Abstract

Cryptocurrencies, such as Bitcoin, have garnered significant attention in scholarship and beyond. Geographical work on cryptocurrencies has focussed on how their energy demand interacts with local communities and economies. Less is said about the organization of cryptoasset firms and their associated demands. This paper illuminates the complex geographies of one such firm, Bitfury Group, to investigate the global and national forms and structures such companies take and the factors encouraging them to concentrate operations in certain areas. To investigate the latter, we adopt the case study of Bitfury’s operations in Georgia, a South-Caucasian country where its presence is significant. We adapt Haberly et al.’s analytical framework to explore Bitfury’s geographical dimensions. We highlight how cheap electricity, regulatory and taxation regimes, personal encounters and personalities, and the materialities of hardware and energy-saving technology define these geographies and illuminate how Bitfury actively curates advantageous regulatory spaces. We encourage future work exploring Blockchain and Bitcoin technologies to understand the companies involved as simultaneously material and virtual, and as centrepieces in global networks interweaving production and finance.

Introduction

Each year, Sir Richard Branson’s private island, Necker, hosts a ‘Blockchain Summit’, conceived by Bill Tai – co-founder and chair of ACTAI Global, former member of Bitfury’s board of directors and current member of its advisory board. The event gathers diverse attendees, such as musician Imogen Heap, economist Hernando de Soto and Saadia Madsbjerg – then Managing Director of The Rockefeller Foundation (Shin, 2017). While the summit’s stated purpose is bringing together ‘world leaders [. . .] to discuss the applications of Blockchain technology for good’, the summit conveniently gathers individuals positioned to direct the flow of capital in the crypto-mining sector. For example, the 2018 sale of a Bitfury datacentre in the republic of Georgia to Chong Sing Holdings was conceived at the 2015 summit (Schmidt, 2018). Furthermore, Bitfury and de Soto have jointly worked in the past on Blockchain projects for land registry digitalization in Georgia (Shin, 2016). The amicable interactions of powerful individuals in tropical locations can thus instigate changes to record-keeping ‘infrastructures’ or corporate holdings in far-off locales. But many other factors contribute to making these plans a reality.

Whilst the Blockchain is often portrayed as something ethereal, existing in liminal ‘cloud’ spaces beyond government control and regulation, the assets and networks supporting it hit ground and find materiality at numerous points. As extensive literature demonstrates, this includes the sites (data centres, ‘mining’ rigs) where computer processing and associated energy use underpin Blockchain operations. However, it also includes offices, boardrooms and brass-plate addresses – spaces of interpersonal relations, research-and-development, IT support, legal creativity – all of which help determine where the aforementioned computer processing and energy consumption takes place.

Though banned in several countries (including Pakistan, Iran, Ecuador and China) Bitcoin remains mostly unrestricted across the globe, creating an industry around ‘mining’ and investing in cryptocurrencies and an oligopoly of transnational corporations and mining ‘pools’. This oligopoly requires further investigation. In this paper, we examine one, particular Blockchain-centred corporation and its role in a broader network of technology, trade and revenue-generation. Geographical scholarship has explored various national and regional experiences of crypto-mining. Less has been said about the agents driving such change and transformation. The rapid formation of Bitcoin entities and their consolidation of market positions raises important questions for economic geography scholarship: particularly, how, and why are transnational crypto-asset producers drawn to specific national and local jurisdictions that then become hub regions?

We herein contribute to answering this question. We do so via a case study of one, particular company’s contribution to the crypto boom in the republic of Georgia. Our study of Bitfury Group (herein Bitfury) in Georgia highlights the multi-dimensional capacities of entities in the Bitcoin sector: Bitfury develops blockchain-related software and crypto-mining hardware and is a leading Bitcoin miner. These multiple capacities require a variegated, transnational corporate structure. Hence, we expand our investigation with a second research question: how do Bitfury’s Bitcoin-mining activities in Georgia fit into the company group’s broader, transnational business activities?

To investigate these questions we draw on global financial networks (GFN) literature (in particularly Haberly et al.’s (2019) analytical framework), on geographical studies of cryptocurrencies and the Blockchain and on literatures on material political economy and cryptoasset regulation. Extant geographical treatments of cryptocurrencies and the Blockchain tend in two directions: local and regional studies of these technologies’ impacts (Atkins et al., 2021; Greenberg and Bugden, 2019; Lally et al., 2022; Rosales, 2021), or macro-geographical studies of the spatially varied concentrations of Blockchain-related firms, crypto-mining ‘infrastructure’ and profits, etc. (Janowicz et al., 2018; Zook and McCanless, 2022).

Haberly et al.’s (2019) framework, which we adopt and adapt, was developed to analyse asset-management firm Blackrock and FinTech’s impact on the geographical distribution of functions in the firm’s overall operations. We show that Bitfury provides further evidence of the porous boundary between the financial and tech sectors in the context of ‘FinTech 3.0’ (Arner et al., 2015; Lai and Samers, 2021), but remains squarely a technology provider, rather than morphing into a financial and advanced business services (FABS) firm. Our article thus heightens the tension in GFN studies between strands of literature emphasizing the financial relationships underpinning production of goods, services and commodities (Coe et al., 2014), and the nexus of financial centres and division of labour underpinning the production of financial products themselves (Dörry, 2016; Wójcik et al., 2022). We emphasize the need for an ‘infrastructural’ perspective on GFNs, which considers FinTech solutions as both software and hardware – examining both what they can do, and what they require to do it.

This paper is organized as follows. We first review the materiality of Blockchain and cryptoassets and the sector employing them. Second, we summarize extant GFN research and describe the framework we employ (Haberly et al., 2019). We subsequently discuss our case study, Bitfury, detailing its transnational and national structure and operations. Lastly, we consider this case study’s value for advancing GFN studies of FinTech and for developing the explanatory power of existing frameworks, drawing attention to the materiality of digital geographies (Kinsley, 2014), the state’s interactions with the cryptoasset sector and the role of personalities and embodied knowledge in shaping business activities.

Our study draws on both English- and Georgian-language sources. These include three annual financial reports for the Bitfury parent company, used to glean information about the names, addresses and home jurisdictions of subsidiary companies, about the location and status of some datacentres, the character of Bitfury’s operations in certain jurisdictions and distributions of capital, plant and equipment. Financial reports from the parent company were compared with those of Georgian subsidiaries to calculate the share of Bitfury’s workforce employed in Georgia. Information about company ownership structure and datacentre locations was enriched using SEC filings, an earnings call transcript for Bitfury’s subsidiary Cipher Mining, documents from Georgia’s National Agency of Public Registry and international news media., Information about changes to company management, personal interactions and certain details regarding company operations and applied technologies were gleaned from international and Georgian news media and from the company website. Information about ownership shares was drawn from a statement of capital. Information about tax breaks, land grants and others of the company’s interactions with the Georgian government was drawn from Georgian and international news media, and where possible verified using Georgian government orders. We contacted Bitfury in early January 2022, but have received no reply. Future research, then, could build on our findings and enrich them through expert interviews and observation.

