11), raising larger concerns about the lack of attention paid to these types of mergers. With relatively low revenues, management consultants largely saw the value of planning in its’ potential to lead to more lucrative contracts. This may be framed in the context of corporate strategies that focus on providing all related services “in house,” yet consultants were often explicit in that planning could have a role in gaining future work. While the potential for cross-selling will vary by firm type or in response to client concerns, this was discussed as a significant benefit for firms offering planning services.

Discussion: Management Consultants, Ethics, and the Clients of Planning

The analysis of management consultant discourses and strategies provides insight into conflicting logics for private sector practitioners. In contrast to long-held professional planning values—such as protecting the public interest, social responsibility, and independent professional judgment—consultant strategies are focused almost exclusively on improving the financial metrics that they promote. While acknowledging that these strategies can have a negative impact on professionals—with one consultant noting that they “would not want to be an urban planner at a [publicly traded firm]” because of the emphasis on utilization (Interview 6)—these same measures are aimed at all types of firms. This is important not only in terms of the working conditions for planners, but also in the potential to influence how planners interact with their clients, and their broader responsibility to the public interest. Planners may be able to manage consultant strategies that explicitly conflict with codes of ethics—such as attempting to influence elected decision-makers—but it is unclear how other tactics aimed at increasing the value of firms may blur professional orientations. While private sector practice for planners is certainly not new, nor are the financial constraints facing planning consultants, 12 the influence of a more diverse group of actors, such as management consultants, financial analysts, and shareholders, suggests the need for a broader understanding of the organizational context of planning.

The ethical implications of management consultants’ work with planning firms require reflection on the “client” of these services. Management scholars have emphasized that the clients of management consultants cannot be seen in a unified way, as the interests of those that commission management consultants are clearly different from those that are “the object of their analysis” (Sturdy, Werr, and Buono 2009, 248), in this case, planners working for these firms. Given the experiences in other professional fields (Allan, Faulconbridge, and Thomas 2019; Alvehus and Spicer 2012; Cushen 2013), it is unlikely that planners—and their professional outputs—would be immune from the re-orientations stemming from these processes. However, the clients of consultant services are not just limited to the firm itself but also include “ultimate” or “unwitting” clients. Ultimate clients, such as the client organizations’ customers, are seen as “affected by the outcomes, but may not even know that anything is going on” and whose “interests should ultimately be protected even if they are not in direct contact with the consultant” (Schein 1997, 231). For firms that provide planning services, the ultimate clients include public sector agencies—such as municipalities, transit agencies, or regional planning organizations—or even more broadly, the communities affected by the plans, policies, and infrastructure developed by these firms. Yet the ethical implications of these complex chains of influence have not been addressed by professional codes of conduct, which focus on the actions of individuals or arguably, loyalty to employers and clients (Linovski 2021; Marcuse 1976). Although management consultants that work with planning firms may not engage directly with public agencies or communities, their advice can have tangible impacts on the work of planners, as they strive to meet utilization and profitability targets.

Despite the belief that management consultants should be aware of the impact of their advice on firms’ ultimate clients (Schein 1997)—and in light of evidence to the contrary (Stein 2020)—it is difficult to see how this would be accomplished for planning work. 13 In other fields, such as manufacturing, if a management consultant advises a firm to cut its workforce, the results may be clear, such as a decrease in product quality and a negative impact on customers who buy the firm’s product. Applying this logic to the ultimate clients of planning work is significantly more complex, with planning work (1) often extending into decades-long processes, (2) influenced by a wide variety of other factors (such as political and funding decisions), and (3) requiring substantial expertise to evaluate. Management consultants are likely not concerned by the implications for the ultimate clients of planning firms, but planners and the associations that regulate them should be. The pressure to meet financial goals can play out in numerous ways that may affect the clients of planning services, such as reducing senior staff, shifting staff time from project work to business development, taking on projects without sufficient staff expertise, or pushing for involvement in multiple stages of projects. While codes of conduct may specify that professionals should only work within their area of competence and “render services with appropriate preparation” (American Institute of Certified Planners 2016; Canadian Institute of Planners 2016), the emphasis on utilization and financial indicators point to the potential for significant conflicts that exist beyond the scope and even influence of the individual planner.

