Abstract

Self-employed labour in transportation is a notoriously precarious form of employment that occurs throughout many developing countries. In order to offset high-cost and insecure vehicle procurement arrangements, paratransit fare structures are formulated on the basis of a set of logics designed to maximise revenues. Although entrepreneurial, when these logics occur in conflict with public fare legislation, they are undertaken illegally, or informally, and are perceived as undesirable by policy makers and transport users. However, the underlying structures that necessitate these practices are seldom examined despite their significant effect on mobilities and the livelihood experiences of male entrepreneurs. This paper engages with critical literatures on the financialisation of poverty reduction to present financialisation as a class-based mechanism that, with the rapid increase of digital payment and ‘alternative’ credit scoring, structures micro-entrepreneurship and precarity in the neoliberal context of India. The paper argues that digitally enhanced financial inclusion techniques may steer low-income workers toward mainstream finance institutions modelled on the global economy. They enable profit to be generated by investors and private microfinance companies. However, new financial technologies do not do little to reduce the risk and expense of microfinance, nor do they increase micro-entrepreneurs' profit margins. Moreover, they threaten the informal practices entrepreneurs use to self-manage their financial precarity.

Keywords

Introduction

‘I took a loan to pay the interest on the older loan and that's how it started’ begins one of Bengaluru's paratransit operators. He is recalling—during our interview—the difficulties of managing finance in a precarious occupation operated at the very low end of profitability. Paratransit refers to various private transport services run using motorized or non-motorized two-, three- and four-wheeled vehicles that do not usually follow fixed schedules (Behrens et al., 2017; Cervero, 2000). Services may, or may not, be regulated by the state although the term paratransit often is used to convey services that operate partially, or entirely, informally. Paratransit is revered for its ability to keep up with the rate of expansion in cities of the global South and to adjust to varying demand in ways that formal, top-down, transport services cannot, or do not (Cervero and Golub, 2007; Finn, 2012). In some contexts, paratransit has been shaped by neoliberal economic policies that have cultivated multiple deregulated private services over comprehensive state-owned public transport systems on the basis of the market's superior efficiency to deliver services (Rizzo, 2017). It forms a significant segment of micro-entrepreneurship in contexts, such as India, where much employment has shifted from industrial waged labour to self-employment.

Despite their key role in transportation systems, paratransit micro-entrepreneurs commonly have little control over their working conditions, suffer substantial precarity and disposability, and are paid insufficiently (Agbiboa, 2017; Doherty, 2017; Rekhviashvili and Sgibnev, 2018). Enduring cycles of debt and financial exclusion feature in their lives and are an expression of their social class in relation to neoliberal policy, practice and discourse, and related processes of individualisation and financialisation (Chhachhi, 2020; Marron, 2013; Lai, 2018; Langley, 2008). A key challenge for paratransit operators is how to secure a vehicle as to the main asset to their business. Operators are often limited to high-cost and insecure finance and it is thought that improving access to mainstream and formal forms of finance will financially empower them (Chadhar, 2016; Garg et al., 2010; Harding et al., 2016). This is the central hypothesis of financial inclusion (FI), which now increasingly occurs through the expansion of finance technologies (fintech). These include digital payment mobile phone platforms and big data-driven credit scoring techniques that are promoted by international development institutions, governments and private companies (Demirgüç-Kunt et al., 2017; Owens and Wilhelm, 2017).

Critical scholars have pointed out, however, that financial exclusion continues on the basis of social class with the entry of new actors and technologies involved in FI as a result of financialisation (Aitken, 2017; Bateman, 2018; Bernards, 2019; Boamah and Murshid, 2019; Gabor and Brooks, 2017; Lai and Samers, forthcoming; Langevin, 2019; Mawdsley, 2018). Financialisation is the mechanism through which financial motives, markets, actors, institutions and technologies, take an increasing role in the operation of economies (Epstein, 2005). The effects of class-based financial exclusion are particularly acute in the global South where financial technologies do not easily adapt to informal economies of micro-entrepreneurship and where the number of unbanked populations is large in scale (Rona-Tas and Guseva, 2018). Currently, the ways in which new financial technologies alter the practices and capabilities of the poor to manage their finance and micro-enterprises, and paratransit services, are not well understood. This is particularly the case for male entrepreneurs, whereas previous research has predominantly considered issues of micro-finance and FI for women. A common understanding in transportation policy is that digital technology, payment and data, will facilitate new understandings of paratransit and its reform for the benefit of transport users (Behrens et al., 2017; Tinka and Behrens, 2019). However, critical research that addresses the limitations and problems of FI for transport workers is much less common. This oversight occurs because in much of transportation research, planning and policy, there is an ongoing commitment to the application of technical solutions without adequate understanding of the social and political contexts of developing cities (Marsden and Reardon, 2017; Uteng and Lucas, 2018).

This paper indicates that financialisation, in this case transitioning to digital mechanisms of finance and commerce to meet the objective of FI, is problematic for low income micro-entrepreneurs in a number of ways. Firstly, micro-entrepreneurs embedded in cash economies have difficulty in adapting to new financial technologies or have little incentive to use them, which limits their ability to develop digital data for credit scoring. Paratransit operators are an example of self-employed entrepreneurs who remain largely dependent on indigenous moneylenders, whom although exploitative, do offer easy entry to – and exit from – finance. Secondly, through financialisation, low-income micro-entrepreneurs are increasingly exposed to high-cost subprime finance. They are brought into formal finance markets that enable the production of capital for an elite class of investors, however, financialisation is doing little to improve the financial insecurity of the poor who may benefit more from improvements to their employment, income and state welfare. Thirdly, fintech is accompanied by obligations for entrepreneurs to reform their business practices. In the case of paratransit entrepreneurs, in order to repay their finance while managing low and fluctuating income, operators often negotiate fares above fixed-fare rates set by governing institutions. Fares are differentiated according to time of day, appearance of passengers, road surface conditions, weather conditions, travel demand, speed, quality of service or time spent travelling, for example (Diaz Olvera et al., 2016; Khayesi et al., 2015; McCormick et al., 2013; Phun and Yai, 2016; Venter et al., 2014). The transparency of digital fare payment and online trip booking now threaten the possibility of informal entrepreneurship in paratransit. This creates resistance to fintech and further exclusion from financial institutions. This paper argues that financialisation is a mechanism cultivated by neoliberalism, which reproduces exclusions on the basis of class. The role of new financial companies and technologies in bolstering FI is therefore unable to offer a straightforward solution that financially empowers low-income entrepreneurs.

