Abstract

Mumbai, along with a few other metropolitan cities in India, witnessed an unprecedented flow of finance capital toward the development of new real estate soon after efforts to liberalize the country’s real estate sector took force in 2005. Fifteen years later, however, the reality on the ground looks bleak. Not only does the demand for housing remain as high as ever before in Mumbai, but hundreds of real estate projects lie unfinished, abandoned, and/or unsold. In its attempt to make sense of the city’s real estate crisis, this paper brings to the fore important insights about the organizing logics of urban land markets. Drawing on an exhaustive database of real estate indicators combined with ethnographic fieldwork, the paper reveals a tendency among Mumbai developers to fight competition by chasing land irrespective of long-term financial prudency, which in turn hinders the development and sale of new real estate. The paper therefore proposes that the reproduction of capitalistic arrangements within Mumbai’s land market is precarious because the very lands that are to be turned into commodities inevitably become entangled in new socio-legal encumbrances, just as the separation of “land from man” begins to seem plausible. By demonstrating how real estate activity is nevertheless, centered problematically, around this unceasing yet always incomplete pursuit of commodified land, the paper contributes to the scholarly project of developing a heterodox conceptualization of land.

Introduction: Mumbai’s real estate crisis

Since the mid-1990s, shortly after the advent of pro-market reforms in India, Mumbai’s land market has been gradually liberalized, opening up new territories for private investment, and prioritizing real estate profit regardless of its social or productive function. The first of many big changes to make real estate markets internationally accessible was the legalization of foreign direct investment (FDI) in “urban township construction” in 2002, and further liberalization of the policy in 2005, by the Indian government. Around the same time, the Securities and Exchange Board of India also began allowing venture capital funds to invest in real estate, which until then was subject to heavy restrictions, thereby spurring the emergence of domestic real estate investment funds (Searle, 2016). As a result, Mumbai, along with a few other metropolitan cities in India, witnessed an unprecedented flow of finance capital toward the development of new real estate. Private, large-scale production and consumption of real estate, and housing, in particular, replaced what had otherwise been a state-led project. This shift was critical in that it not only promised to deliver millions of new housing units for a new post-liberalization middle class but also signaled a newfound footing on the global economic stage for India (Fernandes, 2006).

Construction activities in Mumbai’s island city and northern suburbs soared as the local state began making certain highly valued lands available for development through a series of industrial land conversions, slum clearance schemes, and the de-reservation of certain public lands (Adarkar and Phatak, 2005; D’Monte, 2006). Recognizing an opportunity to build on the new sources of capital, and eager to produce globally familiar elite landscapes, several enterprising private developers threw their hats in the ring (Weinstein, 2008). Mumbai’s redevelopment schemes, in particular, allowed aspiring developers to enter into the city’s increasingly lucrative property markets without the outright purchase of land. As a result, the number of developers operating in Mumbai grew 457% in 15 years (Liases Foras, 2018), with many of the early participants having little or even no building experience. The remarkable rise in developers led to similar growth in the number of projects being developed (+439%) and the number of housing units planned for production (+519%) over the same period (Liases Foras, 2018).

While the quantity and scale of residential real estate projects underway in Mumbai mark the enthusiasm with which finance capital once flowed into the city’s real estate sector, today, many of these projects have been left unfinished, abandoned, and/or unsold, reflecting a bumpy unfolding of liberalization efforts. The city has become littered with thousands of such “zombie buildings,” that are drowning in debt amidst the collapse of Mumbai’s speculative urban development (Ghosh and Pandya, 2019; Goldman, 2023). In turn, several developers in the city, many of whom emerged as a consequence of the new sources of finance available to the sector, have filed for bankruptcy, leaving thousands of small investors and first-time homebuyers stranded (Parkin, 2019). This spate of unforeseen events, begs closer examination into the logic of neo-liberal urban production, wherein capital is channeled into locally embedded assets, namely real estate (Weber, 2010), through the creation of anchoring coalitions by local experts, namely real estate developers (Searle, 2018). For, what explains the impediments to the marketization of land in Mumbai despite the increased availability of funding, easing of regulations pertaining to land use/development, and sustained demand for new real estate?

Recent scholarship on speculative real estate development in India has tried to get at the logics behind “failed infrastructures” or more broadly, the uneven outcomes and spatial configurations of speculation and risk. Drawing on Bengaluru, India’s third most populous city, as a case study, Michael Goldman highlights how modes of urban development are becoming increasingly sensitive to “the imperatives of the rapid turnover of capital” and geared to “luring and tying down investors, while also anticipating their imminent departure” (Goldman, 2010: 230). In a more recent paper, Goldman demonstrates how large private equity firms capture markets of depressed assets of unsold housing and unfilled office space in India, by leveraging these and similar assets as collateral for investments elsewhere, establishing further the vulnerability of urban development to the dynamics of global financial flows (Goldman, 2023: 16).

Furthermore, as, Llerena Searle points out, the routes of accumulation forged to attract foreign capital into Indian real estate have also proved to be messy and paradoxical, as local intermediaries, rather than serving simply as conduits for finance capital, generate different kinds of risks and slow transactions, thus contributing to further uncertainty, or what she calls, the “contradiction of mediation” (Searle, 2018).

The above works, among others (see: Sood, 2017 for a comprehensive overview of speculative urbanism in the Indian context) are compelling in that they identify the goal of speculative investment, especially in the Global South, as not just to corner and monopolize, but also to quickly “get out” with higher-than-average profits. However, the deployment of the “optics of finance” to study speculative real estate development, has been critiqued for positing too mechanistic a relationship between global financial flows and the trajectory of urban development (Rouanet and Halbert, 2016). In particular, Halbert and others have argued that Goldman’s conceptualization of speculative urbanism leaves little space for the agency of local nonstate actors and resistance, partly described by Benjamin’s (2008) occupancy urbanism and Weinstein’s (2014b) durable slum. Besides, even though real estate is a popular financial investment, it entails a great deal of uncertainty, often requiring participants looking to get in, to engage in ad hoc tactics (Baliga and Weinstein, 2022) and faith-based decision-making (Rahman, 2022), which contribute greatly, if not more than the fickleness of global finance, to the crisis- tendencies of speculative urban development. This paper, therefore, shifts attention to the responses of local developers to the uncertainty and indeterminacy of real estate development, by taking their decision to “get in,” as its analytical starting point (Beckert, 2016). In doing so, the paper contributes to a heterodox conceptualization of land, which acknowledges the multiplicity of “impairments” that simultaneously hinder land’s commodification and augment its perverse effects.

