Abstract

This article investigates how distinct tiers of firms contribute to value creation and value capture in the automotive industry. We employ firm-level indicators to evaluate the value creation and capture of distinct supplier tiers in the Czech automotive industry, while considering differences between foreign-owned and domestic firms. Our analysis suggests that the economic effects of the automotive industry largely depend on its capital intensity and that mostly foreign-owned higher tier firms generate and capture greater value than lower tier firms, which include the vast majority of domestic suppliers.

Introduction

The contemporary automotive industry is typified by vertically integrated production networks organized by large lead assembly firms, in which the majority of components production is outsourced to independent suppliers (Sturgeon et al., 2008). Component suppliers are hierarchically organized into supplier tiers that differ by the complexity of manufactured components and also by other firm-level characteristics, such as firm size and the corporate power they wield in production networks (Humphrey and Memedovic, 2003; Pavlínek and Janák, 2007; Sturgeon and Lester, 2004).

In this article, we investigate how these distinct tiers of automotive firms contribute to value creation and value capture in the automotive industry by seeking answers to four questions. First, we ask whether higher tier firms create and capture a higher value than lower tier firms; second, whether higher tier firms possess stronger and more diverse competencies than lower tier firms; third, whether higher tier firms import a higher or lower share of inputs from abroad than lower tier firms; and fourth, whether domestic-owned (henceforth domestic) firms import lower shares of inputs than foreign-owned (henceforth foreign) firms (Frigant and Lung, 2002; Gereffi et al., 2005; Humphrey and Memedovic, 2003; Maxton and Wormald, 2004; Mudambi, 2008; Pavlínek, 2015; Pavlínek and Janák, 2007; Pavlínek and Žížalová, 2014; Sturgeon et al., 2008).

We investigate these relationships between the firm's position in global production networks (GPNs) and its prospects for value creation and capture in the context of the Czech automotive industry, which represents an example of an “integrated peripheral market” (Humphrey and Oeter, 2000). These are peripheral regions that have been integrated into core-based automotive industry production networks through large inflows of foreign direct investment (FDI) by foreign transnational corporations (TNCs). Automotive TNCs seek to benefit there from low production costs, investment incentives, and the advantages of regional economic blocs. The peripheral position of the Czech automotive industry in the European automotive industry is typified by its foreign control (82.4% of employment, 92.4% of value added, and 94.5% of turnover in 2011), which is also reflected in the limited presence of corporate headquarters and strategic higher value-added functions (Pavlínek and Ženka, 2011).

Our goal in this article is to develop an approach to measure value creation and capture in regional production networks based on firm-level indicators. We define value creation as firm-level activities that increase the value of final goods or services compared to the value of raw materials, intermediate goods, services, and other expenses employed for their production. We measure value creation at the firm level by value added in production and labor productivity. Value capture refers to the amount (or share) of created value that is retained by firms or subsidiaries that originally created it and that has not been transferred outside the host region of those firms or subsidiaries. As such, it is composed of two basic components: value captured by firms that created it and value that “leaks” from these firms to other subjects in the host region. We evaluate value capture through wages, tax revenues, reinvestment, and domestic sourcing. The measurements are done for different supplier tiers and for foreign and domestic suppliers in order to evaluate the contribution of different types of firms to value creation at the firm level and value capture at the firm and regional levels since we are interested in the contribution of the automotive industry to regional economic development. Our analysis confirms that higher tier firms have greater economic effects than lower tier firms because of the larger capital intensity of their production, higher corporate tax revenues, and also higher average wages per worker. However, lower tier firms have larger direct employment and wage effects per unit of production.

We begin with a brief discussion of value creation and capture in the contemporary economy. In the following section, we develop a firm-level approach to evaluate value creation and value capture in the context of the automotive industry. In “Hypotheses” section, we present five hypotheses about the distinct tiers of the automotive value chain that guide our empirical analysis of the Czech automotive industry. In the following section, we introduce the Czech automotive industry. Next, we analyze value creation and capture in the Czech automotive industry. Finally, we summarize the findings in the conclusion.

Value creation, value capture, and uneven economic development

The international spatial division of labor has been increasingly influenced by the investment activities of TNCs and their abilities to “slice up” the value chain and relocate its different functions to the potentially most profitable locations (Dicken, 2011; Gereffi, 2005). Economic geographers, among others, have been attempting to uncover where value is created and captured within GPNs in order to understand how GPNs contribute to economic development of particular countries and regions (Coe et al., 2004; Smith et al., 2002) and how flows and transfers of value contribute to uneven development (Hudson, 2011). It has been argued that in the contemporary economy the greatest value creation and capture come from the production of intangible goods rather than from the production of tangible goods and standardized services. Both upstream and downstream knowledge-intensive activities along the value chain, such as R&D on one side and brand management, marketing, advertising, distribution, and after-sales service on the other side, create and capture significantly greater value than manufacturing operations (Mudambi, 2008). Lead firms typically control the production of intangible goods and thus secure higher profits through creating high entry barriers into these activities (Shin et al., 2013). Empirical evidence was found in the electronics industry that brand owners, who are almost invariably large core-based TNCs, capture the majority of value that is created along a particular value chain, while firms that manufacture final products capture a much lower share (Shin et al., 2012).

The automotive industry represents an example of increasingly complex transnational production networks and value chains (Sturgeon et al., 2008). While it differs from the electronics industry in that lead (assembly) firms have not outsourced the final vehicle assembly to subcontractors or contract manufacturers, external suppliers have increased their share of the total value of finished vehicles to 75–80% (Frigant, 2011a). This does not mean, however, that external suppliers also capture the same share of the created value in the value chain. Lead firms along with leading component suppliers have been increasingly shifting production to lower cost “emerging” economies while maintaining crucial knowledge-intensive and high value-added activities in their home countries (Pavlínek, 2012; Sturgeon et al., 2008; Sturgeon and Van Biesebroeck, 2011). Since automotive production networks are no longer predominantly organized at the national scale (Dicken, 2011; Hudson and Schamp, 1995), the international flows of value within the automotive industry have increased rapidly in the form trade, FDI, and profit shifting strategies.

The spatial distribution of economic activities with different value creation and capture potential has important regional development implications. Economic geographers and economists have demonstrated that higher value-added knowledge-intensive activities and corporate control functions tend to concentrate in more developed core regions while lower value-added production activities tend to concentrate in less developed peripheral regions (Dicken, 2011; Hymer, 1972; Massey, 1979). This spatial division of labor is closely related to the patterns of corporate ownership and control (Dicken, 1976; Firn, 1975; Schackmann-Fallis, 1989). In the context of manufacturing, it means that peripheral externally controlled branch plants typically specialize in the high-volume manufacturing while having very limited nonproduction functions. Such truncated branch plants have limited regional development benefits for their host regions and, in the long run, might contribute to technological underdevelopment of host economies (Britton, 1980; Hayter, 1982). In the automotive industry, this continues to be the case despite its reorganization of production and supplier relations in the 1980s and 1990s (Sheard, 1983; Womack et al., 1990), which allowed some peripheral branch plants to acquire nonproduction functions and upgrade into “performance/networked branch plants” (Amin et al., 1994; Dawley, 2011; Phelps, 1993; Pike, 1998). Although branch plants and firms based in peripheral regions might develop various competencies over time (Phelps, 1993), functional upgrading resulting in a significantly improved position of such firms in the automotive industry value chain has been extremely difficult to achieve (Pavlínek and Ženka, 2011; Pavlínek and Žížalová, 2014). Therefore, especially domestic automotive suppliers based in peripheral regions and countries have been increasingly relegated to the bottom of the supplier hierarchy, which translates in the production of simple, low value-added, standardized and slow changing components (Barnes and Kaplinsky, 2000; Humphrey, 2003; Humphrey et al., 2000). Overall, the prevailing spatial division of labor in the automotive industry suggests that peripheral regions, both at the national and international scale, are typified by lower value creation within global value chains (GVCs) and GPNs than core regions. Furthermore, external control contributes to a potential value transfer from peripheral branch plants to corporate headquarters in the form of various profit shifting strategies, including profit remittances and transfer pricing (Dischinger et al., 2014a, 2014b).

