Abstract

We investigate trade fairs as markets. We combine literature on temporary clusters and that on the geography of markets and describe how the particular knowledge ecologies at trade fairs are enhanced by market devices. Our framework distinguishes the following three kinds of market devices: physical arrangements, judgement devices and prosthetic prices. Using this framework, we compare market constructions before, during and after three fairs for contemporary art in Basel. Our study presents the following findings. Firstly, the limited time and space at trade fairs lead to a proliferation of market devices. Secondly, different equipment with market devices leads to a hierarchy of fairs. Thirdly, trade fairs at the top of this hierarchy generate market devices for other temporary markets and thus contribute to the development of a uniform global market.

Introduction

Awareness that sufficient knowledge of markets and their functions is needed to understand spatial economic fragmentation and inequality (special issues in Economic Geography (2019, 94/3) and Environment and Planning A (2015, 47/9)) is increasing. The rising global significance of localised markets, such as trade fairs, has rarely been explored from such a perspective. However, some studies have investigated trade fairs (Bathelt and Schuldt, 2010; Li, 2014; Maskell et al., 2006). Herein, trade fairs are conceptualised as ‘temporary clusters’; that is, these fairs are places for particular knowledge processes, such as learning, information exchange and buzz (Bathelt and Schuldt, 2010), as well as centres where global relations are fused and consolidated (Bathelt and Cohendet, 2014; Li, 2014).

Studies on temporary clusters also investigate the effects of particular knowledge ecologies at trade fairs (Bathelt et al., 2017; e.g. Bathelt and Schuldt, 2010). However, the current research primarily investigates market exchanges as embedded in social relations. Therefore, economic sociologists such as Çalışkan and Callon (2010) or Muniesa et al. (2007), emphasised that markets are not only socially but are also physically established and indicate the importance of objects in the construction of markets and their disembeddment from social relations.

The current research intends to combine the findings of the two ‘schools’ to investigate the role of particular knowledge ecologies at fairs for the construction of markets. We use trade fairs as examples due to their increasing importance (Bathelt et al., 2014) and the contracts and sales that consummate them at trade fairs demonstrate the critical nature of such gatherings for trade (e.g. Andreae et al., 2013; Moeran, 2010). We combine the particular knowledge ecologies at trade fairs with ideas from studies that emphasise the importance of ‘market devices’ (Muniesa et al., 2007) in the construction of markets. Market devices at fairs can take the form of catalogues, awards and prices amongst others, contributing to the valuation of objects (Karpik, 2010). The main argument lies in the enhancement of particular knowledge ecologies at fairs by market devices, which yields an abundance of knowledge regarding the valuation of something, thus making them unique markets.

We will concentrate on three Basel contemporary art fairs, namely Art Basel, LISTE and SCOPE, which all focus on international exhibitors. Art Basel is one of the top fairs (Thompson, 2011) whilst LISTE and SCOPE represent lower-tier fairs. Additionally, Art Basel and LISTE focus on global buyers whereas SCOPE tends to be local (i.e. from Switzerland or neighbouring countries). Contemporary art is particularly suited to such an analysis. Firstly, works of art are traded directly at the fair (Quemin, 2013). Secondly, the value of goods is vague and hard to codify in such a sector (Beckert and Rössel, 2013). Thus, market devices that define value and are the basis for price calculations are especially visible in this field (Karpik, 2010). Thirdly, the market is global considering the highest price segment of contemporary art. That is, works of art would attract the same price in different parts of the world (Renneboog and Spaenjers, 2015; Velthuis and Baia Curioni, 2015). We based our study on 49 interviews with artists, art critics, curators, gallery owners and fair organisers as well as fair-related documents.

The next section describes the knowledge perspective of the temporary cluster literature. Section ‘Knowledge in markets: The role of market devices’ discusses the knowledge perspective on markets and introduces the term ‘market devices’. Section ‘Market devices in temporary markets’ presents the particularity of market devices at trade fairs. Section ‘Art markets and the art fair’ describes the particularities of the art market and the art fair. Section ‘Research design’ provides the methods. Sections ‘Before the fairs: Selection procedures and calculations of exhibitors’, At the fairs: Sites of valuation’ and ‘After the fairs: Dissemination of prices’ illustrate market devices before, during and after the fair, respectively.

Trade fairs as temporary clusters

Trade fairs assemble sellers and buyers in a particular field ‘with the primary goal to showcase, promote, and/or market their products and services to buyers and other relevant target groups’ (Bathelt et al., 2014: 4). 1 Trade fairs have been demonstrated to reduce transaction costs for search processes and offer their participants dense information on various market elements, such as product differentiations and prices (Florio, 1994). Additionally, Rosson and Seringhaus (1995) already emphasised the role of interactions and interactive learning that take place at fairs.

Different types of fairs serve various purposes. Golfetto and Rinallo (2015) distinguished four types of trade fairs concerning the relationship between the location of exhibitors and visitors: local exchange trade shows, which are attended by exhibitors and visitors from the same country or region; export-oriented trade shows with local (i.e. regional or national) exhibitors and non-local visitors; import-oriented trade shows with mostly non-local exhibitors and local visitors; hub trade shows where most exhibitors and visitors originate from other countries.

A particular knowledge-based perspective on trade fairs is adopted by research on temporary clusters (Maskell et al., 2006), which investigates periodic gatherings of professionals for limited times in delimited spaces. In addition to trade fairs, these gatherings also include conferences, conventions or exhibitions. The main argument herein is that these gatherings, similar to permanent clusters, provide a knowledge ecology that is difficult to substitute by other forms of proximity and thus can be best described as ‘temporary clusters’ (e.g. Bathelt et al., 2014; Maskell et al., 2006).

Studies on temporary clusters elaborate on two particularities of trade fairs. Firstly, these fairs contribute to the formation of global relations (Li, 2014) which allow companies to form connections outside their regional locations and help to structure a global network (Yogev and Grund, 2012). Therefore, trade fairs ‘connect knowledge pools that are spatially, culturally and institutionally (more or less) distant from each other’ (Bathelt and Cohendet, 2014: 877). Trade fairs also connect different localised ‘epistemic communities’ that comprise interconnected experts in their field (Bathelt and Schuldt, 2010). Thus, trade fairs facilitate the formation of global epistemic communities that share a similar vocabulary and common understanding (e.g. Entwistle and Rocamora, 2006). The second particularity lies in the knowledge ecology of trade fairs. The physical co-presence of a multitude of agents from industry, technology or a value chain creates a particular buzz at trade fairs (Maskell et al., 2006). The term ‘buzz’ describes the manifold planned and unplanned interactions at fairs that serve to diffuse and evaluate information, whereas ‘global buzz’ refers to how these fairs connect agents from different parts of the world (Bathelt and Schuldt, 2010). Via global buzz at trade fairs, participants gain information on market developments, products, services, customers and competitors.

