Abstract

Our current understanding of knowledge generation over geographical distance relies heavily on studies that focus on producer–user or headquarter–subsidiary settings. Less attention has been paid to the geographical particularities of knowledge exchanges in mergers and acquisitions, which involve high costs and an extraordinary degree of risk and uncertainty with potentially significant (positive or negative) consequences for the respective firms and regions alike. To keep the risks associated with such complex long-distance transactions at bay, buying firms strongly depend on robust knowledge about the structure and value of the target units while the sellers require reliable knowledge about the goals of the acquisition and the price the buyer is willing to pay. This paper aims to investigate the spatiality of related knowledge exchanges during merger and acquisition procedures by analyzing the role of face-to-face contacts and investigating the mechanisms to establish trust in undertaking such risky endeavors. Our empirical analysis focuses on national and international corporate acquisitions and takeovers involving firms located in Germany. It is based on semi-structured in-depth interviews with actors involved in mergers and acquisitions, conducted since 2012. We distinguish between the two extremes of relational and auction-based merger and acquisition procedures and systematically analyze in a process perspective (a) the conditions under which knowledge is exchanged over distance, (b) the importance of temporary proximity and how secretive geographies of meetings evolve, and (c) the ways in which trust is created and uncertainties are reduced.

Introduction

Although economic geographers have long emphasized the importance of knowledge generation in local settings, the competitiveness of firms in the global knowledge economy cannot be reduced to localized learning capabilities alone but strongly depends on their ability to participate in knowledge exchanges 1 over geographical distance (Bathelt and Henn, 2014; Malmberg and Maskell, 2006). Much of our current understanding about such knowledge flows rests on studies about ongoing producer–user or headquarter–subsidiary relationships (Grabher et al., 2008; Lundvall, 2016). In contrast, relatively little attention has been paid to the spatiality of knowledge exchange processes in mergers and acquisitions (M&As), which are characterized by extremely high costs and an extraordinary degree of risk and uncertainty with potentially fundamental (positive or negative) consequences for the respective firms and regions alike. These processes have fundamental implications for regional development, impact multiple locations simultaneously, and require boundary spanning activities across different institutional contexts (Glückler and Bathelt, 2017; Liu and Meyer, 2020). As such, M&A processes are of fundamental interest for both management scholars and economic geographers. The types of knowledge that are exchanged in M&As are quite different from those between economic units in routine transaction or production processes and the consequences can be tremendous if the well-being of many employees and their families depends on the outcome. Therefore, knowledge exchanges associated with M&As are not so much focused on solving problems but on minimizing risks and verifying opportunities.

Current research on M&A processes spans across various disciplines, including economics, business, finance, management, and law. Related studies have dealt with different aspects of M&As, including economic returns to acquiring firms (Fuller et al., 2002), challenges associated with business integration (Schweiger and DeNisi, 1991), post-acquisition performance (King et al., 2004), learning processes associated with failures (Sitkin, 1992), repeated acquisitions (Haleblian and Finkelstein, 1999), and factors driving M&A activities (Mitchell and Mulherin, 1996). Economic geographers have also investigated M&A processes, for example by focusing on the relevance of geographical proximity between buyers and sellers (Boschma et al., 2016; Rodríguez-Pose and Zademach, 2003), the spatial concentration of investment banks (Colombo and Turati, 2014), as well as the extent and distribution of cross-border acquisitions (Zademach and Rodríguez-Pose, 2003).

There is also a literature on knowledge flows associated with M&As, mainly in international business and organizational studies, with contributions about negotiation tactics and styles (Elahee and Brooks, 2004; Zhao, 2000), employee retention (Ahammad et al., 2016), links between communication approaches and M&A outcomes (Angwin et al., 2016), and the role of boundary spanners in reverse knowledge flows in cross-border acquisitions (Liu and Meyer, 2020). Studies have further investigated knowledge exchanges in networks of service providers (Lo, 2003) and how sociocultural interfirm linkages between merging firms affect knowledge flows (Sarala et al., 2014). Despite this rich body of research on M&As, only limited attention has been paid to the spatiality of the M&A process and the role of face-to-face contacts in facilitating knowledge exchanges at various stages (Junni et al., 2012; Reynolds et al., 2003). This is surprising as temporary proximity and face-to-face interaction are essential to finalize M&A processes (Clarke, 2020).

To keep the risks associated with such complex transactions at bay, the buying firm depends on robust knowledge about the structure and value of the target unit. By aiming to generate long-lasting bonds and a stable basis for interaction over distance (Boschma et al., 2016; Malecki, 2010), the seller or vendor requires reliable knowledge about the goal of the acquisition and the price the buyer is willing to pay. Taking this as a starting point, this paper aims to investigate (a) how different parties involved in such risky endeavors exchange knowledge over distance in different stages of the M&A process, (b) how they systematically make use of temporary face-to-face contacts thereby establishing secretive geographies of meetings, and (c) how a level of trust is achieved, which is necessary to finalize the sales process and mitigate the risks and uncertainties involved. In investigating the roles of space, negotiation meetings, and co-present interaction in the context of M&A processes, our study links to work on the importance of face-to-face interaction (Storper and Venables, 2004), temporary proximity (Bathelt, 2019), and processes of knowledge creation over distance (Bathelt and Henn, 2014). This paper particularly extends the proximity literature (Boschma, 2005), which suggests that economic processes require a mix of spatial proximity along with a minimum of cognitive, cultural, technological, or organizational proximity (in the sense of affinities). In our analysis, we use a process perspective to identify the underlying mechanisms that generate a level-playing field for the parties involved in M&As.

Our empirical analysis focuses on national and international corporate acquisitions and takeovers involving firms located in Germany and is based on in-depth interviews, conducted since 2012. We find that the knowledge exchanges related to M&As rely on repeated, highly confidential, and temporary face-to-face meetings between decision makers of the involved firms and supporting third parties or intermediaries, such as specialized lawyers, investment bankers, and management consultants (Walter et al., 2008). These sometimes-secretive meetings take place at different locations and are supported by virtual forms of communication. However, there are different processes in place of how such M&As are organized. We distinguish between two extreme forms: the relational or exclusive procedure and the auction-based procedure.

