Abstract

Over the last decade, private rental sectors have been in rapid ascendance across developed societies, especially in economically liberal, English-speaking contexts. The Netherlands, and Amsterdam in particular, has also more recently experienced the reversal of a century-long decline in private renting. More unusually, the expansion of private renting in Amsterdam has been explicitly promoted by the municipal and national government, and in cooperation with social housing providers, in response to decreasing accessibility to, and affordability of, social rental and owner-occupied housing. This paper explores how and why this state-initiated revival has come about, highlighting how new growth in rent-liberalized private renting is a partial outcome of the restructuring of the urban housing market around owner occupation since the 1990s. More critically, our analysis asserts that restructuring of Amsterdam’s housing stock can be conceptualized as regulated marketization. Market forces are not being simply unleashed, but given more leeway in some regards and matched by new regulations. We also demonstrate various tensions present in this process of regulated marketization; between national and local politics, between existing housing and new construction, and between policies implemented in different time periods.

Introduction

Despite the prolonged, cross-national decline in private renting over the course of the 20th century, this trend was reversed in the lead up to and, more substantially, since, the Global Financial Crisis (GFC). Indeed, the revival of the private rental sector, it is argued, has been ‘an important sub-plot to the GFC story’, although it has only recently begun to attract attention (Kemp, 2015: 601). Liberal economies such as the UK and USA have demonstrated the most intensive growth in private renting and have consequently been the centre of analyses. Initial studies have largely focused on flows of international capital (Beswick et al., 2016; Fernandez et al., 2016), high-end investors such as private equity firms, hedge funds, real estate investment trusts (REITs), and so on (Fields, 2019; Rodgers and Koh, 2017; Waldron, 2018), or increases in small-scale local investors seeking better yields in the face of low interest rates and poor returns elsewhere (Aalbers et al., 2018; Kemp, 2015; Ronald and Kadi, 2018; Soaita et al., 2017; Wind et al., 2020). More regulated contexts such as the Netherlands, where private renting has been historically displaced by the state coordination of social housing, have also more recently seen a palpable revival in the rental market. More specifically, in Amsterdam, where the regulation of housing has been particularly strong, a longstanding decline in private renting was reversed in 2008 and followed by remarkably intense sector investment since 2011 (Bosma et al., 2018), transforming the sector more profoundly. Indeed, while the share of private rental housing has grown from around 22% to over 28% of housing, the rent-liberalized tranche has more than tripled from just 4.8% to 15.4% of the total housing stock between 2007 and 2019 (Gemeente Amsterdam, 2020).

This paper sets out to understand how and why the largely decommodified and deeply regulated Amsterdam housing sector has undergone such a sharp and unexpected shift towards private rental housing. At a broader level, the analysis seeks to elucidate the relationship between contemporary economic restructuring, national and urban politics and housing in three distinct ways. First, we show how the recent upsurge in private renting is intertwined with a more fundamental restructuring of this tenure into a more expensive one. This step aligns with a growing post-crisis, state concern with providing more middle-income housing by increasing private capital flows into rental housing. It should be understood as a direct response to previous rounds of policy reform that have effectively excluded middle-income groups from social rent, while steep price increases have rendered owner occupation unaffordable to many. We thus argue that current private rental policies both build on and amend pre-existing institutional arrangements (see also Brenner et al., 2010; Streeck and Thelen, 2005).

Second, our analysis highlights distinct and pro-active state involvement in bringing about private rental sector growth. While various other countries have also seen the introduction of policies supporting growth private rental housing, such efforts typically follow market forces and demand, resulting in a patchwork of individual policy measures. In contrast, Amsterdam represents a particularly extreme case in which the local and national state have significant capacity in shaping the local housing market, with the municipality owning some 80% of the city’s land, allowing the state to take the lead in pursuing private rental growth through a distinct form of housing liberalization. We explicitly address how such policies have taken shape in Amsterdam, what goals and rationales they reflect, and how they fit within broader urban, social and economic logics.

Third, and relatedly, we argue how policies promoting private rental growth in Amsterdam can be conceptualized as a form of regulated marketization. We understand marketization here as the process by which market mechanisms are increasingly central in supplying and allocating housing, such as by reducing rent regulation or privatizing social rental housing. Market forces are not being simply unleashed though, but are given more leeway when and where they are in line with state ambitions regarding housing, and are also matched by new regulations. At the same time, while we focus of state coordination, we also show regulated marketization is not a coherent effort, and point to the various tensions present in the process – between national and local politics, between regulating existing housing and new construction, and between the objectives and outcomes of different time periods. Regulated marketization is the fuzzy and partial outcome of different forces at work. In recognizing that marketization does not necessarily equate with deregulation, we specifically build on literatures on variegated neoliberalization (Brenner et al., 2010) and regulated deregulation (Aalbers, 2016).

In the following section we establish how housing conditions have shifted in the lead up to and since the crisis, as well as the socio-economic factors that facilitated the revival of private renting in various contexts. We ultimately focus on the role of the state and in particular its part in the recent advance of private renting in the Netherlands’ biggest city. We then address the Amsterdam context in more detail, before moving on to an empirical investigation of the recent restructuring of the city’s private rental stock. We draw on secondary quantitative housing data, and on analyses of recent policies and formal political discussions related to private rental housing. In the final section we situate our analysis of regulated marketization processes in Amsterdam in a broader framework of housing marketization and the neoliberalization of urban and housing policies.

Private renting and the shifting housing context

Systemic housing transformations

The recent revival of private rental housing in various contexts did not emerge out of thin air, but builds on previous rounds of housing sector transformation. Across many countries, the marketization of housing has been at the forefront of urban, social and economic transformations for a number of decades. It has been part and parcel of contemporary financialized capitalism (Aalbers, 2016; Christophers, 2013; Langley, 2008; Schwartz and Seabrooke, 2008). For a long time this process centred on the advance of homeownership, enabled and sustained through pro-active state promotion of the tenure (Ronald, 2008). Fiscal stimulation, mortgage credit expansion and ‘right-to-buy’ schemes, for example, enabled many households to buy. Private rental housing, however, continued to decline throughout the second half of the twentieth century in most countries (Harloe, 1985).