The paper is structured as follows: In Section 2, I deliberate the theoretical productiveness of acknowledging both land’s ability to serve as a conduit for capital accumulation and a hard to assemble resource for capital “fixing.” Then, I provide a background into Mumbai’s real estate landscape in Section 3, highlighting how Mumbai’s unyielding development uncertainties and increasingly stricter conditions for financing, pose as challenges to developers in their strive to fight competition. In wanting to study developers’ responses to these challenges, and ultimately understand which concerns are given more weight over others and how that shapes the land market, I investigate in Section 4, the domains of competition most important to developers, using secondary data on firm-level real estate sales and production indicators. I then delve further into developer behavior in Section 5, relying on a combination of ethnographic research and data on project launches, to demonstrate how developers’ strategies to stay relevant, favors temporally closer concerns linked to land acquisition more so than longer-term concerns such as debt management. The paper ends with the proposition that the speculative logic followed by local developers, to “get in” no matter what, contrasts the logics of global finance, which is most concerned with “getting out” quick. Such a disconnect, I argue, frustrates efforts to commodify land while also contributing to the crisis that ensues from land’s commodification.

Land as a commodity

In recent times, a wide range of scholarship that recognizes land markets as highly demanding arenas of social interaction has brought renewed interest to the debates around land’s commodification (Fraser, 2014; Naybor, 2015; Prudham, 2013, 2015). Scholars such as Li (2014) contend that the spectrum of action and reflection concerning land cannot be captured if we define land narrowly, as “ownable property.” For, as Li points out through her study of privatization of property in upland villages of Sulawesi, Indonesia: “[land] may be privately owned, but for centuries much effort has been dedicated to preventing its privatization by surrounding it with customary injunctions, suppressing land markets, setting aside protected areas, and so on.”

But while land’s diverse affordances make it especially challenging to assemble as a resource available for global investment, this work is nevertheless accomplished, albeit incompletely and often with struggle, as demonstrated by Levien (2018) in his study of land grab in rural India. It is for this reason that Christophers (2016: 137) and others argue for land’s treatment as a real commodity, both theoretically and empirically, because as he notes, “for all the frustration of capital that can occur, the fact remains that land is successfully commoditized – relentlessly and increasingly universally – and it does widely serve as a successful conduit of capital accumulation.”

At the root of this debate lies not whether fictitious commodities like land, labor, and money can be disembedded from their socio-cultural contexts and treated as real commodities, as famously questioned by Karl Polanyi, but rather the theoretical usefulness of analyzing land through the Polanyian lens, which seeks to dismantle the market-state binary (Peck, 2013; Prudham, 2013). Therefore, where Block and Somers (2014) have argued that both disembedding and commodifying fictitious commodities are ideological projects engaged in by market liberals, others have criticized this interpretation for not providing a sufficiently robust framework to capture the multiplicity of perverse consequences that unfold when market forces are unleashed; “setting off chains of real consequences that must be taken seriously” (Polanyi and Kari, 2018). Usefully, the need to acknowledge both concerns has triggered efforts to develop a comparative, heterodox framing of commodification, which, Fred Block notes, involves capturing the dynamics of impairment that neo-Polanyian scholars are concerned with, without engaging in the reification of markets as natural entities separate from the state (Block, 2022).

A small but growing body of literature has contributed to the dialectical project of conceptualizing land’s commodification as necessarily incomplete, involving a double play of association and disassociation of land from its contextual setting (Fairbairn, 2013; Gagné, 2021; Martin, 2019). These works are significant in that they delve into the pluralistic logics and outcomes of “separating land from man. . . to satisfy the requirements of the real estate market” (Polanyi, 2001: 187). A related strand of work that has tended to dominate the discourse on land markets in India, has relied on the frame of “speculative urbanism” to get at the logics behind the turbulent trajectory of land development in the neoliberal era (Goldman, 2010, 2011, 2023; Halbert and Rouanet, 2014; Searle, 2016, 2018). By demonstrating how attempts to transform fixed, illiquid parcels of land into financial assets open to global capital have paradoxically contributed to illiquidity in India’s real estate sector (ultimately requiring further intervention by the state), these works have contributed to the nuanced understanding of land’s commodification as an incomplete, dualistic, and fraught process.

While the frame of speculative urbanism has proved useful to delineate how the whims of finance capital (re)produce an unstable development environment leading to land market dysfunction and crisis, it has largely relied on a “follow the money approach” to uncover the chains of transnational investment that contribute to land’s commodification and decommodification (Halbert and Rouanet, 2014: 475). In particular, the approach has sought to unravel the vulnerability of urban development to the strategies of global financial flows, namely private equity’s ultimate concern of “getting out” (Goldman, 2023) despite the contradictions of mediation and financial capital switching (Searle, 2018). However, as a consequence, the approach seemingly posits a mechanistic, if not orthodox, relationship between global financial flows and the trajectory of urban development, pinning its focus on the “relentless dynamism and hyper-mobility of finance capital” (Goldman and Narayan, 2021), while flattening other fundamental concerns like land being a “strange object” (Li, 2014), the agency of local development actors (Brill, 2022), the uncertainty surrounding future values of land (Weber, 2021), and faith-based decision making in response to such uncertainties (Rahman, 2022).

This paper, therefore, contributes to the theoretical project of developing a conceptualization of land that is sympathetic to both—it’s more often than not function to serve as a conduit of capital accumulation, and the perverse consequences that ensue from land’s treatment as a commodity. It does so by focusing on the responses of local developers to the indeterminacies of land’s commodification. The analysis reveals that a wide range of socio-cultural-economic expectations underpin developers’ pursuit of commodified land (beyond global finance’s relentless quest for higher returns), including and most significantly, the visibility and distinction that successful land acquisition brings to competing developers. The paper argues that for developers operating in a context where temporally closer concerns linked to land acquisition dominate longer-term concerns such as debt management, speculative urban development becomes all about “getting in,” in stark contrast to the logic of global finance, which is most concerned with “getting out.” In highlighting this disconnect between the goals of developers and financiers, which contributes to the multiplicity of “impairments” that simultaneously hinder and produce perverse effects to land’s marketization, the paper seeks to productively build on land’s heterodox theorization, using Mumbai as a case study.

Cracking the messy business of land development in Mumbai

Mumbai’s unique topography and high population density have contributed to a scarcity of land, to such extent that uninhabited, developable land is almost non-existent in the city today. Informal settlements, or “slums,” as they have come to be officially recognized, occupy 36.45 km2, or 48.6% of the total developable land area in Mumbai, and are scattered across the entire landscape of the city, including the south and west regions where real estate is most expensive (Bhagat and Yadav, 2017; Das et al., 2018). Over the last two decades, state authorities have responded to the shortage of developable land by incentivizing redevelopment, under the pretext of ameliorating the city’s housing crisis. These measures most notably involved the scrapping of protective policies such as the Urban Land Ceiling and Regulation Act, which restricted hoarding of land by single persons or entities, diluting laws governing the redevelopment of industrial lands, and the demolition of slum settlements. Efforts to increase land-use efficiency, and make urban land “economically productive,” meant that urban residential redevelopment, and the redevelopment of slums, in particular, became the primary development model for real estate production in Mumbai (Bertaud, 2004). By 2014, redevelopment projects accounted for over 80% of all proposed real estate activity in Mumbai, making the social and technical work of re-purposing land a defining feature of the city’s land market (Bombay High Court, 2016).