The relational procedure is organized as a one-on-one knowledge exchange and negotiation between two transaction partners. The vendor is strongly interested in the continued existence of the business unit to be sold and selects a potential buyer before the actual consultations and negotiations begin. Crucial knowledge exchanges in the initial stages are secretive and limited to a small number of players from both firms and extend over a longer time period. Intensive face-to-face meetings serve to create professional trust between the partners and confidence in the transaction.

In contrast, the auction-based procedure is characterized by a high degree of anonymity between the parties that typically do not need to know one another beforehand. This procedure involves one seller and a larger number of potential buyers. We observe how, in an organized market setting, potential buyers receive increasingly more information about the target unit as their number decreases. Intermediaries intentionally generate a seller’s market that potentially allows the vendor to maximize the sales price if the procedure comes to an end. Although this setting deliberately creates uncertainties at the expense of the potential buyer, mechanisms are in place that allow the buyer to reduce risks. In a highly standardized and controlled process, the number of parties is gradually reduced to a one-on-one setting and intensive face-to-face contacts only matter toward the end.

Our paper proceeds as follows: the next section provides the framework for studying knowledge flows and their spatiality during M&A processes. It discusses the specific framing conditions, learning challenges and risks involved in these processes and introduces the relational and auction-based procedures as two main forms. This is followed by a discussion of the methodological challenges related to investigating knowledge transfers in M&A processes. In the empirical part, we discuss how the two M&A procedures differ in terms of contact initiation, the steps involved in the so-called due diligence process, the social context and spatiality of the process, as well as the management of trust and risks. Finally, we conclude by summing up and discussing under which conditions different M&A procedures are chosen and what their consequences are.

M&A processes and knowledge exchanges in spatial perspective

M&A processes are transactions with a low frequency (as there is typically only one deal between two transaction partners) and an extremely high factor specificity with corresponding high transaction-specific investments on both ends at the selling and buying firm. According to transaction-cost theory, such a transaction would most likely be carried out under unified control as an intrafirm transaction (Williamson, 1985). However, in the case of M&A processes, this is ruled out as the units to be linked are by definition part of different firms and as both partners do not know each other's business structure at the outset. This leaves three-sided control (a neoclassical contract with a third party as accepted arbitrator) or two-sided control (a relational process involving cooperation between the seller and buyer) as governance options that both are subject to imperfection. Such a transaction context becomes especially complicated as it is characterized by very high risks and uncertainties and a situation where opportunistic behavior of both parties cannot be ruled out. It should be emphasized, that the nature of knowledge exchanges and risks involved in M&As is closely related to the spatial and social separation of the two entities involved (Bathelt and Henn, 2014) and that its analysis consequently requires a spatial perspective (Bathelt and Glückler, 2011). The business units are typically embedded in different institutional contexts and territorial production systems and knowledge about each other is incomplete and not easily accessible.

The challenge of M&As is that the firms involved in these processes have to get together and generate proximity at various levels (Boschma, 2005). First, the buyer and seller have to literally come together to negotiate the conditions of their potential transaction, inspect facilities and technologies, and sign a contract face to face. Second, as described in the proximity literature, firms have to ensure that sufficient cognitive, cultural, and technological affinity exists between them (Boschma et al., 2016) to generate trust in a workable outcome. They need to bridge the distant contexts of the corporate units involved to be able to judge the appropriateness, benefits, and costs of the M&A process. Because of different institutional conditions, a good fit of the buyer and seller is anything but guaranteed (Glückler and Bathelt, 2017) and boundary-spanning activities are necessary to accommodate effective knowledge exchanges, especially in international M&As (Ahammad et al., 2016; Liu and Meyer, 2020). This would normally require intensive face-to-face communication and frequent personal visits and inspections (Storper and Venables, 2004).

However, for both the buyer and seller, failure in the process would generate high economic costs and a termination could have long-term negative consequences. Since a deal may also go along with major uncertainties and negative impacts on the workforce of the acquired business unit (for instance, because of looming job losses and fundamental restructuring), the seller is usually interested in keeping the negotiation process secret until confidence into an agreement is achieved (Harwood, 2005). This approach helps to temporarily push aside job concerns in the workforce and criticism by media and regional policy makers, which—in the worst case—could call the deal into question and/or affect the value of the business unit. Vice versa, the buyer carries a high risk by investing a large amount of money into the transaction without being certain that the post-deal structure will be profitable. In addition, the buyer's value is at risk. Because of the risk of failure, personal contact and co-present interaction in the early stages are purposely limited, and the parties involved have to find different ways of exchanging knowledge, clarifying questions and creating trust over distance (Bathelt and Henn, 2014) without being able to benefit from ongoing local buzz (Bathelt and Glückler, 2011; Storper and Venables, 2004). To achieve a sufficient level of proximity or affinity to come to a conclusion of the M&A process, the buyer and the seller employ a mix of electronic and virtual communication in combination with temporary proximity through personal and/or virtual meetings (Bathelt, 2019).

From a process perspective, two generic types of M&A procedures have developed in this context (Heidrich and Mitterlehner, 2014), which are both associated with opportunities but also imperfections and high risks in spanning the locations and contexts of buyer and seller: In the auction-based M&A procedure, quasi-three-sided control 2 is the dominant governance form with intermediaries organizing a sales process in the form of an auction. By so doing, the conditions for a seller's market are created and strict rules are defined as to how the transaction partners involved must interact. In this process, the seller faces multiple potential buyers from different locations, not knowing whom they are competing against and, at least initially, who the seller is and where the firm is located. In a stage-wise process, the number of bidders is successively reduced until a one-on-one situation is reached and a contract is signed (Aktas et al., 2010; Bruner, 2004). The idea behind this process is to find a solution that maximizes the returns for both parties. From a regional perspective, there are many caveats in this process as consequences of a deal, for instance regarding employment, are not taken into consideration. Additionally, the largest and most powerful firms, rather than the most productive ones, may succeed by offering the highest price. Finally, inherent in the process are limitations as to how buyers can evaluate risks involved in the transaction, and what outcome can be expected.

