Abstract

Business angels (BAs) - high net worth individuals who provide informal risk capital to firms - are seen as important providers of entrepreneurial finance. Theory and conventional wisdom suggest that the need for face-to-face interaction will ensure angels will have a strong predilection for local investments. We empirically test this assumption using a large representative survey of UK BAs. Our results show local bias is less common than previously thought with only one quarter of total investments made locally. However, we also show pronounced regional disparities, with investment activity dominated by BAs in London and Southern England. In these locations there is a stronger propensity for localised investment patterns mediated by the ‘thick’ nature of the informal risk capital market. Together these trends further reinforce and exacerbate the disparities evident in the UK’s financial system. The findings make an important contribution to the literature and public policy debates on the uneven nature of financial markets for sources of entrepreneurial finance.

Introduction

Business Angels (BAs) play an increasingly important role financing start-ups across many advanced countries (Cumming and Zhang, 2019). A typical BA takes wealth accrued from their own entrepreneurial endeavours and uses it to provide risk capital, along with advice and support to new firms (Shane, 2009; Wiltbank et al., 2009). There is growing interest in angel investors, not least in the UK where they are regarded as a crucial component of the country’s financial system for small firms (British Business Bank, 2018; Wright et al., 2015), helping establish household names such as Innocent Smoothies (Grilli, 2019). Angels can have positive impacts on venture growth, survival, and employment (Kerr et al., 2014) and can help recycle entrepreneurial wealth within local economies (Clarysse et al., 2014). They play a particularly important role in poorer regions where formal venture capital (VC) is less abundant (Jones-Evans and Thompson, 2009) and can be ‘major catalysts’ of new venture creation allowing localities to follow new development paths (Martin, 2009, p. 19). Because of this, ensuring firms in lagging regions can access BA funding is an important goal of public policy (Nightingale et al., 2009).

The dominant view in the literature is that BAs predominantly have local search horizons. Indeed, one of the pioneers of angel research claimed the likelihood angels invest in firms increases exponentially ‘the shorter the distance between the two parties’ (Wetzel, 1983, p. 27). Owing to this, angels and other equity investors are often ‘dominated by parochialism’ and ‘local bias’ (Cumming and Dai, 2010; Harrison et al., 2010; Shane and Cable, 2002) with a strong preference for investments ‘in local firms’ (Cumming and Zhang, 2019, p. 693). Close proximity facilitates the transfer of ‘soft information’ which encompasses assessments of the entrepreneur, the firm and the competitiveness of its products and managerial capabilities (Hall and Lerner, 2010; Kerr et al., 2014). Consequently, there is a widely-held perception that equity investors utilise decision-rules such as the ‘20 minute rule’ (where VCs only invest in companies located within a 20 minute drive from their office) to inform decision-making (Cumming and Dai, 2010). Whereas the veracity of such heuristics is questionable, a substantial body of empirical evidence suggests that the ‘information intensive’ nature of the investment process means that equity investors have an overwhelming local bias (Cumming and Dai, 2010; Martin et al., 2002, 2005).

BAs remain a relatively under-researched topic partially due to their somewhat ‘hidden’ nature (Mason and Harrison, 2008). Reviews of the literature have noted a relative dearth of research on spatial factors associated with BA investments (Harrison et al., 2010; Tenca et al., 2018). Consequently, little is known about ‘the impact of distance’ on different types of angels (White and Dumay, 2017, p. 206). In other words, what types of angels have the strongest preferences for localised investment patterns, the people element, what types of companies they invest in, and the precise nature of their investments are all poorly understood. These were the questions posed by Cumming and Dai (2010) in their work on local bias and VC investments in the US, but to date these questions have not been addressed in the specific context of BAs. Furthermore, with some notable exceptions (Bertoni et al., 2015; Harrison et al., 2010; Herrmann et al., 2016), the overwhelming body of work on local bias focuses on the US (Harrison and Mason, 2019). This means that the UK – a country where BAs make around 2500 investments annually, amounting to around $1.5bn (British Business Bank, 2018) – has been relatively neglected.

This paper addresses these gaps in the evidence using a unique survey of 546 UK BAs. The data constitutes a significant proportion of the overall population of the UK BA market and should be broadly representative of the overall cohort of UK BAs, echoing calls for greater use of registry-based data sources to ensure a fuller coverage of the entire population of BAs (Avdeitchikova and Landström, 2016). We use this data and a series of probit regression models to answer two overarching research questions:

Is there a local bias in the investment patterns of UK BAs?

If so, what are the personal and behavioural dynamics shaping these spatial investment patterns?

We empirically examine these questions by assessing where BAs invest in the context of distance from their home base, and then identifies potential differences between BAs who have a preference for local investment and their more geographically adventurous peers in the contexts of (a) their human capital and level of investment expertise, (b) the types of investments they make, and, (c) the nature of investee companies.

Our findings make a number of contributions to the literature on the geographies of entrepreneurial finance, a topic which is crucial for regional development (Grilli, 2019; Martin et al., 2005). First, we use a large dataset which is checked for consistency and representativeness against a major UK survey conducted by the UK British Business Angels Association in 2016–2017 on key metrics such as scale of total investments, regional location of business angels, years holding investment stakes and investment motivations. Most prior work on BAs derives from smaller non-representative convenience samples (Mason and Harrison, 2008) or smaller samples as reported in a recent meta-analysis by Fili and Grünberg (2016). Our data is benchmarked against reports by the UK Business Angels Association, 86% of whom claim investor tax relief through the SEIS and EIS schemes (British Business Bank, 2018). Second, we focus specifically on BAs, a set of investors for whom the evidence base on local investment bias is thin and inconclusive. 1 Finally, given the emergence of new investment channels such as equity crowdfunding (Langley and Leyshon, 2017; Wang et al., 2019), there may be further reasons to revisit the issue of proximity (Herrmann et al., 2016).