As a protection against developers coercing residents to participate in redevelopment work, the Slum Redevelopment Authority, and the Maharashtra Housing and Area Development Authority, the two official agencies through which redevelopment work is administered, require that 70% of residents consent to a proposed project before approval is granted. Acquiring consent is, however, a drawn-out process involving tedious negotiations between developers and residents (Baliga and Weinstein, 2022). Since residents have varying concerns regarding compensations and do not constitute a homogenous group of actors, disagreements among them, including over which developer to support, are both common and inevitable (Patel and Arputham, 2007). The struggle over consent acquisition is furthermore, exacerbated by the fundamental problem of unclear titles and ambiguous property rights. Residents and developers must therefore navigate opaque rules of land ownership and exchange, for consent to be acquired (Weinstein, 2014a). Besides, with the redevelopment scheme requiring residents to hand over their land to a developer for a loosely specified period of time while redevelopment takes place, the impact of non-cooperation and development uncertainties is far more significant for residents than for developers, as a consequence of which, developers have found it difficult to get residents to vacate their homes, even when a majority of them consented to a redevelopment project.

Ethnographic accounts of redevelopment efforts at Dhobi Ghat (Baliga and Weinstein, 2022), Dharavi (Weinstein, 2014b), Golibar (McQuarrie et al., 2013), and Santacruz (Arputham and Patel, 2010)—sites that have taken several years to develop, and/or remain hindered by conflicts—reveal just how tedious and unpredictable redevelopment work can be, even for the most experienced developer. These case studies show how urban institutions combine with the space of the slum to produce a distinctively urban subjectivity, that reflects a faith in liberal institutions such as equality before the law, even when the state is a key actor in appropriating land for private construction (Dupont, 2011; Ghertner, 2011; Shatkin, 2016; Weinstein, 2014b). When examined as a field of struggle, these sites reveal a more expansive political possibility that can sustain an inclusive and tolerant urban imaginary, in direct contrast with the way struggles over urban land are usually presented (Blomley, 2004; Doshi and Ranganathan, 2017; Ghertner, 2014; Sassen, 2013; Shatkin, 2014). The challenges of redevelopment moreover, demonstrate how political entrepreneurship, while necessary, is not sufficient to facilitate development work amid institutional fragmentations and political contestations. Instead, land exchange is often pinned on ad hoc, short-sighted strategies geared toward solving highly context-specific problems (Baliga, 2020).

Yet, not long after the Indian real estate sector was opened to new sources of finance, real estate development in Mumbai witnessed an unprecedented shift, with many PE funds lining up to invest in risky slum redevelopment ventures. Omkar Realtors and Developers Pvt. Ltd, was one of the first developers in India to secure PE funding for slum redevelopment work (Nandy, 2011). In 2011, Red Fort Capital Advisors Pvt. Ltd, a real estate focussed investment fund, invested ₹ 250 crores (US$30 million) in a slum redevelopment project led by Omkar. That same year, Omkar raised a second round of PE funding, of ₹ 200 crores (US$25 million), from Indiareit Fund Advisors Pvt. Ltd, making Omkar the most successful developer to reign in PE funding for slum redevelopment work. In keeping with the trend, IIFL Alternate Asset Advisors Ltd, made their first investment from their first private equity (PE) fund, into a central Mumbai slum redevelopment project developed by Sheth Creators, and ASK Property Investment Advisors Pvt. Ltd invested ₹ 100 crores (US$12.5 million) in Godrej Properties Ltd’s first redevelopment project in Mumbai. These deals marked not only many “firsts” but also signaled the enthusiasm with which global capital sought to capture the high rent gap that Mumbai’s slums promised. For, slums, as Kaustuv Roy, executive director of property advisory firm Cushman and Wakefield put it, “occupy some of the most expensive locations in the city [with] very high potential for price appreciation,” and the likes of Omkar, as Forbes reported, had “cracked the messy business of slum redevelopment in Mumbai” (Nandy, 2012; Srivastava, 2012).

These new modes of financing spurred remarkable growth among developers who could successfully acquire inhabited lands for redevelopment. However, since the uncertainties of redevelopment remained unaddressed, financing arrangements were subject to continual re-work, keeping in mind the risks for and interests of lending institutions. Equity-based partnerships were quickly replaced by mezzanine debt- a hybrid between debt and equity, which gives a lender the right to convert to an equity interest in the development firm or project, in case of default, where the broad definition of default covers deviation from scheduled timelines. Developers could, under these new conditions, be replaced out of a project, should they fail to deliver timely and sizable gains from land’s development, that is, the very expectation that wins them access to funding in the first place. In other words, as regimes of financing became stronger and stricter in response to Mumbai’s unyielding development uncertainties, developers found themselves aggressively chasing the promise of commodified land, while being chased by the inevitable crisis that comes with the failure to deliver on that promise. It is within these contradictory realities that developers in Mumbai compete to crack the messy business of land development, struggling to turn land into tradeable global assets via financing routes that risk their long term survival in the market for land.

Developer distinction in the pursuit of land

When I began fieldwork for this project in February 2017, I was intrigued by the world of real estate developers- a group that had experienced rapid expansion following the influx of foreign funding a decade earlier. I embarked on a 15-month-long ethnographic study, involving a total of 87 semi-structured interviews and numerous informal conversations with individuals directly or indirectly engaged in real estate development in Mumbai. Through these interviews, I discovered that I was not alone in attempting to comprehend the field of developers. Various other actors, including financiers, consultants, and developers themselves, were striving to distinguish and categorize developers within a relatively new context. I noticed my interview participants employed terms such as “revolutionary,” “bankable,” and “fly-by-night” when talking about different types of developers. These terms, to me, denoted not just developer distinctions, but also developer strategies, which eventually became a focal point for my research.

During the many real estate conferences I attended as part of my fieldwork, I also found that land market actors in Mumbai talked extensively about transaction costs relating to land acquisition and government approvals, more so than the uncertainty pertaining to demand-supply dynamics. I saw this as their way to signal which developer characteristics or competences are more relevant for success over others. Without any immediate or easy solutions in sight for project delays, financiers especially, referred to the capability of developers to get things done against all odds, as a way to cope with, and make decisions in spite of, developmental uncertainties.

“If a developer is effective in overcoming hurdles, whatever they may be. . . having the right political connections. . . the foresight to prevent roadblocks basically, I will put my money on him,” claimed Vasudev Krishnan, chairman of a non-banking finance company, when asked about the conundrum of financing risky real estate projects (interviewed, September 2018).