Studies on temporary clusters also investigated the role of buzz in market exchanges. Akerlof (1970) already described the importance of knowledge and information in market functions. He offered an example of ‘information asymmetry’ in the used car market, wherein a seller is privy to information regarding the quality of his car that the buyer lacks, leading to a market where good- and bad-quality used cars are both sold for the price of bad ones. A key point lies in the absence of a mechanism that can be used by an owner of a good car to demonstrate its value. Sellers of good-quality cars would not sell their items because they could only expect to obtain the price of a bad car. Consequently, ‘bad cars drive out the good’ (Akerlof, 1970: 490) and a market for good cars does not emerge. At trade fairs, exhibitors gain knowledge regarding the needs of global markets, consumer tastes, quality of goods and requirements of users, thus allowing them to adjust their competencies and products to address such needs (Bathelt et al., 2014, 2017). Buzz also includes learning other markets and facilitates the buying decision concerning a particular good (Bathelt and Schuldt, 2008).

Knowledge in markets: The role of market devices

Research on temporary clusters shows that the knowledge ecologies resulting from the simultaneous presence of a multitude of agents that allow learning processes considering markets. These knowledge ecologies facilitate trade and the respective coordination of agents. However, the temporary cluster perspective describes trade via social relations, whereas the market itself is taken for granted. Scholars, such as Çalışkan and Callon (2010) or Muniesa et al. (2007) suggested that the information upon which buyers and sellers make their calculations is not only embedded in social relations but also in the relations that objects have with other entities (Callon, 1998). Thus, the value calculation of a commodity occurs on its manifold connections, references and associations to standards (Boltanski and Thévenot, 2006), other agents (Aspers, 2009) or symbols (Reckwitz, 2018).

Market devices’ help provide structured calculations on value. Market devices are ‘material and discursive assemblages that intervene in the construction of markets’ (Muniesa et al., 2007: 2). Examples of market devices are pricing models (MacKenzie and Millo, 2003); price tags (Cochoy, 2007) or ranking lists (Karpik, 2010). Market devices are constructed on the basis of values of a particular field. Moreover, market devices contribute to the transformation of these values into a price by integrating them into a calculative space (Muniesa et al., 2007). Thus, market devices not only evaluate something but also define what is valuable to produce an economic value. Therefore, such devices are an example of a valuation process, that is, the process of giving worth to something (e.g. Kjellberg et al., 2013). Additionally, market devices enable a concordance of evaluation criteria between buyers and sellers and thus reduce uncertainty (Muniesa et al., 2007). This reduction in uncertainty is necessary for the emergence of a market (Beckert and Rössel, 2013).

The introduction of the Black–Scholes formula to calculate prices for stock options at the Chicago Board Options Exchange provides a respective example (MacKenzie and Millo, 2003). Before the formula, options trading was considered gambling and therefore forbidden. The Black–Scholes formula suggested a predictability of options prices. However, this formula predicted prices only after it was used by traders. Thus, the formula not only transferred information into the market (Akerlof, 1970) but also integrated knowledge in the market regarding its function.

Market devices take the form of ‘judgement devices’ for the evaluation of ‘singularities’ (Karpik, 2010), that is, unique and incommensurable goods that cannot be measured by standardised methods. Respective examples not only include works of art but also wine, music or films. Karpik (2010) argued that evaluations of singularities require judgement devices to provide assessments of goods and ‘offer buyers the knowledge that should enable them to make reasonable choices’ (Karpik, 2010: 44). Examples of judgement devices are networks that provide buyers with information, appellations, guides, critics, rankings (Karpik, 2010) or exemplary goods that facilitate the derivation of norms of quality (Dekker, 2016).

Calculations can differ between social agents despite having access to the same information. Markets provide an environment for negotiating contradictory valuations of goods, that is, what to include in a calculation and the calculation process (termed ‘framing’ by Callon, 1998). For example, Beunza and Stark (2012) described how derivatives traders check their pricing models against stock prices, which they use as estimates for the assessment of their competitors. If they find differences vis-a-vis their models, then reasons for such deviations are disputed. Negotiations are especially important for valuations involving different orders of worth (Boltanski and Thévenot, 2006). Aspers (2009) stated that such negotiations are also important in the absence of a scale or accepted standard to value a commodity and indicated that knowledge regarding the social status of those involved is required. Thus, negotiations generally occur when uncertainties regarding the value of something exist (Callon, 2016; Çalışkan and Callon, 2010).

Market devices in temporary markets

The construction of markets has particular geography. For example, Berndt and Böckler (2009) established a particular geographical perspective on markets by arguing that their ordering is done via bordering; that is, drawing geographical borders around what belongs to the market and what does not (see also Ouma et al., 2013). However, the reason why certain markets require a particular co-location between market agents is hardly ever investigated. This finding is surprising because many insights into the functioning of markets have been derived from case studies on localised markets. Garcia-Parpet (2007) described the intentional construction of a perfect neo-classical market at the Strawberry Auction in Fontaines-en-Sologne. Çalişkan (2007) described how market prices at the Izmir Mercantile Exchange resulted from different ‘prosthetic prices’, which are used by agents to make a calculation. However, these localised markets were used only to illustrate the social and technical construction of markets, not if and how co-location makes them special.

Investigations of trade fairs show that they are shaped by the density of different forms of market devices without explicitly referring to this concept (Bathelt et al., 2014; Rinallo and Golfetto, 2011). In many ways, these devices are either inherently part of the fair (e.g. via the organisation of the fair (Rinallo and Golfetto, 2011) or especially produced and organised (such as catalogues, flyers or public talks). In the following passage, we categorise market devices at a fair in three parts, which are distinguished via their valuation processes: (1) physical arrangement of things (where valuation is conducted upon the positioning of things), (2) judgement devices (which facilitate qualitative judgement) and (3) ‘prosthetic’ prices that allow a calculation based on other prices.

