Abstract

Market competitiveness forces businessmen of all kinds to be quicker and quicker as far as decision-making is concerned. In this sense, digital accounting has become an essential tool insofar as it presents many advantages for any firm, regardless of its size, allowing it to use technology to automate processes. The present study provides a bibliometric analysis as well as a literature review of this recent topic that has received little attention from academia. A quantitative and qualitative methodology based on Web of Knowledge (WoS) and Scopus databases was used to accomplish this. Using the R Bibliometrix software associated with content analysis, the bibliometric analysis revealed there is a growing interest in the Digital Accounting concept, although it needs to be further researched. The analysis allowed for the identification of three main research topics/clusters: Cluster 1—Scientific mapping of digital accounting; Cluster 2—Digital records management; and Cluster 3—Digital skills. This study aims to make a theoretical contribution to the literature on the subject and a practical one to business managers about the advantages of implementing digital accounting and keeping up with the advances of technology to make their businesses more efficient and simpler, rigorously, and interactively run.

Introduction

The roots of digital accounting go back to the Depression era and the Second World War. According to Deshmukh (2006), at the time, tax regulations were complex, and logistical and data management problems were many. In the late 1950s and early 1960s, some large companies began to handle data that revealed government requirements and could not be handled manually or cost-effectively. As a result, accounting and financial information became prime candidates for automation, and early investments in information technology were controlled by the accounting and finance departments. This mechanization of accounting and financial information expanded the power of CFOs and controllers, allowing them to influence operational and strategic decisions. As tabulation facilities turned into data processing centers, the technology became too complex to be controlled by accountants; instead, data processing managers were responsible for managing data processing centers, leading to the emergence of the Data Processing Management Association (DPMA).

The automation of accounting and financial data soon developed an irreversible momentum (Deshmukh, 2006). The electronic data interchange (EDI) and electronic funds transfer (EFT) can be said to be at the very beginnings of the digital exchange of accounting information between trading partners (Deshmukh, 2006), a notion shared by Ghasemi et al. (2011), for whom new technologies like computers, servers, the internet, and other digital devices and tools were the vehicle for information computerization. This computerization represented for businesses a relevant improvement in their traditional production and operation processes. Naturally, accounting was no exception, and its routines became automated (Silva et al., 2019).

These authors argued that information and communications technologies (ICT) were a great help in performing accounting tasks, increasing productivity, and improving managers’ decision-making processes. As ICT evolved, information systems (IS) were created (Damasiotis et al., 2015), which made it possible to automate such basic accounting operations as data processing and document classification (Damasiotis et al., 2015). Later, the appearance of information systems for management as well as accounting, described by Belfo and Trigo (2013) as a computer method designed to monitor accounting activity through the use of ICT, represented a true revolution in how accounting tasks were performed (Akhter and Sultana, 2018; Damasiotis et al., 2015).

In this sense, clearly, the inclusion of technology in accounting has proved useful to improve productivity and efficiency (Bogasiu and Ardeleanu, 2021). In other words, harmonizing accounting tasks with the novel ICT led to the transition from traditional accounting systems into digital ones, characterized by more agile and practical accounting processes. This represents a challenge to accountants and has a direct impact on how accounting is done. Besides, according to John (2020), it prompted important changes, namely, (i) Technology supports the new skills that are required of accountants (e.g., planning and strategy skills) and improves the quality of services rendered to customers; (ii) Customers’ expectations require accountants to have, for instance, business guidance, strategic planning, and financial forecasting; (iii) Customers continue to be granted a good experience regardless of whether it is face-to-face or not, especially due to accounting platforms and systems gathering all the information in due time and being accessible to everyone everywhere; (iv) Multidisciplinary collaborations will arise to boost innovation and grant the customer value-added; and (v) There are multiple forms of connectivity.

In other words, in view of the business environment and managers’ growing demand for relevant, reliable, opportune, and comparable accounting information (Valentim, 2008), globalization has introduced considerable changes into accounting that require adapting to digital transformation.

Clearly, this highlights an evolution of digital accounting and a change in intra- and inter-company processes and management practices. This line of thinking had already been alluded to by Deshmukh (2006). In his opinion, all areas of business, including accounting and finance, have come under intense scrutiny due to companies’ growth. In fact, the introduction of technological innovation into accounting practice information systems, which need fewer requirements to perform the tasks (Bogasiu and Ardeleanu, 2021), made them more flexible and capable of delivering a speedier response.

In this context, digital accounting can be described as a computer system and/or software already designed and programmed that can be customized to keep a record of transactions to generate financial statements for further analysis (Deshmukh, 2006). Digital accounting is a rapidly evolving field that leverages technology to rationalize and automate various accounting processes, thus leading to greater efficiency, accuracy, and accessibility to financial information. Digital tools such as cloud-based accounting software and mobile applications can revolutionize how companies manage their finances daily, providing real-time insights and enabling remote working (Azzari et al., 2020). In a world of increasingly digitalized businesses, organizations must adopt digital accounting if they are to remain competitive and ensure long-term success. ERPs is software used by the organizations to manage day-to-day activities such as accounting and project management. In recent years, this software has been updated and improved countless times to keep up with technological developments and the orientation of both the economy and customers (Genete and Tugui, 2008). Consequently, digital accounting is increasingly regarded as a common language among accounting professionals (Lehner et al., 2019), and scientific studies on this subject have been proliferating in several areas covering its many dimensions. In the next sections, a description of how these dimensions relate to the organizational, individual, regulatory, innovative, and ethical perspectives will be provided as well as the studies’ authors’ approaches.

Underlining the computerized accounting system there is the concept of a database that is systematically maintained and possesses an active interface based on the use of the accounting application software and reporting system. Therefore, digital accounting has an impact on tax auditors’ audit performance, improving the quality of financial reporting, the usefulness of accounting information, and the effectiveness of strategic decisions in different companies.

Several articles were published addressing the effects of this impact, some of which focused especially on companies and audits in Thailand. One of those articles (Lohapan, 2021) in particular targeted the effects of audits, examining tax auditors’ audit skills and the resulting audit report. The article also describes the process and its possible outcomes both from the digital implementation stakeholders’ perspective and that of auditors knowledgeable in the professional field.

This research revealed that not only does digital culture affect the implementation of digital accounting but also that the latter plays a vital role in improving the whole audit competence and audit report, ultimately leading to the achievement of audit results. Furthermore, the results thus obtained are beneficial for both audit practitioners and all professionals involved in this type of work and may be used to develop training programs designed to improve professional auditing’s efficiency (Lohapan, 2021).

Another study worth mentioning addresses the effects of digital accounting on the quality of financial reporting, the usefulness of accounting information, and the effectiveness of strategic decisions in 313 Thai companies (Phornlaphatrachakorn and Kalasindhu, 2021). In it, their authors show how digital accounting can significantly affect not only the financial reporting quality but also the accounting information’s usefulness and the strategic decisions’ effectiveness. The same article suggests that (i) both financial reporting quality and the accounting information’s usefulness mediate the relationship between digital accounting and strategic decisions’ effectiveness; (ii) digital transformation moderates both financial reporting relationships’ digital accounting quality and digital accounting usefulness but does not moderate other relationships, though (Phornlaphatrachakorn and Kalasindhu, 2021). It follows then that digital accounting is instrumental in determining and explaining how companies’ goals can be achieved. Moreover, it points to executives learning, investing in, and using the digital accounting system in organizing their own companies to ensure and achieve objectives and, ultimately, improve their sustainability (Phornlaphatrachakorn and Kalasindhu, 2021).

There are still some gaps in the existing literature on digital accounting that need filling in, though. According to Diller et al. (2020) and Moll and Yigitbasioglu (2019), previous research focused mainly on ICT’s impact on accounting’s most simplistic functions; namely, Azzari et al. (2020) reminded that digital accounting customers have become more demanding, which requires suitable responses from accounting professionals; hence, the urgent need for more extensive research in this field. Not to mention, the abrupt digital transformation caused by the pandemic left businesses and other organizations no choice but to adapt if they were to stay afloat in the market.

From a practical perspective, technological evolution is imposing new demands on accountants, emphasizing the importance of digital accounting and the acquisition of appropriate technological skills. This affects financial reports’ quality, strategic decisions’ effectiveness, and accounting information’s usefulness. The quality of digitally produced financial information plays a crucial role in the strategic decisions’ effectiveness. To this end, accountants must understand the technology and know how to use it to improve their knowledge of digital accounting. As the working environment becomes more digital, accountants must adapt their working methods and approaches to clients. This means recognizing that their skills and methods cannot remain static, as technology is evolving rapidly, introducing concepts that once seemed futuristic, such as artificial intelligence and advanced robots.

Although the traditional accounting profession and basic accounting principles have stood the test of time, the globalization of organizations and technological innovations are rapidly changing this reality. Accountants face several challenges adapting and transforming their business practices and processes while maintaining fundamental accounting principles. On the other hand, in the digital age, accounting information users want real-time information without delay. These changes have a strong impact on how accountants perform their work and require them to acquire new skills, especially in areas such as engineering, to create new types of accounting professionals.

In short, digital accounting makes use of technology to improve accounting processes’ efficiency and accessibility, leading to greater accuracy and availability of financial information. As digital tools evolve, organizations adopting them will be at a competitive advantage to achieve their financial goals and adapt to market changes. Digital accounting allows organizations to take advantage of such emerging technologies as real-time reporting, forecasting, and expense tracking to stay ahead of the competition and adapt to the demands of the ever-changing business world.

Despite its considerable progress, digital accounting still faces substantial challenges. One of them is ensuring the rigorous protection of clients’ financial information, which includes protecting sensitive and confidential data from cyber threats and sophisticated frauds (Morshed and Khrais, 2025). These threats, which have become increasingly more complex and unpredictable, require implementing innovative protection strategies in line with the digital reality, ranging from phishing attacks to ransomware that can completely cripple entire organizations (Sundaravadivazhagan et al., 2024). The continuous updating of accounting software represents a fundamental challenge. That is why organizations must select the appropriate software, adapting it to their specific requirements, and ensure that professionals receive the necessary training to make effective use of the new technologies and tools available on the market (Artene and Domil, 2024). This qualification should encompass both technical proficiency in the tools and an understanding of market trends and needs (Ibrahim and Tahir, 2024).

