Abstract

This study examined the effects of an integrated intervention involving exposure to aged future self and a writing task on retirement planning among 235 young and middle-aged working adults. Participants were randomly assigned into three groups: control group (CS), experimental group (FS), and experimental group with a writing task (FSW). The experimental groups viewed an age-morphed photo of their future selves while the control group saw a photo of their current selves. Afterward, the FSW group completed a five-day diary writing task about improvement plan for their aged future selves’ well-being, while the FS and CS groups did not. Although no significant main effects of experimental conditions were shown, middle-aged FSW participants reported more financial and psychological retirement planning at the six-month follow-up compared to the CS group and young FSW participants. The implications for targeting specific age groups using unique psychological intervention approaches to encourage retirement planning were discussed.

• This study introduces an optimization of previous self-continuity interventions by smart integration combining aged-morphed photos and diary writing, demonstrating its effectiveness in enhancing future self-continuity and retirement planning among middle-aged working adults. • It highlights the differential intervention effects on young versus middle-aged working adults, emphasizing the importance of age-specific intervention strategies in retirement planning research. • By tracking the impact of interventions over 6 months, the study contributes to the literature on short-term effects of psychological interventions on retirement planning, addressing a gap in previous studies that often focused on immediate outcomes.

• Targeted retirement planning programs should be created to address the specific needs of different age groups, promoting better preparation for retirement. • Healthcare professionals and policymakers can utilize the integrated approach of visual and writing interventions to enhance future self-continuity, leading to improved retirement planning of working adults.What This Paper Adds

Applications of Study Findings

Introduction

The rapid aging of the world’s population and increased life expectancy have extended the number of years spent on retirement. As one of the regions with the highest life expectancy, the proportion of Hong Kong population over 60 years is projected to double in the next two decades, reaching 40% of its entire population by 2044 (Census and Statistics Department, 2023). Moreover, older Hong Kong adults aged 60 years will live another 25–30 years after retiring from their full-time employment, which is approximately a third of the average lifespan (Census and Statistics Department, 2023). Therefore, the demographic changes present an increasing number of working adults facing developmental challenges in preparing for and entering retirement.

Systematic reviews of retirement transition studies showed that although some of the retired individuals were healthy and satisfied with their post-retirement lives, other retirees found retirement stressful and experienced declines in health and well-being after retirement (Ugwu et al., 2024; van der Heide et al., 2013). Many scholars suggested that performing retirement planning, such as developing realistic expectations to financial needs, can facilitate a smooth retirement transition and yield better post-retirement outcomes (Muratore & Earl, 2015; Yeung & Zhou, 2017). Despite its beneficial effects, a substantial proportion of the population is still not actively engaged in retirement planning. For example, a survey found that more than 30% of working adults in Hong Kong had not made any preparations for their post-retirement financial needs (Hong Kong Deposit Protection Board, 2024). The low degree of preparation is particularly problematic in Hong Kong, where retirement protection relies heavily on personal savings and investments (Ng et al., 2025). Drawing on the past literature on retirement planning, the present study aims to examine (1) whether viewing an age-morphed photo alongside a five-day diary writing task can enhance one’s preparation for retirement in various domains over time and (2) whether this integrated intervention has a differential effect on young and older age groups.

Retirement Planning and Future Self-Continuity

Retirement planning is a goal-oriented behavior in which individuals make efforts to prepare for their retirement lives (Yeung & Zhou, 2017). Apart from financial aspects, Law et al. (2006) identified three additional domains of retirement planning, namely, health, psychological, and social planning. A meta-analysis indicated that engagement in retirement planning was associated with favorable post-retirement outcomes in middle-aged American and European adults, including fewer mental and physical health problems and higher life satisfaction (Topa et al., 2009). A longitudinal study conducted among Hong Kong Chinese retirees also found that retirees who engaged in more pre-retirement preparatory activities acquired greater resources in retirement transition, which contributed to better physical and psychological well-being one-year postretirement (Yeung & Zhou, 2017). Therefore, encouraging working adults to make plans for retirement is crucial as it can facilitate a smooth transition from employment to retirement and maintenance of well-being in late adulthood.

Like many important decisions for the future, engaging in retirement planning involves tradeoffs among costs and benefits occurring at different times. For example, spending money on a luxury item or a vacation implies less savings for retirement and old age, while fast food consumption or lack of regular physical activity has a negative impact on physical health. These decisions, such as saving for retirement and spending within a budget, are difficult to make precisely because the present has a stronger impact on emotions than the prospect of an uncertain future outcome (Dunn et al., 2007). Indeed, early studies have found that many individuals discount the value of future rewards for an immediate gratification (Frederick et al., 2002), resulting in less preparation for retirement.

