Abstract

This paper presents an original follow the money methodology and argues for adopting the approach in geographical research. In 2011, Christophers made a compelling theoretical case for following money; however, it is empirically challenging, and his call remains unanswered. I propose an approach for following money in practice, using quantitative methods to do critical financial analysis to map and model flows of money. Drawing on the cases of vaccine bonds and rhino bonds, I illustrate this approach and make the case for this powerful methodology, outlining its contributions to advancing debates in geography. First, following money provides a robust and detailed empirical evidence base, offering a clear and precise understanding of a case study. Second, empirically, the methodology delivers a precise account of the material (re)distribution of resources, revealing who benefits or loses, by how much, and where. Theoretically, the methodology contributes to understanding the social and economic relations which support and are created by money's circulation. Fourth, following money reveals the mechanisms and consequences of financialisation. Finally, the approach contributes to understanding risk in society by uncovering financial risks, who faces them, and their significance. I also present some notes of caution on the limitations of the approach.

Introduction

Follow the money, a catchphrase from the 1976 film ‘All the President's Men’ about the Watergate scandal, is normally associated with crime and investigative journalism. It might conjure images of fighting tax avoidance and tax evasion (see the Tax Justice Network's work), or political corruption, for example, in 2016 when Trump used the phrase to attack Clinton and then, a few years later, the approach was used to uncover the Trump Foundation's financial crimes. In other areas, the concept is used for promoting transparency and accountability, for example, tracking aid spending (see the UK's Development Tracker 1 ). In academia, however, the approach is comparatively under-developed (with a notable exception in Christophers, 2011).

In geography, follow the thing has been used successfully to follow a range of things, from papayas (Cook, 2004) to data (Akbari, 2020), via firms (Brill and Özogul, 2021) and policies (Peck and Theodore, 2012; Wood, 2014). The methodology has its origins in the work of Harvey (1990), who argues we have to get behind the veil of the market, memorably giving the example of how ‘grapes that sit upon the supermarket shelves are mute; we cannot see the fingerprints of exploitation upon them or tell immediately what part of the world they are from’ (1990: 423), and Appadurai (1986), who argues commodities have social and political lives. In this context, methodologically, there is a compelling case to follow the money. In a persuasive provocation, Christophers (2011) presents a theoretical discussion of follow the money. However, it is empirically challenging, and I could not find a paper in geography (or a similar discipline) adopting a follow the money methodology to actually follow money. In academia more widely, a small number of studies draw on follow the money to differing extents, ranging from simply using the expression as a title to engaging with ‘following’ as a methodology. Often these examine spending in medicine, but there are also a few examples in the social sciences in global health (Erikson, 2015), education (Reckhow, 2013), international relations (Graham, 2017) and economics (Coon and Neumann, 2018).

In this paper, I present a follow the money methodology, an original development of follow the thing, drawing on my research in which I have followed the circulation and distribution of money using quantitative methods to do critical financial analysis across multiple case studies (for example Hughes-McLure and Mawdsley, 2022). I argue that follow the money is an informative methodology, making the case for adopting the approach through five themes. First, following money provides a robust and detailed empirical evidence base, offering a clear and thorough understanding of precisely what's going on in a case study. Second, empirically, the methodology delivers a precise account of the material (re)distribution of resources, revealing who benefits or loses, by how much, and where. Third, theoretically, the methodology contributes to understanding social and economic relations which support and are created by money's circulation. Fourth, following money contributes to analysing financialisation, specifically its mechanisms and consequences. Finally, the approach contributes to research on financial risk.

The paper begins with an introduction to follow the thing and a discussion unpacking what money is as the ‘thing’ to be followed. I then introduce two case studies which I use in the subsequent sections to illustrate both the approach and the contributions the approach can make to geography and related disciplines. In the fourth section, on how to follow money, I address some special considerations for following money and present my step-by-step approach. The fifth section makes the case for adopting a follow the money approach through five themes, illustrated through the case studies in the sixth and seventh sections. The penultimate section offers some notes of caution reflecting on what can't be achieved by following money, and the final section concludes the paper.

Follow the thing and money

Building on Marx's concept of commodity fetishism, which captures how markets hide social information and relations, Harvey argues we have to ‘get behind the veil, the fetishism of the market and the commodity, in order to tell the full story of social reproduction’ (1990: 423). To examine social and economic relations, we must go further than the information the market reveals itself (Harvey, 1990). Relatedly, Appadurai (1986) argues commodities, like people, have social lives, and calls attention to the politics in the social life of commodities. To reveal the social context of things, from a methodological perspective, ‘we have to follow the things themselves’ (Appadurai, 1986: 5), in particular their trajectories.

In Harvey’s (1990) compelling case to follow the thing, he argues commodity fetishism conceals the material conditions of the commodity's origination and circulation. This veiling of a commodity's social and spatial background is enabled by money, because it allows the separation of purchases and sales in space and time or, in other words, for commodities’ trajectories to expand across space and time (Harvey, 2018 [1982]). Therefore, for the case of money, tracing its lifecourse reveals and allows analysis of the social and economic relations supporting and created by money's origination and circulation (Harvey, 1990). Following money as the ‘thing’ is particularly important for several reasons (see Christophers, 2011). First, from a Marxist perspective, money is the ‘god of commodities’ and the climax of fetishism (Christophers, 2011). Second, money's creation and circulation are embedded in social and economic relations; third, wealth redistribution is inevitably bound up with money's circulation; and finally, in light of financialisation, money's role is becoming more important (Christophers, 2011).

To follow money as the ‘thing’, we first have to explore what it is, taking heed of Schumpeter's observation that ‘views on money are as difficult to describe as are shifting clouds’ (in Gilbert, 2005: 358). The aim of this paper is not to resolve the debates about money, instead I present a short discussion of what money is for the purposes of following, touching on classical functions theory, Marx's concept of money as capital, the social relations of money, geography and sociology, and network theories of money. For further discussion of the ontology and meaning of money, beyond the scope of this paper, see Gilbert’s (2005) helpful paper (or see also Fine and Lapavitsas, 2000; Ingham, 1996, 2001; Lapavitsas, 2003; Leyshon and Thrift, 1997; Zelizer, 1989, 2000).

Unlike a papaya, ‘money’ can be many objects, ranging from shells to data to gold coins. However, it is not money's materiality which is its defining characteristic, but its economic and social role. A classical functions theory of money argues money is something which functions as a: unit of account; medium of exchange; means of payment; store of value; and world money (medium for settlement across countries) (for variations see Fine and Saad-Filho, 2010; Gilbert, 2005; Lapavitsas, 2003; Leyshon and Thrift, 1997). Beyond these economic functions, money also performs broader social functions, for example, social and political power (Lapavitsas, 2003). In practice, to perform these economic and social functions, money takes a seemingly endless variety of forms such as gold, metallic coins, banknotes, bank deposits, bank and other accounts and credit instruments – this last form represents the majority of modern capitalist money (Lapavitsas, 2003), and holds a high potential for following.

Conceptually, Marx makes a distinction between money as money and money as capital (Fine and Saad-Filho, 2010). Money as money summarises market transactions or simple exchange and leads to the redistribution of monetary wealth. In contrast, money acts as capital when it is employed in the production of surplus value, in other words in the circuit of capital (Fine and Saad-Filho, 2010), which requires the expansion of wealth. Whilst the analytical distinction is clear, in practice it is complex. Money markets are indifferent to the sources and purposes of money as long as borrowers pay interest and return the capital (Fine, 2013). In other words, money markets hide the distinction between money as money and money as capital, so both appear to be capital that gives a rate of return as interest. The concept of loanable money capital therefore captures money markets as a whole, where money as money and money as capital come together.

This money as capital approach provides an understanding of the social relations of money. More specifically, money's social and cultural embeddedness, and a critique of money's homogenising tendencies and centrality in capitalist society (Gilbert, 2005). Going further, Ingham (1996) argues money is a social relation itself. In that sense, money can be conceptualised as a structure of social relations, not just as being socially produced (Ingham, 1996). It is money's social relations, its embeddedness and central role in society, that make it so interesting to follow and so theoretically informative in the light of Harvey’s (1990) call to see behind the veil of the market.

