Abstract

We draw on Social Exchange Theory (SET) and show that a “succession dance”—a phase of joint successor and predecessor activity inside the firm—occurs due to prior social exchanges between successor and predecessor. It can be guided by altruism, friendship, or partnership (i.e., a generalized exchange relationship) as well as a professional need for informational and material social exchanges at the firm-level (i.e., a restricted exchange relationship). By utilizing mixed methods encompassing quantitative data on 522 CEO successions in family firms and qualitative data from 34 in-depth interviews, we find support for these coherences. We also discuss how altruistic versus transactional motives for predecessors to remain active inform the burgeoning debate on positive versus negative nature repercussions of prolonged predecessor activity.

Introduction

Organizations often become attuned to the idiosyncratic characteristics of their leaders, which can affect firm behavior, norms, strategy, and performance (Bigley and Wiersema, 2002; Miller, 1992, 1993; Sonnenfeld and Spence, 1989). The prevalence of this phenomenon increases with the power of the CEO and is likely to be strongest when ownership and operative leadership coincide—as is regularly the case in family firms (Anderson and Reeb, 2003; Hambrick and Finkelstein, 1987; Quigley and Hambrick, 2012). In CEO successions, then, this attunement gradually re-centers from the old to the new CEO (Carroll 1984; Dyck et al., 2002; Handler 1990). Especially in family firms, incumbent CEOs stay engaged with the firm in one way or another (Karlsson and Neilson, 2009; Sonnenfeld and Spence, 1989). As these CEOs influence can be substantial during this transition period (Quigley and Hambrick, 2012), recent family firm research highlights investigating such prolonged predecessor involvement as to understand post-succession firm outcomes and performance (Ahrens et al., 2018; Querbach et al., 2020; Zybura et al., 2021). Yet despite this relevance (Dyck et al., 2002; Handler, 1990; Le Breton–Miller et al., 2004; Mitchell et al., 2009; Sharma et al., 2003b), the antecedents of prolonged predecessor activity following CEO successions in family firms are largely unexplored (Brickley et al., 1999; Umans et al., 2020).

We therefore raise the following research question: What drives continued predecessor involvement subsequent to CEO successions in family firms? We assess this question by drawing on Social Exchange Theory (SET) which fundamentally conceptualizes human interactions as social exchange and thereby explains human behavior (Blau, 1964). In particular, we posit that prior social exchanges inside families owning the firm, prior exchanges at the firm-level that affect work relations, as well as the necessity of further exchanges between successor and predecessor CEO can help to explain a prolonged predecessor activity. More specifically, the exchange inside the family members often nurtures strong relationships based on trust, joint understanding (including the vision of the firm), coherence, and mutual support (Ahrens et al., 2019; Daspit et al., 2016; Long and Chrisman, 2014). Consequentially, a family predecessor may wish to assist in facilitating a smooth family succession inside the firm and to support the next generation in their first steps, and this results in prolonged activity (Davis et al., 1997; Kerkhoff et al., 2004). Similarly, and irrespective of family ties, if prior social exchanges between successor and predecessor at the firm result in a good work relationship that is based on the constructive norms of partnership (or even friendship), then a similar motivation will facilitate prolonged activity (Cropanzano and Mitchell, 2005; Hall and Nordqvist, 2008; Le Breton–Miller et al., 2004). Moreover, we argue that when the CEO-related skills of the successor are not yet fully developed, the need for a prolonged mentoring relationship (Waldkirch et al., 2018) for transfer of the required stock of knowledge and abilities arises (Dyck et al., 2002; Handler, 1990; Hatak and Roessl, 2015; Le Breton–Miller et al., 2004). Likewise, we argue that when the organization is young and the founder generation’s knowledge has not yet diffused to second row management, a necessity of further exchanges fuels predecessor activity (Ahrens et al., 2018; Carroll, 1984; Miller and Friesen, 1980). Further, we posit that ownership transfer preceding or coinciding with the leadership transition decreases the odds of predecessor activity since the full transfer of benefits and risks of ownership decreases the motivation to stay active (Boeker and Karichalil, 2002; Fredrickson et al., 1988). Relying on a mixed methods approach that includes an encompassing quantitative dataset of 522 CEO successions in medium-sized German family firms, 32 qualitative in-depth interviews with CEO successors in comparable firms, and two complementary expert interviews, we find considerable support for these coherences.

Our paper makes several contributions. First, adopting a SET perspective, we empirically highlight several important drivers of prolonged predecessor involvement in family firms (Blau, 1964; Long and Chrisman, 2014). Thereby, we offer evidence for an early conjecture by Handler (1990), who depicted succession in family firms as a complex “succession dance,” in which a predecessor phases out and a successor phases in. Second, we contribute to literature on the antecedents of “succession dances” by introducing SET to examine drivers of this phenomenon leading to variation across family firms (Blau, 1964; Daspit et al., 2016; Thibaut and Kelley, 1959). Seeing succession through the lens of SET helps us to derive exchange constellations that affect the post-succession period by closing skill gaps and facilitating the transfer of knowledge (Hambrick and Fukutomi, 1991; Royer et al., 2008; Waldkirch et al., 2018). Moreover, SET enables us to perceive succession as an event shaped by prior familial exchanges as well as workplace exchanges, explaining prolonged predecessor activity via altruism, reciprocity, and mentoring. Third, we show that the classical stage models (Churchill and Hatten, 1997; Le Breton–Miller et al., 2004; Longenecker and Schoen, 1978) which explore the predecessor–successor relationship might be imprecise in capturing important features of the succession process. Such models regularly overlook long years of predecessor–successor overlap post-succession, a reality for more than three quarters of the cases we analyzed. In this respect, our findings lend empirical support to a priorly mentioned apprenticeship/mentoring relationship between successors and predecessors (e.g., Cadieux, 2007). Finally, by casting a spotlight on the antecedent of predecessor activity, our work further informs the contemporary discussion on the double-edged impact of predecessor activity which is conceptualized to entail a dark as well as a bright side (see Ahrens et al., 2018; Mitchell et al., 2009; Sharma et al., 2003b). Particularly, this highlights that predecessor activity may also have dark-sided implications under certain circumstances and hinder the smooth transition of responsibilities to the successors.

Literature on succession in family firms & predecessor activity

Only a small amount of family firm research explicitly addresses the post-succession activity of a departing CEO, but agrees that predecessor engagement entails important downstream effects on major firm-level variables such as financial performance (Ahrens et al., 2018) or innovation (Querbach et al., 2020; Zybura et al., 2021). As such, the impact of predecessor retention on firms has been found to be both substantial and contingent: It ranges from positive, when successors still need to learn, to negative, or as one expert put it: “We all know the war stories of family members staying on too long to the detriment of the family and the business.” Moreover, its effect scales with the extent of the predecessor’s involvement (Ahrens et al., 2018; Querbach et al., 2020; Zybura et al., 2021). While research generally does not question the importance of departing CEO retention, the potential drivers of a continued exertion of influence still deserve research as these antecedents are uncharted terrain (Handler, 1990). This is surprising, as continuing predecessor activity within the company is a common phenomenon (Dyck et al., 2002). For example, in German family firms, the majority of family successions are characterized by an extended period of successor-predecessor overlap (Ahrens et al., 2018). In Japan, prolonged predecessor activity is even more common as over 80% of outgoing CEOs change roles to a board chairperson position and in North America about 50% of all stock-listed firms prefer a model with supportive, seasoned hands at the helm of the firm after CEO succession (Karlsson and Neilson, 2009). This is also mirrored in findings that only the minority of U.S. CEOs leave office (36%)/leave the board (12%) immediately upon retirement (Sonnenfeld and Spence, 1989).

Thus, although CEO successions might intuitively seem to occur at one point in time, they constitute a complex procedural phenomenon that can be considered as several stages involving multi-faceted challenges that are unlikely to be resolved at a single point in time, as outlined in Handler’s (1990) seminal succession process model. Her theoretical framework based on qualitative work specifically includes a predecessor-successor overlap and importantly details that the predecessor also stays active post-succession, with fading involvement over time. She describes succession as a multi-stage process that focuses on slow-and-subtle, mutual role adjustments between the incumbent and the successor, and coins the phrase “succession dance” for this process. Central to Handler’s (1990) conjecture of a succession dance is the reciprocal nature of the process: Handler (1990) describes a predecessor who successively lowers his/her involvement and the associated old habits of his/her prior leadership paradigm as a successor gradually takes more influential roles in the firm. Moreover, she describes how relinquishing ownership is a difficult and very sensitive step for incumbents in this process, while the adjustment itself seems to be guided by the increasing abilities of the next generation. Le Breton–Miller et al. (2004) further divides Handler (1990)’s succession process into (a) an establishment of ground rules, (b) nurturing and development of the group of potential successors, (c) selection, and (d) final handover to the chosen successor. Cadieux (2007) builds on this research to break down succession into a process that undergoes four different phases: “initiation, integration, joint reign, and withdrawal.” She posits that the roles of the predecessor and the successor will mutually evolve over this period of adjustment: Post-succession predecessor involvement decreases over time as the old CEO’s influence fades out and the successor phases in (Cadieux, 2007; Handler, 1990).