Value creation and value capture in GPNs

The precise measuring of value creation and capture in GPNs has proven to be extremely difficult because it requires access to the internal accounting data of individual firms, such as invoice-level internal data (Seppälä et al., 2014). Firms are generally unwilling to provide this information and even if they do, this level of detail would likely limit the analysis to a single product produced by a single TNC. Because of the unavailability of precise data, analyses of value creation and capture in GPNs of particular products in electronic industries, such as Apple's iPods, notebook computers, and smartphones, had to rely on rough estimates (Dedrick et al., 2010, 2011). It would be difficult to apply these approaches in the context of complex production networks with thousands of suppliers, such as the automotive industry, unless we focus on only a few of the most important suppliers. Alternatively, econometric methods have been used to measure value capture at the national level using firm-level financial data in the electronic industry (Shin et al., 2013). In this article, we develop an alternative way to measure value creation and capture in regional production networks based on firm-level indicators.

In the GPN perspective, created value refers to various forms of economic rent (Coe et al., 2004), which is conceptualized as the super profit of an entrepreneur who is able to exploit either resources of above average productivity or ubiquitous resources more effectively than his or her competitors (Kaplinsky, 1998), while preventing them from exploiting these resources by creating high barriers of entry (Kaplinsky and Morris, 2008). Profits therefore represent a plausible way to measure value creation (Coe et al., 2004; Henderson et al., 2002; Kaplinsky, 2000). 1 However, profits are highly volatile as they are affected by various investment projects, corporate tax reliefs, profit repatriations, transfer pricing, and other profit shifting strategies (Dischinger et al., 2014b). Profits can be reinvested in production in order to upgrade a firm's or subsidiary's production processes, which might increase its overall productivity, wages, and corporate tax revenues in the long run. The (geographical) distribution of profits along the hierarchical value chain (Gereffi et al., 2005) does not necessarily correspond with the distribution of value added. Through transfer pricing, TNCs can allocate the largest share of their profits to subsidiaries with simple low value-added assembly, while subsidiaries with high value-added production may show a negligible or even negative profitability (Seppälä et al., 2014). Therefore, from the perspective of regional development, created value needs to be understood more broadly and should not be limited to profits. In addition to profits, created value is also reflected in technological and organizational innovations, effective collaboration with local suppliers, knowledge spillovers, agglomeration economies, and the local presence of strategic high value-added functions. Different automotive firms are linked through complex supplier relationships and flows of information within automotive production networks that encourage the spatial proximity of certain automotive suppliers to assembly operations (Frigant and Lung, 2002; Larsson, 2002). The need for proximity and the resulting savings that accrue to individual suppliers lead to their clustering around assembly plants (Pavlínek and Janák, 2007; Sturgeon et al., 2008). Therefore, the value creation and capture of individual firms might be affected by the fact of whether or not they are located within such clusters. For the purpose of this study, we therefore consider not only value created in an individual automotive firm, but also estimates of value creation and capture in the network of the firm's regional suppliers, which are induced by domestic sourcing, knowledge spillovers, and other mechanisms.

Since there is no simple and established way to measure value creation, we employ the gross value added (GVA) as the best available accounting indicator for quantifying the abstract and directly nonmeasurable category of created value. GVA includes not only pretax profits that are highly volatile, difficult to trace and interpret, but it also measures wages and the consumption of fixed capital. As such, it is a more complex, territorially bounded, and stable indicator than profits that can be more easily interpreted. GVA per employee (labor productivity) is a key indicator of economic upgrading (Milberg and Winkler, 2011) in terms of productivity and profitability.

What is the difference between value added and created value? The conceptualization of value inspired by the resource-based theory (Peteraf, 1993) distinguishes between the perceived use value and exchange value. The former refers to specific qualities of the product (component, material, machine, service, etc.) as subjectively perceived by customers and the price he or she is prepared to pay for it (Bowman and Ambrosini, 2000). The latter is the actual price paid by the buyer for this perceived use value. Therefore, value creation represents the accumulation, transformation, and appropriation of valuable resources (machines, materials, components, know-how, technologies, licenses, management practices, etc.) that increase the perceived use value of a firm's products. When these products are sold, perceived use value is transformed into (exchange) value added (Bowman and Ambrosini, 2000).

From a host region perspective, captured value is a part of value created by the resident firm or subsidiary that is retained and appropriated for host region benefits (Coe et al., 2004). Regional captured value is composed of two parts. First is value captured for the benefits of the resident firm or subsidiary, which is the share of profits that a firm invests in its upgrading in order to maintain or increase its competitiveness (Szalavetz, 2015). It has multiple forms, such as reinvested profits, employee skills, collaborative relationships with local suppliers, technological innovation, and all other sources of economic rents that are retained by the resident firm or subsidiary and are not transferred to other regions. Second is value that “leaks” to other subjects in the host region, such as households, suppliers, and universities, through various channels, including employee compensation, corporate taxes, regional sourcing, or localized knowledge spillovers. Value is captured at various geographic scales. Profits reinvested into the establishment of a new plant or the expansion and upgrading of an existing plant affect the factory site at the local scale; jobs and wages affect the labor market at the regional scale through labor commute; corporate taxes are collected at the national scale; and domestic sourcing affects value capture at various scales from local to national, depending on the sourcing patterns of individual firms. Therefore, if we subtract this captured value from the total created value, we get the amount of “lost” value, which is transferred outside the region through various mechanisms, such as profit repatriation, transfer pricing, and the transfer of a subsidiary's perceived used value and its commercialization by the parent company (Barrientos et al., 2011; Milberg and Winkler, 2011; Pavlínek and Ženka, 2011).

