Abstract

Lead firms play a dominant role in the governance structure of conventional global production network (GPN) analyses but this framework is not fully applicable in sectors where (new) regulations, technologies and subsequent market changes have a disruptive effect on its governance structure. This paper proposes an analytical framework to examine how disruptive effects of industrial megatrends in forms of new regulations and technologies and the subsequent market changes could alter the competitive dynamics between lead firms and their tier-I suppliers. Although lead firms are becoming more specialized and highly efficient in specific product segments, they may not always have inter-firm control over their tier-I suppliers. GPN boundaries become more permeable when there is an external shock, such as new regulations or massive shifts in consumer demand, or the entrance of an entirely new lead firm, possibly due to a technological breakthrough or innovative use of existing technologies in a product. This external shock could have disruptive effects on the GPN, from the exit of current lead firms to the entrance of new tier-I suppliers or lead firms. Consequently, a reconstituted GPN with a newly established boundary is then produced. Applying the analytical framework to the automotive industry, it is argued that selected (and new) systems suppliers with expertise in micro-electronics are not only in a prime position to capture the value generated by the increasingly stringent regulatory environment on safety and environmental standards, but also more resilient than the incumbent automakers to three emerging megatrends: electrification, digitalization and autonomous driving.

Keywords

Introduction

Lead firms, especially under a captive mode of governance, play a dominant role in the governance structure of global value chain (GVC) or global production networks (GPN) analysis (Coe and Yeung, 2015; Gereffi and Lee, 2016; Humphrey and Schmitz, 2002). To retain their competitiveness, lead firms can either establish inter-firm partnerships with strategic partners or externalize risk by outsourcing production to external suppliers and maintain control over the production processes and the quality of products through inter-firm control (Coe and Yeung, 2015: 135–142). The dominance of a few powerful lead firms in the automotive industry and their weak linkages with domestic suppliers is well documented (Pavlínek, 2018; Sturgeon and Van Biesebroeck, 2011; Sturgeon et al., 2008, 2009).

The automotive industry has, however, undergone significant restructuring by moving to a modular architecture since the 1990s. Lampón et al. (2017) have highlighted the important roles of modular suppliers, those tier-I suppliers with the capabilities of designing and manufacturing sub-systems of components, have on the development of modular platforms by automakers. The recent massive global recalls of Takata’s airbags revealed the reliance of automakers on tier-I suppliers. Although 13 automakers have spent US$136 billion on recalling affected vehicles (Financial Times, 19 March 2018), another two major airbag manufacturers (Autoliv and ZF-TRW) do not have enough spare capacity to produce an additional 42 million airbags to replace the ongoing recalls (Consumer Reports, 2021). This example suggests that the relationship between automakers and their tier-I suppliers are dynamic and symbiotic.

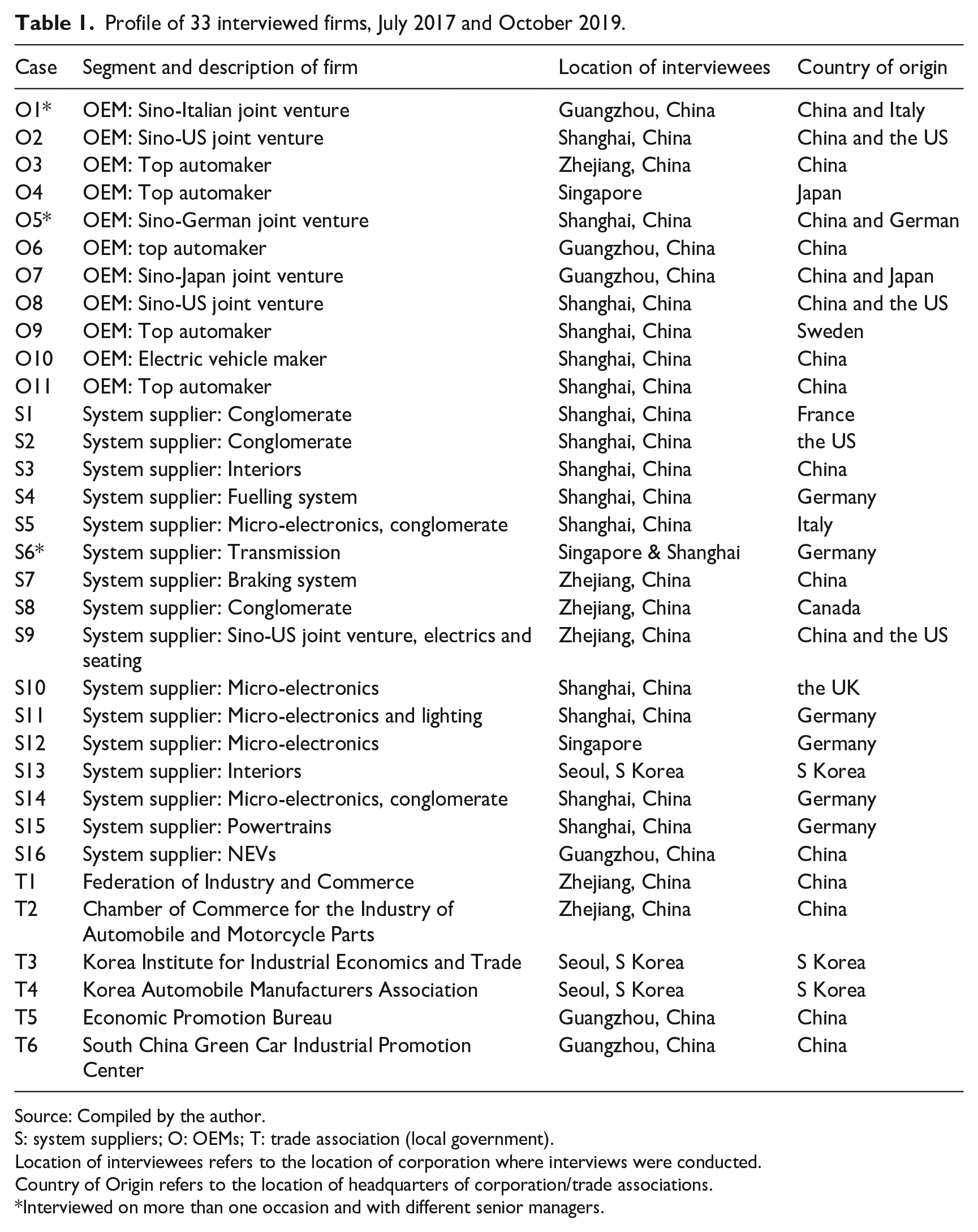

The increasingly stringent emission controls for vehicles with internal combustion engines (ICEs) pushes the automotive industry towards electrification and digitalization. The massive push of European countries to adopt new energy vehicles (NEVs) facilitates the phasing-out of ICEs-driven vehicles. In addition to disruptive impacts of industrial megatrends affected by regulatory and technological developments on the GPNs, the rise in consumers’ environmental awareness further facilitates the change in market demand and thus the competitive dynamics between automakers and their tier-I suppliers. This paper has two objectives. First, I propose an analytical framework to examine the impact of industrial megatrends on inter-firm relationships, especially the complexities and competitive dynamics between lead firms and their tier-I suppliers. Second, I use the automotive industry as a case study to illustrate how the analytical framework operates and why some automakers are unable to maintain their dominance over tier-I suppliers under the emerging industrial megatrends: electrification, digitalization, and autonomous driving. To achieve these research objectives, I conducted in-depth interviews in 33 automotive firms to ascertain how (external) factors could have a disruptive impact on the competitive dynamics between automakers and their tier-I suppliers in Asia between July 2017 and October 2019 (Table 1). All the interviews were semi-structured to facilitate the conversational flow and allow follow-up observations, and each interview lasted for at least an hour. In most firms, I interviewed two to five experienced senior managers (Presidents, Vice-Presidents, Global Sourcing Managers), and the sample includes eleven automakers (including 10 of the top-15 automakers and one battery electric vehicle maker), 16 of the top-100 suppliers and six trade associations. For two particular automakers, I conducted three interviews with different managers from their headquarters and their joint ventures for triangulation. Although interviewees are based in Asia (mostly China), the collected empirical information is applicable to the automotive industry as informants are senior executives with solid work experience in either global automobile giants or their key tier-I suppliers, for example, they were based in various countries before assigning to lead the management teams in Asia. Importantly, the megatrends and its market dynamics in Asian automotive industry, especially in Japan, South Korea and China, is effectively the same as in the global market. To anonymize the interviewees, I refer to all primary materials related to a specific firm by these abbreviated codes: S = systems suppliers, O = OEMs (original equipment manufacturers, i.e., automakers), T = trade association (or just field survey in other cases) and the dates of interviews in this paper.

Profile of 33 interviewed firms, July 2017 and October 2019.

Source: Compiled by the author.

S: system suppliers; O: OEMs; T: trade association (local government).

Location of interviewees refers to the location of corporation where interviews were conducted.

Country of Origin refers to the location of headquarters of corporation/trade associations.

Interviewed on more than one occasion and with different senior managers.

