Abstract

The state has been pivotal in both facilitating financialization and dealing with its consequences, through which the state itself has also been reshaped. This paper proposes a “state selective financialization” framework to highlight the intentionality and selectivity of the state in (de)financialization. Based on practices in China, we examine the latest state efforts to reconfigure the land reserve system in order to cope with local financial risks associated with land-backed borrowing. The state de-leverages reserved land locally and uses it to secure bonds through a state-managed top-down process. The changing mechanism demonstrates the central state’s intentional role in selecting financial instruments and recentralizing its control over land financialization, whereby it has tried to mitigate financial risks and oversee local development. Instead of financialization versus de-financialization, we find financialization in China is a selective governance tactic to address state concerns. Moreover, rather than seeing financialization as a process outside the state, this research emphasizes that selective financialization is an internal process to reconsolidate the power of the central state and rebuild alignment among multi-scalar state actors.

Introduction

The state has been essential to understanding how financialization unfolds in the urban world (Aalbers, 2017, 2023; Belotti and Arbaci, 2021; Bernt et al., 2017). In the aftermath of the global financial crisis, some states laid the foundations for financialization by deregulating financial activities to deal with systemic austerities (Christophers, 2019; Guironnet et al., 2016). Meanwhile, some states not only facilitated financialization but were also proactively involved by acting directly in the process (Belotti and Arbaci, 2021; He et al., 2020; Yeşilbağ, 2020). No matter whether the state leads or enables financialization, the process of financialization has led to severe financial risks and social contradictions (Ashton et al., 2016). Dealing with financial risks and other consequences of financialization, scholars suggest that the state is an important actor in proposing “de-financialization” to combat financial penetration (Karwowski, 2019; Wijburg, 2021). Either promoting or halting financialization, most studies have seen financialization as a process external to the state. Recently, several studies have turned to the financialization of the state itself (Dagdeviren and Karwowski, 2022; Karwowski, 2019; Pike et al., 2019). Nevertheless, they have overlooked the tension within the state in dealing with financialization.

This research puts forward an alternative framework for analyzing the relationship between the state and financialization by seeing (de-)financialization as an integral part of the (multi-scalar) state itself. We propose an agenda of “state selective financialization,” which means that a specific financial process (deployment of a specific financial instrument, agency, intermediary, and technique) has been deliberately chosen, enabled or disabled by the state. It aims to unpack how the multi-scalar state shapes and has been reshaped by a specific form of (de-)financialization. From this perspective, we move beyond the debate on state-enabled financialization or de-financialization but concentrate on why and how a specific form of financial expansion is proposed, implemented, and even replaced associated with state strategies and the implications for the state itself. Hence, state selective financialization focuses on (1) the state intentionality underlying the selection of a specific form of financialization; (2) the institutional reconfigurations and other procedures through which the selective process is enabled; (3) state power reshuffling as a consequence of selective financialization.