Geographies of Bitcoin

Cryptocurrencies are digital assets operating in a distributed, time-stamped, append-only accounting ledger, simultaneously held by all users across a decentralized network – the Blockchain. Whilst the Blockchain has many uses, cryptocurrencies are most prominent. Blockchains are updated and validated following a set of rules, instructions and procedures – a ‘consensus algorithm’ or ‘consensus mechanism’ (Rella, 2020). Though over 20,000 different cryptocurrencies have emerged, Bitcoin remains most popular (representing >40% of total market capitalization of all cryptocurrencies (CoinMarketCap, 2021)) and lucrative – the value of one Bitcoin exceeded US$60,000 in November 2021 and in October 2022 was over $17,000. The current ‘award’ for validating transactions is 6.25 Bitcoins per block (over $29,000 at time of writing).

Bitcoin’s consensus algorithm is called Proof-of-Work, whereby a third-party (‘miner’) validates transactions by solving a complex mathematical equation in a process called hashing. Hashing requires computers to encrypt transaction blocks so that the encrypted value falls within a certain numerical space determined by a parameter called difficulty, adjusted dynamically every 10 minutes. Once completed, the new transaction block is added to the Blockchain alongside an additional transaction ‘awarding’ the miner validating the block with newly generated coins. Since difficulty grows with growth of computing power in Bitcoin’s network, each miner wants the most powerful and expansive mining rigs – collections of computer servers that work 24/7 to solve validation equations before anyone else.

This has provoked a mining hardware ‘arms race.’ Crypto-mining is now dominated not by hobbyists with gaming computers, but by large organizations, operating across state jurisdictions, pursuing revenue and profit. The result is increasing energy demand (to power and cool servers), often with a hefty carbon footprint: Bitcoin’s estimated total annual energy demand as of 2021 was 129.22 terawatt-hours, comparable to that of Norway (Digiconomist, n.d.). Electricity for Bitcoin mining is currently generated mainly using fossil fuels: in 2020, coal and natural gas fulfilled around 38% and 36% of demand, respectively (Blandin et al., 2020). The centralization of mining power encourages clustering as miners seek cheap, reliable energy and non-restrictive regulatory environments. Crypto-mining hub regions include Sichuan, Xinjiang and Inner Mongolia (China; Reuters, 2018), Quebec (Canada; Atkins et al., 2021), Washington state (USA; Greenberg and Bugden, 2019), eastern Siberia (Estecahandy and Limonier, 2021), Venezuela (Rosales, 2021), Kazakhstan (BBC News, 2022), Iceland (Sigurdardottir and Burton, 2021) and Texas (USA; Gkritsi, 2022).

Geographical investigations emphasize how crypto-mining interests, once arrived at these sites of energy use and wealth generation, interact with local ecologies, ‘infrastructures’ and regulations in context-specific ways (Atkins et al., 2021; Greenberg and Bugden, 2019; Lally et al., 2022; Rosales, 2021). However, explanations of why crypto-miners are drawn to particular localities, in both popular and scholarly literature, rarely look beyond the meso-geographical, endogenous factors of energy cost and regulatory environment. Narrow focus on such drivers overlooks micro-scale factors (materialities, interpersonal relationships, embodied know-how) that enable meso-scalar factors to be significant.

To deepen such explanations, we examine one particular cryptocurrency hub: the republic of Georgia. This country has recently been gripped by cryptocurrency enthusiasm: in 2018 an estimated 5% of Georgian households were engaged in cryptocurrency mining or investments, and 10%–15% of Georgia’s electricity consumption was attributed to cryptocurrency mining (World Bank, 2018). We investigate the role of one firm in this boom – Bitfury, a leading Bitcoin miner. In 2018, Bitfury contributed 5% of global hashing capacity – computational power within the cryptocurrency network – and around 2% in 2019 and 2020 (Bitfury Group Limited [BGL], 2019, 2021, 2022a). Bitfury has large-scale mining operations in Georgia.

In seeking to explain ‘why Georgia?’ we follow Mackenzie’s (2017) observation that every political economy is both material and spatial: the macro-spatialities of datacentre and headquarter location are determined not only by meso-spatialities of energy cost and availability, but also micro-spatialities of microchips and cooling systems. We also draw inspiration from scholarship emphasizing professional services firms’ dependence ‘on the embodied knowledge, intricate personal networks, skills, expertise and trustworthiness of their [. . .] employees’ (James, 2008: 110). Transnational firms are not omniscient – their ability to exploit advantageous local conditions often depends on mediation by actors with locally specialized knowledge (Dörry, 2015).

However, Bitfury is not only a Bitcoin miner: they also develop blockchain software solutions and crypto-mining hardware. The firm’s activities in Georgia are linked to their broader operations and can only be fully understood in this context. Next, we explain our approach to investigating this transnational structure.

Cryptocurrencies and global financial networks

A suitable starting point for examining Bitfury’s broader, transnational operations (and Georgia’s role therein) is the literature on global economic networks (GENs; including the global production networks (GPN) and global financial networks (GFN) subfields). This literature studies how lead firms are ‘coupled’ to particular localities via an ‘interactive complementarity’ between their ‘strategic needs’ and endogenous local conditions (Coe et al., 2004), through networks with locally embedded actors and intermediaries (e.g. Dörry, 2015). The geographical distribution of FABS firms’ operations is determined by myriad factors, including financial and managerial innovation (Pan et al., 2020), regulatory changes introduced by states and international organizations (Lai, 2018), mediation of local ABS firms (Dörry, 2016) and the flexible territoriality of financial regulation (Dörry, 2022; Haberly, 2020), offshoring and zoning (Dörry and Hesse, 2022). Finally, GEN scholars have emphasized the diffusion and transfer of non-codified, locality- or sector-specific knowledge (Henderson et al., 2002). This is particularly true for the financial sector, where ‘knowledge network formation’ and harnessing of knowledge gaps are quintessential to ABS firms’ business practices (Dörry, 2015, 2016). GENs therefore have a ‘polycentric spatiality’, ‘embedded’ in numerous localities that both shape and are shaped by the structure and character of the lead firm and network (Coe et al., 2008). It is this ‘polycentric spatiality’ that we wish to illuminate by mapping the transnational structure of Bitfury’s operations.