Financialised development: entrepreneurship and risk

Neoliberalism and the growth of micro-entrepreneurship

Academics have documented how a neoliberal agenda was implemented in low- and middle-income economies since the 1980s under the condition of loans distributed to developing economies by the World Bank and the International Monetary Fund (Mitchell and Sparke, 2016; Natile, 2020; Rankin, 2001; Rizzo, 2017; Soederberg, 2004, 2013). Borrowing states agreed to undergo structural adjustment programmes designed to liberalise local and global trade and deregulate markets so that a self-regulating market based on competition could prevail. The structural adjustments would privatise state-owned resources, banks and industries, and balance government deficits through austerity measures. The influence of Western institutions continued under the norms and codes of the Washington Consensus from 1990 and, consequently, developing economies were restructured to fit into and compete within globalised markets. Economies were developed around ideologies of individual liberty and market flexibility (Amable, 2011; Carroll and Jarvis, 2014; Harvey, 2005; Peck, 2010). To achieve these objectives governments have had a reduced role in controlling economic and social spheres (Harvey, 2005; Soederberg, 2004).

A significant aspect of neoliberalism is the transformation of people into individuals who proactively maximise the potential of their human and financial capital in competition with other individuals and thus contribute to a society of free enterprise (Amable, 2011; Foucault, 2008; Lazzarato, 2009). This notion has evolved in developing economies in the form of micro-entrepreneurship along with financialisation, a specific form of neoliberalism that facilitates and depends on the role of private financial actors. Financialisation is defined straightforwardly as a shift from economies of production to the increasing role of financial motives, markets, actors and institutions, in the operation of the economy (Epstein, 2005). Financialisation encourages individuals to take on debt to improve their financial wellbeing within private, for-profit, markets of finance that are inflated over social welfare and the provision of secure waged employment (Soederberg, 2014). Many scholars contend that financialisation has redistributed financial risks and the management of financial wellbeing to entrepreneurial subjects, often as part of their everyday lives (Chhachhi, 2020; Finlayson, 2009; Kear, 2018; Lai, 2018; Langley, 2008; Lapavitsas, 2013; Lazzarato, 2009; Marron, 2013; Martin, 2002; Mitchell and Sparke, 2016; Mulcahy, 2017).

India has witnessed a shift away from the post-independence socialist ideologies that depicted industrial workers and rural villagers as archetypical citizens and objects of development (Gupta, 1998) to ideologies of enterprise, business, consumption and technology as the source of social mobility and economic growth (Fernandes, 2004; Gooptu, 2007). From 2014, the nation's ruling Bharatiya Janata Party (BJP) government accelerated neoliberalism with shifts in state regulations that have driven self-employment, micro-enterprise and market-based institutions resulting in further casualisation of labour, unemployment and a rise in precarious and informal work (Chhachhi, 2020). Self-employed micro-entrepreneurs now constitute ∼80% of all persons employed in South Asia (ILO, 2019).

The role of FI in neoliberal development: a critical perspective

FI is currently one of the most prevalent development orthodoxies currently used to counter world-wide poverty. It targets 1.7 billion unbanked adults worldwide, including those without an account at a financial institution or mobile money provider (Demirgüç-Kunt et al., 2017). For the World Bank, ‘access to financial services has a critical role in reducing extreme poverty, boosting shared prosperity, and supporting inclusive and sustainable development’ (2014: 1). The provision of (micro)finance to micro-entrepreneurs forms a significant facet of FI policy, practice and commerce, and has contributed to the financialisation of poverty reduction. Following the structural adjustments, regulatory reforms created environments that supported the commercialization of microfinance and encouraged a competitive lending market (Aitken, 2013; Roy, 2010; Soederberg, 2014; Weber, 2006). Financialisation has occurred, for example, through grassroots microcredit programmes seeking to empower (often female) entrepreneurs under the influence of development institutions that devolve responsibility for securing economic opportunity and social wellbeing to individuals (Rankin, 2001; Roy, 2010; Young, 2010).

Critics are concerned that FI exposes previously invisible economies and vulnerable subjects to the workings of profit-driven, globalised, markets (Aitken, 2013; Mader, 2014; Rankin, 2013; Roy, 2010; Soederberg, 2013; Young, 2010). Private finance companies, along with their various technologies, have been institutionalised to supposedly achieve economic development by making credit more available to the poor in such a way that profit is derived (Aitken, 2013; Carroll and Jarvis, 2014; Gabor and Brooks, 2017; Mader, 2014; Natile, 2020; Roy, 2010). This has occurred by making visible, calculating and disciplining the finances of low-income subjects and commodifying their debt and risk (Roy, 2012).

The FI approach has overlooked class-based power, exploitation and inequality in credit markets. Soederberg (2014) reveals unequal power relations in the microfinance industry using a Marxian framework to critique how surplus, low-waged or underemployed workers (required for capital accumulation and the growth of wealth held privately by a capitalist class) are identified as an unbanked population and are brought into the financial market to facilitate FI as a supposedly apolitical strategy against poverty. Mader (2014) is similarly concerned about how the lack of societal wealth among one class of people – the poor – becomes the basis for a financial contract with another class of people able to rent out capital wealth. Thus, rather than redistributing wealth, microcredit is thought to create new relationships of entitlement between lenders and borrowers and financialises relationships between the wealthy and the poor, enabling a market society that reshapes social relationships that contribute to capital accumulation (ibid).

