Abstract

Financial discipline and financialization are transforming Global Production Networks through growing pressures related to shareholder value, short-termism and new financial products and services. However, little focus has been devoted to exploring whether these processes are accelerating rates of sectoral convergence. As financialization creates new challenges and opportunities for non-financial firms, are we seeing greater levels of convergence between the financial and other sectors? If so, which sectors, in which countries and why? We explore these questions by analysing the structure and geographies of inter-sectoral mergers and acquisitions in and out of the financial sector. Drawing from a sample of 25,079 deals between 2001 and 2020, we reveal which sectors are buying and being bought by financial firms, the geographies of this process, trends over time and the key factors driving inter-sectoral activity. Analysed through the Global Production Networks 2.0 framework, and contributing to debates around financial discipline, our findings uncover the growing convergence of finance with other sectors through an increasing share of inward (non-financial firms acquiring financial firms) and outward (financial firms acquiring non-financial firms) merger and acquisition deals. However, far from homogenous, this process of convergence is shown to be temporally, sectorally and spatially uneven. This allows us to make two novel contributions. First, we provide fresh insights into the role of financial discipline in reconfiguring Global Production Networks at country-level. Second, we advance contemporary debates on convergence by revealing how, where and why the boundaries between the financial and other sectors are becoming increasingly blurred.

Introduction

A central aim of the Global Production Network (GPN) 2.0 theory is to examine the impacts of financial discipline on the strategies of firms and the structure of their networked relations (Coe and Yeung, 2019). Financial discipline refers to the financial actors, markets and institutions which organize and condition the geographies of production throughout the global economy (Yeung and Coe, 2015). In addition to shaping the financial architecture that governs global economic activity (Wade, 2007), financial discipline also refers to the challenges and opportunities presented to firms by financialization (Yeung, 2016). Broadly understood as the growing power of finance (Epstein, 2005), financialization reflects a shift in capitalism, albeit unevenly, whereby financial imperatives play an increasingly important role in how the world works (Pike and Pollard, 2010).

While research is beginning to explain the relationships between financial discipline, financialization and GPNs, sectoral convergence remains entirely overlooked as part of these interactions. By convergence, we mean the blurring of boundaries between economic sectors (Bröring et al., 2006). Convergence takes place through a variety of means, with inter-sectoral mergers and acquisitions (M&As) as a principal channel (Green, 2018) and one which has the capacity to harmonize financial and non-financial operations. Financialization has rendered M&As increasingly important as they provide a way for firms to grow their market share, reduce competition and capture new assets while simultaneously increasing their share price. As a result, M&As are now the leading form of foreign direct investment and the key conduit through which corporate control and economic decision-making power move between firms, places and people (Chapman, 2003). So far absent from the literature on financial discipline in GPN 2.0 is an understanding of whether financial and non-financial sectors are converging as their strategic interests become more closely aligned.

The overarching aim of this article is to analyse the structure and geographies of inter-sectoral M&As in and out of the financial sector. We draw from a sample of 25,079 M&A deals involving financial services (including insurance) firms throughout the period 2001–2020. This sample consists of intra-sectoral deals (financial firms acquiring financial firms) and two types of inter-sectoral deals: inward (non-financial firms acquiring financial firms) and outward (financial firms acquiring non-financial firms). Positioning our analysis at the global scale, we answer four interrelated questions. First, which sectors are buying and being bought by financial firms? Second, what are the geographies of this inter-sectoral activity? Third, how have these patterns evolved over time? And fourth, why are these patterns and trends occurring?

Answering these questions we reveal the temporal, sectoral and spatial convergence of finance with the rest of the economy. We highlight the growing convergence of finance with other sectors through an increasing share of inward and outward M&As. While convergence intensifies over time, it is highly uneven in terms of the sectors involved and the geographies of acquirer and targets firms. We reveal high levels of convergence between finance and some sectors (manufacturing, information and management of companies and enterprises (MOCE)) and much lower levels with others (agriculture, arts, education and healthcare). We also reveal the uneven geographical channels of convergence, with key trends including the rise of China, a dramatic pivot away from Europe, and the growing importance of offshore jurisdictions.

These findings provide two original contributions. First, we provide fresh empirical insight into how financial discipline is reconfiguring GPNs across diverse geographical settings (Yeung and Coe, 2015). Addressing a persistent research gap around how finance intersects with GPNs (Coe et al., 2014), our analysis breaks new ground by moving beyond the conceptualization of financial and business services (FABS) firms as intermediaries. Far from playing a clearly defined role based on providing access to finance, brokering knowledge and shaping the global financial architecture (Faulconbridge, 2019; Wade, 2007), we use inter-sectoral M&As to show how FABS firms are increasingly buying and being bought by firms from other sectors. This iterative process, which has accelerated since the early 2000s, helps us reconsider the position of finance in the global economy. It enriches our understanding of financial discipline by accounting for inter-sectoral convergence, highlighting how FABS firms play an active role in exercising power with rather than over other types of firms (Parnreiter, 2019). This allows us to present a more open, dynamic and reciprocal conceptualization of financial discipline, where financial integration is central, FABS firms are not just intermediaries, and financial imperatives are not simply dictated to but constantly negotiated between financial and non-financial firms. Second, and more broadly, we advance contemporary debates on convergence by revealing how, where and why the boundaries between the financial and other sectors are becoming increasingly blurred. In doing so we suggest that GPNs and the Global Financial Network (GFN), a conceptual framework that identifies the interlocking structures and relations of global finance and which will be explained in the following section, do not operate as separate and autonomous networks. Put together, these contributions move towards unravelling the complex relationships between financial discipline and convergence as part of GPN 2.0.

The rest of this article is structured as follows. The next section critically appraises the GPN and GFN frameworks, paying close attention to financial discipline, financialization and the role of M&As in financial sector convergence. Following on from this we explain the research design and data collection process. We then begin our analysis by presenting an overview of intra, inward and outward deals over time. Next we identify which sectors are buying and being bought by finance. This is followed by a section which reveals and explains the geographies of this inter-sectoral activity. Finally, we discuss our conclusions.

Situating finance in GPN 2.0

While GPN 1.0 broke new ground in terms of theorizing and analysing the networked relations of global economic activity (Coe and Yeung, 2015), its implicit focus on production resulted in a lacuna of understanding around the role of finance in shaping these networks. This is a significant omission considering that finance is a necessary input into all GPNs (Coe et al., 2014). GPN 2.0 aims to address this deficiency, amongst others, by placing greater emphasis on the causal mechanisms that underpin production networks (Coe and Yeung, 2015). This means paying closer attention to three competitive dynamics – the cost-capability ratio, market dynamics and financial discipline – in shaping and restructuring the spatial manifestations of production networks (Yeung and Coe, 2015). As part of bringing finance into closer dialogue with the coordination, spatial structure and concentration of power in GPNs, Coe et al. (2014) developed the GFN conceptual framework, outlining the interlocking structures of financial systems, markets and institutions. Mirroring the underlying rationale of the GPN framework, it provides a conceptual map of the actors, places and networks involved in the reproduction of global finance (Wójcik, 2018b).

