Abstract

Extant cluster policy research has largely ignored the particular role that cluster organizations play in reifying cluster policies in practice. Based on a survey of 163 cluster organizations in the European life sciences sector, this study explores the heterogeneity of cluster organizations in geographic space and examines whether and where revealed competition – defined as the combined overlap in service offerings, sub-sectoral focus and funding sources – between life science cluster organizations within European regions is most apparent. The findings indicate that the degree of functional and sectoral substitutability of cluster organizations differs substantially across Europe, though some regions, particularly in Spain, Denmark, France and Estonia, are more prone to revealed competition.

Introduction

Over the past two decades, cluster organizations have become an increasingly prominent component of cluster development policies (Glaser, 2013; Lundequist and Power, 2002; Teigland and Lindqvist, 2007). Policy-makers perceive the primary coordinating tasks of cluster organizations as improving the cluster’s business environment, supporting innovation and collaboration among cluster actors and facilitating the attraction of external resources such as (foreign) investment, skilled labour and tacit knowledge and financial capital, all of which are instrumental in enhancing the competitive advantage of clusters (Lindqvist, 2009). Recent figures reveal that since the 1990s, approximately 1400 cluster organizations have been established worldwide, of which roughly 60% are publicly financed, while the remaining 40% are funded by private investors (Ketels et al., 2012). Particularly in Europe, public policies to develop and finance cluster organizations are ubiquitous and implemented at various administrative and spatial levels – that is, within a multilevel governance framework (Sternberg et al., 2010). For instance, the European Commission (2008) currently promotes the excellence of cluster organizations in innovative sectors. Likewise, many national and local governmental authorities explicitly support the establishment of cluster organizations in their cluster development programmes (e.g., MacNeill and Steiner, 2010; Sölvell and Williams, 2013).

Despite policy-makers’ burgeoning interest in cluster organizations, it is by no means clear whether policies aimed at developing cluster organizations are coherently devised and effectively aligned. The main reason for this lack of clarity is that there still is only limited knowledge about the functioning of cluster organizations and the way their efforts are organized and coordinated across administrative levels and geographical space (see Ebbekink, 2017; Ebbekink and Lagendijk, 2013; Lindqvist, 2009). Extant empirical findings identify variations in the strategy and service offerings of cluster organizations (Skålholt and Thune, 2014; Teigland and Lindqvist, 2007), focus on the efficient symbiosis between cluster organizations and other (local) cluster actors to facilitate cluster development (Glaser, 2013; Laur et al., 2012; MacNeill and Steiner, 2010; Sölvell and Williams, 2013) or show that the importance and effectiveness of managed clusters (Duranton et al., 2010) and cluster organizations (Huber, 2012) are rather limited. Notwithstanding their practical value, these findings are predominantly based on studies of specific clusters and therefore do not provide a comprehensive overview or yield conclusions that are relevant to a wider population of cluster organizations. Besides, without a comparative approach, case study research makes it hard to give a clear overview of how the efforts of cluster organizations are organized and spatially distributed to reify cluster policies.

To the best of our knowledge, only three studies have explicitly addressed the functioning of cluster organizations from a large-scale cross-country comparative perspective: the empirical work by Ketels et al. (2012) on the role of cluster organizations in strengthening clusters; the study by Coletti (2010) on the differences between cluster managers in technology and industrial clusters; and the work by Isaksen and Hauge (2002), who study the activities of cluster organizations and the implementation of (government-induced) cluster policy tools. 1 While all studies reveal considerable heterogeneity in the service offerings of cluster organizations across countries, the findings make it difficult to distinguish sector-specific characteristics and do not reveal whether the activities of cluster organizations operating in the same sector also differ at lower levels of geographical aggregation. Moreover, these studies are predominantly focused on within-cluster implications and, consequently, do not examine whether the different activities of cluster organizations are well aligned with regional cluster development programmes.

However, understanding these differences is valuable because substantial overlap in the characteristics of cluster organizations in the same region and (sub-)sector could imply that cluster organizations compete for the same external resources to facilitate cluster development and that geographical coordination of cluster policies is lacking. In turn, the overlap in cluster organizations’ characteristics and the misalignment of cluster policy portfolios may signal an increasing risk of overinvestment in geographically proximate cluster development programmes and help to sustain less competitive clusters (Hospers and Beugelsdijk, 2002; Isaksen and Hauge, 2002; Jacobs and De Man, 1996). Overall, such uninformed cluster developments are unlikely to be welfare maximizing (Kiese, 2017).

To compare cluster organizations in a wider geographical context, this study complements existing research by examining cluster organizations in one specific sector: the European life sciences. In particular, the activities of cluster organizations are explored based on a framework conceptualizing revealed competition between cluster organizations (see Burger et al., 2013; Thissen et al., 2013) and taking into consideration three analytical dimensions of overlap: (1) functional, (2) sectoral and (3) funding. These insights are used to empirically examine whether and where revealed competition between life science cluster organizations within European regions is most apparent.

Given the particular context of the European life sciences sector, the main contributions of this study are threefold. First, this is one of few studies to explore the characteristics of cluster organizations across geographic space in one particular sector. By focusing on a single (sub-)sector, we are able to control for sectoral differences that drive part of the heterogeneity in the results of previous large-scale studies (Coletti, 2010; Isaksen and Hauge, 2002; Ketels et al., 2012). Second, in line with our conceptual framework we explore unique survey data that we recently collected from a large sample of cluster organizations across Europe. The comprehensiveness of the dataset combined with the functional and sectoral focus allows for initial geographical comparisons and provides a European overview with more general conclusions compared to existing (comparative) case studies on the life sciences sector (e.g., Caspar and Karamanos, 2003; Glaser, 2013; Kaiser, 2003; Teigland and Lindqvist, 2007; Trippl and Tödtling, 2007). Third, we provide findings and recommendations for cluster development that are relevant for policy-makers and cluster practitioners alike. For example, the identified characteristics and activities of cluster organizations across geographic space allow policy-makers and government officials to recognize the regional potential of establishing new or (re-)developing existing cluster organizations. Hence, a good understanding of the local competition between coordinated clusters clears the path for more goal-directed and effective strategic planning and policy-making with regard to regional cluster policies and long-term economic development (Ketels et al., 2012).

The remainder of this study is organized as follows. The next section presents a general background on the cluster organization and policy literature. Following that, we address the survey methodology and the data, before presenting a discussion of the findings. The final section concludes and presents recommendations for policy-makers and suggestions for further research.