Critics indicate that financialisation and entrepreneurship are increasingly creating conditions for indebtedness and the transfer of financial responsibility to credit-seeking vulnerable individuals who can no longer access financial security through employment rights or state welfare to the effect that precarity is now a source of value and enterprise (Bowsher, 2019; Chhachhi, 2020; Lazzarato, 2009; Mitchell and Sparke, 2016). Meanwhile, the structural inequalities that have produced exclusion, exploitation and financial risk among the poor are not addressed (Brigg, 2006; Carroll and Jarvis, 2014; Gabor and Brooks, 2017; Lazzarato, 2009; Mader, 2014; 2018; Natile, 2020; Soederberg, 2014).

FI in the era of big data and digital payment

Public funded philanthropic organisations, development finance institutions and government institutions are partnering with private fintech companies to progress big data-driven credit scoring, which is used to scope, assess and govern previously invisible customers in low-income countries (Aitken, 2017; Boamah and Murshid, 2019; Gabor and Brooks, 2017; Langevin, 2019). This is occurring as international development institutions and fintech companies are promoting mobile phone payment to facilitate micro-entrepreneurship and self-employment (Natile, 2020).

Big data are typically derived from various devices that continually and automatically generate large data of a scale, volume, variety and speed, previously impossible (Kitchin, 2014). Aligned with positivistic scholarship, big data are analysed computationally and algorithmically, to reveal and predict associations, behaviour patterns, and social trends utilising additional data points, or variables, previously unavailable (Sagiroglu and Sinanc, 2013). ‘Alternative’ credit scoring methods derive big data from non-bank and non-financial sources, such as social media data, mobile phone data, mobile money transactions, utility bill and home rent payment histories, online profile data (education, employment), retail spending histories and e-commerce data (Aitken, 2017; Hurley and Adebayo, 2016; Óskarsdóttir et al., 2019). Big data can be used for psychometric and social network analyses that use machine learning techniques to seek associations between the behaviour of potential borrowers and their financial behaviour, categorising them and calculating and pricing their risk accordingly (Langevin, 2019). These methods are designed to overcome a ‘credit catch-22’ whereby to receive credit a person must first demonstrate their successful history of repaying credit (FICO, 2021). Since the techniques are able to extract data from non-bank sources they are considered to improve access to credit for the unbanked and those who rarely use bank accounts, the majority of whom reside in developing countries and belong to the poorest households in their economies (Demirgüç-Kunt et al., 2017).

The use of alternative credit scoring techniques for FI valorises their use in developing countries by private companies (Donovan and Park, 2019). The United States analytic credit scoring company FICO is currently piloting their new product on data gathered from mobile money users in Sub-Saharan African countries where at least 70% of the population use a mobile phone. The area demonstrating the largest number of active accounts (72 million) and the largest value of money transactions is East Africa where Safaricom and Vodaphone launched the mobile money payment, transfer and credit service, M-pesa. The company is ensuring products are directed to where the most data and thus, profit, can be generated. This motivation is endorsed by the International Finance Corporation (IFC) – a member of the World Bank – who suggest fintech can be used to tap into the markets of small and medium enterprises of developing markets; half of which have unmet credit needs valued at ‘approximately US$2.1 to US$2.6 trillion’ (Owens and Wilhelm, 2017: 1).

The wide range of financial and non-financial devices that generate big data used in contemporary credit scoring require digital and technical know-how, and often the use of a smartphone. The exclusion of the poor from formal financial institutions is now more so conceptualised in terms of a technical issue than previously realised by Marron (2013). Financial: ‘others’ continue to be created who cannot conform with the everyday devices promoted for digitised FI. Increasing digital literacy is now, perhaps, becoming more significant to the FI market than financial education. That is because innovations in alternative data scoring allow ‘bad’ behaviour to be more accurately surveyed and priced, which offers greater security to lenders. In order to expedite digital know-how, governments are using government-to-person payments, such as social welfare payments, to force the production of digital data by those who would otherwise not have used, or rarely use, a bank account (Gabor and Brooks, 2017).

Shifts in fintech use and big data analytics, however, have not overcome the existing issues outlined in the previous section of class-based exclusions. As Kear asserts, ‘being inside the financial system’ does not necessarily produce the emancipatory experience FI advocates assume (2012: 936). That is because making the poor visible to financiers in many cases demonstrates their risk with a poor credit score, which opens them to a subprime lending market in which low scoring borrowers are subjected to higher interest rates and more unfavourable terms in order to compensate for their risk. For example, a FICO credit scoring model using alternative data demonstrates – among a sample of consumers in the United States – that a majority (∼65%) produced a score below 620, whereas ∼30% scored between 620 and 699. A good score is considered to be 700 and 850 excellent. Because the latest methods open access to credit outside of the subprime category for some consumers, their utility in FI is legitimised despite that over half of consumers tested by the FICO model are scored to access only the subprime credit market. The potential for digital FI to radically alter the borrowing experiences of low- and precariously-waged workers is questionable.

Researching auto-rickshaw operators in Bengaluru

Auto-rickshaw taxi operators provide analytical insights into how financialisation is experienced by India's micro-entrepreneurs. Auto-rickshaw services are operated by self-employed drivers, who are from here referred to as auto operators, using three-wheeled motorised rickshaw vehicles. The services are aligned with the Indian state's definition of micro-enterprises: businesses in the service sector with investments in machinery under 1,000,000 INR/∼£10,000 including the self-employed (Ministry of MMSEs, 2019). Operators have been brought into digital FI through their use of online smartphone payment platforms (e-wallets) and online trip booking platforms. In Bengaluru, 200,000 auto operators are now registered (TDGK, 2019). Autos account for ∼10–20% of urban transport mode shares (Mani et al., 2012). Due to the scale of their services, auto-rickshaw trips are a key market segmentation for digital payment companies (Redseer, 2019).