Under two-sided control, initial uncertainty generates a major barrier for the M&A process. As opposed to the auction-based procedure, the exclusive or relational procedure 3 begins from the outset with a one-on-one negotiation situation between one seller and one buyer, including some knowledge about their regional and institutional contexts. Since the risks of failure are high, both parties aim to generate embedded relations in the early stages of the process to reduce transaction costs (Granovetter, 1985). It is through high commitment on both sides that relational control becomes a viable option. As the degree of embeddedness increases and the social context of both firms becomes part of the negotiation process, the risk of exit at later stages decreases while prospects for successful integration after the deal grow (Bruner, 2004; Hajro, 2014; Valliere et al., 2008). However, as with the auction-based procedure, there are also imperfections. Since the potential partners principally settle in a very early stage, the danger of a mismatch and suboptimal outcome is substantial as the buying party may not be the best fit. Although locational implications may be explicit components in the seller’s considerations, a mismatch could hamper regional development.

The two procedures differ fundamentally in terms of their governance structure and spatiality and a crucial aspect in both is how the actors involved move from a multilateral to a bilateral negotiation context (Callon, 2017)—a transition that is closely associated with risks of failure. Although both procedures are in principle known in the literature (Aktas et al., 2010; Bruner, 2004), the spatiality of knowledge exchanges, associated learning processes, and risk and trust management have not received much attention (Bathelt and Henn, 2014).

In the context of the German variety of capitalism, which is characterized by a high degree of collaborative relationships between workers and management, unions and employers, firms and banks, and producers and users (Hall and Soskice, 2001; Soskice, 1999; Streeck, 2009), deliberative institutions are crucial for economic success by encouraging, enforcing, and reproducing ongoing interaction patterns even between parties that may follow opposing goals (Green and Paterson, 2005; Katzenstein, 1987). With this in mind, we expected the relational M&A procedure to be dominant in the German context, especially since bidding processes and different forms of due diligence developed momentum only in the late 1990s—much later than in Anglo-Saxon countries (Bengel et al., 2016: 10). Although relational M&A procedures indeed played an important role in our empirical research, we found, however, that a variety of strategies were performed and that auction-based procedures were also important. After describing our methodological challenges in the next section, we discuss the spatiality of knowledge exchanges, the social character of interactions and risk- and trust-related challenges of both procedures in the empirical part.

Methodology

Since the goal of our research was explorative in character, we followed common suggestions of how to gain theoretical insights from case study research (Eisenhardt, 1989; Yin 2017) and conducted in-depth interviews with actors engaged in M&A processes. The empirical circumstances of this research were difficult though since individuals and organizations involved in M&As are tight-lipped about their experiences—unwilling to talk about associated practices in detail. Additionally, it was challenging to access databases from which to select firms to be interviewed. When we became interested in such transactions in the late 2000s, our initial attempts to generate a sample of M&A cases failed. Although we paused our research plans at this point, the general idea remained vibrant. Through other firm interviews conducted in numerous research projects over time and regular contacts with business organizations, we developed contact networks and a small number of personal, trust-based relationships which helped us identify interview partners for this research.

We adapted new goals and changed our strategy from conducting a larger survey of firms to focusing on in-depth interviews with experienced firm managers and other involved actors. For this study, we employed a purposive and snowball sampling design and identified interviewees based on pre-existing contacts that had, in one case, already existed since the 1980s. We stopped looking for further interview partners when maturity was reached in our sample (Eisenhardt, 1989) and responses became repetitive. At this stage, we concluded that there is enough crucial information about the main procedures and knowledge processes involved in M&As to provide thick description.

Although we had many additional, more informal exchanges with firm representatives and other M&A actors, this paper is based on 10 in-depth interviews. Four interviews were conducted with firm managers (buyers), three with M&A consultants, and three with lawyers specialized in M&As (both on the seller and buyer sides). One interview was conducted in 2012, the others in 2018 and 2019. Our interviewees were all males between 40 and 60 years of age, who had leadership positions in their firms. Most interviews were related to acquisition processes in the manufacturing sector although we also discussed examples of service industries (mergers were only in a minority of cases part of the interviews). It is important to note that all interviews focused on firms located in Germany that acquired other businesses nationally or internationally since it can be assumed that the context of the German variety of capitalism influenced the processes we observed. M&A procedures in other political–economic contexts could be differently structured. Although the overall number of interviews appears small, it should be emphasized that these covered the experience of several hundred M&A processes over a period of about 30 years.

The interviews were not focused on specific M&A projects. Instead, the unit of analysis in our interviews was the M&A process. We asked our interviewees to systematically describe typical aspects of M&A process and its different stages. When answers were given, we always encouraged our respondents to use a recent example to describe precisely what had happened and why. In the next step, we asked whether sometimes processes deviated from that structure and again prompted for specific examples and how often those would occur. Through this, we were able to compare practices across different M&A processes. Overall, we believe our interviews provide a very good overview of the important knowledge generation processes in M&As as they unfold in the German manufacturing sector. Although we are aware that not all processes end with a signed contract, the examples discussed in our interviews only included completed M&A processes or cases where partners walked off the table in a very early phase. 4

We used an interview guide to structure our questions but were flexible to add additional questions, change the focus of questions, or follow specific leads of the respondents as far as these were relevant for the goals of this paper. Our interviews began with questions regarding the interviewees’ experiences in M&A processes and at which stage and in what role they were involved in these processes. The next set of questions was related to the initiation of contacts in the M&A process and the first meetings between potential sellers and potential buyers, as well as the clarification of expectations between the parties involved. A large part of the interviews then focused on the due diligence process during which buyers systematically collect information about their acquisition targets in an attempt to control for risks and determine the final sales price. This part included questions about the context, frequency, and procedure of meetings and the types of knowledge exchanged. This was followed by a series of questions about the social character of the meetings and their spatiality, and how both evolved during the M&A process. The final part of the interviews referred to how risks and trust were managed throughout the process. The interviews lasted between one and two hours and took place on the premises of the interviewees' firms, all in a trustful and open atmosphere. All conversations were recorded and later transcribed, coded, and further organized for qualitative content analysis using the software MaxQDA.

