Abstract

Britain is rarely considered an exemplar of ‘state capitalism’. In contrast, we argue that Britain should be treated as the prototype project of state capitalism in the world economic system, the primary contribution of our paper been to outline the parameters of state capitalism in Britain across two historical periods. Turning the conceptual lens of state capitalism towards Britain raises some challenging issues for the wider literature. Recent scholarship has started to consider greater diversity in regimes of state capitalism and moved beyond the typical nation-state geographical imaginary of state capitalism. Similarly, our paper seeks to introduce a new spatiality to state capitalism with deeper sensitivity to multi-scalar relations. State capitalism in Britain has rarely been bound to the geographical limitations of the nation-state; instead, it has been a transnational project, centred variably on empire, Europe, and the global market – with industrial policy tailored to enable the British economy to exploit and/or service these various spaces by ‘making markets’. We emphasize the often-financialized nature of this industrial policy intervention arguing it is constitutive of a ‘financial state capitalism’.

Introduction

Britain is rarely considered an example of state capitalism. This is unfortunate given that the systemic role played by the state in promoting the economic development of advanced industrial nations, including Britain, is well documented (Chang, 2002; Cohen and DeLong, 2016; Reinert, 2008). State capitalism is not something with which only emerging or transition economies engage (see Alami and Dixon, 2020: 88). Indeed, we argue that Britain was an original exemplar of state capitalism in the global capitalist system, an acknowledgement that would do much to increase our understanding of the diversity of state capitalist regimes. A contention that aligns with some of the most important – and widely acknowledged – accounts of British political-economic history, not least Ingham’s (1984) contention that the development of British capitalism, particularly efforts ‘to reproduce it in the face of adverse economic conditions, cannot be explained unless the independent role of the state is taken into account’.

Similarly, whereas perhaps the imaginary of early state capitalist literature focused overly on institutions rooted in the nation-state, our understanding of state capitalism has benefited from scholarship investigating the wider spatial relations of state capitalism. Examples include those identifying the international commercial strategies of ‘national champions’ or ‘sovereign wealth funds’ (Dixon, 2017; Kurlantzick, 2016), and those where trade policy plays a central role in state capitalism formation, especially where it has been used by the nation-state to capture external demand and reduce international competition (Kaldor, 1966).

A further interesting issue within the state capitalism literature we approach in this paper is that of appropriate periodization. Here, we follow Alami and Dixon’s (2020: 86–88) appeal for periodization based on configurations of political and economic power, which allows for a better appreciation of historical continuities and change in forms of state intervention. This approach is clearly influenced by the Regulation School in terms of the temporality of state formation and evolution (Aglietta, 1976; Boyer, 1990). It is these logics we follow in our paper to adequately periodize what we term ‘financial state capitalism’ in Britain. We ground our analysis in a novel understanding of state capitalism, including the relationship with ‘the capitalist state’, although we do not attempt in the paper to offer a fully formed theory of state capitalism.

Instead, the primary contribution of our paper is to outline the empirical aspects of state capitalism in Britain across historical and recent periods (1821–1914 and 1958–2016), which we believe provides a platform for further development of the literature on state capitalism. State capitalism in Britain has rarely been bound to the geographical limitations of the nation-state; it has been a transnational project, centred variably on empire, Europe and the global market, with industrial policy tailored to enable the British economy to exploit and/or service these various spaces by ‘making markets’ (meaning creating, structuring, and sustaining markets). Furthermore, we argue that the institutional organization and policy intervention of British capitalist practice in these historical periods has taken a unique form that we describe as ‘financial state capitalism’.

We make our argument by emphasizing the often-financialized nature of intervention by the British state. In discussion of the institutional organization of financial state capitalism, we inevitably reference institutions such as the Treasury, Bank of England and the City of London, but broaden our frame of reference to include social institutions as well such as the aristocracy and Church of England. Meanwhile, we conceptualize direct intervention to have taken the form of industrial policy. While trade policy is often seen as part of state capitalism, there has been less attention to the creation of external markets for finance. The British case illustrates how visible state interventions, such as monetary and commercial policy, were deployed more than merely neutral instruments of stabilization, but as a financialized industrial policy that serve to sustain accumulation regimes.

State capitalism: Territory and temporality

In this section, we seek to build our later examination of state capitalism in Britain directly upon Alami and Dixon’s (2020) synthesis of the literature and its encompassing tensions, controversies and challenges (see also Ricz, 2018; Wright et al., 2021). Alami and Dixon point towards four issues that require resolution so that state capitalism can become analytically meaningful: the need for a definition of state capitalism, the spatial boundaries of state capitalism, the temporality of state capitalism and the ‘missing link’ with capitalist state. Whilst it is not the aim of our paper to offer a coherent theory of state capitalism, we do think the empirical exploration of state capitalism in Britain identifies issues of relevance to each of these points, which we will address in turn.

We define state capitalism as the use of state agency to (re)produce certain dominant modes of capital accumulation and social organization for the benefit of privileged interest and societal groups, taking place in conjunction with, or in subjugation of, economic agents in the private sector, and involving multi-scalar relations from the individual to the global. Whilst we are content that our definition of state capitalism accurately explains its core features, especially in the British case, we acknowledge that there are clear boundaries around the definition that might not capture the more mechanistic aspects of state capitalism, such as the collection of tax revenue (which might empower elites further) and the relationship between voters and economic growth (with democracy providing voters with the opportunity to exercise power every few years).

Existing definitions of state capitalism do not satisfactorily facilitate analysis of state capitalism in British. Alami and Dixon (2020: 71) are correct to identify, for instance, the absence of a unified definition in the existing literature, with state capitalism used to identify ‘an extremely wide array of practices, policy instruments and vehicles, institutional forms, relations and networks that involve the state to different degrees and at a variety of levels, time frames, and scales’. Nevertheless, there are commonalities in deployment of the term, with the state commonly conceived as using its sovereign authority to orient economic processes (domestic or international) to the political objectives of state actors (see Wright et al., 2021: 2–3). For example, Bremner (2010: 43) defined state capitalism as a ‘system in which the state dominates markets primarily for political gain’. Elsewhere, Lee (2020: 1; see also Sperber, 2019: 102) posited that state capitalism is a ‘capitalist economic system where the role of the state is dominant in investment, production, and distribution in the economy, through its own undertaking in commercial activities or control over corporations’.

Such definitions suggest that industrial policy is critical to our understanding of state capitalism, with Musacchio and Lazzarini (2014: 2) positing that it involves ‘the widespread influence of the government in the economy, either by owning majority of minority equity positions in companies or by providing subsidized credit and/or other privileges to private companies’. The association of state capitalism with what might be termed ‘traditional’ industrial policy is that it risks excluding from analysis those examples, such as the case in Britain, where the role of the state has been more coordinative than directive.

The definition of state capitalism offered by Wright et al. (2021: 2) is therefore more promising: ‘an economic system in which the state uses various tools for proactive intervention in economic production and the functioning of markets… within the home market and abroad, in the interest of domestic firms and for diplomatic purposes’. Wright notes that this definition includes use of industrial policies, such as government ownership, subsidy and investment to intervene in ‘economic production’, but also formal and informal coordinating mechanisms such as macroeconomic policy and regulation to shape the ‘functioning of markets’. Another benefit of this definition is its acceptance that state capitalism might occur across national boundaries and involve a multiplicity of objectives.

While Wright's definition might better capture the nature and scope of state capitalism, a weakness is that it may not help us to appreciate what is distinctly capitalist about state capitalism. Here, we might usefully learn from the concept of the ‘accumulative state’, in which state power is directed towards propping up capital accumulation and managing any emergent social conflicts from that process (Scheiring, 2019). It is our view that the definition of state capitalism must acknowledge that the inherent purpose of any such project within a capitalist system is to promote and support capital accumulation, something we sought to place at the heart of our definition of state capitalism. Without the inclusion of capital accumulation within the definition, there is nothing to stop the addition of centrally planned economies such as North Korea, thereby extending the analytical usefulness of the term to breaking point.