The research was undertaken in Bengaluru based on the aspirations of the local government for its future as a smart city, which indicates an incentive for the digitisation of various services. Bengaluru is becoming younger and, in many areas, gentrified by technologically skilled migrants. A large proportion of paratransit customers demand the use of digital payment. The method aimed for an in-depth study on the particularities of finance and fare-setting of auto operators and therefore, a qualitative approach was taken. Data collection involved semi-structured interviews of 30–60 min undertaken over 12 weeks in 2019 including interviews with 42 individual operators (31 in central city locations, 11 in city periphery locations), four driver union representatives, five finance brokers, six financiers (two private moneylenders, one non-banking finance company (NBFC), two NBFC franchise private moneylenders, one saving co-operative), eight traffic police and four regional transport office (RTO) officials.

Auto operators were recruited on the street using a purposive sampling technique that sought to collect an estimated representation of Hindu and Muslim operators of various ages and of varying socioeconomic dispositions. The later was achieved by recruiting operators working different routes and in areas that are marked with varying degrees of precarity; from central transit stations and shopping malls, to periphery locations. Those working in central and lucrative areas (with many exceptions) have procured access to spaces and associations that enable higher earnings or better working conditions, such as fewer hours worked each day or the opportunity for a day of rest each week.

Financiers were recruited by snowball sampling, asking operators and brokers of their whereabouts. Most are legitimately working as licensed moneylenders under the Karnataka Money Lenders Act 1961 and some were operating as franchises of larger finance companies providing loans on commercial and domestic vehicles. One financier located in a jewellery shop was recruited on the basis of their previous involvement in finance, which eased a discussion of informal practices. I was sensitive to the prospect of participants placing themselves in vulnerable positions as they discussed their practices, experiences and concerns. Considering the ethics of these conversations I chose to position myself as an empathetic listener. It is possible, being a white British female researcher, that I was perceived as reasonably neutral, impartial and non-threatening to those who chose to participate in interviews (Fonow and Cook, 1991). I was visibly an outsider and did not gain access to participants through an influential gatekeeper, which can potentially obstruct trust (Mullings, 1999). Trust was gained with participants by approaching them with a local research assistant, offering anonymity and off-record interviews. I interviewed participants in public shared spaces (a street or coffee shop) rather than inviting them to a more formal space. Although in a privileged position of belonging to an influential Western research institution, in the field, I was someone who apparently knew little about the politics of the associated industry networks or the legality of activities I was researching.

Interviews were either audio-recorded, transcribed and translated by a research assistant. When participants did not wish to be recorded, notes were taken during and/or after interviews. Illicit fare negotiations were discussed openly by auto operators. However, they did not disclose accurately the extent to which passengers were overcharged, of which I was aware based on my experiences of using autos throughout fieldwork, field observations at key locations, and interviews with passengers.

In total 84 interviews were carried out with actors involved in the industry and by cross-referencing participants' narratives, it was possible to determine a convergence in the data collected that signified a credibility sufficient for the purpose of this analysis. For example, the costs and terms of informal and formal loans, the mechanisms and practices of lending and fare negotiating, the use of digital financial technologies and institutions, the roles of actors involved in the industry, the management of subjects, financial risk and operators precarity. These were themes that were identified during fieldwork and revisited later, undertaking a thematic analysis of transcripts and extracting representative participant quotes. Participants were coded for anonymous transcripts (e.g., DD1) based on their role (D = auto operator, B = broker), interview location (A, B, C, D) with an allocated a number (1, 2, 3).

