Abstract

While CSR has become an integral part of most firms’ agendas, questions remain as to why some firms embrace CSR more than others. By drawing on legitimacy theory, we suggest that firms that are exposed to elevated levels of internationalization are more prone to engage in CSR. We differentiate between the internationalization of activities, the internationalization of ownership, and the internationalization of boards and propose that each dimension has a distinct effect on CSR. Our empirical analysis focuses on Japan, a country where CSR has previously been considered a “foreign” concept. With our study, we emphasize the role of legitimacy as a source of firms’ increasing engagement in CSR and underline the necessity for a more differentiated view of the internationalization-CSR relationship. We also provide practical implications as we suggest firms to use CSR as a solution to respond to legitimacy threats resulting from internationalization.

Keywords

Introduction

Corporate social responsibility (CSR) has become one of the most frequently discussed topics in business literature (Agudelo et al., 2019; Frerichs and Teichert, 2023; Kumar and Srivastava, 2022). While there are several definitions, CSR generally refers to firm policies and actions that exceed legal requirements and typically relate to a firm’s involvement in environmental, human resources, and community affairs (McWilliams and Siegel, 2001). This definition, however, should not obscure the complexity of CSR—as Marques and Mintzberg (2015) phrase it, CSR is not a “piece of cake,” nor is there a “simple recipe for responsible corporate behavior”. Consequently, the question of what engages firms in CSR in the first place has led to a long list of propositions that includes internal and external factors (e.g., Ali et al., 2017; Velte, 2022).

Some authors argue that CSR is predominantly a Western concept (e.g., Khan and Lund-Thomsen, 2011). However, it has recently found its way to many countries in which CSR was formerly perceived as “foreign,” such as Russia, India, South Korea, or Japan (Aray et al., 2021; Choi and Aguilera, 2009; Sahasranamam et al., 2022; Yoshida et al., 2022). In today’s international business environment, CSR practices have widely spread around the globe (Michelson et al., 2016). Against the backdrop of an increasingly globalized economy, we thus ask the following question: does the internationalization of firms lead to an increase in CSR, and if yes, how do different dimensions of internationalization affect CSR? Drawing on legitimacy theory (Deephouse et al., 2017; Díez-Martín et al., 2021), we argue that firms strengthen their CSR as a response to legitimacy threats aroused by different forms of internationalization, namely the internationalization of activities, ownership internationalization, and board internationalization.

We empirically investigate the association between a firm’s internationalization and its CSR by analyzing a sample of Japanese Nikkei 400 firms. By placing the emphasis on Japan, we respond to calls to further study the internationalization-CSR relationship in a non-Western context (Rathert, 2016; Strike et al., 2006). Despite the country’s high level of economic development, CSR in Japan is still considered a concept shaped by Western thought—and one that lacks longstanding traditions (Eweje and Sakaki, 2015; Perera and Hewege, 2022)—thereby making Japanese firms challenging candidates to investigate our research question.

We contribute to existing literature on internationalization and CSR in three ways. First, while previous studies mostly regard CSR as a firm resource, a competitive advantage, or a response to the pressures of specific interest groups (e.g., Attig et al., 2016; Oh et al., 2011; Zhang et al., 2021), we argue that legitimacy threats motivate international firms to engage in CSR. In other words: in the pursuit of legitimacy, the more a firm is confronted with internationalization, the more it will rely on CSR activities.

Second, prior research has usually focused on only one dimension of firm internationalization, most prominently the internationalization of activities in the form of, for instance, foreign sales (e.g., Aray et al., 2021; Brammer et al., 2006). We claim that different internationalization dimensions, that is, internationalization of activities, ownership internationalization, and board internationalization, have distinct effects on CSR. The latter two dimensions of internationalization are far less established in the context of CSR, and, to the best of our knowledge, have never been used in a single study. Hereby, we also follow calls to expand our understanding of internationalization in the corporate context, away from the omnipresent focus on the internationalization of activities (e.g., Cerrato et al., 2016). Likewise, we take up the suggestion to differentiate between different dimensions of CSR (e.g., Bertrand et al., 2021). Our empirical data reveal that firms carefully assess the impact of different internationalization pressures and formulate CSR responses accordingly.

Third, by focusing on a context in which firms allegedly have no CSR legacy, that is, Japan, we advance the understanding of internationalization’s far-reaching effects and the spread of CSR practices around the globe (Brammer et al., 2012; Matten and Moon, 2020). We argue that firms’ striving for legitimacy may lead to a certain prima facie convergence of CSR practices. However, CSR has never been (and is still not) universal (Matten et al., 2005), and we demonstrate that CSR motivations and outcomes of Japanese firms might differ from other contexts, thus underlining the need for more single-country and comparative studies.

Background, theory, and hypotheses

CSR and Japanese firms

Several studies have attempted to investigate the impact of national context and culture on CSR (Gallén and Peraita, 2018; Ho et al., 2012; Thanetsunthorn, 2015), but studies which explicitly link Japanese culture to CSR are scant. For instance, the study by Ho et al. (2012) covers Asian cultures and their approach to CSR, but does not specifically focus on Japan. The study by Thanetsunthorn (2015) compares Eastern Asian countries to European countries, but again, does not provide findings for the Japanese context. Some other studies on the link between culture and CSR are at the country level; however, they cover other Asian countries and do not include Japan (Waldman et al., 2006). First valuable hints on the roles of context and culture can be drawn from early literature on business ethics in Japan (Taka, 1994, 1997), as this literature stresses that “‘social responsibilities’ form part of the business ethics agenda of Japanese corporations” (Taka, 1994).

Still, the situation of Japanese firms’ CSR is ambiguous (see also Horiguchi, 2021; Tanimoto, 2009). On the one hand, prior research has highlighted that Japanese firms have long endorsed practices which today commonly fall under the term “CSR”. For instance, due to a history of environmental scandals (e.g., the “Minamata disease” first diagnosed in the 1950s), Japanese firms were relatively early to systematically incorporate environmental protection measures (Nakamura et al., 2001; Perera and Hewege, 2022). Human resources (HR) are sometimes also considered a Japanese CSR strength, with employees often being interpreted as the primary stakeholder of the Japanese firm (Yoshimori, 1995). Japanese firms have long been known for their employee benefits and advanced health and safety schemes (Lewin et al., 1995; Wokutch, 1990; Wokutch and Shepard, 1999). On the other hand, however, these measures were traditionally exclusively aimed at permanent, full-time, domestic, and mostly male employees; other employees (e.g., women, foreigners, employees in subsidiaries, or part-time employees) did not benefit in the same way (Wokutch and Shepard, 1999). Choi and Aguilera (2009) have stressed that traditionally Japanese firms “have failed to improve chronic problems such as discrimination against minorities, women and foreigners, and are also noted for poor corporate governance.” More generally, some authors have argued that CSR, with its underlying Western ideas of philanthropy and altruism, is per se a foreign concept that is at odds with the socio-cultural and ethical traditions of Japan (Fukukawa and Teramoto, 2009; Lewin et al., 1995). This could be a reason why Japanese firms are often considered CSR latecomers and many firms seemingly still find it difficult to embrace CSR practices “full-heartedly” (Fukukawa and Teramoto, 2009; Horiguchi, 2020; Perera and Hewege, 2022).

However, the international expansion of Japanese firms in the 1980s saw them confronted with topics previously not on the agenda, such as equal opportunity issues or calls for more community involvement (Eweje and Sakaki, 2015; Tanimoto, 2009). As Debroux (2015) stated, Japanese firms are “often genuinely baffled by the intensity of the CSR debate in Western companies.” Indeed, there is anecdotal evidence that many Japanese firms were (and still are) overwhelmed by the backlash arising from overseas incidents which might have caused less of a stir back home. There are also signs that the historic trajectory of Japanese firms’ international expansion makes legitimacy issues a well-known concern to many Japanese firms: as latecomers—and as the only major non-Western actors on the international stage for a long time—they are accustomed to legitimacy deficits vis-à-vis their foreign competitors (Mathews, 2002). Moreover, in recent years, their growing expansion across Asia, specifically, acts as a reminder that the legitimacy of Japanese firms is constantly “on probation” (Vekasi and Nam, 2019).

CSR as a source of legitimacy

Legitimacy theory approaches are well suited to explain the association that exists between internationalization on the one hand and CSR on the other hand. These approaches have developed over time; rather than stemming from one particular author, legitimacy theory has been shaped by many scholars (see, for instance, Ashforth and Gibbs, 1990; Dowling and Pfeffer, 1975; Suchman, 1995). Congruently, authors in the field suggest that firms’ actions and behaviors need to be in line with what society considers legitimate, with Suchman (1995) defining legitimacy as “a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate […].” As long as relevant interest groups (e.g., regulators, customers, suppliers, employees) perceive a firm as legitimate, they ensure its right to operate (Deegan, 2019; Deephouse et al., 2017). Legitimacy gaps open up, however, if firms fall out of favor, possibly putting their very existence at risk (Chen and Roberts, 2010). Such gaps are likely to appear when a firm is active in a high number of countries, and when institutional distances between a firm’s home-country and its host countries are substantial (Marano and Kostova, 2016; Xu and Shenkar, 2002).