At this juncture, it is worth reiterating Alami and Dixon’s (2020: 86–88) point about periodization. An analytical framework is required by which to judge when state capitalist projects arise or come to an end, something which our new definition of state capitalism (at least in part) might help to achieve. An appropriate mechanism for periodization is needed because it challenges us to consider the societal interests of who might benefit from projects of state capitalism, and how these interests collude and collide and elide and evolve, over time. For example, the literature on the neoliberal state in the post-crisis era has come to recognize that large-scale state action is essential to maintaining neoliberalized relations in the private sphere (Berry, 2022; Davies, 2016). More simply, without appropriate ways to periodize state capitalism, the risk is run that it becomes synonymous with the ordinary operation of the capitalist system stripping the concept of any analytical usefulness.

We must also push the point about territoriality to its logical conclusion; if state capitalism can involve intervention by governments in international contexts, it can also involve non-intervention by governments in their own domestic contexts, insofar as a range of state actions might serve the overall accumulation regime serviced by the state. State capitalist regimes must therefore be considered at the multi-scalar level. The transnational projection of power by capitalist regimes goes hand-in-hand with the domestic accommodation of transnational capitalist processes and vice versa in Britain's case; and so, if the state capitalist lens does not allow us to elucidate how British capitalism (or American, European, Western, etc. capitalism for that matter) has developed, then our argument is that it is probably not an adequate tool to help us understand the development of capitalism anywhere.

Finally, discussion thus far begs consideration of the ‘missing link’ with the more general and enormous literature around ‘the capitalist state’. Here, we reiterate that we do not engage with a full exploration of this relationship, rather we consider it a productive rather than problematic test of our approach, and another example where the British case identifies interesting issues for the state capitalism literature. At least, by offering some initial views on how we conceive the capitalist state to operate, we hope to begin a process in which literature on state capitalism might in future be grounded within necessary theory (Alami and Dixon, 2020: 84).

In exploring the relationship between state capitalism and the capitalist state, our paper follows the logic set out by Jessop (1983; 2012), by taking a ‘strategic-relational’ (Poulantzas, 1969) approach to understanding the role of the state in the capitalist system in which ‘state power… [is] revealed in the conjunctural efficacy of state interventions… [themselves] a form-determined condensation of the balance of political forces’ (Jessop, 1983: 6). Alternatively, the instrumental approach views the capitalist state as neutral tool that can be used by whichever elites (more often than not a capitalist class) gain control over its institutions (Demirovic, 2010; Miliband, 1969). At the other end of the spectrum, structuralists consider the state to show evidence of ‘prior bias towards capital’ (Jessop, 2012) such that it functions on behalf of capitalist elites (Domhoff, 2021; Offe, 1984).

Although none of these approaches are without criticism, the strategic-relational view benefits from standing at the intersection of the two alternative approaches to the capitalist state (delineated above) in such a way that interesting insights can be drawn about the nature of state capitalism itself. For example, the view that the state is a neutral tool as posed by instrumentalists is rejected because state intervention is considered to be ‘form-determined’ by the structure of the state from which it emanates. Nevertheless, not all ground is ceded to the structuralists, with the state's need to perpetually favour the capitalist class (or one fraction of capital) over other social groups also rejected. Instead, those of a strategic-relational perspective perceive the capitalist state itself is a location of perpetual social struggle in which the structures of the capitalist state (and therefore the ‘form-determined’ nature of state intervention) can be altered.

This allows us to make links between the capitalist state and state capitalism. If ‘state power’ is indeed ‘revealed in the conjunctural efficacy of state interventions’, we can begin to conceptualize how state capitalism is a transformative process in which modes of capital accumulation can either be produced (i.e., new modes instituted) or reproduced (i.e., old modes reinstated, potentially in new forms), which we have sought to capture in our definition. Meanwhile, if those state interventions are merely the ‘form-determined condensation of the balance of political forces’, and if we accept (as per the strategic-relational view) that the capitalist state is a locale for social struggle in which the ‘balance of political forces’ needn't necessarily favour capitalists, then two observations can be drawn about state capitalism.

First, we might conceive how state capitalism needn't serve all capitalists within a state, but quite possibly benefit only the narrow interests of specific fractions of capital (i.e., financial) at the expense of another fraction (i.e., industrial). Furthermore, especially within democratic systems, state capitalism is unlikely to be underpinned by political support from merely one fraction of capital, but involve broader coalitions of interests including potentially non-capitalistic societal groups. In order to appeal to such broad-based ‘balance of political forces’, the possibility is opened up that state capitalism might involve many different types of intervention, such as economic (i.e., monetary) and public policy (i.e., housing policy) that do not commonly fall within the parameters of the term (Alami and Dixon, 2020: 84) potentially expanding the diversity of regimes that could be labelled as state capitalism.

Second, understanding state capitalism as a project that is the ‘form-determined condensation of the balance of political forces’ within the capitalist state strengthens our ability to periodize. This is because the act of discerning the ‘balance of political force’ that underpin projects of state capitalism becomes itself a mechanism for periodization, with the act of tracing the rise and fall in the various ‘balance of political forces’ towards whom state intervention is directed becoming a method for identifying projects of state capitalism. Alternatively, there might be periods in history that cannot sustain a coherent project of state capitalism with the capitalist state entering a period of interregnum.

One difference between our view of state capitalism, and the literature on the capitalist state, regards the nature of capital accumulation. Although it has become commonplace to acknowledge that the capitalist state, especially in its neoliberal guise, plays more than merely a nightwatchman role in the capitalist order (Demirovic, 2010), the literature still risks overlooking the state's role in making markets and sustaining accumulation by directly and deliberately substituting for aspects of the capitalist economy (see Berry, 2022 for an account of substitutive statism in the British context). In contrast, we place capital accumulation front and centre of our understanding of state capitalism, which in the British case has involved the use of state power that allowed financial capital to operate as an economic hegemon over other fractions of capital.

Market-making and internalizing external economic spaces, 1821–1914: Financial state capitalism 1.0

In this section, we explore the first iteration of British financial state capitalism. The multi-scalar nature of its activity, ranging from the domestic to the global, is emphasized. Here, we argue that the British state, in conjunction with the City of London, sought to structure world economic relations around Britain's dominant domestic mode of financial capital accumulation, with external space managed through empire, free trade and the gold standard. Indeed, such was the success of this financial state capitalist project that external economic spaces around the world were successfully internalized, with Britain becoming the epicentre of dense global networks of finance, trade and production (Magee and Thompson, 2010). We argue that this period of financial state capitalism in Britain can be periodized between 1821, when the balance of political forces was in favour of a return to the gold standard after the Napoleonic wars, and 1914, when the national interest in World War One superseded those of the rentier class. We contend therefore that Britain is an original exemplar of state capitalism in the world economic system.

Triumph in the Napoleonic wars left Britain in the early nineteenth century a world superpower with commercial and naval supremacy. Britain's victory in that titanic struggle, and the foundations of military and economic hegemony in the period ahead, rested on earlier institutional innovations associated with the British ‘fiscal-military’ state (Thompson, 2007). Prime among them was the creation of the Bank of England in 1694. The innovation of government bonds and the national debt not only facilitated the emergence of financial capital accumulation, but provided the British state with access to cheap credit and the means to deploy its finance as an instrument of war (Bordo and White, 1990). Military success extended the boundaries of empire and trade, with violence and coercion one aspect through which the British state propagated financial capital accumulation using its power to ‘make markets’ abroad for interests linked to the City of London. The concomitant rise of the bondholder within British society skewed the balance of power towards an emerging rentier class consisting of financiers and merchants, but also the landed aristocracy and professional class (employed in the military, Anglican church, civil service, and universities).

