Abstract

In the past four decades, the UK welfare state has been continuously reduced while asset ownership has gained in importance. Rather than relying on publicly funded welfare when not working, individuals are expected to mitigate future risks such as ill health, unemployment or old-age poverty through accumulating assets. Previous research employing a Foucauldian governmentality framework has explored how these norms of asset accumulation come into being through institutional changes and discourses. Documenting the narratives and practices of 60 UK individuals and bringing in an understanding of resistance being immanent in power technologies, the author sets out two key contributions to the everyday financialisation literature. First, this paper is the first study to conceptualise differential financial discourses and practices as distinct subject positions within the realms of financialisation. Due to feeling ‘trapped’ in having to provide financial security themselves, governable subjects amend asset norms to their own needs. Five subject positions emerged from the complex interplay between norms of conduct and counter-conduct. Second, these variegated financial subjectivities and practices are, it is argued, not only deviating from a theorised investor subject but are also necessary for everyday financialisation to take place. Counter-conduct helps to smoothen ambiguities inherent in norms of conduct, enabling asset accumulation and reinforcing a welfare system based on individual responsibility.

Introduction

As part of a neoliberal turn at the end of the 1970s, the focus of the UK government has shifted away from believing in public insurance provisions for future risks such as income shortfalls due to ill health, unemployment or retirement and moved towards an emphasis on personal responsibility. In line with this belief, the welfare state has been continuously dismantled through a reduction in sickness pay, unemployment benefits and state pensions and greater access to savings and investment products have been offered as a mitigation of future risks, by means of accumulating assets instead of relying on income support by the government (Hillig, 2019a; Langley, 2008). This transformation of society ‘requires […] new identities and forms of calculation from its citizens’ (Froud et al., 2007: 340), calling upon households to internalise the subject position of the everyday investor. An everyday investor aims to earn returns in financial markets and accumulates assets guided by finance rationality, defined as embracing risk willingly and adopting financial strategies such as diversification (Langley, 2007; Martin, 2002).

Inquiries into financialised subjects have been particularly influenced by a Foucauldian governmentality framework (Aitken, 2003; French and Kneale, 2009; Langley, 2008), revealing how mechanisms of governance construct the subject of the everyday investor. Although these studies have contributed substantially to the understanding of everyday financialisation, the notion by the majority of Foucauldian-inspired studies is that institutional changes and discourses translate into conduct (Maman and Rosenhek, 2019; Mulcahy, 2017). Even when acknowledging ambiguities inherent in the investor subject, the focus lies on showing deviations from it. In other words, individuals are seen as either adopting the investor subjectivity, that means building a ‘portfolio of financial market assets’ (Langley, 2007: 74), or ‘pushing back the frontiers of what it means to be an investor’ (Langley, 2007: 81) by investing in property or saving. That a study of differential in place of deviant subjectivities is an important endeavour to undertake can be seen in previous research, which has revealed that property investments and savings are part of a financialised subject position operating as power technology, albeit differently interpreted than theoretically inferred (Hillig, 2019b). For the purpose of ‘afford[ing] subjects a greater degree of agency to determine their own identity’ (Coppock, 2013: 496), a recently growing strand within the everyday financialisation literature has raised awareness of this contingency in financial subject formation and highlighted with the help of qualitative research how emotions, relationships and different temporalities intervene with the investor subject (Lai, 2017; Pellandini-Simanyi et al., 2015; Samec, 2018). Yet, despite calling ‘for variegated subjectivities rather than just financialised or non-financialised subjects’ (Lai, 2017: 914), these studies stop short of a resultant development into distinct financial subject positions. 1 Instead, emphasis is placed on exploring how financialisation unfolds in everyday practices by identifying ‘which aspects of it [the ideal financialised subjectivity] are embraced and which are rejected’ (Pellandini-Simanyi and Banai, 2020: 787).

I, therefore, seek to address the identified gap in the literature by giving insights into how diverse forms of resistance configure varied financial subject positions. Drawing on semi-structured interviews with 60 individuals conducted between 2016 and 2017, the study substantiates two contributions to the everyday financialisation literature. First, although previous research has argued that there are not uniform but multiple subject positions (Coppock, 2013; Lai, 2017), these have not been conceptualised within the framework of everyday financialisation and norms of asset accumulation. 2 The study conducted here thus supplies empirical insights into the differential nature of financial subject formation by revealing the complex relationship between norms of conduct and counter-conduct. Feeling ‘trapped’ in the current system, interviewees develop different ways of dealing with the pressure to accumulate assets and amend asset norms to one's own needs, resulting in five distinct financial subject positions. Second, approaching the study from a Foucauldian understanding of resistance being immanent in power relationships (Foucault, 1978) enables a conceptualisation of these variegated subjectivities and practices not only as deviating from a theorised investor subject but also as essential for everyday financialisation. It is shown here that counter-conduct and ‘the pursuit of a different form of conduct’ (Foucault, 2004: 265) is necessary to tackle the contradictions inherent in norms of conduct. Adjusting asset norms allows individuals to express agency, give meaning to asset accumulation and smoothen its inherent ambiguities; yet doing so reinforces a system that increasingly responsibilises citizens for their financial welfare. The interplay between conduct and counter-conduct is productive in constructing a multiplicity of financial subject positions.

In the following, the theoretical framework is first introduced before discussing relevant insights from previous studies. The preceding sections then outline the research methodology followed by the main research findings. I conclude by highlighting the importance of recognising the productive character of counter-conduct within everyday financialisation.

Willing and unwilling subjects

To elucidate the formation of varied financial subject positions, this paper makes use of Foucauldian insights on power relations, in particular his later works on governmentality (Foucault, 1978, 2003, 2004) which are seen as useful here due to the importance ascribed to resistance. Inherent in Foucault's elaborations are two key concepts, namely conduct (‘how to be governed’; Foucault, 2004: 127) and counter-conduct (‘how not to be governed like that’; Foucault, 2007: 44).

Conduct has, as a prerequisite, a will on the side of the individual to be governed. The term conduct incorporates the double sense of the French terms conduire et se conduire, where one refers to the ‘activity of conducting (conduire)’ and the other to ‘the way in which one conducts oneself (se conduit’; Foucault, 2004: 258). Individuals are, in other words, governed and govern themselves based on two mechanisms operating as power technologies – a disciplinary and a regulatory mechanism. Whereas the former seeks to influence individuals' behaviour through laws and restrictions, the latter has ‘much more to do with the manner in which the individual needs[ed] to form himself’ (Foucault, 1984: 67). In lieu of directly prescribing behaviour through making some activities costlier than others such as risking old-age poverty when relying on state pension or ensuring worker's productivity through supervision (‘disciplinary technology of labour’; Foucault, 2003: 242), the regulatory mechanism is based on interests and desires where subjects choose to adhere to norms. This governmental reasoning brings with it an understanding of power not only as repressive (‘it doesn’t only weigh on us as a force that says no’), but also as productive of subjectivity (‘what makes it accepted, is that it […] produces things’; Foucault, 1980: 119).

A will to be governed necessarily entails with it also the opposite, the will not to be governed in that manner, representing the second key concept of Foucault's discussion on power: counter-conduct. Through giving autonomy to subjects to choose between a ‘field of possibilities’ (Foucault, 1982: 790) norms are not only made admirable but they also implement the opportunity to adjust them. Foucault rejects a binary categorisation of domination and resistance (‘power is not one side and resistance on the other’; Foucault et al., 2012: 108), but instead emphasises the immanence of resistance in power relationships: ‘there are no relations of power without resistances’ (Foucault, 1980: 142). Rather than trying to eradicate power; resistance aims to harness power where subjects transfigure subject positions they are called upon to internalise and adjust them to their own needs. Indeed, ‘there is a plurality of resistances […] that are possible, necessary, improbable; others that are spontaneous, savage, solitary, concerted, rampant, or violent; still others that are quick to compromise, interested, or sacrificial’ (Foucault, 1978: 96). To reflect this multiplicity of resistance, Foucault (2007: 75) employs the term counter-conduct, i.e. ‘the will not to be governed, thusly, like that’, and departs from the narrower meaning of resistance, such as ‘breaking all the bonds of obedience’ (Foucault, 2004: 453).

By moving away from the conventional dichotomy between power and resistance, an analysis of governmentality is enabled where the mutually constitutive relationship between conduct and counter-conduct is productive in creating variegated in place of deviant subjectivities and practices, allowing for different ways of achieving norms of behaviour. Here, counter-conduct is an essential part in the formation of subject positions through problematising governmentalities but also reproducing these. Despite theoretical (Cadman, 2010; Ettlinger, 2017) and empirical discussions outside everyday financialisation (Death, 2010, 2016; Rossdale and Stierl, 2016) having picked up the Foucauldian concept of counter-conduct, an empirical exploration of the productive power of counter-conduct in constructing subject positions is missing. Before returning to this framework, I give insights into previous research and the methodology employed.

