Abstract

Commercial companies are increasingly being recognized as agents of societal governance operating alongside the public authorities in their traditional role as governance bodies. In addition, companies are claiming to be ‘corporate citizens’ in the way they deal with their environmental, employment and social/ethical responsibilities. Given the fact that large corporations are now heavily internationalized in their operational characteristics – with branches, subsidiaries, affiliates and extended supply chains operating in multiple jurisdictions – can such organizations be brought into a democratic register? Citizenship and democracy are conventionally associated with a territorial state, national sovereignty and jurisdictional independence. So, how can internationalized companies be subject to democratic forms of governance? An added problem arises with platform companies and blockchain organized digital currency providers whose operations transcend national borders from the start. This contribution discusses the issues of and provides a way for considering corporate democracy afresh in these rapidly evolving contexts.

Keywords

Introduction

Corporate forms (of which the commercial company is an extremely important example, but not the only one) are becoming ‘parallel governance mechanisms’ operating alongside the public authorities. Thus, we have ‘private’ forms of societal governance as well as ‘public’ forms of societal governance. Indeed, these two forms are becoming so intertwined that they are often indistinct (Gereffi, 2018). The issue confronted in this article is how to bring these – what are at present essentially private forms of social governance – into a democratic register. How do you democratize the corporate form, and in particular the private commercial company, other than via the mechanism of extending limited liability (see Webber, 2018, and below). This issue arises in an acute manner in the context of the internationalized firm (MNC or TNC). How could an MNC with distinct internationalized branches, affiliates and subsidiaries, and often with an extended international supply chain, be brought into such a democratic register, for instance?

One way this is being done is for companies to claim a new form of citizenship: they are ‘global corporate citizens’ (GCC). This concept is examined later in the context of a wider move to constitutionalize the corporate realm more generally. The argument is that the international commercial sphere is progressively being subject to juridical and quasi-constitutional means of regulation, but without there being the competent public authority to initiate or supervise this. It is being done largely at the behest of commercial and private law, ad-hoc administrative law and informal processes of non-transparent ‘custom and practice’ associated with a wide range of commercial activity. It is in the context of this assemblage that firms have been encouraged to claim they are GCCs (Thompson, 2005). Historically, citizenship and democracy have been closely aligned, mainly in the context of national sovereignty, state formation and jurisdictional independence. And citizenship has been considered in terms of individuals that may or may not be deemed to belong to a particular political community. So, what are we to make, first of all, of corporate bodies like companies claiming a form of citizenship and, secondly, them considering themselves somehow ‘global’ corporate citizens, involving citizenly activities that transcend traditional national boundaries? These are issues taken up below in the main text.

This article proceeds as follows. First there are two introductory sections dealing with the contemporary context in which corporate activity is evolving and how companies are facing up to the ‘politics’ of their current situation. The issue of corporate citizenship is then confronted directly, which takes us into matters associated with corporate democracy and the range of stakeholders that might have a legitimate claim to be included in any corporate democratic mandate. How to establish corporate democracy in an operational manner is the next area discussed, where we concentrate upon this in respect to the internationalization of corporate activity in particular. Finally, there is a section that looks at all these issues in the context of new forms of corporate activity associated with platform companies, blockchain cyber currencies and the like. We then conclude.

The corporate context

Productive corporations and financial institutions are under intense official and public scrutiny. Not only do they face the usual pressures arising from the ‘market for corporate control’ – takeover and merger activity continues to abound and is unlikely to decrease in the near future – but the acceleration of technological change means that even the best laid and seemingly robust business models can be quickly swept aside by a clever invention which undermines the possibility of corporate ‘business as usual’. In addition, the largest global firms can be stalked by activist investors – hunted by private equity or sovereign wealth funds seeking added shareholder value extraction. We have come to think of large global firms as powerful and arrogant, particularly the newly emergent platform companies like Google, Facebook, Air B&B, Uber, Amazon and the like. But actually – under present circumstances – even these are potentially weak and vulnerable. Few companies – however large or internationalized – are immune from the threat of takeover or an unexpected technological advance (Schumpeterian ‘creative destruction’ remains pertinent). And although this has traditionally been confined to an Anglo-American business world, such pressures are now spreading beyond this to other commercial environments. So, what are large corporations doing to try to shore up and bolster their prospects under these circumstances: how are they positioning themselves ‘politically’ to combat the potential plundering of their assets and unwelcome attacks on their business models, as they would view it? And, of course, whilst individual companies may be vulnerable, the commercial system as a whole looks to be as strong as ever.