Different from the commonly adopted analytical approach which focuses on inter-firm relationships and regional development (McGregor and Yeung, 2022), this paper complements the generic GPN framework by proposing an analytical framework to examine how disruptive effects of industrial megatrends in forms of new regulations and technologies and the subsequent market changes could alter the competitive dynamics between lead firms and their tier-I suppliers. Although lead firms are becoming more specialized and highly efficient in specific product segments (see Lampón et al., 2017), they may not have inter-firm control over their tier-I suppliers because GPN boundaries become more permeable due to a combination of new regulatory, technology and market changes (Field survey, 2017–2019). This external shock could disrupt the GPN, from the exit of current lead firms or tier-I suppliers to the entrance of new tier-I suppliers or lead firms. Subsequently, a reconstituted GPN with newly established boundaries is created.

Applying the analytical framework to the automotive industry reveals how a combination of regulatory, technology and market changes alter the competitive dynamics (in terms of changing value-added) between firm actors in the production networks. Automakers create demand for parts suppliers but their relationship is symbiotic: automakers do not possess all the necessary expertise to make a car and thus need the technical expertise of selected suppliers to provide technical solutions for their car designs. The external shock of state regulations has changed the matrix of the cost-capability ratio between automakers and suppliers significantly since the 1990s. The competitiveness of conventional automakers in the reconstituted GPN has been diminishing, partly because of the vicious circle of long investment lead-time with excess production capacity, as well as lower profit margins and R&D intensity. Selected systems suppliers (system integrators who work relatively independently on the design of functionally-related non-contiguous component systems for automakers) with expertise in electric powertrains and micro-electronic control systems are not only in a prime position to capture the value generated by the increasingly stringent regulatory environment on safety and environmental standards, but also more resilient to the three emerging megatrends in automobiles: electrification, digitalization, and autonomous driving.

To examine the intricate competitive dynamics between lead firms and their major suppliers, a brief review of GPN and the proposed analytical framework are presented in the next section. The causes of the diminishing competitiveness of lead firms are examined before discussing the effect of megatrends on the competitive dynamics and resilience of selected tier-I suppliers and its implications on regional development. This paper concludes with a summary of its major findings.

GPN and reconstituted GPN

The GPN is reviewed briefly before presenting the proposed framework to improve the analysis of competitive dynamics in GPNs.

GPNs and governance

The GPN is a relational framework which conceptualizes the global economy as a network of interconnected economic processes embedded in specific locations. The GPN focuses on the roles of economic actors and their asymmetrical power relationships in the strategic coupling between lead firms and their suppliers to explain the activities and performance of various network configurations. This heuristic multi-actor and multi-scalar framework allows researchers to unpack the spatial asymmetrical capture of value in various manufacturing activities controlled by various economic actors and their subsequent impact on regional development (Coe et al., 2008: 272).

To address the criticism of unclear analytical boundaries and weak causal explanations (Sunley, 2008), Coe and Yeung (2015) developed the GPN 2.0 to refocus the research, from inter-firm to intra-firm relationships. They identified four major explanatory variables (cost-capability ratio, market imperatives, financial discipline and risk environment) to develop four different actor-specific strategies for organizing GPNs in a competitive market scenario. In an uncertain market environment, when financial pressure affects both firm and non-firm actors, firms respond with four actor-specific strategies: (i) intra-firm coordination, (ii) inter-firm control, (iii) inter-firm partnership and (iv) extra-firm bargaining.

The specific mode of governance (Gereffi et al., 2005) and the strategic coupling between lead firms and their embedded networks of suppliers are crucial for the trajectories of value capture in various locations. Lead firms, especially under the captive mode of governance, are the dominant players in an asymmetrical power relationship with their suppliers (Gereffi and Lee, 2016; Humphrey and Schmitz, 2002). To retain their competitiveness, lead firms can either establish inter-firm partnerships with strategic partners or externalize risk by outsourcing production to external suppliers to keep control of the production processes and the quality of the products/services through inter-firm control (Coe and Yeung, 2015: 135–142). An example of inter-firm partnership is the cross-equity holdings between Japanese automakers and their strategic tier-I suppliers.

Other studies have highlighted the importance of knowledge transfer from lead firms to ensure the high-quality outputs from their suppliers (Ernst and Kim, 2002). They pointed out the effectiveness of knowledge transfer depends on the specificities of knowledge and the suppliers’ absorption capacities and social networks. Ivarsson and Alvstam (2005) pointed out the importance of spatial proximity for knowledge transfer to Volvo’s local suppliers in China, India and Brazil, while Contreras et al. (2012) reported the roles of spin-offs, socio-professional networks and market relations in the emergence of knowledge-intensive local suppliers in Ford’s automotive cluster in Mexico.

Methodologically, the conventional GPN analytical framework helps to identify lead firms by final product before mapping out their supply networks. Although MacKinnon (2012) examined various types of coupling, recoupling and decoupling, Blažek et al. (2018) identified various firm-level drivers on the entrance-exit dynamics of suppliers for lead firms, and Humphrey and Schmitz (2002), and Smith (2015) point out that the power relationship is dynamic, the framework does not satisfactorily delineate the competitive dynamics between lead firms and their suppliers.

Analytical framework of the reconstituted GPN

Regulatory and technology changes are key drivers of the changing market dynamics in manufacturing. Smith’s (2015) criticism was that the state is inadequately conceptualized in the original GPN framework as non-firm actors, such as state and technology, are embedded within regional institutions and assets (Coe et al., 2008). State and technology are not among the four explanatory variables in the firm-centric GPN 2.0, although the effects of technology can be revealed through the cost-capability ratio while the state is presented as one of the extra-firm actors responding to the competitive dynamics of the four explanatory variables (Coe and Yeung, 2015: 124, see also Yeung, 2016a).

Yeung (2016b: 193) justified the framing of GPN 2.0 by arguing that inter-firm competition rather than direct state intervention is important in the strategic coupling of global lead firms. Suppliers and contractors have to use local endowments to strategically link to lead firms and engage in GPNs (Coe et al., 2008; Yeung, 2016b). This is especially the case for producer-driven chains in automobiles, where competitive advantages in technologies and scale economies allow international oligopolies to play an instrumental role in connecting competent local suppliers to GPNs. Sturgeon et al. (2008, 2009) and Sturgeon and Van Biesebroeck (2011) have highlighted the domination of a few powerful lead firms in an asymmetrical power relationship, with limited knowledge transfer to domestic suppliers in the automotive industry (Pavlínek, 2018).

However, Gruss and ten Brink (2016), Butollo and ten Brink (2018), Yeung (2019) and Yeung and Liu (2023) highlighted the importance of pro-active industrial policies for the establishment of new production networks in selected industries. As a regulator (van Apeldoorn et al., 2012), the state can impose regulatory changes that could have a significant impact on the competitive dynamics of an industry. This is especially the case in the drive towards NEVs where regulatory change alters market demand and thus the competitive dynamics of the automotive industry.

Although technology, especially the degree of codification, has long been a crucial factor in the determination of specific modes of governance (Gereffi et al., 2005), new technology as a strategic driver of GPNs has, arguably, not been thoughtfully examined in the literature (Kano et al., 2020). Raj-Reichert (2019) also highlighted the effects of industrial consolidation, especially supply chains coordination and strategic mergers and acquisitions, and (joint) product design and development, on the changing relationships between lead firms and first-tier suppliers in GPNs. Key suppliers with strong capabilities are able to capture more functional and strategic roles and this leads to a shift in power relationships towards multi-polar governance in GPNs (Raj-Reichert, 2019, see also Dallas et al., 2019).