‘Activity of Conducting’: The everyday investor

With the dismantling of publicly funded welfare, the everyday person is increasingly constructed as an investor who develops ‘a portfolio of financial market assets that, carefully selected by the individual through the calculated engagement with risk, holds out the prospect of pleasure through returns’ (Langley, 2008: 93). Under such an interpretation, the mitigation of potential income shortfalls during non-working periods is to take place by way of investments in financial assets guided by finance rationality. On the one hand, everyday investors actively plan the use of money over their lifetime and accumulate financial assets for retirement. They do not solely rely on ‘passive forms of financial practices’ (Lai, 2016: 38) such as savings products with a guaranteed return but include higher risk products such as bonds, stocks and investment portfolios (Guiso et al., 2002; Coppock, 2013). On the other hand, everyday investors adopt financial strategies and ‘embrace, and bear risk as opportunity’ (Langley, 2006: 919). They are confident in making financial decisions and diversifying assets based on risk-return relationships. Employing a competitive stance in dealing with personal financial decisions and aspiring financial growth drives this subject (Martin, 2002; Samec, 2018; Weiss, 2015). While accumulating financial assets highlights the will of the everyday investor to provide financial security, adopting finance rationality reveals that this is someone who enjoys investing.

Foucauldian-inspired studies reveal how mechanisms of governance – institutional changes (e.g. reduction of state pensions), discourses (e.g. policy discourses) and financial products (e.g. private pensions) – shape this conduct of the everyday investor (Aitken, 2003; French and Kneale, 2009; Martin, 2002). Whereas this literature undoubtedly makes a substantial contribution by revealing technologies of power, the majority of these studies implicitly assumes an ‘inescapability of finance’ (Hall, 2012: 405) whereby norms constructed around asset ownership are internalised. The work of Langley (2006, 2008) provides here an additional window into governance mechanisms by acknowledging ambiguities inherent in financial investments. Rising insecurity in the workplace militates against the ability to contribute to asset accumulation on a continuous basis, and even if individuals invest in financial assets as expected, these investments remain uncertain. As a consequence, individuals are argued to be ‘pushing at the frontiers of investment’ (Langley, 2006: 932) by mainly investing in property or retreat to savings. Conduct and resistance are treated as conceptually different categories, with the everyday investor on the ‘savings side’ and the property investor on the ‘borrowing side’ where the question remains what ‘the place of the residential property investor [is] in neoliberal society’ (Langley, 2008: 199–205). Yet, if one follows the Foucauldian logic of the immanence of resistance, not only seeking to subvert norms of conduct but also being productive of conduct, it is not sufficient to shed light on power mechanisms and resistance without exploring how the interplay between conduct and counter-conduct constructs a multiplicity of subject positions. This neglect may stem from the fact that studies of subjectification rely to a large extent on an analysis of policy or media documents (Maman and Rosenhek, 2019; Mulcahy, 2017).

‘Self-Conduct’: The unwilling subject

Apart from investigating the ‘activity of conducting’ (Foucault, 2004: 258), the other sense of conduct, namely mechanisms of self-governance, is picked up by qualitative research which has recently grown in importance in governmentality studies (Fields, 2017; Kutz, 2018). These studies have shown that subjects do not only succumb to or reject categories offered to them but ‘conform, diverge or subvert top-down neoliberal forms of financial subjectification’ (Coppock, 2013: 481). Whereas research into debt behaviour has concentrated on the first meaning of resistance, namely subversion (Di Feliciantonio, 2016; Montgomerie and Tepe-Belfrage, 2019), studies exploring asset management have focused on the second meaning, namely divergence. Integrating one's own rationalities in the form of emotions, moralities and temporalities is argued to lead to selectively draw on one of the two components of the investor subject. Individuals reject investing in financial assets but perform pervasive calculations when conducting alternative investments (Lai, 2017) or they accumulate financial assets but have not internalised finance rationality (Pellandini-Simanyi and Banai, 2020). What these insights into ‘variegated outcomes of financialisation’ (Lai, 2017: 915) highlight is that contrary to viewing resistance as solely opposing, it is a rather fluid concept with various facets.

Strikingly, despite acknowledging that individuals engage with aspects of the investorial subject to a differing degree (Pellandini-Simanyi and Banai, 2020) and should not be categorised as ‘risk-averse or passive’ (Lai, 2017: 927) when not accumulating financial assets and choosing instead to invest in properties, a consequent conceptual development of differential subjectivities and practices into varied financial subject positions is missing. One underlying reasoning might be that qualitative studies have tended to focus on debt (Di Felicantono, 2016; Penaloza and Barnhart, 2011) or one aspect of asset ownership, such as homeownership (Pellandini-Simanyi et al., 2015; Samec, 2018) or non-professional trading (Ailon, 2019; Roscoe, 2015), without integrating a broader set of investment decisions. However, a holistic view of asset management is essential as can be seen in a recent study which revealed that distrusting financial investments did not translate into rejecting them but in an adjustment of the asset portfolio, excluding financial investments which are considered high risk and including non-financial investments which are seen as controllable due to being managed by oneself (Hillig, 2019b).

Building upon the work on everyday financialisation and extending these with insights into counter-conduct, the article attempts to develop a wider project by not only revealing pathways of resistance but also exploring subjectivities based on a holistic view of asset management. Employing the concept of counter-conduct means to look within norms of asset accumulation and its inherent ambiguities and identify how diverse forms of resistance are intertwined with the power relationships they aim to challenge. Such an analysis unveils coping strategies being at play and recognises that counter-conduct is necessary to the process of everyday financialisation. The article thus moves beyond identifying subjectivities deviating from an ‘ideal financialised subject position’ (Pellandini-Simanyi and Banai, 2020: 787) where some aspects are rejected while others are drawn upon and sheds light on the ‘multiple subject positions’ (Coppock, 2013: 480) within the realms of everyday financialisation. Unveiling the complex interplay between conduct and counter-conduct can help us understand the persistence of variegated instead of uniform subject positions.