Various scholars have asked whether FinTech is causing financial and tech companies to begin resembling one another (Arner et al., 2015; Haberly et al., 2019; Lai and Samers, 2021): With the blurring of boundaries between financial and non-financial firms and activities, FinTech should prompt geographers to re-examine the relationships between finance and production, inter-firm relationships, new modes of value capture and creation, and the spatial impacts of reconfigured production networks (Lai and Samers, 2021: 729).

Geographers have also asked whether cryptocurrencies have displaced institutional financial intermediaries and decentralized financial networks (Zook and Blankenship, 2018; Zook and Grote, 2022). Answers to this latter question have generally been negative: cryptocurrencies, far from displacing traditional financial intermediaries, have ‘largely been relegated to store of value and speculative trading’ (Zook and Blankenship, 2018: 253).

Similarly, Haberly et al. (2019) test the hypothesis that FinTech solutions will engender centrifugal tendencies in the asset-management sector, unseating incumbent financial centres, driving technical jobs to back-office technology centres decoupled from ‘client-facing’ relational work and decentralizing the paper and virtual geographies of asset management to ‘offshore’ jurisdictions and server farms that follow cheap land and electricity. For this investigation they employ an elaborated GFN framework, adapted to describing the geographic distribution of functions within FABS firms employing FinTech solutions (like their case study: asset-management firm BlackRock). Their model characterizes GFNs as consisting of four overlapping spheres:

‘Virtual geographies’ denotes siting of datacentres, servers and other hardware constituting the ‘brain’ of FinTech solutions.

‘Technical geographies’ and ‘relational geographies’ encompass two types of labour, the former involving hardware and software expertise and taking place behind the scenes, in ‘back-office technology centres’, while the latter includes ‘front-office client relational roles.’

‘Paper geographies’ indicates legal and regulatory flexibilities and expertise, emerging from the particularities of specific, financially advantageous off-shore and on-shore locales.

While Haberly et al. (2019) find evidence of a ‘technology-driven upheaval’ in asset management, their tested hypothesis does not hold true: despite predictions of dispersion, ‘the identity and geography of digital asset management platform providers has remained, to a rather counterintuitive extent, aligned with their identity as financial firms rather than as technology firms’ (Haberly et al., 2019: 179). Virtual and relational geographies stick together: datacentres are located as near trading centres as possible, to exploit what Mackenzie (2017) calls ‘capital’s geodesic’ and what Zook and Grote (2017) call the ‘microgeographies of HFT [high-frequency trading]’ – trying to scrape milliseconds off transaction time. However, HFT’s siting decisions depend on the physical location of centralized exchanges. Cryptoasset validation is decentralized and distributed across machines, and the industry is dominated by in-house design of application-specific integrated circuits (ASICs; Rella, 2023). We investigate the alternative spatial patterns that emerge from these socio-technical particularities.

While cryptocurrencies are by now well established as financial products and treated as a subset of ‘financial technologies’ (FinTech), they have yet to garner much attention from GEN studies of finance, beyond brief mentions in several GFN articles (Haberly et al., 2019; Lai and Samers, 2021). We can see cryptocurrencies as a site for (re)invigoration of GFN/GEN studies of ‘FinTech 3.0’ (Arner et al., 2015). In particular, we find that Haberly et al.’s (2019) framework is suitable for studying Bitfury, because our case study and theirs concern similar phenomena, from two different viewpoints: their case is a ‘Fin’ firm incorporating ‘Tech’, and ours is a ‘Tech’ firm incorporating ‘Fin’. Both types of firm have server farms (virtual geographies), front-office client-relation work (personal geographies), software engineers and programmers (technical geographies) and special-purpose vehicles in offshore jurisdictions (paper geographies).

Is it possible, then, that tech might come to resemble finance, rather than finance resembling tech? Haberly et al. (2019: 171) hint at this possibility, characterizing Facebook’s Libra cryptocurrency project as an attempt to enter financial services, and commenting that, ‘the burgeoning scale of New York’s FinTech industry underscores the capacity for the largest financial legal-regulatory and exchange hubs to become centres of finance-specific software expertise.’ Our application of these authors’ framework to investigate the geographical distribution of Bitfury’s operations makes initial steps towards addressing this unanswered question. In so doing, we provide a test case for Haberly et al.’s (2019) framework: we demonstrate its applicability, (a) to a different manifestation of FinTech (Blockchain-based cryptoassets rather than DAMPs) characterized by different socio-technical demands, (b) to a nascent sector operating under ostensibly decentralized premises (in contrast to the institutionalized, centralized asset-management sector) and (c) to a tech firm rather than a FABS provider.

However, we do not just apply Haberly et al.’s framework – we also enhance its explanatory power in each of the four dimensions they identify. Firstly, concerning the virtual, we develop an ‘infrastructural explanation’ (Furlong, 2021) of the siting of cryptoasset mining operations based on the materiality of technological devices employed in mining – for example, server cooling. Materiality and technology have yet to be thoroughly explored in GFN literature as factors influencing location choices, ownership structures and development outcomes. Hall (2018) and Töpfer (2018) both mention ‘micro-materialities’, but without exploring this concept in depth. Haberly et al. (2019) make the most ambitious effort to integrate technical factors into a GFN framework, but their analysis primarily considers these technologies as software – their functions, the human labour they can replace, the face-to-face interaction they might make obsolete, the gatekeepers they could displace and the underlying cost-cutting. The materiality of these technologies as hardware – as the server farm powering BlackRock’s DAMP ‘Aladdin,’ and its location next to a hydroelectric station – is engaged only in passing. Second, regarding technical factors, we highlight how, alongside electricity, competitive labour costs for skilled jobs greatly influence Bitfury datacentre locations.

Third, regarding the paper aspects of Bitfury’s activities, we highlight how cryptoasset firms’ relationships with regulators can at times be cooperative rather than agonistic. Zook and Grote (2020: 1570), studying how initial coin offerings foster financialization within and outside cryptoasset markets, identify a variegated process: catalysts (technology, ideologies and cheap capital) are exploited to open cracks in existing value chains – ‘new space for money to flow into’. Cracks create regulatory voids, exploited in the short-term until regulation fills the void, whereafter ‘actors shuffle between territories’ seeking the most advantageous regulatory regimes. We enlarge this perspective: ‘voids’ are not always created by cryptoasset firms discovering and exploiting blind spots that regulatory institutions then rush to fill – sometimes they are actively generated and maintained via cooperation between transnational firms, local ABS firms and the state. In this, we heed Dörry’s (2022) invitation to study how the micro-geographies of law and regulation underpin financial (and technological) innovation, and to consider those innovations’ ‘dark sides’.