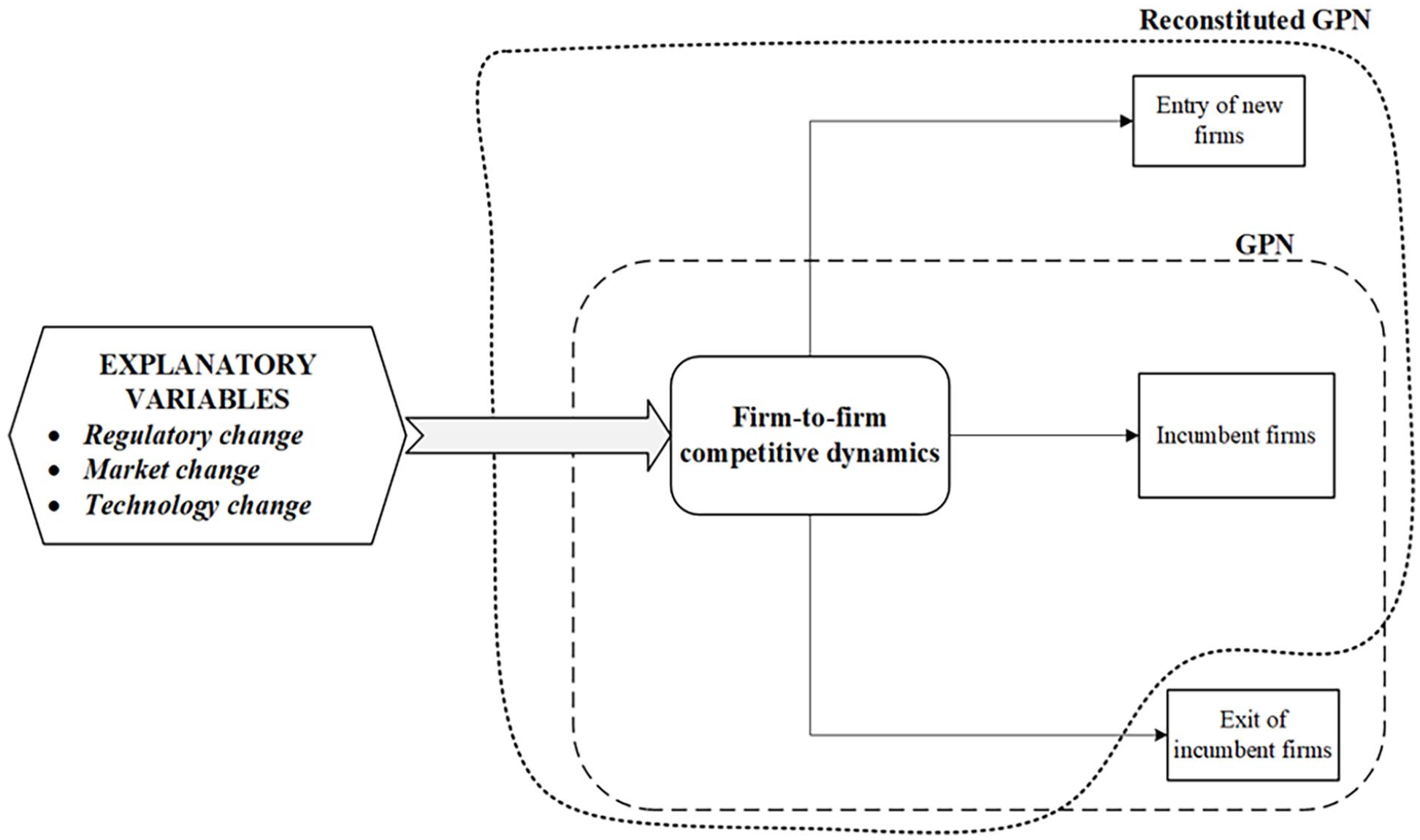

To enhance our understanding of factors that could produce disruptive impacts on inter-firm relationships, I propose an analytical framework to examine how industrial megatrends in the form of regulatory, market and technology changes can affect firm-to-firm competitive dynamics (dependent variable) in the reconstituted GPN (Figure 1). To maintain their profitability, lead firms and their tier-I suppliers are incentivized to maintain the robustness of their boundaries, that is, entry to GPN incurs high costs. The conventional GPN boundaries (illustrated by the broken-lines) become more permeable when there is an external shock from industrial megatrends, which could have a direct and disruptive effect on the governance of GPN and create entry opportunities for new tier-I suppliers or lead firms. Subsequently, a reconstituted GPN with its new boundary is established (illustrated by the dotted-lines). The framework unpacks how a combination of state-driven regulatory changes, massive shift in consumer demand and technological breakthroughs or an innovative adoption of existing technologies in a product could impact the competitive dynamics of the GPN’s constituent parts.

The analytical framework of the reconstituted GPN.

This analytical framework contributes to the existing literature by providing a dynamic account of the operation of GPN 2.0. Instead of focusing on inter-firm relationships and regional development, it shows how industrial megatrends could change inter-firm competitive dynamics due to the changing matrix of the technical and scale production competency between lead firms and tier-I suppliers, and the subsequent disruption to the existing GPN boundary. In contrast to Raj-Reichert’s (2019) framework, which focused on the dyadic forms of bargaining power, the proposed framework highlights the disruptive effects of industrial megatrends on the existing firm actors as well as potential new lead firms that could come into being as part of the reconstituted automobile-automotive GPN (AAG), which exhibits both dyadic inter-firm bargaining and collective institutional power through regulatory changes in multi-polar governance GPNs (see Dallas et al., 2019). The automotive sector is used to illustrate the operation of this proposed analytical framework.

Intricate competitive dynamics in the reconstituted automobile-automotive GPN

The relationship between automakers and suppliers used to be based on a closed and integral architectural system of production with model-specific parts till the 1980s (Frigant and Lung, 2002). Apart from externally sourced commodity parts, automakers were responsible for the R&D and manufacturing of a significant proportion of parts through their vertical integrated production networks with directly-owned subsidiaries (Macduffie, 2013).

The automotive industry has undergone significant restructuring since the 1990s. In addition to spin-off firms for parts manufacturing, like GM’s Delphi, and Ford’s Visteon in 1998–1999, (Carrillo, 2004; Humphrey, 2003), the automotive industry has moved to standardized vehicle platforms based on an open and modular architecture with generic parts developed and pre-assembled separately by different tier-I suppliers before being delivered to automakers for assembly with the chassis and powertrain. This not only reduces the complexity of assembly by automakers, but also transfers the research and development (R&D) costs of modular systems to their tier-I suppliers (Baldwin and Clark, 2000) and shortens design lead times (Ulrich, 1995). Automakers focuses on the overall architectural design of vehicles, including the interfaces and functioning of the different sub-systems within different vehicular specifications (Frigant and Lung, 2002; Lung, 2001; Macduffie, 2013). This business model pushes tier-I suppliers to innovate and develop their expertise in sub-systems and manage their own supply chains efficiently for JIT production systems and quality-at-source production (Humphrey and Memedovic, 2003).

Under the modular architecture, automotive parts are classified in two major groups:

Service (engineering) parts: Non-standardized tailor-make parts whose replacements ordinary car owners have to purchase from authorized dealers or specialist suppliers, for example, engine control units.

Commodity parts: Standardized and replaceable parts which car owners can easily procure and have installed by aftermarket suppliers, according to a set of pre-determined product specifications. For instance, profit margins are low in the volume tyre market as most consumers are price-sensitive and there are 232 brands of standard tyre sizes of ordinary cars (195/65 R15).

Gereffi et al.’s (2005) typology of value chain governance and Sturgeon et al.’s (2009: 18) dualistic global-local supplier classification is useful for examining the potential impact of coupling on local economies but is unable to fully unpack the competitive dynamics between automakers and suppliers. It is estimated that an average automaker has around 250 tier-I suppliers and could incorporated 18,000 suppliers in its full supply networks, from suppliers of raw materials to components (Baumgartner et al., 2020). To understand the governance of GPNs in the automotive industry requires more discrete classification of suppliers. There are three types of suppliers based on their functional/contractual inter-firm relationships. The same supplier can have different contractual relationships with different (or even the same) automakers, depending on the specific model/product cycle:

Strategic partners for service parts who work closely with automakers during new car development.

Systems suppliers of service parts – system integrators who work relatively independently on the design of functionally related non-contiguous component systems for automakers, for example, steering systems. Some of the literature refers to them as mega-suppliers, tier-0.5 or modular suppliers or transnational first-tier suppliers as they have their own supply chains (Frigant and Zumpe, 2017: 666; Humphrey and Memedovic, 2003: 22; Raj-Reichert, 2019). System and strategic suppliers are designated or exclusive tier-I suppliers for automakers but there is no guarantee of preferential treatment of orders from automakers in the long-term.

Sub-contractors of highly codified commodity parts (e.g., steering rods), and where contracts are awarded through public tender.

The competitive dynamics of the automotive industry are more complex than the asymmetrical relationship hypothesized in conventional GPN analysis. Automakers do create demand for systems suppliers but their relationship is more symbiotic: automakers need the technical expertise of systems suppliers to provide technical solutions to their car designs. Automakers are thus more like integrators, designers or architects than lead firms who control their coupled suppliers: automakers control the overall car design (architecture of the car), and have to ensure all component systems sourced from various tier-I suppliers function properly before assembling them into a finished car.