Our work challenges the ‘local bias thesis’ and shows investing at distance is much more commonplace than previously thought. The fact more experienced angels prefer to invest on a wider geographic scale suggests some angels undergo ‘experiential learning’ which temporally and spatially alters their investment behaviour. That said, in regions where the population of BAs are most notable (i.e. South-East of England) these investments are less spatially diffuse suggesting that the nature of local demand conditions and the nature of local context remain crucial for mediating BA investment behaviour. Together these findings present stern challenges for policy efforts designed to encourage and foster angel investments as a tool for promoting regional economic development, especially in more peripheral UK regions.

The remainder of the article is as follows. The following section reviews the literature relating to entrepreneurial finance and distance. Next section presents our data and methodology. Subsequent section presents our econometric analysis and discusses the results. The last section concludes the article.

The geography of entrepreneurial finance

Informational and agency issues

Small business finance is classically thought to be a close-knit affair dominated by ‘home bias’ (De Young et al.). This ‘home bias’ may also exist within countries, and studies have shown it exists for a large number of countries (Lee and Luca, 2019). There are two strong a priori theoretical explanations for this bias: informational and agency problems. ‘Information asymmetries’ are important in credit markets (Ackerlof, 1970) as informational opacity is a key feature of start-ups and SMEs. Young and small firms are less able to convey creditworthiness to potential investors (Berger and Udell, 1998). Most SMEs lack sufficient collateral to offset these informational asymmetries (Berger and Udell, 1998). This problem is exacerbated for innovative SMEs due to their informational opacity, intangible assets and untested technology (Hall and Lerner, 2010). As a consequence, innovative start-ups are unable to access traditional forms of finance and, as suggested by the pecking order of funding preferences (Myers, 1984), resort to equity investors such as BAs and VCs (Berger and Udell, 1998).

Equity finance raises important theoretical concerns regarding agency issues. Under an agency perspective, entrepreneurs are depicted as agents or ‘potential thieves’ and investors are the principals or ‘police officers’ (Arthurs and Busenitz, 2003). This owes to the twin problems of hidden information and hidden action whereby entrepreneurs either conceal information, shirk or invest in ‘pet’ projects unaligned to the objectives of investors (Cumming et al., 2019). To mitigate against these moral hazard issues and poor decision making by entrepreneurs (i.e. the agent), the principal (i.e. the angel) has to closely monitor their investee firms.

These agency concerns are geographical because BAs invest locally to allow close monitoring of their investments (Shane and Cable, 2002). Distance ‘amplifies information asymmetries’ and creates uncertainty because of the unfamiliarity of the context within which a venture is embedded (Colombo et al., 2019, p. 1152). To cope with these problems investors’ often look to their own personal networks. To minimise the uncertainty caused by agency risks, BAs invest in companies in close geographical proximity, which some label the so-called ‘localized investor hypothesis’ (Wong et al., 2009). Shane and Cable (2002, p. 377) found that US VCs and BAs overcome the agency problems by exploiting ‘their social ties to gather private information’ about their investee firms.

There are additional reasons why the market for entrepreneurial finance may be localised. Entrepreneurial opportunities are increasingly viewed as a ‘process of social interaction (between a community and entrepreneur) rather than solely an outcome of thinking’ by entrepreneurs (Shepherd, 2015, p. 491). For angel investors, decision making is informed by close interaction and relational engagement with entrepreneurs rather than hands-off formal due diligence (Croce et al., 2017; De Clercq and Sapienza, 2001). The importance of the entrepreneur in determining investment decisions is conveyed by the metaphor ‘backing the jockey not the horse’ (Harrison and Mason, 2017) because concerns about the entrepreneur are the overwhelming reason why angels reject opportunities. Relationships and social capital are crucial mediating the link between entrepreneurs and sources of finance and these are strongly geographically embedded (Flögel, 2018; Kemeny et al., 2016; Uzzi, 1999; ). In sum, close functional proximity helps offset the risks of taking equity in opaque ventures.

Relational geographies and entrepreneurial finance

There has been an upsurge of interest in relational geographies and how distance, relationships, and networks interact and mediate behaviour (Kuebart, 2019; Wray, 2012). The relational perspective offers insights into innovation activities (Faulconbridge, 2017) because within geographical bounded spaces, relationships, networks, social capital and ‘buzz’ are pivotal relational elements (Kemeny et al., 2016). These processes by their nature are dynamic, fluid and unstructured. Storper and Venables (2004) claim it is the ‘unplanned contact system’ or ‘buzz’ which engenders learning and resource gathering opportunities “among actors embedded in a community by just being there”. By operating in close geographic proximity, entrepreneurs can “meet and mate” with providers such as banks, VCs and local BAs (van Rijnsoever, 2020). These relationships are vital for equity investors because they “depend crucially on access to personal networks and face-to-face contacts in finding, evaluating, and monitoring investment opportunities” (Martin et al., 2005, p. 1213). Not only does this enable entrepreneurs to engage with potential funders, it also facilitates trust which is a crucial ingredient mediating these financial relationships (Huang and Pearce, 2015; Uzzi, 1999). Conversely, given the central role played by social ties and relational connections, non-local ventures may find it harder to build trust with BA investors (Shane and Cable, 2002).

While distance is most commonly conceived geographically, it is also a proxy for cultural and social proximity (Bonini et al., 2018). In addition to functional proximity (distance), economic geographers use the concepts of ‘cognitive’ and ‘relational’ proximity, non-tangible proximities such as behavioural mind-set and trust with social and organisational dimensions (Herrmann et al., 2016; Kuebart, 2019; Wray, 2012). These factors also encompass things such as similar educational, social or professional backgrounds, mutual acquaintances, affinities through clubs/associations which give entrepreneurial actors common frames of reference (Herrmann et al., 2016).

A number of studies have analysed the geographies of equity investments (predominantly VC) from a relational perspective. The term ‘relational coordination’ is used by scholars to summarize the governance of relational distance between VC firms’ and their investee firms (Kuebart, 2019). Constructed relational geometries and found significant heterogeneity between different spatial finance communities in terms of their networks of connections, highlighting how VCs have numerous connections transcending regional boundaries. Whereas VCs in North East of England operated in isolation both from each other and extra-local investor networks, by contrast, East Midland finance agents operated in far less territorially bounded ways. Another German study found that VCs offset the negative effects associated with long physical distances by investing via syndicates (Fritsch and Schilder, 2012). A recent Swedish study of the geography of BAs investments found that geographic proximity was only important insofar as it facilitates close relational proximity (Herrmann et al., 2016).