The commodification and financialization of housing not only led to rapidly increasing homeownerships rates, but also to long-term house price increases that far outpaced income growth. In many cases, households were only able to keep up with price escalation by taking on ever-larger mortgage debts (Fernandez and Aalbers, 2016; Crouch, 2009). Conditions have, however, changed in the post-GFC milieu, with individual access to mortgage credit curtailed and income conditions becoming less stable, restricting access to homeownership (Forrest and Hirayama, 2015). Growing numbers of people, including stable middle- and dual-income households with secure employment, have consequently found themselves excluded from homeownership and forced into other tenures. In many countries, the greatest decreases in homeownership have been among younger adults (Lennartz et al., 2016; McKee et al., 2017). In countries like the UK and USA, this has led to a marked decline in homeownership. In the Netherlands, meanwhile, homeownership rates have not fallen, but have stabilized at around 56% of the housing stock after decades of expansion (Statistics Netherlands, 2019a), signalling, perhaps, the formation of a ‘late’ or ‘post-homeownership’ society (Forrest and Hirayama, 2018; Ronald, 2008; Ronald and Kadi, 2018).

Alongside expanding and, subsequently, contracting access to homeownership, has been a more continuous decline in social rental housing. In the post-war decades, social housing provision was embraced by governments as a means to house large sections of society (Priemus and MacLennan, 1998). In the 1980s, nonetheless, most social housing sectors have undergone sustained residualization and stigmatization, effectively downgrading social renting in many contexts to a tenure of last resort (Fitzpatrick and Pawson, 2014; Malpass, 2004). The material and symbolic degradation of the tenure meant that the latest ‘housing crisis’, associated with the GFC, resulted in very few social housing initiatives, with public resources typically propping up lenders and borrowers in the home-buying sector. In the Netherlands, residualization of the social rental sector may not immediately appear obvious, as the tenure remains relatively large. Here too though, the size of the social rental stock has declined, especially in cities. The tenure increasingly houses the poorest echelons in Dutch society, while rent burdens among tenants have increased (Van Gent and Hochstenbach, 2020).

Why private renting?

In addition to the combined effects of restricted homeownership access and reduced social rental supply pushing more households towards other housing arrangements, several key demographic and economic trends also seem to be shaping the emerging demand for private renting. These include a notable increase in younger adults living alone and partnering later, the expansion of higher education and increases in migrants and international knowledge workers. These trends are related to an increase in more flexible, transitory and urban living arrangements, spurring private rental demand (Buzar et al., 2005; Kemp, 2015).

From a political economy perspective, the pre-crisis focus on homeownership has also been critical to the revival of renting as a driver of capital accumulation practices. The expansion of homeownership in the late 20th century and the associated augmentation of house prices established ‘homes’ as a special class of commodity. Housing became an asset par excellence in terms of its function as both a store of wealth and a vehicle for further wealth accumulation (Ronald, 2008; Ronald et al., 2017; Schwartz and Seabrooke, 2008; Smith, 2008). Since the crisis, however, the role of housing – along with very low interest rates and fading returns on other investment classes – has become ever more central in wealth accumulation dynamics and a revival in ‘rent-seeking practices’. Indeed, as access to, and thus demand for, owner occupation has faded, various new actors have rushed in to buy up property to let.

The new actors involved in, and driving forwards, the re-galvanization of renting include both individual and institutional agents. In terms of the former, the commodification of home and housing that advanced towards the end of the last century have deeply normalized housing investments among private individuals (Langley, 2008; Smith, 2008). While the function of home buying has been traditionally combined with occupancy, housing conditions in the 1980s and 1990s created a particular cohort of households rich in housing equity, well positioned to acquire extra property, especially when prices dipped after the GFC (Arundel, 2017). This facilitated a notable expansion in individual multiple-property ownership (Kadi et al., 2020). These include transnational elites speculatively channelling their wealth into prime real estate (Fernandez et al., 2016), but also, more fundamentally, regular households buying extra property to rent as a steady income stream (Soaita et al., 2017). Such investments often take the form of buy-to-let activities where dwellings are transferred from owner occupancy into rental tenancies (Leyshon and French, 2009).

Apart from such forms of private landlordism, fund managers and major investment companies have also played a central role in increasing private rental supply, with rental markets increasingly integrated in global capital flows (Beswick et al., 2016). Financial corporations have, especially since the GFC, targeted new asset classes featuring real estate (Fields, 2018). Such corporations invest in both existing stock and new construction. Large swathes of housing have thus been transformed into rental properties, from large-scale, multiple-occupancy developments to single-family units. In many cases, housing has been transformed into fictitious capital and circulated (traded), as stock in REITs or securities derived from rental incomes (Van Loon and Aalbers, 2017; Waldron, 2018).

The private rental market and the state

So far we have established how housing conditions shifted leading up to and since the crisis, as well as the socio-economic factors that facilitated the revival of private renting, especially in more economically liberal contexts. Housing systems are, nonetheless, always political by design, with government institutions also playing a critical role in recent tenure restructuring. The role the state has played in supporting revival in private rental housing can, however, often be difficult to discern.

The objective of advancing private renting over other tenures is rarely explicit, and coherent state policies promoting the tenure are scarce. Indeed, housing policy is more typically discussed in relation to political decisions to reduce social housing supply or extend homeownership, particularly in the Anglo-American contexts where the upsurge in private renting has actually been most pronounced. State approaches to renting are thus ostensibly, or even characteristically, ambivalent in such contexts. The UK, for example, has certainly seen policy measures accommodating private rental growth, such as build-to-rent subsidies and post-crisis deregulation measures (Crook and Kemp, 2019). Yet, simultaneously other steps have been taken that also constrain private rent, such as the recent introduction of an additional stamp duty for buy-to-let purchases, the reduction of tax deductibility on buy-to-let mortgages and a ban on no-fault evictions in parts of the UK (see Moore, 2017). Rather than a coherent set of policies, the result is a patchwork of sometimes contradictory policy measures.

While economically liberal countries appear ambiguous in their support of private rental markets, what is more common is a shallow regulation of tenure rights and rent increases that has made investment in them potentially more attractive. In contrast to these liberal market approaches, the most ‘successful’ private rental sectors have been developed in countries like Germany and Switzerland, where rents and tenancies are tightly controlled, housing providers well-regulated and the responsibilities of landlords clearly defined. In these countries, homeownership remains a minority tenure and swathes of low- and middle-income households, especially among urban populations, live in commercial rental units. Kemp and Kofner (2010) explicitly distinguish this approach from the market-liberal one, arguing that strong rent regulation and security of tenure have been necessary to create levels of stability that make the sector attractive to landlords and investors. In recent years, nonetheless, this demarcation has in some respects faded, with German authorities, for example, pursuing policies that open private rental markets up more to global capital flows and rent increases (Wijburg and Aalbers, 2017).

The regulation of private renting in the Netherlands contrasts to both examples above as established by Kemp and Kofner (2010). The Dutch reorientation towards private renting needs to be considered in light of more general, long-term housing marketization in the context of a deeply socialized and highly decommodified urban housing system dominated by not-for-profit housing corporations. Policies have, since 1990, increasingly evolved around private ownership and allocation through market mechanisms following the logic of roll-out neoliberalization (Harvey, 2005; Peck and Tickell, 2002). This roll-out remains, nonetheless, deeply rooted and path dependent, shaping a very particular pattern of market regulatory practice.