Another crucial aspect lies in companies’ ability to adapt to the paradigm shift promoted by digital accounting. The transition to digital processes is an all-encompassing metamorphosis that fully impacts both the organizational and operational structure, requiring a collaborative effort for its successful implementation. This cultural transformation must be meticulously planned and implemented to prevent disruption and ensure continuity of operations. Finally, interoperability between the various systems and platforms used in digital accounting can be a limitation (Zhen and Zhen, 2024). The lack of effective integration between tools can jeopardize the accounting process, resulting in delays, communication failures, and data inconsistencies (Bastos et al., 2022). Thus, digital accounting must overcome these challenges to advance and prosper in the future. Through the focus on data protection, the updating of software, providing continuous training for professionals, and adaptation to new paradigms, organizations can ensure accounting information’s integrity and effectiveness in a constantly changing environment (Alawadhi and Alrefai, 2024).

Digital accounting offers a wide range of benefits that are truly significant for education, not least the ability to provide a learning experience that goes far beyond the traditional and conventional (Bastos et al., 2022). This new teaching model is not only more practical but also much more up-to-date and in line with the real and emerging needs of the modern and contemporary world. With the growing and accelerating adoption of innovative technologies and digital tools, students have a valuable and invaluable opportunity to understand accounting concepts in a much more effective, in-depth, and complete way, as they can apply them in real and dynamic market scenarios (Bastos et al., 2022; Vaz et al., 2023). This practice contributes substantially to a more solid, clear, and concrete understanding of the content covered, better preparing them for the reality of the market. In addition, digital accounting plays a fundamental and essential role in preparing students for the competitive and challenging labor market, since it offers them not only practical skills that are essential and indispensable but also a comprehensive, detailed, and up-to-date knowledge of the latest trends and practices shaping the sector in these dynamic and constantly evolving times (Nurhayati et al., 2023). Concurrently, students become significantly more competitive, skilled, and equipped to deal with the professional challenges that await them in a more effective, conscious, and confident way, which naturally increases their chances of professional success (Kharbat and Muqattash, 2020).

In this sense, this paper aims to draw attention to the importance of technology in accounting’s different areas while seeking to understand how the teaching of this subject and the different professions related to accounting have been able to keep pace with technology’s evolution. The incorporation of technology into processing digital accounting helps manage and store digital files and save and back up information in more secure and cost-effective ways; besides contributing to a reduced use of physical files and more efficient tax processes. This study proposes, therefore, to answer the following research questions:

Simultaneously, this article aims to analyze the field of research related to digital accounting to improve decision-making, considering other technologies, such as cloud computing, blockchain, artificial intelligence, social networks, and the Internet. Accomplishing these goals involved doing a systematic literature review, which included a bibliometric analysis obtained by resorting to R Bibliometrix software. The empirical evidence contained in the present study is a valid contribution to increasing the interest in digital accounting as regards the way managers see this tool and its possible implementation. This interest results from the current knowledge of an area of study that still offers a lot of potential, either from the viewpoint of digital accounting’s practical application to businesses or its relevance for academia as far as scientific research is concerned.

The novelty of this work lies in its ability to map and analyze digital accounting research systematically, providing empirical insights into its evolution, trends, and gaps. This approach allows for a better understanding of how emerging technologies—such as cloud computing, blockchain, artificial intelligence, and social networks—are being integrated into accounting processes. Unlike traditional reviews, which often focus on specific aspects of digital accounting, this study identifies overarching themes, research patterns, and the longitudinal distribution of topics, offering a broader and data-driven perspective. Studying digital accounting is essential as it remains a developing field. Tracking its evolution helps academics and professionals anticipate trends, while monitoring technological advancements ensures research stays relevant to changes in financial reporting and auditing. Identifying key bibliometric indicators provides a roadmap for future studies, addressing research gaps. Practically, understanding digital accounting supports better business strategies, education, and regulatory policies, aligning the field with technological progress.

The following sections present the methodology, the results and their discussion, and finally the study’s conclusions, limitations, and suggestions for further research.

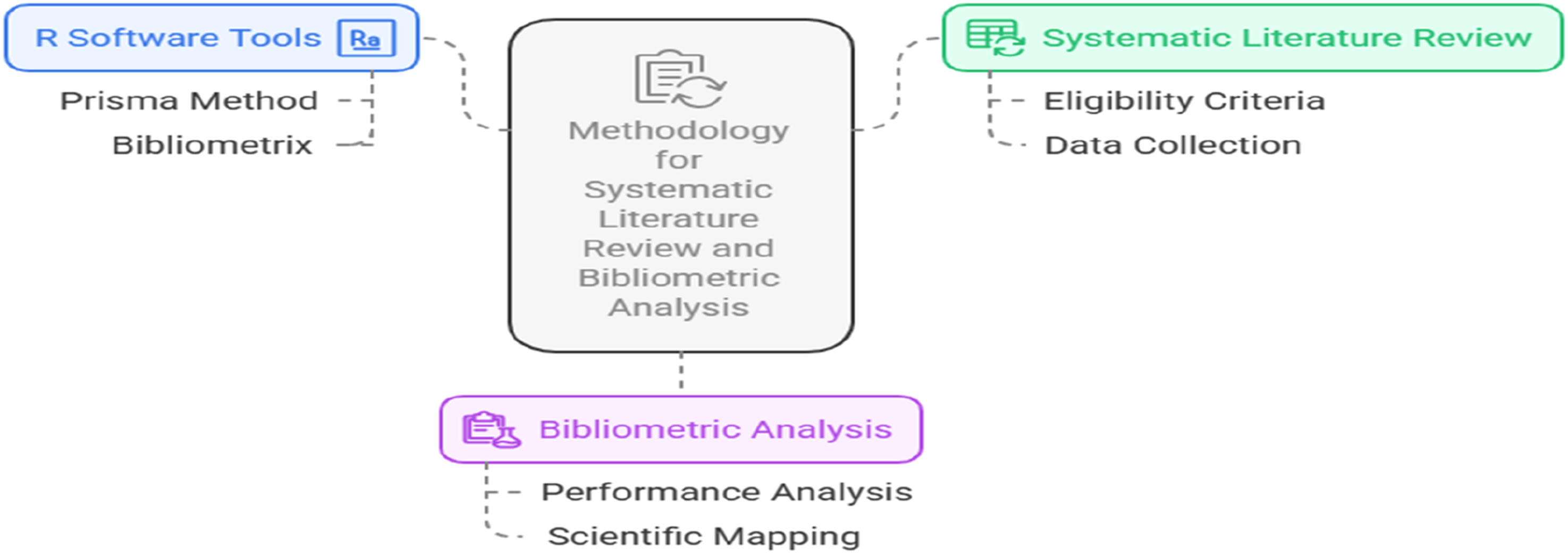

Methodology

Systematic literature review

The Systematic Literature Review (SLR) is an essential method for identifying relevant publications on a given topic, ensuring that the synthesis of results is comprehensive, accurate, and impartial (Donato and Donato, 2019; Siddaway et al., 2019). Unlike traditional reviews, SLR requires rigorous criteria for selecting and analyzing studies, allowing results to be replicable and regarded as scientifically valuable (Briner and Denyer, 2012). This approach provides a detailed mapping of existing knowledge, helping to identify gaps and guide future research (Mentzer and Kahn, 1995). Transparency in the process of data collection and document selection is a fundamental principle, ensuring that the review is structured and reliable (Hadengue et al., 2017). According to Tranfield et al. (2003) and Xiao and Watson (2019), a systematic review should follow well-defined steps, including problem formulation, development of a review protocol, definition of inclusion/exclusion criteria, literature search and selection, quality assessment, data extraction and analysis, and finally, synthesis and discussion of the results. This study adhered to these guidelines by conducting a bibliometric review based on statistical methods to assess both the quantitative and qualitative scope of academic production on the topic (Connor and Voos, 1981; Garfield, 1979; Powell et al., 1996; Quinlan et al., 2008; Wasserman and Faust, 1994; White and Griffith, 1981). In this context, bibliometrics is used as a quantitative approach to map and assess scientific output while minimizing bias through specialized tools (Lim et al., 2022; Sharma et al., 2023).

To ensure methodological rigor, this study adopted the PRISMA method (Preferred Reporting Items for Systematic Reviews and Meta-Analyses), which is widely recognized for providing greater transparency and standardization to systematic reviews (Page et al., 2021). This method is extensively used to ensure that the selection and analysis of studies follow a logical and well-documented flow, reflecting advances in identifying, evaluating, and synthesizing literature (Page et al., 2021: 3). It is based on a checklist and a flowchart that guide the rigorous selection of documents, ensuring that the final sample consists of relevant, high-quality studies (Liberati et al., 2009). The PRISMA protocol includes the following stages: (1) definition of eligibility criteria; (2) identification of information sources; (3) search and selection of studies; (4) data collection; and (5) defining the final dataset of documents to be analyzed (Adiyarta et al., 2020). After applying the PRISMA method, the R Bibliometrix software was used, which enables network analysis, co-authorship mapping, bibliographic coupling, and other key metrics to map scientific output in a particular field (Grácio, 2016). Bibliometrix is an R package designed for bibliometric analysis and is widely recognized for its robust statistical capabilities, access to efficient algorithms, and integrated visualization tools (Aria and Cuccurullo, 2017). This software facilitates the identification of patterns and trends in large volumes of scientific publications, allowing for a systematic and replicable approach to bibliometric analysis (Darvish, 2019). Additionally, it enables the extraction of different matrices, such as co-authorship networks, author publication counts, bibliographic coupling analysis, distribution by country, and identification of key publishing journals (Ekundayo and Okoh, 2018). The combination of PRISMA and R Bibliometrix strengthens the reliability of the review, ensuring a structured and evidence-based process for mapping the scientific development of the studied area. Although Bibliometrix (R) was used, there are others such as pyBibX and Scientopy, CiteSpace, CitNetExplorer, CRExplorer, Metaknowledge, Tethne and VOSviewer, Bibexcel, BiblioTools, Litstudy, Sci2 Tool and SciMa, among others, that could have been used (Pereira et al., 2025).

The reliability of bibliometric analysis depends on the careful choice of databases, the precise definition of search terms and inclusion criteria, as well as careful review of the data to avoid inconsistencies (Donthu et al., 2021; Passas, 2024; Rousseau and Rousseau, 2021). Bibliometric indicators, such as the number of citations and the h-index, should be analyzed with caution, considering factors such as the impact of the research and the social and political context (Alsharif et al., 2020; Gan et al., 2022). For a more complete understanding of scientific production, it is recommended to combine bibliometrics with qualitative methodologies such as content analysis and systematic review (Tomaszewski, 2023).