The sections that follow dealing with corporate governance are mainly addressed to an Anglo-American business environment though – as suggested immediately above – the issues confronting this environment are rapidly spreading. Nevertheless, forms of corporate governance still differ widely. The ‘foundation model’ of business organization, for instance – which is strongly embedded in some Scandinavian and northern-European countries – presents a different set of problems (Thomsen, 2018). Democratic and governance issues associated with this organizational form are not the focus of the present analysis (see Thompson, 2014).

However, all in all, the business world confronts a very uncertain and complex future. It remains on the defensive: apprehensive, insecure and anxious about what challenges await it in the turbulent world of contemporary economic disruption and geo-political dislocation. For some time to come it will have to cope with an uncertain and cowed political class unclear of what exactly to do in the face of the onslaught from popularism, stoked by an often angry, disaffected and resentful public. All this presents a volatile and unstable mix. The question this poses is what will happen – and indeed is happening – in terms of the regulation and governance of this rapidly evolving environment. How might this translate into both internal corporate governance moves and external governance of the overall commercial sphere?

Elsewhere it has been suggested a key shaping move in this complex emerging picture is the increased subjection of business activity to formal and informal legal or quasi-legal mechanisms of regulation – what has been termed a process of the ‘constitutionalization of the corporate sphere’ (Thompson, 2012). The high tide of voluntarism and self-responsibilization on the part of corporate governance – which involved complex relationships of self-regulation and the self-responsibilization on the part of corporate players (both internal and external) – may have passed (Thompson, 2020). The issue now is one of a more formal or quasi-juridical mechanism of accountability and transparency than we have seen over the recent past. The constitutionalization of the global corporate space represents a process that is increasingly subjecting the corporate world to forms of regulation and governance that display a quasi-constitutional formation – a terminology perhaps unfamiliar in a corporate environment or business context. It involves several conceptual and practical clarifications, ones associated with the ideas of juridicalization and citizenship in particular. While the first of these is operating more to frame the ‘external’ field to which companies are increasingly being subject, corporate citizenship is a category more closely associated with the ‘internal’ responses of companies to the developments and is the one concentrated upon here. Together, however, these external and internal conceptual frameworks and operational reactions provide the contours around which the problem of corporate political relationships is being cast.

Corporate reproduction

When operating under normal conditions companies face the issue of their reproduction. Traditionally this has been considered in respect to three headings, each of which involves a major constitutive element of their operations: at a minimum they must reproduce themselves organizationally, financially and legally if they are not to go out of business (Thompson, 1982). Organizational reproduction involves such activities as production planning and execution, organizing the routines of work tasks and remuneration systems, the implementation of cost control systems, initiating and managing Research and Development (R&D), the allocation and monitoring of divisional responsibilities, operationalizing accounting procedures and internal reporting, and the like. Financial reproduction invokes issues in respect to markets, sales and prices, which address revenue generation, cost control, strategies in respect to investment and the capital markets, to mergers and acquisitions, and finally strategies towards governments in respect to marketing privileges, seeking subsidies, and financial regulation and reporting. It is important to note that financial reproduction does not just involve ‘profit maximization’ as usually understood – companies can financially reproduce themselves through attracting subsidies, for instance. Finally, legal reproduction concerns the preservation of the boundaries around the firm as an entity; issues associated with contracting, health and safety regulations, statutory working conditions, ownership structures, conforming to binding obligations in terms of statutory and stock market governance procedures, responses to regulation, and so on.

Of course, these dimensions are not independent of one another. Rather they exist as overlapping but semi-autonomous dimensions of company existence. But each presents its own unique problems for companies, and demonstrates its own typical operational modality, mechanisms of performance, evolutionary dynamic and rhythmic cycle. Together they constitute an ‘assemblage’; so, with this conception the company represents a definite entity, though not necessarily a unity in the sense that everything neatly ‘fits together’. Companies can be loose configurations; they are a dispersed locus of organizational features, competences, information flows, functions and practices. And there are several ways in which this has been characterized in the literature: as a ‘nexus of contracts’ (Jensen and Meckling, 1976; Aoki et al., 1990); as a ‘moebius-strip’ organization (Sabel, 1991). It is suggested, however, that the company still needs to be considered as a definite entity despite the looseness of its configuration in these respects (hence the entity terminology in Thompson, 2020).

