Abstract

Despite its increasing importance, digital financial literacy (DFL) is yet to be adequately understood. This article reports on one aspect of DFL, namely, digital asset planning literacy (DAPL) which is an individual’s awareness of what happens to their digital assets on their death or incapacity. Our results from Australia and Singapore suggest that single, less-educated women are less likely to possess DAPL, and that the number of digital assets is negatively associated with DAPL, while having a Will is positively related to DAPL. With this study, we put forward that financial education should include consumer rights regarding digital financial assets.

1. Introduction

It has long been established that poor financial literacy results in poor saving, poor spending, excessive credit card use and bad investment decisions (Lusardi and Mitchell, 2014; van Rooij et al., 2011). In addition to the direct financial consequences of poor financial literacy, the stress of financial insecurity in families can trigger problems that lead to divorce, suicide, homelessness, domestic violence and crime (Cumming and Peterson, 2017; Reher, 2011).

Despite the ongoing debates in defining and measuring financial literacy (Huston, 2010; Li, 2020), it is generally accepted that it involves the ability to understand and effectively use a set of financial skills and knowledge to successfully manage one’s finances (Lusardi and Mitchell, 2011). Among others, Remund (2010: 276) attributes financial literacy to a measure of the degree to which one understands key financial concepts and possesses the ability and confidence to manage personal finances through appropriate short-term decision-making and sound, long-range financial planning, while mindful of life events and changing economic conditions.

Similarly, the Australian Securities and Investments Commission (ASIC, 2003: 10) defines financial literacy as ‘the ability to make informed judgments and to take effective decisions regarding the use and management of money’.

Analogous to financial literacy, the concept of digital literacy has been discussed in terms of the application of skills to enable users to operate effectively with software tools or in performing basic information retrieval tasks (Buckingham, 2010). More recently, the concept of digital financial literacy (DFL) has been used to describe how effectively one uses digital devices to conduct financial transactions (Kaiser et al., 2020). As our lives are increasingly online, including those aspects that relate to personal financial management, poor digital skills and limited access to digital technology (referred to as the ‘digital divide’) can adversely impact the ability of a person to manage their finances efficiently and effectively (Wright, 2019). Consequently, it is no surprise that DFL has been associated with financial wellbeing (Tony and Kavitha, 2020).

Increasing application and use of digital technologies has given rise to what is referred to as ‘digital assets’. Understanding one’s rights and the consequences of using digital technology and emerging ‘digital assets’ is arguably as important as being able to use digital technology to undertake financial transactions. In general, these digital assets can be defined as any item of text or media that has been formatted into a binary source over which a person has ownership rights (Van Niekerk, 2006). As such, the scope of digital assets is quite extensive. For example, Zhang and Gourley (2008) include digital documents, audible content, motion pictures and other relevant digital files as digital assets that may be stored on currently existing digital appliances or those that may be developed in the future. Johnston (2015) notes that digital assets include not only items with direct monetary value such as domain names, online businesses or cryptocurrency, but also data of sentimental value such as photographs and emails. Some of these items may be held in cloud storage or on third-party hosting sites. 1

The relatively recent development and widespread adoption of digital technology has meant that digital assets are often forgotten by testators/donors in the preparation of a Will or Power of Attorney (POA). With non-digital estate assets, there is usually some paper or physical trail, such as credit and debit cards, indicating the presence of an account with a particular financial institution that can then be approached. The absence of a paper trail and existing processes to identify estate assets can make the administration of a deceased estate more difficult. Furthermore, once a Will or POA has been prepared without the inclusion of digital assets, it is inevitably too late to rectify this situation once the executor takes control of an estate or an attorney exercises their powers. Illiteracy in this context of digital assets can therefore have serious financial and non-financial consequences for beneficiaries and principals (Kaiser et al., 2020). While there is a substantial body of literature on financial literacy, there is a paucity of literature that specifically deals with financial literacy and estate planning in general, and estate planning and digital assets in particular. Arguably, the literature that comes closest to examining estate planning and financial literacy deals with financial planning and its impact on retirement planning decisions (Lusardi and Mitchell, 2011).

It has only been recently acknowledged that the scope of digital literacy and DFL is wider than the mere ability to effectively use digital products (Kaiser et al., 2020). Morgan et al. (2019) expand the definition of DFL from the purely functional to one that covers four dimensions, including knowledge of digital financial products and services (DFS), awareness of digital financial risks, knowledge of digital financial risk control, and knowledge of consumer rights and redress procedures. In this article, we focus on one key aspect of DFL, the awareness of the fate of digital assets on death or disability. We refer to this aspect of DFL as digital asset planning literacy (DAPL).

Through a sample of the Australian and Singaporean populations, we explore the extent of digital asset holdings (including digital financial assets) of individuals and awareness of the fate of their digital assets on death or disability. Our results demonstrate Australians and Singaporeans are generally unaware of what will happen to their digital assets on death or disability (i.e. low DAPL). We find that the relationship status and educational level of respondents are positively associated with DAPL. Conversely, women are significantly less likely to possess DAPL. We also find that DAPL is influenced by how many classes of digital assets an individual holds and whether they have a Will. We consider our results in light of the theory of structuration (Giddens, 1979) to examine why some people engage with emergent technology while others are disadvantaged and excluded from the benefits of new technologies. These findings have important implications for social policy indicating that financial literacy education should not just focus on effective functional use of digital assets, but also on consumer rights and risks. Furthermore, professional financial advisors should be cognisant of not only their clients’ financial literacy but also their DAPL.

The article is divided into the following sections. Section 2 provides a review of the literature with respect to both financial and digital literacy, and digital assets. In Section 3, the overarching research question and hypotheses of this study are presented. In Section 4, we outline the research methods used and data collected. In Sections 5 and 6, respectively, we report and discuss the findings. We conclude the article in Section 7 with a summary of the contributions and implications of this study.

