Abstract

Co-investment funds – which invest alongside private investors, especially business angels – thereby leveraging their networks and experience and minimizing public sector transaction costs – are a recent approach by governments in various countries to address the early stage entrepreneurial funding gap which is perceived as a barrier to the ability of firms to scale-up. However, little literature exists on their operation, impact and effectiveness. This paper assesses the early operation of the UK’s Angel Co-investment Fund, established in 2011. Interview evidence from angels and business managers suggests that the Angel Co-investment Fund is improving the availability of finance by enabling firms to raise funding rounds of between £500,000 and £2 m, hence addressing some aspects of the broken finance escalator model. However, our evidence suggests that it is not yet impacting the supply side, either in terms of stimulating the formation of new angel groups or enhancing learning amongst less experienced angels. Some aspects of the operation of the investment process have attracted criticism from angels and entrepreneurs which need to be addressed. Nevertheless, there is sufficient evidence for positive impact to justify the scheme’s expansion.

Introduction

Policy interventions to address the funding gap for entrepreneurial ventures have largely involved the establishment of Government Venture Capital Funds (GVCFs) to invest in those parts of the market which private sector VCs avoid, typically in the sub-£250,000 range but increasingly also larger amounts as VC funds have progressively shifted to larger and later stage investments, and in peripheral regions (Baldock and North, 2015; Lerner, 2009, 2010; Mason and Pierrakis, 2013; Murray, 2007; Technopolis, 2011). Over time this approach has shifted from direct investment via publicly funded and managed funds to hybrid funds (Murray, 2007) in which public money is used to leverage private investment into funds that are operated by private sector fund managers. These hybrid fund principles are now increasingly used by governments to establish co-investment funds (CIFs). These fall into two distinct categories. First, some CIFs pre-approve their investment partners (angel groups and venture capital funds): every investment that these partners make that meet the investment criteria of the CIF will automatically attract co-investment. Second, there are CIFs which make their own decision on every investment opportunity that is brought to them.

However, both approaches maintain the principle in which public sector money follows private sector investors – both VC funds and business angels, but more often the latter – investing alongside them in deals that these investors bring to the CIF, and thereby leveraging their networks and expertise and at the same time minimising the public sector’s transaction costs.

The concept is widely attributed to the creation of the Scottish Co-investment Fund, established in 2003 in response to the contraction of the VC sector following the post-2000 technology crash (Pierrakis, 2010; Technopolis, 2011). It has since been replicated in New Zealand and Ontario, Canada. CIF schemes have also been established in various UK regions, notably by the former Regional Development Agencies and in London (London Seed Capital). Co-investment schemes have also been established in several other countries, including Denmark (since closed), Sweden, Belgium, Germany and Portugal. More recently in 2012 the EU, through the European Investment Fund (EIF), established pilot European Angels Fund (EAF) CIFs in Germany, Spain and Austria and will soon expand the scheme to other EU countries (EIF, 2015). However, there are significant differences in the design and emphasis of these various schemes.

The importance of evaluating GVCF schemes at an early stage has been highlighted by several authors (Baldock, 2016; Lerner, 2009, 2010; Tokila and Haapanen, 2009). Whilst this cannot predict scheme success it can adjust for agency failures around poor management and mission creep, and assess scheme additionality versus duplication (Baldock, 2016). This enables design improvements to be made around management, promotion and implementation (e.g. selection processes) and to establish wider impacts on the supply-side (Lerner, 2010), including the business angel community (Mason and Harrison, 2015) and VC development (Baldock, 2016).

This paper is an attempt to address this need for early evaluation. It examines the role, operation and initial impacts of the UK Angel Co-investment Fund (ACF). Established in 2011, the ACF offers up to 49% matching funds for angel investments with between £100,000 and £1 m public spending cap per investment. The Fund has two aims: first, conventionally, to invest alongside angel groups to enlarge the funding round and facilitate follow-on funding, giving investee businesses sufficient financial ‘runway’ in which to scale; and second, to stimulate the supply side by encouraging the creation of new angel groups and disseminating best practice in investing.

The paper proceeds by examining current theoretical debate around CIFs and their role in overcoming a seemingly broken entrepreneurial funding escalator. It then presents an overview of the ACF, research methodology and propositions and key findings, focusing on the scheme’s business demand-side and business angel supply-side impacts. It concludes with theory, policy and further research observations.

Co-investment Funds: A theoretical review

This section examines early stage entrepreneurial finance gap theories in the context of the developing post GFC UK finance escalator. It then goes on to consider key agency and design theories relating to the operation and delivery of government VC funds (GVCFs) and more specifically the evolution of Angel-Oriented CIFs (A-OCIFs).

The finance escalator, finance gaps and emerging new UK escalator

The need for CIFs arises on account of the break-down of the so-called funding escalator (NESTA, 2009) which provides a supply-side theory-informed representation of the different types of entrepreneurial finance available to businesses as they progress from seed finance through the stages of development to a trade sale or IPO 1 (for example, see NESTA, 2009). This adopts Berger and Udell’s (1998) entrepreneurial finance model which explains how the range of finance available to businesses changes and increases as they become less opaque and overcome information asymmetries with funders. Baldock and Mason (2015) adopt Myers and Majluf’s (1984) pecking order theory of entrepreneurial preferences for types of finance, suggesting that within equity finance, some entrepreneurs will prefer more personalised and tailored angel finance over the more formal and less intensive support of VC managers.

Indeed, post-GFC, the role of angels as a source of risk capital has increased significantly both in the UK and internationally (OECD, 2011; Wilson and Silva, 2013). In those countries where data are available there was either no decline in business angel investment in the immediate aftermath of the GFC (Mason and Harrison (2015) or only modest short-term decline and subsequent strong growth (EBAN, 2014; Sohl, 2015), in marked contrast to trends in bank lending and venture capital investment (Wilson and Silva, 2013). This has fundamentally damaged the often critical complementarity between business angel and VC funds, which, in turn, has severely undermined the funding escalator (Gill, 2010). It has also been a key driver for angels to group together into managed angel groups to create the financial capacity to make follow-on investments to bridge this widening VC gap (Mason et al., 2013).

Recent UK evidence suggests an emerging post-GFC finance escalator that has been impacted by a number of structural and cyclical changes. First, the banks have retreated to a ‘new norm’ of not providing equity finance under loan terms and conditions and, therefore, not funding early stage businesses with less than two year trading records (Davis, 2011). Second, private VCs have retreated from early stage investment, a trend that is traceable to the Dot.com bubble burst (Wiltbank, 2009) and evidenced by Murray (2007) and Mason and Pierrakis (2013). Third, a much tougher post-GFC investment exit market for trade sales and IPOs (given the illiquidity of the UK AIM 2 public feeder market for small cap firms, Baldock, 2015) has led to the extension of investment horizons (CfEL, 2013; Mason et al., 2010). This has resulted in the locking-in of angel and VC funds as these investors have been forced to maintain and continue to finance those companies in their portfolios that were unable to exit 3 (or abort and lose investments). Fourth, the seed capital market has been revitalised by the introduction of the Seed Enterprise Investment Scheme (SEIS) investor tax incentives in 2012. 4 However, the consequence has been the creation of a ‘series A crunch’ with increasing numbers of seed capital-backed companies seeking follow-on investment. A final change has been the exacerbation of the ‘Rowlands gap’ (Rowlands, 2009; SQW, 2009) for patient capital. Recent evidence from Baldock et al. (2015) found two persistent gaps for longer horizon (R&D taking five years plus to reach market) early and growth stage finance (particularly in the 2–5 year trading stage). The first is the classic £200,000 to £2 m gap which the UK ACF is seeking to address and the second is the ‘series A-B time-bomb’ where larger scale £2 to £10 m plus finance is required for relatively young pre-trading or early trading businesses with under the £5 m annual sales turnover qualification for the Business Growth Fund (BGF). 5 The ability of the ACF to provide follow-on funding may provide an important bridge in this respect.