The GFN is comprised of four key building blocks: financial centres, offshore jurisdictions, FABS firms and world governments. Financial centres are cities that host agglomerations of financial firms and institutions, existing as key nodes of financial decision-making power in the GFN (Cassis and Wójcik, 2018). Offshore jurisdictions are specialized territories that provide legal and regulatory flexibility to the owners of financial firms and assets located elsewhere (Wójcik, 2013). FABS are firms operating in the finance, insurance and real estate sectors, as well as other areas including law, accounting and business consultancy. As some of the most globalized firms in the world, FABS are the ‘multi-industry players’ that bridge the connections between financial centres and offshore jurisdictions (Yeung and Coe, 2015: 49). Finally, world governments refer to the leading central banks and other state authorities which have the capacity to enforce regulations and provide sovereign protection to the entire financial system (Wójcik, 2018a).

While the GFN has helped conceptualize the relational characteristics of global finance (Coe et al., 2014), it does not yet address some of the persistent gaps in our understanding of how finance intersects with GPNs (Coe and Yeung, 2019). Put differently, the GFN helps us understand the underlying geographies, mechanisms and actors of global finance but it does not tell us how these emergent structures then intersect with the geographies of production.

Enter financial discipline: As a central component of GPN 2.0, financial discipline refers to the ways in which financial actors organize and monitor the geographies of production throughout the global economy (Yeung and Coe, 2015). Underpinning financial discipline are processes of financialization, defined as the ‘increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies’ (Epstein, 2005: 3). While this definition provides a broad overview, most important in explaining the role of financial discipline in GPN 2.0 is corporate or firm-level financialization, a strand of research which focuses on the growing interconnections between non-financial firms and financial intermediaries, institutions and markets (French et al., 2011).

Understanding the core constituents of firm-level financialization can help us identify the specific ways in which financial discipline plays out (Keenan, 2020). For example, firms are being compelled to reconfigure their production networks through growing pressures to provide shareholder value (van Treeck, 2009), adhere to short-term financial targets and metrics (Dodig et al., 2015), increase M&A activity (Milberg, 2008), assetize value and income streams in new ways (Birch, 2017) and accrue more debt (French et al., 2011). These core constituents of financialization are therefore disciplining non-financial firms through creating financialized modes of competition that force them to compete in novel ways to match the expectations of financial markets and institutions (Williams, 2000).

Just as the processes of financialization are uneven, contested and contingent (Keenan, 2020), so too are the ways in which firms and their production networks respond to their myriad pressures (Yeung and Coe, 2015). There is no doubt that finance plays a causal role in coordinating the geographies of global production, however, this is by no means a standardized and uniform process, as it unfolds unevenly depending on the sector, firms and institutional settings involved (Yeung and Coe, 2015). Empirical research has captured this unevenness by revealing the role of financialization in stretching agri-food chains (Clapp, 2014), increasing rates of outsourcing and offshoring in the manufacturing of pharmaceuticals (Busfield, 2020), concentrating production in the global brewing industry (Keenan, 2020), creating excess capacity and greater financial fragility in South African platinum mining (Bowman, 2018) and shifting the strategic focus towards investments in financial assets in the automotive industry (do Carmo et al., 2019). These examples form part of a growing range of studies that highlight the role of financialization in shaping patterns of uneven development throughout contemporary capitalism (Pike and Pollard, 2010).

Addressing these new financial imperatives can impact other parts of a business. For example, downsize and distribute strategies may generate shareholder value by reducing costs but also result in redundancies and negatively impact employment (Lazonick and O’Sullivan, 2000). Financially disciplined firms may satisfy shareholders and financial markets but decisions made here could come at the expense of employee welfare, environmental concerns and longer-term planning horizons. Put simply, financial discipline is anything but inherently virtuous. It reflects the narrow focus of financialization which transforms relationships into transactions (Dembinksi, 2009).

Ultimately, financial discipline helps us understand how industries and their spatial configurations are being transformed as firms adapt to the challenges and opportunities presented to them by financialization (Yeung and Coe, 2015; Yeung, 2016). While it could be argued that financial discipline and financialization are one and the same, we do not use the terms interchangeably. This is because while financial discipline is inevitably underpinned by the processes of financialization, it also encompasses the laws and regulations which make up the global financial architecture (Wade, 2007) and form part of the wider structures and relations of the GFN (Haberly and Wójcik, 2022). In this sense, financial discipline refers to the longstanding formal institutions of the GFN, while also referring to a set of qualitatively new transformations induced by financialization.

Conspicuous by its absence in the financialization literature is an explicit treatment of sectoral convergence. Defined as the ‘blurring of boundaries between industries due to converging value propositions, technologies and markets’, convergence takes two forms; supply-side convergence, which relates to the application of standardized technologies across different industries; and demand-side convergence, which relates to evolutions in consumer preferences that require the merging of different products and services (Bröring et al., 2006: 488). Considering our empirical focus on financial discipline, we adapt these insights to put forward a definition of financial convergence as the merging of financial and non-financial sectors through inter-sectoral M&A deals.

M&As are central to processes of financial discipline, financialization and convergence. They play a crucial role in ensuring that GPNs and GFNs remain global and networked. In some ways, they support the development of firms, people and places through investment, while at the same time, they can act as a destructive force by reallocating labour and capital away from particular places and actors. M&As are categorized as being horizontal, vertical or inter-sectoral (Green 2018; Motis, 2007). Horizontal mergers happen between two companies operating in the same industry, vertical when two companies operate in the same production network (e.g. vertical integration) and inter-sectoral when two companies operate in entirely different industries or sectors (Green 2018). Whatever the type, there is always some degree of shift in decision-making power between the acquirer and target (Zademach and Rodriguez-Pose, 2009).

Most important for our analysis are inter-sectoral M&As. Linked to the rise of conglomerates in the 1980s and often described as a ‘past relic’, inter-sectoral M&As have made a comeback since the early 2000s (Lim, 2020: 47). Growing in number and value, their revival has been driven by the world's leading technology firms and the heightened integration of technology across all sectors and markets – for example, FinTech and BioTech (Heo and Lee, 2019; Lim, 2020). Inter-sectoral M&As underpin processes of convergence, which is increasingly seen as a way of enhancing competitive advantage (Heo and Lee, 2019).

Crucially, inter-sectoral M&As bridge GPNs with the GFN. This is because when financial and non-financial firms merge, so too do their networks and spatial entanglements. In this sense, M&As are a central mechanism in bringing together what would be separate sets of actors, relations and configurations. While GPNs and the GFN remain distinctive, M&A activity is a critical force in ensuring that these networks do not remain autonomous.

Building on these insights, the analysis of inter-sectoral M&As in and out of the financial sector allows us to explore the role of financial discipline as part of GPN 2.0. Strikingly, little to no research has explored the phenomenon of convergence within the context of GPNs. We do not know which sectors are converging, the geographies of these transformations, and the pace at which they are occurring. Extending and enriching the work of Coe et al. (2014), by addressing these unknowns we can begin to unravel the complex relationships between financial discipline, financialization and convergence, and consequently provide novel empirical insights towards a clearer understanding of finance as part of GPN 2.0.

Researching financial convergence through M&A data

We analyse all domestic and cross-border M&A deals valued at or above US$10m involving financial services and insurance firms throughout the period 2001–2020. This time period gives us full coverage of the 21st century at the time of writing. Deals were collected from the Zephyr database, a proprietary source of M&A, IPO, private equity and venture capital transactions with an unparalleled coverage of over 1.8 million deals. We then cleaned this data before undertaking a long and arduous process of geocoding to identify the headquarters address for all firms in the database.