2. Literature review

2.1. Digital assets and social change

It is not difficult to argue that digital assets have caused, and are continuing to cause, enormous social change. Mazumda (1996) notes that social change occurs where there is a new fashion or mode that modifies or replaces the old in the life of people or in the operation of society. Being defined in sociology as the alteration of mechanisms within the social structure, social change is characterised by changes in cultural symbols, rules of behaviour, social organisations or value systems (Wilterdink and Form, 2017). Social change can evolve from a number of different sources, including contact with other societies (diffusion, see Migdal, 2015), changes in the ecosystem (Cumming and Peterson, 2017) which can cause the loss of natural resources or widespread disease, technological change (Cowan, 1976) epitomised by the Industrial Revolution which created a new social group, the urban proletariat, and population growth and other demographic variables (Reher, 2011). Social change is also spurred by ideological, economic and political movements (King and Pearce, 2010). Ogburn (1964) identifies technology as a fundamental cause of social change, in which technology changes first and cultural changes follow suit. As Mutekwe (2012: 232) describes, ‘we play catch-up with changing technology, adapting our customs and ways of life to meet its needs’.

Jones and Karsten (2008) note that various theories have been used to gain insights into the development and impact of information systems such as digital technologies, and among these, the most influential is arguably structuration theory (Giddens, 1984). Structuration theory examines the production and reproduction of social systems through the interaction of actors (described as human agents) and social structure (rules and resources). Jones and Karsten (2008: 129) submit that ‘human agents draw on social structures in their actions, and at the same time these actions serve to produce and reproduce social structure’. In employing structuration, Jones and Karsten (2008: 131) state that ‘Giddens sought to emphasize that social structure is continuously being created through the flow of everyday social practice’. Accordingly, the process of social change can be observed, for example, using new technology to facilitate the management, planning and transaction of personal wealth and assets. Jones and Karsten (2008) suggest that the influence of technology on social practice depends on how social agents engage with it in their actions. For example, Alhassan and Adam (2021) posit that human agents are free to choose what various digital technologies they engage with to enhance their quality of life. In addition, social structures have the possibility to serve as both enablers and restraints for human agents (Stoecklin and Fattore, 2018).

An important feature of Giddens’ structuration theory is that the ability of human agents to participate and shape social structures is linked with their knowledge, participation and use of these structures (Jones and Karsten, 2008). However, as highlighted by Matli and Ngoepe (2020), many individuals may be excluded from participating in new and emerging social structures brought about by digital technologies because of a lack of adequate skills, education and resources. This suggests that not all actors have agency to freely choose what various digital technologies they engage with to enhance their quality of life. Furthermore, structuration theory elaborates that exclusion does result not only from social actors’ lack of access to, but also from their inactive participation in, or incapability of, engaging with the social structure emerged from adopting digital technologies (Giddens, 1984). Consequently, it may be necessary to formulate crucial policy measures and interventions to ensure that all sections in society can participate in the opportunities presented by the digital economy, and these policy measures need to be informed by appropriate research.

2.2. From digital financial literacy to understanding digital assets, death and disability

The link between financial literacy and digital skills has been the focus of some recent studies. For example, Yakoboski et al. (2018) consider the relationship between financial literacy and use of fin-tech among millennials Generation Y. They note that over 90% of millennials own a smartphone, and 80% of them use their device to some degree for transactional fin-tech purposes and 90% for informational fin-tech purposes. However, they could not determine whether fin-tech use resulted in better personal finance outcomes.

Studies such as Yakoboski et al. (2018) and Oggero et al. (2019) identify digital skills from a functional perspective as the ability to use computers or other digital devices such as smartphones. Wihbey (2013) notes that the lack of digital literacy may include the inability to perform simple functions, such as composing emails, logging into online platforms and even saving work to a thumb or disk drive, and that without these basic skills, one becomes unmarketable to potential universities and job opportunities. Similarly, Staliski (2017) posits that a combination of poor financial literacy and poor digital literacy can put people at a severe disadvantage.

While digital skills and the use of digital technology have been examined in relation to building financial capability, one relatively new theme in financial literacy research deals with the relationship between financial literacy and the access to digital technology (see Wright, 2019). These papers argue that the lack of financial literacy and access to information technology contribute to socio-economic division or the ‘digital divide’. For example, Servon and Kaestner (2008) argue that better access to information and communications technology, combined with financial literacy training and training on how to use the Internet, turns low- and moderate-income individuals in inner-city neighbourhoods into more effective financial actors.

Recently, the term DFL has been used (Morgan and Trinh, 2019; Morgan et al., 2019; Prasad et al., 2018) in the context of the knowledge and application of digital platforms and systems used to facilitate financial transactions. Thus, DFL provides a broader focus than merely using digital technology to complete financial transactions. Morgan et al. (2019) note that there is no standardised definition of DFL. They propose that it consists of four dimensions, namely, knowledge of DFS, awareness of digital financial risks, knowledge of digital financial risk control, and knowledge of consumer rights and redress procedures. While Morgan et al. (2019) do not specifically examine DFL in the context of whether people know what will happen to their digital assets on death, their second dimension of DFL, awareness of digital financial risks, considers whether individuals understand the risks involved with DFS. They describe DFS as more diverse and sometimes harder to identify than those associated with traditional financial products and services but could presumably include the preparation and execution of online Wills and POAs. While their focus is on online fraud and cyber security risks and excessive use of credit, they note that DFS users should fully understand terms and conditions stipulated in contracts they digitally sign with DFS providers. They should also be aware of (risky) implications of digital contracts. They should understand that DFS providers may use their personal information for other purposes such as calculating their credit demands, advertising and credit evaluation. (Morgan et al., 2019: 6)

The fourth dimension, knowledge of consumer rights, presumably would also include knowledge of whether digital assets can be bequeathed on death or accessed on disability by legal personal representatives (LPRs) (i.e. estate executors or administrators).

Existing research that aims to examine DFL is remarkably scarce, but one recent study by Setiawan et al. (2020) applies a definition broadly consistent with Morgan et al. (2019) to investigate the relationship among DFL, current saving behaviour, current spending behaviour, and foresight of future spending and saving behaviour among Indonesian millennials. The research surveyed around 500 millennials in the 25–40 age group in multiple urban areas of Java Island. They asked respondents questions including how well they understood (and had experience with) various categories of digital financial platforms and products as well as rights and risks with regard to services from digital financial products and providers. The results indicate that DFL is influenced by socio-economic standing and is also positively related to current saving and spending behaviour. Furthermore, current saving and spending behaviour contribute to future saving and spending foresight. Like Setiawan et al. (2020), we aim to examine in this study individuals’ understanding of their digital financial assets, and we approach this from an estate planning perspective, which is practically meaningful but under-researched in existing literature.

