Abstract

Social capital is an important factor explaining differences in economic growth among regions. However, the key distinction between bonding social capital, which can lead to lock-in and myopia, and bridging social capital, which promotes knowledge flows across diverse groups, has been overlooked in growth research. In this paper, we address this shortcoming by examining how bonding and bridging social capital affect regional economic growth, using data for 190 regions in 21 EU countries, covering eight waves of the European Social Survey between 2002 and 2016. The findings confirm that bridging social capital is linked to higher levels of regional economic growth. Bonding social capital is highly correlated with bridging social capital and associated with lower growth when this is controlled for. We do not find significantly different effects of bonding social capital in regions with more or less bridging social capital, or vice versa. We examine the interaction between social and human capital, finding that bridging social capital is fundamental for stimulating economic growth, especially in low-skilled regions. Human capital also moderates the relationship between bonding social capital and growth, reducing the negative externalities imposed by excessive bonding.

Introduction

Social capital has become an attractive concept for both scholars and policy-makers. The former (e.g. Asheim, 2003; Beugelsdijk and Smulders, 2009; Boschma, 2005; Crescenzi and Gagliardi, 2015; Farole et al., 2011; Putnam, 1993; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013) see it as a useful concept in explaining differences in economic growth among regions. The latter – for example the World Bank (1998), the OECD (2001) and the European Union (Eurobarometer, 2005) – are increasingly thinking about how to use social capital as a policy tool for facilitating growth. While in theory, social capital is an attractive concept, in practice “it is difficult if not impossible to imitate one region’s social capital process in other places” (Malecki, 2012: 1033). Without understanding how social capital works, policies, programmes and projects using it to foster economic growth across regions are bound to fail.

Broadly, social capital can be defined as a variety or combination of aspects of social structure or features of social organisation, and aggregates of institutionalised relationships, such as trust, networks and norms that facilitate cooperative action (Bourdieu, 1986; Coleman, 1988; Putnam, 1993). Within the social capital literature, an important distinction is often made between bonding and bridging forms of social capital (Patulny, 2009; Putnam, 2000; Westlund and Larsson, 2016). Bonding social capital refers to closed networks that link homogenous groups, whereas bridging social capital refers to open networks that link heterogeneous groups (Putnam, 2000). The balance of bonding and bridging social capital either blocks or fortifies the sorting and matching of economic activities with consequences for uneven economic growth among regions (Beugelsdijk and Smulders, 2009; Farole et al., 2011; Putnam, 2000; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013; van Staveren and Knorringa, 2006).

Empirical studies have implicitly (Beugelsdijk and Van Schaik, 2005) or explicitly (Beugelsdijk and Smulders, 2009) paid attention to the differences between the effects of bonding and bridging social capital on economic growth. However, empirical findings on the effects of bonding and bridging social capital on regional economic growth remain inconclusive (Beugelsdijk and Smulders, 2009; Westlund and Adam, 2010). The dominant theoretical assumption is that bonding and bridging social capital complement each other (Putnam, 2000; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013; Woolcock, 2010), but this has so far not been adequately explored.

Furthermore, the relationship between social and other forms of capital, notably human capital, in promoting economic growth remains unclear (Ketterer and Rodríguez-Pose, 2018; Rodríguez-Pose, 2013). Putnam (1993) and Fukuyama (1995) have, for example, suggested that human capital may have a moderating effect on both bonding and bridging social capital. An important question is whether social capital can, to some extent, substitute for human capital and, as such, represent an alternative path to growth for low-skilled regions. Or, conversely, whether the two are mutually dependent, such that social capital requires a high level of human capital in order to foster growth.

This paper extends existing knowledge on how bonding and bridging social capital affect economic growth, as well as on how their effects are moderated by human capital. Accordingly, we address the following research questions: First, we examine how bonding and bridging social capital affect regional economic growth. Second, we look at whether the effects of bonding social capital on economic growth depend on the levels of bridging social capital in the region, and vice versa. Finally, we assess the extent to which the effects of bonding and bridging social capital on regional economic growth vary depending on human capital.

In order to address these questions, we conduct a panel data analysis of 190 regions in 21 EU countries. Using the eight waves of the European Social Survey from 2002 to 2016, we construct a purpose-built dataset covering more data and for a longer period than prior studies on the role of social capital for economic development at the regional scale (Beugelsdijk and Smulders, 2009). The findings confirm the differences between the effects of bonding and bridging social capital on economic growth. The two are highly correlated, and individually each is associated with higher levels of growth. However, when both are included in the same model, interesting differences emerge: while bridging social capital has a positive effect on regional economic growth when controlling for bonding, bonding social capital is negative for growth when controlling for the level of bridging in the region. Furthermore, the findings confirm that human capital moderates the effects of social capital on economic growth. An increase in human capital reduces the negative effects of bonding social capital – i.e. bonding is particularly harmful in low-skilled regions. Meanwhile, bridging social capital works as a substitute for human capital. Specifically, bridging social capital has a stronger effect on growth in regions with lower levels of human capital. Hence, high levels of bridging social capital can, to some extent, compensate for a lack of human capital in low-skilled regions.

The rest of the paper follows this structure: First, we examine the literature on social capital and economic growth. Then, we present the data and empirical model, before moving on to the results and discussion. The final section is the conclusion.

Social capital and regional development

This paper conceptualises and operationalises social capital as an aggregate construct at a regional level (Beugelsdijk and Smulders, 2009; Beugelsdijk and Van Schaik, 2005; Putnam, 1993). At the same time, it takes a multi-dimensional approach in which social capital is considered to comprise bonding and bridging social capital (Patulny, 2009; Putnam, 1993; Westlund and Larsson, 2016). Specifically, the focus is on the structural or network dimensions of bonding and bridging social capital and their effects on economic growth.

According to Putnam (1993), networks transmit trust, reduce transaction costs and information asymmetry, and increase the density and intensity of interactions with positive externalities on economic growth in regions. Although the paper focuses on economic growth, it also draws on related studies looking at other socio-economic outcomes, such as innovation (Crescenzi and Gagliardi, 2015), regional diversification (Antonietti and Boschma, 2018; Cortinovis et al., 2017), and entrepreneurship (Feldman et al., 2019).

The next section starts by separately discussing bonding and bridging social capital and their effect on economic growth. This is followed and concluded with a synthesis that brings the two together to develop the hypotheses that inform the empirical investigation.

Bonding social capital

Putnam (2000: 22) defines bonding social capital as “inward looking [networks that] tend to reinforce exclusive identities and homogeneous groups”. The term is related to concepts such as strong ties and within-group cohesion. Bonding is fundamentally characterised by a tightening of relationships and networks within the group, while, simultaneously, excluding non-members (Granovetter, 1973).

There are three different positions in the literature on how bonding social capital operates. The first position treats bonding social capital networks as “Olson-type groups” or “distributional coalitions” (Antonietti and Boschma, 2018; Cortinovis et al., 2017; Crescenzi and Gagliardi, 2015; Knack and Keefer, 1997; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013). This builds on the observations by Olson (1982) that interest groups create benefits for members, but impose disproportionate costs on the wider society. Thus, despite their benefits in terms of interest articulation and preference matching, their total effect is negative on the whole of society. From this perspective, strong bonding within a place will result in rent-seeking, insider-outsider problems, clientelism, and nepotistic practices, which block economic progress (Crescenzi et al., 2013; Crescenzi and Gagliardi, 2015; Farole et al., 2011; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013).

The second position is that bonding social capital is complementary to bridging social capital and therefore leads to beneficial social and economic outcomes (Portes, 1998; Storper, 2005, 2013; Woolcock, 2010). Social control and sanctions, as well as the supporting nature of bonding social capital, are to a certain degree necessary for developing bridging social capital and achieving broader socio-economic outcomes.

The third position, which is perhaps the most reconciling, is that bonding social capital can have both positive and negative consequences, depending on the context (Farole et al., 2011; Patulny and Svendsen, 2007; Portes, 1998). Thus, other contextual factors, such as human capital, influence the effects of social capital on growth. Human capital could either substitute for or complement social capital (Schuller, 2001). For instance, building on Putnam (1993) and Fukuyama (1995), human capital can have a moderating effect that reduces the potential negative externalities of bonding social capital. The mechanisms through which human capital works include what Wollebaek and Selle (2002) describe as cumulative and moderating effects. Directly, human capital facilitates the interaction between heterogenous groups (Dinda, 2014). This process is cumulative in that an increase in interaction leads to more interaction. Indirectly, human capital promotes trust and openness, which encourages interaction beyond bonding social networks (Akçomak and Ter Weel, 2009; Fukuyama, 1995; Tabellini, 2010; Uslaner, 2008). This has moderating effects in that it improves the quality of relationships across heterogenous groups of people within and across regions. At the same time, regions with high levels of human capital generate more new knowledge and have higher absorptive capacity that promotes economic growth and development (Andersson and Johansson, 2010; Andersson and Karlsson, 2007; Smith and Thomas, 2017), reducing the danger of lock-in associated with bonding social capital. Conversely, the effects of bonding social capital in these contexts can also be positive as it helps to promote the flow of knowledge in the region.

Empirical research on the effects of bonding social capital remains inconclusive. Findings from studies on economic growth (Beugelsdijk and Smulders, 2009; Hoyman et al., 2016), innovation (Crescenzi and Gagliardi, 2015) and regional diversification (Cortinovis et al., 2017) generally show a negative coefficient, but rarely a strong and significant effect. Overall, these findings are ambivalent as to whether bonding social capital has a negative effect on economic growth. However, Beugelsdijk and Smulders (2009) find an indirect negative effect, insofar as bonding social capital tends to reduce the levels of bridging social capital.