Money is not just an economy but also a geography, sociology and anthropology (Leyshon and Thrift, 1997). Zelizer (1988, 1989, 1994) argues more attention is needed to social relations and social values in all areas of economic life. Modern money is complex and heterogenous – there is not ‘one money’ (Zelizer, 2000), and non-economic spheres are influential – money is not limited to the market economy, and social structures limit money's power (Zelizer in Leyshon, 1997). This sociological theory has been criticised for being too specific and not proposing a general theory of money (Fine and Lapavitsas, 2000; Ingham, 2001). Social network theories of money demonstrate money's embeddedness in the social, the role of individuals and institutions, the necessity of information and trust, and recognise context dependency (Gilbert, 2005; see also Dodd, 1994; Leyshon, 1997). Leyshon and Thrift (1997) draw on actor-network theory (see Callon, 1991; Latour, 1991; Law, 1994) to argue monetary networks are better seen as actor-networks, drawing attention to the existence of many actor-networks, their contingent and unstable nature, performativity, and the work required (Leyshon, 1997; Leyshon and Thrift, 1997; Thrift, 1994). Network theories provide a useful account of money in terms of social relations of credit, debt and trust, and explicitly give a role to space. Many have made the case for a geography of money, highlighting the critical role of space (Corbridge et al., 1994; Harvey, 2018 [1982]; Leyshon and Thrift, 1997; Martin and Pollard, 2017). Money is neither place-based nor place-less but both together (Harvey, 1989). Geography is constitutive of money and credit in terms of its forms, practices, and institutions which are contingent in space and time, and money allows social relations to extend across space and time (Leyshon and Thrift, 1997).

So, what is money? Money is something which, through many forms, functions as a unit of account, medium of exchange, means of payment, store of value, and world money, and can take on a broader phenomenon as money as capital, but it is not confined to the economic sphere. Money is embedded in social relations, grounded in material practices, and situated in time and space. In this paper, money is understood as a material practice and a social relation. This is in line with Gilbert's call to pay attention to ‘money's “indeterminacy”, with its multiple functions and roles, with its paradoxical universality and particularity, with its global reach and its local effects’ (2005: 361).

Having grappled conceptually with the question of what money as the thing to be followed is, the paper now turns to the challenging and unanswered question of how to follow the money. In his theoretical discussion, Christophers (2011) argues follow the thing methodology can be applied to money like other non-monetary commodities, although, as Gilbert (2011) notes, he provides little detail on how to do this following. Christophers (2011) suggests following credit as a potential solution to three unique challenges he identifies for following money: scope, distinguishability and the temporal dimensions of credit money (I address these in more detail in the fourth section). In a response on following credit, Gilbert (2011) problematises the commodity model of money, arguing money is more than a commodity and highlighting the importance of alternative theories of money which foreground money as a social relation. According to Gilbert (2011), the three challenges Christophers (2011) identifies are some of the very aspects of money which make it different from a commodity. Furthermore, Gilbert (2011) suggests credit is more traceable because it may not be money, raising the possibility that a follow the money approach may only work for quasi-money (e.g. credit) or commodified money (e.g. credit securities).

The Christophers–Gilbert debate highlights how puzzling defining money is, and the implications that has for following it. Like Christophers (2011) and Gilbert (2011) the aim of this paper is not to solve the ongoing discussions in the study of money (see the extensive debate in Economy and Society: Bryan and Rafferty, 2007; Dodd, 2005; Fine and Lapavitsas, 2000; Gilbert, 2005; Ingham, 2001, 2006; Lapavitsas, 2005; Zelizer, 2000, 2005). Rather, the aspiration is to move forward follow the money as a methodology by making a proposal for an approach inspired by Christophers (2011) but that takes seriously Gilbert’s (2011) contention that money is more than a commodity, without foreclosing other approaches.

Given the debates, it is worth explicitly clarifying what flows of money the approach presented in this paper proposes to follow. Bonds feature in the two case studies introduced in the next section, however, they do not fulfil the criteria outlined above for money. Consequently, they are variously considered not to be money, to be quasi-money, or credit money (a particular form of money), although they are often generally understood as money, in the spirit of Bryan and Rafferty’s (2007: 140) ‘duck’ theory of money ‘i.e. if it waddles like money and quacks like money, then it must be money’ (for more discussion, see Bryan and Rafferty, 2007; Gilbert, 2005, 2011; Ingham, 2002; Lapavitsas, 2003). The issue does not need to be fully resolved here for our purposes, regardless of which camp one subscribes to on bonds. The proposed approach is not to follow the bond itself, but rather the payments of money which arise in connection to it. The ‘thing’ that is followed is the flows of money connected to the bond notes. Specifically, for a typical bond, the main flows of money to be followed would be the transfer of bond issue proceeds, the payment of interest, and the repayment of the principal at redemption. These are transactions of money. Analogously, there are many other credit or financial instruments which do not meet the criteria of being money (in Gilbert's argument, quasi-money or commodified money), but which would be interesting case studies 2 , where the approach can be adopted to follow the (related flows of actual) money. I argue that the paper's approach addresses a methodological challenge of how to follow money, being attentive to an understanding of money as at once a material practice and a social relation. However, it does not mean the approach escapes the possibility that it remains limited to the study of particular forms of money (a point I return to in the penultimate section).

Case study introductions

In the next sections of the paper, I present my approach to following money, and make the case for adopting the methodology by outlining what can be learnt or achieved by following money. In those sections, it is helpful to illustrate certain points with examples so, first, I briefly introduce the two case studies I will draw on. The first is the International Finance Facility for Immunisation (IFFIm) (for a more detailed analysis of this case see Hughes-McLure and Mawdsley, 2022) and the second is the Rhino Impact Investment project. Both case studies are leading examples of ‘innovative’ financing models in their respective areas, IFFIm in the development and global health arena, and rhino bonds in the world of conservation and the environment. Both also speak to the narratives of ‘leveraging’ private finance across social and green finance (see Cohen and Rosenman, 2020). IFFIm is situated in the context of a ‘beyond aid’ development landscape where the role of aid is reduced compared to other contributions to development finance (Janus et al., 2015), and, in particular, private finance is playing an increasing role (Blowfield and Dolan, 2014; Mawdsley, 2015). Furthermore, attention has been called to the financialisation of development (see for example Brooks, 2016; Carroll and Jarvis, 2014; Erikson, 2019; Mawdsley, 2018; Soederberg, 2013). Similarly, the rhino bonds project sits in the wider conservation context of the financialisation of nature (see for example Ouma et al., 2018; Sullivan, 2013) and rise of neoliberal conservation models (see for example Buscher et al., 2012; Dempsey and Suarez, 2016; Fletcher, 2012).