But this terminology of reproduction might appear controversial since it does not – in the first instance at least – invoke the problem of accumulation. Companies are compelled to expand, it is often argued, driven by the forces of competition, based upon market exchange and surplus extraction, which does not just involve the issue of their reproduction – rather it is one of their ‘expanded reproduction’. However, reproduction is a base category, a default position. Companies can reproduce themselves much as they are without necessarily accumulating in the sense of expanding and growing. This depends crucially on market position, the circumstances of the competition they face, industry characteristics and technological advance, and exactly how they play the reproduction game in connection to the three dimensions mentioned above. From this perspective reproduction does not rule out accumulation but it sees accumulation as one possible strategy involved in such a reproduction.

Given this, however, it is argued here that firms are facing a newly emergent (semi-autonomous) dimensional problem, one additional to the three classic reproductive dimensions just outlined. This is a problem of their political reproduction. Companies are having to face the issue of legitimizing themselves politically, which means they must become political players in an overt sense (Scherer, Palazzo and Matten, 2014. Companies have, of course, always played a very important role as political actors: they are adept at political lobbying, manoeuvring for advantage, contributing to political campaigns, sometimes even directly intervening in politics to secure their advantage or neutralize an opposition (see Macher et al., 2011). And in ‘organized’ polities business has often been formally drawn into governance arrangements as an ‘interest’ represented in overall societal governance mechanisms (Hall and Soskice, 2001). Nevertheless, much of this has traditionally been done informally, behind the scenes, sometimes reluctantly, and without an overt public mandate. Things are changing in the current era, where communications technology and an explosion of campaigning and lobby organizations require companies to adopt a different style and approach. And companies are themselves somewhat ‘willing partners’ in this process since they want to shore up their position in relationship to the vulnerabilities and uncertainties discussed immediately above. So, they are being forced – and forcing themselves – to play the political game as part of their day-to-day business activity. In this situation, amongst other things, they are under pressure to become continuously and publicly transparent and accountable.

Of course, this is a dangerous game for companies. It exposes them to new and unfamiliar pressures and scrutiny as they become more openly political actors. Thus, they are proceeding along this path cautiously – not all at the same speed or with the same enthusiasm (and many are trying to quietly – or even noisily – avoid it; Thompson, 2012: ch. 3). So, they are exploring this hesitantly, feeling their way into a relatively unfamiliar territory with its own new potential pitfalls and setbacks, which will be discussed in a moment.

In addition, a completely new problem is arising in the context of what are often termed ‘platform companies’ (Google, Facebook, etc.). These are inherently ‘internationalized’ from the start but how should they – or could they – be subject to some form of ‘democratic corporate governance’? What is more, there is an even greater problem emerging in respect to developments like private ‘cyber-currencies’, blockchain-based organizations, etc., which are also internationalized but designed to operate anonymously. Such that these are constituting new forms of money they have a decidedly social impact but seem to escape any form of (or much) public regulation, governance, control, supervision, etc. We return to these issues in the final main section.

Nevertheless, there is a two-pronged political process going on, whether companies fully appreciate it or like it or not. The first of these concerns the ‘external’ pressures to take a more overtly political stance; to become an open, responsible, and transparent political player with concomitant rights and obligations. The second arises from ‘internal’ pressures for companies to demand political protections, react to external pressures, and so on. The vulnerabilities associated with the modern business world sum up this configurative environment. And it is within the framework of these trends that the issue of ‘corporate constitutionalization’ has arisen explicitly.

What, then are companies doing to address these problems?

Corporate citizenship

As suggested above, the failure of public governance institutions to keep pace with corporate economic internationalization has created what is often termed a ‘governance deficit’, which is increasingly being addressed by private bodies and corporate initiatives. These take many forms which are often summed up under the banner of corporate social responsibility (CSR) (Gereffi, 2018). But in addition to this – and something that is threatening to eclipse CSR – is the claim by companies to be good ‘global corporate citizens’ (Thompson, 2005, 2012). This is both a claim made by leading international companies and a form of address by international governance organizations like the UN (through its ‘Global Compact’), the Global Reporting Initiative (a leading body dealing with corporate reporting and accounting standards) and the World Economic Forum (the organizer of the famous Davos meetings in Switzerland) (Schwab, 2008; Scherer and Palazzo, 2010).