Knowledge flows in the relational M&A procedure

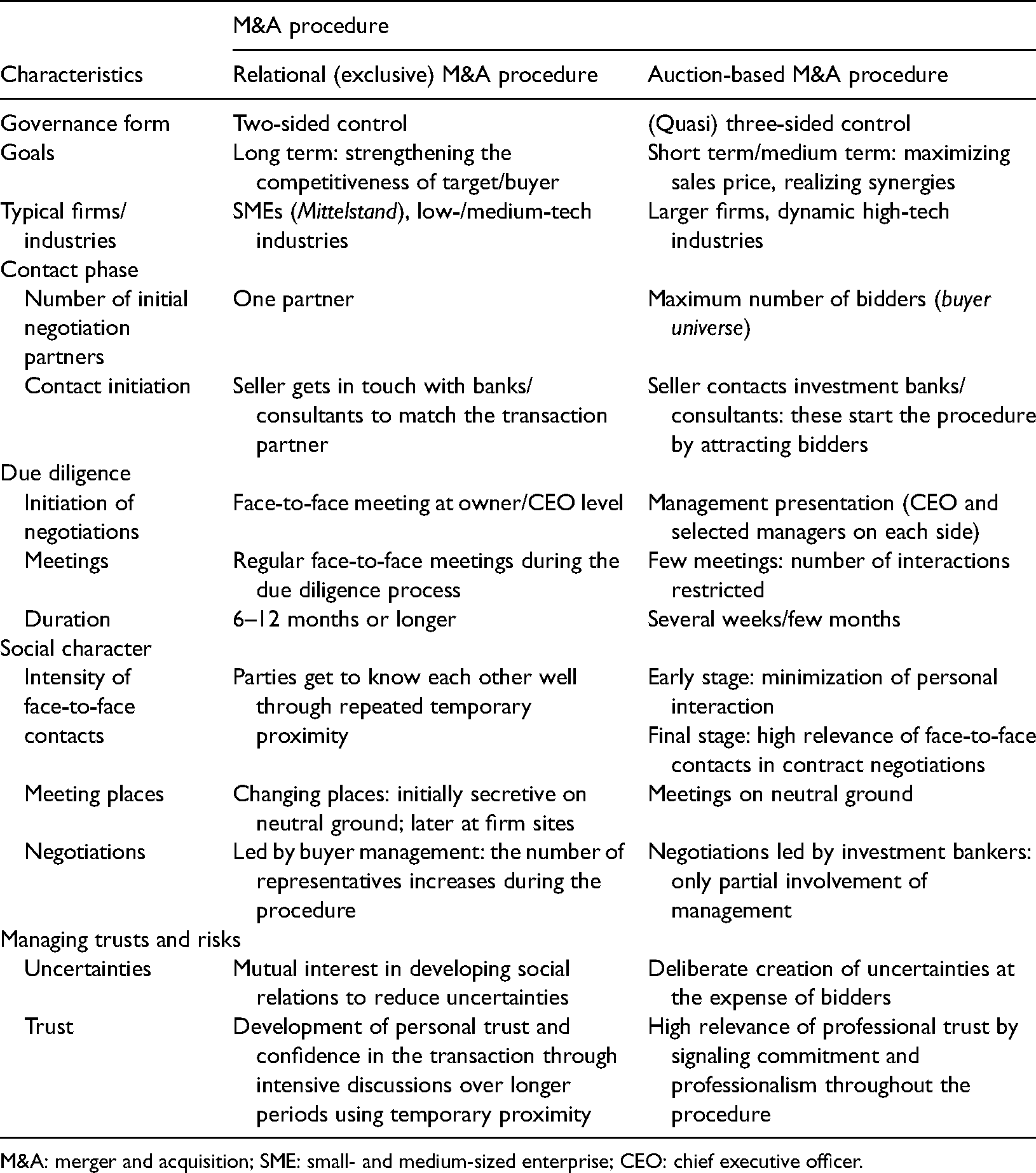

The M&A process we expected to prevail in the context of the German economy was the relational procedure. Here, consultations between the parties occur until mutual agreement is achieved that is advantageous to both and results in a new business entity that can realize synergies from the formerly separate operations. Indeed, we found that such processes played an important role in the German economy and were especially popular in the so-called German Mittelstand, 5 which is at the core of the competitiveness of the German model of capitalism (Streeck, 2009). Relational M&A procedures are organized as one-on-one knowledge exchanges and negotiations between two potential transaction partners. Therein, the seller has a strong interest in the continued existence of the corporate unit to be sold, which is often the accomplishment of a person’s entire work-life (Deloitte, 2012: 29). A potential buyer is selected before the actual consultations and negotiations begin. The procedure extends over a longer time period during which professional trust is created (Ettlinger, 2003) and risks and uncertainties are minimized (Table 1).

Stylized process characteristics of relational and auction-based M&A procedures.

M&A: merger and acquisition; SME: small- and medium-sized enterprise; CEO: chief executive officer.

Contact initiation

In the relational M&A procedure, a key question is how the seller and potential buyer find each other before negotiations start. According to our interviews, the initiation often begins with the seller’s plan to give up a certain business unit. In the German Mittelstand, this can be associated with the retirement of the owner who aims to find a new future for a lifetime’s economic ventures and to cash in on prior business successes (Weber, 2009). However, there may also be other rationales at play, for instance, if a diversified firm aims to focus on core competencies and decides to sell off other business units (Hinne, 2008).

The seller in the relational procedure often starts by contacting the house bank about these plans. The bank then conducts an initial check of the respective business unit and collects information for the development of a short anonymous information leaflet, referred to as teaser, which characterizes the selling unit with some basic data. The teaser is distributed to other banks and important players in the industry. Additionally, potential buyers are directly contacted, and the anonymity of the sales target may be given up. Potential buyers in turn often independently contact banks or M&A consultants to express their interest in acquiring new business units and specify what industry segment and business scale they are thinking of and the geographical market they aim to cover through an acquisition.

