Abstract

Using the 2019 Canadian Financial Capability Survey (CFCS), this study examines whether social equity gaps persist in financial knowledge and retirement savings participation between newcomers and those born in Canada. Compared to well-established immigrants and their Canadian-born counterparts, the results suggest that newcomers have significantly lower levels of financial knowledge and are less likely to participate in registered retirement savings plans. To catalyze actions for better financial outcomes for newcomers in Canada, the Financial Consumer Agency of Canada could consider establishing a Financial Literacy Working Group for Newcomers (like the one for Indigenous Peoples). Furthermore, to reduce the information gap, Immigration, Refugees, and Citizenship Canada could add a “Financial Education Courses” category box on the settlement services Canada.ca webpage, which would help newcomers easily filter and find settlement organizations offering financial literacy services.

Introduction

Governments are responsible for ensuring that financial institutions offer appropriate and accessible products and services to consumers, adopting financial inclusion policies, and establishing a national financial literacy strategy to equip citizens to navigate the financial system landscape. Financial literacy, or financial knowledge, matters for public administration because it empowers households and vulnerable groups to make appropriate and informed financial decisions, such as retirement savings, which can help alleviate the burden on social welfare. However, researchers have documented disparities or inequities in financial knowledge and savings participation in Canada among certain socio-demographic groups, including immigrants (Khan et al., 2022; Rostamkalaei & Riding, 2020). Using the Canadian Financial Capability Survey (CFCS), they found that immigrants had significantly lower levels of financial knowledge than their Canadian-born counterparts (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 951). Furthermore, they found that immigrants are less likely to prepare financially for retirement or hold long-term investments compared to their Canadian-born counterparts (Morissette, 2019, p. 21; Rostamkalaei & Riding, 2020, p. 951).

Unlike those papers, this study uses a social equity theory grounded in the most recent available CFCS data to contribute to the limited work that has examined the financial knowledge of immigrants (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 953). Focusing on immigrant populations is important because they are identified as a vulnerable group, at risk for financial precarity (Khan et al., 2022, p. 3184), and are at a high risk of income poverty (Khan et al., 2022, p. 3185; D. Rothwell & Robson, 2018, p. 17). More precisely, this study tests the equality of opportunity and block equality of the compound theory of social equity (Frederickson, 1990, p. 230; 2010, p. 56) in financial knowledge and saving participation between newcomers (those who have lived in Canada for less than 10 years) and people born in Canada. Block equality, proposed by Frederickson, postulates equality between different social groups (Frederickson, 1990, p. 230; 2010, p. 56). Equality of opportunity states that equality exists when two individuals have the same chances or probability of obtaining or accessing a good or service (Frederickson, 1990, p. 231; 2010, p. 57). Biaou and Charbonneau (2024) tested the compound theory of social equity using the 2019 Survey of Financial Security (SFS). They found disparities in contributions to Tax-Free Savings Accounts (TFSA) and Registered Retirement Savings Plans (RRSP) based on the level of education and gender of single parents. More precisely, they found that single-parent women are less likely to contribute to TFSA and RRSP compared to their male counterparts and that having a postsecondary education makes a difference in the effect of a variation in the contribution to RRSP on the TFSA, even after controlling for income (Biaou & Charbonneau, 2024, p. 46). However, Biaou and Charbonneau (2024, p. 48) did not analyze the newcomers’ population because the related variables were excluded from the publicly available 2019 SFS data. Therefore, this study utilizes the 2019 CFCS data to provide up-to-date results and verify whether quantitative models of financial knowledge and saving participation between newcomers and individuals born in Canada continue to capture the social equity gap. 1

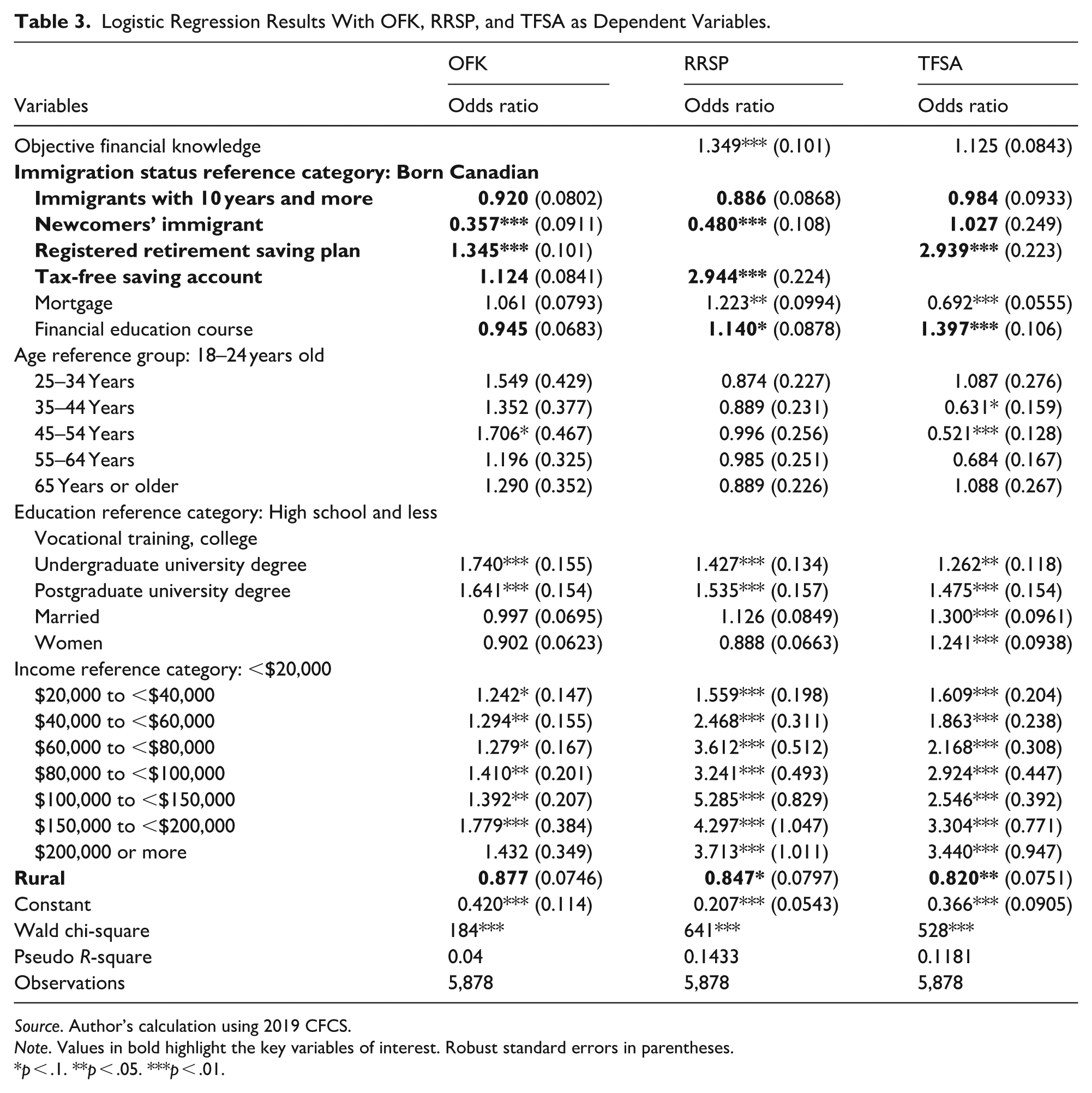

The primary research question is: Does the social equity gap persist in financial knowledge and savings participation between newcomers and individuals born in Canada? Consistent with previous studies (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 953), the regression results in this study suggest that newcomers have a significantly lower level of financial knowledge and are less likely to participate in the RRSP compared to well-established immigrants (those who have lived in Canada for 10 years or more) and their Canadian-born counterparts. More precisely, the results suggest that newcomers are 64% less likely to have the highest score on financial knowledge and are 52% less likely to participate in the RRSP compared to their Canadian-born counterparts (see Table 3), which does not meet the expectations of equality of opportunity and blocks equality as outlined in the compound theory of social equity. Compared to well-established immigrants, newcomers are 61% less likely to achieve the highest score on financial knowledge and are 46% less likely to participate in the RRSP. However, the results suggest no statistical significance in TFSA participation between newcomers, well-established immigrants, and those born in Canada. This result aligns with the expectations of equality of opportunity and block equality, as outlined in the compound social equity theory.