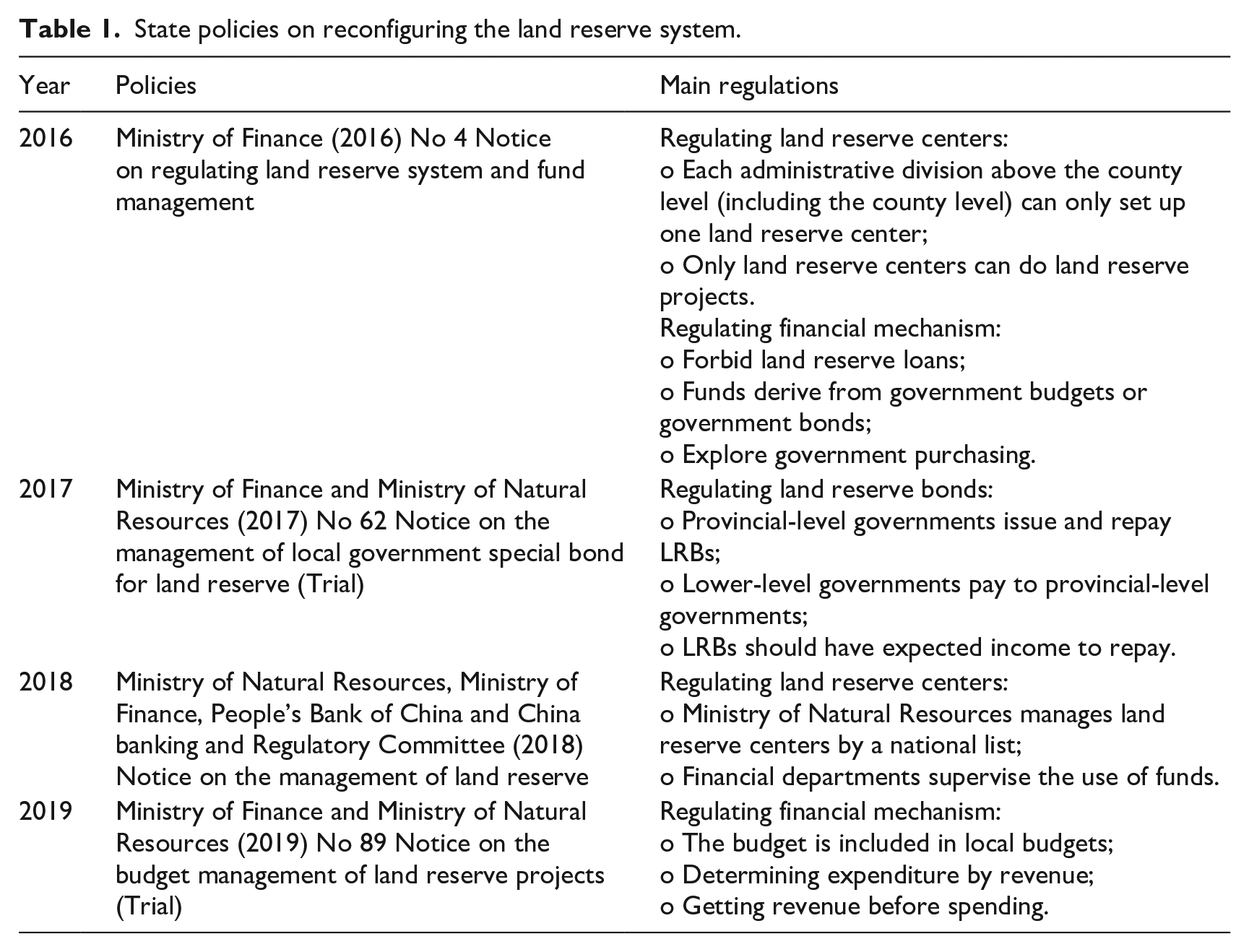

Empirically, we study the latest state efforts to reconfigure China’s land reserve system (tudi chubei zhidu) and investigate how a specific form of land financialization has been initiated and implemented. First, we contextualize the Chinese state’s attempt to redesign the land reserve system in combating financial risks associated with local government borrowing. Dealing with the recession due to the financial crisis, Chinese state enacted a four-trillion Yuan stimulus plan to stimulate the economy from 2008 to 2010. This plan was mainly implemented by local governments through their affiliated agencies, especially urban development and investment corporations (UDICs, chengtou in Chinese) (Bai et al., 2016; Feng et al., 2022). Consequently, chengtou accumulated massive liabilities during the stimulus period. To deal with the debt, they issued corporate bonds and turned to shadow banking for refinance between 2012 and 2015 (Chen et al., 2020). Because of financial expansion from 2008 to 2015, the local debt issue has been looming. Coping with the local debt issue, the central state has enacted a series of re-regulations and developed local government bonds (LGBs) since 2014 (Li et al., 2023a). This research is situated in the context of regulating financialization and focuses on the top-down reconfiguration of the land reserve system since 2016.

Land financialization means that land has been mobilized as a type of valuable asset to channel funds for development (Wu, 2022). Land reserve system is the pillar of land financialization in China because land reserve projects produce reserved land (chubei di), which can be used to accrue funds or leverage funds (Huang and Chan, 2018; Lin, 2014; Wu, 2022). For instance, trading reserved land in the primary land market contributes to the fiscal revenue of local states (Lin, 2014; Tsui, 2011; Yeh and Wu, 1996). Besides this, there have been various forms of land-backed borrowing, such as land mortgages, chengtou bonds, and shadow banking (Chen et al., 2020; Wu, 2022). Land financialization has intensified in the aftermath of the stimulus package in China.

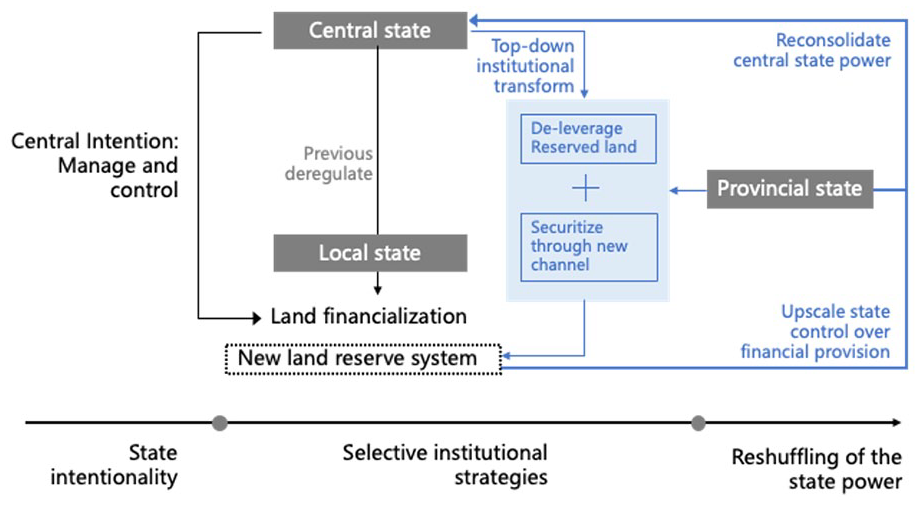

Dealing with the rampant local debt issue associated with land-backed borrowing, the central state has initiated a top-down institutional reform to regulate the land reserve system to mitigate and control financial risks since 2016. Through studying the institutional reconfigurations, we find two seemingly contradictory processes led by the central state: the prohibition of collateralizing reserved land (chubei di) and the introduction of state-controlled land reserve bonds (LRBs). That is, the state attempts to both de-leverage reserved land and uses it to secure bonds through a state-managed process. Beyond state-led financialization or de-financialization, we find that the state redesigns the financial mechanism to control the pace of financialization and strives to manage financial risks.

In addition, we find the reshuffling of state power together with institutional reconfigurations. First, the central state manipulates selective financialization to reconsolidate its power over financial provision. Meanwhile, it should be noted that the newly adopted financial mechanism empowers provincial governments while disempowering local agencies such as chengtou in land financialization. Together with the selective financial mechanism, new power dynamics on land financialization unfold.

This paper is organized as follows. The next section will review the literature focusing on the state’s role in financialization and proposes “state selective financialization” as a framework. It will be followed by reviewing the role of the state in China and studies on land financialization. The methodology section will illustrate our methods and data sources. The analysis relies on data retrieved from semi-structured interviews mainly conducted in Shanghai and available open data. For empirical studies, we will first investigate the transformation of the land reserve system against the background of local financial risks. Then we illustrate how the state reconfigures the financing process of land development in two aspects: the administration of government agencies and the management of the financing mechanism. Finally, the features of state selective financialization will be discussed. The conclusion section will discuss all the findings.

The relationship between the state and financialization

This research focuses on the relationship between the state and financialization (Belotti and Arbaci, 2021; Gotham, 2016; He et al., 2020; Karwowski, 2019; Wijburg, 2019). A precondition for financial expansion in urban areas is a “state willing to finance and guarantee long-term, large-scale projects” in the built environment (Harvey, 1978: 107). In the aftermath of the global financial crisis, the enabling role of the state in urban financialization has been noticed as an approach to crisis management (Christophers, 2019; Lapavitsas and Powell, 2013). In particular, local governments are at the receiving end of the global financial market, systemic financial shortage, and local demand (Birch and Siemiatycki, 2016; Peck, 2017). Responding to fiscal stress, local practices vary (Davidson and Ward, 2022). Municipalities in the US are practicing “pragmatic municipalism” to deliver public goods rather than being shifted to austerity (Kim and Warner, 2016). In some cases, previous entrepreneurial practices have been amplified to achieve development goals (Beswick and Penny, 2018; Dagdeviren and Karwowski, 2022). Local governments have resorted to financial instruments, channels, and products in many fields, such as housing, infrastructure, and urban development projects (Ashton et al., 2016; Belotti and Arbaci, 2021). In contrast to seeing a relatively unintentional role of the state (Bernt et al., 2017), scholars argue that financialization is a deliberate state policy (Ashton et al., 2016). For example, Wijburg (2019) focuses on “the national state in regulating the private flow of finance capital” in France (p. 210). More proactively, scholars have evidenced state-led financialization (Yrigoy, 2018). In the financialization of social rented housing in Italy, the interplay of different layers of the state has played a leading role, particularly in regional-level governments (Belotti and Arbaci, 2021).