GVCFs and emerging role of CIFs

Co-investment Funds are a relatively recent public sector response to these structural changes in the supply of entrepreneurial finance. They have emerged during a period of increasing perceived need and reliance on government interventions (Mason and Pierrakis, 2013; Murray, 2007; Wilson and Silva, 2013) to address the seed and early stage funding gap post the Dot.com crisis (2001).

Very few GVCFS have been deemed successful (Brander et al., 2008; Colombo et al., 2014; Lerner, 2009; Mason, 2016; Munari and Toschi, 2014). Many have experienced agency failures (Akerlof, 1976) leading to inadequate approaches to information asymmetries (e.g. ineffective due diligence) and policy implementation. This has occurred through too much government control with investment decisions made by bureaucrats rather than experts (Lerner, 2002), their inappropriate investment focus (size of investment, sector, geography) and insufficiently skilled local VC managers.

A major finding of Lerner (2009, 2010), stemming from Israel’s Yozma funds transformation of Israel’s VC industry from 1993, was the importance of enabling private sector VC leadership and attracting leading, experienced fund managers internationally to take the lead on investment decisions and to train and develop local junior VC managers (North and Baldock, 2016). Studies point to the importance of experienced hands-on private sector fund managers, indicating that successful VCs have niche ‘hard to imitate’ knowledge of sectors and stages (BIS, 2011) and are persistent performers who build on their experience over time (Gompers et al., 2010; Zarutskie, 2010). This argument can be extended to the key role of experienced business angels in leading angel investment groups and their ability to pass on their skills to junior angel investors through syndication and networking activities. This can potentially raise angel investment standards through communities of practice (Mason and Harrison, 2015; Mason et al., 2016).

Murray (2007) describes the development of private VC-led CIFs as ‘hybrid funds’, where government provides a proportion of funding to lever matched funding from private VCs. A key feature of these schemes is their different approaches to incentivising and encouraging private investment. These can be generated directly through setting attractive minimum matching percentage requirements for private investors (i.e. one third for UK ECFs, 6 50% for the New Zealand Venture Investment Fund (NZVIF) and 51% for the ACF) and scheme upside investment returns (e.g. UK ECFs 7 ), or through allowing indirect tax breaks such as the UK’s SEIS 8 for angel investors which applies to the ACF (Baldock and Mason, 2015).

Lerner (2010) suggests that the emphasis on CIFs to finance experienced and previously successful private fund managers and allow them to make business portfolio investment decisions within the parameters of the schemes (e.g. sector, location, business stage) improves targeting into viable businesses. However, he also recognises that investments require regular monitoring for market distortion and duplication (Leleux and Surlemont, 2003) and mission creep (Murray et al., 2009) to ensure that schemes continue to address funding gaps. We now look more specifically at CIF design.

CIF design theories

Mounting evidence has also led to an understanding of key GVCF design features (Baldock, 2016). First, Lerner (2010), Technopolis (2011), Cumming et al. (2014) and Baldock and North (2015) recognise that funds require sufficient size, scale and range. Small-scale, regional and sector specific funds often fail to find sufficient high quality investments, or have insufficient funding for follow-on investments into their better performing portfolio companies. This leads to a failure to achieve Markowitz (1952) optimal VC portfolio fund size and to facilitate follow-on investment to keep their best portfolio firms to a point of optimal exit, typically via trade sale or IPO (Cumming et al., 2014).

Second, Lerner (2010) highlighted Yozma’s 10 year restricted Limited Partnership funds as encouraging a cycle of dynamic fund investment and return redistribution into new funds, overcoming the potential for mission creep and poor incentive to deliver returns experienced by evergreen public VC schemes (e.g. GVCFs in Finland: Murray et al., 2009). However, investment horizons for early stage investments to reach exit, notably post-GFC, have doubled from four to eight years on average between 2000 and 2015 (Axelson and Martinovic, 2012; Mason and Harrison, 2015), requiring flexible ‘long game’ thinking in relation to VC programme length (Lerner, 2010). 9

Third, this has brought into sharper focus the need for second fund financing rotation (Baldock, 2016; Dittmer et al., 2014), or to revisit evergreen funding options, such as through deal based CIFs (Baldock and Mason, 2015). These can potentially combine with the trend for larger angel groups to make ongoing multiple rounds of funding by stretching their funding capability, even in some cases enabling them to take businesses to an exit without raising follow-on investment from VC funds.

Finally, Hopp (2010) and Baldock (2016) introduce VC management practice as a way of smoothing portfolio companies’ funding continuity through improved syndication between VCs and angel groups notably in developing international investment and market opportunities. This can be extended to angel-led investments, such as those operating through the ACF. Here, the scheme’s scale-up of angel investment may offer more opportunities for angel groups to negotiate syndicated VC partnership arrangements on equal terms, empowering them to avoid negative later stage ‘VC crushing’. In this respect, Mason et al.’s (2016) development of Wenger et al.’s (2002) communities of practice theory, suggests that angel groups, such as those operating under the ACF, can enable diffusion of best practice angel investment, raising investment quality and improving ability to syndicate, follow-on fund and successfully exit.

The emerging role of Angel-Oriented CIFs

From the early 2000s, other forms of co-funding arrangements have emerged which focus on providing government funding which could be matched to individual business investment deals. Many, such as the pioneering Scottish Co-investment Fund and the New Zealand Seed Co-investment Fund, primarily operate with business angels, since they are responding to the early stage funding gap vacated by private VCs during this period (Mason and Pierrakis, 2013; Murray, 2007). This study focuses on recent A-OCIFs development and specifically the role of the UK ACF.

A-OCIFs are typically evergreen in design, working on a revolving fund principle of reinvesting returns. In the post-GFC economic environment with increased investment exit timetables the greater flexibility afforded to the evergreen ACF is considered by industry experts (BVCA, UKBAA, EIF 10 ) to be a considerable advantage (Baldock and Mason, 2015).

There is little literature on A-OCIFs. The main sources are an early evaluation of the Scottish CIF (Hayton et al., 2008) and overviews by the Swedish Agency for Growth Policy Analysis (Tillväxtanalys) (2009, 2013). International overviews are provided by Wilson and Silva (2013), EBAN (2012), OECD (2011) and Aernoudt et al. (2007). They highlight a small but growing number of A-OCIFs dedicated to angel investment operating at national and regional scales with several common features. The CIF invests a maximum of 50% of the total investment in the business with an upper limit to the size of its investment: for the Scottish CIF this was initially £500,000 and subsequently increased to £1m. Matched funding is usually equity based, although some schemes have provided loan funding. Normally the equity funding is made on a pari passu basis (i.e. with no direct private sector return incentive) with the CIF investing on the same terms and conditions as the private investor.

The main contrast between A-OCIFs relates to their involvement in identifying and selecting investments. The Scottish CIF is passive, based on selecting approved private sector investment partners – managed angel groups and VC funds. The investments that these partners bring to the Fund automatically qualify for co-investment if they fall within its parameters (e.g. sector). The Scottish CIF, therefore, does not generate its own deal flow, undertake its own due diligence or play any part in the investment (but retains board rights). It invests on identical terms and conditions as its private investors. So, rather than ‘picking winners’ (businesses) as in the past, in this model the public sector is ‘picking partners’ (investors), removing any uncertainty for the investor, and reducing scheme operating costs to a minimum (Hayton et al., 2008). This model has low delivery costs.

