Abstract

The workings of monetary systems have been controversially discussed. Mainstream economists assert that money creation is a ‘top down’ process governed by centralized monetary policy decisions (central banks => banks => customers), while heterodox economists emphasize ‘bottom up’ dynamics in the opposite direction, driven by customers’ demand for credit. The article draws on sociological insights into the complementarity of formal and informal structures to show how this paradigmatic alternative can be read as a real structural dualism, with two conflicting but complementary chains of influence and initiative. It suggests a ‘dual circuit’ of money creation, with a formal ‘top down’ chain inscribed in institutional competencies, clearing and control mechanisms, and an informal ‘bottom up’ chain emerging spontaneously from everyday maneuvers and pragmatic accommodations by participants. Both chains are contradictory in theory but compatible in practice. This dualistic solution cannot be officially acknowledged, but it is highly viable and apt to operate under complex, uncertain, and variable conditions.

Introduction 1

‘Monetary theory is less abstract than most economic theory; it cannot avoid a relation to reality’ (Hicks, 1967: 156). It was an economist who expressed this hope, half a century ago. Sociologists, who have criticized economists for formalistic and over-rationalistic model-building, should be expected to fare even better in this regard. This article tentatively sketches a sociological model of money creation and monetary systems that combine some elements of economists’ specialist knowledge with sociologists’ sense of social realities.

The workings of monetary systems have been quite a challenge for theorists and practitioners recently. We have witnessed a period of unorthodox monetary policies, growing global money supplies relative to real economic output, the dogged absence of inflation despite this situation, and, even before that, the rise of a shadow banking sector that operates outside the official monetary sphere but deals in practically very money-like instruments (Gorton, 2010; Joyce et al., 2012; Langley, 2015; Thiemann, 2018). At the heart of all this, there is the puzzle of money creation. Money creation is the process by which the volume of money of a given currency is expanded (or contracted) by banks extending credit to customers (or customers paying back those credits), in an institutional hierarchy with prescribed clearing procedures and an apex player – the central bank – that commands a set of monetary policy tools. Money creation is, on the one hand, a highly ‘technical’ process that is described in daunting equations and informed by huge amounts of data and rigorous causal models. On the other hand, it is a highly ‘enigmatic’ or ‘esoteric’ process (Luhmann, 1970c; Riese, 1995) that leaves observers wondering how money can be created out of thin air and evaporate into nothing again. It evokes all the fundamental puzzles of modern money: the paradox of an intrinsically worthless object figuring as the ultimate value substance, the paradox of money being scarce for any user but being, on principle, in unlimited supply, or the mysterious transformation or transubstantiation of debt – sovereign debt or bank debt – into currency and legal tender (Dodd, 2014; Ingham, 2000; Paul, 2012).

The problem of money creation naturally falls into economists’ jurisdiction, who are, however, deeply divided on the issue. Sociologists have approached the issue mainly through the study of central banks. There has been extensive research on central banks’ decision-making processes, their use of academic theories and paradigms, their exposure to political pressures and predicaments, their communicative strategies toward different publics, and their adjustment to conditions of second-, third-, and fourth-order observation (Braun, 2015; Krippner, 2011; Sparsam and Pahl, 2018; Velthuis, 2015; Walter and Wansleben, 2020; Wansleben, 2018). This focus seems an evident choice given that central banks are the most powerful actors on the scene and the central locus of authority and decision in the monetary sphere. 2 However, the focus on policy carries the risk of obscuring structure. Central banks and monetary policy constitute the decision-aspect of money creation, but they do not fully reflect its structural or systemic aspects.

In this article, I choose an alternative approach that widens the focus to the more operational layers of money creation at the levels of banks and customers, as well as inter-bank-markets (Birk and Thiemann, 2020; Braun, 2020; Walter and Wansleben, 2020). To map the processes that are at work here, I draw on long-established sociological insights into the complementarity of formal and informal structures and strategies. I sketch a ‘dual circuit’ model of money creation that includes two countervailing chains of influence which are not fully consistent with and not fully transparent to each other. The model sociologically accommodates the controversy among economists on whether the monetary process is a ‘top down’ (supply-driven) or a ‘bottom up’ (demand-driven) process and whether its role in the economic process must be seen as stabilizing and equilibrating or as endogenously turbulent and destabilizing. While it is not a model in any technical sense and lacks all the attributes of economists’ models – formalization, predictability, rationality – it gains a sense of the tensions, practical contradictions, and precarious balancing operations that are involved in the operation of a complex system.

The model draws on two sources in particular. The first source is a systems theoretical model of dual circuit processes that was developed by Niklas Luhmann (2010) and originally described power processes in political systems. The second source is the post-Keynesian (heterodox) strand of economic theorizing, which has contributed some deep insights on the nature of money. 3 These two sources may not seem to go together well, since systems theory has a reputation for being ‘conservative’ or ‘affirmative’ and for preferring conceptual elegance over empirical relevance, while post-Keynesians are decidedly ‘progressivist’ and ‘critical’ in outlook and are more concerned with policy implications than with conceptual artistry. But creative recombination of elements is the stuff of which scientific progress is made, and ideological affinities or antipathies are quite irrelevant to this.

I am not the first to express the intuition that the monetary system involves more than one causal conduit or more than one direction of selective process. Simone Polillo (2011), for one, described banking and credit systems as shaped both by factors working top down through centralized and specialized players such as banks, states, and credit rating agencies, and factors working bottom up through subsidiary mechanisms of interpersonal ties and business communities. Martijn Konings (2015) described a similar duality for the social architecture of money in general, in that money is both an incontrovertible social fact imposed on us through general symbolic meanings and institutions and an implication of highly differentiated, personalized, and localized meanings and practices. And economist Perry Mehrling (2017), in an attempt to ‘sociologize’ post-Keynesian insights, emphasized the social dynamism – and dynamite – that is produced by the inherent hierarchy of money, in which some forms of money or liabilities/IOUs are more inviolable or more high-powered than others, which spawns structurally induced discontent among those further down in the hierarchy. In a way, my argument picks up there and develops these loose suggestions into an explicit model.

The article is organized as follows. I first summarize economists’ debates on the nature of money creation, in particular, the dominant or mainstream view and a heterodox, post-Keynesian view (section ‘Money creation’). I then introduce the dual circuit model (section ‘The dual circuit of power’) and transfer it to the field of monetary processes (section ‘The dual circuit of money creation’). In concluding, I comment on some features of my model that position it within broader debates on money and monetary theory (section ‘Conclusion’).

A terminological remark is in order before I begin. The term ‘monetary system’ is conspicuously undefined in sociological usage. While economists use it loosely to denote the institutional and regulatory arrangements that are in place to manage money of a given currency – including commercial banks, central banks, treasuries, national and international treaties, and authorities – sociologists have not bothered to define it, be it for all-out rejection of the term ‘system’ or for other reasons. It is not even clear whether systems theorists would consider it a system. 4 To resolve this issue would be beyond the scope of this article. For the time being, I take the monetary system as if it could be analyzed as a system and likened to other cases of complex system dynamics, without, however, making overly strict assumptions as to its systemness.

