Abstract

Recent political economy scholarship has interpreted the recent resurgence of capital controls across the Global South as attempts by some developing countries to preserve their policy space to pursue heterodox economic policies. This article critically engages with this literature and argues for the need to study capital controls in light of the social constitution and the class character of the capitalist state, money, and private capital flows. This argument is substantiated through a class analysis of the deployment of capital controls in Brazil from 1945 to 2014, which emphasizes the crucial role that capital controls have historically played in the reproduction of capitalist social relations and particular forms of class rule in Brazil.

JEL Classification: F30, F32, F38, F54

1. Introduction

The politics of regulating cross-border capital flows and the impact of international capital mobility on state policy-making have been widely discussed in academic, activist, and policy-making circles, particularly in the aftermath of recurring financial crises over the past twenty-five years (Deeg and O’Sullivan 2009; Mosley 2003; Nesvetailova 2006; Watson 1999). While contributions from Keynesian and Structuralist economics perspectives have focused on the rationale for and effectiveness of capital controls (CC) to prevent and mitigate financial crises (Chang and Grabel 2004; Epstein 2005; Ocampo and Stiglitz 2008), 1 political economists have analyzed the drivers and consequences of capital account liberalization in developing and emerging capitalist countries (DECC) since the early 1990s (Ghosh 2005; Marois 2012; Orhangazi 2014; Tutan and Campbell 2016; Vernengo 2006; Wade and Veneroso 1998). More recently, a burgeoning international political economy literature set out to specifically examine the “re-regulation of the capital account in those nations that liberalized in the 1990s” (Gallagher 2015a: 80; see the Mini-Symposium in RIPE 22 (1)). Indeed, the recent global financial crisis and subsequent sharp swings of unregulated capital movements sparked off an array of policy responses across the developing world, including measures that aimed at taming the destabilizing effects of these flows. Particularly, DECC such as Brazil, South Korea, Indonesia, Costa Rica, Uruguay, the Philippines, Peru, Taiwan, Colombia, and Thailand 2 deployed a variety of CC (Grabel 2015). This is quite remarkable, given that from the 1980s until recently, such measures were largely considered as heresy by the international finance establishment (financial market actors, the International Monetary Fund [IMF], credit rating agencies, etc.), and a strong policy stigma was associated with them (Abdelal 2007; Chwieroth 2009).

There has been remarkably little engagement from a historical materialist perspective with the recent deployment of CC, and more broadly with analyses of CC in general. The present article addresses this gap. It offers an analysis based on a theoretical examination as well as on a critical exploration of a case study widely used in the literature: the deployment of CC by the Brazilian state (Baumann and Gallagher 2015; de Paula 2014; Gallagher 2015a, 2015b). The example of Brazil is important, given its long history of CC, but also because it is often portrayed in the literature as a successful case of deployment of CC to reclaim policy space, as explained in the following. I draw on historical materialism in two ways. First, I highlight a series of theoretical shortcomings in the aforementioned literature and in its use of the concept of policy space as an analytical device to explain the resurgence of CC in Brazil. Those shortcomings, I argue, prevent commentators from offering a satisfactory understanding of the recent resurgence of CC in DECC, and they can be revealed by drawing on the Marxian critique of the state and money as alienated forms of social existence under capitalism (e.g., Bonefeld and Holloway 1996; Clarke 1991). Importantly, the literature on policy space conceptualizes private capital flows as a structural feature of the contemporary capitalist world economy, which constrains national state policy-making, and CC are seen as attempts from developmentally minded governing élites to better manage/control this constraint. My claim is that this conceptualization of the relation between private capital flows and the capitalist state is highly problematic, and obfuscates the class-based relations of domination and exploitation that underpin them, with important implications for how we understand CC. Second, and from a more empirical point of view, I offer a class analysis of the deployment of CC in Brazil from 1945 to 2014.

The rest of the article is organized as follows: Section 1 critically reviews the key arguments recently put forward in the literature to explain the resurgence of CC across the developing world. Section 2 then goes on by outlining a historical materialist framework that allows studying CC in light of the social constitution and the class character of the state, money, and private capital flows. My key argument is that CC must be examined with respect to a fundamental contradiction: from the perspective of the capitalist state, money-capital constitutes a source of social wealth that can be distributed to various social subjects through diverse state policies for the purpose of fostering accumulation and managing class relations, but the movement of money-capital also shapes the modalities through which the state politically contains and integrates labor within its national space of valorization. I suggest viewing CC as a political form of mediation of this contradiction. Section 3 puts this theoretical perspective to work and provides a class analysis of the deployment of CC in Brazil from 1945 to 2014. By focusing on class dynamics and by locating recent CC in a longer historical trajectory, the case study produces a significantly different interpretation of those policies than that of the policy space literature: it emphasizes the crucial role that CC have historically played in the reproduction of capitalist social relations and particular forms of class rule in Brazil. This argument seriously challenges the narrative, widespread in heterodox economics and critical international political economy, which tends to portray CC as inherently progressive policies. This has important theoretical implications for how we understand CC, but also, from a more political standpoint, for how to push for development friendly forms of financial governance.

2. Global Financial Crisis and Recent CCs: Regaining Policy Space?

The recent literature has largely relied on the notion of policy space as an analytical tool to explain the resurgence of CC (Gallagher 2015a, 2015b; Gallagher, Griffith-Jones, and Ocampo 2012; Grabel 2015). The concept of policy space refers to the scope for domestic policies that is available for each country at a particular point in time to implement its national development strategy and manage its integration into the global economy (Chang 2006; UNCTAD 2002; Wade 2003). Based on this concept, and drawing from Keynesian, Structuralist, and Developmentalist-Statist political economy, scholars have formulated the argument that CC can play a key role in enhancing policy space (e.g., Chang and Grabel 2004; Epstein 2005; Ocampo and Stiglitz 2008). Indeed, the argument goes, by curtailing volatile cross-border movements of capital, CC can:

Maintain financial stability and reduce the vulnerability of domestic financial systems;

Facilitate counter-cyclical macroeconomic management;

Ease the constraint on monetary policy that is imposed by cross-border capital flows;

Assist in harnessing capital flows and channeling them toward the real economy;

Help controlling the modality of a country’s integration into global financial markets.

However, as the norm of free capital mobility became hegemonic in the 1990s, a policy stigma became associated with the deployment of CC (Abdelal 2007; Chwieroth 2009; Moschella 2010), that is, the policy space to deploy CC was constrained, despite their developmental potential.

In light of this analytical framework, the following argument has been put forward to explain the recent resurgence of CC: the 2008 global financial crisis has “catalyzed” a variety of economic, political, and ideational changes in the global political economy, 3 which have led to “an important turn in the direction of post–World War II (WWII) support for [CC] by the economics profession, government officials and the IMF” (Grabel 2015: 11). This has resulted in a propitious setting for experimentation with CC, or what Grabel has termed an era of “productive incoherence” (Grabel 2011: 805). If the changes in practice and thinking around CC have been “messy, uneven, and uncertain” (Grabel and Gallagher 2015: 3), they have nevertheless widened the policy space to deploy them in the post-crisis environment.

In that context, state managers in a variety of DECC were able to deploy an array of CC, which in turn (and according to the logic outlined earlier) allowed enhancing policy space to prevent and mitigate financial crises. Indeed, after a brief episode of capital flight when the global financial crisis burst in 2008, private capital flows to DECC rapidly recovered between 2009 and mid-2013. Large and volatile inflows were driven by the better economic dynamism in DECC than in advanced capitalist countries (the so-called two-speed recovery). Besides, large interest rates, differentials between DECC and advanced capitalist countries provided a lucrative opportunity for carry trade. Faced with the usual effects triggered by massive capital inflows, 4 the argument goes, developmentally minded state managers deployed CC, thereby regaining policy space that allowed room for counter-cyclical macroeconomic policies.

Gallagher (2015a, 2015b) goes a step further in the argument with his theory of countervailing monetary power. According to him, some DECC benefited from sufficient policy space “to countervail political pressure and sophisticated global capital markets to manage financial stability between 2009 and 2012,” and the deployment of CC was part of this endeavor (Gallagher 2015a: 17). Gallagher uses the recent Brazilian experience to support his claim. Brazilian state managers deployed CC on inflows and foreign exchange derivatives regulations in 2009–2012. The reasons they were able to do so, he argues (Gallagher 2015a: 79–89), include:

Their training in Minskyan-Developmentalist and Structuralist-Keynesian economics traditions made them inclined to use CC;

They secured the political backing of special interest groups (such as exporters of tradable goods) that were penalized by currency appreciation;

They re-framed CC as “macroprudential measures” to gain support for their policy objectives from both domestic and international forces;

Brazil had made little commitment to financial services liberalization in the framework of global economic governance arrangements (bilateral trade agreements, General Agreement on Trade in Services, etc.). Indeed these often prevent the use of CC.