Reproduction of financial capital accumulation after the Napoleonic wars was not preordained, but rather the conscious result of a project of financial state capitalism. Defeat of the Napoleonic dynasty had required significant adaptation of the prevailing mode of finance-commerce capital accumulation. The fear of French invasion caused a run on the banks that led the Bank of England to suspend specie payments in February 1797, ensuring Sterling left the domestic gold standard it had been operating since 1717. This proved beneficial to the war effort with increases in the money supply supplementing the borrowing and taxing efforts of the British government (Duryea, 2010). Only ever envisaged as a temporary suspension to fulfil the exigencies of war, Kynaston (2017: 113, 142) and Ingham (1984: 92, 94, 106–107, 110) note how the impetus for the resumption of cash payments in 1821 came from the British state, and not the Bank of England or City of London. This is surprising given a strong motivation behind the return to the gold standard appears to have been the promotion of the latter as a global financial centre and commercial entrepot in the world economy (Hobsbawm, 1999: 214–215).

The return to gold is less remarkable if we accept that projects of state capitalism are merely a ‘form-determined condensation of the balance of political forces’. After the Napoleonic wars the balance of political forces still resided with the aforementioned rentier class. Tied together through the income they derived from their holding of government securities (Ferguson, 2004: 46), rentiers provided strong support for membership of a monetary system that protected the values of assets, something the gold standard offered through its prioritization of the stabilization of Sterling within a fixed exchange-rate as the guarantor of price stability in the domestic economy (Dewey, 1997: 84; Middleton, 2010: 240). Indeed, Rubenstein (1994: 140–9) persuasively sketches how financial capital accumulation benefitted this rentier class. Between 1809 and 1839 only 905 persons left an inheritance of more than £100,000. 43.2% of these were either financiers or merchants, 22.3% were landowners, 19.8% were in the professions or public administrations and only 9.8% were industrialists. This distribution of wealth created a strong economic impetus for the resurrection of financial state capitalism after 1815.

Financial state capitalism was abetted by the political power the rentier class wielded within the British political system. Members of parliament with direct links to the City of London, presumably supplying the private wealth to fight elections and fund the associated lifestyle, rose from 64 in 1832 to 200 by 1885, with the landed aristocracy dominating the British cabinet until 1895 before declining thereafter (Hobsbawm, 1994: 40). The rentier class were not only politically powerful, but were socially important as well. The financial class and landed aristocracy, for example, were increasingly socially enjoined in the nineteenth century through shared educational backgrounds, familial connections caused by inter-marriage and the social status still enjoyed by land ownership within British society (Alford, 1996: 21). Industrial capital, in the shape of northern manufacturers, was largely excluded from this political and social elite, although some conformist manufacturers did ascend to positions of political influence throughout the century (Dintenfass, 1992: 61–2). The rentier class would provide a strong basis of support for the vigorous use of state power in support of financial capital accumulation (including when such actions were to the detriment of accumulation by industrial capital).

State power was employed in the propagation of financial capital accumulation via the unusual confluence of macroeconomic and commercial policy (something we refer to as financialized industrial policy) and British imperialism. Central to financial state capitalism was economic management in the pursuit of ‘sound money’ provided in the symbiotic relationship between the City, Bank and Treasury (Ingham, 1984). The macroeconomic element of the ‘anti-collectivist temple’ (Checkland, 1983) of nineteenth century British economic policy, consisting of the Bank of England's management of the gold standard, and the Treasury's proclivity for balanced budget and reduction of the national debt, served to elevate Sterling as the international reserve currency of the world economic system. Legally a private institution, the Bank of England's biographer described the institution by the nineteenth century as one of the ‘great engine[s] of state’ (Kynaston, 2017: Chap. 2), rapidly assuming the public functions of a modern central bank, including that of ‘lender of last resort’ to the financial sector (Capie and Wood, 1994: 230–232).

Whilst obviously fulfilling an objective for economic stabilization, these macroeconomic policies were far from neutral. Indeed, in their embodiment of the principle of ‘sound money’ as the practical basis for capitalist expansion, they were deployed at the vanguard of financial state capitalism. For instance, the global role for Sterling, supported by the macroeconomic policy implemented by the British state, aided the expansion of the insurance and shipping services provided by the City to expedite international trade (Gamble, 1994: 128–129), turning the City into an ‘international clearing house’ for global economic activity (Ingham, 1984: 82). Indeed, it was through these macroeconomic policies that the ‘basic conditions for the City's international activities… [were] embodied in the practices of the state’ (Ingham, 1984: 131), thus delivering significant support for financial capital accumulation.

Illustrative of how financial capital accumulation was hard-wired into macroeconomic management by the British state was the operation of the gold standard. Far from being the autonomous method of monetary adjustment its proponents often claimed, by maintaining the Sterling's role as international reserve currency, the gold standard was a discretionary monetary policy used by the Bank of England to intervene and restructure world economic relations around Britain's dominant mode of financial capital accumulation. Here, the Bank of England used the combination of bank rate and open-market operations to manipulate external economic space through short-term interest-rates by altering the attractiveness of the City (internal economic space) as a repository for international capital (Ford, 1981; McCloskey and Zecher, 1981; Whale, 1937). The Bank of England ably assisted in this endeavour after been granted exclusive control over note issue (linked to the gold reserves) in Britain and monopoly status in the domestic banking sector in the 1844 Bank Charter. The City's domination of global financial markets was assisted by the Bank of England's manipulation of external economic space through the gold standard.

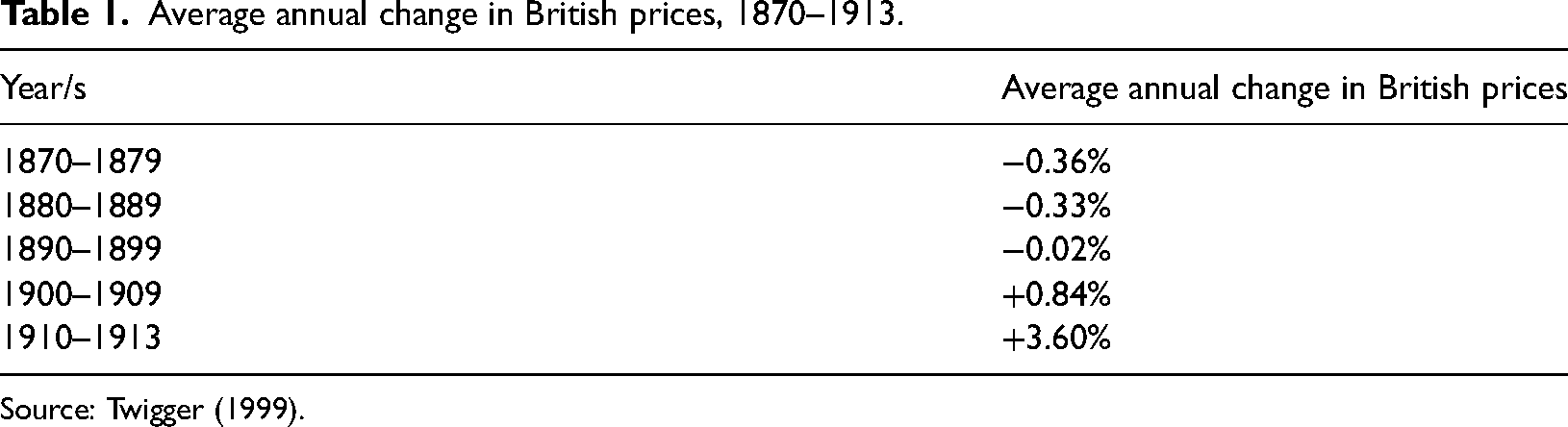

Indeed, Table 1 documents the Bank of England's success in manipulating external monetary space between 1870–1913 in the achievement of domestic price stability. Almost certainly operating to the detriment of industrial capital, the high interest rates often required to achieve this price stability were not conceived as such by the Bank of England, Treasury, or City of London in the period. Instead, it was through its anti-inflationary credentials these institutions could conceive the gold standard as a domestic employment policy (Sayers, 1970: 88–91). Price stability, both in terms of domestic prices and international currencies, considered the key to orderly market exchange that would efficiently allocate resources and deliver the full employment of labour (elites of the nineteenth century undoubtedly viewed the domestic economy according to neoclassical economic theory as a self-regulatory economic system) (Glynn and Booth, 1983: 348, 1996: 134). Unemployment that did occur was attributed to institutions, such as welfare programmes or trade unions, which hindered market exchange (Pigou, 1913). The period covered in Table 1 is commonly described as the international or classical period, during which discretionary operation of the gold standard sometimes, if not always, meant the British economy avoided international deflationary pressures. The deep and liquid financial markets of the City of London allowing the Bank ‘to shift much of the pain of [monetary] adjustment on to other countries’ (Sayers, 1970: 92; see also Tomlinson, 1990: 17).