But what do these terms mean? Corporate citizenship is more than just CSR. It represents a substantial claim to be a full agent of civic virtue: one deserving the recognition of its duties, obligations and protections equivalent to that of ordinary citizens. It developed from the particular legal fiction of the company being a person in law, but one that has a continuity of existence beyond and above the activities of those who manage it or who work in it. And although it can claim certain features equivalent to the legal claims of ordinary citizens (though not all – see Thompson, 2012: Table 3.3, p. 73), unlike them it cannot be morally responsible in any meaningful sense (though see Erskine, 2003). In fact, this is a form of what Isin and Saward have called ‘acts citizenship’: that if agents act in a civic manner – in the case of companies, paying close attention to their environmental, social and employment responsibilities – then they are effectively acting as citizens (Isin and Nielsen, 2008; Isin, 2017; Isin and Saward, 2013). Note that this is a voluntarist and behavioral claim on behalf of companies. It is not a conception of citizenship based upon a conferred status: the citizen as a constituted entity of a definite polity, with rights originating from that polity and responsibilities and obligations towards it, secured by a legal apparatus underpinned by state authority and legitimacy. Such authority able to confer legitimacy does not exist in the international system.

In contrast to this conception of ‘acts citizenship’, companies might be better considered in the context of what I would term ‘real citizenship’ (i.e. one not based upon a ‘fiction’). This is a form of citizenship that may be beyond a conception organized simply by the category of sovereignty but that is, nevertheless, not totally beyond constitutionality or the law. This is not a substitute for all other aspects of citizenship – even that residually associated with sovereignty – but a parallel aspect of citizenship. Given that the current corporate world is saturated by constitutionality, which appears as the formation of the rules and regulations that govern corporate day-to-day activities, this is something that constructs them as ‘real citizens’. Thus, this notion of citizenship is not simply the consequence of an action or an enactment. Real citizenship – as termed here –whilst similarly concerned with the everyday activity of corporations as political actors, differs in that it sets this within a ‘constitutional order’ of rules, administrative governance, legal restraint and performative regulatory oversight. The mundane day-to-day of citizenly activity always bears a legal moment and is supported by a (sometimes informal or implicit) quasi-constitutional framework or settlement. It is difficult to see how we can talk about ‘citizenship’ (as, perhaps, in distinction to the general conflicts and struggles that accompany any form of social existence) other than in these terms. For the ‘acts’ approach, however, it would seem that it is the mere fact of any act as such, intermediating between political subjectivity and the citizenship, that confirms both by the sheer force of its enactment.