To avoid legitimacy gaps, firms thus need to engage in legitimation efforts. Dowling and Pfeffer (1975) propose that there are three different strategies to gain and maintain legitimacy. First, firms can adjust their (bad) conduct and adapt to public expectations. Second, they can actively seek to change the prevailing definition of legitimacy. Third, firms can seek to become more identifiable with what is considered legitimate. Since the second option, that is, changing the very definition of legitimacy, is often difficult, firms usually resort to either adapting their behavior or trying to appear more legitimate, albeit variations and overlaps between strategies are possible (Dowling and Pfeffer, 1975; Rana and Sørensen, 2021).

CSR, specifically, provides firms with options to gain and maintain legitimacy, as it opens up various possibilities for the firm to align—or at least seemingly align—its actions with the expectations of its manifold interest groups (Díez-Martín et al., 2021; Matten and Moon, 2020; Velte, 2022). For instance, firms facing legitimacy threats over the use of child labor can adapt their CSR-related HR policies to prevent such practices in the future. Alternatively, they can point at other areas of CSR to distract from the main problem, for example, by stressing their engagement in enhancing the community infrastructure. Overall, there is ample evidence of how concerns regarding legitimacy influence firms’ CSR (e.g., Ali et al., 2017). We argue herein that legitimacy is even harder to maintain in an international environment, and that CSR fills a key role in protecting this legitimacy.

Hypotheses

In this study, we extend prior findings on the relationship between internationalization and CSR by investigating how different dimensions of internationalization affect the CSR of firms from a particular background, that is, the Japanese background. We argue that internationalization of activities, ownership internationalization, and board internationalization have distinct effects on CSR.

Internationalization of activities and CSR

Prior studies investigating internationalization-CSR relationships have, most prominently, focused on the internationalization of firm activities in the form of foreign sales or foreign assets. Results for countries such as the UK (Brammer et al., 2006), USA (e.g., Attig et al., 2016; Strike et al., 2006), China (Zhang et al., 2021), or India (Sahasranamam et al., 2022) have shown a positive impact of this internationalization dimension on CSR. Research suggests that firms that are active in international markets face high levels of uncertainty, as they have to deal, for instance, with differences in cultures, regulations, and customer expectations (Bai et al., 2022; Kostova and Zaheer, 1999; Sharfman et al., 2004). In other words, as firms internationalize their activities, their exposure to various interest groups increases (Aray et al., 2021; Brammer et al., 2006). Consequently, firms’ environments and legitimacy challenges are characterized by more complexity (Ahmadjian, 2016; Kostova and Zaheer, 1999; Marano and Kostova, 2016).

The level of complexity rises further when firms have to cover a large geographic scope or deal with large institutional distances between home and host countries (Kostova and Zaheer, 1999; Kostova et al., 2020). For example, customers in foreign markets may value different qualities than customers in the domestic market and, in the worst case, feel offended by certain products or marketing campaigns (e.g., Abosag and Farah, 2014). Accordingly, international firms need to consider that they are dealing with a much larger and more diverse audience when formulating their legitimation strategies (Scherer et al., 2013).

Today, many CSR issues, such as environment- and labor-related issues, are universally considered important, and international firms, due to their pivotal role in the global economy, are sometimes expected to exceed in such areas compared with their domestic counterparts (Sharfman et al., 2004). Adding to these heightened expectations, international firms often face legitimacy-defying issues to begin with, as the liability of foreignness puts them at a disadvantage compared with established local firms (Zaheer, 1995). On many occasions, the attribute “foreign” applies a lasting penalty on a firm’s legitimacy. Japanese firms are frequently made aware of this penalty, especially when they are active in neighboring Asian markets (Vekasi and Nam, 2019). To overcome such adversities, CSR offers firms a wide array of options to defend their legitimacy. Efforts in this realm can be of real substance or of a merely cosmetic, communicative nature—both approaches considered suitable to fend off legitimacy threats (Dowling and Pfeffer, 1975; Scherer et al., 2013). In sum, we propose that CSR enables firms to protect their legitimacy when it is jeopardized by increasing internationalization. Hence, we hypothesize:

A firm’s internationalization of activities is positively associated with its CSR activities.

Ownership internationalization and CSR

Some studies have already investigated the role of growing ownership internationalization and its effect on CSR, mostly in emerging market environments. Studies on firms in countries such as China (Guo and Zheng, 2021; McGuinness et al., 2017) or India (Tokas and Yadav, 2020) suggest a positive impact of foreign owners on CSR. The underlying argument for this positive relationship is that foreign owners, that is, predominantly institutional investors from Anglo-American countries, have superior know-how, monitoring capabilities, and higher expectations compared to domestic owners, thus resulting in higher CSR efforts by firms (e.g., Oh et al., 2011).

As capital markets around the world have become global (Lane and Milesi-Ferretti, 2018), the influence of foreign shareholders is deemed to spread further: for example, in Japan, foreign investors have replaced domestic financial institutions and corporations to become the single largest ownership group, holding more than 30% of all shares in 2020, up from less than 5% in 1990 (TSE, 2022). Foreign investors are noted to have different knowledge, ideas, and expectations compared to domestic owners, and they are known to import new business practices, for instance, in areas such as firm strategy, corporate governance, and disclosure standards (e.g., Yoshikawa et al., 2007).

As CSR in Japan is sometimes referred to as a foreign concept per se (Fukukawa and Teramoto, 2009; Horiguchi, 2020), it is not surprising that foreign investors have been identified as a driving force behind the increased diffusion of CSR in Japan (Eweje and Sakaki, 2015). For example, foreign ownership is associated with advanced career opportunities for women, as well as better support for working parents (Suzuki et al., 2008; Tanaka, 2019). Japanese firms with higher foreign shareholdings were also among the first to institutionalize CSR by creating designated CSR departments (Suzuki et al., 2010).

With regards to firms’ legitimacy, it is well documented that increasing foreign ownership levels have had far-reaching implications for Japanese firms in the past. For instance, firms in Japan have adjusted their governance and reporting standards as a response to foreign investors’ expectations (Choi et al., 2013). Furthermore, foreign investors were able to shift the debate on previously practically unheard-of practices in Japan, such as corporate downsizing; as downsizing became the “new norm” in the 1990s, firms that did not follow the trend were suddenly at risk of losing their legitimacy (Ahmadjian and Robinson, 2001). More generally, it has also been suggested that firms are prone to address the expectations of their foreign investors to avoid legitimacy gaps which could, ultimately, lead to worse positioning in global capital markets (Haniffa and Cooke, 2005). As the importance of socially responsible investments (SRI) is on the rise, “good CSR” can signal to foreign shareholders that firms are aware of heightened expectations, and it proves that they are “international players” (Amran and Siti-Nabiha, 2009) worthy of the attention of and capital provided by foreign investors. Given these considerations, we predict a positive relationship between increasing ownership internationalization and CSR and formulate the following hypothesis:

A firm’s ownership internationalization is positively associated with its CSR activities.

Board internationalization and CSR

The internationalization of firms’ upper echelons is another internationalization dimension that has seen increasing attention in recent years. Early evidence in this field includes a study of US firms by Slater and Dixon-Fowler (2009), who suggest a positive relationship between CEOs’ international experience and CSR. Miska et al. (2016) highlight the pivotal role played by internationally experienced members of Chinese top management teams in navigating their firms’ global CSR strategies. Zhang et al. (2018), again in a Chinese context, note that it is specifically directors with long-term foreign experience that influence firms’ CSR. Furthermore, Kang et al. (2019) report a positive influence of non-Anglo-American directors on CSR involvement of Korean firms, while Garanina and Aray (2021) find that foreign directors on boards of Russian firm’s positively impact CSR disclosure.

The role of board internationalization with respect to firms’ legitimacy and CSR is two-fold. First, individual board directors can be an immediate source of legitimacy (Hillman et al., 2009). The origin of this legitimacy is grounded in positive outward perceptions of directors’ characteristics, such as their professional background, experiences, or social networks (De Andres et al., 2022; Hung, 2011). There is also evidence that legitimacy can stem from demographic factors, especially if these factors increase the board’s level of diversity (Bertrand et al., 2021; Zhang et al., 2013). For instance, female or foreign board directors can have a positive signaling effect and enhance firms’ legitimacy if the external environment deems such director profiles appropriate (Bertrand et al., 2021; Tanaka, 2019). Not surprisingly, foreign directors are considered a particularly good fit for firms operating in a highly international environment (Garanina and Aray, 2021).

Second, aside from the immediate positive effect on legitimacy, foreign directors, once in place, add to boards’ pool of resources by providing unique skills, knowledge, and competencies (Beji et al., 2021; Singh, 2007). Foreign nationals are likely to come with their own set of values, norms, beliefs, and attitudes, thereby embodying the potential to stir up board room debates significantly (Hambrick et al., 1998). Prior research has shown how board diversity can enrich board resources, and, ultimately, benefit firm outcomes (e.g., Singh, 2007; Yamauchi and Sato, 2022). More specifically, studies have found positive links between board diversity and CSR (e.g., Beji et al., 2021; Kang et al., 2019; Zhang et al., 2013). While it has been suggested that boards may require a certain critical mass of members with diverse backgrounds to make a real difference (e.g., Post et al., 2011), others have found that just one board member that diverges from the norm can have an impact (e.g., Zaichkowsky, 2014). Although research on the internationalization of Japanese upper echelons is rather scant (Schmid and Roedder, 2021), evidence suggests that boards are still very homogenous, and positions continue to be overwhelmingly filled by Japanese managers (Hartmann, 2018; Schmid and Roedder, 2022). This implies that even the inclusion of only one foreign national would likely cause disruption and bring new ideas to the boardroom. In sum, we believe that the internationalization of boards leads to increased CSR. Thus, we hypothesize:

A firm’s board internationalization is positively associated with its CSR activities.