Average annual change in British prices, 1870–1913.

Source: Twigger (1999).

In the century before our case study begins, Britain's industrialization had been facilitated by protectionist trade policies (bound up with management of its ‘first’, eighteenth-century empire), as well as the kind of industrial policies that would later be perfected elsewhere (Bairoch, 1993; Chang, 2002). Britain may have pioneered the conventional ‘developmental’ state in this period, but as the nineteenth century progressed it gave way to a different kind of state capitalism aligned with free trade, which empowered landed elites ahead of industrialists as Britain externalized its financial and industrial leadership. The landed elite of course profited from industrialization – the divide between financial and non-financial interests should not be over-stated – but free trade and empire were critical in allowing capital accumulation to proceed in a way that did not uproot British political economy, especially its class system, beyond recognition.

Indicative of this was the considerable support for free-trade that aligned the interests of both financial and industrial capital (Booth, 2001). Indeed, the turn towards free trade had a more significant impact on another element of the rentier class: the landed aristocracy. Alongside technological advances, such as the steamship and refrigeration, British capital exports were responsible for building the railways that enabled agricultural imports to flood into Britain under its free trade regime. No longer able to enjoy the agricultural rents that had once sustained them, the more astute among the landed aristocracy financialized their income by diversifying their activities into real-estate development, land-lease to industry, and overseas investment (Pollard, 1994: 76), thus retaining their economic and social power as part of the rentier class. Their political position, meanwhile, was protected by the ever-astute leadership of Disraeli at the helm of the Conservative party.

Much like the restoration of the gold standard then, the institution of free trade could be pursued, and its impacts managed, in a way that preserved ‘the balance of political forces’ in the rentier class. It was also further an attempt to ‘make markets’ that would preserve British economic superiority, an endeavour wholly in keeping with British state policy since the seventeenth century to enhance and facilitate the commercial opportunities available to its corporations and entrepreneurs (Gamble, 1994: 50, 55–57). Free trade was pursued in the context of the competitive advantages in manufacturing production derived from Britain's status as the world's only industrial and urbanized economy, something that protectionism in the global economy threatened. It offered the British state another opportunity to manage external economic space bringing ever more international markets into the orbit of British exports of goods, services and capital. Starting in the 1846 repeal of the Corn Laws, Britain, then the world's largest market for imports was systematically opened up drawing other countries into the world economic system through their exports. In turn, as Britain became the global hub of trade, more and more countries were brought under the influence of the gold standard; cementing the City of London's position as the centre of global finance and creating demand for its commercial services (Harley, 1994: 317–318). Consequently, we conceive of the gold standard and free trade as forms of financialized industrial policy.

Where countries were not willing to accept the benefits of free trade and international movement of finance, imperialism was another policy intervention through which external economic space was managed by the British state. Empire an important policy to ‘make markets’ for financial and commercial interests in accordance with free trade (Darwin, 2013). Perhaps the most egregious example in the nineteenth century were the wars fought with China in order to keep its economy open to imports of opium from British India. The British state also continued the practice of ‘making markets’ via the use of ‘Royal Charter’ (granted among others to Cecil Rhodes’ British South Africa Company in October 1889), partially underwriting the entrepreneurial risk undertaken by private multinational corporations by offering monopoly status in conquered (or soon to be conquered) markets.