Technological change seems crucial in altering relational geographies. A good example of this is the rapid onset of equity crowdfunding (Langley and Leyshon, 2017). Arguably, the digitalization of early-stage finance is reducing the need for proximity between a firm and the investor (Wang et al., 2019). Risk averse angels can piggyback on the due diligence undertaken by platforms and have their investments de-risked by small investors – the so-called ‘crowd’ (Langley and Leyshon, 2017) – obviating the need for physical closeness. So while the debate spatial proximity between investor and investee firms remains inconclusive, recent work suggests that some investors may be able to overcome negative distance effects by relational means (Kuebart, 2019; Wray, 2012).

Hypothesis development

Risk and investor experience

In the context of distance and local bias in BA investing, we discuss two key issues that may help determine preferences for investing locally: risk and investor experience. Both matter given the information asymmetries that characterise the market for capital for younger, smaller private companies (Berger and Udell, 1998). Informal equity investment markets are characterised by significant risk and investment uncertainty (Wiltbank et al., 2009). Given a significant majority of angels, have accrued entrepreneurial and business ownership experience, a form of accumulated and relevant human capital, we might expect a positive association between accumulated experience and confidently investing at distance, an empirical feature identified in prior VC studies.

As investors become more experienced they may get better at due diligence and organising their deal flow (Wiltbank, 2009). For example, Cumming and Dai (2010) found that more experience US VCs had less local bias, although specific technological knowledge could increased local bias. VCs in Canada demand a ‘lemons’ premium to offset the uncertainty of long-distance investments (Carpentier and Suret, 2006). These positive reputational effects on distance are attributed to the demand-side of the market as companies conducted active searches for VCs with a good reputation (i.e. bigger, older, more experienced, etc.), and to an asymmetric information reducing effect as ‘good’ companies seek out better quality VCs. Consistent with the sorting and matching process outlined in Cipollone and Giordani (2019), as better projects from better companies present themselves to VCs with a good reputation, this reduces the need for VCs to have representation on the boards of distant companies.

All these general inferences apply to the BA equity investment market. We have several measures of experience including: (a) having a financial qualification, (b) number of companies previously run, (c) years of investment experience, and, (d) current business ownership. Linking back to the theoretical agency concerns identified earlier, we would envisage that greater experience offsets the need for close proximity. We propose two broad hypotheses: H1: Relevant business-related human capital will be positively associated with investing at distance H2: Relevant investment related experience will be positively associated with investing at distance

Soft information flows, screening, and monitoring

Physical proximity has long been recognised as reducing the informational opacity of small firms (Flögel, 2018). Closer physical proximity facilitates the capture of soft information that more distant transactional arms-length relationships cannot replicate (Uzzi, 1999). This increases the quality of information available when making lending decisions. Intuitively, much of this would seem applicable for BA equity investments. In the angel investment setting, knowledge shared through frequent interaction is seen as a way of fostering mutual understanding and informational exchange (De Clercq and Sapienza, 2001). Plus, the transfer of tacit knowledge in both directions decreases the ‘relational risk’ by reducing misunderstandings between investors and entrepreneurs (Fili and Grünberg, 2016).

Harrison et al. (2010) identify three main informational drivers of local bias. First, the set of potential investments is geographically restricted due to ‘distance decay’ regarding information. Given sunk costs in gathering information, which rise with distance, it is cheaper and more efficient to use established local networks to identify new investment opportunities. Secondly, they argue that entrepreneur themselves has a higher weighting, and a more important role, in the investment decision of angels than by VCs (Kelly and Hay, 2003). Local networks and personal knowledge about individual entrepreneurs and investment opportunities reduces information asymmetries when investing locally (Wong et al., 2009).

Thirdly, close geographical proximity also enables effective monitoring through regular visits. This need for close monitoring was depicted in an Australian study with one angel expressing their desire to stay ‘close to my money’ (White and Dumay, 2017, p. 22). Once an investment has been made, monitoring costs increase with distance and monitoring of investments can be extended to include a more general desire for BAs to take an active role within the investee business (Shane and Cable, 2002). Sørheim and Landström (2001) found that local bias was a particular characteristic of active investors. Trust may also be geographically mediated; it appears to be an important transactional lubricant for BAs (Kelly and Hay, 2003) and has been shown to be pivotal ‘heuristic’ shaping angel investments (Huang and Pearce, 2015). Investing locally enables angels to identify entrepreneurs that they know and trust.

To obviate informational problems, BAs seek recourse to close post-investment involvement to remain in close relational proximity to their investee companies. This gives rise to our third and fourth hypotheses: H3: Business angels who want to take an active operational management role are more likely to invest locally H4: Business angels who want to take an active strategic management role are more likely to invest locally

Data, methodology and descriptive statistics

Our data was collated by Ipsos Mori, a large independent survey house, via a Computer Aided Telephone Interview (CATI) survey process in 2014, using a stratified sample drawn from a register of UK BAs. In total, our sample includes responses from 546 active BA investors. 2 The total number of BAs in the UK is estimated to be between 8000 and 15,000 (the total membership of the UK British Business Angels Association), but not all angels are actively investing at any time (British Business Bank, 2018). To the best of our knowledge this constitutes one of the largest ever samples of BAs to date (see Fili and Grünberg, 2016), 3 representing between 3.3% and 6.3% of all UK BAs.

In terms of the sample construction, the starting point was a total of 3823 individual records of individuals who had sought tax relief on their investments since 2011. After a series of checks this generated 2434 usable leads with a further 254 individuals opted out after an initial screening letter. The remainder were batched at random into subsamples with 1255 investors being uploaded into the CATI system. The questionnaire included screener questions to ensure that respondents were eligible having applied to take advantage of the tax relief. This sample was checked for its regional and investment year equivalence against UK government annual published records of risk capital investments. Random probability telephone surveys were undertaken from 5 August to 5 September 2014 after an initial pilot testing of the survey instrument between 30 July and 4 August 2014. Finally, we checked the representativeness of our achieved sample against the largest UK survey of business angels published by the UKBAA and these comparisons are reported below.