Besides state-led or state-enabled financialization, the state is also central in dealing with and protecting itself against adverse effects of financialization through de-financialization (Ban and Bohle, 2021; Karwowski, 2019). For instance, Ban and Bohle (2021) analyze de-financialization featuring financial repression and domestic control in three countries in East-Central Europe. Although these states all pursue policies of de-financialization, the results vary because of the varieties of state-finance relationships, state capacity, and supra-national constraints. Their attempt to understand ongoing state responses toward financialization also demonstrates that financialization is not an inexorable process (Christophers, 2015).

The prevailing understanding of state-financialization relationship regards financialization as an external process. They focus on how the state mobilizes financialization or remedy its adverse effects. However, the distinction between the state’s enabling (or regulatory) role in financialization and financialization within the state itself should be noticed. The former regards financialization as an external process to state, while the latter emphasizes the “financialization of states’ own activities” (Dagdeviren and Karwowski, 2022: 689). Second, the tension within the state and the transformation of the state itself along with financialization has been insufficiently addressed. For instance, Aalbers (2017) argues that “the state filters the financialization process while financialization at the same time furthers the transformation of the state itself” (p. 550). Even though the state deliberately chooses a specific pathway of (de-)financialization, it transforms itself during the process (Ban and Bohle, 2021; Dagdeviren and Karwowski, 2022). For example, Fastenrath et al. (2017) interpret resorting to the financial market as a governance mechanism and the embeddedness of financial logic as two interrelated processes through which state-led financialization has been reshaped to align with the financial market.

Instead of emphasizing the prevalence of financialization or highlighting the role of financial investors, we propose a framework called “state selective financialization.” It is a state-centric perspective to unpack how the (multi-scalar) state shapes and has been reshaped by a specific form of (de-)financialization. First, this framework highlights the intentionality of the state (in various scales) when dealing with financialization (Belotti and Arbaci, 2021; Wijburg, 2019). Even the most passive role of the state in financialization demonstrates strategic selectivity—opening a specific area or agenda for financial activities (Jessop, 2007). More importantly, selectivity normalizes the recurrency of financial (de)regulations (Ashton et al., 2016; Gotham, 2016). Second, we pay attention to how the state intervenes in forming a specific process of financialization, usually through institutional transformations, policies, and governance innovations (Smyth, 2019; Weber, 2021). Third, this framework investigates how the (multi-scalar) state is reshaped by financialization. Existing studies have shown how the state is penetrated by the financial market and financial rules, suggesting that the external financial market exerts pressure on the state (Beswick and Penny, 2018; Guironnet et al., 2016). Our study shows how the financialization leads to tensions within the state at various scales and the restructuring of the state itself along with the state selective financialization.

The Chinese state and state selective financialization

This research is not only situated in the global debate on financialization, but also in the political economic system of China. Zheng and Huang (2018) use “market in state” to indicate the defining feature of the political economic system in China, where “a substantial part of the market and market mechanisms is firmly embedded and confined within institutional mechanisms of the state” (p. 126). Unlike its Western counterparts, the Chinese state does not operate in the market rules; instead, it has set the rules for the market (albeit with changes) and even operates as the market actor. In urban studies, Wu (2018) uses “state entrepreneurialism” to combine two features in urban governance in China: planning centrality and market instruments. The state deliberately adopts market instruments to achieve its own goals. In doing so, “rather than being replaced by market power, state power is reinforced by its use of market instruments” (p. 1396). The domination of the state in the state-market relationship is also a key feature of understanding financialization in China.

Albeit with state dominance, the state does not remain unchanged. The market can also influence the state, leading to a mutual transformation of the state and the market and rebuilding the state dominance (Zheng and Huang, 2018). First, the state is not a static ensemble but embodies internal tensions and changes, as shown in the central-local relationship in China. The central and local governments “have combined in a paradoxical way a high degree of centralization with much decentralization” (Huang, 2012: 593). Centralization means that the central state has great authority in bureaucratic management, while decentralization is reflected by local excessive attempts to promote economic development (Huang, 2012; Wu, 2018; Yang and Wang, 2008). Second, the transformation of the state is usually due to the interaction between the state and the market. Zheng and Huang (2018) use the “middle ground” to identify the interface where the state meets the market. The middle-ground effect means that the market logics penetrate the state itself, causing problems between the central state and local governments, and between the state and its agencies. Compared to controlling bottom-up market development, the state faces a more challenging task in dealing with “marketization from within the state” (Zheng and Huang, 2018: 297). Given the tension within the state and between the state and the market, the state is in a dynamic transformation to both maintain its dominance, deal with intrastate tensions, and implement its political agenda.

In recent studies on financialization, scholars have emphasized the role of the state in steering financialization in China (He et al., 2020; Liu and Dixon, 2022; Pan et al., 2021). Financialization does not lead to state retreat. Instead, financialization demonstrates the extension of the power of the state to achieve its own purposes (Pan et al., 2021; Wu, 2020, 2023). For instance, China’s state-led infrastructural financialization is designed to support production-based growth and consumption-based development (Liu and Dixon, 2022; Theurillat and Graezer Bideau, 2022). Petry (2020) also argues that financialization facilitates “the authorities’ ability to control markets and direct their outcomes towards state policies” (p. 213). Unlike many studies seeing financialization as an overwhelming trend, financialization in China has been understood as a means used by the state to fulfill its own goals (He et al., 2020; Liu and Dixon, 2022; Pan et al., 2021; Wu, 2020).