Cluster organizations, policy and revealed competition

Clusters and cluster organizations

Ever since the seminal work of Porter (1990), clusters that represent spatial concentrations of interconnected firms and institutions in economically related activities have been regarded as potentially powerful engines of regional economic growth. Irrespective of the elusiveness and elasticity of the cluster construct (e.g., Benneworth et al., 2003; Martin and Sunley, 2003), the predominant factor in distinguishing clusters from mere agglomerations is the interaction between cluster actors (Malmberg and Maskell, 2002). Particularly in knowledge-intensive sectors such as the life sciences, clusters stimulate knowledge exchange and collaborative efforts between complementary cluster actors, thereby creating an advantageous environment for interactive learning and innovation (Waxell and Malmberg, 2007). In most cases, cluster activities are also directed at improving interactive channels of communication with complementary actors outside the cluster community to improve the cross-fertilization of knowledge (Bathelt et al., 2004; Moodysson, 2008) or establish links to international sales markets (Birch, 2008; Ketels and Memedovic, 2008).

Because the benefits of clusters in enhancing regional economic development may be substantial, it is not surprising that the cluster concept is featured prominently in many policies to stimulate regional and urban development (Lindqvist, 2009). Although cluster policy is an inherently hybrid concept combining elements of various policy areas (Raines, 2002), a common goal of cluster policies is the development of cluster initiatives, defined as organized efforts to enhance the competitive advantage and growth of clusters (Sölvell et al., 2003). These efforts generally involve collaborative actions of public and private actors (Teigland and Lindqvist, 2007), including governments, the local research community and the private sector. The general aim of cluster initiatives is to fulfil the needs of all participants within the cluster and, accordingly, to organize the objectives of cluster development.

Cluster initiatives typically result in the establishment of a cluster organization (Lindqvist, 2009; Sölvell et al., 2003). Cluster organizations are intermediate organizations with a diverse range of activities that implement and coordinate the explicit tasks and strategies devised in the cluster initiative (see Benneworth et al., 2003; Coletti, 2010; Glaser, 2013; Lindqvist, 2009). One result of this broad definition is an apparent diversity and scope of cluster organizations. As an intermediary, cluster organizations may represent clusters, science parks, (research) networks and associations or even entire regions or provinces. Although the strategic objectives of cluster organizations differ according to the regional and institutional conditions under which the organization is established, there are three broad categories of mutually dependent activities that can generally be distinguished: networking activities, the facilitation of cluster innovativeness and cluster promotion (Isaksen and Hauge, 2002; Ketels et al., 2012; Skålholt and Thune, 2014; Sölvell and Williams, 2013).

Cluster fundamentals, cluster policy and coordination

While the service offerings of cluster organizations may contribute to the development and competitive advantage of clusters, their effectiveness also depends on the role of cluster policy in shaping the cluster fundamentals (Angeles Diez, 2001). As argued by Fromhold-Eisebith and Eisebith (2005), clusters are the outcome of either implicit bottom-up initiatives or explicit top-down policies. Implicit bottom-up initiatives are developed by non-governmental actors, including firms, industry associations and universities. In contrast, explicit top-down policies represent clusters that are established, funded or even governed by state authorities at distinct spatial and administrative levels, that is the local, regional, national or, in the European case, supranational level (see Sternberg et al., 2010).

As underlined by Kiese and Hundt (2014), the simultaneous involvement of multiple actors and state authorities in a multilevel governance setting requires goal congruence and a shared cluster development strategy to avoid coordination problems. Particularly, top-down cluster policies are not always successfully devised and implemented. Because public actors tend to have higher expectations concerning the impact and importance of cluster initiatives than do private sector actors (Teigland and Lindqvist, 2007), policy-makers run the risk of overestimating the feasibility of creating or developing clusters. According to Hrdy (2016), for example, the future benefits of clusters are often over-predicted as the investments by local authorities do not always weigh up against the benefits from increased tax revenues and job creation. 2

In practice, the extent to which cluster policies can facilitate the development of clusters hosting economic activities that are unaligned with existing regional economic strengths is limited (Hospers et al., 2009; Ketels et al., 2012). Regional policy efforts are often directed at developing the same type of high value-added clusters, leading to so-called bandwagon effects (Jacobs and De Man, 1996). Although mimicking cluster development policies provides a means to learn relevant practices from others (Common, 2004), policy-makers are often unaware that this can result in overinvestment in particular economic activities (Hospers and Beugelsdijk, 2002). For instance, given the specific location requirements of life sciences firms, the use of cluster development policies by less well-endowed clusters can be questioned, because it is unrealistic that every region can be made into a life sciences hotspot (Malecki, 2004; Turok, 2009). Hence, neglecting the preconditions for creating competitive clusters makes cluster policies prone to fail or slow to deliver the expected results (Ketels and Memedovic, 2008; Laur et al., 2012).

At least partly driven by ‘wishful thinking clusters’ of local policy-makers (Enright, 2003), increasing competition can be observed between clusters (Isaksen and Hauge, 2002). Because geographically proximate clusters compete for the same external resources to facilitate their development, both horizontal and vertical coordination efforts (i.e. between adjacent regions and different levels of governance, respectively) are essential to overcome persistent information asymmetries. Asymmetries may arise between different authorities responsible for directing cluster development (Nishimura and Okamuro, 2011), and their extent depends on the degree of administrative centralization and the role of the state (Baier et al., 2013; Rodríguez-Pose and Bwire, 2004; Sternberg et al., 2010). Within institutionally decentralized countries where sub-national administrative levels have the authority and resources to customize cluster policies to the local context, there is more need for horizontal and vertical coordination than in countries with a clear, centralized, top-down governance structure. Without any coordination, regional efforts to develop clusters and cluster policy might, unintentionally, lead to regional cluster policies that are relatively similar and lack the necessary complementarity and coherence to become effective (Angeles Diez, 2001). Also, increased competitive pressures and overinvestment renders less competitive clusters obsolete (Hospers and Beugelsdijk, 2002), a typical example being the biotechnology cluster in Lombardy (Orsenigo, 2001). Consequently, understanding when and how clusters compete is essential for policy-makers to evaluate their efforts in policy design and implementation.

Revealed competition between cluster organizations: a framework

To conceptualize the extent to which cluster policies are coherently devised and cluster organizations might compete for attracting and maintaining the same (type of) business activity (i.e. firms), a framework is built to examine revealed competition between cluster organizations in the European life sciences sector. As previously argued, effective cluster policies are coordinated in such a way as to obtain goal congruence and to avoid excessive duplication of policy efforts at different spatial and administrative levels (Hospers and Beugelsdijk, 2002). Since cluster organizations are considered crucial intermediaries in regional policy-making and cluster development (Ketels et al., 2012), their characteristics and activities are perceptible reflections of cluster policies.