Methodological notes

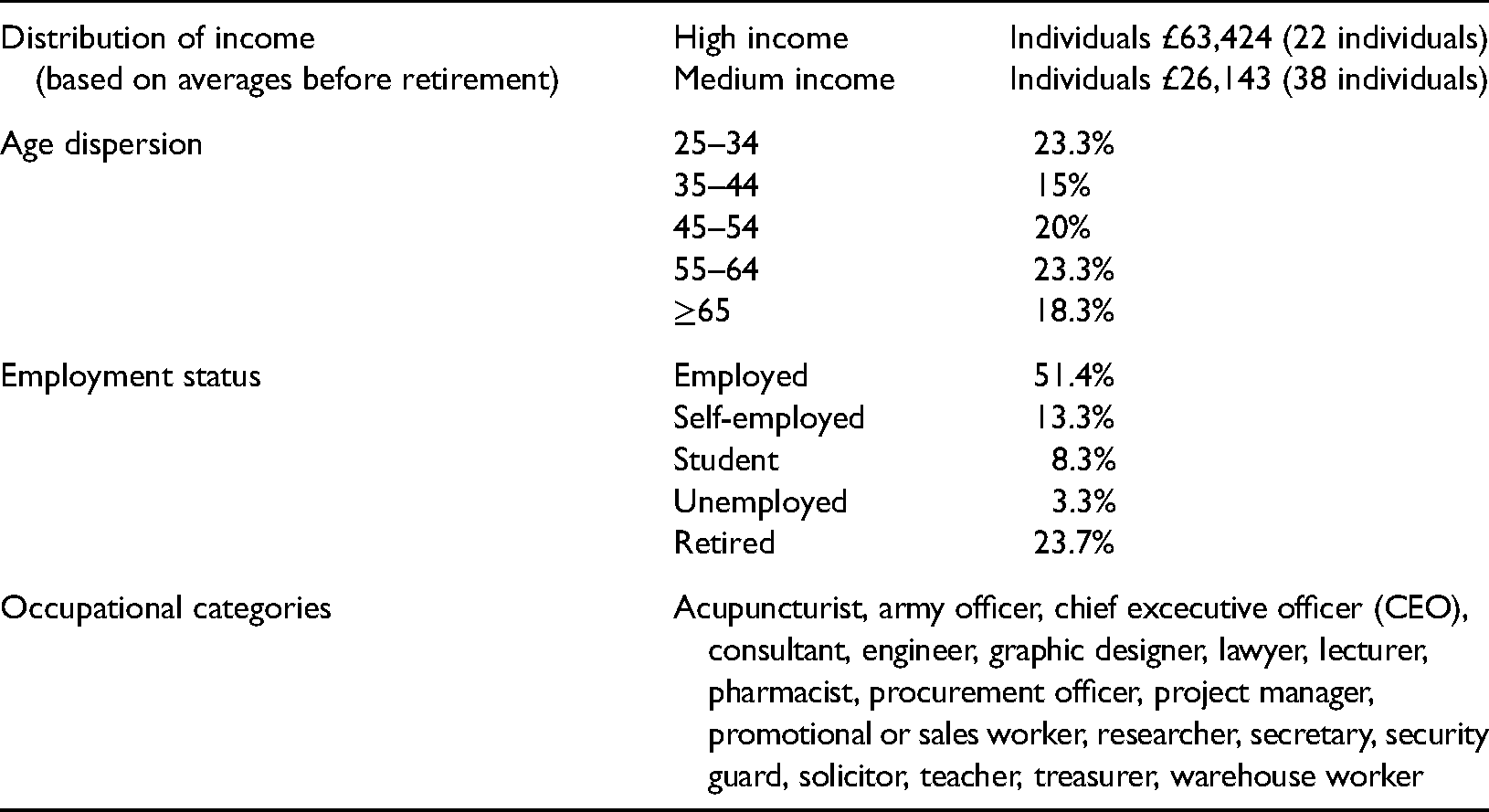

This study is based on semi-structured interviews with 60 medium- to high-income individuals conducted over the course of 2016 and 2017. Although qualitative research is not meant to produce generalisable results (Bryman and Bell, 2007), the interviews are helpful in developing new insights into financial subject formation. Foucault (2003: 30) himself advocates the use of an ‘ascending analysis of power’ due to subjects' practices not only being influenced by the constitutive power of discourses and institutional changes but also ‘possess[ing] up to a point their own specific regularities, logic, strategy’ (Foucault, 1991: 75). To achieve a diversity of interviewees (see Table 1), purposive sampling was employed (Bryman and Bell, 2007). The selection of medium- to high-income participants was made due to these income groups being ‘able to manage at least an awkward performance of the financial subject positions they have been assigned’ (Kear, 2013: 940). This, however, means that the research participants are in a fairly advantaged position compared to lower income earners who are more constrained in their responses to norms of asset accumulation. Participants were recruited by employing three strategies: advertisements on local noticeboards and websites, attending community events and employing personal networks. Two waves of interviews were conducted: July-mid–November 2016 (31 interviews) and mid-January–May 2017 (29 interviews). By pausing two months, I was able to go through the first round of analysis and weave these insights into the data collection. Interviewees have a diverse age range with the youngest one being 24 and the oldest 88 years old while 20% have a different ethnic background than white. Interviews that lasted on average between 60 and 90 min, were digitally recorded, transcribed verbatim and anonymised.

Profile of interview participants.

To analyse the interview data, a pluralistic approach including thematic and discourse analysis – the two main forms of discovering themes from qualitative data – was applied (Hesse-Biber and Johnson, 2015). Employing a pluralistic approach enables an integrated exploration of language in use where discursive dependencies (discursive patterns which are constitutive of social phenomena) are put into relation to non-discursive, or in Foucauldian terms (1991: 58), ‘extradiscursive dependencies’. By means of discourse, financial subjects are constructed, yet it is also a tool of resistance. Exploring subjects' discourses therefore opens up the possibility of unpacking different dimensions of financial subjectivities. Thematic analysis then reveals ‘the places where it [discourse] implants itself and produces its real effects’ (Foucault, 2003: 28) in terms of financial practices. This analytic approach offers valuable insights into how financial practices are reflected in subjects' conceptualisation of asset norms while being sensitive to participants' asset composition. The uniqueness here consists of combining discourses with interviewees' balance sheets. After having been given examples of assets and liabilities, interviewees were asked to fill in a provided balance sheet. A total of 50 interviewees either followed the request of providing an overview of their assets and liabilities or gave the relevant data during the interview.

‘Locked in the Rat Race’: financial subjectivities in the United Kingdom

Since the 1980s, a ‘regime of truth’ (Foucault, 1980: 131) has been established in which it is seen as normal that individuals take over responsibility over future risks by building an asset stock – diversified across ‘a range of different asset classes […] and markets’ (DWP, 2011: 17) – on which they can draw upon during periods of income shortfalls (‘everyone needs money to live on when they retire’; DWP, 2013: 6). Saving and subsequently investing are normalised to the degree that ‘the only time you shouldn’t save or invest is if there are more important things you need to do with your money. For example, getting your debts under control’ (MAS, 2021). Putting emphasis on ‘values of personal conduct’ is accompanied by ‘a weakening of the political and social framework’ (Foucault, 1984: 41). Pensions, sickness pay and unemployment benefits have been continuously reduced and labour market regulations weakened. Consequently, the United Kingdom has one of the lowest social service provisions and one of the weakest employment protections among OECD countries (OECD, 2015, 2017), creating an environment where it is costlier for individuals not to provide financial security themselves. Less ‘money security’ (IP02_MI_48) originating from decreasing state provisions (‘if you are not working, the money the government will give you is not sufficient’; IP38_MI_56) and rising job insecurity (‘I don't believe there are secure jobs anymore’; IP17_MI_43) result in a desire to establish a ‘safety net’ (IP10_MI_46) through asset accumulation. The disciplinary mechanism, that means the ‘activity of conducting’, thus works in tandem with the regulatory mechanism (‘the way in which one conducts oneself’; Foucault, 2004: 258) in constructing asset norms.