This line of argument on the resurgence of CC (across the developing world and in the specific case of Brazil) is interesting in many ways, not least because it takes into account a variety of factors such as changes in policy ideas and practices, transformations in international organizations, the intellectual background of state managers, global governance arrangements, power dynamics in the global economy, and domestic factors. However, as I elaborate in the following, my claim is that it suffers from a series of theoretical shortcomings that ultimately prevent commentators from offering a satisfactory understanding of the recent resurgence of CC in DECC.

There has been remarkably little engagement from a historical materialist perspective with the recent deployment of CC, and more broadly with analyses of CC in general. Notable exceptions include the work of Soederberg (2002, 2004) and more recently Dierckx (2013, 2015). In an important article, Soederberg (2002: 491) identifies three analytical weaknesses in the Keynesian-inspired analyses of CC in DECC: (1) the tendency to “treat CC as ready-made, technical policy instruments devoid of political and historical dimensions”; (2) the lack of attention to specific power relations; and, (3) to the role of CC in broader class-based strategies and in sustaining particular forms of capital accumulation. Regarding (1) and (2), it is worth noting, the recent policy space literature fares relatively better than the accounts Soederberg was criticizing in 2002. For instance, in his comparison of post-crisis capital account policies in Brazil, South Korea, South Africa, and Chile, Gallagher (2015b) interestingly examines the conflicting relations between different social groups with competing material interests (exporters of tradable goods, workers and consumers, domestic and international finance, etc.). However, this “political” analysis is relatively disconnected from the changing material conditions of accumulation and social relations of production prevailing in each country, the unfolding of social class struggles, and how those processes are mediated by a variety of state policies. In other words, Gallagher’s account (and I would argue that this is generalizable to the literature on policy space as a whole) performs quite poorly with respect to weakness (3) that is, it pays little attention to the role of CC in broader class-based strategies. Consequently, a number of class-based dynamics and processes remain invisible in those accounts, and in particular the role of CC in the reproduction of particular forms of capital accumulation and capitalist class rule. In my view, and as the case study of Brazil illustrates, those are fundamental in making sense of the deployment of CC in Brazil and beyond.

Another limitation of the literature hereinabove mentioned resides in its view of private capital flows as a constraint on policy space: private capital flows are conceptualized as a structural feature of the contemporary capitalist world economy, which constrains national state policy-making, and CC are seen as attempts from developmentally minded governing élites to better manage/control this constraint. The problem with this view is that it reifies states and markets as two intrinsically opposed social spheres of existence. This is not the place to provide an extensive critique of such conceptualization, 5 suffice it to say here that the danger of this conceptualization is that there is a risk of introducing a bias in the explanation of the resurgence of CC: if capital flows are seen as an exogenous force that externally constrains the policy space of states, then state policies that aim at regulating capital flows (such as CC) tend to be automatically interpreted as endeavors to enhance/maximize policy space. Now, this is not to deny that volatile capital flows have an important effect on state policies. My point is rather that there is a need for a more problematized view of the relation between the state and private capital flows. More precisely, as I argue below, highlighting the class character and the social constitution of both the state and private capital flows allows developing a more nuanced view of the dialectical relation between the two, with important implications for how we interpret CC.

Finally, a significant limitation of the policy space literature is that relatively little is said on the logic and drivers of private capital flows, what they express, and most importantly, their form: money. This is problematic in as much as most of the private capital flows discussed in the policy space (equity and debt flows, bank loans, etc.) are capital in the form of money, which makes it crucial to clearly establish the role and nature of money in capitalist social relations. Yet, remarkably little is said on money, except that money-capital flows can have a destabilizing impact, and that monetarist policies can favor certain social groups at the expense of others. As the article emphasizes in the following, money is a peculiar social form in capitalism, an understanding of which is necessary to establish a solid conceptualization of the state, private capital flows, their relation, and ultimately making sense of CC. The following section is dedicated to this task.

3. A Theoretical Framework Grounded in Marxian Theories of Money and the State

The theoretical framework for the study of CC suggested here emphasizes that the state and money need to be conceptualized within the totality of capitalist social relations from which they are constituted. From that perspective, the state is a historically specific political form assumed by antagonistic class relations (Clarke 1991, 1992). Capitalist class relations, it is worth insisting, are inherently global, and the production of surplus value is a global process (Marx [1894] 1991, [1857] 1993). This global character sharply contrasts with the fragmentation of the world into nationally constituted political entities, national states, within which capitalist exploitation is processed (Burnham 2006; Clarke 1991). The class character of the state is evident in its role, even though it is obfuscated by its fetishized appearance as an independent political form that guarantees public interest, formally separated from the process of surplus value production and from civil society: it strives to regulate capitalist social relations and secure the conditions for capitalist accumulation within its territory, by politically mediating the contradictions in global accumulation (Clarke 1991). This is restricted by, and subordinated to, the conditions imposed by uneven capitalist reproduction and class struggle on a global scale (Burnham 2006; Holloway 1994). Accordingly, state policies are understood as nationally differentiated political forms taken by the global unity of capitalist reproduction. It follows that the deployment of CC is a (national) political form that mediates the global movement of money-capital. Importantly, this points to the relation between the state, money, and money-capital.

One of the fundamental tasks at the heart of states’ attempts at securing the conditions for capital accumulation is preserving the quality of its national money. This is because the availability of money in adequate quantity and quality is a socially necessary condition for capitalist reproduction, and the imposition of monetary relations—money-wages and money-prices—is fundamental to capitalist class relations (Harvey [1982] 2006). Reproducing money, however, is not a neutral, technical choice; it is a form of class struggle (Bonefeld and Holloway 1996). Indeed, money in capitalism is a social relation of power, the power of capital in its “most abstract and impersonal form,” “the command of people’s lives as labor” (Clarke 1978; Cleaver 1996: 142). Therefore, the state is conceived of “as containing the working-class through imposing the elementary form of capital, money” (Bonefeld 1993: 65). From that perspective, the movement of money-capital across the world market (private capital flows such as portfolio investment, bank loans, etc.) does not simply express the investment decisions of financial investors. It is one of the contemporary forms of expression of the social power of money: under the form of abstract wealth, money-capital obtains “as essentially the common capital of a class”; it expresses the disciplinary power of “capital-in-general” (Marx [1894] 1991; Clarke 1978). The flow of money-capital transmits the global conditions of capital accumulation and the competitive discipline of capitalist relations to the various national spaces of accumulation through exchange rate dynamics (de Brunhoff 1981). It transforms the deterioration in present conditions (and future prospects) of labor exploitation, into monetary and financial crises: a capital account reversal triggers exchange rate pressures, a drain on foreign exchange reserves, and, potentially, a convertibility crisis (Bonnet 2002). To sustain the integration of their economy into the global circuits of capital, and sustain their creditworthiness (necessary to roll-over their debts, state fictitious capital, 6 and reproduce themselves), states need to maintain the convertibility of their currencies (de Brunhoff 1981). They are, therefore, forced to restore the confidence in their currency and their creditworthiness by re-imposing the “capitalist rules of the game” through labor disciplining and deflationary adjustment (Cleaver 1989).

This is the source of the contradictory relationship between the disciplinary power of capital, the reproduction of the money-form, and the reproduction of the state-form: the state is central to reproducing and enforcing the rule of money but is also disciplined by it. Clarke summarizes this as follows: “the relation between money-capital and the state is realized through the state’s responsibility for the regulation of the monetary system” (Clarke 1978: 65). In other words, instead of conceptualizing the money-power of capital as constraining the policy space of national states, it is conceived here as shaping the modalities through which states foster capital accumulation and manage class relations within their national space of valorization. Indeed, from the perspective of the capitalist state, there is a contradiction immanent in the form of money-capital: money-capital constitutes a source of social wealth that can be distributed to various social subjects through diverse state policies for the purpose of fostering accumulation and managing class relations, but the movement of money-capital also shapes the modalities through which the state politically contains and integrates labor within its national space of valorization. 7 Accordingly, CC must be conceptualized as the concrete historical political forms through which the capitalist state mediates the contradiction between money-capital as a source of social wealth and money-capital as the expression of the disciplinary power of capital-in-general.

This provides the basis for a more problematized understanding of the particular constraints that limit the scope of state action: from the perspective adopted, state action is not externally limited by market forces (as stated by the policy space literature) but by the imperative that capital accumulation imposes on its form. Consequently, CC are not interpreted through the lens of the state-versus-market dichotomy. Rather, they are examined within the broader context of the capitalist state’s contradictory attempt at (1) fostering accumulation (by channeling social wealth to support accumulation and containing the class struggle) and (2) reproducing itself as well as the money-form. The following section puts this theoretical perspective to work and provides a historical analysis of CC in Brazil from 1945 to 2014 in light of the crisis-ridden conciliation of these two imperatives.

4. A Class Analysis of CCs in Brazil between 1945 and 2014

The policy space literature uses a narrow definition of CC, as the set of state regulations that govern the capital account (by opposition with other regulations that concern the current account, such as exchange controls). The definition adopted here is broader: following Nembhard (1996: 9–10), CCs are defined as “the set of official, legal, and quasi-legal regulations in an economy that govern the movement of capital (money, credit, and other financial assets; direct investment; and capital goods) across national borders.” They, therefore, include regulations on both the capital and current accounts in the balance-of-payments. They can be grouped into four categories: foreign exchange regulations (and exchange rate regime), quantitative and tax policies, investment and credit regulations, and commercial restrictions. This choice of definition is not arbitrary. The larger definition allows examining CC (narrowly defined, restrictions on the capital account) as part of a larger arsenal of measures (concerning both the capital and current accounts, as well as macroprudential and other forms of domestic financial regulations) that participate in the national mediation of the global flow of money-capital. It is shown that this approach gives a richer picture than the one used in the policy space literature.