Cochoy (2007) described how the physical arrangement of supermarket aisles and the products within them guide the customer. Trade fairs show some similarities to supermarkets in that they are functional spaces. The physical arrangements of booths and objects within the booths indicate the value of things. These arrangements occur on different scales: fair organisers curate the fair space (Rinallo and Golfetto, 2011) and booths are small or large and placed in central or peripheral areas of the fair. The spatial structure serves to describe the position of the exhibitor in the global market. Furthermore, the booth is connected to its immediate physical environment (i.e. mostly the neighbouring booths), which also affects the standing of the exhibitor. Skov (2006: 764) described this relation between neighbouring booths. ‘Trade fairs,’ she said, ‘constitute a kind of ‘neutral ground’ onto which exhibitors inscribe their relative positions vis-a-vis other exhibitors’. Thus, fair organisers and exhibitors curate the space. The spatial arrangements create a ranking order amongst exhibitors and showcased objects. The second form takes the shape of judgement devices. Trade fairs include media coverage, workshops, talks, newspapers, catalogues and awards that introduce additional information (Entwistle and Rocamora, 2006). This form particularly accounts for flagship fairs (Bathelt and Schuldt, 2008). The third form of market device is ‘prosthetic prices’. Çalışkan and Callon (2010: 17) described the functioning of price as a market device as follows: ‘The price of any particular transaction […] is always calculated on the basis of other prices’. For example, during art fairs, prices of sold pieces of art are either announced publicly or visible via ‘sold’ stickers (Thompson, 2011). Thus, fairs provide an environment of prosthetic prices.

Additionally, the effect of market devices and the buzz at fairs mutually reinforce each other. For example, journalists gather information from the fair and contribute with their writings to the buzz at fairs (Entwistle and Rocamora, 2006). Thus, the knowledge ecology at fairs is not only produced via interactions but also via knowledge and information introduced through market devices.

In addition to their creation of market devices and the buzz to reinforce their effectiveness, fairs provide an environment for interactively negotiating value (i.e. what and how to include something in a calculation). The context for these negotiations as well as the resulting prices differs. Hutter and Stark (2015) argued that different situations result in varying calculations of the same object, which is similar to different assemblages of technologies, devices and people that lead to different types of valuations. In the Izmir Mercantile Exchange example of Çalişkan (2007), which is a commodity market for cotton, the exchange itself comprised different places where varying prices were produced. The prices had different meanings despite all referring to cotton. Thus, different fairs provide various endowments with market devices and different situations of valuation accordingly.

Overall, market devices are assumed to affect fairs as markets in the following three ways. Firstly, trade fairs are shaped by a proliferation of market devices due to their design and integration in the fair and the buzz. This proliferation also yields an abundance of knowledge regarding the evaluation of goods, thus producing unique fairs. Secondly, trade fairs can be distinguished by market devices and the quantity and quality of information they introduce into the fairs. Thirdly, these differences affect the negotiations regarding the valuation of a piece of art.

Art markets and the art fair

Works of art are singularities (Karpik, 2010) because their value cannot be evaluated on the basis of standards or scales (Aspers, 2009). Works of art receive their value from their relation to particular entities as well as practices that assign value to these relations (Velthuis, 2003). A further particularity of the art market lies in works of art that cannot be consumed and have a particular ‘social life’ (Appadurai, 1988) because they move from their places of production to galleries, collections or museums. These places give an indication of the work's value, which is especially observed for world-class museums, such as the Museum of Modern Art, New York (MOMA). Giuffre (1999) described this effect using the example of galleries with different reputations. She shows that ‘[g]alleries are considered prestigious when they show the work of prestigious artists and vice versa’ (Giuffre, 1999: 817). This condition also applies to art fairs. Exhibiting an artwork at a prestigious fair usually increases its price (Thompson, 2011).

The markets for artworks can be distinguished between primary and secondary markets. Primary markets are those where a piece of art is sold for the first time. Examples of primary markets are direct sales from the artist, galleries and at art fairs, wherein galleries exhibit works of the artists they represent (Velthuis, 2011). The primary market is shaped by uncertainty due to minimal consensus regarding the price, especially for ‘newcomer’ artists. Therefore, gallery owners set prices for pieces of art according to conventions and similarly price different works of art by the same artist but of varying quality (Velthuis, 2003).

Pieces of art are often sold several times; thus, secondary markets are of particular importance in the field of art. Prices from previous sales are strong indicators for future prices, especially because social norms prevent gallery owners or art dealers from decreasing the price for an artwork (Velthuis, 2003). Examples of secondary markets include auctions or art dealers. Trade fairs can be primary and secondary markets.

Sales in the art market usually transpire either via auction houses, galleries or via art dealers. Sales via auction houses comprised 47% of the market in 2015 (TEFAF, 2016). In the sector of contemporary art, auctions are dominated by Southeby's and Christie's, which have a share of 70% of all public auctions. TEFAF (2016) reported that sales via art dealers (which also comprise galleries) accounted for 53% of the global market. Art dealers performed 48% of their turnover at the gallery, 40% of turnover at trade fairs and the remaining turnover transpire via channels, such as auctions, online platforms or private sales.

The art market is currently growing with the number of trade fairs and their share in this market. Whilst the overall sales volume of artworks nearly doubled from $35.9 billion in 2005 to $63.8 billion in 2015 (TEFAF, 2016), the number of art fairs worldwide tripled in the same period from 68 to 220 (O’Mealley, 2015). Additionally, their share of the overall market increased from 15% to 20% between 2010 and 2015. 2 Furthermore, fairs became geographically diverse with the growth of the art market, with places such as Miami Beach, Hong Kong, Dubai and New Delhi becoming important locations for art fairs.

The categorisation of fairs by Golfetto and Rinallo (2015) only roughly fits to art fairs because most of these fairs are international at the level of the exhibitors. As part of a status market (Aspers, 2009), fairs are distinguished by their position in a hierarchy. This hierarchy is defined by the number of exhibitors and visitors and the capability of fairs to limit admission by strong selection procedures (Thompson, 2011). Thus, top fairs, such as Art Basel, Art Basel Miami, Frieze or Armory Show, have a large number of visitors and exhibitors and strong selection procedures. Fairs at the lower ranks of this hierarchy have a small number of visitors and exhibitors and a weak or absent selection procedure. Owing to these differences in selection mechanisms, art fairs are a prime example of what Berndt and Böckler (2009) call ‘ordering by bordering’ to construct differences between markets.