While all these stage models seemed to share a common grounding and point towards a process of mutual adjustment, they did not put the succession dance conjecture to a rigorous test. However, these stage models allow us to highlight an interesting theoretical perspective which is linked to social exchanges that have overarching implications for understanding the outcomes of succession processes, in particular for detailing the predecessor activity and mutual adjustment in the “final handover” phase. In this final phase, all stage models lack detail (including those of Longenecker and Schoen (1978) and Churchill and Hatten (1997)), thus it is the predecessor’s activity in this final phase, when the successor has already taken a CEO position, that is focal in our mixed-methods study.

Theory development

As a broad umbrella theory, SET is capable of maneuvering the puzzling multi-level and multi-phase context of a family firm succession (Blau, 1964; Coleman, 1986; Handler, 1990). Moreover, SET enables a coherent analysis of conditions that facilitate or hinder predecessors’ post succession activity. For instance, its breadth allows an interlinked theorizing across pivotal obligations and preferences resulting from social relationships, while at the same time accounting for a need for non-social, that is, more material, informational, or transactional exchanges that regularly occur during succession (Long and Chrisman, 2014).

At its heart, SET sees human interaction as the exchange of resources, be they social or material in nature (Long and Chrisman, 2014). Social Exchange Theory postulates that continual exchanges lead to the emergence of social norms and structures, which, in turn, foster the formation of behavioral expectations and obligations, as well as a shared frame of references and vision (Emerson, 1976; Granovetter, 1985; Simmel, 1909). Furthermore, having its roots in sociology, SET considers exchanges to be based on the contexts in which they are embedded. For instance, an exchange may either occur as part of a familial relationship between mother and daughter or in a more transactional or contractual setting, such as in an unrelated business environment or also in every-day life, for instance when paying for goods received in return. Social Exchange Theory thus categorizes exchanges into two broader groups: restricted exchange versus generalized exchange, depending on the reciprocity of the exchange (i.e., whether a direct compensation is requested or no prompt or equal complimentary return is expected) (Daspit et al., 2016; Ekeh, 1974; Meeker, 1971). Generalized exchange typically occurs, for example, within families and between family members, or within partnerships or strong friendships where the relation and accordant commitments and obligations are so strong that a return might not even be expected (Long, 2011; Long and Mathews, 2011). Parents who care for their offspring are an excellent example, as they typically give more than they can reasonably expect to get back in return. In contrast, norms of direct reciprocity, potentially based on economic value or market value in extreme cases, which are central to relationships that have a contractual, instrumental, or competitive contest-oriented character are fundamental to restricted exchange (Daspit et al., 2016).

Social exchange and predecessor activity in the family firm

The years of exchange inside a family, for example, in a parents-child relationship, almost certainly evoke a constellation of stable kinship relationships characterized by mutual trust, commitment, and a shared vision for the family (Chua et al., 1999; Long and Chrisman, 2014; Pearson et al., 2008). In families influencing a firm, this vision regularly extends to the firm which often represents the embodiment of the familial economic aspirations (Zellweger et al., 2012). Likewise, in this context such relationships are also carriers of obligation and responsibility—the product of prior generalized exchange, as parents typically give more than they get in return (Cropanzano and Mitchell, 2005; Miller et al., 2003). As a result, the family predecessor may feel a heartfelt wish to responsibly ensure a smooth within-family succession and the perpetuation of the firm as a family business (Calabrò et al., 2018). With such altruistic intentions, senior CEOs are likely to intend to help procure the family’s wealth and to secure the fortune of the business upon stepping down when the next family generation succeeds to the helm of the firm. Predecessor activity is thus guided by the norms of generalized exchange (Astrachan and Jaskiewicz, 2008; Kerkhoff et al., 2004; Le Breton–Miller et al., 2004; Levinson, 1971). In this case, post-succession resource exchanges are more likely to take the form of (potentially partly or even fully voluntary) support and assistance via reduction of the successor’s job burdens via the predecessor. Moreover, even the physical presence of the predecessor at the firm may be perceived as a resource exchange itself. In exchange, the predecessor is rewarded for this via utility and a sense of fulfillment. On the other hand, in case of non-family successors, pivotal relationships often run under the norms of restricted exchange (Ekeh, 1974) and are typically characterized more by a professional and less familial stance such that the above-described coherences connected to familial altruism as an exchange motive are not at work and will not evoke prolonged predecessor activity. Therefore, we posit:

The likelihood of observing post-succession predecessor activity is higher when a family CEO successor is installed.

A different, but closely related aspect relates to those social exchanges between successor and predecessor that occur prior to and during succession at the firm-level as work interactions which—beyond a family or non-family origin of the successor—also shape and affect the work relationship between successor and predecessor (Blau, 1964; Daspit et al., 2016; Emerson, 1976). Due to repeated human interaction at the firm, social structures and social capital may have emerged or may have been fostered among exchange participants (successor–predecessor), such as a sense of trust, mutual support, and potentially even a shared identity or vision for the firm as part of a good work relationship (Emerson, 1976; Long and Chrisman, 2014; Pearson et al., 2008). In fact, the family firm succession literature assigns a central role to the successor–predecessor relationship as it is known to affect the chances of successful transition (Le Breton–Miller et al., 2004; Miller et al., 2003; Shi et al., 2019). Such a harmonious work relationship is likely to affect the future exchanges, including predecessor activity: As Meeker (1971) and Emerson (1976) note, the emergence of elements of social capital in an exchange relationship in turn affects the exchange rates (or prices, in more economic terms) between exchange participants. Therefore, harmonious work relationships between predecessor and successor, which can also be achieved by successful non-family CEOs (Blumentritt et al., 2007), should improve the cost-reward structure of prolonged predecessor activity making it more attractive for both successor and predecessor (Homans, 1961). Moreover, intact working relationships instill and foster a sense of belonging and embeddedness in a professional environment, and reciprocity norms may trigger offers of support that are guided by the predecessor’s intention to see the successor master the passage of succession as well as possible, making predecessor activity as a form of generalized exchange more likely (Gouldner, 1960; Holtom et al., 2008; Mitchell et al., 2001). In this scenario, the resource exchanges during the post-succession period are likely to be influenced more by friendship and professional partnership, akin to the collaborative relationship between two policemen on extended patrol duty. These exchanges may also entail the availability of the predecessor’s resources post-succession and the predecessor’s collegial support at the helm of the firm in return for remuneration (potentially below market prices) and potentially a flow of utility in exchange for each other’s presence (potentially for both sides due to the intact work relationship). Therefore, we posit:

The likelihood of observing post-succession predecessor activity is higher when the successor-predecessor work relationship is harmonious.

Human capital in general can be defined as resource endowments which affect future economic success of individuals (Becker, 1964). A specific form of such capital, CEO-relevant (or managerial) human capital, is deemed as an important constituent of the managerial capabilities and is shown to have a strong impact on the quality of managerial decisions, strategic change, and organizational performance (Helfat and Martin, 2015). CEO related human capital may be formed via various factors such as leadership experience, industry knowledge, academic education or professional training, and is important for success of family business leaders (see Skorodziyevskiy et al., 2023), especially in turbulent succession contexts (Istipliler et al., 2022). From a SET perspective, lack of such human capital may give rise to a professional demand that can lead to a situation where the predecessor transitorily stays on board after passing on the baton to his/her successor (Ahrens, 2020; Ahrens et al., 2019; Handler, 1990). Specifically, a general lack of human capital, independent of a family/non-family succession, may create a need for the current CEO to stay longer (Le Breton–Miller et al., 2004). With the help of a leadership overlap, the successor might learn crucial insights that increase his/her leadership ability (Block, 1993; Le Breton-Miller and Miller, 2015; Le Breton–Miller et al., 2004). Indeed, prior research finds a positive association for high successor CEO-related human capital and firm performance in the period following succession and makes successor CEO human capital a central factor affecting the fate of successions in family firms (Ahrens et al., 2019; Pérez-González, 2006). Thus, when successor CEO-related human capital is not yet fully evolved, a period of adjustment and mentoring via prolonged predecessor activity during which information and leadership insights are exchanged between predecessor and successor seems to be essential (Dyck et al., 2002; Handler, 1990; Le Breton–Miller et al., 2004; Ren and Zhu, 2016). Such post-succession resource exchanges may even be part of a contractual succession agreement where the predecessor is remunerated in exchange (with pecuniary rewards, but potentially also with prolonged power). Likewise, this requirement for informational resource exchange in the post-succession period dissolves once the successor has acquired the relevant knowledge, which leads to the “mutual adjustment” described by Handler (1990) which is guided by the successor’s competencies: the predecessor steps back after a period of overlap (Cadieux, 2007; Handler, 1990).

