Abstract

Fraud against individuals is a major and growing problem. Understanding why some people fall victim to fraud, while others do not, is crucial in developing effective prevention strategies. We therefore studied the effect of socio-demographics, personality traits, mental, general, and cognitive health, routine Internet activities, and prior fraud knowledge on general fraud victimization, susceptibility to fraud attempts, and exposure to fraud attempts. We modeled data from a Dutch fraud victimization survey, using an exhaustive fraud taxonomy and a representative sample for which an elaborate set of historical background variables were available. Results show that there is no clear personality or other profile of those most at risk for fraud, except for having low self-control, having a non-Western, immigrant background or being a frequent Internet user. Improving fraud knowledge could be an effective way to prevent fraud victimization by reducing susceptibility to attempts.

Introduction

Since the end of the last century, general statistics on registered crime and victimhood have dropped (Blumstein et al., 2000; De Jong, 2018; Hopkins, 2016; Van Dijk et al., 2012). This phenomenon has been dubbed the ‘crime drop’. When all types of crimes are considered, this decrease holds true and persists. However, a different picture can be seen when crime data are inspected more specifically, for instance, when focusing on fraud.

Fraud statistics across the globe, namely, have shown an increase in recent years, causing billions ($) of damage (Hine, 2021; PwC, 2022). New peaks in registered fraud have been seen in, for example, the United States (FTC, 2022a), the United Kingdom (ONS, 2022), and across Europe (EPC, 2022; Kemp et al., 2020), part of which may be explained due to a surge related to the coronavirus disease (COVID)-19 pandemic (Zhang et al., 2022). These increases form a worrying trend, as fraud causes considerable damage to society. If nothing changes, the problem may only become worse.

Fraud can be defined as ‘intentionally and knowingly deceiving [a] victim by misrepresenting, concealing, or omitting facts about promised goods, services, or other benefits and consequences that are non-existent, unnecessary, never intended to be provided, or deliberately distorted for the purpose of monetary gain’ (Beals et al., 2015: 7). It can be divided into fraud targeting organizations and fraud targeting individuals. These two major categories of fraud have distinct forms (Beals et al., 2015); thus, investigations into them also require vastly different research methods. While both are highly relevant, the current research focuses on fraud against individuals.

An important question in research on fraud against individuals (or: ‘consumer fraud’, ‘personal fraud’, ‘individual fraud’) is why some people fall victim, while others do not. Answering this question is key for effective and efficient measures that prevent victimization (Burke et al., 2022; NFA, 2011: 12). The goal of the current study is to contribute to that goal by thoroughly investigating the relation of a wide range of various personal risk factors in relation to fraud victimization, with a focus on personality traits. Socio-demographics, mental, general, and cognitive health, routine Internet activities, and prior fraud knowledge are also investigated as personal risk factors.

In the next sections, we will first discuss current issues in fraud victimization research that this study aims to address. Then, we will discuss potential personal risk factors for fraud victimization, summarizing previous findings and various theoretical perspectives. Finally, we will present the research questions of the current work.

Issues in previous fraud victimization research

The use of a unified fraud taxonomy

The types of fraud that individuals may fall victim to are many (Button et al., 2009). Moreover, fraudsters constantly evolve their methods and adapt to the latest events (e.g. COVID-19 frauds surged quickly after the onset of the pandemic (Hoheisel et al., 2022; Kennedy et al., 2021; Ma and McKinnon, 2022). Beals et al. (2015) recognize that this has led to a wide array of research instruments based on various fraud definitions, some of which quickly became outdated. This troubles knowledge synthesis, as comparing and merging insights from studies based on different fraud taxonomies is difficult if not impossible.

Therefore, Beals et al. (2015) set out to develop a general fraud taxonomy, with exhaustive and mutually exclusive categories. This taxonomy was successfully tested with the Federal Trade Commission’s Consumer Sentinel Network database, which contains many fraud complaint cases. By use of this fraud taxonomy, the current study will produce insights into a distinct set of fraud types with varying modi operandi (methods). The unified and broad nature of the fraud taxonomy ensures that these insights are robust, futureproof, and suitable for future knowledge synthesis (Beals et al., 2015).