Bridging social capital

Bridging social capital refers to the existence of open networks that connect heterogeneous groups (Antonietti and Boschma, 2018; Beugelsdijk and Smulders, 2009; Boschma, 2005; Cortinovis et al., 2017; Crescenzi and Gagliardi, 2015; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013). These networks are often also called “Putnam groups”, building on the argument by Putnam (1993) that participation in civic or voluntary associations, such as educational and cultural groups, leads to positive social and economic outcomes. There are several mechanisms through which bridging social capital may work directly or indirectly to promote economic growth (Bjørnskov, 2006). Connections between heterogeneous groups increase the diversity of knowledge sources (Rodríguez-Pose and von Berlepsch, 2019; Solheim et al., 2020). This facilitates creativity (Florida, 2002; Florida et al., 2008), innovation (Crescenzi and Gagliardi, 2015), firm entry (Malecki, 2012), and entrepreneurship (Feldman et al., 2019).

Bridging social capital is generally considered to have positive effects on socio-economic outcomes (Beugelsdijk and Smulders, 2009; Farole et al., 2011; Patulny and Svendsen, 2007; Putnam, 2000; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013; van Staveren and Knorringa, 2006; Westlund and Larsson, 2016). Although bridging is beneficial both individually and collectively, developing and maintaining it also involves considerable costs.

Since bonding and bridging social capital are presented as opposite concepts in the literature, one might expect regions with a high level of bridging social capital to have low levels of bonding social capital, and vice versa (Bürcher and Mayer, 2018). However, this is not necessarily the case, as regions can have either high or low levels of both forms of social capital. Indeed, the two forms often go together, as regions that develop strong networks within groups are frequently also those that experience higher degrees of bridging across them.

Furthermore, the effects of bridging social capital may also depend on the degree of bonding social capital in a place (Halpern, 2005; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013; Woolcock, 1998). Thus, the two interact and operate at a continuum from low to high social capital, and their different mixes produce different outcomes. According to Halpern (2005), Rodríguez‐Pose and Storper (2006), and Storper (2005, 2013), high forms of both produce better socio-economic outcomes, whereas high bridging and low bonding social capital result in an ‘anomie’ or lack of sanctions to ensure common expectations. Low bridging and high bonding results in amoral familism, while low levels of both lead to amoral individualism.

There is a close relationship between social capital and trust (Putnam, 1993). Patulny (2009) argues that the concept of a narrow and wide radius of trust (Fukuyama, 1995) can be extended to bonding and bridging social capital, respectively. Arguably, bonding social has a limited radius, allowing some exchanges and interactions to happen, while also providing forms of social control and solidarity. This is beneficial, but only to a certain extent. Bridging normally involves networking across different groups, which in turn, require some bonding in their formation. However, without a balance between the two types of social capital, high levels or excessive forms of bonding social capital can have an overall negative effect. As alluded to earlier, the interaction between bonding and bridging remains underexplored in empirical research.

As in the case of bonding, differences in human capital may also affect bridging social capital, as well as moderate its effects on socio-economic outcomes (Akçomak and Ter Weel, 2009; Alesina and La Ferrara, 2000; Dinda, 2014; Fukuyama, 1995; Rupasingha et al., 2006; Tabellini, 2010). Human capital contributes to bridging social capital directly (Dinda, 2014) and indirectly (Akçomak and Ter Weel, 2009; Fukuyama, 1995; Tabellini, 2010). Directly, schooling increases interaction, which facilitates bridging networks. Indirectly, it promotes trust and openness, which, in turn, reduce conflict among dissimilar groups and increase their interaction. Human capital has been previously used as a control variable in empirical studies (e.g. Beugelsdijk and Smulders, 2009), but its interaction with bridging social capital has not been considered. Human capital can strengthen the positive effects of bridging social capital following the same mechanisms that reduces the negative effects of bonding social capital, insofar as it creates or attracts more new knowledge, which is then shared more effectively across heterogeneous groups in regions with high bridging social capital. However, bridging social capital can also be a substitute for human capital. Bridging promotes collaborative problem-solving and the effective exchange of knowledge across diverse groups, which can potentially compensate for stronger capabilities of individual problem-solvers in regions with high human capital.

Overall, empirical studies on economic growth (Beugelsdijk and Smulders, 2009) innovation (Crescenzi and Gagliardi, 2015), regional diversification (Cortinovis et al., 2017), and income inequality (Hoyman et al., 2016) have, by and large, found bridging to be positively and significantly connected to growth. However, research on the relationship between bonding and bridging social capital remains inconclusive. There is also little research on how human capital might moderate the effects of bridging.

Hypotheses

Based on this overview of the literature on how bonding and bridging social capital influence economic growth, we develop three types of hypotheses. First, we examine the direct effects of each type of social capital on economic growth. The literature notes that bonding and bridging have opposite links to economic growth, as bridging tends to be beneficial while bonding can be harmful for growth (Beugelsdijk and Smulders, 2009; Farole et al., 2011; Putnam, 2000; Rodríguez‐Pose and Storper, 2006; Storper, 2005, 2013; van Staveren and Knorringa, 2006). However, empirical findings (e.g. Beugelsdijk and Smulders, 2009), especially for bonding, have often not resulted in significant findings. Therefore, we test the following hypotheses:

Model and data

Empirical strategy

To examine the association between the two types of social capital and economic growth, we first run a pooled OLS model using levels of GDP per capita across regions as the outcome.

1

We assess hypotheses H1a and H1b with the following model

Second, we estimate a fixed-effects model to account for heterogeneity across regions. The fixed-effect model controls for unobserved heterogeneity across regions by incorporating regional fixed effects, denoted by ρr

For testing H2, we add an interaction term between bonding and bridging social capital, transforming the model in the following way

In order to test H3a and H3b, we include interaction terms between bonding social capital and human capital, and between bridging social capital and human capital, respectively

Finally, we bring the three models in equations (2) to (4) into a combined interaction model. We include the two-way interaction terms between the three sets of equations: bonding and bridging social capital, bonding and human capital, and bridging and bonding. Equation (5) shows the overall interaction model

Data and variables

We use data from the European Social Survey (ESS), European Values Survey (EVS), and European Statistical Office (Eurostat) for 190 regions in 21 EU countries at NUTS 1 and NUT S2 level, 2 covering eight ESS waves from 2002 to 2016. The ESS and EVS data are collected at the individual level across regions every two and nine years, respectively. The Eurostat data are compiled on a yearly basis. Appendix 1 shows the definitions of the variables of interest and the respective indicators used to operationalise them.

The dependent variable is regional economic growth, using the level of GDP per capita taken from Eurostat. The data are log transformed, due to skewness in the distribution of regional GDP.

For the explanatory variables, bonding and bridging social capital, we use the EVS data to calculate the share of the population in each region actively participating in different types of organisations. We adopt the approach by Beugelsdijk and Smulders (2009) and Cortinovis et al. (2017) based on their argument that active participation is the most accurate way of operationalising bonding (bonding social capital) and bridging (bridging social capital) social capital, rather than focusing on membership, as previous literature has done (e.g. Putnam, 2000).

Similar to Beugelsdijk and Smulders (2009) and Cortinovis et al. (2017), we distinguish between bonding and bridging social capital by classifying different types of organisations into “Olson” and “Putnam” groups which respectively exhibit rent-seeking behaviour, and openness and benefit for non-members. This also corresponds with Knack and Keefer’s (1997) division. Accordingly, we classify participation in political parties, local political action groups, labour or trade unions and professional associations into “Olson” type groups. This is the indicator for bonding social capital networks. In the same way, we assign voluntary associations which exhibit different characteristics such as religious or church organisations, welfare, youth work, cultural activities, sports and recreation, women’s groups, development and human rights, environment and animal rights, peace and health into “Putnam” groups. These make the indicator for bridging social capital networks. In Appendix 1, we provide an overview of the individual voluntary associations and their classification into bonding and bridging social capital.

For human capital, we follow existing literature in using the share of the population that has completed tertiary education as a proxy. Ideally, we would have restricted the analysis to human capital among members of “Olson” or “Putnam” groups for the estimation of how human capital interacts with social capital. However, we rely on aggregate data for European regions, which do not provide this level of detail.

We control for other factors normally considered to influence economic growth at the regional level, such as research and development expenditure (R&D), employment in manufacturing (employment in manufacturing), population density (population density), and road accessibility (road accessibility). The last two variables are log transformed. Employment in natural resources (employment in natural resources) is used as an additional control in a robustness check. The control variables are from the Eurostat database.