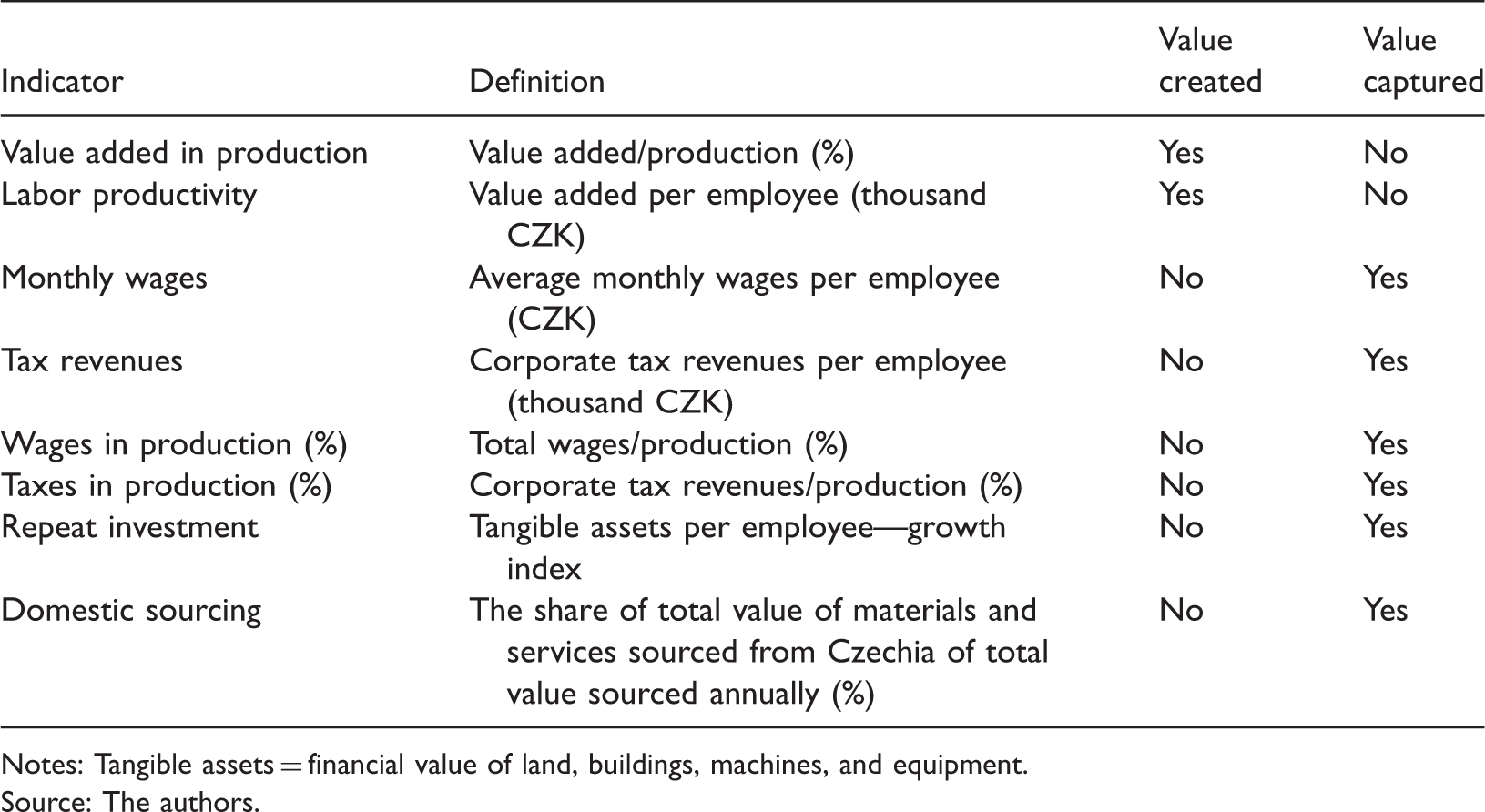

Firm-level indicators for measuring value creation and value capture.

Notes: Tangible assets = financial value of land, buildings, machines, and equipment.

Source: The authors.

Wages

A monopoly position that is derived mostly from technological or branding innovations generates an excess rent (Kaplinsky, 1998). In an integrated monopoly firm, the excess rent is likely to translate into higher wages for all workers, including unskilled workers who are employed in routine low value-added activities (Nathan and Sarkar, 2011). When routine low-value added and easily replaceable activities are outsourced to external suppliers, there is no excess rent and wages tend to be lower for workers in supplier firms that take on outsourced activities (Nathan and Sarkar, 2011). Therefore, if we were to control for size, industry, and regional specifics, we would expect the corporate power and the presence or absence of strategic nonproduction functions to be key factors that influence wage levels at the firm level in the context of a particular economy. Lower tier firms that are engaged in routine low-value added activities with low entry barriers have generally the lowest wages and worst prospects for wage increases (Ženka and Pavlínek, 2013).

Profits and corporate tax revenues

Profits generated in the host economy can be reinvested or used to pay for corporate income taxes there or can be repatriated and invested abroad (UNCTAD, 2013). Reinvestment and corporate taxes contribute to value capture in the host economy while profit repatriation transfers the value abroad. The share of repatriated profits is affected by the nature of the activities conducted by foreign firms in host economies and by the position of foreign subsidiaries in the corporate hierarchy. The value is also transferred from host economies by TNCs through various profit shifting strategies, including transfer pricing (Dicken, 2011; Dunning and Lundan, 2008; Huizinga and Laeven, 2008). Overall, approximately 60% of global FDI income on equity was transferred back to home countries of foreign investors in 2010 (UNCTAD, 2013). Regions that host corporate headquarters tend to capture a higher share of value than those hosting subsidiaries because corporate headquarters concentrate on the production of intangible goods. As such, they tend to be more profitable than their subsidiaries and tend to pay higher taxes (Dischinger et al., 2014a, 2014b; Mudambi, 2008). The headquarters and their geographic vicinity also benefit from high expenditures of gross profits on high value-added functions, such as R&D and corporate support functions, including strategic planning, marketing, management, and administration (Dedrick et al., 2011; Pavlínek, 2012). Overall, countries and regions benefit significantly more from hosting TNC headquarters than subsidiaries that have similar firm characteristics (Dischinger et al., 2014a).

Reinvested profits can increase value capture in host regions in a number of ways. For example, the investment in a more advanced technology should translate into higher marginal labor productivity and higher wages (Szalavetz, 2005). Repeat investments can also enhance ties of foreign-owned plants to particular regional economies and extend the survival time durations of foreign-owned plants in host regions (Wren and Jones, 2009). We measure reinvested profits indirectly through the annual change in tangible assets, which includes repeated investment into buildings, machines and equipment, and also their depreciation. We use tangible assets as a proxy measure of reinvested profits due to their spatial fixity and despite the fact that reinvested profits are only partially reflected in the annual change in tangible assets. The annual change in tangible assets represents a part of value captured in the host region, while the depreciation of tangible assets represents value that is sunk and, therefore, lost both for the region and for the firm (Melachroinos and Spence, 1999). In addition to tangible assets, reinvested profits may also flow into the employee training, licenses, software, and other intangibles.

To the best of our knowledge, there is no coherent theoretical framework linking the position of firms within GPNs with the amount of value captured through corporate tax revenues. There is no systematic evidence that higher tier firms are more prone to profit shifting and tax avoidance than lower tier firms. Therefore, we assume that the distribution of corporate tax revenues along the value chain follows the distribution of profits. Highly profitable assemblers and Tier 1 suppliers should pay higher taxes per employee than lower tier firms. At the same time, we assume that foreign firms are more likely to engage in profit shifting and tax avoidance strategies than domestic firms. The concentration of domestic firms among Tier 2 and Tier 3 suppliers should therefore translate into their higher relative corporate tax revenues as a share of total production than among higher tier firms.

Domestic sourcing

We consider the extent of domestic sourcing a measure of value capture for two basic reasons (Table 1). First, domestic procurement stimulates job creation among local suppliers and linkages between foreign and domestic firms that might help facilitate spillovers and knowledge transfer from foreign to domestic firms (Blomström and Kokko, 1998; Görg and Strobl, 2005; Pavlínek and Žížalová, 2014; Santangelo, 2009; Scott-Kennel, 2007; UNCTAD, 2001). Second, increased production by domestic suppliers improves their internal scale economies, while the spatial concentration of suppliers in the proximity of assembly plants can contribute to the development of external scale (localization) economies (Frigant and Lung, 2002; Larsson, 2002). In the contemporary automotive industry, spatial proximity to assembly operations is especially important for module and Tier 1 suppliers that produce modules and components dedicated to a particular automaker and supply them sequentially just in time (JIT) (Frigant and Lung, 2002; Klier and Rubenstein, 2008). The geographic proximity of Tier 1 suppliers to assembly operations decreases transportation and logistical costs, allows for the better synchronization of their production, improves the ability of Tier 1 suppliers to quickly react to changes in the production scheduling of assemblers, increases the reliability of JIT delivery, and speeds up the delivery of technical assistance by Tier 1 suppliers to assembly firms (Frigant and Lung, 2002; Larsson, 2002; Pavlínek and Janák, 2007). A large volume vehicle assembly should therefore translate in a high share of preassembled modules and dedicated components being sourced by assembly firms from the host economy in which the assembly plant is located.

Tier 1 suppliers supply preassembled highly customized modules that are often color and model specific in the JIT regime to a particular automaker. We expect Tier 1 suppliers to import more components from abroad than vehicle assemblers. This is because high value-added and sophisticated components for Tier 1 suppliers may not be available from domestic firms and standardized, nondedicated and simple components supplied by Tier 3 to Tier 1 suppliers can be supplied from larger distances. The sourcing patterns of simple components are therefore more affected by scale economies and labor costs than geographic proximity. Tier 2 suppliers should be positioned somewhere between Tier 1 and Tier 3 suppliers (see Pavlínek and Žížalová, 2014). At the same time, the globalization of the supplier base (Sturgeon and Lester, 2004) has relegated the majority of domestic suppliers to the supply of simple, low value-added components in less developed economies (Barnes and Kaplinsky, 2000; Humphrey, 2000; Humphrey et al., 2000). As a result, domestic suppliers may lack capabilities to supply certain specialized or sophisticated components or are uncompetitive because of their small scale of production, which necessitates the import of such components from abroad (Crone and Watts, 2003; Pavlínek and Žížalová, 2014, 2009–2011 interviews).