The case study draws on the following sources: for data on the CC deployed in Brazil, I use the extensive lists provided in the works of Teixeira (2003), Goldfajn and Minella (2007), Nembhard (1996), de Paula (2011, 2014), and the IMF’s Exchange Arrangements and Exchange Restrictions database (1999–2014).

4.1. CC and ISI development (1945–1980s)

The postwar period saw the consolidation in Brazil of a growth strategy based on capital accumulation through Import-Substituting Industrialization (ISI). In that context, a comprehensive framework of CC was deployed, including CC on banking deposits and payments in foreign currency, the forced conversion of export earnings in domestic currency, and central bank’s monopoly on foreign exchange operations (Nembhard 1996; Teixeira 2003). This was facilitated by the Bretton Woods system, under which CC played an important role in allowing states to nationally process class relations in relative isolation from the speculative movement of money-capital. In Brazil, this consisted in deepening a populist-corporatist class compromise, “in the form of wage hikes, nationalist economic initiatives, and patronage for the faithful,” at least partly in response to massive industrial strikes (Skidmore 1999: 136).

CC were not only instrumental in containing labor, but they were also adjusted and modified in accordance with the expansion (or contraction) of the revenues from primary commodity exports. For instance, in the 1950s, the democratic regimes led by Vargas then Kubitschek reinforced CC (foreign exchange regulations, and an import licensing system) to take advantage of the boom in primary commodity markets associated with the Korean War (Grinberg 2011: 45). 8 CC were also adjusted in accordance with cross-border patterns of money-capital flows. For example, in the late 1950s, a legislative framework was designed to govern booming global money-capital inflows (mainly under the form of bank loans) (Goldfajn and Minella 2007: 371, Teixeira 2003: 12). Simultaneously, CC on outflows (profits, interests, and royalties repatriation) were reinforced to prevent capital flight and to facilitate the reproduction of money in a context of weak currency and inflation.

Between 1963 and 1967, a fall in global commodity prices and a slowdown in money-capital inflows resulted in balance-of-payments pressures, creeping inflation, and the acceleration of the collapse of the class compromise based on corporatist arrangements (Chodor 2015; Hudson 1997). The associated political crisis led to a military coup d’état that toppled the Goulart administration in 1964. The newly established military dictatorship lifted CC on the capital account (CC on capital and profit remittances), which was clearly motivated by the will to restore access to the flow of foreign money-capital (Teixeira 2003: 14). 9

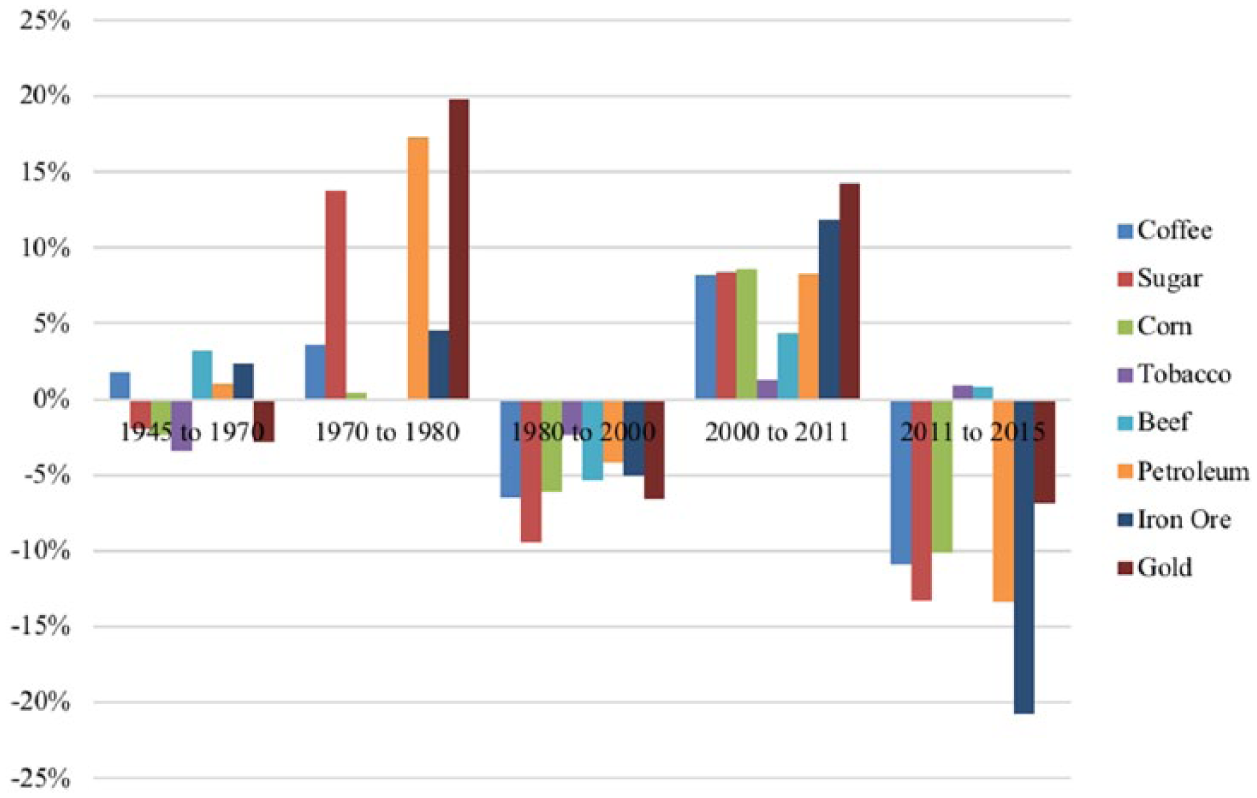

Both revenues from commodity exports and money-capital inflows recovered in the early 1970s, respectively driven by the 1972–1975 commodity boom (see Figure 1) and Euromarkets expansion.

Average Annual Change in Prices of a Series of Key Agrarian and Mining Commodities, 1945–2015

The demand for foreign money-capital was initially driven by the need to finance the expensive military and police repression of working classes, in a context of intensifying social struggles (Cleaver 1989). Subsequently, in the face of growing political opposition to the dictatorship by the organized labor movement and emerging social movements, the Geisel and Figueiredo governments financed short-term concessions (such as wage-indexation and increases in public spending) to working classes, by relying on foreign money-capital (Herold 1996). All in all, the recovery of revenues from commodity exports entailed the redeployment of trade-related and foreign exchange CC. The increasing reliance on foreign money-capital also involved the strengthening and deployment of new CC on the capital account, and particularly, strict restrictions on foreign borrowing (such as minimum maturity requirements, quantitative limits on net foreign borrowing positions) and on capital outflows to facilitate the reproduction of money (Nembhard 1996: 146; Teixeira 2003: 18–19).