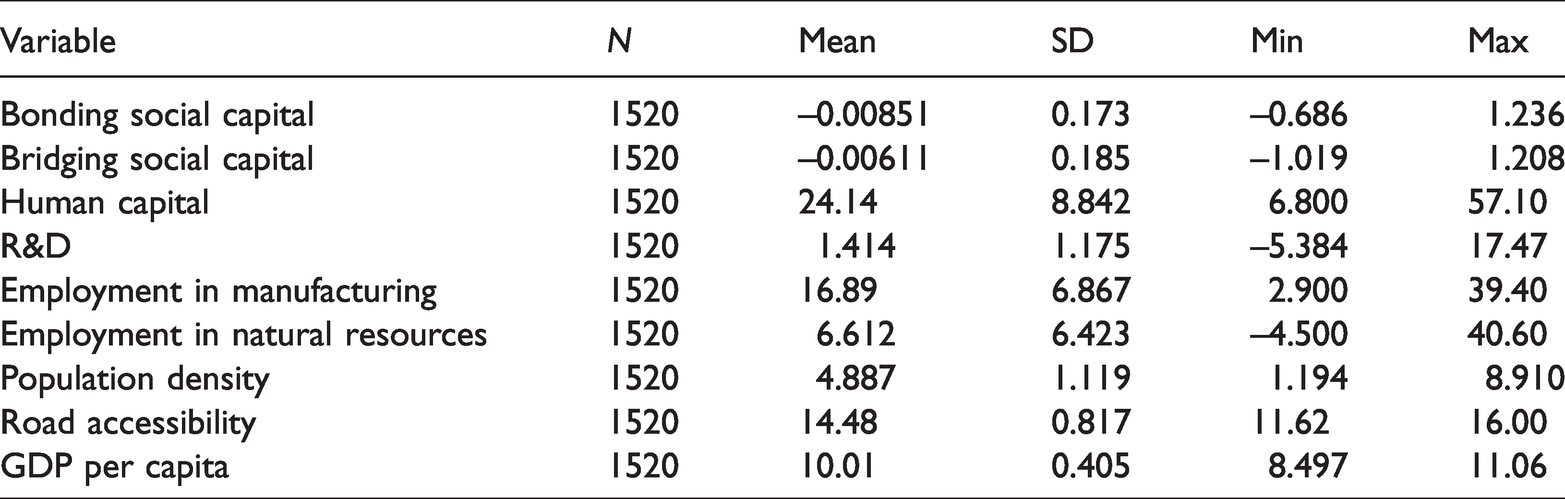

For all variables building on individual responses (i.e. the social capital measures), we first normalise the scales for each variable at the individual level by standardisation with a mean of 0 and a standard deviation of 1. Second, we calculate the mean across all individual respondents in each region to create regional level measures. For the social capital variables, we use the EVS data for 1999/2000 and 2009/2010 and match them with ESS data for 2002 and 2010, respectively. This can be done as both surveys consider the same social capital phenomena. Given that the ESS is run biennially, we use the ESS data to extend the EVS data to create measures of social capital. Consequently, the trend line of the ESS is used to extrapolate the EVS data to create a combined panel dataset for the period between 2002 and 2016. 3 The advantage of combining both datasets is that they are unique surveys that complement each other: The ESS is more precise at measuring generalised trust, while the EVS contains several more robust indicators for voluntary associations. The summary statistics for all the variables is presented in Table 1.

Summary statistics.

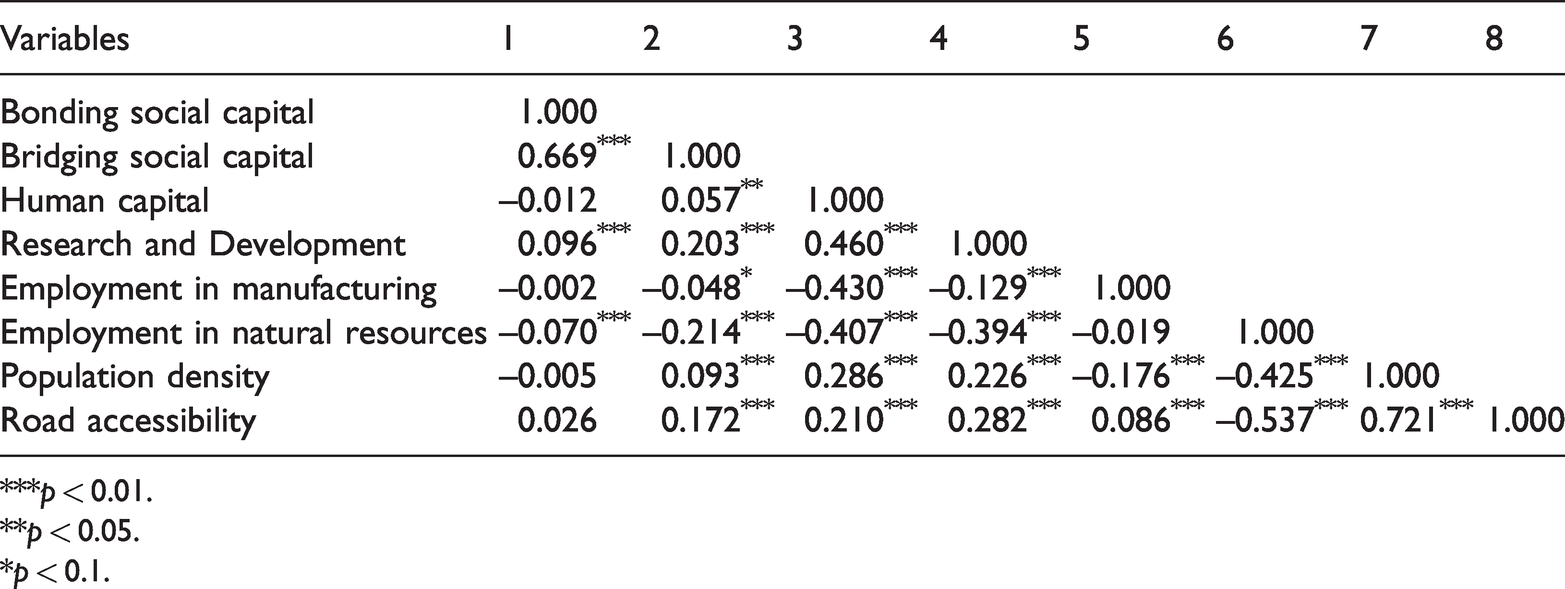

Table 2 shows the pairwise correlations between the variables. All variables are significantly and positively correlated with GDP, except for employment in manufacturing and employment in natural resources, which are both negative and significant. The correlations between most of the variables are low. However, bonding and bridging networks are highly correlated with a coefficient of 0.669. This strong and positive correlation supports the argument made earlier that bonding and bridging social capital are not opposites but can – and frequently do – go together. Indeed, the close association between them suggests that bonding social capital is necessary for the formation of bridging social capital (e.g. Halpern, 2005; Storper, 2005, 2013; Woolcock, 1998). Analysing this relationship further is beyond the scope of this paper, but the high positive correlation provides an important background for the analysis of the data.

Pairwise correlations.

***p < 0.01.

**p < 0.05.

*p < 0.1.

We check for multicollinearity and get an average variance inflation factor (VIF) of 1.87, with VIF scores between 2 and 2.5 for bonding and bridging social capital, as shown in Appendix 3. This indicates that there is no severe multicollinearity affecting the analysis.