While our database includes city-level information for each acquirer and target firm, our analysis is positioned at the global scale, with countries adopted as our unit of analysis. Analysing national and international trends allows for a comprehensive interpretation of where finance is situated as part of the global economy. This decision reflects the need to start this exploratory enquiry at the national level to paint a global picture before more detailed research can be undertaken (Coe and Yeung, 2019). This global approach, which does not exclude any region, also addresses concerns about an inherently Western and Eurocentric focus permeating financial geography (Gal, 2015).

Our economic sectors are defined using the North American Industry Classification System (NAICS). Developed in 1997 by the US Census Bureau, the NAICS structure consists of 20 economic sectors (Appendix 1). These sectors are assigned 2-digit codes, with further digits assigned to sub-sectors (maximum of 6). NAICS has been adopted throughout social science research and provides a detailed structure of contemporary economic activity (Kelton et al., 2008). The financial sector (NAICS52) includes banks, insurance firms and other financial institutions such as brokers and asset managers. While interrelated processes of globalization and financialization render it close to impossible to neatly define economic sectors, the NAICS structure provides the most suitable means of answering our research questions and generating fresh empirical insights on financial sector convergence.

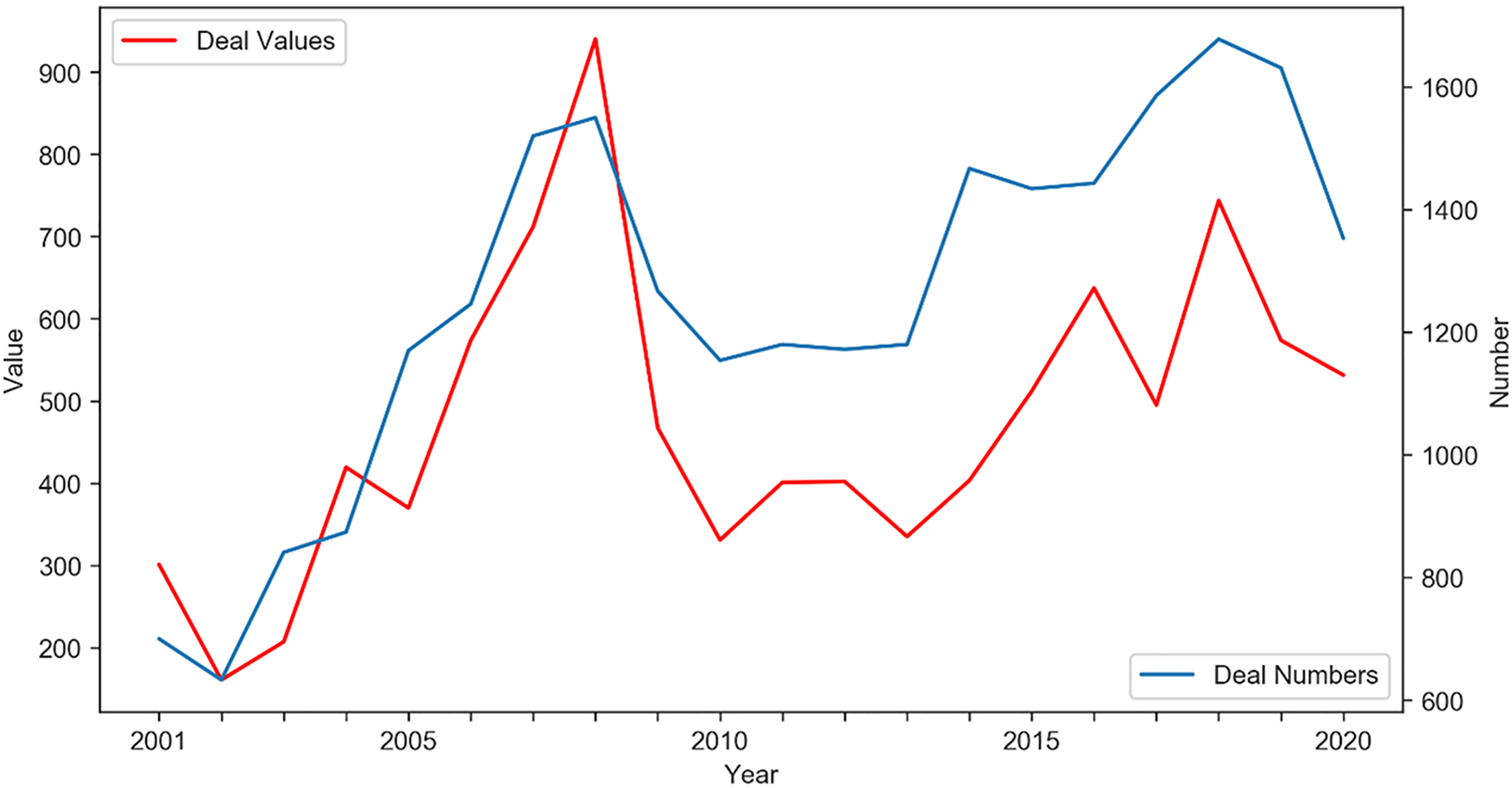

Our sample covers a total of 25,079 deals with a combined value of $9.52trn. This consists of 9947 intra-sectoral deals worth $4.61trn, 4612 inward deals worth $1.58trn and 10,520 outward deals worth $3.32trn. Figure 1 provides an overview of the entire sample, with one line showing the total number of M&A deals each year and the other showing the total value. It highlights the significant impact of the financial crisis on both of these variables. It is notable that by 2018 the value of deals exceeded that in 2007, and the number surpassed the previous all-time record of 2008. As later analysis will show, this points towards newer and different types of financialization and financial integration.

Number and value (US$bn) of merger and acquisition (M&As) deals involving financial firms (2001–2020).

As reflected in Figure 1, we analyse both the number and value of deals. While a $10m limit means that our analysis misses smaller deals, this limit was necessary given the size of the database, the time period we analyse, and most importantly the complexities of the geocoding process. We focus more on deal value and this is because analysing the number of deals helps us identify wider geographical trends and patterns but focusing on value helps us explore shifts that are likely to have a greater impact on the structure and spatial composition of GPNs.