Interviews with several other finance professionals led me to think that the perceived ability of a developer to acquire land without incurring unexpected delays was the key to accessing the new sources of finance capital waiting to be deployed for real estate development in Mumbai.

Of course, for a more definitive claim, a controlled experiment would need to be carried out, to assess how financiers make decisions when lending toward real estate development, and the degree to which they favor developer reputation over asset value securing the deal, and the project’s projected financial revenues. However, this was not quite the intent of this research. Rather, I was interested in studying developers’ quest to be noticed and become distinguished among a sea of competing developers, and more specifically the strategies they adopted to get there.

To delve deeper into the nature of competition among developers, and more specifically their distinction strategies, I examined the primary domains of competition that are of significance to developers in Mumbai, and thereby the uncertainties that are given more weight over others when making decisions about land’s development. Carrying out such an investigation, however meant relying more on quantitative data on real estate sales and production indicators, as opposed to the initial ethnographic work that led me to this investigation, and which informs the broader project that this paper is a part of. The rest of this section therefore focuses on what aspect of land’s marketization is most relevant for developers looking to “get in,” and whether or not this bounds their ability to successfully develop land, and ultimately create a stable environment for land’s marketization.

Mapping developer distinctions

Methodology

In order to examine how, and to what extent, real estate developers distinguish themselves from each other to beat competition, I measure standard deviations across three primary domains of competition that influence developers’ organizational life chances. These are competition for customers, financing, and land, which are directly or indirectly reflected in the real estate units of launch price, sales velocity, and ongoing projects. Launch price is the publicly advertised price of a property when a developer launches a new project. While this may not be the actual price at which the property is transacted, launch prices are a good indicator of how developers view themselves in relation to other developers (and consumers) when pricing their products. Sales Velocity, on the other hand, is a measure of how quickly developers are able to sell off their stock (of apartments). Sales velocity is, therefore, an indicator of how consumers differentiate between developers when buying property on the one hand, and the holding capacity, or crudely put, the financial power of a developer, on the other. Finally, ongoing projects is the number of projects a developer has ongoing at any point, which is a rough measure of the scale of operations of a developer, as well as their resourcefulness in sourcing land.

For measuring standard deviation across price, sales velocity, and ongoing projects among a group of developers, other variables, such as time and location, must be kept constant. Since it is impossible to study projects or developer activity in a single location, the closest alternative is to identify a locational cluster with (1) a fairly high representation of developer types and (2) a fairly low price-differentiation across properties (per unit area) within the cluster. I identified two such locational clusters, one in East Mumbai, comprising the adjoining neighborhoods of Ghatkopar and Vikhroli, and one in North Mumbai, in the neighborhood of Kandivali, where several new residential buildings have come up in the past decade (Figure 1). Since the price and sales velocity of real estate does not change significantly in a 1-year period, data is collated in yearly cycles. However, to avoid bias toward a particular phase in the evolution of Mumbai’s real estate market, I examine deviances in five different years (2009, 2011, 2013, 2015, and 2017). Data for this study was procured from Liases Foras (LF) India—a private real estate data agency based in Mumbai; hence minor errors in LF’s dataset are reproduced in this research as well. Most noteworthy of these errors are: delay in noting of launch price, 1 and misreporting of sales velocity in the first few quarters. 2 To mitigate these errors, I only considered fourth-quarter data in case of launch price, and the average performance of the first four quarters in case of sales velocity.

Locations analyzed for standard deviation across price, sales, and projects (Compiled by Author; Map: Kepler.gl).

Other discrepancies in the methodology include, as mentioned above, the attribution of the price difference to developer reputation as opposed to locational features; ignoring project size/scale in the calculation of sales velocity 3 ; as well as ignoring the size of each project in the counting of a developer’s ongoing projects. While the discrepancy related to price difference has been left unaddressed (since the selection of neighborhood clusters already attempts to minimize locational price variation), data on sales velocity has been normalized to account for the vastly different sizes in projects. Discrepancies in project count on the other hand, while possible to correct, is not essential, since the intention of this exercise is not to measure the absolute size of a developer’s land bank, but rather their resourcefulness in acquiring new lands. As a result, standard deviations, in reality, would be lower than the findings presented below in case of price, and to some extent sales velocity (since projects located in better areas would also sell faster, irrespective of developer reputation), and higher in case of project count (as larger land parcels are more difficult to acquire).

Findings

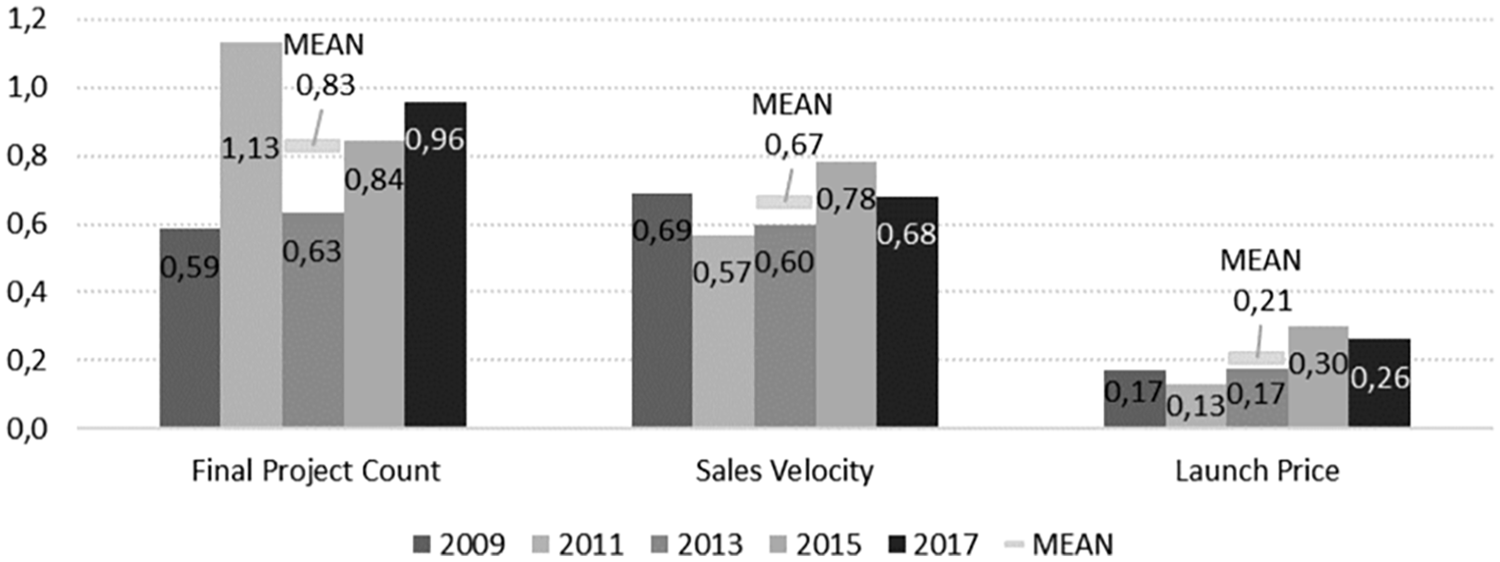

My analysis reveals that launch price across all 5 years has the lowest coefficient of variation (average of 0.21) as compared to sales velocity and project count (Figure 2). Put differently, quoted price of built property (per unit area) seems to be the least distinguishing factor among developers in Mumbai. There also appears to be little consistency in which type of developer commands a higher or lower price for their product. This is because many other factors such as project location, its scale, the holding capacity of a developer, and product features (amenities, material specifications, etc.) determine the price of real estate.