As a result, the banks or consultants become active in trying to find matching buyer–seller pairs. Once contact has been established and an interest from both sides has been signaled, an initial meeting is arranged at the owner or chief executive officer (CEO) level. In this meeting, the seller and buyer scan each other to verify their interest in the transaction and compatibility of goals. Since the potential costs and risks of a failed M&A process are substantial, both parties have an interest to quickly come to a mutual agreement indicating that they wish to continue with this procedure and that they have a rough idea about the value of the transaction. One manager explained how the top representatives will discuss the magnitude of the sales price: “This should be done early on to avoid talking over each other’s heads. This is often done at a personal level.” 6 The owners try to reduce uncertainty in the negotiations by “exchanging a house number [price tag] for the deal—for instance stating a multiple of the sales volume or some EBIT 7 ratio or other indicator. This is not a fixed price but a rough agreement about the magnitude.” The interviewee insisted that “one wants to know that this deal is about 20 million Euros, not 10—that needs to be fixed before operative due diligence can begin.” If such agreement is found, commitment is established and negotiations can start.

Due diligence process

What follows is a so-called due diligence process during which all aspects of the business unit relevant for the buyer are discussed. The idea of this process is to identify risks and opportunities of the business unit to be acquired to see whether the original sales price is adequate. If risks are identified they become an object of negotiation. This can for instance lead to a reduction in the sales price. In extreme cases, negotiations might be terminated if both sides cannot come to an agreement (Straub, 2007). The due diligence process covers multiple aspects of the business and differs according to industry and buyer needs. Due diligence topics are dealt with one after the other in a structured form and typically will not be brought up again once discussed. Among the topics of prime interest are (a) liabilities, risks, and future business plan; (b) product pipelines and licenses; (c) quality control; and (d) purchasing. The entire process can be subdivided into financial, legal, commercial, human resources, management, pensions, tax, environmental, information technology (IT), technology, intellectual property, and anti-trust due diligence stages (Howson, 2018). Once these topics are discussed, a sales price will be fixated as a basis for further negotiations.

Typically, the seller establishes a physical data room with all sorts of detailed information about the respective due diligence topics that can be used by buyer representatives for a pre-defined time period, usually one day. Documents have to be checked in that data space and cannot be taken home. In recent years, as our interviewees mentioned, firms increasingly use virtual data rooms with temporary remote access. This is quicker and cheaper for the buyer, but it also makes it more difficult to guarantee the confidentiality of the data.

Each phase of the due diligence process begins with an analysis of the prepared data by the buyer and leads to discussions about open issues, potential problems or aspects that are not well documented. In areas where the seller is lacking specific expertise, external experts may be involved to conduct an analysis of the seller’s situation for later deliberations.

Since there are many relevant topics, these are dealt with in sequence, and meetings at each stage are organized between specialists of both firms to discuss questions of the buyer as our interviewees described. If discussions focus on sensitive aspects or the sales price, the chief negotiators will immediately get involved. Teams from both firms meet over an extended time period repeatedly to deal with different due diligence aspects. Once a topic has been discussed and questions have been clarified to the extent that both parties are satisfied, the next topic will be approached. Although the due diligence process has been described in various business textbooks (e.g. Gole and Hilger, 2009; Howson, 2018; Weber et al., 2014), topics and procedures can substantially deviate from these depictions and are experience-based. As one negotiator explained, “there is no predetermined number of due diligence stages. It depends on the complexity of the acquisition. This is much less formal than a textbook would suggest.” And further, “to know the right questions that need to be asked … it is all experience.”

Once all due diligence topics have been completed, the acquisition contract will be drafted that translates the results of the entire project into a legal format. At this stage, lawyers play a fundamental role and details are being fixated. Although this sounds like a standardized process, it is quite time-consuming and, according to one interviewee, “can easily take one or even two years before signing will take place,” especially since aspects such as antitrust regulations also have to be clarified.

Social character and spatiality of meetings

Since the parties may not know each other beforehand and since the complexity of the process generates substantial uncertainty, the two parties involved meet many times over a longer period and in different social and spatial constellations to generate confidence in a positive outcome. The process from the first meeting until the signing of papers involves a dozen or more face-to-face meetings, as one experienced manager specified. In particular, during the due diligence process, extensive exchanges of information take place and the individuals involved get to know each other. International M&As entail a particularly high degree of uncertainty and are comparatively more complex since they involve different cultures and institutional–legal systems, as was pointed out by several of our interviewees. In these cases, specialists are typically called in who act as boundary spanners between these different contexts (Liu and Meyer, 2020).

Interestingly, the places where these meetings occur and the number and function of the firm representatives that get together systematically change throughout the process. During the initial get-together that sets the themes and tone for later discussions, conversations are highly secretive and involve only the corporate leaders or owners. This may take place, for instance, in a relaxed atmosphere over dinner on neutral ground, such as a hotel in a different city (Mayfield et al., 1998). For instance, when Rhône-Poulenc and Hoechst decided to begin merger negotiations in the late 1990s, the two CEOs met privately over their interests in soccer and wine and discussed the possibility of a mega-merger in the chemical industry during personal visits (Sommer, 2002). During such meetings, the decision makers try to generate a mutual agreement for a deal and establish a “common chemistry” for later discussions. Our interviewees emphasized that it is important that the atmosphere of these meetings enables open discussions without interruptions. At the end of this stage, both parties are committed to move on with the deal, have an understanding of its magnitude or will leave the table and exit—“without others ever getting to know or becoming involved” as one interviewee pointed out.

At the beginning of the due diligence process, the degree of secrecy is still high as neither the seller’s nor the buyer’s workforce or media should know about the negotiations to avoid the spread of rumors. Although the owners will no longer directly take part in the discussions, few leading managers will be involved on either side, often supported by a lawyer. They conduct due diligence by analyzing the seller’s data and discussing the buyer’s questions. Although the topics discussed are usually determined by the buyer, one interviewee emphasized that the seller also requires information about the goals and integrity of the buyer before making a deal. 8 As the selling owner aims for a positive outcome for the business to be sold, there is a strong interest to get to know about the future plans of the buyer. Since the discussions are very intense and stretch over a longer time period, both sides gradually gain confidence in the deal (Ghauri, 2003).