Figure 1 shows the methodology followed in this SRL. Methodology.

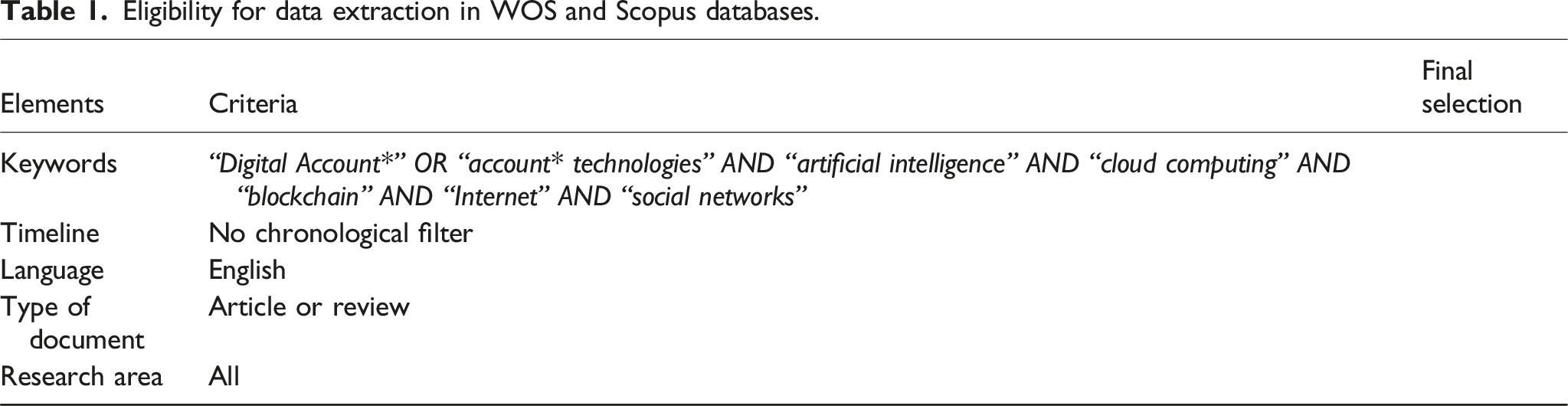

Data collection

Eligibility for data extraction in WOS and Scopus databases.

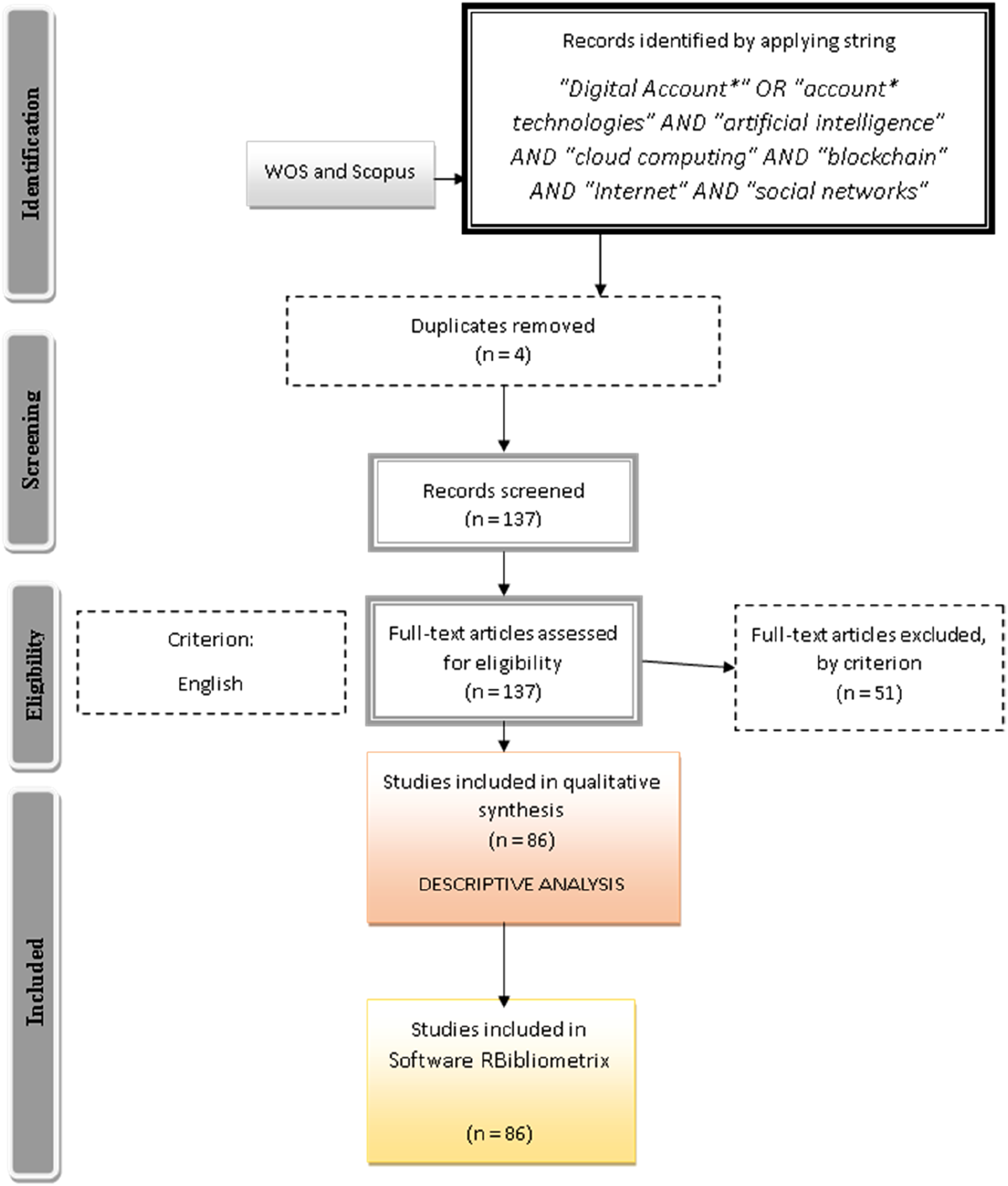

Based on the above, Figure 2 shows the application of the Prisma method. Prisma method.

In the following section, the scientific mapping of the 86 articles is presented along with the bibliometric analysis and content analysis.