Money creation

We have been living in a pure fiat money world for at least half a century. Fiat money is money, the value of which is not backed by gold or other ‘intrinsically’ valuable substances but is managed by states and monetary authorities. The last remnants of gold-backed money withered away with the repeal of Bretton Woods in 1973, when the gold convertibility of the dollar was abolished. But gold-backing had eroded long before, in a gradual process stretching over centuries, during which the gold- or silver-convertibility of currencies was declared, renounced, and diluted in an on and off-process with many twists and turns through phases and countries (Carruthers and Babb, 1996; Davies, 2002). Even where gold-backing was retained – the guarantee to convert, say, a dollar note into a specified amount of gold upon demand – this guarantee was targeted at the individual dollar note and the individual dollar owner, while the total amount of dollars in circulation had long been decoupled from – or only loosely and ‘fractionally’ coupled with – the amount of gold stored in the vaults of a central bank. This is because a modern economy requires flexibility in the supply of money. It cannot operate with a currency that is limited by a factor as accidental as the physical availability of bullion, which would imply that the occasional discovery of a gold mine or the occasional loss of a shipload of gold would seriously affect economic dynamics (Hayek, 1931; Ingham, 2004; Lerner, 1947).

Rather than being a proxy for gold, modern money is a creature of historically evolved arrangements of banks, central banks, governments, and financial markets. At its heart is a network of banks that operate via book-entries and mutual clearing of accounts. Since one, two, or three centuries (depending on country), the system has had a central bank at its apex, which has banks settle on its books and act as a regulating authority in a number of ways. In this arrangement, gold has played a role as a backstop mechanism, panic-container, and trust-amplifier, but it was never the effective driver or basis of the system. Rather, the cornerstone of the system is the fact that banks lend more money to customers than they ‘have.’ The money that is lent does not need to be ‘there’ before the act of lending; rather, any act of lending by a bank increases the amount of money in existence by approximately the sum that is lent. When a bank advances a €100,000 credit to a customer, these €100,000 are created anew, or at least most of it is, although the bank may be required to hold a fraction – usually somewhere between 1% and 10% – as reserves in a central bank account. The money is created ‘out of thin air’ through the very act of crediting the customer’s account, technically: through entering a new deposit on the liability side of the bank’s balance sheet and a new loan on the asset side (Bundesbank, 2017; McLeay et al., 2014). Conversely, when the customer retires the credit, the money disappears. Modern money – some say: any money – is based on credit, or debt, which implies that debt cannot be a vicious or profligate thing at the system level (as opposed to the level of individual maxims and moral), since if no one were willing to go into debt, there would be no money, and if everyone repaid their debt at the same time, the monetary system would implode (Dodd, 2014: 92–93). Money emerges from the books of the bank and disappears into them again, via the stroke of a pen or a computer key.

These are the facts. However, the theoretical interpretations of the process diverge widely, and it is not easy to even describe it without taking sides for one paradigm or the other by the mere choice of words. Different strands of theorizing offer directly conflicting accounts of what actually goes on in money creation. For purposes of this article, I will draw on the orthodox version, which is defined by the neoclassical-neo-Keynesian synthesis, and the heterodox version that is advanced by the post-Keynesian school of thought. I refer the orthodox version first, and I add the warning that if this seems dull and familiar to the reader, this is because it is the dominant story which has diffused into newspapers and textbooks, but that this view of things is by no means self-evident and will be challenged and turned on its head immediately afterward.

According to the mainstream view, the monetary process is ultimately controlled by the central bank, which sits at the top of the system and watches over equilibrium conditions in the economy. Money, in this paradigm, is a numerical expression for or a reduplicating ‘veil’ over the real values of things – goods, services – that are produced in the economy, and the amount of money that is available in the system must reflect the amount of real values produced, otherwise there will be inflation. What is more, the money supply must reflect the productive potentials or theoretical optima that would be attainable in the economy through an optimal allocation of resources, that is, through optimizing decisions on who buys what, who invests in what, how many resources are channeled into one sector or another. These processes tend toward optimum or equilibrium, but they are distorted by all sorts of frictions, such as business cycles and sticky prices. An optimal money supply will bring the system closer to those equilibrium conditions in which full use of the economy’s resources is made, or in which the ‘output gap’ between potential and actual output is minimized. Hence, the role of monetary policy is to equilibrate allocation decisions among economic sectors and among present and future uses of resources.

Classical monetarists had seen money as an exogenous element that is introduced into the system by a god-like entity, or at least by an actor who is not an economic actor, that is, not motivated by economic profit. More recently, economists have stressed not exogeneity and discretion, but rather the predictability and intelligibility of central bank decisions, because the latter will have full effect only to the degree in which they mold participants’ expectations regarding the future, not only their present actions (Woodford, 2003, 2010). This is why today, central banks publicly explicate their policy rules and make them as transparent as possible. In either variant, there is a money supply chain that is set up in a ‘top down’ way, with the central bank setting the critical parameters and the effects trickling down into the decisions made by economic participants.

This view is based in the medium-of-exchange theory of money. Money, on this account, is a lubricant in exchange, which facilitates the exchange of goods and relieves us of the arduousness of barter. More technically: money is an intermediate good that has no value in itself but helps in bringing goods to their point of greatest utility. And banks, according to a related theory, are intermediaries in the flow of capital which organize the allocation of a scarce good named capital in the economy (see for the intermediation paradigm, e.g. Allen and Gale, 2004; Bhattacharya and Thakor, 1993). Some participants accumulate funds, they own more money than they currently need; others need more money for investment or consumption purposes than they currently own; and what banks do is that they channel funds from ‘surplus pockets’ to ‘deficit pockets.’ From a macroeconomic point of view, Banks collect funds first and then lend them out to customers. They do not really create money, they allocate funds that were accumulated before. In the traditional imagery, someone needs to carry a bag of money into the bank before someone else can take out a bag of money as a loan. And even if any economist knows that banks can technically create money without collecting money from depositors first, it is assumed that the technicalities of the process do not alter banks’ overall place in the economic process. There must be some ‘loanable funds’ on one side so that borrowers can take out loans on the other (Krugman, 2012, 2013)

If this is the conventional wisdom, here comes the counter-story, which has been told under the name of ‘endogenous money’ (Lavoie, 1984; Moore, 1988a, 1988b; Wray, 1990). Money, here, is created ‘endogenously’ in the normal course of the economic events, by profit-minded actors responding to economic opportunities. Money is created when customers turn to their bank and request credit, and the bank, applying its own standards of creditworthiness and profitability, approves of these requests. How much credit is extended, and how much money is in effect created, is primarily a matter of financial cycles: during boom times, moods are up, participants are eager to increase their leverage, and there are many prospective borrowers who can produce highly valuated assets to serve as collateral, while during bust times, leverage is reduced and assets eligible as collateral depreciate in value (Adrian and Shin, 2010; Minsky, 1986). The same cycles determine the profit opportunities and ‘risk hunger’ of banks. Hence, money is inherently procyclical and irremediably turbulent. It is a source of instability rather than stability, a dynamic agent rather than a passive reflection or a tool of equilibration.

Central banks, according to this paradigm, oversee the process only precariously and imperfectly. With all their instruments of monetary policy, they can only determine the price (interest rate) but not the volume of credit extended, and, hence, money created. Since money can be created ‘out of thin air’ by banks, money supply is not an independent factor; rather, supply will always match demand. The monetary process is an emergently or endogenously turbulent process; it is more of a ‘bottom up’ than ‘top down’ nature. Central banks cannot be an effectively restricting or governing factor, even if they can be a driving or pushing factor at times (which seems logical from an ‘emergent order’ point of view: they can join the ranks of actors or participants, but they cannot control or design the system). Central banks are, for the most part, accommodative players: they act supportively or defensively, they cater to the needs of the system, and, in moments of crisis, come to the rescue of failing banks. In an acute crisis, the central bank will go to great lengths and even bend some rules in order to help a bank in distress, because anything else would jeopardize the stability of the system. When it comes to the crunch, central banks prioritize collapse prevention over rule enforcement (Goodhart, 2011; Lavoie, 2013; Mehrling, 2010).