Concerning relational factors, we expand on Haberly et al.’s (2019) emphasis on the importance of client- and partner-facing relational work. Despite mentions of the ‘complex circulations of capital, knowledge and people that underlie the production of all goods and services’ (Coe et al., 2008: 75), there has been little in-depth GEN investigation of the role played by key relations and interactions between particular individuals. Hence, we illuminate the role of individuals as paramount in influencing wider systemic variables such as regulations and their impacts on technology with debates around infrastructures. Particular infrastructures and relationships are essential to the creation and exploitation of advantageous regulatory regimes.

We adopt a case-based approach because of difficulties tracing these geographies, treating one company – Bitfury – as exemplary of broader patterns across this industry. We do not seek to make overarching, generalizable statements about the sector, wishing, instead, to illuminate the complexity of one firm operating within it.

Bitfury group

Founded in 2011, Bitfury operates as a Bitcoin ‘miner’, a developer and supplier of mining hardware – ASICs, servers, immersion cooling technology and containerized datacentres – and a developer of software applying the Blockchain to various industries: net security and investigation, payments, intellectual copyright and software for aiding customers in Blockchain integration (Forbes Georgia, 2016; Kimmell, 2021).

Bitfury – like other transnational firms – is not a single legal entity. As of April 2022, Bitfury Group consisted of 46 corporations across 16 national jurisdictions (Canada, the Cayman Islands, Georgia, Hong Kong, Iceland, Kazakhstan, Latvia, Luxembourg, Malta, the Netherlands, Norway, Russia, the UAE, the UK, Ukraine and the USA; BGL, 2022a). The greatest numbers of Bitfury subsidiaries are concentrated in the Netherlands (9), Cayman Islands (9) and Georgia (5). The group is structured as a hierarchical series of holding companies, primary subsidiaries and auxiliary subsidiaries supporting the primary subsidiaries and parent company (BGL, 2022a). This structure’s apex – the UK-based company BGL and the Dutch Bitfury Top HoldCo B.V. and Bitfury Holding B.V. – are direct parents of most primary subsidiaries. BGL is itself majority owned and controlled by a further parent company, V3 Holding Limited (Cayman Islands); V3 is owned by Bitfury founder Valery Vavilov (Cipher Mining Inc., 2022b).

This on-paper structure does not fully capture the geography of Bitfury. While the greatest number of constituent companies are concentrated in north-west Europe (UK, Netherlands) and the Caribbean, much of Bitfury’s revenue-generating activities, material assets, employees and material capital are located elsewhere. Research and development activities – ‘technical geographies’ as per Haberly et al.’s (2019) framework – largely overlap with executive functions in the Netherlands (through subsidiaries Bitfury Surround B.V., Crystal Blockchain B.V., Bitfury I.P. B.V., Peach B.V., Axelera AI B.V.), but also take place in Eastern Europe (e.g. Exonum LLC (Russia)) and East Asia (LiquidStack (Hong Kong); BGL, 2019, 2022a). Furthermore, this geography has been complicated by possibilities of remote work, the COVID-19 pandemic and Russia’s invasion of Ukraine, which have further dispersed the workforce beyond the list of countries where R&D officially takes place – for example to Poland, Czechia, Germany, the UAE and Turkey (BGL, 2022a).

‘Paper geographies’ are by nature difficult to investigate: company leadership are unlikely to publish much information about subsidiaries established for the sole purpose of exploiting financially advantageous tax and regulatory environments, and such companies are rarely the subject of press coverage. Nevertheless, the very names of many Bitfury subsidiaries are revealing, and allow us to fairly confidently infer that this is why they were established. So, we see that special-purpose vehicles (BTSPV Limited, CHSPV Limited, CVSPV Limited and IXSPV Limited) as well as V3 Holding Limited (the aforementioned holding company by which Vavilov maintains control of the company group) and Bitfury Finance Limited are all in the Cayman Islands. Bitfury Holding B.V. and Bitfury Top HoldCo B.V. are located in the Netherlands, Bitfury Finance Holding Limited in Malta and Bitfury Securities S.a.rl. in Luxembourg (BGL, 2022a; Cipher Mining Inc., 2022b).

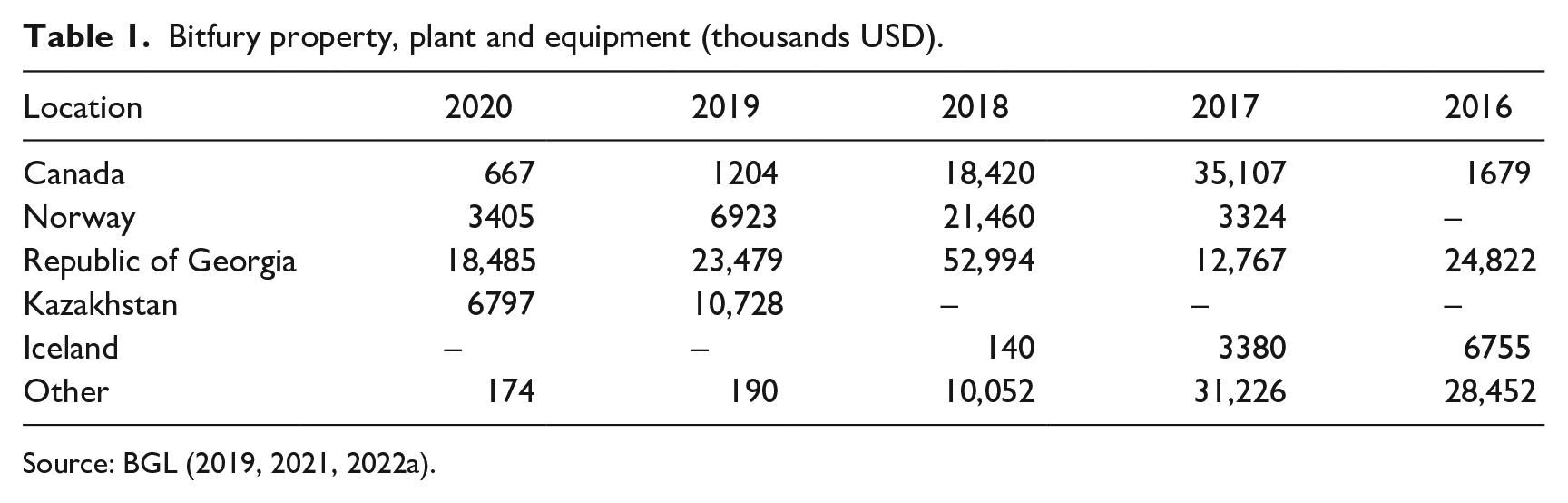

Bitfury’s datacentres (virtual geographies), key sites of revenue-generation and employment (Table 1), are in Canada, Iceland, Norway, Georgia, the USA and until recently Kazakhstan. Datacentres are located in peripheral and/or (post)industrial locations, like Mo I Rana (Norway), Gori and the Gldani district of Tbilisi (Georgia), Medicine Hat, Drumheller and Three Hills (Alberta) and Sarnia (Ontario, Canada), Ekibastuz (Kazakhstan) and Andrews, Happy and Odessa (Texas, USA; BGL, 2021, 2022a; Cipher Mining Inc., 2022b). Many of these facilities, like those in Kazakhstan and Texas, are located directly next to power plants, to ensure uninterrupted, stable energy supply, while others (in Norway and Georgia) are in special economic zones.