Results of bibliometric analysis

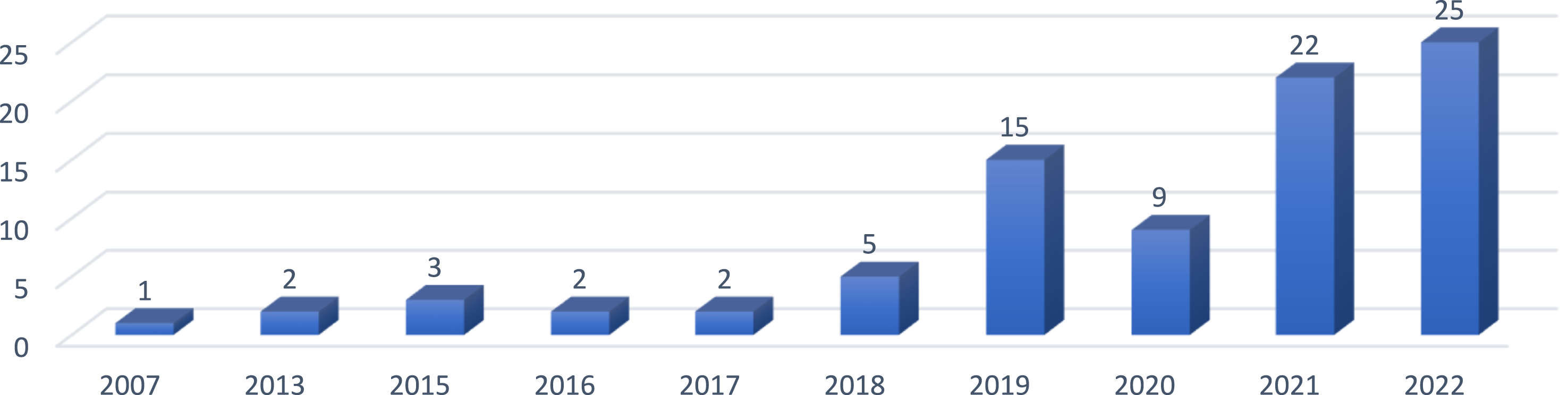

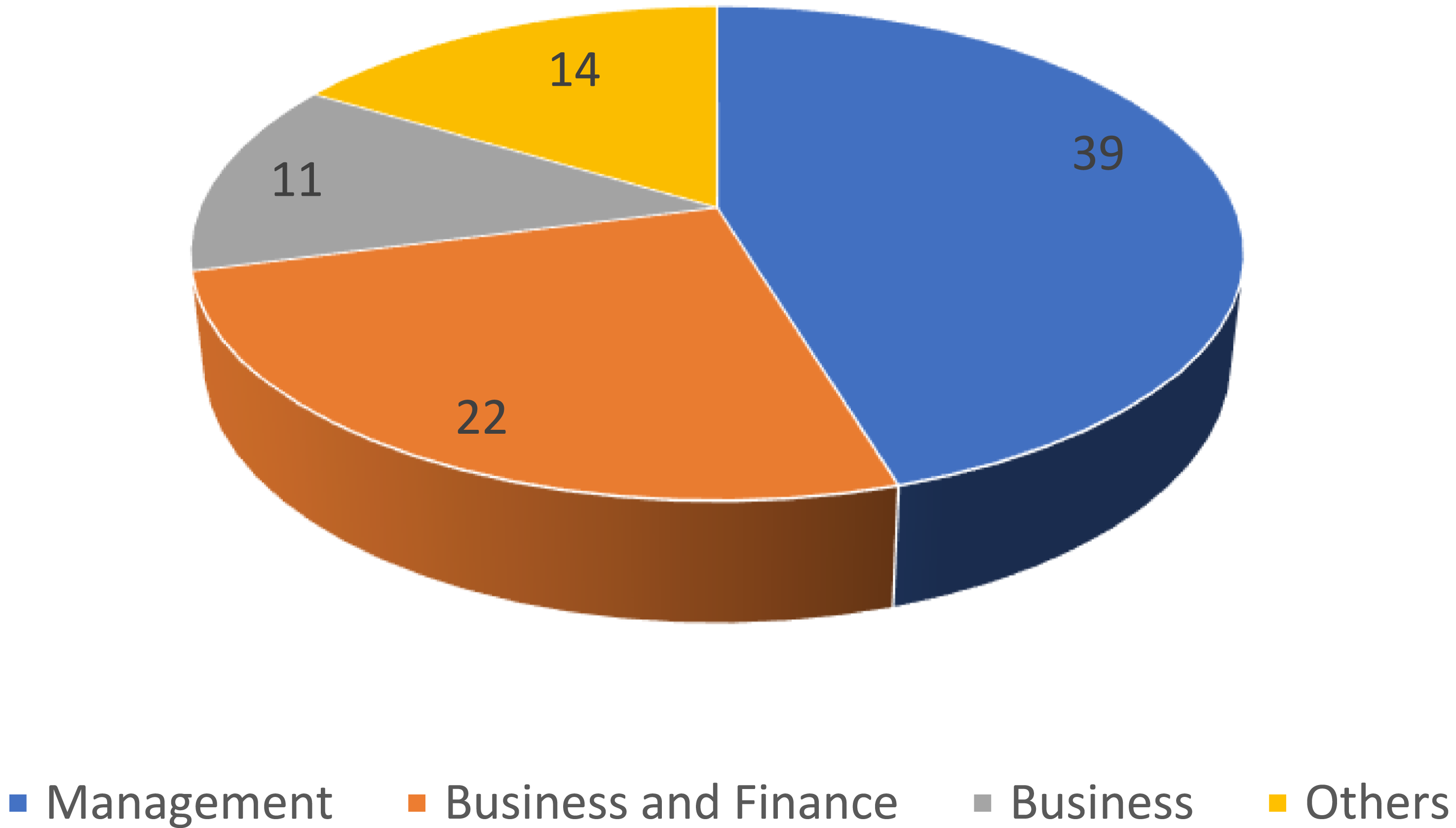

Of the 86 eligible publications, 11 regard the business and management research areas, with 2022 being the year in which more articles were published, as can be seen in Figure 3. Publications by year (n = 86).

This high number of publications in 2022 is revealing of the few effects of the pandemic, during which resorting to ICT and teleworking happened. The whole of the 86 publications includes nine systematic literature review articles between 2017 (one) and 2022 (four).

No less importantly, Figure 4 shows the research categories covered by the 86 articles under analysis. Web of science and scopus categories (n = 86).

Figure 4 shows that the business and management research categories were the ones more frequently published on the subject of digital accounting between 2007 and 2022, as a result of accounting’s being more and more perceived as a timely management tool that can be used to organizationally enhance executive managers’ decision-making processes. As previous research has shown (Chakravarty et al., 2013; Govuzela and Mafini, 2019; Mircea, 2013; Nejatian et al., 2019), organizations are constantly faced with more and more disruptive and volatile business environments in which organizational agility constitutes a positive response.

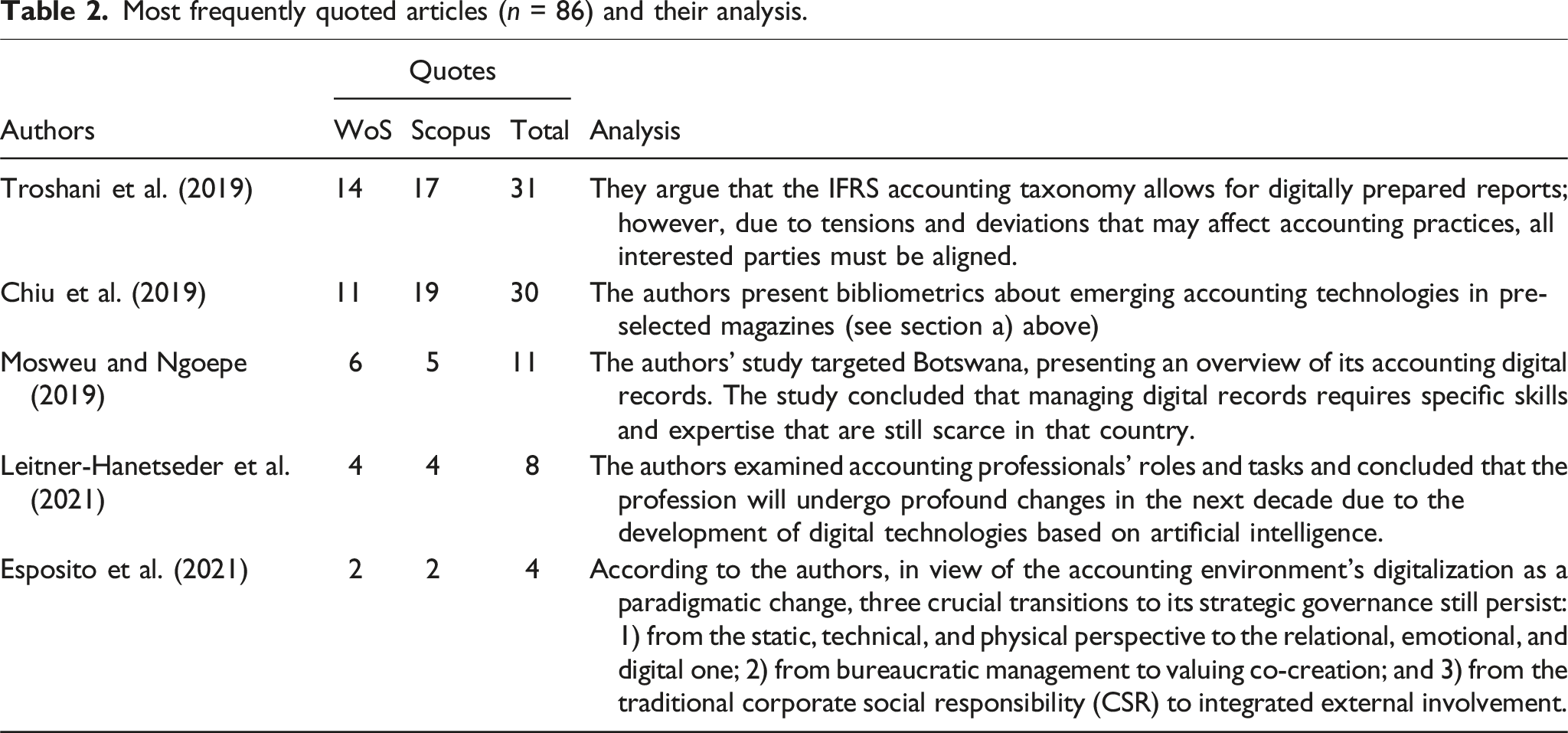

Most frequently quoted articles (n = 86) and their analysis.

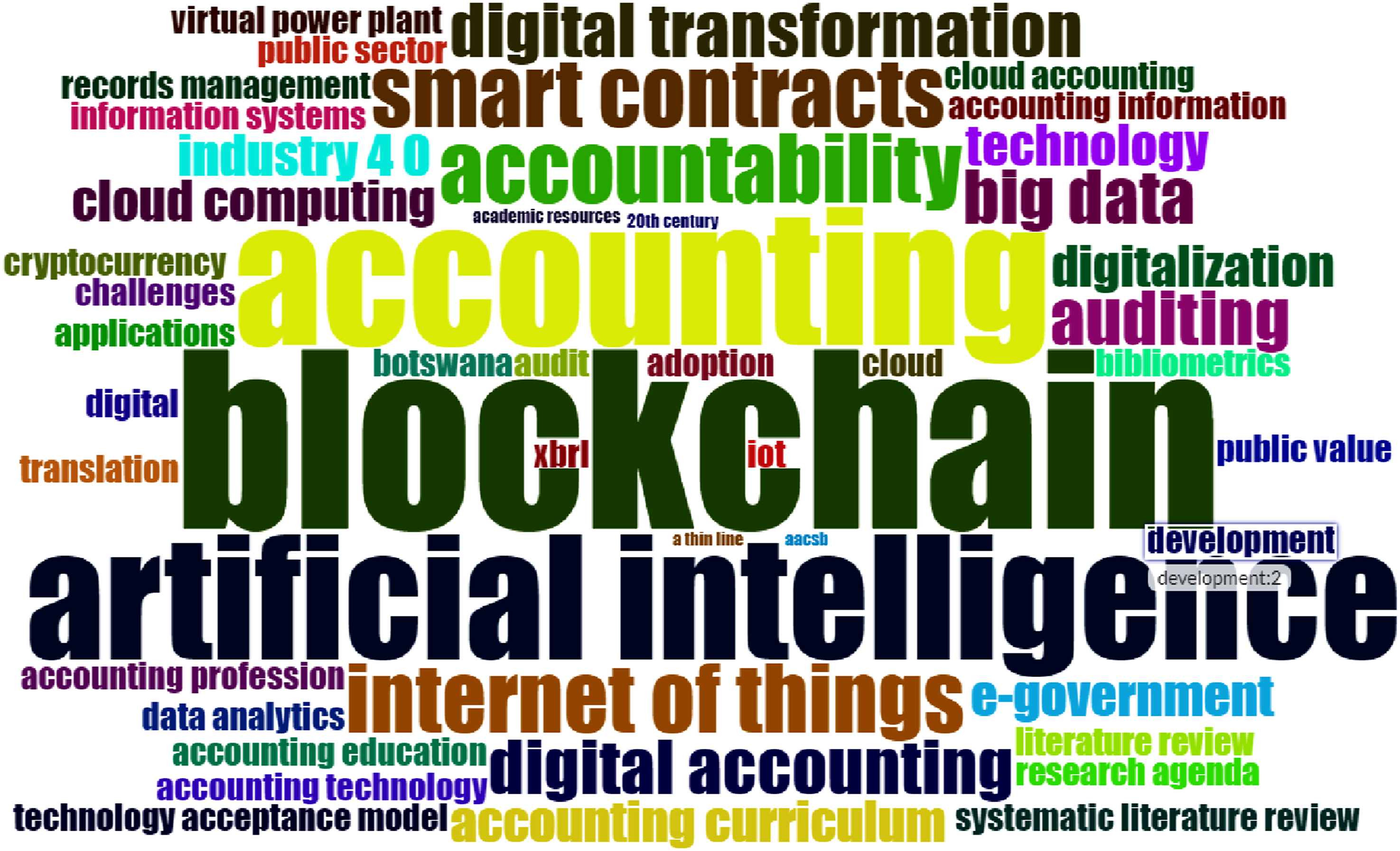

After this descriptive scientific mapping, a bibliometric analysis using the R Bibliometrix software is presented. Thus, Figure 4 shows the word cloud originating from the 86 articles. The mentioned cloud highlights words that stand out in the articles. In Figure 5, the larger the font, the more pertinent the subject is being studied. Cloud of words (n = 86).