Important art fairs, such as Art Basel, can have nearly 100,000 visitors (Thompson, 2011); however, the number of buyers worldwide is limited. Approximately one-third of the demand comprises public institutions, corporations or other art dealers, whilst approximately two-thirds of the demand comes from private collectors (TEFAF, 2016). TEFAF (2016) provided some estimates regarding the numbers and buying powers of these collectors. Approximately ca. 120,000 individuals whose net personal wealth exceeds $50 million exist worldwide. Furthermore, the individuals of this group are expected to account for nearly 40% of spending in the art market; amongst these multimillionaires, only 2% can be counted as collectors, which reduces the number of this group that represents the major share of the market to 2000–3000 people. Therefore, Art News (www.artnews.com) lists 200 individuals as important collectors. These individuals are not selected solely by their wealth but by their reputation and perceived importance in the field of art (Braden, 2016). Thus, most buyers are individuals and the number of individuals that can buy art to a considerable extent and of high quality.

Research design

The analysis focuses on how to market devices distinguish and differentiate temporary localised markets. This intention requires a comparative case study approach, wherein the cases should differ in the dimension of interest (Eisenhardt, 1989; Yin, 2011) (i.e. in our case, market devices). We chose the following three contemporary art fairs that occur in Basel yearly in June: Art Basel, LISTE and SCOPE. The three events were chosen because they differ in their hierarchical position amongst art fairs, which is reflected by their various endowments with market devices.

Art Basel in Basel, which has approximately 300 galleries and 100,000 visitors, is regarded as a premier international art fair (Thompson, 2011). SCOPE is considered a low-tier fair and LISTE is located between Art Basel and SCOPE. Information regarding the importance and reputation of these art fairs was obtained through literature research (e.g. Thompson, 2011) and by short inquiries and conversations with experts of the global art market.

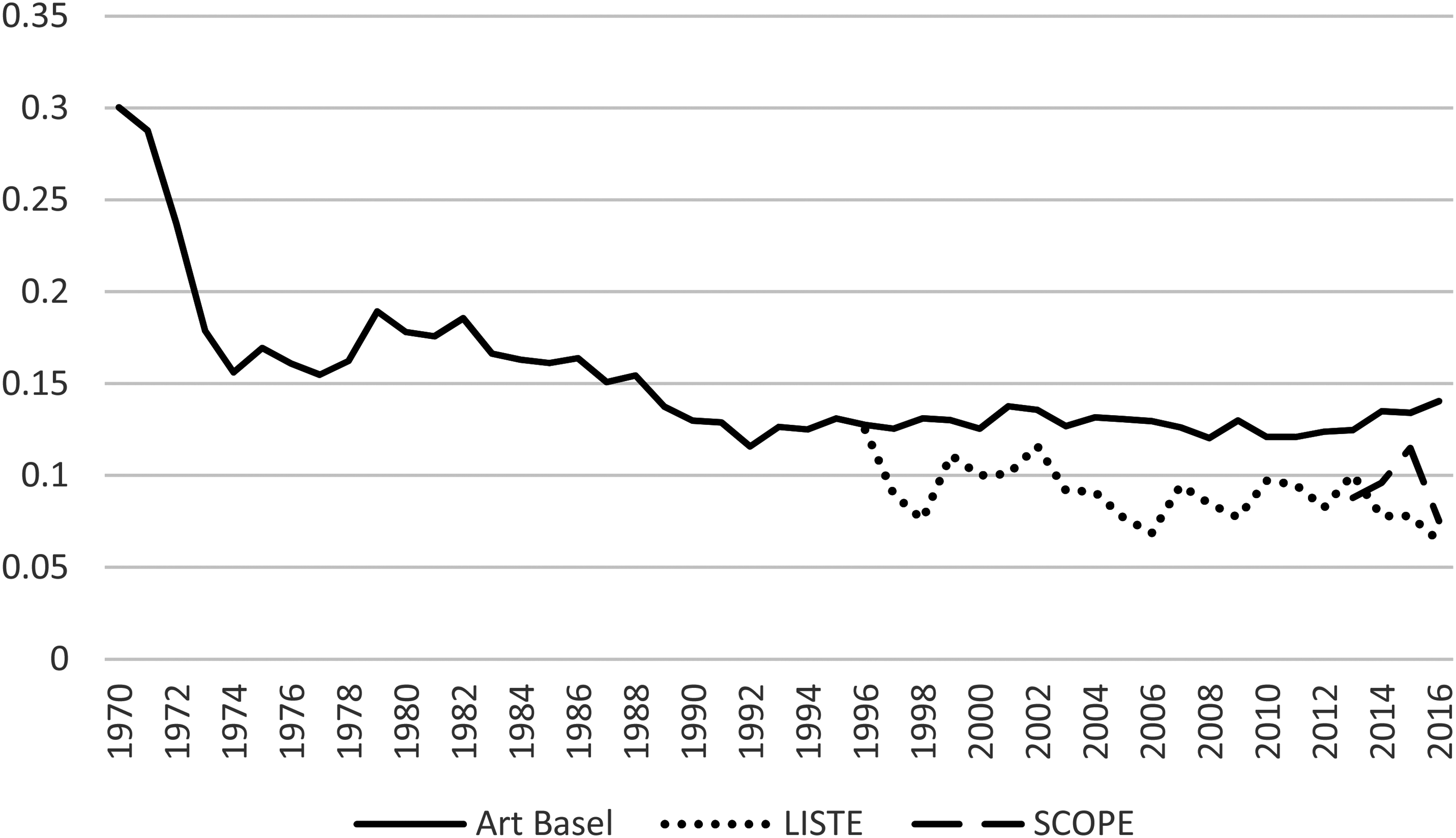

Taking the categorisation by Golfetto and Rinallo (2015), who distinguished trade fairs based on their degree of internationalisation, we firstly analysed the internationality of exhibitors on the three fairs. Figure 1 shows the Herfindahl index for the number of galleries per country. The Herfindahl index is the sum of the squared shares and is a standard indicator to measure the market concentration (Jacquemin and Berry, 1979). In our case, the index is one if all exhibitors come from one country. The index approaches zero with an increasing number of countries and an equal distribution of exhibitors per country. The figure shows that all fairs are highly internationalised, whereas LISTE and SCOPE are even more diverse in this respect than Art Basel as the top tier fair, which reflects a large number of American galleries at Art Basel. 3

Herfindahl-index for a number of galleries per country at Art Basel, LISTE and SCOPE (data for Art Basel from www.artfacts.net, data for LISTE and SCOPE from fair organizers).