However, the Chinese state is a complicated ensemble with tensions within hierarchical governments and agencies. “State-led financialization” has obscured the internal tension within the state and dynamic adjustments between the state and the financial market. For instance, in the post-stimulus era, local governments have extensively intersected with the financial market through their agencies and accumulated enormous local debt. Even though the stimulus plan (2008–2009) could be interpreted as “state-led financialization” in terms of the central government’s deliberate strategy to deregulate local government borrowing, the central government has not continuously supported or led financialization after that. Instead, the central state was prudent in dealing with local debt from 2008 to 2014. Although the central government realized the financial risks in 2010 and enacted several tentative policies to control, local debt still surged (Bai et al., 2016; Chen et al., 2020). This is also a reification of the “middle ground” effect as the financial market penetrates local states, causing tensions between central and local governments (Zheng and Huang, 2018). Until 2014, a debt-bond swap plan and local government bonds have been implemented, and the central intention of mitigating financial risks has become pronounced. The multi-scalar relationship within the state is pivotal in understanding “selective financialization” instead of a simplified state-led one.

Land reserve system and land financialization in China

Although many studies have discussed land financialization in China (Lin, 2014; Theurillat et al., 2016; Wu, 2022), the understanding of the land reserve system has been largely simplified. Land reserve projects mean “practices including acquiring land with legal permits, conducting primary land development and holding land for land supply” (Ministry of Land and Resources et al., 2018). Land reserve projects lay the foundation for land financialization by producing reserved land, which can become a tradable commodity or mortgage. Land reserve projects have four steps, including land acquisition, the primary development of land (or site preparation), land holding, and land disposition (Huang and Chan, 2018). Generally, local governments expropriate land from farmers whose land is owned by their collectives. At this stage, local governments collect raw land that is not permitted for selling. Landless farmers usually get lower compensation according to the agricultural uses (Cao et al., 2008; Zheng et al., 2014). Local governments then conduct primary development to change raw land to serviced land. After that, the serviced land is held by the land reserve authorities as reserved land until there is a plan for land transactions. Finally, reserved land can be transferred to developers with a bidding price. Besides, land reserve projects may also include urban demolition and urban land acquisition to prepare urban land for future transactions (cf. Shin, 2016). Some scholars regard land reserve projects as “land banking,” echoing practices in other countries, for example, the Netherlands. Yet they are different. Land banking in the Netherlands has expanded to reap land appreciation based on cooperation between municipalities and developers. The developer and the municipality can share the land appreciation (Van Loon et al., 2019). However, in China, the state exclusively owns all the urban land. Developers cannot share profits from the land sales income with local governments.

The basic understanding of land financialization in China is land finance (tudi caizheng), which means that reserved land is traded as a commodity in the land market whereby the state (especially the local state) receives desirable land conveyance fees (Ho, 2001; Huang et al., 2015; Lin et al., 2015; Yeh and Wu, 1996). In addition to land leasing, local states leverage future income from reserved land to borrow from the financial market (Theurillat et al., 2016; Wu, 2022). Local states were not allowed to borrow externally before 2014, so they used affiliated agencies to borrow. Two typical examples were land reserve loans and chengtou debts (including chengtou bonds and shadow banking). Land reserve loans were a specific type of loan that land reserve authorities could borrow from banks based on reserved land (Huang and Chan, 2018). Previously, although land reserve authorities could receive funds from local financial departments, they relied heavily on land reserve loans to invest in land reserve projects. Another type of land-backed borrowing was through chengtou. Chengtou are state-owned enterprises owned by local states to conduct land development projects and infrastructure (Jiang and Waley, 2020; Pan et al., 2017). Scholars believe that as local governments could transfer their ownership of state-owned land to chengtou, chengtou managed to use land as collateral to secure funding from various channels, such as banks, shadow banking (trust products), and bonds (Bai et al., 2016; Chen et al., 2020; Liao, 2014; Tsui, 2011; Wu, 2022). With the funds collected from land conveyance fees and land-based borrowing, local governments have invested in land development and infrastructure projects (Lin, 2014; Ong, 2014).

In previous studies, land financialization has been characterized by decentralization, featuring local entrepreneurial-like endeavors based on land to achieve political and economic goals (Hsing, 2010; Lin, 2014; Wu, 2018). First, to deal with the fiscal mismatch caused by the tax-sharing system, land-leasing became a vital channel to supplement local revenue (Lin, 2014; Tao et al., 2010). Second, in China, due to the fierce competition among cities and the cadre promotion system based on GDP, local governments promoted urban and infrastructure development. As city entrepreneurs, local governments used land conveyance fees to invest in urban infrastructure and attract investors (Theurillat et al., 2016; Yang and Wang, 2008). Apart from land sales income, local states also helped chengtou borrow and conduct local development projects to boost the local development (Ong, 2014; Pan et al., 2017). Based on the practices, local states not only capture land rents but also build their power (Hsing, 2010; Lin et al., 2015). In 2008, the central state initiated a four-trillion-yuan stimulus plan to invest in the built environment to stimulate the economy. This plan was implemented through the local land-based development model. Hence, endorsed by the central state, land financialization featuring decentralization was intensified (Ambrose et al., 2015; Wu, 2022).

Land financialization, especially land-based borrowing, led to over-borrowing and caused severe local debt problems in the post global financial crisis era (Pan et al., 2017; Wu, 2022). For instance, land reserve authorities were even able to use a zoning map to get funds (Theurillat et al., 2016). Banks regard expected land revenue as a secure source for repayment (Huang and Chan, 2018). Therefore, the issue of over-borrowing was pervasive (Huang and Chan, 2018; Theurillat et al., 2016). Besides, land-based borrowing via chengtou led to massive contingent liabilities of local governments (Bai et al., 2016; Liao, 2014). Therefore, the central state has regulated the financing mechanism of land reserve projects and halted debts collateralized on reserved land. These regulations have significant impacts on the land reserve system and land financialization, which have been hardly noticed. To fill the research gap, this paper aims to examine land reserve system in contemporary China.

Methodology

We aim to investigate the role of (multi-scalar) state in the current land reserve system to demonstrate how the central state initiates a specific form of land financialization through institutional transformations and its consequences (Figure 1). Based on the framework of state selective financialization, we first highlight the intentionality of the central state in dealing with local financial risks and reconsolidating its power. Second, we analyze the top-down institutional transformations and local outcomes in two aspects. The first approach is that the central state authorizes land reserve centers as public institutes responsible for land reserve projects. Here Shanghai is used for illustration rather than a particular case study. Moreover, the central state has prohibited any external financing mechanism and introduced a financial instrument called LRB. Using LRB to replace previous land-backed loans, the central state selectively rearranges the financing mechanism in order to manage financial risks. In the meantime, we discuss the implications for multi-scalar state actors and the changing financial mechanism.