The evolution of financial sector M&A deals over time

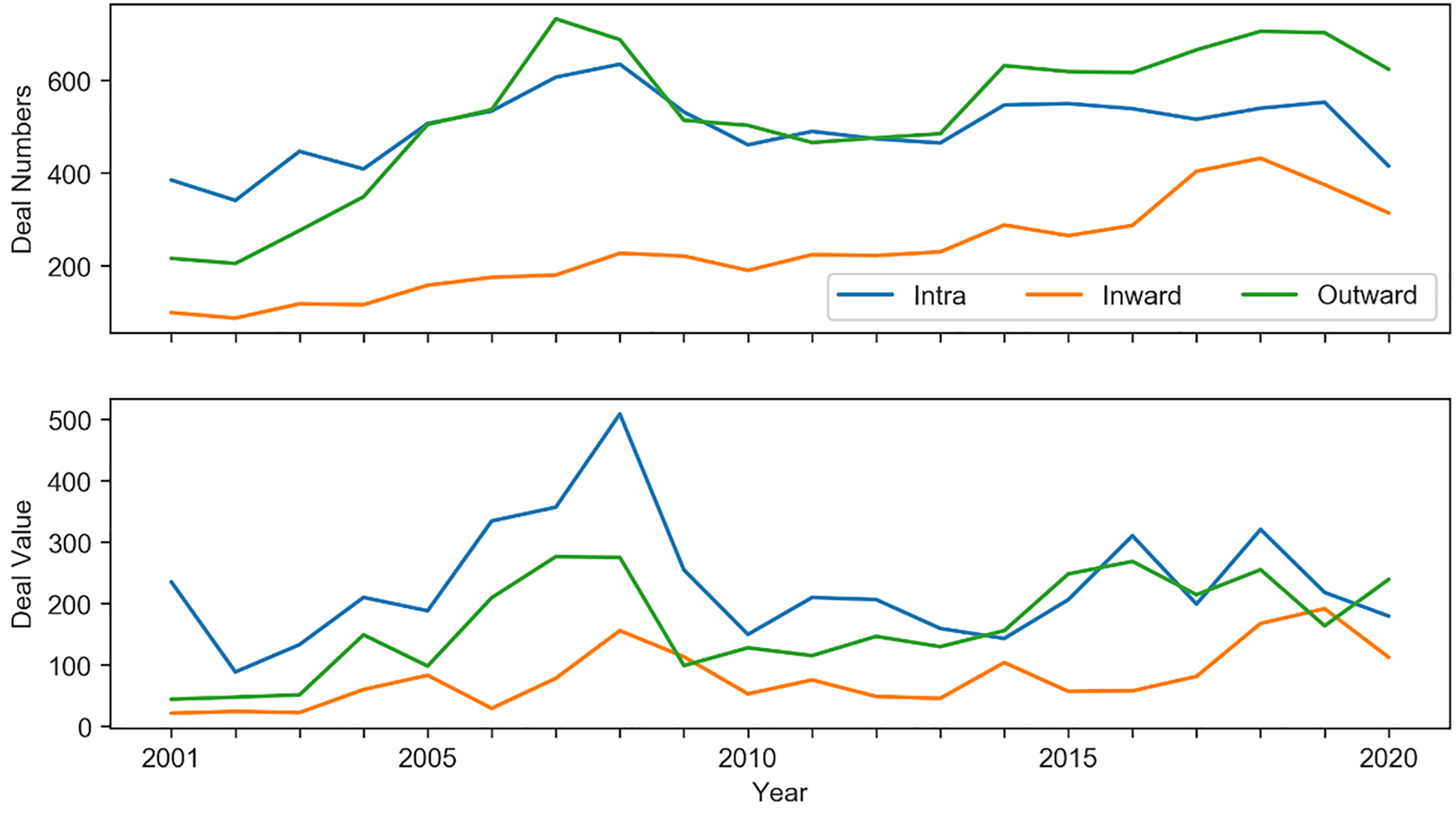

In terms of inter-sectoral M&A activity, financial convergence takes place through a combination of outward (financial firms buying non-financial firms) and inward deals (non-financial firms buying financial firms). Figure 2 charts the evolution of intra, inward and outward deals by number and value.

Number and value (US$bn) of intra, inward and outward deals (2001–2020).

At the start of the period, the number of intra deals (385) was greater than the number of inward and outward deals combined (315). Leading up to 2007, all types of deals involving the financial sector were on the rise, but outward deals were growing particularly fast, highlighting the outward expansion and buoyancy of the financial sector prior to the crisis. In 2008, both intra and outward deals declined, but inward deals continued to rise, reflecting the acquisition of financial firms by national governments as part of state-funded bailouts (Grossman and Woll, 2014). While the number of intra and outward deals never recovered from their pre-crisis heights, the number of inward deals more than doubled between 2007 and 2018 (180 to 432). By 2020 and the start of a pandemic induced slowdown, the combined share of inward and outward deals (69%) was more than twice the share of intra deals (31%). Considering that in 2001 the share of intra deals (55%) was greater than the combined share of inward and outward deals (45%), this reveals a stark turnaround over a 20-year period.

Deal values underscore these trends. In 2001, the value of intra deals ($235bn) stood at over three times the combined value of inward and outward deals ($65bn). By 2020, the combined value of inward and outward deals ($351bn) was close to double the value of intra deals ($180bn). These trends are reflected to some extent by changes in the average deal values. Between 2001 and 2010, intra deals had the highest value ($487m), followed by inward ($382m) and outward deals ($286m). Throughout 2011–2020, intra ($423m) and inward ($299m) average deal values declined, whereas the average outward deal value increased ($321m). This suggests that it became cheaper to acquire financial firms following the financial crisis but more expensive for financial firms venturing into other sectors. Overall, the data shows that the composition of the financial sector is changing. With declining rates of intra-sectoral consolidation and the growing number and value of inward and outward deals, it appears that the core of the financial sector is being hollowed out, with financial firms expanding outwards and non-financial firms developing their own financial capabilities through strategic acquisitions.

Growth in financial convergence can be partly explained by the changing nature of M&As. Inter-sectoral M&As were traditionally seen as a way for firms to reduce risk through diversification (Lim, 2020) but this has changed under financialized modes of competition, which now compel firms to acquire unrelated businesses to generate shareholder value and capture financial synergies (Heo and Lee, 2019). Importantly, we cannot unequivocally state that financial discipline is the only or even the main driver of convergence. It is impossible to fully isolate causation and identify motivations behind M&As, which are diverse, complex and contingent (Green, 2018). For example, while financial discipline has undoubtedly been important to the growth of FinTech, technological innovations have played an equally central role in the convergence of finance and technology (Wójcik, 2021). Hence, financial discipline on its own does not provide a universal explanation for convergence. We do believe, however, that the convergence we observe reflects financial discipline because of the size, scale and pervasiveness of financialization throughout the global economy. Put differently, while our analysis provides clear evidence of financial convergence, we are cautious in terms of how we interpret these empirical observations.

Overall, data from this section suggests that while the internal consolidation of the financial sector has slowed down, financial firms are simultaneously expanding outwards while becoming more susceptible to non-financial ownership. Conventional financial consolidation seems to have lost pace, with financial regulators around the world weary of too-big-to-fail banks in particular (Haberly and Wójcik, 2022). As financial convergence has intensified, and the boundaries of the financial sector have become more porous, it is important to consider which sectors are buying and which are being bought.