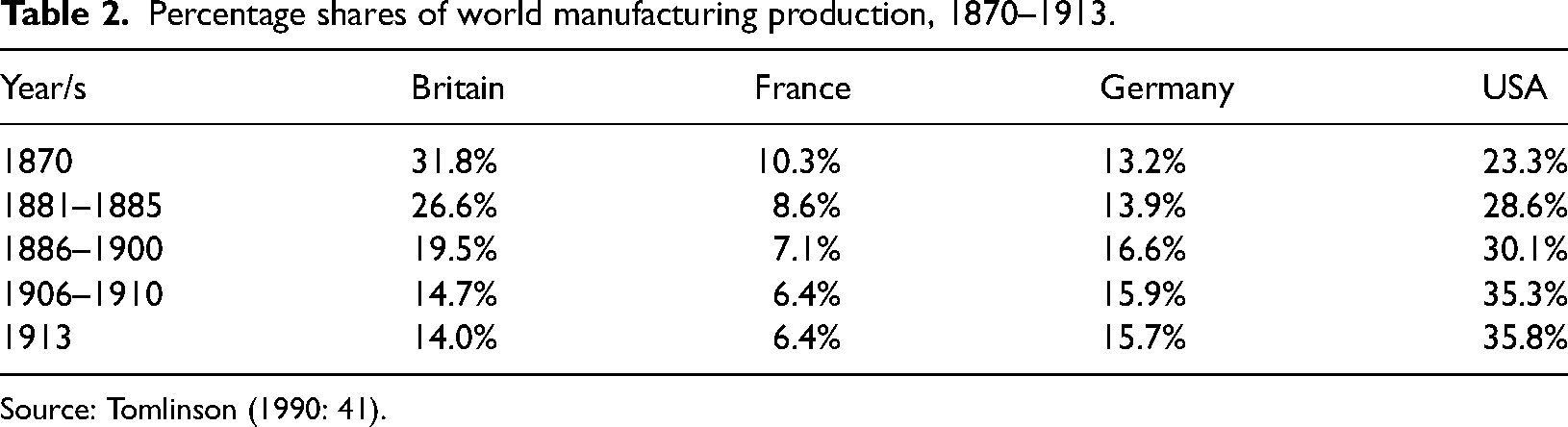

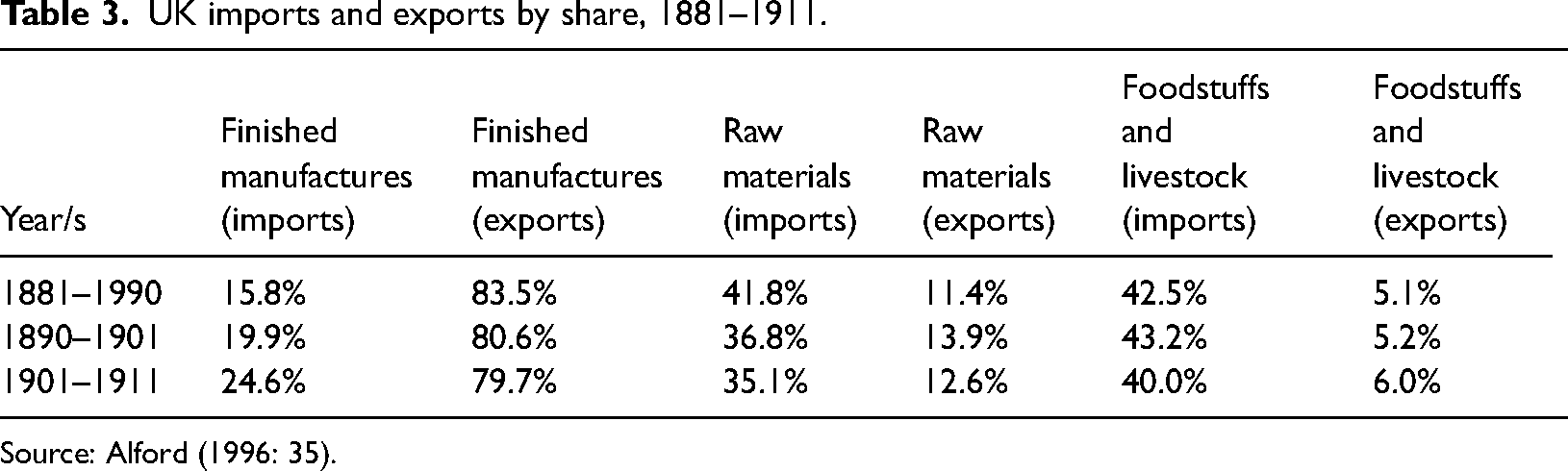

Britain's zenith as workshop of the world was not to last. The great depression of 1873 to 1896 placed British-led economic globalization under strain, with many countries erecting protectionist barriers to stimulate industrial development and protect agricultural producers. The effect of industrial competition is shown in Table 2 with Britain's percentage of world manufacturing production declining significantly under competitive challenge from Germany and the United States. Britain's dominance of international trade in the nineteenth century had rested on its ability to import raw materials and food and export finished manufactures but, as Table 3 demonstrates, Britain's decline in industrial competitiveness undermined the basis of this beneficent exchange of global capitalist production. Between 1881–1890 and 1901–1911 imports of raw materials and foodstuffs and livestock waned, whilst imports of finished manufactures into Britain amplified.

Percentage shares of world manufacturing production, 1870–1913.

Source: Tomlinson (1990: 41).

UK imports and exports by share, 1881–1911.

Source: Alford (1996: 35).

The later nineteenth century thus saw financial state capitalism come under significant strain, with Britain's manufacturing trade coming under significant competitive pressures. In these circumstances, however, financial capital became ever more critical in Britain's accumulation strategy rather than less. Growing deficits in the balance of payments from trade in goods (the visible balance) only overcome through expanding surpluses on service exports alongside returns from overseas investment (the invisible balance) (Booth, 2001: 55). The City of London was critical to this increasingly financialized balance of payments. Capital flows overseas rose from the equivalent of 7% of national wealth in 1850, to 14% in 1870, to approximately 32% in 1913. The destination of British capital exports also evolved; Europe was replaced as the main recipient of British capital export, with 34% flowing to North America between 1865 to 1914, 17% to South America, 14% to Asia, 13% to Europe, 11% to Australasia and 11% to Africa. The largest single national recipient over these years were the United States (20%), but the rest could be found in formal (dominions and colonies) or informal (countries where Britain exerted significant diplomatic influence) empire including Canada and Newfoundland (13.7%), India and Ceylon (10%), South Africa (9.8%), Australia (9.4%), Argentina (8.5%) and Brazil (3.9%). An estimated 70–80% of this capital export was portfolio investment, thereby fulfilling the requirements of the domestic rentier class for income, with the rest made up of direct investment in the activities of multinational corporations and social projects, such as railways and telecommunication systems (Edelstein, 1994: 173–179).

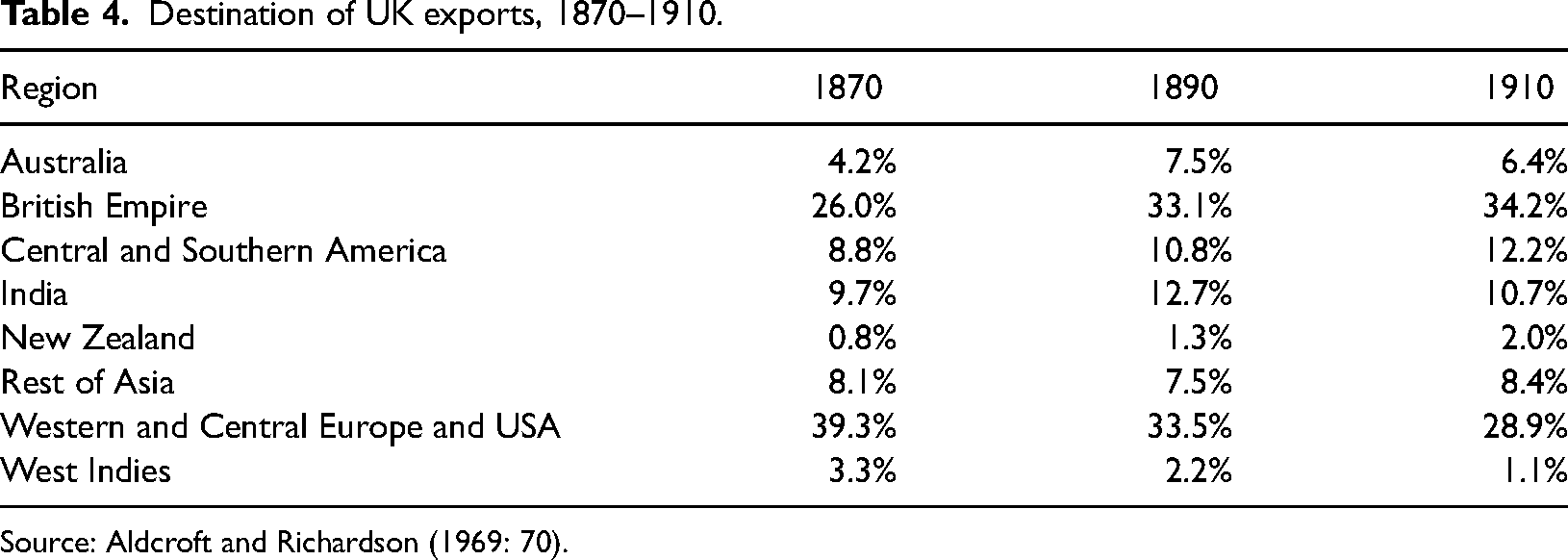

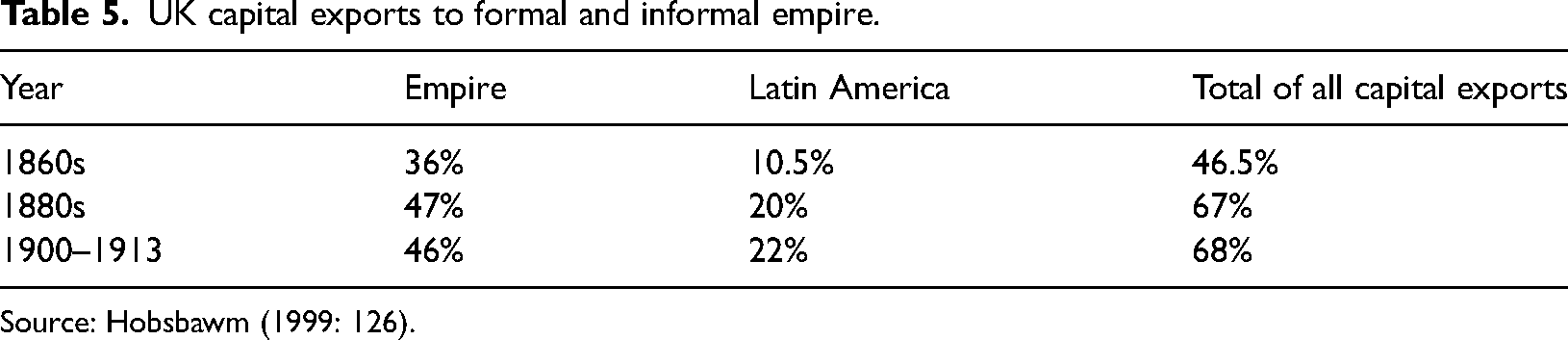

Much like in the aftermath of the Napoleonic war then, the response to economic dislocation and turbulence was to reproduce, rather than replace, financial capital accumulation. This is explicable if we consider the underlying political and economic power of the dominant rentier class and its relationship to empire. Table 4 documents the strengthening role of empire as a location for British exports. A similar drift was mirrored in Britain's overseas investment as revealed in Table 5 with formal and informal empire accounting for 68% of all Britain's capital exports between 1900–13, rising from 46.5% in the 1860s. Whilst the overall gain to public welfare from the empire was most likely minimal, it was of enormous benefit to those industries of importance to the rentier class, such as banking and insurance, shipping, cotton and iron and steel. Empire provided an outlet by which the rentier class could avoid the competitive pressures of the later nineteenth century afflicting industrial capital. In turn, the coalition of interests involved in the rentier class remained unified and were successfully able to fend off challenges to the economic status quo such as the call for tariff reform by Joseph Chamberlain.