Understanding state selective financialization in China based on the reconfiguration of land reserve system.

This research is based on desk research and semi-structured interviews. We first analyze policy documents from a historical political economic perspective to position the regulations in 2016. To examine the latest operations in land reserve projects, we mainly use Shanghai LRC and practices in Shanghai for illustration. The analysis is dependent on 22 semi-structured interviews with government officials (including two interviewees from Shanghai LRC), managers from three chengtou in Shanghai conducting primary land development, and scholars in urban studies. Interviews were conducted from 2019 to 2021. In addition, open data for LRBs are also used to examine bond issuance and repayment.

Transforming the land reserve system to cope with local government financial risks

The land reserve system was set up in the 1990s. The demand for urban land soared during that period, along with establishing the land market. Nevertheless, “developers could not even develop the land they bought because basic preparation including land demolition was not finished” (Interviewee 6, official of Shanghai LRC, 2019). To deal with the problem, Shanghai established the first LRC in China in 1996, called Shanghai Land Development Center (Shanghai tudi fazhan zhongxin). To meet the increasing demand for prepared land, the State Council encouraged local governments to introduce a land reserve system in 2001. The basic role of LRCs was to prepare state-owned land for sale and hold it for future development. In 2007, LRCs were authorized to oversee land reserve projects on behalf of local governments. At this stage, however, LRCs had many forms and were not directly managed by the state.

In some cities, to facilitate land reserve projects, the function of LRCs was incorporated into specific corporations. For instance, the LRC for Shanghai municipality was incorporated into Shanghai Land Group (a chengtou). In this case, the enterprise and government functions were integrated. In practice, LRCs did not usually conduct expropriation or primary land development themselves. Instead, these projects were undertaken by relevant project companies, mostly chengtou. Consequently, the role of LRCs was marginal. For financial sources, LRCs could use allocated funds as well as “land reserve loans.” Nevertheless, not only LRCs but also chengtou that conducted land reserve projects could secure funding based on land reserve projects. Therefore, implicit borrowing against reserved land was pervasive.

In the post-crisis era associated with the stimulus plan, local borrowing against land has expanded. The four-trillion-yuan stimulus plan aimed to invest mostly in urban infrastructure, while local governments were responsible for seeking matching funds. Local governments were not allowed to borrow externally before 2014. Therefore, they relied on other agencies, such as LRCs and chengtou, to borrow from the financial market. These entities would obtain loans from banks based on reserved land or the implicit ownership of state-owned land (Liao, 2014). Hence, chengtou borrowing led to massive liabilities that generated financial risks for local states (Pan et al., 2017; Wu, 2022). Local states resorted to land sales to repay contingent local debts. Restricted by the central government policy on preserving agricultural land and land development quotas, the local government managed to control supply and land prices to maximize land income. Land financialization, including land sales and land-based borrowing, has increased land prices and led to looming local financial risks.

Coping with local financial risks, the central state aims to tighten its control over local land-based borrowing. As summarized in Table 1, the central state has enacted two main strategies: empowering land reserve centers and tightly managing their financial sources. First, since 2016, LRCs have become specific public institutes responsible only for land reserve projects but not for financing land development. Institutionally, LRCs are public institutes for public welfare (gongyi lei shiye danwei). Local governments (above county level) should establish their LRCs affiliated with local departments of natural resources. Managing land reserve projects is the only task of LRCs, and only LRCs can manage land reserve projects (Table 1). This stipulation excludes any development agencies like chengtou. LRCs that were incorporated in chengtou should be detached from chengtou. The rationale is to separate the local government and chengtou and hence to prohibit chengtou from borrowing for the local government and thus control local government debts. Chengtou are required to detach from local governments, meaning they should become financially independent entities rather than relying on local governments for repayment.

State policies on reconfiguring the land reserve system.

The second set of regulations is about the financial management of LRCs (Table 1). In the new land reserve system, all the financial sources of LRCs should be allocated from local financial departments, which are fully controlled by the central state. LRCs should only rely on local revenue and LRB, and land reserve loans are prohibited. Effectively, LRCs are insulated from the financial market. We will explain the impacts of these two strategies respectively in the following sections.

Detaching local governments from accessing the financial market, converting LRCs into government agencies

The fundamental regulation is the management of LRCs, whereby local governments and their affiliated chengtou have been insulated from using reserved land to borrow. LRCs used to have various forms and were active in the financial market. However, the state has stipulated that the status of LRCs is exclusively public institutes. More importantly, LRCs are not allowed to borrow themselves. To inquire about the outcome of these regulations, we investigate the operations of Shanghai LRC.

In Shanghai, the municipal-level LRC used to be an enterprise. 1 “Before 2016, the Shanghai LRC and Shanghai Land Group shared the same group with two titles (yitao banzi liangkuai paizi). In that circumstance, government and enterprise were integrated.” (Interviewee 5, official of Shanghai LRC, 2019) Although Shanghai LRC was the management body of all the land reserve projects in Shanghai, district-level LRCs, chengtou, and administrative committees for industrial zones could also conduct land reserve projects. In 2016, according to the central regulations on land reserve, Shanghai Land Group as an enterprise should not be an authorized LRC. Therefore, Shanghai Municipality separated Shanghai LRC from Shanghai Land Group in 2016. Since then, Shanghai LRC has been a public institute affiliated with the local Bureau of Land and Resources. It has become the exclusively legal authority for land reserves for Shanghai Municipality since 2016.

According to the national list of LRCs released by the Ministry of Natural Resources in 2020, there are 2484 LRCs in China. These LRCs are all public institutes affiliated with a local bureau of natural resources. Hence, the management bodies of land reserve projects have been thoroughly reconfigured nationwide. However, LRCs do not conduct land expropriation or primary land development themselves. These projects are conducted by “contractors through bidding in principle” (Interviewee 13, governmental official, 2020). In practice, many local governments still choose their reliable partners to conduct land reserve projects as operating institutes. In Shanghai, for example, Shanghai Land Group still undertakes land reserve projects in the name of “functional development” (gongnengxing kaifa). However, its financial operation has changed because Shanghai Land Group could not leverage reserved land to get loans for land reserve projects. Instead, the Shanghai government allocates money within the fiscal scale to Shanghai Land Group to cover the cost of land reserve projects.