In line with the work of Burger et al. (2013), the basic premise of our conceptualization is to identify sources of similarity in the characteristics of cluster organizations within regions. This notion of competition reflects the idea of niche overlap, and it is omnipresent in the field of organization studies (Hannan and Freeman, 1977) and social network analysis (McPherson, 1983). Accordingly, the combined degree of overlap between the characteristics of cluster organizations reveals the extent to which these organizations are local complements or revealed competitors. Given the explicit local context of clusters and, correspondingly, cluster organizations, revealed competition exists inherently within regions (or across adjacent regions). Using this interplay between competition and complementarity of cluster organizations, it is argued that revealed competition can be identified across three different dimensions of overlap: (1) functional, (2) sectoral, and (3) funding. The higher the combined overlap in service offerings, sub-sectoral focus and funding sources respectively, the higher the level of revealed competition. For example, when two cluster organizations offer the exact same services to their customers, complete functional overlap exists, which implies that these organizations are true functional substitutes. Similarly, when two cluster organizations offer services but none of these services is offered by both, these cluster organizations are true functional complements. Hence, revealed competition is a basic composite measure to identify duplications in the characteristics and activities of cluster organizations.

However, it is important to note that a high degree of revealed competition combined with a high density of cluster organizations within a region does not immediately refer to adverse implications. Following Porter (1990), competition can also be beneficial as it ensures that cluster organizations stay focused on their customers, differentiate among rivals and, consequently, continue to evolve. Besides, some regions simply host larger life sciences sectors than others. Yet, it does reveal that the initial preconditions for uninformed cluster developments are present and, consequently, which regions deserve closer scrutiny and discussion at a case level.

Contextualization: the European life sciences sector

The focus on the life sciences is primarily motivated by the fact that it is one of the key industries of the emerging knowledge economy, exhibiting considerable potential for innovation, dynamism and future economic growth (Cooke, 2004). Given this context, Europe is an exceptionally valuable case because there exist large differences in the number and nature of cluster policies, local industrial and science bases and the presence of supporting institutions such as local financial and labour markets (Reiss et al., 2004). Furthermore, within Europe the life sciences is the sector with the highest density of cluster organizations per employee (Ketels and Protsiv, 2013), and cluster actors are known to particularly benefit from activities that are generally promoted or facilitated by cluster organizations (e.g. Moodysson, 2008; Powell et al., 2002). Unravelling the variety in service offerings of cluster organizations in this sector thus provides a unique opportunity to identify overlap in the functional dimension of these organizations’ activities. Accordingly, the degree of local functional substitutability of cluster organizations is defined by the degree of overlap in the different services they perform.

Obviously, the life sciences include a wide array of different but closely related sub-sectors. Based on the classification of industry sectors used by the European Cluster Observatory (ECO), the life sciences sector encompasses biotechnology, medical devices and pharmaceuticals. This broad sector definition is unavoidable because most clusters and cluster organizations are not pure representatives of a particular sub-sector, especially in the life sciences, where sub-sectors are highly related and interdependent (see Moodysson, 2008). However, each sub-sector does not only have its own characteristics in terms of market structure, competitive advantage, innovation capacity or focus, but also a varying need for support from cluster organizations or other actors involved in the cluster (see Ketels et al., 2012; Sternberg et al., 2010). Given that the sector classification of ECO does not contain enough detail to identify overlap in the sectoral dimension, each cluster organization needs to be closely examined at the sub-sector level to determine the exact sub-sectoral focus and hence the degree of sectoral substitutability.

Across Europe, government authorities at various administrative levels have long been involved in funding life science cluster development programmes (Cooke, 2004), with a primary focus on biotechnology and medical technology (Enright, 2003). Given this focus and the fact that the necessary local endowments and preconditions for building such clusters, including inter alia a (local) tacit and explicit knowledge base combined with entrepreneurial activity (Hospers et al., 2009), are not omnipresent across European regions, these (sub-)sectors are particularly susceptible to uninformed investment decisions by policy-makers. If these competing cluster organizations are subject to public funding and the coordinating efforts across administrative levels is low, the probability that these funds are not optimally allocated is most likely to increase in countries that are institutionally decentralized and where local governments have the authority to implement cluster policy portfolios. The identification of regional overlap in funding sources, observed in the context of regional autonomy and cluster policy-making, hence reveals a potential source of uninformed competition for (local) government support.

Overall, the life sciences represent the most likely sector in Europe to not only benefit from the activities provided by cluster organizations, but also to boost a disproportionate share of uninformed cluster development programmes.

Methodology and data

Sample selection of cluster organizations

The sample of cluster organizations was selected based on three main data sources. First, we extracted the cluster organizations present in the database offered by the Council for European Bioregions (CEBR). The CEBR defines the members of its platform as cluster organizations that support their local bio-community through direct services. Second, we retrieved the cluster organizations from the database maintained by the European Secretariat for Cluster Analysis (ESCA). The ESCA aims to offer an open platform to maintain a permanent policy dialogue at the European level among national and regional public authorities that are responsible for developing cluster policies. From their website, we extracted all cluster organizations involved in biotechnology, as well as the health and medical sciences. Finally, from the comprehensive database provided by the ECO, we added all cluster organizations that are present in the biotechnology, medical devices and pharmaceuticals sector to our sample.

Note that the ECO database is based on self-reported data and simply records the existence of a cluster organization. Consequently, the appearance of a cluster organization in the ECO database does not guarantee that this organization is currently in existence. In contrast, the CEBR and ESCA require formal membership and active participation by the cluster organizations and are therefore considered up-to-date. After accounting for duplicates, these three databases generated a total sample of 262 cluster organizations in the life sciences sector, located in 25 countries across Europe. 3 Likewise, it is very difficult to make a distinction between different types of facilitating organizations based on their formal status, such as science parks or cluster organizations. As such, we decided to include both types of organizations in our sample and allow the distinction to be based purely on the service offerings of these organizations as indicated in the survey.

Survey design and data collection

To examine the particular services that the cluster organizations in our sample provide, we conducted a survey consisting of a series of questions on the basic characteristics of the cluster organization and its service offerings to cluster firms and other actors within the cluster. Because we are interested in the life sciences sector across Europe, it was essential for us to avoid item non-response and to obtain survey results from cluster organizations located in as many countries possible. For the basic characteristics, straightforward open-ended and scaled questions were asked. To improve the response rate we also designed closed-ended questions with a dichotomous response format (i.e. yes/no questions) to survey the service offerings of cluster organizations. While this type of questioning facilitates quick and easy answers, it does sacrifice some content validity due to the limited number of questions. Furthermore, relative to open-ended questions, closed-ended questions facilitate easy inference and comparison of the findings across countries and regions, especially in the context of a large-scale survey.