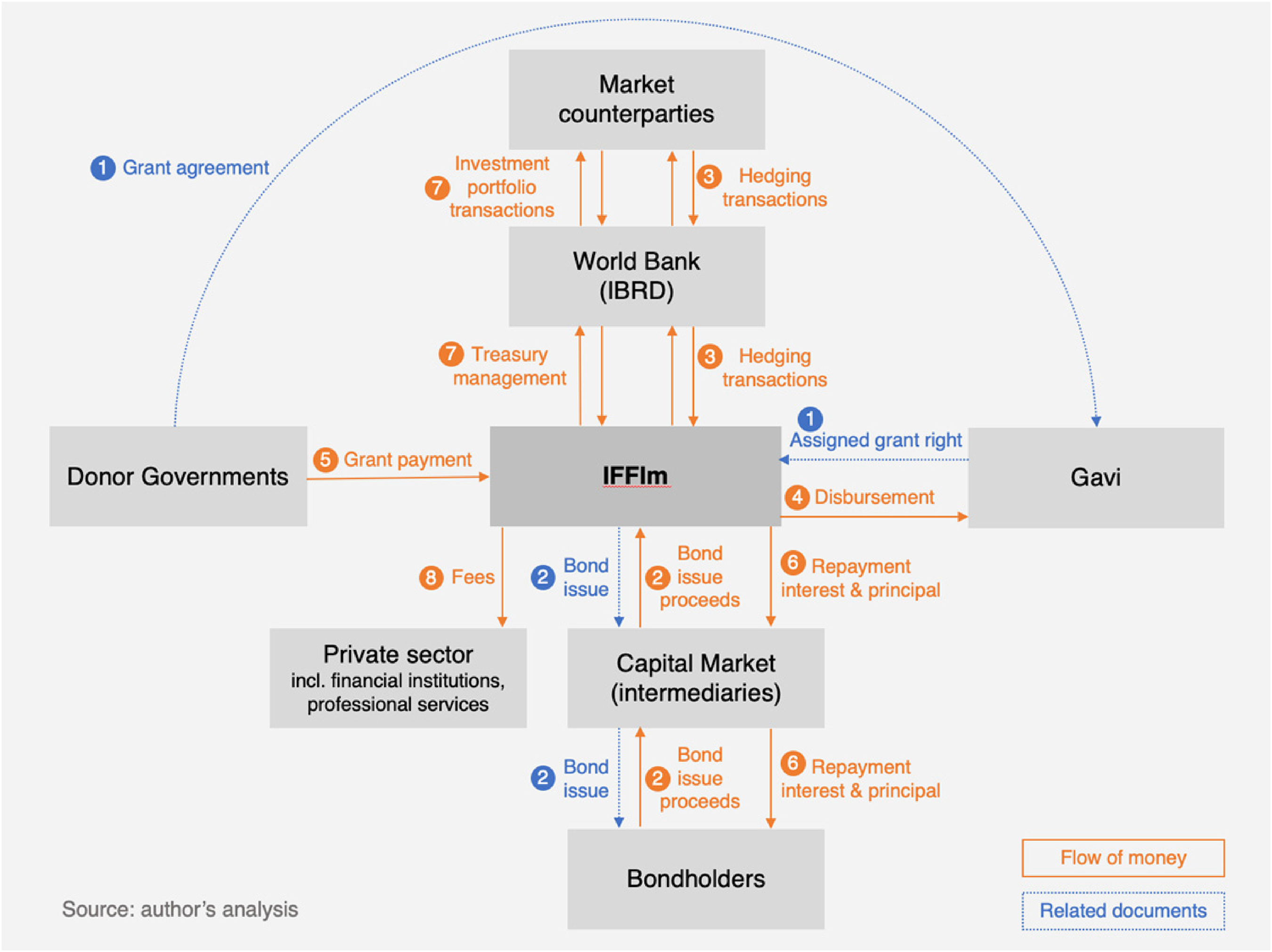

The International Finance Facility for Immunisation issues vaccine bonds to ‘frontload’ aid funding for Gavi, the Vaccine Alliance (referred to hereafter as Gavi). Gavi uses this funding for its immunisation and health system strengthening programmes. IFFIm plays a significant role in financing health globally. Since its launch in 2006, it has secured $7.6 billion in commitments from ten donor governments (the United Kingdom and France are the largest contributors) and disbursed $2.9 billion to Gavi up to 2020. More broadly, IFFIm has played a leading role in developing social bonds and has been praised as a success story, earning recognition from the UN, World Bank, G8, OECD, and Financial Times among others. IFFIm's financing model is to issue vaccine bonds in capital markets backed by long-term legally binding donor government pledges. The capital raised through bonds from investors is used to finance Gavi programmes. Income from donor government grants (or proceeds from new bond issuances) is later used to pay the vaccine bonds’ interest and principal. Figure 1 shows more detail on IFFIm's financing model. Proponents of IFFIm argue the benefits of IFFIm's model are front-loading to make funds available to Gavi earlier, low funding costs and its ability to leverage private sector funds for development.

IFFIm – flow of money (simplified).

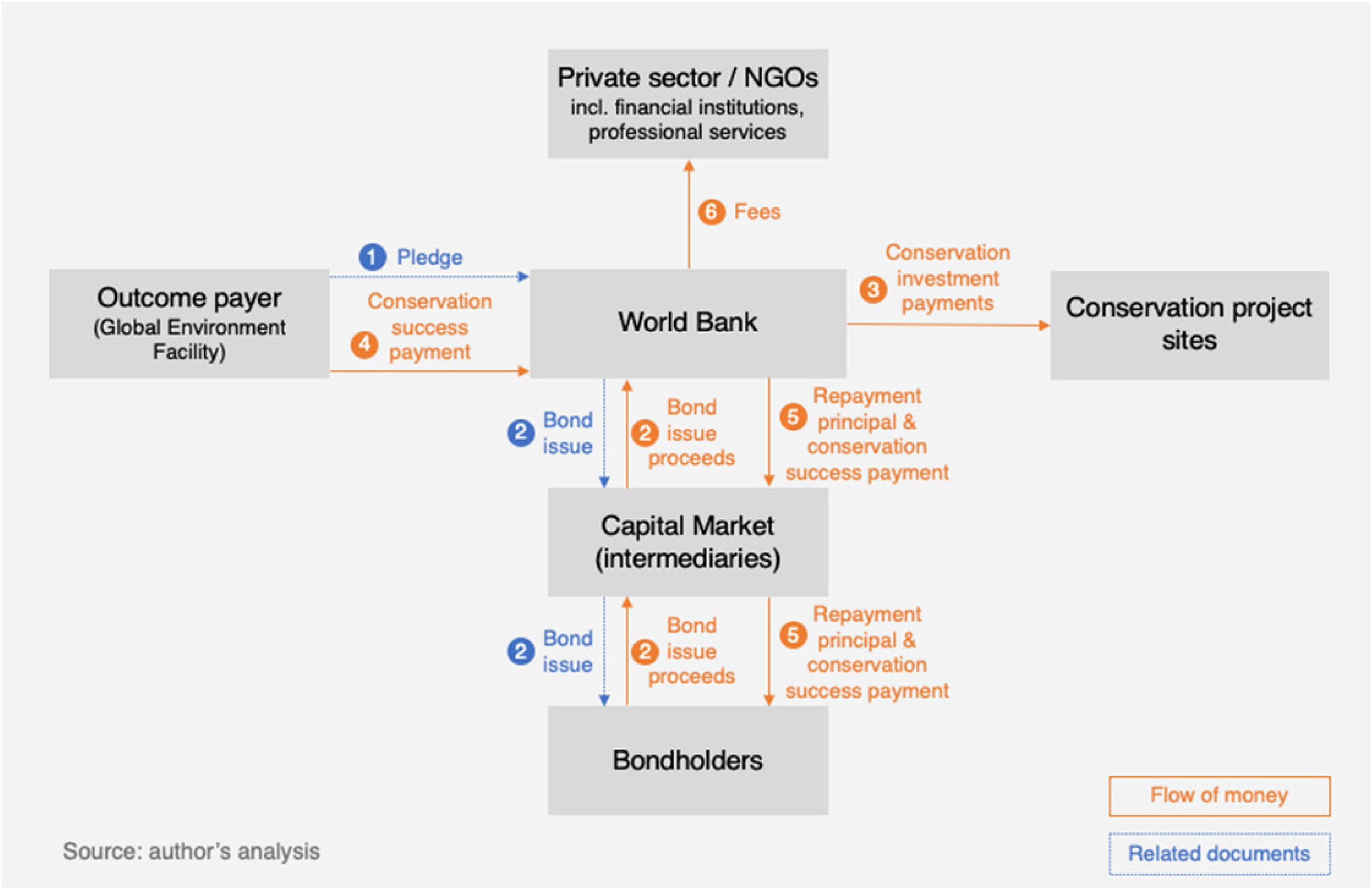

The Rhino Impact Investment project is a conservation initiative which aims to increase black rhinoceros populations globally by raising funds through rhino bonds. The project, which started in 2016, is the world's first pay-for-results financial instrument for species conservation. The pilot phase was implemented and funded by UNDP, the Global Environment Facility, UK aid, United for Wildlife, and the Zoological Society of London. The Rhino Impact Investment project's financing model is an outcomes-based financing mechanism, where the rhino bond links financial return for investors to conservation outcomes, in this case black rhino population. First, targets are set for black rhino population growth at project sites. The model is then to issue rhino bonds to investors backed by pledges from outcome payers (traditional conservation funders). The capital raised through bonds from investors is (in part) used to finance conservation work at project sites. After five years, the rhino population is evaluated against the growth targets and this determines the financial return on the bonds. Outcome payers then make a payment to investors based on the conservation outcome. The first rhino bond, called the Wildlife Conservation Bond, was issued in March 2022 and is linked to two protected areas in South Africa. The five-year $150 million rhino bond is structured such that around $10 million in conservation interventions are funded instead of coupon payments, and the return on the bond – the Conservation Success Payment – is tied to black rhino population growth (note: the bond principal is not linked to rhino populations). The first rhino bond was issued by the World Bank, with the performance-based element paid through a grant from the Global Environment Facility. See Figure 2 for more detail on the rhino bonds model. More broadly, beyond supporting a species’ recovery, the rhino bonds project is about changing the conservation funding model in the context of constrained fundraising by raising capital from new sources and shifting funding to focus on outcomes. Black rhinos are the initial focus, but the outcomes-based financing mechanism is scalable to other species and sites.

Rhino bonds – flow of money (simplified).

How to follow the money

My approach to following the money uses quantitative methods to do critical financial analysis, following Kass (2020) in arguing ‘financial information can provide powerful empirics that can expose inequity, be used to probe institutional norms and priorities, and provide insight into processes of neoliberalization and financialization’ (112). Financial data is the ‘field site’ through which the (re)distribution of rewards and risks, and the economic and social relations of the case study are explored. Paralleling Kass (2020), who blends critical geography theory with public finance tools, I adopt a critical approach drawing on private finance techniques. Necessarily, this approach requires the knowledge and skills to understand and analyse financial statements, commercial models and other financial data 3 . In this section, I first discuss special considerations for following money as the thing, before outlining the step-by-step approach I developed to follow the money.

To begin, I draw on some of the many interesting empirical studies of follow the thing to address more precisely what I propose to follow. In following papayas (Cook, 2004) or hot pepper sauce (Cook and Harrison, 2007), the authors draw on interviews with actors who are representatives of a step in the commodity chain to build a picture of the whole chain. Other examples, such as bananas (Raynolds, 2003) or data (Akbari, 2020), adopt desk-based research methods to present a detailed overview of the commodity chain. Others, for example, end-of-life ships being made into furniture (Gregson et al., 2010) or flip-flops (Knowles, 2014), use mixed methods relying on desk-based research for an overview of some parts of the chain and interviews for others. Although these papers use a range of data collection methods, they have in common the approach of tracing a generic commodity chain, in the sense of a generic object (i.e. the banana trade) rather than following a specific individual object (i.e. a particular banana's journey). To follow the money, this translates into building a picture of all the money flows in the chosen case study, not following the journey of an individual dollar.