The survey covers issues relating to; (a) the personal characteristics and experiences of BAs, (b) their motivations for investing, and, (c) the nature of the investments. We note that this is a survey, rather than official data, and the answers need to be seen in this context. However, we have no particular grounds to believe that results are skewed in any particular direction. For consistency we compare our survey data against that reported by a large (n = 658 business angels) survey in 2016–2017 conducted amongst members of the UK Business Angels Association (see British Business Bank, 2018). On total value of investments, we find a close correspondence with 53% of UKBAA respondents reporting investments < = £50,000 (47% in our survey), 20% £50–99,000 (19%), and 28% >£100,000 (33%). Regarding years business angels hold their investment stakes the UKBAA survey reported 3% held their stakes for < = 2 years (11% in our survey), 57% for 3–5 years (46%), and 40% for more than 5 years (43%). The UKBAA respondents indicated that 76% invested for the returns compared to 69% investing for financial reasons in our survey. Overall, we find a degree of correspondence in responses across several key metrics which gives us confidence in its broader representativeness.

The key survey question that allows us to distinguish between BAs who have a preference for local, regional, or national investments ascertains where angels invest using the following spatial demarcations:

Within 20 miles (32 km) of you (‘Local’) Within your region (‘Regional’) Outside of your region but in the UK (‘National’) Outside of the UK (‘International’)

The survey elicited the following responses: Local, 26.8%; Regional, 18.0%, National, 53.6%, and International, 1.7%. For the following descriptive statistics and core empirical analysis we merge the last two categories due to the small numbers of BAs who invested internationally. These findings compare to European VC investment figures reported by Bertoni et al. (2015) of 48.6% within 31 miles (50 km), 22.6% between 31 and 186 miles (300 km), and 28.8% over 186 miles (300 km).

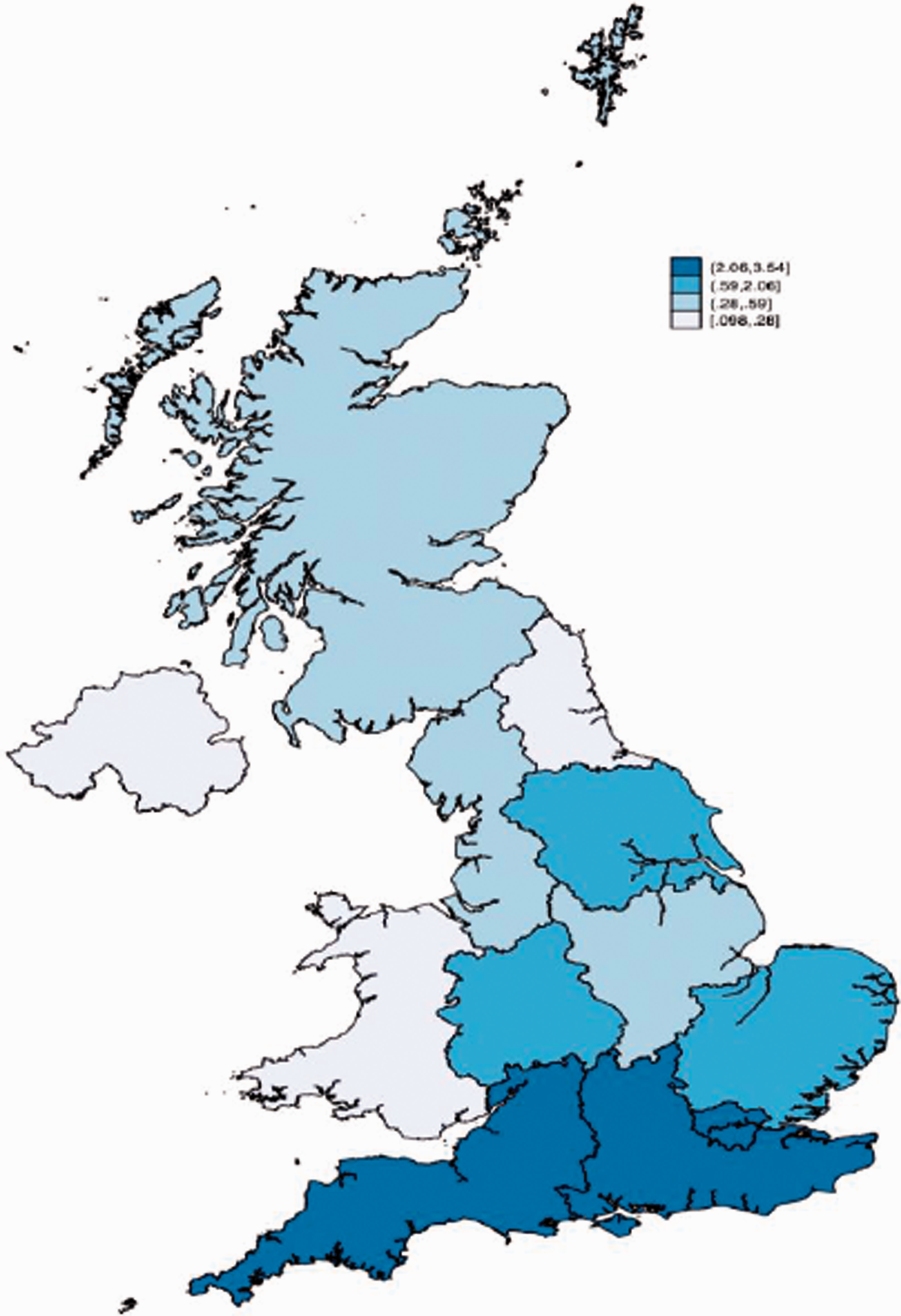

Figure 1 shows how the angel population is distributed across the UK regions. There are strong regional disparities in the respective population shares. Five regions have a greater angel share than their respective population share - London, South East England (SE), South West England (SW), West Midlands (WM), and Yorkshire & Humberside (YH). The South East has 3.5 times its population share, the South West 2.6 times its population share, and London 2.4 times, suggesting the spatial composition of our sample is consistent with the London/South Eastern focused overall BA population (British Business Bank, 2018). In contrast, the North East of England (NE) has only 1/11th of its population share, Northern Ireland (NI) 1/9th, and Wales (W) 1/5th. This highlights the significant regional disparities apparent in the UK in terms of the distribution of BAs. If all angels exclusively invested in their locality, then this would generate an uneven pattern of angel investment activity.