Destination of UK exports, 1870–1910.

Source: Aldcroft and Richardson (1969: 70).

UK capital exports to formal and informal empire.

Source: Hobsbawm (1999: 126).

Market-making and externalising internal economic space, 1958–2016: Financial state capitalism 2.0

In this section, we consider what we believe to be the second iteration of financial state capitalism in Britain. In this epoch, we again emphasize the multi-scalar nature of its operation, but in a reversal of the economic geography of earlier financial state capitalism, state power was directed at restructuring internal space by ‘making markets’ for the forces of international finance. This was no more evident than in the transformation of the City of London itself, which was reshaped by the British state as the locale of choice for financial multinational conglomerates. In pursuing this form of financial state capitalism, the economic space inhabited by individual British citizens was also fundamentally reordered. We suggest that an appropriate periodization for this later episode of financial state capitalism in Britain is between 1958 and 2016. The opening date chosen because a coalition of interests began the unravelling of the post-war consensus in economic policy, a turn in British political economy that was solidified in the election of Margaret Thatcher and the Conservative party. The latter date chosen to coincide with the vote for Brexit in the EU referendum which has clearly disrupted the operation of financial state capitalism and triggered a set of major dilemmas in British political economy that have yet to be resolved. In delineating another case study of financial state capitalism in Britain, we hope to strengthen our argument for why Britain should be considered among the diversity of state capitalist regimes.

Britain ended the Second World War in a perilous financial position. Under instruction of the financial agreement signed with the United States, the Labour government, led by Clement Atlee, attempted to restore the convertibility of the Sterling in 1947. The results were disastrous. Gold fled the Bank of England's vaults at an alarming rate, with the decision being overturned within weeks.

1947 represented therefore an important year, if not instrumental like 1958, for two reasons. First, it marked an opening attempt in what would become the hallmark of financial state capitalism 2.0; a willingness on the part of the British state to use its agency to restructure internal economic spaces and ‘make markets’ for international financial capital. Indeed, although the attempt at convertibility was ultimately unsuccessful, other efforts were taken in 1947 to restore the City as a global financial powerhouse through attracting international financial capital, such as when the Bank of England actively encouraged the formation of the Foreign Banks Association in the City, consisting of the Bank of China, Credit Lyonnais, and the Swiss Bank Corporation (Kynaston, 2001: 20). Attempts to ‘make markets’ in the City for international capital was maintained throughout the 1950s, with a number of foreign exchange and commodity markets re-opened and the deregulation of futures dealing in gold bullion to fend off competitive challenge in this market from Zurich (Kynaston, 2001: 101, 236). It was not until 1958, however, that the Sterling became a freely convertible currency once more, both ‘symbolically and substantively, a sign of the City's determination to reassert itself as an international financial center’ (Kynaston, 2001: 105).

These consistent efforts to introduce financialized industrial policy between 1947 and 1958 are important because they indicate the political interests within (Bank of England) and without (City of London) the British state willing to agitate almost immediately after the end of the Second World War for a return to financial state capitalism. Whilst the balance of political forces might not have turned drastically in their favour until the 1970s, they were able to secure significant concessions for the City of London that undermined attempts to institute alternative state capitalist projects for the benefit of industrial capital. This achievement was delineated in the conjunctural inefficiencies of post-war British economic policy until at least the 1970s. The vision of a national capitalist project (Edgerton, 2019: 253–359) consisting regularly coming into conflict with those, both within and without the British state, who had no desire to jettison the external economic policies (Gamble, 1994: 143–144) that prioritized Sterling as an international reserve currency and protected the role of the City of London in global financial markets. The first project necessitated Keynesian demand management and industrial modernization delivered by state-led intervention requiring the consistent deployment of public expenditure. The latter dictated a periodic retrenchment in government spending and a restriction in credit conditions to dampen inflation and ensure ‘sound money’. Internal and external economic policy were not in alignment and the result was an economy blighted by ‘stop-go’ crises in which economic recessions were followed by economic booms.

1958 is consequently a pivotal year because Sterling convertibility was the first step in setting the City free from domestic financial control. It also indicated that the priorities of financial capital were elevated above its industrial counterparts as higher interest rates were deployed to promote a strong currency that choked the competitiveness of British manufacturing (Booth, 1995: 140–143). This undermined the efficacy of Keynesian demand management, but ensured that the City could attract flows of international short-term capital and strengthen its contribution through the invisible earnings it made to the balance of payments.

Sterling's convertibility also put the City in a good position to take advantage of the emergence of the Eurodollar and Eurobond markets, which the City increasingly came to dominate. Far from being an innovation springing solely and spontaneously from the fertile minds of the City's bankers, the emergence reflected ‘a conscious act of policy by the Bank of England’ (Moran, 1991: 55–56), which had by now been nationalized. By essentially turning a blind-eye to the illegalities of the Eurodollar markets in an era of ‘embedded liberalism’ (Ruggie, 1982), the Bank of England reflected a desire to reestablish London as the world's preeminent international financial centre (Helleiner, 1994). In effect, the Bank of England's failure to enact its regulatory responsibilities ‘made markets’ with internal economic space in the City of London externalized for use by international capital. Rising from 53 (12 US) in the 1950s, the number of foreign banks located in the City of London after the emergence of the Eurodollar markets rose to 77 (15 US) in 1960 to 255 (61 US) in 1980 (Pollard, 1994: 335–336).

When Britain transitioned to a floating exchange rate in 1972, the delusion that the City of London's international competitiveness rested on Sterling's reserve currency status, a mainstay of thinking by those domestic interests who wished for a return to financial state capitalism was exposed. The Health government (1970–1974) focused on securing entry to the European Economic Community (EEC), which was seen as necessary to step to alleviate Britain's post-war economic decline by offering access to European markets to offset those lost in the British empire's disintegration (Booth, 2001: 79). Joining the EEC increased opportunity to trade in goods and services (including financial services) (Thompson, 2017a: 215). By offering tariff-free access to European markets, entry to the EEC also cemented post-war trends in foreign direct investment making Britain an even more attractive proposition for American and Japanese multinationals, including those flowing into the City of London (Booth, 2001: 84; Pollard, 1994: 309). Entry to the EEC was consequently another example by which the British state sought to externalize internal economic space by ‘making markets’ for the benefit of international capital. The Thatcher governments would later play an important role in the creation of a European single market to cement the competitive advantages of the City of London in Europe (Thatcher, 1988).

The turbulent decade of the 1970s saw the balance of political forces swing further in favour of a new state capitalist project based on finance. For example, the introduction of Competition and Credit Control by the Bank of England in 1971 (Copley, 2017) can be seen as in important milestone in the financialization of the British economy. With trust in the efficacy of capital accumulation under Keynesianism beginning to wane, the Treasury became willing to engage in the Bank of England's policy experimentation in the hope that financial capital might become a new engine of domestic economic growth. Free from post-war monetary controls, the British banking system engaged in an orgy of lending directed increasingly towards the property and financial sectors, which quadrupled to £6.4billion; a quantity of lending significantly more than that delivered to manufacturing (Reid, 2003: 43–67), which subsequently led to a housing boom and secondary banking crisis.