The words “accounting,” “auditing,” and “accounting information systems” are employed more frequently, which means that digital accounting is emergent and current as a research subject, and justifies the present study’s being included in the selected no-filter articles (n = 86).

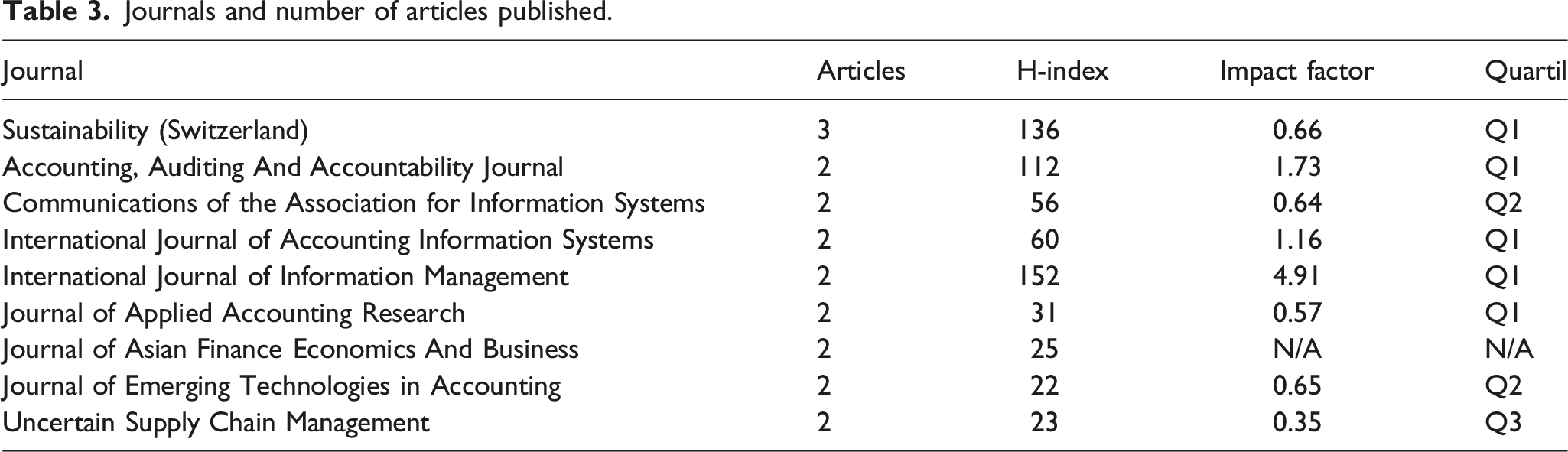

Journals and number of articles published.

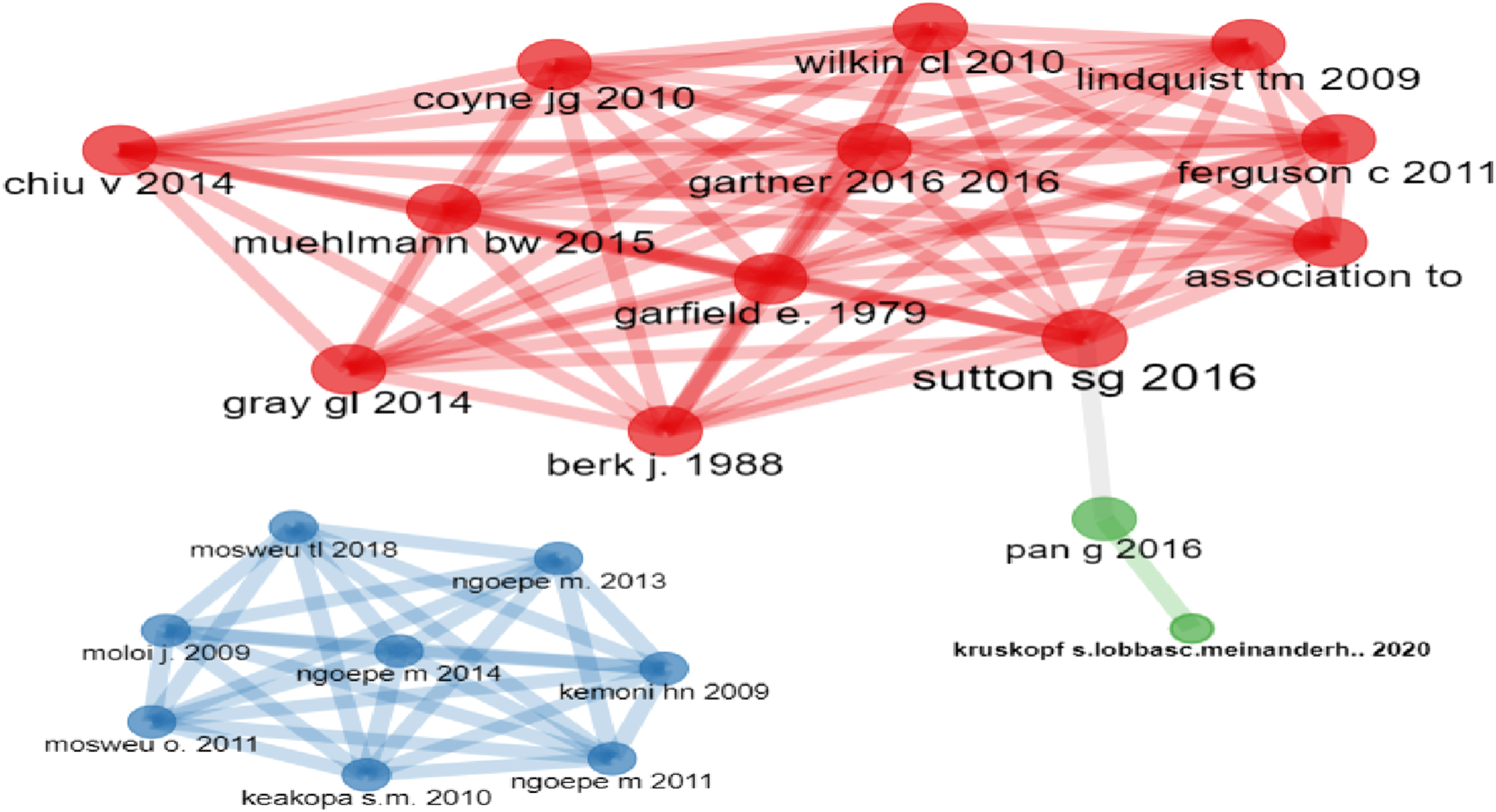

After reading the content of the articles, the R Bibliometrix software grouped them by research topic based on the keywords. As well as being grouped by theme, the grouping is organized by a network of co-citations in which the grouped themes assume different degrees of importance according to the number of citations each author has. The more significant the author’s impact, the larger the circle surrounding them. The co-citation matrix is analyzed using statistical techniques and algorithms. This makes it possible to identify groups of documents that are frequently cited together, revealing associations and trends in the field of research. In turn, the results of co-citation analysis can be visualized using network graphs, heat maps or other visual representations that allow researchers to identify clusters of related documents and understand how different topics are interconnected. Co-citation analysis is a powerful tool for identifying the structure of knowledge in each field of research, identifying influential works and critical authors, and even discovering new areas of interest. It is a valuable approach for assessing the evolution of a field and tracking how ideas and concepts develop over time. After reading the content of the articles, the R Bibliometrix software grouped them by research topic based on the keywords. As well as being grouped by theme, the grouping is organized by a network of co-citations in which the grouped themes assume different degrees of importance according to the number of citations each author has. The more significant the author’s impact, the larger the circle surrounding them. The co-citation matrix is analyzed using statistical techniques and algorithms. This makes it possible to identify groups of documents that are frequently cited together, revealing associations and trends in the field of research. In turn, the results of co-citation analysis can be visualized using network graphs, heat maps or other visual representations that allow researchers to identify clusters of related documents and understand how different topics are interconnected. Co-citation analysis is a powerful tool for identifying the structure of knowledge in each field of research, identifying influential works and key authors, and even discovering new areas of interest. It is a valuable approach for assessing the evolution of a field and tracking how ideas and concepts develop over time (Aria and Cuccurullo, 2017). This collation by R Bibliometrix enabled the definition/organization of the clusters listed above and their names. Figure 6 presents three clusters (red, blue, and green). Clusters.

Cluster content analysis has revealed that the topics addressed are as follows: • Cluster 1: Scientific mapping of digital accounting (in red) • Cluster 2: Digital records management (in blue) • Cluster 3: Digital skills (in green)