Regional share of Business Angels relative to regional share of population.

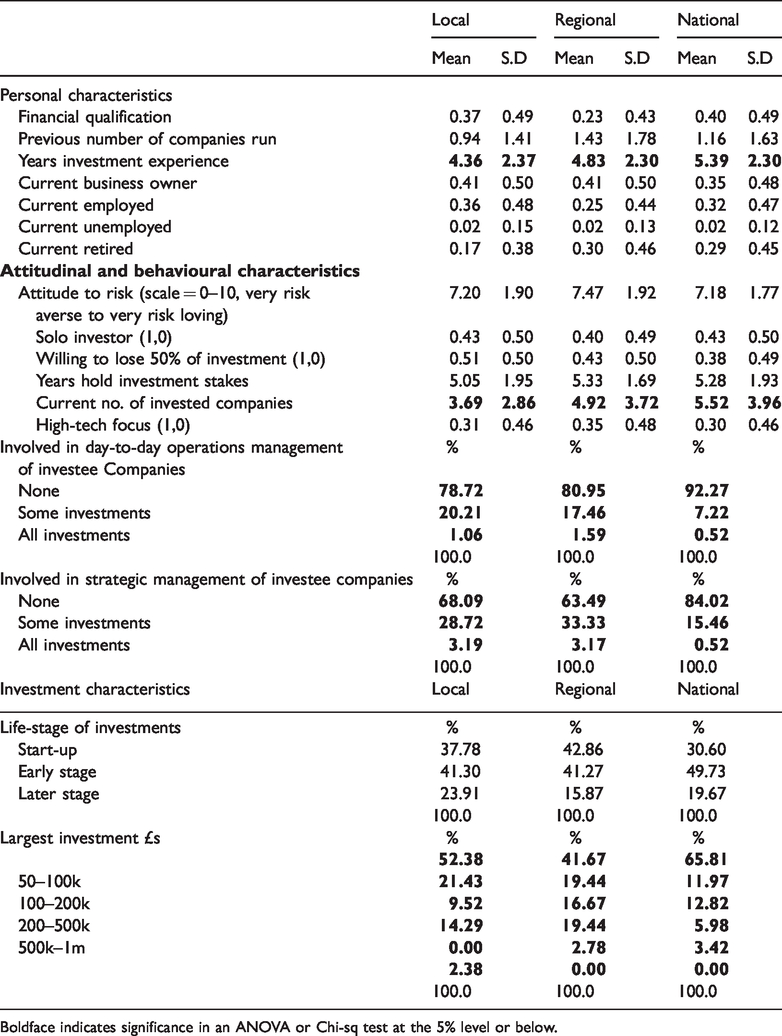

Table 1 reveals BAs with a preference for local investment are no more likely to have a financial qualification. Number of years of investment experience was clearly associated with longer-distance investments. This suggests that a willingness to invest at greater physical distance is associated with direct human capital relevant to investing, a longer track record. It also avoids the ‘stepping-on-toes’ effect which was identified by Cipollone and Giordani (2019) as a notable feature of localised investing.

Summary statistics: Personal characteristics, attitudes and behaviour, and investment characteristics.

Boldface indicates significance in an ANOVA or Chi-sq test at the 5% level or below.

Table 1 shows that risk tolerance has no effect on the distance at which they are willing to invest. Solo or co-investing investing also did not matter. On the involvement of the BA in the day-to-day operations, the majority of BAs do not undertake such roles in any of their investee companies. Importantly, the probability of being active in day-to-day operations diminishes with distance suggesting that there is a time cost which increases with distance and this constrains BA involvement. This finding is supported in respect of involvement in the strategic management of investee companies. Again, there is a negative association with investment distance. Taken together, the two strands of evidence suggest that UK BAs are very passive investors, and that this passivity increases with physical distance in the investment relationship.

Table 1 also details our data on investment patterns. There is a positive association between the number of companies a BA is currently invested in and distance, with local BAs averaging 3.69 investee companies and national BAs averaging 5.32 investee companies. This might suggest that distance encourages BAs to adopt a broader portfolio approach to de-risk their total investment.

In relation to what stage in a company’s life BAs invest in we find no spatial differences. On size of largest investment, we find that the majority of BA investments in total are for less than £50,000 supporting the consensus that angels operate at a level far below that of VCs. Nationally focused BAs have the highest incidence of the very smallest scale of investments, at 65.8%. However, we also find that the incidence of very substantial large-scale investments over £0.5 m increases with distance which again chimes with other previous studies (Harrison et al., 2010).

Results

We estimate econometric models to identify key differences between BAs who operate at three distinct spatial levels, local, regional, and national. As the classification is ordered and categorical (from local, to regional, to national), we choose to estimate a series of ordered probit models where an underlying score is estimated as a linear function of the independent variables (personal, behavioural, and investment characteristics) and a set of cut-points. The probability of observing outcome i corresponds to the probability that the estimated linear function, plus a random error, is within the range of the cut-points estimated for the outcome: Pr(outcomej = i) = Pr(κi−1 < β1x1j + β2x2j + · · · + βkxkj + uj ≤ κi) where uj is assumed to be normally distributed. We estimate the coefficients β1, β2, . ., βk together with the cut-points κ1, κ2, . ., κI−1, where I is the number of possible outcomes. κ0 is taken as −∞, and κI is taken as +∞.