DFL has also been examined in the context of entrepreneurship, with it being associated with men rather than women in entrepreneurial activity (Oggero et al., 2019). This research based on bank records in Italy finds that males are much more likely to start a new business if they have both financial and digital skills and understanding. DFL has also been discussed as an important driver of economic activity as it helps enable sophisticated and empowered financial transactions for citizens, especially in the transition away from a cash-oriented economy (Prasad et al., 2018).

As the number of digital assets held by the average person increases, questions surrounding the access to and management of digital assets upon the individual’s death or incapacity are increasingly common. To distinguish this aspect of DFL, we use the term DAPL. Understanding one’s rights with regard to digital assets on death and disability is an obvious prerequisite for responsible access and management of them.

3. Research question and hypotheses

As discussed above, the Internet and digitisation have led to rapid and dramatic economic and societal changes. Economic change has occurred through accelerated innovation, enhanced productivity and irreversible transformation of employment (Brynjolfsson and McAfee, 2011). For society, the Internet has changed life fundamentally, for example, in the way people communicate, with email replacing physical mail, and the way people transact using digital currency and digital platforms facilitating financial transactions. As indicated earlier, email and digital currency are just two digital developments that have been categorised as ‘digital assets’. As discussed below, with the rise of digital assets, we argue that a critical emerging component of DFL is in regard to estate planning, which we refer to as DAPL, that is, planning for what will happen to an individual’s digital assets in the event of their incapacity or death.

The term digital asset is increasingly used in estate planning, acknowledging the importance of assets that are created and/or held in digital forms and for which there is an intrinsic and/or monetary value. As a result, it is increasingly important to identify, manage and store digital assets. Despite this, digital assets may be forgotten by testators/donors when giving an asset list to relatives/practitioners in the preparation of a Will or POA. If this is the case, it may be too late to rectify this situation once a fiduciary takes control of an estate or an attorney exercises their powers. Illiteracy in the context of digital assets can therefore have serious financial and other consequences for beneficiaries and principals.

In addition, Walter et al. (2012) indicate the Internet and digitalisation have changed a range of practices relating to dying, grief, and memorialisation and inheritance. They note that the Internet and digitalisation also raise several questions involving control, power and privacy. Difficulties arise because service agreements between users and digital vendors and online platform operators usually stipulate that the contractual relationship is between the registered user and the vendor/operator. Given the nature of this contractual relationship and concerns about maintaining privacy, vendors/operators have been either unwilling or unable to allow relatives or trustees to access the personal records and other online material of the account holder in the event of death or disability. This has resulted in legal challenges by families and LPRs against vendors/providers in many countries (McCallig, 2014). Legislation designed to allow LPRs to access the digital assets of the disabled and deceased has only recently been enacted in most US states (Genders and Steen, 2017). In other jurisdictions, legislation has been proposed or is in early stages of discussion if being considered at all. Hence, social change driven by technological developments has caused problems which society needs to address.

Given the existing and increasing importance of digital assets, an important aspect of DFL is to understand terms of service, particularly with respect to one’s rights at death. The ability to pass on one’s assets (freedom of testamentary disposition) is a fundamental right that has been acknowledged universally. Knowing what will happen to one’s assets at death would therefore be necessary and important if not essential. Therefore, we argue that a key emerging aspect of DFL is an individual’s knowledge of what will happen to their digital assets if they are incapacitated or die, namely, their DAPL. In general, studies find that financial literacy is positively correlated with planning for retirement, savings and wealth accumulation (Ameriks et al., 2003; Hung et al., 2009; Lusardi, 2004; Lusardi and Mitchell, 2007; Stango and Zinman, 2009; van Rooij et al., 2012). Drawing on previous research on financial literacy, digital literacy and financial planning, below we present our hypotheses that examine the determinants of DAPL, that is, whether individuals are aware of what will happen to their digital assets on death.

Age has been found to be positively associated with financial literacy (Kadoya and Khan, 2020; Taft et al., 2013). Lusardi and Mitchell (2014) find that an individual’s confidence in their own financial literacy increases with age. Lusardi (1999) reports that two-thirds of those under 50 years of age did not plan for retirement and therefore may be less likely to be concerned with DAPL. As a consequence, we propose the following hypothesis:

H1a. DAPL is positively associated with the age of an individual.

Women have been found to possess significantly lower levels of financial literacy compared to men (Lusardi and Mitchell, 2008, 2014; Potrich et al., 2018). Women have also been found to have lower levels of retirement planning compared to men (Lusardi, 1999), and therefore may be less likely to possess DAPL. Therefore, we propose the following hypothesis:

H1b. DAPL is associated with gender. Specifically, compared to men, women are less likely to possess DAPL.

Taft et al. (2013) found that marriage is positively related to financial literacy. As a result, we propose the following hypothesis:

H1c. DAPL is positively associated with the relationship status of an individual.

In an Australian survey, Baker and Gilding (2011) found that being a parent/grandparent is positively associated with making a Will. Accordingly,

H1d. DAPL is positively associated with the parental status of an individual.

Lusardi and Tufano (2009) and Lusardi and Mitchell (2011), among others, find that income is positively associated with financial literacy. Accordingly,

H1e. DAPL is associated with the income of an individual. Specifically, low-income earners are less likely to possess DAPL.

Lusardi and Mitchell (2014) found that an individual’s financial literacy increases with their level of education. Education has been argued as a way of improving the financial literacy of the general population, and particularly disadvantaged groups (Brimble and Blue, 2013). Thus, we propose the following hypothesis:

H1f. DAPL is positively associated with the educational level of an individual.

Rates of financial literacy have been found to vary from country to country (Lusardi and Mitchell, 2014). While Australia and Singapore have similar levels of financial literacy (Klapper and Lusardi, 2019), this does not necessarily mean they have the same levels of DAPL. Compared to Australia, Singapore ranks significantly higher on several indices dealing with digital competitiveness and readiness (2nd vs 15th) (CISCO, 2020; Combes, 2020; The IMD and World Competitiveness Center, 2020). This suggests Singaporeans may have higher levels of DFL and consequently DAPL. Also, there are also important cultural differences between these two countries, where Singapore rates significantly higher on long-term orientation compared to Australia (Hofstede Insights, 2020). This suggests Singaporeans may take a long-term perspective to managing digital assets and consequently have higher levels of DAPL. Accordingly,

H1g. DAPL is associated with the country of residence of an individual. Specifically, compared to Australians, Singaporeans are more likely to possess DAPL.