However, the position of firms in GPNs has to be controlled for contingent characteristics that may affect the relationship between the tier and the extent of local sourcing, such as plant size and its age, the mode of entry of foreign firms, the firm's nationality, and its corporate sourcing strategies (Barkley and McNamara, 1994; Crone and Watts, 2003; Tavares and Young, 2006). Larger plants tend to source domestically relatively less than smaller ones because it is often difficult to find local suppliers capable of supplying the large volumes required. In those cases when assembly firms and Tier 1 suppliers are significantly larger than Tier 2 and 3 suppliers, the plant size may negatively affect their level of domestic sourcing. The linkages and sourcing relationships between foreign and domestic firms typically develop over time (Dicken, 2011). Older plants and plants acquired by TNCs show a generally higher propensity to source domestically than more recently established greenfield factories (Tavares and Young, 2006). However, local content requirements and follow sourcing often result in high levels of local content as the outcome of the localization of foreign-owned suppliers around new greenfield assembly plants, which do not have to translate in extensive supplier linkages between foreign firms and domestic suppliers (Pavlínek et al., 2009).

Hypotheses

Based on the discussion of the literature, we present five hypotheses about different tiers and firm ownership of the automotive value chain that we will test on the Czech automotive industry. First, higher tier firms create higher value than lower tier firms and, therefore, they gradually increase their share of the total value added in the automotive industry. This is because higher tier firms produce more complex and higher value-added components than lower tier firms (Humphrey and Memedovic, 2003; Maxton and Wormald, 2004; Pavlínek and Janák, 2007). Together with assemblers, they wield greater corporate power in automotive value chains, which they use to maintain their privileged position and to squeeze lower tier firms (Pavlínek, 2015; Ravenhill, 2014; Sturgeon et al., 2008). Second, domestic suppliers import a lower share of inputs from abroad than foreign suppliers because foreign suppliers are more affected by the centralized sourcing strategies of TNCs (Pavlínek and Žížalová, 2014). Third, higher tier firms and assemblers import a lower share of inputs from abroad than lower tier firms because they are forced to source greater shares of their inputs locally in order to satisfy the imperatives of modular and JIT production (Frigant and Lung, 2002; Pavlínek and Janák, 2007). Fourth, higher tier firms possess stronger and more diverse competencies that are reflected in the presence of more nonproduction (strategic) higher value added functions than in lower tier firms. Lower tier firms produce simple components and are often captive suppliers that depend on higher tier buyers for various nonproduction functions (Gereffi et al., 2005; Pavlínek and Žížalová, 2014). Fifth, higher tier firms capture a greater share of created value than lower tier firms because they conduct more nonproduction higher value-added functions (Mudambi, 2008) and because they are able to offer higher wages than lower tier firms in order to attract skilled labor. This is because jobs in nonproduction functions create greater value and tend to be better paid than production jobs. Furthermore, the presence of nonproduction functions increases the chances for the reinvestment of profits in a particular locality. Better paid jobs and increased chances for reinvestment have potentially important implications for regional and national economies.

The Czech automotive industry

Before turning to the empirical analysis, we first need to provide a brief context of the Czech automotive industry. Since the early 1990s, the Czech automotive industry has been integrated in the European production networks through large inflows of FDI (CNB, 2015). Czechia had the largest automotive FDI stock (€10.1bn) and largest per capita FDI in the automotive industry (€963) in East-Central Europe (ECE) in 2012. 2 Large FDI inflows resulted in rapid increase in production from 197,000 vehicles in 1991 to 1.25 million in 2014 (AIA, 2015; OICA, 2015).

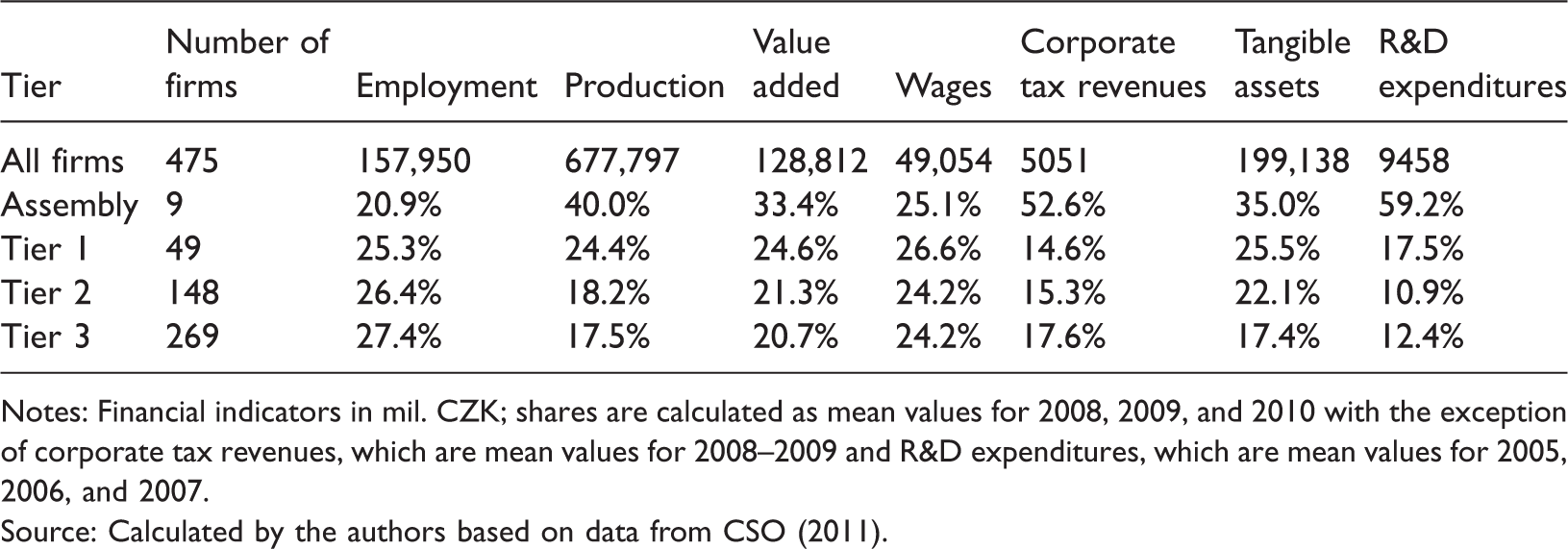

Shares of individual supplier tiers on selected indicators of the total Czech automotive industry in 2008–2010.

Notes: Financial indicators in mil. CZK; shares are calculated as mean values for 2008, 2009, and 2010 with the exception of corporate tax revenues, which are mean values for 2008–2009 and R&D expenditures, which are mean values for 2005, 2006, and 2007.

Source: Calculated by the authors based on data from CSO (2011).