Other A-OCIFs are more actively managed, inviting investors to bring deals to them, or they may approve deals from particular sources, such as specific business angel networks (BANs). For example, London Seed Capital co-invests with the London BAN. The critical difference with this co-investment model is that these Funds make their own investment decisions and may invest on different terms and conditions to those of the angel group. For example, London Seed Capital co-invests with the London BAN.

Although evidence is limited, A-OCIFs appear to have significantly increased the volume of investment activity in the early stage equity market, enabling angels to participate in larger deals than would otherwise have been the case. However, the only scheme to have been evaluated is the Scottish CIF (Hayton et al., 2008) and this is now dated. This highlights angel groups as the main partners, representing 82% of its early investments (and likely to be higher post GFC). By offering matched funding the A-OCIF provided angel groups with greater liquidity to make new investments, larger investment and develop substantial follow-on investments that were otherwise not possible.

A-OCIFs have three limitations. First, like other GVCFs, they are constrained by the supply of investable businesses. The partners in the Scottish CIF identified investment readiness as an issue, notably in the West of Scotland. One way in which the funds overcome this is by operating at a national scale and across a wide range of sectors to ensure that sufficient numbers of viable investible businesses can be found. This could potentially include investing pan-nationally (Dittmer et al., 2014), as in the case of some VC-led CIFs such as the UK Innovation Investment Fund (Baldock and Mason, 2015).

Second, CIFs require to partner with organised angel groups in order to provide efficient gateways for collective angel funding into the schemes (Mason and Harrison, 2015). The existence of angel groups is therefore critical. This requirement clearly limits their role in regions with undeveloped angel markets, or dominated by angels investing individually or in ad hoc groups. In this regard the abolition of the English Regional Development Agencies (RDAs) in 2012, which funded the development of regional business angel networks (which provided an introduction service to enable angels and entrepreneurs to connect) may have undermined the ability of the ACF to invest across the UK. The recent emergence of managed angel groups – angels who invest together rather than as individuals or small ad hoc groups (Mason et al., 2016) – has therefore also been critical for the establishment of A-OCIFs. Scotland was fortunate in having a handful of established angel groups at the time that the Scottish CIF was conceived. Indeed, these groups had lobbied hardest for this type of initiative. The success of the Scottish CIF can be linked in large measure to the encouragement and support for new angel groups undertaken in parallel by LINC Scotland, the trade body for business angels (Mason et al., 2016). A further consideration is therefore that Wilson and Silva (2013) find that A-OCIFs give little consideration to investor training which, given the importance of their working with organised angel groups, may form an important agency related policy consideration.

Third, there is a possible risk of moral hazard, with angel groups funding their best deals themselves but bringing their weaker deals to the A-OCIF. However, in practice there is no evidence to support this concern, since the main advantage of the A-OCIF is to stretch-fund investments to create more substantial and sustainable investments (Baldock and Mason, 2015).

Despite their growth, there has been relatively little policy evaluation of CIFs. Moreover, the demand-side is often overlooked in such evaluations (Wilson and Silva, 2013). The recent study of public UK VC by Munari and Toschi (2014), which focused on fund exits as a barometer of success, highlighted the problems of fund evaluation, whilst Baldock and Mason (2015) and Baldock (2016) note that it is even more difficult to evaluate funds at an early stage, prior to exits. However, as Lerner (2010) suggests, early stage evaluations are about addressing agency and programme design and delivery issues to refine schemes, ensuring that they are operating efficiently in addressing a market gap, demonstrating additionality, avoiding duplication and displacement and avoiding mission creep. At the early stage, therefore, focus should be on scheme processes such as promotional visibility and accessibility (including timelines to accessing finance), additionality and spillover measurements (Baldock, 2016; Baldock and Mason, 2015) and assessments of displacement (Lerner, 2010) between public funds and crowding out of the private sector (Leleux and Surlemont, 2003).

Overview of the ACF

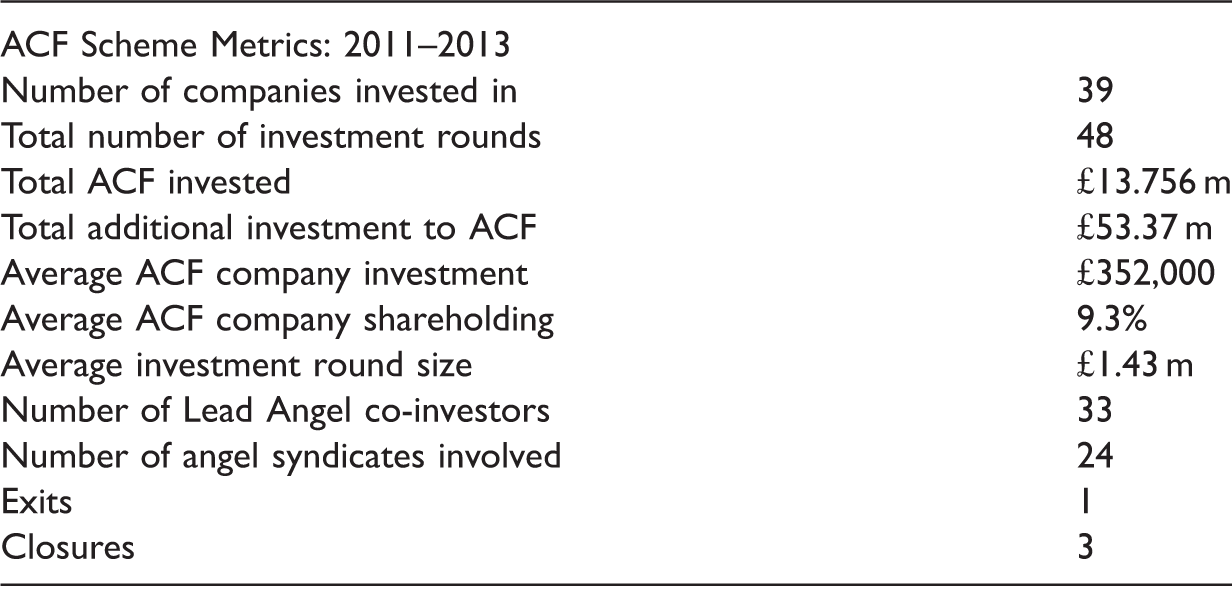

The UK government’s £100 m 11 ACF, launched November 2011, invests between £100,000 and £1 m in SMEs alongside syndicates of business angels. 12 Qualifying SMEs have under 250 employees, €50 m annual sales turnover and €43 m of assets on their balance sheet. 13 All sectors are eligible, with investments addressing the current equity finance gap for early stage, potential high growth firms. The ACF is evergreen, reinvesting investment returns to enable its perpetual operation. Initially, restricted to England, following Parliamentary Assent in Spring 2014, it now has a UK-wide investment mandate. At the time of this early assessment all 39 ACF initial investments were in England. 14

ACF Scheme Metrics 2011–2013.

Source: British Business Bank, December 2013.

ACF: Angel Co-investment Fund.