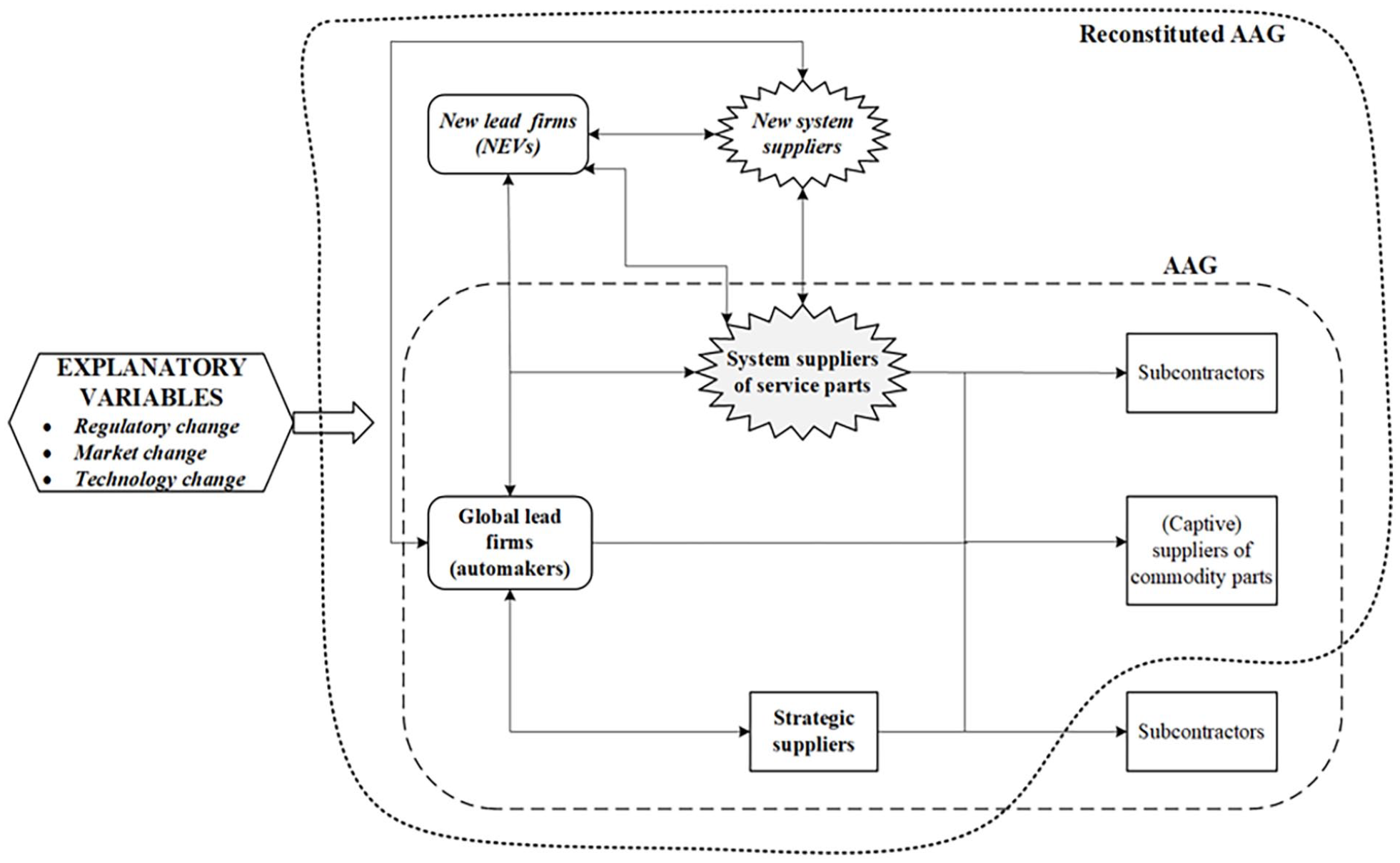

Applying the analytical framework to the automotive industry, regulatory changes on emission control and the phasing-out of ICE-driven vehicles and changing consumer demand for vehicles equipped with active safety systems and electric powertrains all reflect the industrial megatrends in forms of state regulations on the industry as well as shifting market demand and the technological challenge encountered by firm actors. Regulatory and market changes accelerated the adoption of advanced micro-electronics and battery technologies by the incumbent lead firms in automotive sectors while the technological innovation in micro-electronics have altered the changing cost-capability ratios and thus the resultant competitive dynamics between OEMs/automakers and their systems suppliers as well as the entry of new lead firms in the reconstituted automobile-automotive GPN (AAG).

The AAGs have two ‘distinctive’ production networks to account for their dynamic symbiotic and arm-length relationships, emphasizing the complexity of multi-tiers supply networks and their governance, and the competitive dynamics (in terms of changing value-added) in the automotive industry and its impact on regional development (Figure 2):

Automakers and their captive commodity parts sub-contractors in automobile GPNs, as hypothesized in conventional GPN analysis.

Systems suppliers are technology leaders in selected product segments in automotive GPNs (such as electric drivetrains and electronic control units) where they are able to either establish inter-firm partnerships with strategic suppliers or control their sub-contractors through inter-firm control.

The reconstituted automobile-automotive GPN (AAG).

Rising cost-capability ratio of lead firms in the AAG

Moving up the value chain is a common pathway to functional upgrading (Humphrey and Schmitz, 2002) and being the lead firm is the ultimate benchmark of competitiveness in the sector. The dominance of incumbent automakers in the AAG has, however, been diminishing due to the rising cost-capability ratio, the result of a vicious circle of long investment lead-time, excess production capacity, low(er) profit margins and R&D intensity.

Heavy investment with long lead-time and excess production capacity

Car design and development involves heavy capital investment with long lead-time. To develop a new model, automakers typically invest a billion dollars between 5 and 9 years. To rein in rising development costs, automakers adopt various strategies, from platform sharing to option-model rationalization. Volkswagen Aktiengesellschaft (hereinafter Volkswagen) is a typical example of platform sharing, where its MQB platform is used for 14 models, from superminis to sedans under the brand names of Audi, VW, SEAT and Škoda. Similar arrangements exist among other automakers with cross-equity holdings, for example, Nissan and Renault, Ford and Mazda and so on. To cut costs, Ford has slashed its personalized options on its mass market sedans significantly (from 35,000 to 96 in the Fusion and from 360 to 26 in the Fiesta), and phased out 5 of the 17 engines by 2022 (Financial Times, 5 October 2017).

Automakers have to maintain production volumes for economies of scale so their target selling prices are feasible in a highly competitive market. Although automakers managed to sell 98% of their products in 2019 (International Organization of Motor Vehicle Manufacturers [OICA], 2020a, 2020b), this does not reveal the excess production capacity in the industry. The average capacity utilization of the global automobile sector was at 66% in 2019, with an idle capacity of 48.6 million units (Arthapan, 2019). Excess production capacity is especially pronounced in emerging fast growing markets. China, the largest producer (and market) in the world, had an excess production capacity of 40% (17 million vehicles) in 2019. To illustrate, Ford has the largest manufacturing capacity outside Detroit in China, but the excess capacity of five joint-venture plants at Changan-Ford is 37.5%, a staggering 0.6 million units out of an installed capacity of 1.6 million vehicles a year. Another joint-venture, GAC-FCA (Fiat-Chrysler Automobiles), has an annual production capacity of 328,000 vehicles in its Changsha and Guangzhou plants but its sales were only 63,783 vehicles in 2015 (Field survey, O2, 27 September 2017; O1, 14 August 2017). 1

Given the long lead-time for new model development, automakers with the ‘wrong’ model portfolios are unable to adjust to the volatility of market demand in specific vehicular segments, and this contributes to overall excess production capacities. This is illustrated by the rapidly changing market demand from sedans to sports utility vehicles (SUVs) in China. Although the units of sale remained stable, the market share of sedans declined from 70% in 2010 to 46% in 2020, while the sales of SUVs jumped by seven times to 9.46 million units, with a market share of 47% in 2020 (China Association of Automobile Manufacturers [CAAM], 2021). 2

To deal with volatile market demands, automakers have negotiated flexible labour agreements and reduced three (8-hour) shifts a day to one. Modern plants are also capable of building multiple models and moving production to popular models as needed. Retooling is, however, costly and could only be cost effective for producing large volumes of similar parts. For instance, VW converted part of a car-engine plant to produce electrical generators during the global financial crisis when there was a 10% decrease in the number of vehicles assembled worldwide between 2008 and 2009 (OICA, 2020a).