Vice versa, a well-prepared, highly skilled successor and his or her predecessor may perceive that an extended period of joint reign is not nearly as rewarding as in the other case (Ahrens et al., 2018; Hambrick and Finkelstein, 1987; Virany et al., 1992). In this case, the exchange relationship transforms to a net negative for the successor due to a potential loss of successor discretion, while the predecessor needs to be remunerated for his/her superfluous services. Thus, to avoid issues such as those related to curbed successor discretion or commitment to the status quo where continued incumbency of the predecessor may be dysfunctional for the firm (Geletkanycz and Black, 2001; Hambrick et al., 1993; Hambrick and Fukutomi, 1991; Quigley and Hambrick, 2012), the implication is that the predecessor can retire rather quickly and completely from his/her business-related obligations.

As such, the above coherences describe a setting of contingent demand for restricted exchange—that is, a professional exchange of human capital between successor and predecessor in a professional setting—provided this is necessary. Therefore, we posit:

The likelihood of observing post-succession predecessor activity is negatively related to the successor CEO’s human capital.

In a similar vein, but in nuances different from the above argument, informational exchanges which are related to the predecessor’s person-centric firm knowledge (i.e., independent of the successor’s ability) may also become necessary during family firm succession (Ahrens et al., 2018). This is particularly the case in younger family firms. In such a context, crucial firm-specific knowledge and the “tricks of the trade” are often still captured, for example, in the founder and in those at the helm of the firm in its early years (Carroll, 1984), and have not yet diffused across the firm, which makes the predecessor a central informational nexus that is difficult to substitute (Adams et al., 2009; Miller and Friesen, 1980). By contrast, mature family firms have gathered experience with successions and thus have often professionalized further (Rubenson and Gupta, 1992), such that essential knowledge has been made exchangeable and is now likely to be more decentralized across agents in the firm and the family, which makes the mature family firm more self-contained and independent of the incumbent because it can avail itself of a redundancy of competencies (Ahrens et al., 2018). Therefore, we argue that, in younger family firm successions, there is often a need for a restricted informational exchange beyond CEO-related human capital, which increases the likelihood of predecessor activity in the post-succession phase. In the post-succession phase, this increases the likelihood of resource exchanges which are characterized by the access to and the flow of firm specific knowledge from the predecessor to the successor in return for prolonged power, monetary reward, and utility. Hence, we posit:

The likelihood of observing post-succession predecessor activity is positively related to successions in early generation family firms.

Arguably, there are two central aspects to succession processes in family-owned businesses: the transition of leadership and the transition of ownership (Le Breton–Miller et al., 2004). Therefore, one important dimension of succession concerns the exchange of ownership (Barry, 1975) which, from a SET perspective, constitutes a material exchange between predecessor and successor (Blau, 1964; Long and Chrisman, 2014). We argue that the temporal occurrence of this exchange has significant implications at the firm-level, especially on the observation of prolonged predecessor activity that may be motivated by the obligation and duties, but also amenities, that ownership evokes (Rubenson and Gupta, 1992; Wasserman, 2003). For example, ownership might endow a predecessor with status and a long-term orientation (Le Breton–Miller and Miller, 2006), while the barriers to retirement for a departing CEO may include a substantial loss in terms of status or mission (Handler, 1990; Sonnenfeld, 1991). However, once the exchange of ownership is put into effect, the successor has acquired firm ownership and the responsibilities, liabilities, and private benefits have shifted to the next leader, the predecessor’s endowment is considerably lower. Regardless of the exchange relation, this will deteriorate the cost-reward structure of predecessor activity for the predecessor (Handler, 1990; Homans, 1961). Accordingly, this dissolves an important exchange condition and the predecessor’s engagement can be reduced as barriers to his or her retirement are alleviated (Boeker and Karichalil, 2002; Fredrickson et al., 1988; Jensen and Meckling, 1976). We thus argue that ownership exchange preceding or coinciding with the CEO succession reduces the likelihood of predecessor activity in the firm. Therefore, we state:

The likelihood of observing post-succession predecessor activity is reduced if ownership transfer to the successor has occurred.

Methods section

Quantitative sample

We employ a quantitative data analysis as well as a qualitative data analysis to test our presumptions. Our quantitative dataset comprises 804 German family firms experiencing a CEO succession, which is a well-researched and—due to its depth—frequently used dataset in family firm research. The dataset rests on several data sources: The Mannheim Enterprise Panel (MUP) database, the Bureau van Dijk database (Amadeus), Hoppenstedt data, German Bundesbank data, standardized computer-aided telephone interviews, and web searches. The databases serve as a data source for company data on the privately held firms, while the interview data serve as an in-depth source regarding succession information. Originally, this dataset was based on the MUP, which is representative of all German firms (Almus et al., 2002). Within MUP, all firms are required to match the following criteria: (1) 30 to 1000 employees, (2) going concern, and (3) being a family firm. We identify family firms as follows: A family firm is regarded as present if a maximum of three individuals (as opposed to legal entities) own more than 50% of the firm and at least one of these owners is an executive director (CEO) (Ahrens et al., 2015, 2019). 1

Then, a filter has been used to identify potential succession cases: A succession is likely between 2002 and 2008 if, during these years, a CEO resigned, or a new CEO was appointed, or a previous owner reduced his share, or a new or prior owner (natural person, i.e., not an enterprise entity) increased her share, and one of the previous owners and CEOs was at the relevant retirement age of at least 55 years or older. Firms that fulfilled these criteria had then been merged with the other databases according to the following hierarchy: (1) MUP, (2) Amadeus, (3) Hoppenstedt, and (4) web searches. Firms with a missing telephone number had been dropped (<1%).

To verify that all potential succession cases indeed identified a real succession, the companies had been phoned to screen for real succession cases and to schedule an appointment with their CEO to participate in a standardized computer-aided telephone interview (CATI) in 2010. All CATI participants needed to match the following four criteria: (1) became successor in the event window, (2) is an executive director, and (3) holds an ownership fraction (full or partial) of the firm or an ownership transfer is planned. We adhere to the common definition of family firm succession as an exchange of ownership (Barry, 1975) and management (Alcorn, 1982), while these transitions may not necessarily occur simultaneously.

Overall, the above collection resulted in CATI data on 804 succession cases. During the CATI, the target (succession case) rate of contacted firms was 21%. The overall (both succession and non-succession cases) response rate of the CATI after refusals, aborts, and non-functioning telephone numbers was 59% and the target (succession case) response rate was 29%, which is a sound rate considering we ask for sensitive CEO and firm data. Due to missing observations in some variables, we have complete data for 522 succession cases across all variables of interest and controls, which comprise our final resultant sample.

Variables and operationalization

Dependent variable

Our main dependent variable predecessor active is a binary variable that indicates whether the predecessor remained involved in any role following a succession (1) or not (0). During the CATI, we recorded formal as well as informal roles for each succession case. These roles comprise: Co-ownership and management; co-owner (without management); supervisory board membership; and other roles such as: employed, but leaving key decisions to the successor; key account holder; conducts special tasks; coach and consultant (without other roles); and other (not specified).

Harnessing this information on these roles, we additionally performed auxiliary quantitative analyses to also provide detail regarding the extent of the predecessor’s post-succession activity. Specifically, we categorized the predecessor’s roles as strong (continued-owner-management; 3); moderate (supervisory board member; continued owner without being manager; 2); and weak (employed, but leaving key decisions to the successor; key account holder; conducts special tasks; coach and consultant; and other roles; 1). We then record the strongest role of each incumbent resulting in a scale from 0 (no role) to 3 (strong role) that serves as an ordinal proxy for the strength of the predecessor’s role which we use as an alternative dependent variable in auxiliary regressions.