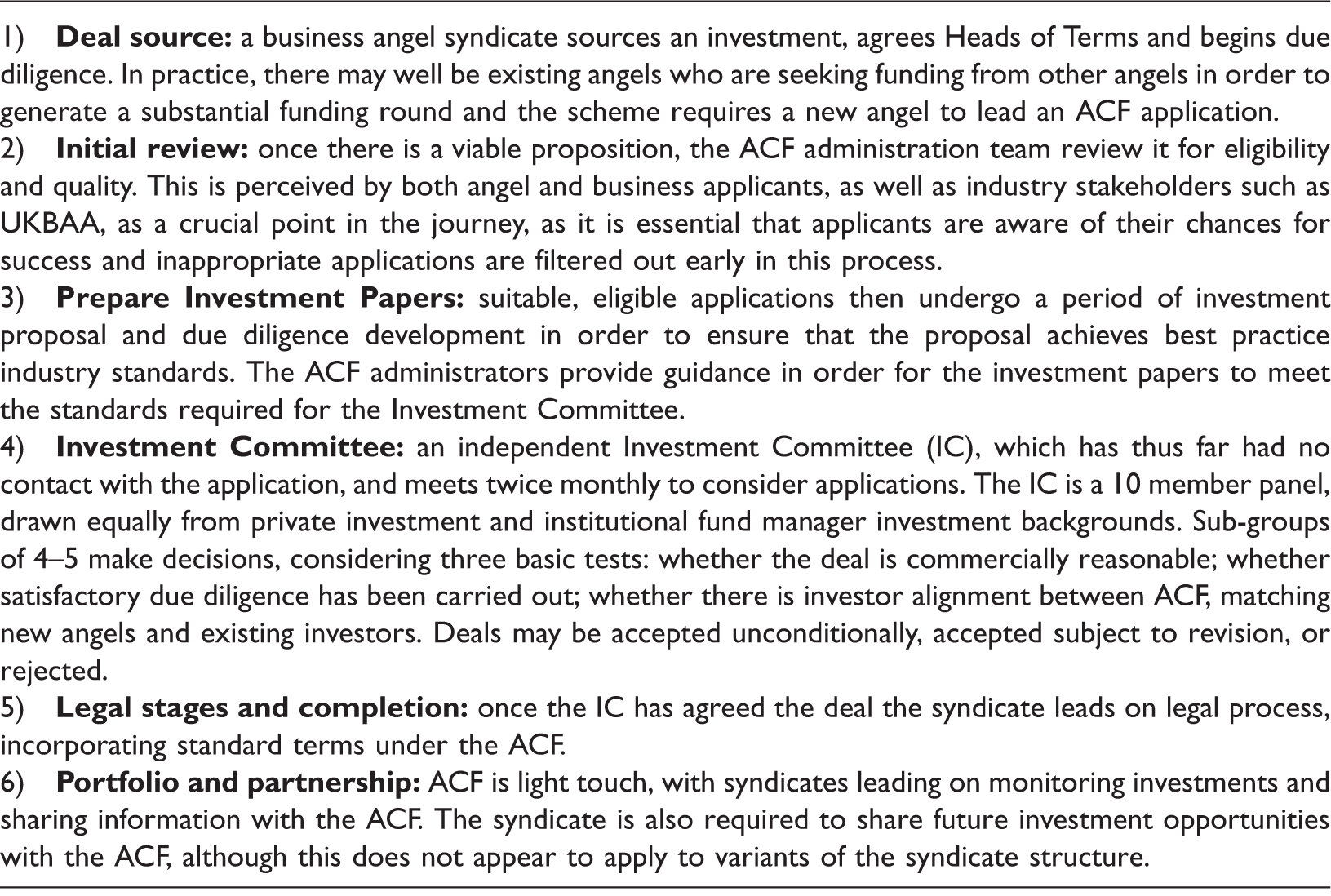

The ACF has two aims: (i) to address the current potential high growth SME finance gap; and (ii) to increase the number of UK business angels and raise their investing competence through disseminating best practice. A distinction from other UK Scottish and RDA CIFs is that it undertakes individual deal-based assessment. Investment opportunities must come through syndicates of at least three private angel investors who are independent of the business and investing in it for the first time, although other investors in the round, outside the syndicate, can form a mix of new and existing investors. Syndicates need not be formally constituted, but require a Lead Angel to ‘lead’ the investment process as principal contact with the ACF.

Summary of the investment process of the ACF.

ACF: Angel Co-investment Fund; UKBAA: UK Business Angel Association.

Interest in the ACF has been high, with circa 250 enquiries in its first 26 months. However, attrition at the initial review stage has been about 80%, with some rejections, but mainly due to syndicates withdrawing or not following through on their initial contact. After passing initial screening review syndicates are requested to submit a business overview Investment Paper (14–16 pages

18

). IC assessment is based on this paper and a 45 min telephone interview session with the Lead Angel, focusing on three main issues:

Does the investment offer the prospect of a commercial return, relative to the risk? Does the Lead Angel have a detailed understanding of the business, based on sufficient due diligence, enabling them to convincingly explain why the proposal represents a good investment? Are the terms and conditions appropriate?

As such, the IC is judging the Lead Angel as much as the business.

The IC approves over 80% (39 of 47 applications) of the investments it considers. Rejected applications are not allowed to revise and resubmit. If the ACF decides to invest then the syndicate must lead on the legal process and produce an investment agreement incorporating standard terms. Where possible, the ACF follows the investment terms of the syndicate, 19 although the IC occasionally requires investment agreement revision. This is one aspect of the investment process in which the ACF seeks to spread best practice.

Where the ACF invests, a one-off fee of 2.5% of the amount that it invests is payable to the syndicate to cover the costs of providing on-going information to the IC. The ACF expects to make follow-on investments in many cases, with the same or different angel syndicates, subject to further IC approval. Accordingly, for every £1 it invests it holds a further £1 back for potential follow-on rounds. The ACF aims to be a passive investor, without an appointed director or Board Meeting observer, but retains these rights.

Methodology

Survey respondents.