Acknowledging various theories concerning the relationship between current and future selves, Ersner-Hershfield, Wimmer, and Knutson (2009) proposed the future self-continuity hypothesis to account for temporal discounting and suggested that individuals who feel more connected to their future selves are more likely to sacrifice their present pleasure for the future benefits. Future self-continuity refers to the sense of similarity and connection between the current self and the future self (Ersner-Hershfield, Garton, et al., 2009; Sun et al., 2023). Previous studies adopting different intervention strategies have shown that individuals with higher future self-continuity are more likely to delay monetary temporal discounting and save money for their future (Hershfield et al., 2011; Kausel et al., 2024). For example, Kausel et al. (2024) presented customers of an investment firm with a text referencing their future selves, accompanied with an age-morphed image of themselves. They found that, compared with participants who received no future self-reference, this intervention enhanced participants’ connection to their future selves, which in turn increased their intentions to save for retirement and the actual amount of money invested at a five-day follow-up. Despite that the effect of future self-continuity may extend to non-financial intertemporal decision-making, such as charitable donation and physical exercise (Rutchick et al., 2018; Zhang & Aggarwal, 2015), prior work largely focuses on the relationship between future self-continuity and temporal discounting in the financial domain of retirement planning (Bryan & Hershfield, 2012; Marques et al., 2018). Therefore, the present study first aims to examine whether the beneficial effect of future self-continuity on financial planning can also be extended to health, psychological, and social domains of retirement planning.

Activating Future Self-Continuity Through Exposure to an Age-Morphed Photo

Interactive tasks and writing are often used to manipulate future self-continuity (Hershfield et al., 2011; Rutchick et al., 2018). For example, imagination exercises require participants to describe their future selves through guided imagery (Blouin-Hudon & Pychyl, 2017; Sokol & Serper, 2019) or to think explicitly about their future selves through hypothetical vignettes (Bryan & Hershfield, 2012). Such tasks have been shown to increase saving behavior (Bryan & Hershfield, 2012) and physical activity (Rutchick et al., 2018), and reduce procrastination (Blouin-Hudon & Pychyl, 2017). However, imagining a future self poses many challenges, for example, one may be uncertain which of these infinite future selves to identify with. In addition, the effects of manipulation largely depend on one’s imaginative ability and motivation, which vary considerably across individuals (Hershfield et al., 2011).

An alternative approach to activate future self-continuity is to have participants exposed to age-morphed representations of their future selves (Hershfield et al., 2018). A more vivid impression of oneself in the future facilitates anticipation about his/her future life, which in turn allows the person to be better informed about the future consequences of a present decision. Previous studies have shown an increased tendency to make more future-oriented decisions among participants who were exposed to their age-morphed future selves. For example, after exposing to images of their age-morphed future selves, young adults exhibited an increased tendency to accept later monetary rewards (Hershfield et al., 2011) and to attend more long-term financial planning workshops (Sims et al., 2020).

Exposure to an age-morphed future self photo and guided imagery are believed to work in tandem that exposure overcomes the reliance on imaginative ability and motivation, while guided imagery ensures individuals to contemplate their future selves in a specific scenario. For example, a recent study has demonstrated that an integrated exposure and imagination exercise using virtual reality to embody age-morphed future selves can increase the rate of initiating goal-oriented behaviors in university students 1 week after the experiment through enhanced connectedness with future self (Ganschow et al., 2024). Furthermore, the vividness of a future self, and consequently the connectedness with that self, may be more challenging to achieve for a distant future self than for a proximal one (Löckenhoff & Rutt, 2017). Therefore, a more intensive intervention approach is preferred for retirement goals benefiting a distant future self (e.g., retirement savings) (Hershfield et al., 2018).

Strengthening Connection to Future Selves Through Combining a Diary Writing Task

In addition to exposure and guided imagery, another effective way for increasing the salience of future self and continuity between current and future selves is through a diary writing task (Rutchick et al., 2018; Simić et al., 2021). Visual interventions like age-morphed images (Hershfield et al., 2011) primarily enhance future self-continuity by presenting one’s future self in a vivid way, making it feel more real and connected to his/her future self and thus reducing temporal discounting. In contrast, writing tasks, such as writing a letter to a distant future self (Rutchick et al., 2018; Simić et al., 2021), often engage more narrative or goal-oriented processes. These may promote clarification and prioritization of future-oriented goals, fostering commitment to future goals. For example, Rutchick et al. (2018) asked their undergraduate participants to write a letter to their distant future selves in 20 years and completed a series of daily diaries. They found that participants exercised more in the days following the writing task. Similarly, Simić et al. (2021) found that participants who wrote a letter to their distant future selves in 10 years exhibited greater intentions to adhere to the COVID-19 safety measures, compared with those who wrote to their proximal future selves.

In a systematic review of 24 future self-continuity intervention studies focused on behavioral changes, Grekin et al. (2025) found that a majority of interventions employed explicit techniques, such as viewing aged-morphed images (Hershfield et al., 2011; Kausel et al., 2024) or vividly imagining a future self (Gao et al., 2024; Schanbacher et al., 2024), followed by writing letters to one’s future self (Rutchick et al., 2018; Simić et al., 2021). Although conclusions remain tentative due to heterogeneity in intervention approaches, studies reporting larger effect sizes were more likely to involve age-morphing technology (Gao et al., 2024; Hershfield et al., 2011; Sims et al., 2020), suggesting that such techniques may be more effective than other intervention types. Furthermore, integration of multiple approaches can yield additive or synergistic effects (Ganschow et al., 2024), potentially outperforming single-modality interventions such as visual simulation alone. Therefore, to leverage the strengths of aforementioned interventions, the present study integrates exposure to an age-morphed future self with guided imagery and a five-day daily writing task that requires participants to identify ways to improve the well-being of the person inside the age-morphed photo whom they have seen in the experiment. It aims to examine whether this integrated intervention approach can strengthen the positive effect of future self-continuity on various domains of retirement planning in young and middle-aged working adults.