This study offers practical recommendations in the discussion section that can be useful for practitioners to bring about change. For instance, this study suggests that the Financial Consumer Agency of Canada (FCAC) could consider establishing a Financial Literacy Working Group for Newcomers, like the one for Indigenous Peoples. Further, this study recommends that Immigration, Refugees, and Citizenship Canada (IRCC) consider adding a category box for financial education courses on the Canada.ca settlement services webpage, as this would help newcomers easily filter and find settlement organizations offering financial literacy services courses, as well as shed light on the availability of such services, hence reducing the information gap.

In the subsequent sections, the author presents a literature review on equity in social problems and financial literacy, followed by the data and descriptive statistics, the methodological framework, the results, the discussion, and the conclusion.

Equity in Social Problem Dealings

Social equity in public administration is typically traced back to the Minnowbrook conference held in 1968 (Cepiku & Mastrodascio, 2021, pp. 1019–1020). During that conference, social equity was introduced as a third pillar of public administration alongside efficiency and effectiveness (Blessett et al., 2019, p. 285; Frederickson, 1971, pp. 294–295) with the intent to ensure policymakers consider the impact of public policies on visible minorities, marginalized groups, and low-income individuals (Frederickson, 1974, pp. 1–2; 2010, p. 41; Rubin & Bartle, 2021, p. 8). More precisely, the proposal was to advocate for quality-of-life improvements for all by infusing social equity into public management, such as in planning, project management, budgeting, citizen participation, resource distribution, and accountability (Frederickson, 1971, pp. 295–296, 299–300), including financial literacy and inclusion.

This proposal of Frederickson (1971), which serves as a precursor to the New Public Administration, is a response to the classical school (orthodoxy) in public administration, which puts only efficiency, effectiveness, and rationality at the center of the objectives of public administration (see Frederickson, 1971, p. 295; 2010, pp. 28–31). The New Public Administration stipulates that on top of efficiency and effectiveness, public actors must consider social equity, which includes activities that improve the political power and economic well-being of minorities and the marginalized (Chitwood, 1974, pp. 30–31; Frederickson, 1971, p. 295; 2010, p. 41; Rubin & Bartle 2021, p. 8), with the ultimate value of public service.

Frederickson (1990, 2010) proposed the compound theory of social equity, which captures several forms of equality. For instance, block equality postulates equality between different social groups (Frederickson, 1990, p. 230; 2010, p. 56). Equality of opportunity states that equality exists when two individuals have the same chances or probability of obtaining or accessing a good or service (Frederickson, 1990, p. 231; 2010, p. 57). Segmented equality postulates equality within a segment in a group and inequality between two segments within the same group (Frederickson, 1990, p. 230; 2010, p. 56). The domain of equality seeks to know in which area to resolve existing inequalities (Frederickson, 1990, p. 230; 2010, p. 56). Equality in values advocates equal shares (Frederickson, 1990, p. 231, 2010, p. 57). Simple individual equality states that a unique price should apply to everyone (Frederickson, 1990, p. 230, 2010, p. 56). This study does not address all other forms of equality within the compound theory of social equity, either because they involve inequalities (for instance, segmented equality) or because they are too broad (for instance, the domain of equality).

Equity, fairness, and inclusion are extensively discussed in public administration literature (Aoki et al., 2021, p. 46; Blessett et al., 2019, p. 129; Borry et al., 2021, p. 392; McCandless et al., 2022, p. 129) with various loci and standpoints (Cepiku & Mastrodascio, 2021, p. 1028; Rivera & Knox, 2023, pp. 11–12). A few studies that have attempted to define social equity portray it as an input, an output, a result, a process, a right, and as payment capacity (Cepiku & Mastrodascio, 2021, pp. 1024, 1028; Rivera & Knox, 2023, pp. 11–12). In addition to these, equity is viewed as either horizontal or vertical. Horizontal equity implies equal treatment among social groups, while vertical equity implies unequal treatment among social groups to bridge existing gaps (Cepiku & Mastrodascio, 2021, p. 1025; Chitwood, 1974, pp. 33–34; Frederickson, 2010, pp. 46–47). Shen et al. (2023), in their systematic review of 127 articles in the public administration and policy literature, revealed that pay and hiring gaps between subgroups, particularly those related to gender equity, have been a primary focus for public administration scholars. Most recent studies for international readership devoted to social equity have focused, for instance, on the impact of payment as a public good on saving and credit access (Desai et al., 2024), as well as on inclusive coproduction in public infrastructure (Hwang et al., 2024) and inclusive policies in the workplace (Schachter, 2025) or for women (Sarkar & Sensarma, 2024; Taylor et al., in press).

To promote equity and reduce financial vulnerability, Buckland and Spotton Visano (2022, pp. 13, 60, 158, 165) recommend integrating social and economic interests for a more holistic resolution, balancing individual responsibility with embeddedness, and striking a balance between financial literacy and poverty literacy. They also suggest improving the affordability and availability of banking services. From an institutional perspective, barriers to better saving and financial inclusion (Heckman & Hanna, 2015, p. 187) are, but not limited to, branch closures in low-income neighborhoods (Buckland & Martin, 2005, pp. 6–42), restricted access to affordable banking services and products (Simpson & Buckland, 2009, pp. 974–975), and customer experiences with mainstream banking services (Buckland, 2012, p. 5; Buckland & Spotton Visano, 2022, pp. 27–28). Nevertheless, individual accountability is favoured in the policy framework (Clark, 2013, p. 137; Rostamkalaei & Riding, 2020, p. 952), albeit scholars argue that joint accountability is instead in play (Biaou & Charbonneau, 2024, p. 47) within the financial ecosystem. As such, governments, financial institutions, community organizations, and not-for-profit organizations (Buckland & Spotton Visano, 2022, pp. 27–28; Khan et al., 2022, pp. 3196–3197; Rostamkalaei & Riding, 2020, p. 952) are indeed accountable for financial knowledge inequities between newcomers and their Canadian-born counterparts.

Financial Literacy, Financial Knowledge, and Financial Education

Scholars adopt multiple, yet convergent, views to define financial literacy. Financial literacy is defined as knowledge and understanding of financial matters (Atkinson & Messy, 2012, p. 6; Lusardi & Mitchell, 2008, p. 413; 2014, p. 6), as financial behaviors (Atkinson & Messy, 2012, p. 7; Calvet et al., 2009, p. 397), and as attitudes toward savings (Atkinson & Messy, 2012, p. 9). Financial knowledge sometimes narrowly equates to financial literacy (D. W. Rothwell & Wu, 2019, p. 1725), which refers to individuals’ understanding of everyday financial matters (Khan et al., 2022, p. 3184), a concept that can be achieved, for instance, through financial education. Financial education includes any activities, courses, and programs that aim to enhance or improve the financial knowledge of individuals and households and appropriately change their financial behaviors and attitudes toward savings, debt management, budgeting, and financial planning (Fox et al., 2005, pp. 196–199; D. W. Rothwell & Wu, 2019, p. 1728), hence enhance financial capability (D. W. Rothwell & Wu, 2019, pp. 1725–1726; Wagner & Walstad, 2019, p. 234; Xiao & O’Neill, 2016, p. 712; Xiao & Porto, 2017, p. 805).