Neoliberalization is an ongoing process that forwards ‘the market’ as the main distribution mechanism. It does not, however, necessarily imply a smaller state. State interference in housing has not just been reduced in favour of market free rein. Instead, governments have restructured and reoriented their efforts to support market forces, and mould them in such a way that they can be introduced and expanded into new spheres and spaces. In other words, housing markets are not just deregulated, but state regulation has moved in the neoliberal era from constraining to supporting the market. This is what Aalbers (2016) terms regulated deregulation: some actors are given more market freedom, while new regulation is to ensure continued state enforcement. Furthermore, the neoliberalization of housing policies is often uneven, partial and contradictory (Brenner et al., 2010). Brenner and colleagues conceptualize neoliberalization as unfolding unevenly across time, space and scale. While the overall tendency may be towards market-oriented reforms, market-constraining measures may also be introduced. In so doing, states keep a certain degree of control over markets – regulating where and to what extent market forces are accommodated.

Neoliberalization also builds on existing institutional frameworks. Older institutional arrangements are not necessarily, or at all, eradicated. Instead, existing institutions may, for example, be converted to fit new purposes, or new policy arrangements may be added on top of existing institutions (Streeck and Thelen, 2005). Neoliberalization may thus result in the formation of different policy layers that complement or contradict each other as new policies are introduced to correct or amend older arrangements (Brenner et al., 2010). Additionally, the state is not one coherent entity, but rather consists of different entities and internal struggles (Bourdieu, 2005), contributing to the formation of different policy layers.

In many ways, then, Dutch housing sector restructuring falls into established models of neoliberalization, with the state taking a lead role in creating the market by setting the rules of the game (Aalbers, 2016). In our analysis of the Amsterdam case, we conceptualize recent rental market restructuring as a form of regulated marketization. Conceptually, this can be considered a specific adaptation of variegated neoliberalization ‘on the ground’. Substantively, what sets the Amsterdam case apart, nonetheless, are the type of state interventions possible and its capacity to steer. Marketization is, in this case, not only state-controlled but also state-initiated. It reflects a particular institutional layering of the housing system (cf. Van Gent, 2013) that facilitates the purposive pursuit of a particular conception of housing affordability and urban growth. This does not mean that the Dutch housing sector has resisted market vagaries and disruptive flows of global capital investment and deepening financialization. Rather, as the following analysis of private rental sector restructuring in Amsterdam demonstrates, the roll-out of market renting has largely sought to compensate for the successful, state-led development of low-cost social renting and rapid expansion of the owner-occupied housing market, with the objective of creating a new layer of ‘affordable housing’ (although actual affordability is questionable) for middle-income households.

The revival of private renting in Amsterdam

Setting the scene

Amsterdam has a rich history of providing affordable rental housing to large segments of its population. While, like most industrial cities, private rental dwellings housed the vast majority of working households at the end of the 19th century, over the course of the 20th century, a large and well-funded social housing sector was built up by not-for-profit housing associations (Van der Schaar, 1987). Social housing intensified in the post-war decades, with private renting diminishing in scale, from the largest to the smallest tenure. Moreover, due to the dominance of the social sector, rents in the private sector typically remained low to remain competitive (see Kemeny, 1995), supporting high levels of decommodification in housing and welfare overall (Uitermark, 2009).

In the 1990s, a series of social, economic and urban policies came to the fore, which have ultimately reversed this trend. This first phase of housing system liberalization derived from national-level re-regulation, but had a particular impact in cities. Dutch housing policy reforms set out to promote homeownership (e.g. Heerma, 1989), with this sector considered more suitable to middle-income households. In the social sector, meanwhile, rents were brought closer to market levels and social housing providers were made into private, not-for-profit corporations (Van Kempen and Priemus, 2002). This policy allowed housing associations greater economic stability, as well as the capacity to generate more income through the construction of housing for sale in mixed-tenure developments.

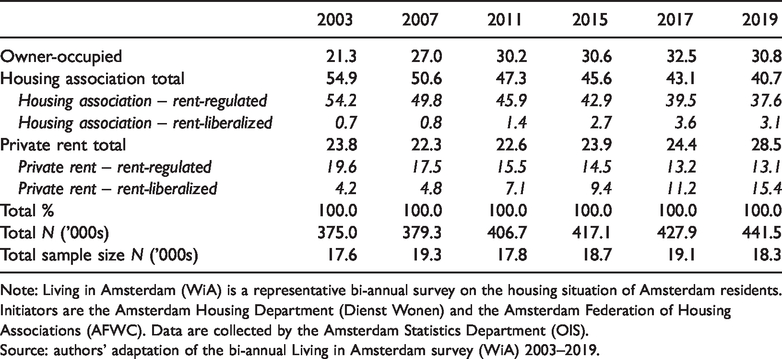

In Amsterdam, this contributed to a notable restructuring of the housing stock, with the share of owner-occupied dwellings increasing from 12% of all housing in 1998 to 32% in 2017 (Table 1). This shift was also part of a municipal state-led gentrification agenda, to provide more housing options to middle-class and affluent households (Van Gent, 2013). As part of this same agenda, the city’s social rental sector has seen a substantial decrease, mainly through demolitions as part of urban renewal and the sale of social rental dwellings. This led to a net decrease of almost 30,000 housing-association units between 2002 and 2017 (Hochstenbach, 2017). As of 2019 still some 41% of all housing was let by housing associations, down from 55% in 2003. Private renting was, initially, also a significant victim of restructuring, with its share of the housing stock in Amsterdam falling from 34% in 1998 to 22% by 2007.

Tenure composition of the Amsterdam housing stock.

Note: Living in Amsterdam (WiA) is a representative bi-annual survey on the housing situation of Amsterdam residents. Initiators are the Amsterdam Housing Department (Dienst Wonen) and the Amsterdam Federation of Housing Associations (AFWC). Data are collected by the Amsterdam Statistics Department (OIS).

Source: authors’ adaptation of the bi-annual Living in Amsterdam survey (WiA) 2003–2019.

Ostensibly, the data point to a new stage in the commodification of the Amsterdam housing stock over the last decade. One element is the post-crisis slowing of growth of owner occupation (Table 1; +2.3 percentage points between 2011 and 2017, compared to +8.9 percentage points between 2003 and 2011). In fact, most recent data even indicate that between 2017 and 2019 the share of owner-occupied units decreased from 32.5% to 30.8%, despite new construction. Another element is the remarkable increase in private renting since 2008, as we will discuss in detail shortly. Also at the national level, the private rental sector is growing but stands at a substantially lower 13% in 2018 (Statistics Netherlands, 2019a).