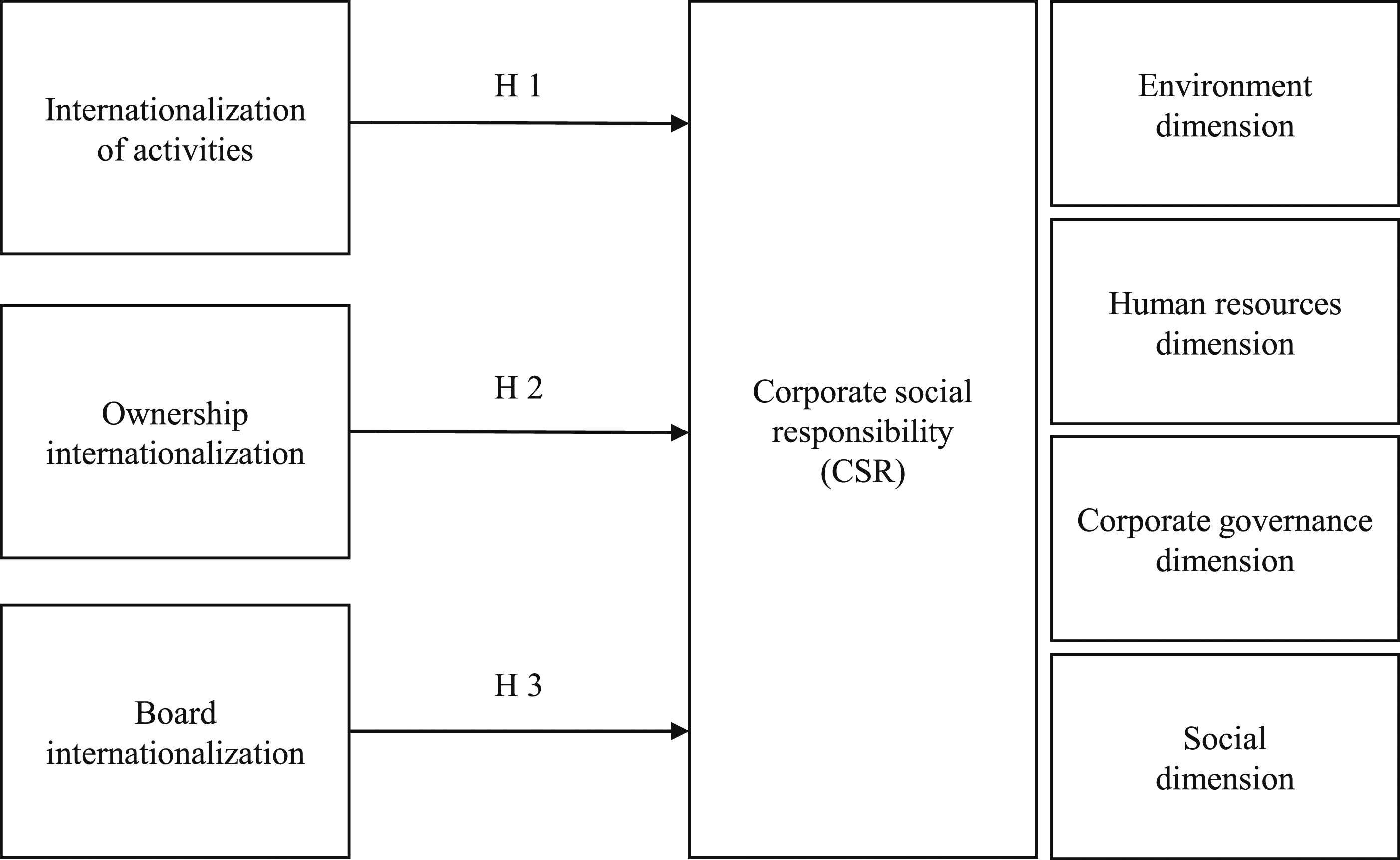

Figure 1 summarizes our research framework, indicating the relationship between our internationalization dimensions and CSR activities. Figure 1 also includes the CSR sub-dimensions that will be part of subsequent additional analyses. Our detailed operationalization of CSR and its sub-dimensions will be addressed in our methodology section. Research framework.

Methodology

Sample and data collection

Our sample builds on the Nikkei 400 index, which comprises a broad set of Japanese firms listed on the Tokyo Stock Exchange and is mainly based on market capitalization (TSE, 2019). We opt for this sample because there is considerable variation across Nikkei 400 firms; for instance, global heavyweights, such as Toyota or Panasonic, are as much part of the index as internationally relatively unknown firms, such as Nishimatsu Construction or Kyowa Kirin. In addition, most firms in the Nikkei 400 are “international” to some degree. 1 Since “modern” CSR has found its way to Japan later than elsewhere, we collected our data for a recent period, that is, the years 2015 to 2019. To account for any subsequent effects of internationalization on CSR activities, we incorporated a one-year lag between our predictor variables (i.e., 2015 to 2018) and dependent variables (i.e., 2016 to 2019).

We retrieved data on internationalization of activities, ownership internationalization, and the majority of control variables from the Nikkei NVS and Refinitiv Eikon databases. Annual reports, corporate websites, and security reports were consulted to complement missing data. Information on board internationalization was obtained from annual reports, corporate websites, and other websites, such as Bloomberg. Since most firms do not provide detailed background data for directors, we hand-collected information on firms’ board internationalization by using name analysis. Given the discriminability of Japanese names, the distinction of nationality based on names is an established approach (Harzing, 2001; Sekiguchi et al., 2011). Albeit we admit that there are some limitations to our approach, the chance of coding Japanese nationals as foreigners (or vice versa) is low, given that even foreign-inspired names of Japanese are “japanized,” and (the very few) foreigners who become Japanese citizens usually take a Japanese or at least “japanized” name. In addition, dual citizenship is not allowed in Japan, thus limiting potential uncertainties about nationality (MOJ, 2023). To limit the margin of error further, we consulted web sources, such as LinkedIn or news reports, for ambiguous cases.

For our CSR variables, we used the Tōyō Keizai CSR database. Similar to KLD’s CSR ratings for US firms or the KEJI Index for South Korean firms, Tōyō Keizai’s CSR data is acknowledged as the standard for Japanese firms (e.g., Suzuki et al., 2010; Nakamura, 2013). Tōyō Keizai’s rating is based on the evaluation of a total of approximately 150 items grouped into four CSR sub-dimensions: environment, HR, corporate governance, and social. The environment dimension encompasses a track-record of a firm’s environmental performance along with an account of its range of preventive environmental protection measures. HR includes, for instance, indicators of equal opportunity and parental leave policies. The corporate governance dimension focusses on CSR-related aspects of corporate governance and considers, for example, whether firms have created designated CSR departments and appointed CSR officers. Lastly, the social dimension includes firms’ policies and actions in fields such as charitable giving and support for educational or cultural activities. The collected information is published in the form of an overall CSR score as well as scores for the four sub-dimensions of each firm.

We had to drop some firms from our original sample, as we excluded those with incomplete data. The absence of CSR information for some firms, and the lack of data on internationalization of activities, particularly for (financial) services firms, proved to be bottlenecks. We conducted t-tests to verify that no substantial differences between the dropped firms and those comprising the final sample exist. Ultimately, our sample contains 190 firms and a total of 760 firm years.

Dependent variable

Our dependent variable, CSR, is based on Tōyō Keizai’s overall CSR score. Scores go up to 300, with 300 being the best achievable score. In line with previous studies (e.g., Brammer et al., 2006; McGuinness et al., 2017), we chose a composite measure of CSR to capture a firm’s overall CSR. While Tōyō Keizai’s composite CSR score is used for our main analysis, we also employed the different CSR sub-dimensions as part of our additional analyses.

Independent variables

The first independent variable is internationalization of activities, which is operationalized as a firm’s foreign sales to total sales (FSTS) ratio. While we are aware that multiple ways of measuring a firm’s overall involvement in international activities exist (Sullivan, 1994), FSTS is an established and frequently used measure (e.g., Attig et al., 2016; Kang, 2013). For our second independent variable, ownership internationalization, we follow the approach taken by other studies (e.g., Ahmadjian and Robbins, 2005; Motta and Uchida, 2018) by measuring the percentage of shares held by foreign investors. Hence, we capture firms’ overall foreign ownership ratio and do not only consider the presence of foreign shareholders. Our third independent variable, board internationalization, codes boards of directors (torishimari yakkai) with at least one foreign director as 1, and boards without any foreign directors as 0. Opting for this binary operationalization is in line with previous studies (e.g., Sekiguchi et al., 2011) and considers the overall very low number of foreign directors in Japan (Hartmann, 2018).

Control variables

We included multiple control variables to account for other firm characteristics that may influence CSR. Board independence measures the percentage of outside directors on the board, since a higher ratio of outside directors can lead to better monitoring and representation of external expectations (Post et al., 2011). Additionally, a higher overall number of directors might foster the exchange of knowledge and opinions, and it opens up the board to more diverse director profiles and a subsequent positive effect on CSR (De Villiers et al., 2011). We thus include the control board size, that is, the number of total board directors, in our analysis (Hafsi and Turgut, 2013).

