Abstract

Objective:

Provincial and territorial governments are considering how best to improve access to psychotherapy from the current patchwork of programmes. To achieve the best value for money, new funding needs to reach a wider population rather than simply replacing services funded through insurance benefits. We considered lessons for Canada from the relative uptake of private insurance and public funding for allied health psychotherapy in Australia.

Method:

We analysed published administrative claims data from 2003–2004 to 2014–2015 on Australian privately insured psychologist services, publicly insured psychotherapy under the ‘Better Access’ initiative, and public grant funding for psychotherapy through the ‘Access to Allied Psychological Services’ programme. Utilisation was compared to the prevalence of mental disorders and treatment rates in the 2007 National Survey of Mental Health and Wellbeing.

Results:

The introduction of public funding for psychotherapy led to a 52.1% reduction in private insurance claims. Costs per session were more than double under private insurance and likely contributed to individuals with private coverage choosing to instead access public programmes. However, despite substantial community unmet need, we estimate just 0.4% of the population made private insurance claims in the 2006–2007 period. By contrast, from its introduction, growth in the utilisation of Better Access quickly dwarfed other programmes and led to significantly increased community access to treatment.

Conclusions:

Although insurance in Canada is sponsored by employers, psychology claims also appear surprisingly low, and unmet need similarly high. Careful consideration will be needed in designing publicly funded psychotherapy programmes to prepare for the high demand while minimizing reductions in private insurance claims.

Less than half of Canadians with mental illness use mental health services, 1 and receipt of evidence-based psychotherapy is even lower. Only 13% of individuals diagnosed with depression received minimally adequate psychotherapy or counselling from 2010 to 2011. 2 Consequently, there has recently been substantial interest in how best to improve population access to psychotherapy. 3 –5 Increasing psychotherapy provision by psychiatrists and general practitioners (GPs) would likely be costly, delayed by workforce scale-up, and unlikely to directly improve access on its own. 3 However, with the Canada Health Act’s focus on physicians and hospital care, public funding for psychotherapy delivered by psychologists and other allied mental health professionals has not developed beyond a patchwork of community and hospital-based programmes. In 2001, the Canadian Psychological Association estimated that 80% of psychologist consultations occur in private practice. 6 For the two-thirds of the population with access to employer-sponsored health insurance, 7 benefits for psychotherapy may be available but the degree of coverage varies across policies. 8 Provincial psychological associations estimate that a further 5% to 39% of private psychology services are paid in full by the client. 9 Consequently, Canadians with less comprehensive employment benefits and little ability to self-fund their treatment face significant financial barriers in accessing allied health psychotherapy; this results in inequitable access for economically disadvantaged individuals, who also experience higher rates of mental disorders. 10,11

Based on available evidence and the experience of countries like Australia and the United Kingdom, various options are being considered to increase access to allied health psychotherapy in Canada, including through the expansion of public health insurance plans or government grants. 5,8,9 Vasiliadis et al. 5 have shown the potential economic benefits of increasing publicly funded psychotherapy coverage, but the substantial expenditure on these services in Australia also provides a warning about the potential costs of such a scheme. 12 The impact of any new funding on the status quo needs to be considered as well; even though public financing of psychotherapy is likely to improve access, it would not be desirable to simply shift services that are currently funded privately onto the public purse. Historical data from Australia on the relative provision of publicly versus privately insured psychotherapy provides useful learnings from a health system that is relatively similar to that of Canada, and can inform current policy deliberations in the Canadian context.

In the late 20th century in Australia, allied health-delivered psychotherapy in the community was available to very small numbers of people with the most severe mental disorders at no cost through state-funded community mental health teams or, alternatively, from private practitioners via full client payment or private insurance. After 1997 survey data showed that only 1 in 3 Australians with mental disorders reported using professional services, the ‘Access to Allied Psychological Services (ATAPS)’ programme was introduced in 2001. 13 ATAPS provided modest government block grants to district-level primary care coordinating bodies to supply low-cost psychotherapy to disadvantaged groups, including people on low incomes and indigenous populations. ATAPS funded the delivery of psychotherapy by allied health professionals, such as psychologists, social workers, mental health nurses, occupational therapists and Aboriginal and Torres Strait Islander mental health workers; the exact delivery models varied across districts to match local resources and needs.