The main focus of the survey concerns the services that cluster organizations offer to firms within the cluster. We subdivided these services into three different groups. First, cluster organizations were asked to indicate which promotional activities they perform. Second, a set of questions was asked about the extent to which cluster organizations facilitate cooperation between different actors within the cluster. The third set of questions related to financial services and included the offering of support with the acquisition of subsidies and capital. Finally, cluster organizations were asked to indicate whether they received any type of public funding or subsidies. If such funding was received, the respondents had to indicate whether the funding source represented an institution organized at the regional, national or European level. The data collection process took place in the period January to September 2013.

Survey response, response characteristics and response bias

The overall response rate was relatively high at 62.2%; however, another 61 organizations indicated that they were willing to participate in the survey but ultimately did not respond. From all cluster organizations that we contacted, only seven refused to participate. Furthermore, 31 organizations could not be reached by either telephone or email. The cause of this failure is difficult to determine, but these cluster organizations may no longer exist or could have been renamed or merged over time. The response rates are rather uniform between countries. Most of the variation stems from the response rate for countries, with a smaller number of organizations in the sample being naturally more sensitive to individual observations. The relative distribution of organizations across countries corresponds to our expectations based on the relative size of the regional life sciences sector within these countries. 4

A general problem with surveys of this type is response bias. Asking cluster organizations about their characteristics and activities may yield responses that are exaggerated. To validate the accuracy of the responses, the service offerings of all cluster organizations are cross-checked through web-based research – that is, retrieving information mainly from websites, policy reports and presentations. The results of the validation show that promotional and networking activities have matching rates of 90% and above. For financial support these figures are somewhat lower but still reasonable at 74% and 82% for support with acquisitions and capital respectively.

Empirical findings

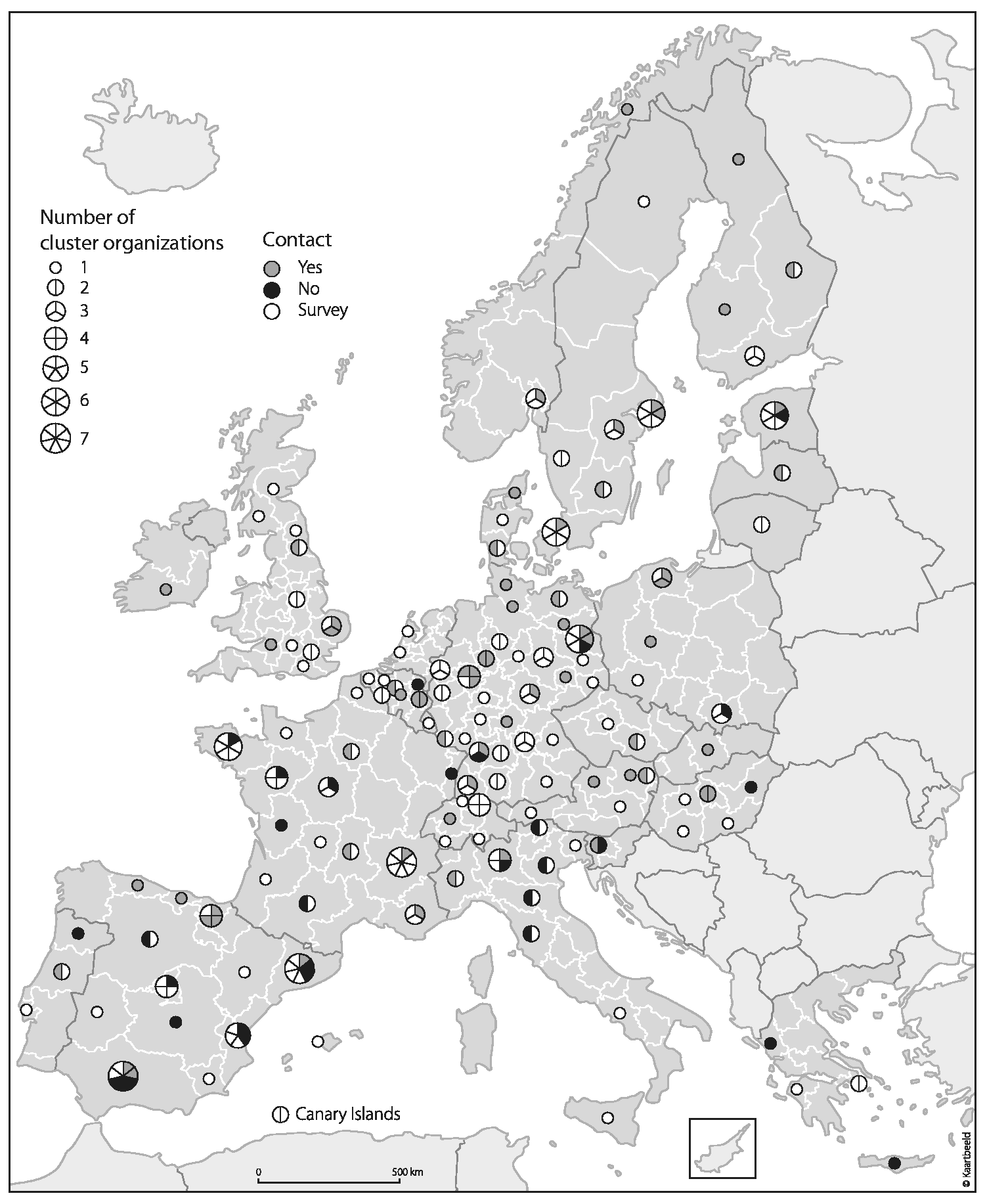

To provide an overview, Figure 1 shows the regional density of the 262 cluster organizations in the European life sciences sector that appear in the overall sample. To display and analyse the data, the NUTS-2 level is used, because this territorial unit represents the larger administrative region that is typically applied to define regional policy and to analyse regional issues (Vieira et al., 2011). The figure shows that nine regions display a relatively high density of cluster organizations of more than five cluster organizations per NUTS-2 region. These main regions include Tallinn/Tartu in Estonia; the capital city regions of Stockholm, Copenhagen and Berlin; Brittany and Rhône-Alpes in France; and Catalonia, Valencia and Andalusia in Spain. When observing the composition of the response characteristics of cluster organizations, there exists considerable regional variation. Of particular interest is the ‘No Contact’ group. That these cluster organizations are likely to have ceased operations signals a preliminary exhibition of relatively weak cluster competitiveness. The three regions that have more than one cluster organization in the ‘No Contact’ group are all located in Spain in Catalonia, Valencia and Andalusia.