Who's buying and who's selling: Financial convergence and sectoral unevenness

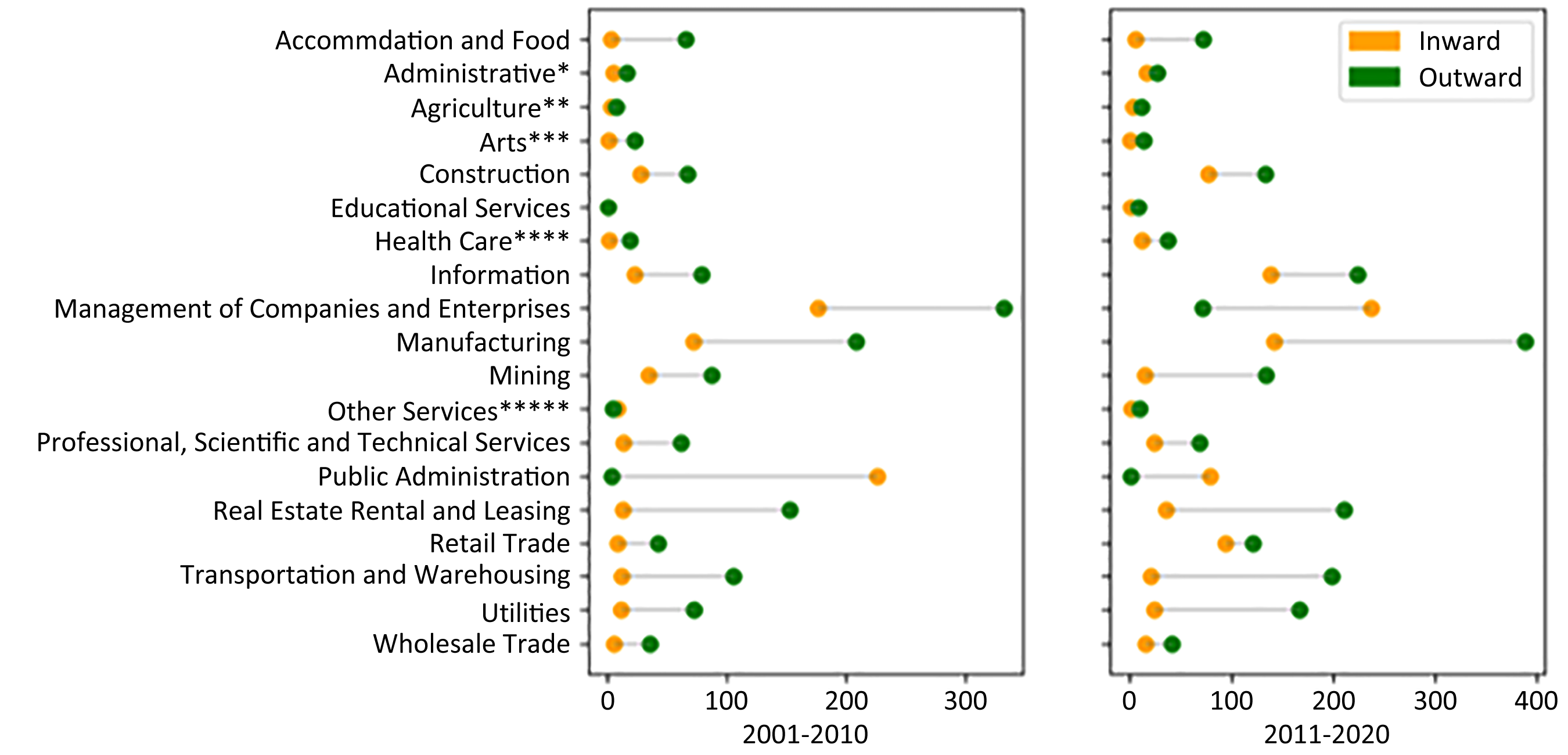

Financial convergence is sectorally uneven, with firms from some sectors more likely to buy or be bought by financial firms than others. Figure 3 reveals the value of inward and outward deals by sector between 2001 and 2010 and 2011 and 2020. Showing the absolute and relative positions of all sectors from the NAICS structure, we split them into two time periods to highlight the evolution of sectoral unevenness over time.

Value (US$bn) of inward and outward deals by sector in 2001–2010 (left panel) and 2011–2020 (right panel).

Between 2001 and 2010, there were 6097 inter-sectoral deals involving the financial sector. Valued at $2021bn, this consisted of $642bn inward (32%) and $1379bn outward deals (68%). The sectors converging the most with the financial sector throughout this period were MOCE, manufacturing and public administration. MOCE made up $176bn (27%) worth of inward and $332bn (24%) of outward deals. MOCE consists of three sub-sectors which are offices of bank holding companies, offices of other holding companies and corporate, subsidiary and regional managing offices. The most prominent sub-sector of MOCE was offices of other (non-bank) holding companies, defined as firms that own a ‘controlling interest or share in the capital of other subsidiaries for the purpose of permanent control and management of their activities’ (Madina, 2021: 37). This prominence of holding companies in M&A activity is high as they support the development of conglomerate networks under a standardized and unified corporate structure (Ibid). Second, manufacturing made up $72bn (11%) worth of inward and $209bn (15%) of outward deals. This level of activity reflects the growing pace of innovation in FinTech, as well as the high share of the manufacturing sector relative to global economic activity. Third, public administration was the only net acquirer of financial firms throughout this period. The $226bn (35%) worth of inward deals, in stark contrast to the $3bn (<1%) of outward deals, reflects the publicly funded bailout of banks following the global financial crisis (Grossman and Woll, 2014). This scale of acquisition from national governments was exceptional, matching the severity of the crisis.

Between 2011 and 2020, there was a total of 9035 inter-sectoral deals involving the financial sector. Valued at $2881bn, this consisted of $943bn of inward (33%) and $1938bn of outward deals (67%). MOCE (25% of inward deals, 20% of outward deals) and manufacturing (15% of inward deals, 20% of outward deals) continued to feature prominently throughout this period. Importantly, MOCE joined public administration as the only other net acquirer of financial firms. Between 2011 and 2020, MOCE made up $237bn (25%) of inward deals and only $72bn (4%) of outward deals. This is an important development that highlights a shift in the relationships between MOCE firms and finance. As holding companies make up a large share of the MOCE sector, this transformation reflects the wider trend of a growing number of inward deals, as financial firms are increasingly being bought through holding companies and assimilated into wider conglomerate networks (Madina, 2021).

The growth in conglomerate ownership models also relates to the emergent pressures of financialization. The core motivation behind conglomeration is financial synergy with conglomerate models offering greater financial advantages compared to unified corporate structures (Kumar, 2019). The management of subsidiary businesses through a holding company reduces financial risk through the distribution of liabilities and separation of investments, allows for lower debt financing costs through economies of scale and scope, and generates financial savings through centralized corporate functions (Feldman, 2019). The predominance of MOCE firms in our analysis, therefore, suggests that financial discipline might not only be encouraging convergence but also influencing the types of corporate models being used to enact it.

Across both time periods, there was also a significant growth in the information sector, which increased its share of inward deals from 4% to 15% and outward deals from 6% to 12%. The growing convergence between finance and information reflects recent developments in FinTech. While finance and information technology have always been intertwined (Knight and Wójcik, 2020), our data supports the argument that the scale and pace of FinTech innovations since 2008 reflect a new and distinctive era in its trajectory (Arner et al., 2016).

Another key sector, particularly in terms of outward deals, is real estate, rental and leasing. Growing convergence between finance and these types of firms is linked to the financialization of land, real estate and housing (see Aalbers, 2020; Christophers, 2017). Decades of pervasive, albeit uneven, processes of neoliberalization and financialization have rendered real estate and housing ‘just another asset class’, paving the way for financial firms to take direct ownership of rental and property companies (van Loon and Aalbers, 2017: 221). Equally, albeit to a much lesser extent, real estate firms have also acquired financial firms to help develop their own in-house financing and extend their property networks (KPMG, 2018).