Age Differences in Retirement Planning Among Working Adults

While retirement planning may be relevant to most working adults, its relevancy might differ by age. Previous studies suggest that young and middle-aged adults differ in their perception towards time remaining in their lives, which impacts the degree to which they prepare for aging, including retirement (Kornadt et al., 2019). For example, a previous study conducted among the general population in Kirkcaldy, Scotland, found that fewer than 70% of non-retired respondents aged under 50 had given some or much thoughts to retirement, whereas more than 80% of those aged 50 and older had considered retirement-related issues (Anderson et al., 2000). Similarly, Qi et al. (2022) found that only about 20% of American adults aged between 22 and 36 had prepared for their retirement, compared to 30% of their older counterparts.

The low percentage of retirement planning among working adults until later in their career might be due to its low perceived relevancy to oneself. Previous study in educational psychology found that college students who completed writing assignments about the personal usefulness of course materials showed better performance in introductory science courses (Priniski et al., 2019). Inspired by such an idea and applied it to our study, we increased personal relevancy by asking participants to identify ways to improve the well-being of the person inside the age-morphed photo whom they have seen in the experiment. With the increase in personal relevancy, we hypothesize that middle-aged working adults might find the intervention to be more relevant to their future selves compared to young working adults.

The Present Study

Given the impacts of increased life expectancy on retirement life and low engagement in retirement planning, the present study aims to examine (1) whether an integrated intervention by viewing an age-morphed photo alongside diary writing can effectively enhance different domains of retirement planning among young and middle-aged Hong Kong Chinese working adults over time and (2) whether the intervention has differential effects on young and middle-aged working adults. Specifically, this study first examines whether exposure to age-morphed photo of oneself and guided imagery at the baseline (Time 1) will increase engagement in retirement planning two weeks (Time 2) and six months (Time 3) later. The time interval of two weeks was adopted with reference to previous studies examining the relationship between future self-continuity and behavioral changes (e.g., Blouin-Hudon & Pychyl, 2017; Rutchick et al., 2018), while six-month timeframe allowed participants with enough time to carry out retirement planning activities and for examining the short-term intervention effects (Hershey et al., 2007; Schanbacher et al., 2024; Simić et al., 2021). Additionally, this study examines whether a five-day diary writing task can further increase retirement planning two weeks and six months later. Moderating effect of age on retirement planning at two-week and six-month follow-ups is also examined. The study consisted of three conditions, a control group viewing a photo of one’s current self (CS), an experimental group viewing a photo of an aged future self (FS), and an experimental group viewing a photo of an aged future self plus a five-day diary writing task (FSW). Four hypotheses are proposed:

After exposure to the age-morphed photo of oneself and guided imagery, participants in the experimental groups (FS and FSW) will engage in more retirement planning two weeks later than the participants in the control group.

After exposure to the age-morphed photo of oneself and guided imagery, participants in the experimental groups (FS and FSW) will engage in more retirement planning six months later than the participants in the control group.

Middle-aged participants in the experimental groups (FS and FSW) will engage in more retirement planning activities six months after the experiment compared to their younger counterparts in the control group.

After the five-day diary writing task, middle-aged participants in the FSW group will engage in more retirement planning activities six months after the experiment compared to middle-aged participants in FS and CS groups.

Method

Participants and Procedures

Ethical approval for this study was obtained from the affiliated university. Participants were recruited through several means, including the promotion flyers distributed by the human resources department of public and private organizations and labor unions in Hong Kong, and through a research marketing firm. An online registration form was distributed to the target employees who were aged 20–60 years. A total of 235 working adults (age = 43.2 years, SD = 11.3; 60.4% female) were successfully recruited and completed all subsequent assessments (i.e., retention rate = 100%). A majority of the participants (80.0%) were full-time workers, and 52.3% of them had a monthly income ≥ HKD25,000 (approximately USD3,216).