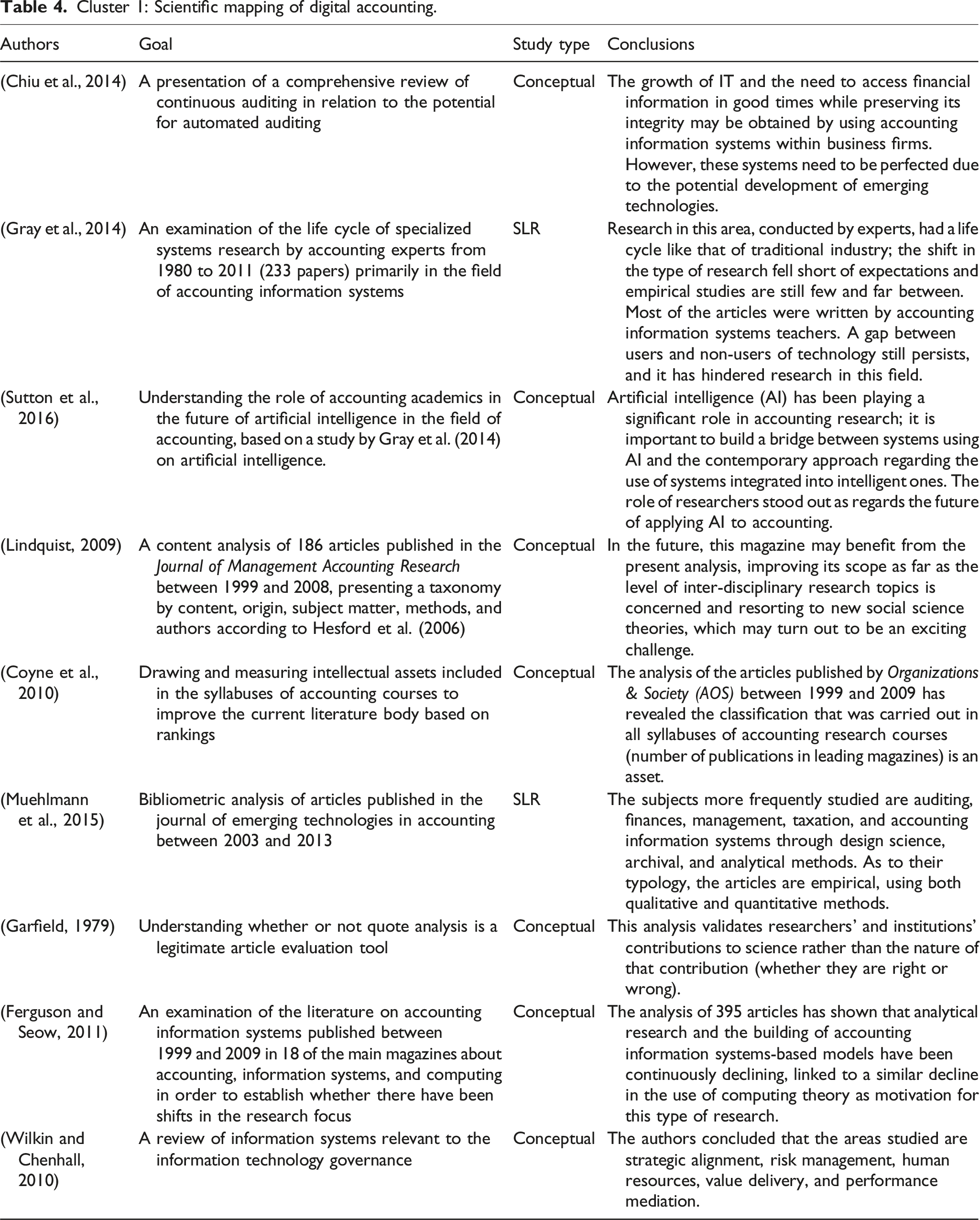

Cluster 1: Scientific mapping of digital accounting.

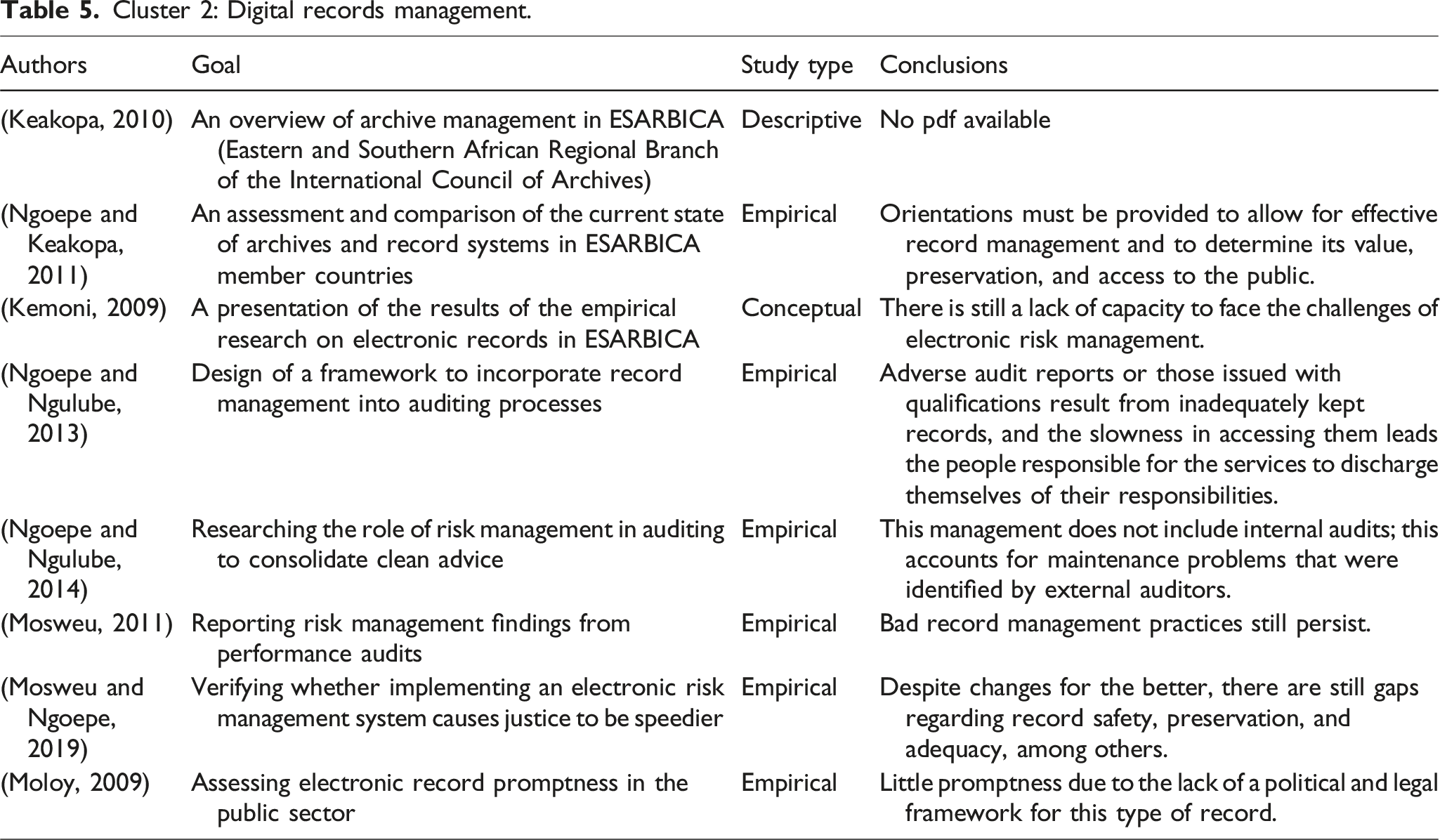

Cluster 2: Digital records management.

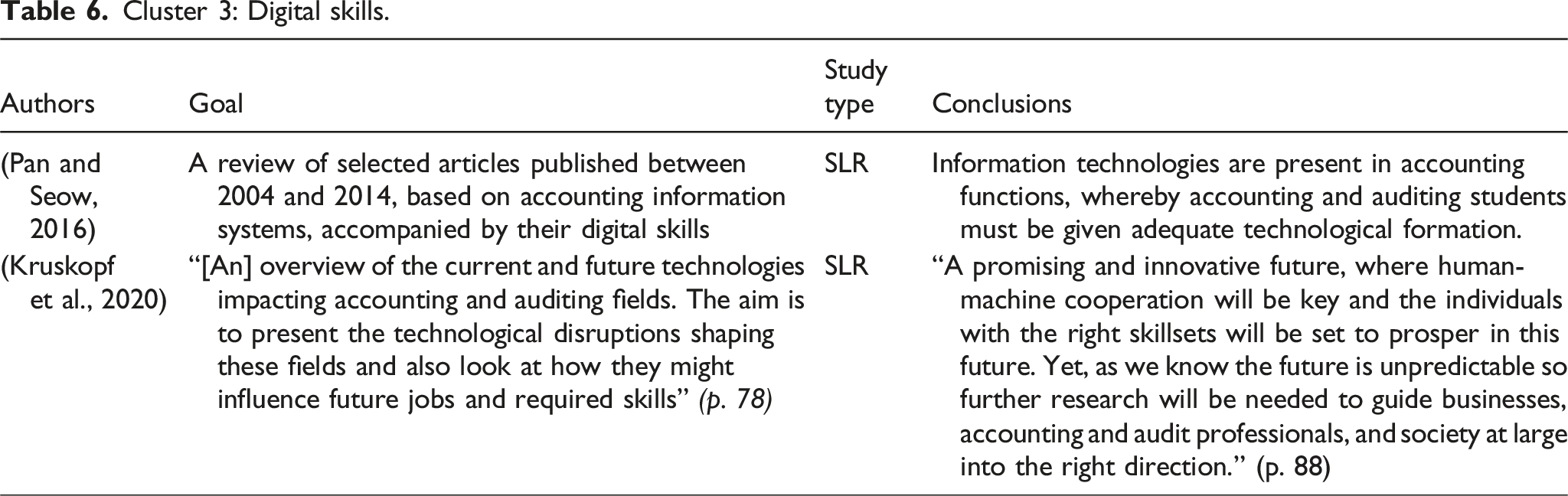

Cluster 3: Digital skills.

According to the information in Table 4, cluster 1 scientifically maps information systems-related topics, especially in what concerns accounting and its connection to auditing processes. It was possible to verify that this cluster is merely conceptual and theoretical and that some of its literature and conceptual reviews are based on a time classification when selecting the articles. Some of these studies present taxonomies regarding research methodologies and the most studied subjects. The cluster’s focus on theoretical articles shows not only that research on digital accounting is scarce, but also that there is no bibliometric analysis about it, which is proof of the present study’s pertinence in itself. In this scenario, this cluster allows one to say that digital accounting offers accounting services that include information technologies and information systems, thus providing extra time for the compilation and analysis of both financial and non-financial data that are important for customers. The continuous use of accounting information systems places accounting at a different level from its traditional one. Cluster 1 is centered on the field of information systems, suggesting that the studies included in this cluster were concerned with the intersection between information technology and accounting, given that information systems play a critical role in collecting, processing and analyzing accounting data. Some of these studies (e.g., Chiu et al., 2014) made a connection with auditing and its inherent processes, which is affected by information systems in a positive way, that is, the automation of auditing associated with technology improves the process of detecting fraud and accounting irregularities. Most of these authors have drawn up theoretical rather than empirical studies, to take an important step towards understanding digital accounting (e.g., Coyne et al., 2010; Garfield, 1979; Muehlmann et al., 2015). Finally, some studies present taxonomies (e.g., Lindquist, 2009), which means that they create classification or categorization systems to organize the research topics, and these studies also analyze the research methodologies used in studies related to information systems and accounting.