As noted above, Christophers (2011) identifies three unique challenges which need to be addressed for following money. Firstly, scope: where and when to start and end the following. Secondly, distinguishability: how and whether money can be tracked. Finally, the temporal dimensions of credit money, or the issue of money flowing backwards and forwards in time. I argue following money in a particular form in a case study, rather than its more general form, presents solutions to these challenges. This approach is analogous to Cook (2004) following papayas, not the more general category of fruit or food. In my research for example, the IFFIm case involved following money in the form of development finance through a development project. For a particular case of money, a meaningful temporal frame can be found. In the case of development finance, for example, its creation as the giving of aid by a government can represent the start, rather than the origination of a more general money form at a central bank. Similarly, end points can be identified as, for example, the repayment of debt or final consumption (e.g. purchasing a vaccine), limiting the potential for perpetual circulation of money more generally. The challenge of distinguishability can also be overcome. Drawing on empirical examples, I propose to build a picture of all the flows of money for a particular case study, not following a specific dollar through bank accounts – Cook (2004) does not follow a single papaya, even though it might be possible by looking at its colouring, bruises or weight, instead a picture is built of a more general papaya food chain from one of many farms in Jamaica to a consumer in a UK supermarket (which may be unconnected to that particular farm). Finally, in a development project with credit money, it is possible to follow money flowing backwards and forwards in time once that debt is repaid. In the event that it is not repaid within the timeframe of study, a reasonable flow of money can be estimated based on the credit's provisions for the time that has not yet elapsed.

In the next part, I outline the specific step-by-step approach I adopted to actually follow the money and, as part of that, I address data collection and data analysis methods. I hope the three steps will provide a guide of how to approach following the money empirically in a reasonably broad set of cases. However, it is worth noting at this stage, that these exact steps may need some adjustment to the particulars of the case study or sector, and there will be alternative approaches and methods which could be adopted to successfully follow the money.

The first step to follow the money is mapping the network of flows of money and actors. Identifying the actors and the money flows which connect them is, in a sense, what allows the following or quantifying of those flows of money at a later stage. Each actor can also be connected to space. Figure 1 and Figure 2 show examples of maps of the flow of money for the IFFIm and rhino bonds cases, respectively. This sort of mapping, or something similar, has been done by others, drawing on a range of methods (see for example maps in Rosenman, 2019, of a social impact investment project in affordable housing; Weber, 2010, of tax increment financing notes, a financial instrument; or Johnson, 2014, of a typical catastrophe bond issuance). Given the goal of following money, I propose careful documentary analysis to source the information to create the map of the flows of money which constitute the case study of interest. This means first identifying the various actors involved. Second, drawing out the financial connections between them. Third, identifying the precise financial instruments which form those connections and, fourth, the specific flows of money involved for those instruments. For example, there might be a single flow of money between two actors for a simple fee payment (see number 8 in Figure 1). Alternatively, there may be several flows of money for a more complex financial instrument, such as a bond, which involves the transfer of bond issue proceeds, interest payments, and the repayment of the principal (see numbers 2 and 6 in Figure 1). The specific documentary sources will vary significantly depending on the case; however, some starting points might be project websites, brochures, investor presentations, prospectuses, or other project documentation, and press releases and other media coverage. Later, based on the detailed financial information collected and analysed in steps two and three, the map can be refined in an iterative process to reach the final picture of flows and actors.

The mapping process is key not only to create clarity to identify the money to follow, but also to determine the scope of the study. It defines a starting point for following money. For example, for IFFIm, the point where the development finance money originates: when donor governments make a binding promise of future money in the form of a grant agreement. Similarly, it defines a conceptual end point. For example, when Gavi receives IFFIm's disbursement. From an IFFIm development finance perspective, the money is then spent by Gavi on vaccines, health infrastructure, wages or other goods and services. In the rhino bonds case, the conceptual starting point for conservation finance money is the outcome payer making a pledge, and conceptually ends with expenses at project sites on rangers or infrastructure such as fences or water pipelines. It is worth noting that the scope of the study could vary depending on the conceptual framing of the research. In addition to clarity and scope, the map itself is revealing, pointing to the complexity (or not) of the network, the range of actors involved, the types of financial instruments connecting different actors, and the financial mechanisms which constitute the case study.

The second step is collecting and compiling financial data on these flows of money, in as much detail as possible. The critical source of data for following money is annual reports. The front part, often called the Report of the Directors or Trustees or Management Discussion and Analysis, contains general information on the organisation, operating and financial review information on that year's activities, and can also include management analysis, discussion of trends, forecasts, and other useful supporting information. The second part consists of the Financial Statements, made up of the Balance Sheet, Income Statement, Cash Flow Statement, and Notes to the Financial Statements. Together, these statements contain the majority of the financial data for following money. Importantly, the data available in the financial statements is more detailed than the flows captured in the map in step one, allowing them to be broken down further into detailed line items. For those less familiar with annual reports, it is worth highlighting, here, the importance of carefully reviewing the Notes to the Financial Statements. These should not be disregarded as they are an integral part of the financial statements, which contain the most detailed financial data on the organisation's activities, often further breaking down line items featured in the three main statements. For example, the rather general ‘expenses’ item on the Income Statement is typically broken down into more detail. In the case of IFFIm's expenses, line items include expenditure on vaccines (via Gavi), legal fees, and bond interest expenses.