Studies have shown that different owners have different expectations, and consequently also different effects on CSR (Nakamura, 2013). Hence, we control for domestic corporate ownership, 2 namely, the percentage of shares held by domestic corporations. Aside from foreign shareholders, this group constitutes the largest ownership group in Japan (TSE, 2022). Furthermore, we also include individual ownership as a measure of shares owned by individual investors. As individual investors are mainly interested in private financial gain, an overall negative relationship between this ownership group and CSR has been suggested (Dam and Scholtens, 2012). We also account for a firm’s ownership concentration, operationalized as the aggregated percentage of shares held by the ten largest shareholders (Hu and Izumida, 2008). Large owners can either discourage CSR initiatives, if they fear these will eat into their financial profits (Dam and Scholtens, 2013), or, if in favor of CSR, encourage even stronger CSR efforts (Li and Zhang, 2010).

We consider that larger firms possess more financial resources and are more visible to the public, which may induce greater pressures to act responsibly (Adams and Hardwick, 1998). We control for the relationship between firm size and CSR by including the natural logarithm of total assets (Strike et al., 2006). Furthermore, there is evidence that high-performing firms tend to have superior CSR (McGuire et al., 1988), which is why we control for accounting performance, operationalized by a firm’s return on equity. We include another performance indicator, that is, dividend yield. Measured as a firm’s dividend ratio relative to its stock price, we build on the idea that a higher dividend yield might come at the expense of CSR (Rakotomavo, 2012). We also control for leverage, that is, the ratio of a firm’s total debt to total assets, since firms with more slack resources might choose to invest more in CSR (Waddock and Graves, 1997). There is a possibility that intangible assets can affect firms’ CSR, which is why we account for market-to-book ratio, that is, the ratio of a firm’s market value of assets to its book value of assets (Kang, 2013). Furthermore, we control whether a firm is a member of a keiretsu (a large industrial group, such as Mitsubishi or Sumitomo) to account for a potential effect of keiretsu membership on CSR (O’Shaughnessy et al., 2007; Suzuki et al., 2010; Yoshida et al., 2022). We code firms as keiretsu members based on their association with a president club (shachōkai) (Lincoln and Shimotani, 2010). Lastly, we control for industry, based on firms’ SIC codes (Jeong, 2021).

Analytical approach

To test the hypothesized relationships between different dimensions of internationalization and CSR, we conduct several random effects (RE) regression analyses. The performance of a Breusch-Pagan Lagrange multiplier test suggests the general appropriateness of RE regressions. Whereas results of a Hausman test indicate that the use of fixed effects (FE) regressions may be in order for some of our models, we are aware that the Hausman test mainly indicates whether the within and between effects are different (Clark and Linzer, 2015). However, following established practice, we base our choice of regression analysis type on several considerations (Bell et al., 2019; Clark and Linzer, 2015). Ultimately, we decided to use RE regressions for our main analysis for the following reasons: first, RE regressions allow for the inclusion of time-invariant but potentially important firm characteristics, that is, variables that are of interest but that do not change over time (Bell et al., 2019; Clark and Linzer, 2015). Our models show that our control variable keiretsu is such a firm characteristic that would otherwise be lost. Second, an initial exploration of our data revealed that many independent (and control) variables only change gradually over time. For example, it is unlikely that a firm’s internationalization of activities will change drastically from 1 year to the next. Such “sluggish” developments have potential adverse consequences for effects estimations in FE regressions, but they are not relevant for estimations of RE regressions (Clark and Linzer, 2015).

To strengthen the robustness of our analysis, we include year and firm effects in all our models to control for the panel nature of our data. Lastly, to compensate for problems relating to autocorrelation and heteroscedasticity, we use clustered and robust standard errors.

Results

Main results

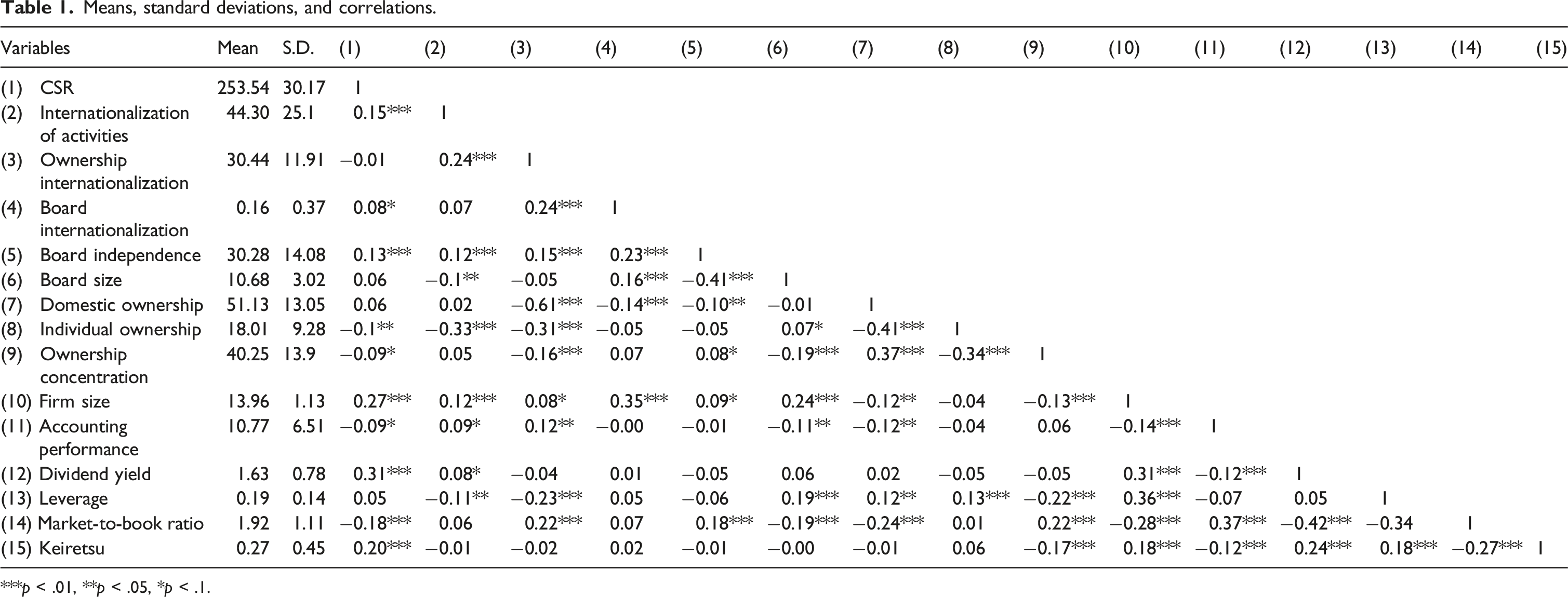

Means, standard deviations, and correlations.

***p < .01, **p < .05, *p < .1.

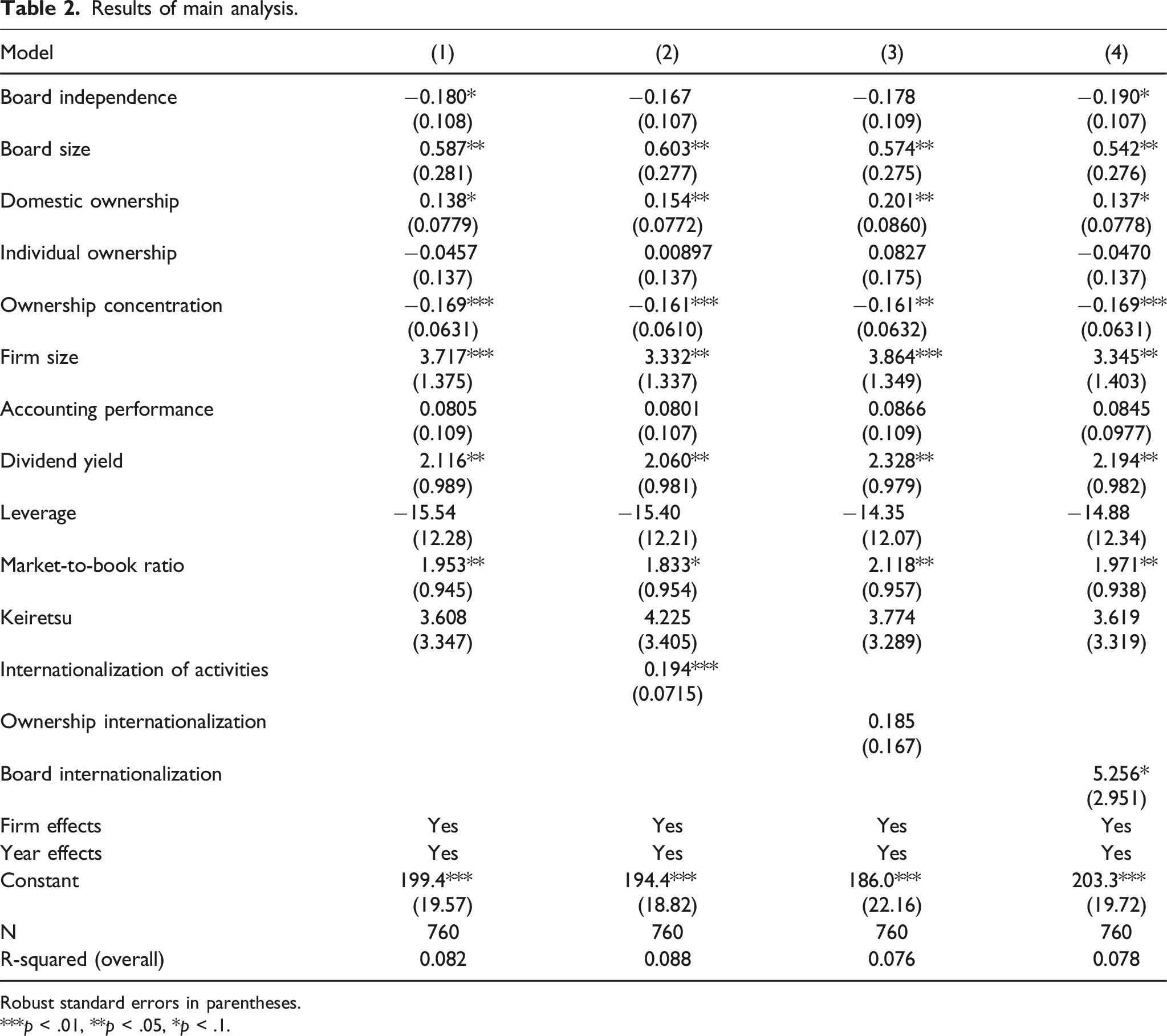

Results of main analysis.

Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .1.

The results of the empirical test of Hypothesis 1 (Model 2) indicate a positive and significant relationship between firms’ internationalization of activities and CSR (0.19 at p < 0.01). While the effect size appears small, we are careful to assess what this means in terms of “how much” a firm’s CSR improves, given the nature of our composite CSR score. Overall, our results indicate support for Hypothesis 1.

To test Hypothesis 2, we include ownership internationalization as our dependent variable (Model 3). Although the results reveal a positive coefficient for this variable, we cannot confirm a statistically significant association between ownership internationalization and CSR (0.19 at p > 0.1). Hence, we have to reject Hypothesis 2.

In Hypothesis 3, we assume that board internationalization positively influences firms’ CSR. Our results (Model 4) indicate a significant positive relationship between board internationalization and CSR (5.26 at p < 0.1). Again, while we are cautious in interpreting effect sizes, it is striking that board internationalization has by far the greatest coefficient out of all variables. In conclusion, Hypothesis 3 is supported.

Additional analyses

We conduct a number of additional analyses to support our findings.

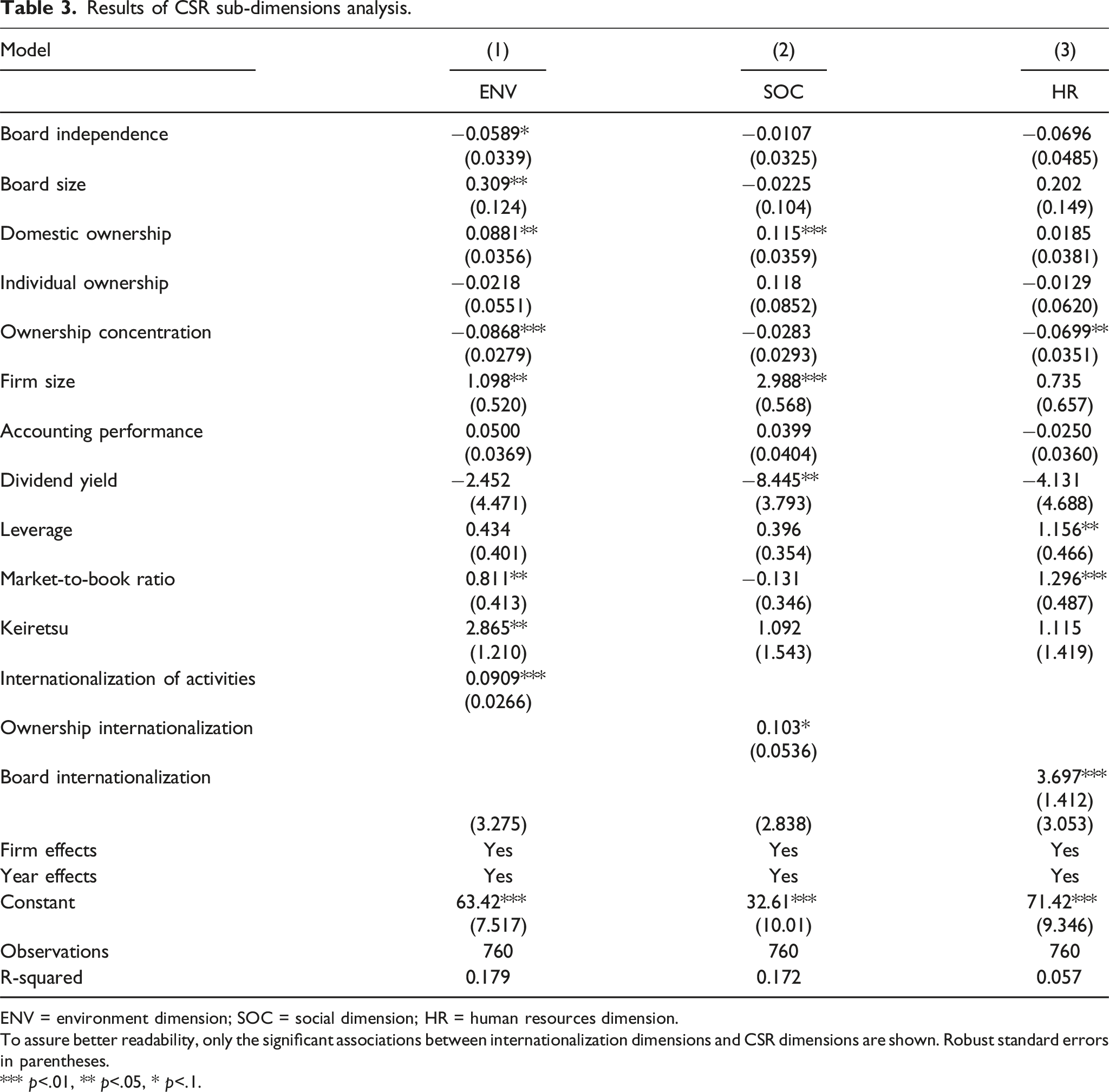

(i) In our first additional analysis, we take a refined look at our dependent variable by utilizing Tōyō Keizai’s environment, HR, corporate governance, and social sub-dimensions of CSR—instead of the overall CSR score. The results in Table 3 (Models 1–3) reveal that each of the internationalization dimensions has a significant positive relationship with one of the CSR sub-dimensions. Internationalization of activities is associated with the environment dimension (p < 0.01), whereas ownership internationalization and board internationalization are associated with the social and HR dimensions, respectively (p < 0.1 and p < 0.01, respectively). Hence, we find evidence that ownership internationalization is associated with a particular CSR dimension, the social dimension, despite an absent positive effect on firms’ overall CSR. Reasons for this surprising finding will be examined in our discussion and contributions section.