4.2. CC during the crisis period (early 1980s to early 1990s)

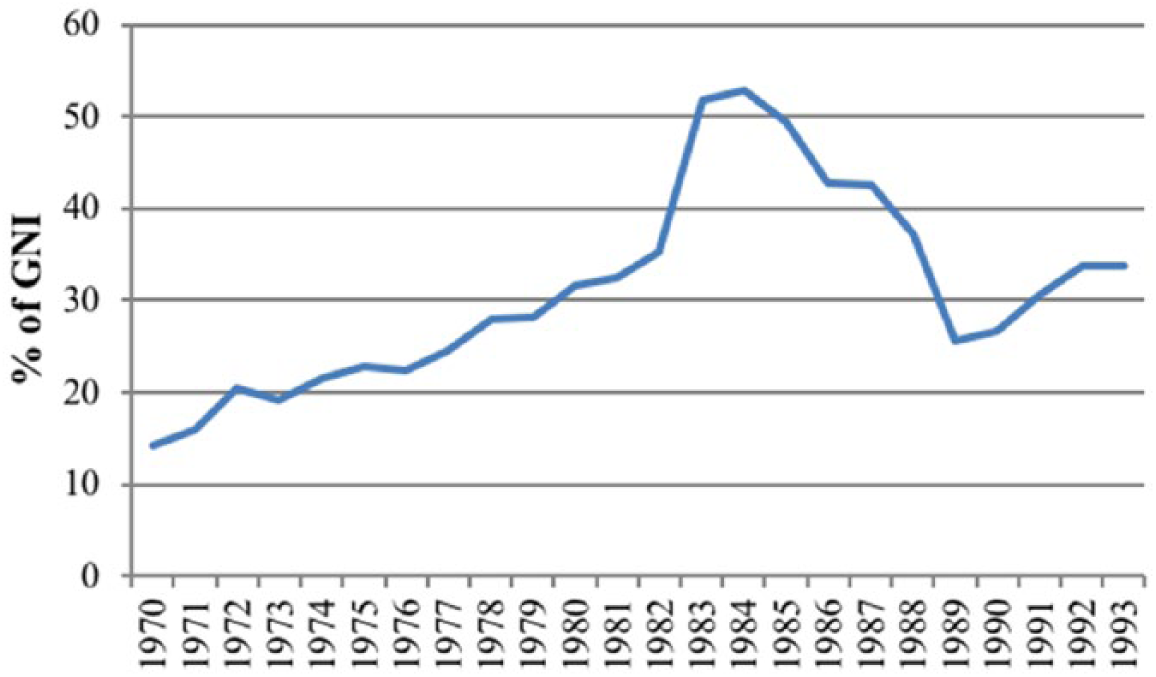

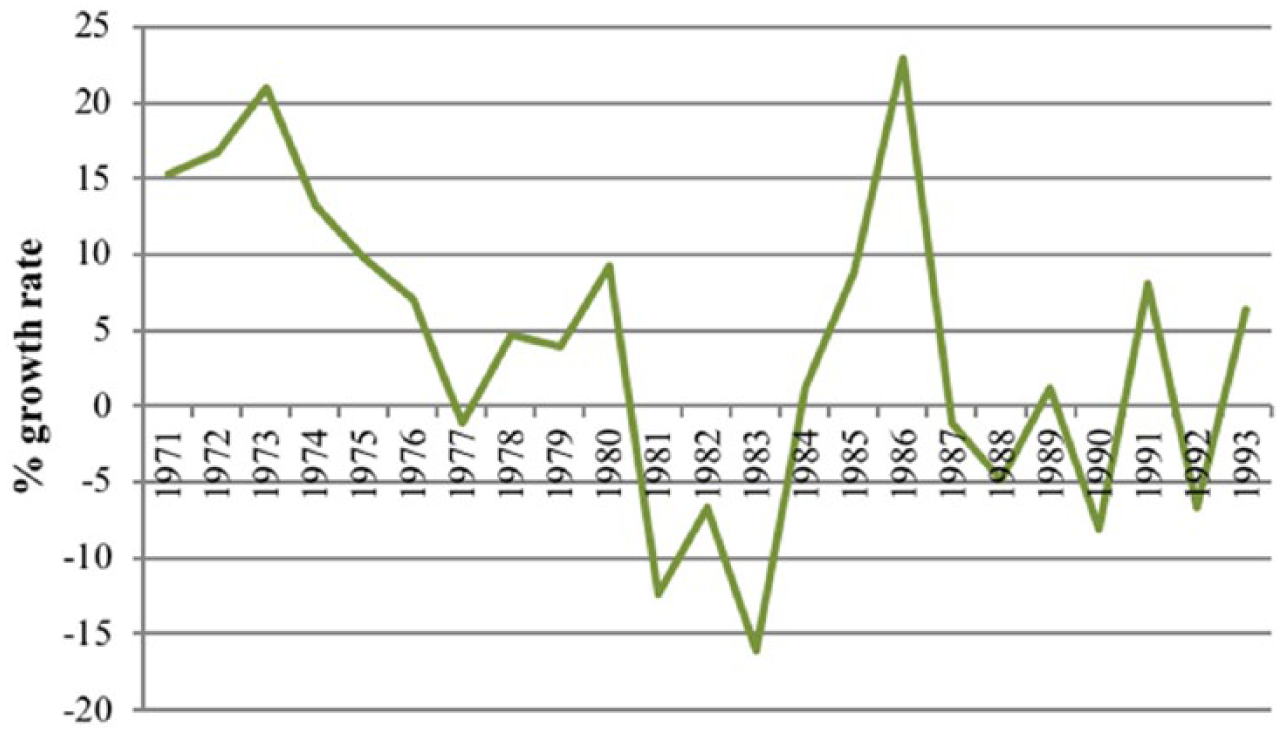

In the 1980s, Brazil entered a decade-long capitalist crisis, worsened by declining nonoil primary commodity prices on global markets (as shown on Figure 1 earlier). Moreover, the increasing reliance on external money-capital in the 1970s did not enhance capital accumulation. Credit was used to maintain consumption and income levels and finance concessions to dissenting working classes. In that context, despite the build-up of foreign debt (see Figure 2), jumping from 14.3 percent in 1970 to 51.7 percent in 1983, annual rates of growth of productive capital accumulation collapsed between 1973 and 1983 (Figure 3).

External Debt Stocks (Percentage of Gross National Income) 1970–1993

Annual Growth of Productive Capital Accumulation (Percentage Growth Rate of Fixed Capital Formation)

Persistently high rates of inflation were also evidence that the state had lost the ability to “regulate the balance of class power in money terms” in ways compatible with accumulation, leading to an escalation of the social conflict around the use of money (Cleaver 1996: 152).

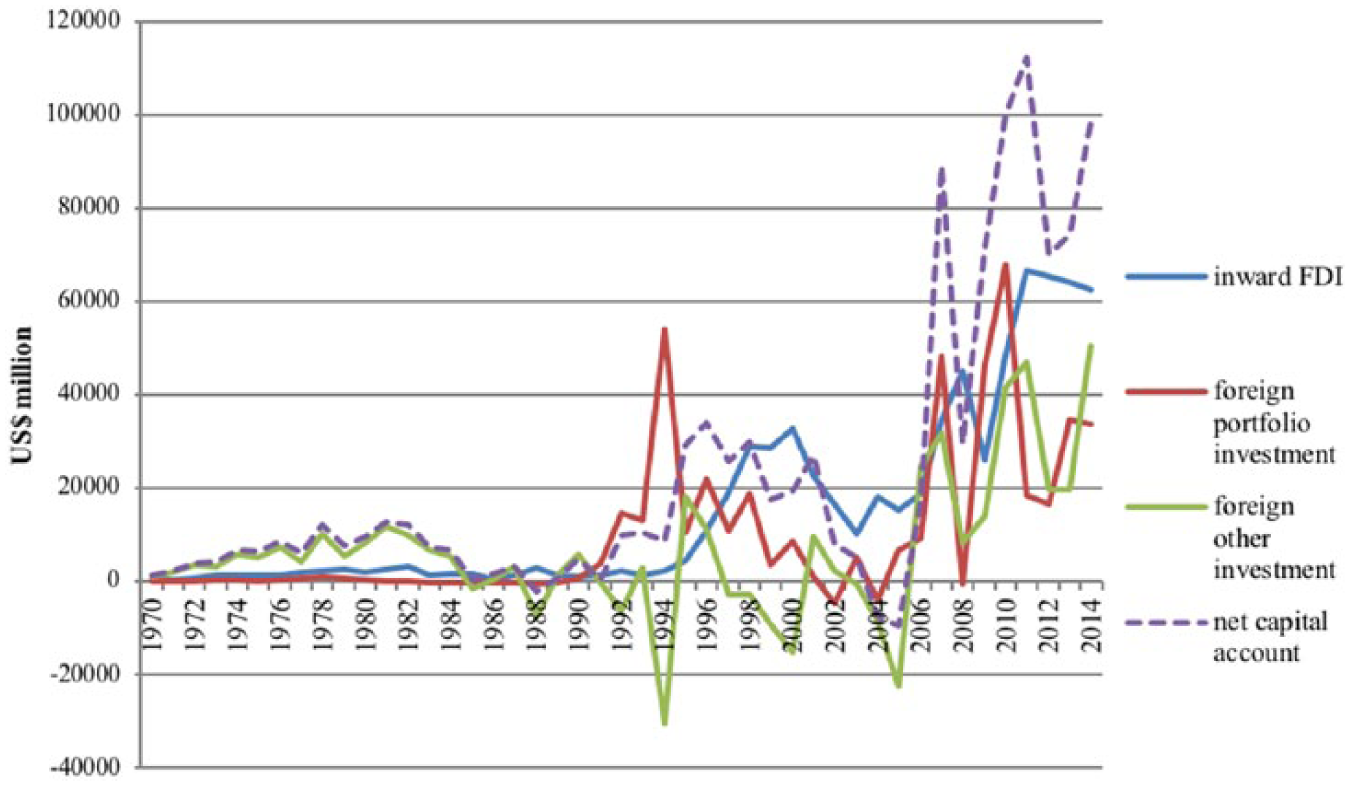

In 1982, the international financial community stopped lending to Brazil and demanded that the dictatorship imposed structural reforms. This was nothing else than the historically specific mode through which the capital relation reasserted itself on the Brazilian state to restore class power. It was expressed through an economic form (refusal to roll over Brazilian sovereign debt, and capital flight) and a political form (pressures from the consortia of international commercial banks, the IMF, the World Bank, and the US Treasury Department). In that crisis context, the Brazilian state initiated a series of neoliberal reforms, particularly after the return to civilian rule in 1985. The process of trade liberalization initiated under the Sarney administration involved the scaling-down of the mechanisms transferring surplus from the primary sector to industrial capital, including trade-related and foreign exchange CC (Teixeira 2003: 24; Nembhard 1996). Measures were taken to restore access to foreign money-capital. This initiated, in 1987, a deep process of capital account liberalization that would continue until the mid-2000s. Between May 1991 and 1992, under the Collor de Mello administration, changes in CC on the capital account and on foreign exchange markets further allowed foreign investors to invest in domestic debt, equity, and futures markets (de Paula 2011; Goldfajn and Minella 2007). Real interest rates were maintained at high levels to stimulate the demand for public bonds, fight inflation, and attract foreign loanable money-capital (de Paula 2011: 32–34). These policy changes allowed Brazil to take advantage of abundant liquidity in international financial markets, in a context of expansionary monetary policies in advanced capitalist countries 10 (see Figure 4).