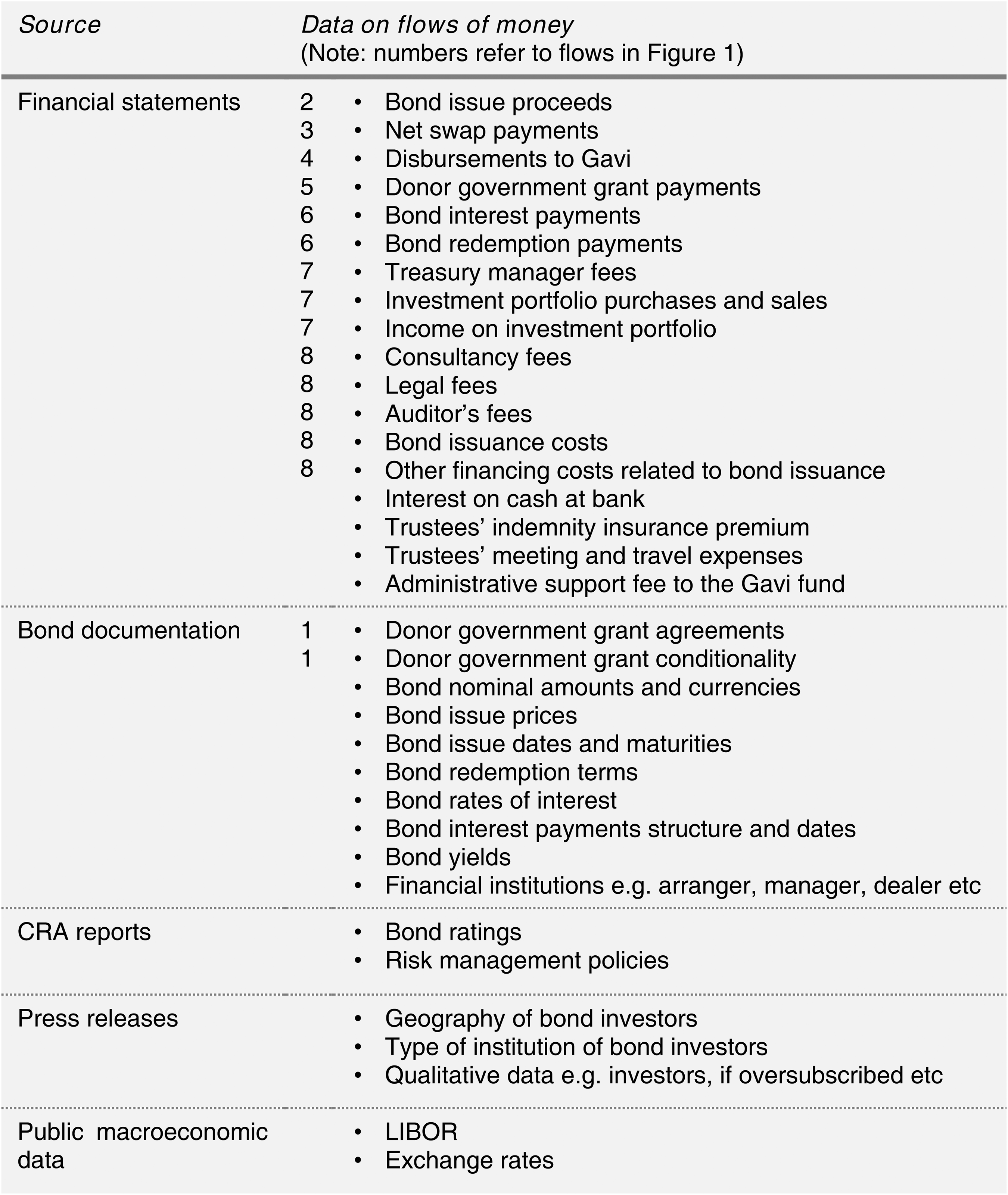

To complement financial statements, there are many other data sources for following money. These might include filings with stock exchanges or regulators for data on listed financial instruments and companies; credit rating agency reports, which cover risk management policies and financial metrics; press releases for information on significant events; investor presentations, which often include financial information or a business case; public macroeconomic data, for example, for information on interest rates or currency exchange rates; specialised financial market data reports, for example, insurance industry publications; and, for more information on an organisation’s activities, its own website, publications, statements and evaluation reports. The types of relevant documents available will vary depending on the case study. To illustrate an example, Figure 3 outlines the data sources for the main flows of money in the IFFIm case. This shows that, with IFFIm, the bond documentation filed with the Luxembourg stock exchange, consisting of the Offering Memorandum, Prospectus and Pricing Supplements, contained crucial information on donor government grant agreements and the vaccine bonds’ interest rate terms. The data sources listed above are often publicly available and can be collected through desktop research. This raw financial data can then be inputted and processed in excel (or similar), ready to be analysed in the next step. Interviews with key actors involved in the case study identified from the map might be helpful to fill in any gaps in following money. Additionally, in practice, this careful documentary review and analysis, whilst focused on gathering data to follow money, yields interesting information beyond financials. I found I uncovered significant information on, for example, the (political) history of how projects were set-up, or the narratives which justified important decisions that shaped the financial model.

IFFIm – main sources of data.

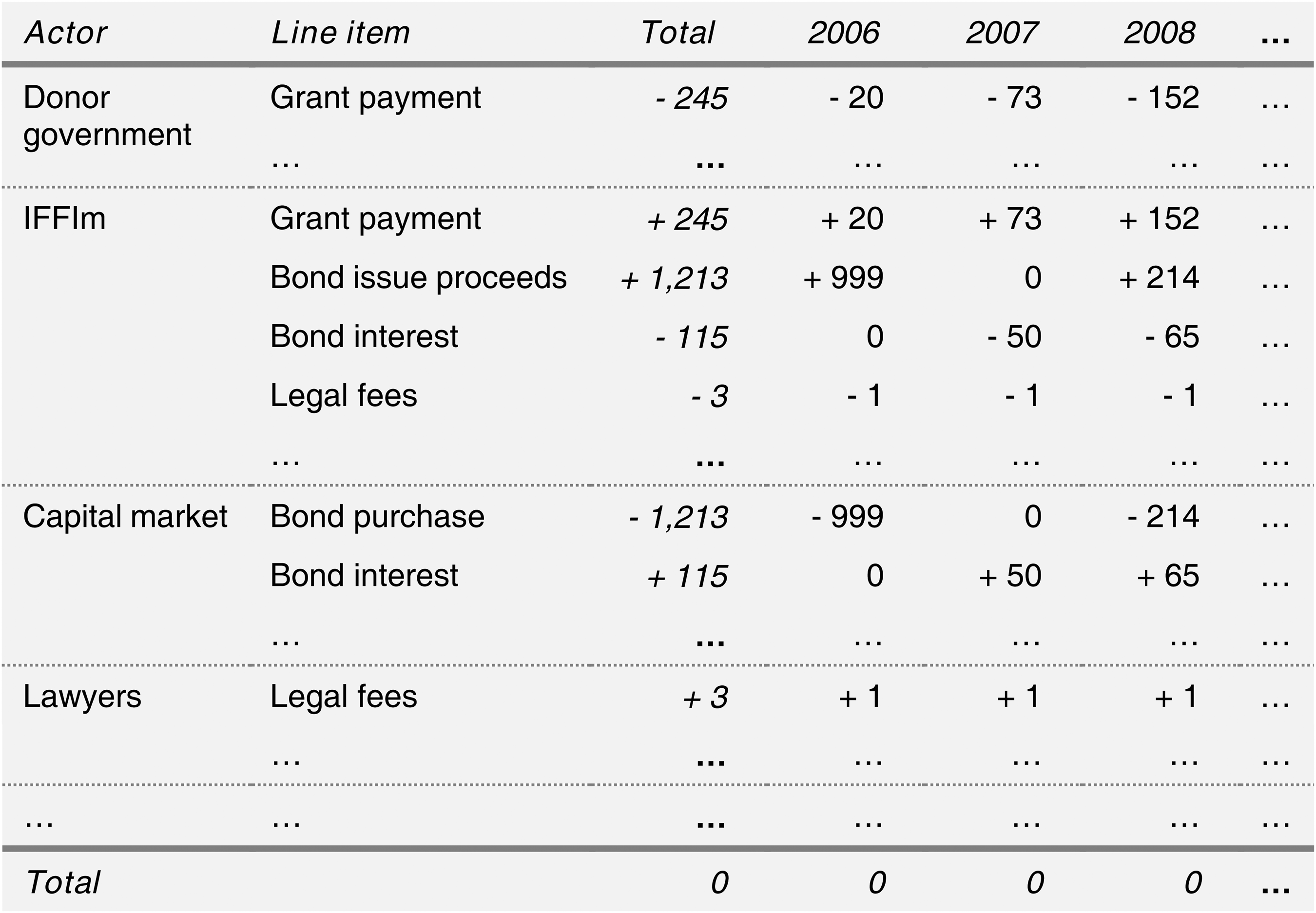

The third step is to do critical financial analysis to build a detailed model to follow all of the flows of money between all of the actors for the entire duration of the case study. Data analysis involves mapping the financial data collected in step two to line items for each actor in the model, covering all of the flows of money, keeping a granular level of detail (which goes beyond the map in step one). For this analysis, I set up a model in excel 4 . The first stage is to create the framework for the model to represent each actor over time (on an annual basis), and then, for each actor, to list all of the flows of money which they are involved in as line items. The second stage is to populate these line items drawing on the financial data collected in step two. The model is structured so that each money flow from an actor is captured as a negative entry, and each money flow to an actor is a positive mirrored entry (linked through formulas in excel). Figure 4 provides an illustration of the model, showing the ‘following’ logic of mapping each flow of money from an actor (negative entry) to another actor (positive entry) such that the model columns net out at zero, or in other words the following circuit is closed, and the model rows capture the cumulative (re)distribution of money to or from an actor via a particular financial mechanism. For some line items this is a straightforward process, for example, linking raw data from the Financial Statements on legal fees to a positive flow for the legal firm and a negative flow for their client. For other line items this is a more complex process requiring calculations, for example, IFFIm's net swap settlements to the World Bank. In the final model, each line item represents a particular flow of money, for example, donor grant payments, bond issue proceeds, investment portfolio movements, bond issuance costs, or various professional services fees. This is detailed work – the IFFIm analysis, for example, took about four months to complete. Analysing this follow the money model reveals many interesting findings which are the focus of the next section.

IFFIm – illustration of an extract of the model.

Why follow the money

In this section, I make the case for adopting a follow the money approach through five themes: the robust and detailed empirical evidence base, the (re)distribution of resources, social and economic relations, financialisation, and financial risk. In this section, I expand on these themes and, in the two subsequent sections, illustrate them through IFFIm and the Rhino Impact Investment project.

A follow the money methodology provides a robust and detailed empirical evidence base about the case study of interest. The methodology gives a clear and detailed picture of precisely what's going on, providing a wealth of information about the case study of interest. The approach delivers a precise and thorough understanding of the financing model, the network of actors, as well as insights on the scale of financial transactions which are only revealed through a meticulous quantitative approach. Here, I briefly outline highlights of the information revealed through the approach's three steps. First, the map of the flows of money reveals the network of actors involved, the nature of each actor's involvement, their significance for the wider network, the connections between actors, the complexity of the network, and where in space the flows are taking place. Second, compiling the financial information reveals detailed information on financial relations, the financial mechanisms involved, the terms and structure of financial instruments, and the nature of the financial relationships between actors. Third, the model of all of the flows of money provides a precise, quantitative view of the amounts of money flowing to or from each actor, the scale of each financial transaction or mechanism, how the amounts change over time, and the accumulation of wealth by each actor. The approach is particularly effective in cases where there is an element of uncovering needed to understand the financial model, network, or size of financial transactions.