Comparison of the builder groups’ coefficients of variations (Compiled by Author; Data: Liases Foras, 2019 ).

The coefficients of variation of sales velocity across the 5 years are higher (average of 0.66) than launch price but lower than project count. Again, there is no consistency in the pace of sales of different developers, that is, reputed developers do not necessarily sell their stock faster than lesser-known developers. On the contrary, developers of low repute clocked in the highest sales velocity in most years. According to real estate analysts, this is because small developers tend to focus on the small-scale redevelopment of old residential building clusters, wherein (the few) additionally built flats are sold to family members or friends of existing residents. Hence many redevelopment projects of this type are sold out almost instantly after being launched.

The highest coefficient of variation among the three factors is of ongoing project count (average of 5 years = 0.83). Therefore, the most distinguishing feature of a Mumbai developer is the number of projects they have ongoing at any point. However, it is worth noting that there is no correlation between project count and launch price or sales velocity. In other words, having a high number of ongoing projects does not give developers any advantage in speed of sales or product pricing. This is because, when developers venture outside their neighborhood of dominance, which is inevitable when expanding project count, they lose their network advantages. Yet, as these findings confirm, developers in Mumbai are most inclined to distinguish themselves by increasing their project count.

Mapping developer growth

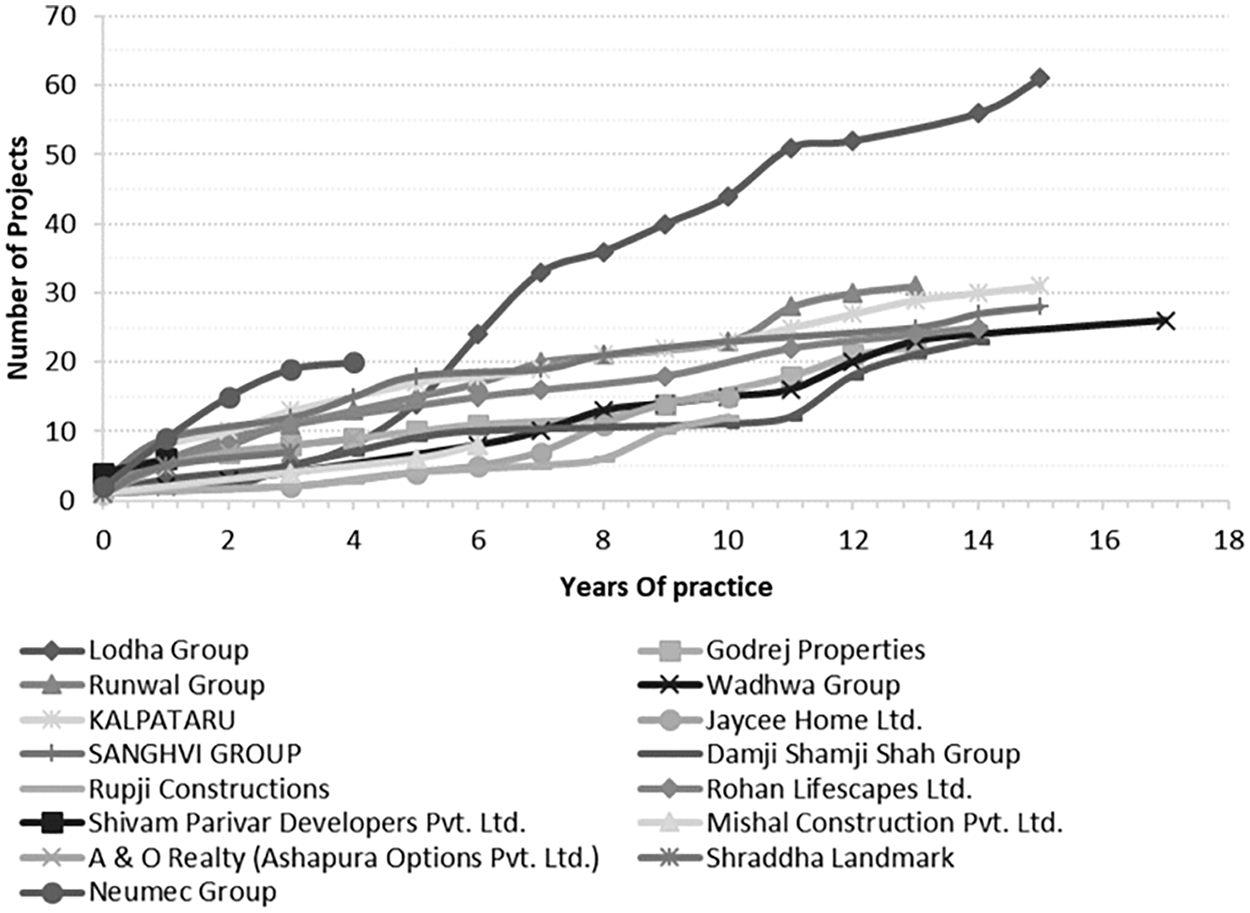

To further investigate the nature of competition that distinguishes between developers with an unequal number of ongoing projects, I look at the past project records of the same developers whose performance I analyzed above. The intention is to determine whether the deviance in developers’ ongoing project count relates to their different points of entry into the market, or rather a difference in each developer’s ambition/ ability to scale up. I, therefore, examine the pace of growth of each developer, in terms of project count, by ignoring the staggered starts of their operations. Since the idea is to test how quickly developers increase their project count, I filtered out developers with less than five projects. Doing so reduced the sample size to a total of 16 developers, from the original pool of 64 developers. Among the selected 16 developers, the lowest project count to date is that of Shivam Parivar Developers (year 0: 4 projects; year 1: 7 projects), and the highest project count is of Lodha Developers (year 0: 1 project; year 15: 61 projects).