Democracy and stakeholder governance

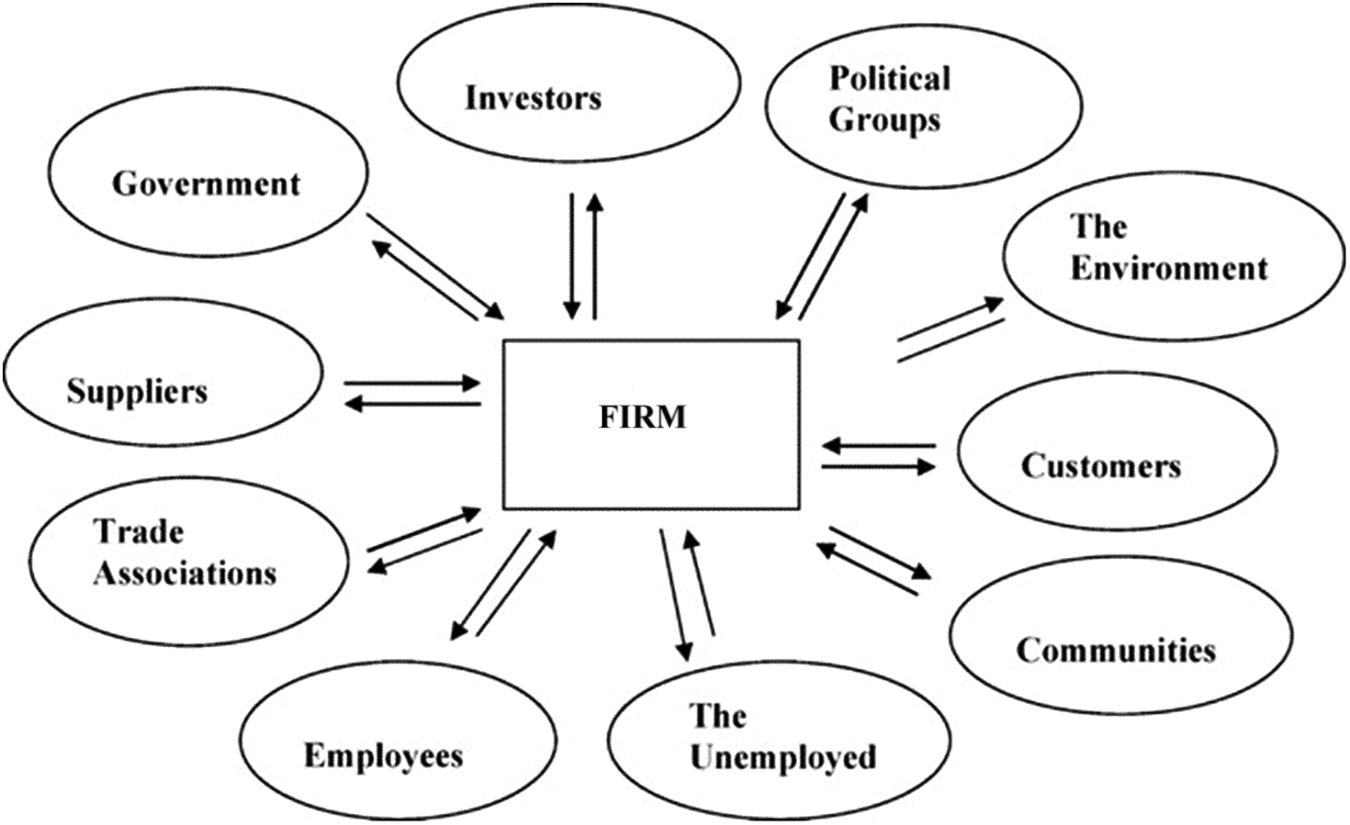

Figure 1 shows the full range of corporate stakeholders that in principle could have a legitimate stake in company governance if these organizations are claiming to be citizens with a public purpose and operating as political actors.

Corporate stakeholders.

Only one of these – the investor/shareholder – is traditionally considered a stakeholder from the point of view of corporate governance. A number of the others have a direct contractual relationship with the company (for example, workers, customers and suppliers), so it is often argued that there is no need to consider these as explicit stakeholders. However, the rapid expansion in importance of the category of intangibles in company balance sheets, which includes the customer base and goodwill as assets (along with ‘firm-specific human capital’), implies a radical change in the nature of company activity that bolsters the idea that customers (and workers) should be considered as genuine stakeholders. If these categories of assets are included in the balance sheet, they implicate new explicit stakeholding interests analogous to those of shareholders.

These stakeholders vary considerably in their characteristics. The traditional investor-shareholder interest is already well accommodated. A further traditional concern is with employees, though how to accommodate this interest is itself fraught with tensions and conflicts. These two are the main ‘internal’ stakeholders. Then there are a range of ‘external’ ones. Some of these are well constituted into a definable interest, others are not. Some have a contractual relationship to the company, others do not. There is a body of opinion that suggests only those with a contractual relationship to the company should legitimately be considered as stakeholders. Thus, along with shareholder-investors and workers would be included suppliers and probably customers. This leave out of account, however, many who it could be argued have a legitimate interest in company activities if these organizations are to fulfill their wider social responsibilities. The unemployed could also be considered as having a stake in companies in as much that decisions taken by such companies might have important implications for their future employment. One other key stakeholder in this respect is the ‘environment’, but – rather like the ‘unemployed’ – this suffers from the obvious difficulty of constituting it as an agency which can express an interest. Later this problem is addressed head on, but it also serves to raise another issue associated with the elements illustrated by Figure 1, that is, the progressive internationalization of these stakeholders.

Internationalization has come about in the wake of the development of TNCs and financial diversification. This means that shareholding has become spread across different national territories and jurisdictions, but so have workers and all the other potential stakeholders shown in Figure 1. A key practical question, then, is how to deal with such an internationalization of stakeholders, even the traditional ones, if the objective is to directly increase the accountability of the organization to those varied interests. Again, this is directly addressed later in this article. But the final point to make here is that it is not always easy to know quite how to involve various new constituencies that are indicated by the stakeholders in this figure, even if they are fairly clearly demarcated. For instance, ‘local communities’ seem to present little difficulty, but in many countries it is not quite clear how to access these properly. What often happens, therefore, is that local activists are suggested, who sometimes have their own hostile anti-corporate agenda firmly in place, and who claim to speak for the wider community in this respect. They are not interested in CSR or GCC, but only in ‘seeing off’ what they consider to be potentially exploitative international companies.

An explicit role for other stakeholders directly in corporate decision-making remains the missing link here. Traditionally this has been called ‘corporate democracy’, but the term has somewhat fallen out of favour (Turnbull, 1994). Even the most progressive of companies that have embraced the full CRS agenda enthusiastically do not talk much about corporate democracy. In large part, then, CRS was a substitute process and a less threatening one for corporate reform than corporate democracy, hence, to some extent at least, its enthusiastic embrace by the corporate world. And corporate democracy is not the same as some form of ‘worker control’ as favoured by the British Labour Party. Worker shareholding is perhaps an interim arrangement that gives one very neglected stakeholder a voice in corporate governance (Webber, 2018) but proper corporate democracy should not neglect the other important stakeholders sketched in Figure 1 and discussed above.