Independent variables

The first relational independent variable of interest, family CEO successor, denotes a family succession in which successors are related by marriage or blood (Pérez-González, 2006) to at least one of the three persons whom they succeed and who previously owned (in total) more than 50% of the firm. To complement the operationalization of the family CEO successor variable, we also test our hypotheses using a dummy variable child is successor, taking a value of 1 in case a predecessor’s child has been installed as successor and 0 otherwise, for example, if an uncle, a nephew, or another relative (including those related by marriage) is installed as CEO. Also, we measure with binary indicators son(s) only if the predecessor has only male children, daughter(s) only for only female children, and mixed children for both daughter(s) and son(s). Furthermore, we denote the cases where the successor gender is not provided with our binary variable children (unknown gender). The second relational variable of interest, harmonious work relationship, is an ordinal scale ranging from 0 (very low harmony) to 3 (very high harmony) and emerge from a single item that inquired about the successor’s perception of the harmony in their work relationships with the predecessor (Miller et al., 2003; Shi et al., 2019).

Regarding informational exchange, the human capital of the successor CEO is measured using the CEO human capital score from Ahrens et al. (2015). This score captures the sum of five binary indicator variables leadership experience, business education, use of business plan, industry experience, and high general experience. The underlying rationale of this measure is to capture general managerial skills that contribute substantially to a CEO’s ability to steer a company (Murphy and Zabojnik, 2004). The second informational exchange variable is early generation family firm and captures instances in which the knowledge of the early generation might not yet have diffused to second row management, which is approximated via firm age being less or equal to 50 years, following Carroll (1984), Rubenson and Gupta (1992), and Wasserman (2003).

Using CATI information from the CEO successor, the variable ownership > leadership transition indicates whether at least partial ownership transfer to the successor had occurred at or prior to CEO succession. As an additional perspective on material exchanges and also based on CATI data, the indicator variable ownership transfer by the time of interview depicts cases in which ownership transfer has occurred in the post-succession period up to the telephone interview date.

Control variables

We add additional control variables at the temporal, individual, firm, and industry level. At the temporal level, and in line with a process view on succession (Handler, 1990), years since succession counts the time passed in years since the successor became an executive director de jure. On the individual level, time worked at controls for the time in years the successor has been an employee in the firm prior to succession to account for firm specific knowledge as well as for potential further social ties between predecessor and successor. As female successors in family firms often report that, due to gender biases, their competencies are not fully recognized, which could induce the predecessor to remain in office longer (Dumas, 1992; Vera and Dean, 2005), we control for the female CEO successor ratio via the number of female successors as a percentage of total number of CEO successors, which we also include as this could affect whether the predecessor’s capacity is still demanded.

Firm-level controls include firm size, as complexity and coordination become more pronounced in larger firms (Wasserman, 2003), for which we account via number of employees, transformed logarithmically for a better fit. We control for firm health at the time of succession by including the credit rating score (Credit reform solvency index) in the succession year (Chen et al., 2011). Additionally, based on CATI data, we record whether the CEO successor experienced unexpected sudden financing requirements in the year following succession, which serves as an indicator (equal to 1 if true) that controls for cases in which the predecessor might have dumped non-obvious firm issues on the successor which might affect predecessor activity. Finally, industry-level controls are applied as indicators (base left out is consumer services) according to the ZEW industry classification code.

Empirical strategy

Following an initial descriptive analysis, we test our hypotheses by estimating a logistic regression

Qualitative sample

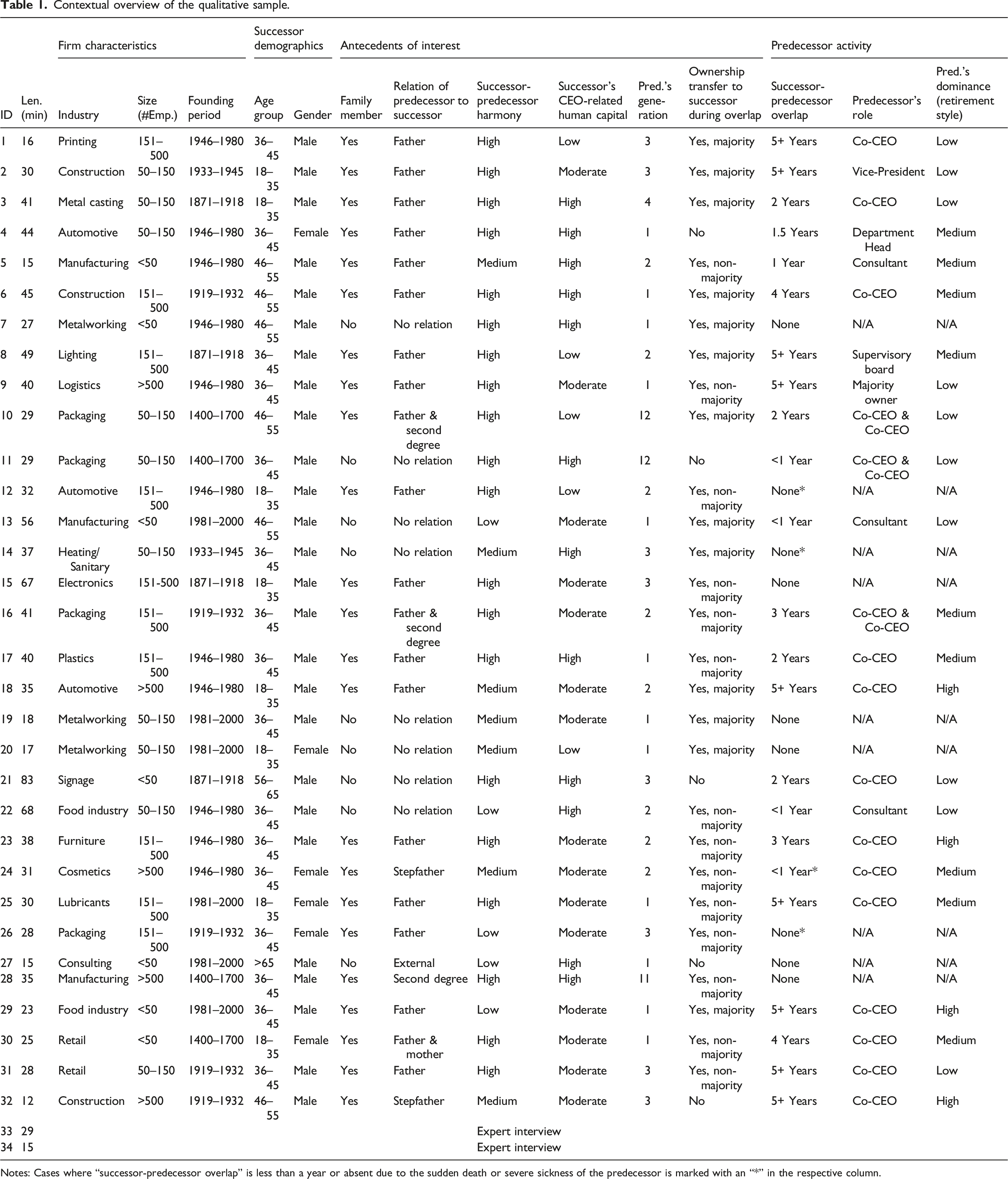

We carried out 34 in-depth interviews to complement evidence beyond our quantitative perspective. In addition to the two expert interviews, we conducted 32 interviews with family firm successors. We reached out to experts to acquire additional practical insights into the succession process and typical procedures found in German family businesses. Not only did they assist us in refining and customizing our interview protocols for family firm interviewees going forward, but they also shared valuable anecdotes that informed our analyses and aided in organizing our ideas. We ensured that the firm characteristics of our quantitative sample are also matched in these 32 typical medium-sized German family firms that have experienced a succession.

Contextual overview of the qualitative sample.

Notes: Cases where “successor-predecessor overlap” is less than a year or absent due to the sudden death or severe sickness of the predecessor is marked with an “*” in the respective column.

The analysis of the qualitative sample was conducted after preliminary quantitative results were elaborated. Upon transcription, interviews are read iteratively in line with the cross case analysis approach suggested by Eisenhardt (1989). We first used open coding, to understand cases and generate a pool of codes emerging based on our expertise and intuition. Thereafter, we referred to our research problem and the main quantitative variables under investigation, re-iterated through all cases to successively extend the code list (we also included codes suggested by anonymous reviewers) and to identify codes relevant to our research-question whose patterns emerge across cases (Gibbert et al., 2008).

During this process, the quotes corresponding to the codes are inserted in a table to facilitate axial coding. Next, via a juxtaposition of codes along with their manifestation as quotes, we iteratively re-investigated and discussed the results for multiple rounds until consensus and saturation are achieved (Gioia et al., 2012). Thereby, we merged overly similar codes, dropped codes with low cross-case evidence, grouped codes into categories, and, finally, as a selective coding step, we identified categories that belong to overarching themes. As our approach is quantitative dominant (Aguinis and Molina-Azorín, 2015), we report themes, the key evidence these themes stand for, which can further inform and corroborate (or enfeeble in case of conflicting or non-evidence) quantitative results, as well as theme-related quotes to offer a complementary qualitative view on our theoretical and quantitative aspects (Greene et al., 1989).