Leading up to the economic shock of the GFC, a second phase of market-oriented housing sector restructuring was already in the making. Since the mid-2000s, Dutch private developers had been contesting, at the EU level, the dominance of non-profit providers in the market for housing (Gruis and Priemus, 2008). At the same time, a number of public scandals had revealed high levels of mismanagement in the social sector (Boelhouwer and Priemus, 2014). Subsequently, along with the election of market-liberal Rutte cabinets from 2010 onwards, a series of new measures were rolled out enforcing EU regulations on open competition. Specifically, new regulations stipulated that access to rent-regulated housing would mostly be limited to low-income groups (Elsinga et al., 2008). 1 On top of this, the providers of rent-regulated housing – mostly housing associations – were confronted with an additional austerity tax measure in 2013 (the landlord levy), which has led to a steep decline in new construction and rent increases (Boelhouwer and Priemus, 2014).

Other national rule changes also helped open the landscape of rent-seeking in Dutch cities. Dutch rent regulation is based on a point-scoring system that calculates maximum rents based on dwelling size, quality and other characteristics. Rent-regulated dwellings scoring below a set number of points have a rent below the maximum threshold of monthly rent (€711 in 2018, subject to inflation-related corrections). This rent regulation system applies to dwellings owned by housing associations and private landlords. Rental dwellings that score enough points ‘pass’ a liberalization threshold above which no restrictions exist regarding rent levels and income criteria. In 2015, the national government adjusted the point-scoring system to allow rent levels to be recalibrated to local market demand. They have done so by including housing values (Dutch: WOZ), which are based on local sale prices on the owner-occupied market. As a consequence, in expensive locations – including large parts of Amsterdam – most rental units score enough points to be shifted to the free-market sector once sitting tenants move out.

An important distinction on the Dutch rental market, then, is not only whether the landlord is a private ‘for-profit’ entity or a social ‘not-for-profit’ provider, but also whether the dwelling is rent-regulated – with limited rents and restricted access – or rent-liberalized – with freely determinable rents and accessibility. Rental dwellings owned by both housing associations and private landlords can be rent-regulated and rent-liberalized. In all segments of the rental market, tenant rights are relatively well enshrined and indefinite contracts still tend to be the norm. 2 The rent-regulated sector is under pressure due to its shrinking size and the imposition of stricter eligibility criteria (maximum household income) diminishing access. Furthermore, rent-regulated dwellings owned by housing associations are allocated through a central waiting list system in which average waiting times in Amsterdam are roughly 9–11 years, rendering this housing segment all the more inaccessible to relative newcomers and outsiders.

Meanwhile, a series of post-GFC reforms and developments has pushed homeownership increasingly out of reach as well. Stricter mortgage-lending practices have been introduced, and maximum mortgages lowered (both loan-to-value and loan-to-income). Ongoing labour market flexibilization has further complicated access to mortgage credit. In addition, Dutch urban house prices, especially in Amsterdam, have been booming at an unprecedented rate since 2013 (Hochstenbach and Arundel, 2019). These developments mean that for a growing urban population homeownership is out of reach – particularly for younger first-time buyers and middle-income households.

Demand for private rent

Decreasing access to social rental and owner-occupied housing has thus created a core problem for housing market outsiders. Housing has become a particular issue for middle-income groups who earn too much for social rent allocation, but are also unable to buy in the current market (Hoekstra and Boelhouwer, 2014). This has spurred a surge in demand for rent-liberalized private renting. Awareness of the issue preceded the 2008 crisis. For example, the 2007 municipal housing policy whitepaper stated: For a long time Amsterdam has focused its housing policies on the people with the lowest incomes. However, in the current housing market middle income [persons] too are unable to buy a dwelling or to rent above the rent subsidy threshold. Amsterdam therefore wants to expand the target group of its policies and include this income group. There will be more attention to the middle segment, in the rental as well as owner-occupied sector. (Gemeente Amsterdam, 2009: 11, authors’ translation)

More recently, policy focus has more explicitly shifted towards promoting the rent-liberalized segment, which is assumed to benefit those middle-income households falling between tenures, specifically young upwardly mobile households who want to stay in the city. The 2014–2018 municipal coalition agreement between the local political parties in government D66 (liberal-democrat), VVD (conservative-liberal) and SP (socialist) also stressed the need to cater to middle-income groups in the rental housing sectors: We will step up our efforts to increase the supply of affordable rental housing for middle income groups. We will do so by giving more room for dwellings with rents between 700 and 1000 Euro in new-build developments. We will call on the landlords to ask suitable rents. (D66 et al., 2014: 7, authors’ translation)

While not strictly delineated, the target group of middle-income households is typically considered to have a gross household income between €37,000 and €50,000 per year. For these income groups such rent levels translate into relatively high rent burdens, and it has been assessed that 28% of middle-income households are unable to afford a rent above €700 per month at all (Van Middelkoop and Schilder, 2017). This unaffordability makes the strong focus on expanding this so-called ‘middle segment’ itself remarkable.

More recently, ambitions to expand the middle segment have also become a priority of national housing policy. In the coalition agreement of the Rutte III cabinet, led by the conservative-liberal VVD party, it is stated that: There should be more affordable rental housing in the liberalized sector. Opportunities in municipal policy to increase the supply, to steer on price levels and to sell social rental housing must be fully exploited. (VVD et al., 2017: 31, authors’ translation)

Charting the revival of private rent

Political ambitions and growing demand have translated into an unlikely increase in private renting since the onset of the crisis. This return to growth is also closely intertwined with a more substantial restructuring of private rent as a tenure (see Table 1). Throughout the 2000s, the majority of private rental dwellings belonged to the comparatively affordable rent-regulated segment. This affordable sector provided cheap housing options to a broad population and easy access to newcomers from various backgrounds, including migrants, students, middle-income and upwardly mobile households (Dienst Wonen, 2008). Decline in the regulated (cheap) segment of the rental stock had already begun before the onset of the GFC, with the private rental sector as a whole still in retreat at that point. After 2007, however, the overall private rental sector began to grow again, but driven by expansion in the liberalized rather than the rent-regulated subsector. In fact, between 2007 and 2019 the share of more affordable, regulated private rental dwellings continued to decline from 17.5% to 13.1%.

While rent-liberalized housing was still a niche sector in 2003, it has expanded considerably since. The revival of the total private rental sector since 2007 is solely accounted for by expansion in this segment. In 2007, only 4.8% of Amsterdam’s housing stock was liberalized private rental dwellings, but by 2019 this had increased to 15.4%. The revival of private rent is thus inextricably linked to its restructuring – away from affordable rents catering to a broad segment of the population, and towards more exclusive and expensive housing. Most recently, expansion of the liberalized private rental stock has gone at the expense of not only regulated social and private rent, but also owner occupation. What this highlights is that private rental growth in Amsterdam is essentially a story of marketization, even though these two need not always be related. Furthermore, policies also focus on liberalized private rental housing, as we show below, further highlighting the link between private renting and marketization.