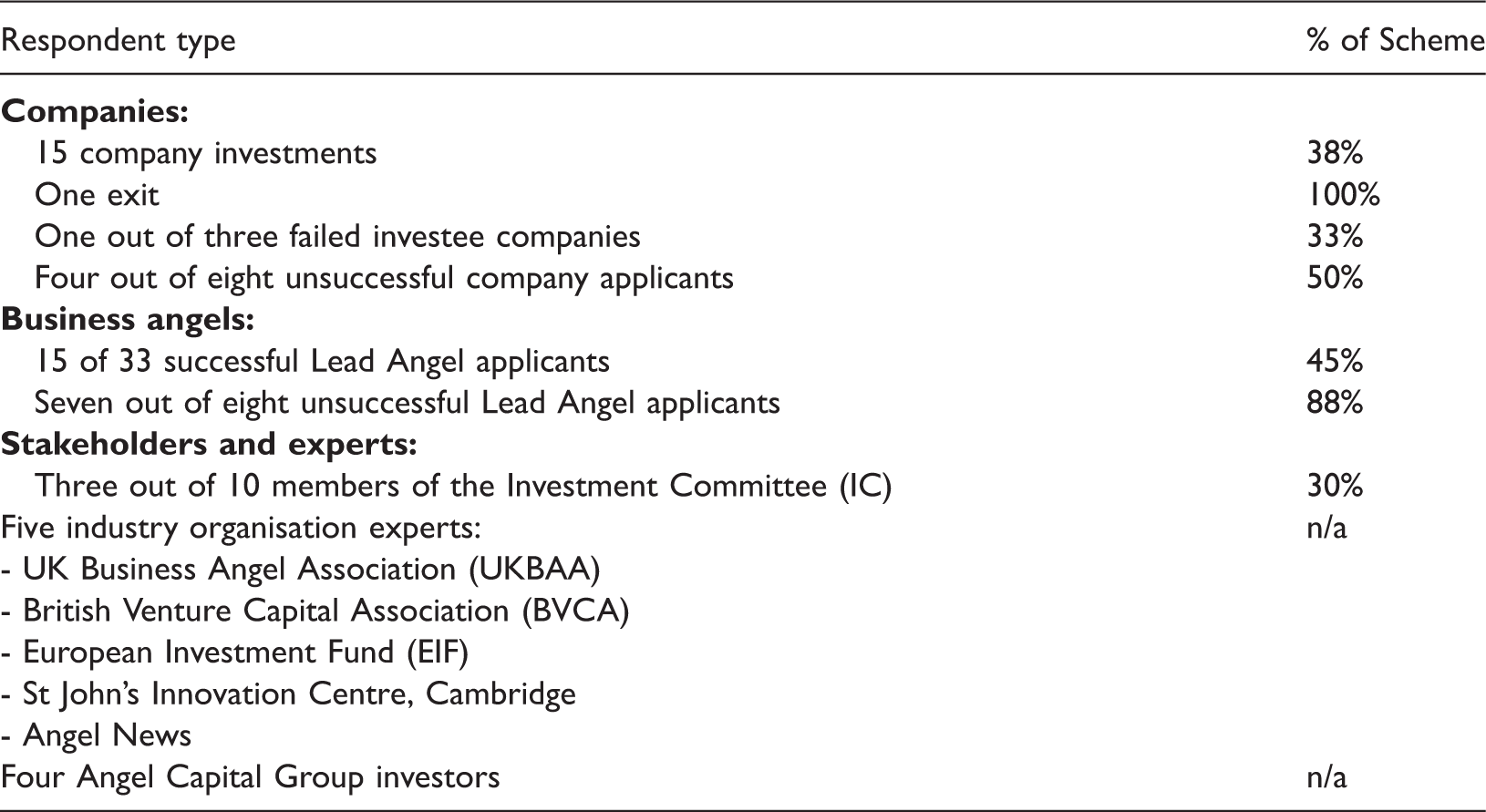

The unsuccessful businesses and angels interviewed are drawn from the eight unsuccessful applications to the IC. The successful and unsuccessful business case interviews were matched to interviews with their Lead Angel investor applicants. Semi-structured survey instruments profiled the respondent investor, business or key informant and specifically examined the role and operation of the ACF, the process of finding and applying for the ACF, the outcomes from successful or unsuccessful applications and the scheme’s impact on the UK early stage equity market. Interviews typically took one hour and were cross-checked with respondents for accuracy. The business data analyses used a mixture of quantitative (e.g. financial) and pre-coded categorical (e.g. broad sector, satisfaction scales) data and qualitative responses which were input into Excel to provide linear business case (all or subset business group) and variable content analyses, using key word and phrase searches to form inductive group clusters and trend findings (Eisenhardt, 1989; Yin, 2003). Both the qualitative business and investor data underwent double-blind post coding checks with senior research colleagues in order avoid interpretive bias. Additionally, in order to fully apply a robustly triangulated mixed methods approach (Creswell, 2003) 12 key stakeholder and expert informant interviews were undertaken, either face-to-face or by telephone, to gain greater understanding of the ACF in terms of its internal operations and external role and impacts (Table 3).

Results

The findings presented examine three propositions exploring the aims of the ACF and drawing on the finance gap and VC design theories presented: P1: To what extent are ACF investments determined by the location of organised BANs, angel investment sector preferences and demand from young early stage businesses? There is an expectation that investments will be clustered into two types of regions: (i) those with organised BANs (Mason and Harrison, 2015; Mason et al., 2013) and vibrant entrepreneurial ecosystems with plentiful sources of seed capital that will have generated highly innovative businesses positioned towards the end of early stage funding where angel group follow-on funding would appear to require ACF stretch funding and (ii) those with large numbers of short digitech businesses which offer a investment horizon (Baldock, 2016; Baldock and Mason, 2015). In reality there is a high level of overlap between these two geographies. P2: To what extent is the ACF meeting the needs of the current UK finance escalator and positively impacting on the funded businesses (Baldock and Mason, 2015; North et al., 2013)? There is an expectation that the ACF will help to generate larger deal sizes than occurred previously, while achieving considerable additionality, little displacement (Leleux and Surlemont, 2003), effective follow-on funding and providing timely, optimal exits (Baldock, 2016). Entrepreneur pecking order preferences for angels over VC might also be better served (Baldock and Mason, 2015). P3: To what extent is the ACF’s focus on syndication, individual deal quality selection and dissemination of best practice encouraging and improving angel investing? The expectation is that the scheme will lead to more organised angel group/network activity, with successful Lead investor skills being passed on to both other investors in the group and also the wider angel community through communities of practice (Mason and Harrison, 2015; Mason et al., 2013; Mason et al., 2016), ultimately creating a sustainable evergreen CIF model that reduces transaction costs (Hayton et al., 2008) and agency failures (Akerlof, 1976).

(P1) ACF supply orientation: location, sector, innovation and stage

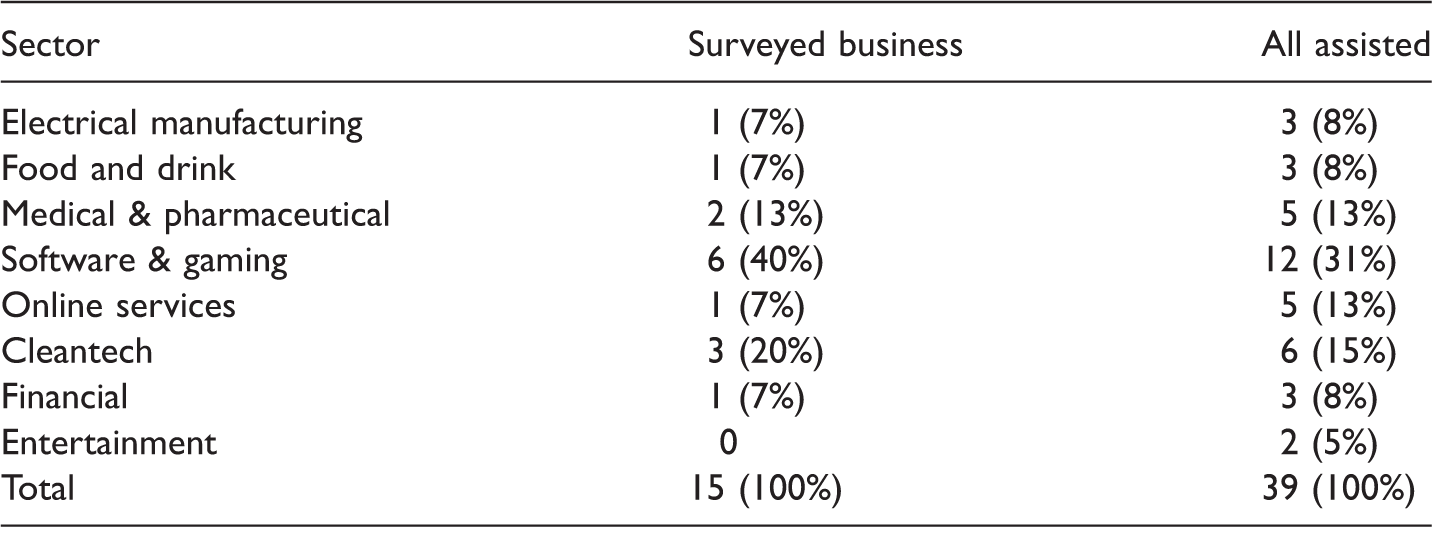

Sectoral distribution of all ACF assisted and surveyed businesses.

Source: British Business Bank, December 2013, and Recipient Business Survey.

ACF: Angel Co-investment Fund.

Note: Mann–Whitney U test at .05 level revealed significant difference in Z-score (−2.305, p = 0.02088) and U-value of 9.5 where critical value is 13. This is explained by under representation of online services, including retail, lettings and fashion activities. Exclusion of this sector leads to U-value of 8.5, at above the critical value of 8.