The fact that money is created out of thin air is taken seriously here. Banks are the true source of money, they do not merely allocate funds that have been accumulated elsewhere (Jakab and Kumhof, 2019). Rather, money ‘emanates’ from them and flows back to them when credit is repaid. 5 This view is based on the credit theory of money. Money, here, is primarily rooted not in relations of exchange but in relations of debt or credit (Graeber, 2011; Wray, 1990, 1993). It is the unit of account in which debts are written, the unit in terms of which participants record how much one owes the other. Money is essentially a temporal arrangement. It is not about the exchange of qualitatively different things, as in commodity exchange, it is about the exchange of the same thing at two different points in time – a forward contract of the form ‘wheat now for more wheat later,’ or ‘money now for more money later’ (Minsky, 1986: 192, 196; Wray, 1990: 9). The credit theory of money is more social, more constructivist, and less essentialist than the medium-of-exchange-theory, in which money is a reflection of some material or otherwise pre-existing value. Money, here, reflects nothing but trust among participants and expectations concerning the future, and this is why it can genuinely be created by participants entering into credit relations and why it can be a genuine ‘positive sum game,’ rather than the ‘zero sum game’ assumed in the orthodox allocation frame (Chick, 2000: 125).

So, we are faced with two diametrically opposed theories of money creation and are left to wonder: Who got it right? Sociologists may not be in a position to adjudicate this debate, even if they may sympathize with the credit theory of money and the heterodox notion of money as an essentially social and temporal arrangement (Dodd, 2014; Ingham, 2004; Konings, 2015; Sahr, 2017a), or with the post-Keynesian emphasis on the ‘endogenous’, spontaneous, turbulent nature of money creation (Konings, 2018; Polillo, 2011), which resembles the sociological notion of the emergence of social order from an endless stream of situations, struggles, and events (Abbott, 2016; Latour, 2005; Luhmann, 1996; White, 1992). But vague sympathies will not suffice. The controversy involves complex chains of causality and is waged with formal means far beyond sociologists’ grasp. The two monetary paradigms have been fiercely antagonistic and have fuelled passionate debates over theoretical fundamentals as well as policy implications. Heterodox scholars have attacked the mainstream view as fatally erroneous and disastrous in its practical consequences, while mainstream proponents have continuously refined their assumptions and have warned of the theoretical and practical indiscipline and ‘anything goes’ that would result from a triumph of post-Keynesian thinking, in particular, its most radical variant, Wray’s Modern Money Theory.

And yet, sociologists may have something to add to this debate, and not just by taking sides. Sociologists are trained in the art of stepping back and observing from a distance. Faced with an entrenched clash of paradigms, they can refuse to choose sides and remember the classical dictum that contradictions in theory can point to practical tensions and antagonisms – to real, factually existing faultlines in social arrangements, not just to unresolved intellectual problems (Lukács, 1967 [1923]). Maybe both theories got something right, and both got something wrong or under-complex, and the sociologist’s task is to devise a model that accommodates both versions and incorporates them into a coherent model or conceptual idea.

The dual circuit of power

Social realities have a tendency to be less orderly than the institutional blueprints that describe them. This has long been known from the study of organizations, which always produce informal layers of activities, roles, and expectations that sit uneasily with the formal order – sometimes in neutral co-existence, sometimes in direct breach of formal rules (Kühl, 2021; Meyer and Rowan, 1977). In most organizations, the levels of talk and action are only loosely coupled (Brunsson, 1989). Also, entire institutional fields have been shown to generate high levels of isomorphism at the level of formal structures and window dressing while tolerating highly diverse factual practices and daily activities (Scott and Meyer, 1994; Thomas et al., 1987). This has been shown for fields as diverse as national polities and international policy regimes, legal systems, schools, universities, and so on.

In what follows, I employ a model for formal/informal dualities that was developed by Niklas Luhmann (1994, 2010) in the 1970s, but published only later, and that describes the flows of power and influence in political systems. Such a transfer from political sociology to the sociology of money must, of course, be done with care. But I see this as a chance rather than a hindrance, given that cross-fertilization among different fields of research has always been a strength of sociology as compared to other, single-focus disciplines such as political science, pedagogy, epistemology, economics, and so on. I also wish to make clear that, by drawing on a Luhmannian model, I do not commit myself to embracing a Luhmannian theory of money and the economy. Luhmann has not been particularly popular among economic sociologists, and there are good reasons for this in his conception of money, which uncritically sets out from the notion of money as a medium of exchange (Luhmann, 1970c), or a means of payment (Luhmann, 1988), and merely transposes it into a general theory of media of communication. But this does not rule out the possibility that there are powerful conceptual tools in other parts of his theory. It is an open secret among systems theorists that Luhmann’s knowledge of the economy was less deep and less comprehensive than his knowledge of, say, politics or science, and if we are to exploit Luhmannian ideas, we should certainly draw them from those parts of his work where he was at his best. Thus, the model presented here, while drawing on a Luhmannian system model, is a radical alternative to Luhmann’s conception of money and is based on completely different assumptions.

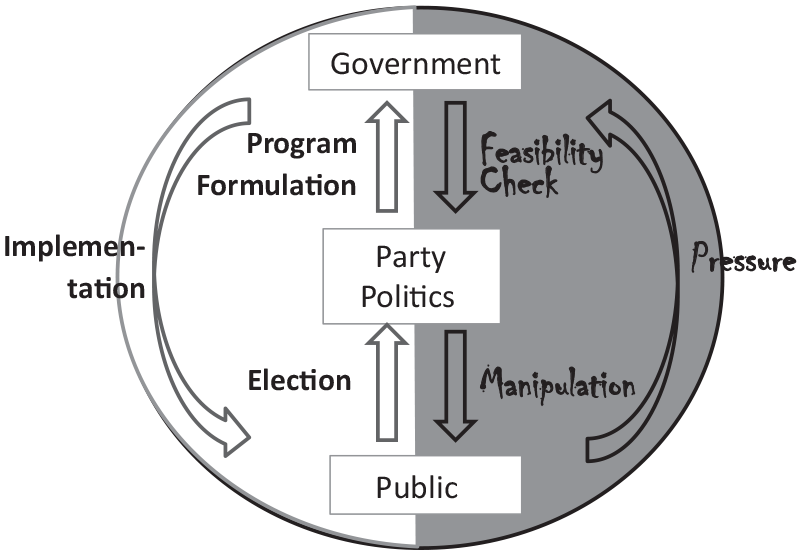

The model in question describes the chains of power and influence that operate in modern political systems. There are flows of power between three parts or subsystems: government, party politics, and the public or citizenry (Luhmann, 2010: 130–148). ‘Government’ includes any authority with the power to make collectively binding decisions, from presidents or prime ministers and national parliaments down to local authorities. ‘Party politics’ refers to those players, activities, and events which do not involve binding decision-making but prepare the ground for it, such as political parties and other associations, social movements, public debates, and so on. Finally, the ‘public’ is the general population of citizens who enter the stage both as voters and as claimants to administrative acts, permits, or benefits (Figure 1).

The dual circuit of power.