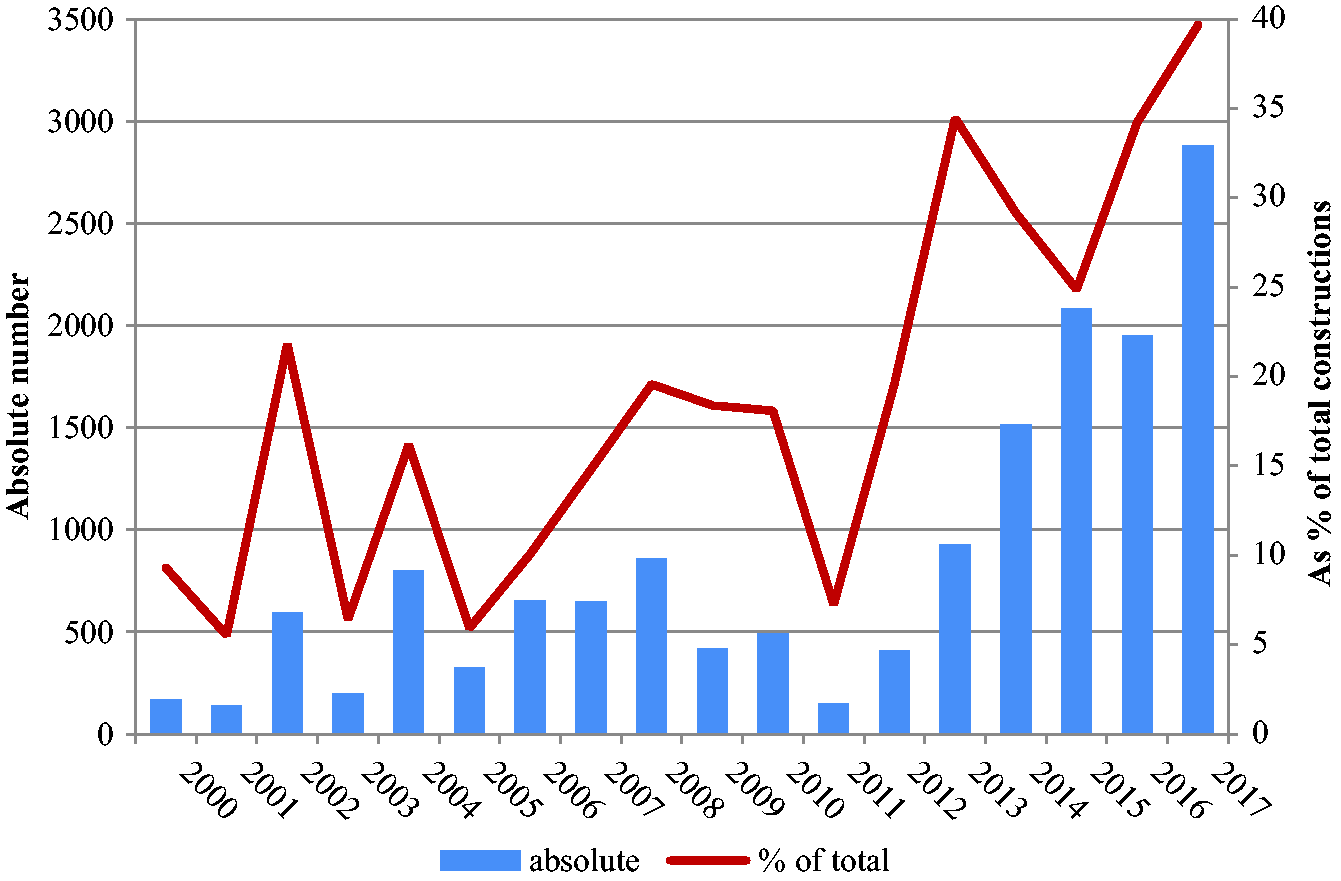

New construction has played an important role in reshaping Amsterdam’s post-crisis tenure profile. In the pre-crisis period the majority of new developments were owner-occupied, while only a small share of new construction was rent-liberalized. In the years following the GFC, the number and share of rent-liberalized housing units among new construction rapidly increased – up to 2881 new constructions started in 2017, or almost 40% of all new construction (Figure 1). The main financers of these dwellings are large institutional investors. For them, the construction of rent-liberalized housing has become an attractive long-term investment with stable revenues (CBRE, 2018; also see Raco et al., 2019). Furthermore, the municipal government stipulates that a substantial share of all new developments should consist of middle-income rental housing, a point we will turn to below.

Rent-liberalized housing constructions per year in Amsterdam in absolute numbers and as percentage of total new constructions (source: Van der Molen (2018); authors’ adaptation).

Another way in which the rent-liberalized sector has grown is through the liberalization of existing rental units. The majority of Dutch tenants enjoy relatively strong rent protection, meaning that rents can only increase incrementally. Residential turnover, then, typically allows landlords to raise rent levels (for new tenants) more substantially. The vast majority of new allocations in the private rental sector have been in the rent-liberalized sector, often in the most expensive segments (Gemeente Amsterdam, 2020; Van Duijne and Ronald, 2018). Not-for-profit housing associations have also started to rent out a larger share of their stock in the liberalized segment to accommodate middle-income households barred from entering the regulated sector (from 0.8% in 2007 to 3.1% in 2019; Table 1). In so doing, they have complied with political ambitions to expand this housing segment. The aforementioned landlord levy only applies to rent-regulated dwellings – thus providing an additional financial incentive to move dwellings from the regulated to the liberalized sector, as well as to sell off social rental units.