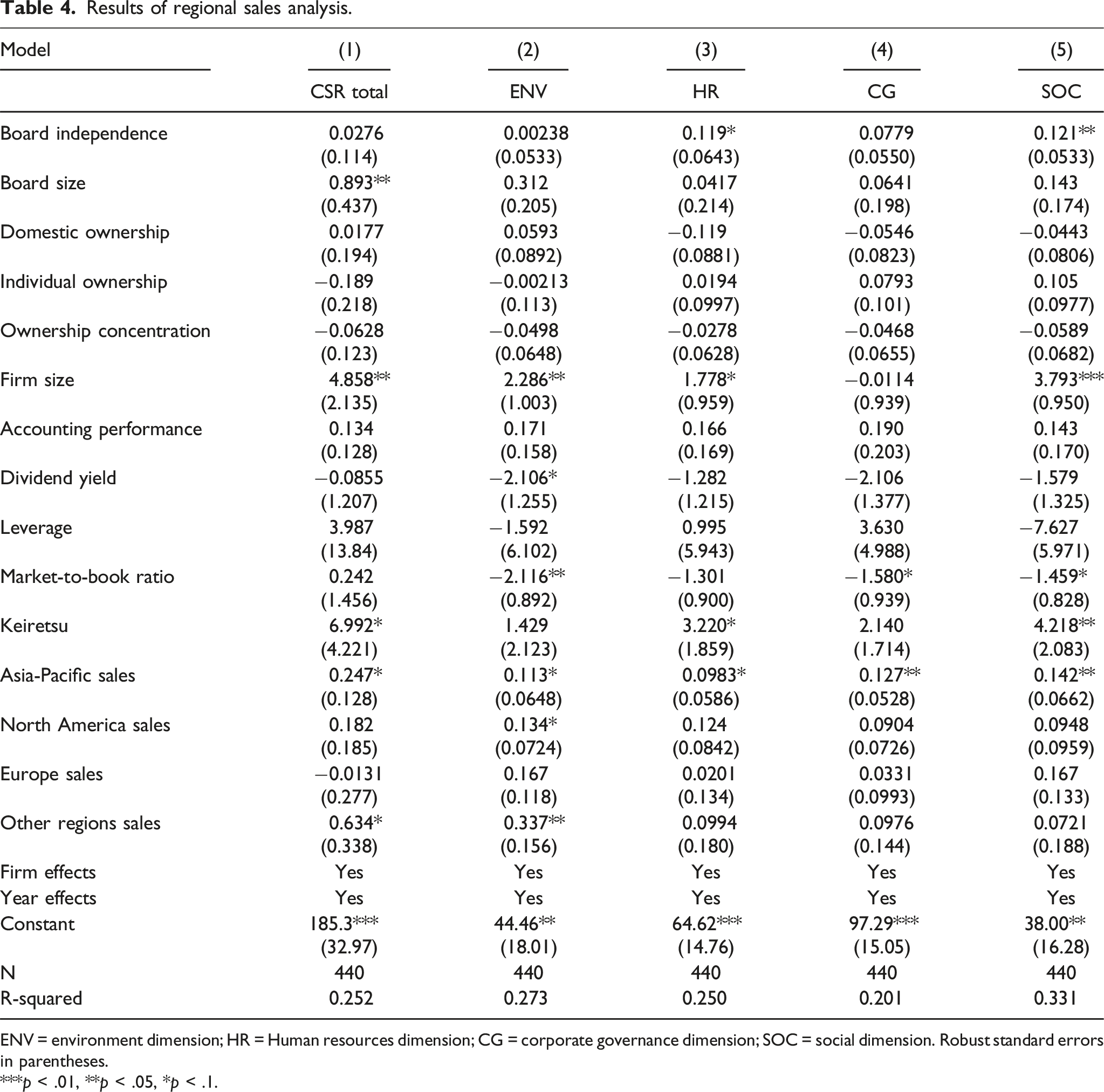

(ii) Second, we take a closer look at the internationalization of firm activities, by investigating their regional dispersion. We did this to strengthen the robustness of our results from our main analysis and to respond to the idea that specific geographic locations propel firms’ CSR. As many firms have a distinct geographical focus (Rugman and Verbeke, 2004), we analyzed firms’ activities in different regions, after collecting data on firms’ foreign sales in three major economic regions, namely, Asia-Pacific, North America, and Europe. Together, these regions account for approximately 95% of our firms’ overall foreign sales. The remaining 5% are summarized as “other” regions. Results of analyses using the overall CSR and sub-dimension scores are reported in Table 4. Model 1 shows that stronger sales activities in the Asia-Pacific region, as well as in “other” regions, strengthen firms’ overall CSR (both at p < 0.1). In addition, the CSR sub-dimensions analysis (Models 2–5) shows a clear picture: it is—specifically and exclusively—the Asia-Pacific region that consistently positively affects all sub-dimensions of CSR. Only the environment dimension receives additional positive stimuli from North America and the “other” regions.

Results of CSR sub-dimensions analysis.

ENV = environment dimension; SOC = social dimension; HR = human resources dimension.

To assure better readability, only the significant associations between internationalization dimensions and CSR dimensions are shown. Robust standard errors in parentheses.

*** p<.01, ** p<.05, * p<.1.

Results of regional sales analysis.

ENV = environment dimension; HR = Human resources dimension; CG = corporate governance dimension; SOC = social dimension. Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .1.

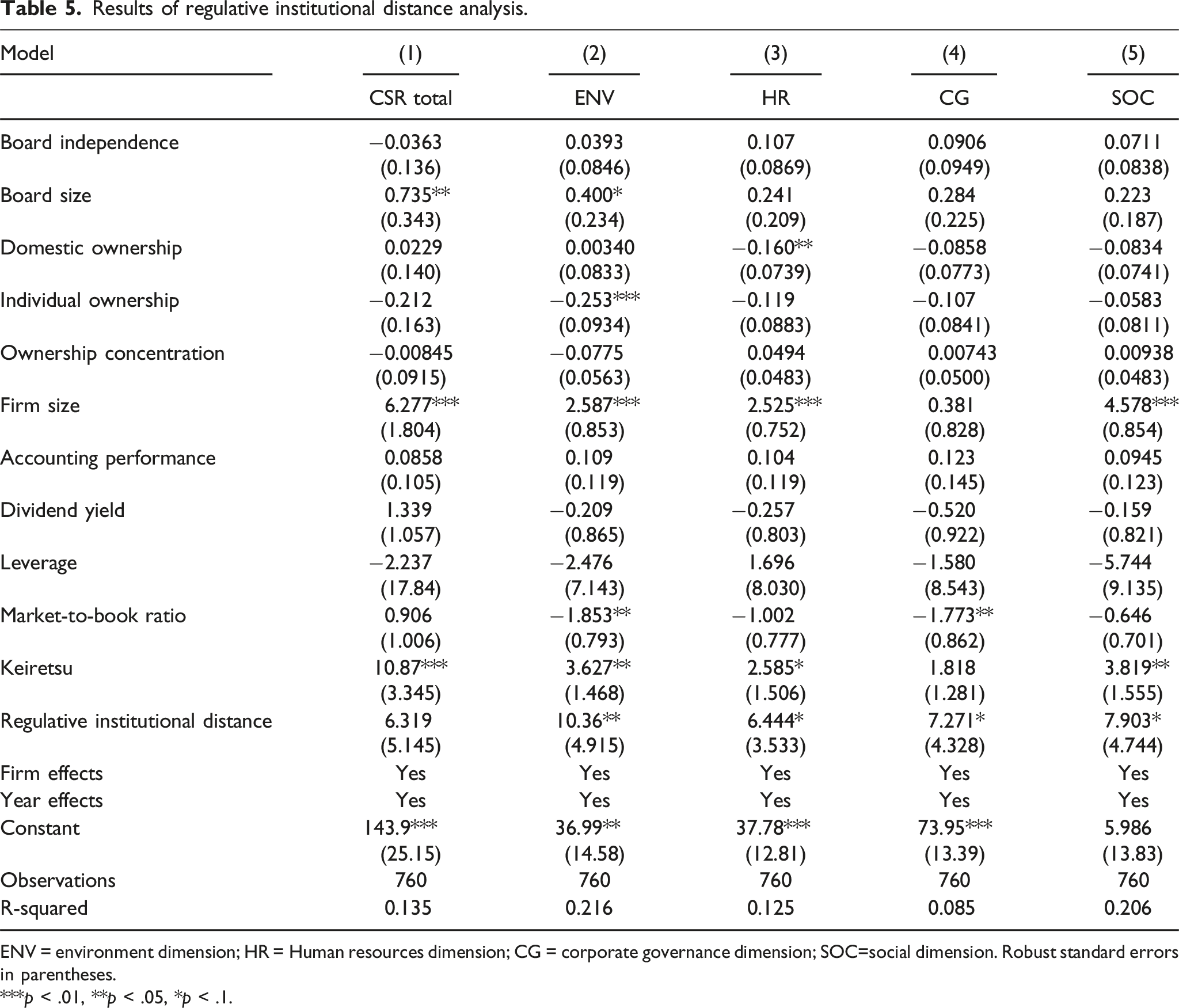

Results of regulative institutional distance analysis.

ENV = environment dimension; HR = Human resources dimension; CG = corporate governance dimension; SOC=social dimension. Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .1.

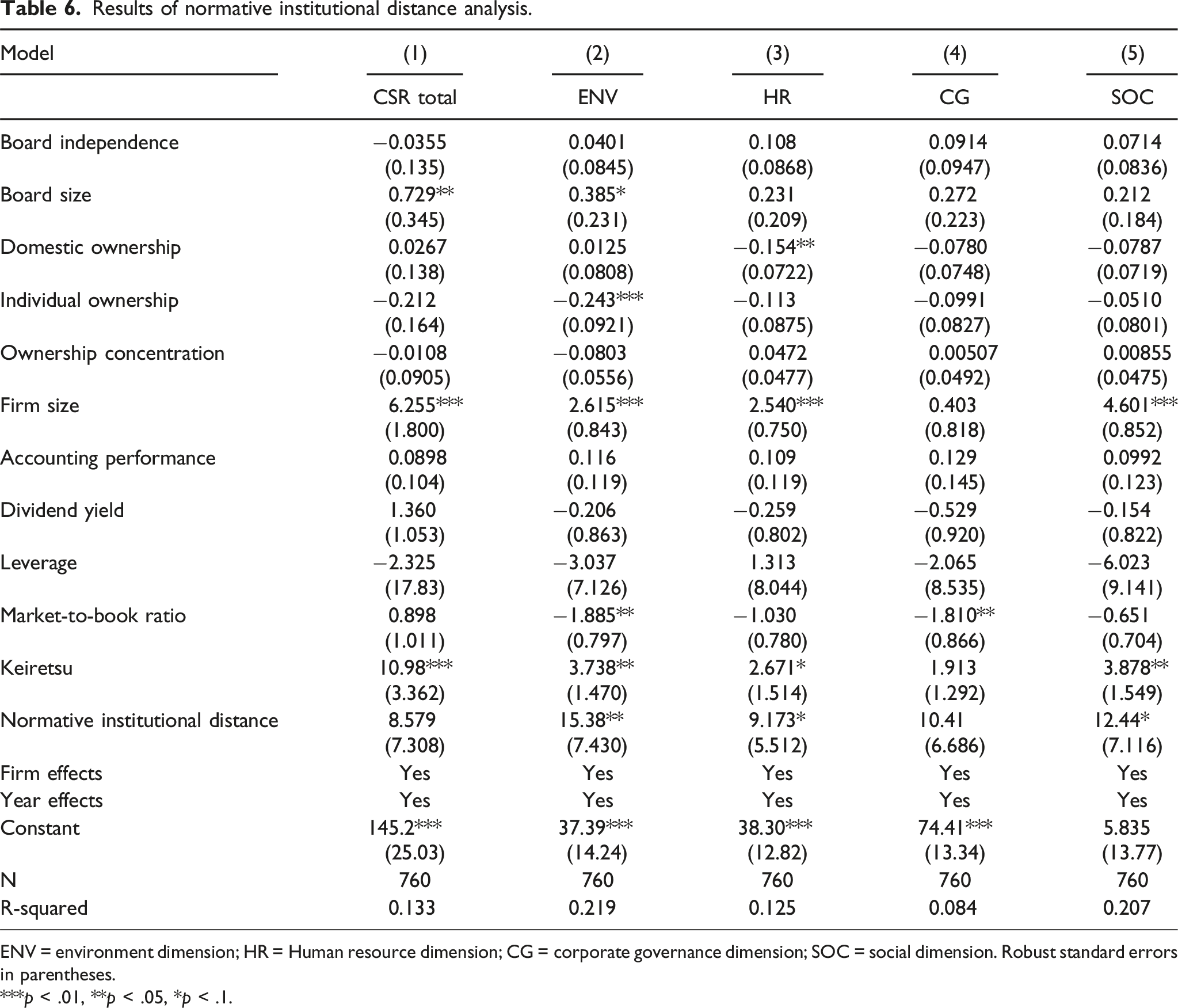

Results of normative institutional distance analysis.