The distribution of bonding and bridging social capital in the EU

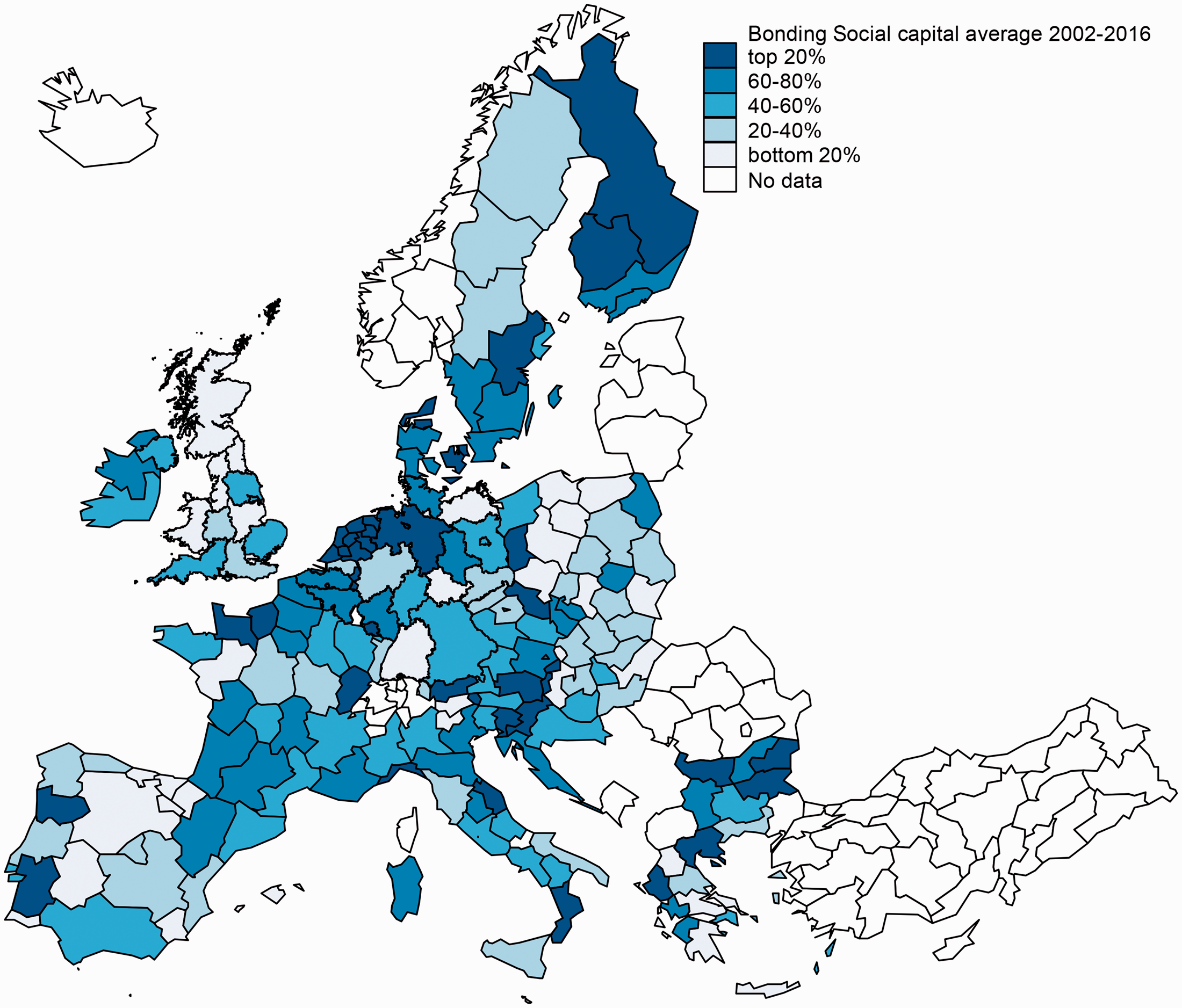

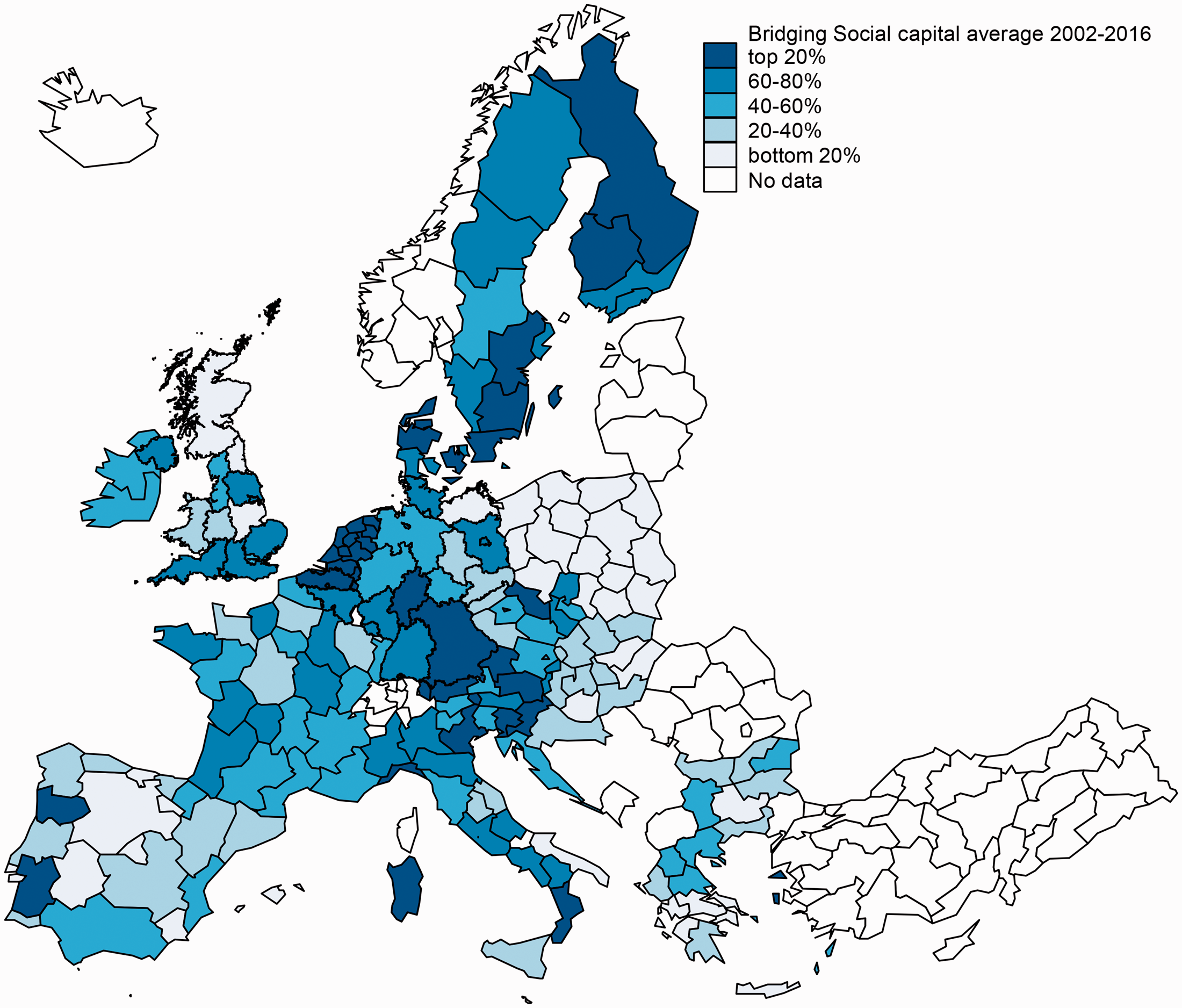

The maps in Figures 1 and 2 display the average intensity of bonding and bridging social capital, respectively, in EU regions across the period 2002–2016. Overall, Western Europe has a higher intensity of both types of social capital than Eastern Europe. Nordic countries also show high levels of bridging social capital. Important within-country differences are detected in both bonding and bridging in many countries.

Bonding social capital networks, average for 2002–2016.

Bridging social capital networks, average for 2002–2016.

The maps confirm the positive correlation between bridging and bonding social capital at the regional level. The extent to which the distribution of bonding and bridging is relatively similar on the maps is consistent with the idea that the two types of social capital can co-exist and are present in various mixes (e.g. Halpern, 2005; Storper, 2013; Woolcock, 1998).

Findings

Regression results

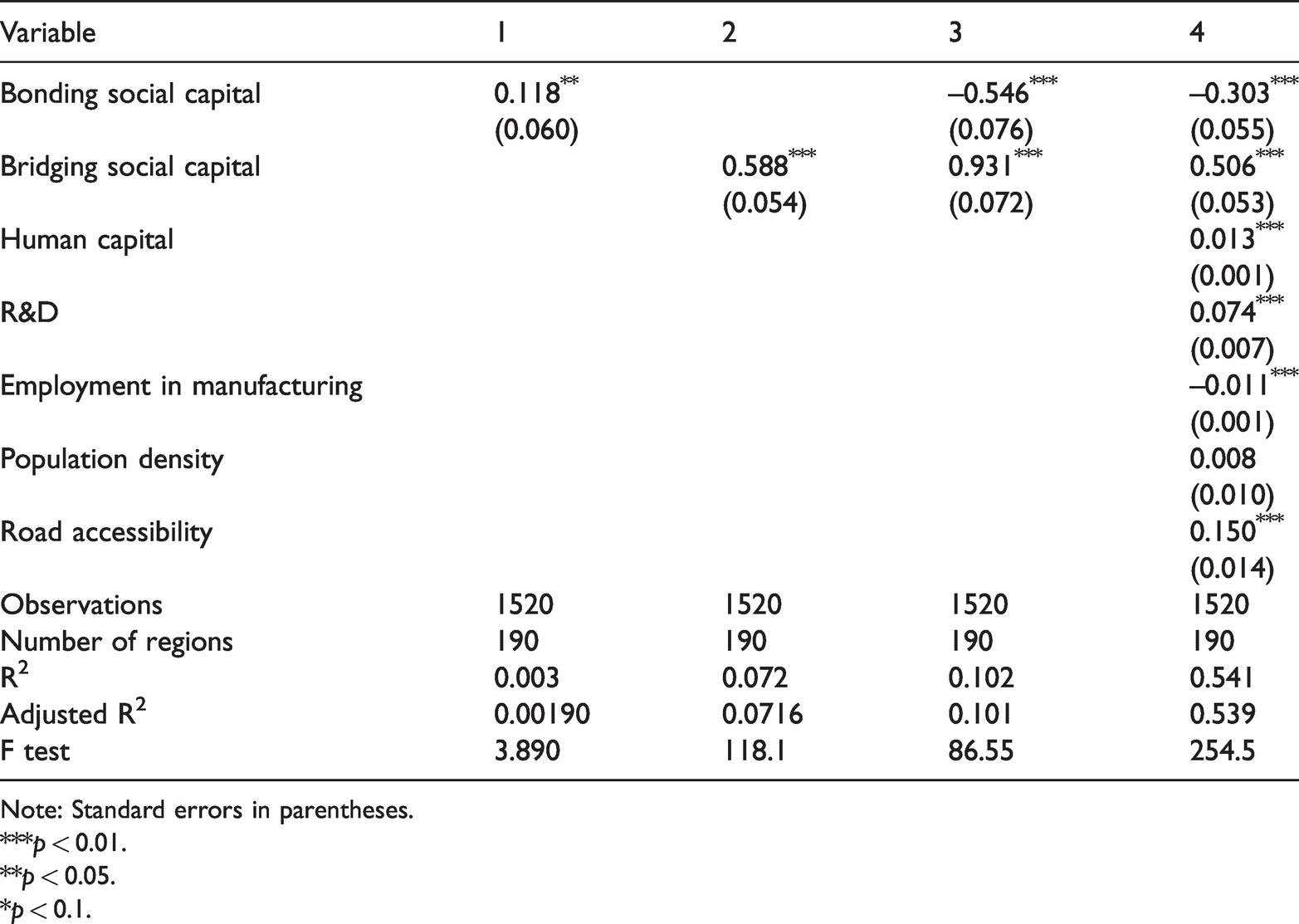

First, we conduct a pooled OLS regression as a baseline to estimate model 1 to test hypotheses H1a and H1b, using a stepwise approach, as shown in Table 3. We start with bonding social capital in regression 1, followed by bridging social capital in regression 2, and both types of social capital in regression 3. Finally, we add the control variables in regression 4.

OLS – The effects of bonding and bridging social capital on economic growth.

Note: Standard errors in parentheses.

***p < 0.01.

**p < 0.05.

*p < 0.1.

Table 3 shows that when bonding and bridging social capital are entered separately as in regression 1 and 2, both have a positive and significant association with the level of GDP per capita. Even though bonding and bridging are correlated, the coefficient for bridging social capital is almost five times higher than that for bonding social capital. When bonding and bridging social capital are entered into the analysis together in regression 3, bonding social capital turns negative, while bridging social capital remains positive, supporting H1a and H1b. This implies that – when controlling for bridging – high levels of bonding can limit economic performance. Meanwhile, bridging social capital is a fundamental factor for economic growth. When control variables are included in regression 4, the signs of the coefficients do not change, although the magnitude of both is reduced.