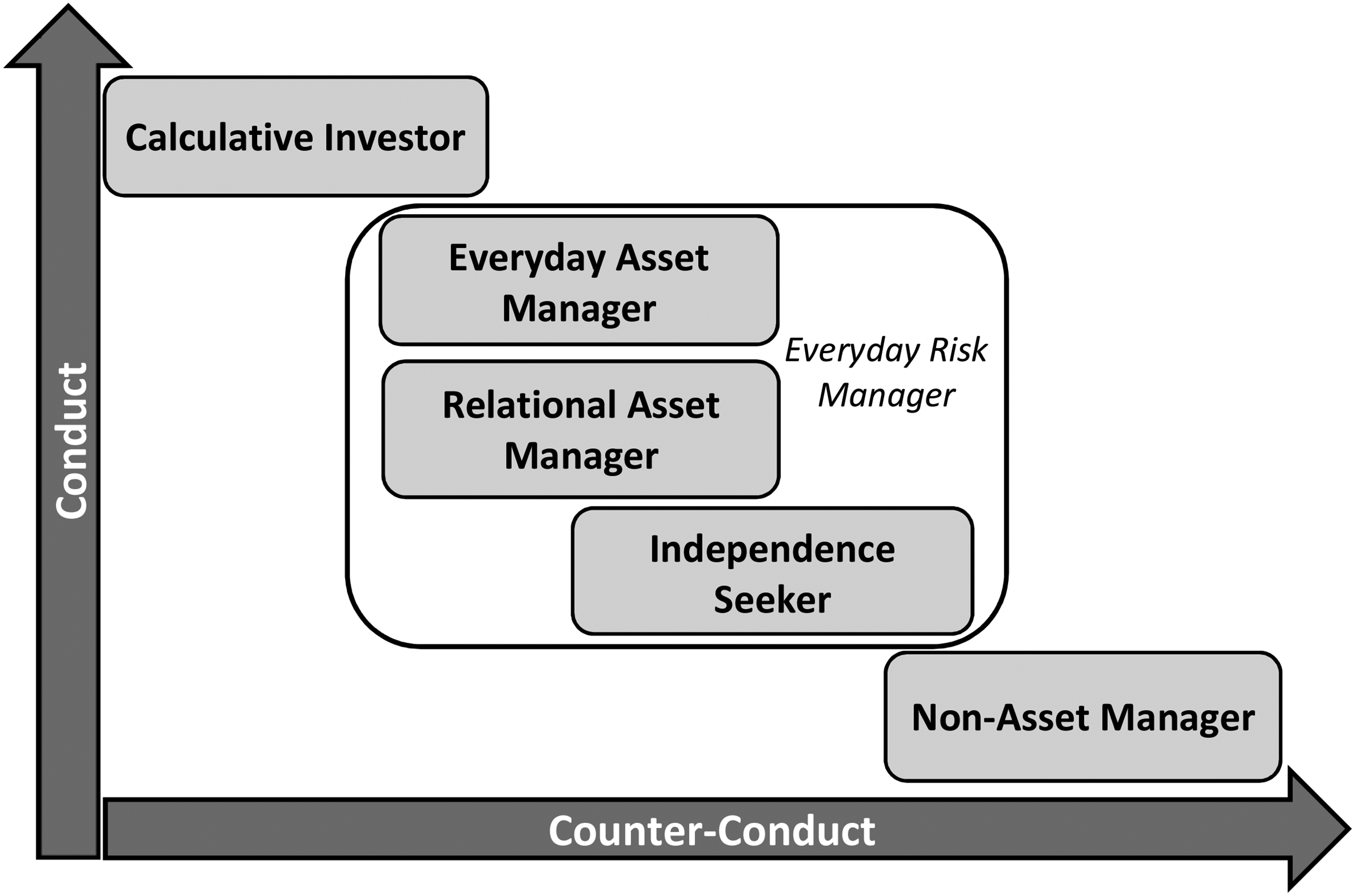

Yet, governmental construction of conduct brings with it not only the freedom to adhere to norms of conduct but also the possibility of counter-conduct. Interviewees engage critically with notions of asset accumulation due to financial institutions being perceived as profit-seeking (‘they can speculate with our money on the stock market and make themselves big bonuses’; IP53_MI_77). Although a discourse of distrust is omnipresent (‘fees that you’re charged are quite hidden’; IP20_MI_58), the resultant counter-conduct occupies ‘different tactical positions’ (Foucault, 2003: 208), ranging from a weaker form, that means a ‘will not to be governed, thusly, like that’ (Foucault, 2007: 75), to a stronger one, reflecting the will ‘not being governed quite so much’ (Foucault, 2007: 45). Five financial subject positions 3 emerged from this interplay between conduct and counter-conduct (see Figure 1). Whereas the calculative investor develops a highly diversified asset portfolio and enjoys investing, interviewees internalising the everyday risk manager subjectivity tend to feel ‘locked in the rat race that creates their [financial institutions’] wealth' (IP17_MI_43). Taking over responsibility is not seen as positive, but as having no other choice than to mitigate potential future risks (‘you can’t assume everything is there for you’; IP41a_MI_28). Individuals therefore look within constructed asset norms and adjust these to their own needs, culminating in either avoiding direct investments in financial assets (everyday asset manager), focusing on relationships when investing (relational asset manager) or giving preference to property or business investments (independence seeker). A stronger form of counter-conduct then seeks to subvert norms by aiming to avoid asset accumulation (non-asset manager).

Variegated financial subjectivities in the United Kingdom.

The calculative investor

Calculative investors call on the subject position of the everyday investor, positioning themselves as financial persons (‘I always looked at things from a financial point of view’; IP13_HI_76) who enjoy investing (‘I get a buzz off investing’; IP41a_MI_28). In line with the expected conduct of an investor, as outlined above, they speak of risk as an opportunity instead of a loss (‘if you want to seriously improve your financial position, you have to take some risks’; IP23_HI_32) and aspire to use a diverse set of financial investments (see Table 2), including riskier investments (‘you have to speculate to accumulate’; IP09_HI_50). A discourse of growth centring on climbing up the social ladder (‘always trying to get one step better’; IP35_MI_26) is accompanied by an aspirational discourse (‘We’re not unrealistic but we’re aspirational’; IP41b_MI_28) where competition is established as a measure of success, even resulting in figuratively competing with parents: ‘better than them [parents] yeah, we beat them, that's the goal’ (IP41a_MI_28). Because of being confident in making investment decisions, (‘it's just part of our brain’; IP12_HI_59), prominence is given to investing directly, with a conviction of making better decisions than professional investors: ‘We had a portfolio with Santander on shares, which I have to say, up until we handed it to them, it did very, very well. We handed it to them and it was very little’ (IP32_HI_60). Weaving through these discourses is the notion that investments and asset accumulation are enabling mechanisms to go further (‘that emotion thing that would be nice like I’m richer today than I was yesterday’; IP35_MI_26), putting arguments forward for less state regulation: ‘it's a bit too much nanny stating’ (IP09_HI_50).

Balance sheet of a calculative investor. 4

Apart from finance rationality leading to directly investing in stocks and shares, clearly differentiating calculative investors from saver subjects, it results in an ‘improbable’ counter-conduct (Foucault, 1978: 96). As discussed in previous research (Hillig, 2019a; Sotiropoulos et al., 2013; Weiss, 2015), a welfare system focused on individual asset accumulation ‘isn’t outside power or lacking power’ (Foucault, 1978: 131) but enables the dismantling of publicly funded welfare measures and creates new profit opportunities for the financial sector. Although calculative investors draw on an agency discourse in the form of individual responsibility and believe in asset accumulation as a mechanism of personal growth (‘it’s about growing value’; IP08_HI_65), the second component of the underlying power relationship is critically reflected upon. It is realised that by investing in financial assets, financial institutions gain profit and might not put the interest of their customers first (‘any sort of financial product are just an absolute value for the bank’; IP12_HI_59). This distrust in financial products (‘I’ve known about malpractice in the personal finance’; IP58_HI_49) and having confidence in managing investments (‘We are quite knowledgeable’ (IP09_HI_50) translates into investing in non-financial assets. Due to its ‘tangible’ (IP12_HI_59) character and not being managed by someone else who is ‘out to make their own money’ (IP13_HI_76), property is considered to be more controllable (‘even if the property prices were to go down, you can still rent the property to earn cash yield’; IP58_HI_48). To diversify the risk of changing house prices, properties in different locations are chosen, for instance, the domestic market is identified as risky (‘we see sort of domestic property markets likely to continue dropping’; IP04_HI_59) and investments in foreign properties are conducted (‘my property in Australia, they’re investments’; IP60_HI_55).

As a result, calculative investors develop ‘a good cross-section of shares, property, pensions, insurances’ (IP32_HI_60). Echoing previous findings (Hillig, 2019b; Pellandini-Simanyi and Banai, 2020), property investment should not be seen here as deviating from investorial concerns but forms part of a financialised subjectivity. Tackling the distrust in financial institutions with the help of further diversifying the asset portfolio aligns with the governmental discourse of individual responsibility. Individual solutions are searched for and a belief in the importance of self-reliance through conducting investments in place of relying on the state is reinforced. The interplay between conduct and counter-conduct thus intensifies prevailing forms of governance.

The everyday asset manager

In contrast to the calculative investor, everyday asset managers identify themselves as non-financial persons (‘I don't think I ever been very good at finances, I’ve always found them a bit scary’; IP56_HI_34). Risk is not perceived as an opportunity to grow but as the possibility of losing money that you worked for: ‘there is the potential that you won't get anything […] I suppose more so when you’re parting with money that you have earned’ (IP45_MI_27). Despite the declaration of being ‘not a financially investment-oriented sort of person’ (IP16_HI_65) and realising the inherent uncertainty in financial investments (‘you don’t really know what’s happening’; IP10_MI_44), interviewees drawing on this subjectivity still take the necessary steps and accumulate assets to keep ‘their [my] head above the water’; IP26_MI_50).

Reminiscent of Foucault’s (2003: 96) elaboration on the role of fear in governing (‘sovereignty is always shaped from below, and by those who are afraid’), the fear of old-age poverty acts as an enabler here (‘in the past you had a final pension, you had security’; IP46_MI_59). Notions of distrust (‘who's gonna get the profits, the directors and the board’; IP18_MI_46) and the consequent justification of asset accumulation based on having no other choice are a common discursive pattern (‘It's a necessary evil’ (IP42_MI_24); see also Hillig [2019b]). Instead of embracing asset accumulation (‘We’re not enthusiast about making more money’; IP21a_MI_65), the underlying relationship between asset norms and a retreating welfare state is foregrounded (‘everybody is encouraging you to do it, actually I think, it was a way of the government feeling less responsible’; IP01_HI_52). Feeling trapped in the treadmill of asset ownership results in being relieved when escaping the pressure to accumulate assets upon reaching retirement:

[…] hunting the house, buying the house, selling, the job changing and things like that and thank goodness, it's over really (IP21a_MI_65) Now the only time I get on a treadmill is at the gym. I am not on the treadmill of life anymore. The house is bought and paid for […] I’ve got another four pensions (IP21b_MI_65)

This coexistence of antagonistic modes within the same subject position reflects a ‘sacrificial’ form of counter-conduct where individuals express an unwillingness to submit to asset norms but are ‘quick to compromise’ in action (Foucault, 1978: 96).