According to textbook theories of democracy, power works its way up from the people or the citizenry, via political parties and other vehicles for the articulation of interests and opinions, to government, and back to the people. The three interfaces involved are: (1) Citizens vote for their preferred parties or candidates. (2) Winning parties or candidates form a government and set priorities for governmental action. (3) Governmental agencies implement these decisions and pass them back to citizens through administrative acts. This order of things implies that the people as an aggregate are always governed as they deserve, that government is an instrument of a people ‘governing itself’, and that interests and opinions will always take the route through public articulation and contestation, and – if they prevail – incorporation into official governmental courses of action. This sense of direction or this ‘spin’ of the process is celebrated in national civil ceremonies, presidential addresses, and political education classes.

However, there is a second set of processes that operates in the opposite direction. It includes the less visible and less respectable operations of power and influence that occur at the following, reversed interfaces: (1) In elections, parties, and candidates will go to great lengths to influence citizens’ ‘sovereign’ decisions by targeting them with slogans and buzzwords, alarming or placating rhetoric, or custom-tailored canvassing. (2) In governmental decision-making, elected leaders rely heavily on experts and bureaucrats from the administrative machinery, whose professional take on the feasibility or unfeasibility, affordability or unaffordability, advisability or unadvisability of considered courses of action will often outweigh regard for voters’ concerns. (3) In implementing governmental decisions, governmental agencies are often pressured by the very recipients of those decisions – in legal, illegal, or not-exactly-legal ways – in particular, if these recipients are not ‘ordinary citizens’ but large corporations, local dignitaries, or other powerful groups.

For Luhmann, maneuvers in the second sense of direction are equally essential contributions to the operation of a political system as those in the official half. They lack transparency and legitimacy, they carry an odor of dubiousness or inappropriateness, and they may be concealed or downplayed in public and discussed only with close collaborators. Nevertheless, they make up a prominent part of participants’ daily activities, and Luhmann contends that a political system would be unable to operate without them, at least at the established level of complexity. This is parallel to the way in which organizations would break down if all their members adopted a ‘work-to-rule’ attitude and dropped all non-formalized activities.

For the power medium to work at its full potential, there must be arrangements that combine the two directions or spins of the process. This gives the system the elasticity and pragmatic flexibility that it needs in order to accommodate the complexities of modern conditions – such as universal political participation, proliferation of groups with political stakes and voices, proliferation and (technical or juridical) complexification of issues at stake, deepening of administrative penetration of everyday life – which entail delicate problems of balancing different needs and requirements against each other. If the system were reduced to either one of its halves, complexity would be reduced too drastically, and the system would tend to rigidify and become vulnerable to attack or disruptive change (Luhmann, 1970b, 2010: 226–249). Exclusive reliance on official chains of power would render politics ideological and formalistic, while exclusive reliance on unofficial chains would spell clientelism and ‘despotic power.’ On the contrary, in a well-balanced political system, both sides can be developed and refined together. The smooth, fine-tuned operation of the political system requires a careful balancing of both halves or spins of the process. The official half provides the institutional scaffolding and semantic self-conception of the system; it provides anchors for political structures and identities, but it would be naïve to take it for the system itself. The unofficial half provides leeway for practical shortcuts, situational maneuvering, and outlets for participants’ activism; it parasitizes but also energizes the official circuit. Both have, in fact, developed and flourished together, even if their co-existence must be hidden behind an asymmetry of visibility and legitimacy.

Most commentators emphasize either the first or the second half but do not acknowledge the delicate balance that exists between them. On the one hand, there are the political theorists and propagandists of the system who celebrate the official half and tend to see the unofficial traffic that goes on in the system as minor defect and inevitable pollution, caused by human flaws and addressable with suitable measures of containment and control. On the other hand, there are the debunkers and ‘critical critics’ (Marx), such as lobbyism-control activists or proponents of ruling-class theories, who point their fingers at the unofficial practices, emphasize their pervasiveness, and condemn existing political systems for being corrupt and ‘not really democratic.’ The latter stance, while critical and in a way the polar opposite of the first, also implies that the unofficial practices should not be there and does not accept them as a vital part of the system. Within the political discourse, the unofficial circuit cannot be embraced as a genuine contribution to the system. This can only be done by sociologists or other outside observers, who do not share the normative standards or the constitutive ‘illusio’ (Bourdieu) of the system and can advance views that, within the orbit of the system, would be cynical.

The sociologist can ‘take a unitary view of complexes of action functionally and structurally, even if they appear controversial and conflicting to participants, and can even understand the function of these controversies themselves’ (Luhmann, 2010: 125f., my translation). Luhmann’s model transcends both partial theories that are prominent within the system. Against the proponents of democracy theories, Luhmann holds that they subscribe to an idealistic view of things that can never be matched by factually existing political systems. Against the critics and debunkers, he argues that legitimacy cannot be the touchstone of sociological theorizing and that sociologists have always acknowledged the hidden, non-obvious, illegitimate, and illicit aspects of social reality. While criticism of this sort can be a meritorious part of the political discourse – as in Durkheim’s ‘colère publique,’ it serves the affirmation of the official values or spin of the system – it does not make good sociology either. Luhmann agrees that corruption and lobbyism must be held in check, but in his eyes, they are held in check by the total architecture of the system, which relegates such practices to the unofficial half of the system and thus to a hidden and discomforting mode of existence, at least in the Organisation for Economic Co-operation and Development (OECD) part of the world.

Similar to conventional ‘division of powers’ or ‘checks and balances’ models of political systems, the dual circuit model posits two countervailing forces that are balanced against each other. But contrary to conventional models, it cannot be made the official theory of the system because it is too ‘cynical,’ or rather: because it is too symmetrical in its stance toward the official and unofficial, legitimate and illegitimate, presentable and unpresentable aspects of political life.

The more general point is that conflicting orders of causality need not be conceived as mutually exclusive, but can be seen as complementary and mutually facilitating – and ‘complementary’ not only in a statistical sense in which events of both types can be shown to occur at certain frequencies, but in a systematic sense in which it is their very interplay that allows the system to operate at high levels of complexity. This implies an intricate theoretical relation between system and element, or system and action (Kieserling, 2012). In any given situation, the official and unofficial orientations of the political process require conflicting actions, and they cannot be satisfied through one and the same act. Hence, actors will frequently find themselves in conflicts of interest or conscience. However, at the system level, the two orientations or spins of the circuit are complementary or even mutually constitutive. The informal order owes its existence or its potency to the formal order to which it attaches itself and which it parasitically inverts. But the formal order owes its necessity and demonstrated desirability to the informal order which would otherwise take over and which, with all its arbitrary and despotic nature, would obviously not be acceptable. The co-existence of these two orders of influence is precarious at the element level and stressful for the individual actor, but it is stable and functional at the system level.

It is this complexity differential between action and system that Luhmann based his theory on. Systems are more complex than actions, and system rationality is more complex and more ambivalent than action rationality. This is why research questions targeted at the system level will often be more revealing or more illuminating than questions targeted at the actor level. Actors are often overburdened, and what we want to know is not only how they act and on what grounds, but how they are overburdened and by which structural arrangements (Friedland and Arjaliès, 2021; Wendt, 1987). But what is of interest here are not the ramifications of this argument in systems theory but its implications for the problem of money creation, to which I now turn.