Follow the money can be powerful for engagement and impact beyond academia by building on the detailed and robust evidence base which reveals a wealth of interesting information. This evidence can contribute to greater transparency and accountability, policy making, and broader societal change. The evidence is likely to be highly impactful for several reasons. First, financial evidence is often more persuasive for certain groups of stakeholders, including activists holding power to account, policymakers working within an economic or financial frame, or shareholders and management for whom financial evidence is often paramount. Second, the quantitative nature of the analysis can convey the importance of findings in terms of scale and provides different, often complimentary, insights to qualitative methods or interviews. Third, it creates a significant degree of transparency and clarity, revealing or uncovering what's happening in the case study under scrutiny. Finally, the information is difficult to challenge or refute as it is grounded in published financial information.

Empirically, following money delivers a precise account of the material (re)distribution of resources as money circulates in a case study. The approach reveals who benefits or loses, by how much, and where for the case study of interest. The approach precisely and quantitatively reveals the organisations and people benefitting and losing, the exact amounts of value peeled off (as money) by each actor along money's lifecourse, and the spatial distribution of that value. By answering who benefits and/or loses, by how much, and where, follow the money methodology makes a valuable contribution to fields such as political economy, political ecology or economic geography. The methodology's strength is providing a precise and quantitative answer to these questions. The approach is able to examine the (re)distribution of material resources, going beyond a descriptive view – it is able to say how much. The methodology is also able to analyse the (re)distribution of resources spatially, identifying where money is flowing by connecting each flow to an actor and place.

Theoretically, the methodology reveals the social and economic relations which support and are created by money's circulation. Follow the thing methodology allows research to see behind the ‘veil’ of the market to examine social and economic relations (Harvey, 1990). Following money, therefore, reveals and allows an examination of the social and economic relations which support and are shaped by the circulation of money in a case study of interest. For money as the thing, the approach can be applied to many areas of research, depending on the case study. For example, following money in the form of development finance in IFFIm informs a theoretical understanding of international development and global health. For the rhino bonds case, the methodology allows us to ‘see’ social and economic relations in conservation, contributing to political ecology. Beyond detailing networks of actors and financial instruments, as part of examining social and economic relations, the approach can be a springboard to inform a range of political issues, for example, power and space, which I elaborate on through the case studies.

The methodology can contribute to understanding financialisation. Financialisation, defined as the ‘growing influence of capital markets, their intermediaries, and processes in contemporary economic and political life’ (Pike and Pollard, 2010, 29), has been studied extensively in a range of disciplines. There is a significant body of interesting work addressing theoretical questions and examining empirical studies of actually existing financialisation (see for example Allen and Pryke, 2013; Brooks, 2016; Weber, 2010). However, critiques of this literature have emerged, pointing to limited engagement with the specific processes of financialisation or that studies present a descriptive ‘financialisation of’ account (see for example Aalbers, 2017; Christophers, 2015; Engelen, 2008; Mader et al., 2020; Ouma, 2015). In this context, follow the money can make a helpful contribution, specifically contributing to understanding the mechanisms and the consequences of financialisation. First, in focusing its lens on financial relations, instruments and transactions, the approach engages with the precise mechanisms of financialisation, including the specific mechanisms through which value as money is transferred. Alternatively, this can be conceptualised as part of getting in between M and M’ (Ouma, 2015; see also Ouma et al., 2018). Second, by precisely and quantitatively measuring the material (re)distribution of resources following the circulation of money, the methodology analyses some of the economic and political consequences of financialisation, including the (re)distribution of profit and accumulation of wealth.

Finally, follow the money informs research on financial risk in society. Follow the money provides a clear and detailed understanding of the distribution of financial risks, uncovering who faces them and their significance. This can contribute to the broader study of risk in society and answers political questions around risk in fields like political economy or political ecology, such as what are the risks, who faces those risks, and how significant are those risks in terms of size? In examining the financial instruments, the follow the money approach provides information on the financial risk structure, the distribution of risks between the different actors, and an insight into the probabilities of the different risks materialising. In assessing the quantities of money involved for each flow of money, the approach provides information on the scale of these financial risks.

International finance facility for immunisation

The IFFIm case shows how a follow the money approach reveals the processes, mechanisms and logics of financialisation behind ‘frontloading’ aid (theme 4); quantifies the significant redistribution of resources to private actors (theme 2), which is an important consequence of financialisation (theme 4). Furthermore, follow the money provides detailed evidence on technical features of the financial model which have significant political consequences (theme 1); and reveals how the model's financial risk management measures protect investors (theme 5). Following the money also informs an understanding of the case's social and economic relations (theme 3) by uncovering a complex network which connects vaccines in low-income countries to global finance, highlighting the power of credit rating agencies, and showing the uneven spatial distribution of material resources.

Follow the money methodology reveals the processes, mechanisms and logics of financialisation which lie behind IFFIm's ‘frontloading’ model. The main process of financialisation is securitising aid. Through vaccine bonds, IFFIm bundles and sells the rights to income from future donor government aid grants, pledges which amounted to over $8 billion by 2021 and last as long as 19 years. The long-term legally binding donor government grant agreements are the stable income stream which is converted into financial instruments – over $8 billion of vaccine bonds by 2021 – and exchanged in capital markets to be made available for speculative capital (see Leyshon and Thrift, 2007). Examining the financial instruments beyond the headline, IFFIm's vaccine bonds are mostly fairly simple, straightforward transactions, or ‘plain vanilla’ in financial market jargon. Typical bonds are issued at an issue price between 99.7% and 100% with redemption at par, and with straightforward fixed interest rate terms of on average 4.7%. A minority of bonds have floating interest rates set at a small margin of on average 0.15% above LIBOR, and a small number are deep discount bonds or zero-coupon instalment notes. Beyond detailing the mechanisms of financialisation, including the financial instruments and their terms, follow the money also reveals the financial logics of those mechanisms. IFFIm's model has a complex debt-driven financial logic where it must issue more bonds in order to make interest and redemption payments on previously issued bonds (similar to the ‘debt machine’ in Peck and Whiteside, 2016). This contrasts sharply with the simple frontloading logic expressed in typical narratives surrounding IFFIm, where bonds are issued to frontload funding for Gavi and government grants are used to pay investors. An important economic and political consequence of this financialisation, which follow the money reveals, is the redistribution of resources.

Scrutinising IFFIm's financing model through a follow the money approach reveals significant opportunities for private profit hiding in plain sight. Following the money quantitatively reveals the distribution of financial gains and losses, in other words it reveals who benefits or loses, by how much, and through what mechanisms. In IFFIm, there are a range of mechanisms through which money is transferred to financial actors. The most significant include the yields on bonds for investors, which are determined by the interest rate provisions, issue price and redemption structure; and fees for bond issuance costs and other professional services. Between IFFIm's launch in 2006 and 2019, interest payments to bondholders totalled $879 million. On top of this, investors were paid $135 million in principal repayments above the purchase price (when the issue price is below 100% of the note's nominal amount and redemption is at par, redemption payments exceed the issue price). Third, financial institutions earnt $33 million for bond issuance costs, professional services $22 million (lawyers $10 million, auditors $5 million, insurance companies $4 million, and consultants $3 million), and $29 million was paid to the World Bank as treasury manager. To put these figures into perspective, together they represent 35% of the $3.137 billion IFFIm received from donors over the same period or 17% of the $6.546 billion of donor pledges. These sums are substantial, they are paid for through publicly funded aid and ultimately come at the expense of Gavi and its beneficiaries. IFFIm made substantial disbursements to Gavi for immunisation and health system strengthening, totalling $2.942 billion over the same 2006 to 2019 period. This represents a significant contribution to global health spending; however, it also underscores the non-trivial size of the financial rewards distributed to investors and intermediaries, which represent 36% of the amount of Gavi disbursements (excluding payments to the World Bank). Despite claims to ‘leverage’ or ‘mobilise’ private sector funds, there is no aid additionality in IFFIm's model. This is similar to findings from analysing other social finance mechanisms where public resources are transferred to private actors (see for example Dowling, 2017; Rosenman, 2019). In particular, the findings from IFFIm show how two distinct groups of financial actors, investors and intermediaries, gained significant sums in the financialisation of global health (see also Allen and Pryke, 2013; Folkman et al., 2007). What is unique in the insights gained from adopting a follow the money approach is quantifying precisely how much each actor benefits.