Individuals are, however, not passive participants in the everyday financialisation process but are actively involved. Contrary to not investing because of the uncertainty involved in financial investments (Langley, 2007; Lai, 2017), everyday asset managers seek to amend asset norms according to one's own possibilities (‘I don’t have a shit load of money to invest’; IP25_MI_51) and ‘avoid risks that jeopardizes your family’s security’ (IP10_MI_44). Perceiving stocks and shares as too risky (‘I wouldn't want to take this risk’ (IP49_MI_52), even comparing investing in them to betting on horses (‘I don't ever go to a casino, no I never bet on horses’; IP29_MI_25) leads to excluding direct investment in them. At the same time, due to ‘money being safe in bricks and mortar’ (IP01_HI_52), property is included where the home is seen as an investment that can be traded up and then used as retirement income:

We can afford to buy a place and it made sense, even if it was for a short period four or five years, with the UK housing market as it is to invest some money […] that would help us long-term (IP56_HI_34)

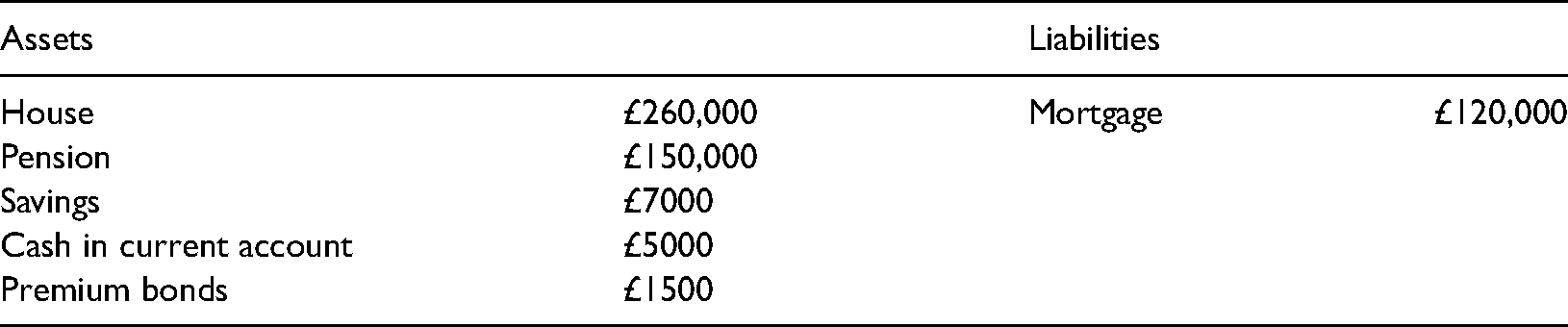

Whereas pensions are also depicted as not stable (‘pension schemes […] had actually been raided’; IP16_HI_65), ‘pension is important for everyone because the state pension is not gonna be enough’ (IP18_MI_46). Trying to reduce the risk in pension investments, interviewees invest in managed, diversified products (‘There's no point in you’re going like specific companies as such, you get like a mixed fund’; IP35_MI_26) and diversify pension income sources: ‘not just stick with the [workplace] pension, get another’ (IP42_MI_24). A typical expression used here is the metaphor: ‘keeping eggs in different baskets’ (IP16_HI_65). Everyday asset managers thus follow a three-pronged asset strategy including savings, homeownership and pension investments (see Table 3; see also Hillig, 2019b) and adopt an elementary form of diversification (i.e. discourses reflect the logic of diversification, yet they apply it in an unsophisticated way).

Balance sheet of an everyday asset manager.

Far from being irrational when not taking on higher risk investments, financial discourses and practices of the everyday asset manager represent logical responses to limitations of asset norms. Realising the uncertainty of financial investments (‘it's better to have the money under your pillow’; IP18_MI_46) and the need to have sufficient income and wealth to adopt sophisticated diversification (‘I don't think we’re at the financial stage to be doing things like that’; IP37_MI_29) constitutes a fairly robust understanding of the inherent contradictions of the investor subject. Counter-conduct, or the unwillingness to engage with the investor subjectivity and its notions of risk (‘investment is risk’; IP10_MI_44) and investments (‘I don't really have any investments, you know, I don't really have stocks and shares’; IP56_HI_34), helps to cope with these contradictions while nevertheless accumulating assets in order to provide long-term security. This highlights the mutually constitutive relationship between conduct and counter-conduct where counter-conduct enables conduct, reproducing a welfare system based on individual responsibility. Incorporating the asset manager subjectivity culminates in individualised solutions by adopting practices of ‘self-mastery’ (Foucault, 1984: 84) to achieve asset ownership and redefining asset norms according to one's own needs (‘risk a little bit, but only what I can afford to lose’; IP31_MI_50).

The relational asset manager

As the name of the subject position indicates, it is brought to life by the ‘importance [is] granted to relationships’ (Foucault, 1984: 42). In line with the everyday asset manager, relational asset managers position themselves as non-financial persons (‘I am not good with numbers’; IP02_MI_48). Yet, rather than being borne out of a criticism of asset norms and the accompanying dismantling of the welfare state, they ‘don't feel confident enough [myself] to get into it’; IP52_HI_41) due to finance being too confusing (‘lots of confusion’; IP31_MI_50) and uncertain (‘you just don't know what's really gonna happen’; IP44_HI_58). Driven by this lack of confidence, they accept the responsibility to accumulate assets for the future but are unwilling to actively engage in financial decisions (‘finance doesn’t interest me, only as much as I’ve got it get it sorted’; IP19_MI_73). On the one hand, advice from family and friends is taken on when making decisions (‘I did ask a lot of my friends who they went with’; IP39_MI_36), leading in some cases to success (‘We were good friends and he said if you got any spare money, buy as many as you can […] it must have increased by 50%’; IP33_MI_88) and in others to losses (‘I did go to a financial advisor through a friend of mine who actually, I think, gave me the wrong advice’; IP44_HI_58). On the other hand, service outweighs any lack of substantive asset management.

I always been able to get hold of Gemma […] when I walk into the bank, she says Hello, so I am a friend [..] they're pleasant in a way that banks have gone very distant […] I don't think they manage them particularly well. They don't ring me and say Good Lord and smashing an offer (IP06_HI_79)

Taking time to explain a mortgage is taken as a selection criterion: ‘I didn't bother to do a lot of comparisons […] they gave me two hours and sat down and we went through everything in fine detail’ (IP31_MI_50). Relationships, not finance rationality, become the dominant force in making financial decisions, representing a necessary form of counter-conduct. Because of not feeling confident enough, involving help from someone else allows individuals to conform to norms of conduct: ‘If I had to do it entirely by myself, I would not have had this spread of stocks and shares. Because I don't think I’ll be confident enough’ (IP19_MI_73).

Relationships not only help to shape one's own asset strategy but also enable family members to achieve financial security through asset accumulation. Instead of employing an ‘individualistic attitude’ of growth and competition (such as wanting to outperform family members as in the case of the calculative investor), conduct of the relational asset manager ‘entails an intensification of the values of private life’ (Foucault, 1984: 42). Prominence is given to helping friends and family (‘gave £10,000 to each of my grandchildren, purely to use towards deposit of their house’; IP19_MI_73), undeterred by the aspect that this might be misused:

He [son] moved back in because he broke up with his girlfriend, so he's come back home to save a deposit up. That was April, I've been paying out him rather than him saving a deposit up, that's the situation and he's gone on holiday for the second time this year (IP31_MI_50)

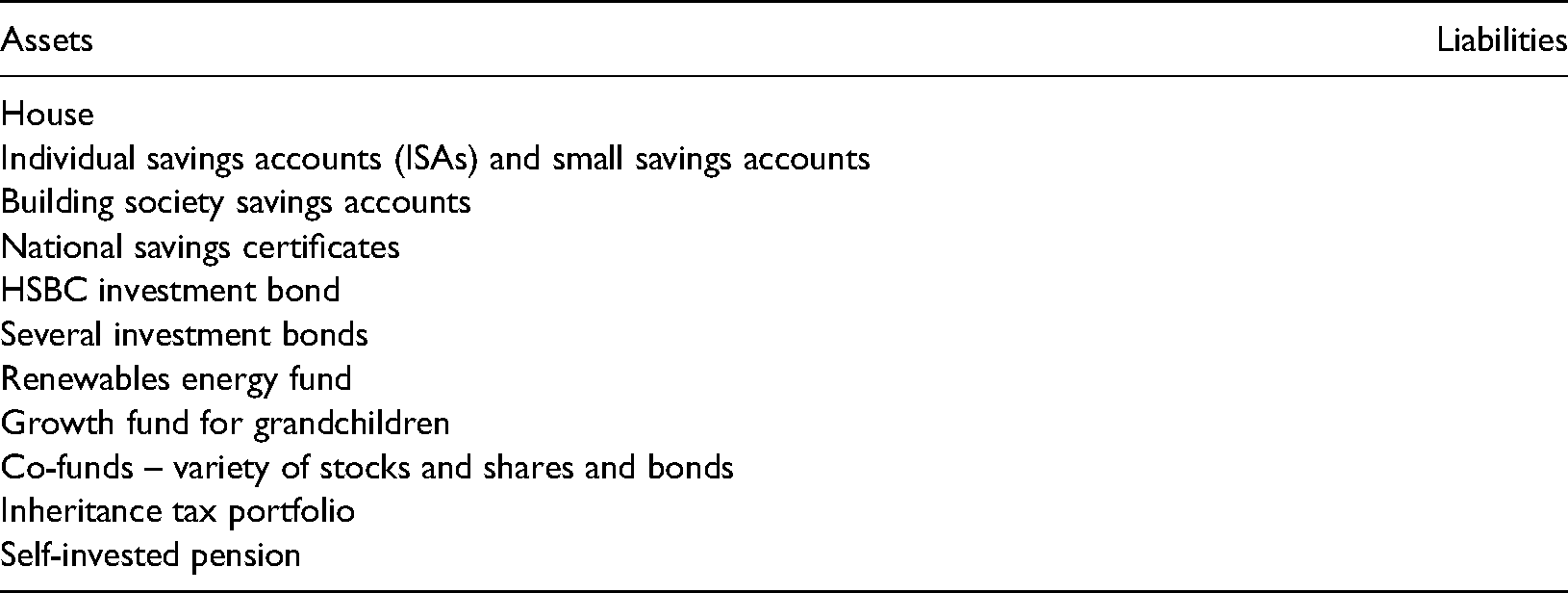

This sometimes leads to buying flats for family members who are not perceived as being good in dealing with money which is excused with not being naturally a finance person: ‘I own this flat where Bruno lives and he wouldn't be able to […] I’m doing him a big favour and he could have over his life saved money, but he's not a saver. Some people are, some people aren't' (IP14_MI_65). When being a landlord and renting out to friends, the tenant is included into the will for inheriting the house: ‘I actually rent that out to a friend of mine. […] if I was to die that house goes to him’ (IP44_HI_58). This focus on helping others is even reflected in their balance sheets as illustrated in Table 4 where assets are earmarked according to family members.