Results

Quantitative results and hypothesis testing

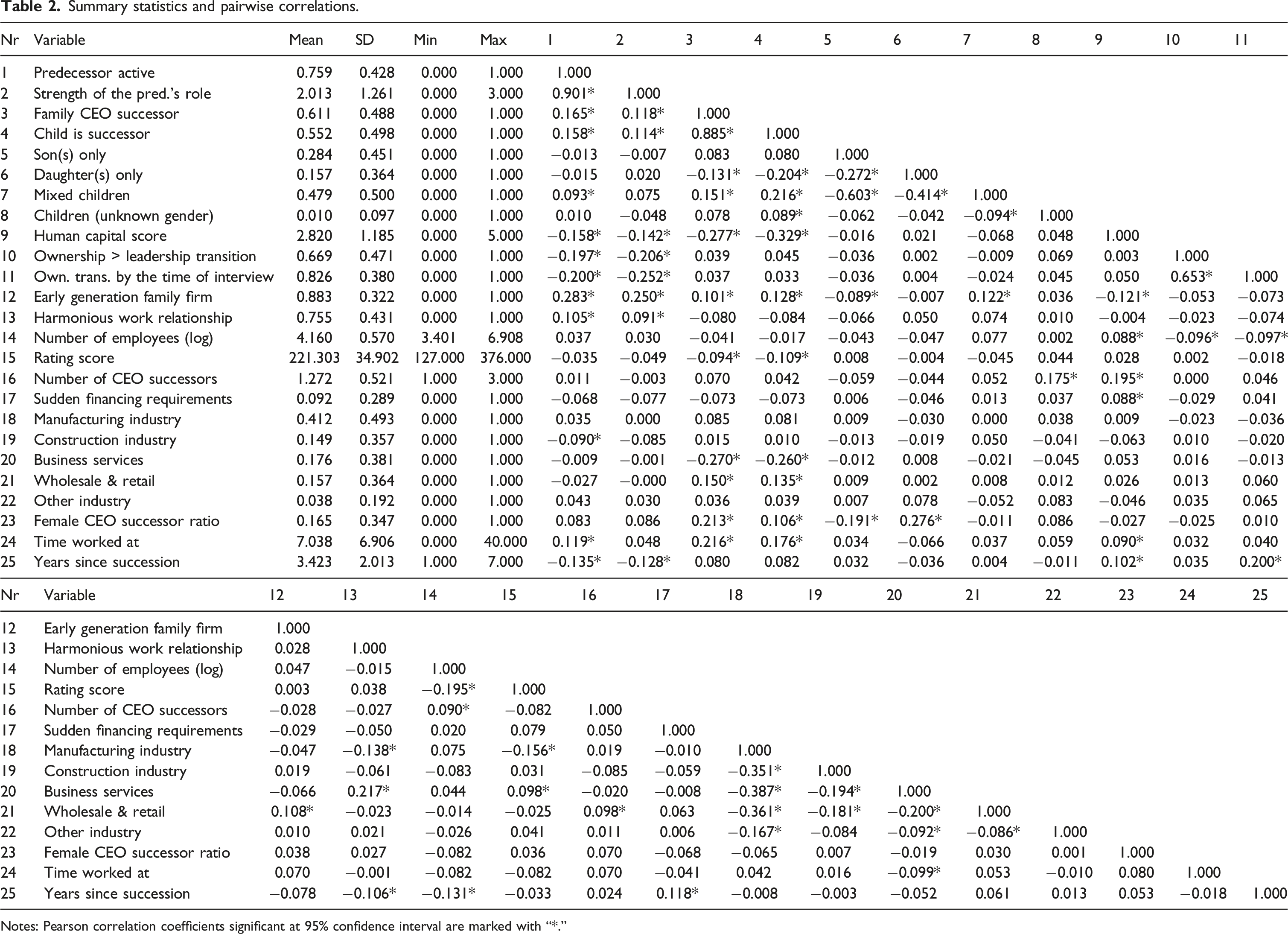

Summary statistics and pairwise correlations.

Notes: Pearson correlation coefficients significant at 95% confidence interval are marked with “*.”

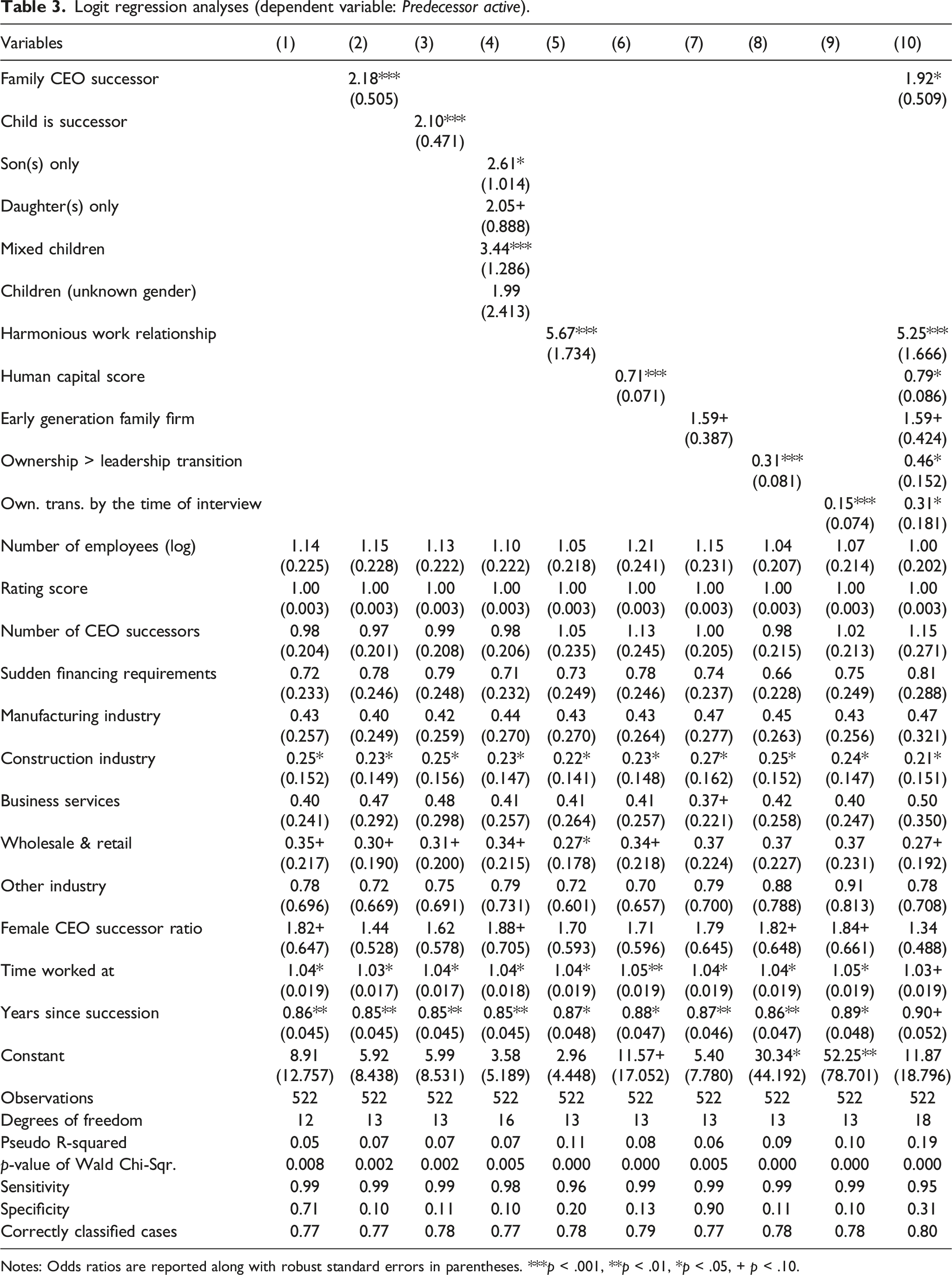

Logit regression analyses (dependent variable: Predecessor active).

Notes: Odds ratios are reported along with robust standard errors in parentheses. ***p < .001, **p < .01, *p < .05, + p < .10.

Model 1 of Table 3 includes control variables only. Model 2 to 5 address familial or work relationship (H1a/b). In line with H1a, the odds ratio of family CEO successor is greater than one and significant when added to the control model (Model 2: odds ratio = 2.18, p < .001) and remains significant in the full model where multiple explanations compete (Model 10: odds ratio = 1.92, p < .05). These findings imply that existence of a family successors makes it about twice more likely to observe predecessor activity in the firm. To alter perspectives with alternative proxies (Model 3 and 4 of Table 3), we further investigate whether the assumption of office of a direct offspring of the predecessor as successor drives prolonged predecessor activity (Model 2: odds ratio = 2.10, p < .001), which finds support and aligns with the arguments leading to H1a.