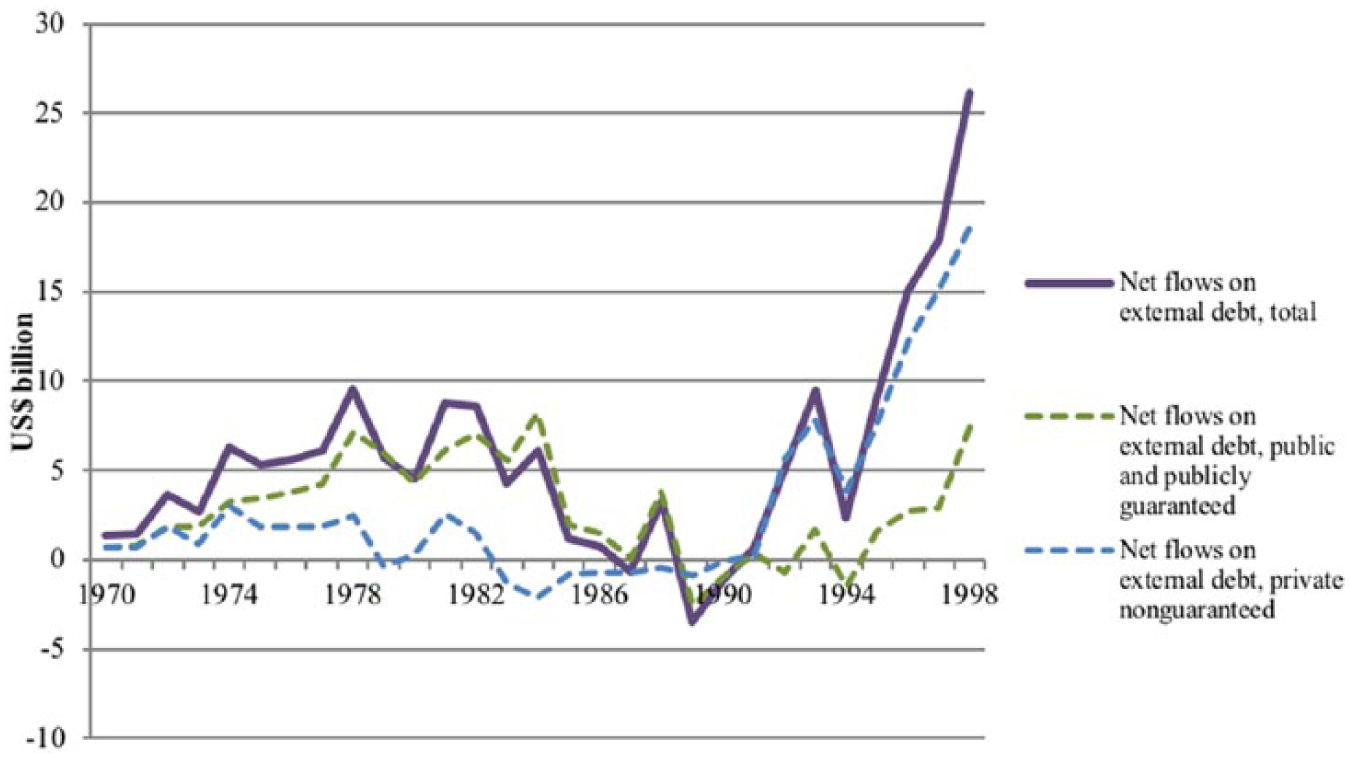

Net Capital Account and Composition of Foreign Inflows 1970–2014 (US$ Million)

The period also marked an important change regarding the inflow of money-capital. The nature and composition of the flows changed: they became driven by portfolio investment and foreign direct investment (FDI) rather than debt flows (as illustrated in Figure 4), and debt flows changed from a dominance of sovereign debt to private debt (see Figure 5).

Composition of Debt Flows in Current Billion US$ (1970–2000)

This had considerable implications in terms of the modalities through which the money relation impinged on the state. This became expressed by the movement of highly volatile private money-capital (as shown in Figure 4), which increasingly determined the exchange rate. In Brazil, this new relation first took the form of the Plano Real (1994–1999) deployed under the neoliberal administrations of Itamar Franco and Fernando Henrique Cardoso: a price stabilization plan based on the introduction of a new currency, tight monetary policy, the widespread de-indexation of the economy (to repress distributive conflicts over money), the reduction of public deficits, and the liberalization of the balance-of-payments (Saad-Filho and Mollo 2002), as discussed in the following paragraph.

4.3. CC during the neoliberal period (mid 1990s–1998)

As revenues from commodity exports also recovered in the mid-1990s, the Brazilian state re-introduced some trade-related and foreign exchange CC and subsidies to transfer a portion of those revenues to industrial capitals. While measures such as the de-indexation of wages in the context of the Real Plan, privatization, and reduction in public employment contributed to the fragmentation and disciplining of the labor force, a degree of social consent was initially achieved thanks to the success of the Real Plan in drastically reducing inflation, in particular from the middle classes (Saad-Filho and Mollo 2002; Skidmore 1999). This provided room for maneuver for the Cardoso administration to deploy a series of policies designed to sustain foreign money-capital inflows. 11 It proceeded with capital account liberalization (mainly by removing CC on outflows such as those on capital remittances abroad), and allowed the entry of foreign banks in the domestic market (Goldfajn and Minella 2007: 374). Other important policies to sustain foreign money-capital inflows included the setting of high real interest rates, tight monetary policy, and the implementation of monetary sterilization measures (de Paula 2011: 36; Saad-Filho and Mollo 2002). At the same time as these policies were implemented to sustain the inflow of loanable money-capital, a series of CC on the most volatile inflows were deployed. The Cardoso administration implemented a financial transaction tax on portfolio inflows (Imposto sobre operações financeiras, IOF) and increased the minimum maturity requirement for inflows (de Paula 2011). These were strengthened or loosened according to the evolution of inflows. For instance, CC were temporarily loosened up in 1995 during the Tequila crisis, to maintain inflows. These CC aimed at facilitating the reproduction of the national money without reversing the capital account liberalization trend.

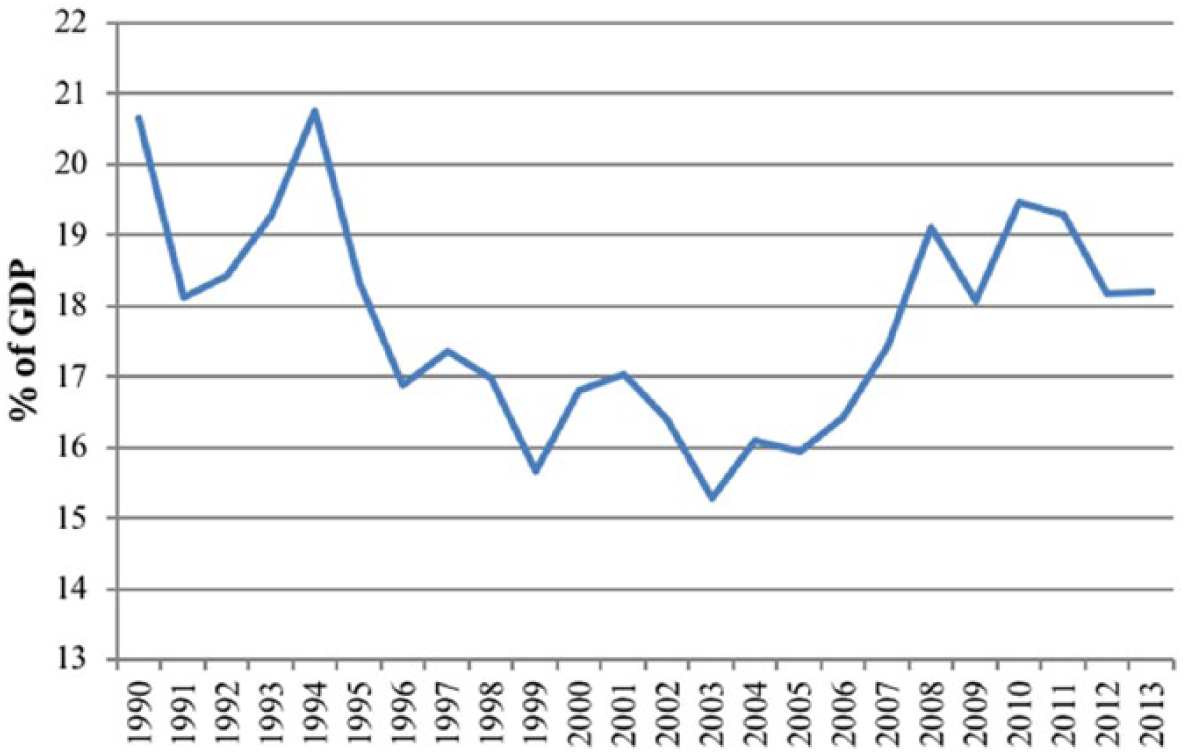

Nonetheless, abundant money-capital inflows during the period did not contribute much to capital accumulation: Figure 6 shows that accumulation rates were very modest (far below 20 percent of GDP) and followed a clear downward trend, at the same time as money-capital inflows were booming (1993–1998).