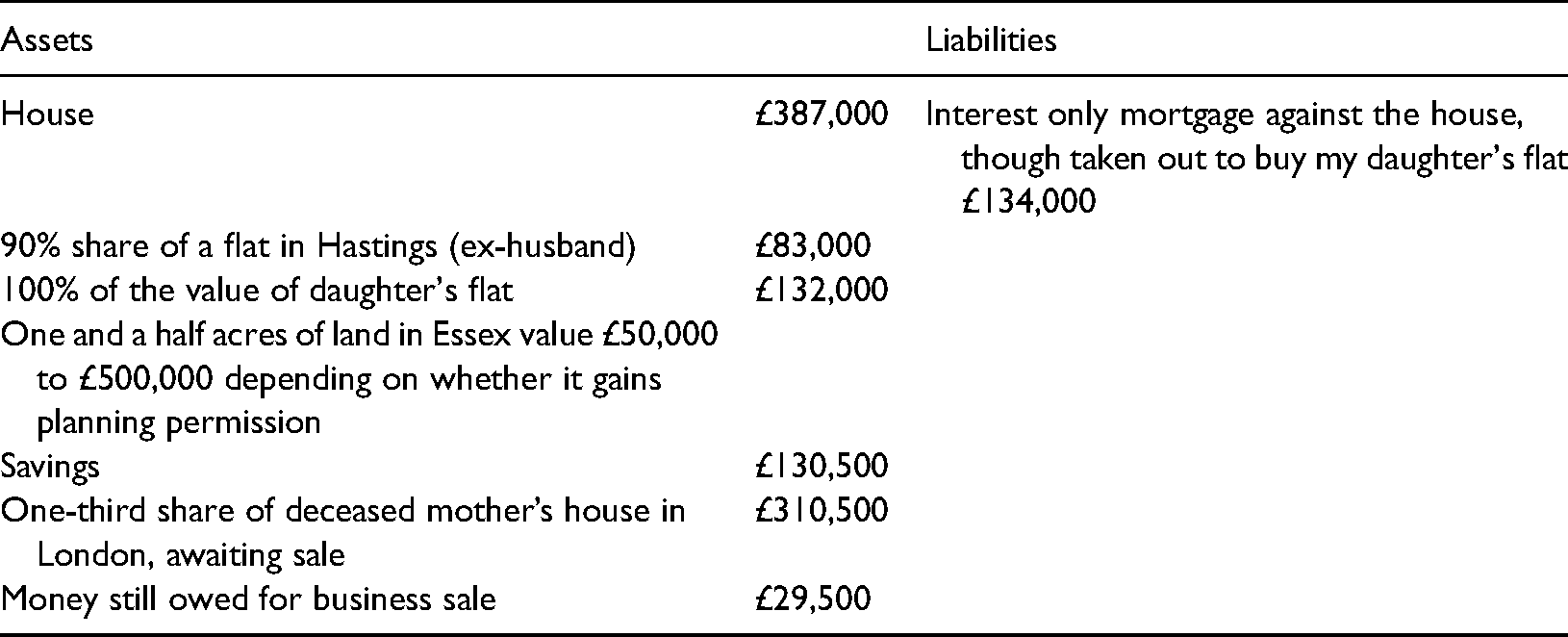

Balance sheet of a relational asset manager.

Whereas these findings echo previous research where emotions and relationships are shown to outweigh economic considerations (Lai, 2017), it emanates mainly from the subject position of the relational asset manager instead of being a wider phenomenon. Moreover, the importance of relationships should not be perceived as a form of rejection of the investor subject because of not internalising finance rationality (Pellandini-Simanyi et al., 2015) or focusing on care more than on one's own retirement planning (Lai, 2017). Instead, the mutually constitutive relationship between conduct and counter-conduct is productive in assuming responsibility for one's own financial security (‘I need some sort of security there to make sure […] I got money to rely on’; IP44_HI_58). Arising from the complexity of financial products, the relational asset manager invokes relationships to accumulate assets. This avoidance of finance rationality can be argued to be rational since it reduces the time investment in understanding financial investments which remain inherently uncertain. In the case of the everyday asset manager and the relational asset manager, the practices and discourses of interviewees thus reveal a weak form of counter-conduct operating as ‘handles in power relationships’ (Foucault, 1978: 95), enabling them to smoothen contradictions inherent in norms of conduct. Being able to adjust norms of asset accumulation leads to accumulating financial and non-financial assets and through this unwillingly reinforcing a system which places the responsibility onto individuals while dismantling the welfare state.

The independence seeker

In comparison to the previous two subject positions, the independence seeker takes up a more active or ‘savage’ (Foucault, 1978: 96) form of counter-conduct. A desire for independence ‘vis-à-vis […] the institutions to which they are [he is] answerable’ (Foucault, 1984: 42) is the driving force in shaping this subject position which in turn alleviates ambiguities inherent in asset accumulation. On the one hand, seeking to escape the disciplinary technology of labour appears to solve the contradiction between investing and rising job insecurity. On the other hand, wanting to avoid financial institutions helps to address the inherent uncertainty of financial products by giving more importance to non-financial assets. In both approaches, the independence seeker employs an agency discourse to resist governance mechanisms, in contrast to the calculative investor, who talks from a position of opportunity when employing the discourse.

The entrepreneur

Besides increasing profit opportunities for financial institutions and enabling the dismantling of the welfare state, a welfare system focused on asset accumulation also intensifies capital–labour inequalities. As shown elsewhere (Hillig, 2019b), everyday asset managers make sure to work hard to not lose their job in an insecure work environment and increase work hours to ensure financial security. Yet, even then job insecurity militates against the ability to save on a continuous basis. Interviewees internalising the subjectivity of the entrepreneur aim to liberate themselves from this disciplining mechanism of work (‘I’m free of what my timetable is and how much I want to work’; IP24_MI_42) and overcome the risk of job insecurity hindering asset accumulation ‘because if you’re self-employed, you only earn in lumps, so it's easier to actually save a chunk than putting away if you’re on a monthly salary’ (IP20_MI_58). Employing metaphors such as wanting to avoid becoming ‘kind of great machines of society’ can be thought of bolstering this form of counter-conduct:

School, I see as training young kids to be kind of great machines for society […] It's always, you know, you have to be able to do your mathematics and your English and your science because you need to be, I don't know whatever it is, a profession which […] is safe (IP54_MI_34).

Prominence is given to breaking free from the disciplinary technology of labour and accumulating assets (‘I always worked for myself and invested in myself’), even when this means being responsible for losses (‘I look for me own advice and if I fall flat on my face it's my fault’; IP53_MI_77). On the surface it thus appears to be a liberating subject position, overcoming the ambiguity between job insecurity and asset accumulation.