Findings

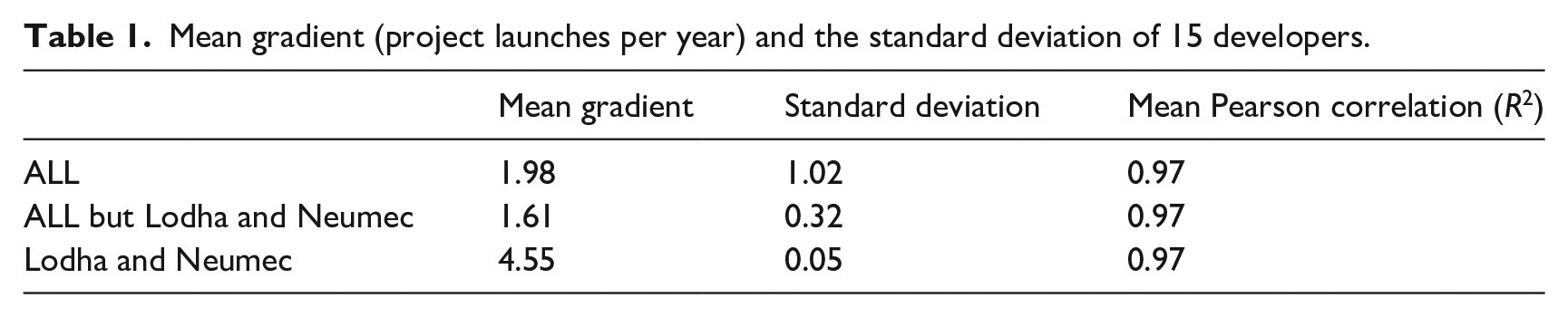

My findings reveal, firstly, that all developers follow a linear growth progression (Pearson coefficient for the linear correlations is 0.97 ± 0.03, Figure 3). This means that developers continue to launch new projects at a steady pace as time progresses—irrespective of their firm size or changes in market conditions. In other words, there is no observation of exponential growth or sudden decline in any developer’s project count. Secondly, all developers, except two (from a total of 16), have a very similar growth gradient. The mean gradient among the majority of developers is 1.62 launches per year (with a standard deviation of 0.32). This means that most developers with a project count greater than 5, follow each other in their pace of new launches, to launch 1–2 new projects every year, even though land acquisition and approvals have no standard timelines. The two exceptions to this trend are Lodha and Neumec, with gradients of 4.5 and 4.6, respectively (Table 1).

Project growth rate of 16 developers shows a linear growth of about 1.62 launches per year (Compiled by Author; Data: Liases Foras, 2019).

Mean gradient (project launches per year) and the standard deviation of 15 developers.

To summarize, an examination of variance across three primary domains of competition reveals that developers in Mumbai distinguish themselves, least of all, through the pricing of their products. While the difference in speed of sales is more noteworthy, it is the number of projects in a developer’s portfolio (ongoing or completed) that mostly sets developers apart from each other. Furthermore, among the developers that stand out because of their high project count, there is an observable pattern and similarity in the pace of portfolio expansion, barring a few exceptions. Developers, therefore, seem to follow each other to launch a certain number of projects every year, even though doing so has no positive impact on their performance in other domains of competition.

Resource administration over real estate production

A linear growth pattern, achieved through steady expansion of project portfolio is peculiar for Mumbai developers, especially those engaging in redevelopment work, which, cannot be carried out through standardized practices within pre-determined timelines. More importantly, a linear pace of growth is hard to sustain given the strict restrictions on land financing in India. As per guidelines set by India’s central banking regulator, the Reserve Bank of India, private developers cannot avail, in part or full, bank finance for the purchase of land for real estate development. The unavailability of bank finance for land acquisition means that developers must either wait until they are flushed with cash at the end of a project’s sales or take on a high-interest loan from shadow banks, to be able to purchase land for a new project. However, both options are unviable, as, on the one hand, developers’ revenues are neither consistent nor quick to come through, as is evident from the high unsold inventory recorded by the city every year since 2017 (Urs, 2020). On the other hand, since project uncertainties are highest at the land acquisition stage, lenders of all sorts are averse to extending loans to developers until all acquisition and permit-related uncertainties are out of the way. Under such conditions, developers must look for alternate means of resource management to keep up with the competitive pace of portfolio expansion.

One such alternate, and not-so-legal means of acquiring new lands for development, I was made aware by my participants, was through the diversion of funds, from one project to another. Financiers I talked to, claimed that funds diversion is the most significant risk when lending to a developer, or investing in real estate development in India. And that, even though the rules of financing have gotten tighter over the years to ensure that cash outflow and income from a project remains dedicated to the project, developers nevertheless find ways to overcome these restrictions, partly because of financiers’ own laxity. Since developers normally rely on a combination of financing sources for a single project, and since most real estate financing is debt-based, financiers tend to be less vigilant about the flow of funds, so long as a developer is not defaulting on repayments.

Developers acknowledge, off the record, that the practice of funds diversion is not uncommon, especially during real estate booms, when financiers have their guards down. Developers may, therefore, at such times, divert revenue earned from one project through customer advances, toward the purchase of new land parcels for future development, instead of using that money for project completion. Since financing provided by customers comes at zero cost, any increase in the value of a newly purchased land is pure profit for the developer. In seeking to restrict such malpractices, the Indian Parliament, in March 2016, established a Real Estate Regulatory Authority (RERA) in each state for regulation of the sector. As per the newly introduced RERA regulations, 70% of all revenue collection of a project must now be protected in an escrow account managed by a third-party bank or recognized lender. Developers are, however, able to bypass the restricted access to customer payments by delaying the official registration of the property sale and collecting a large amount of pre-payment in the form of cash. According to real estate agents, a developer may typically collect up to 25% of the sale price from customers within the first 3 months of booking, while registration of the sale may only take place after all approvals have been received, which could be as much later as 4 years, or more.

Conversely, when real estate sales are slow, and developers have access to thinner streams of income, the goal shifts from portfolio expansion to debt management. Developers strive to service their debt obligations, at such times, by typically replacing expensive debt with less expensive debt, such as customer advances, or bank borrowing. However, since developers usually have multiple ongoing projects at any time—all at varying levels of economic productivity—this practice also entails the diversion of funds from one project to another to ensure that their overall earnings or EBIDTA (Earnings Before Interest, Tax, Depreciation, and Amortisation) stays healthy. While financial firms receiving the repayments should ideally flag this practice, financiers acknowledge that they rarely carry out due diligence to ascertain whether the sources of repayments are fresh sales, further borrowing, or diverted funds from another project. This practice of debt management by moving project resources around—though illegal—is “all too common among Indian developers” according to Pankaj, ex-chairman of a housing and development finance company. The logic behind the practice is, however, peculiar, he notes. Adding that, “most businesses operate on reverse logic. That is, when the firm is cash-rich, they pare debt. Developers, on the other hand, behave abnormally by leveraging themselves further in good times and settling their debt when most pressed for cash” (interviewed November 2017). Pankaj further notes that Indian developers behave this way because they have been traditionally deprived of funding, and hence their actions reflect what he calls a “scarcity mentality,” which compels them to prioritize resource administration over real estate production.