In November 2006, a more ambitious attempt was made with the addition of the ‘Better Access to Psychiatrists, Psychologists and General Practitioners through the Medicare Benefits Schedule’ (Better Access) initiative. 14 Better Access introduced rebates for short-term psychotherapy for common mental disorders delivered by allied health providers within the national universal health insurance system, which had previously included only physician-based treatment for mental disorders. The new fee-for-service billing items applied to psychologists, mental health social workers, and occupational therapists. Like physicians, Better Access permits allied mental health providers to choose whether to charge clients a co-payment in addition to the government rebate provided under the Medicare Benefits Schedule (MBS). If a co-payment is charged, clients pay for the session in full and are reimbursed (usually immediately) for the MBS rebate amount; otherwise providers can ‘bulk bill’ Medicare for the MBS fees directly, with no payment required from the client.

Under both ATAPS and Better Access, individuals must be referred by a physician (usually a GP) to access psychotherapy and could initially receive up to 12 group and 12 individual sessions per year (18 in exceptional circumstances). In 2011, following growing concerns about the rising cost of Better Access 12 and evaluation results showing average claims of only 5 sessions per person, 14 the maximum number of Better Access sessions was reduced to 10 individual and 10 group sessions per year. 15

Australia also has a parallel system of private health insurance, purchased directly by individuals rather than through employer-sponsored schemes, and subsidized by the federal government. 16 Because policies are purchased by the individual, fewer Australians on low incomes have private health insurance. 17 Individuals can choose to purchase pre-defined packages of benefits for hospital and/or ancillary out-of-hospital services. In June 2017, 13.5 million Australians (55% of the population) had some form of ancillary coverage. 18 Typically, only the most comprehensive tiers of ancillary coverage include benefits for services provided by psychologists (but not other allied mental health professionals). 16 Physician referral is not required and a co-payment for each treatment session is usual, with capped annual rebates. The amount of coverage for psychologist services varies by insurer and policy; for the 2 largest insurers, individual claim limits range from AU$200 to AU$500 per year. 19,20 In 2017–2018, the Australian Psychological Society recommended fee for a 45 to 60 min consultation was AU$246. 21

This paper explores the impact of introducing ATAPS and Better Access on the utilisation of psychotherapy benefits under private health insurance in Australia, with a view to informing policy in the Canadian context. Specifically, we sought to identify: 1) whether private insurance claims for psychotherapy decreased with the major expansion of public funding in 2006; 2) the relative importance of any decrease in private insurance claims to the bigger picture of the overall prevalence of mental disorders and potential service utilisation; and 3) differences in co-payments for privately insured v. publicly-insured services.

Methods

We drew on publicly available data: Quarterly numbers of sessions claimed, fees paid by clients and benefits provided by insurers for ‘psych/group therapy’ services across all Australian private health insurers, from 1 July 2003 to 30 June 2015.

18,22

–24

Annual numbers of sessions claimed, fees paid, and benefits provided for MBS psychological services by provider type (clinical psychologist, other psychologist, other allied health provider) from 1 July 2003 to 30 June 2015;

25,26

and published co-payment data.

27

Annual numbers of ATAPS sessions, co-payment rates and amounts from 1 July 2003 to 30 June 2015.

28,29

Rates of mental disorders and service utilisation for mental health from the 2007 Australian National Survey of Mental Health and Wellbeing.

30

Quarterly and semiannual data were summed to create figures for each Australian fiscal year (1 July to 30 June), and MBS data were summed across the 3 provider types. To plot changes over time, numbers of sessions were converted to rates per 1,000 population using the Australian estimated resident population for December of each year. 31 We estimated the population using private health insurance psychologist services in 2006–2007 by dividing total sessions by an estimated average of 5 sessions per person, based on the average number of Better Access sessions. 27