Representation or champions and stewardship?

Company reform to increase internal democratic decision-making is a complex issue, made even more so by the progressive internationalization of business activity as suggested above. Political sentiment is not at present in favour of radical reform but it is important, nevertheless, to outline how this could be practically organized and implemented if circumstances were to change.

First, there are conceptual and terminological issues to be addressed. The conventional manner of considering issues of democracy is via the mechanism of ‘representation’. Let us take a classic liberal political representation as an example (Pitkin, 1967, Stanford Encyclopedia of Philosophy, 2018 [2006], Runciman, 2007). Here the citizens to be represented are divided into a series of ‘constituencies’ and candidates are selected and elected by those constituents to represent them in the decision-making legislative arena. This is a form of ‘indirect democracy’: the ‘interests’ of the constituents are not directly involved in decision-making, they are mediated by the figure of the representative who makes decisions on their behalf. Accountability is ensured by various mechanisms of report back, consultation, periodic re-selection and new elections.

This seemingly simple procedure is, of course, fraught with problems which have been recognized – though never totally resolved – since liberal democracy was consolidated during the 19th century and later. What is the exact role of the representative in this arrangement? Formally, he or she is not a ‘delegate’ mandated to vote is a particular way: representatives are supposed to exercise their own judgement is making decisions on behalf of their constituents. As is well known, however, this is the site of huge controversy as to how much flexibility representatives are allowed or can claim in these situations. As argued persuasively by Saward (2006), all representative systems can only be ones of ‘claims’: there is no guarantee of true representation, other than a claim to exercise or fulfil it.

The basic problem haunting all representational systems is that they make present an absence: in the above case the absent constituency view or interest is made present in the legislative arena via the figure of the representative. In aesthetics, linguistics and economics similar problems arise with respect to representational theories. To be brief, representational art projects an ‘authentic’ object onto a canvas or into a performance, so the art object represents the absent referent it is supposed to signify (but is it a true likeness or not, etc.?). In linguistics, representation make a hidden thought present in the spoken word; as a representational system, language serves to make present in the spoken enunciation the absent thought context. In economics representational theories of value and money make an absent and unmeasurable domain of ‘utility’ (for neoclassic economics) or ‘socially necessary abstract labour time’ (for Marxist economics) – which are the respective true determinants of value – present as measurable quantities via them being represented as money in a price domain. Each of these systems demonstrates the same basic theoretical structure. But ultimately all these mechanisms fail since something cannot be both present and absent at the same time: this is a logical impossibility.

Foucault (1970) drew attention to the huge intellectual effort it took to break with the idea of verisimilitude to establish that of representation in these domains during the late Middle Ages. But this was only established at the expense of creating the ‘impossible’ process of an absent-presence in a logical sense. What is needed now is to break the link between representation and signification so that things may signify without necessarily representing anything (other than themselves).

One way of doing this in respect to corporate democracy is to abandon the idea of representation in that context. The main problem is exemplified by the case of treating something like the environment or the unemployed as a stakeholder. How could these be constituted into viable and convincing ‘entities’ able to be involved in any direct decision-making activity? And these examples, whilst extreme ones perhaps, are illustrative of the wider difficulty of constituting all stakeholders as decision-making entities for MNCs as the international bases of their activities spread (Driver and Thompson. 2002; Thompson and Driver, 2004). How could any stakeholder be constituted as an interest? The way round this is to abandon the language – and indeed, the conception and practice – of both representation and interests. Instead, it is a former language of political analysis that is invoked here: that of championing and stewardship. Any reformed decision-making arena within the firm needs to be thought of as an ‘arena of stewardship or championing’ rather than of representation. This is a suggestion made forcefully by the English pluralist tradition, particularly by Harold Laski and GDH Cole (Hirst, 1989). In whatever way champions were elected or appointed, they would simply act as ‘decision-makers’, not as representatives of an interest. They would be there to champion a cause, nurture it and act as a steward of that cause through the decision-making and implementation processes.

Clearly, this approach raises all sorts of difficulties of its own, not least as to the mechanism of how such champions would be appointed or how they would be made accountable for their stewardship. One way forward would be to strengthen the non-executive directorship role via this route. As it stands, most existing non-executive directors are appointed very much through the old-boy network. They are already known to the firm or are in its immediate network of contacts. But they lack a clear alternative brief and legitimacy as a result, which is why there has been such an interest in re-vamping their role in the rather restrictive corporate responsibility reform so far enacted. The suggestion here would be much more radical and would strengthen the role of the non-executive directorship by making it the job of such directors to champion the cause of the unemployed, the environment, the community, the employees, the customer, etc. – even the shareholder. And this would put these various considerations at the very heart of the organizational decision-making processes.