The evolution of macroeconomic policy in the 1970s is further evidenced in the political momentum provided towards a new era of financial state capitalism in Britain. Starting in the 1976 IMF crisis (Keegan and Pennant-Rea, 1979: 131–136) and lasting until the implementation of significant austerity in the public finances by the Conservative-Liberal government between 2010 and 2015 to placate international bondholders (Lee, 2011), the confidence and credibility of financial markets became a sine qua non of British economic policymaking; signifying a reassertion of the City's historical structural power within British capitalism (Strange, 1994). Keynesian approaches to demand management had always been implemented in a somewhat half-hearted fashion by the British state, with taxation (as opposed to public expenditure) favoured to curtail inflation and promote economic growth and employment (Matthews, 1968). Even this, however, was effectively abandoned in Denis Healey's 1975 Labour party conference speech (Jessop, 2017: 135). In place of Keynesianism, the British state experimented with a number of rule-based regimes for macroeconomic policy which targeted financial variables in the defeat of inflation; finally settling on the inflation target system administered by an independent Bank of England. Much like the gold standard, these macroeconomic strategies fulfilled priorities for economic stabilization, but in the prioritization of price stability as the only basis for which economic growth might proceed, these macroeconomic policies also sustained a financial accumulation regime.

Evolution towards financial state capitalism in the post-war era was accelerated into full-blown revolution via the election victory of the Conservative party in 1979. Expertly summarized in Gamble’s (1988, 1994: 147–156) aphorism, Britain's ‘strong state’ would now be vigorously directed to ‘free the economy’. An important element of this economic strategy was to reintegrate the British and global economies, with state agency used to externalize internal economic space by ‘making markets’ for penetration by international capital. Here, financialized industrial policy consisted of privatization, denationalization, liberalization, and the outsourcing of public services (Riddell, 1991: Chap. 5). For instance, the increasing trend towards privatization through contracting-out gave rise to a new breed of multinational corporation in the form of Serco, G4S and Capita, with public procurement policy also becoming a component of financialized industrial policy (Mabbett, 2018). Much like how the externalization of the City of London led to an influx of international capital in the form of multinational financial institutions, the contracting-out of public services led to an influx of foreign capital to operate Britain's infrastructure. This was often from European state-owned enterprises of the type that British governments effected to despise (Meek, 2015).

Elsewhere, industrial policies were aimed at the reduction of state intervention in the economy (such as those to achieve the diminution of the role of trade unions) and those to boost international competitiveness. In regard to the latter, these industrial policies typically sought to make the British economy a generally more hospitable location for international capital. Meanwhile, macroeconomic policy continued its trajectory towards financialization, deployed in service of the objective of price stability. This joint approach to economic policy provided the fundamental framework for the Major and New Labour governments thereafter, with industrial policy under these governments aiming to improve the capabilities of domestic companies to compete in international markets (Crafts, 2007) whilst also promoting Britain as a location for international capital. This industrial policy framework survived the 2008 financial crisis with the Conservative-Liberal Coalition government, despite a lukewarm flirtation with more conventional industrial policy, thus developing its growth strategy around the principles of deregulation and tax cuts (Berry, 2016).

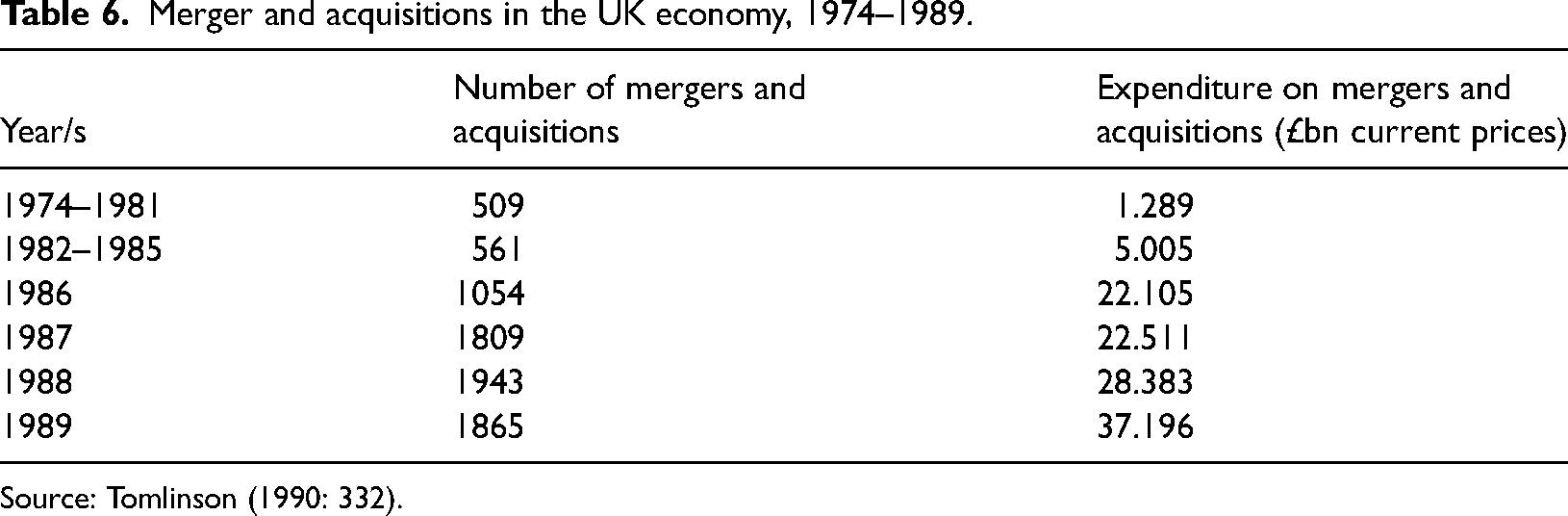

Further examples of financialized industrial policy after 1979 abound, but none more so than those directed towards the financial services. Controls on foreign exchange were completely abolished just four months after the Conservative's election victory. The City came to dominate a third of the global foreign exchange market, with turnover rising from $25billion in 1979 to $90billion in 1985 (Kynaston, 2001: 664–665). The City also became a significant actor in the international futures and options market, which opened in 1982. This was followed by the Big Bang of 1986, which liberalized entry to the London Stock Exchange (LSE) and prompted a wave of mergers and acquisitions of existing City firms by their international competitors, as shown in Table 6. By 2021, the City of London (2021) claimed that 51% of investors in companies listed on the LSE were international, that the LSE listed 574 international companies (more than any other stock exchange), and 12.4% of all foreign companies listed globally were located in London. Elsewhere, the City handled $2.73trillion of foreign exchange business, more than New York, Hong Kong, Tokyo and Singapore combined, and dominated 70% of all business in the secondary market for international bonds. Other industrial interventions directed towards the City of London to improve its international competitiveness included grand infrastructure projects (Willets, 2017) and the provision of a new ‘light-touch’ regulatory regime (Moran, 1991). The centrality of financial services to Britain's accumulation strategy was exposed in the 2008 global financial crisis, when the British state stepped in to rescue ailing financial companies with a taxpayer bailout and guarantees worth £1.162 trillion at its peak level (National Audit Office, 2011).

Merger and acquisitions in the UK economy, 1974–1989.

Source: Tomlinson (1990: 332).

State agency was also used to promote the financialization of the British economy through other means, such as the 1980 Housing Act which introduced the ‘right to buy’ council homes (Kirkland, 2015) and the 1986 Building Societies Act (Boddy, 1989) which allowed building societies to offer a range of comparable services to banks. Through these policies the everyday experience of individual British citizens was irrevocably financialized. Policies such as ‘Right to Buy’ and the 1986 Building Societies Act contributed to the explosion in personal household debt, which rose from £16billion in 1980 to £47billion in 1989; with mortgage debt rising from £42billion to £235billion over the same period. In total, household debt rose to 62% of British GDP in 1989 from 29% in 1980 (Pugh, 2008: 347). Far from the economic miracle lauded by the Thatcher government, economic recovery in the 1980s was built on a consumer boom paid for by credit cards and overdrafts. Economic growth was further supported by consumer booms fueled by debt in the 2000s and 2010s, meaning that by 2016 household debt in Britain stood at 127% of income (Harari, 2018). Critically, the new financialized realities of everyday experience of many British citizens created a ‘political force’ in the shape of homeowners and consumers in favour for financial state capitalism.