Low profitability and R&D intensity

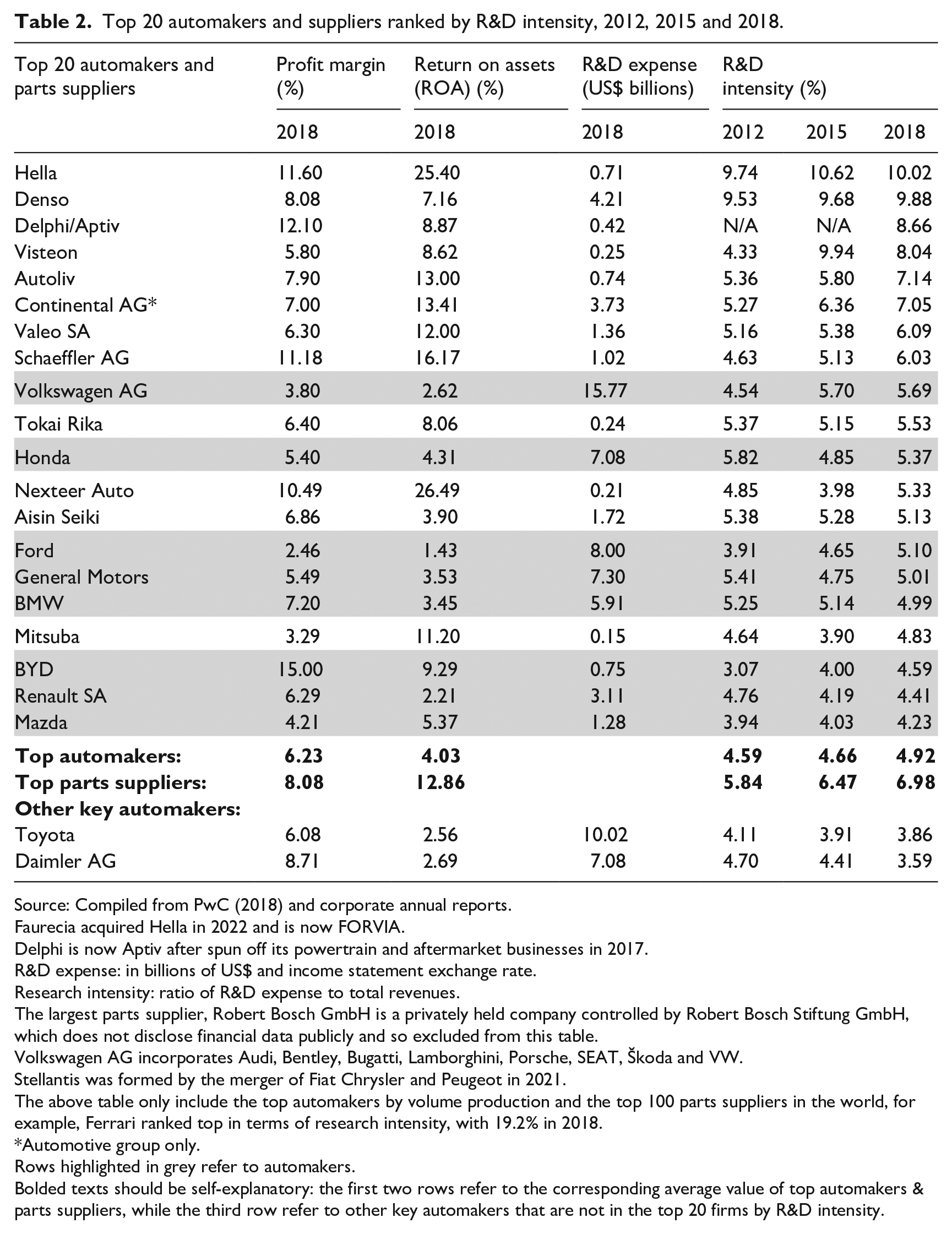

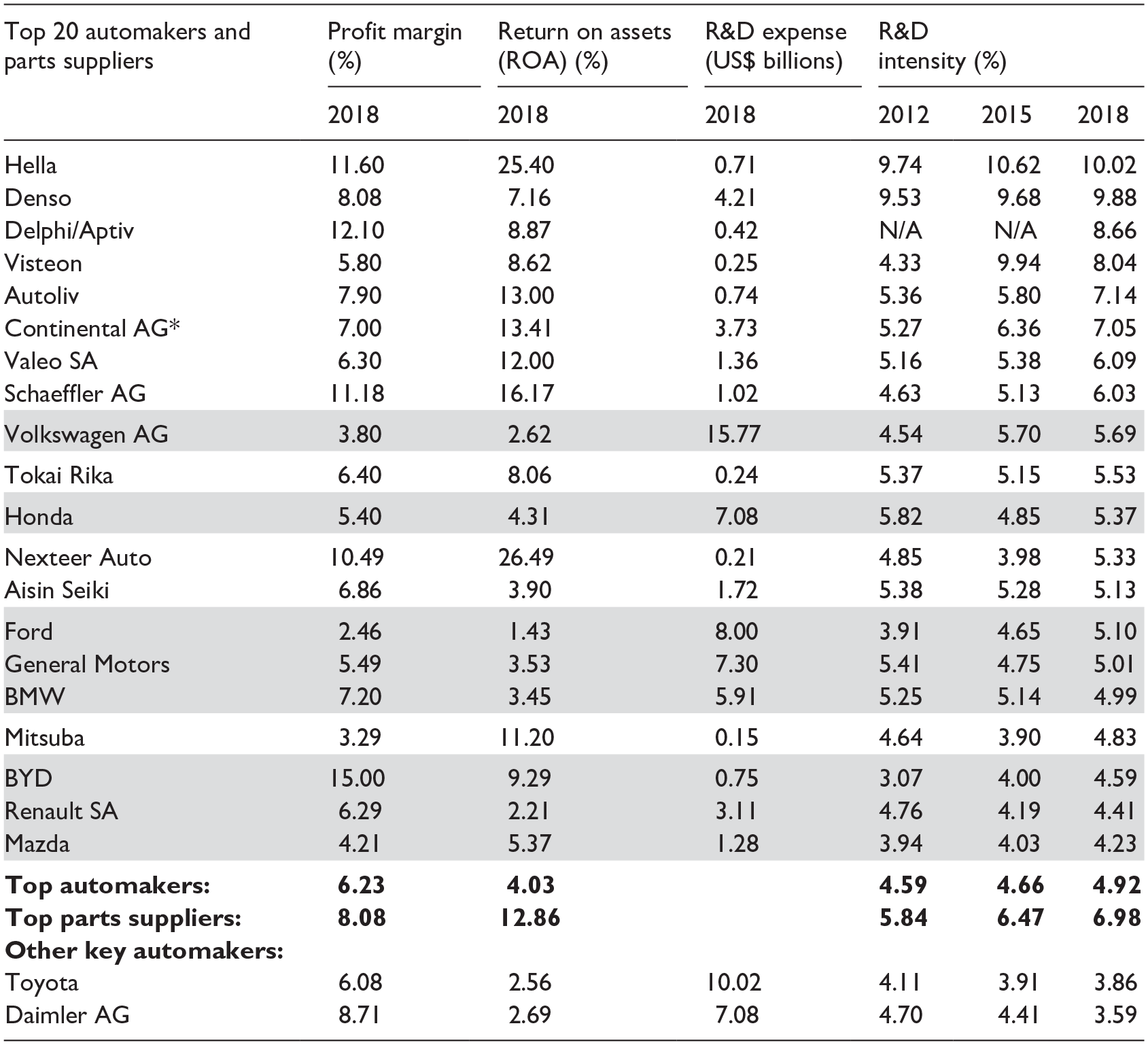

Keen competition and excess capacity translate into lower profit margins: automakers recorded an average profit margin of 6.23%, 1.85 percentage points lower than parts suppliers in 2018 (Table 2). Automakers specialized on luxury models with higher value-added, such as BMW and Daimler, were more profitable but their profit margins were still in single-digit and lower than the lower double-digit profit margins recorded in Hella, Delphi/Aptiv, Schaeffler and Nexteer in 2018. All top 15 automakers have single-digit profit margins, ranging from as low as −18.42% recorded by the Renault, to 5.91% recorded by Toyota in 2020 (WSJ, 2021). The low profitability of automakers has been documented by Womack et al. (1990), who concluded that only three automakers (Honda, Toyota and VW) were in profit during slow growth years.

Top 20 automakers and suppliers ranked by R&D intensity, 2012, 2015 and 2018.

Source: Compiled from PwC (2018) and corporate annual reports.

Faurecia acquired Hella in 2022 and is now FORVIA.

Delphi is now Aptiv after spun off its powertrain and aftermarket businesses in 2017.

R&D expense: in billions of US$ and income statement exchange rate.

Research intensity: ratio of R&D expense to total revenues.

The largest parts supplier, Robert Bosch GmbH is a privately held company controlled by Robert Bosch Stiftung GmbH, which does not disclose financial data publicly and so excluded from this table.

Volkswagen AG incorporates Audi, Bentley, Bugatti, Lamborghini, Porsche, SEAT, Škoda and VW.

Stellantis was formed by the merger of Fiat Chrysler and Peugeot in 2021.

The above table only include the top automakers by volume production and the top 100 parts suppliers in the world, for example, Ferrari ranked top in terms of research intensity, with 19.2% in 2018.

Automotive group only.

Rows highlighted in grey refer to automakers.

Bolded texts should be self-explanatory: the first two rows refer to the corresponding average value of top automakers & parts suppliers, while the third row refer to other key automakers that are not in the top 20 firms by R&D intensity.

As expected, automakers are asset-heavy and thus with much lower average return on assets (ROA): 4.03 versus 12.86% in parts suppliers (Table 2). Importantly, the average profit margin and ROA of automakers are skewed by the much higher figures recorded by the Chinese automaker BYD (specialized in hybrid and battery electric vehicles): the corresponding figures decreased from 6.23 to 4.98% and 4.03 to 3.27% respectively should BYD is excluded). Automakers are relying on system suppliers rather than investing on capital-intensive assets to develop specialized parts (see next section).

In addition to low profit margins, automakers have structural disadvantages compared to systems suppliers due to their different business models. To maintain production volume, automakers spend more on advertising to attract customers than other industries. Systems suppliers operate in a business-to-business environment, needing a much lower advertising budget, mainly to have a presence at trade conferences. For instance, GM spent US$5.3 billion on advertising in 2016, while their top supplier, Delphi, spent a mere US$123 million. The total advertising budget for 14 major systems suppliers accounted for 0.7% of sales value (US$1.25 billion), which is a fraction of the 2.8% (US$42 billion) spent by the top 12 automakers (Financial Times, 9 August 2017). Consequently, automakers spend lower proportion of their revenue on R&D, perpetuating their reliance on systems suppliers for technical solutions to car architecture concerns.

The R&D intensity illustrates the rising R&D expenses of systems suppliers vis-à-vis the top automakers (Table 2). The top eight automotive firms by R&D intensity were all systems suppliers in 2018, and a few have increased their R&D intensity significantly, notably Visteon, Autoliv and Continental whose R&D intensity has increased by 33–85% over 6 years. Automakers have invested more capital in R&D but on average, it accounts for less than 5% of their revenues, while top systems suppliers have not only invested a higher proportion of their revenue in R&D, but also increased their average R&D intensity to 6.98% in 2018.

Excess production capacity, razor-thin profit margins and low R&D intensity has led to a rising cost-capability ratio among automakers, which suggests the competitive dynamics could be shifting towards systems suppliers, even without any external shock in the AAG.

Emerging industrial megatrends and shifting competitive dynamics of AAG

Expertise in powertrains and systems integration (to ensure all parts are functioning as designed and are reliable under various conditions) are two core competitive advantages of automakers (Field survey, 2017–2019). In addition to high entry costs and tacit knowledge in volume manufacturing, Sturgeon et al. (2009: 9) argued that a lack of industrial standards has led to suppliers being dependent on automakers. Although suppliers are more involved in car development, Sturgeon et al. (2008: 308) point out that ‘supplier relations did not change [as] American automakers tend to systematically break relational ties after the necessary collaborative engineering work has been accomplished. . . . [and] after a year or so of production’. Ponte and Sturgeon (2014: 205) also concluded that ‘supplier power appears to be a rare commodity in GVCs’.