Accumulation of Productive Capital (Gross Fixed Capital Formation as Percentage of GDP)

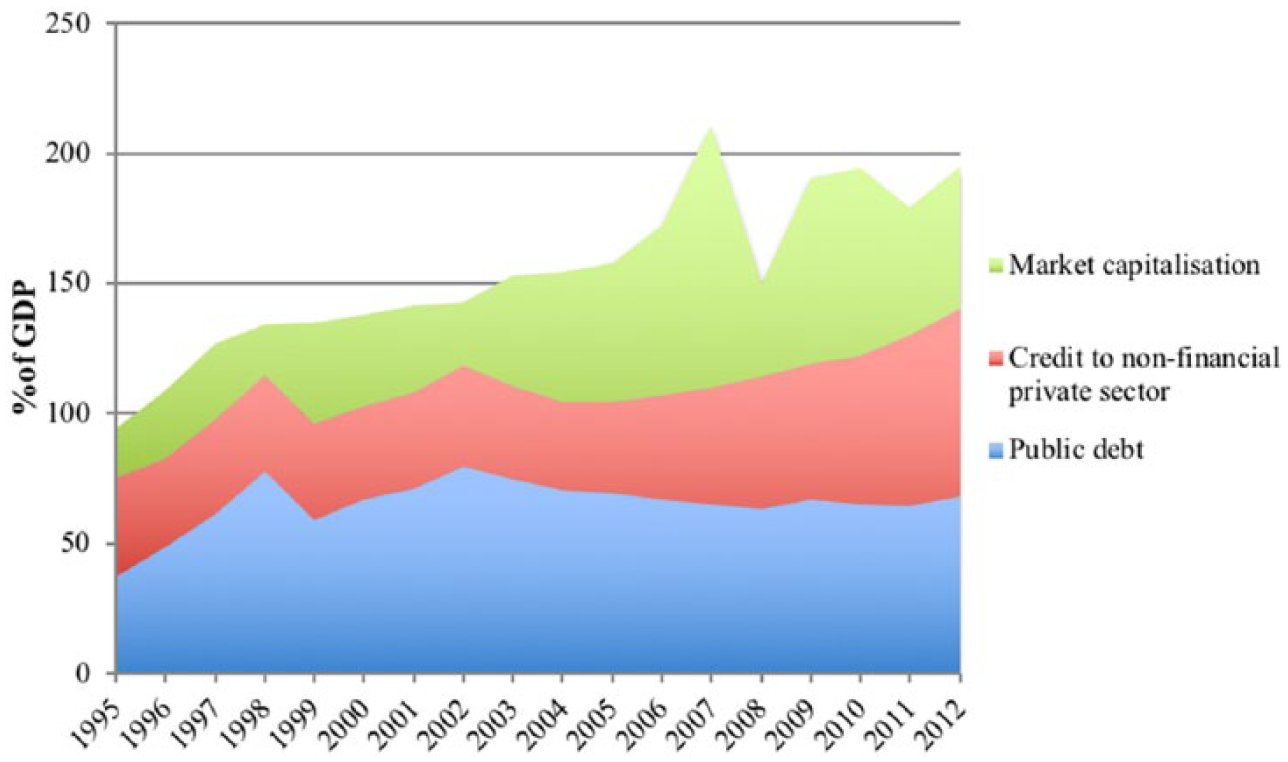

This clearly contrasts with the significant fictitious capital accumulation that happened during the same period, as Figure 7 shows. 12 It is, therefore, reasonable to assume that growing quantities of money-capital contributed to the build-up of fictitious capital, instead of being converted into expanded command over labor, which made the reversal of flows even more brutal.

Accumulation of the Three Elementary Forms of Fictitious Capital (Percentage of GDP)

4.4. CC during the 1999–2003 period

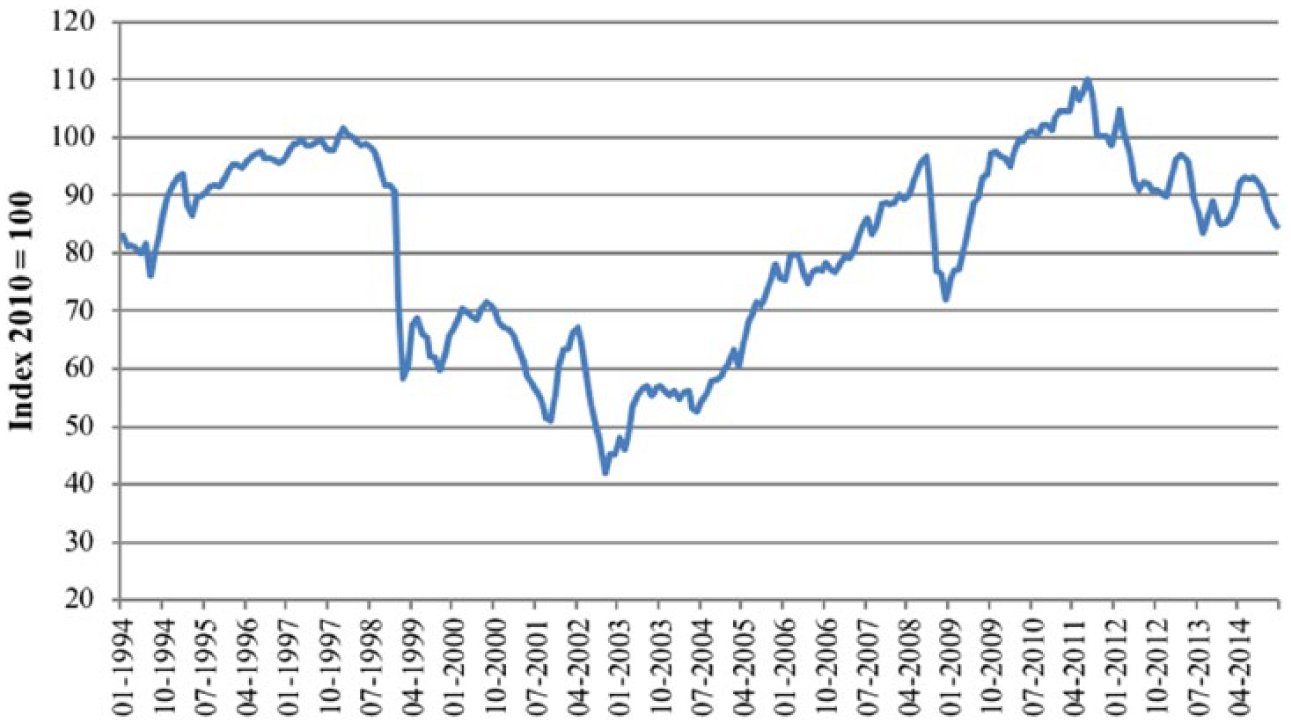

Between 1999 and 2003, Brazil entered another crisis period. Global liquidity conditions contracted, due to a series of financial crises that rocked the developing world (Asia, Russia, Turkey, Argentina) between 1997 and 2001 and the bursting of the dotcom bubble. Money-capital inflows to Brazil turned into massive outflows, amounting to about 6 percent of surpluses produced in the economy (Grinberg 2011: 100). A global economic slowdown also constrained the global demand for primary commodities, resulting in a drastic reduction in revenues from commodity exports. In late 1998, speculation against the currency and capital flight (due to deteriorating economic conditions and growing contestation from social movements and working classes) led to the collapse of the exchange rate peg in 1999 and a brutal currency devaluation, despite a large IMF loan (Saad-Filho and Mollo 2002: 129). From 2000, a resurgence of popular struggles against neoliberal policies and social inequalities further deepened the crisis: protests from indigenous movements, massive land occupations by the Movimento dos Trabalhadores Sem Terra (MST) (violently repressed), demonstrations by teachers, health workers, bank workers, and transit workers (Chodor 2015; Lewis 2001). The impact of this sequence on the exchange rate can be seen in Figure 8.