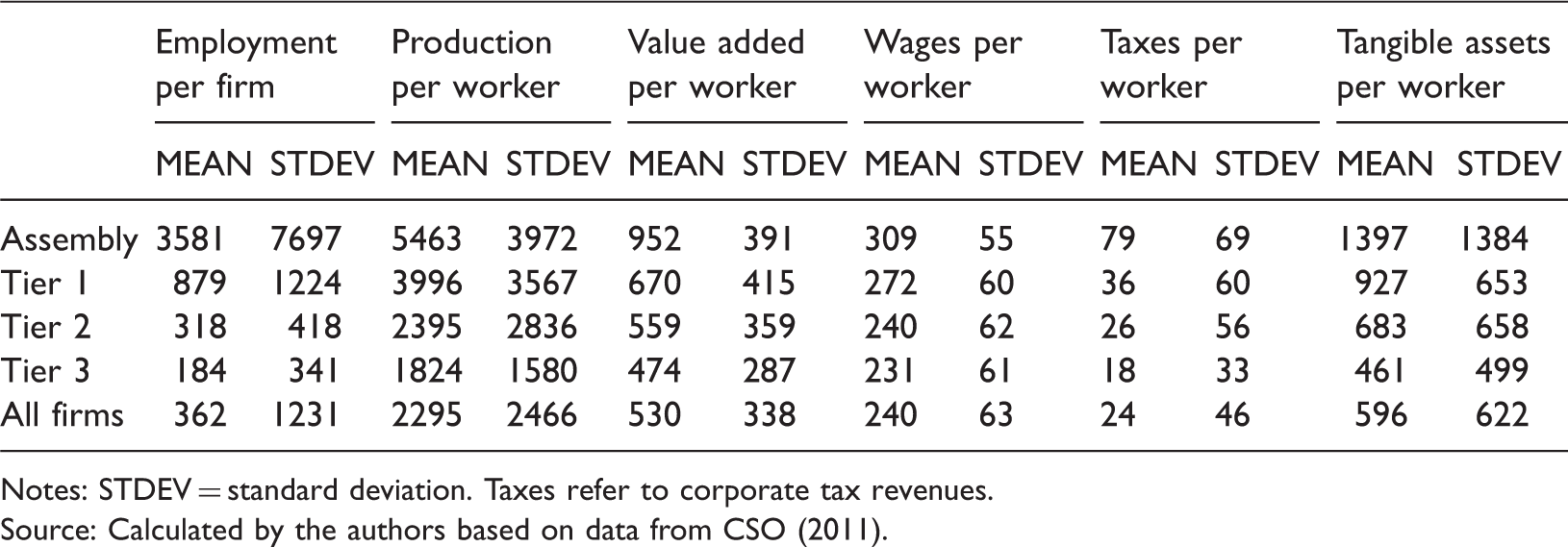

Descriptive statistics for different tiers of Czech-based automotive firms (mean values for 2006, 2007, and 2008) (value creation and value capture).

Notes: STDEV = standard deviation. Taxes refer to corporate tax revenues.

Source: Calculated by the authors based on data from CSO (2011).

Value creation and value capture in the Czech automotive industry

Our analysis of value creation and value capture in the Czech automotive industry draws on a unique 2011 dataset of 475 Czech-based automotive firms with 20 or more employees that was constructed by the authors from the data provided by the Czech Statistical Office (CSO, 2011). In addition to narrowly defined automotive industry firms (NACE 29), the database includes employment and financial indicators for firms in related supplier sectors, such as iron and steel, rubber and plastic, electronics and machinery industries, for 1998, 2002, and 2005–2011. Additional data, such as the share of automotive products in sales, sourcing patterns, and high value-added functions conducted at the firm level, were collected through a 2009 telephonic survey of 475 firms in our database, which was administered by the authors and yielded a response rate of 34.6% (274 firms). Finally, the interpretation of data analysis benefited from 100 firm-level interviews with the directors and top managers of Czech-based automotive firms conducted by the authors between 2009 and 2011.

Individual firms were classified into five categories according to the share of automotive products in their sales (0–24.9, 25.0–49.9, 50.0–74.9, 75.0–99.9, and 100%). The data for every firm were then weighted by a corresponding weight (0.125, 0.375, 0.625, 0.875, and 1) in order to reduce distortions resulting from the inclusion of firms that are only partially engaged in the automotive industry. In the next step, we classified all 475 firms according to their position in the automotive value chain into lead firms (assemblers) and three supplier tiers according to the technological complexity of their components (Humphrey and Memedovic, 2003; Maxton and Wormald, 2004; Pavlínek and Janák, 2007; Pavlínek et al., 2009; Veloso and Kumar, 2002). 3 Tier 1 suppliers supply the most complex components, such as sophisticated parts of engines (compressors, turbochargers), transmissions and brakes, and complex preassembled modules, such as dashboards, door systems, or seats. Tier 3 suppliers produce the least complex parts and components, such as car bodies and their parts, metal and plastic pressings, exhaust pipes, windscreen wipers, and simple interior parts, such as seat upholstery. We are including weighted data for raw materials suppliers among Tier 3 suppliers. Tier 2 suppliers produce the rest, i.e. medium complex parts, such as simple engine parts, lights, or locks. We are aware that large suppliers, such as Bosch, for example, supply various components that differ in terms of their sophistication. As such, these suppliers may play different roles in the value chain as Tier 1, 2, and 3 suppliers or as system integrators (Frigant, 2011b; Pries, 1999). In those cases, we have classified individual suppliers as a whole based on the highest tier into which at least some of their components would fall since we were unable to determine what proportion of supplier activity falls under different tiers. These three levels of the complexity of components are related to their value added. Generally, we assume that the production of the most complex and sophisticated components adds more value than the production of simple parts and components.

Value creation in the Czech automotive industry

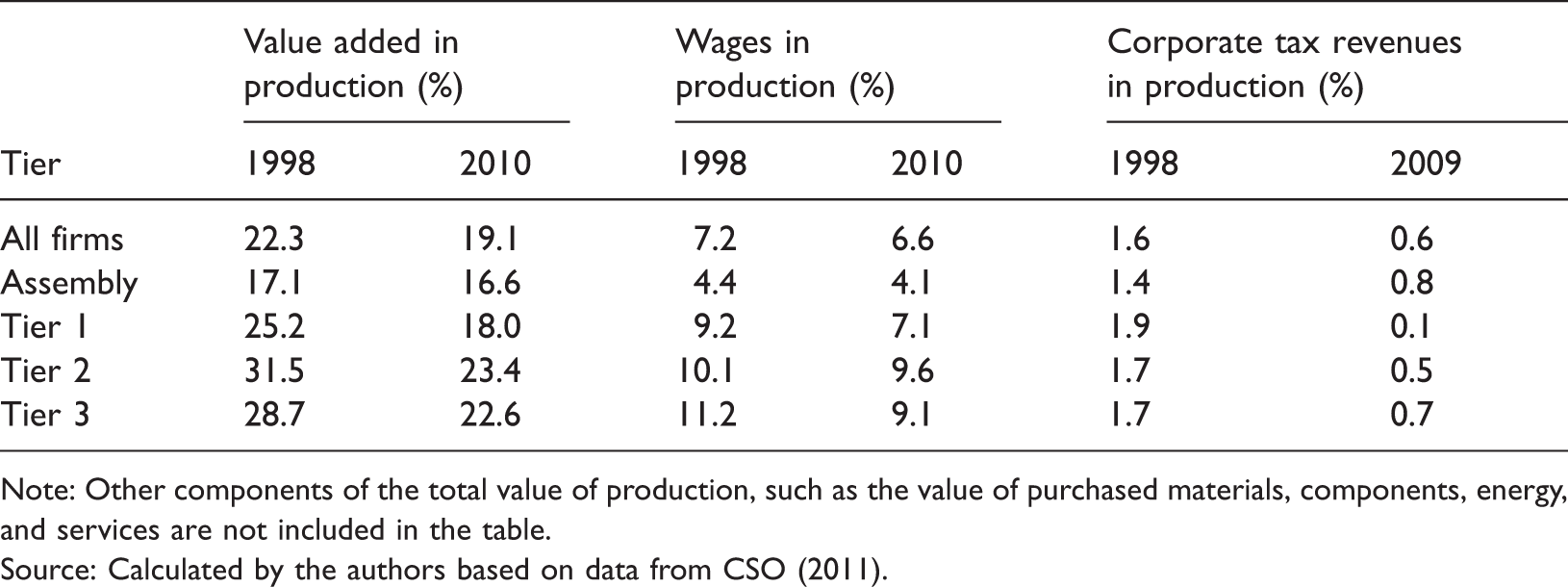

Change in the share of value added (value creation), wages, and corporate tax revenues (value capture) of the total value of production by supplier tier.

Note: Other components of the total value of production, such as the value of purchased materials, components, energy, and services are not included in the table.

Source: Calculated by the authors based on data from CSO (2011).

The stronger economic performance of assemblers and Tier 1 suppliers compared to the rest of the automotive industry supports the theoretical assumptions of GVC/GPN literature that link their “super profits” in terms of economic rent to strategic functions and privileged position in value chains (e.g. Kaplinsky, 1998). Empirical studies have also illustrated how assemblers and the so-called mega-suppliers wield their corporate power and exercise control over strategic functions within automotive production networks, which effectively discourages lower tier suppliers from functional upgrading (e.g. Pavlínek and Ženka, 2011; Rutherford and Holmes, 2008). They also squeeze lower tier suppliers often to the brink of bankruptcy, especially during economic crises, in order to maximize their own profits (Pavlínek, 2015; Pavlínek and Ženka, 2010). This was reflected in a very uneven decrease in the profitability in the Czech automotive industry during the economic crisis in 2008 as it fell on average by 19% for assemblers, 59% for Tier 1 suppliers, 73% for Tier 2 suppliers, and by 71% for Tier 3 suppliers (Pavlínek, 2015).