We conducted 42 qualitative interviews with exhibitors, which took place in June 2014 and 2015: 13 at Art Basel, nine at LISTE and 20 at SCOPE. Some of the interviewees at Art Basel had previously exhibited at LISTE, which helped fill in the obtained information from LISTE. Opportunities for interviews were only brief and thus might occasionally have been interrupted by potential customers or colleagues. Interview partners were selected on the basis of their responses. Our experience reflected those of others who conducted research at trade fairs. Andreae et al. (2013: 197) described the experience as follows: For social scientists accustomed to deploying the usual repertoire of research methodologies, the trade show performance presents a fleeting target that does not always lend itself to lengthy interviews, focus groups or even detailed qualitative surveys. In consequence, normal research methodologies may not be practical, depending on the nature of the show itself.

The interviews were conducted by both study authors. Taking minutes during the interview was only possible in a few cases. In most cases, minutes were written directly after the interview. On average, the interviews lasted between 10 and 40 min, whereas 90% of the interviews lasted around 25 min; only one interview lasted longer than an hour.

Potential interviewees were generally quite open to talking to when the intention of the interview was revealed. However, the interviewees were reluctant to accept standard interview techniques (recording, note taking and completing a questionnaire); thus, the interviews usually took the form of discussions regarding works of art and the questions were embedded in these discussions. Nevertheless, the research context was clear for the interviewees. They regularly asked for the opinion of the interviewers or what others had said; in some instances, the interviewees approached the interviewers afterwards during taking minutes close to the booth to provide additional information.

The questions referred to the following topics: (1) selection processes (i.e. why the gallery selected this fair, why the gallery itself might be selected and why the gallery selected which artists to be presented at the fair); (2) valuing pieces of art (e.g. what determines the value of the exhibited pieces of art); (3) customers (e.g. origin, description of sales talks, numbers of sales); and (4) general remarks of being at the fair. We did not ask for specific market devices, thus allowing exhibitors to state what they perceive as important factors in the valuation process. However, particular questions regarding selection processes and valuation of art resulted in information regarding market devices. We categorised the market devices according to the logic with which something is valued: valuing by physical arrangements (e.g. positioning an object as an eye-catcher in the booth); valuing by prosthetic prices (e.g. reference to prices of past sales); and valuing by judgement devices (which could include referring to an award, a critic or a ranking). The numbers and categories of market devices mentioned allowing differentiation of valuation processes.

Many exhibitors not only sell but also buy pieces of art; thus, they could also offer the perspectives of buyers. This condition partly filled a blind spot in our analysis because accessing buyers, especially important collectors, is difficult.

The interviews were complemented by seven additional meetings with experts, such as fair organisers, critics and curators as well as representatives of auction houses. The interviews yielded detailed information regarding processes (e.g. how value is created in the art field, how fairs select galleries and the role of market devices). The setting outside the fair allowed a more structured procedure than inside. The 30-to-70-min interviews, followed by a semi-structured questionnaire, were recorded and transcribed.

In addition to interviews, we gathered information regarding market devices through observation or desk research. Consequently, we appended documents published by the fairs or related organisations to our observations. Additionally, we used information gathered during different discussion sessions and participated in informal talks during the fair and at evening events. Finally, the last version of the case study was discussed with several experts from the art market to ensure a high level of validity and reliability concerning the findings derived from the data analysis.

Market construction is a temporal process (MacKenzie and Millo, 2003). This temporality requires a process study approach that understands that the existence of something (e.g. markets) does not explain its evolution. Therefore, the temporal order of events is important to explain the evolving phenomena. Langley et al. (2013) suggested ‘temporal bracketing’ as analytical heuristics for qualitative process studies. Temporal brackets ‘are constructed as progressions of events and activities separated by identifiable discontinuities in the temporal flow’ (Langley et al., 2013: 7). This bracketing allows for the comparison of different temporal sequences that can be distinguished via their particular process dynamics. This distinction into different phases is also consistent with Rosson and Seringhaus (1995), who distinguished between processes taking place before, during and after the fair to analyse the behaviours of visitors and exhibitors. This separation was used in this study to distinguish processes of valuation and market construction. The first phase describes valuation processes before the actual fair by fair organisers (what galleries to select) and gallery owners (what pieces of art to exhibit and how to price them). The second phase describes the valuation processes at the fair itself. The third phase ‘After the Fair’ describes how valuation processes at the fair feed into other valuation processes. We used the concept of market devices to characterise and distinguish valuation processes amongst the three phases and the three art fairs.

Before the fairs: Selection procedures and calculations of exhibitors

We investigated three Basel art fairs: Art Basel, LISTE and SCOPE. Founded in 1970, Art Basel represents a primary and secondary market fair, exerting an increasingly restrictive selection process for galleries over the years. LISTE opened a parallel fair in 1996 to promote young galleries in response to the highly exclusive access to Art Basel. In contrast to Art Basel, LISTE is a purely primary market. However, LISTE has developed similarly tight restrictions over the years for its segment. Another contemporary art fair, SCOPE, was established in Basel in 2006. 4 SCOPE sister fairs were founded in New York in 2000 and later extended to Miami Beach and Basel. Compared with Art Basel and LISTE, the entry barriers of SCOPE are remarkably low. Galleries mainly present original artwork that has never been exhibited before. Thus, SCOPE also represents a primary and secondary market. This section describes the selection procedures of the three fairs as well as the artwork exhibited. Therefore, the processes that define the supply side of the market are also depicted.

Selection procedures at Basel Art fairs

For all fairs, galleries must submit a dossier containing their concept and philosophy and which artworks and artists they plan to exhibit. However, the selection procedures differ. At Art Basel, a selection committee comprising esteemed international gallery owners selects approximately 300 galleries for Art Basel from a pool of 1000 to 1500 applicants. Being selected as an exhibitor considerably increases the chance to be selected for the next year. Therefore, once chosen, galleries continually exhibit yearly and mostly retain their booths for decades. Consequently, approximately only 10–15 booth spaces are granted to new galleries each year.