Before I set out to present my model, I wish to point out that Luhmann (1988: 131–150) himself, in one chapter, sought to identify dual circuit structures in money and the economy. But this model falls short of its own aspirations, at least if the dual circuit of power is taken as a baseline. What it offers is basically a standard macroeconomic model of circular flows of income – money flowing one way and commodities/labor flowing the other way – that addresses more or less trivial issues, such as: When money is spent (or: illiquidity is accumulated), it must be replaced (or: liquidity procured) by new inflows, either by way of profitable undertakings, or by way of tax collection, or by way of labor. 6 But the model lacks all the essential attributes of a Luhmannian dual circuit model, such as (1) genuine antagonism between the two spins, rather than a simple quid pro quo, an exchange of goods for money and (2) an asymmetry in legitimacy and transparency. 7 Hence, I assume the liberty not to be convinced by this model. Instead, I take this passage as an invitation to reconsider the problem and do it all over again.

The dual circuit of money creation

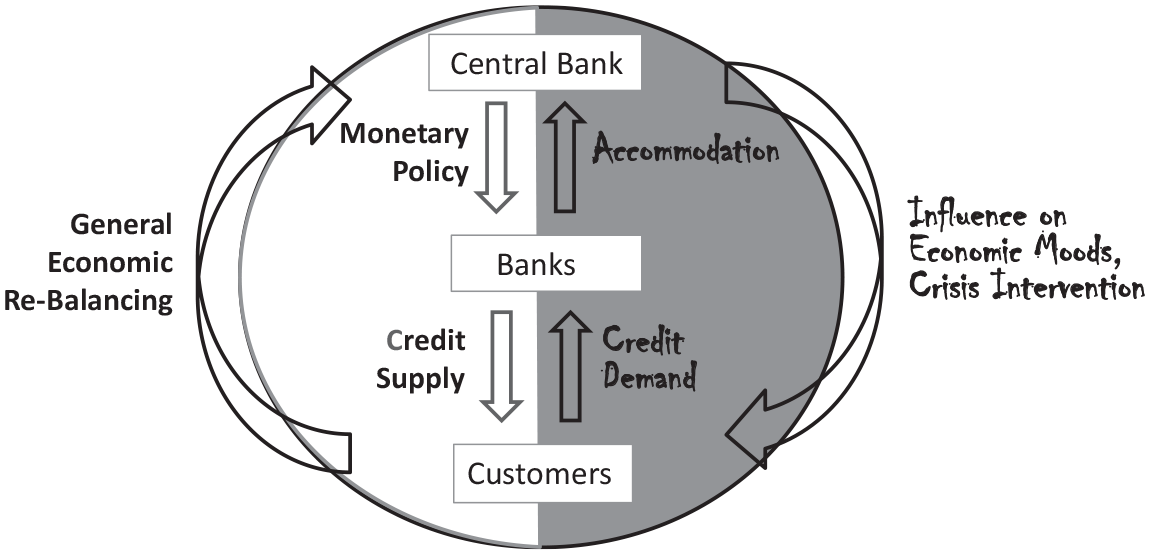

In modern monetary systems, we conveniently find three positions involved in the process, too: central banks, commercial banks, and customers, that is, borrowers, whether individuals/households or firms. There is an obvious hierarchy among these positions, and after what was said in section ‘Money creation,’ a duality of directions of influence is not hard to come up with.

On the one hand, there is the chain of control that works ‘top down’ through the following interfaces: (1) Central banks determine interest rates and act as clearing and oversight institutions in the banking sector. (2) Banks extend credit to customers. (3) The money created in this way feeds back into general economic processes, boosting or curbing growth and affecting allocation decisions, and observation of these processes informs the central bank in its next round of decisions. This chain of influence defines the institutional architecture of the system and is inscribed in institutional rules, competencies, and clearing procedures. (And we can note in passing that the official circuit here follows the inverted order – top down rather than bottom up – from what we saw in political systems, which are emphatically not set up as top down systems of rule and domination.)

The technicalities of this chain are continuously adjusted according to the development of credit practices and the business networks in which banks operate (Birk and Thiemann, 2020; Davies, 2002; Gabor and Ban, 2016; Mehrling, 2010; Mehrling et al., 2013; Walter and Wansleben, 2020). The interface between central banks and banks has evolved from a setting in which central banks determined interest rates simply by decree, that is, by quoting the conditions at which they would lend to banks (Lombard rate), to today’s more indirect mechanisms, with central banks targeting interbank money markets – for short-term credit – and bond markets – for longer term credit – as those private markets where the bulk of the wholesale credit business is done. The bank–customer interface is more steady and usually more trivial, even it if can cause some trouble when, for example, banks refuse to pass on the liquidity provided by central banks to their customers. The third interface, in which these monetary processes feed back into general economic growth and re-balancing, is permanently reworked through central bankers’ absorption of academic theories and models, through learning from historical experience, but also through learning by economic participants, in what sometimes looks like a cat-and-mouse-game: Who can incorporate more of the other’s anticipated moves and rationalities?

But this is not the complete picture, and the interfaces of this chain have produced and absorbed a great deal of informal orientations, strategies, and rationales. These informal mechanisms form an inverse circuit of influence that follows a bottom up or ‘grassroot’ logic: (1) Banks create money upon customers’ demand, responding primarily to financial cycles, that is, to high or low expectations, favorable or unfavorable risk climate. (2) Central banks behave largely accommodatively, playing along with the game in normal times and pouring oil on troubled waters in crisis times. (3) However, central banks may influence economic conditions in ways other than through the money creation chain, for example, by spreading optimism or wariness among economic actors in general and by assuming a key position in crisis management and financial system stabilization that was not envisioned by their institutional architects. 8 As usual, participants’ orientations and practical maneuvers are not identical with institutional blueprints, and the blueprints themselves were made necessary by the spontaneous grassroot dynamism of the system that historically preceded the institutional controls and cannot be completely undone by them.

The informal spin follows an ‘emergent order’ logic that is captured in the tenet advanced by heterodox monetary theorists: ‘loans make deposits, deposits make reserves, and money demand induces money supply’ (Lavoie, 1985; Wray, 1990: 73). And we may add, ‘[. . .] and monetary crisis induces survival reactions as needed’. The emergent dynamism of the system sustains a top player that may be called upon with great urgency and that draws great hopes by some, but that is, in fact, more a cork on the waves than a pilot in control of events. Its power is lent and ‘owned’ by the system rather than by some higher rationality based in science or some actor-of-last-resort status. Central banks can be rigid rule-enforcers only in theory; in practice they have behaved quite softly and permissively. They cannot help but come to the rescue of a failing bank, even if that requires some laxness in rule enforcement, such as generous interpretation of the bank’s solvency situation, flexible handling of collateral requirements, or flexible definition of eligibility criteria (Goodhart, 2011; Lavoie, 2013; Mehrling, 2010). 9 This is because anything else would entail the collapse of the bank and, possibly, the collapse of the entire banking and credit system. Stabilization and crisis prevention have always been among the noblest – formal or informal – duties of central banks. Sociologically, this makes them a case of an organization with multiple goals that are not, or not under any set of conditions, compatible with each other (Kühl, 2021). And within economic theory, this emergent order quality is the reason why the conceptual dichotomy of supply/demand is less symmetrical than it seems and why the switch to demand takes us to an entirely different mode of theorizing, one that describes a much more turbulent, unruly, and decentralized world.

Thus, the official chain of causality is not impotent but it is incomplete. Money creation in banks does not take place irrespective of central bank policies, but it is much more than the implementation chain of central bankers’ decisions – as any subordinate organization is more than the implementation agency of its headquarter. Central banks do wield impressive powers, but they ‘do not have it in their power to nonaccommodate’ (Moore, 1988a: xii). To expect them to effectively determine the rules or set the pace of the game would be pretty much to expect the tail to wag the dog. And monetary processes as a whole can be employed as stabilizing and balancing mechanisms in complex economies, but they also feature an endogenous monetary and financial rationality that is itself a source of instability and turbulence. Systems theorists might cite the principle of system formation here: once they are established as a system in their own right, they cannot be subjected to any outside logic – including any larger, overarching logic – to any degree of perfection. But this would require that we resolve the issue of the monetary system’s systemness, which I will put off to a separate article (Kuchler, 2022).