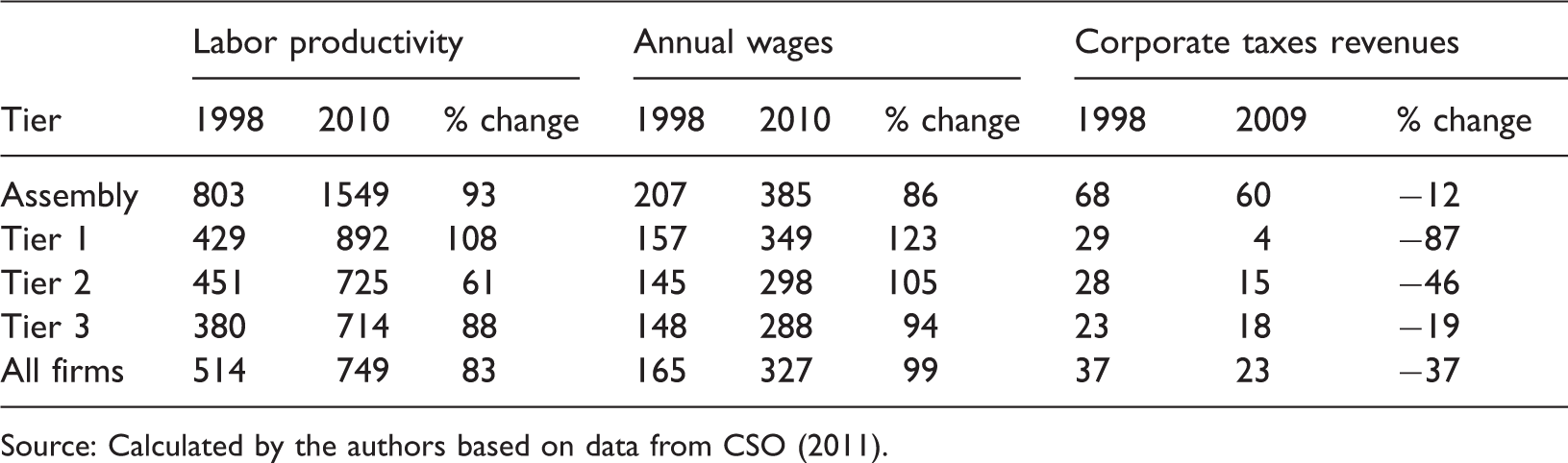

1998–2010 changes in value creation by supplier tiers

In the next step, we consider changes in the value creation indicators by individual tiers during the 1998–2010 period. Our previous research on upgrading in the Czech automotive industry has identified the two prevailing trends (Pavlínek and Ženka, 2011). The first one was the highly selective functional upgrading that was limited mostly to Škoda Auto and a few of the largest Tier 1 suppliers. It contributed to the increasing productivity and profitability gaps between assemblers and Tier 1 suppliers on one hand and lower tier suppliers on the other hand. The second trend was the widespread process and product upgrading among domestic Tier 2 and Tier 3 suppliers following their integration into GPNs and the pressure to increase the efficiency and quality of their production. As a result, domestic Tier 2 and Tier 3 suppliers outpaced foreign-owned firms in the rates of growth of labor productivity.

The development of labor productivity (value creation), annual wages, and corporate taxes revenues per employee (value capture) by supplier tier, 1998–2010/2009 (in thousands of CZK).

Source: Calculated by the authors based on data from CSO (2011).

Overall, the value creation in the Czech automotive industry significantly increased during the 1998–2010 period. Did this increased value creation lead to increased value capture in Czechia? We consider this question in the next section.

Value capture in the Czech automotive industry

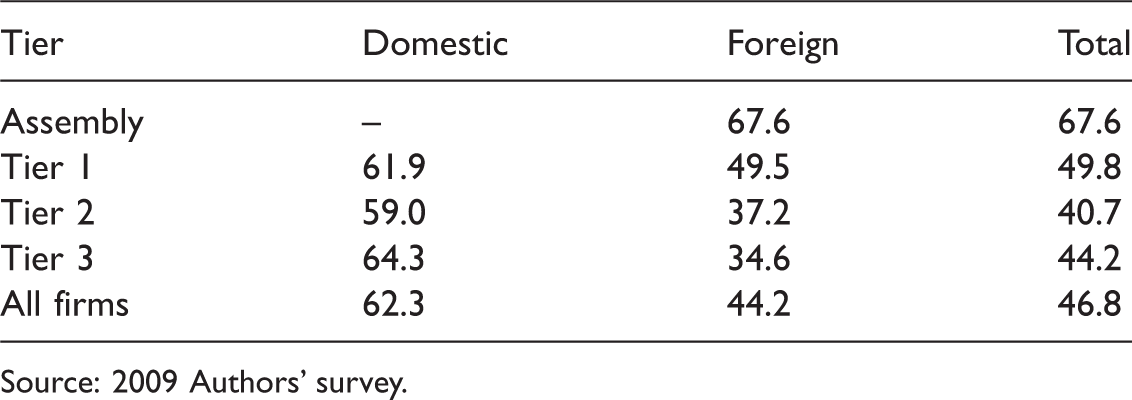

The percentage share of components sourced from Czechia in 2009 by supplier tier (value capture).

Source: 2009 Authors' survey.

Reinvested profits represent an important component of value capture in the Czech automotive industry. As of 2013, the total FDI stock in the narrowly defined Czech automotive industry stood at €9.6bn, of which €7.3bn (76%) was in the form of reinvested profits. Total repatriated profits stood at €4.4bn, which means that the total amount of reinvested profits exceeded repatriated profits almost 1.7 times (CNB, 2015).

The share of wages of the value of total production did not change significantly between 1998 and 2010. The total value of wages increased in a similar rate as the overall volume of production during this period. The total employment grew more slowly (by 68%) than average nominal wages per employee (by 99%). However, the share of corporate taxes of the value of total production decreased from 1.6 to 0.6% between 1998 and 2009 for three basic reasons (Ženka and Pavlínek, 2013): First, the Czech corporate tax rate decreased by 40% (from 35 to 21%) between 1998 and 2008. Second, Czechia introduced a generous system of investment incentives in 1998 (see Pavlínek and Ženka, 2011), which provided a corporate tax relief for foreign investors. Third, the profit repatriation abroad in the form of dividends increased rapidly in the 2000s and peaked during the economic crisis in 2008 and 2009 when it reached €813m and €754m, respectively. The 1998–2012 data thus suggest that the overall value capture in the Czech automotive industry tended to decrease during this period despite large FDI inflows.

Between 1998 and 2010, Tier 1 suppliers experienced the fastest increase in wages per employee (by 123%), while assemblers experienced the slowest (by 86%) (Table 5). Consequently, the wage gap between assemblers and suppliers slightly narrowed during this period. In contrast, the gap between assemblers and suppliers significantly increased in corporate taxes per employee (Table 5), which illustrates the ability of assemblers to concentrate increasing shares of profits at the expense of their suppliers. At the same time, assemblers, who accounted for 18.2% of the total automotive employment and 47.3% of total profits, accounted for 49.8% of corporate tax revenues between 2006 and 2008. Different tiers thus contribute to value capture and, consequently, regional development potential in different ways. While foreign assemblers and Tier 1 suppliers account for a disproportionately high share of total corporate tax revenues in the automotive industry, Tier 2 and Tier 3 suppliers are much more important in terms of the number of jobs they generate and related wage effects.