The density and response characteristics of life science cluster organizations in European NUTS-2 regions.

To extend the assessment of cluster organizations within NUTS-2 regions, an additional measure of geographical proximity is used to examine whether there exist adjacent regions that host multiple cluster organizations. 5 Figure 1 shows that the German Länder Baden-Württemberg and Nordrhein-Westfalen host a relatively high density of cluster organizations in adjacent NUTS-2 regions. Note that some of the nine high-density regions are also neighbouring regions with a substantial amount of cluster organizations – for example, Catalonia and Valencia or Brittany and Pays de la Loire. Finally, it is important to note that cluster organizations across regions serve differently sized sectors. For instance, the Copenhagen area hosts the same amount of cluster organizations as Estonia, but the life sciences sector in Copenhagen is 17 times larger.

Functional overlap

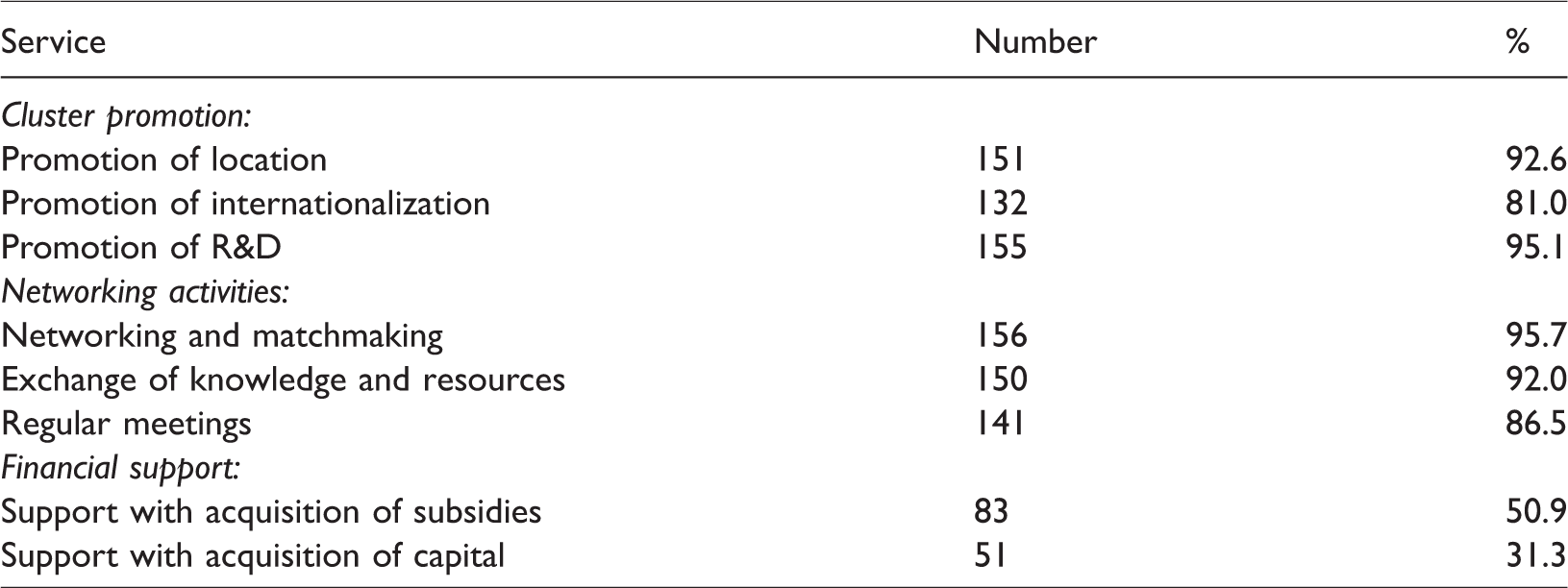

Following the sequence of our survey design, the results with regard to the service offerings provided by the cluster organizations in our sample are presented in Table 1. The service offerings can be divided into three broad categories covering promotional, networking and financial support activities, all with several sub-categories. The results make it instantly clear that cluster organizations in the European life sciences sector are relatively homogeneous with regard to cluster promotion and networking activities, as a large majority of the organizations within the survey offer these services. Given that these service offerings represent the minimal set of activities that one would expect a cluster organization to perform, the results are in line with our expectations.

Service offerings of cluster organizations.

In contrast, the survey results reveal substantial differences with respect to financial support activities. In particular, support through the acquisition of subsidies is only provided by 50.9% of the cluster organizations in the survey, while a mere 31.3% of the cluster organizations facilitate the acquisition of capital. Although previous research has identified that the provision of capital is among the most pervasive difficulties confronting firms located in clusters (Sölvell and Williams, 2013), this result implies that financing activities are often beyond the scope of the activities of a typical cluster organization (see Ketels et al., 2012). Furthermore, the relatively strong emphasis on providing financial support by acquiring subsidies rather than capital is indicative of the importance of public funding sources for clusters in general and cluster organizations in particular. However, providing help with subsidies and access to capital differs strongly between some countries. For instance, 80% of the cluster organizations in Spain provide help with obtaining subsidies, while this figure is only 20% in Sweden. In addition, cluster organizations in the UK are most active in supporting access to capital, which is not surprising given the local availability of well-developed capital markets and the presence of many (international) investors.

In addition, the survey response data reveal that the cluster organizations within regions with a high cluster density are relatively homogeneous in the services they offer. Some variation exists with respect to financial support activities, but even in this respect the cluster organizations are largely homogeneous. A notable exception is Estonia, where the cluster organizations are relative complements in terms of their service offerings, particularly when taking the regional division between the Tallinn health care cluster and the Tartu biotechnology cluster into account.