Bitfury property, plant and equipment (thousands USD).

Unlike remotely performed R&D activities or peripherally sited datacentres, the offices and registered addresses of most Bitfury companies (including those operating datacentres) are in or near international and/or national financial and regulatory centres (Amsterdam, Dubai, Kyiv, London, Upper Marlboro (Maryland), Moscow, New York, Nur-Sultan, Reykjavik, Riga, Tbilisi and Washington D.C.; BGL, 2022a). Our empirics suggest these locations were specifically chosen because they facilitate particular aspects of Bitfury’s business activities, which we can understand as the ‘relational geographies’ of the company’s operations. As stated in BGL’s 2019 annual report, the ‘Company’s business is constantly evolving and, in many aspects, can be considered being [sic] a start-up’ (BGL, 2021: 63) – the group regularly seeks external financing and partnerships to support development of its business lines (BGL, 2021, 2022a). Proximity to financial centres and the agglomeration of financial institutions they offer is likely key to securing this financing, as well as for interfacing with potential clients. Bitfury leadership are also forthcoming about their desire to influence regulation, and the importance of offices in national regulatory centres. To quote Bitfury’s founder and former CEO, Valery Vavilov: ‘Any regulation can make a business less attractive for investors. For this reason we are setting up a representative office in Washington [D.C.], and have relations with regulators’ (Tskhovrebova, 2015).

This is a necessarily transitory and incomplete snapshot of Bitfury’s activities. In most jurisdictions where Bitfury operates there are subsidiaries that play undefined support roles (e.g. GEO Maintenance LLC, Georgia Technology Park LLC, Georgia Technology Park Logistics LLC (Georgia), Bitfury Infrastructure Limited (Kazakhstan) and Bitfury UK Limited (UK)); other subsidiaries’ function is simply unclear (e.g. Goodston Developers Limited, and Ballard Carriers Limited (Cayman Islands)). Bitfury also operates in national jurisdictions where it has no official subsidiaries, for example Azerbaijan, Kyrgyzstan (BGL, 2021, 2022a) and the remote-working locations mentioned above.

Furthermore, Bitfury entities and facilities are frequently relocated and reconfigured. In 2018, the parent company BGL, formerly of the Cayman Islands, was reincorporated in the UK (BGL, 2021). Bitfury Finance Holding Limited recently moved from the Caymans to Malta (BGL, 2021); and in July 2021, as part of a ‘fundraising exercise’, all employees of Bitfury AI B.V. transferred to Axelera AI B.V. (BGL, 2022a). In spring-summer 2018 Bitfury sold its Georgia datacentres, only to re-acquire them soon after (BGL, 2021; Schmidt, 2018). Bitfury sold its Drumheller (Canada) site to former associate Hut 8 (BGL, 2019) but has since opened and continues upgrading new Canadian sites at Three Hills and Sarnia (BGL, 2022a ).

In the following section, we turn to the factors that have drawn Bitfury to establish datacentres in Georgia, a national jurisdiction that is part of the company’s ‘virtual geographies,’ and where it has one of its most intense concentrations of fixed capital and employees. In addition to the usual suspects of energy cost and advantageous regulation, Bitfury has become ‘coupled’ to Georgia via local expertise, interpersonal relationships, hardware solutions and national regulatory innovation, enabling the successful accommodation of Bitfury’s ‘strategic needs’ to endogenous conditions and local aspirations. Where possible, we also provide empirics that suggest these dynamics might not be unique to Bitfury’s operations in Georgia, but rather representative of how the company comes to operate in other jurisdictions around the globe.