The control variables give the expected results. Economic growth is linked to higher human capital and R&D investment, as well as to better accessibility. However, population density does not have a significant effect. Employment in manufacturing has a negative association with the level of GDP per capita. Consistent with Beugelsdijk and Smulders (2009), we find that bridging social capital is positive and significant at the 1% level, and is a fundamental factor for economic growth and development. Furthermore, there is a direct negative association between bonding social capital and GDP per capita, significant at the 1% level. It is worth restating that this result depends on controlling for bridging social capital. Hence, if bonding social capital is associated with higher levels of bridging social capital, as the strong positive correlation between them indicates, the relationship between bonding social capital and economic growth could be more complex than the simple negative coefficient would suggest. However, what the results do indicate is that the direct relationship between bonding and economic growth is negative when controlling for bridging social capital. Hence, if two regions have the same level of bridging, the one with lower bonding would be expected to have higher levels of GDP per capita.

The results imply that a one standard deviation increase in bridging social capital is associated with an increase of approximately 9.8% in the level of GDP per capita. On the other hand, one standard deviation increase in bonding social capital is associated with a reduction of approximately 5.1% in the level of GDP per capita in the region. These increases should be viewed in the context that social capital is relatively stable and changes slowly, and therefore, such increases happen over a long term.

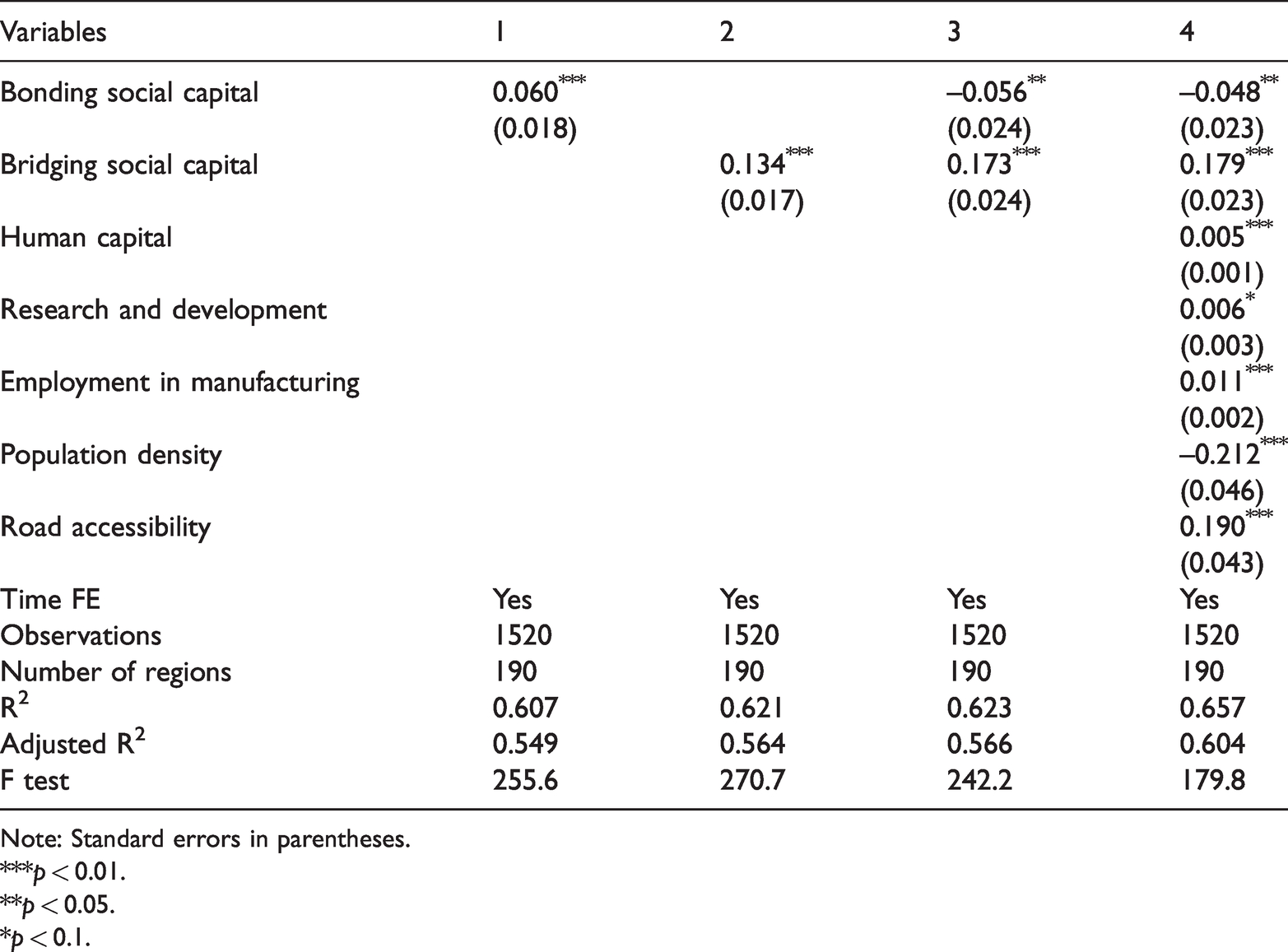

However, a pooled OLS estimation method does not account for unobserved heterogeneity across regions. Therefore, we move on to a more robust fixed effects estimation to exploit the richness of the panel data. Table 4 shows the fixed effects estimation results.

Fixed effects – The effects of bonding and bridging social capital on economic growth.

Note: Standard errors in parentheses.

***p < 0.01.

**p < 0.05.

*p < 0.1.

The results from the fixed effects regression confirm the signs of the coefficients of the OLS results. However, the magnitude of the coefficients is reduced. More bonding social capital is associated with a reduction of GDP at constant levels of bridging, while bridging social capital is associated with higher GDP at constant levels of bonding. A one standard deviation increase in bridging is linked with an increase of approximately 3.4% in the level of GDP per capita. Conversely, a one standard deviation increase in bonding is associated with a reduction of approximately 0.8% in the level of GDP per capita in the region. Overall, these results confirm the theoretical proposition that bonding is not conducive to – and can even be detrimental for – economic growth, while bridging is beneficial for growth (Beugelsdijk and Van Schaik, 2005; Putnam, 2000; Storper, 2013).