Sociologically, there is no need to see the two circuits as incompatible. In fact, at a deep structural or systemic level, they are mutually complementary or even mutually constitutive, even if they may be conflictual at the immediate action level. In the long run, the two can only persist together, each crystallizing as a counterpart or corrective to the other. The formal circuit provides the institutional grid and official narrative of the system and installs a sense of monitoring and control that is vital for the public trust in the system. If people were told that banking and money creation were a matter of spontaneously bubbling events that could not really be controlled by anyone, this would not help the trust in and the stability of the system. The informal circuit provides everyday orientation for players and means of pragmatic flexibility, which mitigate but do not undermine the official chain. The whole arrangement nicely illustrates Luhmann’s tenet that is ‘any system, to be viable, must contain more information than it can integrate and legitimate’ (Luhmann, 1965: 178, my translation).

That the two circuits have been seen as mutually exclusive, and have fuelled paradigmatic debate, is for two reasons: first, because of economists’ taste for rational causal models, and second, because of the deficient legitimacy of the second kind, which has prevented it from being fully acknowledged. In fact, neither of those two selective conduits could survive without the other. The formal chain can never control the complete operation of the system down to the last euro or dollar, and if it could, it would stifle the system and choke off its energy. The informal side, while in a way more elementary or primordial, would be unstable and bound to self-destruction if left to itself. 10 Realistically speaking, their uneasy co-existence may be the best solution that is to be had in a world of ill-defined problems and imperfect solutions.

In this case, maybe the deepest reason for this structural dualism is the fundamental paradox of modern fiat money: that it can, on the one hand, be freely created and flexibly adapted to the needs of a dynamic economy, and, on the other hand, must retain the status as a scarce commodity and stand-in for the scarcity premise of economic life (Ingham, 2000; Paul, 2012). As any logical paradox, this one does not have a once-and-for-all-solution but calls for a structural arrangement that somehow reflects this impossible mission – for example, a dual arrangement that allows for some oscillation between the imperative of limitation and control and the imperative of flexibility and accommodation, or for a pragmatic ‘balance between discipline and elasticity’ (Mehrling, 2010: 4). In general, it does not come as a surprise to a systems theorist that stability and instability coexist within the same arrangement. Systems need both a capacity for stabilization and invariance and a capacity for flexibility and change. This does not constitute an alternative at the system level. To pit them against each other would be absurd for any systems theorist.

The dual circuit model elegantly explains the asymmetry in standing between the two monetary paradigms. Orthodox theory defines and codifies the institutional framework of the system; it is a self-idealization, but a self-idealization that has sedimented into the structural architecture of the system, or that has become performative. It serves as the self-simplifying and self-regulating device of a system that, as a system, is basically more turbulent and uncontrollable than it can itself digest. On the contrary, heterodoxy lends a voice to the underlying ‘wild,’ spontaneous, emergent processes in the system. It challenges the reassuring vision of the orthodox view and is thus condemned to the role of spoiler and ‘heretic’ – the eternal underdog theory that brings to light the disturbing back side of the system which suffers from irremediable ‘legitimatory homelessness’ (Sahr, 2017b: 131). This theory is condemned to a fringe existence, no matter how well-elaborated its papers may be. The two theories do not compete on academic ground only, they occupy different positions in social reality. The dual spin model, on the contrary, takes a symmetrical stance toward both paradigms, at least in theory. In social fact, of course, the symmetrical handling of a dominant and a challenger theory is never a symmetrical act – it implies an elevation or dignification of heterodoxy. But in its conceptual construction, the model offers a symmetrical and, hence, potentially irritating argument. In my eyes, this is the only way in which a sociologist can hope to produce even the slightest effect or irritation among economists. 11

The model also allows to map the argumentative strategy of the most radical branch of post-Keynesianism, Modern Money Theory (MMT) (Wray, 2012). MMT selectively emphasizes one informal link in the system that is not even included in Figure 2, the link between central banks and ‘their’ governments. MMT holds that governments can create as much money as they wish, since they are the ultimate source of money and can never run out of money in their own currency. This axiom is built on the refusal to distinguish between central bank and government/treasury, which are collapsed – or ‘consolidated’ – into the generic entity ‘the state.’ This entity, then, not surprisingly, has almost unlimited power over monetary affairs. While MMT has its merits as an antidote against overdrawn austerity talk, I think it cuts too many edges in ignoring the institutional – formal – autonomy that central banks indeed have enjoyed in most countries most of the time. In seeing central banks as unproblematically amenable and serviceable to governments, it celebrates some of the informal alliances and imperatives that have crystallized in the system, but it fails to grasp the subtle balance supporting the total arrangement, in which central banks’ cooperative stance toward governments is indeed a fragile, hard-to-earn, never taken-for-granted resource (for similar critique, see Lavoie, 2013).

The dual circuit of money creation.

Turning away from theory, we find that the practice of central banking has, in recent years, incorporated a great deal of this dualistic arrangement. Central bankers, as both the ‘holy ghost’ and the engine room operators of the modern monetary economy, have adopted a remarkably flexible and pragmatic stance, or as Luhmann would say: an opportunistic stance, toward their job. (And I hasten to add that ‘opportunism’ is a positively connoted term in Luhmann’s writing, not a pejorative term; it describes the flexibility in the setting of priorities that is required for any complex system, which can never be streamlined to accomplish one goal, one mission, one purpose alone.) Central bankers in major countries and currency areas have absorbed some heterodox lines of thought and have been ready to conduct unorthodox operations, irrespective of whether or not they are theoretically tenable and formally well-designed. In this spirit, Fed chairman Ben Bernanke once said, ‘The problem with Quantitative Easing is it works in practice, but it doesn’t work in theory’ (quoted in Harding, 2014). His predecessor at the Fed, Alan Greenspan, is quoted – somewhat triumphantly – by heterodox monetary theorists with the casual concession that ‘there is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody’ (quoted in Kelton, 2020; Svetlik, 2019). And there is a much-cited paper by the Bank of England that officially acknowledges that money is indeed created out of thin air without restriction by reserve requirements and without being based in any kind of pre-accumulated funds (McLeay et al., 2014).

In general, many insiders will off the record acknowledge that the practical imperatives to which central banks respond are not always congruent with their official mission – which reads: monetary policy and inflation control – and that central banks have for some time now factually served to stabilize financial cycles. This pragmatic duality cannot be officially admitted because that would make central banks unpredictable, erratic, or overdetermined players who pursue incongruent goals at the same time. There is a ‘necessary fiction’ component that is built into in this arrangement, as Marxists would say, or an irremediable institutional ‘hypocrisy,’ as Brunsson (1989) would say. There can be no theory for the pragmatic combination or alternation between the two frames, which would have to be a meta-theory, which would soon run into the same problem of consistent formulation of something that is, by its very nature, not consistent. It would be interesting to describe in more detail central bankers’ actual procedures and deliberations in this regard. I am not competent to do this, but it has been suggested by two reviewers of this article that this might be a worthwhile thing to do. My feeling is that central bankers may, by virtue (or curse) of this indeterminacy, feature the attributes of a classic profession, analogous to lawyers, teachers, physicians, or therapists. Professions in this sense are organized around complex, overdetermined systems, and this is why they cannot be based on theory (at best: on theories, which implies controversy and uncertainty), but only on experience, intuition, and good judgment.