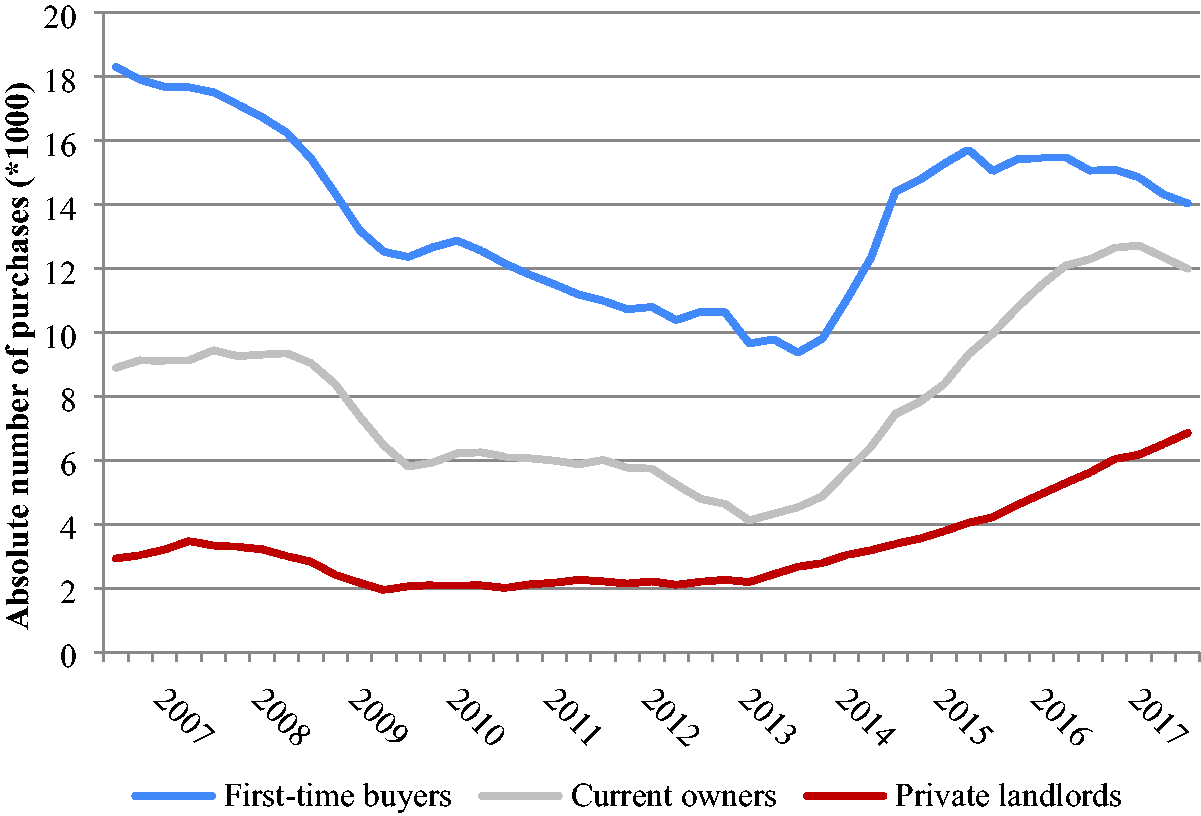

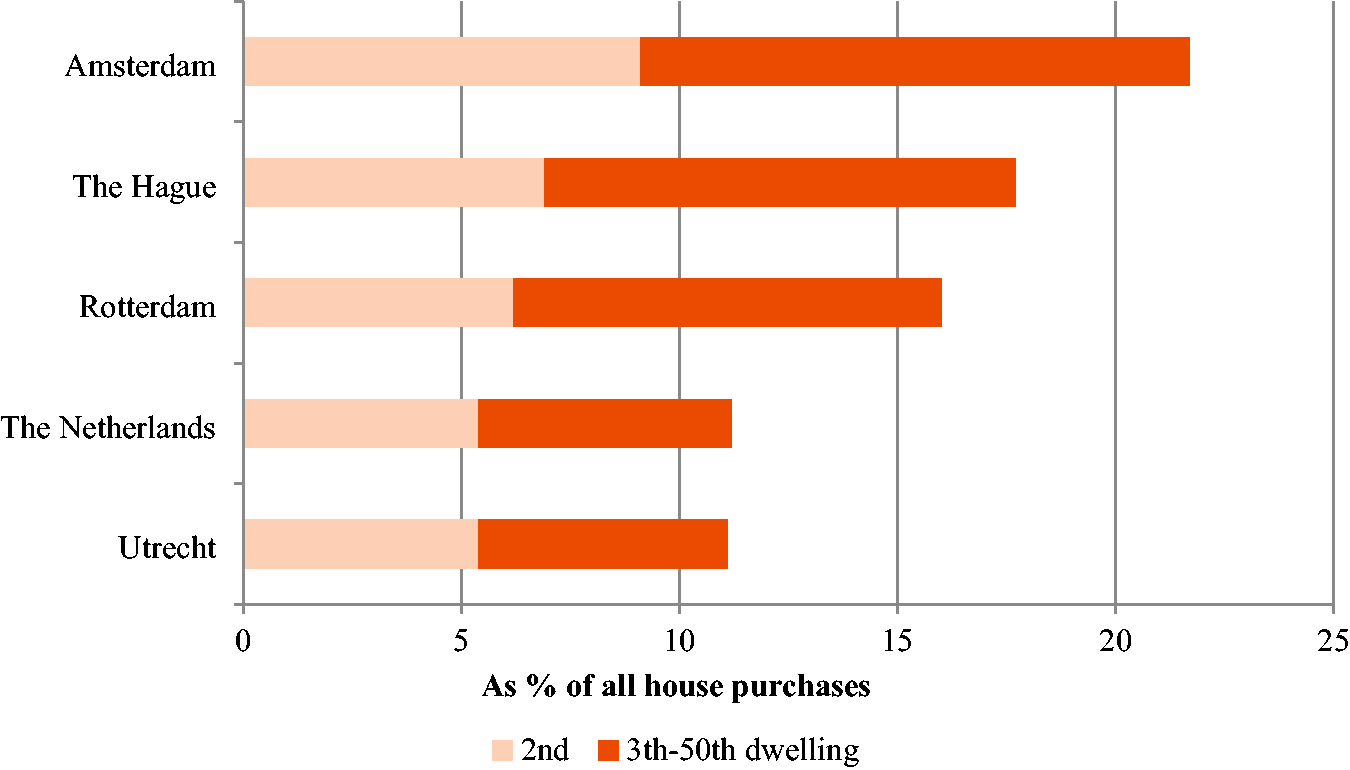

Tenure conversions are also important in expanding the rent-liberalized sector. For a long time, tenure conversions from rent to owned facilitated the expansion of homeownership (Boterman and Van Gent, 2014; Hochstenbach, 2017). Rent regulation and rising house prices meant it was often more profitable for private landlords to sell. For social housing providers too, selling was a strategy for generating the capital necessary for reinvestment in existing and new dwellings. Conversely, recent years have seen a rise in ‘reverse’ tenure conversions from owner occupation to rent. Such buy-to-let purchases are typically associated with small-scale landlords snapping up property to rent out (Aalbers et al., 2018). The number of such buy-to-let purchases in the four biggest cities has increased considerably in recent years (Figure 2), with the number of purchases by first-time buyers and, to a lesser extent, by existing owner-occupiers declining since 2015 and 2017 respectively. In 2017, some 20% of all house purchases were earmarked as buy-to-let, up from around 10% before, and shortly after, the GFC. Cross-sectional data for 2016 further reveal that the buy-to-let share is higher in Amsterdam than in other major cities and the country overall (Figure 3).