The conflicts between profit and professional values that have been widely observed in other professional fields (Allan, Faulconbridge, and Thomas 2019; Cushen 2013; Faulconbridge and Muzio 2009) raise the need for more nuanced work on the organizational contexts of planning and the impacts for the profession. As an agenda for future research, I suggest the following areas of inquiry:

More nuanced understanding of the different contexts for private sector planners, and how they are affected by, or accountable to, actors such as management consultants, shareholders, or firm executives, and the impact on professional ethics.

An exploration of how management practices intersect with the clients of planning services, particularly in the public sector.

Analysis of how planning educators and professional organizations should respond to this complexity in organizational contexts for professional planners.

To complement the long-established analysis of the relationship of planning policy to business interests (i.e., D. Adams and Tiesdell 2010; Roweis 1981; Valler, Tait, and Marshall 2013), there should be a similar situating of planners themselves. As Beauregard (1983, 184) noted early on, for planners, it is “the structure of the political economy, and the positions of planners’ within that structure which shape their practice.” With an increasingly diverse range of interests that planners may be accountable to, this requires more distinction in understanding professional practices.

Conclusions: Implications for Planning Practice

This research establishes a framework for understanding the broader range of financial, managerial, and entrepreneurial values that increasingly intersect with planning practice. While there remain questions about how firms and professionals respond to the discourses promoted by management consultants, understanding their priorities and strategies offers insight into potential conflicts between firm goals and professional planning practice. As shown in other fields (Froud et al. 2000; Muzio and Faulconbridge 2009), management consultants are adept at promoting specific discourses of success and value, and firms that offer planning services are not exempt from this. Financial metrics are promoted heavily by the management consultants that work with AEC firms. For professional services firms, whose main resource is their staff, this translates into measures related to efficiency, utilization, and business development, all of which have the potential to re-shape the work of professional planners. Evidence from other fields points to professionals being “captured” by financialized strategies—unable to reconcile them with professional logics such as autonomy and “good citizenship” (Allan, Faulconbridge, and Thomas 2019)—making it critically important to understand these processes for planners, especially in their day-to-day work. However, links to other fields such as law and accounting are limited when considering the unique position of planning in complex and long-range plans or projects. Management consultants spoke about the “value” of planning in its potential to lead to future contracts, viewing planning as setting the framework for selling a firm’s full range of services. While private sector firms clearly need to be profitable, the intense focus on financial metrics, previously only the domain of publicly traded firms, and the perceptions of planning as an entrepreneurial strategy raise significant questions about how the planning profession responds to these pressures, and planners in practice are able to reconcile professional and market conflicts.