But from where would such champions be found and how would they be appointed? Here we might think of the formation of a pool of such persons from which could be drawn suitable individuals to serve on different company boards or senates, or who were ‘elected’ to do so (this would be a way of increasing the ‘gene-pool’ of directors). But who should be responsible for generating this pool of expertise? Here it is suggested that already existing global governance organizations, national bodies and governments, NGOs, trade and professional association, pressure groups, and even other companies in completely different sectors, etc., that already address these separate issues, constitute themselves into ‘quasi-constituencies’ around their existing concerns and provide lists of such acceptable personnel as potential candidates. They could then be either elected or appointed to companies, as suits the purpose, but operating in an open and transparent manner. The champions so produced by such a process would then have to ‘report back’ to such bodies on their stewardship: their accountability would be addressed to these new ‘civil-associations’ as they might be termed. This would be, in turn, an attempt at the operationalization of a form of associative democracy as advocated by Paul Hirst (1994), amongst others. In a sense, then, what is being promoted is a form of ‘indirect democracy’ to address the issue of accountability. But what about legitimacy, the other pillar of democracy?

Here the suggestion would be that to gain such legitimacy the new civic associations outlined above might have to be accredited by existing international representative organizations (UN, World Bank, OECD, BIS) and perhaps lists of the candidates proposed by them as appointable champions would be allocated in proportion to rules established by those bodies. In this way legitimacy would be established even at the international level for activist involvement. Thus, the legitimacy of the process relies upon the legitimacy of the organizations that support it and feed personnel into it in the two-stage manner as outlined here. But these would not be considered ‘representatives’ as such, only ‘decision-takers’.

New problems and issues

As suggested above, the commercial environment is fast moving and uncertain. Nowhere is this more so than in respect to technological advance in the world of platform companies and software-based organizations, particularly in respect to blockchain cyber operations. This creates new players and problems if we are concerned with democratizing this world. Some of these organization refuse to acknowledge they have ‘workers’ at all (e.g. Uber, some food delivery companies), so the establishment of a stakeholder environment is doubly complex. Juliet Schor (2020) suggests that the only way to roll back the worst excesses of the gig-economy is to institute a regime of shared governance where a wider range of parties get a say in how the platforms are organized and run. But that is some way off.

In the context of the 2018 Facebook–Cambridge Analytica privacy scandal and many other events that have fallen foul of basic civic responsibilities, open source software organizations are under intense scrutiny over their ‘corporate governance’ arrangements. In fact, Cambridge Analytica was doing much the same thing as all other such platform companies. Many parties want to subject this kind of organization to a traditional ‘fiduciary duties’ legal framework of governance, where such software developers and service providers would be subject to claims and counter-claims associated with their duty of care and duty of loyalty: they must not advantage themselves in various ways at the expense of potential third-party ‘beneficiaries’ (Reyes, 2020). For those who are championing a more libertarian agenda for such platform companies and open source operational organizations this would, in effect, stifle the technological developments because the objective of their activity is to create a ‘community of developers and users’ who largely work in privacy and anonymity on a decentralized distributed network basis, where such duties are impossible to clearly establish and police effectively without undermining their whole operational credibility and business rationale. They argue it would mean the constant tracking and monitoring of activity. Reyes suggests instead that there is a need to introduce robust contractually-based governance mechanisms to bring software organizations into line with existing corporate governance law. Algorithmic protocol organizations would then be rendered into legally recognized business units but not ones in the form of a traditional corporation – what he describes as ‘(un)corporate crypto-governance’: a new form of corporate body.

But there are other approaches to such governance that do not, in the first instance at least, involve elaborate legal developments. The field of financial instruments provides one example. Since crypto currencies, for instance, reside to a large extent in the ‘anonymousphere’/cyberspace – they are not embedded in any specific institutional setting or any one country in particular. They are ‘internationalized’ from the start: they are a new kind of transnational organization. The leading alternative/crypto currency, Bitcoin, is a case in point, where its blockchain protocol is not owned by any party but exists in the ‘anonymousphere’ of the distributed ledger. Several crypto-currency issuers are constituted as ‘corporations’ with a CEO, etc., and are thus minimally subject to the usual corporate governance requirements. But many others are not. The shortcomings associated with the ‘governance’ of these crypto-currency organizations are well testified by Cohney et al. (2019): protections for investors and users which are supposed to be embodied in the coded protocols are either not fully disclosed or are completely absent.