A typical place for secretive meetings at this stage would be an airport hotel in a different city with easy access for both parties for a duration of up to two days. One experienced negotiator explained: “Airport hotels are quasi-natural places for such meetings. Logistically, they are the best as you can save time. And they are anonymous—they are neutral.” It is no coincidence that major international airports have developed extensive office and conference facilities for such and other forms of business meetings (Appold, 2015; Florida, 2012; Kasarda and Lindsay, 2011), although in later stages “meetings also take place in cafes [at or near airports], not only in conference rooms,” as one manager pointed out. The meetings are set up as formal discussions about the specific due diligence topics but also include informal dinners where specific aspects from the daily discussions are brought up, problem solutions discussed, and generic conversations take place. Crucially, these meetings enforce constant engagement of both parties, during which the participants get to know each other well. One lead negotiator highlighted the role of dinner meetings before a negotiation day: “To have a full day of meetings, you get together the evening before … and start with a joint dinner. This sequence is clever since you do not have business papers with you … Because you do not want to anticipate negotiations you talk about general topics, about the industry … Sometimes you frame the next day discussing the topics that need clarification. But this is not a negotiation—it has the character of sorting your thoughts … You get closer to each other—you have some limited amount of alcohol in a relaxed atmosphere … but you always talk business … [Including the next day], you spend 8 to 10 hours together.”

At this point, still, only a few selected representatives of the involved firms are informed about the process and only after a preliminary agreement about sales price and conditions has been reached will the number of participants grow. Although still in a relatively early stage, this provides the basis for experts from different corporate divisions to become involved in the discussions. Secrecy is now gradually given up and face-to-face meetings take place at the seller’s or buyer’s sites and may even alternate between these locations. As the commitment of the parties increases parallel to the establishment of social relations between the firms, both release information about the acquisition process and present a positive view of the future deal to their workforce. And since more and more specialists from both sides become involved, social relations begin to develop between future colleagues.

Managing trust and risks

The general context of relational M&A processes is characterized by a high degree of information asymmetry and associated risks. This is a high-pressure environment, in which mistakes must not be made. The economic costs could be tremendous as the value of the selling business may drop, as political pressure in the region may rise, or as employees and suppliers terminate contracts and leave. Therefore, it is necessary to keep risks at bay, develop professional trust (Ettlinger, 2003), and gain confidence in the entire process (Bathelt and Glückler, 2011; Bathelt and Henn, 2014). This occurs in several stages over an extended period through different types of face-to-face meetings and mixtures of business and non-business conversations. In the relational M&A procedure, it is of essential interest to both parties to develop social relations. This begins with the initial contact between the owners during which a mutual agreement is reached. As emphasized in several interviews, this requires that a joint chemistry and cognitive proximity (Nooteboom, 2000) between the owners exist and swift trust (Grabher, 2002) be mobilized that will be verified and extended later on (Bachmann, 2001). In meetings, “when the partner brings lots of business materials,” as one interviewee explained, “this is viewed as a good sign. The seller is often more insecure than the buyer … because for them it is a new situation.”

Until a more definite agreement about the sales price has been reached, the discussions between both parties can falter and are thus top secret. However, as the process moves on, the leading negotiators of both parties increasingly involve more representatives, get to know each other better, and gain professional trust (Ghauri, 2003). This is a crucial part of the discussions as one lead negotiator explained: “We try to find out, of course, how trustworthy [our partner] is. You pay attention to specific things, usually positive signs that I try to identify … The more often we meet, the more relaxed, not casual, the atmosphere of the discussion becomes because we get to know each other and can judge each other’s reactions. We never talk about private issues however.” Although fewer meetings might be sufficient, it is the regular exchange between the two parties that drastically reduces uncertainty. It is because of the regularity of “up to 10 to 15 meetings sometimes in a bi-weekly rhythm,” as one interviewee described, that trust in the deal increases and, with more specialists becoming involved, social relations spread. All of this is meant to produce a robust basis with broad support for the deal. “At later stages [of due diligence], 6 to 8 individuals may be involved” in the discussion with varying specialists, as described in one interview.

Although it is possible that some discussions could also take place via video conference, interviewees involved in relational M&A procedures remained skeptical. As one manager explained: “The most important issue is to get to know each other in person. This is success factor number one … When you sit face-to-face across from each other and get to experience your partner’s reactions and emotions, this is a crucial part. Video conferences are good when you have stable teams on both sides who have met 30 times in person before. We do this, of course, but not in M&A processes … The personal contact cannot be replaced. Even though video conferences are not a big cost factor, they are not accepted as much … I can only repeat myself: especially in the early stages of getting to know your M&A partner, there is no alternative to meeting face to face.”

Knowledge flows in the auction-based M&A procedure

Although the relational M&A procedure was widespread among German Mittelstand firms, in retrospect it should not come as a surprise that other cases were characterized by an auction-based M&A procedure. This is a reflection of widespread liberalization tendencies and the spread of hybrid forms of corporate governance that have occurred within the German variety of capitalism since the 1990s (Jackson, 2003; Jackson and Thelen, 2015). In the auction-based procedure, the sales process is organized as a bidding process during which the initially large number of potential buyers is narrowed down to one in a stepwise process. This creates a seller’s market that is highly organized and operates quite differently from the relational procedure. As it normally extends over a much shorter time span, we expected the potential for more conflict. Below, we analyze the differences between both procedures in a comparative manner (Table 1).