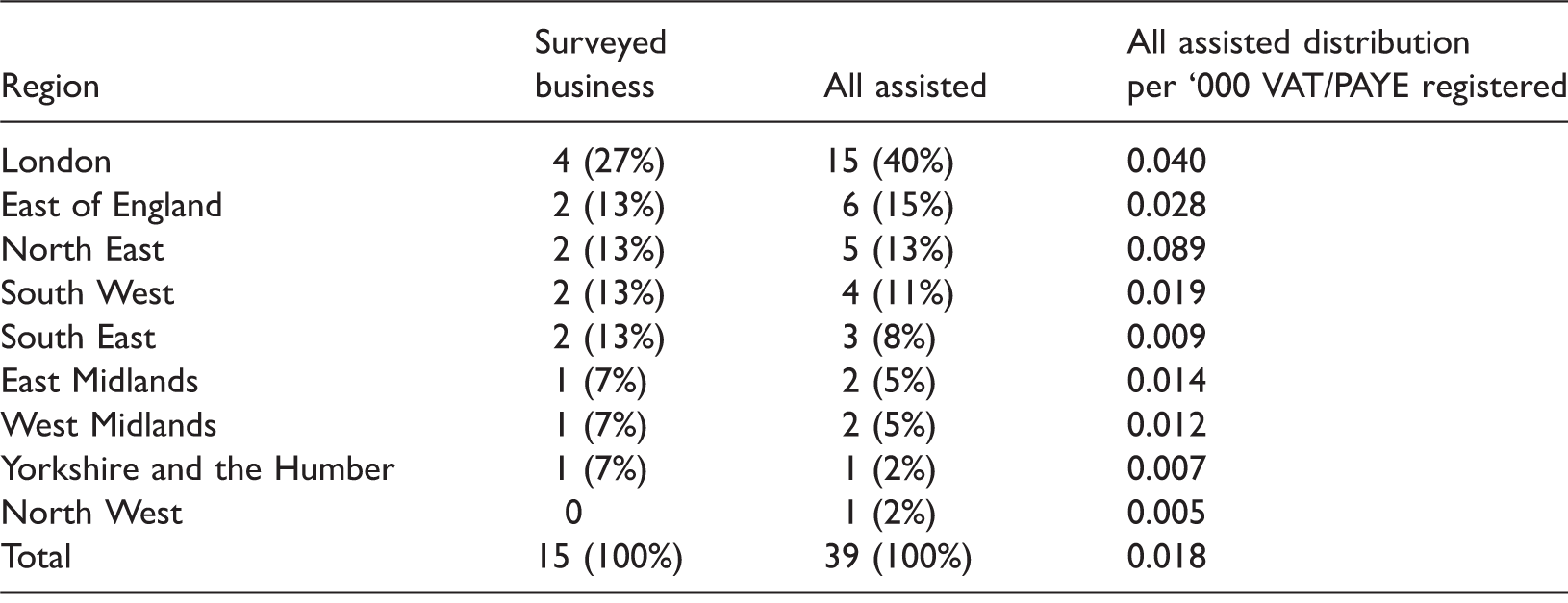

Regional distribution of all ACF assisted and surveyed businesses.

Source: British Business Bank, December 2013, and Recipient Business Survey.

ACF: Angel Co-investment Fund.

Note: VAT/PAYE enterprise data from UK IDBR 2013 (n = 2,167,580). Mann–Whitney U tests at .05 level indicate no significant difference between samples: Z-score −1.7219, p = 0.08544; U-value 20.5 where critical value is 17.

Characteristics of the surveyed successful applicant businesses (n = 15). The 15 surveyed businesses are highly innovative, often global market leading (12 hold patents or trademarks) at the time of ACF funding. They are young and small businesses (median establishment age three years, median six staff), either approaching or in their early trading stages. They are beyond proof-of-concept and early R&D prototyping and are reaching later R&D product and service refinement or technical market regulatory testing stages (in the life science and electronics sectors). At the time of approaching the ACF they had already received ‘3F’ (founders, family, friends) funding and in several cases already had angel investment. They required considerable step-change external finance (e.g. from under £100,000 for early R&D, to considerably more than £200,000 for later R&D and commercialisation), representing levels of funding beyond the capacity of the existing investors. These businesses conform to the classic market gap scenario (Baldock and Mason, 2015), describing themselves as ‘requiring too much funding for angel investment, but too early stage for either bank or private VC investment’.

(P2) The ACF’s role and impact on the current UK Finance Escalator

Further examination of the surveyed 15 successful ACF business applicants demonstrates that the ACF is providing considerable step-change ‘stretch’ funding, with average round sizes more than double those for overall UK angel investment (UKBAA, 2013). These businesses received an average of £379,000 in ACF funding (range £120,000 to £1.07 m, including four follow-on rounds), with average funding of £1.43 m (range £260,000 to £5.9 m) for an average overall shareholding of 12.3% (range 7.9–22.6%), suggesting for later R&D stage funding the scheme’s 30% share cap is appropriate (Baldock, 2016).

Typically for later R&D, early market entry businesses, funds were sought to commercialise, recruit and develop sales teams, promote products/services and undertake later stage R&D refinement. Key staff recruitment and increased capacity (two businesses), alongside plant and machinery investment in recycling and manufacturing (two) were also mentioned. Notably, few were undertaking manufacturing, which was typically subcontracted, mainly within the UK.

The businesses were seeking funding upwards of £200,000 to beyond £2 m. Since they did not have sufficient trading track records of more than two years they recognised that they were ‘unsuited to banks’ and that ‘equity was the only viable type of funding’. The most common sources of alternative funding considered were private VC (nine businesses), followed by public and corporate VCs, these cases all contacting at least five different VCs. A common observation from the feedback they had received from VCs was that ‘… we are too small for VCs and they ask us to come back to them when we have a trading record and profitability’. Only one-quarter had received offers from VCs: these were more likely to be corporate/trade related with detailed knowledge of their sector. However, these investments offered unacceptably low valuations and restrictive terms. Overall, in line with pecking order theory there was a preference for ‘smart hands-on angel investors’ and to ‘avoid VC controlling influences’. For these businesses, the approach to the ACF was via business angels and ‘the ACF came in at the end of the funding search and followed-on from angel funding’.

Additionality. Additionality is measured from the CEOs’ judgment of the counterfactual policy-off scenario 22 and triangulated with assessments from the Lead Angels and the performance of the unsuccessful businesses. Primarily, the 15 ACF assisted businesses present a stronger case for project additionality (relating to perceived improved timing and scale) rather than finance additionality (relating to perceived lack of availability of alternative funding), confirming longitudinal findings for other BIS VC schemes where lead investors observed that portfolio business CEOs are typically overly optimistic about fundraising (Baldock and North, 2015). In this study, more than three-quarters of Lead Angels felt that the investment would not have gone ahead without the ACF.

Only one-fifth of CEOs indicated that they would probably or definitely not have raised the finance required in the ACF round, whereas almost four-fifths indicated that the project would have been restricted without ACF finance, with one-fifth likely to have closed and the remainder evenly split between the project proceeding at reduced scale, or taking longer to commence. One typical comment was that ‘without the ACF we would have been set back by as much as a year’. This is a vital consideration for fast moving digitech sectors where ‘being first to the market is everything’. There were four businesses that would have progressed at the planned project scale and timetable without the ACF, due either to alternative funding offers or a view that the 3–4 months application process would have yielded sufficient alternative investors. However, all of these CEOs recognised that the ACF represented a better deal than more restricted deals offered by corporate VCs or more complex alternative angel syndicate arrangements. The overriding pecking preference for angel investments over VCs was widely evidenced: The VC was only concerned with forcing a quick exit, which was not in the best interest of the business; Going with a single corporate VC would have restricted our market potential; We did not want a large single investor or VC controlling us.

Impacts on recipient businesses. Assessing the impact of the scheme at such an early stage is difficult to calculate, particularly with five businesses assisted within the last year and four in pre-trading at the time of receiving ACF funding. However, it is possible to triangulate qualitative assessment from CEO and Lead Angel interviews with some quantitative assessment, including benchmarking with a parallel study of the Enterprise Capital Funds (Baldock and Mason, 2015).