Absolute number of house purchases per quarter by first-time buyers, current owners and private landlords in the big four cities combined (Amsterdam, Rotterdam, The Hague, Utrecht) for 2007–2017 and private landlord share per city in 2016 (source: DNB (2018)).

The share of purchases by private landlords (% of all purchases) per city in 2016 (aggregate data provided by Kadaster, the Dutch Land Registry)).

There are various factors contributing to the current boom in buy-to-let. Historically low interest rates, as set by the European Central Bank, make real estate a comparatively attractive investment vehicle (Fernandez and Aalbers, 2016). Private landlords pay an annual wealth tax of 1.2% over assessed property values (plus other taxes), while rental revenue and property gains are not taxed. Capital has thus been channelled into the built environment by large investors and different types of private households alike, echoing patterns and trends in other countries. This may also include parents buying housing to rent to their children – often a combination of intergenerational solidarity and financial investment strategy (Druta et al., 2018; Hochstenbach and Boterman, 2017).

While new private rental developments are typically pursued by larger institutional investors, small landlords – owning one or two additional properties – dominate the buy-to-let market. Around half of all Dutch private rental dwellings are owned by private individuals, and the other half by institutions. Growth has been concentrated in both segments (Statistics Netherlands, 2019b).

The increase in buy-to-let also follows from the increased demand from middle-income groups, which is in turn the result of Dutch housing policies that have curbed access to social rent and owner occupation, and allowed for greater rent increases. Some specific housing policy measures have more directly facilitated the rise of buy-to-let, such as the introduction of temporary rental contracts in 2016 and the lowering of purchase taxes (stamp duty) in 2011. The rise of buy-to-let should thus be considered the outcome of (international) capital flows, demand from middle-income groups and political choices, which are, as we explore below, intertwined.

The politics of private rental’s revival

We have so far shown that the push to expand the rent-liberalized housing sector has gradually intensified and expanded into a national policy priority. This has translated into growth of the tenure. More recently, concern has mounted regarding the exclusionary effects of liberalization, with rent levels quickly spiralling upwards, rendering the tenure unaffordable to all but the highest-income groups. Such a development is evidently at odds with the ambition to expand housing options for middle-income groups, and has led to calls and efforts to introduce new policy layers to regulate rent levels even in the liberalized sector.

Market forces have thus not simply been given free rein in the context of Amsterdam’s rental sector. Instead, the expansion of Amsterdam’s liberalized rental segment has taken the form of what we have termed regulated marketization. Simply put, while marketization has been facilitated by policy changes that allow landlords to more easily evade the liberalization threshold, regulation is also being put in place to prevent rents becoming too expensive. Local government has now embarked on various paths to regulate marketization processes in the private rental sector. Regulated marketization is not a clear, one-directional and concerted effort though. It is the outcome of different and often contradictory forces at work, and tensions between them.

A first key tension is between national and local politics. Successive national (Rutte) cabinets, led by the conservative-liberal VVD party since 2010, have focused on expanding market housing at the cost of decommodified social rent. A specific post-crisis goal of the central state was to facilitate the rapid recovery of house prices and ameliorate the exposure of Dutch lenders to risk on domestic mortgage debt (Boelhouwer, 2017). National politics focused not only on stimulating home buying, but also means by which the rental sector could be liberalized and expanded. This included direct attempts to entice international investors into buying up and subsequently liberalizing social rental housing (Hendriks, 2018), as well as embracing buy-to-let investment, as is evidenced by this quote from Minister of the Interior Kajsa Ollongren: ‘Buy-to-let can, generally speaking, contribute to a desirable expansion of the supply of rental housing, especially when this expansion concentrates in the still relatively small middle segment’ (Ollongren, 2017: 1, authors’ translation).

Despite acknowledging that buy-to-let crowds out prospective first-time buyers from the Amsterdam housing market, Minister Ollongren has not considered ‘national measures to slow down buy-to-let’ to be fitting (Ollongren, 2017: 4). The Amsterdam municipal coalition government has subsequently pushed back, calling for more regulation, as can be seen, for example, in the 2018 coalition agreement: Especially people with a low income and people with a middle income can barely access the housing market. Distributing the increasing scarcity calls for more regulation; for more of a grip of the municipality on the housing market. (GroenLinks et al., 2018: 32, authors’ translation)

Inter-class politics lie at the heart of government motivations for, and approaches to, the regulated marketization of rental housing. In the 1990s and 2000s, the expansion of homeownership absorbed increasing numbers of middle-class households, especially in Amsterdam. Lower-income households continued to be well housed under the new social housing model based on self-financing not-for-profit housing corporations (Ronald and Dol, 2011). In the late 2000s, however, both middle- and low-income households found it increasingly difficult to house themselves due to house price increases and diminishing social stock. Given the city’s limited capacity to cool the owner-occupied market – in the context of national-level stimulation – the long-neglected private rental sector provided an expedient means to reduce pressure on both sides of the housing market. That is, stimulation of private renting provided greater access to the city for middle-income households, while also reducing pressure on the shrinking social rental stock.

Attempts by local government to introduce new regulations relate to a second key tension in regulated marketization: between the existing housing stock and new construction. Local government has held a tight grip on new construction as it owns most of the city’s land, which it issues through a leasehold construction system (erfpacht). The leasehold allows the municipal government to retain ownership and control, and to pose strict requirements for new developments, including tenure composition. The 2017 municipal Housing Agenda stipulates that 40% of new dwellings should be regulated rent, and a further 40% of dwellings should be in the middle segment (both owned and rented), leaving 20% for the high-end segment (Gemeente Amsterdam, 2017). This represents a notable break with recent history, which sought to expand owner occupation by stipulating that new development incorporated 70% homeownership. Leasehold also allows local government to pose additional requirements: on the quality and size of dwellings, on allocations, and on rent levels for fixed periods (e.g. 50 years).

Stringent criteria for new construction were heavily contested by institutional investors, who argued that their rates of return were put at risk. They threatened to pull out of new projects and tenders, which would reduce new housing supply. In early 2020, the municipal government and the IVBN, the Association of Institutional Property Investors in the Netherlands, nevertheless struck a deal to build a further 10,000 rent-liberalized units by 2025. While many criteria remain in place, the municipal government has nonetheless relaxed requirements in terms of starting rents and tenure mix to accommodate institutional investors’ concerns.