At LISTE, a committee comprising art critics and museum curators selects approximately 80 galleries out of 350 applicants yearly, of which 18 are first timers. The selection process focuses on potential young galleries for Art Basel. One fair organiser described LISTE as a ‘spring-board for young galleries that want to be among the future top galleries of the world’. LISTE grants selected exhibitors a booth for at least 3 years to provide a sustainable recognition in the global art market. Thus, one of the main objectives of LISTE is to function as an incubator for young galleries and place them at Art Basel.

Accordingly, the boundaries between Art Basel and LISTE are permeable and organised. Forms of presentation, such as ‘Statement’ or ‘Feature’, occur at Art Basel but are decisively considered to be located between Art Basel and LISTE because they are the first steps into the former. Galleries can exhibit several artists in the ‘Feature’ section whilst the ‘Statement’ section is dedicated to only one. Access to ‘Statement’ or ‘Feature’ is granted for one year. The Art Basel committee chooses to present 18–20 galleries from around 400 applications, wherein two-thirds are LISTE alumni.

The selection committees are crucial to gaining access to Art Basel and LISTE. The modalities under which the selections occur often appear opaque to outsiders. However, these modalities are evident to insiders. As one member of the LISTE selection committee said, ‘it is pretty clear for us as art critics to distinguish what is of value and what is not’.

The selection process at SCOPE for the 80 booths is substantially less rigid. In contrast to Art Basel and LISTE, the selection mechanism mainly focuses not on the art but the price of the booth. Nonetheless, a selection committee at SCOPE comprises curators and programme managers. SCOPE receives 10%–20% more applications than its exhibit space. Exhibiting at SCOPE is considered important by its exhibitors. In the words of one gallery owner, ‘it is important to just be at a fair and in Basel’. The presence offers visibility of the gallery and the exhibited works and allows one to meet collectors who are not visiting SCOPE.

Overall, all three fairs define the borders of their market but their bordering varies. Especially at Art Basel, access is organised via different gateways, such as strong selection criteria and preferred access by previous LISTE exhibitors. By contrast, the borders at SCOPE are permeable.

Price calculations of exhibitors

Prices at the fairs have been decided beforehand. The ‘social life’, that is, previous exhibition at museums, collections or galleries, affected the calculated price of artworks at all investigated art fairs. However, works at Art Basel had often been exhibited at numerous venues, many of which are quite renowned. Artworks at LISTE had been exhibited in famous museums such as MOMA. The same finding did not hold true at SCOPE. The price calculations included an exhibition at SCOPE, LISTE or Art Basel. Additionally, pieces of art were more widely reviewed by media at Art Basel compared to SCOPE and LISTE; artworks at SCOPE received the least attention. Therefore, awards were important for price calculations at SCOPE.

Differences could also be observed regarding prices: prosthetic prices are an important indicator for calculating the price for a piece of art. Prices that were announced or achieved at previous fairs send a price signal to the next exhibition; prices tend to rise between fairs even if a piece of art is not sold. Prosthetic prices mainly exist for Art Basel, to a lesser extent for LISTE and almost never for SCOPE. Additionally, we found works of art whose prices differed considerably from the price in their home market at SCOPE. In one case, the price at the fair was higher than that in the home market due to a large spending capacity in Basel. In another case, the price was low because the home market was a hot spot for this art form. The latter case is an exception to the rule that prices are not lowered (Velthuis, 2003). The interviewee justified this exception to promote pieces of art in a new market, which increases reputation and prices in the long run. We did not find these adjustments of prices at LISTE and Art Basel.

Exhibitors calculated prices considering works by the same artist in all three fairs. However, missing previous sales, media coverage and places of previous exhibitions increased the importance of calculations based on the artwork and the artist as elements at LISTE and SCOPE. In these fairs, we found several examples where the price was set in accordance with the normative impetus described by Velthuis (2003) because gallery owners set the price to appreciate the value of the artist. Furthermore, weak embedding into market devices at SCOPE led to two particular reactions. Firstly, gallery owners consider the craftsmanship and materials of an artist when setting a price. This form of calculation was not found at the two other fairs. Secondly, art exhibited at SCOPE was often produced especially for this fair. Buyers were usually unfamiliar with the oeuvre of the artist and were therefore unable to estimate the price of a particular work. SCOPE gallery owners and artists consider the missing knowledge of potential buyers regarding pricing when they produce a piece of art for their fair.

At the fairs: Sites of valuation

Works of art are integrated into a new environment during fair exhibitions. This section describes the difference in market devices of the three fairs and the effects of such differences on calculations as well as the functioning of these markets.

Market devices at the fairs

We use market devices in the form of physical arrangements, judgement devices and prosthetic prices to describe different environments of the three fairs. Firstly, the physical arrangement of booths and artworks, that is, the position of the galleries within the fair, the size of the booths, their relation to the immediate environment and the arrangement of the artworks within the booths are all indicators of value. At Art Basel, the size and location of the booth express the status of the gallery considering its reputation and importance in the global art market. Accordingly, a change in the reputation of a gallery may entail its repositioning within the fair space. One gallery owner stated the following: At the beginning, we had a bigger booth. Now we got a smaller one. We would have liked to keep a bigger one but in order to preserve continuity we accepted the smaller booth in order to prevent being excluded completely next year.

Additionally, this gallery, which had been exhibited at Art Basel for decades, realised its decreasing importance when it was moved to a peripheral position at the fair.

In addition to the position, the immediate environment of the booth is also important. Interviewees mentioned that the quality of art presented in neighbouring booths influenced the ‘charisma’ of the art that they were presenting. They appreciated that neighbouring galleries exhibited art they liked and that matched their own. The following quote by a gallery owner is exemplary of this. It is important where you are located in the art fair. If your next-door gallery's art is of lower quality, it affects your own prestige and it also has an impact on prices.

At the booth, exhibitors intend to create an adequate environment for their art. The possibilities are limited by a modular exhibition space at Art Basel and SCOPE, wherein booths can differ in size but neither in height nor in colour. LISTE is located in an old and convoluted industrial building, which offers minimal freedom but provides additional possibilities for adapting the booth design to the building. Exhibitors at the three fairs also applied different strategies to present pieces of art. Exhibitors at SCOPE and LISTE indicated that they selected and arranged pieces of art in such a way that they created an ensemble. Exhibitors at SCOPE promoted only a few artists, occasionally only three or four and only one in one case. This limited selection allowed galleries to exhibit a large number of pictures from each artist, which highlighted the connections between the different works. We also found these forms at LISTE to a lesser extent. By contrast, galleries at Art Basel usually exhibited up to 10 artists and often showed only one or two pieces of them each.