Financing vehicles and experiences of exclusion

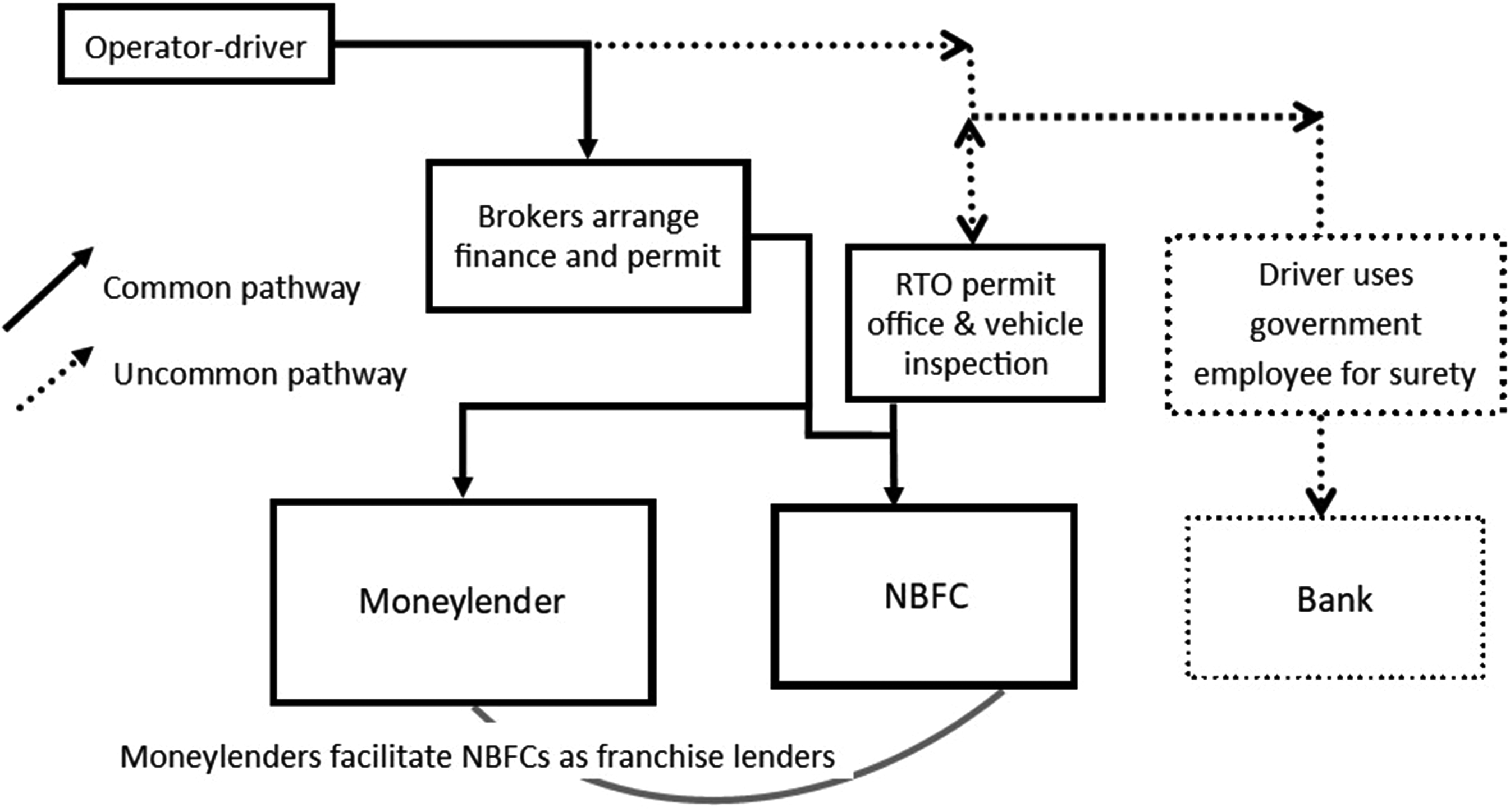

Based on knowledge derived from interviews Figure 1 maps the pathways to vehicle procurement available to operators and Table 1 details the documents and credit scores auto operators must provide to the different lenders available.

Pathways to various financiers for auto operators.

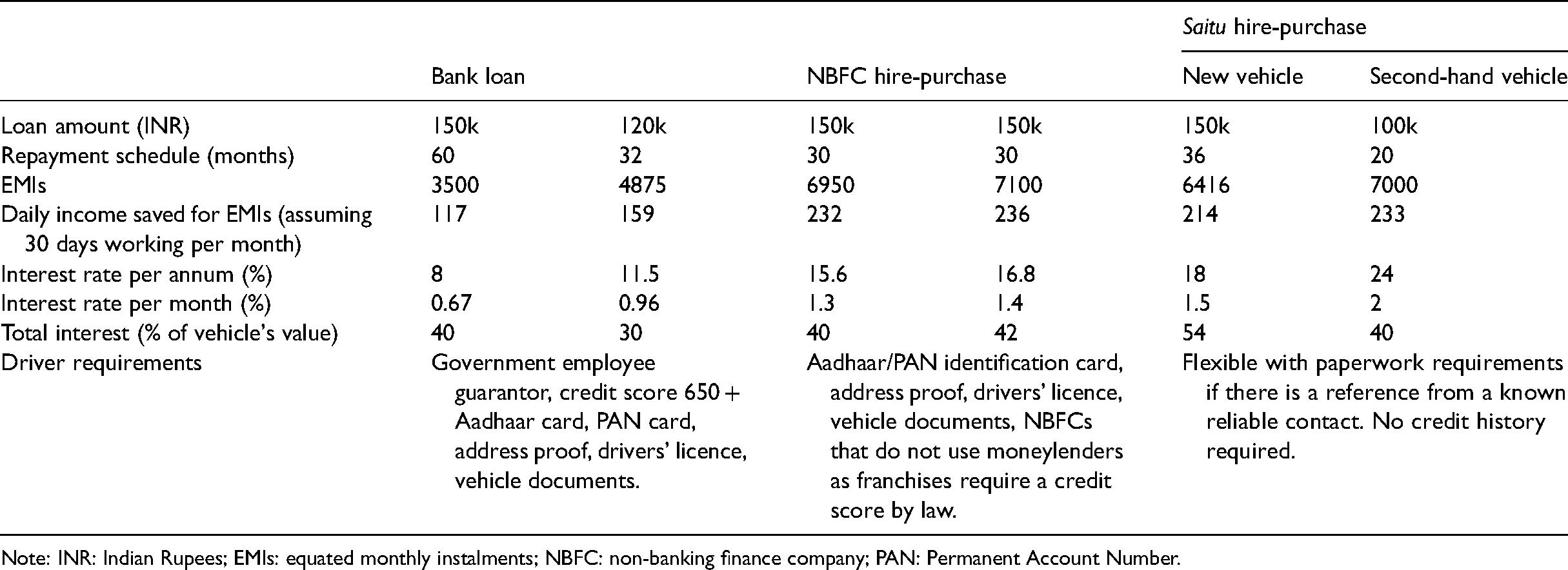

A comparison of auto-rickshaw finance including borrower requirements and equated monthly instalment costs.

Note: INR: Indian Rupees; EMIs: equated monthly instalments; NBFC: non-banking finance company; PAN: Permanent Account Number.

Banks do not usually finance auto operators unless they can provide the surety of a government employee and a worthy credit score. Most auto operators purchase vehicles by entering into a hire-purchase contract with either a private moneylender or an NBFC. NBFCs are registered and monitored by the state's Reserve Bank of India (RBI) to receive deposits and to provide infrastructure for bank related services, including loans, without a banking license. The leading NBFCs providing auto loans are lenders that specialise in transport and logistic enterprises and vehicle finance. These relatively new companies are using existing moneylenders as franchise lenders who have access to a market of auto operators and who are not required to undertake credit score checks to assess borrowers. Moneylenders, instead, use specialist knowledge and their social and economic networks to manage defaulting operators. On rare occasions, drivers approach a bank directly to take a loan for a vehicle using a government employee as surety. Operator workers' unions sometimes assist operators to do this using their social networks.