Detailed technical features of IFFIm's model, such as grant conditionality, have important political consequences for donor governments and impact frontloading for Gavi. Donor government grant agreements include a feature such that payments to IFFIm are technically conditional. The conditionality is based on a reference portfolio of all Gavi-eligible countries that are members of the IMF, with a weighting assigned to each of those countries. Donor grant payments are reduced by a percentage based on the weighting of the Gavi-eligible countries which are in protracted arrears to the IMF. In practice, at the outset in 2006, the actual weighting stood at 96% and then, as countries cleared their arrears, it had increased to 99.5% in 2020, meaning donor governments were paying almost all of the pledged amount. There are two important consequences of the grant conditionality. First, donor governments keep pledges off their balance sheets, similar to social impact bonds (see Dowling, 2017), often seen as an advantage in the political climate of the mid 2000s, particularly in the United Kingdom where IFFIm has its origins (for more see Kitson and Wilkinson, 2007; Sawyer, 2007). Following accounting rules, conditional payments only affect donor government budgets in the year they are expensed, rather than being accounted for as debt at the moment the pledge is made. Second, more buried in the detail, IFFIm's ability to frontload funding for Gavi is limited. IFFIm maintains a gearing ratio limit to mitigate the risk that more Gavi-eligible countries might fall into protracted arrears. This would mean payments from donor governments would be reduced which may impact IFFIm's ability to meet its obligations to bondholders. The gearing ratio is the relationship between IFFIm's assets, mainly donor government pledges, and its liabilities, especially payments due on bonds. IFFIm only issues bonds against a proportion of the net present value of donor government commitments, keeping the remaining proportion as a reserve to protect bondholders. The gearing ratio limit stood at 70.3% in 2006 and 2019 (it has varied only slightly over the period). The buffer therefore stands at around 30% of the present value of donor pledges, meaning IFFIm can still pay bondholders if donor payments are reduced by close to 30%. This is important detail on the financial mechanisms which determines who benefits and how risk is distributed (expanded on next). Not only do we find that risk management measures constrain IFFIm's frontloading of funds to Gavi and use of capital, but the approach reveals the significant scale of this constraint – the 30% cushion protecting investors is significantly higher than the actual reductions of between 4% and 0.5% over the period.

IFFIm has implemented several financial risk management measures oriented towards protecting investors. Here, I present two examples. The gearing ratio, introduced above, which also has implications for the distribution of risk. IFFIm maintains the gearing ratio such that it only issues bonds against up to 70.3% of the present value of donor government pledges. This limit means investors can still be paid if donors default on up to 29.7% of their commitments. In addition, between 2013 and 2020, the World Bank applied a further buffer of 12% of the present value of donor government pledges (due to IFFIm's significant swap exposure level). At this level of 58.3%, IFFIm could pay investors even if donor governments default on 41.7% of their pledges, a highly unlikely scenario. It is worth noting that IFFIm typically operates below these limits, meaning the reserves buffer protecting investors is actually larger. This example shows two specific mechanisms through which public finance is protecting investors (see also Rosenman, 2019), limiting the credit risk bondholders face. This example also illustrates how the approach can analyse the scale of this protection – these policies can be characterised as very prudent towards investors, noting that the UK or French governments 5 are unlikely to default on their commitments.

IFFIm involves a complex network of social and economic relations, as alluded to in the analysis so far, in which the recipients and delivery of vaccines in low-income countries become connected to and contingent on global financial institutions, capital markets and large-scale financial transactions. IFFIm makes a significant contribution to global health by providing about 20% of the funding for Gavi (IFFIm, 2020), which operates immunisation programmes in low-income countries and vaccinates almost half the world's children against infectious diseases (Gavi, 2021). In turn, IFFIm sources its funding from donor governments and frontloads these funds by issuing vaccine bonds. Following the money, reveals what this frontloading entails in terms of the social and economic relations to which vaccine recipients become connected. I provide a flavour of this here with respect to the financial actors and markets involved in the vaccine bond issuance itself, which includes single bonds up to a nominal value of $1 billion and over $8 billion in bonds in total. The vaccine bond programme is arranged by the London office of one of the world's largest investment banks, Goldman Sachs; a plethora of large financial institutions, typically based in London, carry out roles such as manager, dealer, placer, paying and transfer agent, registrar or listing agent; the three dominant global credit rating agencies rate the bonds; and investors represent a range of financial institutions such as pension funds, asset managers and central banks. The bonds are listed on the Luxembourg stock exchange and, in parallel, IFFIm engages in significant hedging transactions in derivative markets, with market counterparties intermediated through the World Bank, to swap all its currency and interest rate exposure on its repayments on the bonds.

As part of examining social and economic relations, the approach reveals the power and influence of credit rating agencies in the network identified above on IFFIm's design. Credit rating agencies, as gatekeepers to debt, are powerful financial actors (see for example Omstedt, 2019) and IFFIm is no exception. Their rating processes influenced several important technical design features of IFFIm's financial mechanism. For example, IFFIm using swaps to hedge all its currency and interest rate exposure for both assets and liabilities; the World Bank being part of the financial structure; not giving security to bondholders over IFFIm's rights to receive the donor government grants; and ensuring government pledges were legal, binding and enforceable (Hughes-McLure and Mawdsley, 2022; McCormick, 2007). These instances speak to the technocratic financial management practices operating in global health and development and how political decisions are constrained by financial market practices (see also Allen and Pryke, 2013; Bryan and Rafferty, 2014; Peck and Whiteside, 2016).

Furthermore, the social and economic relations are profoundly spatial, with the redistribution of material resources concentrated in financial centres in the Global North. The flows of money and actors are necessarily fixed in particular places, which can be identified. Financial rewards are distributed primarily to investors in the Global North, which accounted for 75% of the face value of the notes issued by the end of 2019. Going into more detail reveals that $2.4 billion or 34% of the value was placed in Japan, through 23 Uridashi bonds issued between 2008 and 2013. After the Global Financial Crisis, IFFIm relied on a geographically specific market, Uridashi bonds, to access lower borrowing costs, connecting retail investors in Japan with vaccine recipients in Gavi-eligible countries. In line with other research, the spatial pattern of the distribution of financial resources is concentrated in the Global North; however, this example shows how following the money also reveals nuances in the spatial pattern not necessarily available without detailed financial analysis.

Rhino impact investment project

The rhino bonds case illustrates how following the money provides clarity about the case study's aim to mobilise new capital for conservation (theme 1); reveals the detailed mechanisms of financialisation (theme 4); measures the redistribution of resources quantitatively, in particular to investors, revealing the rhino bond model's financial cost (theme 2); and offers insights on the model's claim to shift risk from the outcome payer to investors (theme 5).

Following the money provides clarity about the rhino bonds model and raises questions over its claim to mobilise new capital for conservation, a key aim in the context of many conservation projects struggling to raise funding from traditional sources (UNDP, 2018). A typical presentation of the project, given this aim, foregrounds the investor's financial contribution to rhino conservation 6 . At the outset, bond proceeds raised from investors are (in part) used to fund conservation interventions. Later, investors are repaid with a return determined by the conservation outcome - rhino population growth. Often unaddressed, or not explicitly, is where this payment comes from. Taking a follow the money approach, specifically building the map, shifts the perspective to the complete picture of all of the flows of money over the lifetime of the project. This map clearly highlights the final step, when the outcome payer makes the payment to investors (numbers 4 and 5 in Figure 2). This last, crucial, part of the flow of money is often overlooked. Its importance shouldn't be underestimated. Ultimately, under the terms of the first rhino bond, unless rhino populations decline, the outcome payer (a traditional conservation funder) is funding the conservation work with an adjustment of the exact amount paid based on results at a later date. Shining this light on the rhino bond project reveals critical facts, raising questions over the project's claim to mobilise new capital for conservation, in line with findings from other critical work on similar social and green financial models claiming to mobilise new capital (see for example Dempsey and Suarez, 2016; Rosenman, 2019).

Following money reveals the mechanisms of the financialisation of conservation, going beyond the obvious financial instrument of bonds. The project's financialisation process converts conservation grant pledges into financial instruments, rhino bonds, which are available to investors. In this way, the environment, more specifically in the case of the first rhino bond, black rhino numbers in two parks in South Africa, become connected to the financial fortunes of investors. Whilst on the surface the headline financial instrument – bonds – appears similar to the IFFIm case, the instruments differ in important ways in their structure, information revealed through forensic financial analysis methods. In contrast to IFFIm's mostly ‘plain vanilla’ bonds, the rhino project structured the Wildlife Conservation Bond to create an outcomes-based payment model. The rhino bond links part of the financial return for bondholders to future realised black rhino population growth at project sites five years later, meaning the financial return for investors is unknown at the outset. The bond is structured such that the principal is independent of rhino populations. On top of that, in lieu of interest, there is a conservation success payment which varies depending on rhino population growth rates at maturity, funded through a performance-based grant from the Global Environment Facility. Next, I turn to the important distributional consequences of this financialised conservation funding model, including for the cost of conservation interventions.