Financial knowledge is vital as it positively influences mainstream banking financial inclusion (Asaad, 2015, p. 109; Disney & Gathergood, 2013, p. 2246; Gathergood & Weber, 2017, p. 58; Lusardi & Tufano, 2015, p. 332; Salas-Velasco, 2024, p. 442). Financial knowledge is related to paying bills on time (Allgood & Walstad, 2016, p. 675; Hilgert et al., 2003, p. 311), saving (Babiarz & Robb, 2014, p. 40; Hilgert et al., 2003, pp. 316–318), budgeting, planning financially (Hilgert et al., 2003, p. 312) for retirement (Alessie et al., 2011, p. 527), holding more significant levels of wealth or stock market participation (Blay et al., 2024, p. 15; Lusardi & Mitchell, 2007, p. 205; Van Rooij et al., 2011, p. 449; 2012, p. 449). Financial knowledge is also an individual-level factor influencing financial well-being (Chetioui et al., 2024, p. 102; Khan et al., 2022, p. 3184) and financial resiliency or financial vulnerability. Financial vulnerability is defined as a person facing liquidity stress (the risk of not meeting current financial commitments), insolvency (financial insecurity and the inability to make future financial commitments), or both (Buckland & Spotton Visano, 2022, pp. 3, 18).

Socio-demographic characteristics, financial and economic situation, and institutional factors influence and contribute to households’ financial knowledge and savings. More precisely, financial education (D. W. Rothwell & Wu, 2019, p. 1729), age (Agarwal et al., 2009, pp. 52–53; Lusardi & Mitchell, 2014, p. 17; D. W. Rothwell & Wu, 2019, p. 1729; Xiao et al., 2015, p. 387), gender (Bucher-Koenen et al., 2017, p. 255; Lusardi & Mitchell, 2008, p. 413), immigration (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 951), income, and level of education determine financial knowledge of individuals and saving of households. For instance, research showed that immigrants have significantly lower levels of financial knowledge than their Canadian-born counterparts (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 951). Socio-demographic characteristics such as gender (Babiarz & Robb, 2014, p. 46; Zaman, 2017, p. 342), level of education (Zaman, 2017, p. 342) and income level (Zaman, 2017, p. 342), psychological aspects such as emotions and heuristics (Berger et al., 2023, p. 1), to name a few, determine households’ savings. Based on those findings and grounded on the equality of opportunity and block equality of the compound theory of social equity (see Frederickson, 1990, 2010), this study tests the following hypothesis:

Data and Descriptive Statistics

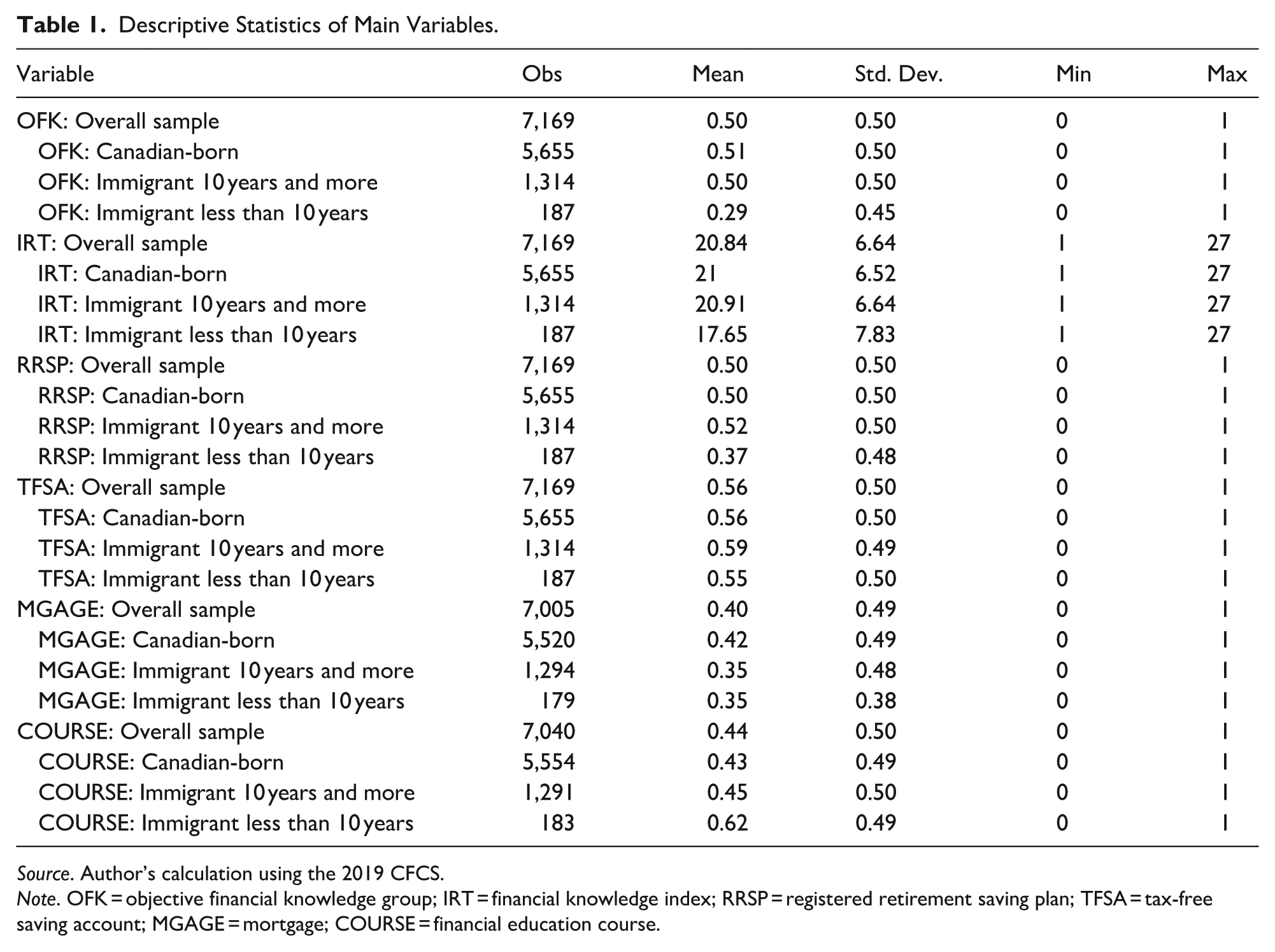

This study uses the 2019 CFCS data, which contains information on Canadians’ financial decision-making knowledge, skills, and confidence (Financial Consumer Agency of Canada [FCAC], 2019). The survey conducted from March 18, 2019, to May 30, 2019, used a probability-based sample representative of the Canadian population (FCAC, 2019). The core sample included 7,169 respondents aged 18 years or older. The response rate was 11%, and a Random Iterative Method (RIM) weight was calculated based on the 2016 Census for age, region of the country, education, and marital status to correct for response bias between the population distribution of the final sample and population estimates (FCAC, 2019). Among the respondents, 16% reported living in a rural region, 45% were married, 53% were male, 46% were female, and 25% had a high school education or lower (FCAC, 2019). In this study, all analyses were conducted using the weighted variable unless otherwise stated. In addition, this study focuses more on financial knowledge questions and saving participation questions across different immigration statuses. It is worth noting that, although the sample of newcomers appears dramatically smaller than the other two groups (see Table 1), the proportions reflect those of the Canadian population. According to FCAC (2019, p. x), “[w]hether respondents were born outside of Canada or not was also added as a population target in the weight” using the 2016 Census. The Census 2016 reported 35.15 million people living in Canada, 2 7.54 million foreign-born individuals, and 1.21 million newcomers 3 . Based on the Census 2016, newcomers represented 3.44% (1.21 million divided by 35.15 million) of the population, which is close but not identical to the numbers (2.61% or 187 divided by 7,169) documented in Table 1. However, depending on the model, regression analysis solely with the newcomer sample would generate inaccurate estimates, given that the rule of thumb is to use at least 10 records per right-hand side variable, including dummies. For further details on the survey’s methodology, readers can skim the 2019 CFCS’s methodological report (FCAC, 2019, p. x). 4

Descriptive Statistics of Main Variables.