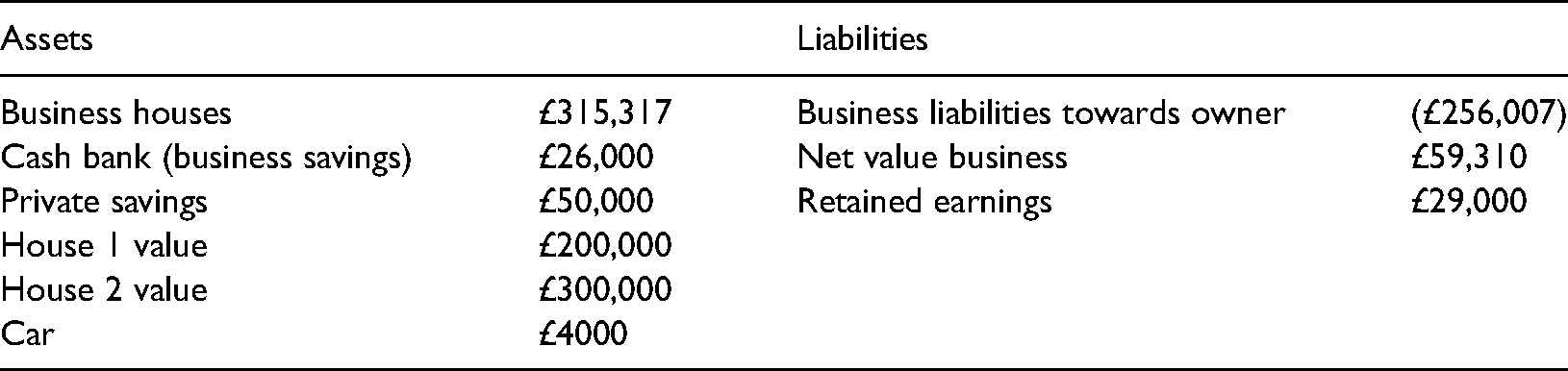

However, upon further analysis, being self-employed is rather restrictive and disciplining. On the one hand, having a business limits asset accumulation. Because income is received in lumps, pensions are excluded from the asset strategy (‘I’ve got very little pension provision ‘cause when you’re self-employed, it’s the last thing you tend to put money by for’; IP20_MI_58). Also, wanting to put enough money away for unexpected expenses in the business puts a strain on asset accumulation. This goes as far as not identifying savings as one's own: ‘I’ve got 25 grand in a pot but in my head that's not my money […] I won't put it into anything, because I want it there if the tax man comes’ (IP51_MI_36). To nevertheless realise asset ownership, interviewees drawing on notions of entrepreneurial subjectivity work ‘very long hours’ (IP54_MI_34). On the other hand, business debt becomes entangled with personal finance (‘well the personal debt was basically to fund the business’ (IP55_MI_65; as can also be seen in Table 5 listing both in one balance sheet)). A focus on business growth (‘want to push on and make money’) where a standstill is seen as the worst-case scenario (‘we were running faster and faster to stand still’; IP53_MI_77) results in using personal debt in the business. In case of difficulties, this debt functions as a disciplining mechanism in which individuals have to ‘work damn hard’ (IP55_MI_65) to pay it off. Despite wanting to gain freedom (‘I’m quite an independent person’; IP20_MI_58) by escaping the disciplining mechanism of work and revolting against the intensification of capital–labour inequalities through asset accumulation (‘I think money was invented by the capitalists to keep the working masses under control’; IP47_MI_60), the interplay between personal and business finance culminates in rising pressure and in an increase of work hours.

Balance sheet of an independence seeker.

The defiant investor

Because of not being able to mitigate uncertainty with the help of financial investments and a strong distrust in financial institutions, the defiant investor seeks to gain independence from them. Rather ‘than the alternative of ploughing your money into something that has let people down’ (IP17_MI_43), they not only avoid direct investment in financial products as in the case of the everyday asset manager but aim to also reduce the reliance on managed financial products (‘Do not touch pensions […] You’re better off buying gold bars and keep them in Switzerland and then wait for 40 years’; IP55_MI_65). Emphasis is put on ‘wanting [wanted] a retirement fund where they [I] have some control’ (IP17_MI_43) in contrast to financial investments which have been hit by ‘big pension and mis-selling scandals’ (IP28_MI_62) and regulation changes (‘Gordon Brown comes along and taxed the dividends and all the figures on the pension growth […] came nowhere near what the projection was’; IP55_MI_65). Evidential discourse based on experience and metaphorical expressions ‘down the tube’ are prevalent here:

My Mum invested in Heineken, that went down the tube, my brother invested in Equitable Life, that went down the tube, and I am like well then what's the point […] I am not gonna put 70 quid a month into something for the next years only to be told that some CEO is, you know, banging some secretary and it's all gone tits up and you haven't got any money (IP07_HI_50).

For the purpose of being ‘financially independent no matter what happens’ (IP07_HI_50), the subject position enacted here gives preference to tangible assets such as property (‘something more tangible, like a house’; IP36_MI_41) or gold and silver (‘buy silver, as in troy in ounce of silver, the coins every month […] I try to keep it away from the banks’; IP36_MI_41). Alongside conducting alternative investments peer-to-peer lending is used to circumvent the traditional banking system (IP27_MI_59):

People are lending to each other, so we don't touch the banks […] He's got redundancy money and he takes a little bit every year so as not to go over his tax bracket, and I said Why do you do it? He said, Because I have to pay tax otherwise. Well, you could lend me the money, and I can pay you 8% interest.

However, the trust in non-financial assets produces unbalanced asset compositions (see Table 6), reflecting characteristics of the ‘leveraged investor’ (Langley, 2008: 242) who takes on debt to accumulate property. Perhaps most importantly to note here is that the concomitant high debt levels tend to be ignored with the help of drawing on an agency discourse (‘it's giving me financial freedom’). Despite emphasising that ‘once you’ve got a mortgage […] you are trapped’, variable, interest-rate only mortgages are described as liberating in contrast to constraining: ‘they give you a bit more flexibility and freedom’ (IP17_MI_43). The defiant investor sees finance as negative even though it is at the same time acknowledged that accumulating wealth is a necessity (‘you need to look out and do something for you’; IP28_MI_62) to be free, revealing the strong promotion of hidden meanings of asset norms. Both, the entrepreneur and defiant investor, challenge existing governance mechanisms of conduct without rejecting its underlying premises of asset accumulation, creating their own versions of financial subjectivities and practices, yet, reproducing the very system they aim to challenge.

Balance sheet of a defiant investor.

The discussions presented above challenge an understanding of resistance as opposing, revealing how forms of counter-conduct are deeply embedded within mechanisms of governance. Instead of embracing finance, a discourse of distrust is omnipresent in interviewees’ statements, manifested in wanting to be ‘led differently, by other men, and towards other objectives than those proposed’ (Foucault, 2004: 265) and culminating in differentiated asset trajectories. Some individuals avoid direct investment in financial assets (everyday asset manager), others leave financial decisions to others (relational asset manager) and yet others give prominence to non-financial investments (independence seeker). These asset strategies, or diverse ‘values of personal conduct’ (Foucault, 1984: 41), are not irrational but represent logical responses to contradictions inherent in norms of conduct. Through problematising governance mechanisms and amending asset norms to one's own needs, ambiguities immanent in norms of conduct are smoothened and asset accumulation enabled, albeit with much more complex outcomes than theoretically expected. Besides variegated subjectivities and practices deviating from a theorised investor subject, the discussion above has unravelled that counter-conduct is necessary for everyday financialisation to take place.

The non-asset manager

In contrast to the previous subject positions who want to ‘be conducted differently’ based on ‘other procedures and methods’, the non-asset manager seeks ‘to escape directions by others’ (Foucault, 2004: 259) and rejects asset accumulation as a means to provide financial security (‘I just don't have that relationship with money’; IP59_MI_32). Suspicions are present concerning whether institutional changes are in the interests of ordinary people (‘it's façade, it's a scam’; IP03_MI_52). While the everyday asset manager and independence seeker also display distrust in finance and distance themselves from financial investments, non-asset managers question the benefits of conducting any form of investments (‘you can't be one of those blinking persons that thinks you work and pay their mortgage off when they’re 60 because that don't work, they’re in for a shock’; IP03_MI_52). This subject position is driven on the one hand by fear of losing ‘money that you’ve worked really hard for’ (IP50_MI_42) and on the other hand by having to give up ethical values when investing (‘if you actually want a return on it, you probably have to wave goodbye to ethics’; IP40_MI_43). Consequently, they take up an ‘adversary’ resistance (Foucault, 1978: 95) in two distinct ways, building upon the deviations from an investor subject discussed in the literature: ‘passive saver’ (Lai, 2017: 927) and ‘revolver’ (Langley, 2008: 16).

The passive saver (‘it is essential to save something every month’; IP37_MI_29) is someone who subverts the discourse of asset accumulation as a means of welfare and works from a basis of deconstruction. Within this subjectivity, a clear difference is made between homeowners and homebuyers:

The house isn't your own anyway even when you've got a mortgage […] If you lost your job, yeah, you gotta worry over the mortgage and having the house taken from you […] If anything goes wrong in the house, you are responsible for it, the maintenance of it whereas if it's rented, you know, all that's taken away from you and if you decided to move, the flexibility obviously is there with renting (IP50_MI_42).