Focusing on inward deals, while there are limits to which financial firms can integrate a variety of non-financial services within their structures, the expansion of non-financial firms into finance does not face such limits. As part of the FinTech revolution, finance is becoming more modular, digitized, and akin to a set of functions that can be delivered through various platforms and apps (Lai and Samers, 2020). This makes it easier, cheaper and more attractive, as well as more important for non-financial firms to develop their own financial capabilities. Rather than procure external financial services, non-financial firms may acquire financial firms to develop their knowledge and expertise, as well as in-house payment, credit and insurance systems (Buchanan and Cao, 2018; Wójcik, 2021). It is important to acknowledge that FinTech is not exclusively driven by the financial sector. FinTech products and services are being developed through both outward and inward deals. Consider that 58% of FinTech patents in the United States come from non-financial firms (Wójcik, 2021; Chen et al., 2019). This shows how the boundaries between finance and technology are blurring, with firms ‘becoming financial actors as well as ‘productive’ ones’ (Lai and Samers, 2020: 725).

Crucially, the pressure to internalize financial capabilities extends across sectors. Financialization has increased the number and types of financial functions which GPNs rely on (Coe et al., 2014). Retail firms require cashless and online payment systems, car manufacturers require credit and insurance platforms and management consultancy firms require financial knowledge and expertise to support clients. Importantly, these transformations also relate to the increased servitization of the global economy (Vandermerwe and Rada, 1988). Firms across all sectors are adding value to their operations by providing a wider range of services, which subsequently transform GPNs, creating new challenges and opportunities (Kastalli and Van Looy, 2013). While the provision of financial services forms only one part of the servitization of economic activity, it demonstrates how financial discipline intersects with wider economic processes in the mediation of GPNs.

Ultimately, findings from this section point towards a much broader and dynamic conceptualization of financial discipline as part of GPN 2.0. Above and beyond financial discipline reflecting the core constituents of financialization such as shareholder value and new financial metrics and logics (Yeung, 2016), our analysis also emphasizes the importance of convergence through revealing processes whereby non-financial firms are acquiring and being acquired by financial firms. As reflected in the growing number and value of inward deals, convergence suggests that financial discipline is not exclusively projected outwards by financial firms, as there appears to be a growing impetus from within non-financial firms to develop their own financial capabilities. In this sense, FABS firms are simultaneously reshaping GPNs by exercising power over non-financial firms through enacting the rules and regulations of the global financial architecture (Wade, 2007), while also actively taking part and exercising power with actors in non-financial sectors through M&A activity. This suggests that financial discipline is much more than just financial actors governing their non-financial counterparts from a position of power and authority but rather more about the closer integration of these different types of actors through the alignment of strategic goals and preferences under the conditions of financialization.