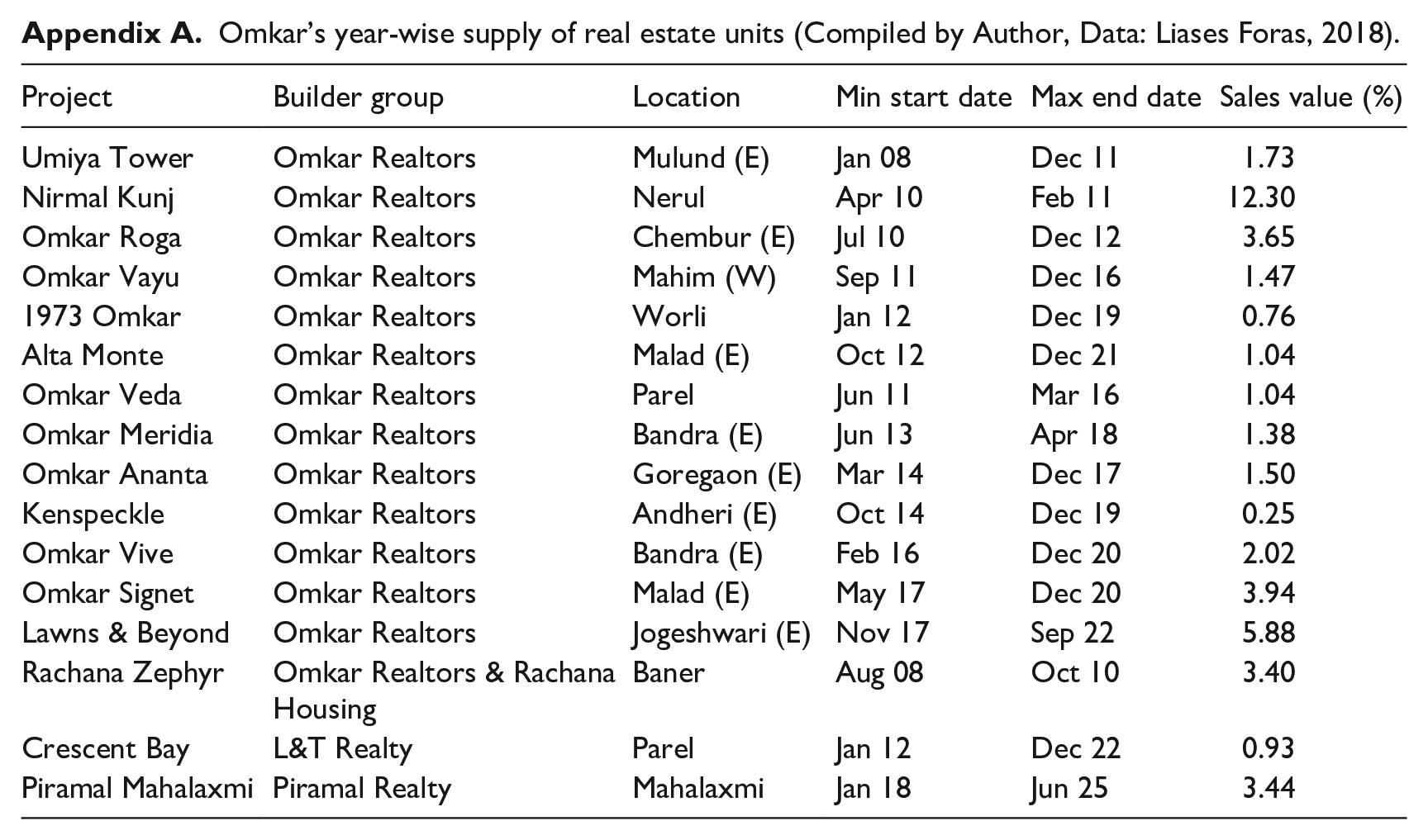

While there is no way for researchers like me to prove financial discrepancies, I found the case of Omkar developers, a firm whose promoters Babulal Varma and Kamal Kishore Gupta have been charged by India’s Enforcement Directorate “for cheating and diversion” of a ₹ 410 crore (US$50 million) loan taken from India’s Yes Bank, useful to illustrate the plausibility of Pankaj’s assertion (Yadav, 2021). A study of Omkar’s development activity shows that the firm’s production followed a steady growth, even when its sales did not keep pace, or were relatively tumultuous (see: Appendix A). Furthermore, from 2015 on, Omkar had at least 10 projects—on-going or available for sale—in parallel, all at varying levels of economic productivity, ranging from 12.3% to 0.25% (calculated as a ratio of sales velocity and total available supply). Therefore, where slow sales contributed to Omkar’s resource scarcity, their multiple project count made possible, or rather rationalized, from Omkar’s perspective, the administration of incoming resources, through its redistribution among the many projects. In following such a logic, Omkar could have utilized funds reserved for the completion of an ongoing project, for the acquisition of future ones. Omkar’s case, therefore, illustrates that while new sources of formal finance made it possible for developers to increase their pace of production and land acquisition to match that of their competitors, it paradoxically opened new doors for developers to adopt practices outside of contractual expectations, to service the increased pace and scale of operations.

Fluctuating fortunes of real estate developers

Market actors in Mumbai recognize that turning land into salable real estate takes work, and this recognition has come to define the nature of competition and distinction strategies among developers. With no easy resolution to the hurdles of land development, developers with a demonstrable track record of project launches understandably stand out, if not appear bankable, amidst a sea of relatively new players.

For firms like Omkar that began their real estate careers with small residential redevelopments in the outskirts of Mumbai, the initial success with land acquisitions, and the funding opportunities that came with it, allowed them to quickly graduate to carrying out multiple, very large-scale developments in the most expensive neighborhoods. However, in the process, not only did these developers take on large amounts of debt under precarious conditions, but they also eschewed uncertainties of the future, like demand-supply mismatch, spurring them to deviate from contractual-legal obligations, ultimately risking their own long-term survival.

Though stricter rules of borrowing and newly introduced governmental regulations around funds management aim to curtail malpractices and instill financial discipline among developers, these rules are, in reality, difficult to enforce, and not always in the best interest of financiers. Rather than disciplining developers into being earnest debtors (Kallin, 2021), finance’s dominance over real estate activity, has exacerbated opportunistic behavior, because of developers overstretched, almost unrealizable debt obligations on the one hand, and the wider pool of projects developers have been able to create to move resources among, on the other. Nonetheless, the consequences of unserviceable debt and financial fraud has begun to catch up, triggering the downfall of several prominent developers, including, Omkar (Yadav, 2021). In the 2 years between 2017 and 2019, real estate topped the bankruptcy chart in India, with over 235 companies, mostly from Mumbai and Delhi, admitted for resolution under the Insolvency and Bankruptcy Code (John, 2019). Several developers, who had emerged as a consequence of liberalization of the real estate sector, and were recipients of much of the new sources of financing available for real estate development over the past decade, have had to shut operations abruptly, leaving thousands of small investors and homebuyers stranded.