Measuring fraud victimization as a two-stage process: exposure and susceptibility

Fraud victimization can be considered a two-stage process (Fan and Yu, 2022; Holtfreter et al., 2008; Policastro and Payne, 2015). First, a part of the entire population is exposed to a fraud attempt; then, a part of the exposed (or ‘targeted’ 1 ) population is susceptible to the fraud attempt and becomes a victim. In other words, victimization is a product of both the likelihood of exposure and susceptibility. 2 Different factors may affect exposure and susceptibility, and the same factors may affect exposure and susceptibility differently (Fan and Yu, 2022). Thus, improving upon previous fraud victimization studies which did not make the distinction between exposure and susceptibility (e.g. DeLiema et al., 2017b), this study will measure fraud as a two-stage process. This allows for a better understanding of the mechanisms behind fraud victimization.

The use of a representative sample

As DeLiema et al. (2017a: 7) note, a problem with fraud victimization surveys is that many rely on non-representative samples. Some surveys, for instance, only use a sample of confirmed victims, as identified by law enforcement or complaint agencies (e.g. Consumer Fraud Research Group, 2006; Pak and Shadel, 2011). Other studies are only done in specific subgroups of the population, like older adults (e.g. Burnes et al., 2017; Judges et al., 2017; Xing et al., 2020; Yu et al., 2021), or, more generally, with sampling methods that may not have been adequate for reaching a truly representative sample (Deevy et al., 2012: 10). The latter could, for example, be because of a too-small sample, a relatively low response rate (e.g. Centraal Bureau voor de Statistiek (CBS), 2022), the use of self-selection sampling (Scherpenzeel, 2018), or the lack of inclusion of computer illiterate participants (Eckman, 2016). Consequently, the outcomes of fraud victimization studies are hard to compare, and sampling problems may have led to results not being true for the general population. The current study will make use of a sampling strategy that addresses these problems.

The use of longitudinal data

As Van ’t Hoff-de Goede et al. (2023) point out, many previous victimization studies only used data collected at one point in time. This hinders the establishment of causal relationships since there is no temporal ordering between independent and dependent variables. 3 In other words, it cannot be said with certainty that a variable affected the risk of victimization, because victimization may have also affected the variable; Agnew et al. (2011), for instance, show that self-control may be reduced after victimization. The current study will therefore make use of longitudinal data.

Personal risk factors for fraud victimization: previous findings and theory

Socio-demographics

Characteristics that are associated with the risk of fraud victimization may first and foremost be socio-demographics. Basic socio-demographic information is almost always measured in victimization research. However, considering the relatively limited amount of research specifically about fraud, and considering the sampling and measurement issues mentioned in the previous section, it remains unclear what the precise influence of socio-demographic variables is, if there is any at all. The Office for National Statistics (UK) states that unlike many other types of crime, fraud . . . [is] often committed anonymously, with the offender not having a specific target in mind. As such, there tends to be considerably less variation in demographic groups than with other types of crime. (ONS, 2022)

In line with this idea, large studies found no relationship between sex and fraud victimization (Morgan, 2021; ONS, 2022). Yet, this may be different for specific forms of fraud, like dating fraud (‘romance scams’) which has women as the most common victim (Whitty, 2018). A popular idea is that older people are more vulnerable to fraud, but there is no clear evidence for this (Ross et al., 2014; Shang et al., 2022). Instead, it may be younger people that are victimized more often (DeLiema et al., 2017b) or perhaps middle-aged people (Anderson, 2019; ONS, 2022). Data collected among US residents by the Federal Trade Commission show that the effect of age differs per fraud type, with younger people falling victim more often to online shopping fraud and older people more to tech support (helpdesk) fraud and prize fraud (FTC, 2022b). As Deevy et al. (2012) review, studies have shown that people with a lower income or in financial stress have higher odds of being victimized, though this too may depend on the type of fraud: investment fraud victims may have a higher than average income, while lottery fraud victims may have a lower than average income (Kieffer and Mottola, 2017; Pak and Shadel, 2011). The literature contains mixed findings on whether education is associated with more or less fraud victimization, with some research suggesting that people at the educational extremes (dropped out of high school or a with a master’s degree) are least likely to fall victim (see reviews in Deevy et al., 2012; Zhang and Ye, 2022).