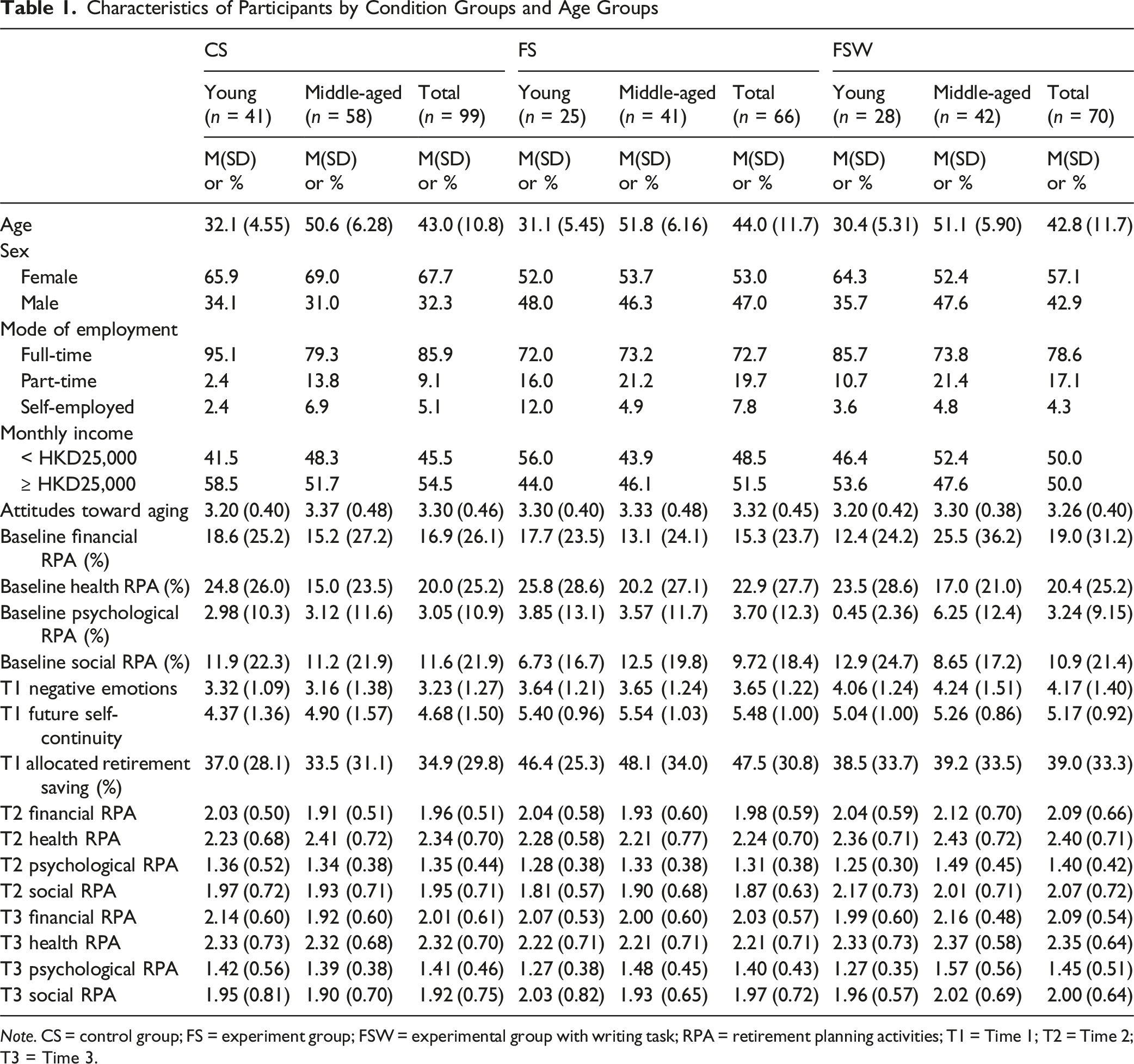

Characteristics of Participants by Condition Groups and Age Groups

Note. CS = control group; FS = experiment group; FSW = experimental group with writing task; RPA = retirement planning activities; T1 = Time 1; T2 = Time 2; T3 = Time 3.

In the experiment (Time 1), the participants in the FS and FSW groups were presented with an age-morphed photo of their future selves (approximately aged 65–70), which was immediately created using the AgingBooth app (PiVi & Co, 2023), while the participants in the CS group were presented with a photo of their current selves. Each participant was asked to undergo a guided imagery task in which he/she had to imagine himself/herself walking along the beach with the person in the photo. This imagery task helped to strengthen the connection with the person seen in the photo. After the imagery task, the participants were asked to complete an online questionnaire assessing their emotional reactions to the photo, future self-continuity, and their allocation of an unexpected income to retirement savings and other expenses.

Immediately after the experiment, the participants in FSW group were invited to complete a five-day diary writing task via an online platform. During the five-day period, they received a daily WhatsApp message between 6:00 pm and 7:00 pm inviting them to write down their plans to improve the well-being of their future selves. If they had not completed the diary writing task by 12:00 am, an instant message reminder was sent at 8:00 am in the following morning, allowing them an additional one hour to complete the writing task for the previous day. Thus, the adherence to writing task was 100%. Two weeks (Time 2) and 6 months (Time 3) after the experiment, all participants were contacted again and asked to complete a 10–15-minute online questionnaire assessing their engagement in retirement planning activities. Participants who successfully completed all three assessments received a total amount of HKD300 (approximately USD38.2) as a token of appreciation for their participation.

Measures

Except for the measurements already available in Chinese, the measurement scales were translated into Chinese by two bilingual translators through the back-translation procedure.

Measures Assessed Before the Experiment

Retirement Planning Activities

A locally developed and validated scale of retirement planning activities (Law et al., 2006; Yeung & Zhou, 2017) was adapted, which covers preparatory behaviors in four domains, including financial (five items), health (four items), social life (four items), and psychological (seven items) planning for retirement. Four more items were added in the present study to capture a wider coverage of health (three items) and psychological (one item) planning based on the feedback to the previous research on retirement planning (Yeung et al., 2023; Yeung & Zhou, 2017). The participants were asked to indicate whether they had completed each of the retirement planning activities (0 = had not completed and 1 = completed). The completion percentages of each retirement planning domain were calculated. Higher percentages indicate greater completion rates of planning activities. The Cronbach’s alphas for financial, health, social, and psychological planning were 0.82, 0.81, 0.61, and 0.78, respectively, which were similar to those of a previous study (Yeung, 2013).

Measures Assessed at Time 1 (Immediately After the Experiment)

Negative Emotional Reactions to the Photo

With reference to previous studies assessing emotional responses to an age-morphed photo or avatar (Hershfield et al., 2011; Lee et al., 2020), the participants were asked to rate the extent of their emotional reactions to the photo they had viewed using four emotional adjectives, including negative, unfamiliar, worried, and distressed. These items were rated using a seven-point scale, ranging from 1 = not at all to 7 = extremely. Higher scores indicate more negative emotions. The Cronbach’s alpha was 0.86.