Source. Author’s calculation using the 2019 CFCS.

Note. OFK = objective financial knowledge group; IRT = financial knowledge index; RRSP = registered retirement saving plan; TFSA = tax-free saving account; MGAGE = mortgage; COURSE = financial education course.

The descriptive analyses indicate that 51% of Canadian-born individuals achieved the most outstanding results in the first three financial literacy questions (OFK), compared to 50% among well-established immigrants and only 29% among newcomers. The financial index knowledge scores (IRT ranging from 1 to 27 in the dataset) are consistent with those of the OFK in that, on average, Canadian-born individuals have a score of 21, well-established immigrants have a score of 20.91, and newcomers have a score of 17.65, the lowest. Notably, 62% of newcomers reported taking financial education courses in the past 5 years, compared to 43% among Canadian-born individuals and 45% among well-established immigrants.

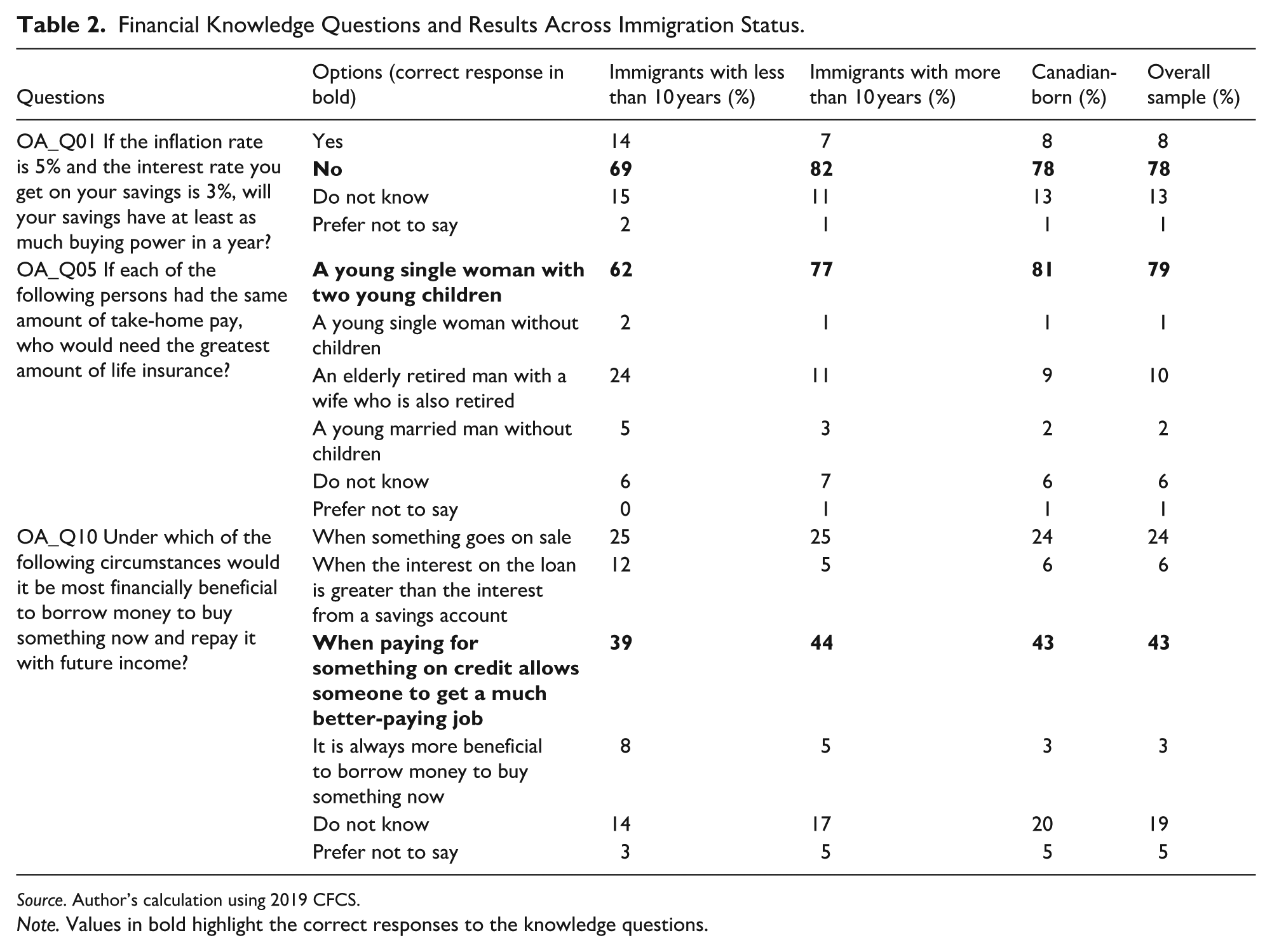

Regarding access to financial products, 50% of Canadian-born respondents reported participating in RRSPs, compared to 52% among well-established immigrants and only 37% among newcomers. TFSA participation rates are similar across immigration status. Mortgage ownership rates are lower than TFSA participation rates across immigration status. Mortgage holding rates are higher among Canadian-born compared to well-established immigrants and newcomers. Table 2 presents the results across immigration status for the first three literacy questions for the reader’s reference.

Financial Knowledge Questions and Results Across Immigration Status.

Source. Author’s calculation using 2019 CFCS.

Note. Values in bold highlight the correct responses to the knowledge questions.

Overall, respondents performed better on the saving and inflation question (OA_Q01) and life insurance question (OA_Q05) compared to the debt management question (OA_Q10). The financial knowledge score gap between newcomers and Canadian-born is wider on the life insurance question (19% difference) compared to the inflation and saving question (9% difference) and the debt management question (only 4% difference). Notably, the financial knowledge scores of Canadian-born or well-established immigrants are similar overall to those of the three literacy questions.