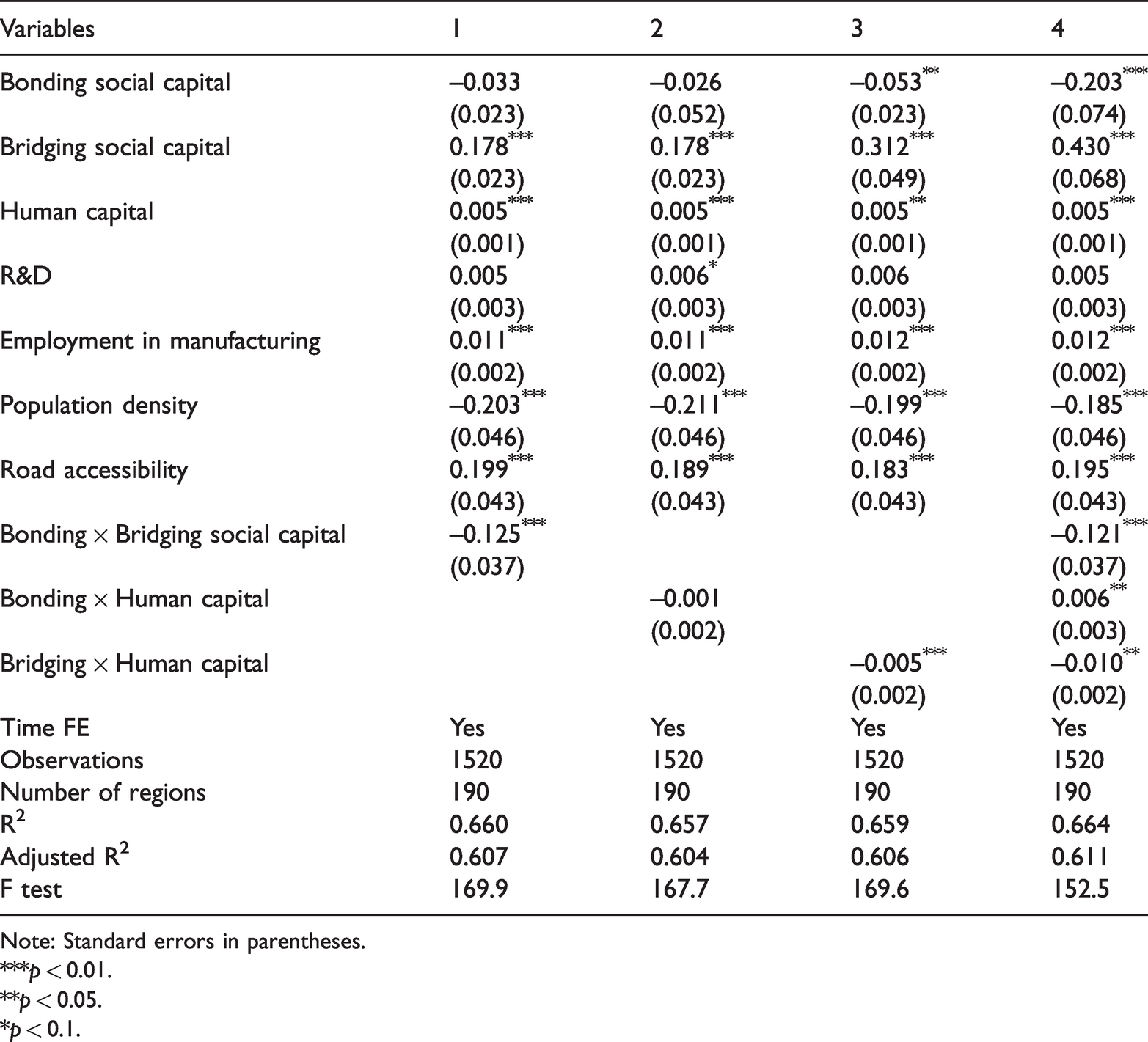

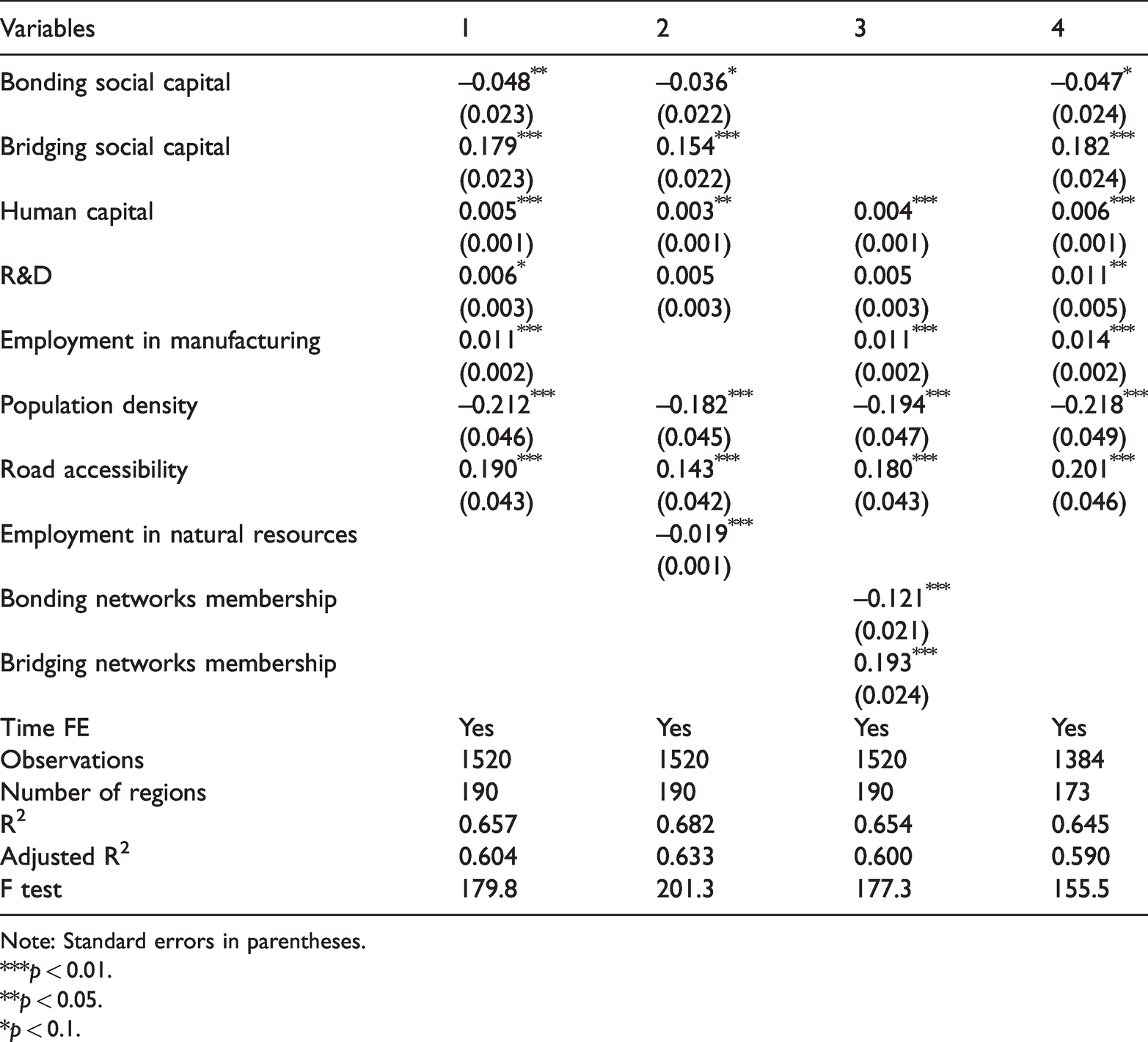

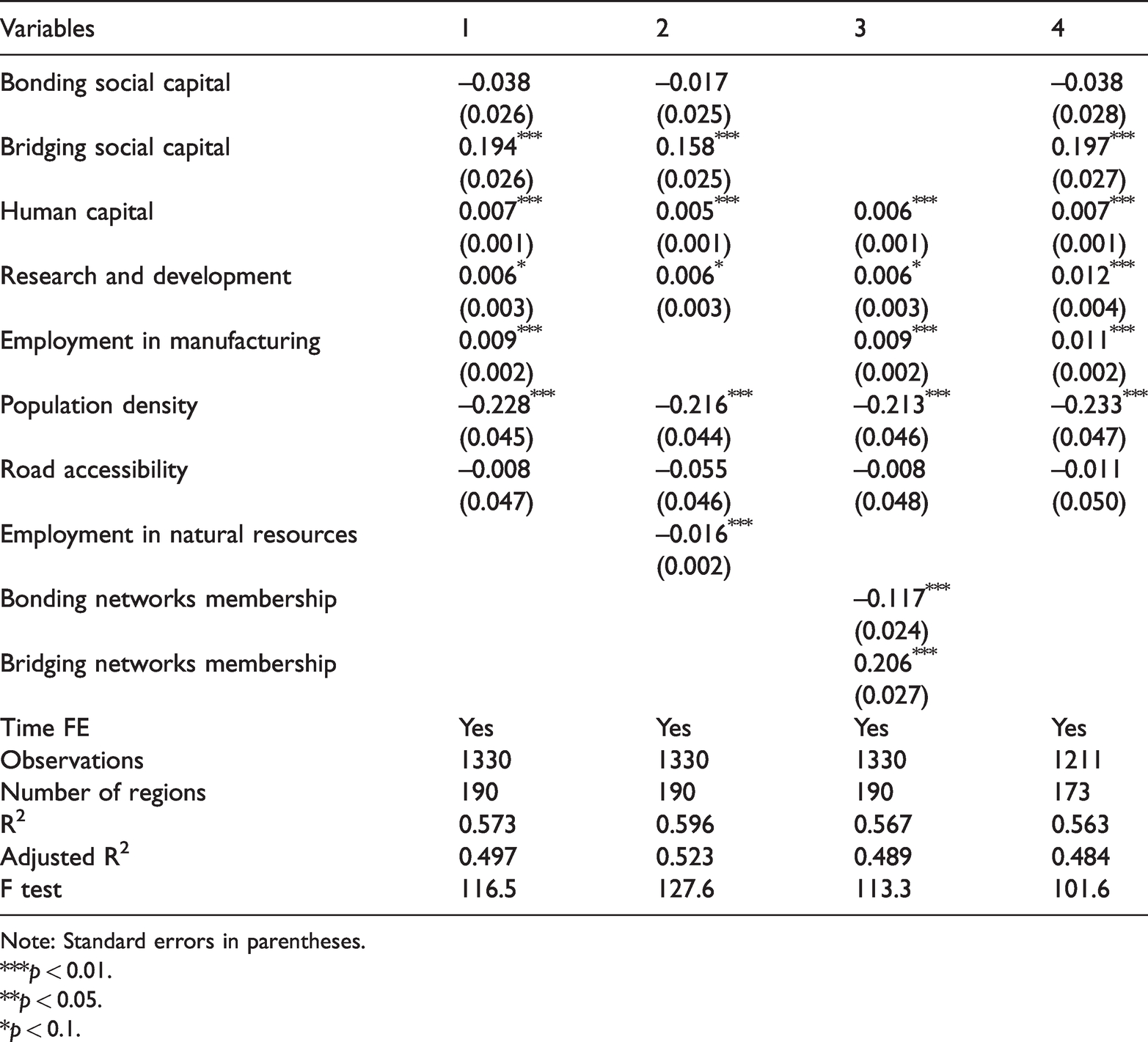

Third, in Table 5, we test hypotheses H2, H3a and H3b by examining the three interaction terms in a stepwise approach. We start by entering the interaction between bonding and bridging social capital in regression 1, followed by bonding and human capital in regression 2 and bridging and human capital in regression 3. Finally, we bring all the interactions into a combined model in regression 4. We report all the regressions but base our conclusions on the margin plots for regression 4.

Fixed effect-interaction models.

Note: Standard errors in parentheses.

***p < 0.01.

**p < 0.05.

*p < 0.1.

In regression 1, we test H2. We expect bonding and bridging to be complementary and hence to find a positive interaction term. The interaction effect, as shown in Table 5, is significant, but, in contrast to expectations, with a negative sign. This suggests that bonding and bridging are substitutes. In regressions 2 and 3, we estimate how variations in human capital endowments shape the relationship between social capital and economic growth, testing hypotheses H3a and H3b, respectively. The interaction between bonding and human capital is negative but not significant. The interaction between bridging and human capital is negative and significant, suggesting that the two are substitutes; that is, at lower levels of human capital, bridging social capital becomes more important for economic growth.

Finally, we bring all the interactions into a combined model in regression 4. The results are consistent with those from regressions 1–3. The interaction between bonding and bridging is negative and significant, suggesting that the two are substitutes. Furthermore, the interaction between human capital and bonding is positive and significant, suggesting that human capital moderates the negative influence of excessive bonding on growth. Finally, the interaction between human capital and bridging is negative and significant, suggesting that bridging social capital can act as a substitute for human capital.