All of the assisted businesses mentioned positive factors, including progressing R&D (seven businesses improved or licensed new patents and trademarks), testing and sales and marketing, in one case leading to a £2 m licensing contract. Overall, the ACF was judged attributable for at least one-third (median 33%, mean 37%) of subsequent business development (ranging from the 9% ACF share of the business up to 100% where without ACF closure would have occurred). In the vast majority of cases CEOs considered that the ACF contribution was making a substantive contribution, over and above its proportional share of investment; ‘the extra funding received from ACF allowed us to pass a tipping point to generate sales and marketing momentum’. In net terms, this catalytic effect can be expressed as + 10.4% on average (37% average impact, less 26.6% average ACF investment contribution) and is similar to that recorded for the ECF (Baldock and Mason, 2015).

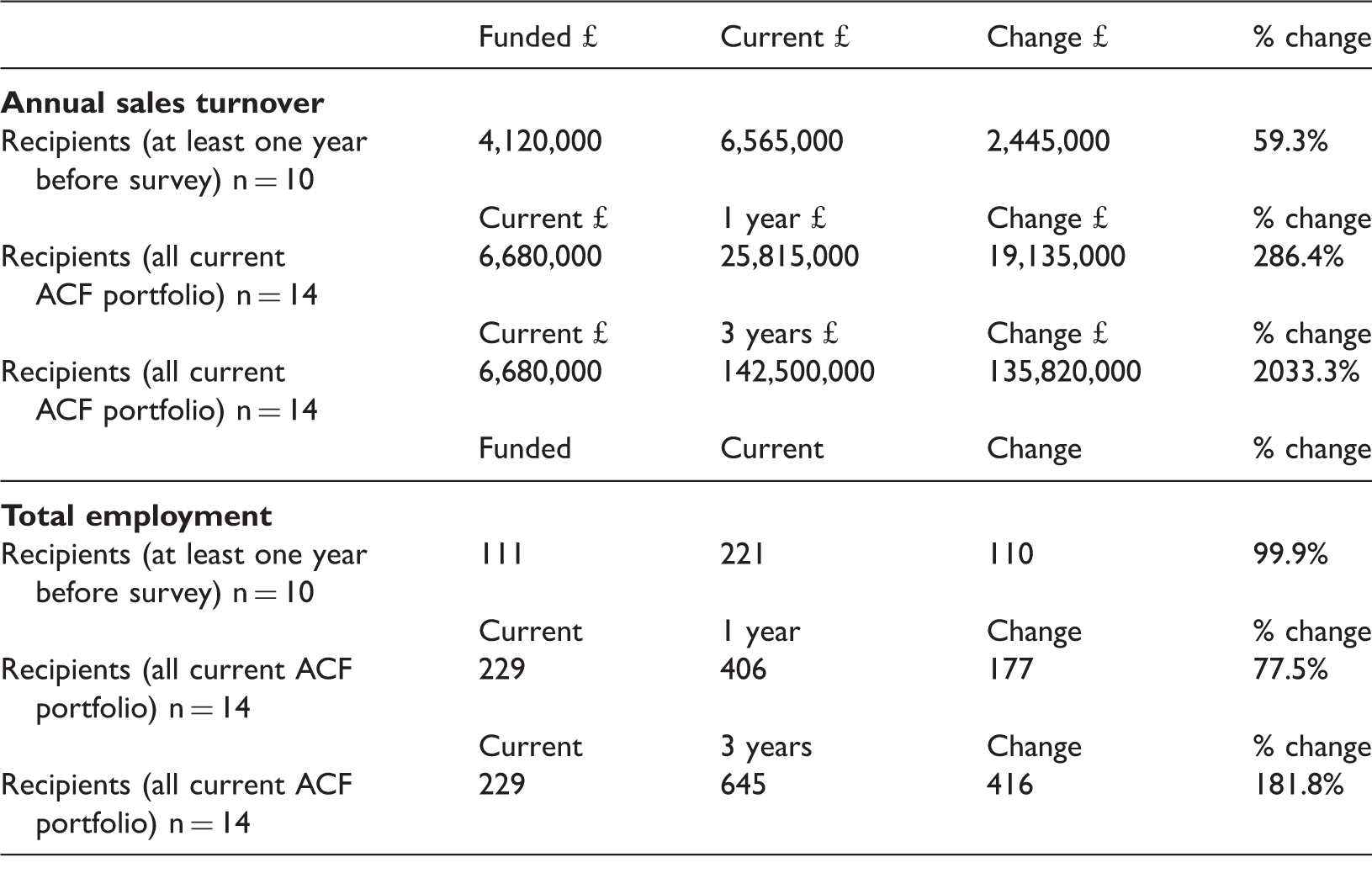

Aggregate actual (when funded and current) and forecast (for one and three years) for annual sales turnover performance and employment.

ACF: Angel Co-investment Fund.

Note: Only 10 cases have received ACF at least one year prior to the time of the survey and only 14 cases provided current and future projections as one case had been sold.

These projected figures are in-line with those found in the early assessment of the ECF and UKIIF, 23 as the businesses project their rise out of the base of the ‘J’ curve, from only one currently in profit to all being profitable within three years, as they approach investment exit, typically estimated at between two to at least five years (median four years). However, as noted by the surveyed Lead Angels and by VC managers in other recent UK studies (Baldock and Mason, 2015; Baldock and North, 2015), CEOs are typically over-optimistic in respect of growth and exit timetables and these figures should be treated with caution. It is notable that one-third of the surveyed ACF businesses had already slipped back by up to six months in their exit timetables, reflecting the increasing length of time required to achieve an exit in the post-GFC period (Axelson and Martinovic, 2012; CfEL, 2013; EVCA, 2013; Mason and Botelho, 2016). This is an area of concern for angels but they, like their portfolio businesses, are buoyed by the capacity for the ACF to provide substantial follow-on funding. Three-quarters (11) of the businesses envisage requiring further follow-on funding (ranging from £100,000 for working capital up to £20 m to fund international business growth) and one-third (5) believe that this will include further investment from the ACF, whilst four have already received further ACF finance. It remains too early to predict the likely success of the future ACF exits.

(P3) The ACF’s impact on UK business angel investing

These findings draw upon the interviews with 19 Lead Angels. All exhibited considerable business management experience. Two-thirds (12) had made at least five previous investments, whilst just one had only made one previous investment. Eight had managed their own business, eight had financial management experience (including buying and selling businesses and raising external finance) and nine had consulted for businesses. There was no obvious difference between the successful and unsuccessful angels. Indeed, three of the unsuccessful investors had previously made successful applications to the ACF. They admitted that, if anything, they had been ‘guilty of expecting the second application to be easier than the first’. It is therefore clear that the ACF, in its early stages, has attracted experienced, sophisticated Lead investors, whether successful or not.

The syndication process was dominated by loose and ad hoc angel groupings, with little involvement by professionally-managed angel capital groups, as found in Scotland (Mason et al., 2016). Just three Lead Angels managed their own syndicates and one other was a member of a formal syndicate. A further six were members of loose, fluid groups where the Lead Angel role rotated, including membership of BANs where the actual investors and Lead Angel varied with each investment. The remaining Lead Angels had been attracted to the business or were recruited through an intermediary. The concept of Lead Angel therefore appears quite flexible with some of these already experienced angels appearing in other ACF cases as syndicate members. Leadership was determined by a variety of factors, including experience, strong desire to invest in the business including sector knowledge and invitations from existing business investors who could not lead under ACF rules.