We include three broad groups of control variables. As with any such survey, there is a trade-off between speed of completion and detail in the questions asked. This survey provides a relatively large sample of a hard-to-reach group, and to do so the emphasis was on clarity and concision. The first set of controls are for personal characteristics. We follow Harrison and Mason (2017) in considering financial qualifications of the BA which we feel may influence perceptions of risk. We also consider two measures of experience, number of previous companies and years of experience, and other activities, whether a business owner, employed, unemployed, or retired. Second, we include a set of behavioural or attitudinal variables. This includes perception of risk, whether sole investor, degree or day-to-day or strategic management, and whether willing to lose half of their investment. Finally, we include a set of variables for investment characteristics. This includes variables for the years they tend to hold stakes, number of companies, and whether they invest in high-tech companies. Life-stage is likely to be closely related to supervision. We also include both largest investment and, to capture a potential non-linearity as very large investments require closer and so more local supervision, largest investment squared. There is a trade-off between length or the survey and response rates. Some of these variables will, of course, hide significant nuance. But their brevity allows a larger sample size.

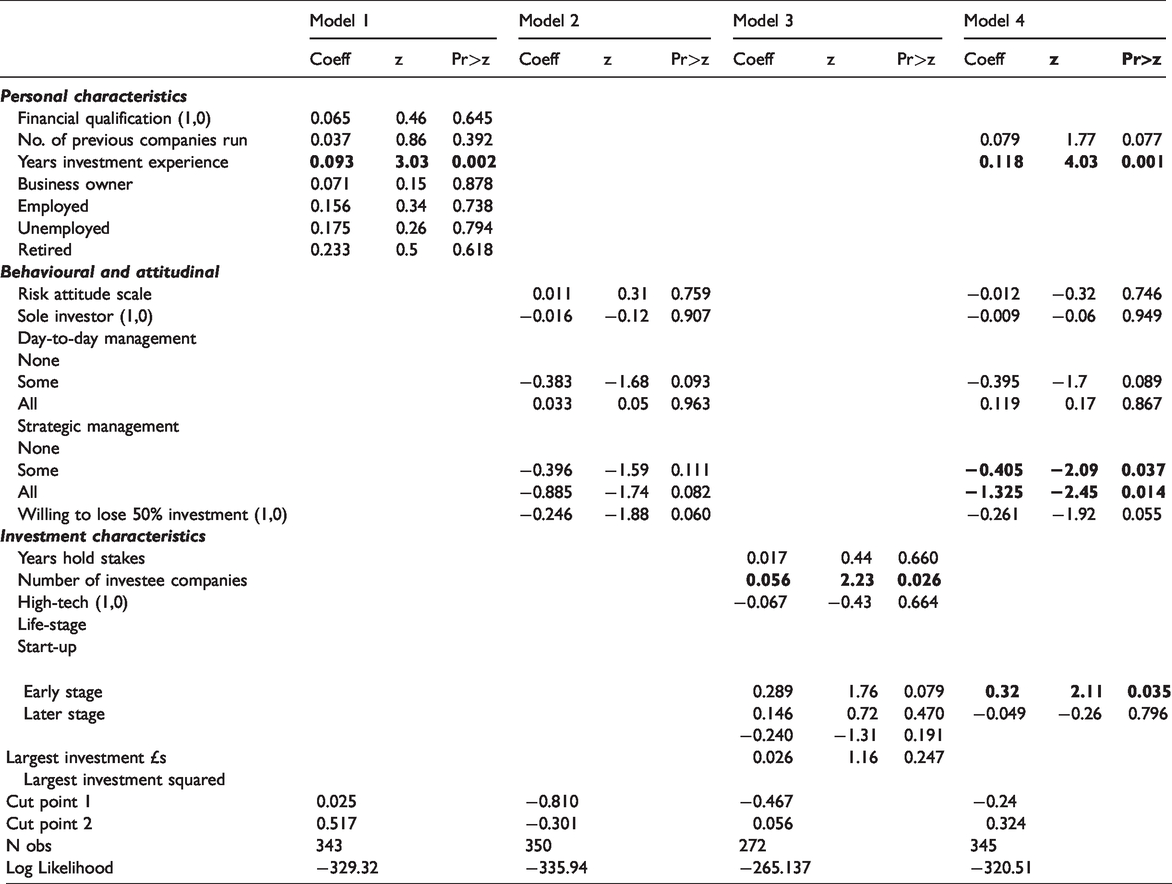

The full set of models are contained in Table 2. The first model includes the personal characteristics. This model is well specified, but the only variable that is significant is years of investment experience, which is positively associated with distance in investment behaviour: knowledge and experience gained through prior investments appears to give BAs greater confidence to invest at distance. This is in accordance with the VC literature which found that older, and more experienced VCs, with a stronger IPO track record, exhibited less local bias (Cumming and Dai, 2010).

Personal, behaviorial and investment characteristics.

Our second model, which relates to behavioural and attitudinal characteristics described in Table 1, shows that several characteristics have a weak and negative association with investment distance. A focus on day-to-day operational involvement in some investee companies (weakly) reduced the distance a BA invested at. Equally, being involved in the strategic managements of all investee companies also (weakly) reduced the distance invested at. In this sense, the more hands-on and involved BAs are, the lower the likelihood that they will invest in companies located outside their locality or region. We also find – albeit only at the 10% level of statistical significance – that BAs who are more accepting of the fact that some investment lose money, appear more willing to invest locally.

Our third model includes our set of investment characteristics. BAs with a larger set of currently invested companies in their portfolios are associated with greater investment distance. This suggests that to build up a portfolio, angels are forced to look beyond their immediate locality. In addition, BAs who invest in early-stage companies have a wider spatial reach. There were some very specific results regarding size of largest investments, with investments between £50k and £100k and between £200k and £500k having a stronger local bias than other smaller scale investments. This chimes with other work in Sweden and suggests that smaller investments with no or minimal post-investment involvement are less dependent on close spatial proximity between BAs and firms (Avdeitchikova, 2008). While very small overall, investments in the largest categories (£500k-£1m) only featured at regional and national levels. These larger investments are typically made by “super-angels” with the capacity to undertake extensive due diligence to evaluate and oversee long-distance investments.