Bitfury in Georgia

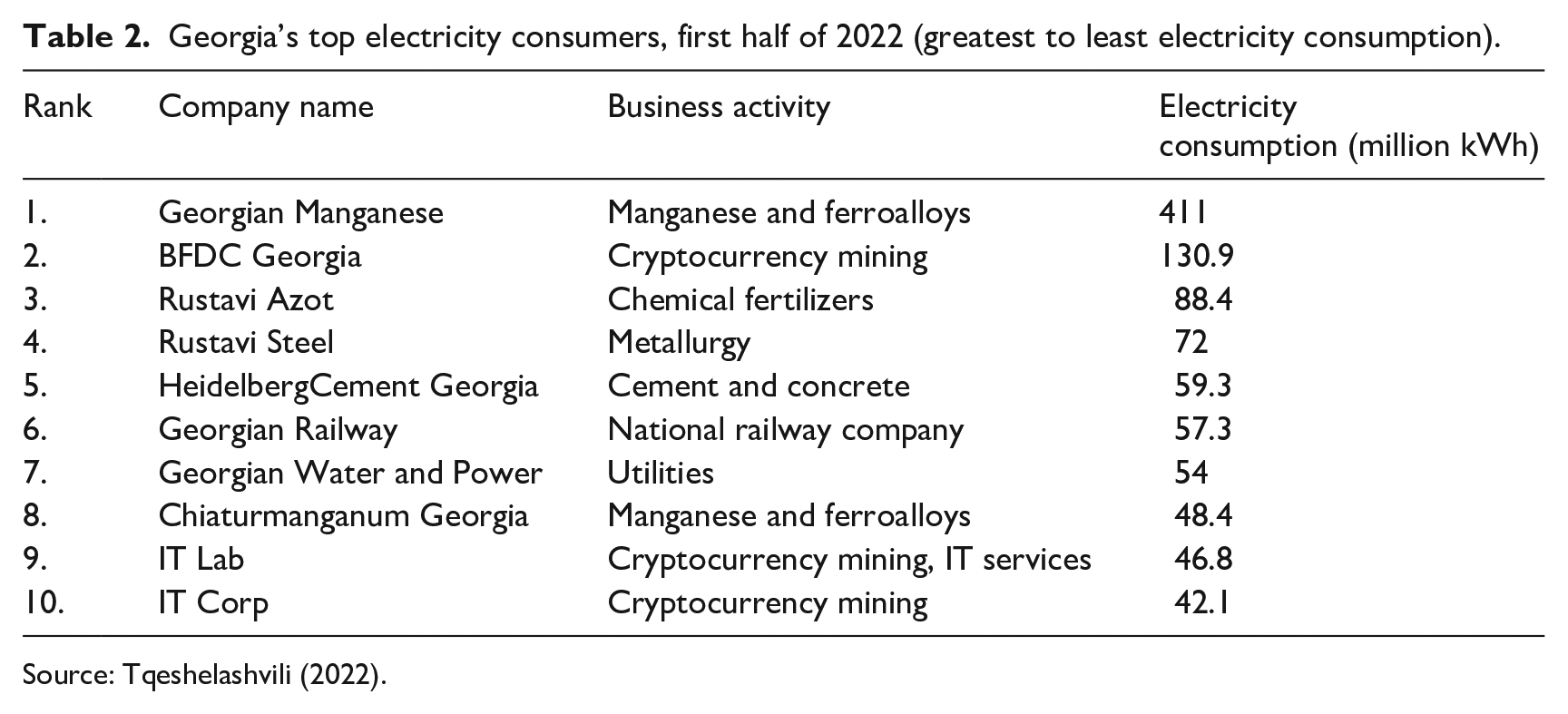

Georgia has recently experienced an explosion of cryptocurrency-related activities. While private citizens, local firms and transnational corporations have all contributed to this phenomenon, large firms have taken the lead, helping to both fuel popular enthusiasm in and raise energy consumption of cryptoasset mining. In recent years, crypto-mining companies have regularly appeared in the list of energy-hungry ‘direct users’ (otherwise dominated by metallurgical firms and utilities providers) published until recently by the Georgian electricity market regulator, ESCO. In the first half of 2022, three of the top electricity consumers in Georgia were crypto-miners, among them Bitfury subsidiary BFDC Georgia (Table 2). Below, we detail Bitfury’s history in Georgia, with a particular focus on what brought the company to operate in this location.

Georgia’s top electricity consumers, first half of 2022 (greatest to least electricity consumption).

Source: Tqeshelashvili (2022).

Bitfury opened its first Georgia datacentre in July 2014 – a 20 MW facility on the site of a former cotton mill in Gori, west of Georgia’s capital, Tbilisi (McCarthy et al., 2015). Their second―a 40 MW centre in Gldani district, on Tbilisi’s outskirts―was established in 2015.

The decision to locate these datacentres in Georgia reflects, firstly, the increasing centrality of energy costs in Bitfury’s business model. Electricity fees comprise as much as 90%–95% of expenditures for Bitfury’s datacentres (Bakradze, 2016), and the group’s executive vice chairman recently argued that declining technological efficiency gains and a maturing market make electricity cost the central consideration for mining profitability (Kikvadze, 2019). As such, the presence of cheap, reliable energy is a key factor in siting decisions. Georgia’s power sector, which can in some seasons be supplied almost entirely by hydropower, a cheap source of electricity (Wyeth, 2022), meets this need. Indeed, Bitfury’s founder Valery Vavilov has stated that low electricity fees were key in convincing the company to choose Georgia over other potential datacentre locations (Tskhovrebova, 2015).

Alongside electricity, land and labour costs help determine Bitfury datacentre locations. In discussing why Bitfury built datacentres in Georgia, the group’s founder, Valery Vavilov, has mentioned the ‘high professionalism and low cost of local personnel’, stating that, ‘In Georgia, one person works three times more efficiently than three in Iceland and it is much cheaper to service datacentres here’ (Tskhovrebova, 2016). In 2020 the average monthly nominal earnings for men and women employed in ‘information and communication’ activities in Georgia was 2089.8 and 1659.7 GEL (roughly 672 USD and 534 USD) respectively – substantially less than the average 757,000 and 662,000 ISK (roughly 5593 USD and 4891 USD) earned by men and women employed in similar activities in Iceland (authors’ calculation based on Geostat (n.d.), Statistics Iceland (n.d.) and (Exchange Rates UK, n.d.)). Cost of labour is undoubtedly a significant consideration in Georgia, where up to 50% of Bitfury’s workforce have been employed.

As regards land, Bitfury’s 40 MW Gldani facility sits on an 18.5-ha land plot – formerly the TARZ (Tbilisi Automotive Repair Depot – Russian:

These particular plots are advantageous not only because of the cost of the land itself. The aforementioned 18.5-ha plot was divided into smaller plots (National Agency of Public Registry of Georgia, 2015), 17 ha of which Georgia’s government declared a ‘free industrial zone’ (FIZ; Government of Georgia, 2015a). This means that companies operating therein are freed from paying taxes to the state budget (income, property and value-added taxes); the removal of value-added tax reduces the already-low cost of electricity by an additional 18% (Bakradze, 2016; Brown, 2020). Several of Bitfury’s Georgian subsidiaries are registered within that FIZ, and benefit from the advantages it provides. Subsidiaries not located in the FIZ (like the one that owns the Gori datacentre) nevertheless benefit from national regulation, like a recently created law on cryptocurrencies that favours foreign investors: legal and natural persons who become residents of Georgia are exempted from VAT on profit generated from selling cryptocurrencies, and sale of computing power (hash) from Georgia abroad is also not subject to VAT (Brown, 2020).

Just as cheap electricity is essential to Bitfury’s business, so too is application of energy-saving technology to reduce operating costs. Bitfury develops such technologies (like containerized, air-cooled datacentres and immersion cooling technology) both for sale and to operate in its own datacentres. But cooling systems do not merely reduce operating costs – they are likely a key foundation for the geographies outlined herein.

Whilst Bitfury operates air-cooled facilities in colder climates (Norway, Iceland and Canada), in the subtropic-continental climate of Tbilisi they appear to have gone to great lengths – adopting immersion-cooling technology – to ensure their Gldani facility can exploit the friendly business environment. This technology involves immersing crypto-mining servers in a non-conductive liquid called Novec, within sealed containers. As the servers heat up, the liquid boils, rising as a gas to the top of the container. There, it encounters pipes carrying cold water – the heat carried by the evaporated Novec is transferred to the pipes, and the now-cooled liquid condenses and drips back into the pool containing the servers, beginning the process anew. It appears that material, technical innovation is necessary to ensure Bitfury can take advantage of the tax breaks secured in this jurisdiction. Such a reading of our empirics is lent credence by the company’s efforts to deploy liquid cooling technology in Texas – another subtropical location (Cipher Mining Inc., 2022a).