Contact initiation

In the auction-based M&A procedure, sellers do not aim to have a single transaction partner from the outset. With a lack of information about who might actually be interested in acquiring their business unit, they approach third parties such as specialized investment banks or consultancies, inform these about their intention, and ask them to organize the sales process. These parties do not only have a good overview of the market and know potentially interested buyers, but they are experienced in arranging the complex sales process. They start the sales procedure as intermediaries by sending out teasers about the sales target to a large pool of firms that could potentially be interested in an acquisition. Those who reply create what some of our interviewees referred to as the universe of buyers (Frankel and Forman, 2017: 148). The target firm remains anonymous, which makes contact initiation a formal, impersonal process. Within 4–8 weeks after the teaser has been sent out, those potential buyers interested in an acquisition sign a non-disclosure memorandum which binds them to secrecy about further steps. Once signed, the potential buyers will be sent a more detailed information memorandum of approximately 80–120 pages including economic data of the target firm, which will then be known by name for the first time.

Due diligence process

In the next step, all firms interested in the target unit hand in a non-binding offer (Hwang, 2018) without having met representatives of that firm thereby agreeing to enter into the diligence process. The intermediary starts a highly structured process with distinct stages and timelines and ensures that this is strictly followed. In contrast to the relational procedure, multiple bidders take part in the process. Typically, five or more bidding firms are involved based on their offers, as an experienced M&A consultant explained. Since the intermediary will try to prevent the potential buyers to become aware of each other, this process is conducted separately for each bidder, which makes due diligence a complicated and costly procedure. Usually, the process begins with a so-called management presentation by representatives of the target firm that includes a general overview of the business unit (Gole and Hilger, 2009: 132ff.). Although, as was mentioned in one interview, “up to 25 representatives of each firm, including the CEOs,” meet at this stage for the first time, there is no opportunity to discuss open questions. One interviewee stated that the “management presentation rarely offers the opportunity to get into a conversation. There is very limited time, … few possibilities for real questions.”

In subsequent stages of the due diligence process, the potential buyers are given the opportunity to review relevant seller data within a defined period by accessing a physical or online data room. In addition, they are given the opportunity to approach the target firm at each stage with a limited number of questions about the materials, typically in a written form. As explained by several M&A managers, it is occasionally necessary for expert teams from both firms to discuss uncertainties in this process. This is usually done by phone but specific circumstances can include short face-to-face meetings. Overall, the due diligence process takes place under great time pressure and is typically completed within only a few weeks. Although it provides the potential buyer with important information about the target, many questions remain unanswered. This creates substantial information asymmetry. As one interviewee explained: “It is the task of the [buyer’s] own investment bankers to find out more [about the target firm], first of all informally, because it is precisely in this initial phase that you cannot ask too many questions and make too many demands—to find out how [valuable the target firm and reliable the information] is through contacts with banks, customers, anyone else …—to make sure they are not prosecuted somewhere by the FBI or the SEC … If we know the participants [from some prior transaction], we can find colleagues who were involved. Yes, [through such information] we can develop a certain feeling [for the target]. This is almost a detective’s job.” Since this process only takes few weeks, potential buyers are under great pressure to collect additional information and make a decision of whether to remain in the bidding process. At the end of the due diligence stages, those potential buyers interested in an acquisition submit binding offers. The seller compares these offers and decides with whom to continue negotiations.

Social character and spatiality of meetings

In auction-based M&As, the already high degree of uncertainty for potential buyers is reinforced by the fact that the prospects for success are unknown even if the buyers have a pronounced intention to acquire the target. This is because a potential buyer neither knows the number and names of the other bidders nor their willingness to pay. Also, social contacts between the seller and the buyers are kept to a minimum. This uncertainty is purposely maintained throughout the process and direct contact and get-togethers are avoided. In the early stage, face-to-face contacts do not occur, apart from the management presentation at the beginning of the due diligence process and occasional expert conversations. Instead, the intermediary operates as a knowledge brokerage or go-to point (Burt, 2005) linking both sides and preventing social interaction between them. This is enforced through strict rules that aim to guarantee equal treatment of all parties involved. For the bidders, this approach assures that fellow bidders do not have significant information advantages.

Although face-to-face contacts are initially insignificant, they rapidly gain in importance at the end of the due diligence stages once the (likely) buyer is known. In fact, as one experienced interview partner mentioned, “often, the first official meeting with representatives of the target only takes place after the first draft of the contract.” Since the initial stage of the process is characterized by maximum anonymity between the parties engaged in the bidding process, the investment banker or consultancy organizes personal interaction on neutral ground. Similar to the relational process, such encounters would not take place on the premises of the target but can take place in easily accessible conference hotels or at the investment bank or consultancy. Visits at the seller's or buyer's location will only take place at the very end of the procedure.

Managing trust and risks

One important feature of auction-based M&As is that the intermediary hired by the seller deliberately creates uncertainties at the expense of the bidders. For instance, our interviewees described that the total number of bidders is kept secret and that disclosed information about the target firm is limited. Further, by intentionally spreading rumors (e.g. about the number of bidders), intermediaries sometimes seek to push the negotiation process into a certain direction, as mentioned by a lawyer specialized in M&As: “If we have such a process—yes, they are keen on spreading news … They deliberately play with this … Gossip is also being distributed and you do not have to name any sources for this.” As a consequence, the bidders cannot easily satisfy their information needs.

At the same time, the intermediary is responsible for ensuring reliability by signaling strong commitment and professionalism. This is done, for instance, by reacting promptly to a bidder’s requests and by treating every bidder in the same manner. This generates confidence in the process (Ettlinger, 2003) and supports the firms’ willingness to remain involved. As a lawyer specialized in M&As described, “trust is, of course, formed through experience. People do keep what they have promised … You notice somehow that it works—that what they have said is being implemented.” Although confidence in the process is stronger on the side of the selling firm, potential buyers can rely on a fair process that is closely tied to a renowned third party whose reputation depends on the professional character of the procedure. The overall risks for a potential buyer also rely on prior experience in similar processes and existing decision-making capabilities.