Personality traits

Personality can be defined as ‘individual differences in characteristic patterns of thinking, feeling, and behaving’ (APA, 2023). Such differences may explain why in similar situations different people reach different outcomes (see, for example, Haslam and Smillie, 2022; John and Srivastava, 1999; Roberts et al., 2007; Roberts and Yoon, 2022). Victimization researchers studied the personality profiles of victims of various types of crime, although the work so far has been relatively sporadic and limited (see overviews in Cawvey et al., 2018; Norris et al., 2019; Van de Weijer and Leukfeldt, 2017). Below, we will discuss how various personality traits may relate to fraud victimization and what theories are available to explain these relations.

Self-control

Perhaps the most important and most frequently studied personality trait in relation to victimization is self-control. According to self-control theory, people with low self-control are more risk-taking and impulsive, making them more likely to be both perpetrators and victims of crime (Gottfredson and Hirschi, 1990; Pratt et al., 2014; Schreck, 1999). A meta-analysis found self-control to be a modest yet highly consistent predictor of victimization (Pratt et al., 2014). Studies have confirmed that this is true for consumer fraud victimization (Holtfreter et al., 2008; Van Wilsem, 2013) and forms of cybercrime that involve individual choice (Bossler and Holt, 2010; Louderback and Antonaccio, 2021), which includes forms of fraud.

Big Five

The Big Five personality index has been studied extensively in relation to victimization. The Big Five is perhaps the most widely adopted personality typology and consists of five distinct traits: openness to experience, conscientiousness, extraversion, agreeableness, and neuroticism (Abood, 2019; Goldberg, 1990). Cawvey et al. (2018) and Van de Weijer and Leukfeldt (2017) both investigated the Big Five in relation to victimization with large, representative samples. Cawvey et al. (2018) focused on general victimization, while Van de Weijer and Leukfeldt (2017) focused on the comparison of traditional crime and cybercrime victims and found that the same personality traits predicted both forms of crime; thus, the traits that apply to general crime may apply to fraud victimization. Other more specific studies also linked certain Big Five traits to fraud victimization, however sometimes with conflicting findings (Judges et al., 2017; Kirwan et al., 2018; Modic and Lea, 2012; Xing et al., 2020). Based on these studies and the hypotheses put forward by their authors, several Big Five traits may relate to fraud victimization via various mechanisms:

Openness to experience may increase the risk of victimization (Cawvey et al., 2018; Van de Weijer and Leukfeldt, 2017). Cawvey et al. (2018: 126) propose that individuals high in openness to experience thrive on novelty and regularly put themselves into unfamiliar contexts, while they are unconcerned with potential victimization threats. In the context of phishing, Van de Weijer and Leukfeldt (2017) hypothesize that users with a high degree of openness to experience may be more inclined to open e-mail attachments; this may be due to heightened curiosity associated with the trait.

Low conscientiousness may increase the risk of victimization (Judges et al., 2017; Van de Weijer and Leukfeldt, 2017). As Van de Weijer and Leukfeldt (2017) point out, conscientiousness has both conceptual and empirical overlap with self-control, so self-control theory may at least partly explain the relationship between conscientiousness and victimization. Judges et al. (2017) furthermore argue that conscientious people are detail-oriented and avoid taking impulsive decisions, taking time to consider potential outcomes; this would make them less likely to be swayed by the false promises of fraudsters.