In support of H1b, we observe an odds ratio which is significant and greater than one for the harmonious work relationship variable when added to the control specification (Model 5: odds ratio = 5.67, p < .001) as well as in the full model (Model 10: odds ratio = 5.25, p < .001). These findings suggest that one point of increase in the harmonious work relationship variable is linked to roughly a five and a half times higher likelihood of predecessor activity. Moreover, note that the odds ratios for time worked at variable is significant and greater than one across all models, pointing at successor–predecessor relationships that had evolved due to repeated prior human exchange and now make predecessor activity more likely.

Models 6 and 7 are linked to informational exchange (H2a/b). Higher successor CEO-related human capital (H2a) significantly reduces the likelihood of predecessor activity (Model 6: odds ratio = 0.71, p < .001), which also holds in the rival explanations Model 10 (odds ratio = 0.79, p < .05). As such, every point of increase in human capital score is associated with approximately a 30% decrease in the likelihood of observing predecessor activity. Similarly, the early generation family firm indicator (H2b) is marginally significant both when added alone (Model 6: odds ratio = 1.59, p = .056) and in the full model (Model 10: odds ratio = 1.59, p = .081) and rather tentatively suggests that in early generation family firms, likelihood of observing predecessor activity increases roughly by 60%. Moreover, note the controls revealing that, in some industries, predecessor activity is significantly less likely, which might hint at the need for informational exchanges which might vary with the industry in which the firm operates.

Models 8 and 9 address the material exchange of ownership (H3). We observe that an immediate transfer of ownership to the new CEO (i.e., at or prior to succession) reduces the likelihood of the incumbent staying involved by 70% (Model 8: odds ratio = 0.31, p < .001). The effect remains robust in the full model although becomes less strong (Model 10: odds ratio = 0.46, p < .05). Further, we also observe that ownership reduces the likelihood of predecessor activity even more (i.e., by 85%) if the ownership transfer took place after the leadership transition, but before the time of interview (Model 9: odds ratio = 0.15, p < .001) and remains robust in the full model (Model 10: odds ratio = 0.31, p < .05). As an aside, and in line with expectations, the significant (and smaller than one) odds ratios of the variable years since succession in all models indicates that post-succession predecessor activity fades over time.

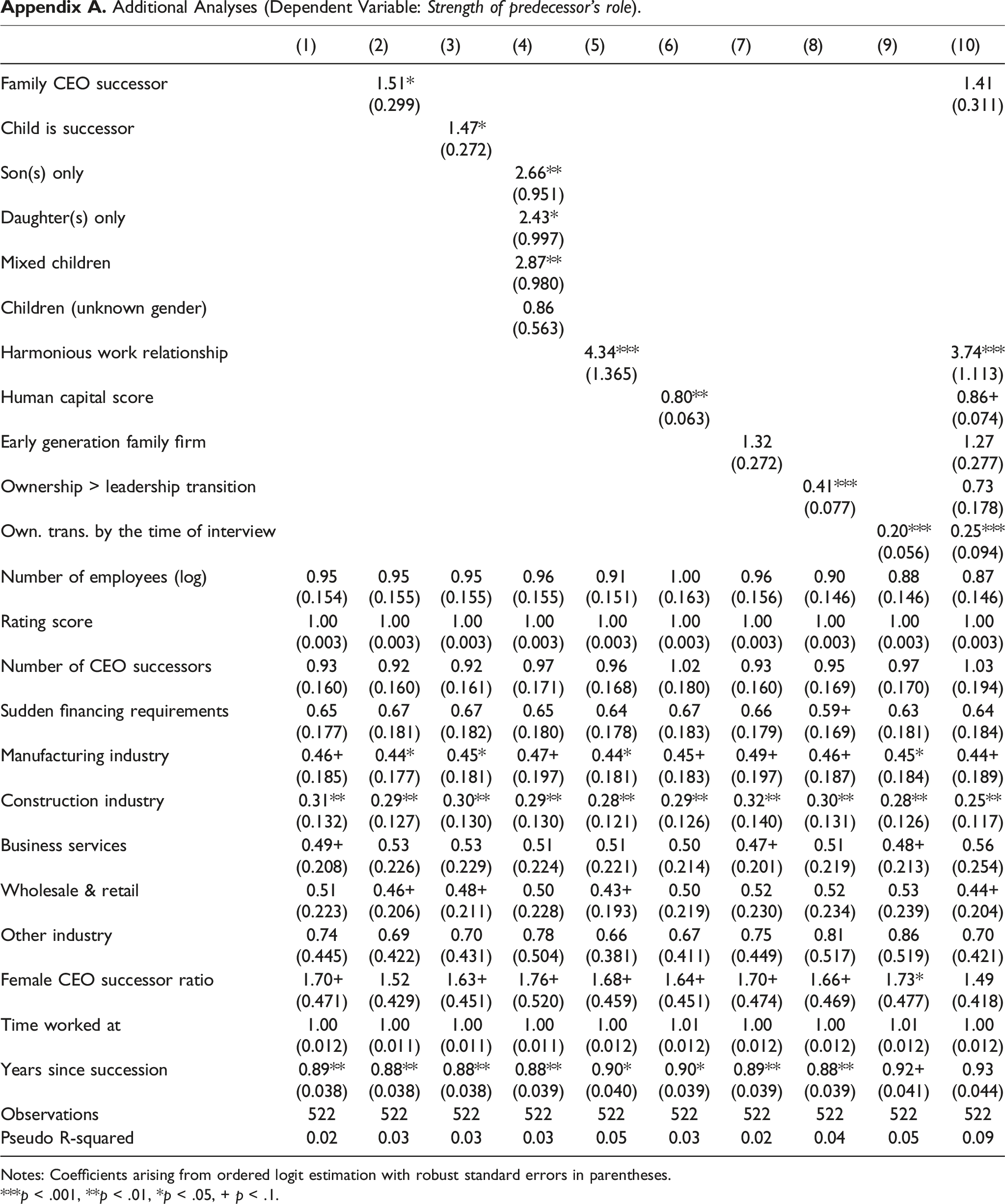

In addition to testing our hypotheses with our binary dependent variable, we also run additional analyses using an alternative dependent variable, strength of the predecessor’s role. Such a consideration is important given the active predecessors may have different degrees of involvement in the firm depending on the different needs of the specific succession context. Specifically, we categorized the predecessor’s roles and assigned a respective ordinal value to these roles. Accordingly, these roles can be strong (continued-owner-management; 3); moderate (supervisory board member; continued owner without being manager; 2); and weak (employed but leaving key decisions to the successor; key account holder; conducts special tasks; coach and consultant; and other roles; 1). We then record the strongest role of each incumbent resulting in a scale from 0 (no role) to 3 (strong role) that serves as an ordinal proxy for the strength of the predecessor’s role which we use as an alternative dependent variable in auxiliary ordinal logit regressions.

As a result of this analysis, we find that only our marginally supported hypothesis regarding the early generation family firm (i.e., H2b) finds no support although the effect direction remains the same. Thus, we can also conclude from that analysis that a stronger role of the predecessor is more likely given familial and harmonious relationships, whereas weaker positions are taken when the successor’s need for informational exchange is lower and when the obligations and amenities of being a shareholder have been transferred to the successor.

Qualitative results

Qualitative analysis of in-depth interviews.

The qualitative evidence also mirrors that relationships affect predecessor activity. Family successions often lead to predecessor activity that is guided by familial support and altruistic intentions, making it a form of generalized exchange. Interviewee no. 1 notes: “Well that [how well the takeover is going] of course always depends on the relationship you have with your parents and of course we have a very familial relationship. That is very close, very harmonious; and that is the basic requirement for a good partnership. That’s why I was very grateful that I was able to gather the experience I have today with him [predecessor father] in an office for many years.” The evident notion behind this quote is that the post-succession resource exchanges from predecessor retention will likely be positively affected for both parties if there is an intact familial relationship. Both predecessor and successor will likely incur additional utility from each other’s presence at the firm and their joint reign, while the utility gains from familial and altruistic support are also augmented due to the familial relation.

Similarly, we observe that successors report a sound working relationship in cases where the predecessor stayed active and in which the norms of generalized exchange in partnerships facilitate constructive solutions to succession-related challenges: “unity nourishes, disunity starves. […] Above all you have to get on well with the person from whom you are taking over the company” (interviewee no. 2). This quote further illustrates that the resource exchanges emerging from predecessor activity post-succession are crucially affected by the successor-predecessor relationship. Indeed, they are likely to be more positive for both successor and predecessor when the relationship is harmonious.