Additionally, if digital records are efficiently and effectively run, digital accounting leverages auditing processes, which brings us back to cluster 2. Cluster 2, represented in Table 5, deals with record management, albeit in a given region. The conclusions drawn from these studies are important to digital accounting insofar as it is based on digital/electronic records that are associated with some risks mentioned in this cluster, such as data integrity, safety, preservation, maintenance, and access, among others. Digital records render physical archive management-related administrative processes unnecessarily, reducing fixed costs inherent to them because information technologies turn documents into data that can be treated by an accounting information system, which reduces the time consumed in performing routine tasks. This means that documents are recorded and filed in the intelligent archive, as it is called, by similar characteristics. These procedures are only effective and efficient if rigorously managed. Therefore, leading managers must take management within the context of digital transformation very seriously since manual archives will tend to be replaced by digital ones that are associated with accounting information systems and are still the object of further development by the emerging technologies related to Big Data and artificial intelligence. Digital Records Management refers to the practice of managing records and documents in digital format within an organization, which involves the proper creation, storage, organization, retrieval and disposal of digital records throughout their lifecycle. If this management is effective, it is essential to guarantee integrity, authenticity, accessibility and compliance with digital documents over time. Despite this, the conclusions of the studies included here indicate that the associated risks persist, that precise indications are emerging for the effective management of these archives, and that there is an urgent need to work on the preservation and adequacy of records, among others (Ngoepe and Keakopa, 2011). In addition, the management of these archives is essential for bridging the gap with audits (Mosweu, 2011).

Finally, cluster 3 launches a challenge to the bridge that is being built between digital accounting and the certified accountant’s essential skills. Digital accounting refers to the use of information technology, software and digital systems to carry out accounting and financial tasks, which integrates the automation of accounting processes, the creation of digital records, the analysis of financial data with the aid of software tools and the use of electronic accounting management systems. The aim is to improve the efficiency, accuracy and accessibility of financial information within an organization. Nonetheless, this requires professionals in the field to acquire digital skills to effectively use the tools and technologies available to conduct accounting and financial tasks efficiently, accurately and securely. These skills are increasingly valued in the labor market and are essential for accounting professionals seeking to remain up-to-date and competitive in a constantly evolving digital environment. Pan and Seow (2016) advocated the need to transform the curricula of undergraduate students to cope with this incessant and almost obligatory move towards digital accounting. It is argued that the same applies to those who have already graduated in accounting and management, so that accountants must be continuously learning and master information technologies, besides having soft skills, such as (1) the ability to communicate remotely, which includes high interpersonal skills, mastering collaboration tools, and being sensible to other cultures and languages; (2) good oral communication skills, encompassing the creation of critical value to third parties, the use of multimedia contents, and the ability to systematize information; (3) agility and flexibility before change, uncertainty, and risks; (4) the ability to be creative and to innovate, that is, to think outside the box and develop new, creative, and innovating ideas; (5) willingness to be an entrepreneur and, this way, keeping their motivation high, attending training courses in new tools, and clearly defining goals and priorities; (6) the ability to efficiently manage time and provide the required information in due time; (7) the ability to automate all routine tasks, and (8) the willingness to relearn every day, fostering knowledge sharing and transfer. These arguments are in line with Kruskopf et al. (2020), who postulated how technological disruptions can influence future jobs and the skills they will require, is to present the technological disruptions that are shaping these domains and to analyze how they might influence future jobs and the skills required.

Some heterogeneity is perceived in the publications over time to the authors of the documents, for example: (1) A curious study applied animal health information systems in a hospital that “...has a digital accounting system, which is widely used in Japan, having a support of maintenance contract that operates to download data by remote control” (Tanaka et al., 2017: 2). This research includes the remaining authors who published in 2017 (Tanaka, N.; Takizawa, T; Tanaka, R.; Okano, S.; Funayama, S.; Iwasaki, T), and who continued researching in 2019 in “two referral hospitals for companion animals [that] have the same digital accounting system, which is the most widely used hospital management system in Japan. The system is supported by a remote-controlled system under a maintenance contract” (Tanaka et al., 2019: 298); (2). From 2019 onwards, academics’ interest in digital accounting has grown, although publications are still few and far between. Lehner, for example, published three articles on digital accounting as a co-author: (a) According to Lehner et al. (2019), digital accounting is increasingly being regarded as a common language among accountants and an early competitive advantage; also, they advocated for future research to be conducted from an organizational, individual, regulatory, innovative, and ethical standpoint; (b) Kruskopf et al. (2020) presented an overview of information technologies’ impact on accounting and auditing; (c) Leitner-Hanetseder et al. (2021) approached accountants’ functions through artificial intelligence, emphasizing the idea that the latter is going to cause paradigmatic changes in accounting professionals. Other authors like Chiu et al. (2019) and Liu et al. (2021) published articles each referring to bibliometrics regarding digital accounting and information technologies.

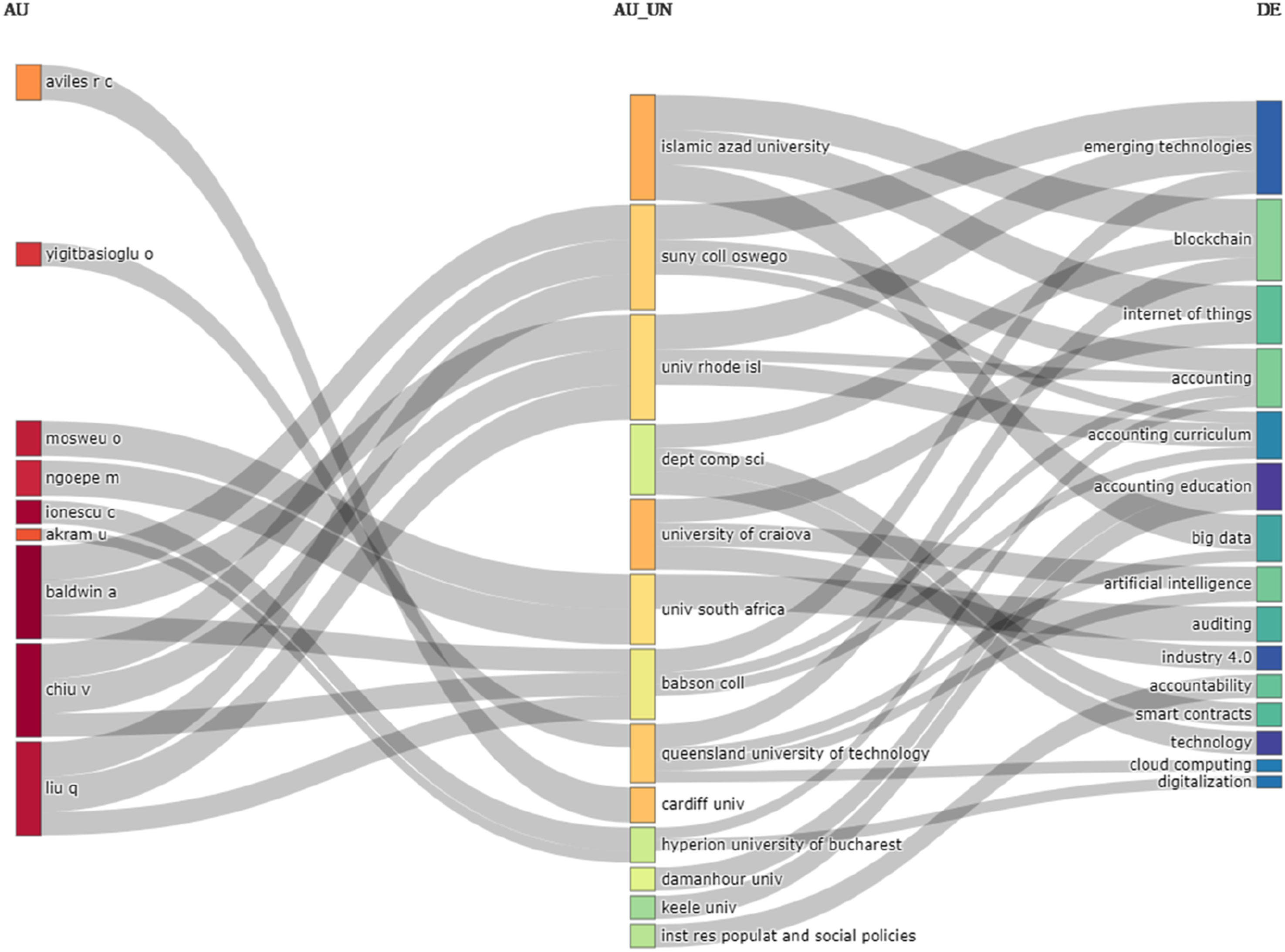

Finally, Figure 7 highlights bibliometrics in the authors, the universities in which they work, and the subjects they have been researching. Bibliometric view of authors, universities, and research subjects.

Figure 7 uncovers a relevant interaction network between teachers and universities at the publication level, which comprises: (a) Authors of single-authored documents (n = 5); (b) Authors of multi-authored documents (n = 51); (c) Documents per Author (0.429); (d) Authors per Document (2.33); (e) Co-Authors per Documents (2.96); (f) Collaboration Index (2.68). It goes to show that scientific knowledge dissemination among authors and their respective universities is important. Particularly relevant, according to Figure 5, are Chiu et al. (2019) and Liu et al. (2021), whose red rectangles are the biggest, meaning they publish more. As to the subjects studied, emerging technologies and digital accounting stand out (green bigger rectangles).

In short, bibliometrics has shown that this subject is still in need of further empirical and conceptual research, given that it involves little studied constructs, and the current research is still limited to few authors and more frequently associated with information systems, which, by no means, exhausts the subject.

Conclusions and implications

The present bibliometric analysis of the research on digital accounting shows that the number of publications in this field has been steadily increasing since 2019. Due to its being recent, digital accounting needs to be further researched to enhance the evolution of scientific knowledge, exploring recent technologies and putting it at the service of accounting. The growing number of publications focuses on topics related to emerging accounting technologies, accounting information and accounting systems, and the quality of accounting and auditing services. The approach to these subjects unequivocally demonstrates that the current services rendered by accounting are becoming more and more digital, therefore requiring accounting professionals to acquire new skills that will bear on their future as accountants.