As Shanghai Land Group has worked with the Shanghai LRC to conduct municipal-level land reserve projects, most projects are about urban renewal in built-up areas. In suburban areas, various chengtou used to be responsible for primary land development in a designated zone. For example, the Lingang Group was responsible for primary land development in the Lingang area, and the Zhangjiang Group was responsible for land reserve projects in Zhangjiang High Tech Park. After the regulations, chengtou have also been widely involved in land reserve projects in suburban development only as operating institutes. A manager of chengtou in Shanghai explained: Actually, I (chengtou) still work for the government before or after the regulations. The only difference is that I covered all the costs and received all the benefits in the past. Besides necessary expenses, the government also gave me (chengtou) the rest. Profits and losses were in my own hands. OK, for now, chengtou do not have to pay for the cost, and the income is also none of your (chengtou’s) business. The government just pays for labor costs. How much is the profit rate for us? A few thousandths. (Interviewee 11, chengtou manager, 2020)

Based on the explanation, local governments still use chengtou to conduct land reserve projects under the new land reserve system. However, the financial mechanism has changed. Previously, chengtou themselves sought funds for land reserve projects, and they received a large part of land conveyance fees. For now, although they still do land reserve projects with funding allocated by the government, they cannot share the benefits—land conveyance fees.

Therefore, the state has successfully retained financial control over land reserve projects without hampering project delivery. First, as chengtou are not eligible to be LRCs and cannot collateralize reserved land, implicit land-based borrowing has been avoided. These practices also contrast with the literature where land financialization means chengtou using allocated land as a financial asset (cf. Liao, 2014; Tsui, 2011). Second, land reserve projects can only be conducted with sufficient funds. Even though chengtou are still operating institutes, they do not shoulder financing responsibilities. Only LRCs are empowered to make local plans, subject to budgetary constraints. We will discuss financial management later. In sum, through the empowerment of LRCs as state agencies and the disempowerment of chengtou in land reserve projects, the state de-leverages reserved land at the local level to mitigate financial risks.

However, chengtou are not insulated from the financial market and can issue their corporate bonds. Chengtou have still accumulated liabilities after all the state restrictions on local debt (variations in different areas) (Feng et al., 2022). They can transform themselves to access funds. For example, several corporations under the same local government can group together to form a chengtou group in order to enlarge the asset level. With more assets, chengtou can still borrow with less reliance on land. Besides, although chengtou are not allowed to use state-owned land as assets for financing, they strive to find other forms of funding such as corporate bonds and shadow banking products (Chen et al., 2020).

Centralizing the financial control by redesigning the financial mechanism of land reserve projects

This section focuses on the financial institutions of land reserve projects. Since 2016, the financial sources of LRCs have been derived from local revenue and LRBs, and both funds should be incorporated into local fiscal budgets. We discuss the operations of LRCs under the new regulations.

Integrating the financial operation of LRCs into the local fiscal system

LRCs are authorized to compile local plans for land reserve projects under budget limits. Two main financial management strategies include separating income from expenditure (shouzhi liangtiao xian) and determining expenditure by income (yishou dingzhi).

First, separating income from expenditure means that the income and expenditure of land reserve projects are separately calculated and monitored by local financial departments. This discipline was enacted in 2007 and aimed to manage land revenue in local budgets and restrain local incentives to sell land. However, local governments had other channels to raise funds for land reserve projects, such as funds self-raised by chengtou. These funds were not monitored by local financial departments. Since 2016, however, local financial departments have managed all funds for land reserve projects and land conveyance fees from the land market. This practice prevents shadow banking or contingent liabilities related to reserved land. For Shanghai LRC, the costs for land reserve projects have increased to an extreme level. “The investment in the early stage of land development is huge. We (Shanghai LRC) are the department with the largest financial expenditure. Meanwhile, our (Shanghai LRC’s) income is the largest for the Municipality.” (Interviewee 6, official of Shanghai LRC, 2019). Meanwhile, the financial sources of land reserve projects have been limited to fiscal revenue and special bond. “Since there are limited sources, local governments become more careful about plans for land reserve projects.” (Interviewee 13, governmental official, 2020)

Moreover, in 2019, the state stipulated that LRCs should compile plans for land reserve projects based on their expected income. That is, “you (Shanghai LRC) first calculate how much land conveyance fees you (Shanghai LRC) will receive, through which you (Shanghai LRC) decide the amount of investment” (Interviewee 5, official of Shanghai LRC, 2019). On the one hand, this tactic limits the local impetus to develop too many land parcels in case their investment exceeds the land sales income limit. On the other hand, local governments must invest in land reserve projects based on their gains. As noticed by an official of Shanghai LRC, this management tool is profound because “from the perspective of input and output, I (Shanghai LRC) do not have motivations to do land reserve projects to make money” (Interviewee 6, official of Shanghai LRC, 2019). The Shanghai LRC continues to invest in land reserve projects not to earn direct profits but to “keep the engine running” (Interviewee 6, official of Shanghai LRC, 2019). That is, in Shanghai, the main contribution of land reserve projects has shifted from direct fiscal contribution to steady investment, whereby various industries related to land development can be stimulated, and the local economy can be promoted. This management tactic also demonstrates the dual objectives of the state, both to manage financial risks and to maintain investment in land.

Upscaling the central power through the introduction and management of LRBs

Far from simply de-leveraging reserved land, the central state introduced a new land-backed financial instrument called LRB to control land financialization. LRB is designed to be backed by local land income. It is also a type of local government bond (Li et al., 2023b). Unlike previous land borrowing supported by local governments, the management of LRB is upscaled to provincial governments and the central state.

The LRB is managed by a quota approval system. First, LRCs (county-level and beyond) compile local plans for land reserve projects for the next year, including projects as well as financial demand. These plans are sent to local finance departments and natural resources departments. After that, local financial departments file the demand with their provincial governments. Then, provincial governments submit their financial demands to the Ministry of Finance (MOF). Based on the demand and the expected income from land conveyance fees, the MOF finally determines the quota of LRBs for the next year and distributes quotas to all provinces. Given the national plan, provincial governments prepare distribution plans for municipalities and counties. Provincial governments are in charge of issuing and repaying LRBs on behalf of all the local governments within a province. That is, the state strictly controls and manages the issuance of LRBs through a top-down bureaucratic system. The provincial government is responsible for the repayment of LRBs, reflecting the separation between land reserve projects and financial operations. In this process, the provincial government is less directly associated with the growth impetus and hence should, in theory, be more financially prudent.