Although it cannot be ruled out that the final bidder having gone through the entire process will leave the table without a deal, our interviewees insisted that such an outcome was rather unlikely. The risk of a mismatch is kept at bay due to the large number of firms involved in the process and the fact that the potential buyers discover in a competitive process how well the target firm fits their expectations in comparison with other bidders. At the same time, the due diligence process appears rushed and, as a consequence, less thorough compared with the relational M&A procedure. A lawyer with broad experience in M&As commented on this aspect as follows: “I [tend to] create pressure on the auction process in every respect … so I have the chance to get it done a lot faster. If I negotiate one on one with someone, then it might be delayed.” As a consequence, the process increases the risk that the buying firms do not fully disclose their intentions or that the vendor does not reveal potential problems. In both cases, challenges in the integration process or other problems are more likely to come up in the aftermath of the transaction, for instance, conflicts with the workforce or regional policy makers.

For both the potential buyers and the selling firm, the role of the third party creates trust that a completion of the transaction with a favorable deal is possible. One experienced M&A consultant described the role of the intermediary in trust building as follows: “How is trust built in this situation? [This happens] when you realize [the intermediary] really thought about how to best organize this process so that another party will be able to go through it in the fastest possible time … The consultant is liable for what he writes in all sorts of documentations with a given amount of money. This signals some degree of trust … It is therefore worthwhile to properly prepare the process and to do it with a consultant.”

Throughout the entire process, the seller has the advantage of collecting information about the bidders and is thus able to compare between them effectively. The process allows the selling firm to choose the party that offers the highest price or meets a more complex set of criteria best.

Conclusions

In this paper, we have explored questions surrounding what knowledge is exchanged in the context of M&A processes that take place under great uncertainty and how. A particular focus of this inquiry has been the role of face-to-face interactions and social relations in mitigating associated risks (Amin and Cohendet, 2004; Sarala et al., 2014). Our analysis builds on previous studies of M&As that have investigated the motives, structure, geography, and success factors of M&As. The findings from our interviews clearly show from a process perspective that knowledge exchanges in M&A procedures rely heavily on professional trust building associated with repeated face-to-face meetings that are characterized by varying and evolving geographies. By exploring the very mechanisms that generate affinity between the actors, such as cognitive, cultural and technological proximity, and trust, our study extends the findings of the proximity literature (Boschma, 2005; Boschma et al., 2016). While that literature focuses on identifying correlations between economic outcomes and different proximity measures, our analysis investigates underlying practices through which actors exchange knowledge over distance and reduce uncertainties due to their different geographical and institutional contexts to enable and finalize M&A processes (Bathelt and Henn, 2014).

Even though many variations of M&A processes exist and although each is to some extent unique, we were able to distinguish two main procedures that differ greatly in terms of the role of face-to-face contacts, risk management, and social contexts in knowledge exchanges (Table 1):

The relational M&A procedure takes place between the selling firm and one potential buyer. The procedure is from its beginning to its end characterized by intensive face-to-face interaction with intensive knowledge exchanges between the spatially separated parties. This helps to facilitate the development of professional trust and social relations and creates confidence in the completion of the process in such a way that the risk of failure decreases during the process. At the same time, a suboptimal outcome is possible if the partners have been a mismatch from the very beginning. In this case, problems in the post-merger stage will be a likely consequence. Our findings indicate that the relational M&A procedure seems to fit well in the context of coordinated market economies, such as Germany, that are characterized by strong deliberative institutions (Hall and Soskice, 2001)—albeit that we identified substantial variety in M&A processes. The relational procedure seems to play an important role when the buying firm strives to increase its competitiveness with a long-term perspective and when corporate owners aim to retire and plan for their succession. It is therefore not surprising that we identified this procedure, particularly in small- and medium-sized enterprises, typical for the German Mittelstand. In line with this observation, we found relational M&A procedures specifically in low- and medium-tech industries. The auction-based M&A procedure, in contrast, is characterized by a highly structured and largely anonymized process between one seller and multiple bidders, during which limited opportunities for direct interaction exist. The process is highly secretive in the beginning and only opens up toward the end. The auction-based procedure appears especially relevant when vendors aim to maximize the sales price and involves substantial information asymmetries. Yet, the competitive nature of the process allows the seller to efficiently compare between the bidders, which keeps risks at bay. This procedure appears to fit well with large sellers that operate in a liberal market economy context under short- or medium-term goals, for example, in dynamic high-tech and knowledge-based service industries.

Altogether, our research clearly indicates that the complex knowledge required to conduct and conclude M&A processes can by no means be exchanged through virtual interaction alone but that occasional or repeated temporary proximity is crucial (Bathelt, 2019). This is an important finding, especially during the current COVID-19 pandemic, as media reports suggest that future economic processes may be much more reliant on virtual interaction than in the past. Initial studies on M&A processes during the pandemic, however, rather support our conclusions. Although such reports emphasize the importance of new communication platforms, these tools can only partly compensate for the lack of opportunities for face-to-face exchanges. In a report about trends in M&A processes by the consulting firm Ernst & Young (Leach and Kaske, 2020), one manager—representative for others—emphasizes new problems: “The loss of that personal connection, sitting in a room with the other side when there is a hard discussion—that we haven’t figured out how to make up for.” Similarly, an M&A banker is quoted in a different report as complaining that “you just can’t get these deals over the line without face-to-face meetings—it’s impossible” (Clarke, 2020). The routine due diligence checks of the target prove to be difficult, if not impossible, when conducted from a distance due to the lack of direct interaction in face-to-face settings (Galpin and Mayer, 2020).

In the course of the procedures investigated in this paper, secretive meetings are repeatedly held at different neutral locations to exchange specific knowledge, reduce information asymmetries, and create professional trust. In exploring these secretive geographies, our study contributes to recent work in economic geography interested in understanding the different settings of knowledge exchanges over geographical distance (Bathelt and Henn, 2014). Although this study has focused on Germany as a location of M&A processes, future studies should broaden their scope to more systematically investigate how M&A-related knowledge exchanges differ between different varieties of capitalism.

Footnotes

Acknowledgements

Parts of this paper, to which both authors contributed equally, were presented at the Annual Meeting of the Association of American Geographers in Washington, DC, in April 2019. The authors would like to thank Max Buchholz, Dominik Lentz, Sebastian Lentz, and Wolfgang Stahl for their terrific support.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Canada Research Chair in Innovation & Governance at the University of Toronto and the Chair of Economic Geography at the University of Jena.