Private moneylenders are referred to as Saitu lenders by auto operators. The term Saitu is given to people belonging to the Marwari community (originating from Rajasthan), although in Bengaluru we also identified moneylenders with family lineage originating from Gujarat and Maharashtra. Indigenous lenders exist in other areas of India within key merchant communities, such as Marwari, Nat-tukottai Chettiar, Shikarpuri or Multani, and Gujarati (Martin, 2015). They are referred to as indigenous lenders having had a role in India's economy before the arrival of the British colonial government and global systems of finance to supply microfinance to the poor, by the government, as a means to facilitate entrepreneurship. A report of the Study Group on the Indigenous Bankers to the RBI in 1971 details how the government earmarked ‘indigenous bankers’ as a means to supply loans to millions of ‘small borrowers’ ‘with comparable ease and informality’ and ‘on the basis of personal creditworthiness rather than tangible securities’ in order to compliment the ‘formal’ banking system of credit provision (Gupta, 2007: 159). In this way, Saitu moneylenders are considered to operate outside of the formal system but are regulated in order to protect borrowers. Saitu moneylenders' original role as intermediaries between informal and formal economies continues today despite recent technological shifts in line with financialisation.

Moneylenders are the most accessible lenders for operators, and, as Financier 4 describes, ‘can do a loan on trust and not through CIBIL [credit] scores or all those paperwork requirements’. Moneylenders take on more risk than other lenders because they have developed social networks of ‘informers’ to reach and prompt defaulting operators to repay agreed equated monthly instalments (EMIs). Vehicles are seized from defaulters and withheld to prompt repayments and as a last resort are sold to recover loans and interest fees. Vehicles are easily sold in an active second-hand market, which is essential for operators who need to exit early from their hire-purchase contracts to release money for other needs. This is considered acceptable and normal among Saitu financiers and does not affect future access to finance for operators, at least to high-cost loans.

Moneylenders and NBFCs are approached using a broker that functions as a one-stop shop for operators to procure finance, a vehicle (second-hand or new), and vehicle documentation including a permit and vehicle fitness certificate from their local RTO. A down payment of 60,000–80,000 INR (£630–£840), or about 40% of a vehicle's value, is paid to a broker. On a second-hand vehicle, this amounts to ∼25% of the vehicle's value (this figure differs between lenders). A copy of the hire-purchase contract is required in order to get a vehicle permit. The contract is held by the lender who is the agreed owner of the vehicle until the operator-driver pays off the loan and interest. A vehicle cannot be sold without a permit and, therefore, without permission of the lender. These loans are repaid in EMIs usually over 30–36 months for new vehicles and fewer for second-hand vehicles.

Based on interviews with drivers, brokers and financiers, Table 1 further details the different finance options (giving two examples of each) available to drivers, their EMI repayment schedules and the effects of these on the daily expenditures of drivers, as well as the various requirements of operators seeking loans.

The lowest-cost finance available for vehicle procurement is through banks and they offer terms allowing operators to make smaller EMIs over a longer period. NBFCs are the next best option although operators must pay back EMIs over a shorter period at higher interest rates. At the highest cost to operators are Saitu lenders. However, in terms of drivers' EMI repayments, they have remained competitive with NBFCs. The longer repayment schedules of Saitu lenders ensure their EMIs are of no extra cost to operators (Table 1). This means that loans acquired through NBFCs and Saitu lenders bear equal pressure on operators' daily income targets.

Operators' experience of digital FI

Auto operators are drawn into the global financial system through their engagement with a number of technologies that have been used in credit scoring. Most relevant to auto operators is a digital payment of fares demanded by customers and platform companies through smartphone ‘e-wallets’. In future, it is hoped that digital payment will be used for operator's payment of utility bills, house rent, groceries, goods and loan repayments. The appeal of technology for FI to the government of India is evident in its ‘Digital India’ campaign that was announced during a speech by Narendra Modi on 1 July 2015 to an audience in California (India Times, 2015). The campaign seeks to increase digital literacy, access to the internet and digital infrastructure in order to shape the country's digital commerce and governance. The demonetisation ordinance of 2016 was thereafter used to steer the public towards digital transactions since it removed ₹500 and ₹1000 notes (∼£5 and £10) from circulation, creating a sharp shortage in cash notes (Athique, 2019).

By means of increasing digital literacy, bank use and digital payment, the government's 2016 Aadhaar Act has linked digitised identification to the targeted delivery of government welfare subsidies and services. Possessing an Aadhaar card is not mandatory per se, however, it is mandatory for receipt of a wide range of government benefits and services. It is also mandatory for citizens in possession of a Permanent Account Number (PAN) card, issued by the Income Tax Department for filing income tax returns, to link it with their Aadhaar card. The Aadhaar and PAN cards feature in the government's FI strategy. For example, the Jan Dhan–Aadhaar–Mobile payment interface, used for welfare payments, has connected the Aadhaar to the government's FI Pradhan Mantri Jan Dhan Yojana scheme (PMJDY). The PMJDY allows citizens to open a savings account with no minimum balance and offers other benefits, such as accident insurance. Aadhaar has utility in producing new flows of income, bank, transaction and credit history data, linked with personal demographic data that enable credit scoring across a wider population than has previously been possible in India (Athique, 2019).