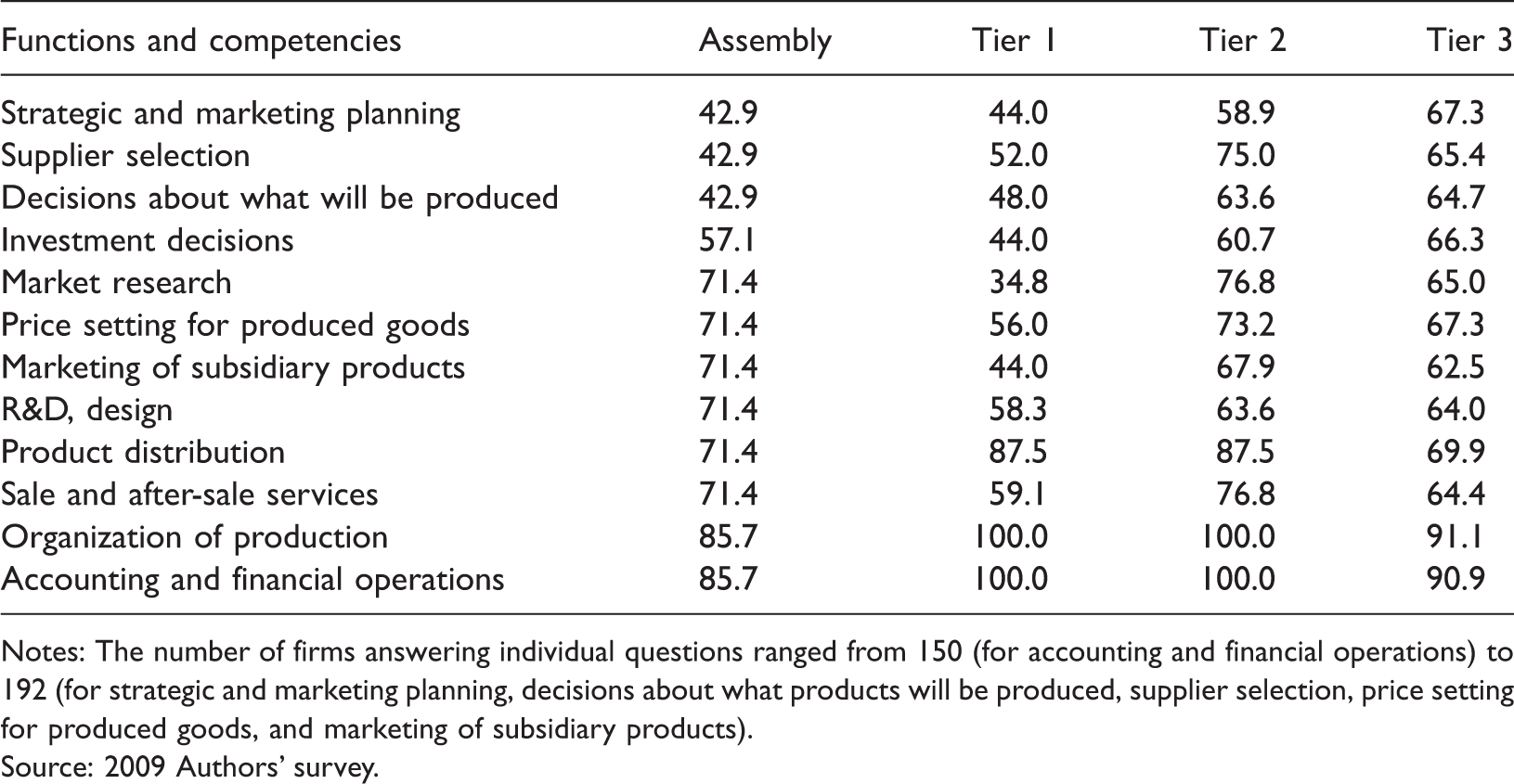

The percentage of automotive firms conducting selected high value-added functions in Czechia by supplier tier in 2009.

Notes: The number of firms answering individual questions ranged from 150 (for accounting and financial operations) to 192 (for strategic and marketing planning, decisions about what products will be produced, supplier selection, price setting for produced goods, and marketing of subsidiary products).

Source: 2009 Authors' survey.

Strategic nonproduction functions and competencies in the Czech automotive industry

Finally, we evaluate the presence of nonproduction functions and competencies in Czech-based automotive firms in order to test our fourth and fifth hypotheses. We assume that strategic nonproduction functions activities contribute to value creation and value capture more than production activities (Mudambi, 2008). Our 2009 survey collected the data about strategic nonproduction functions conducted by individual firms. Depending on a particular function, between 150 and 192 firms replied whether or not they performed each of 12 different functions. These functions represent high value-added activities that are typically associated with high-paid professional jobs. As such, the presence or absence of these functions at individual firms has potentially important implications for their value creation and value capture. However, we need to stress that our data refer only to the presence or absence of these functions and do not provide any information about their extent within individual firms. We are also aware that firms would tend to exaggerate rather than understate the presence and importance of these activities. Therefore, our data should be interpreted with caution as the representation of general trends rather than exact measurements.

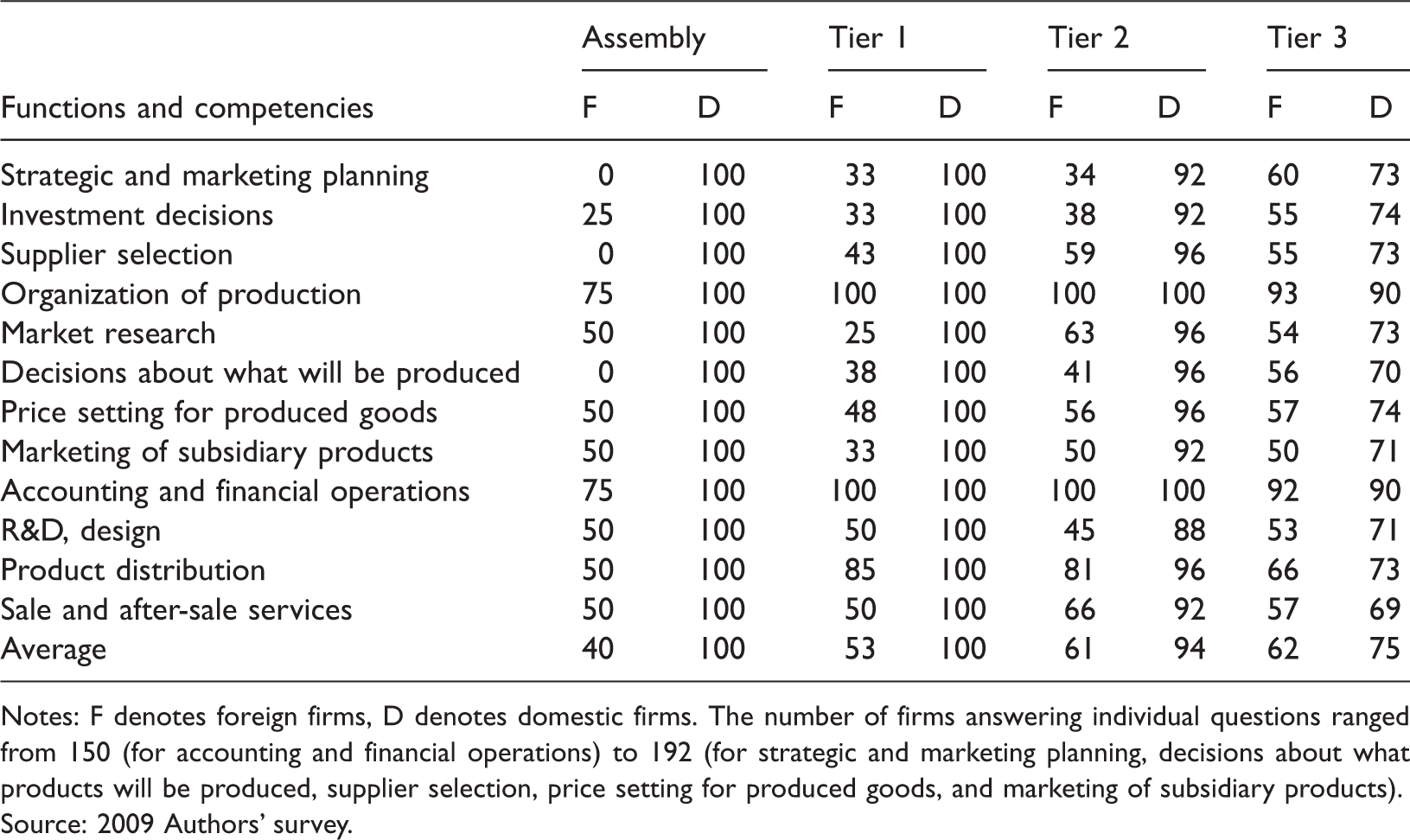

The percentage of automotive firms conducting selected high value-added functions in Czechia by ownership and supplier tier in 2009.