Contrasting previous discussions in the literature which have argued that passive savers retreat to property investments (Clark, 2012; Leyshon and French, 2009), non-asset managers reject investments in non-financial assets due to realising the incorporated risks such as losing your house and the extra burden of maintenance costs. Also, buy-to-let properties are seen as additional work rather than posing the possibility of earning income: ‘being stuck, paying the mortgage, living somewhere or trying to get tenants in somewhere […] I’d rather not do that' (IP37_MI_29). As can be seen here, the non-asset manager reworks the agency discourse into a resistance discourse by emphasising flexibility and freedom when providing reasons for not wanting to buy a house. It is realised even when employing tactical ways to cope with ambiguities in financial investments such as investing in property that these cannot reduce but instead intensify uncertainty (‘worry about it, perhaps losing money’; IP50_MI_42).

The credit revolver then relates back to the subject position of the consumer, wanting to express their autonomy with the help of debt-financed consumption and exploiting numerous credit card offers. The ambiguity between being expected to become an everyday investor while at the same time being called upon to be a consumer subject who uses consumer credit to finance their lifestyle (Langley, 2008) is solved here by withdrawing from the everyday investor subjectivity. Debt is seen as having the potential for financing their lifestyle:

I had probably four or five bank accounts, credit cards, which had anywhere between £5 and 10,000 on them […] use that money to go on holidays […] I was quite good at it and I never, I never missed payments or anything but I did have, I had loads of debt but I managed to also, well, you rob Peter to pay Paul. You take money out to give to something else and you balance it off (IP48_HI_58).

Since ‘it’s always manageable and they [I] can still pay for things, and cover the payments on it’, they are not ‘scared of debt’ (IP40_MI_43). Describing it by use of figurative speech ‘rob Peter to pay Paul’, the revolver feels confident in managing these different credit cards by means of rolling over debt (‘I kind of use one to pay the other’; IP48_HI_58) and exploiting interest rate differentials (‘the system is there to be exploited’; IP03_MI_52). Because ‘banks basically are not in it for you’, interviewees diversify credit cards and shop around for the best deal: ‘I found them exceedingly unhelpful and I thought you know what I can afford to pay this debt for a little while longer and that's when I started to shop around’ (IP59_MI_32).

What the subject position of the non-asset manager shows is that power relationships do not represent a relationship where one is solely ‘trapped’ but there ‘are always possibilities of changing the situation’ (Foucault, 1997: 167). Non-asset managers reject not only financial but also non-financial investments due to realising risks involved in investments (‘I don't like the risk element, I don't like it at all’; IP50_MI_42) and distance themselves from actively planning ahead (‘get your salary and live your life […] I don't look too much into the future, I just look in the now’; IP37_MI_29). At the same time, ‘resistance is never in a position of exteriority in relation to power’ (Foucault, 1978: 95). Finance rationality is adopted in a wider form by employing extensive strategies to exploit the financial system and contributions to workplace pensions are made (see Table 7) ‘because the government has more stringent, you know, laws on that and also on the tax on things that an employer needs to do’ (IP59_MI_32). Yet, pensions are not actively chosen but rather one does not opt-out (‘I pay in and the company pays in and I paid, I mean I never tested to see what else is there’; IP48_HI_58), indicating a passive engagement (‘it's a pound for every, hmm, I don't even want to say because I’m probably completely wrong’; IP50_MI_42).

Balance sheet of a non-asset manager.

Conclusion

Moving beyond a discussion of financialised and non-financialised subjects, this study has set out to show how multifaceted acts of resistance shape differential financial subject positions. Integrating a holistic view of asset accumulation and anchoring the empirical insights within the analytical frame of counter-conduct has allowed me to contribute to the literature in a twofold way.

First, whereas it has been highlighted that everyday financialisation is not a monolithic process, this is the first study to suggest a typology of five distinct financial subject positions, originating from the complex interplay between conduct and counter-conduct. Having internalised a discourse of self-reliance and personal growth through asset accumulation, the calculative investor employs a rather improbable counter-conduct. Reflecting critically on financial institutions, which are depicted as profit-seeking institutions at one's own expense, norms of conduct are extended by including non-financial assets in the asset portfolio. A more critical view of the current system, yet being quick to compromise in action, can be found in the following subject positions. Whereas the everyday asset manager and the relational asset manager seek to establish financial security, it does not originate from the belief in its benefits but from the pressure to accumulate assets due to a retreating welfare state and rising job insecurity. Feeling trapped in the current system results in looking within norms of conduct and aligning these to one's own needs. Aiming to minimise the risk exposure culminates in avoiding direct investments in financial assets (everyday asset manager) or in transferring the responsibility of accumulating assets to someone else (relational asset manager). As its name indicates, a desire of independence is then displayed by the independence seeker reflected in taking up a stronger form of counter-conduct. Seeking to reduce the reliance on the formal financial system leads to concentrating on investments in non-financial assets (defiant investor), and wanting to escape the disciplining mechanism of work translates into pursuing self-employment (entrepreneur). Finally, rather than amending asset norms, the non-asset manager displays the strongest form of counter-conduct and refuses to actively invest and engage with norms of asset accumulation. The unifying thread in the asset strategies introduced above is counter-conduct where subjects critically reflect upon governance mechanisms of conduct. Wanting to establish financial security, while, at the same time, expressing distrust of financial institutions is seemingly omnipresent. Yet, the resultant variegated financial discourses and practices suggest a nuanced engagement with asset norms, displaying differing degrees of counter-conduct. Being able to transfigure the subject position they are called upon to internalise to their own needs enables individuals to give meaning to asset accumulation and overcome the contradiction between not trusting financial institutions and yet accumulating assets in order to provide financial security.

Second, the paper differs from existing studies in that the focus lies on the ‘relational character of power relationships’ whose ‘existence depends on a multiplicity of points of resistances’ (Foucault, 1978: 95). The above-identified varied subject positions not only deviate from the theorised everyday investor subject but are also necessary for everyday financialisation to take place. The subject position of the everyday investor assumes a person who is able to conduct continuous investments over their lifetime. Yet, as highlighted by previous studies (Hillig, 2019b; Langley, 2007), on the one hand, this stands in contradiction with the rising job insecurity and on the other hand even if individuals invest as theoretically expected financial investments remain uncertain. Strikingly, interviewees' statements depict a rather robust understanding of these inherent contradictions. To differing degrees, they foreground the exploitative character of financial institutions and the accompanying uncertainty of investments, and how asset accumulation enables the dismantling of the welfare state and intensifies capital–labour inequalities reflected in rising money and job insecurity. Yet, problematising these underlying power relationships and amending asset norms according to their own needs provides not only a sense of agency but also smoothens ambiguities inherent in norms of conduct. Uncertainty of financial investments is tackled by choosing lower risk investments (everyday asset manager), investing in property (calculative investor, defiant investor) and/or transferring responsibility onto someone else (relational asset manager), and the contradiction between investing on a regular basis and job insecurity is addressed by being self-employed (entrepreneur). These insights suggest an even more pessimistic view as previously introduced where it has been suggested that everyday financialisation can take place without individuals willingly adopting the mindset of the everyday investor. Besides ‘not even need[ing] to change people's subjectivities but [can] progress[ing] by co-opting existing moral economies’ (Pellandini-Simanyi and Banai, 2020: 787), everyday financialisation cannot exist without counter-conduct. Put differently, variegated subjectivities and practices are not solely militating against a unique financial subject position but are also essential for a welfare system, which responsibilises its citizens for their financial welfare. Due to its inherent imperfections, everyday financialisation could not take place without amending norms of asset accumulation to one's own rationalities and subjective life positions. Ways of not being like that are thus deeply embedded in mechanisms of governance, assimilating tactics from within a welfare system based on asset accumulation.

Taken together, the findings presented here point to a need to rethink the theorisation of a financial subject. Having employed the concepts of conduct and counter-conduct has brought to the forefront how the imperfections of everyday financialisation are representing on the one hand possibilities for ruptures and on the other hand reproduce the very system they challenge, albeit differently practised than theoretically inferred. Conduct and counter-conduct are inextricably interlinked within the frame of everyday financialisation. Revealing this mutually constitutive relationship explains why differential subjectivities and practices in contrast to the investor subject emerge and continue to exist in even advanced financialised countries. Interestingly, these forms of counter-conduct seem to have been ‘re-implanted, and taken up again in one or another direction’ (Foucault, 2004: 282) in mechanisms of conduct. Property investment is included in governmental strategies and households are called upon to invest in managed products with pre-given risk categories (Hillig, 2019b). What we experience here is the promotion of cautious financial behaviour in contrast to a full embracement of risk. Digging more deeply into everyday dimensions from the subject's perspective in connection to policy suggestions could produce novel insights and open up spaces for critical reflection on existing policies and forms of resistance that do not coalesce into conformity or rejection.

Footnotes

Acknowledgements

The author wishes to thank Paul Auerbach, Philip Roscoe, Dimitris P. Sotiropoulos, Andrew B. Trigg, Hadas Weiss as well as two anonymous reviewers for their insightful comments on an earlier draft of this paper. Any remaining errors or omissions remain my responsibility.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.