Our consolidated model in Table 2, which incorporates elements of all three broad sets of variables, generates some very clear findings relating to investment distance. Our first key finding is that BAs who favour becoming involved in the strategic management of investee companies have a strong local bias. Again, there may be a practical aspect to this, it is easier to become involved if a company is nearby. In line with agency theory, there may also be a monitoring aspect to this as BAs can oversee the management team to ensure that they are adopting the strategic direction desired. Again, we find a positive relationship between investing at distance and years of accumulated investment experience. This may relate to confidence and also to competency. Weaker evidence shows a positive association between the number of businesses previously run by the BA, another proxy for relevant human capital and experience, and distance when investing. Finally, we note that BAs who invest in early stage businesses, as opposed to start-ups or later stage, are more willing to invest at distance. Early state businesses may require less relational support that start-ups.

Given the clear regional disparities in the distribution of BA across the UK regions displayed in Figure 1, we also augmented all four models to include a regional identifier for the business angels’ home region. Reassuringly, the core findings remain the same, but we did establish some consistent regional effects in relation to distance when investing. In our augmented model 1 which captured business angels personal characteristics, we observe weak (at the 10% level of significance) and negative effects for London (β = −0.687*) and the West Midlands (β = −0.867*). In our augmented model 2, which considered behavioural and attitudinal characteristics again we only observe two significant regional effects on distance when investing and in the same two regions, London (β = −0.916**) and the West Midlands (β = −0.780*). Our augmented third model focused on investment characteristics and here we found no regional effects. However, in our augmented fourth, and final, model, we find that three regions were associated with a distance effect. London (β = −0.773**), the West Midlands (β = −0.957*), and the East of England (β = −0.866*). This is also true to a lesser degree for BAs located in the West Midlands and the East of England. These findings strongly suggest that not only is London a place where there is a disproportionate representation of BAs per se, they also tend to invest locally and regionally than angels from other parts of the UK.

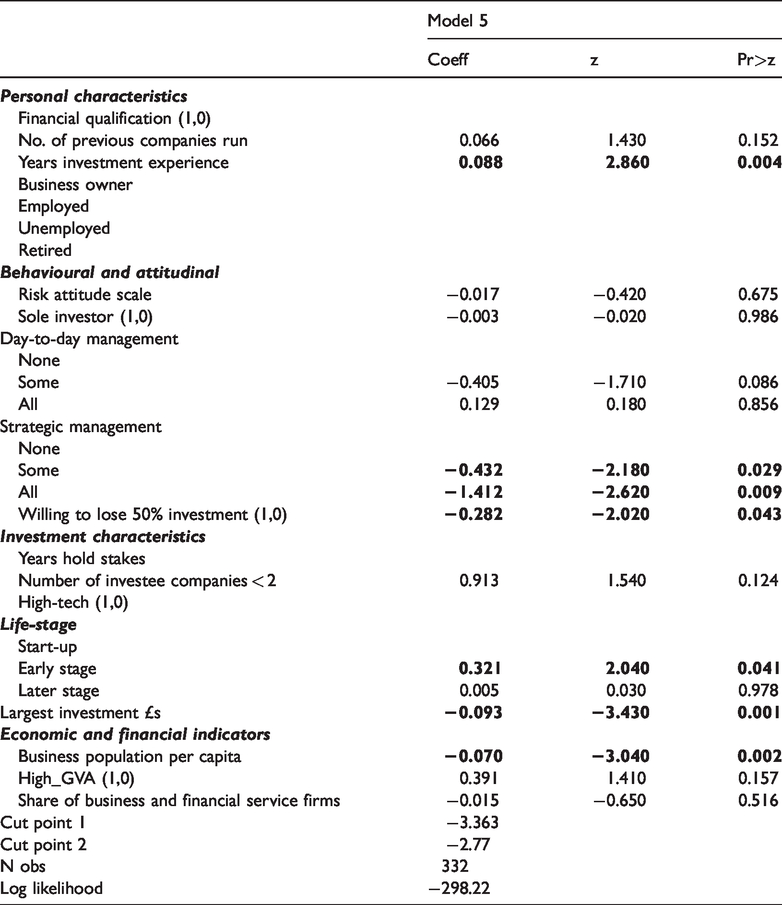

We conducted some additional analysis with the specific purpose of adding more nuance into the potential effects that economic and financial development of the business angels home region might have on their spatial investment strategy. We augmented Model 4 to include three new variables including, (i) business population per capita in the home region, (ii) whether the home region had above UK average Gross Value Added, and, (iii) the share of the business population represented in the business and financial services sectors. In order, these variables are intended to capture (a) the potential pool of investment opportunities, (b) the productivity of a region, and, (c) the level of economic and financial development proxied by business and financial services business activity which derive their incomes from the activities and growth of the core business sector. We also included a dummy variable to test whether there was something systematically different between single investment business angels and those with several (i.e more than one investment in their portfolio).

Our results are reported in Model 5 of Table 3. We find that more experienced investors are much more willing to invest at distance, but angels who prefer to adopt a more hands-on approach to strategic management in their investee companies want their largest investee companies to be geographically proximate. A greater willingness to lose money invested is associated with a preference for more local investing. In addition, business angels who invest at a larger scale are also associated with a more localised investment strategy. These latter two findings suggest that investment scale is not an issue for local investors but if they lose they would prefer to lose locally rather than in some distant company. This might relate to the greater ease of taking action to try and prevent this cash loss in a crisis situation. On our economic and financial indicators, we find that home regions with a higher per capita business population are associated with more local investment. This is unsurprising as there are costs associated with finding suitable investments at geographic distance and it is easier for a BA to locate potential local investments when there is a large business population of potential investee companies. Finally, we find no significant difference between single investment angels and multiple investment angels which reassures us that our findings are not unduly distorted by focusing on the single largest investment.

Regional economic and financial development indicators.