Abreu and Mendes (2010) find evidence that financial literacy is positively related to portfolio diversification. In the same way, we propose that the number of digital asset categories in possession of an individual is positively related to their DAPL. Therefore, our second hypothesis is as follows:

H2. DAPL is positively associated with the number of types of digital assets an individual owns.

As discussed earlier, an important feature of Giddens’ structuration theory is that the ability of human agents to participate and shape social structures, such as digital assets, is linked with their knowledge, participation and use of these structures (Jones and Karsten, 2008). Many individuals may be at a disadvantage in aspects associated with their involvement with digital assets, such as their management and preservation, because they lack the requisite skills, education and resources. As outlined in the arguments supporting H1a–g, these disadvantages may stem from their limited education, life experience, family circumstances and country-of-origin influences. However, seeking expert advice to develop a Will may represent one type of intervention to overcome such disadvantages and acquire the knowledge and resources required to more effectively manage and preserve of their digital assets. This is because the process of establishing a Will explicitly addresses issues surrounding the administration and legal ownership of an individual’s assets, regardless of whether they are tangible or intangible. Consequently, we argue that those that plan for death or disability as illustrated by their having a Will should, other things being equal, have better knowledge of the fate of their digital assets on death or disability. Hence, our third hypothesis is as follows:

H3. DAPL is positively associated with whether an individual has a Will.

4. Research method

4.1. Survey design and participants

An online survey was used to collect data for this study. Online surveys offer certain advantages over traditional surveying methods including saving time and money and reaching a wider population. The survey invited people to share their experience and engagement with estate planning and various issues surrounding the intergenerational transfer of assets.

We chose to sample individuals from Australia and Singapore to explore the effect of country differences on an individual’s DAPL. Australia and Singapore are both recognised as wealthy, advanced countries with similar common law legal systems. However, as argued when presenting H1g, they differ with regard to their digital competitiveness and readiness, and long-term cultural orientation, which we believe will have a significant effect on an individual’s DAPL.

The research team drafted a survey and completed a pre-test with several estate practitioners in early 2017. Basic questions were adapted from previous studies such as Tilse et al. (2015) and consisted of 32 questions regarding estate planning practices and knowledge as well as participants’ demographic data. 2 Ethical clearance for this research was obtained from the team’s affiliated institutes for both surveys in Australia and Singapore.

Participant data for this project were collected via a leading online survey panel provider Qualtrics. The use of an online survey was felt appropriate as it ensures respondents have some digital engagement, awareness and capability in keeping with the theme of the study. An email containing background information and a survey link was sent to members of each national Qualtrics Research Now panel. The online survey was open to participants for a period of 3 weeks and took around 15 minutes to complete. Qualtrics does not store IP addresses or other information that could be used to identify the participants. All responses, therefore, remained anonymous and confidential.

The Australian survey went live on Qualtrics in April 2017. There was a 93% response rate (1034 individuals with 70 indicating they did not wish to participate), and 32 incomplete surveys, resulting in a total of 932 usable surveys from Australian respondents. The Singaporean survey went live on the Qualtrics platform in October 2019. There was a 94% response rate (553 individuals with 32 indicating they did not wish to participate), and 56 incomplete surveys, resulting in a total of 465 usable surveys from Singaporean respondents. The samples were consistent with the Australian and Singaporean population in terms of gender split and age. Overall, the data provide a good representation nationally in terms of income, occupation and level of education attainment. Given the focus of this study is to evaluate determinants of an individual’s DAPL, respondents who owned no digital assets were removed from the sample. This reduced the sample size to 762 surveys from Australian respondents (i.e. removal of 170 respondents) and 420 surveys from Singaporean respondents (i.e. removal of 45 respondents). In order to derive a balanced sample of an equal number of participants from both countries, 420 of the 762 Australian respondents were randomly selected to be included with the 420 Singaporean respondents, resulting in a total sample of 840 respondents (50% Australian, 50% Singaporean).