Results

Changes in Privately Insured Services After Expanded Public Funding

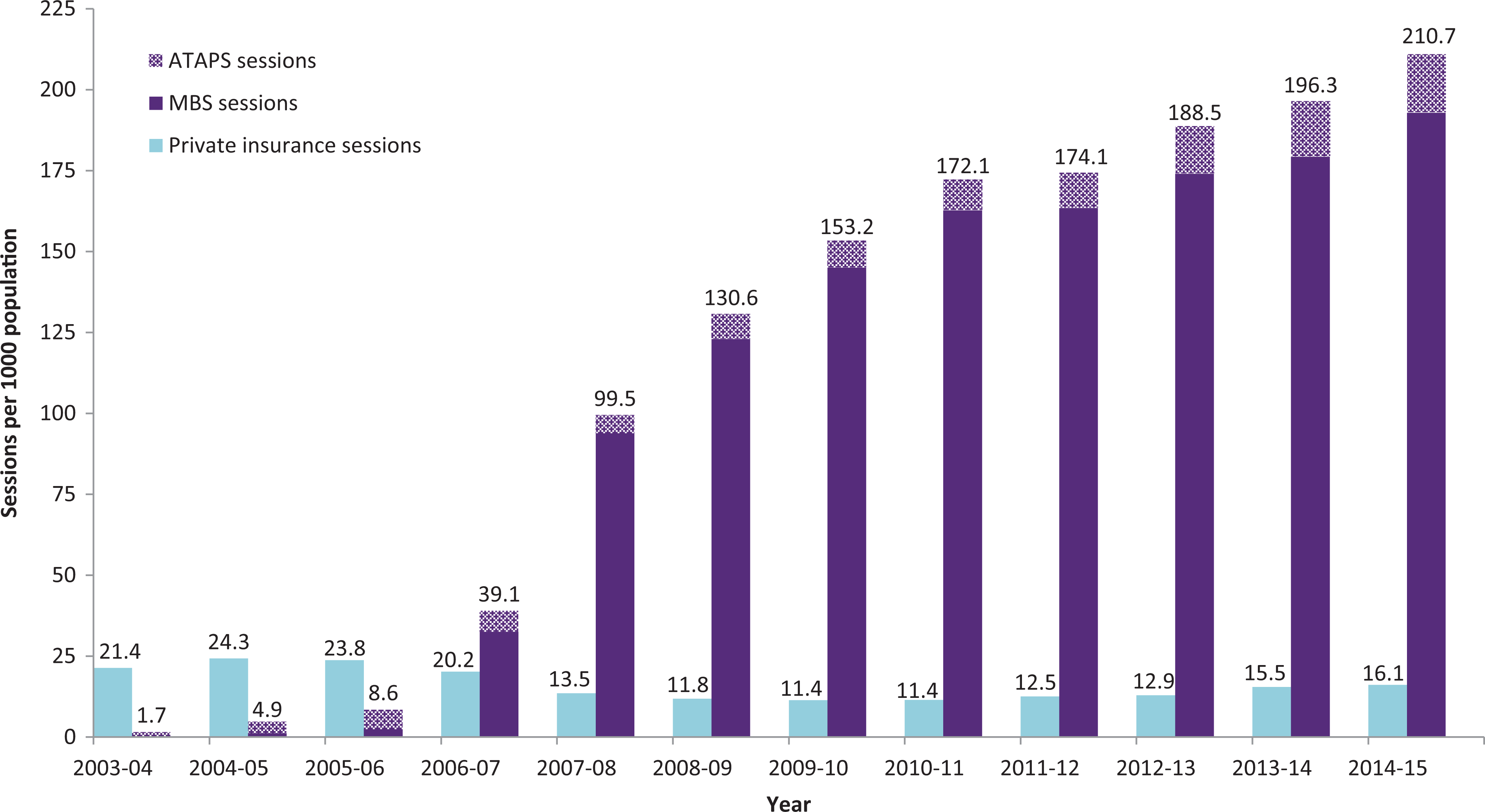

In 2003–2004, when expansion of public funding through ATAPS was commencing, Australian private health insurers provided benefits for 423,758 sessions of psychotherapy, or 21.4 sessions per 1,000 population (Figure 1). In the 4 y from 2005–2006 to 2009–2010, there was a 52.1% decrease in the number of privately insured sessions, which corresponded with the introduction and rapid growth of Better Access from November 2006. After Better Access caps were reduced in 2011, there was a gradual increase in private health insurance and ATAPS sessions, alongside slower growth of MBS sessions compared to earlier years. Although numbers of people using privately insured services were not available, the numbers of people receiving psychotherapy through Better Access and ATAPS grew alongside total sessions delivered. 13,25

Privately insured v. publicly funded psychotherapy provided in Australia, 2004–2015.