Sectoral overlap

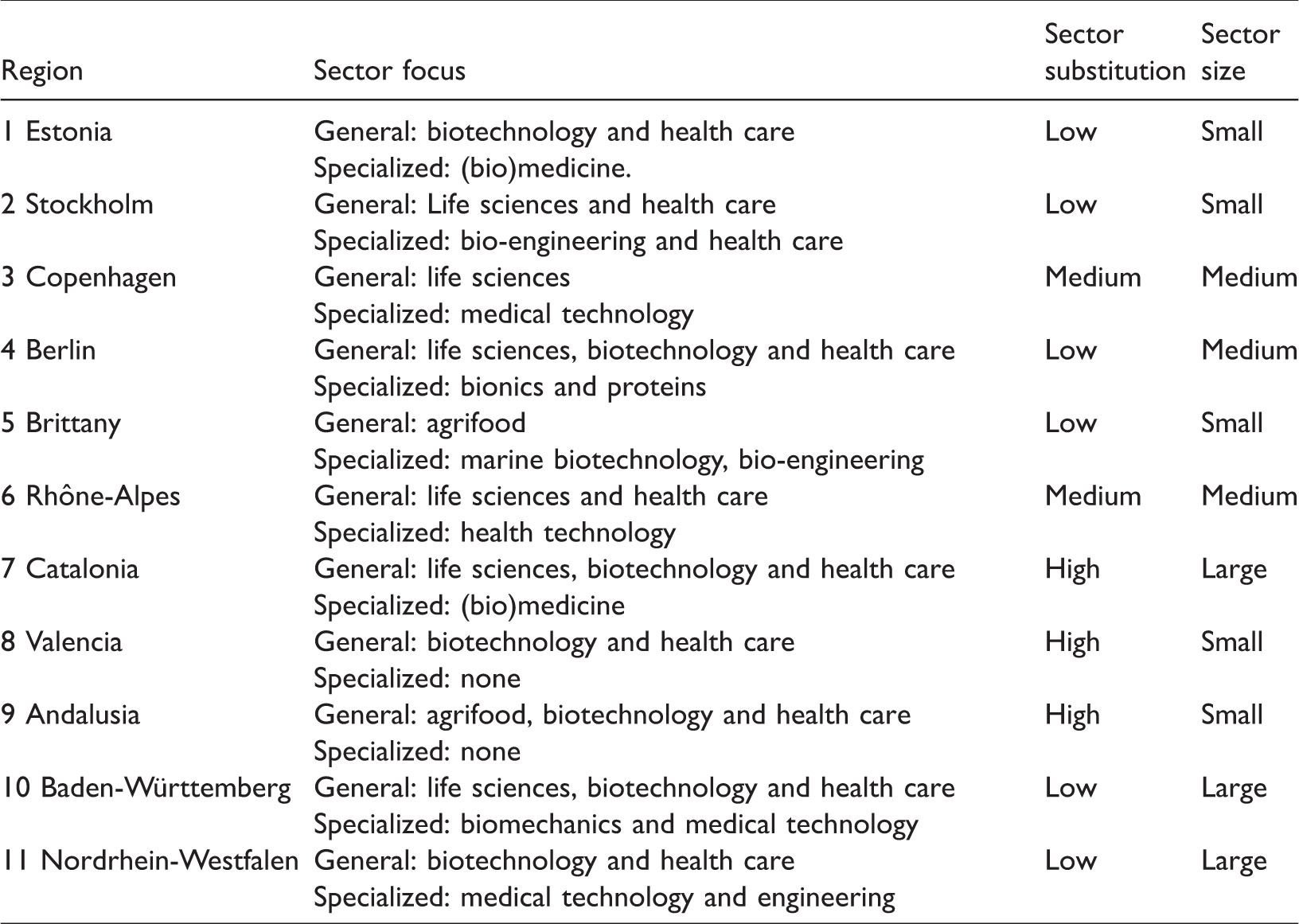

Regarding the sectoral focus, there are significant differences between the various regions with a high density of cluster organizations. An overview of the sectoral focus of each region with a high density of cluster organizations is presented in Table 2. 6 According to the characteristics of the cluster organizations, Estonia and the city regions of Stockholm and Berlin, Brittany and the German Länder Baden-Württemberg and Nordrhein-Westfalen all host cluster organizations that have relatively low substitution levels in terms of sub-sectoral focus, and they are thus predominantly complementary.

Sectoral substitutability and life science cluster–region typologies.

For instance, the Stockholm region features both cluster organizations and science parks that are highly specialized with respect to different sub-sectors, ranging from health care and bio-engineering in Stockholm to biotechnology in the Uppsala area (see Waxell and Malmberg, 2007). Moreover, cluster organizations in Germany are regionally specialized and coordinate well-developed, highly complementary (research) networks between universities and the private sector (Trippl and Otto, 2009). Government-instated regional competition for public funds stimulates a division of labour between cluster initiatives (Dohse, 2007), which already indicates regional complementarity. While the sectoral variety and the number of cluster organizations is high, it should be noted that the size of the life science sectors in Estonia, Stockholm and Brittany is relatively small. In contrast, the life sciences sectors in Baden-Württemberg and Nordrhein-Westfalen are large, even when considered at the NUTS-2 instead of Länder level. However, relative to sector size, these regions host few cluster organizations.

In contrast, the focal activities of the cluster organizations in Copenhagen and the Rhône-Alpes region are not necessarily distinct. In Copenhagen, the main activities of the cluster organizations in the sample are directed to life sciences in general, yet with a distinct regional, national or international focus. However, those cluster organizations in Copenhagen that differentiate in terms of spatial focus are functional substitutes in their (international) cluster promotion and network activities, which, in turn, increases their degree of revealed competition. Similarly, cluster organizations in the Rhône-Alpes region are either highly specialized (with only a limited life science focus), such as Plastipolis, or generally active in health care. Yet, the level of sectoral substitution in this region is best classified as medium, with a low differentiation of service offerings, making this region also susceptible to revealed competition. A useful addition to this discussion is Brittany, where several small cluster organizations with a high degree of functional and sectoral substitutability merged into a new cluster organization, Atlanpôle. By doing so, the overlap in cluster activities within the sector and region is substantially reduced.

Finally, the cluster organizations in the Spanish regions of Catalonia, Valencia and Andalusia typically represent science parks with a general life sciences focus. The homogeneity in the sectoral characteristics combined with a high overlap in the service offerings of the cluster organizations in these regions increase the degree of functional sectoral substitutability. Notwithstanding this result, the value and importance of the cluster organizations in Catalonia should not be underestimated as the region hosts one of the largest life sciences sectors across Europe. In contrast, the number of cluster organizations in Valencia and Andalusia is relatively high but the sizes of the life sciences sectors are very small. This makes the potential for revealed competition particularly high in these regions.