Another complex of themes which emerged in the qualitative analysis was that predecessor activity in the post succession phase is linked to (potentially necessary) informational resource exchanges, thus to reasons that have the typically more instrumental character of restricted exchange. Successors frequently report that their own human capital was improved through a period of activity overlap with the predecessor, as interviewee no. 16 notes: “My father was there for 2-3 more years and we shared an office. I actually learned a lot from him during that time.” In social exchange terms, this illustrates a positive (informational) resource exchange post-succession. Similarly, a reoccurring aspect in the in-depth interviews is that predecessor activity is driven by circumstances when the founder or early generation of the firm still constitutes the central nexus of information and knowledge that needs to be exchanged: “He [the father] is the one who has been in this field for 50 years. […] He has an expertise that only very few have and that is also the reason why it is important and has to be maintained for as long as possible” (interviewee no. 5). Clearly, this quote directly highlights the sheer necessity to find ways post-succession for informational resource exchanges between successor and predecessor that propel predecessor activity especially in case of early generation firms. This along with further quotes pertaining to this theme (see Table 4) are especially valuable as they highlight mechanisms which we propose regarding early generation firms. This is the case since our quantitative analyses offer only marginal support for the effects of these mechanisms and could not be exactly replicated with our alternative dependent variable.

Similarly, it is visible in the qualitative narratives how the amenities (and obligations) of ownership propel predecessor activity (from the predecessor’s perspective), as interviewee no. 24 says: “It [being Co-CEO while step-father still owned the firm] was actually cool, yes, because I could think of every step and then just bring it to the market when he said: ‘Yes, come on, let’s do that now!’ Because there were two of us. So, it was his shop, that was, in the end, his money, it was also play money at the end of the day in that sense.” Interestingly, in this quote the successor seems to enjoy the opportunity of being given the freedom to pivot while not being fully liable. In this case, predecessor activity in the form of delayed ownership transfer also results in exchanges which are associated with a positive utility. Once again, in this case the predecessor seemed mindful not to curb the successors discretion, which easily could have resulted in negative effects from the post succession exchanges.

Overall, the qualitative results in Table 4 mirror the quantitative findings and corroborate the theoretical arguments (especially regarding respective resource exchanges) underlying the hypotheses.

Discussion

We set out to understand more about the antecedents of predecessor post-succession activity in family firms because recent literature merely highlights its implications for firm outcomes (Ahrens et al., 2018; Querbach et al., 2020). Our results are in line with and confirmatory of the phasing out logic and mutual role adjustment processes called a “succession dance” (Handler, 1990) in a joint reign and withdrawal phase occurring post-succession (Cadieux, 2007).

Our data reveals that family ties of the successor CEO seem to play an important antecedent role: Predecessor activity is significantly more likely when a family member takes the helm. Similarly, predecessors are significantly more likely to be active when they have children, which is associated with a family succession. Our interpretation is that prior generalized exchanges at the familial level lead to stable kinship relationships, trust, a shared vision, coherence and mutual obligations. Thus predecessor activity is often guided by an altruistic interest to secure a smooth transition to the next generation and to help procure the family’s wealth—a form of generalized exchange (Astrachan and Jaskiewicz, 2008; Kerkhoff et al., 2004; Le Breton–Miller et al., 2004; Levinson, 1971). This may include a wish to establish a basis for continued, future generalized exchange at the family and firm level. This can potentially be achieved by helping out as Co-CEO, board member or mentor, or by staying active to avoid conflicts among siblings, which may foster the success of the firm and the harmony of the family (Ahrens et al., 2019). Beyond a familial relation, harmonious work relationships, which are frequently achieved by non-family successors, antecede and evoke similar motivations for predecessor activity (Blumentritt et al., 2007). Predecessors seem to increase stability and smoothen the transition (Kotlar and Sieger, 2019; Tabor et al., 2018). Our qualitative evidence adds further nuance to our answers regarding when predecessor activity occurs.

From a restricted exchanges perspective, our evidence reveals that the need for informational exchange represents an important antecedent of predecessor activity. Knowledge exchanges between predecessor and successor can bridge a potential skill gap between the outgoing and the new CEO. This attested compensation for a not yet fully developed successor skill set can become especially relevant when successors have been installed due to nepotistic preferences (Ahrens et al., 2015) or if running the business requires apprenticeship learning. Indeed, mentoring and knowledge transfer can be highly advantageous to both the successor and the firm (Royer et al., 2008), but also to the predecessor: A new role in the company (e.g., mentor and teacher; see also Cadieux (2007)) can give the predecessor a feeling of being a valuable expert rather than “a write-off”, increasing the harmony and effectiveness of the knowledge exchanges. A successor’s inherent (and likely) disadvantage with respect to facts, trends, contacts, and task-specific knowledge, as described by Hambrick and Fukutomi (1991) is thereby counterbalanced, which may be especially relevant in early generation succession (Carroll, 1984; Miller and Friesen, 1980).

Finally, our results suggest that material exchanges of firm ownership constitute a key antecedent explaining continued incumbent involvement. Accordingly, relinquishing ownership seem to reduce barriers to retirement for the incumbent (Sonnenfeld 1991; Sonnenfeld and Spence 1989), as ownership incentivizes a predecessor’s activity in the company (Emerson, 1976). When ownership is exchanged, this insulating effect is dissolved, such that we observe an increased likelihood that predecessors reduce their activity in the company.

Contributions

First, we contribute to research on the succession dance conjecture (Cadieux, 2007; Handler, 1990). In particular, we reveal that the underlying logics of gradual, mutual role-adjustments as part of the succession process (see also Le Breton–Miller et al., 2004), which had been developed theoretically and on the basis of cases in early family firm literature (Handler, 1990), are reaffirmed by this work’s large-scale quantitative data and its complementary qualitative interviews. We consider this a first empirical reaffirmation of the succession dance conjecture. Moreover, to the best of our knowledge, we are the first to assess and quantify the likelihood of prolonged predecessor activity conditional on several contextual factors that the succession literature regards as central, such as key successor attributes (Ahrens et al., 2019; Chrisman et al., 1998), personal relationships at multiple levels (Miller et al., 2003; Shi et al., 2019), and ownership-exchange-related barriers to retirement (Barry, 1975; Daspit et al., 2016; Le Breton–Miller et al., 2004). Together, this evidence provides a crucial addition to stage models of succession in family firms (Churchill and Hatten, 1997; Le Breton–Miller et al., 2004; Longenecker and Schoen, 1978).

Second, this manuscript provides a theoretical conceptualization of the succession dance which is grounded in SET (Blau, 1964; Daspit et al., 2016; Thibaut and Kelley, 1959). Thereby, it enables and informs a deeper understanding of succession dance mechanics, in particular its antecedents, as well as the heterogeneity of its salience across family firms and the contextuality of its various downstream effects on outcomes at the family and firm level (Ahrens et al., 2019; Davis and Harveston, 1999; Querbach et al., 2020). In particular, this extension to the multilevel and multiphase context of family firm succession makes SET a powerful tool for understanding how past human interactions and social exchanges fuel the emergence of social relationships (Coleman, 1986; Emerson, 1976; Long, 2011) which favorably alter the exchange rate (cost-reward structure) of predecessor activity (Homans, 1961; Meeker, 1971; Mitchell et al., 2001) and induce the predecessor to keep on dancing the “succession dance” with altruistic, reciprocal, and supportive intentions that follow the norms of generalized exchange (Gouldner, 1960; Long and Chrisman, 2014). Social Exchange Theory is likewise valuable for identifying predecessor activity as a successor-predecessor exchange constellation whose formation was anteceded by a professional need for informational exchange. Additionally, the breadth of SET facilitates theorizing on antecedents that affect the predecessor’s cost-reward structure of the “predecessor activity” exchange (Emerson, 1976; Homans, 1961), such as how the material exchange of ownership affects the amenities and obligations linked to prolonged activity in the firm.

Third, conceptualizing the “succession dance” through the lens of SET facilitates a better assessment of resulting implications on post-succession firm level outcomes. Predecessor activity has been conceptualized as a double-edged sword, productive when needed but counterproductive when excessive (Ahrens et al., 2018; Mitchell et al., 2009; Sharma et al., 2003b). In this respect, prior social exchanges which lead to the emergence of rich relationships with abundant social capital (Adler and Kwon, 2002; Blau, 1964) make predecessor activity more likely. Yet as this part of the increase in the likelihood of predecessor activity is grounded in relationships, an SET perspective facilitates seeing that relationships paradoxically also make the downside of unproductive predecessor activity (with potentially best intentions) more likely, that is, when predecessors stay active and constrain successor’s discretion without any professional reason for it. This casts light on a potential downside of social capital in family firms (Miller et al., 2003; Portes and Landolt, 2014): It may lead to “a prior generation’s excessive and inappropriate involvement in an organization, possibly causing social disruptions in the organization” (Davis and Harveston, 1999: 311). Further, we also observe that such dark-sided implications of predecessor activity are highly evident when non-family members take over the firm. Our results indicate that in these cases the negative effects for the firm and successors may become even more serious given problems may lead to more radical solutions such as legal action.