Importance of Decrease in Private Insurance Claims to Overall Prevalence and Service Utilisation

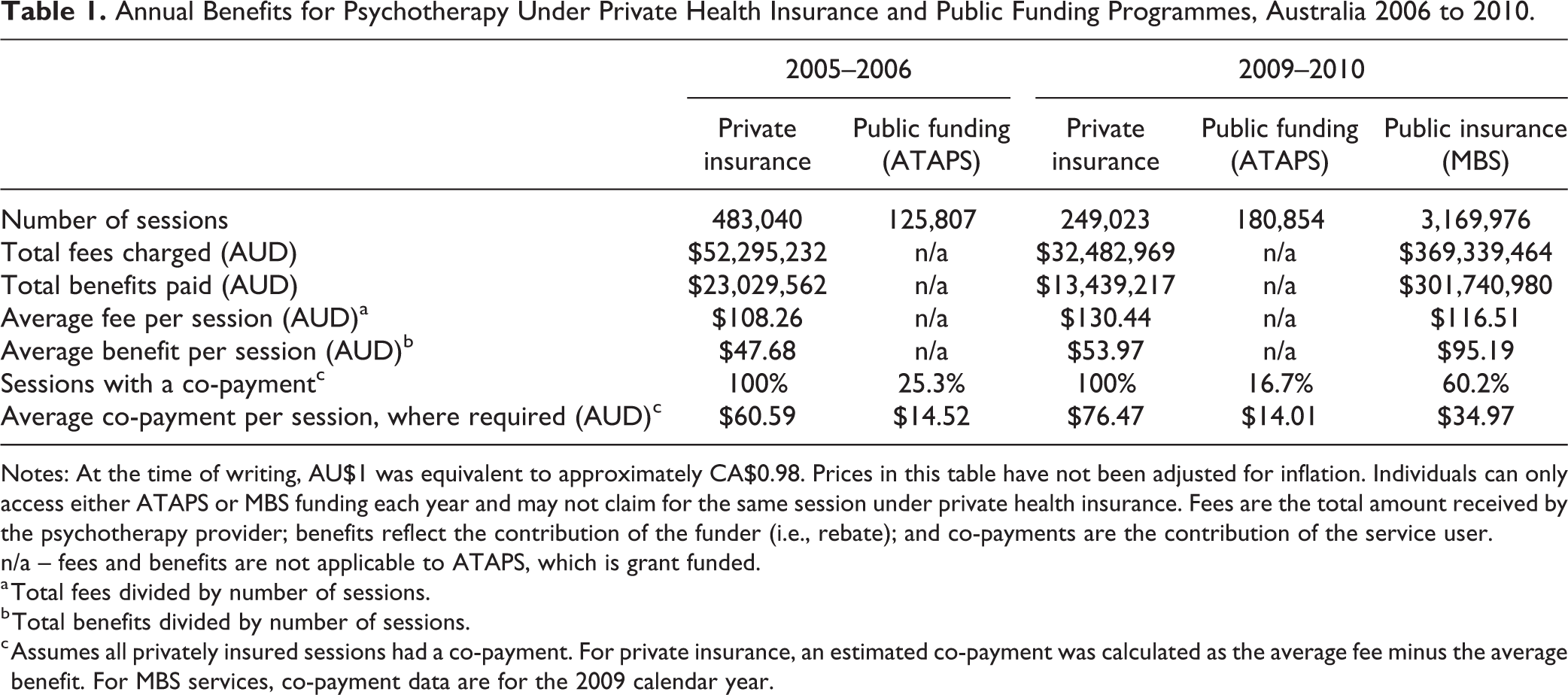

The decrease notwithstanding, total private insurance claims for psychotherapy were dwarfed by the rapid growth in uptake of the Better Access programme. By 2009–2010, the number of MBS sessions claimed had risen to 3.2 million, 12.7-times the number of sessions claimed under private health insurance in the same year, and 17.5-times the ATAPS sessions (Table 1). Privately insured psychotherapy therefore accounted for only 6.9% of the combined total of private, Better Access, and ATAPS sessions. There was an even greater difference in benefits provided: the AU$301.7 million in MBS benefits paid under Better Access was 22.5-times the AU$13.4 million of private health insurance benefits.