The fact that accounting is intimately linked to small, medium, and large business firms and enterprises of all types and sizes has raised the interest of researchers dealing with business management. Executive managers regard accounting as a valuable management tool that provides themAccounting is regarded as a management tool that provides them with timely organizational agility in decision-making processes. In fact, business organizations constantly must face increasingly disruptive and volatile business environments, to which the appropriate positive response is organizational agility.

Another important finding ensuing from this bibliometric review has to do with the scarce number of quotes in the articles due to their recent date of publication.

The content analysis of the articles revealed three lines of research, here represented as Cluster 1—scientific mapping of digital accounting; Cluster 2—digital records management; and Cluster 3—digital skills. These research lines point to digital accounting being an emergent, current research subject, which emphasizes the relevance of the present study. From reading the articles included in each cluster, it was possible to conclude that digital accounting integrates information technologies and information systems into accounting services, leaving accountants with more time to compile and analyze financial and non-financial data that are important to customers.

Thus, the continuous use of accounting information systems takes accounting to a whole different level.

On the other hand, the clusters draw attention to digital records’ usefulness since they allow for the elimination of administrative procedures inherent to physical archive management by reducing fixed costs associated with them; actually, information technologies turn documents into data that can be treated by an accounting information system; in turn, this reduces the time consumed in performing routine tasks. Documents are recorded and filed in the intelligent archive, as it is called, by similar characteristics.

The arguments above direct this research towards the implications of digital accounting for effective accounting practices, namely, (i) Digital accounting allows the automation of manual accounting tasks, such as data entry, reducing human errors, improving efficiency, and freeing up time for value-added activities, like strategic financial analysis; (ii) With digital systems, financial information is available in real time, which facilitates decision-making based on more accurate and timely information; (iii) Digital accounting paves the way for advanced financial data analysis (big data and artificial intelligence), providing deeper inputs/outputs and more accurate forecasts of the company’s financial performance; (iv) It can make international standardization more widespread, enabling greater comparability of the financial reports of companies operating internationally; (v) It leads to greater transparency of the company’s financial cycle, ergo greater stakeholder legitimacy; (vi) It explains the need to adopt accounting systems with other business systems, such as enterprise resource planning (ERP) systems, to ensure more efficient data exchange and eliminate duplication of effort; (vii) Auditors can benefit from digital accounting, as they can access financial records more efficiently and perform audits in real time, identifying anomalies or fraud more easily. (viii) Companies must implement strict security measures to protect their information; (ix) implementing digital accounting involves analyzing implementation costs and data security.

In summary, manual archives tend to be replaced by digital ones associated with accounting information systems that are still being developed by emerging technologies dependent on Big Data and artificial intelligence. Therefore, accountants must be willing to embrace continuous learning and master information technologies, besides having soft skills such as remote collaboration, good oral communication, creativity, and innovation, as well as the ability to do effective time management, provide all the requested information in due time, automate all routine tasks, and learn something new every day through knowledge sharing and transfer.

However, digital accounting has theoretical impacts on the way financial information is collected, processed, and utilized, of which the following stand out: (a) The Paradigm Shift: Digital accounting represents a paradigm shift from traditional paper-based accounting, which implies making the transition from physical records to electronic/digital records, thus fundamentally changing the way financial data is recorded and accessed; (b) Real-Time Accounting: It means that digital accounting allows companies to keep financial records in real-time, where information is always up-to-date, providing a more accurate and just-in-time view of the company’s financial situation. This entails a change in the way financial reports are generated and in decision-making based on real-time information; (c) Automation: This plays a central role in digital accounting, since manual data entry tasks are replaced by automated systems that collect and process financial information, increasing efficiency and accuracy and reducing potential errors; (d) Big Data and Advanced Analysis: With digital accounting, companies can collect large volumes of financial data, which represents a window of opportunity for advanced analyses, such as big data and artificial intelligence; (e) Cybersecurity and data privacy: These are considered critical, for it is crucial to protect financial information from threats; (f) International accounting standards: Since digital accounting often involves adopting international accounting standards, such as IFRS, it is important that the accounting theories applied continue to ensure compliance and international comparability; (g) Adaptation Skills: Digital accounting challenges the evolution of existing theories; therefore, traditional theories must be adapted to deal with the new challenges and opportunities presented by digital technology; (h) Transparency and Accountability: These are aspects that can increase the transparency of companies’ financial operations, revealing theoretical issues related to accountability to shareholders, regulators, and other stakeholders; (i) Skills Acquisition: The transition to digital accounting requires a new set of skills for professional accountants.

In short, digital accounting affects accounting practice but also has significant theoretical implications in how accounting principles are perceived and applied in a digital and constantly evolving environment. This represents a fundamental change for accounting, demanding that traditional theories be adapted to better meet the challenges of the digital world.

Due to rapid technological evolution, digital accounting is profoundly transforming the professional landscape of the accounting field. This change entails a series of implications for accounting professionals, who consequently need to adapt and develop new skills so that they can continue to be competitive in the labor market. These skills and competencies go way beyond traditional technical knowledge. Accountants are expected to master new technologies such as accounting management software, cloud storage platforms, and data analysis tools. In addition, they must have the ability to interpret data, identify trends, and provide strategic insights for clients. Digital accounting makes it possible to automate repetitive, manual tasks such as posting invoices, reconciling banks, and generating reports. This frees up professionals to engage themselves in more strategic activities, like data analysis, tax planning, and financial consultancy.

The vast amount of data available in the digital age urges professionals in the field to develop data analysis skills that allow them to extract relevant information and make strategic decisions. In such a context, the ability to interpret financial and accounting data, identify trends, and provide insights for clients becomes a competitive differentiator. Digital accounting makes room for professionals to act as strategic advisors to their clients, offering insights and recommendations to improve financial management and business performance. The ability to analyze data, identify opportunities for improvement, and provide personalized solutions becomes instrumental.

The profile of the professionals in this field is drastically changing because, in addition to technical knowledge, they are required to be able to communicate, show leadership, and possess critical thinking and problem-solving skills. Also essential is the ability to work as a team, adapt to change, and be continuously learning. Actually, digital accounting poses difficult challenges such as the need for constant updating, fierce competition, and data security, but it also gives professionals the opportunity to act as strategic consultants, develop new skills, and work more efficiently and productively.

The increasing use of data and technologies in digital accounting increases the importance of ethics and transparency. Professionals need to ensure the integrity of data, rules and regulations, and the confidentiality of client information. That is why it is essential to invest in ongoing education and courses, workshops, and event attendance to keep up-to-date with new technologies, trends, and regulations. Digital accounting allows professionals to work remotely and more flexibly, which can translate to greater quality of life and autonomy. Conversely, working remotely with efficiency requires discipline, organization, and communication skills.

Digital accounting can also have an impact on professionals’ remuneration. The more they master new technologies and exhibit strategic skills, the higher their salaries and the better their career opportunities.

This study proposes to further the global agenda on digital accounting research, shedding some light on what has been studied so far and encouraging future researchers to continue researching a subject that is certainly more than a hope for the future; it is a certainty for the present.

Limitations and future research agenda

All research has limitations that must be taken into account. Although this study was based on reference databases like WoS and SCOPUS, the few scientific articles on digital accounting that have been published so far did not allow for a more robust analysis, be it at the level of quantitative statistical content or qualitative content analysis. Bibliometric analysis, a quantitative methodology that uses publication and citation data to map and evaluate scientific production, has become an indispensable tool for researchers in any field of knowledge. Despite its growing popularity, it is crucial to recognize that bibliometric analysis has important limitations that can affect the interpretation of data and lead to erroneous conclusions. One of them, and probably the most important one, lies in the quality and coverage of the databases; it is proven that the latter index only a fraction of the world’s scientific literature, leaving out a significant number of publications, such as lesser-known journal articles, “grey” literature (reports, unpublished theses, and works in less common languages). This incomplete coverage can lead to a distorted representation of scientific production in a given field, favoring authors and institutions that publish in more visible journals. Therefore, despite its usefulness, bibliometric analysis is not a perfect tool and has limitations that need to be considered. In other words, when using bibliometric analysis, it is important to be aware that the results obtained are only a partial picture of reality and should be interpreted with caution, considering the biases of the databases, the limitations of the indicators, and probable methodological problems.

In the future, there should be more studies that could result in empirical articles in this field to help publications in this area grow. A good example of this would be the conducting of comparative studies on how digital accounting is used in different countries.

Finally, there should be more studies that highlight digital accounting’s usefulness and how it may contribute to the necessary changes in the accounting profession, going over those issues that are inherent to digital accounting, namely, the use of digital technologies, software, and tools to perform accounting tasks and processes. Digital accounting involves the automation and digitization of accounting functions that were traditionally performed manually or through paper-based systems. It also leverages technology to streamline and optimize various accounting processes, such as bookkeeping, financial reporting, budgeting, and analysis.

From what has been said before, there are several key aspects of digital accounting to be included in the future research agenda, namely, (1) Software and Tools—Digital accounting relies on specialized accounting software and tools that automate and simplify tasks such as data entry, ledger maintenance, invoicing, and financial statement preparation. These tools often offer features like data integration, real-time updates, and advanced reporting capabilities; (2) Cloud Computing—Cloud-based accounting platforms allow businesses to access their financial data from anywhere, at any time, using internet-connected devices. Cloud accounting solutions offer benefits such as data security, scalability, collaborative features, and automatic backups; (3) Automation—Digital accounting incorporates automation to minimize manual intervention in repetitive tasks. For example, bank feeds can be automatically imported into accounting software, reducing the need for manual data entry. Automated processes enhance efficiency, reduce errors, and free up time for accountants to focus on analysis and decision-making; (4) Data Analytics—Digital accounting enables the collection and analysis of large volumes of financial data. With the help of data analytics tools, businesses can gain insights into their financial performance, identify trends, detect anomalies, and make data-driven decisions. (5) Integration and Connectivity—Digital accounting systems can integrate with other business software, such as customer relationship management (CRM), inventory management, and payroll systems. This integration facilitates seamless data flow between different systems, eliminating the need for duplicate entries and enhancing overall operational efficiency.

In conclusion, digital accounting places several benefits at everyone’s disposal, including improved accuracy, faster processing, enhanced data security, cost savings, and greater accessibility to financial information. It enables businesses to make informed decisions based on real-time financial data, improves collaboration between accountants and stakeholders, and provides a solid foundation for digital transformation in finance and accounting functions.

Footnotes

Acknowledgments

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge financial support from National Funds of the FCT – Portuguese Foundation for Science and Technology within the project «UIDB/04007/2020».