Echoing, from the other side, this backstage flexibility displayed by central bankers, one of the post-Keynesians whom I talked to informally conceded that a monetary system probably does need some agents who uphold the official chain of control and preach restrictions on money creation and that otherwise things would get out of hand. A conservative newspaper commentator also comes close to getting the full picture when he writes that the potential for unlimited money creation by banks and governments may not harm our monetary systems, but only on condition that governments do not ‘know’ or do not officially acknowledge this potential.

Of course it is true that the dollar has been strong and there is no immediate danger of inflation. But would that still be the case if the US officially switched over to Modern Monetary Theory, the Fed found itself forced to finance government deficits and the government officially declared that it could do whatever it wanted without going bankrupt? (Piper, 2019, my translation)

This, again, parallels the situation in politics, where many politicians will informally and off the record admit that much of politics is about maximizing personal or party success, but who would be ill-advised to make an official declaration to this effect. It is this precarious epistemological status that is hard to accept for non-sociologists or positivists of all sorts: that there are truths that are known to everyone but cannot be officially acknowledged, and vice versa: that there are indispensable fictions, founding myths, and working illusions that would not survive close scrutiny and yet cannot be dismissed.

The model presented here is obviously very coarse and tentative. At the present stage, it is no more than a fresh sociological idea contributing to an extended debate, at best inducing some thought about compatibility and incompatibility. But what I believe it can do is provide a novel version of the widespread notion of the murkiness or intransparence of money. When sociologists or economists talk about money being ‘murky,’ they usually refer to the public’s insufficient understanding of monetary mechanisms. Some assume that this murkiness impairs the legitimacy of the monetary system, since it implies an irremediable legitimacy gap or ‘perception gap’ between professional observers with degrees in economics on the one hand and the lay public on the other, so that the work of central banks – despite all efforts at transparency and explication – can never be fully appreciated by the public (Haldane, 2016). Others assume, similar but different, that the murkiness of money guarantees the legitimacy of the monetary system – ‘legitimacy,’ here, in the sense of factual acceptance and acquiescence by the population – reasoning that trust and acceptance would collapse if everyone knew just how the system worked (Braun, 2016; Kraemer et al., 2020). By contrast, my model implies that monetary systems are, to a degree, intransparent even for their professional and fully competent participants – that they can never be fully transparent for themselves, since they contain elements with different degrees of acknowledgeability. But in fact, no system can never be fully transparent for itself, even in its technical or professional core, because its operative complexity always exceeds its reflexive capacities. This seems to be true even for the economic system and the monetary system, despite half a century of ‘rational expectations.’

Conclusion

I think that the model presented here has some immediate charm and some obvious drawbacks, both of which can be condensed into the question: how is it that a model can simply declare a long-standing controversy to be irrelevant or baseless? In fact, it is not declared irrelevant, but transposed from a paradigmatic controversy into a real structural dualism, which seems to me the more instructive way of dealing with it. To be sure, the price to be paid for this shift is sterility at the action level. The model does not imply recommendations for the conduct of monetary policy, nor does it have immediate implications for the institutional design of monetary systems. Rather than policy relevance, it propagates sociological distancing and second-order observation. In concluding, I want to put my model in perspective and sharpen its contours relative to other approaches by discussing its implications for two issues: (1) the issue of shadow money and shadow banking and (2) the role of the state in the constitution of money and monetary systems.

1. The past half century has witnessed the development of a huge shadow banking sector, in which credit instruments of all sorts are traded among large, professional players (Adrian and Shin, 2009; Gorton, 2010; Pozsar, 2014; Thiemann, 2018). Of particular interest in our context are short-term credit instruments with maturities of a few days, weeks, or months, which include repos, money market funds, and asset-backed commercial paper. The markets for such instruments are known as money markets, as opposed to capital markets, where instruments with longer maturities are traded for investment or capital-raising purposes. Money markets serve the purpose of liquidity management, that is, the short-term parking or borrowing of money by participants who need to even out incoming and outgoing payment flows – and hence, the same purpose that is traditionally served by demand deposit accounts in banks. Demand deposits are money in an M2 sense, but money market instruments are not, which is why they are called shadow banking instruments or even ‘shadow money’ by some (Gabor and Vestergaard, 2016; Murau and Pforr, 2020; Pozsar, 2014).

According to the mainstream view, these instruments are not money but are part of markets – if markets are those regions of the economic system where money is used but not created. They are privately traded instruments, whether bilateral contracts or marketable securities, that enjoy full freedom of contract and operate outside the purview of monetary authorities. That they do not qualify as money is because they are not routinely used as a means of payment, and circulation as a medium of exchange is the crucial attribute of money in the orthodox approach. In my figure, this would be reflected in the fact that an orthodox scholar would enter ‘shadow banking’ or ‘money markets’ outside the circle that delineates the monetary system and somewhere in the wider economy.

On the other hand, heterodox scholars emphasize that, from a practical point of view, these instruments are money (Gorton, 2010; Gorton and Metrick, 2010; Pozsar, 2014; Pozsar et al., 2010; Ricks, 2016). They are used for the same purposes, they carry the same risks of run, dry-up, and collapse as nominal money – as is well known since the crisis of 2008 – and they are simply known as ‘cash’ among practitioners such as corporate treasurers or CFOs. Post-Keynesians call them ‘near money,’ ‘quasi money,’ or ‘money equivalents’ and argue for the use of broad monetary aggregates such as M3 or money of zero maturity (MZM), which include money market instruments in addition to M2 instruments. For post-Keynesians, money market instruments are money in all but a nominal sense, and they draw the conclusion that they should also be regulated analogously to – or even in outright fusion with – traditional monetary and banking systems, with instruments such as mandatory deposit insurance, reserve requirements, capital requirements, and so on.

In my model, post-Keynesians would enter ‘shadow banking’ or ‘shadow money’ inside the monetary system circle – in the right, informal half of the circle – or they would generally see the boundaries of the monetary system as dotted, blurred, and ever evolving. They have highlighted bottom up, emergent, demand-driven dynamics in monetary creation all along, and from this perspective, it doesn’t make too much of a difference whether customers’ demand for credit is satisfied through official M2 money or through informal alternatives. For post-Keynesians, the defining attribute of money is not its use as medium of exchange but use as a means of credit and a unit of account, and this implies that any credit instrument that is stable in value in the short run or that ‘trades at par’ on demand can be counted as money. The dominant forms of money have changed more than once historically – from coins to bank notes, from bills of exchange to entries in bank ledgers, and later from bank notes to plastic cards and entries in electronic accounts. Each new form emerged as a marginal and frowned upon alternative and then came to figure as the quintessential form of money for some time (Pozsar, 2011; Ricks, 2016). Money market instruments are but the next candidate to follow this trajectory.

For reasons of space, I leave the discussion of shadow banking at this point. The issue will be covered in a separate article by the author (Kuchler, 2022). In our context, it suffices to say that the dual circuit model is equipped to capture also this important issue and to trace the boundary contests that are waged under the shibboleth of ‘shadow banking.’