4.2. Variables

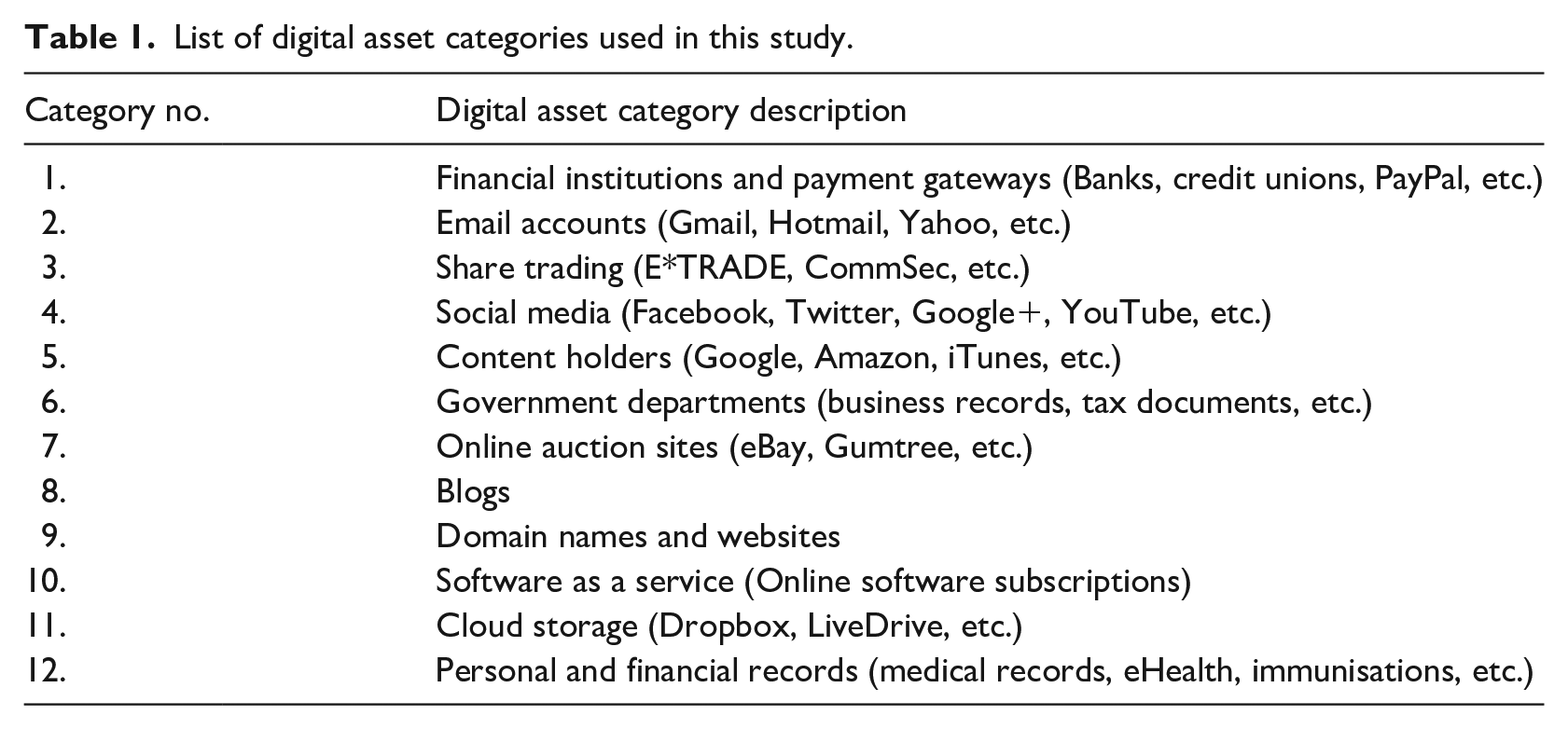

Table 1 provides the various classes or types of digital assets identified in this study by drawing on Ploss’ (2017) list of digital assets. Survey participants were asked to check which digital financial assets they had as indicated in Table 1, and they were then asked whether they knew what would happen to these online assets in the event of their incapacity or death. As indicated below, questions covering a range of demographic characteristics were also used.

List of digital asset categories used in this study.

4.2.1. Digital Asset Planning Literacy

The dependent variable used in this study was measured by asking participants ‘Do you know what will happen to your digital assets if you are incapacitated or die?’ This variable was measured using a dichotomous measure (yes = 1, no = 0).

4.2.2. Number of different categories of digital assets owned

The independent variable ‘number of categories of digital assets owned’ was measured by asking participants to identify each of the digital asset classes using a dichotomous measure (yes = 1, no = 0). In total, participants were asked whether they owned digital assets in 12 different digital asset categories (see Table 1 for the full list). Consequently, the measure of these variables ranged from 0 (no digital assets) to 12 (own assets in all 12 digital asset categories).

4.2.3. Have a will

The independent variable ‘have a Will’ measured whether a participant had a legal Will in place at the time of the survey. Each respondent was asked ‘Do you have a Will?’ and was measured using a dichotomous measure (yes = 1, no = 0).

4.2.4. Demographic characteristics of participants

The following demographic characteristics of participants were measured:

Age – because of issues surrounding confidentiality in Singapore, it was not possible to ask the specific age of respondents. As a consequence, an ordinal measure was used to measure age (1 = <35 years of age; 2 = 35–64 years of age; 3 = 65+ years of age);

Gender – the respondent’s gender was measured using a dichotomous measure (1 = male; 2 = female);

Relationship status – the respondent’s relationship status was measured using an ordinal measure and assessed the formality of the relationship (1 = not in a relationship; 2 = de facto relationship; 3 = married);

Children status – whether the respondent had children was measured using a dichotomous measure (0 = no, 1 = yes);

Low-income earner – whether the respondent was considered a low-income earner was measured using a dichotomous measure. Specifically, respondents earning less that AU$20,800 were identified as a low-income earner (1 = yes, 0 = no); 3

Educational level – the respondent’s highest level of educational achievement was measured using a 3-point ordinal scale (1 = school, 2 = technical and further education, 3 = university and above);

Country of residence – as this survey was conducted in two different countries, a dichotomous measure was used to control for the influence of the country of residence (1 = resides in Australia, 2 = resides in Singapore).

4.3 Model specifications

As the dependent variable for this study (DAPL) is a dichotomous variable, binary logistic regression was used to test the three hypotheses using the following model:

5. Results

5.1. Descriptive statistics of respondents sampled

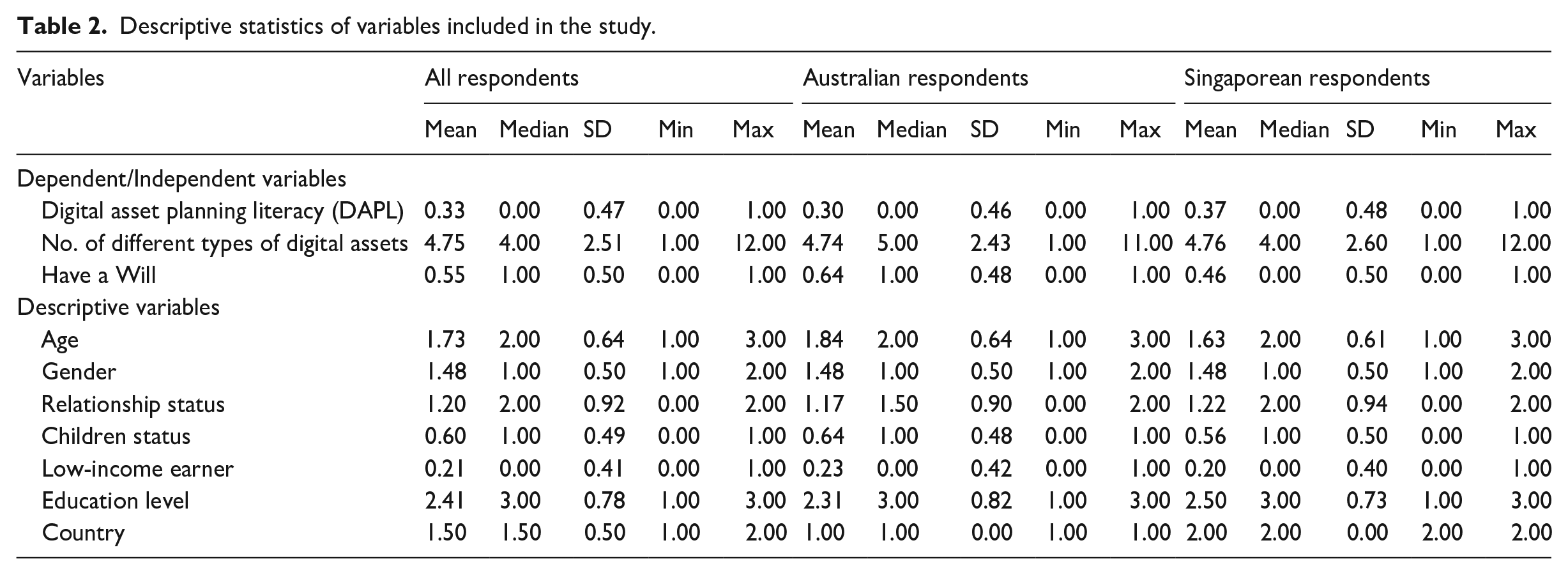

Table 2 presents the descriptive statistics of the variables included in this study, broken down by the country of residence of the participants. In the discussion of the descriptive statistics below, mean scores are used when discussing dichotomous and continuous variables, while median scores are used when discussing ordinal variables.