Judgement devices comprise public talks, discussions, catalogues and fair-related publications. Art Basel provides a catalogue with an overview of participating galleries, which includes artists and pictures of all exhibited works. Additionally, the fair hosts a talk series where artists, curators, critics, collectors and art journalists offer insights into recent art issues and the market function. Furthermore, the Baloise Art Prize, one of the most highly remunerated art awards worldwide, is presented at Art Basel. In addition to these devices provided by the fair, Art Basel is covered by several blogs (e.g. Sotheby's, which offers a private blog for their customers) and newspapers dedicate special sections to the fair (e.g. http://www.nytimes.com/topic/subject/art-basel).

LISTE also provides an art catalogue; contrary to the Art Basel catalogues, this catalogue of LISTE focuses on the artists, their work and their past exhibitions. At LISTE, the Helvetica Art Prize is awarded to graduates of Swiss colleges of visual arts and media. Talks or panel discussions are also non-existent. However, some newspapers and art-related blogs and websites (e.g. http://blog.artbinder.com/orbit-liste-basel/) report on LISTE.

SCOPE neither has talks or panels nor even awards. The fair does not also publish a catalogue. However, SCOPE is mentioned in some blogs as well as reviewed in the Basler Zeitung, a regional newspaper with a national distribution. Therefore, the number and density of judgement devices are on a diminishing scale from Art Basel to LISTE to SCOPE.

Finally, fairs are marketplaces where supply meets demand. Interviewees emphasised that the size of the market created by the fairs enables galleries that represent slightly known artists to sell their art. The size of the market allows for variety. All fairs provide an environment where buyers can see and use prosthetic prices, but the three fairs differed in the visibility of their supply and demand. At Art Basel, exhibitors mentioned that they usually know their buyers because they send invitations and arrange meetings with their collectors and museum curators in advance. The reason for such an approach lies in the limited number of individuals who can invest considerable amounts of money in works of art. Collectors, art dealers and curators receive catalogues from several galleries, thereby gaining an overview of the artworks and their prices before the fair starts. A similar yet less comprehensive overview is available at LISTE. Buyers at SCOPE were most often people that do not regularly buy art whereas collectors were a minority, which made for volatile demand.

Overall, these judgement devices, physical arrangements and prosthetic prices were produced by and for the fair. These market devices were further condensed by the temporal and spatial limitations of the fair. Thus, we could observe a proliferation of market devices, particularly via media coverage. This proliferation was especially visible at Art Basel but only minimal at SCOPE, wherein exhibitors complimented a missing respective environment by using basic booth strategies (e.g. art arrangement).

Negotiations regarding value

Different endowments with market devices as well as various bordering processes resulted in different negotiations at the booths. On the seller side, selection procedures at Art Basel and LISTE limit the turnover of galleries. Especially at Art Basel, some galleries have participated for decades. Thus, Art Basel has a stable but limited number of approximately 300 sellers. These sellers meet an equally limited number of 200 collectors that can afford the art presented at these fairs. Interviewees mentioned an even lower number of around 150 collectors. Thus, this bordering at the Art Basel considerably limits the number of sellers and buyers.

The fluctuation of sellers is substantially high at SCOPE due to the slightly rigid selection procedure. Lower prices compared to the other fairs also made art affordable for the middle class. Only one interviewee mentioned that a piece of art was sold to a known collector. Thus, a large volatility is also observed on the buyer side. Therefore, the permeability of the market is substantially higher at SCOPE compared with Art Basel, whereas LISTE is again somewhere in between the two.

We also observed different buyer geographies. Especially at Art Basel, exhibitors mentioned that they sold pieces of art to collectors or museums worldwide. One example was a gallery exhibiting a Japanese artist, which sold most of its pieces to a Japanese collector. Interviewees at LISTE mentioned a comparable geographical reach. This phenomenon was different at SCOPE, wherein interviewees stated that the customer base is rather local (i.e. in Switzerland and neighbouring countries). One gallery complained that the visitors at SCOPE in Basel are less diverse and international compared with those in SCOPE Miami. Two further galleries mentioned that their art (street art) did not sell in Basel but only at other art fairs.

The different bordering and endowment with market devices influenced negotiations between sellers and buyers. We found two differences amongst the three fairs in this respect. The first pertains to time, that is, the duration of negotiations and the day when the galleries made most of their sales. Art was sold quickly at Art Basel. Interviewees told us during the fair that they either closed deals in the first two days of the fair or expected many fast sales when asked on the first day. Interviewees explained that buyers usually know in advance what they want to buy and use the time at the booth only to confirm their intentions. Only one gallery mentioned that it sold a piece of art to a collector they did not know and who bought it ‘at first sight’.

At LISTE and SCOPE, interactions between gallery owners and buyers were remarkably extensive and sales, especially at SCOPE, usually occurred towards the last days of the fair. Buyers visited galleries several times to discuss a piece of art, its background, the gallery, the artist and which collectors had already collected the artist. Exhibitors used these discussions to describe their art and its various connections to the large world of art. Fairs provide an environment that enables these lengthy forms of interactions, during which potential buyers receive information regarding the exhibited pieces.

Only SCOPE had three galleries where artists were present. When we talked to these artists regarding their intentions to be at the fair, they said they were interested in seeing the reactions of visitors to their art and talking with them about their work. The presence of artists at booths fits into the general picture in which galleries at SCOPE rely on the booth setting to communicate the value of a piece of art. LISTE is located between Art Basel and SCOPE considering the time and timing of sales.

A second difference amongst the fairs lies in the volatility of turnover. Galleries at Art Basel and LISTE sold or expected to sell most of their works. At Art Basel, a sold artwork was replaced by a new one from stock. Galleries exhibiting at SCOPE showed increased variety in sales. The sample showed that four were happy with their sales. One of them said that it replaced these from stock. Most of the interviewees, however, mentioned that they sold almost nothing. Nevertheless, these galleries participated in the fair for exposure and presence in Basel.

After the fairs: Dissemination of prices

After the fair, sales information was collected and published via platforms, such as www.artnet.com and www.artmarketmonitor.com. However, we found only sales made at Art Basel on these platforms. On a global level, fairs whose sales prices were collected and published include FIAC, The Armory Show, Art Basel Miami Beach or Frieze. Furthermore, art organisations, such as auction houses, collect sales and their prices for their statistics.