What Sturgeon et al. (2008) have argued is based on partial evidence of a continuum of automaker-supplier relationships. American automakers do change suppliers through public tender to reduce procurement costs when models have entered their late product cycle and parts have been codified, that is, after long-term (5-year) contracts with strategic suppliers have expired. GM develop new models with a few strategic suppliers to avoid risk in the supply network, while Ford relies on a single supplier for each major class of part (Field survey, 2017–2019). 3

Importantly, state regulations has been significantly changing the cost-capability ratio between automakers and systems suppliers since the 1990s. Publicly listed automakers are under pressure to generate financial synergies by spinning off their non-core businesses in parts manufacturing. This allows some parts suppliers, such as Delphi and Visteon, to develop as systems suppliers. Systems suppliers are not only in a prime position to capture the value generated from the increasingly stringent safety and environmental standards driven by the new regulatory environment and market demands, but also resilient when faced with changing market demands and technologies for NEVs and other automotive megatrends.

Rising safety and emission parameters: Shifting of value-added to systems suppliers for service parts

A combination of new standards on passive and active safety, and state emission control in major automobile markets has led to change in market demand and the accelerated adoption of micro-electronics in the automotive industry, shifting the competitive dynamics between automakers and systems suppliers.

The introduction of the European New Car Assessment Programme (Euro NCAP) has had a significant impact on the competitive dynamics of automakers and their systems suppliers. Automakers develop expertise in passive safety by improving the structural integrity of the chassis and crash absorption capacity of front and side crumple zones by utilizing high strength steel, aluminium and reinforced polycarbonate. A higher level of structural integrity in the chassis coupled with well-tuned suspension and steering systems (and tyres with good traction) improve a vehicle’s handling and lowers the chance of an accident.

Initially conceived largely for driver and passenger safety when it was launched in 1997, the Euro NCAP has incorporated elements of active safety into the NCAP Advanced reward scheme since 2010, for example, autonomous emergency braking with post-collision assist systems, and vision enhancement system and so on. To secure the top rating of NCAP Advanced reward as a marketing slogan, automakers have to rely on the expertise of systems suppliers for active safety by integrating advanced driver assistance systems (ADAS) into engine management systems to ensure various devices with complex micro-electronics and algorithms function as designed. An average modern vehicle has seven times more code in its 150 electronic control units than a modern passenger jet (Deichmann et al., 2019: 2). This explains parts and components significantly increased share in a car’s value, from 40 to 50% in the early 1990s to more than 70% today (Field survey, 2017–2019). Automakers have competitive advantages in passive safety but changing market demands allow the system suppliers of active safety devices to capture a larger proportion of value in a passenger vehicle.

In addition to increased consumer awareness in safety, the increasingly stringent emission standards have further facilitated the shift of value-added from automakers to systems suppliers since the 1990s. This is especially the case when ‘Euro 2’ environmental standards were introduced in 1996 and then subsequently more stringent and comprehensive emission standards by incorporating hydrocarbon, nitrogen oxide and particulate matter in petrol engines (Delphi, 2017: 6–8). The implementation of Worldwide Harmonised Light Vehicles Test Procedure (WLTP), effectively on 1 September 2018, further increased the regulatory compliance costs of automakers, for example, Volkswagen must individually test its 260 different motor-gearbox combinations along with other variations affecting emissions (Financial Times, 15 November 2018).

Automakers specialize in the energy efficiency of ICEs and transmissions, but the increasingly stringent emission standards call for wider use of both physical and micro-electronic control systems to reduce the emission of harmful gases (such as carbon monoxide, nitrogen oxides) and particles. For instance, the common high-pressure fuel injection and engine management systems in modern vehicles have networks of catalytic converters and exhaust gas recirculation systems, which allow systems suppliers to capture a larger proportion of the value created in car manufacturing.

To comply with the emission standards, automakers have to rely on the technical expertise of their systems suppliers for the bespoke design of uncodified parts. Automakers and systems suppliers are locked-in to the existing AAG until the development cycle of a new model. Automakers do not normally change their systems suppliers as only a few have the technical capabilities and capacity for volume production. Reputation does matter as ‘who will cooperate with [us] in the future if [we] cut [our] suppliers off without good reasons?’, according to the Deputy General Manager of a top automaker – one of its system suppliers corroborated this view (Field survey, O2 and S9, 27 September 2017). Development costs are high as the specifications of some seemingly simple parts such as air intake systems and fuel tanks are different within the same car segment as they are tailor-made by systems suppliers to maximize the fuel efficiency of a specific model and its drivetrains while fulfilling the stringent safety and emission requirements, for example, from optimization of air-fuel ratio to minimization of fuel vaporization (Field survey, 2017–2019).

Moreover, the emphasis on passive and active safety systems and passengers’ comfort (noise reduction inside the vehicle) increases the weight of a vehicle and this negates some of the thermal efficiency improvements of ICEs; for example, the curb weight of a basic VW Golf was increased by 14% (993 kg in 1992 Mk3 to 1131 kg in 2016 Mk7). Automakers are thus forced to include even more advanced micro-electronic control modules to improve thermal efficiency and emissions, for example, powertrain control module (PCM) controls solenoids to adjust hydraulic valves in Variable Camshaft Timing (VCT). The adoption of start-stop systems and (mild and plug-in) hybrid powertrains further move the competitive dynamics from automakers to systems suppliers, for example, the current Ford’s F-150 pickup truck contains more than 800 types of micro-chips.

The shift of competitive dynamics towards systems suppliers was admitted by a senior sourcing manager of a top automaker:

[We] don’t have the technical capability to develop every part. . . . [We] have to rely on external R&D teams/[system] suppliers to develop parts, especially complex parts. 80 percent of our parts are sourced outside and the only parts that we do ourselves are steel body panels. (Field survey, O5, 25 April 2018).

This pattern is common among volume automakers, even in the case of vertically integrated Volkswagen, which assembles a high proportion of its own engines and transmissions from parts sourced externally in 56 plants in five different continents, employing 80,000 workers.

The intricate linkages between automakers and their suppliers in just-in-time (JIT) supply networks suggest that the relationship between automakers and systems suppliers is symbiotic, partly due to the regulatory, market and technology changes in the automotive industry.

Regulatory, market and technology changes: Resilience of systems suppliers to automobile megatrends

Regulatory, market and technology changes partly facilitate the three emerging megatrends in automobiles: electrification, digitization and car sharing and autonomous driving. The phasing-out of ICE-driven vehicles and the rising environmental awareness of customers in key markets has accelerated the adoption of advanced micro-electronics and battery technologies by automakers, thus altering the competitive dynamics with systems suppliers further. Selected systems suppliers with technical and production competency are not only more resilient than automakers to these emerging megatrends, but they could also develop into the new lead firms in the reconstituted AAG (Figure 2).

The electrification of powertrains eliminates the core competitive advantage of automakers in ICEs and further enhances the value capture of systems suppliers vis-à-vis automakers. This is especially the case with the massive push of European countries to adopt NEVs after Norway’s decision to ban the sale of new vehicles with ICEs by 2025. Subsequently, major automakers have announced their plans for partial to full electrification of their vehicle powertrains, for example, Volvo was the first automaker to claim to electrify its entire portfolio of vehicles by 2030, while GM will only sell zero-emission vehicles by 2035 (New York Times, 28 January 2021).

Battery electric vehicles’ drivetrains have far fewer components than a vehicle with an ICE. For instance, a Chevrolet Bolt electric vehicle has only 21% of the 167 wear and tear parts of a VW Golf’s powertrain, which has a much more complicated ICE with 113 parts plus another 27 parts in the 6-speed automatic transmission gearbox with a clutch and differential (USB, 2017: 27). In addition, a vehicle with an ICE also has to be equipped with an emission control system (catalyst and particulate filters plus muffler).

The electrification of powertrains will have significant ramifications not only for subcontractors making codified commodity parts but also for systems suppliers with technical expertise solely in ICEs and ICE-drivetrains. For instance, NSK, one of the world’s leading producers of bearings based in Japan, could lose a significant proportion of its business. A vehicle with ICE uses up to 150 bearings, but an electric car with less serviceable parts will need only half that number. Even the biggest electric power steering supplier, Jtekt (with 25% share of the market), may not be competitive in the era of autonomous driving. The scenario of incumbent firms’ exit from the AAG is consistent with the dark side of GPNs highlighted in the literature (Phelps et al., 2018).

In addition to the electrification of powertrains, digitization and autonomous driving further negate another core competitive advantage of automakers’ in systems integration. These megatrends demand the expertise to integrate micro-electronic monitor and control modules and their related software systems. Selected systems suppliers are expected to play an increasingly important role in aspects that distinguish different brands of car as core competency is moving from powertrain thermal efficiency to the integration of software algorithms and micro-electronics. For instance, the Chevrolet Bolt electric vehicle’s powertrain contains US$580 worth of semi-conductors, which is 6–10 times more than an equivalent car with an average ICE-driven VW Golf (UBS, 2017: 8). Safety features today typically add about US$2,500 to the cost of a car, and the value of the ADAS market could reached US$59 billion by 2025, a 195% increase from US$20 billion in 2018 (Coffman et al., 2019: 7).