Annual Benefits for Psychotherapy Under Private Health Insurance and Public Funding Programmes, Australia 2006 to 2010.

Notes: At the time of writing, AU$1 was equivalent to approximately CA$0.98. Prices in this table have not been adjusted for inflation. Individuals can only access either ATAPS or MBS funding each year and may not claim for the same session under private health insurance. Fees are the total amount received by the psychotherapy provider; benefits reflect the contribution of the funder (i.e., rebate); and co-payments are the contribution of the service user.

n/a – fees and benefits are not applicable to ATAPS, which is grant funded.

a Total fees divided by number of sessions.

b Total benefits divided by number of sessions.

c Assumes all privately insured sessions had a co-payment. For private insurance, an estimated co-payment was calculated as the average fee minus the average benefit. For MBS services, co-payment data are for the 2009 calendar year.

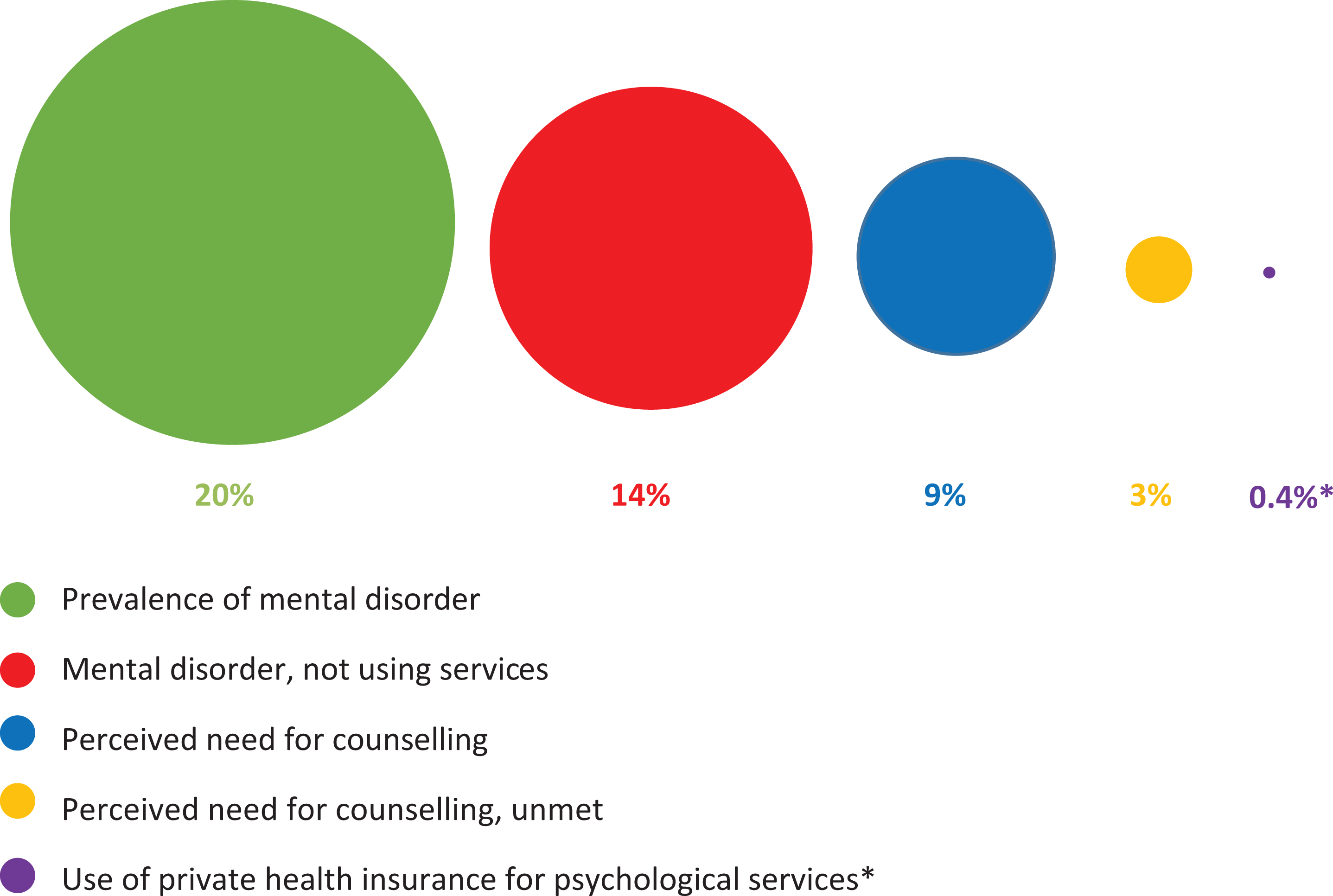

Further, in 2006–2007, we estimate that only about 0.4% of the population made private insurance claims for psychotherapy, even though 20% of Australians had a mental disorder (Figure 2). This is surprising given that more than half of Australians have some form of ancillary private insurance coverage (even if not all of these plans include psychologists) and levels of unmet need are high. As can be seen in Figure 2, in 2007, 14% of Australians had a mental disorder but were not accessing care, 9% of the population reported having a need for counselling services, and 3% reported a need for counselling that was not being met. At the same time, publicly insured services proved very popular. Driven by the growth in Better Access services, between 2006–2007 and 2009–2010, overall mental health treatment rates increased from 7.5% to 9.3% of the Australian population, or 37.3% to 46.1% of people with mental disorders. 32 Whereas privately insured psychotherapy dropped steeply over the same time period (from 417,199 to 249,023 sessions), this drop represented only 6.7% of the growth in Better Access services (from 668,902 to 3,169,976 sessions).

Private health insurance use for psychotherapy relative to prevalence of mental disorders and perceived need for services, Australian population aged 16 to 85 y (NSMHWB, 2007). 30 *Proportion of the people accessing private health insurance for psychotherapy in 2006–2007 was estimated as total sessions (417,199) divided by an estimated average of 5 sessions per person based on Better Access,27 and calculated as a percentage of the total December 2006 Australian population. 31

Differences in Co-payments for Privately V. Publicly Insured Services