Discussion

Empirically, our research suggests the tendency for local bias when making investments was less prevalent than expected, especially given the informational and agency concerns identified earlier. This was particularly true for BAs located outside the more dynamic parts of the UK, such as London and the South East of England. In these southern locations there is a stronger propensity towards more localised investment which we unpack below. Overall, however, this corroborates others who have suggested that the prevalence for local investing by BAs has decreased over time which may reflect a wider evolution of the BA investment market (Avdeitchikova, 2008; Harrison et al., 2010; Herrmann et al., 2016).

We generate novel findings suggesting investment experience is the dominant form of human capital in UK BA investing. In the context of our four initial hypotheses, we find weak support for a positive relationship between business related human capital/experience and investing at distance, but a much stronger and clearer positive relationship between investment experience and investing at distance. On active involvement in investee companies, we find no relationship in respect of active involvement in day-to-day operational management and local bias, but a strong local investment bias for BAs who like to actively participate in the strategic management of their investee companies. On balance, we have some consistency with the VC based evidence on distance and local bias, and indeed banking and crowd funding too.

What is driving the process of greater longer-distance angel investing? It is now widely considered that the angel market is much more organised via networks whereby angels collectively pool their resources and investments via syndicates (Kerr et al., 2014). This changes the dynamics of BA finance, altering the manner and professionalism within the investment process (Bonini et al., 2018). In turn, this may be leading to less spatial embeddedness across angel investors, enabling local angels to access firms across a wider spatial catchment area. This chimes with work showing how syndicates offset the risks of more spatially diffuse VC investments (Fritsch and Schilder, 2012).

Another related explanation attributes this trend to the increased use of equity crowdfunding platforms. Some studies have revealed almost half (45%) of all UK angels invested via equity crowdfunding platforms (Wright et al., 2015). Crowdfunding platforms may prove attractive for less experienced angels seeking passive investments with a limited administrative burden. Given the increased propensity for angels to invest in crowdfunding platforms (Brown et al., 2018; Wright et al., 2015), in time this may recalibrate the nature of local bias within BA investing, especially for smaller more ‘hands off’ equity investments.

From a theoretical perspective, we anticipated informational distance decay and agency concerns to preclude long-distance investment. However, it appears that some BA investors may be adopting different strategies to obviate distance effects by other relationship enhancing means which are reconfiguring the relational geography of these informal equity investments. Clearly, the relational geographies of BA investors are being reformulated by a range of professional networks (e.g. syndicates) and technological processes (e.g. equity crowdfunding). The angels examined also displayed an ‘effectual’ or experimental logic by starting out close to home and then expanding their investment networks further afield (Wiltbank et al., 2009). Clearly, the attitudes and behaviours of angels change with experience (Herrmann et al., 2016). As BAs gain experience their proclivity to invest more widely increases, suggesting important ‘learning by doing’ effectual processes. With accrued experience the need for a hands-on approach based on close physical distance diminishes.

In this sense, we could argue that local bias is important for novice BAs as it provides a good ‘nursery’ where they can use their well-established local networks and strong relational proximity to actively monitor and get physically involved in the management and strategic decision-making of their investee companies. But once sufficient experience has been accumulated, angels are happier making more passive ‘hands off’ investments across the UK and feel less need to ‘babysit’ their investee companies. To mitigate attendant agency risks of longer-distance investing, UK BAs seem to concentrate their larger investments locally with longer-distance investments in the small sub-50k categories.

Conclusions

This study considers the under-researched issue of local bias in informal risk capital. First, we found that an absolute majority of BA investments are made outside of the angel’s immediate locality and home region, calling into question the ‘local bias thesis.’ In this sense, perhaps due to its geographical ‘compactness’ and changing relational geographies the angel market in the UK is becoming more mobile, especially for more seasoned BAs. Clearly, the relational geographies of BA investors are being reformulated by a range of professional networks, new investment vehicles and technological processes (e.g. equity crowdfunding).

A key finding is that investment experience dominates business experience in the context of investing at distance. Plus, there appears to be a strong ‘learning-by-doing’ effect through which individuals engage in investment activity become more experienced and gain the confidence to invest at arms-length in a literal (passive investor) and physical way (at greater distance). Angels undergo important changes to their investment behaviour which are temporally, experientially and spatially mediated. The second major empirical contribution centres on the major spatial imbalances identified within the geography of informal risk capital in the UK. These regional disparities and stronger propensity for localised investment patterns by angels in southerly regions are undoubtedly mediated by the well-developed or ‘thick’ nature of informal risk capital market in these locations compared to the ‘thin’ markets evident within the UK’s more northerly peripheral regions. 4 A concentration of BAs in the most affluent parts of the UK is reflected in a higher number of investable opportunities in these areas as well. This is symptomatic of the spatial centralization of the UK’s financial system which new fintech technologies (i.e. crowdfunding) seem to be exacerbating rather than overcoming, thereby providing further evidence that financial markets – in driving capital to core regions – are perpetuating uneven regional development (Klagge et al., 2017).

The research has important public policy implications. As noted earlier, there are deep-seated spatial imbalances in the distribution of BAs across the UK which restrict the ability of start-ups and new ventures to obtain inter-regional capital transfers from BAs located in the South-East of England. Additionally, while considerable policy efforts have been devised to help develop localised networks of BAs across some peripheral UK regions such as Scotland and the North-East of England (Martin et al., 2002), these may not necessarily benefit local start-ups if more experienced angels seek out investment opportunities further afield. Clearly, however, steering the locational whereabouts of BA investments is a difficult, if not impossible, policy objective. However, policy makers in finance-deficient regions may have to make concerted efforts to foster links between their nascent entrepreneurial ventures and angels located outside their local region to facilitate ‘cross-regional’ access to angel investment (Clarysse et al., 2014).

Our research opens up interesting avenues for further research. Our data is from 2014 and there have been significant changes to the market for entrepreneurial finance since then, most recently the shock caused by the Covid-19 pandemic. If time-series or panel data on BAs becomes available, it would be interesting to establish the temporal dynamics of the experience-distance relationship. A future key issue warranting further investigation is what impact the growing role of equity crowdfunding is having on BA investors. Further in-depth research on this topic would be useful for probing how technology is changing the relational geographies of BA activities and how this affects the investment-distance nexus.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.