Overlap in funding sources

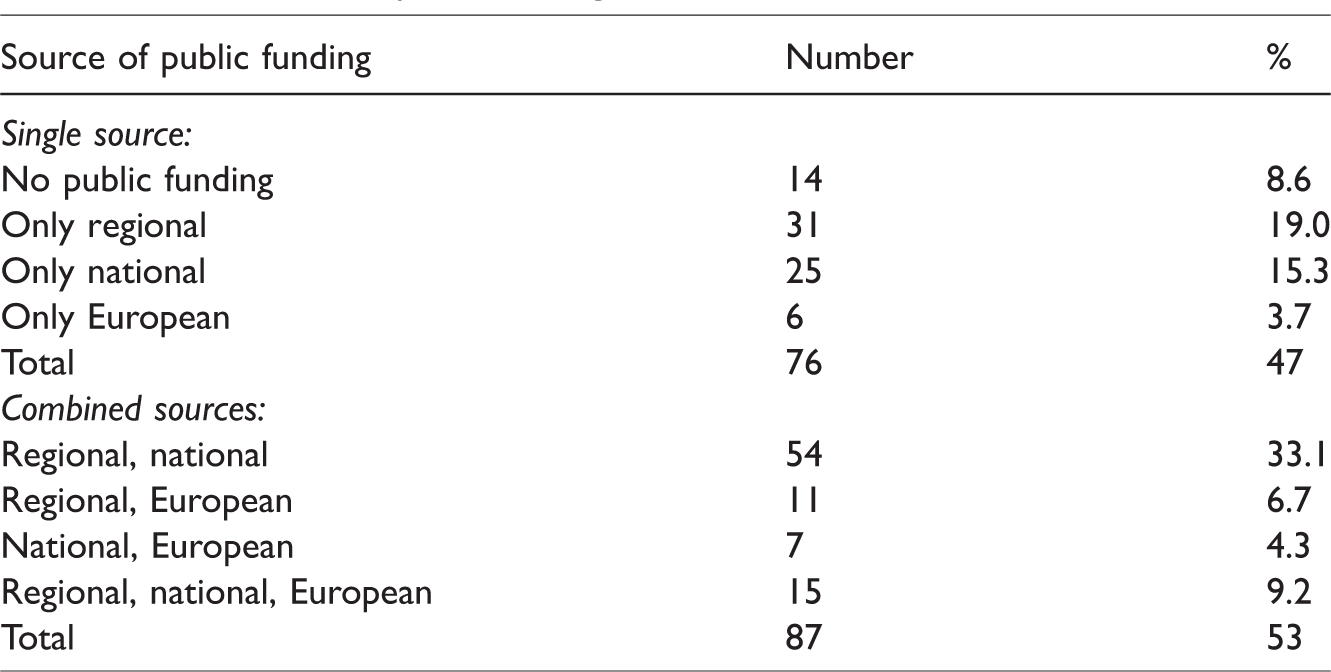

Next, we present the sources of public cluster funding in Table 3. The figures clearly reflect the central elements in the implementation of cluster development policies and the fact that financially supporting cluster organizations is popular. In particular, only 8.6% of the cluster organizations receive no funding from governmental or other public funding sources. All other cluster organizations receive at least partial funding from one or more public sources, often in addition to contributions from private sector actors (Ketels et al., 2012; Teigland and Lindqvist, 2007). Most public funding is provided by regional and national government-related sources, with 34.3% of the cluster organizations receiving either regional or national funding and 33.1% receiving both. Furthermore, 23.9% of the cluster organizations receive some form of European funding through one of the many EU platforms and initiatives for cluster development. Most of this European funding (20.2%) is received in combination with national or regional funding sources. There is no clear pattern to discern whether certain general or specialized (sub-)sectors are associated with specific funding sources.

Distribution of public funding sources.

Regarding organizational characteristics, cluster organizations that receive European funding are on average larger (in terms of number of employees) and were established more recently than cluster organizations that receive national or regional financial support. Also, note that the cluster organizations located in Western Europe that are partially funded by European government support are more actively involved in international cluster promotion and financial support activities and are also substantially more internationally oriented (Burger et al., 2015).