Descriptive statistics of variables included in the study.

Regarding the dependent variable used in this study, the mean score for the DAPL was 0.33. As this variable is a dichotomous variable, this indicates that 33% of all respondents believed they understood what would happen to their digital assets on incapacity or death. Respondents from Singapore were more likely to know what will happen to their digital assets compared to Australian respondents (37% and 30%, respectively).

Regarding the demographic characteristics of respondents sampled, the median age was 2, which corresponded to an age range between 35 and 64 years. The mean score for gender was 1.48, and as this was a dichotomous variable (male = 1, female = 2), this equates to 48% of respondents being male and 52% of respondents being female. The median for relationship status was 2, which suggests most respondents were married. The mean score for children status was 0.60, and as this is a dichotomous variable, this result indicates that 60% of respondents had at least one child. The mean score for low wage earner variable was 0.21, and as this is a dichotomous variable, this result indicates that 21% of respondents were considered low-income earners. Regarding educational levels, the median score was 3, which indicates that the majority of respondents were university-educated. The mean score for country of residence was 1.5, which indicates that 50% of respondents resided in Singapore while 50% resided in Australia.

The mean number of different categories of digital assets owned by the respondents was 4.75 and ranged from 1 to 12. The mean score for this variable was slightly higher for respondents from Singapore, but was not significantly different and suggests the ownership of digital asset categories of Singaporeans is similar to their Australian counterparts.

The mean score for whether respondents had a Will was 0.55. As this is a dichotomous variable, this result indicates that 55% of respondents had a Will. In general, Australian respondents were more likely to have a Will compared to respondents from Singapore (64% and 46%, respectively).

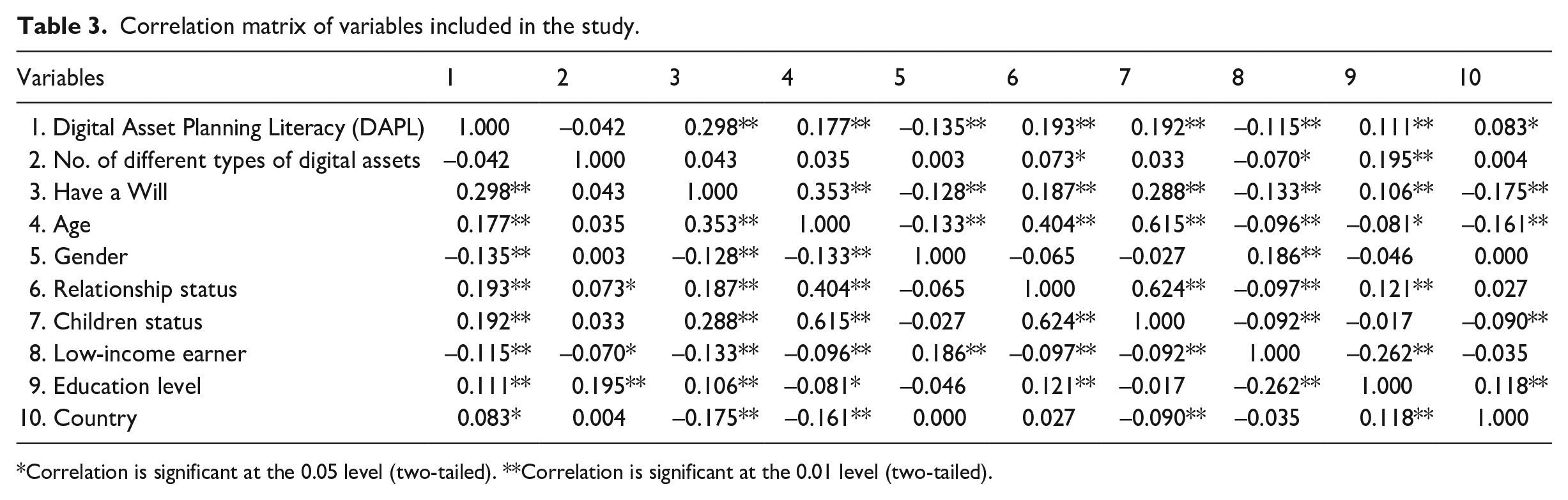

Table 3 presents the correlations between the variables included in this study. DAPL (the dependent variable) is negatively correlated with the independent variable ‘number of different categories of digital assets owned’ but positively correlated with the independent variable ‘have a Will’. With regard to the demographic variables, DAPL is positively correlated with age, relationship status, children status, education level and country (specifically, Singapore) and negatively correlated with gender (specifically, female) and low-income status.

Correlation matrix of variables included in the study.

Correlation is significant at the 0.05 level (two-tailed). **Correlation is significant at the 0.01 level (two-tailed).

The highest correlation between all independent and demographic variables was that between relationship status and children status (0.624). To test for problems of multicollinearity between the independent and demographic variables included in the modelling, the Variance Inflation Factor (VIF) scores were calculated. All independent and demographic variables have VIF scores below 2, well below the threshold of 10 prescribed by Gujarati (2003), which suggests multicollinearity is not a problem in this study.