Finally, our study addresses a pressing question for practitioners: What happens to the predecessor CEO after leadership is transferred? This is important because our evidence shows the answer to that question entails implications at the firm and familial level, for the successor as well as for the predecessor. While able and strong successors with high human capital might be hindered by a predecessor’s excessive interference (Quigley and Hambrick, 2012; Sonnenfeld, 1991; Sonnenfeld and Spence, 1989), mentoring and facilitating the handover process can aid the knowledge transfer and stabilize the transition. Successors may benefit from the predecessors’ deep and tacit knowledge gained through many years of experience, and these benefits would be more valuable especially when the successors lack the human capital required to lead their organization. Moreover, as some successors highlight in the qualitative cases, the journey of working together with one’s parents can be a particularly rewarding and unique experience which deepens familial relationship. Our results equip practitioners with new insights into the initial conditions that compel predecessors to hold onto their activity and into those that make them more prone to let go. Reasonable succession planning that considers such aspects may help ensure a smooth post-succession period (see e.g., Sharma et al., 2003a). In this respect, this manuscript helps to rationalize such decision processes with regard to the plannability of predecessor activity.

Limitations and future research suggestions

Our study comes with limitations and offers avenues for further research. First, it is cross-sectional in nature and bears all the shortcomings associated with such research designs. Despite our extensive control vector and solid temporal ordering, concerns regarding the unobserved heterogeneity arising from time-invariant factors remain an issue. Thus, future research would benefit from using panel data and related estimators which alleviates such concerns. Second, our study focuses only on a German setting. The nature of the familial relationships in different settings such as openness of communications between family members or other societal dynamics such as patriarchy may skew our results. Thus, further studies should include multiple countries with higher variance in terms of these aspects and investigate their effects on the argued coherences. Third, our study also does not include very small and very large firms. It is possible that in smaller firms where the craftsmanship nature of business is more evident observed relationships may get stronger whereas for the very large ones it could get weaker or vanish completely.

Fourth, future research might also provide further detail on the interplay of the length of successor-predecessor overlap with the exchanges at multiple levels and how this, potentially in a contingent way, affects succession outcomes (Dyck et al., 2002). Fifth, while our study quantitatively captured formal as well as informal roles, future empirical studies might wish to address how the qualitative retirement styles suggested by Sonnenfeld and Spence (1989), such as the rather entrenched “Monarch” style versus the more graceful “Ambassador” style which are likely to alter how those roles are given life, affect the exchange relationships we have identified, including potential repercussions at the firm level, but also at the familial wellbeing level (Sharma, 2004).

Finally, while our study mostly covered SET-informed sociological and economic aspects of the exchange relationship, it may also be instructive to shed more light on how the psychological aspects of exchange relationships influence the cost-reward structure of participating in the exchanges related to predecessor activity. Psychological tensions are high for family CEOs facing the retirement transition. Stepping down from their position as a triumphant corporate “hero” and reintegrating with society as a mere “mortal” is the last great task the classical monomyth must fulfill (Campbell, 1949). We believe there will be merit in a scholarly exploration of this untraveled avenue, as there is likely to be a psychologically sourced heterogeneity in the mastery of this challenge.

Conclusion

By theorizing on determinants of prolonged predecessor activity and by highlighting central mechanics underlying the succession dance empirically, we reveal important antecedents of prolonged predecessor activity, which recent research has identified as crucially affecting post-succession firm outcomes. We highlight that predecessor activity is guided by social exchange processes that have a generalized exchange character in the form of altruism, but also restricted exchange components in the form of informational (knowledge) and material (ownership) exchanges. Overall, we provide empirical evidence that many successions seem to follow a “mutual role adjustment” logic. Thereby, this study offers an empirical confirmation of Handler (1990)’s succession dance conjecture.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Note

Appendix

Additional Analyses (Dependent Variable: Strength of predecessor’s role). Notes: Coefficients arising from ordered logit estimation with robust standard errors in parentheses. ***p < .001, **p < .01, *p < .05, + p < .1.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Family CEO successor

1.51*

1.41

(0.299)

(0.311)

Child is successor

1.47*

(0.272)

Son(s) only

2.66**

(0.951)

Daughter(s) only

2.43*

(0.997)

Mixed children

2.87**

(0.980)

Children (unknown gender)

0.86

(0.563)

Harmonious work relationship

4.34***

3.74***

(1.365)

(1.113)

Human capital score

0.80**

0.86+

(0.063)

(0.074)

Early generation family firm

1.32

1.27

(0.272)

(0.277)

Ownership > leadership transition

0.41***

0.73

(0.077)

(0.178)

Own. trans. by the time of interview

0.20***

0.25***

(0.056)

(0.094)

Number of employees (log)

0.95

0.95

0.95

0.96

0.91

1.00

0.96

0.90

0.88

0.87

(0.154)

(0.155)

(0.155)

(0.155)

(0.151)

(0.163)

(0.156)

(0.146)

(0.146)

(0.146)

Rating score

1.00

1.00

1.00

1.00

1.00

1.00

1.00

1.00

1.00

1.00

(0.003)

(0.003)

(0.003)

(0.003)

(0.003)

(0.003)

(0.003)

(0.003)

(0.003)

(0.003)

Number of CEO successors

0.93

0.92

0.92

0.97

0.96

1.02

0.93

0.95

0.97

1.03

(0.160)

(0.160)

(0.161)

(0.171)

(0.168)

(0.180)

(0.160)

(0.169)

(0.170)

(0.194)

Sudden financing requirements

0.65

0.67

0.67

0.65

0.64

0.67

0.66

0.59+

0.63

0.64

(0.177)

(0.181)

(0.182)

(0.180)

(0.178)

(0.183)

(0.179)

(0.169)

(0.181)

(0.184)

Manufacturing industry

0.46+

0.44*

0.45*

0.47+

0.44*

0.45+

0.49+

0.46+

0.45*

0.44+

(0.185)

(0.177)

(0.181)

(0.197)

(0.181)

(0.183)

(0.197)

(0.187)

(0.184)

(0.189)

Construction industry

0.31**

0.29**

0.30**

0.29**

0.28**

0.29**

0.32**

0.30**

0.28**

0.25**

(0.132)

(0.127)

(0.130)

(0.130)

(0.121)

(0.126)

(0.140)

(0.131)

(0.126)

(0.117)

Business services

0.49+

0.53

0.53

0.51

0.51

0.50

0.47+

0.51

0.48+

0.56

(0.208)

(0.226)

(0.229)

(0.224)

(0.221)

(0.214)

(0.201)

(0.219)

(0.213)

(0.254)

Wholesale & retail

0.51

0.46+

0.48+

0.50

0.43+

0.50

0.52

0.52

0.53

0.44+

(0.223)

(0.206)

(0.211)

(0.228)

(0.193)

(0.219)

(0.230)

(0.234)

(0.239)

(0.204)

Other industry

0.74

0.69

0.70

0.78

0.66

0.67

0.75

0.81

0.86

0.70

(0.445)

(0.422)

(0.431)

(0.504)

(0.381)

(0.411)

(0.449)

(0.517)

(0.519)

(0.421)

Female CEO successor ratio

1.70+

1.52

1.63+

1.76+

1.68+

1.64+

1.70+

1.66+

1.73*

1.49

(0.471)

(0.429)

(0.451)

(0.520)

(0.459)

(0.451)

(0.474)

(0.469)

(0.477)

(0.418)

Time worked at

1.00

1.00

1.00

1.00

1.00

1.01

1.00

1.00

1.01

1.00

(0.012)

(0.011)

(0.011)

(0.011)

(0.012)

(0.012)

(0.012)

(0.012)

(0.012)

(0.012)

Years since succession

0.89**

0.88**

0.88**

0.88**

0.90*

0.90*

0.89**

0.88**

0.92+

0.93

(0.038)

(0.038)

(0.038)

(0.039)

(0.040)

(0.039)

(0.039)

(0.039)

(0.041)

(0.044)

Observations

522

522

522

522

522

522

522

522

522

522

Pseudo R-squared

0.02

0.03

0.03

0.03

0.05

0.03

0.02

0.04

0.05

0.09