ENV = environment dimension; HR = Human resource dimension; CG = corporate governance dimension; SOC = social dimension. Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .1.

Discussion and contributions

In our paper, we argue that firms strengthen their CSR as a response to legitimacy issues that arise across different dimensions of internationalization. We thus highlight the differentiated nature of the relationship between internationalization and CSR.

Our study adds to existing literature in several ways. First, many prior studies attempting to establish relationships between internationalization and CSR stress the importance of certain interest groups or host country premises on CSR (e.g., Attig et al., 2016; Rathert, 2016; Sahasranamam et al., 2022). Instead, we propose that different dimensions of internationalization put firms’ legitimacy in jeopardy, and CSR can shield this legitimacy. While CSR efforts are certainly not enough to protect against every single legitimacy issue, CSR has the potential to create a basic form of immunization against a wide range of threats (e.g., Martínez-Ferrero et al., 2016). Good CSR ratings can signal firm actions and policies that are either of real substance or of a rather communicative, manipulative nature—or, most likely, a mix between the two. This coincides with legitimacy theory, which stresses the importance of firms’ outward appearance based on both actions and communication (e.g., Choi et al., 2013). Whereas legitimacy theory has already been frequently applied to theorize on the more communicative nature of CSR in the form of CSR disclosure practices (e.g., Aray et al., 2021), our study uses legitimacy theory to expand the scope to firms’ overall CSR.

By acknowledging the links between legitimacy theory and institutional approaches (Fernando and Lawrence, 2014), we argue that legitimacy threats increase in line with rising institutional differences between a firm’s home and host countries (Ahmadjian, 2016; Kostova and Zaheer, 1999; Zhang et al., 2021). Our additional analysis shows that higher levels of regulative and normative institutional distances trigger stronger CSR responses. We stress that institutional distance does not equal geographical distance; activities in countries with similarly strong institutions as those in Japan (and thus low institutional distance) do not threaten the legitimacy of Japanese firms as much as activities in countries with weaker institutions (and thus high institutional distance), even if the latter are in closer proximity. It hence also seems consistent that international activities in the Asia-Pacific region are the strongest driver of Japanese CSR. Japanese firms are widely active in this region, but, importantly, it is also a region where countries on average are more institutionally distant to Japan than in North America or Europe (see Appendix A). Japanese firms frequently experience that their legitimacy is on “thin ice” in neighboring Asian countries, particularly when the relatively large institutional distances are accompanied by occasionally surfacing anti-Japanese sentiments (e.g., Vekasi and Nam, 2019).

As a second contribution, we reveal the complex relationships between different dimensions of internationalization, on the one hand, and different CSR dimensions on the other. Our results show that it is predominantly the environment sub-dimension that is positively affected by the internationalization of firm activities. This seems reasonable: first, the “pollution haven hypothesis,” according to which increasing internationalization simply leads to a relocation of pollution-intensive businesses to emerging countries, has only produced mixed evidence in the past (e.g., Shapiro, 2014). Instead, environmental protection is considered increasingly important across the world—and not only in developed countries (e.g., Shirodkar and Shete, 2022). Hence, it is plausible for firms to place emphasis on this “commonly accepted” and globally legitimizing dimension of CSR (Rathert, 2016). Second, environmental policies and actions are core strengths of Japanese CSR. While studies have suggested that, overall, Japanese firms only occupy mid-table positions in international CSR comparisons, the environment dimension is the only one where Japanese firms are at the forefront (Jackson and Bartosch, 2017; Nakamura et al., 2001). Thus, instead of “experimenting,” Japanese firms are building on their traditional strengths in the face of increasing internationalization. After all, other dimensions of CSR are traditionally met with more skepticism by Japanese firms, since their implications are often perceived as being less straightforward (Choi and Aguilera, 2009; Perera and Hewege, 2022). This might also explain the mixed links between internationalization of activities and the other CSR dimensions, such as the HR or social dimension.

However, it is precisely in these dimensions where ownership internationalization and board internationalization have an impact. Board internationalization is positively related to overall CSR and the HR dimension. The HR dimension contains many aspects not considered strengths of traditionally oriented Japanese firms, such as the promotion of employee diversity, gender equality, or better working conditions for parents (Mun and Jung, 2018; Suzuki et al., 2008). Thus, even when foreign directors do not assume immediate responsibility for HR affairs, their different backgrounds and ideas might propel firms to advance in CSR-related issues. By uncovering the effect international board members have on CSR in more detail, we hence expand the still relatively scant literature on the important role of board internationalization in the CSR context (e.g., Garanina and Aray, 2021; Zhang et al., 2018).

By comparison, the relationship between ownership internationalization and CSR is more complex. Importantly, we cannot confirm any effect of higher foreign ownership levels on overall CSR of Japanese firms. This is contrary to the positive role of foreign investors reported in other studies, most of which are set in emerging market contexts (e.g., Guo and Zheng, 2021; Tokas and Yadav, 2020). Possibly, Japanese firms are less concerned with legitimacy issues than firms from other countries when facing increased foreign ownership levels. Instead, they might prioritize more immediate foreign shareholder pressures, such as increasing financial performance (e.g., Baba, 2009). Conversely, many foreign portfolio investors might also prefer a shareholder-friendly management and “hard facts” over rather intangible, costly, and long-term-oriented CSR (Motta and Uchida, 2018; Yoshikawa et al., 2007). This might explain foreign ownership’s positive relationship with the social dimension of CSR, despite the absence of a positive effect on overall CSR; a closer look at Tōyō Keizai’s social dimension reveals that it incorporates items that arguably spur the interest of foreign shareholders, such as information on regular investor dialogues or on firms’ inclusion in SRI indexes and funds (e.g., Michelson et al., 2016).

As a third contribution, our study supports the notion that firms around the globe seem to respond to internationalization with increased CSR efforts—at least on a superficial level. While previous studies have extensively focused on Western firms (Attig et al., 2016; Strike et al., 2006), and, more recently, on firms from emerging markets (e.g., Sahasranamam et al., 2022; Zhang et al., 2021), our study finds evidence that internationalization also enhances CSR in the context of Japan. This is striking, in that in spite of Japan’s high level of economic development, the country has no longstanding CSR legacy, and many CSR measures are considered at odds with the “traditional” Japanese firm (Fukukawa and Teramoto, 2009; Horiguchi, 2021). For instance, many Japanese firms respond to pressures for more gender equality by installing women in prominent top management positions, but not by tackling gender-related issues at their core (Mun and Jung, 2018).

However, it is precisely here where legitimacy theory can provide an explanation: Japanese firms do not (primarily) struggle with CSR because of potential cultural differences or because they are a latecomer to CSR—they struggle because CSR is rather a response to legitimacy threats than an intrinsic motivation of firms (Horiguchi, 2020). Put differently, Japanese firms choose a “foreign weapon” (CSR) with which they are neither fully familiar nor convinced of, to fight “foreign legitimacy threats.” This could be interpreted as a hint that CSR is yet another selective foreign import that does not necessarily alter the structural integrity of Japanese firms but is rather part of a long-term evolutionary process (Westney, 2006). This appears to relate mostly to Suchman’s idea of “pragmatic legitimacy” rather than to “cognitive legitimacy” or to “moral legitimacy” (Suchman, 1995). Japanese firms use CSR to counter legitimacy threats by responding to claims addressed by the firm’s most immediate audiences, which nowadays are not just Japanese, but increasingly international.

In this context, our study provides evidence of the spread of CSR practices around the globe—at least at the surface level. This is in line with expectations that explicit manifestations of CSR are on the rise. In their seminal article, Matten and Moon (2008) certified that Japan, through its “exposure to global capital markets, the adoption of American business techniques and education models, and challenges to their national governance capabilities,” is on a fast-track to adopting explicit forms of CSR. Although we cannot confirm the suggested impact of global capital markets, the general prediction of Matten and Moon (2008) appears to hold.

However, Matten and Moon (2020) more recently contended that CSR developments are less straightforward than originally anticipated and that lines between explicit and implicit are becoming increasingly blurred. Moreover, there are signs that the effects of different CSR antecedents are neither always immutable nor the same across contexts. For instance, foreign investors were considered drivers of CSR in Japan a while ago (Suzuki et al., 2008, 2010), but now seem to have lost this power—unlike in other places (e.g., McGuinness et al., 2017) Thus, although CSR may be spreading around the globe, its drivers and manifestations are not necessarily universal.