5.2. Influence of demographic characteristics of respondents

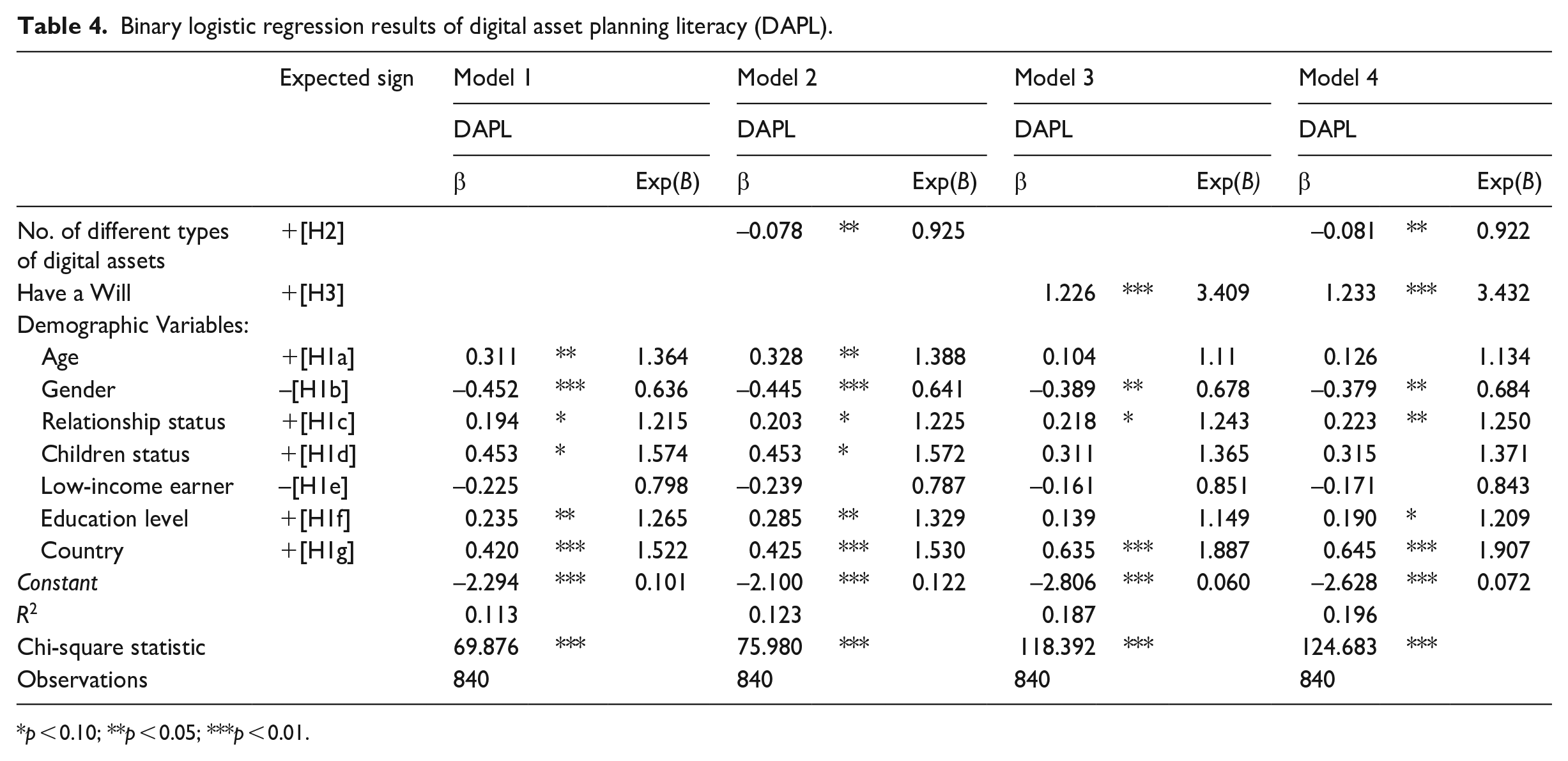

Model 1 in Table 4 presents the binary logistic regression results of the effect of demographic characteristics of respondents on the knowledge of what will happen to digital assets on incapacity or death (i.e. H1a–H1g). As binary logistic regression is used in this study, parameter estimates are converted to cumulative odds ratios to gain insights into the relative effect sizes of the significant independent and control variables (see Table 4 for Exp(B) values) on the likelihood of a respondent possessing DAPL. Odds ratios with values below 1 are associated with decreased odds of possessing DAPL, while values above 1 are associated with increased odds.

Binary logistic regression results of digital asset planning literacy (DAPL).

p < 0.10; **p < 0.05; ***p < 0.01.

With the exception of low-income status, all the demographic variables were significant in their hypothesised direction. The results suggest that age (p < 0.05), relationship status (p < 0.10), children status (p < 0.10), educational level (p < 0.05) and country of residence (p < 0.01) all had a positive significant association with DAPL, providing support for H1a, H1c, H1d, H1f and H1g. Conversely, gender (being female) (p < 0.01) had a significant negative association with DAPL, providing support for H1b. In summary, older university-educated, married men with children located in Singapore are statistically more likely to know what will happen to their digital assets in the event of their incapacity or death.

Based on the odds ratios (Exp(B)) reported in Model 1 of Table 4, whether a participant has a child had the largest positive significant effect on the likelihood of possessing DAPL. Specifically, having a child was associated with a 1.574 increase in the odds of possessing DAPL. This was followed by country of residence (1.522), age (1.364), education level (1.265) and relationship status (1.215).

5.3. Influence of the number of different types of digital assets

Model 2 in Table 4 presents the binary logistic regression results of the effect of the number of different categories of digital assets owned on DAPL while controlling for the demographic characteristics of the respondents. The results of the variable ‘number of different types of digital assets’ were significant (p < 0.05) but in the opposite direction to that hypothesised. Consequently, H2 is not supported. Specifically, as the number of different types of digital assets owned by a respondent increases, their likelihood of possessing DAPL decreases.

5.4. Influence of having a Will

Model 3 in Table 4 presents the binary logistic regression results of the effect of having a Will on DAPL while controlling for the demographic characteristics of the respondents. The results of the variable ‘have a Will’ were positively and significantly (p < 0.01) associated with DAPL and therefore provide support for H3. Specifically, respondents with a Will are significantly more likely to possess DAPL.

5.5. Combined influence of demographic characteristics, number of digital assets and having a will

Model 4 as in Table 4 presents the binary logistic regression results of the combined effects of demographic characteristics, the number of digital assets and having a Will on DAPL. Age ceases to be statistically significant. The results of the variable ‘have a Will’ were positively and significantly (p < 0.01) associated with DAPL and therefore provide support for H3. Specifically, respondents with a Will are significantly more likely to possess DAPL. Compared to in Model 1, in Model 3, the demographic characteristics ‘age’ and ‘children status’ cease to be statistically significant. This suggests that having a Will, rather than being older or having children, significantly influences DAPL. Consequently, this suggests that support for H1a and H1d reported earlier is questionable.