Notes: F denotes foreign firms, D denotes domestic firms. The number of firms answering individual questions ranged from 150 (for accounting and financial operations) to 192 (for strategic and marketing planning, decisions about what products will be produced, supplier selection, price setting for produced goods, and marketing of subsidiary products).

Source: 2009 Authors' survey.

There are important differences among individual supplier tiers and between foreign and domestic firms. Among foreign firms, higher tier firms on average conduct fewer nonproduction functions than lower tier firms, suggesting that higher tier foreign suppliers are more tightly integrated into transnational corporate production networks and controlled from abroad. The opposite situation is true for domestic firms because higher tier domestic firms conduct more functions than lower tier firms (Table 8). Higher tier domestic firms cannot stay competitive and survive without R&D and other nonproduction functions (2009–2011 interviews). Lower tier domestic firms, especially Tier 3 suppliers, are often captive suppliers that depend for many nonproduction functions on higher tier buyers of their components (Gereffi et al., 2005; Pavlínek and Žížalová, 2014), which explains why domestic Tier 3 suppliers reported the lowest share of nonproduction functions of all tiers. Small sample size affects the results for foreign assemblers. There is a difference between foreign assemblers that were taken over by foreign TNCs and kept certain strategic functions in what has been previously called embedded path-dependent transformations (Pavlínek, 2002), such as Škoda Auto and Iveco (former Karosa), and new greenfield assembly plants, such as TPCA and Hyundai that lack these functions and have no plans to develop them (2009–2011 interviews). Although higher tier firms capture a greater share of created value than lower tier firms, it is not because they conduct more nonproduction functions. Our data only confirm that assembly and Tier 1 firms pay significantly higher wages per employee than Tier 2 and Tier 3 firms (Table 5). Therefore, we have to reject the fifth hypothesis that higher tier firms capture a greater share of created value than lower tier firms because higher tier firms conduct more nonproduction functions and offer higher wages than lower tier firms.

Conclusion

In this article, we set out to evaluate the value creation and capture in the Czech automotive industry by different tiers of automotive firms. We empirically tested whether two theoretical assumptions apply in the automotive industry in the context of integrated peripheral markets. First, whether higher tier firms create and capture higher value than lower tier firms because they produce more complex components and possess a strong bargaining power that allows them to squeeze their suppliers (Sturgeon et al., 2008). Second, whether intangible knowledge-based assets and strategic nonproduction functions represent a key source of value added for higher tier firms (Mudambi, 2008).

Our analysis suggests that the economic effects of the automotive industry largely depend on its capital intensity of production, especially in terms of wages and value added per employee, which tend to increase with the increasing capital intensity of production and vice versa. Since the highest capital intensity of production is found among assemblers and Tier 1 suppliers, these firms should have stronger economic effects than lower tier suppliers. Additionally, assemblers and Tier 1 suppliers account for much higher corporate tax revenues than lower tier suppliers and they have higher average wages per worker. This also points toward stronger economic effects of assemblers and Tier 1 suppliers than Tier 2 and Tier 3 suppliers. However, the vast majority of assemblers and Tier 1 suppliers are foreign owned in the Czech automotive industry, which has two important implications. First, Czech-based subsidiaries of foreign lead firms and Tier 1 suppliers primarily concentrate on export-oriented assembly and production and their strategic nonproduction functions are weakly developed. Second, an increase in value creation by foreign firms does not necessarily have to translate into an increase in value capture because of profit repatriation, tax holidays, and other profit shifting strategies employed by foreign firms. At the same time, lower tier suppliers have larger direct employment and wage effects per unit of production and investment capital than higher tier suppliers. This is important for regional development since Tier 2 and Tier 3 suppliers are much more numerous, more spatially dispersed, and received on average significantly lower investment incentives per newly created job than assemblers and Tier 1 firms.

The data analysis from the Czech automotive industry confirmed our first hypothesis that higher tier firms generate greater value per employee than lower tier firms. As a result, their share of the total value added in the automotive industry has been increasing. Our data also confirmed the second hypothesis that domestic suppliers import a lower share of inputs than foreign suppliers. Our third hypothesis that higher tier firms import lower shares of inputs than lower tier firms was confirmed for foreign but not domestic firms. Therefore, it has to be rejected. Nevertheless, in the case of foreign firms, a higher share of domestic sourcing by assemblers and Tier 1 suppliers is another supporting evidence of higher tier foreign firms creating and capturing greater value than lower tier suppliers as confirmed by the first hypothesis. Our fourth hypothesis arguing that higher tier firms possess stronger and more diverse competencies that are reflected in the presence of more nonproduction (strategic) higher value-added functions than in lower tier firms has to be rejected since higher tier foreign firms conduct fewer nonproduction functions than lower tier foreign firms in the Czech automotive industry. Parent companies typically conduct these functions for higher tier foreign firms abroad. We also have to reject our fifth hypothesis. Higher tier firms capture a greater share of created value than lower tier firms because they offer higher wages than lower tier firms but not because they conduct more nonproduction higher value-added functions. The rejection of the fourth and fifth hypotheses allows us to conclude that the high value creation and capture by assemblers and Tier 1 suppliers in the Czech automotive industry is not a function of the presence of valuable intangible assets and strategic nonproduction functions. Rather, it is a function of firm size and capital intensity of production. A significantly larger firm size contributes to high profitability by allowing higher tier firms to capitalize on their internal scale economies and strong purchasing power, which translates into their very strong bargaining power. The capital intensity of production can at least partly explain the high labor productivity of higher tier firms. The combination of a strong bargaining power with the high capital intensity of production and high labor productivity is probably the key explaining factor for relatively high wages, profitability, and corporate tax revenues of higher tier firms, especially assemblers. Further empirical research is needed to determine if this finding will hold in other integrated peripheral markets. If it does, we can expect a similar distribution of value creation and capture in countries with a similar or lower concentration of strategic nonproduction functions in the automotive industry, such as Spain, Portugal, Poland, Hungary, Slovakia, Mexico, and Thailand.

The greater economic potential of higher tier firms than lower tier firms in the automotive industry has important policy implications for less developed countries. In the absence of a strong domestic automotive industry, it makes sense to attract foreign assembly firms because Tier 1 foreign suppliers will likely follow, which will also encourage foreign Tier 2 and Tier 3 suppliers to invest. Most ECE countries have followed this approach and engaged in aggressive bidding for foreign assembly plants in the 1990s and 2000s (Drahokoupil, 2009; Pavlínek, 2014). However, less developed countries with a weak domestic manufacturing sector need to factor in potential long-term less tangible costs of these FDI-oriented policies, such as increased economic dependence on foreign TNCs, outflow of profits, and the danger of being locked in an unfavorable position in the international division of labor (Nölke and Vliegenthart, 2009). It is reasonable to expect that the small and open ECE economies will continue to be heavily influenced by inflows of FDI and activities of foreign TNCs in the future. At the same time, the overwhelming economic dependence on foreign capital and economic control by foreign capital will make it extremely difficult for ECE to close the economic gap, including the gap in standards of living, with Western Europe as ECE countries are facing the danger of falling into the “middle income trap” (e.g. Ravenhill, 2014). A successful long-term development strategy of the automotive industry should therefore combine the presence of foreign firms with a simultaneous promotion of the strong domestic sector. A key policy issue is finding a balance between the degree of external control and dependence and indigenous economic development based upon policies that would allow for a gradual upgrading of the position of ECE countries in the international division of labor.

Footnotes

Acknowledgements

The authors wish to thank three anonymous referees and the editor for their comments on an earlier version of this article and Pavla Žížalová for help with conducting company interviews.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research and article preparation were supported by the Czech Science Foundation (Grant Number 13-16698S).