Extraversion may either increase (Kirwan et al., 2018; Modic and Lea, 2012) or reduce (Cawvey et al., 2018) the risk of victimization. Modic and Lea (2012) argue that introverts are more at risk due to two reasons. First, introverts may prefer contact over the Internet, which is a less rich form of communication and diminishes the ability to judge the trustworthiness of others. Second, introverts may be less aware of the various types of constantly changing scams since knowledge about fraud spreads through social contact. However, Cawvey et al. (2018) argue that extraverted individuals are more likely to be exposed to offenders, through their higher need for social interaction and consequent increased contact with others; furthermore, extraverts may be more prone to inadvertently reveal sensitive information about themselves, which offenders can abuse.

Agreeableness may either reduce (Cawvey et al., 2018; Xing et al., 2020) or increase (Modic and Lea, 2012) the risk of victimization. Xing et al. (2020) argue that agreeable people tend to have good and trustful interpersonal relationships; these relationships allow them to acquire knowledge and make better social judgments, which protect them from fraud. Agreeableness, like conscientiousness, may overlap with self-control, as Van de Weijer and Leukfeldt (2017) and Cawvey et al. (2018) note. However, Modic and Lea (2012) argue that agreeable people, due to increased friendliness and empathy, are more willing to respond to fraudulent offers; this could render them particularly vulnerable to fraud forms which rely on empathy, like charity fraud and friend-in-need fraud.

Neuroticism may increase the risk of victimization (Van de Weijer and Leukfeldt, 2017). While Van de Weijer and Leukfeldt (2017) do not provide an explanation for this relationship, it may rely on the same mechanism that connects mental health and fraud victimization, as neuroticism encompasses the tendency to experience negative emotions (see the section on ‘Mental health and optimism’).

Self-esteem

Self-esteem is a trait that has been previously connected to peer victimization (children falling victim to the aggressive behavior of non-sibling other children, i.e. bullying) (Van Geel et al., 2018). Van Geel et al. (2018) hypothesize that those with lower self-esteem may be easy targets for offenders and that those with low self-esteem may fail to defend themselves (see Veenstra et al., 2010; Volk et al., 2014). High self-esteem has also been found to be associated with reduced susceptibility to persuasion (Kropp et al., 2005; Leary and Baumeister, 2000; Rhodes and Wood, 1992). It can thus be expected that people low in self-esteem are at higher risk for falling victim to fraud, but, to the best of our knowledge, no research has yet examined this relationship.

Mental health and optimism

Some research suggests that mental health may play a role in fraud victimization. Victimization data show that traits related to mental health, like happiness, life satisfaction, psychological well-being, and positive affect, may reduce the risk of becoming a fraud victim (Ebner et al., 2020; Yu et al., 2021; Yulei et al., 2021). As Norris and Brookes (2021) outline in an extensive review of the literature, an explanation for this mechanism could be that people in negative emotional states are more receptive to the appeals in fraudulent communication because they seek to repair their mood, connecting to theories about mood management like the Negative State Relief Model (Cialdini et al., 1973) and the Hedonic Contingency Hypothesis (Wegener and Petty, 1994). Following this line of thinking, positively framed fraudulent communication may present as an opportunity to alleviate negative feelings. One could expect poor mental health to be connected to fraud categories such as prize fraud and investment fraud, in which victims are lured by promising rewards, but not to categories such as debt fraud, in which victims are instilled with fear about ‘missed’ payments and subsequent negative consequences. However, there is also other work that points out that a negative mood may be associated with more vigilant, detail-oriented information processing, as well as with more skepticism (Forgas, 2017; Norris and Brookes, 2021); this suggests that those with worse mental health could be less instead of more vulnerable.