This spate of sudden liquidations, marks a new kind of fragility that has come to underpin Mumbai’s land market: the fluctuating fortunes of real estate developers. With the organizational life chances of developers wildly uncertain, investors and consumers of real estate alike, are faced with the indeterminacy of decisions to plan for the future. Such indeterminacy undermines the preconditions for market exchange, wherein, at the very least, the reproduction of capitalistic arrangements and continued participation of market actors is assured. A collapse of expectations regarding future opportunities and foreshortening of future perspectives, is already evident from the dwindling foreign investments into real estate development in India (RBI, 2019). Therefore, while developers may or may not bounce back from bankruptcy, their unpredictable life expectancy, has indeed set-off a recurring crisis that poses obstruction to the marketization of land’s development, despite the sustained demand for housing in Mumbai.

Conclusion: Lessons from a crisis

The crisis of destabilized money supply and fluctuating fortunes of real estate developers offers important insights into Mumbai’s land market, particularly, the eternal pursuit of commodified land, and the contingencies that this chase brings with it. One of the key findings presented in this paper is that land market decisions are often guided not by expectations of future land-price behavior or increased production and sale of new real estate, but by temporally closer concerns related to the complications of land’s private acquisition and thereby, commodification. As a result, the timely completion and eventual sale of real estate projects through competitive pricing, end up becoming less important as compared to a developer’s ability to simply acquire new projects, at a steady albeit unsustainable pace. Such a tendency, toward the continual launch, if not actual production, or even deliberation of new projects, reveals the organizing power that the allure of commodified land has within land markets.

In a city like Mumbai, where much developable land is contested, it is no surprise that the imagination of commodified land dominates the minds of developers, investors, and home buyers alike, especially after the recent relaxation of land-use restrictions and financing regulations. The perceived success in acquiring new lands for development, in turn, serves as the means for developers to differentiate and distance themselves from competitors and assign themselves greater value, or distinction, in the process. This distinction tactic, I note, can be understood as a competition in which the styles of a “bankable developer” are in continual development, and those who do not follow this trend soon become stale, and irrelevant to their market peers. However, with ever more developers in Mumbai claiming to be good at overcoming uncertainties that accompany land’s privatized development, the strive for distinction has unfortunately meant hasty land acquisitions and project launches, supported by costly, if not precarious, financial arrangements. For local developers, therefore, speculative urban development is all about “getting in,” in stark contrast to the logic of global finance, which is most concerned with “getting out.”

Recognition of this disconnect in the speculative logics of global finance and local real estate production is useful not just for making sense of the thousands of unfinished and abandoned “Zombie” projects, but also to capture the variegated impairments that underpin land’s commodification. By examining why developers struggle to follow through on the execution and sale of launched projects despite the sustained interest and demand for real estate in the city, the paper unravels an important paradox. The very lands that are to be turned into commodities inevitably become entangled in new socio-legal encumbrances, just as the separation of “land from man” begins to seem plausible. The pursuit of commodified land cannot but be held back by the uncertainties that the promise of commodified land seeks to overcome. This self-compromising tendency of land markets points to impediments that are, despite the distress caused to homebuyers, linked to reasons intrinsic to the market’s organization, rather than an external, societal push back to land’s commodification, as is commonly expected and documented by orthodox scholars of the double movement.

Notwithstanding the impediments that keep Mumbai’s land markets in a perineal state of crisis, land’s development, or rather the promise to produce globally familiar elite landscapes, and the possibility to accrue profits from this promise, nevertheless lives on, unceasingly. Learnings from Mumbai’s real estate crisis are therefore useful for unraveling land’s duality, to serve both as a conduit for capital accumulation, and as a strange object that is challenging to assemble as a resource for global investment. In Mumbai, this duality plays out in peculiar ways. Developers turn to strategies that undermine their ability to create a stable development environment in order to stay relevant in a development context where the acquisition of land is a challenge in itself. And yet, with every incremental, and ever-so-often successful stride toward land’s assembly as a resource for accruing profits, the imagination of land as a commodity is reinforced, encouraging developers and allied market actors to continue to participate in and uphold land’s marketization. Such a dialectical understanding of the land market’s organization is significant for advancing land’s heterodox theorization, without getting caught in the theoretical frustrations of its analytical classification as a fictitious or real commodity.

Footnotes

Appendix

Omkar’s year-wise supply of real estate units (Compiled by Author, Data: Liases Foras, 2018).

| Project | Builder group | Location | Min start date | Max end date | Sales value (%) |

|---|---|---|---|---|---|

| Umiya Tower | Omkar Realtors | Mulund (E) | Jan 08 | Dec 11 | 1.73 |

| Nirmal Kunj | Omkar Realtors | Nerul | Apr 10 | Feb 11 | 12.30 |

| Omkar Roga | Omkar Realtors | Chembur (E) | Jul 10 | Dec 12 | 3.65 |

| Omkar Vayu | Omkar Realtors | Mahim (W) | Sep 11 | Dec 16 | 1.47 |

| 1973 Omkar | Omkar Realtors | Worli | Jan 12 | Dec 19 | 0.76 |

| Alta Monte | Omkar Realtors | Malad (E) | Oct 12 | Dec 21 | 1.04 |

| Omkar Veda | Omkar Realtors | Parel | Jun 11 | Mar 16 | 1.04 |

| Omkar Meridia | Omkar Realtors | Bandra (E) | Jun 13 | Apr 18 | 1.38 |

| Omkar Ananta | Omkar Realtors | Goregaon (E) | Mar 14 | Dec 17 | 1.50 |

| Kenspeckle | Omkar Realtors | Andheri (E) | Oct 14 | Dec 19 | 0.25 |

| Omkar Vive | Omkar Realtors | Bandra (E) | Feb 16 | Dec 20 | 2.02 |

| Omkar Signet | Omkar Realtors | Malad (E) | May 17 | Dec 20 | 3.94 |

| Lawns & Beyond | Omkar Realtors | Jogeshwari (E) | Nov 17 | Sep 22 | 5.88 |

| Rachana Zephyr | Omkar Realtors & Rachana Housing | Baner | Aug 08 | Oct 10 | 3.40 |

| Crescent Bay | L&T Realty | Parel | Jan 12 | Dec 22 | 0.93 |

| Piramal Mahalaxmi | Piramal Realty | Mahalaxmi | Jan 18 | Jun 25 | 3.44 |

Acknowledgements

The author would like to thank Gavin Shatkin, Tim Bartley, Liza Weinstein, Leon Wansleben, Suzi Hall, and members of the REFCOM group at KU Leuven for their thoughtful feedback and insightful comments on earlier drafts of this work. Additionally, sincere thanks to the three anonymous reviewers whose rigorous assessments and constructive critiques significantly enhanced the quality of this paper.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.