Interviewees stated that prices in one temporary market influence those at subsequent markets. These temporary markets comprise not only of fairs but also of public auctions whose prices are also published and collected on websites, such as www.artprice.com. For example, the large auctions that occur in New York influence prices at Art Basel one month later whilst these prices, in turn, affect auction prices in London 10 days later. Therefore, these temporary markets produce prosthetic prices that are used for price calculations in subsequent temporary markets.

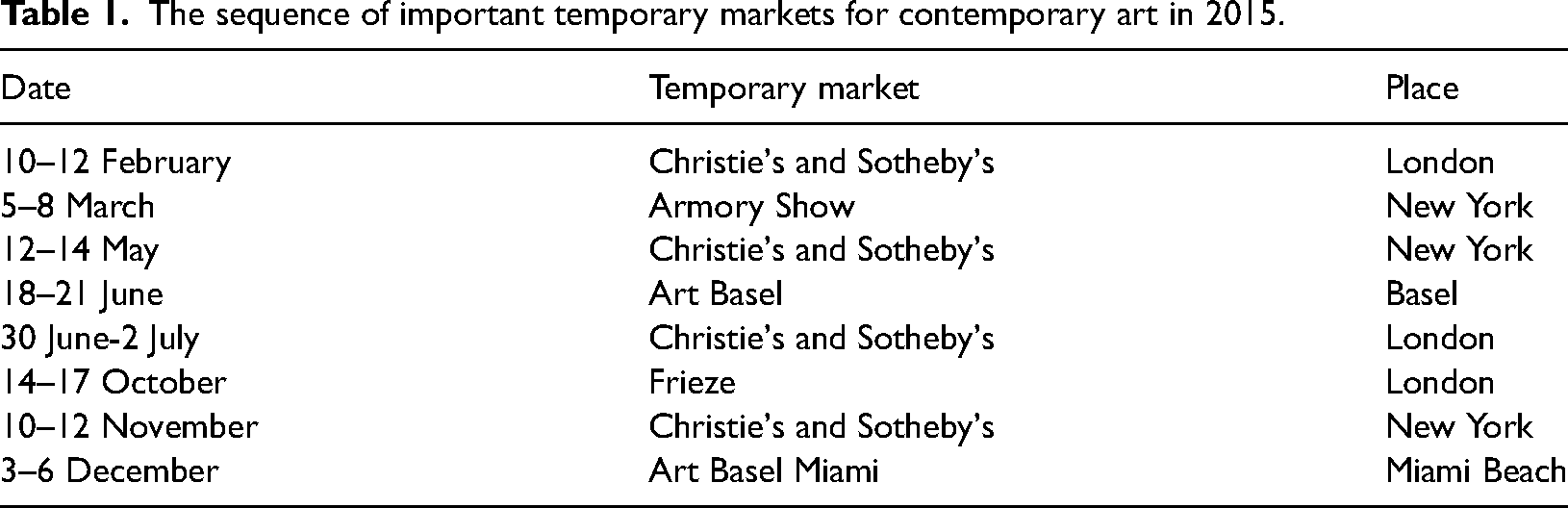

Table 1 describes this sequence of temporary markets that define prosthetic prices. We included Art Basel, Art Basel Miami Beach, Frieze and the Armory Show, which are suggested as amongst the most important in the art market. We also included auctions with the most sales of the two dominant auction houses, namely Sotheby's and Christie's. 5 Fairs with 21% of the market share and auctions with 47% of the market share cover the largest part of global sales in 2015 (TEFAF, 2016). Thus, the global art market is predicated upon these temporary markets.

The sequence of important temporary markets for contemporary art in 2015.

Table 1 shows two things. Firstly, the large auctions and fairs are alternately scheduled. Secondly, the locations also alternate, often between continents (except for The Armory Show and the May auctions, which both take place in New York). This sequence of temporary markets contributes to the construction of a single global market by alternating between temporary markets that relate to each other by including respective prosthetic prices in calculations. However, this single market might be refined to that segment of the most recognised and most expensive works of art (Renneboog and Spaenjers, 2015).

Conclusion

Markets require knowledge (Akerlof, 1970; Aspers, 2009). The current research focused on market devices (Çalışkan and Callon, 2010; Karpik, 2010; Muniesa et al., 2007) that integrate knowledge into fairs considering the valuation of pieces of art. This research contributes to the literature on temporary clusters by emphasising the role of market devices in enhancing knowledge ecologies at trade fairs. Additionally, market devices introduce another layer of distinction between fairs by creating a hierarchy between trade fairs (Golfetto and Rinallo, 2015). Particularly, flagship fairs, such as the Art Basel, not only served as a hub to facilitate connections on a global field but also generated market devices for other temporary markets. Therefore, this top-tier fair contributed to the development of a uniform global market. This global market is defined herein by artworks achieving the same prices on different temporary markets (Renneboog and Spaenjers, 2015).

Our research also contributes to a further understanding of the geography of markets. Our study emphasised the role of agglomeration effects for the construction of markets (i.e. self-reinforcing effects via certain densities in spatial proximity). Furthermore, this research demonstrated different geographical scales of market devices, whereas the geographical scale of market devices defined the geographical scale of the market (see also Berndt and Wirth, 2019).

This research also has limitations. We focused on different arrangements of market devices; thus, we did not provide the depths of other studies that investigated particular market devices (e.g. Cochoy, 2007). Furthermore, the field of art might be regarded as a special case (Aspers, 2009) because works of art are singularities (Karpik, 2010). However, trade fairs might generally be markets for singularities. What is often traded is not a homogeneous good but a batch of goods that is tailored for the specific needs of the customer (Andreae et al., 2013) and whose price cannot be estimated in accordance with standard measures (Aspers, 2009; Karpik, 2010).

We propose that further research that investigates the connection between temporary and global markets will be particularly beneficial. Studies have already investigated how connections between trade fairs contribute to forming global relations and communities (Power and Jansson, 2008). We suggest these connections, particularly those between the top levels of temporary markets, contribute to the creation of a global market. In analogy to global city research (Sassen, 2001), we assume that these temporary markets are more strongly connected to each other than to their environment (e.g. respective low-tier trade fairs). Such a perspective would further clarify the role of temporary markets in global integration (Li, 2014) as well as exclusion (Berndt and Wirth, 2019) of places.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.