Future Self-Continuity

In the experiment, the participants’ future self-continuity was measured using the overlapping circles scale (Ersner-Hershfield, Garton, et al., 2009) after viewing the photo. The scale consists of a series of seven pairs of increasingly overlapping circles, signifying the degree of perceived connection between current self and future self at the age of 70 years. Participants were asked to select a pair of circles that best represent the level of connection between their current selves and themselves at aged 70 years on a seven-point Likert scale (1 = no overlap between the current and future selves to 7 = almost overlap between the current and future selves). Higher scores indicate greater future self-continuity.

Percentage of Retirement Savings in a Money Allocation Task

With reference to the study of Hershfield et al. (2011), a money allocation task was designed. In this task, the participants were told to imagine that they had just unexpectedly received HKD10,000 (approximately USD1,280) and were asked to allocate it among six options (1) “spend it on something nice immediately,” (2) “use it for household expenditure (e.g., housing or food),” (3) “expenses for improving family members’ future development or healthcare services (e.g., children’s tuition fee or medical expenses),” (4) “save it for retirement,” (5) “invest it in annuity or wealth plan for retirement,” and (6) “others.” Preliminary analyses did not find any significant difference in the amount being allocated to each of the six options among the three condition groups (all ps > .05). The total amount of money allocated to options (4) and (5) were then summed up to indicate the amount of retirement savings while the remaining options were considered and grouped as non-retirement savings.

Measures Assessed at Time 2 and Time 3 (Two Weeks and Six Months After the Experiment, Respectively)

Retirement Planning Activities

A locally developed and validated scale of retirement planning activities (Law et al., 2006; Yeung & Zhou, 2017) was adapted, which covers preparatory behaviors in four domains, including financial (five items), health (four items), social life (four items), and psychological (seven items) planning for retirement. Ten more items were added in the present study to capture a wider coverage of financial (six items) (Stawski et al., 2007), health (three items), and psychological (one item) planning. Preliminary analysis showed that, with the additional items, Cronbach’s alpha of the overall scale was slightly improved from 0.84 to 0.89. These items are reported in the Appendix. Two weeks and six months after finishing the experiment session, the participants rated their engagement in each activity in the past two weeks and six months, respectively, on a four-point Likert scale (1 = not at all to 4 = always). Higher scores represent greater preparation for retirement in the respective domain. The Cronbach’s alphas for financial, health, social, and psychological planning at Time 2 were 0.80, 0.77, 0.62, and 0.85, respectively. The longitudinal invariance across Time 2 and Time 3 was examined by applying constraints on the factor loadings. The results revealed metric invariance (Δχ2 = 36.84, df = 26, p = .07), indicating the stability of factor structure. Therefore, the mean scores of financial, health, social, and psychological planning were computed.

Covariates

Age and sex (0 = female and 1 = male) were measured at the intake. With reference to a local program supporting middle-aged workers (Hong Kong SAR Government, 2025), participants aged below 40 were regarded as young participants while those aged 40 and over were considered as middle-aged participants. Given the positive association between income and voluntary saving and financial planning activities (Hershey et al., 2007; Yeung et al., 2023), monthly income (0 = <HKD25,000 and 1 = ≥HKD25,000) was also recorded. In addition, attitudes towards aging were measured by the 12-item Attitudes to Aging Questionnaire (Laidlaw et al., 2007). Participants rated the items on a five-point Likert scale (1 = strongly disagree to 5 = strongly agree). Higher scores indicate more positive attitudes towards aging. The Cronbach’s alpha was 0.70.

Results

Descriptive Statistics

The means and standard deviations of the major variables are presented in Table 1. Two-way ANCOVAs, with experimental conditions and age groups as between-group variables, were conducted to compare the completion rates of four types of retirement planning activities prior to the experiment. Sex, monthly income, and attitudes toward aging were controlled as covariates. Results revealed no significant main effects or interaction effects between experimental conditions and age groups on the completion rates of all four types of retirement planning activities (all ps > .05), indicating adequate randomization.

Similar two-way ANCOVAs were conducted to compare the levels of negative emotions, future self-continuity, and percentage of retirement savings in the money allocation task at Time 1. Results first revealed that significant main effect of experimental conditions on negative emotions and future self-continuity (F = 22.07, p < .001, ηp2 = .09 and F = 7.95, p = .005, ηp2 = .03, respectively). Contrasts analysis showed that participants in the CS group (estimated marginal mean (EMM) = 3.23, SE = 0.13) reported significantly fewer negative emotions at Time 1 than those in the FS (EMM = 3.68, SE = 0.15), Cohen’s d = 0.37, 95% CI = [0.05, 0.69] and FSW groups (EMM = 4.12, SE = 0.15), Cohen’s d = 0.73, 95% CI = [0.42, 1.05]. In addition, participants in the FS (EMM = 5.48, SE = 0.15) and FSW (EMM = 5.17, SE = 0.15) reported greater future self-continuity than those in the CS group (EMM = 4.49, SE = 0.13), d = 0.65, 95% CI = [0.33, 0.97] and Cohen’s d = 0.40, 95% CI = [0.09, 0.71]. No other significant main effects or interaction effects between experiment conditions and age groups were found on other outcome variables at Time 1.