Following the money through the first rhino bond, the Wildlife Conservation Bond, reveals the redistribution of resources quantitatively as money circulates. The bond's structure, detailed above, delivers financial returns to bondholders in two ways. First, with respect to the principal, redemption payments exceed the issue price. The bond was priced at 94.84% of the aggregate nominal amount with redemption at par, meaning the World Bank raised $142.26 million in bond proceeds at issuance and will repay investors $150 million. For investors, this represents a certain financial return of 5.44% ($7.74 million), as the principal is not connected to rhino population growth. Second, a conservation success payment is paid, linked to rhino population growth. The exact terms of the bond deliver a $13.8 million payment to bondholders if rhino population growth rates exceed 4%, $11.0 million for growth rates between 2% and 4%, $5.5 million for growth rates between 0% and 2%, and no payment if rhino populations decline 7 . For the outcome payer, the Global Environment Facility, compared to the $10.3 million spent on conservation interventions, the conservation success payment is 7% higher if rhino growth rates exceed the target 2% and 34% higher if growth rates exceed 4%. The model's benefit is that the outcome payer's payment is only 53% of the cost of the interventions if rhino population growth rates do not meet the 2% target, and $0 if rhino populations actually fall. For investors, taken together, the two mechanisms deliver a financial return on investment over five years of 15.1% if rhino growth exceeds 4%, 13.2% if rhino growth rates exceed the target 2% but remain below 4%, 9.3% if rhino growth rates do not meet the 2% target but are positive, or 5.44% even if rhino population declines. Accordingly, investors make a financial gain regardless of rhino population growth rates. The exact return varies from an acceptable 5.44% to a rewarding 15.1% depending on the scenario. For the outcome payer and World Bank together, if rhino population growth is positive then the cost of the rhino bond model exceeds the amount spent on conservation interventions 8 . Analysing the complete picture of the flows of money, including both the principal and conservation success payment, reveals the money redistributed to investors exceeds the actual spending on conservation interventions in all scenarios but rhino populations declining. Given this opportunity cost, to evaluate the model, we must also consider risk.

Following money reveals the financial model has not effectively shifted risk away from the outcome payer, and that the nature of the risk has been transformed from an environmental risk to a financial risk. The project's promoters argue an important benefit of the outcomes-based financing mechanism is that the risk of conservation interventions failing to achieve their desired impact is shifted from outcome payers to investors, in exchange for a financial return. In this story, the outcome payer faces no risk. In an alternative reading of the story, which takes into account the detail of the financial instruments, it becomes clear the risk the outcome payer faces hasn't disappeared but simply changed. In a traditional funding model, the outcome payer funds an intervention with a risky unknown conservation outcome – the risk is in terms of rhino population numbers. In the rhino bonds model, the outcome payer pledges money and faces a risky unknown future payment to investors – the risk is financial in terms of a dollar amount, in turn determined by the conservation outcome and the terms of the bond. For the outcome payer, an environmental risk has been transformed into a financial one. This financial risk is a significant five-year deferred liability of an unknown amount to be determined five years later. Furthermore, the key environmental unknown figure driving that financial unknown is the same rhino population number. Notably, the probability of success in increasing this number, which requires higher rhino reproduction rates, is arguably unlikely to be affected by whether the bill was settled at the outset of the project or the end (see also Sullivan, 2013, on using financial derivatives to sell species extinction risk to investors). In conclusion, in contrast to its claims, this innovative financing model has not completely shifted risk to investors. Traditional conservation funders are not only still funding conservation as new capital is not necessarily mobilised, but also still facing risk, only now it is a financial risk. Additionally, a return for investors who have lent money for a five-year period has to be funded, so the total costs of the model exceed the actual cost of the conservation intervention, unless rhino populations decline – the opposite of the desired outcome.

Notes of caution: What following money cannot achieve

Having laid out five themes which I argue make a compelling case for following the money, I now turn to two important notes of caution which address what cannot be achieved from the approach: the challenge of unfollowable segments and the more general case of ‘money’.

In adopting this paper's follow the money approach, the researcher will most likely find unfollowable segments in money's flows. While this can be an important limitation of the methodology depending on the scale of the challenge, unfollowable segments are also interesting findings in themselves. The story of why some segments or things are unfollowable is also interesting as the approach reveals the gaps, their causes, and opens up analysis of what those gaps contribute to the chain (see Hulme, 2017). In the case of IFFIm, I found two flows of money one step removed from IFFIm – transactions between the World Bank and market counterparties – were, in part, unfollowable because they do not feature in a disaggregated way in those organisations’ financial statements. These unfollowable flows showed the limitations of transparency once market counterparties, who are one step removed, become involved in development finance, raising questions of accountability in innovative development finance models. Importantly, these unfollowable flows were not so significant that they meaningfully impacted my analysis. I had information that those flows of money were there, what the financial instruments were, who the actors were, and an approximate view of their quantity – only information on the exact quantity was missing. In practice, lack of information on unfollowable flows can be mitigated or filled in through interviews, learning from other flows in scope, and a careful choice of case study based on data. Specifically, selecting cases such that the project or initiative or organisation under study appears sufficiently in financial statements, in other words published at a sufficiently disaggregated level or even on a standalone basis.

What about money? Perhaps adopting the follow the money approach presented in this paper is akin to the study of a case or a form of money rather than a more general money. Returning to the paper's understanding of money as a material practice and a social relation, money can take on many forms. In the context of the case studies in this paper, for example, which both happen to feature bonds, following the money informs an understanding of credit money, the majority of money in capitalism (Lapavitsas, 2003). Perhaps following a more general case of money would be starting from its origination at a central bank and following its circulation through financial institutions, corporations and households, potentially indefinitely. Or perhaps, that too, remains a particular form of money. Indeed, Gilbert (2011) cautions that following a universal form of money may be impossible, and Zelizer (2000) argues against the very concept of ‘money in general’. Alternatively, perhaps applying this methodology to IFFIm informs an understanding of the material (re)distribution of wealth in development projects, and the social and economic relations of development finance and global health. In that sense, the thing being followed was money in the specific form of development finance. Equivalently, studying rhino bonds is following money in the form of conservation finance, contributing to the study of the financialisation of conservation and understanding the politics of new conservation funding models. This conceptual viewpoint links to the study of finance, a different analytical concept to money. Indeed, critical for the methodology proposed in this paper is data from annual reports and financial statements, so it is applicable to cases where money flows in a form of finance such that it appears in financial reports. This discussion returns to and highlights the challenging task of defining money, and the consequences for what forms of money can be studied through a follow the money methodology.

The aim of this paper is not to resolve open debates in the study of money; it remains to move forward the idea of following money by proposing a feasible approach. Depending on one's camp in the literature on money, this proposed approach may be limited to the study of certain (more or less broad) forms of money, such as credit money or a different analytical framework of finance. Nevertheless, the methodology remains a practical approach for following money. I argue that, as in other areas of academic research, following money in various forms as case studies can contribute to our understanding of the general case, and, for the challenging and puzzling ‘thing’ that money is, makes research practically feasible. The call for future research is, therefore, to use a follow the money approach to examine more cases of money in order to build up a better understanding of the more general thing: money. As money is a special ‘thing’ to follow in that it is tricky to define and ubiquitous, such research is particularly interesting because it contributes to, at best, the study of money and, at a minimum, the area of research within which the case study fits, in this paper's examples international development and conservation, but it could have been urban geography or inequality among others.

Conclusion

The concept of following money has been employed successfully in several spheres, often appearing in connection to tackling crime or in investigative journalism. Taking up the challenge raised by Christophers (2011) who presents a compelling theoretical case for following money, I have followed the circulation and distribution of money in my research. In this paper, I present my innovative follow the money approach which uses quantitative methods to do critical financial analysis (on this, see also Kass, 2020). The three-step approach I outline starts with mapping the network of flows of money and actors, then collecting and compiling financial data on these flows of money, and ends with critical financial analysis to build a detailed model of all of the flows of money between all of the actors for the duration of the case study.

Follow the money is a powerful methodology which can make important contributions to debates in geography. In this paper I make the case for adopting the approach through five themes. The first, that following the money provides a robust and detailed empirical evidence base is both simple and powerful. The methodology reveals a wealth of information about a case study, providing a clear understanding of what's happening and shining a light on details which might otherwise be concealed or overlooked. This evidence base can provide a powerful platform to engage outside academia and create impact. The second theme addresses the approach's most significant empirical contribution; follow the money provides a precise account of the material (re)distribution of resources, revealing who benefits or loses, by how much, and where. The third theme is analysing social and economic relations for a case study, or seeing behind the ‘veil’ of the market, including relations in space as money has a geography. Theme four argues that, by its nature, the methodology is particularly valuable for contributing to the study financialisation through a detailed and precise engagement with the specific mechanisms, processes and complexities of financialisation as well as addressing its economic and political consequences quantitatively. Theme five, on financial risk, captures the methodology's contribution to the study of risk in society through analysing the types of risks, who faces them, and their significance in terms of scale and probability.

Footnotes

Acknowledgments

I would like to thank the reviewers and editor, Brett Christophers, for their helpful comments on developing the paper. I would also like to thank Chris Sandbrook for pointing me to the rhino bonds project, Carolina Alves for her comments on earlier work on the ontology of money, as well as Emma Mawdsley and Frances Brill for their advice and support developing my ideas.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Economic and Social Research Council (grant number ES/P000738/1).