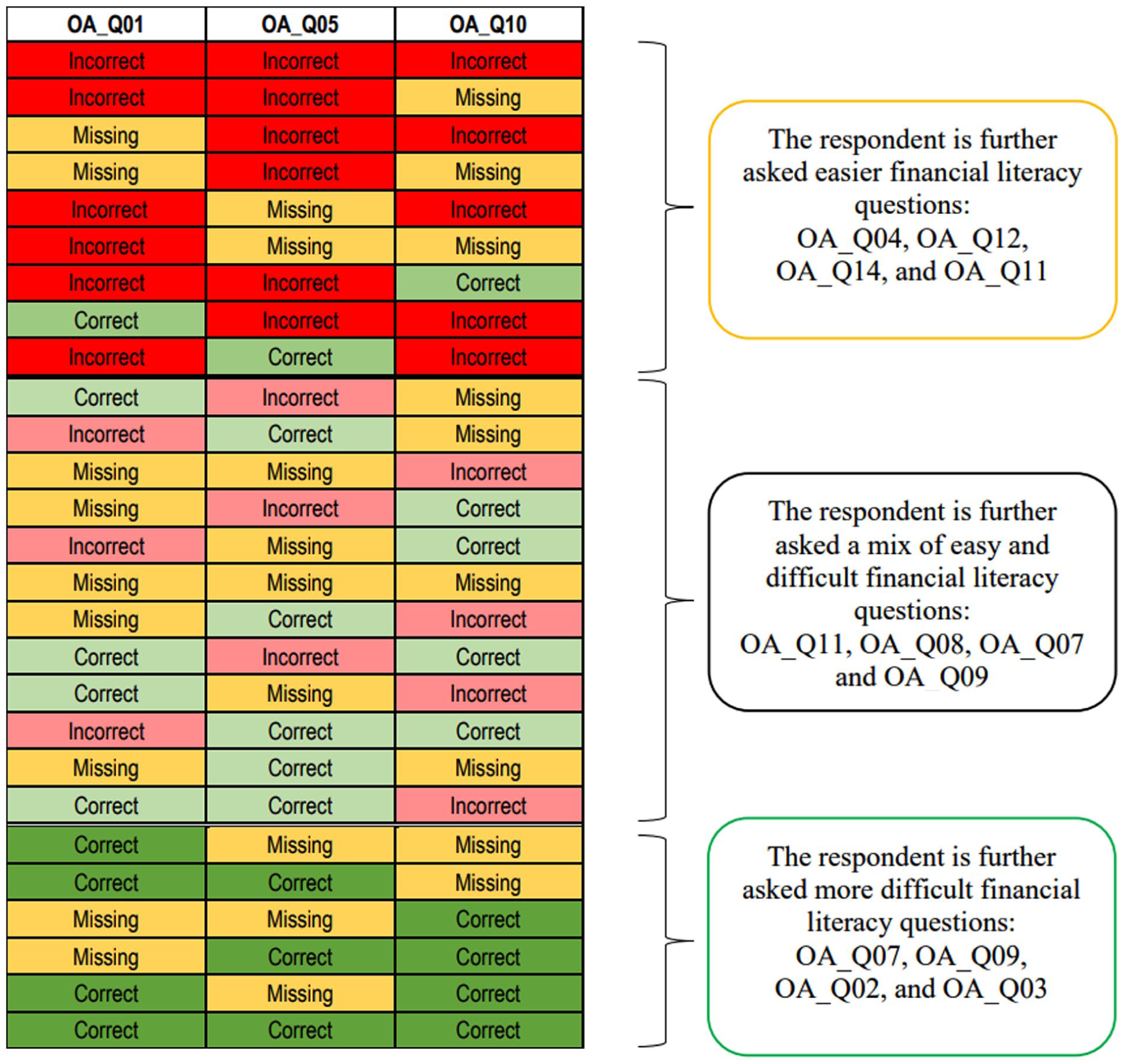

In the 2019 CFCS data, the literacy questions were designed to create an index of financial knowledge (IRT) computed using the performance of respondents on three literacy questions (OA_Q01, OA_Q05, and OA_Q10), an innovative approach compared to the previous CFCS data. All respondents were asked three financial literacy questions, after which four more questions were assigned depending on their performance on the first three questions. The following graph depicts the logic flow used to determine which four questions each respondent received among the remaining literacy questions in the survey and to compute the financial knowledge index (IRT) available in the 2019 CFCS dataset (Figure 1).

Logic used to compute the index of financial knowledge.

Respondents were assigned four additional questions based on correct, incorrect, and missing responses (prefer not to say). Doing so is comprehensive, as it is plausible that individuals who left a question unanswered are more aware of their lack of knowledge than those who answered it incorrectly (Rostamkalaei & Riding, 2020, p. 965). As such, three categories of respondents could be identified: (1) respondents who were asked more straightforward financial literacy questions as they provided wrong and missing answers in the first three questions, (2) respondents who were asked a mix of easy and difficult literacy questions since they got a mix of correct, incorrect, and missing responses, and (3) respondents who were asked difficult questions as they did not get any incorrect but some missing responses in the first three financial literacy questions. By leveraging this logical design of the quiz, the binary variable of objective knowledge score (OFK) is therefore computed as follows: takes the value 1 for respondents who were asked difficult questions (those who did not get any incorrect responses but some missing responses in the first three financial literacy questions), otherwise 0. In other words, OFK assigns a value of 1 to participants who provide correct answers to all questions they responded to (i.e., excluding questions for which they selected “prefer not to answer”). For example, if respondents provided answers to two questions, they should get all of them correct to belong to the group with the highest financial knowledge score. The same logic applies to respondents who answered one or three questions. They should receive all correct answers to be assigned to the group with the highest financial knowledge score, that is, OFK taking the value 1. The financial index knowledge scores (IRT) range from 22 to 27 when OFK takes the value 1 and from 1 to 21 when OFK takes the value 0.

Methodological Framework

To test the hypothesis that there is a significant difference in financial knowledge and saving participation between newcomers and Canadian-born, this study employs Ordinary Least Squares (OLS) regression for IRT and logistic regression for OFK and Savings. Inspired by Khan et al. (2022), Rostamkalaei and Riding (2020), and D. W. Rothwell and Wu (2019), this study employs logistic regression models with immigrant status as the primary right-hand-side variable of interest. Other control variables were added since financial education (D. W. Rothwell & Wu, 2019, p. 1729), age (Agarwal et al., 2009, pp. 52–53; Lusardi & Mitchell, 2014, p. 17; D. W. Rothwell & Wu, 2019, p. 1729; Xiao et al., 2015, p. 387), marital status (Rostamkalaei & Riding, 2020, p. 958) gender (Babiarz & Robb, 2014, p. 46; Bucher-Koenen et al., 2017, p. 255; Lusardi & Mitchell, 2008, p. 413; Zaman, 2017, p. 342), income, and level of education (Rostamkalaei & Riding, 2020, p. 962; Zaman, 2017, p. 342) determine financial knowledge of individuals and households’ savings. The rural-urban variable was included as a control variable, as respondents’ financial knowledge and practices may differ across geographic locations (Rostamkalaei & Riding, 2020, p. 959).

With

The correlation analyses on the independent variables suggest no multicollinearity issue, as the correlation coefficients are not very high (the largest is .31). There is a positive association (coefficient of .31, p < .01) between TFSA and RRSP participation.