Intervention Effect Over Time and Moderating Effect of Age

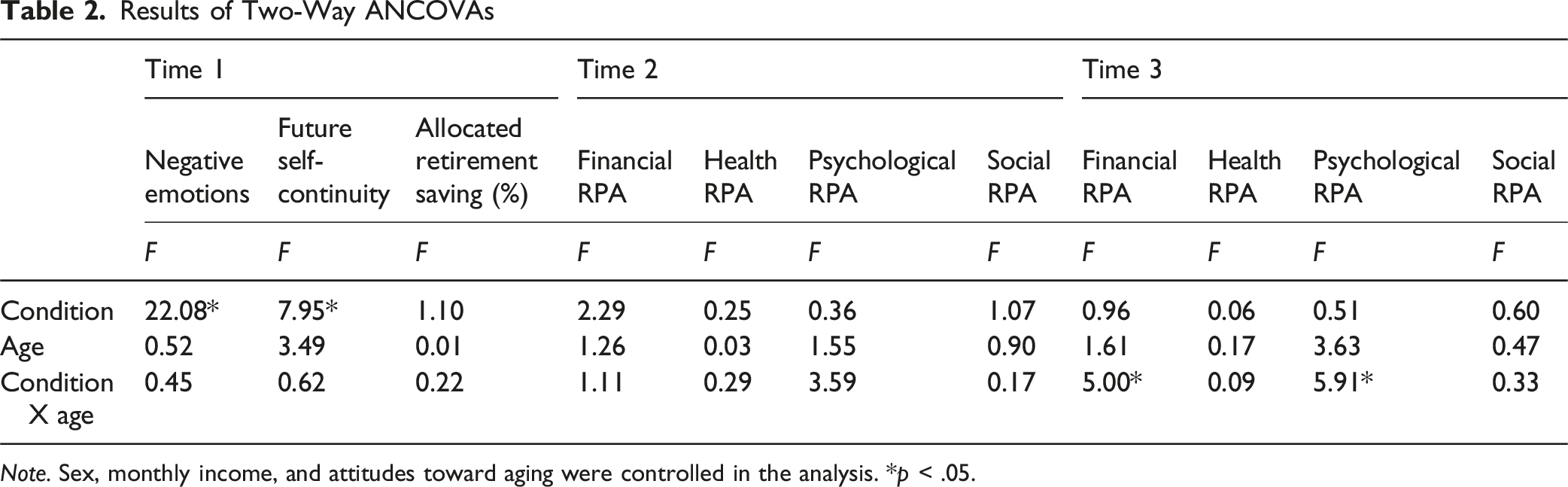

Results of Two-Way ANCOVAs

Note. Sex, monthly income, and attitudes toward aging were controlled in the analysis. *p < .05.

Two-way ANCOVAs were conducted to examine whether participants in the FS and FSW groups engaged in more retirement planning activities at Time 3 (H2) and the moderating effect of age in the relationship between experimental conditions and retirement planning activities at Time 3 (H3 and H4). Experimental conditions and age groups were treated as between-group variables, and the four types of retirement planning activities at Time 3 were the dependent variables. Sex, monthly income, and attitudes toward aging were controlled as covariates. Results revealed significant interaction effects between experimental conditions and age groups on financial and psychological retirement planning activities at Time 3 (F = 5.00, p = .03, ηp2 = .02 and F = 5.91, p = .02, ηp2 = .03, respectively), but no other significant main effects or interaction effects. Contrasts analysis revealed that middle-aged participants in the FSW group (EMM = 2.17, SE = 0.09) reported greater engagement in financial retirement planning activities at Time 3 than their middle-aged counterpart in the CS group (EMM = 1.91, SE = 0.08), Cohen’s d = 0.45, 95% CI = [0.05, 0.86]. In addition, the engagement in psychological retirement planning activities of middle-aged participants in the FSW group (EM mean = 1.58, SE = 0.07) was significantly higher than that of young participants in the FSW group (EMM = 1.29, SE = 0.09), Cohen’s d = 0.63, 95% CI = [0.14, 1.12] and was significantly higher than that of middle-aged participants in the CS group (EMM = 1.38, SE = 0.06), Cohen’s d = 0.43, 95% CI = [0.02, 0.83]. No other significant group differences were found. Therefore, H2 was not supported while H3 and H4 were partially supported.

Robustness of the Moderating Effect of Age

To examine the robustness of age as a moderator, participants were further divided into two groups based on the median age of 45. Those below 45 were regarded as young participants while those aged 45 and above were considered as middle-aged adults. Two-way ANCOVAs were re-conducted to examine the moderating effect of age in the relationship between experimental conditions and retirement planning activities at Time 3. Similar result pattern was revealed. Specifically, the interaction effects between experimental conditions and age groups were significant for psychological retirement planning activities at Time 3 (F = 4.83, p = .03, ηp2 = .02) and were marginally significant for financial retirement planning (F = 2.95, p = .09, ηp2 = .01). Contrast analysis reveals that the engagement in psychological retirement planning activities of middle-aged participants in the FSW group (EMM = 1.59, SE = 0.08) was significantly higher than that of young participants in the FSW group (EMM = 1.21, SE = 0.08), Cohen’s d = 0.60, 95% CI = [0.13, 1.08] and was significantly higher than that of middle-aged participants in the CS group (EMM = 1.38, SE = 0.07), Cohen’s d = 0.46, 95% CI = [0.02, 0.90]. In addition, middle-aged participants in the FSW group (EMM = 2.15, SE = 0.09) reported marginally greater engagement in financial retirement planning activities at Time 3 than their middle-aged counterparts in the CS group (EMM = 1.90, SE = 0.10), Cohen’s d = 0.43, 95% CI = [–0.00, 0.87]. Thus, the hypothesized moderating effect of age is supported regardless of the cutoff age at either 40 or 45.