Among other objectives, by increasing digital payment, the government has set out to advance the information lenders have about potential borrowers (KOAN, 2019). The state set up a credit rating bureau in 2000 consisting of the United States' global company TransUnion to assist in delivering the infrastructure required to undertake credit scores mandated for use by banks and NBFCs from 2007. TransUnion's members gain access to customer scores to assist them in managing investment risk and in devising ‘lending strategies to reduce costs and increase portfolio profitability’ (TransUnion CIBIL, 2020, n.p.). The introduction of credit scoring in India was part of wider global, neoliberal, financialisation of credit designed for efficiency that increases the market's productivity and reduces its outgoing costs by calculating risk and transferring it to individual borrowers (RBI, 2014). By means of highlighting this point I quote Shri R. Gandhi of the RBI who, during a keynote speech, states ‘borrowers with a good credit history will be rewarded for their discipline while delinquent borrowers will no longer be subsidized by lower-risk consumers’ (2015, n.p.).

Despite market and state intentions for fintech to increase FI, auto operators are continuing to experience exclusion from secure and affordable finance. Most operators interviewed are unaware of credit scores since their knowledge of finance is produced through the experiences of other operators and brokers. Financial literacy programmes are occurring through civil society and drivers' unions to counteract this problem. Digital payment companies seek out auto operators at gas stations to encourage them to adopt products that will enable their customers to pay using a quick response code from an e-wallet. Platform trip booking companies Ola and Uber have also been active in educating operators to use digital payment. However, despite the activities of new corporate actors to scale up the use of fintech, digital payments remain limited with only 6% of micro-enterprises in India, including transport workers, using them (KOAN, 2019).

The literacy approach has not substantially contributed to auto operators' FI because a lack of knowledge does not entirely determine their exclusion. Financier 4 shared a common perception that ‘there is such a demand for moneylenders because operators are not educated. They need agents to do their paperwork’. But, he then went on to say ‘They [operators] move around and cannot keep up with their address proof. Then when they go to banks and Shriram or Bajaj [NBFCs] they have a problem tracing their repayment history. Then they come to us’. Financier 4 is describing one of the difficulties operators have in producing data applicable for credit scoring. This problem indicates the mobile and precarious lives of operators rather than their supposed lack of education. Operators living in low-cost rented housing often encounter problems with landlords, which add to their residential movements, commonly every 2 years (DQ2).

Based on the research undertaken it seems unlikely that addressing technical issues in the short term will lead to increased autonomy for operators to access a wider range of financiers and lower cost loans that might address their economic precarity. That is primarily because operators on meagre incomes cannot create the consumer spending, income and household data that would generate a credit score rating deemed suitable for low-cost finance provided by banks. Additionally, their income falls within a tax-free allowance and, therefore, operators have had very little incentive, or need, to report it to the Income Tax Department and therefore do not use PAN cards.

Furthermore, there are significant differentiations in the use of digital and cash monies in India determined by class that is not easily overcome through education because of the social meanings associated with cash (Zabiliūtė, 2020). This is compounded by a lack of trust in digital technologies among operators. Examples given were issues with activating ATM cards and not receiving fares into their digital wallets. There is a concern among operators that they might be taken advantage of by those who are more technically literate. Distrust was not limited to operators and one broker thought that cash loan repayments reduced the possibility of an auto operator ‘cheating’ a lender by cancelling direct debits, whereas a transaction in cash offers a material confirmation. This is relevant when operators delay an EMI so that they can make an alternative and more urgent payment.

A number of everyday inconveniences and costs associated with digital payments further influence operators' withdrawal from them. For example, DA1 states: ‘It's very difficult to pay rent to the vehicle owner every day if fare payments are credited to a bank account’. The government have placed charges on ATM use and a minimum withdrawal limit of 100 rupees to deter the use of cash, which mostly affects those needing to withdraw small amounts frequently. Here, the ‘unstable incomes of the poor’ are in conflict with the ‘financial stability stipulated by financial institutions and cashless infrastructures’ (Zabiliūtė, 2020: 80). Furthermore, there are gender norms in saving and handling household expenses. Operators are accountable to take a certain proportion of their salary to their spouse and handing over cash on a daily basis forms an obligation on operators. Accruing cash ‘under the mattress’ is bound to its materiality and signifies distrust in financial institutions and the immateriality of digital money, whilst a sense of security, on the other hand, is initiated through the personal guarding of cash (Sjørslev, 2020). The significance of gender norms in managing household finances is demonstrated by DB4 who claims ‘my wife is my safety’.

The experiences of auto operators contrast with the efficiency of digital transactions as promoted by advocates. For example, operators are sensitive to the temporality of digital payments. DH1 commented that if his first ride was paid online then the simple act of buying a morning cup of tea became uncertain. Those using trip booking platforms preferred the next day payments of Ola compared with the weekly payments of Uber. These are issues faced by those who utilise all of their income on their outgoings and have little money to save in an account. These issues and inconveniences are significant barriers to operators in accepting digital fares and thus in creating the credit scores used by NBFCs and banks to determine their chances of timely loan repayment. Ultimately, though, if operators were to evidence their income, credit and consumer histories, the data would unlikely produce credit scores that satisfy the needs of banks. That is since their low-cost interest fees cannot cover the costs and risks associated with customers who are more likely to default on payments. The credit scores of auto operators given their current income and employment precarity would likely only provide access to subprime NBFCs.

Auto operators' fare setting practices

Micro-entrepreneurs working as rickshaw taxi operators have a history of precarity in Southern and South East Asia. Colonial governments sought to restrict their operation through various policies such as restricting permit allocation, introducing laws that relegate services from main roads, city centres or terminals in favour of allocating space and travel demand to more advanced forms of motorised-vehicular traffic most relevant to the upper- and middle-classes (Notar et al., 2018; Pante, 2014; Warren, 1986). These class-based policies continue today and impact operators’ ability to negotiate with local governments for improved terms of employment. The auto operators participating in the research comprise almost entirely of working-class (self-identified) men embedded in cash-based economies. They tend to set themselves a target daily income of 1000 rupees (∼£10–£11). From this, operators deduct fuel costs, daily subsistence and vehicle rental fees or loan repayments (if applicable). Most take home 500–700 rupees each day. The Indian states do not intervene to subsidise the procurement of vehicles, nor raise the wages of self-employed micro-entrepreneur operators.