Lastly, as regards relational factors, George Kikvadze – Bitfury’s current Executive Vice Chair – was in 2013–2016 a member of the advisory board for Georgian Co-Investment Fund, the private equity firm that loaned 10 million USD to help Bitfury establish its Gori datacentre, in 2014 (Forbes Georgia, 2016). Elene Dighmelashvili, a former Senior Lawyer in Georgian governmental organizations now works for Bitfury as Senior Counsel (Eternity Capital, n.d.). But no individual has been more decisive for Bitfury in Georgia than Ephrem (Remi) Urumashvili, one of the titular partners of a Georgian law firm specializing in banking, finance, corporate and tax law. It was he who convinced Vavilov to begin operations in Georgia, over dinner in Tbilisi in 2013, with promises of near non-existent taxes and a friendly business environment (Schmidt, 2018; Tskhovrebova, 2016), and he has since become Bitfury’s official representative and primary advocate in Georgia (Tskhovrebova, 2016).

Bitfury not only utilizes such insider knowledge and ABS services, but actually integrates it with the company, compensating many such individuals with company shares (Bitfury Group Limited [BGL], 2022b). Moreover, this is not merely a peculiar characteristic of Bitfury’s business activities in Georgia. Bitfury has also, for example, worked to accumulate American insider regulatory knowledge among its leadership. In November 2018, the company added Anette Nazareth, a former member of the US Securities and Exchange Commission, to its advisory board (Baydakova, 2018), and in November 2021, Bitfury announced that Vavilov would be replaced as CEO by Brian Brooks, a former US Comptroller of the Currency (Quarmby, 2021).

How did Georgia become a crypto-mining ‘hub region’?

We began this investigation by asking how a particular locality like Georgia comes to be a cryptomining ‘hub region,’ and how Georgia fits into the geographical distribution of a cryptoasset firm’s operations. Our investigation of Bitfury and its activities suggests answers which both reinforce and expand upon literature on GFNs and the cryptoasset sector.

As for how cryptoasset firms become coupled to particular localities, our investigation supports calls from GFN scholars (Lai, 2018; Töpfer, 2018) to better appreciate how the state and politics shape financial geographies, even if ‘the concept of territory in the firm–territory nexus at the heart of both GFNs and GPNs [already signifies] agency, including the state’ (Wójcik, 2018: 273). The Georgian state, and particularly its eagerness to create advantageous regulatory spaces for Bitfury, is central to our analysis. Georgia is hardly alone in this: from the Crypto Valley in Zug, Switzerland (Williams, 2018) to the Blockchain District in Hyderabad, India (Blockchain District, n.d.), the crypto industry thrives on special zones and districts, within a broader trend in global capitalism that sees zones as ‘laboratory’ and lubricant for policies’ (Dörry and Hesse, 2022).

Extant literature on cryptoasset regulation assumes a somewhat agonistic tension between crypto firms and the state (e.g. Zook and Grote, 2020): cryptoasset firms find advantageous conditions for their business primarily by outmaneuvering and outwitting a cumbersome, often oblivious state that is slow to regulate technological or financial innovation. Our analysis, conversely, indicates that Bitfury is not exploiting voids as passive spaces of opportunity overlooked by regulators. Rather, Bitfury actively creates and curates spaces of opportunity via lobbying, collaboration and mutual exchange with Georgia’s government. Furthermore, Bitfury’s R&D activities help regulate the crypto industry: products like their ‘Crystal blockchain analytics solutions [. . .] help banks, regulators, and law enforcement agencies to analyze, audit, and possibly regulate digital asset networks. Crystal works with Europol, Interpol and various National Police and Prosecutors offices around the world’ (BGL, 2022a: 9). This suggests that literature on cryptoasset regulation should pay more attention to the crypto industry’s cooperation with national and transnational regulatory bodies in creating advantageous regulatory spaces.

Our analysis also highlighted a phenomenon at the intersection of relational and paper geographies that, we believe, has not received the theoretical attention it deserves: the indispensability of individual actors in facilitating the coupling of transnational lead firms with particular localities. In the case of Bitfury in Georgia, the role of individuals in establishing relational geographies is exemplified by Urumashvili – partner in a corporate tax law firm – who convinced Vavilov to operate in Georgia. Kikvadze – Bitfury’s current Executive Vice Chair – was on the advisory board of the Georgian investment fund that helped finance Bitfury’s first datacentre in Georgia. Bitfury has also absorbed numerous other former regulators and individuals with jurisdiction-specific expertise (represented in the examples of Dighmelashvili, Nazareth and Brooks) – specialist knowledge often circulates together with the individuals in whose heads that knowledge is stored. Extant GFN literature has emphasized the importance of knowing how to navigate and exploit local regulatory particularities (e.g. Dörry, 2015, 2016). Our observation that knowledge and individuals circulate together is not new: this is one of the mechanisms by which ‘knowledge transfers’ are assumed to take place. Nevertheless, despite longstanding emphasis on the movement (transfer, circulation, capture and diffusion) of specialist knowledge, there has been little work in the GEN literature exploring the nitty-gritty of how this movement actually take place.

Finally, Bitfury’s deployment of specific technological solutions in certain localities suggests that hardware solutions like liquid cooling tech do not merely reduce operating costs – they may be key in enabling the group to exploit jurisdictions where it has secured favourable regulatory regimes. The ‘technicity’ (Kinsley, 2014: 366) of crypto-mining produces specific geographies. These result from tensions between ‘internal’ trade-offs inherent to particular hardware solutions, and ‘external’ regulatory and economic incentive structures, rather than stemming from analytically independent forces. Techno-material fixes and regulatory incentive structures are mutually reinforcing: the techno-material enables the regulatory, and the regulatory provides the raison d'être of the techno-material. This represents a divergence from extant GFN literature due to the emphasis on material ‘infrastructures and ‘micro-materialities’ of hardware underpinning Bitfury’s activities. We reflect on this further below.

Bitfury – At the intersection of finance and production

We noted above two overarching questions related to the transformation of finance – and technology – by FinTech: will the finance and tech sectors increasingly come to resemble one another? And will the siting of tech firms’ operations remain dispersed, thanks to novel forms of connectivity unbounded by territory or will their growing involvement with FinTech draw them to financial centres, like their financial sector counterparts? Our answer is mixed. On one hand, the very fact that Haberly et al.’s (2019) framework can effectively describe Bitfury’s operations suggests that the differences between finance and tech really are being eroded: Bitfury’s operations, like those of BlackRock, can be described in terms of technical, relational, virtual and paper geographies. The fundamental building blocks of a financial or tech firm are, indeed, similar.