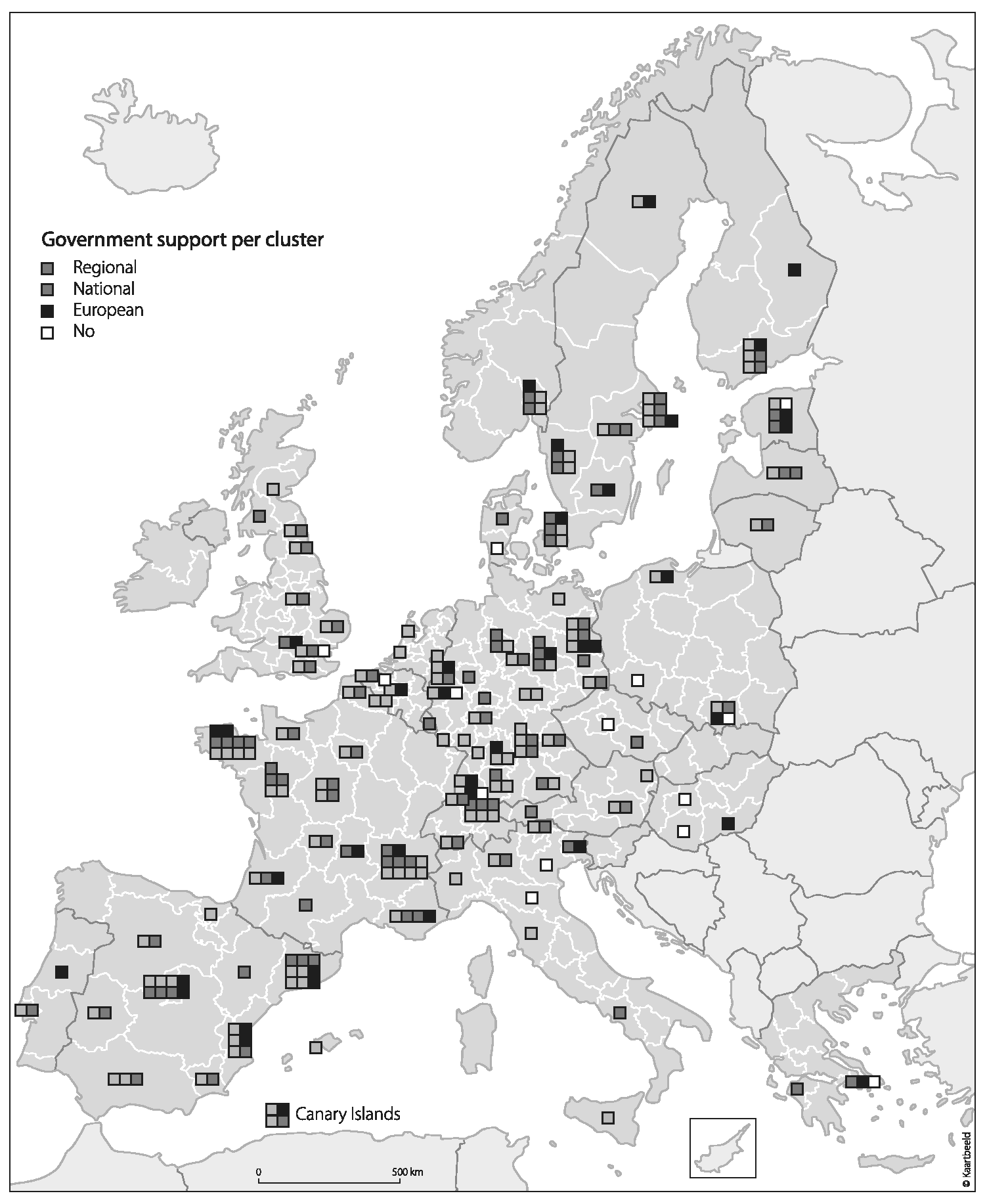

Although the above typology constitutes a certain amount of generalization, it allows us to conjecture that the probability of revealed competition between cluster organizations is higher in some regions than in others. Based on the survey data, Figure 2 displays the NUTS-2 regional variation in the government funding support of cluster organizations in Europe. Clearly, most cluster organizations receive local, national and/or supranational government support; however, some regional variation is revealed in Figure 2, of which the emphasis on national support in France and the widespread regional support in Spain are the most apparent. These findings are in line with the cluster development policies implemented at the national level (see OECD, 2006 for comprehensive discussions). In France, cluster policies are mainly coordinated at the national level and involve the regional allocation of national budgets to develop clusters. In contrast, cluster policies aimed at innovation and regional development in Spain are predominantly implemented at a decentralized regional level. A similar decentralized system was recently introduced in Denmark, although national governmental institutions still actively monitor and promote cooperation and innovative activity among different actors in the sector.

Government funding support of life science cluster organizations in European NUTS-2 regions.

One potential setback of such a decentralized system is that without cross-regional coordination, the risk of bandwagon effects increases considerably (Kiese, 2017; Nishimura and Okamuro, 2011). A typical example is provided by Todt et al. (2007), who, in studying the Valencia region, argue that a well-developed public research sector in biotechnology does not necessarily lead to a strong biotechnology sector. Hence, the existing cluster organizations in the region compete for limited business activity. Of course, this does not mean that a national cluster development policy is always successful or that a decentralized system only yields similar clusters that vie for the same resources. For instance, the Sophia Antipolis information technology and life sciences cluster in France is not necessarily a success and it has been criticized for its low level of embeddedness in the regional economy (Hospers and Beugelsdijk, 2002). On the contrary, the peripheral region of Andalusia successfully implements regional development policies to boost innovation in its traditional functional foods cluster based around Granada and Seville (Arias-Aranda and Romerosa-Martínez, 2010).

Discussion and conclusions

Based on the results of a unique survey among 163 cluster organizations, this study presents an initial comprehensive geographical examination of the heterogeneity of cluster organizations and their corresponding service offerings in the European life sciences sector. The primary objective of this study is to empirically derive those regions that host cluster organizations with a high degree of functional and sub-sectoral overlap, while at the same time receiving sources of public funding. In this way, we are able to identify European regions in which revealed competition between cluster organizations is high, potentially indicating bandwagon effects or overinvestments in specific economic activities. As the majority of cluster initiatives receive financial support from governmental authorities at different administrative levels, neglecting regional economic structures or bandwagon effects is not likely to be welfare-enhancing (Kiese, 2017) or, as previously argued by Storper (1995), even presents risks for the misallocation of public funds.

Our results suggest that the degree of revealed competition markedly differs across regions. In Copenhagen, Rhône-Alpes and the three Spanish regions of Catalonia, Valencia and Andalusia, cluster organizations display a relatively high degree of revealed competition. On the contrary, Estonia hosts relatively complementary cluster organizations in terms of sub-sectoral focus, but in this region relatively many publicly funded cluster organizations service only a small life sciences sector. Hence, it can also be questioned to what extent the cluster organizations in this region are all contributing to the development of the life sciences sector.

While the overlap in cluster activities and uninformed cluster policies can be prevented by establishing explicit coordination between the administrative levels responsible for cluster development policy and investment (Nishimura and Okamuro, 2011), only Rhône-Alpes and, to a lesser extent, the Copenhagen regions have such an alignment system. Spain exhibits a decentralized regional system of cluster development, which in the absence of coordination considerably increases cross-regional information asymmetries and hence the risk of bandwagon effects (see Angeles Diez, 2001; Rodríguez-Pose and Bwire, 2004). Because overinvestment makes cluster policies prone to fail, a lack of coordination may be a potential explanation for the relatively high degree of revealed competition in the three Spanish regions of our survey. Interestingly, while Germany also has relatively high regional autonomy concerning innovation policy (Baier et al., 2013), our findings do not indicate an increased risk of overinvestment. However, this does not mean that the simultaneous promotion of relatively similar clusters in the same (sub-)sector does not exist (Kiese and Hundt, 2014).

Our findings have important implications for policy-makers and cluster practitioners. Because more than 90% of the cluster organizations in our sample are at least partly supported through various types of government funding, it can be questioned whether competition between publicly funded cluster organizations induced by the geographical and functional overlap of activities is a preferred outcome. Regions that are known to host high-performing life sciences clusters, such as the Stockholm/Uppsala and Baden-Württemberg regions, boost well-coordinated and highly complementary cluster organizations that serve specific sub-sectors with a variety of service offerings. Hence, the coordination of cluster development policies across administrative levels can overcome information asymmetries and may create an effective division of labour between cluster organizations. As a result, the allocation of public funds becomes more effective and less arbitrary, while firms will face reduced coordination costs of working with cluster organizations that offer similar or overlapping services. Especially for decentralized regional systems such as those in Spain and, currently, Denmark, an overarching cluster development framework that functions on an aggregate administrative level can be an effective means to avoid the duplication of cluster organizations’ activities and hence more competitive cluster development projects. In addition, to facilitate the interregional or international embeddedness of clusters and their corresponding cluster organizations, national or even more explicit European-level coordination mechanisms may be valuable.

Although this study provides one of the first systematic attempts to compare cluster organizations, more research is needed to link the performance of clusters to cluster organizations’ operations. Since there are only a few outperforming clusters in the life sciences industry, a more qualitative research approach could address how cluster organizations in these well-functioning clusters contribute to the performance of these clusters and to what extent competition between proximate cluster organizations is harmful or beneficial for cluster performance. Such research can also be insightful to conduct for other sectors, particularly because considerable cross-sectoral heterogeneity in the activities of cluster organizations exists (Isaksen and Hauge, 2002; Ketels et al., 2012). A qualitative approach would also be helpful to develop a more fine-grained conceptual framework of revealed competition by studying the quality of the services that cluster organizations offer. Insightful questions that should be answered include: how do the quality of services play a role in the competition between cluster organizations, and when is competition desirable or should it be avoided?

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.