The strong control over new development stands in stark contrast with the lack of control over existing housing. Local government lacks instruments to prevent landlords from substantially raising rents when new tenants move in. Furthermore, it is currently not able to dampen the growing buy-to-let sector, or tackle the potentially negative consequences. Critically, while Amsterdam city council has called to expand rental regulation, the power to change this policy lies with the national government: We will forcefully continue our lobby towards the national government to make regulation of the middle segment possible. In so doing, we try to prevent that social rental dwellings (housing association and privately owned) after liberalization immediately disappear in the most expensive segment. (GroenLinks et al. 2018: 32, authors’ translation).

A final tension in regulated marketization concerns temporality. Rental market liberalization has only been matched retrospectively by attempts at re-regulation. In other words, the ambitions established in one era have created new conditions that have demanded a reversal in policy. This temporal shift is particularly evident at the local level: while the Amsterdam municipal government was quick to embrace middle-segment rental housing, years before the national government, they are now also the first to call for re-regulation. A similar, though less pronounced, temporal dynamic is now materializing at the national level. In the wake of rapidly rising rents, the national government has recently proposed an ‘emergency button’ aiming to cap monthly rents based on property values (Ollongren, 2019). This measure has not been introduced yet, but the national government accepted a motion in November 2019 to limit rent increases for sitting tenants in the liberalized sector. Another example concerns new-build construction. Following the GFC, new construction ground to a halt, not least due to the municipal decision for a temporary stop in building. When the housing market picked up again, new development was welcomed, especially in the liberalized rental sector. This included some highly expensive rental developments that have become emblematic of new housing stock. Only later, in response to such projects, were stricter requirements set regarding rent levels, housing standards and rent increases.

Conclusions

This paper has addressed how and why a revival of the private rental sector has taken place in Amsterdam since 2008. We have shown that private rental growth and liberalization have come about in various ways: through new construction, through rent increases of existing rental housing and through buy-to-let conversions. The Amsterdam case is particularly salient, because it allows us to identify what a state-initiated revival of private renting looks like. While states are typically ambivalent towards private rental growth, in Amsterdam the state has taken the lead in achieving growth. Still, however, growth is the product of uneven efforts by both local and national governments. From our case study, it is possible to distil three broader analytical points.

First, state support for private rent should be considered in light of pre-existing policies and institutional arrangements, which generate and reflect perceived failures, naturalize certain situations and reflect key qualities (cf. Brenner et al., 2010). State support for private rental growth should be considered in light of government attempts to revive the housing market through intensified capital investments during the deep housing market slump following the GFC. The notion that current policies have created a middle-income group falling between tenures is strong, and has fostered popular support for stimulating middle-segment rental housing. The revival of private rent has been part of a restructuring in favour of a more expensive and liberalized rental sector. As such, promoting private rent can be considered an instance of more general housing marketization also found elsewhere, but mediated by and tailored to the specific Amsterdam housing context.

The focus on stimulating the middle segment also stems from ongoing efforts to normalize the notion that social rent should only cater to low-income residents. The perception that Amsterdam has an oversupply of cheap housing for the poor has been a discursively powerful one. Expansion of rent-liberalized housing should therefore be considered part of a politics catering to the perceived needs and wishes of the middle classes (Van Gent and Boterman, 2019). Policy support for the growth of private rent cannot be seen independently from relatively strong levels of tenant protection in the tenure, in contrast to, for example, the precarious English private rental sector (Kemp, 2015; Moore, 2017). Again, this shows how current restructuring efforts are moulded by pre-existing institutional arrangements – as they build on certain ‘givens’ and strengths.

Second, expansion of the rent-liberalized private sector in Amsterdam takes the form of regulated marketization. Market forces are not simply unleashed, but are instead given more leeway and directed into certain domains (i.e. middle-segment private rent). We consider regulated marketization a specific materialization of variegated neoliberalization in a post-GFC urban context, marked by intensified capital investment in urban space. Regulated marketization of Amsterdam’s rental housing stock should be understood as the latest of successive ‘waves’ of housing neoliberalization (Brenner et al., 2010). While previous waves focused on expanding owner occupancy, the most recent wave seeks to facilitate capital flows and market forces in the private rental sector. Yet, regulated marketization represents the simultaneous accommodation of these capital flows, and attempts to mould, regulate and constrain them. Liberalization of the Amsterdam rental sector has been accompanied by the introduction of new incentives and new regulations in order to structure private rental growth. More specifically, our case represents a highly concerted mode of regulation that accommodates rent increases but simultaneously seeks to prevent rents from becoming too expensive and ensure that new rental dwellings will remain affordable to middle-income groups.

Nevertheless, regulated marketization is marked by its own tensions. While national politics has introduced legislation to spur liberalization, local politics seeks to introduce new regulations to keep market forces in check. But where the Amsterdam government has a tight grip on new construction, it has little control over developments in the existing stock. This translates into strong regulation in the former, and a lack of regulation in the latter. Finally, regulated marketization was not consciously implemented, but has gradually developed over time. While liberalization and broader housing marketization have been prominent features of the Dutch housing market for a longer time, local calls for re-regulation have only emerged recently. We understand these tensions as the materialization of several hallmarks of neoliberalization as put forward by Brenner et al. (2010). For them, neoliberalization unravels unevenly across spatial scales, is to be understood in relation to preceding policies and their contradictions, conflicts and failures, and constantly evolves as market-facilitating and -constraining measures develop in dialogue.

Third, while distinguished by the regulated marketization approach, the Amsterdam case aligns with other recent scholarly work on private rental growth in other ways. Amsterdam’s private rental market is increasingly integrated in capital flows, and attracts investments from different types of investors, ranging from large international institutional investors to small-scale landlords (Beswick et al., 2016; Ronald and Kadi, 2018). Increasing levels of demand make the private rental sector an attractive market for investment, especially in the existing stock where current regulations and restrictions cannot hold back liberalization. In central neighbourhoods, these developments may fuel specific forms of rental gentrification (August and Walks, 2018; Paccoud, 2017). In such neighbourhoods, highly speculative and more volatile investment may sweep through the rental market with little regard to equitable housing distribution, urban liveability and population mix.

The overall effect of current efforts to expand the rent-liberalized housing sector go in two directions. On the one hand, the inclusion of a substantial share of middle-segment rental dwellings in new developments accommodates middle-income populations and prevents the development of exclusive upscale areas. On the other, these efforts are part of intensifying marketization of housing. In the existing stock particularly, further price increases will exclude low- but also middle-income populations. Private rental growth and restructuring will thus add to already forceful gentrification sweeping through Amsterdam.

Footnotes

Acknowledgements

The authors thank the editor and three anonymous reviewers for their supportive and helpful feedback.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Cody Hochstenbach acknowledges the financial support of a VENI grant (VI.Veni.191S.014, ‘Investing in inequality: how the increase in private housing investors shapes social divides’) from NWO, the Dutch Research Council.