The uneven geography of financial sector M&A deals

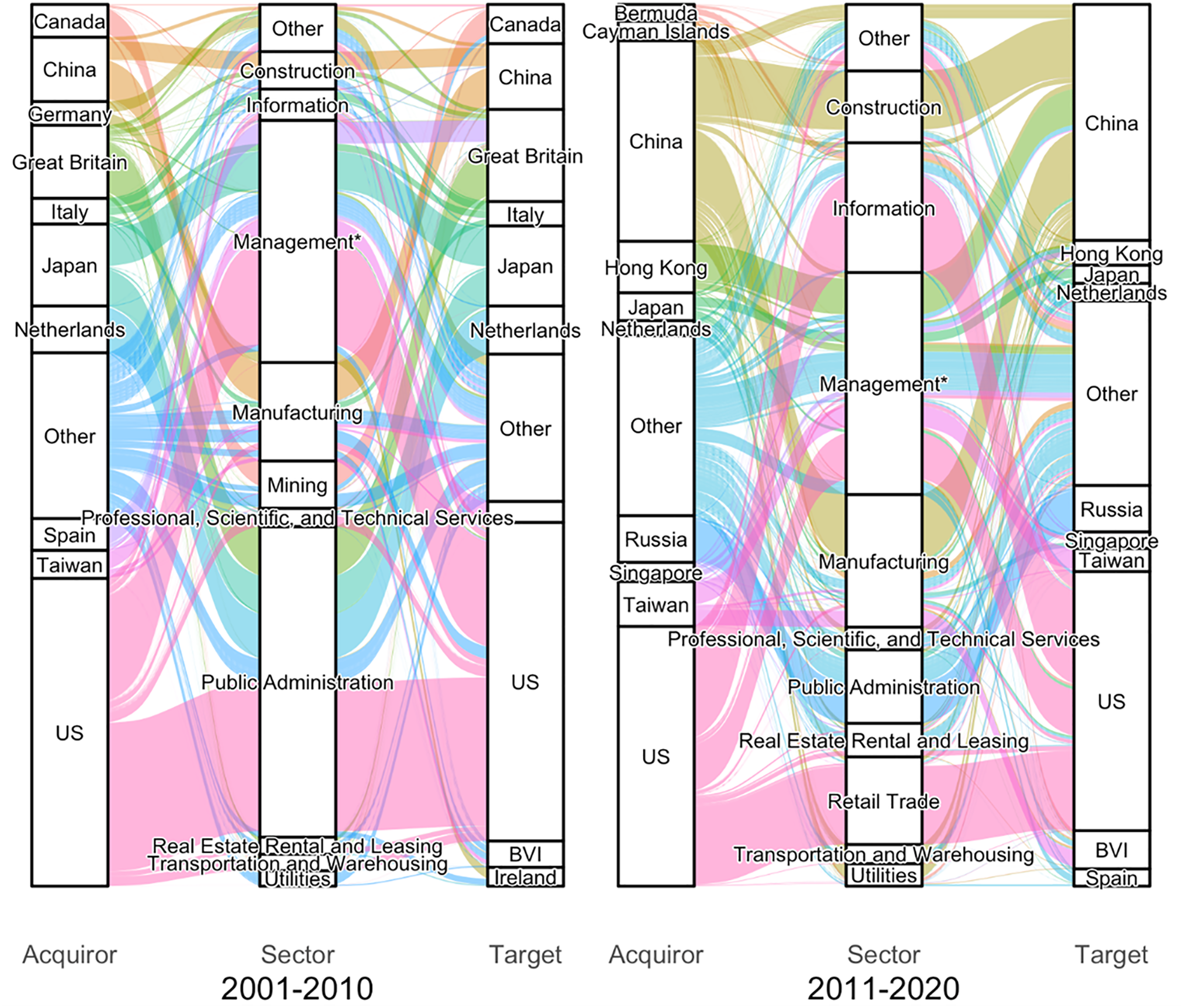

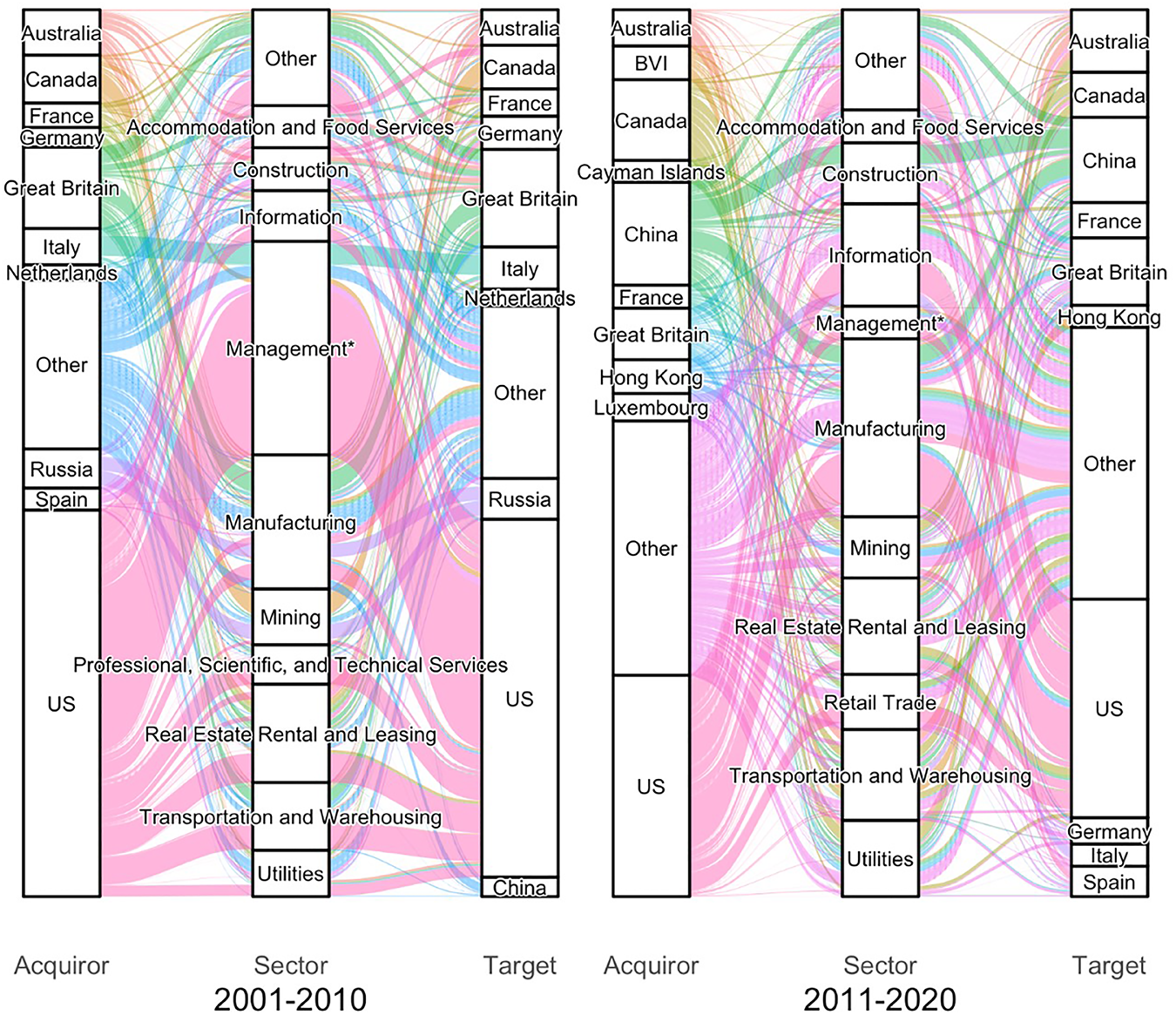

Just as the sectors involved in financial convergence are uneven, so too are the geographies. Acquirer and target firms are unevenly distributed across countries. This unevenness is driven by political economic, institutional and cultural conditions, as national economic specialization has strengthened the ties between particular countries and sectors. Figures 4 and 5 reveal the geography of inward and outward deals. They measure value and include the top 10 acquirer and targets countries to show the main geographical patterns and country-sectoral channels of convergence. Broken into two time periods (2001–2010 and 2011–2020), they depict the evolution of geographical patterns over time.

Geography of inward deals by value (US$bn) – by top 10 acquirer and target countries in 2001–2010 (left panel) and 2011–2020 (right panel).

Geography of outward deals by value (US$bn) – by top 10 acquirer and target countries in 2001–2010 (left panel) and 2011–2020 (right panel).

Figure 4 reveals the shifting geographies of inward deals. From left to right, it shows the country of the non-financial firm making the acquisition, the sector they come from and the country of the financial firm that has been targeted. Between 2001 and 2010, firms from the United States made up the most acquisition value (35%), followed by Japan (9%), Great Britain (8%) and China (7%). This geography was mirrored by the targets, with the United States (36%), Great Britain (10%), Japan (9%) and China (8%) leading with the largest shares. Acquisition value in 2011–2020 was dominated by the United States (29%) and China (23%), and again mirrored in terms of targets, with the United States (29%) and China (27%) accounting for a significantly higher share than any other country. While this data included both domestic and cross-border deals, the alignment between acquirer and target countries is likely to reflect the importance of geographical proximity in M&As and the tendency to invest in the same country (Zademach and Rodriguez-Pose, 2009).

Considering changes over time there are three key trends worth emphasizing. First, we see the rapid rise of China as both an acquirer and target, with a threefold increase in its share of acquisition value, from 7% to 23%. This rise reflects the growth of the domestic Chinese economy and the government-supported ‘go-global policy’, with Chinese firms becoming more adept at acquiring foreign firms and entering overseas markets (Caiazza et al., 2015: 249). At a more granular level, considering country-sector combinations, Chinese acquirers of financial firms are more likely to be based in the construction and manufacturing sectors, whereas the US acquirers are more likely to be based in information, MOCE and retail trade. These differences can be attributed to political, economic and geopolitical conditions. Chinese information sector firms have been confronted with a mixture of political, regulatory and cultural barriers when attempting to buy foreign firms, mainly due to assumed security threats to digital infrastructures of the host countries. For example, firms such as Huawei attempting to invest in the United States have faced regulatory obstacles, particularly from the Committee of Foreign Investment, which have limited their overseas expansion (Wu et al., 2011). In contrast, driven and reflected by the scale and success of China's Belt and Road Initiative, Chinese manufacturing and construction firms face far fewer obstacles and have been much more successful in acquiring foreign competitors, particularly throughout developing countries, where state-supported Chinese investments have cultivated stronger diplomatic ties. These so-called ‘flying geese’ have been most successful in Africa, exporting Chinese manufacturing capacity abroad and structurally transforming parts of the continent through infrastructural megaprojects (Brautigam et al., 2018: 29).

In stark contrast to the ascendancy of China, there has been a dramatic pivot away from Europe. While Germany, Great Britain, Italy, the Netherlands and Spain were in the top 10 acquirers between 2001 and 2011, in the second decade only the Netherlands was there. This sharp decline in European acquisitions is likely to be the result of the combined impacts of the global financial and Eurozone crises, which not only curtailed the expansion strategies of already highly leveraged European non-financial firms but also reduced the valuations of Euro-denominated financial firms (Erel et al., 2012). This decline in inward deals reflects wider economic trends impacting Europe, particularly its declining competitiveness in many areas and diminishing share in global manufacturing (Marschinski and Martinez Turegano, 2019).

Third, there was significant growth across offshore jurisdictions as acquirers. In the second period, we see the emergence of Bermuda (2%) and the Cayman Islands (2%) amongst the top 10 acquirer countries. This is significant and highlights the intersection of GPNs and GFNs. Our findings shows that non-financial firms owned through offshore jurisdictions are increasingly acquiring financial firms based elsewhere. This suggests that the functions performed by offshore jurisdictions are increasingly important to financial convergence (Haberly and Wójcik, 2022). Put simply, we see a growing trend of financial convergence and conglomeration through offshore jurisdictions.