In summary, the evidence points to the ACF collaborating (although not working directly) with experienced angel investors and members of established angel groups and networks, notably in London, Thames Valley and Cambridge, enhancing their effectiveness in making investments. The London Business Angels have been particularly active in promoting the scheme, resulting in members engaging with the ACF and providing a high proportion of Lead Angels (almost one third), although some investee companies were outside London. However, the overall feature of investment syndicates is of ad hoc, constantly changing groupings. The scheme has not impacted on the formation of new managed groups, or networks. Indeed, for the vast majority there was no indication that the ACF syndicate would invest again together in another business. Nor has ACF encouraged involvement of new angels. 24 It also appears that the ACF regional roadshows have made a limited impact on raising awareness of the scheme amongst organised network groups.

Process issues. A key ACF aim is to improve the quality of angel investment by operating a rigorous application process. This involves producing a business investment proposition paper and a telephone presentation to the IC. This was not a concern for the vast majority of the interviewed angels who were experienced and successful investors and business people. One even praised the ACF as ‘easily the best public VC’ that they had dealt with. Crucially, the ACF administration team at the British Business Bank provide clear guidance from the start of the process, ensuring that only strong cases are developed iteratively with them and reach the IC with a high expectation of success. Those with the best experiences had engaged fully with the ACF throughout the process, receiving helpful high level feedback. Three angels (including two unsuccessful applicants) complained about lack of clarity (website and written documentation) and delays in receiving information.

From a business perspective the ACF was widely welcomed. From the Lead Angels’ perspective the IC’s available time is quite limited and it was understood that they were assessing the angel’s competence, as one put it ‘to push back the concerns and risks raised in the investment paper’. However, for a minority of investors its process seemed incongruous, as it lengthened the application period, led to uncertainty of outcomes and did not directly involve the entrepreneurs. Indeed, they had no contact with the IC. The entrepreneurs therefore treated the IC with suspicion and several mentioned that it was an unreasonable burden to expect the Lead Angel to have the technical knowledge to present their case. These interviewees mostly failed to comprehend that the IC was testing the angel, rather than their business.

Only a small minority of businesses and Lead Angels criticised the application process. These were mainly unsuccessful applicants. They revealed agency and transactional cost factors (Akerlof, 1976). First, whilst the scheme saved search time for more investors, some business CEOs mentioned this was off-set by the several months required to prepare an investment paper (the median application to funding receipt time was four months). As one Lead investor commented, ‘we had put all our eggs in one basket’. Indeed, rejected ACF applicant businesses faced the risk that investor pledges would not be honoured because of the time delay and one business failure occurred for this reason. Second, application process delays occurred where administration staff were under pressure from the volume of enquiries and applications. A third criticism is that the scheme is overly rigid, notably in defining new money, the effect of which is to exclude knowledgeable existing investors from being ACF Lead investors. Fourth, there were concerns that ACF behaves as a ‘lead investor’, rather than following investors (like the Scottish CIF and recent EAF pilots). However, this can be seen as a consequence of the scheme’s objective of raising the standard of investments. Fifth, investors wanted the IC to provide clear, detailed feedback for rejections, offering opportunity to reassess and re-apply. Finally, although the experienced angels are mostly successful and understand the process, particularly those with institutional 25 investment experience, it was widely viewed by the angels and business CEOs that the application process could be ‘daunting and off-putting to less experienced angels’.

Conclusions and policy implications

This early assessment of the ACF is limited by the scheme’s initial scale and data restrictions, not least their cross-sectional nature. Nonetheless, it reveals clear, important messages with resonance for CIF theory, policy development and Lerner’s (2010) call for further public VC scheme evaluations.

Proposition one revealed the ACF’s initial business funding distribution as heavily biased towards the London, East of England and North East regions where existing formal BANs are strongly present, supporting previous findings of A-OCIF linking to thriving entrepreneurial ecosystems, BAN clusters (Mason and Harrison, 2015; Mason et al., 2013). ACF investment was also skewed towards shorter horizon digitechs (underscored by the low median prediction of four years to exit) favoured by UK investor tax incentives (Baldock and Mason, 2015). The ACF assisted highly innovative, early stage businesses, typically at the second angel round where substantial funding is required to scale-up (Baldock and Mason, 2015). From a policy perspective, anecdotal UKBAA 26 evidence demonstrated limited ACF knowledge amongst angels, supporting the suggestion of key informants to increase scheme promotion regionally, through UKBAA roadshows. This would be feasible where there are existing angel networks, but might be ineffective in reaching angels in regions that lack networks and where more infrastructural linking and support for angel collaborations may be required.

Proposition two clearly demonstrated that the ACF is meeting its aim of addressing the funding gap for early stage potential high growth businesses, particularly those seeking second round step-change ‘stretch’ funding in the £500,000 to £2 m range, beyond the normal scope of angel syndicates (Mason et al., 2016). It is therefore helping the new post-GFC UK funding escalator gain traction (Baldock and Mason, 2015; North et al., 2013). The scheme exhibited high levels of attributed additionality (Baldock and North, 2015), very low levels of potential crowding out (Leleux and Surlemont, 2003) – none with other public sector schemes including the ECFs (Baldock and Mason, 2015), and with business managers demonstrating a preference, consistent with pecking order theory, for ‘smart angel money’ over ‘controlling VCs’ (Baldock and Mason, 2015; Wiltbank, 2009).

From an economic development policy perspective, the initial ACF impacts on funded businesses were considerable, driving forward R&D, creating jobs (including spillovers to UK manufacturers) and increasing business revenue. The scheme’s evergreen flexibility to accommodate substantial follow-on funding rounds, either to reach exit or bridge the gap to further finance (e.g. BGF), will help meet growing ‘series A-B’ demands (Baldock, 2016; Baldock and Mason, 2015), and has already demonstrated ability to deliver growth momentum in assisted businesses, maintaining their market primacy.

Proposition three, relating to the ACF’s individual investor case assessment approach, as opposed to the Scottish CIF and EAF preferred partner, passive investment model, proved most problematic. Whilst the ACF undoubtedly attracted successful experienced investors who could provide good hands on investment management skills (Mason and Harrison, 2015), provided credibility and facilitated ad hoc syndication, there was no evidence that the good practice that was being espoused by ACF was being diffused to other group members or the wider angel community. From an agency (Akerlof, 1976) and transaction cost (Hayton et al., 2008) perspective, there were concerns that the application process took too long (median of four months), creating investor uncertainty and undermining investment time advantages offered by CIFs. Furthermore, although the ACF is a light touch investor, only intervening post-investment if angels require assistance, it does require quite intensive initial application support from the administration team to quickly filter out poor applications and nurture stronger ones. Early assessment suggests the ACF’s complex application process and demanding due diligence suit experienced institutional investors, and are off-putting for less experienced investors, with high initial application attrition rates seemingly influenced at least as much by discouragement as unsuitability. Future policy research should therefore focus on better assisting formal angel group and network development across the regions and more directly raising the standard of angel investing (Mason et al., 2013; Wilson and Silva, 2013) to enable more effective take-up of the scheme.

In the final analysis, a decision is required regarding whether ACF is to be niche or volume intervention. Currently it is too small to ‘shift the needle’ sufficiently to make a substantial difference to the early stage entrepreneurial finance market. It therefore requires to scale-up to make an impact. However, we have noted that even in its pilot phase administrative capacity points have been reached on certain occasions. If the scheme does significantly expand in scale it will require to substantially increase its administrative and IC staffing capacity to effectively meet the demand that will be stimulated by its greater visibility.

Footnotes

Acknowledgements

This paper is based on research undertaken on behalf of the UK Department for Business, Innovation and Skills (subsequently renamed Department for Business Energy and Industrial Strategy) and the British Business Bank. All views expressed are those of the authors only.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.