Real Real Effective Exchange Rate 1994–2014 (Monthly Averages, 2010 = 100)

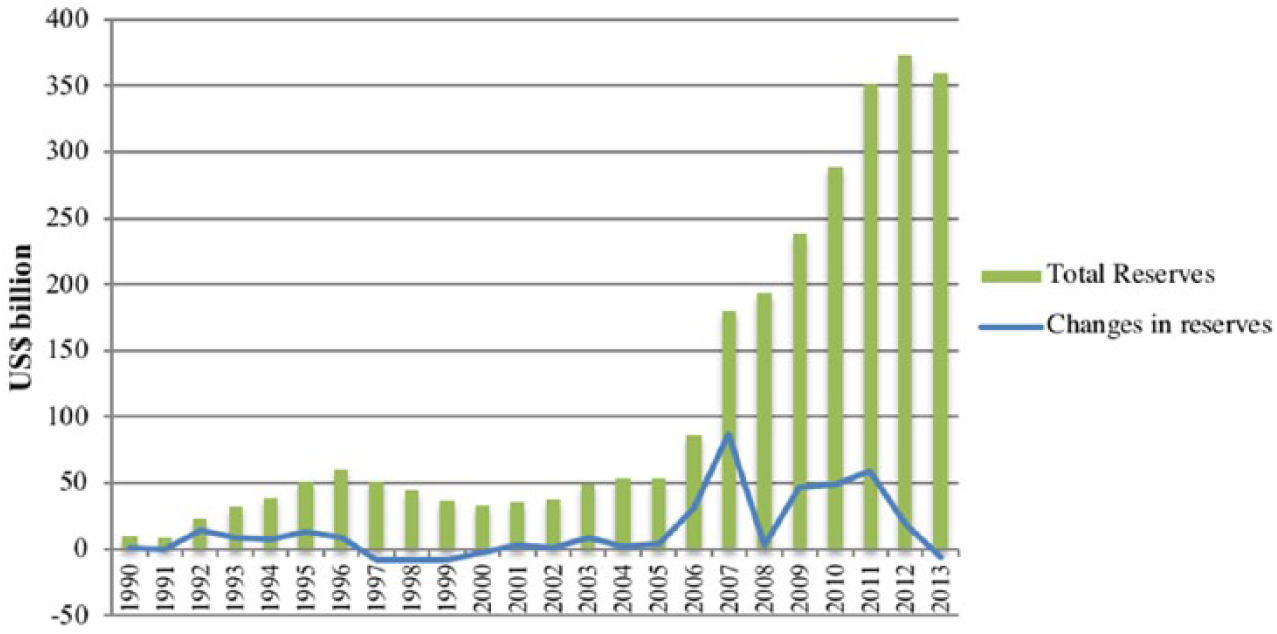

This led to a change in the regulation of money, featuring a shift to a floating exchange rate, and an inflation-targeting regime. In 2002, the prospect that a radical leftist government (the Partido dos Trabalhadores PT led by Lula)—supported by trade unions and social movements—would be elected triggered another major confidence crisis, characterized by a brutal exchange rate depreciation. The money-power of capital, expressed economically through massive capital flight, politically by the IMF, and ideologically by the Brazilian mainstream media, forced Lula to issue a Letter to the Brazilian People, “declaring that his government would respect contracts (i.e., service the domestic and foreign debts on schedule) and enforce the policies agreed with the IMF” (Morais and Saad-Filho 2011: 20). Lula also implemented a series of policies to restore the inflow of foreign money-capital. First, the CC on inflows largely used during 1993–1998 were lifted, as well as several foreign exchange CC. 13 Capital account liberalization was deepened with the removal of CC on outflows (de Paula 2011; Goldfajn and Minella 2007: 376). Other important policies to restore money-capital inflows included high real interest rates, increasingly high primary budget surpluses (reaching 4.4 percent in 2003), the beginning of a policy of overaccumulation of foreign exchange reserves (that would culminate after 2004, as shown in Figure 9), and expansion of state fictitious capital (for monetary sterilization purposes).

Foreign Exchange Reserve Accumulation (in US$ Billion)

4.5. CC during the 2003–2014 period

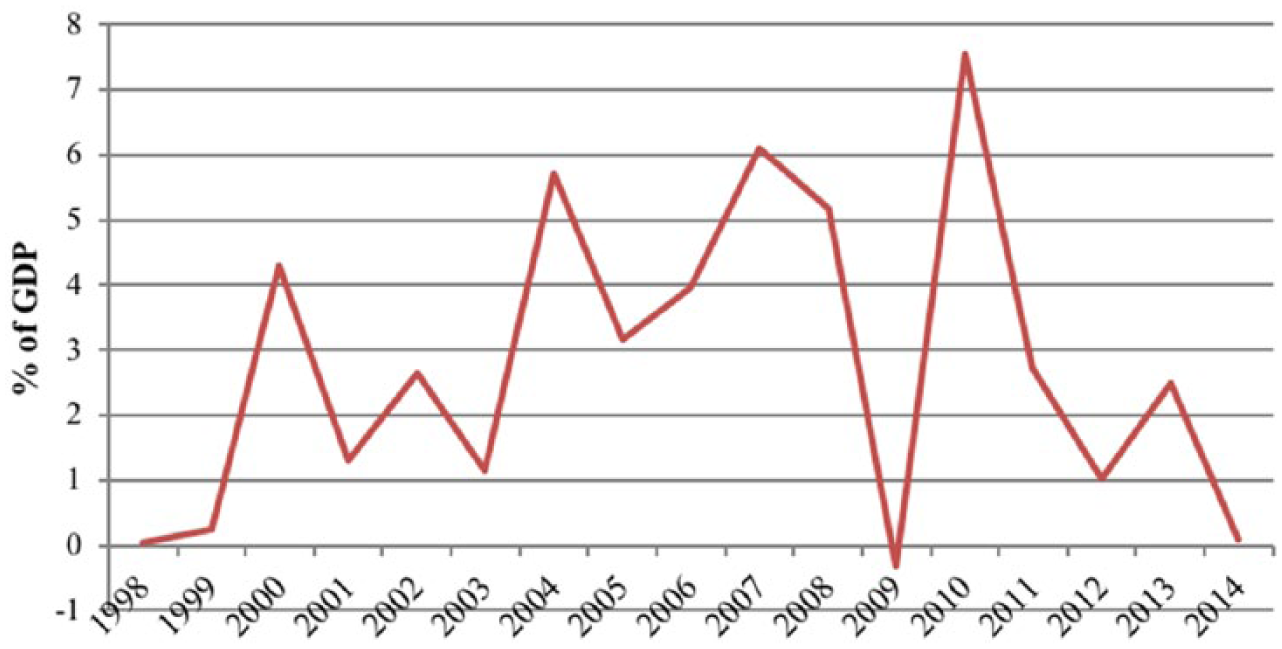

In 2003 and 2005, respectively, commodity export revenues and foreign money-capital recovered, in the context of a phase of credit-fueled accumulation on a world scale and a primary commodity boom driven by the demand of industrial development in China. The boom resulted in significant economic growth in 2003–2008 (see Figure 10), especially in comparison with the modest economic performance of the 1990s.

Annual Economic Growth Rates in Percentage of GDP

Under the guise of “neo-developmentalism,” the PT administration resorted again to several policies to channel a share of surplus from the primary sector to industries: local industry protection, import taxes and other trade-related CC, infrastructure provision, and credit at subsidized rates by national development banks (Boito 2010; Grinberg and Starosta 2014). It also deepened the financial policies previously mentioned to sustain the money-capital inflows. The removal of CC on outflows continued apace until 2006 (de Paula 2014).

Large commodity export revenues and foreign money-capital inflows contributed to a certain renewal of capital accumulation in 2003–2008 (see Figure 6), and significant gains for working classes were made: real increase in the minimum wage, public sector employment, extension of welfare regime and direct income redistribution, and extension of consumer credit for the poor (Morais and Saad-Filho 2011). This allowed the PT to engineer a new mode of labor containment, based on securing the consent of the poorest stratum of the population, the “neutralization” of relatively well paid workers in strategic sectors (mainly automobile and oil), and the neo-corporatist integration of a unionized working-class élite into state power (Boito 2010; Morais and Saad-Filho 2011). However, in comparison with other emerging capitalist countries, 14 accumulation levels remained modest. By contrast, the build-up of fictitious capital was impressive (see Figure 7). An important consequence of the growing stock of fictitious capital (often short-term foreign investment), as well as the tendency of local firms to increasingly rely on international money markets to fund their operations and hedge financial risks (Kaltenbrunner and Karacimen 2016), is that it has deepened the reach of the money-power of capital in the Brazilian space of valorization. The vulnerability to the volatile movement of private money-capital has become more acute, as was made clear when the 2008 global financial crisis erupted. International investors “sought refuge” in high quality assets in core advanced capitalist countries, which triggered a massive currency depreciation in Brazil (see Figure 8). Yet money-capital flows to Brazil quickly resumed, as financial investors took advantage of quantitative easing: cheap money borrowed in advanced capitalist countries was massively invested in the form of fictitious capital in DECC with higher interest rates and better prospects of labor exploitation.