Systems suppliers, especially those with expertise in the integration of software algorithms and micro-electronics control systems, are actually marketing themselves as one-stop ‘solution providers for mobility’ (Field survey, 2017–2019). Systems suppliers have expertise in the design and making of precision parts and can provide automakers with proprietary and knowledge-intensive mobility solution packages, from technical design services for model-specific service parts, to manufacturing them to exact specifications before delivering them to auto plants for JIT and just-in-sequence (JIS) assembly. For instance, the value of systems suppliers for Mercedes-Benz is their ability to design and provide integrated electrical and electronic distribution systems. As explained by the Vice-President and Managing Director of a key system supplier:

Wire harness is the most complex part in a modern vehicle . . . Our competitive advantages is to work with Hella and 600 other suppliers all over the world on the architectural design of the wire harness system. . . . In an E-class sedan, our engineers have to ensure that the wire harness system is able to provide a reliable transmission of data between the central control module and its 60 interlinked control units, which are connected to a total of 2,000 electric circles/connections with different sensors/devices under 1,200 possible combinations of (optional) specifications. The manufacturing of wire harness has to be based on the exact specifications ordered by Mercedes-Benz’s customers as each of them can order different active driver assistance and safety, electric seats and infotainment system options in addition to the standard control systems for drivetrain, comfort, diagnostics, and power management system management in their vehicle. . . . No other company in Asia-Pacific with only a single product line [wire harness] has registered a US$2 billion business. (Field survey, S10, 9 October 2017, emphasis in original)

The importance of wire harness in vehicles is reconfirmed by the production cost data provided by a key automaker: cables and wiring alone account for more than half the production costs of engine in a mass market ICE-driven SUV (5+ versus 10%) (Field survey, O1, 14 August 2017). Electrification and autonomous driving demand reliable power and data connections and further enhance the importance of wire harness in vehicles.

Selected systems suppliers and other firm actors could be in a better position than automakers to capture value created by this external shock. The bottom line is that whether cars are shared or autonomously-driven, they need a host of semi-conductor control modules, electronic gadgets and safety features to be installed in a typical vehicle. Selected systems suppliers could also be the ‘turnkey [mobility] solution providers’ for electric powertrains with integrated control modules (ADAS, battery management and regenerative braking systems), to push forward electrification in automakers’ model portfolios (Field survey, S5, 21 July 2017). It has been estimated that electrification increases the semi-conductor costs of a typical vehicle by US$377–1000 and autonomous driving will further increase semi-conductor costs to another US$1150–1250 per vehicle by 2030 (Infineon, 2020: 28; Financial Times, 4 January 2023). The chief financial officer, Wolfgang Schäfer, at Continental (a system supplier), commented: ‘[t]hese three megatrends – electrification, car sharing and autonomous driving – change the business model for the [automakers] more than they do for the suppliers’ (Financial Times, 9 August 2017).

In addition to conventional systems suppliers, such as Infineon, Valeo, Delphi and Continental (UBS, 2017: 59), new firm actors, like micro-electronics and other device makers, could benefit from the megatrend towards electrification and autonomous driving. UBS (2017: 51–52) estimates that 56% of the production costs of Bolt electric vehicles come from non-traditional suppliers: the LG Group supplies the entire electric powertrain, battery and other electronic modules. Importantly, automakers production costs have halved, from an average of 20% of conventional powertrains, to 11% in electric vehicles.

The world’s automotive semi-conductors market was US$35 billion in 2020, and is dominated by existing platform leaders, such as Infineon (13.2% of market share), NXP (10.9%), Renesas (8.5%), Texas Instruments (8.3%), and ST Micro-electronic (7.5%) (Wagner, 2021). Infineon, NXP and Renesas are in a leading position to reap the value generated from electrification and autonomous driving as they have the comprehensive product portfolios with low cost-capability ratios and able to mass produce 1200 V (160 A) insulated-gate bipolar transistors (IGBT) and Silicon Carbide (SiC) with much higher breakdown field strength and thermal conductivity for high voltage power semi-conductors (Field survey, S12, 17 January 2018). Bernhart and Alexander (2020) pointed out that traditional tier-I suppliers based on electrical or electronic architecture must design their parts around next generation processors to be competitive. As a response to the challenge from autonomous driving, they have consolidated their competitive positions by forming multiple partnerships with automakers and potential lead firms (internet companies) in the development of electric and autonomous vehicles.

Other firm actors can create synergies using their existing micro-electronics products and thus benefit from megatrends in automobile production. Notable examples of autonomous driving suppliers are the producer oligopolies in Graphics Processing Units (GPUs, especially Nvidia), radar, LIDAR (Light Detection and Ranging, such as RoboSense), camera (Intel-Mobileye) and system integrators, as well as internet giants which have collected colossal mapping and other data (such as Google). In response to the massive US$400 billion pumped into firms related to the emerging megatrends over the last decade, mostly by non-automaker investors, automakers are investing US$330 billion in electric and battery technology over the next 5 years (Cornet et al., 2021). Although warned in 2020 that ‘the current business model of the car industry is going to collapse’ under the ongoing transition to battery electric vehicles, Mr Akio Toyoda resigned as President of Toyota in 2023 and publicly admitted that his ‘old-fashion’ mentality on industrial megatrends partially contributed to the adoption of a modified TNGA modular ICE-platform rather than a dedicated NEV-platform in the bZ series and the significant delay of a large-scale rollout of battery electric vehicles (Financial Times, 26 January 2023).

The Vice-President and Managing Director of a top system supplier highlighted the reliance of the automobile industry on the innovative power of their systems suppliers (most are oligopolies, with no more than three competitors), claiming:

Most of the innovations you see in the car industry were developed by [systems suppliers] like us. (Field survey, S10, 9 October 2017)

This claim is echoed by Thomas Manfred Muller, the executive Vice-President of Volkswagen Group China, responsible for R&D, who estimated that 80% of the innovations in the automotive industry will be based on semi-conductors as there will be around 6,000–10,000 chips in a car (China Daily, 19 April 2021). The tacit knowledge embedded in service parts and their technological capabilities provide systems suppliers with competitive advantages in the AAG. This argument is consistent with the information rents generated from the monopoly of intellectual property rights on intangible assets (Durand and Milberg, 2020) and the subsequent redistribution of endogenous (innovation) and exogenous (policy) rents from assemblers to other actors in the supply chains (including pre- and post-production activities), as argued by Kaplinsky (2019).

Selected systems suppliers with the appropriate technological capabilities for NEVs and autonomous driving not only have a higher level of resilience to the emerging megatrends, but are also in a prime position to retain, if not reinforce, their competitive advantages. They could even develop as the new lead firms in the reconstituted AAG.