The LRB is a project-based local government bond or called special local government bond (zhuanxiang zhai). As the LRB is managed through a top-down quota system, the MOF determines the total amount as well as the distribution of LRBs. Moreover, the MOF manages LRBs to align with the strategic development goals of the central state. It facilitates the issuance of LRBs to promote local land reserve projects and limits issuance to restrict land development. For instance, with the endorsement of the central state, the issuance of LRBs was generally stable from 2017 to 2019. It reached 0.68 trillion yuan in 2019, comprising around 26% of special local government bonds issuance. However, in 2020, the MOF stopped the issuance of LRBs because the central state aimed to encourage more investment in infrastructure projects. In 2021, the issuance of LRB was generally prohibited except for land reserve projects for rental housing. In this sense, the LRB has become a strategic instrument to achieve the state goal of promoting rental housing. To sum up, the LRB operates following a quota system whereby the central state can guide the usage of LRBs to comply with state goals.

As LRB is a project-based bond, bond issuance may be backed by self-balancing land reserve projects. However, we find that the LRB is actually backed by the credit of provincial governments and even the central state. That is because LRBs are issued and repaid by provincial governments, while provincial governments do not usually undertake land reserve projects. Hence, the bond issuer is not the direct manager of the projects. This separation strengthens state monitoring from upper-level governments. Moreover, as long as the issuance of LRBs is within the limit authorized by the MOF, credit rating agencies evaluate them as safe. However, no province can issue LRBs exceeding the amount allocated by the central state. Therefore, all LRBs have top ratings, regardless of issuers or projects. That is, LRBs are guaranteed by the credit of the state as a whole rather than by the profitability of a single project.

This mechanism of the LRB is in contrast with project-based financial instruments such as tax incremental financing (TIF) in the USA. Based on TIF in Chicago, Weber (2010) argues that the municipality is betting on the future appreciation of property and land in a small area, which entails risks. In contrast, the repayment of LRBs is not directly related to the benefits of targeted projects. LRBs are issued and repaid by provincial-level governments. In doing so, local governments confront less pressure imposed by the financial market in terms of debt repayment. Moreover, the central state demonstrates absolute control over the financial sources of land reserves based on the approval system. Strict managerial tactics are deployed to prevent financial risks and deliver central concerns. This system now helps the overall management of land financialization. Moreover, it reduces the possible leverage of the financial market on local governments by which financial premiums and bond holders’ values might dictate urban land development (cf. Peck and Whiteside, 2016).

State selective financialization to rebuild state centrality

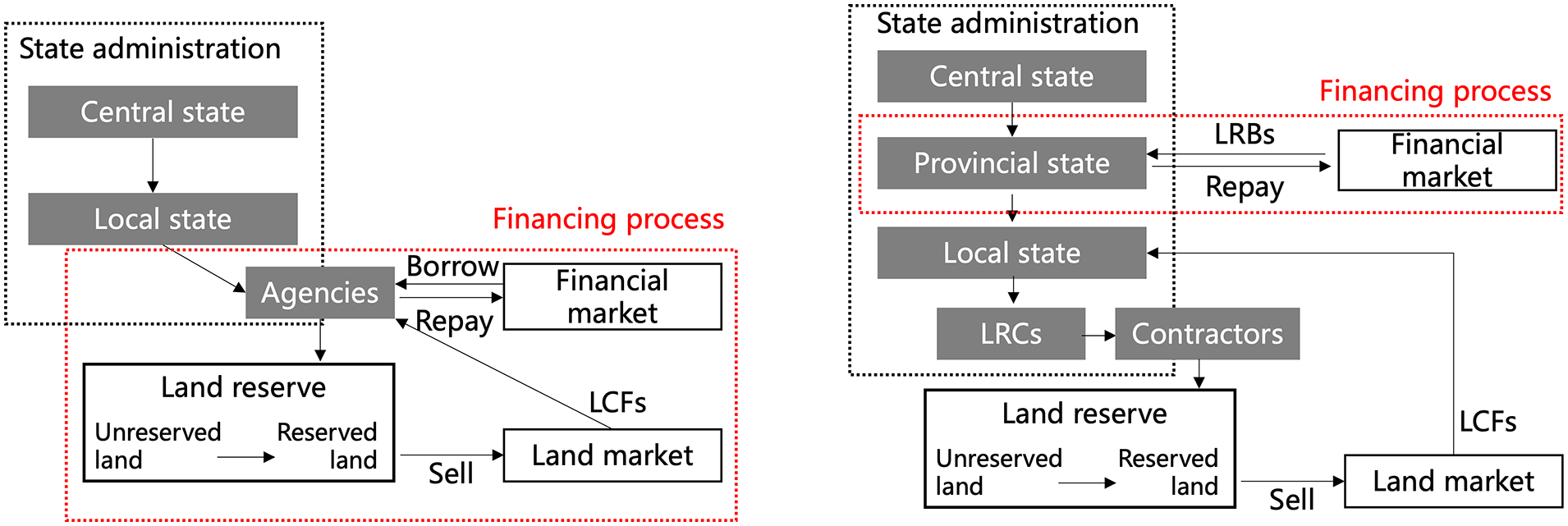

This section summarizes the features of the transformation of the land reserve system and illustrates how the central state manipulates top-down institutional reconfigurations to rebuild centrality (Figure 2).

The shift of land reserve system (pre-2016: left, post-2016: right).

The whole institutional design aims to upscale the financing process of land reserve projects from local governments to provincial-level governments, which is eventually under central control. In doing so, local land-backed borrowing is overseen by the top-down bureaucratic system, and the state centrality is rebuilt. Previously, local governments could use their agencies to borrow extensively from the financial market, leading to local government debt. Using cheap credit enhanced by land, local governments could quickly get funds to stimulate local growth. The central state realizes that financial risks are associated with local growth incentives. Therefore, it “restrains local impetus for development by controlling the financial channels of LRCs” (Interviewee 13, government official, 2020). Because of the repositioning of LRCs as public institutes, they are not simply profit-oriented and are entirely under the administration of the state. Moreover, the evaluation of LRCs is not based on the amount of land revenue but on the “comprehensive benefits of urban development such as industrial upgrading” (Interviewee 5, official of Shanghai LRC, 2019). Meanwhile, the state does not suppress investment in land reserve projects, which lay the foundation for land finance and urban development. The state requires local governments to continuously conduct land reserve projects based on their expected land income. In a sense, the state is finding a balance between entrepreneurial growth and controlling financial risks. Through the management of LRCs, the central state ensures that the whole state apparatus is aligned with it.