Co-payment data may help to explain why Better Access claims dwarfed those through private health insurance. Benefits per person for Better Access were higher than those available through private insurance, with lower co-payments (or no co-payment if providers opt to bill at MBS rates; see Table 1). In 2009–2010, MBS benefits accounted for 81.7% of the total fees paid out under Better Access, compared to only 41.4% for privately insured psychotherapy. Further, less than two-thirds of Better Access service users paid a co-payment, and those that did paid on average less than half the co-payment estimated for people using privately insured services. ATAPS had even lower co-payments but was available to fewer people through its capped funding.

Discussion

Before the expansion of public funding for psychotherapy in Australia, the use of privately insured services was not even close to meeting the community demand for psychotherapy. Consequently, the introduction of cheaper and more accessible public insurance coverage for allied mental health professionals precipitated a sizeable increase in service use. Although there was a 52% reduction in claims for privately insured psychotherapy over the first 4 y of Better Access, this reduction was dwarfed by the rapid growth in utilisation of Better Access services, and further dwarfed by the overall prevalence of mental disorders in the population. Even if the drop in private health insurance claims shifted costs from the private to the public sector, it seems to have been relatively unimportant in the broader Australian context of large unmet need. At the same time, this drop would have impacted on 1) government budgets paying for some services which would otherwise have been funded privately; 2) private health insurance industry profits, with benefits paid out for this small part of ancillary coverage dropping by half; 3) private health insurance holders, who could not choose to drop coverage for just psychologist services, even though these were now publicly insured; and 4) providers of privately insured services. It is unclear whether similar cost-shifting occurred in response to reforms introduced in the United Kingdom, but the number of people with private health insurance there is lower (at most 11% of the population). 33

Alongside allied health billing items, Better Access also introduced new mental health assessment and care planning items for GPs and psychiatrists, 27 and earlier MBS psychotherapy items were introduced in 2002 for trained GPs. 34 Over the period from 2006 to 2015, comparatively few sessions of focused psychological strategies were delivered by GPs, with little change over time (on average, 36,000 sessions per year nationally compared to 3.3 million sessions delivered by allied health providers under Better Access). 25 However, there was substantial growth in GP mental health planning items alongside the Better Access allied health items. Thus, GPs in Australia seem to have primarily taken on the role of assessment and referral rather than psychotherapy. Although there are no specific psychiatrist billing items for individual psychotherapy under the MBS, total psychiatrist consultations provided under the MBS have remained largely static over time. 25