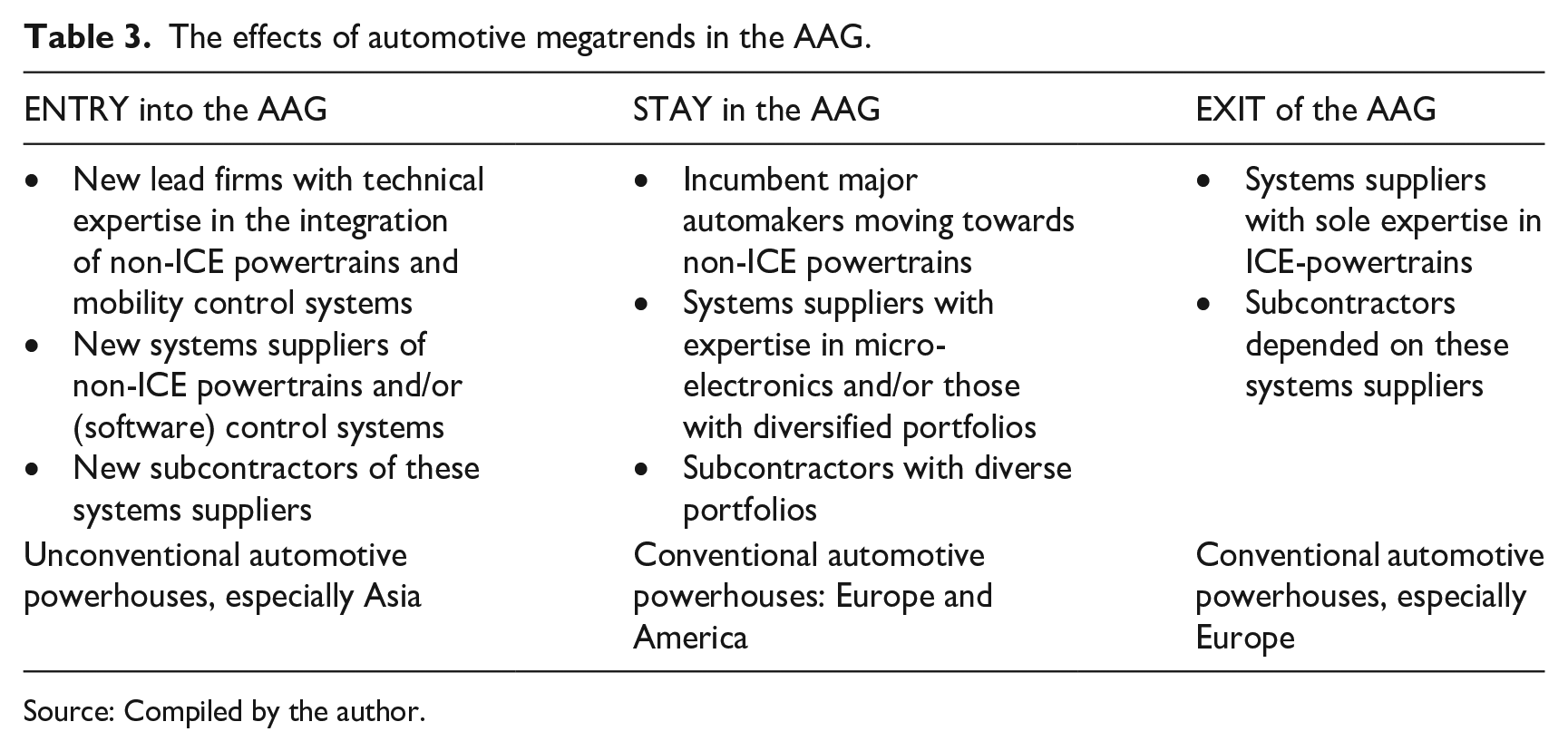

Regional implications for the automotive industry

What are the implications from the above analysis? The changing competitive dynamics in the reconstituted AAG could result in a significant shift in the spatial reconfiguration of AAG between the conventional powerhouses in Europe and North America and the emerging actors in Asia (Table 3).

The effects of automotive megatrends in the AAG.

Source: Compiled by the author.

Traditional automobile powerhouses in North America and Europe have the technologies but not the capacity to efficiently scale up production of NEVs. Importantly, the largest and most rapidly growing market for battery electric vehicles is in China, and this has already had an impact on the existing GPNs: existing lead firms in conventional powertrains have had to rejig their product portfolios significantly towards electrification in order to remain in the largest automobile market in the world (Yeung, 2019; Yeung and Liu, 2023).

To facilitate the move to electrification, Volkswagen invested heavily to establish manufacturing capacities in China and Europe: €1 billion to increase its equity to 75% at JAC-VW, the joint-venture making battery electric vehicles in China. In addition to invest €1.1 billion for 26% of equity in a Chinese battery-maker, Guoxuan High-tech, Volkswagen is investing US$18 billion to build six battery factories in Europe (China Daily, 29 May 2020). Partly due to the significant investment from Volkswagen and other automakers in China, China exported 0.68+ million of battery electric vehicles and, at 3.11 million vehicles, bypassed Germany as the world’s second largest automobile exporter of in 2022 (South China Morning Post, 26 January 2023). The European Association of Automotive Suppliers (CLEPA) points out that Europe lags behind in the production of sensors, micro-electronics and batteries. It estimated that European automakers were paying US$5,000–US$8,000 to Asia (China, South Korea and Japan) for batteries for every battery electric car produced in Europe (Reuters, 15 September 2017). Major electric vehicle battery-makers based in Asia, noticeably LG Energy Solutions, SK Innovation and Samsung SDI in South Korea, CATL, Guoxuan High-tech and BYD in China and Panasonic in Japan, have the technological and production capabilities and capacities to scale up their production to cater for the rising demand for electric cars. The CEO of Ford, Jim Farley, recently argued that the electrification will lead to a ‘very large consolidation . . . [in the industry and the] shakeout is going to favor many of the Chinese new players’ (Automotive News, 1 June 2022). This could be a shift in the terms of trade between Asia (especially China) and Europe should this trend is sustainable.

The automotive industry accounts for 5.7% of the total workforce (12.6 million jobs) in the European Union, five million working with suppliers (Reuters, 15 September 2017). The Institute for Economic Research (IFO) estimates that automakers account for 13% of industrial value creation and 5% of gross domestic product; and with their suppliers, they support more than two million jobs and directly employ a total of 800,000 in Germany (Economists, 3 March 2018: 53–54; Financial Times, 29 September 2020). The operations of automobile giants (Volkswagen, BMW and Mercedes-Benz) rely on the efficiency of their networks of suppliers, of which about 1000 are based in Germany and together account for 10% of Europe’s biggest economy (Reuters, 5 February 2018). The VDA (German Association of the Automotive Industry) and CLEPA estimate that the European Union’s proposal to ban new ICE-driven vehicles will result in 5–600,000 jobs lost (and a net loss of 275,000 when account for the new jobs arise from NEVs powertrains) in Germany by 2030 (Financial Times, 18 April 2022; Automotive News, 23 June 2022). The rapid decline of diesel-engine powertrains has already put 20,000 jobs at Bosch, the world’s largest supplier of these systems and with factories in the less economically developed regions of Germany (such as Saarland or Franconia), in jeopardy. A (significant) shift in the spatial configurations of AAG will have profound implications for regional development in Europe and this is one of the reasons why European governments and companies have invested US$5.6–6.7 billion and formed an alliance for developing next-generation batteries for battery electric vehicles.

Conclusions

The asymmetrical power held by lead firms portrayed in conventional GPN analysis is not fully applicable in sectors where (new) regulations, technologies and the subsequent market changes could have a disruptive effect on the governance structure of inter-firm relationships. Different from the commonly adopted analytical approach which focuses on inter-firm relationships and regional development, such as strategic coupling and regional diversification (McGregor and Yeung, 2022), this paper complements the generic GPN framework by proposing an analytical framework to examine the disruptive impacts of industrial megatrends on inter-firm relationships, especially the competitive dynamics between lead firms and their tier-I suppliers in GPNs. Industrial megatrends are accounted for by three explanatory variables in forms of regulatory, market and technology changes, while the firm-to-firm competitive dynamics is the dependent variable in the framework (Figure 1). Although lead firms are becoming more specialized and highly efficient in specific product segments, the GPN boundary becomes more permeable due to the disruptive effects of industrial megatrends, the result of a combination of new regulatory, technology and market changes. This external shock alters the cost-capability ratios between lead firms and their tier-I suppliers, which could result in the exit and entrance of some lead firms or tier-I suppliers. Subsequently, a reconstituted GPN, with a newly established boundary, is formed.

Applying the reconstituted GPNs to the automotive industry reveals how a combination of regulatory, technology and market changes alter the competitive dynamics between firm actors. The standardization of vehicle platforms based on modular architecture (Lung, 2001) pushes certain tier-I suppliers to develop as systems suppliers of service parts: system integrators who work relatively independently on the design of functionally related non-contiguous component systems for automakers. Automakers (lead firms) create demand for systems suppliers but their relationship is a symbiotic one: automakers need the technical expertise of systems suppliers to provide technical solutions for their car designs. A reconstituted automobile-automotive GPN (AAG) with two relatively ‘distinctive’ production networks illustrates their symbiotic and arm-length relationships: (i) automakers and their captive subcontractors for commodity parts, as hypothesized in conventional GPN analysis, and (ii) systems suppliers and strategic partners (Figure 2).

The AAG provides a dynamic account of the industrial megatrends, namely the disruptive effects of electrification, digitalization and autonomous driving, on the competitive dynamics between lead firms and their suppliers in the automotive industry. The domination of conventional automakers in the AAG has, however, been curtailed by the rising cost-capability ratio, partly due to the vicious circle of long investment lead-time with excess production capacity, and low profit margins and R&D intensity. Importantly, the state regulations has changed the matrix of cost-capability ratios between automakers and suppliers significantly since the 1990s. Selected systems suppliers with electric drivetrain and micro-electronic control systems expertise are not only in a prime position to capture the value arising from the increasingly stringent safety and environmental standards, but are also more resilient to the changing market demands for electric powertrains. The bottom line is that whether cars are shared or autonomously-driven, they need more sophisticated micro-electronics control modules, electronic gadgets and the safety features that make up the 30,000 parts that go into a typical vehicle. Selected (new) systems suppliers with the right matrix of technological capabilities in NEVs and autonomous driving can more easily respond to the three emerging megatrends in automobile development: electrification, digitalization and autonomous driving. Instead of the asymmetrical power held by lead firms portrayed in conventional GPN analysis, this paper demonstrates that the inter-firm relationships could be symbiotic and arm-length in the reality.

This paper highlights the potential disruptive effects of regulatory, technology and market changes that could change the trajectory of industrial megatrends and thus alter the competitive dynamics between lead firms and their tier-I suppliers. Further research can conceptualize these disruptive events, from the nature, forms to functions of such shocks, on the inter-firm competitive dynamics. Given the ongoing industrial restructuring of the automotive industry from tier-I suppliers to OEMs, it is possible that the competitive dynamics may shift further under the ongoing industrial megatrends. This is especially the case for the accelerated pace of electrification of drivetrains and the adoption of even more sophisticated micro-electronic control systems in the drive toward autonomous driving.

Footnotes

Acknowledgements

The author is also very grateful for the valuable comments and suggestions from the handling editor, Prof Jennifer Bair and three anonymous reviewers on the earlier draft of this paper. As usual, the author is responsible for any remaining omissions.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author would like to show his gratitude for the financial support of the NUS Strategic Research Grant (R-109-000-183-646) awarded to the Global Production Networks Centre (GPN@NUS) for the project entitled ‘Global Production Networks, Global Value Chains and East Asian Development’ and the AcRF tier-I grand (R-109-000-281-115).