Footnotes

Appendix

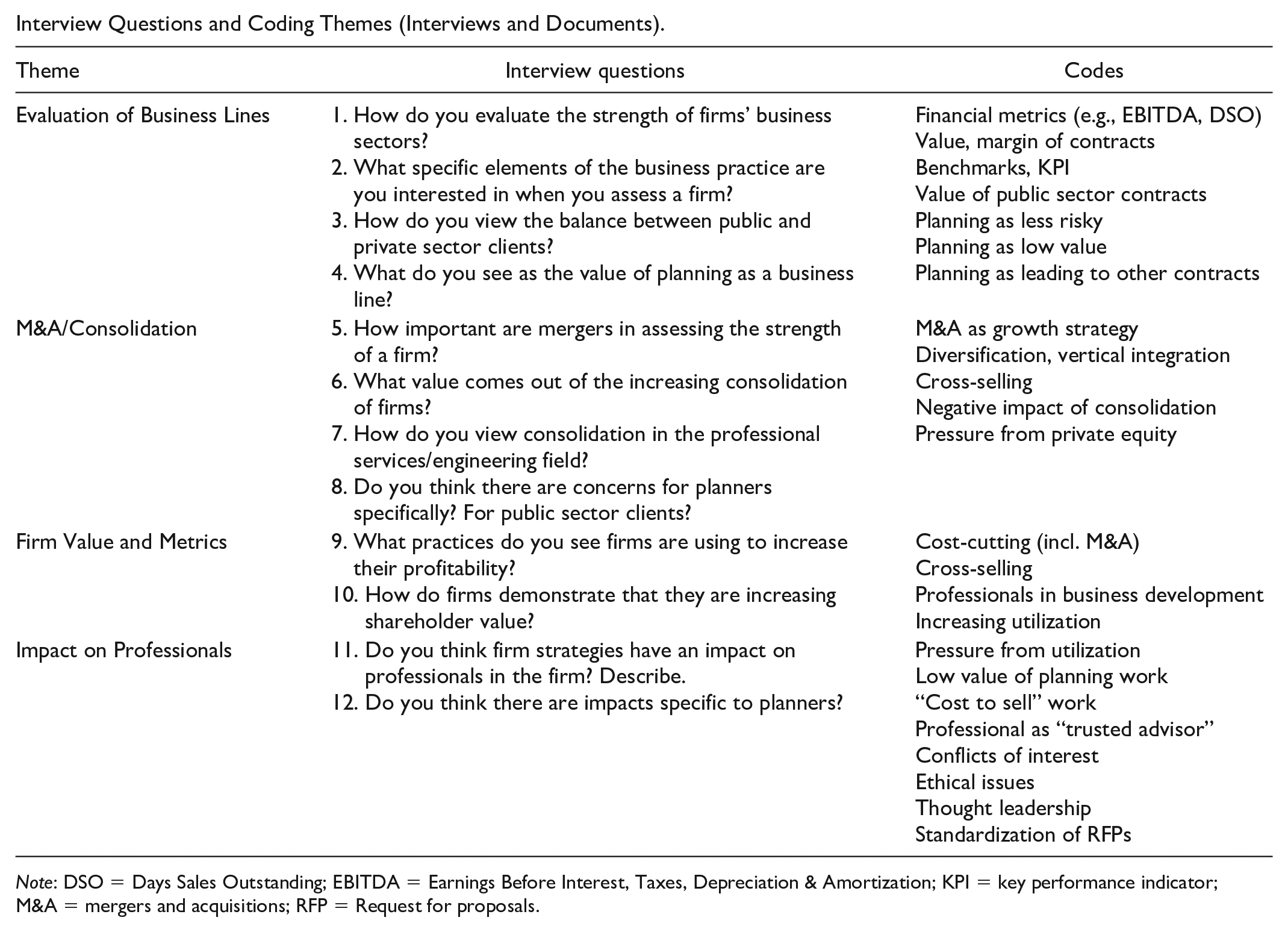

Interview Questions and Coding Themes (Interviews and Documents).

| Theme | Interview questions | Codes |

|---|---|---|

| Evaluation of Business Lines | 1. How do you evaluate the strength of firms’ business sectors? 2. What specific elements of the business practice are you interested in when you assess a firm? 3. How do you view the balance between public and private sector clients? 4. What do you see as the value of planning as a business line? |

Financial metrics (e.g., EBITDA, DSO) Value, margin of contracts Benchmarks, KPI Value of public sector contracts Planning as less risky Planning as low value Planning as leading to other contracts |

| M&A/Consolidation | 5. How important are mergers in assessing the strength of a firm? 6. What value comes out of the increasing consolidation of firms? 7. How do you view consolidation in the professional services/engineering field? 8. Do you think there are concerns for planners specifically? For public sector clients? |

M&A as growth strategy Diversification, vertical integration Cross-selling Negative impact of consolidation Pressure from private equity |

| Firm Value and Metrics | 9. What practices do you see firms are using to increase their profitability? 10. How do firms demonstrate that they are increasing shareholder value? |

Cost-cutting (incl. M&A) Cross-selling Professionals in business development Increasing utilization |

| Impact on Professionals | 11. Do you think firm strategies have an impact on professionals in the firm? Describe. 12. Do you think there are impacts specific to planners? |

Pressure from utilization Low value of planning work “Cost to sell” work Professional as “trusted advisor” Conflicts of interest Ethical issues Thought leadership Standardization of RFPs |

Note: DSO = Days Sales Outstanding; EBITDA = Earnings Before Interest, Taxes, Depreciation & Amortization; KPI = key performance indicator; M&A = mergers and acquisitions; RFP = Request for proposals.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by a fellowship from the Centre for Professional and Applied Ethics (University of Manitoba).