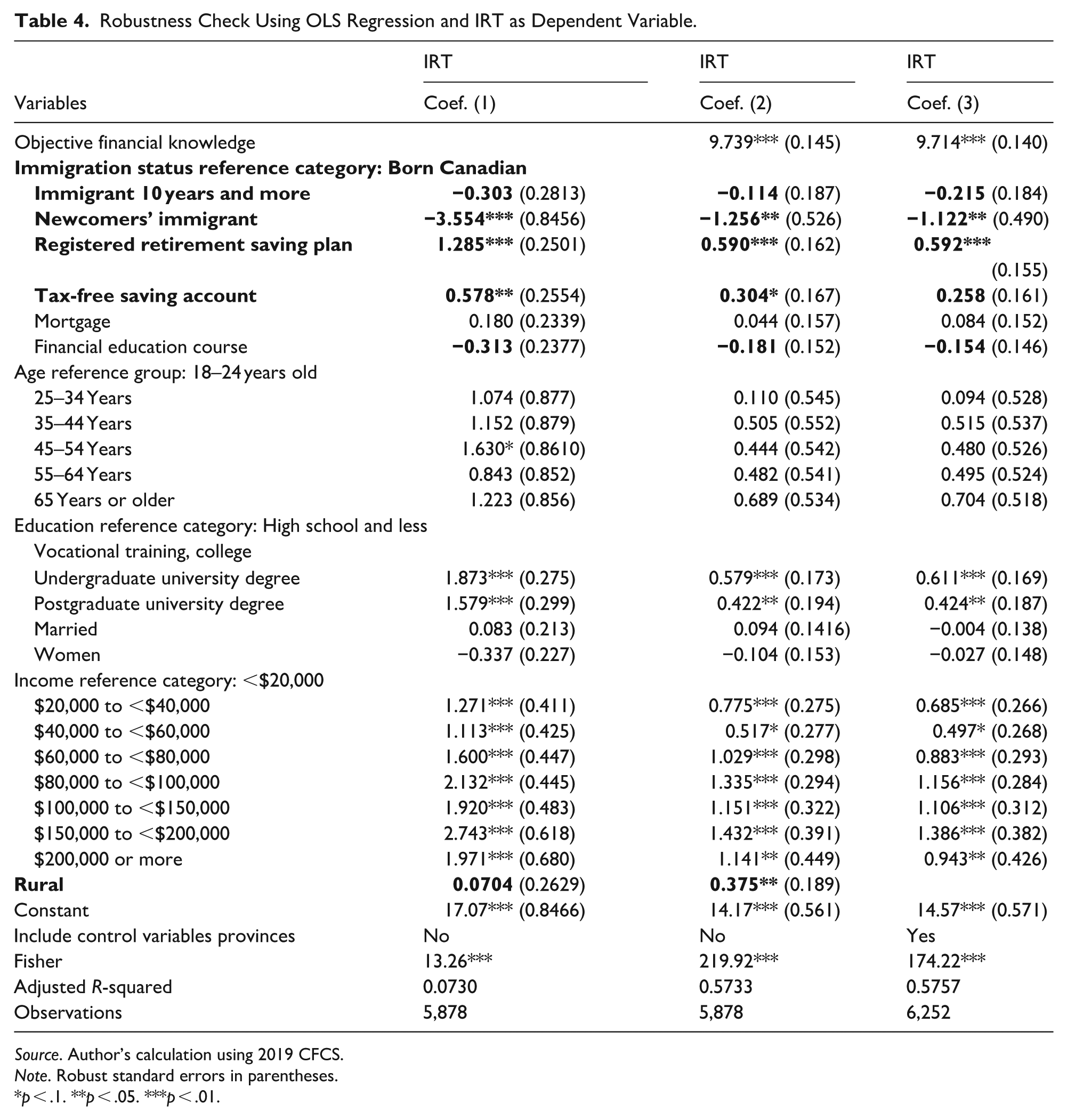

To assess the robustness of the findings, this study employs an alternative measure of financial knowledge (as the dependent variable), the index of financial knowledge (IRT), which is available in the 2019 CFCS data. First, IRT is regressed on the same independent variables as in Equation 1. Secondly, since OFK is derived from the same logic design as IRT (OFK and IRT strongly correlate, r = .75, p < .01), OFK is added to the regression as an independent variable to test the robustness of the relationship between newcomers and born Canadians. Should the differences still be significant between newcomers and born Canadians despite including OFK as an explanatory variable, it would be fair to indicate that the findings are stable and robust. Furthermore, since Rostamkalaei and Riding (2020, p. 963) found a significant correlation between objective financial knowledge and provinces of residence, variables for provinces were included as control variables. To avoid multicollinearity, the variable for rural versus urban was excluded from the regression.

With

Finally, as a robustness check (Equation 3), this study also examines the interaction between immigration status, savings participation, and the financial knowledge index score to determine whether social equity (newcomers’ status) affects financial literacy.

Results and Interpretation

Compared to their Canadian-born counterparts, newcomers have a significantly lower level of financial knowledge. They are less likely to participate in the RRSP, 5 which is consistent with Khan et al. (2022, p. 3184), Rostamkalaei and Riding (2020, p. 951), and Morissette (2019, p. 21). The results suggest that newcomers are 64% less likely to achieve the highest score on financial knowledge and 52% are less likely to participate in the RRSP compared to their Canadian-born counterparts, which does not meet the expectations of equality of opportunity and block equality of the compound theory of social equity. Block equality postulates equality between different social groups (Frederickson, 1990, p. 230; 2010, p. 56). Equality of opportunity states that equality exists when two individuals have the same chances or probability of obtaining or accessing a good or service (Frederickson, 1990, p. 231; 2010, p. 57).

However, the results suggest no statistical significance in TFSA participation between newcomers and those born in Canada. These results align with the expectations of equality of opportunity and block equality, as outlined in the compound social equity theory. It is also worth noting that the results indicate no significant difference between Canadian-born and well-established immigrants in financial knowledge and savings participation, which is congruent with the expectations of equality of opportunity and block equality of the compound social equity theory.

In addition, the results suggest a significant association between RRSP participation and financial knowledge. Compared to their counterparts, those who participated in RRSPs are 35% more likely to achieve the highest score on financial knowledge. Conversely, those with the highest financial knowledge score are 35% more likely to participate in RRSPs. Further, the results indicate no significant association between having taken financial education courses in the past 5 years and financial knowledge performance, contrasting previous findings documenting a significant association between financial education and financial knowledge (D. W. Rothwell & Wu, 2019, p. 1729).

However, there is a significant relationship between having taken financial education courses in the past 5 years and TFSA participation (p < .01), which aligns with scholars who documented a significant relationship between financial education and enhanced financial capability (D. W. Rothwell & Wu, 2019, pp. 1725–1726; Wagner & Walstad, 2019, p. 234; Xiao & O’Neill, 2016, p. 712; Xiao & Porto, 2017, p. 805). Compared to their counterparts, those who reported having taken financial education courses in the past 5 years are 40% more likely to report participating in a TFSA, all other things being equal.

On demographic variables, the results suggest that income and education levels make a difference in financial knowledge performance and participation in the RRSP and TFSA, consistent with Khan et al. (2022, p. 3184) and Zaman (2017, p. 342). Compared to their counterparts, households with the highest incomes and those holding university degrees are more likely to achieve the highest scores in financial knowledge and participate in RRSPs and TFSA. Furthermore, gender, marital status, and living in rural regions have a significant impact on TFSA participation, but do not have a statistically significant impact on RRSP participation or financial knowledge performance. This result contrasts with previous findings that document a gender gap in financial knowledge (see Bucher-Koenen et al., 2017, p. 255; Lusardi & Mitchell, 2008, p. 413). Compared to their counterparts, those who reported marriage are 30% more likely to participate in a TFSA. However, marriage does not statistically affect RRSP participation and financial knowledge performance. Compared to men, women are 24% more likely to participate in TFSA, consistent with Zaman (2017, p. 342). Those who reported living in rural regions are 18% less likely to participate in TFSA than those who reported living in urban regions in Canada.