In that context, between 2009 and 2012, the PT administration deployed a series of (market-friendly) CC on inflows. These consisted in financial transaction taxes on nonresident fixed-income and portfolio inflows and on external loans (various IOFs). It also implemented foreign exchange derivatives regulations to tame currency speculation on derivatives markets, and reinforced macroprudential financial regulations (de Paula 2014). However, at the same time as this timid attempt to alter the composition and movement of money-capital, the PT administration maintained the class-based arrangements and policies that underpinned the inflow of external money-capital: inflation-targeting, real high interest rates, liquidity provisions, primary fiscal surpluses, large reserve accumulation, and so on. This is a clear example of the state’s attempt at managing the antagonism between encouraging the inflow of money-capital to support accumulation, and simultaneously facilitating its own reproduction and that of the national money.

CC were then gradually lifted when inflows slowed down in late 2012 to early 2013, as international investors expected monetary authorities (especially the US Federal Reserve) to taper quantitative-easing programs, and global commodity prices slumped. Moreover, social and political unrest further deteriorated prospects of labor exploitation. This included active mobilization of indigenous movements and the MST, student and left-wing activism, urban workers and public servants’ strikes against reduction in real wages, demonstrations against the 2014 World Cup and increases in public services fees, and the growing discontent of upper middle-classes (Saad-Filho 2013). This diversity of social forces clearly showed the PT’s failure to manage class relations, especially in a context where the commodity boom came to an end, and money-capital inflows slowed down. 15 The situation incredibly quickly turned into a severe economic and political crisis, epitomized by Dilma’s presidential impeachment in 2016, and the fragile social gains achieved under the PT rule are rapidly being reversed.

5. Conclusion

The article offered a historical materialist engagement with the political economy literature on the post-crisis resurgence of CC in DECC. After critically reviewing the recent policy space literature and identifying a series of analytical shortcomings, I outlined a theoretical framework grounded in historical materialism, which allows studying CC in light of the social constitution and the class character of the state, money, and private capital flows. My main contention is that CC must be grasped in light of a fundamental contradiction: from the perspective of the capitalist state, money-capital constitutes a source of social wealth that can be distributed to various social subjects through diverse state policies for the purpose of fostering accumulation and managing class relations, but the movement of money-capital also shapes the modalities through which the state politically contains and integrates labor within its national space of valorization. I have substantiated this argument by showing how the historical deployment of CC in Brazil since 1945 can be understood as the concrete historical forms through which the state has politically mediated this antagonism, depending on the dynamics of capital accumulation, global liquidity conditions, and variegated state attempts at containing social class struggles.

This historical materialist perspective has important implications for the understanding of the politics of regulating cross-border capital flows in DECC (and more broadly the relationship between capital mobility and uneven forms of state power), since it highlights a series of class-based dynamics and processes that have so far remained invisible to most of the international political economy scholarship on the topic, including the recent policy space literature. This is largely due, in my view, to its grounding in two foundational arguments about the international political economy of capital mobility: on one hand, the “capital mobility hypothesis,” which sees global financial integration and enhanced capital mobility as a structural constraint of the policy autonomy of national states (e.g., Andrews 1994; Cerny 1999; Germain 1997; Strange 1996), and on the other, the Neo-Realist argument according to which global capital mobility is enforced and maintained by the most powerful states of the global political economy (e.g., Andrews 2006; Kirshner 1995, 2002).

While both of those theoretical traditions have provided valuable insights into the nature of global capital mobility, they have largely neglected class processes. More importantly for the purpose of this article, this has resulted in difficulties (exemplified in the recent policy space literature) in grasping why DECC would simultaneously deploy policies that appear to be directly conflicting, such as CC that (allegedly) constrain financial market power, and other policies (such as a long-term commitment to an open capital-account, high real interest rates, high primary fiscal surpluses, etc.) that encourage the inflow of money-capital. By contrast, the historical materialist approach outlined in this article shows how the conjunction of those seemingly inconsistent policies can contribute to reproducing—though in a contradictory and crisis-driven way—various forms of capital accumulation and capitalist class rule in DECC. The case study of Brazil has provided ample illustrations of this.

This argument seriously challenges the narrative, widespread in heterodox economics and critical international political economy, which tends to portray CC as inherently progressive policies. This leads to the political argument of this article: while there has been a growing consensus among critical and heterodox voices about the need for CC, commentators have tended to neglect the class dynamics associated with CC. My claim is that if we are to push for CC that aim—beyond the mere macroeconomic stabilization of capital accumulation—at empowering labor vis-à-vis capital to achieve a more egalitarian social order (Epstein 2010: 239), an analytical focus on class processes is crucial. By downplaying the important distinction between the types of CC analyzed in this article (fully functional, and in fact instrumental, in the reproduction of capitalist social relations, as shown in the case of Brazil), and the more “transformative” forms of CC, that is, CC that aim at transforming social relations and class configurations (Alami 2018; Dierckx 2015; Epstein 2012), debates about CC run the risk of being depoliticized and domesticated by the IMF, mainstream economists, and state managers. In fact, there is evidence that this is already happening (e.g., Grabel 2015). Critical reflections on the potential for transformative forms of CC are necessary if any meaningful project of progressive and development-friendly forms of financial governance is to be successful. This is particularly important at the current historical juncture, where unprecedented creation of money and fictitious capital have been maintaining global capitalism on life-support in the post-crisis environment but have resulted in frenetic movements of money-capital across the world market, desperately looking for satisfactory prospects of labor exploitation. As the policies of cheap money are gradually coming to an end, the impacts in terms of the global movement of money-capital remain to be seen, especially for DECC.

Footnotes

Acknowledgements

Thanks are due to Adrienne Roberts, Stuart Shields, Greig Charnock, and the three RRPE reviewers Annina Kaltenbrunner, Elif Karaçimen, and Firat Demir for insightful comments on earlier versions of this article. I would also like to thank the Union for Radical Political Economics for its generous funding (URPE dissertation fellowship 2017–2018).

Author’s Note

Ilias Alami is now affiliated to the Department of Society Studies at Maastricht University, Netherlands.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the Union for Radical Political Economics for its generous funding (URPE dissertation fellowship 2017–2018).

1

By contrast, mainstream economists have broadly rejected CC, both on theoretical grounds and on the basis that they are in practice (allegedly) ineffective.

2

And three more advanced capitalist countries, Iceland, Cyprus, and Greece.

3

To list but a few: power dispersion in the global financial architecture, a crisis of the financial globalization project and of the Anglo-American brand of liberal capitalism, the rise and growing assertiveness of the so-called BRICS, as well as “self-insurance” strategies on the part of DECC (Grabel 2011; Helleiner 2010; ![]() ).

).

4

These include upward pressures and higher volatility of the exchange rate, the formation of asset-price bubbles, the build-up of financial fragility, the loss of monetary policy autonomy, and the risk of capital flight.

5

For an examination of the persistence of this dichotomy in international political economy, and its ontological, epistemological, and methodological implications, see ![]() . In the case of the literature on policy space, this dichotomy is expressed in the tendency to interpret power relations between states and markets as some kind of mechanical zero-sum game situation. For instance, more financial capital mobility = less policy space.

. In the case of the literature on policy space, this dichotomy is expressed in the tendency to interpret power relations between states and markets as some kind of mechanical zero-sum game situation. For instance, more financial capital mobility = less policy space.

6

“States must constantly be able to recycle existing state debts. This involves demonstrating that the state’s fictitious capital claims held by financial capital today can be honored in the future” (![]() : 312). According to Marx, fictitious capital is a capitalized claim on future surplus value production. Accordingly, state fictitious capital is a capitalized claim to future tax revenue.

: 312). According to Marx, fictitious capital is a capitalized claim on future surplus value production. Accordingly, state fictitious capital is a capitalized claim to future tax revenue.

7

8

The manipulation of foreign exchange markets and state control of trade were used to cheapen the local price of foreign exchange for strategic imports (such as machinery and industrial inputs). This allowed transferring a share of surplus from primary commodity exporters to various sectors producing for the domestic markets. This was a central aspect of the ISI growth strategy (![]() ).

).

9

During this period, violent police repression resulted in significant wage contractions, benefitting capital especially in the industrial sector.

10

Furthermore, Brazil reached an agreement with its creditors under the framework of the Brady Plan in 1991 (and the agreement was concluded in 1993–1994), allowing a return to international financial markets.

11

By establishing an (overvalued) semifixed exchange rate as the “anchor” of prices to control inflation, the Real Plan also made the continuous inflow of money-capital necessary to reproduce the national money.

12

This figure only displays the accumulation of the three elementary forms of fictitious capital (following Marx). It does not include more complex forms such as derivatives and other financial instruments, nor fictitious capital accumulation in the built environment. It is, therefore, highly likely that the figure shows a conservative picture of fictitious capital accumulation in Brazil over the period.

13

This move was at least partly motivated by the fact that the use of some of these CC was forbidden under the IMF stand-by agreement.

14

According to data from the World Bank World Development Indicators, gross fixed capital formation in Brazil averaged 17.6 percent of GDP between 2003 and 2013. The figure for China is 43 percent, 30.7 percent for India, 21.7 percent for Mexico, and 20 percent for Turkey.

15

Serious troubles in China since mid-2015 have worsened the situation and triggered the worst episode of capital flight from DECC since the 1980s, with Brazil severely hit. In 2015, the Brazilian real depreciated by a third against the dollar.