In the Canadian context, reforms may be quite different to those introduced in Australia, so it is important to understand what may have driven the drop in private insurance claims. This shift from the private to the public sector can likely be explained at least in part by co-payments that were substantially lower (or non-existent) under the new publicly insured Better Access programme than under private insurance. Further evidence of the sensitivity of private health insurance utilisation to changes in public insurance coverage can be seen in the modest growth in private insurance claims after the reduction in Better Access session caps in 2011. In economic terms, this sensitivity seems to be a substitution effect related to the elasticity of demand. Essentially, Australians seem to have sought lower-cost alternatives once they became available. This does not appear to have been intentional offloading from the private insurance sector; we are not aware of any significant policy changes to private health insurance psychology coverage before or after the introduction of Better Access that would explain the reduction in claims and, over the same time period, the numbers of services and benefits paid for all ancillary coverage continued to increase. 23,24

It is also important to consider why private insurance claims were so low despite the high prevalence of mental disorders. Even before the introduction of Better Access, privately insured psychotherapy was used by only a minority of Australians. No data are available on what proportion of people with ancillary coverage have psychologist benefits available, but it may be quite small. Leach et al. 35 found that having private health insurance was not a significant predictor of seeing a mental health professional in 2009, indicating that even those with coverage may not use it. Our analysis highlights the low average rebates provided by private insurers (less than half the cost of a service), as well as indicative annual limits for psychologists of only AU$200 to AU$500; the significant out-of-pocket costs still required from private insurance holders may have discouraged uptake.

Given the low use of private insurance, why then did Better Access grow so rapidly? Apart from the programme being universally accessible and at lower cost than private services, there was also an available workforce ready to meet the demand. From the late 1990s, there was steady growth in the psychology workforce (who comprise most of the Better Access providers), but between 2007 and 2008, there was a further sharp increase from around 58 to 85 full-time equivalent psychologists per 100,000 population. 36 This increase has been attributed to both the new demand generated by Better Access and concurrent national programmes to reduce community stigma and improve help-seeking. 36 It is likely that psychologists completing their training or working in other sectors found it more attractive to work as a private psychologist with the resultant increased community demand for their services. Additionally, the use of GPs as gatekeepers, education for GPs, and new GP mental health billing items seem to have strengthened awareness, partnerships, and referral pathways between GPs and allied health providers, 37 facilitating access to psychotherapy for the majority of individuals whose main mental health service contact is with a GP. 38 As more people sought psychotherapy, they appear to have turned to Better Access as the more affordable and better-publicized programme rather than using more expensive, privately insured services. Even though providers receive higher fees on average through private insurance, the workforce appears to have been drawn to Better Access where demand was higher. Capped funding and targeting to specific groups limited ATAPS to more modest growth over the same period; however, ATAPS has been much more equitably distributed than services provided under the Better Access fee-for-service model. 39,40

Implications for Canada

With CA$5 billion in targeted federal funding recently committed to improving access to mental health services in Canada over the next 10 y, 41 provincial and territorial governments are considering various options to improve access to psychotherapy. 42,43 Lessons learned from Australia regarding the reduction in private insurance claims after the expansion of public insurance are instructive but need to be considered in the context of the overall similarities and differences to the Canadian context. Coverage of employer-sponsored private health insurance is slightly higher in Canada, at two-thirds of the population, 7 compared to 55% for ancillary coverage in Australia. 18 From the limited Canadian claims data available, the magnitude of private health insurance benefits for psychotherapy appears similar or perhaps slightly higher in Canada. One large insurer covering 9 million people (roughly 37.5% of insured Canadians and 26% of the total population) reported paying benefits of CA$28.5 million for psychologists in 2011. 9 Based on a typical annual limit of CA$500 for psychotherapy, 9 this amount may have provided benefits to approximately 57,000 people, just 0.6% of the 9 million beneficiaries. Conversely, Peachey et al. 9 modelled available data to suggest that as much as CA$950 million is spent on private psychology in Canada, some portion by insurers and the remainder by clients in full or part payment. It is not clear why these figures diverge so widely, but the recent CA$28.5 million claims data from a large private insurer is likely to be most indicative of the industry given that it is based on actual claims rather than modelled from assumptions.