2. My model begs the question: What about the state? How does the state figure in the process of money creation? There can be no doubt that states and governments are major players in monetary affairs, in a variety of ways: they install a particular currency as legal tender and regulate payment transactions; they issue government bonds and thus furnish the prime tool in central banks’ monetary policy toolbox as well as in collateralized private lending; they pass legislation and regulation, sign international treaties and mechanisms, mandate and staff central banks, and so on. Despite these facts, my model does not mention the state. This requires some comment.

Many heterodox economists have advanced the view that money is constituted by the state – historically through the tax mechanism, the underwriting of trust among participants, the chartering of banks, and, today, through various institutional oversight and backstop mechanisms (Ingham, 2004; Knapp, 1924; Lerner, 1947; Mitchell Innes, 1913, 1914; Wray, 1990, 1998, 2012). Within sociology, chartalist thought has resonated well with the general embeddedness paradigm that has been paramount in economic sociology, as well as with widespread progressivist attitudes. In a way, chartalist assumptions have become the hallmark of critical conceptions of money, while on the contrary, the assumption that a self-sustaining and self-constituting order of money is possible is somehow seen as fused with neoclassical views and the medium-of-exchange theory of money. I depart from this majority view. Instead, I see heterodox monetary theory as composed of two strands of reasoning – the theorem of endogenous money and the theorem of money as a creature of the state – that are often twisted into each other but that can be disentangled and that may not even be smoothly compatible (Dodd, 2014; Febrero, 2009).

The model reflects the intention to build an ‘internalist’ theory of money creation, in which money is a medium that stands on its own feet and the elementary hydraulics of money creation can be mapped without reference to the state. This intention, in turn, is related to the general assumption that in modern society, any institutional field must operate as a self-constituted entity with its own specific values, standards, codes, conflicts, resources, rationalities, and so on, and any medium of communication is a self-constituted web of meanings, symbols, and interrelations. Money, at its heart, is built on a rationale of inducement or investment, rather than a rationale of threat or coercion, as is power, politics, or government. Money’s rationale is of the type ‘You do something nice to me and I will do something nice to you,’ while a power rationale is of the type ‘You do something nice to me or I will do something nasty to you’ (Boulding, 1963). Establishing or vitalizing a rationale of the inducement type is beyond what the state can do.

Concerning the historical emergence of the money medium, the constitutive role of economic forces and the secondary role of the state finds support even in some of Wray’s writing (in fact, this in an implication of the broader credit theory of money, which traces credit money back even to stateless societies; Graeber, 2011; Wray, 1990, 1993). For example, in a passage on early modern Italy, Wray writes that state-issued fiat money could deliver a boost to the money supply only on condition that it was acceptable to participants on their own terms and was equally desirable, in their eyes, as private credit money (bills of exchange), because otherwise it would have circulated at a discount in the private ‘giros’ of merchants and bankers (Wray, 1990: 42). Today, other moderate post-Keynesians warn against the overstretching of chartalist assumptions and say that the fact that the state can impose tax liabilities and can spend money first and ‘collect back’ taxes later should not be taken to mean that the state can imbue value to or determine the value of money, and that private bank money is but a derivative, leveraged form of state-issued fiat money. ‘[I]t is private money that precedes state money and not the other way around’. (Febrero, 2009: 532–533) Similarly, writing on current regulatory issues, Morgan Ricks argues that in the task of stabilizing a monetary system and finding a ‘good’, cooperative equilibrium of trust and credit extension, rather than a ‘bad’, defective equilibrium of panic and dry-up, the state can be a facilitating but not a formative factor (Ricks, 2016: 147–148). Within sociology, Hanno Pahl arrives at the same conclusion: The fact that the monopoly for issuing money is held by the central bank as a more or less political institution does not justify the frequent technicist fallacy of an exogenization of money. Quite the contrary: Money and its higher-order derivatives are endogenous elements of the economy, they come into existence by spontaneous emergence and not by plan or intention, and they are furnished with political underpinning only secondarily and at an organizational level. (Pahl, 2008: 176, my translation)

In my eyes, the theorem of endogenous money creation and the theorem of money as a creature of the state sit uneasily with each other. It is not self-evidently compatible to say, on the one hand, that money creation cannot be controlled by an exogenous entity like the central bank because of its spontaneous, endogenous, bottom up nature, and to assert, on the other hand, that the medium of money as such is constituted by an external entity like the state and cannot emerge from economic acts and economic constellations alone. At least in my sociological mind, these two assertions produce some friction – and so they do in Febrero’s (2009) economic mind. Quote Wray (1990: xiii): ‘money enters the economy through the normal economic processes of a capitalist economy.’ Why would this proposition describe the ongoing process of money creation in contemporary monetary systems but not the constitution of money as a medium of social interaction as such? It requires some theoretical leap to get from making the first assumption to denying the second, or at least it does not require a theoretical leap to accept both assumptions and argue for the endogeneity of money in both senses.

The assumption that money is endogenous in this sense is compatible with the fact that the state steps in at quite a few points in the process – as issuer of debt, backstopper, regulator, and so on. This is a matter of theory construction. Even if money and monetary systems are fundamentally self-constituting and self-sustaining social complexes, they may draw on the state and draw in the state at certain points. But then, this is an invited and not a constitutive role. The state cannot constitute the medium of money, but it can – as a unique force with unique resources and capacities – provide some solutions to the monetary system’s self-generated problems.

This may seem like a pretty scholastic dispute, but it is not. This can be seen from other, comparative cases of institutional fields that are secondarily supported or protected by the state but cannot be seen as constituted by it. For example, the introduction of schooling as a standard element in children’s lives was greatly helped by governments making schooling compulsory. The latter was a sovereign act, the passage of a law, backed by law enforcement agencies – and yet, in content and mission, it was an educational achievement. The ‘grid of intelligibility’ from which it must be understood is that of education, not that of the state qua state. The state does not constitute school when it makes schooling compulsory. Similarly, modern universities and research institutes were – and are – often set up and financed by governments, but they cannot be understood as offshoots of government power. Marriage and family are protected by legal and tax privileges, protection of privacy, and so on, but their essential operations, meanings, and dynamics are safely beyond the access of the state. Many institutions of modern society have developed in co-evolution with states and governments, but this does not make the answer ‘It’s the state!’ a good theory of modern schooling, or modern research, or modern families. And remember that political sociologists found themselves in a parallel – and inverse – situation when, after extended battles, they refuted the answer ‘It’s the economy!’ as a clue to understanding the nature of the state and emphasized the relative autonomy of the political sphere and the non-derivability of political conflicts from economic conditions instead (Evans et al., 1985; Hall, 1984; Mann, 1984; Skocpol, 1979).

I dare to suggest a loose or distortive use of economists’ terminology. In rephrasing the view just expressed, we might say that when the state intervenes in or backstops monetary systems, it answers a demand that originates in the monetary sphere. It supplies services such as: lending sovereign status, defining legal settings, performing oversight – that are prompted by monetary conditions, dynamics, and turbulences. Monetary systems generate their own endogenous ‘demand’ for stabilizing and facilitating forces, and the state steps in to ‘supply’ them. The state is uniquely capable to do so because it possesses some unique resources and capacities and because it accepts some overall responsibility for the welfare of its population. But there was a demand for it in the first place, and this is why the state is not a constitutive or formative factor, but only a facilitative or supportive factor. This may be taking things to far, but this is how my sociological mind, tuned to the analysis of self-constituting and self-sustaining social fields, reads and recycles the tenet of demand always being the driving force.

Footnotes

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by DFG-grant N° 452530257, project ‘Processes of Commensuration in Financial Markets’, Deutsche Forschungsgemeinschaft, Bonn, Germany.