As a robustness check, the financial knowledge index (IRT) is regressed on the same independent variables as in Equation 1. Overall, the findings remain consistent with the logistic regression results. Compared to their Canadian-born counterparts, newcomers have significantly lower levels of financial knowledge. 6 This result is consistent with Khan et al. (2022, p. 3184) and Rostamkalaei and Riding (2020, p. 951). More precisely, the results suggest that newcomers scored 1.122 significantly less on the financial knowledge questions than their Canadian-born counterparts, all other things being equal (see Table 4). Additionally, the results indicate a significant correlation between RRSP participation and financial knowledge. Those participating in RRSPs scored 0.592 significantly higher on financial knowledge questions than those without an RRSP, suggesting that long-term retirement savings or savings inclusion have a positive influence on financial knowledge. Those with a postgraduate university degree scored 0.424 significantly more on the financial knowledge questions than those with a high school degree. Compared to those with the lowest household income (less than $20,000), individuals with higher incomes scored significantly higher on the financial knowledge questions. All these results underscore the social equity gaps in financial knowledge, not only for newcomers but also for those with lower educational attainment and lower income. The results suggested that immigration and socio-economic status were sources of block inequalities and inequalities of opportunities in financial knowledge.

Meanwhile, there is no significant association between having taken financial education courses in the past 5 years and financial knowledge performance. There are also no significant associations between financial knowledge performance and the following variables: age, gender, marital status, and mortgage ownership. The results of the interaction variables between immigration status and the financial literacy variables reveal that newcomers without an RRSP scored 3.71 points lower on the financial knowledge questions than Canadian-born individuals without an RRSP. Furthermore, newcomers with an RRSP scored on average 3.43 points lower on the financial knowledge questions than Canadian-born individuals with an RRSP, highlighting equity issues as immigration status makes a statistically significant difference in financial knowledge performance.

Discussion

This study contributes to the limited work that has examined the financial knowledge of immigrants (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 953). Grounded in the 2019 CFCS data, this study tested the equality of opportunity and block equality of the compound theory of social equity (Frederickson, 1990, p. 230; 2010, p. 56) in financial knowledge and saving participation between newcomers and people born in Canada. First, immigrant populations matter because they are identified as a vulnerable group, are at risk for financial precarity (Khan et al., 2022, p. 3184), and are at high risk of income poverty (Khan et al., 2022, p. 3185; D. Rothwell & Robson, 2018, p. 17). Second, immigrant populations have received scant attention in the public administration literature because the related variables were excluded from publicly available data (Biaou & Charbonneau, 2024, p. 48) or because gender equity (Shen et al., 2023) is a more attractive focus for scholars and readers more broadly.

The regression results suggest that social equity issues exist in financial knowledge and retirement saving participation between newcomers and people born in Canada, which does not meet the expectations of equality of opportunity and block equality of the compound social equity theory. Block equality postulates equality between different social groups (Frederickson, 1990, p. 230; 2010, p. 56). Equality of opportunity states that equality exists when two individuals have the same chances or probability of obtaining or accessing a good or service (Frederickson, 1990, p. 231; 2010, p. 57). However, the results meet the expectations of equality of opportunity and block equality of the compound social equity theory for TFSA participation, given that there were no statistically significant disparities in TFSA participation between newcomers, well-established immigrants, and those born in Canada. Newcomers’ financial knowledge and participation in retirement savings are among the social inequities that the financial ecosystem, including governments, must address to foster a more inclusive society.

In addition, the regression results suggest that block inequalities and inequalities of opportunity are not only issues for newcomers but also for those with lower educational attainment and lower income. The financial ecosystem must step up its efforts to bring about change by targeting newcomers, lower-income households, and individuals with lower educational backgrounds in policies, programs, and interventions, without neglecting other socio-demographics. Although this paper does not find any significant evidence of sources of inequities across age and gender, inequities may still exist when considering segmented equality, which was out of scope in this study. Segmented equality of the compound theory of social equity considered that equality could be present within a segment in a group and inequality between two segments within the same group (Frederickson, 1990, p. 230; 2010, p. 56). Inequities in financial knowledge may exist between newcomers who are women and newcomers who are men, or between older newcomers and younger newcomers.

To explain this social inequity, scholars argued that language barriers (Khan et al., 2022, p. 3194; Rostamkalaei & Riding, 2020, p. 970), historical experiences (Rostamkalaei & Riding, 2020, p. 953), and a policy framework favoring individual responsibility instead of collective responsibility (Rostamkalaei & Riding, 2020, p. 952) impede financial literacy and inclusion of newcomers. To complement these views, this study offers recommendations that practitioners could lean on to bring about change.

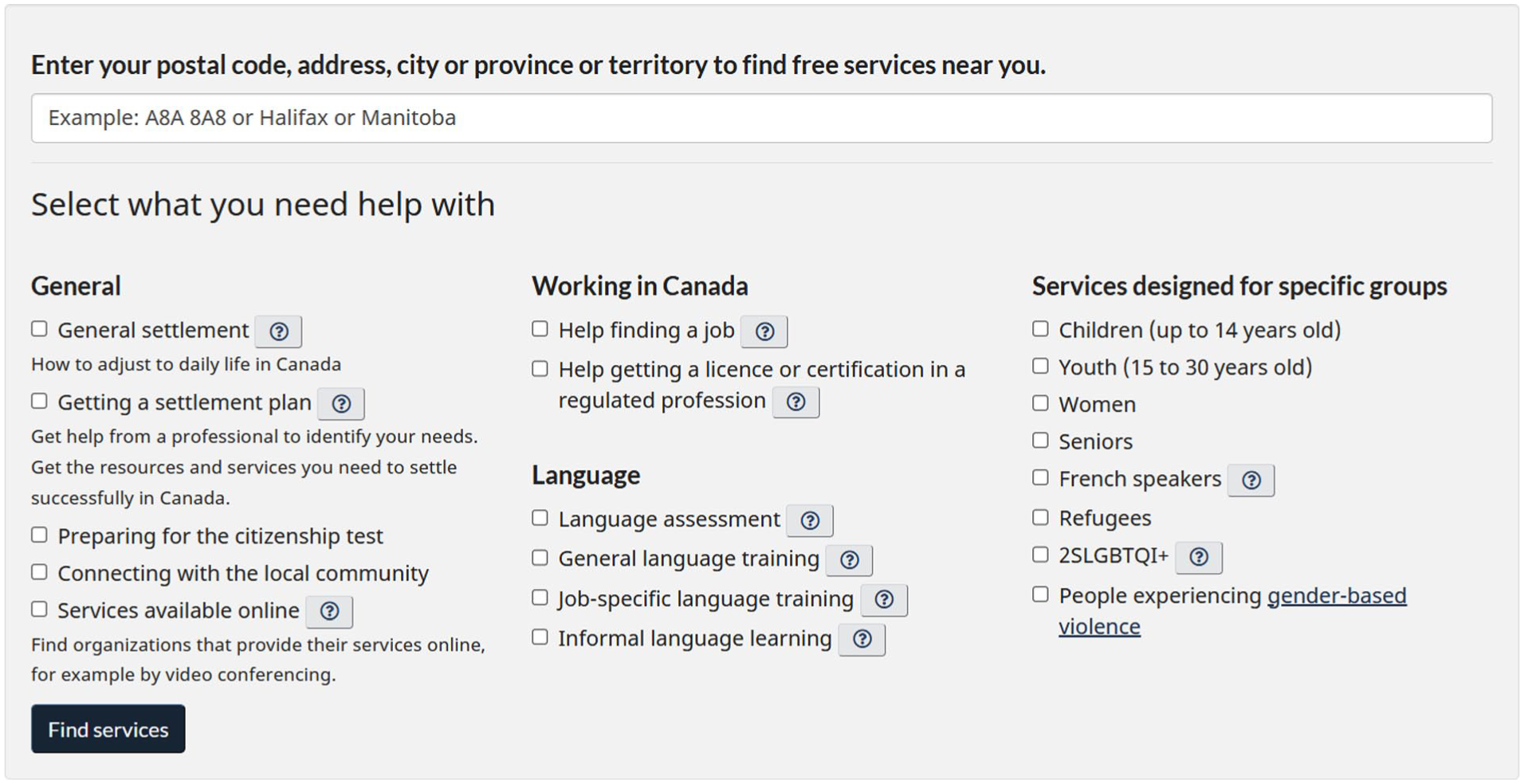

The first recommendation is that IRCC could add a category box for financial education courses in the “General section” on the Settlements Services Canada.ca webpage (see Figure 2). No category box is displayed for financial education courses 7 albeit a couple of settlement organizations offer such courses. 8 Adding that category box allows newcomers to filter and find settlement organizations offering financial literacy courses easily. Further, it might be beneficial for newcomers that IRCC consider adding FCAC’s information on the “Prepare Life” Prepare Financially IRCC’s page 9 to raise awareness of FCAC’s banking information before newcomers arrive in Canada. FCAC’s information is available on the “New Life in Canada” Money 10 IRCC’s page, but no such information exists on the “Prepare for Life” Prepare Financially IRCC’s page. 11