Managing financial risks does not necessarily mean de-financialization. Instead, the state deliberately selects conduits for land financialization to control it. To insulate the local (municipal) government from borrowing through land, LRB, as a form of local government debt is hosted in order to be contained. In doing so, the state internalizes the land reserve system’s financialization process into the state’s administration (Figure 2). To raise money for land reserve projects, provincial-level governments are empowered to issue and repay LRBs on behalf of local governments. The state manages the issuance of LRBs through a quota approval system.

This brings in our second point: such a quota system has been widely used in the centrally planned economy rather than a deregulated financial system. The containment and annexation of financial operations has led to a more regulated financialization process. It fundamentally challenges our imagination of financial operations in the boardroom of multinational financial corporations (Peck, 2017). Moreover, this practice advances the understanding of state-led financialization. In previous studies, state-led financialization means that the state guides or orchestrates the process of financialization (Belotti and Arbaci, 2021; Pan et al., 2021; Yeşilbağ, 2020). The state may cooperate with the private sector or play a dominant role in the financialization process (Yeşilbağ, 2020; Yrigoy, 2018). Nevertheless, these states do not overturn the trend of financialization, and local states or state agencies directly face pressures from the financial market (Wijburg, 2019). However, using LRBs, neither provincial governments nor local governments in China confront financial pressures themselves. Instead, the state as a whole faces the financial market through a state administration system. Most importantly, the state aims to set the pace for the financialization process according to its strategic goals. Therefore, it halted the issuance of LRBs in 2020 and resumed it in 2021. The management dynamic reflects the state’s capacity to filter the financialization process (Aalbers, 2017) and adjust the state structure to fit specific conditions (Christophers, 2019).

Conclusions

Based on the regulations of the land reserve system in China, we contribute to understanding the relationship between the state and financialization by providing an alternative understanding of “state selective financialization” and emphasizing that financialization is integral to state restructuring (Aalbers, 2023; Ban and Bohle, 2021; Dagdeviren and Karwowski, 2022; Whiteside, 2019). The pervasiveness of financialization is not just a means but an end itself (Birch and Siemiatycki, 2016; Karwowski, 2019; Peck and Whiteside, 2016). Financialization does not only mean the usage of financial means but also signifies the penetration of financial value and the empowerment of financial actors (Beswick and Penny, 2018; Guironnet et al., 2016; Peck and Whiteside, 2016). On the contrary, studies on financialization in China have concurred that financialization is only a means the Chinese state uses to achieve its own goals (Liu and Dixon, 2022; Pan et al., 2021; Petry, 2020; Shen et al., 2022; Wu, 2020, 2023). Although we agree that the role of the state is significant in facilitating and guiding financialization in China, “state-led financialization” has oversimplified the relationship between the state and financialization. This paper has provided a more nuanced understanding of two aspects.

First, rather than state-led financialization or de-financialization, we have identified a process of state selective financialization, which means that the state deliberately selects a specific financial means to proceed with financialization and exert its control. The specific form of financialization has been conducted through a top-down institutional reform. On the one hand, the state mitigates financial risks by de-leveraging reserved land at the local level. On the other hand, it further introduces another type of bond issued against reserved land. Albeit with implementing a financial tool, the state manages the financial instrument through managerial tactics. For example, it stops or resumes the issuance of LRBs to achieve its goals. That is, the central state controls the pace of financialization rather than just guiding the expansion of financialization. Using selective financialization as a governance tool, the state acts through the market (Wu, 2020).

Second, focusing on tensions within the multi-scalar state, we find that financialization is a process to reconsolidate the power of central state and strengthens the provincial governments as a side effect in the case of local government bonds. Current studies show that financialization triggers changing power dynamics between the state and the financial market, which implies that financialization is an external process posing a burden on the state (Ban and Bohle, 2021; Belotti and Arbaci, 2021; Bernt et al., 2017; Guironnet et al., 2016), However, we argue financialization exposes tensions within the state and is integral to state restructuring.

The central state has initiated institutional reconfigurations to deal with financial risks. These financial risks derive from excessive local borrowing, endorsed by the central state in the four-trillion-yuan stimulus plan (Bai et al., 2016; Wu, 2022). In a sense, financial risks were raised when the central state deregulated local borrowing. Now, the central state aims to control financial risks. Previous land financialization under the four-trillion-yuan stimulus plan was characterized by decentralization (promoting local government borrowing) (He et al., 2020; Pan et al., 2017), while this paper demonstrates land financialization characterized by centralization. The central state reasserts its power over state-owned land through institutional and financial management. Now, land development in China is subject to two sets of quotas: land development quotas to control the amount of land to be developed and financial quotas to ensure the limit of debt in land development. Indeed, in China, land financialization does not encroach on state power in contrast to the literature (cf. Karwowski, 2019; Peck and Whiteside, 2016). Based on changing forms of land financialization, we find that selective financialization is utilized to rebuild state centrality and alignment within the state, similar to building a “market in state” (Zheng and Huang, 2018).

This paper also contributes to the knowledge of land financialization in China by illustrating the impacts of the latest regulations. Due to these regulations, previous practices of land financialization, such as land-based borrowing through chengtou and land reserve loans, were forbidden (Huang and Chan, 2018). Nevertheless, the state cannot control every aspect of financialization in a more neoliberal system (Gotham, 2016; Wijburg, 2019). In China, there are compromises at every point in the negotiation (Zheng and Huang, 2018). Although chengtou were prohibited from borrowing against reserved land, they could still conduct land-related projects and enter the financial market as so-called “independent entities” (Feng et al., 2023). The reconfiguration of the land reserve system should be regarded as a central government endeavor to rebuild its authority over land borrowing. It does not terminate local borrowing or land-based development. Therefore, these institutional arrangements also leave space for local governments to maneuver. More research is needed to understand negotiation within the state and reassess local financial risks under stringent control.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the European Research Council (ERC) under Advanced Grant No. 832845—ChinaUrban and the China Scholarship Council.