Despite this potentially low utilisation of privately insured psychotherapy, the prevalence of mental disorders and unmet need appears similarly high in Canada to that in Australia. 44 In Canada, prevalence is estimated at between 10% with 1 of 6 common disorders 45 to 20% with a broader range of disorders. 46 Like Australia, less than half of Canadians with mental disorders were using services in 2012, and rates of unmet perceived need for counselling were similarly small if somewhat higher in Canada in 2012 (4.3% of the population) compared to Australia in 2007 (2.6%). 1 These figures suggest that expanding public funding for psychotherapy in Canada could have a similar impact on uptake to that seen in Australia, particularly if public programmes are readily affordable and accessible to potential clients. Canadian policy-makers and stakeholders would be wise to prepare for noticeable demand for any new publicly funded services, including the potential for long waitlists.

However, the Canadian experience may be different. For example, the applicability of lessons from Australia regarding the reduction in private insurance claims will depend on the relative attractiveness of employer-sponsored private insurance and new public services to a range of interests: service users, service providers, employers, and private insurance companies in each province and territory. Unlike in Australia, charging a co-payment for services, or extra-billing, is not allowed under the Canada Health Act. If public psychotherapy services are offered free at the point of delivery, in keeping with Canada’s overall health system, reductions in private insurance claims could be more dramatic than in Australia. Although some high-profile employers have recently increased benefits to as much as CA$10,000 per year, 47,48 most coverage limits remain low. For their part, service providers will have new incentives to provide either privately insured or publicly funded services, depending on both their potential earnings and ability to attract clients. Perhaps of more concern, employers in Canada sponsor private insurance and may have new incentives to reduce benefits for psychotherapy while enjoying the advantages of increased public funding of services for their employees. Under this scenario, there is potential for individuals to lose access to private insurance benefits for psychotherapy while not necessarily qualifying for new publicly funded programmes. The Canadian insurance industry could lose some business and may also face increased pressure to release more of its claims data to assist in tracking the impact of reforms, along the lines of what is available in Australia.

The impact of potential reductions in private insurance claims is likely to vary depending on the scope of expanded public services. If a universal programme is introduced along the lines of Better Access, the financial impact of any reduction is more likely to be small relative to the potential uptake and funding required for new public services. However, cash-strapped provincial and territorial governments in Canada are likely to take a more cautious approach. Funding announced to date by Ontario (CA$72.6 M over 3 y) 43 and Quebec (CA$35 M) 42 is more in line with launching pilot projects than a universal programme. The impact of reduced private insurance claims could be much more significant for these smaller-scale reforms. Although the efficient use of public funds necessitates minimised cost-shifting from privately funded services, there will be other considerations for policy-makers, such as equity and the consistency of new programme rules with other parts of the health system (e.g., minimising co-payments).

Conclusion

Although the introduction of public funding for psychotherapy in Australia reduced private health insurance claims, the relative importance to the overall increase in utilisation was small. Whereas Canada has apparently similar levels of baseline service use and unmet need, there are important differences in the context of private and public funding for psychotherapy. Just as in Australia, population-wide public programmes in Canada could see demand outstrip the impact of any potential reductions in employment-based insurance. However, in the Canadian context, the introduction of smaller-scale public programmes with low or no co-payments is more likely and could therefore see more significant impacts from such reductions. Further, with Canada’s employment-based insurance model, increased public funding could create incentives for Canadian employers to reduce available insurance benefits, thereby compounding the potential impact of reduced claims. Policy-makers should think carefully about how to expand public funding to minimize potential cost-shifting from the private to the public sector, while addressing the high rates of unmet need for psychotherapy services to the greatest extent possible.

Footnotes

Acknowledgements

The authors thank Howard Chodos, Lara Di Tomasso, Francine Knoops, Paul Kurdyak, Bonita Varga and Harvey Whiteford for their helpful comments on an earlier version of this manuscript.

Data Access

All data used in this paper were publicly available at the time of writing via the sources referenced in the methods.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.