Another ‘political force’ formed by, and in favour of, financial state capitalism was an emerging managerial class. Prior to 1979, the highest 20% of wage earners secured 37% of all income after tax. The poorest 20%, in comparison, secured only 9.5%. By 1988, these proportions had widened to 44% and 6.4%, respectively (Pugh, 2008: 351–352). This was driven in large part by significant wage increases among senior managers in the private sector, including the newly privatized industries, which rose by 250% between 1979 and 1988 (Dunn and Smith, 1990: 41). This trend continued in later decades. The average total pay of Chief Executive Officers (CEO) of FTSE 100 companies rose 13.6% per year between 1998 and 2010, from £1million to £4.2million (Petrin, 2015: 3). By 2018, average CEO pay has risen to £4.7million per annum (CIPD, 2020: 5).

Nevertheless, despite these sources of domestic support, financial state capitalism was not a national project been very much to the benefit of the forces of international financial capital. An illustration of this phenomena is shown in the distribution of the proceeds of privatization, where attempts to create a ‘share-owning democracy’ have been illusory. By 2018, 54.9% of all UK quoted shares were held by foreign institutions and individuals, with only 13.5% held by British-based individuals, 9.6% by unit trusts and 8.1% by other financial institutions (ONS, 2020).

Elsewhere, material reward distributed by financial state capitalism is even more explicit. Bell and Van Reenen (2014) estimate that between 1999 and 2014 around 66% to 75% of all total income gain by the wealthiest 1% of the British population went to those working in the financial sector. This included a recovery in pay after the global financial crisis that saw banker's wages (not including bonuses) rise above their pre-crisis peak by 2011; a recovery of wages that would allude the average worker in Britain until February 2020 (BBC News, 2020).

Meanwhile, industrial capital was very much excluded from the privileged interest and social groups favoured by financial state capitalism in this period. Even so, manufacturing decline in the post-war period cannot simply be associated with the financialization of the British economy. A series of domestic problems, including poor or outdated managements practices, under-investment in innovation and competition from countries such as Germany, the United States and Japan (Elbaum and Lazonick, 1986) all contributed to the waning political power of industrial capital. Of course, these issues cannot be easily disentangled from the operations of financial state capitalism. The unwillingness of British financial institutions to invest in manufacturing was undoubtedly a contributory factor in Britain's post-war manufacturing decline. Elsewhere, empire, whose colonies continued to provide ‘captive’ markets for manufacturing exports, allowed elites in the early post-war period to evade more radical experiments to secure domestic industrial modernization and helped, at least for a time, to mask Britain's industrial decline relative to its competitors (Silverwood and Woodward, 2022; Williams, Williams and Thomas, 1979).

The well-documented failures and limitations of British industrial policy in this period are also part of this story (Chang and Andreoni, 2020). Yet, it would be incorrect to say that conventional industrial policies were entirely absent, even as neoliberalism was ostensibly embraced by elites after 1979 (Woodward and Silverwood, 2022). Instead, as we have sought to show in this section, these conventional industrial policies were increasingly directed to secure competitive advantages for financial capital (Silverwood and Woodward, 2018). Moreover, Britain increasingly pursued aggressive trade policies via the World Trade Organisation, including the Trade-Related Aspects of Intellectual Property Rights agreement (TRIPs), which benefited the international operations of key manufacturing industries like pharmaceuticals (Chang and Andreoni, 2020). It is also necessary to acknowledge that, firstly, trade policies that benefited financial services (such as the General Agreement on Trade in Services) were probably higher priorities, and secondly, that the interests of industries such as pharmaceuticals were shared by the financial institutions and investors which had facilitated stock market flotations and M&A activity. Consequently, trade policy under financial state capitalism, much like during its earlier variant in the nineteenth century, was financialized. The promotion of both manufacturing and service industries within international markets via trade policy should not in any meaningful sense be understood as the promotion of a set of ‘national champions’, but rather as a further example in which the British state externalized internal economic space for the benefit of international financial capital. Although ostensibly in the service of British firms, trade policy under financial state capitalism in this period served a management and ownership class that was increasingly dominated by international capital.

Conclusion

The primary contribution of our paper has been to outline the contours of what we consider to be a financial state capitalism in Britain across two historical periods. In so doing, we have sought to consider how the British case relates to the existing body of literature on state capitalism in four key areas.

First, is our observation that the British experience invites us to consider the spatiality of state capitalism. A methodologically nationalist approach does not help us to understand the nature of financial state capitalism, even with the transnational turn in scholarship on state capitalism overlooking the inherently transnational nature of some state capitalist regimes. The elite interests shaping the state/capitalism relationship in Britain are not aligned with those of the nation (as economy or society) in general. They have used the state to gain access to overseas opportunities for accumulation, with the state often occupied or significantly influenced by overseas actors in alignment with British elites. Similarly, domestic economic space has been remodelled in service of transnational elites. In this account, national sovereignty is not a foundational feature of state capitalism, but rather a tool of state capitalism. It should be problematized as well as recognized in the literature. Our analysis contributes therefore to scholarship investigating the wider spatial relations of state capitalism (Dixon, 2017; Eagleton-Pierce, 2022; Kurlantzick, 2016).

Second, there remains a tendency in the literature to view state capitalism as a phenomenon related principally to ‘catch up’ capitalist development in emerging or transitional countries. By relocating state capitalism to what we believe is its origins in the capitalist economy of Britain between 1821 and 1914, and then observing a later period of state capitalism in Britain between 1958 and 2016, we hope to have avoided that trap – and thus contributed to a broader literature on the role of the state in capitalist development in already-developed economies (Chang, 2002; Cohen and DeLong, 2016; Reinert, 2008).

Third, having developed the notion of ‘financial state capitalism’ to distinguish the model of state capitalism that has tended to prevail in Britain, we hope to have persuasively contributed in a practical sense to expanding the diversity of regimes considered as state capitalist. Financial state capitalism, centred on the financial sector's operations both domestically and overseas, was shaped profoundly by the actions of the state, from central banking to imperial conquest. A financialized model of state capitalism could, in a simplistic sense, be seen as a counter-example to the general focus on industrialization (specifically, the protection and promotion of manufacturing and extractive industries) in the state capitalism literature. At the same time, it contributes to a broader literature on financialization which, to date, has not adequately conceptualized the relationship between state and finance sector power (Berry et al., 2022; Davis and Walsh, 2016; Eagleton-Pierce, 2022; Schwan et al., 2021; Van Der Zwan 2014). Nonetheless, our objective is not to suggest that financial state capitalism is an alternative to conventional state capitalism, but rather an analytical concept that helps us to understand how the British economy developed the way it has.

Fourth, the British case illuminates an approach to the appropriate periodization of state capitalism (Alami and Dixon, 2020). There is a tendency in some studies on British economic history to assume that economic elites, predominantly associated with the financial sector, have ‘captured’ state powers or at least ‘occupied’ state institutions. In reality, the British state has developed around the entrenchment of key economic interests (Ingham, 1984). Although always retaining enough power to limit available options for economic reform, notably in the post-war era when efforts to restore financial state capitalism in Britain undermined efforts to secure industrial modernization through Keynesianism, this has not meant those interests have always been represented in a coherent project of state capitalism. Our analysis therefore contributes to recent debates on the deliberateness of state support for finance in British economic development (Anderson, 2021; Edgerton, 2019).

There have of course been periods of interregnum in British economic history when the country has had no discernible project of state capitalism. This underscores our decision to conceive of state capitalism, akin to relational approaches to the capitalist state, as a form of ‘state power… revealed in the conjunctural efficacy of state interventions… [themselves] a form-determined condensation of the balance of political forces’ (Jessop, 1983: 6). When the balance of political forces have aligned behind financial state capitalism in Britain, these have brought with it radical and transformative policy changes that challenge economic elites whilst sustaining financialization more generally.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.