Finally, our paper also provides a managerial contribution. Top managers are well advised to use CSR as a shield against legitimacy threats. Hereby, they should consider that different dimensions of internationalization have different implications for the respective CSR dimensions. Since our study is designed as a quantitative one, we are unable to reveal in how far each single firm (and, even more specifically, the top management in each firm) approaches CSR in the context of firm internationalization. We should, however, acknowledge that, in managerial practice, CSR is likely to be firm-specific, since each firm has its own corporate culture and requirements that strongly shape its CSR (Gorondutse and Hilman, 2016). While CSR has become increasingly important across the globe, CSR should not be interpreted as a universally applicable management tool and concept—at least if we move beyond CSR as a mere rhetoric in society and business (Preuss, 2023).

Limitations

The limitations of our study pave the way for future research. First, we are aware that our measure of CSR can be criticized. Like most quantitative CSR studies, we rely on an existing CSR rating (e.g., Dam and Scholtens, 2013; Zhang et al., 2021). However, measuring CSR is arguably a complex matter and we, for instance, have no insights to what extent firms live up to their CSR claims (Dahlin et al., 2020). Our theoretical argumentation considers this problem by assuming that firms utilize both symbolic and substantive CSR measures to maintain legitimacy. However, for future empirical studies, this very differentiation—as well as the differentiation between peripheral and embedded CSR (e.g., Chen et al., 2021) or implicit and explicit CSR (Horiguchi, 2021; Matten and Moon, 2008)—could lead to a powerful increase in our understanding of the nature of CSR.

Second, we call on future research to look at different levels in firms. The obvious starting point would be to untangle headquarters and foreign subsidiaries and to survey how these entities differ in terms of CSR. While our CSR measure sets out to capture the overall CSR of firms, we do not know if subsidiaries in host countries are in tune with the CSR approach of headquarters, or how foreign subsidiaries differ from each other. A reason for the absence of such studies is the unavailability of quantitative data, as conventional CSR ratings are only published as home-country or overall firm scores. However, recent qualitative studies have shown the potential to shed more light in this regard (e.g., Acquier et al., 2018).

Third, we analyzed the impact of institutional distance on CSR. Based on prior literature, we relied on regulative and normative institutions as commonly utilized institutional pillars (Kostova et al., 2020). However, while there are arguments that these two pillars are particularly relevant with regard to firms’ internationalization strategies and their legitimacy (Xu and Shenkar, 2002; Xu et al., 2004), we neglect the third, that is, cognitive, institutional pillar (Scott, 1995). Arguably, a country’s cognitive institutions are hard to capture, and it is the institutional pillar probably closest related to “culture” (Chao and Kumar, 2010; Kostova et al., 2020). Hence, aside from theoretical arguments, there are also good practical reasons for our approach, such as the newer data availability for our utilized institutional pillars compared with established culture constructs (e.g., Hofstede or GLOBE). However, we believe that in the future more studies should use proxies for the culture of countries as well as the culture of individual firms to approach the culture-CSR nexus (e.g., Gorondutse and Hilman, 2016).

Lastly, we only focused on one country. We believe that Japan is an interesting case and a valuable addition to the large amount of studies that have only considered firms from Western or, more recently, emerging market countries (e.g., Brammer et al., 2006; Zhang et al., 2021). Nonetheless, we are aware of the limitations with regards to the transferability of our findings. Hence, more single-country, comparative and cross-country designs (e.g., Dyck et al., 2019; Rana and Sørensen, 2021) could help unravel potential differences and commonalities between internationalization antecedents and CSR outcomes around the world.

Conclusion

Almost two decades ago, Matten (2006) asked: “Why do companies engage in corporate social responsibility?” To give a simple answer to this question was as impossible back then as it is today. However, we are beginning to unravel some of the drivers of CSR. In this study, we posit that internationalization is one of these drivers and that different dimensions of internationalization have different implications for firms’ CSR. As firms internationalize, they draw on CSR to offset the threats of legitimacy gaps. While not necessarily exclusive, we suggest that the association between internationalization and CSR might be particularly applicable to firms from contexts where CSR previously played no significant role—such as Japan. For these firms, CSR can function as a shield that helps to take on the challenges of internationalization. Regardless of their location, our study suggests that managers should carefully consider their firm’s internationalization across different dimensions and carefully select the appropriate CSR responses to strengthen their firm’s legitimacy.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data availability statement

Data will be made available upon reasonable request.

Notes

Country scores for regulative and normative institutions

RI = regulative institutions; NI = normative institutions

Country

RI

Country

NI

Country

RI

Country

NI

Finland

6.09

Switzerland

5.74

Liberia

3.93

Peru

4.30

New Zealand

6.01

Norway

5.66

Czech

3.93

Panama

4.30

Singapore

5.86

New Zealand

5.64

Jamaica

3.93

Mexico

4.27

Switzerland

5.83

Singapore

5.57

Poland

3.86

Senegal

4.27

Hong Kong

5.81

Qatar

5.57

Panama

3.81

Slovenia

4.26

Luxembourg

5.80

Denmark

5.54

Thailand

3.80

Brazil

4.24

Qatar

5.80

United States

5.54

Slovenia

3.79

Ecuador

4.23

Norway

5.79

Malaysia

5.51

Turkey

3.77

Spain

4.21

Netherlands

5.76

Lao

3.77

Nigeria

4.19

United Kingdom

5.69

Finland

5.50

Romania

3.76

Azerbaijan

4.17

Sweden

5.50

Uganda

3.76

India

4.14

Ireland

5.54

Luxembourg

5.49

Malawi

3.73

Jamaica

4.14

Canada

5.53

Netherlands

5.46

Egypt

3.69

Romania

4.11

Sweden

5.51

United Arab Emirates

5.43

Azerbaijan

3.69

El Salvador

4.11

Germany

5.46

Ireland

5.36

Vietnam

3.67

Malawi

4.11

United Arab Emirates

5.41

Belgium

5.34

Philippines

3.66

Russia

4.06

Australia

5.29

Canada

5.33

Iran

3.63

Ukraine

4.04

Denmark

5.27

Germany

5.30

Tanzania

3.57

Morocco

4.03

Austria

5.21

United Kingdom

5.30

Ethiopia

3.56

Georgia

4.03

United States

5.19

Hong Kong

5.27

Trinidad and Tobago

3.56

Mongolia

4.01

Malaysia

5.14

Austria

5.26

Greece

3.56

Croatia

4.00

Belgium

5.09

Australia

5.19

Colombia

3.51

Trinidad and Tobago

4.00

Estonia

4.97

Taiwan

5.11

Algeria

3.50

Ghana

4.00

South Africa

4.91

Estonia

5.04

Mongolia

3.44

Madagascar

3.99

France

4.91

Philippines

4.94

Guatemala

3.44

Cambodia

3.99

Saudi Arabia

4.84

Bahrain

4.89

Mexico

3.43

Kuwait

3.99

Chile

4.81

South Africa

4.87

El Salvador

3.43

Greece

3.97

Taiwan

4.80

France

4.83

Hungary

3.41

Lebanon

3.97

Bahrain

4.76

Czech

4.76

Brazil

3.39

Bulgaria

3.94

Mauritius

4.67

Lithuania

4.73

Italy

3.36

Uruguay

3.93

Jordan

4.57

Indonesia

4.71

Russia

3.31

Vietnam

3.89

Uruguay

4.50

Costa Rica

4.70

Croatia

3.29

Uganda

3.89

Israel

4.46

Saudi Arabia

4.66

Bosnia–Herzegovina

3.27

Liberia

3.87

Oman

4.44

Latvia

4.66

Nigeria

3.26

Hungary

3.86

Costa Rica

4.41

Thailand

4.61

Pakistan

3.24

Zimbabwe

3.84

Georgia

4.19

Israel

4.61

Serbia

3.21

Argentina

3.83

Zambia

4.17

South Korea

4.60

Bolivia

3.19

Slovak Republic

3.83

Portugal

4.14

Mauritius

4.59

Peru

3.17

Pakistan

3.77

Senegal

4.14

Sri Lanka

4.59

Lebanon

3.11

Tanzania

3.73

China

4.11

Guatemala

4.59

Mozambique

3.11

Italy

3.70

Kuwait

4.10

Jordan

4.54

Cambodia

3.07

Egypt

3.69

Spain

4.09

Chile

4.49

Ecuador

3.06

Ethiopia

3.69

Sri Lanka

4.09

Kenya

4.43

Bulgaria

3.04

Paraguay

3.66

Indonesia

4.04

Portugal

4.40

Zimbabwe

3.03

Venezuela

3.66

Latvia

4.04

China

4.39

Bangladesh

2.93

Bolivia

3.60

Morocco

4.04

Lao

4.34

Slovak Republic

2.87

Mozambique

3.59

Kenya

4.04

Colombia

4.34

Paraguay

2.86

Bangladesh

3.54

India

4.03

Kazakhstan

4.34

Madagascar

2.80

Bosnia–Herzegovina

3.53

Ghana

4.01

Oman

4.33

Ukraine

2.80

Serbia

3.47

Kazakhstan

4.00

Zambia

4.33

Myanmar

2.79

Iran

3.46

South Korea

3.99

Turkey

4.31

Argentina

2.71

Myanmar

3.40

Lithuania

3.97

Poland

4.31

Venezuela

1.61

Algeria

3.33