Discussion

With an increasing life expectancy in Hong Kong, it has become much crucial to promote retirement planning in working adults to facilitate a smooth retirement transition and positive post-retirement outcomes. One of the objectives of the present study was to investigate whether an integrated intervention through exposure to the aged future self photo and guided imagery, alongside a five-day diary writing task, could effectively enhance working adults’ engagement in retirement planning over time. The findings of this study suggested that the integrated intervention could increase future self-continuity immediately after the manipulation and retirement planning six months after the experiment among middle-aged working adults.

This study, besides being the first that targets middle-aged working adults, also extends the literature on future self-continuity and retirement planning by tracking the effect of future self-continuity intervention on retirement planning at a longer term. Previous studies often focused on the immediate experimental effect on intention for retirement saving among young adults (Hershfield et al., 2011, 2018), while the present study examined the two-week and six-month short-term effects on actual engagement in retirement planning, and compared age differences on intervention efficacy between young and middle-aged working adults. Such design allowed the participants in the experimental group to make plans after receiving the experimental manipulation. It is possible that certain preparatory activities require longer time and greater effort, such as quitting harmful habits, buying a property for retirement, or developing social networks with healthcare professionals. Therefore, the lengthened interval between experimental manipulation and assessment allows us to capture the positive change in performing financial and psychological retirement planning activities. Furthermore, the absence of significant intervention effects at the two-week follow-up and the emergence of benefits at six months may suggest a sequential process wherein the intervention initially activates attitudinal shifts within the first six weeks, such as enhanced future self-continuity and intention to prepare for retirement and old age, that subsequently manifests in behavioral changes and results in more retirement planning activities. This aligns with behavior change models suggesting that attitudinal modifications often precede and enable sustained actions over extended periods (e.g., Ajzen, 2020).

This study also expanded the literature on using an integration of age-morphed photo and diary writing intervention to encourage retirement preparation. Previous studies have demonstrated the effectiveness of visual and textual aging primes (e.g., age-morphed image and text featuring future aging) in activating future self-continuity and promoting decisions of retirement saving immediately (Hershfield et al., 2018; Marques et al., 2018). However, such positive effects were not found significant in the present study. Cultural differences in perceptions of aging may partially account for this divergent effect. It has been suggested that a vivid presentation of future self would intensify negative emotions towards future self and promote self-conscious thinking about future appearance and situation, which in turn motivates individuals to make behavioral changes to avoid undesirable consequences in the future (Marques et al., 2018; Stockdale & Sanders, 2020). However, such practices can be discouraging as their positive effects are driven by anxieties about aging. Previous studies have well-documented that Chinese adults often hold a much more negative perception of aging than their Western counterparts (North & Fiske, 2015; Voss et al., 2018). Hence, the exposure to physical display of age progression may trigger fear and anxiety regarding the psychological realm of aging to a greater extent in Chinese adults (Rittenour & Cohen, 2016). Such excessive anxiety towards aging can be counterproductive (Chen, 2016; Lee et al., 2020) as it discounts the benefits of retirement planning via inhabiting the development of closeness to the future self. However, an exploratory mediation analysis in the present sample did not reveal significant mediating effects of negative emotions on the four types of retirement planning at two-week and six-month follow-ups, suggesting that other underexamined factors such as changes in future self-continuity before and after the experiment, cognitive process (e.g., goal clarification), and motivation to change may better explain the underlying mechanism. Future studies are needed to examine more complex, multidimensional explanatory models through which future self-continuity interventions may exert their effects.

Practical Implications

Retirement preparation is not solely a momentary decision but also a psychological and behavioral process unfolds over time (Yeung & Zhou, 2017), and therefore, it is essential to alter the lens through which individuals prepare for their future selves regarding well-being in the context of their retirement lives. The current findings further highlight the importance of interventions that target certain age groups with a particular approach (Löckenhoff & Rutt, 2017). Strategies to activate and strengthen connection to future selves towards retirement life and/or aging may be crucial to contribute to the recursive process underlying the downstream effects of closeness to future self on retirement preparation.

The findings of this study, demonstrating the efficacy of an integrated intervention in boosting financial and psychological retirement planning among middle-aged adults over six months, provide practical insights into real-world settings such as financial advisory services, employee wellness programs, and mobile apps for personal finance. For example, banks or retirement fund providers can incorporate age-morphing tools into client consultations or online platforms to vividly connect customers with their future selves, promoting savings contributions (Hershfield et al., 2011; Kausel et al., 2024). In the context of customer marketing, promoting retirement financial products by framing the purchase decision as acts of self-care for future well-being (e.g., supporting desired lifestyles in retirement) rather than emphasizing financial risks or losses can reduce procrastination and avoidance, particularly for middle-aged workers (Bryan & Hershfield, 2012). Additionally, use of positive slogans on posters, leaflets, or app notifications may enhance users’ recall of personal motivations, thereby encouraging proactive planning (Walker et al., 2020).