But, at its best, blockchain-based organization could in principle be governed by decentralized communities of developers and users, by centralized corporations or as hybrid operations between these two: ‘decentralized autonomous organizations’ is perhaps the best way to describe them (Campbell-Verduyn, 2019). Blockchain organizations put the technical protocol of the algorithm at the centre of their organizational structure and personnel at the margins. Developers establish and modify the blockchain, miners validate it, and users verify the transactions. This puts the ‘customers’ (i.e. ‘investor-users’ and ‘transactional-users’) into a potentially much more powerful position than in traditional company stakeholder governance arrangements and presents a different configuration of stakeholders than that described in Figure 1. Incentives are not written into well-defined contracts (contrast to Reyes above) but established by – and written into – the coded protocol itself. Often there are no headquarters and subsidiaries but a network existing in cyberspace that is essentially borderless. Crypto users play an important part in external governance but in principle anyone can voluntarily choose to join a crypto organization by establishing an account and begin transacting. But some are ‘investors’ only looking for a return on the fluctuating price of the crypto currency. Hsieh et al. (2019) suggest that miners/validators/users are the key ‘internal stakeholders’: they have the power to determine whose transaction is accepted and under what terms. They are equivalent to the ‘owner controllers’ at this level. But there are also the ‘developers’ who write the rules of the algorithm. These are another key ‘internal stakeholder’. These organizational actors (miners, validators, users and developers) can often establish a voluntary group who effectively ‘govern’ the protocol and the blockchain organization, sometimes with a formal voting procedure, but in ‘open-systems’ (like Wikipedia) anyone can, in principle, contribute. On the other hand, where there is a more centralized organizational structure – with centralized finance and traditional investors, branches, a CEO, etc. – a more usual governance structure can be envisaged, with all the issues discussed above being in play. By and large in these contexts indirect ‘external governance mechanisms’, like public opinion, the media, regulatory bodies, even external investors where applicable, are weak. These ‘stakeholders’ are disadvantaged by the technicalities of the blockchain protocol and the insider knowledge of developers, validators, and closely involved users. And Cohney et al.’s (2019) analysis, mentioned above, adds to the disquiet.

All of this presents huge challenges, and how this can be addressed via notions of citizenship and democracy is not at all clear. Those who advocate for open-systems protocol organization see this as a natural way of increasing democracy and citizenly involvement: their decentralized systems are an embodiment of democratic control, and the fact that a wide range of ‘citizen user-consumers’ have greater impact on the activity only enhances engagement and potential civic type involvement. But they suffer greatly from lack of transparency and accountability to a wider civic polity than just those directly involved. Facebook’s recent suggestion was for a digital crypto-currency (the Libra) to be organized and governed by a consortia of initially 23 ‘partners’ (the Libra Association) – including the likes of Uber, Lyft and various tech-payment companies; see: www.libra.org/en-US/association/#the_members). But these are all investors and will be ultimately subordinate to Facebook; they do not include any of the wider stakeholders, as indicated in Figure 1 (Tischer, 2020). On the question of the international repercussions, non-Western governments of a more authoritarian bent remain hugely suspicious of the consequences of these protocols and are looking to circumvent their impact (e.g. China’s Great Firewall and Russia’s ‘sovereign internet’ initiatives – China has recently moved to curtail its domestic internet providers and blocked mergers between them).This is the site of a huge controversy which cannot be properly tackled here.

Conclusions

Corporate democracy remains a controversial and highly charged issue. But in a world where commercial corporations are increasing their visibility and presenting themselves as responsible organizations prepared to take account of their environmental, ethical, and social impact there is a need to re-visit this concept anew. If companies want to be considered as somewhat analogous to ‘citizens’, they must take the public scrutiny this will involve directly onboard. This contribution has summarized the issues involved and proposed meaningful responses and remedies. In particular, the difficulties of conceiving such responses in an environment of the increasing internationalization of business activity presents severe challenges. But this is confounded by the emergence of new platform companies and cyber-based organizations that are internationalized for the start. These provide a vital public service and should really be considered as public utilities and regulated accordingly. But the difficulties here are legion. It is unlikely that anything but a very weak internal democratic governance regime could be envisaged under present circumstances, so the emphasis should shift to the external regulatory environment where opportunities seem more likely (Beaumier et al., 2020). We have only just begun to think about the formidable obstacles this presents for citizenship, democracy, and civic involvement – something opened up in the latter parts of this article.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.