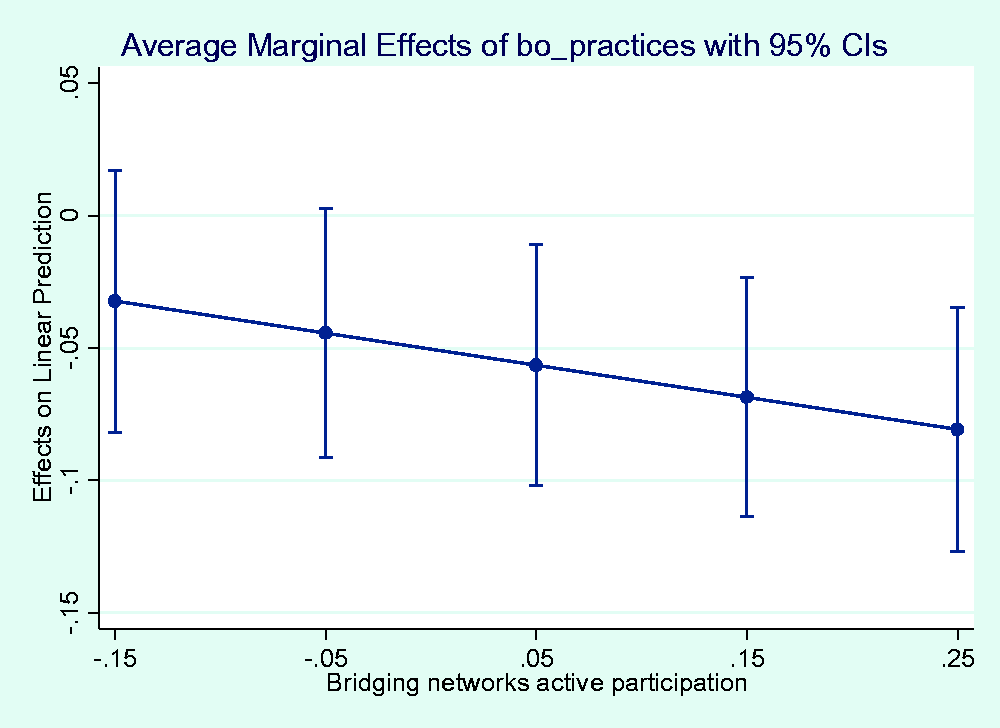

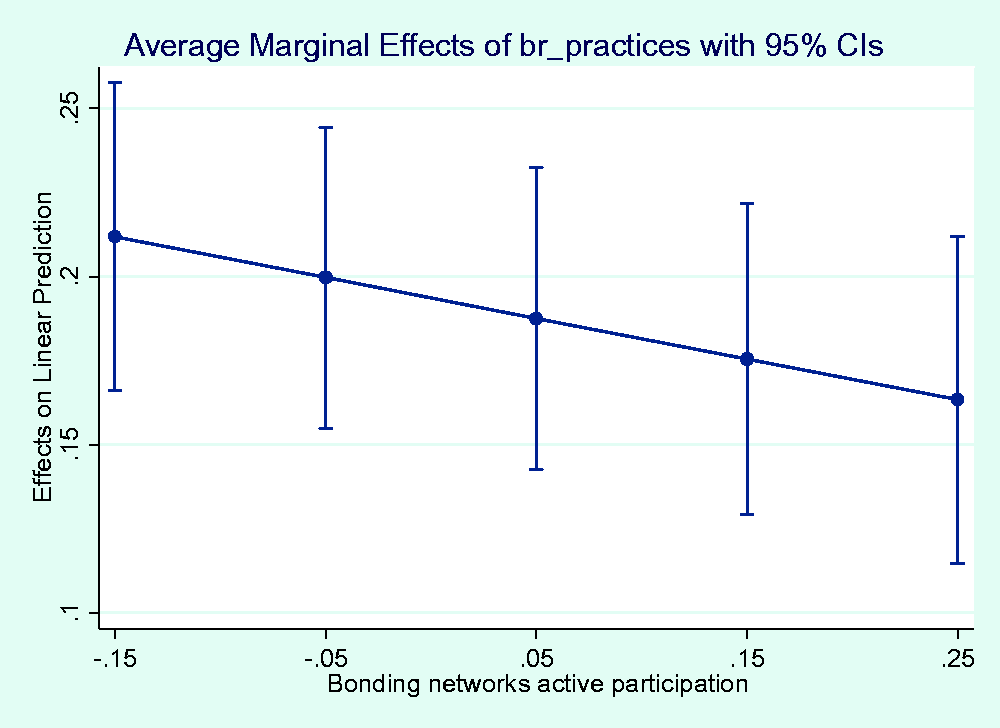

In order to interpret the interaction effects, we proceed, as advised by Brambor et al. (2006) and Kingsley et al. (2017), to plot the marginal effects (Figures 3 to 6) in order to visualise what these results mean in substantive terms. Accordingly, we plot the marginal effects of bonding social capital at different levels (from the 10th to the 90th percentile) of bridging social capital in the region, as shown in Figure 3.

Marginal effect of bonding social capital by level of bridging social capital.

Figure 3 shows the marginal effects of bonding at different levels (from the 10th to the 90th percentile) of bridging social capital in the region. Although there is a negative slope, there are no significant differences between the marginal effects of bonding at the 10th and 90th percentile of bridging social capital. The effect of bonding social capital is significantly negative at levels of bridging social capital above around -0.03, which is slightly above the median score on this variable (53rd percentile). Thus, bonding reduces economic growth only in regions with high levels of bridging. Hence, we find no evidence to support H2 that there is a positive complementarity between bonding and bridging social capital.

We also check the inverse relationship by plotting the marginal effects of bridging by different levels (from the 10th to the 90th percentile) of bonding social capital in Figure 4. Once more, there is a negative slope, but the marginal effect of bridging remains positive at all levels of bonding social capital. Bridging is associated with economic growth regardless of the level of bonding social capital in the region. There are also no significant differences between the effects of bridging at the 10th and 90th percentiles of bonding social capital. Therefore, we do not find support for H2 and theoretical propositions (e.g. Storper, 2013) that the two types of social capital complement nor substitute each other. These findings also supported by the high positive correlation between bonding and bridging, which suggests the need to investigate whether bonding social capital contributes to bridging social capital.

Marginal effect of bridging social capital by level of bonding social capital.

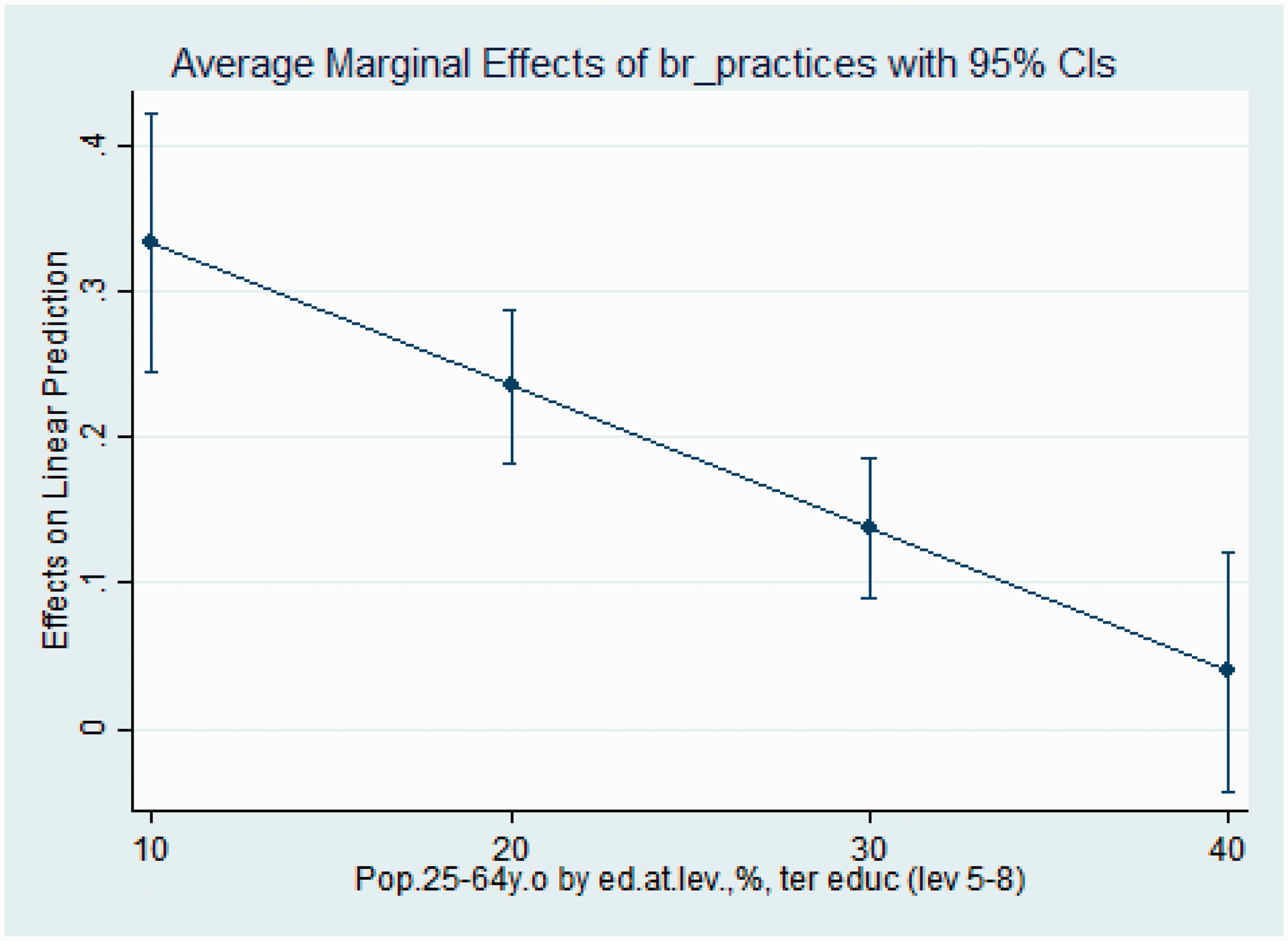

Figure 5 shows that an increase in human capital reduces the negative effect of bonding social capital. The effects of bonding turn insignificant when the share of the working-age population with tertiary education increases above 25%. This is slightly above the median level of human capital in European regions (55th percentile). The marginal effects of bonding are also significantly lower in regions where 10% of the working-age population have tertiary education than in regions where 40% have tertiary education. We thus find support for H3a that human capital moderates bonding social capital, reducing its adverse connection to economic growth. These findings confirm theoretical propositions that human capital directly (Dinda, 2014) and indirectly (Akçomak and Ter Weel, 2009; Fukuyama, 1995; Tabellini, 2010) reduces the negative externalities of bonding. Regions with high levels of human capital can generate and absorb more knowledge (Andersson and Johansson, 2010; Andersson and Karlsson, 2007; Smith and Thomas, 2017) which reduces the adverse effects of bonding social capital.