Although the five-day diary writing task was demonstrated to be effective in promoting financial retirement planning, its time-intensive nature may limit scalability in practical applications. To address this, the task can be adapted into a simpler format, such as a single guided letter-writing exercise to one’s future self or 5–10-minute daily prompts delivered over 2–3 days via smartphone apps or online portals. Such modifications align with “wise interventions,” which are concise yet targeted psychological strategies that yield sustained behavioral changes by focusing on key processes like self-reflection and goal-setting (Blouin-Hudon & Pychyl, 2017; Walton, 2014). For instance, integrating abbreviated writing prompts into corporate retirement seminars or financial planning apps can make the intervention more accessible, cost-effective, and user-friendly while maintaining its benefits for middle-aged adults.

For young adults, where the intervention showed limited effects possibly due to perceived irrelevance or emotional distance from an elderly future self, strategies to encourage participation in age-morphed image simulations can emphasize engagement and positivity. For example, to mitigate potential anxiety or negative stereotypes triggered by viewing age-morphed images (Lee et al., 2020; Rittenour & Cohen, 2016), simulations can be framed with empowering narratives (e.g., “shape your thriving future”) and paired with nearer-term visualization (e.g., 10–20 years ahead) to heighten personal relevance and perceived control (Stockdale & Sanders, 2020; Sun et al., 2023). Gamification, such as interactive apps with rewards, progress tracking, or social sharing features, or embedding the tool in educational contexts like university career courses can boost motivation (Gao et al., 2024; Sims et al., 2020).

Limitations and Future Directions

Several limitations should be considered when interpreting the findings of the present study. First, although efforts have been put into recruiting working adults from various industries, only 17.4% of blue-collar workers (e.g., manufacturing or transportation) participated in the present study, limiting the generalizability of the findings to certain industries. Second, previous positive intervention effects of exposure to age-morphed photo or avatar and guided imagery on saving and health behaviors were found in Western populations (Hershfield et al., 2018; Marques et al., 2018; Rutchick et al., 2018; Simić et al., 2021) but such effects were not shown in the current Chinese sample. Whether the non-significant intervention effects were due to cultural differences in aging stereotypes await further investigation. Third, the proportion of funds allocated to retirement savings in the money allocation task is a hypothetical task rather than an actual saving behavior, which often fails to capture the complexities of actual decision-making under uncertainty, resource constraints, and competing priorities. Thus, a substantial gap between the simulated allocation and actual saving behaviors may exist. Future studies should incorporate objective measures, such as tracing actual contributions to saving accounts, to better bridge this gap and strengthen the evidence for intervention efficacy. Fourth, while the present study posited that exposure to an age-morphed photo would exert a greater effect on retirement planning, a potential ceiling effect of age-morphing technology may have masked the possible impact of the newly added intervention component, that is, the writing task. Future studies should include a condition in which participants complete only the five-day diary writing task, allowing researchers to differentiate the unique contribution of the writing task from that of the age-morphing technology in shaping retirement planning. Lastly, given the time constraints and concern of potential practice effect, a baseline measure of future self-continuity was not included in the present study. Future studies should incorporate measures of future self-continuity and other attitudinal variables such as intention to prepare for retirement at multiple time points, including baseline and short and longer follow-up intervals (e.g., 1–2 years), to empirically examine the attitudinal-to-behavioral pathway and the medium-term intervention effect and better elucidate the mechanisms underlying delayed behavioral changes in retirement planning.

In conclusion, the present study contributes to the current literature on future self-continuity and retirement planning by identifying effective approaches to increase Chinese middle-aged working adults’ engagement in retirement planning. Future interventions are recommended to integrate activating and strengthening connection to future self to improve retirement planning among middle-aged working adults.

Supplemental Material

Supplemental Material - Activating and Strengthening Connection to Future Selves Boosts Retirement Preparation Among Middle-Aged Working Adults Over a 6-Month Period

Supplemental Material for Activating and Strengthening Connection to Future Selves Boosts Retirement Preparation Among Middle-Aged Working Adults Over a 6-Month Period by Dannii Yuen-lan Yeung, Edwin Ka Hung Chung, Michael Cheuk Hon Chan, Alvin Chong Hang Lam, and Gloria Jiahui Lin in Journal of Applied Gerontology

Footnotes

Acknowledgments

The research team would like to acknowledge all the participants for their support and participation in this study. We would also like to thank Amy C. H. Ng, Jolie W. L. Man, Alvin K. K. Ho, Esther Y. K. Tang, and Daisy S. Li for assistance in data collection.

Ethical Considerations

The study was approved by the Human Subjects Ethics Sub-Committee of City University of Hong Kong (H002953).

Consent to Participate

The written informed consent of each participant was obtained prior to their participation in this study. All experiments were performed in accordance with relevant guidelines and regulations.

Authors’ Contributions

All authors listed have made a substantial, direct, and intellectual contribution to the work. The research funding was received by DY. The study design was developed by DY, MC, and AL. Data collection and management were performed by GL. Data analysis was conducted by DY and EC. The draft of the manuscript was written by DY, EC, and MC, and all authors commented on draft versions of the manuscript. All authors read and approved the final manuscript.

Funding

The study was supported by the General Research Fund from the Research Grants Committee of the Hong Kong Special Administrative Region (Project no.: 11610022), which was awarded to DY. The funder had no role in study design, data collection, data analyses, data interpretation, or preparation of the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data on which this article is based is available from the corresponding author and can be shared upon reasonable request.

Supplemental Material

Supplemental material for this article is available online.