Drawing operators into formal finance markets using fintech does little to improve their working conditions, low incomes or the cost and precarity of their debt. However, additional to the significant caveats of digitising FI, the transparency instilled in digital payment poses a problem for operators managing their economically precarious positions through informal fare negotiations. The fare setting strategies of paratransit services operate between binary categories of informal and formal, and have ensued, at least to some extent, because of neoliberal economic policies that have shaped their governance and precarity. In certain contexts, as Rizzo (2017) describes for Dar es Salaam, competition within and across various paratransit services has contributed to the low incomes of paratransit operators. Additionally, the deregulation of paratransit, pursued under neoliberalism, has resulted in governments' subsequent difficulty in re-regulating services and their operation between formal and informal mechanisms (Cervero, 2000; Rizzo, 2017).

When working in areas they are familiar with, operators know the price of a trip according to their fare meter and ‘based on that’, explains DD2, ‘ask 10–20 rupees more’. This is a common example of fare surcharging, although a modest one, whereas in lucrative locations (bus, metro and train stations, shopping malls and hospitals), fares can be negotiated up to as much as double the meter rate (Author, forthcoming). In these spaces, auto operators have divided into peer/kinship associations they call ‘unions’. They often pay extortion money to the police who, either overlook their operation in spaces not legally allocated to autos or, assist operators in keeping a space closed to non-members of an association. The additional fares charged in these areas substantially impact travellers who are unfamiliar with the city and cannot easily predict fares (ibid).

Tacit knowledge is used to calculate a customer's willingness to pay based on any urgency in their need to travel, if going to an evening event, accompanied by young children, or if elderly. In particularly congested areas of the city, autos offer an advantage over other public transport as they weave through standing traffic. Operators ask for higher fares through congested areas to offset the time of being ‘stuck in traffic’ (DB1) and the costs of ‘burning [additional] gas’ (DF1). Congestion can also surge during heavy rain, elections and festivals. At these times operators charge passengers one and a half times the fare rate. Operators' tacit fare calculations are a set of entrepreneurial practices set to profit from, geographical and temporal circumstances, as well as class distinctions and their conjunction with the city's geography. These practices are required to survive on low-profit margins and to compensate for costly and insecure finance. Given that most operators practise illegal fare setting techniques, there is resistance to having those transactions opened for monitoring, which is likely made possible through removing cash payment and the discretion it affords (ibid). Digitised forms of FI are threatening the techniques that low-income entrepreneurs currently use to self-manage their precarity, which remain necessary even as they are drawn into formal mechanisms, institutions and markets of finance.

Conclusion

Micro-entrepreneurship is imparted through neoliberal policies that have reduced opportunities for waged employment and have instilled an ethos for individuals to seek out livelihood opportunities that cater to market demands. Responsibility to manage the risks associated with debt is passed on to self-employed, self-starters. Studies have suggested that formal sector finance has the potential to improve auto operators' income by overcoming the highest interest rates of indigenous moneylenders that are not fully compensated, additional to a reasonable income, within the government's flat-fare rate (Chadhar, 2016, Garg et al., 2010; Harding et al., 2016). However, this solution cannot be actualised without first understanding the difficulties many micro-entrepreneurs experience with fintech, their exclusion from credit scoring and that global processes of financialisation do not guarantee financial security. Rather, these processes tend to reproduce the precarity of paratransit labour (high monthly repayments and vehicle asset seizures). Beyond the case of transportation labour, questions arise about the implications of FI as a development ideology, its increasingly technological apparatus, and its private ownership and management. It is difficult to see how policies that seek to open a market of subprime borrowers to finance companies by evidencing their incomes and credit histories will achieve economic empowerment. That is since being on the inside of the financial system – in this case gaining access to NBFCs – does not place micro-entrepreneurs in a position of greater financial autonomy and freedom (Kear, 2012). Fitting risky subjects into mainstream systems that calculate their risk based on digital data flows will not necessarily reduce the cost or conditions, of their credit. Nor will it ease the financial precarity of micro-entrepreneurs experiencing ongoing class-based exclusion from lower-cost and more secure bank loans.

The lowering of interest charged by NBFCs may legitimate the adoption of technologies that facilitate alternative credit scoring for FI. However, low-income auto operators have little to benefit while they gain no additional security over loan repayments through NBFCs, and have less flexibility to access finance or to sell their vehicles to release equity when necessary without it affecting their access to future credit. Rapid changes to payment technologies are also threatening the strategies devised to fulfil paratransit operators' hire-purchase finance contract obligations (among other household and business expenses). Meanwhile, private, formal, financial institutions (NBFCs, e-wallet and other fintech companies) are profiting from a steady supply of low-income working-class entrepreneurs seeking credit and from whom capital can be extricated with greater efficiency under the guise of financial empowerment. This paper demonstrates that financialisation and related digital forms of FI are contributing to the continuation of inequitable structures of social class from which rentier capitalists profit. These profits circulate within private markets of finance.

In the future of the less-cash Indian economy, self-employed and low-income workers, who are rarely visible as human agents, may well be steered into systems of income evidencing and credit scoring through FI programmes. They are yet to receive surety from governments that their right to work in the city is secure, and without are not particularly moving away from the exploitation previously suffered through their dependence on indigenous and informal moneylenders. Unless conditions of employment are improved for the self-employed to the effect that they can gain access to the terms and interest fees more closely aligned to those of bank credit, underbanked micro-entrepreneurs will not benefit as much from digital FI as its advocates promise.

Footnotes

Acknowledgements

Many thanks to Professor Tim Schwanen for guidance on earlier edits of this manuscript and to the anonymous reviewers for their contribution to the publication.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the PEAK Urban programme, funded by UKRI’s Global Challenge Research Fund (grant no. ES/P011055/1).