However, the distribution of Bitfury’s operations more closely reflects Haberly et al.’s (2019) hypothetical test case – the tech firm layout expected to result from asset-management firms’ adoption of FinTech – rather than the distribution they observed in their case study. Bitfury’s ‘paper’ geographies are concentrated in ‘offshore’ jurisdictions and some of Europe’s longstanding financial and business centres: London, Luxembourg, Amsterdam and the Caribbean account for 20 of 46 constituent Bitfury corporations, including special-purpose vehicles, financial subsidiaries, holding companies and the group’s parent company. Front-office, ‘relational’ geographies are in international and national financial and regulatory centres. The ‘virtual’ (datacentres, including most property, equipment and employees) is concentrated in marginal, (post)industrial locations. ‘Technical’ geographies of R&D are distributed across tech hubs and still further afield because of opportunities for remote working.

The siting of Bitfury datacentres in particular contrasts with that of asset-management firms employing fintech. As in HFT, crypto miners race one another, but there is no central hub (trading floor or stock exchange) to be closer to, thereby shaving milliseconds off transaction validation. To edge out the competition in this race, one must crunch numbers faster, not send a signal faster. The technical details of crypto-mining enable firms to pursue cheap electricity and computing power in a way that financial firms perhaps cannot. Furthermore, the relative concentrations of Bitfury’s activities in particular locales also contrast with that of asset-management firms. BlackRock has a datacentre underpinning its asset-management platform Aladdin; its activities are primarily concentrated in global and regional exchange hubs (Haberly et al., 2019). Bitfury has numerous datacentres across the globe, and these are its primary sites of employment and concentrations of productive capital.

The distribution and concentrations of Bitfury’s operations do not, then, generally reflect those of financial actors, suggesting that the overlap between finance and tech is still quite small. The siting of Bitfury datacentres more closely resembles, for example, electricity-hungry, productive-capital-centric heavy industry, which is often located as close as possible to cheap power sources (generally hydropower); for example, consider the close association of metallurgy with hydroelectricity in Brazil (Bunker and Ciccantell, 2005), Canada, Norway (Cohn et al., 2020), Iceland (Guðmundsdóttir et al., 2018) or even Georgia (Table 2).

We should therefore be reticent to characterize crypto as ‘fintech’ or ‘financial services’, as in the rare instances where cryptocurrencies have been mentioned in the GFN literature (Haberly et al., 2019; Lai and Samers, 2021). This conclusion reflects extant tensions within the GEN literature, regarding how finance should be understood and examined: as the GFNs of productive processes or the GPNs of financial products – the tangle of financial relationships underpinning production of goods, services and commodities (Coe et al., 2014) or the nexus of financial centres and division of labour that underpin the production of financial products themselves (Dörry, 2016; Wójcik et al., 2022).

Bitfury’s activities advance our understanding of the ‘production of finance’ (Dörry, 2016). Speculative financial industries cannot develop unless someone produces the assets to be speculated upon. As a Bitcoin miner, producing units of cryptocurrency, Bitfury does precisely this. However, this means Bitfury’s business activities are directly dependent on continued financial speculation: ‘The Company [BGL] remains closely linked to the Bitcoin market for both mining revenue and equipment sales with overall demand of equipment depending significantly on the price of Bitcoin and the sentiment of the market’ (BGL, 2022a: 5). Our case study thereby exemplifies both the finance of production and the production of finance. Whilst traded as a financial asset, Bitcoin is produced in a way that more closely resembles metallurgy than finance: in the geographies of crypto-mining, at least, digital metallism endures.

Conclusions

We have herein provided a case study that sheds light on the positioning of cryptoasset mining within FinTech and, by extension, can contribute to study of FinTech’s impact on GENs. Whilst geographical literature on Blockchain and cryptoassets remains ‘at the moment mainly a speculative literature’ (Lai and Samers, 2021: 723), the example of Bitfury highlights how crypto-asset companies not only reflect scholarly understandings of GENs – but also trouble and extend our assumptions.

The siting and clustering of Bitcoin ‘mines,’ whilst motivated by potential profits, depend on numerous factors operating across jurisdictions. This paper has worked to illuminate how Georgia fits into the economic network centred on Bitfury as ‘lead firm.’ Georgia’s primary role in this network is to support the generation of currencies, revenues and profits via tax breaks and cheap energy, labour and land. Whilst previous work on cryptocurrencies highlights their materiality through their impacts (e.g. Atkins et al., 2021), our case study emphasizes ‘upstream’ forms of materiality – the materiality of technological ‘infrastructures’ that enable the aforementioned revenue generation.

We have also worked to deepen the geographical literature’s understanding of how ‘paper,’ ‘relational’ and ‘infrastructural’ factors – and the interplay between them – root particular companies’ operations in specific locations. We demonstrate the importance of key actors, in contrast to the GEN literature’s tendency to think in terms of collective actors. We emphasize the cooperation of state and corporate actors, as opposed to the tendency to see their relations as agonistic. And we highlight how advantageous regulatory environments are meaningful only in the context of enabling technologies, localized knowledge.

Bitfury’s activities more closely resemble a finance-adjacent GPN than a GFN. They exemplify the finance of production and the production of finance. Bitfury’s profits depend on assetization of and financial speculation on their products. That finance supports production (Coe et al., 2014), and production finance (Dörry, 2015, 2016) is not a new observation in the GEN literature. Our case study unites these two strands of literature, clearly illustrating how finance and production are tightly interwoven, particularly in producing certain, speculative asset classes. This topic deserves further investigation. Productive routes of inquiry include: tracing these places’ ‘offshoreness’ and potential overlaps between ‘data havens’ and ‘tax havens’ in providing emergent spaces; investigating the local development outcomes of these firms coupling with specific jurisdictions; and more closely investigating how and why other, non-datacentre (i.e. ‘relational’, ‘paper’ and ‘technical’) sites are integrated with the economic networks of cryptoasset firms.

Though Bitfury primarily produces ‘virtual’ products, material events and processes affect their operations (like any other company) because their digital operations remain predicated upon hardware and ‘infrastructure’. This is one example, based on one company in one jurisdiction. Future studies of the GENs of cryptoasset firms should consider how the interlacing of these aspects across the economic network works to bring lead firms to specific localities – and spatialize cloud technologies and place them in multiple dimensions. In this sense, if Bitcoin miners’ ‘ASIC clouds’ represent the first instance of a planetary-scale computational assemblage (Taylor et al., 2020), what sites, places and regions will be brought together – and how?

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research underpinning this paper has been partially funded by the European Research Council Advanced Grant “Algorithmic Societies - Ethical Life in the Machine Learning Age”. Grant code: 883107.