Marginal effects of bonding social capital by level of human capital.

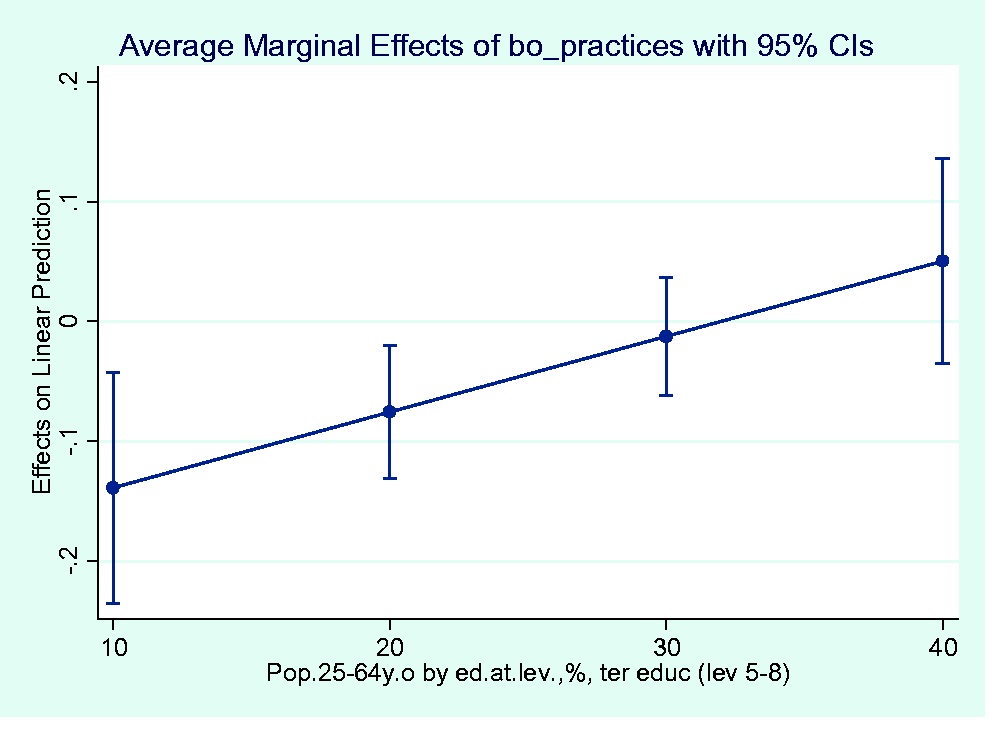

Figure 6 shows the marginal effects of bridging social capital at different levels of human capital in the region. The effect of bridging decreases as the level of human capital increases, from 0.33 in regions where 10% of the working-age population have tertiary education to 0.04 (ns) in regions where 40% have tertiary education. There are statistically significant differences between the marginal effects of bridging at low and high levels of human capital. The effect of bridging turns insignificant when the tertiary education share increases above 37% (around the 91st percentile of the variable). Hence, we find that human capital and bridging social capital are to some extent substitutes: as the human capital endowment increases, there is less need for bridging. However, bridging has a significant positive link to growth in most regions in Europe, with a few very highly educated regions representing the exception. Hence, we find support for H3b that human capital moderates the effects of bridging social capital. The findings suggest that bridging is more important for regions with low levels of human capital than for high-skilled regions. It facilitates collaboration and access to knowledge outside the region, which is particularly important if the region’s internal knowledge capacity is lower (Andersson and Johansson, 2010; Andersson and Karlsson, 2007; Mayer and Baumgartner, 2014).

Marginal effects of bridging social capital by level of human capital.

Robustness tests

We assess the robustness of the results in Table 6. Regression 1 repeats the results of the fixed-effects model in Table 4. First, in regression 2, we use the share of employment in natural resources instead of manufacturing as a control variable. The results are very similar to the results in regression 1, except that bonding social capital is only significant at the 90% level. Second, in regression 3, we use the membership of voluntary associations instead of active participation. The results retain the same signs of coefficients and adjusted R2, but the estimated coefficients are higher and the significance levels stronger. Third, in regression 4, we omit regions in the Nordic countries, which traditionally have high levels of social capital due to widespread, but often passive, membership of trade unions. Sweden also represents an anomaly relative to Denmark and Finland in terms of its low levels of bonding, especially in Central and Northern Sweden. The results retain the same signs of coefficients, but a lower significance for bonding social capital at 10% compared to 1%.

Robustness tests.

Note: Standard errors in parentheses.

***p < 0.01.

**p < 0.05.

*p < 0.1.

Finally, in Table 7, we lag the explanatory variables and controls in the regression equations in Table 6 such that they explain the level of GDP per capita in the next period (two years later). The results are consistent with those reported in Table 6. However, bonding social capital is no longer significant, although the coefficient retains the same sign. When measured in the form of membership, bonding social capital remains negative and significant. Overall, the results of the regressions in Table 6 and Table 7 show that the findings are robust to alternative specifications. However, it is not our intention to make a causal claim in this paper. Rather, we aim to offer an understanding of the phenomenon.

Robustness tests with lagged variables.

Note: Standard errors in parentheses.

***p < 0.01.

**p < 0.05.

*p < 0.1.

Conclusion

There has been a considerable amount of interest in the role of different types of social capital for economic growth (e.g. Beugelsdijk and Smulders, 2009). However, this research has remained inconclusive on how bonding and bridging social capital shape economic growth (Westlund and Adam, 2010), in particular when it comes to the effects of bonding social capital. There are gaps in our knowledge about the interaction between bonding and bridging social capital, and between social capital and human capital, especially at the regional level. The main contribution of this paper has been to address these gaps. Accordingly, we have extended existing knowledge on bonding and bridging social capital by examining the interaction between them, as well as analysing how their effects depend on the level of human capital in the region.

The analysis has three main findings. First, we confirm that bonding social capital has a negative and significant connection with economic growth when controlling for bridging social capital, while the connection of bridging is positive and significant. Second, contrary to the dominant theoretical assumptions (Storper, 2013), we do not find evidence that bonding and bridging social capital complement each other, nor that they are substitutes. Third, we find that while human capital has a moderating effect that reduces the negative effect of bonding, it is, to some extent, a substitute for bridging. Hence, bridging social capital is more important for growth in regions with deficiencies in human capital endowment.

The main policy implication stemming from the analysis is, first, that not all types of social capital are the same. Policy-makers need to focus mainly on promoting bridging social capital with the aim of bringing together heterogeneous groups as a potential channel to achieve higher levels of development. Second, building bridging networks can be a particularly effective strategy for promoting growth in low-skilled regions. Bridging social capital allows for more effective knowledge exchange and collaborative problem-solving that can, to some extent, compensate for lower levels of formal education. These traits are even more important when education levels are generally low. However, the marginal effects of bridging social capital remain positive in all but the most high-skilled regions of Europe. Regions with high levels of human capital can therefore also benefit from the promotion of bridging. At the same time, investments in human capital is an alternative approach that policy-makers can use to mitigate the negative effects of excessive bonding social capital and promote economic growth and development in less developed regions.

This study is, however, not without limitations. First, we focus only on EU regions and this limits the generalisability of the findings. Future studies should consider including more regions from other parts of the world. This will potentially improve the explanatory power of social capital and the generalisability of the findings. Second, the dependent variable is limited to economic growth. There is therefore a need to consider other socio-economic outcomes alongside economic growth. It is possible that social capital may have different effects on other socio-economic outcomes (Hauser et al., 2007; Hoyman et al., 2016; Maskell, 2000).

Furthermore, the study focused on understanding the differences and interactions between bonding and bridging social capital and how they affect economic development. The study did not examine their structural relationships, whether bonding is a necessary condition for bridging, and if it has an indirect association with economic development. However, the study reports a high positive correlation between bonding and bridging social capital, which cautions against a simplistic view of their characteristics and how they affect economic development. Therefore, there is a need for future studies to examine the structural relationship between bonding and bridging social capital and how this relates to economic performance. The same applies to the relationship between social capital and human capital.

Supplemental Material

sj-pdf-1-epn-10.1177_0308518X211000059 - Supplemental material for Social capital and economic growth in the regions of Europe

Supplemental material, sj-pdf-1-epn-10.1177_0308518X211000059 for Social capital and economic growth in the regions of Europe by Jonathan Muringani, Rune D Fitjar and Andrés Rodríguez-Pose in Environment and Planning A: Economy and Space

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The research for this article was funded by a Toppforsk grant at the University of Stavanger.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.