For newcomers’ financial literacy, although IRCC participates in the Interdepartmental Committee on Financial Literacy 12 Chaired by FCAC, the author recommends that FCAC consider establishing a Financial Literacy Working Group for Newcomers, like the one for Indigenous Peoples, should there be no duplication of effort. FCAC established a Financial Literacy Working Group for Indigenous Peoples to respond to specific financial literacy needs of Indigenous Peoples, even though Indigenous Services Canada participates in the Interdepartmental Committee on Financial Literacy (see Note 12).

Future research could document the effectiveness of offering financial services in non-official languages (Rostamkalaei & Riding, 2020, p. 970), as well as the procedure and effectiveness of offering a financial education program for newcomers as part of a welcoming settlement plan (Khan et al., 2022, p. 3196). Evaluating the impact of immigration on the financial literacy, financial inclusion, and financial well-being of newcomers would also be worthwhile to study in Canada and globally. Does immigration significantly matter in the financial outcomes of newcomers? Does immigration make newcomers better off, or does it worsen their financial well-being, financial inclusion, and financial literacy? Future research in public administration could also expand our common understanding of social equity in other public matters, such as budgeting for social equity (McDonald & McCandless, 2025) and applying social equity in a collaborative governance network (see Blomqvist & Winblad, 2022, pp. 235–238; Grossi & Argento, 2022, pp. 279–281; Hou et al., 2022, p. 424; Lægreid & Rykkja, 2021, pp. 685–687; Lee & Ospina, 2022, pp. 64–68, for a starting point).

Conclusion

This study utilizes the 2019 CFCS data to provide up-to-date results and test the equality of opportunity and block equality of the compound theory of social equity (Frederickson, 1990, p. 230; 2010, p. 56) in financial knowledge and retirement savings participation between newcomers and individuals born in Canada. Block equality postulates equality between different social groups (Frederickson, 1990, p. 230; 2010, p. 56), and equality of opportunity states that equality exists when two individuals have the same chances or probability of obtaining or accessing a good or service (Frederickson, 1990, p. 231; 2010, p. 57).

The results show that social equity issues exist in financial knowledge and retirement saving participation, which do not meet the expectations of equality of opportunity and block equality of the compound theory of social equity. Consistent with previous studies (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 953), the logistic regression results of this study suggest that compared to their Canadian-born counterparts, newcomers are 64% less likely to achieve the highest score on financial knowledge and are 52% less likely to participate in the RRSP. Compared to well-established immigrants, newcomers are 61% less likely to achieve the highest score on financial knowledge, and 46% are less likely to participate in the RRSP. The robustness check results suggest that newcomers scored 1.122, significantly less on the financial knowledge questions than their Canadian-born counterparts, all other things being equal.

However, the results for TFSA participation meet the expectations of equality of opportunity and block equality as outlined in the compound social equity theory. The results suggest no statistically significant difference in TFSA participation among newcomers, well-established immigrants, and those born in Canada. There was no statistically significant difference in financial knowledge and savings participation between well-established immigrants and people born in Canada.

This study contributes to the public administration literature in two ways. First, given that the hypothesis had been tested in previous studies using the 2009 and 2014 CFCS data (Khan et al., 2022; Rostamkalaei & Riding, 2020), this study contributes to the limited work that has examined the financial knowledge of immigrants (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 953) by referring to previous studies methodology but using the most recent CFCS data grounded in the compound social equity theory that Frederickson (1971, 1990) proposed following the Minnowbrook conference held in 1968. This study’s theoretical lens echoes Gerring and Seawright (2022, p. 62), who asserted that “[o]nce a theory has been propounded, it must be interrogated by the research community.” Disseminating studies that tested theories helps advance and challenge our common understanding of social matters. For Gerring and Seawright (2022, p. 67), “[w]hen a study tests a hypothesis drawn directly from a previous study (that tests the same hypothesis) [, the result may be described as a replication” and contributes to knowledge as a reanalysis (Gerring & Seawright, 2022, pp. 39, 67).

Second, this study provides practical recommendations on information gaps that may help explain this social inequity. By connecting the findings with practical recommendations that are of interest to public administrators, this study responds to the call of public administration editors for a more pragmatic approach to convey results (Frank et al., 2024; McDonald et al., 2022). In this study, the author recommends establishing a Financial Literacy Working Group for Newcomers at the federal level (like the one for Indigenous Peoples) and adding a financial education courses category box on the settlement’s services Canada.ca webpage (see Figure 2).

Qualitative fingerprint (as of November 25, 2024).

However, it is worth mentioning that by employing regressions without time variation and continuous variables not present in the dataset, the results of this study cannot and should not be interpreted as indicating causality, which constitutes a limitation. Given the “static” nature of the data used in this study and the lack of continuous variables, examining causality was impossible. As such, future research using longitudinal panel data could focus on causality techniques such as matching and difference-in-difference while evaluating the impact of immigration on the financial literacy, financial inclusion, and financial well-being of newcomers, for instance. For readers’ awareness, it is also important to note the extremely low pseudo R-square values (0.04–0.14) for the logistic regressions (see Table 3), although they are consistent with previous studies (see D. Rothwell & Wu, 2019, p. 1741). The findings should be interpreted as correlational, and the data model presented in this paper should not be used for forecasting purposes.

Logistic Regression Results With OFK, RRSP, and TFSA as Dependent Variables.

Source. Author’s calculation using 2019 CFCS.

Note. Values in bold highlight the key variables of interest. Robust standard errors in parentheses.

p < .1. **p < .05. ***p < .01.

Robustness Check Using OLS Regression and IRT as Dependent Variable.

Source. Author’s calculation using 2019 CFCS.

Note. Robust standard errors in parentheses.

p < .1. **p < .05. ***p < .01.

Adopting a holistic approach to empower newcomers financially is crucial since immigrant populations are at high risk of income poverty (Khan et al., 2022, p. 3185; D. Rothwell & Robson, 2018, p. 17) and have lower levels of financial knowledge (Khan et al., 2022, p. 3184; Rostamkalaei & Riding, 2020, p. 953). Immigrants or newcomers (Buckland & Visano, 2022, p. 49) play a vital role in the Canadian economy by contributing to population growth, cultural diversity, and a talented workforce (Prosper Canada, 2015). As the number of newcomers has grown, more than 8.3 million in 2021, compared to 7.5 million in 2016, 13 the government is expected to contribute to building houses (Department of Finance, 2024, p. 9) and ensure newcomers feel “financially” at home upon arrival by implementing a comprehensive welcoming program. Nevertheless, investing in the financial literacy of vulnerable groups can lessen the burden on social welfare.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.