Based on the odds ratios (Exp(B)) reported in Model 4 of Table 4, whether a participant had a Will had the largest positive significant effect on the likelihood of possessing DAPL. Specifically, having a Will was associated with a 3.432 increase in the odds of possessing DAPL. This was followed by country of residence (1.907), relationship status (1.250) and education level (1.209).

5.6. Summary of results

Overall, the combined results reported in Model 4 of Table 4 provide support for H1b, H1c, H1f, H1g and H3. The results of the variable ‘number of different types of digital assets’ were significant (p < 0.05) but in the opposite direction to that hypothesised, and therefore H2 was not supported.

These results suggest that a respondent’s DAPL is influenced by their demographic characteristics (gender, relationship status, educational level and country of residence). Independent of their demographic characteristics, respondents who have a Will are more likely to possess DAPL. Conversely, the more the types of digital assets a respondent has, the less likely they are to possess DAPL.

6. Discussion

Our results show that only 33% of all respondents understood what will happen to their digital assets on their incapacity or death. The question is how we explain the lack of DAPL with respect to digital assets and death or disability.

As discussed earlier, technological change has been identified in the literature as a common precursor for social change. The pervasiveness of digital technology is changing society in countless ways, including the preparation and management of deceased estates and POAs. Part of good estate planning is the identification of one’s assets, including digital assets, and understanding what will happen to these on death or disability. If individuals fail to account for their digital assets or if they have digital assets that cannot be accessed by their attorneys in the case of disability, or their LPRs in the event of death, then this can cause stress and loss for beneficiaries. Social change theory can in part explain how society changes and reacts to the introduction of new technology.

As discussed previously, the theory of structuration (Giddens, 1979) notes that people may have substantial interaction with digital technology but still not fully engage with it and understand the implications of dealing with that technology. Further structuration also explains that a lack of adequate skills, educational background and lack of access to enabling resources mean certain sections of society may be excluded from benefiting fully from digital technology. Those who have been benefiting most from the technology are digitally literate and can understand and manage their digital assets. In the context of estate planning, understanding what will happen to one’s digital assets on death or disability will have a positive impact on Will-makers, LPRs, and beneficiaries.

Our results, which relate to DAPL, are consistent with those of previous studies in financial literacy. Whether one knows what will happen to their digital assets on their incapacity or death is influenced by their demographic characteristics (gender, relationship status, educational level and country of residence). Furthermore, we find that those who have a Will are more likely to know what will happen to their digital assets in the event of their incapacity or death. Contrary to what we hypothesised, the greater the number of categories of digital assets owned by an individual, the less likely they are to possess DAPL. This may be because knowledge of one’s rights with a particular digital asset category may not be transferrable to other categories. For example, given the complexity of different digital asset categories, having a thorough understanding of one’s ability to transfer ownership rights of social media accounts may not be applicable to other digital asset classes such as domain names and websites. Consequently, the greater the number of different digital asset categories held, the greater the complexity and difficulty in understanding and managing the transfer ownership rights involved. Arguably, this is in line with structuration theory’s emphasis on human agents’ active participation in the emerging social structure, which suggests that individuals do not necessarily benefit from their access to or possession of a variety of digital assets; rather, it is their understanding of the nature of the digital assets and capability of managing such nature that leads to meaningful advantages. Our results indicate that having a Will as an intervention mechanism helps build this understanding and capability (i.e. DAPL), which echoes structuration theory in that social structure is both the medium and outcome of the human agent’s active participation.

7. Conclusion

This article contextualises the issue of financial literacy within the digital economy. As a growing amount of wealth is held in digital space and increasingly impacts testamentary wealth, understanding the fate of digital (and digital financial) assets on death and disability is of greater importance. We find a low level of DAPL in our dual-country study of estate planning practices as indicated by respondents’ overall lack of understanding of the fate of their digital assets on death. Structuration theory offers an explanation as to why some groups within society, whether by choice or circumstance, are excluded from the full benefits of understanding the implications of engaging with digital assets from an estate planning perspective. This has important implications for social policy indicating that financial literacy education should not just focus on effective functional use of digital assets, but also on consumer rights and risks. Furthermore, professional financial advisors should also be cognisant of not only their clients’ financial literacy but their DAPL.

Consistent with prior studies of financial literacy, we find that most of the demographic factors are positively associated with digital (and digital financial) literacy. Echoing existing studies on financial literacy education (Kaiser and Menkhoff, 2017; Kaiser et al., 2020; Lusardi, 2019; West and Mitchell, 2022), our work suggests that financial literacy educators need to place a specific focus on lifting the knowledge of females as well as those who are poorer, less educated and single. Based on the way in which relationship status was measured in this study, the results suggest that while being in a relationship is positively associated with DAPL, those in marriage are more likely to have higher levels of DAPL compared to those in a de facto relationship. Underlying reasons as to why this might be is an avenue for further research.

Based on our findings, we believe that there are multiple important avenues for investigation in future research. As both countries surveyed are first-world common law countries, future studies could consider other jurisdictions to see whether our results are generalisable across dissimilar economies and societies. Second, recent work that highlights the importance of intra-family communication in developing financial skills and literacy (Hanson and Olson, 2018) and future research could be extended in the context of digital financial skills. Third, research could consider not only what digital assets are used and how actively they are used but also the extent of wealth held in digital form. Such detail may enable the investigation of whether these factors are positively associated with greater appreciation of the risks and rights associated with digital assets. Fourth, future research can investigate the efficacy of interventional educational programmes to increase the DAPL of the population, particularly those identified to be vulnerable. Last but not least, given that our study examines perceived DAPL, that is, a participant’s self-evaluation of their DAPL, future research can investigate whether an individual’s perceived DAPL is an accurate measure of their actual DAPL. The degree of correlation between perceived and actual DAPL will have implications for policy interventions and education strategies.

Footnotes

Final transcript accepted 24 January 2023 by Philip Gray (DE Finance

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: Funding for this project was gratefully received from the Society of Trust and Estate Practitioners (STEP).