Figure 5 reveals the shifting geographies of outward deals. From left to right, it shows the country of the financial firm making the acquisition, the sector they are acquiring from and the country of the non-financial firm that has been targeted. Between 2001 and 2010, the United States has the largest share of acquisition value (44%) and the UK the second (9%). While the United States held its position at the top during the second period (25%), China had the second largest share (12%). This development was matched in terms of target value, with the United States (40%) and Great Britain (11%) leading in the first period, followed by the United States (25%) and China (10%) leading in the second period.

In analogy with inward deals, we see the growing position of China, a decline in European countries as acquirers and the emergence of offshore jurisdictions. While this reveals overarching similarities between the evolving geographies of inward and outward deals, some important differences exist. First, Chinese firms grew their share of both types of deals but had a much higher share of inward (23%) than outward (12%) deals during the second period. This makes sense considering the historical concentration of power in the GFN and the relatively weaker, albeit rising, power and influence of Chinese financial firms (Haberly and Wójcik, 2022). While the recent rise of Chinese financial firms has started to transform the country's position in the GFN (Wójcik, 2018a), the history of Chinese economic development and state capitalism has supported production over services. This means that while Chinese manufacturing and construction firms have achieved world-leading product-quality standards and successfully acquired overseas assets, Chinese services and financial firms often lag behind (Brautigam et al., 2018).

Second, we see a decline in European countries as acquirers in inward deals but not to the same extent as in outward deals. This reflects the stickiness of power in the GFN and the ability of Western financial firms to retain more global influence than their non-financial counterparts (Haberly and Wójcik, 2022). Third, we see offshore jurisdictions emerging as key acquirers in outward deals – Cayman Islands (2%), Luxembourg (3%) and the British Virgin Islands (BVI) (4%) – but these are not the same as the offshore centres in the top 10 of inward deals – Bermuda and Cayman Islands. While we tend to homogenize offshore spaces, this finding suggests a level of specialization in terms of the types of functions these jurisdictions perform as part of GPNs and GFNs.

More generally, and in contrast to the geography of outward deals, we see the prominence of Canadian financial firms acquiring targets from the mining and utilities sectors. These sectors include all firms attached to the production and distribution of renewable and non-renewable forms of energy. This trend not only reflects the size and strength of these sectors as part of the Canadian economy but also reveals the growing convergence of finance and energy. Albeit to a lesser extent, Australia also contributes to this trend. Both countries have large and growing institutional investors based on their funded pension schemes and natural resource exports.

In overview, spatial disparities in convergence emerge as a result of the inherent unevenness of financial discipline, as it unfolds differently depending on both the sector and the geographical context through which it is enacted. Political economic, institutional, regulatory and even cultural conditions shape the nature of financial discipline, partly determining who is involved, the powers they have and the challenges and opportunities they face. While the need for financial capabilities is universal, the pace, scale and nature of financialization is not, as sectors and countries undergo different types and magnitudes of transformations (French et al., 2011). Put simply, financial convergence is heterogeneous. It is mediated by the agency of firms and the geographies in which they operate. Our country-sectoral channels of convergence speak to this idea by revealing how different national financial sectors are more or less likely to converge.

Conclusions

The overarching aim of this article has been to analyse the structure and geographies of inter-sectoral M&A deals in and out of the financial sector. Drawing from our sample of domestic and cross-border M&A deals throughout the period 2001−2020, we revealed how patterns of inter-sectoral activity have evolved over time, which sectors are buying and being bought by financial firms, the country-sectoral channels of convergence, and the motivations behind this convergence. Analysed through the GPN 2.0 framework and paying close attention to financial discipline (Yeung and Coe, 2015), we have identified temporal, sectoral and geographical unevenness in financial sector convergence.

In terms of key findings, we have shown how inward and outward deals have grown their share of financial sector M&A activity over time. With a slowdown in intra-sectoral consolidation, a growing share of inter-sectoral deals havs reconstituted the boundaries of the financial sector. Importantly, while convergence between finance and other sectors is widespread and increasing, it is not sectorally and geographically homogenous. There are differences in the types of sectors buying and being bought by finance and in the country-sectoral channels of convergence. This unevenness is constantly shifting and evolving, exemplified by the rise of Chinese firms in acquisitions, the pivot away from Europe, and the growing importance of offshore jurisdictions.

In terms of looking forward, our findings suggest that the need to internalize and autonomize financial capabilities is only likely to become more urgent following the global pandemic. COVID-19 has revealed the weaknesses and vulnerabilities of GPNs, as repeated lockdowns, labour shortages and rising inflation have created frictions in the production and distribution of goods and services (Javorcik, 2020). These frictions have exposed tensions between efficiency and resilience, forcing firms to develop more robust and agile production networks to mitigate disruptions (Hobbs, 2020). Regardless of whether firms decide to maintain more efficient just-in-time networks or establish more resilient local networks, financial knowledge is essential, and is available and developed by FABS firms helping firms restructure their networks through expert legal, tax and procurement advice. Problems with production networks translate into more demand for financial expertise. Given the strategic importance of these types of decisions, it is reasonable to expect rates of financial convergence to rise.

Our findings lead to two key contributions. First, our analysis highlights the role of financial discipline is transforming GPNs, while also providing a more nuanced, comprehensive and holistic understanding of what financial discipline is. Much more than non-financial firms responding to the pressures of shareholder value, short-termism and financial metrics and logics (Yeung, 2016), our findings point to a qualitatively different form of financial discipline centred around convergence through inter-sectoral M&As. The challenges and opportunities of financialization mean that we see more inter-sectoral acquisitions as non-financial firms seek financial knowledge and expertise to compete, while financial firms also seek investment opportunities outside of the financial sector. Highlighted by the increasing share of both inward and outward deals, power is not exclusively projected outwards by the financial sector, as greater levels of financial integration through M&A activity mean that FABS firms play an active role in exercising power with rather than over other types of firms across a variety of different sectors (Parnreiter, 2019). M&A analysis, therefore, allows us to present a more open, dynamic and reciprocal conceptualization of financial discipline, where financial integration is central, FABS firms are not just intermediaries and financial imperatives are not simply dictated to but negotiated between financial and non-financial firms.

Second, and more broadly, we advance contemporary debates on convergence by revealing how, where and why the boundaries between the financial and other sectors are becoming increasingly blurred. Fundamentally, our findings suggest that GPNs and the GFN do not operate as separate and autonomous networks. Our M&A analysis demonstrates how these networks coalesce around key sectors and geographies, as financialization incentivizes inter-sectoral convergence and leads to the concentration of economic decision-making power in particular firms and places. This novel contribution not only demonstrates how porous the boundaries of the financial sector are but also encourages us to reconsider how and whether we need to distinguish the geographies of finance and production throughout the global economy.

While we have provided a broad overview of the types of sectors converging with finance, more finely grained empirical studies are required to unpack this process further. Our findings on convergence take the first step and provide fresh evidence around a new kind of financial discipline but more in-depth and qualitative analysis is required to explain why these transformations are occurring. Perhaps most importantly, and based on acknowledging that financial discipline does not provide a universal explanation for convergence, there is little understanding of what the different and often competing motivations behind sectoral convergence are and how existing geographies of finance, production and consumption are being transformed as a result. These ideas provide more opportunities to explore the nature, impacts and geographies of financial discipline, pushing forward GPN 2.0 and shedding new light on the position of finance in the global economy.

Footnotes

Acknowledgements

This research was supported by funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement No. 681337). All errors and omissions are the sole responsibility of the authors.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the H2020 European Research Council (grant number 681337).