A personality trait strongly related to mental health is optimism (Conversano et al., 2010; Scheier et al., 2001). Following the above notion about how worse mental health increases the risk of fraud victimization, one can thus argue that optimism is associated with a reduced risk of fraud victimization. Moreover, optimism is associated with taking proactive steps to protect oneself and solving one’s problems (Carver et al., 2010), which means it could be connected to behaviors that protect oneself against fraud. However, optimism can also have drawbacks. As Gibson and Sanbonmatsu (2004) have shown, the positive expectancies and persistence of optimists makes them lose more money at gambling, that being a context in which these traits are punished. This may extend to victimization of, for instance, investment fraud, where an optimist may have too much faith in a fraudulent investment scheme.

Relation to others

Some personality traits explicitly describe how an individual relates to others. Since individual fraud tends to involve interaction with fraudsters, these traits may affect that process and consequently the victimization risk. Below, we will discuss three of these traits that we will investigate: general trust in others, closeness to others, and social desirability.

It has been hypothesized that a high level of general trust in others may be a risk factor for fraud victimization (see review in Shao et al., 2019). While an intuitive idea, recent research has not been able to confirm this relation (Ebner et al., 2020; Judges et al., 2017). Some research even suggests that people with higher general trust may have a lower risk of fraud victimization, since they are better at detecting lies (Carter and Weber, 2010); in line with this, Anderson (2003) found that lottery scam victims have a lower than average level of general trust.

Closeness to others has been commonly measured with the ‘Inclusion of Other in the Self’ (IOS) scale (Aron et al., 1992). Self-other overlap has been linked to empathy-induced helping, though this relationship has been up for debate (Batson, 1997; Cialdini et al., 1997; Eisenberg and Sulik, 2012; Ioerger et al., 2019). Closeness to others could thus render individuals more vulnerable to forms like charity fraud, friend-in-need fraud, and dating fraud, during which victims are asked to help others.

Social desirability scales have been used to assess participant social desirability bias, with the idea that it merely reflects reporting differences. Bell and Naugle (2007), for instance, found that social desirability is connected to less self-reported victimization of partner abuse, which, they hypothesize, is due to impression management and not due to an actual difference, though they note that not all research agrees with this hypothesis (e.g. Riggs et al., 1989). Evidence from Connelly and Chang (2016) suggests that social desirability captures personality. Items from the Marlowe–Crowne social desirability scale include, among others, ‘I never hesitate to go out of my way to help someone in trouble’ and ‘I am sometimes irritated by people who ask a favour of me’ (Crowne and Marlowe, 1960). Thus, social desirability measurements may very well reflect how people react to requests of fraudsters, with more socially desirable acting people being more prone to cooperate with requests of fraudsters.

Other personal risk factors

Physical health, health risk behaviors, and cognitive health

A range of studies investigated the effects of fraud victimization on health (Burnes et al., 2017; DeLiema et al., 2017a; Golladay and Holtfreter, 2017; Lamar et al., 2022). Less research has investigated the effect of health on the risk of fraud victimization. In a sample of older adults, DeLiema et al. (2017a) found that good self-rated general health was associated with significantly less fraud victimization in the following years. Health risk behaviors, such as alcohol use, recreational drug use, and smoking, may then also be associated with fraud victimization. However, to the best of our knowledge, this has not been researched to date. Other work did for instance link alcohol use to an increased risk of violent victimization (Thompson et al., 2008).

Cognitive health (or: ‘cognition’) may be another characteristic that affects the risk of fraud victimization. Multiple studies have linked markers of cognitive health to scam susceptibility (Ebner et al., 2020; Judges et al., 2017; Ueno et al., 2021; Yu et al., 2021). This is in line with research that has linked cognition to financial decision-making (Agarwal and Mazumder, 2013; Gamble et al., 2015; Wilson et al., 2017), risk-taking (Rogalsky et al., 2012) and being able to doubt questionable information (Asp et al., 2012). As Deane (2018) summarizes, cognitive decline may be a key factor that makes the elderly susceptible to financial exploitation: because of it, making sound financial decisions can get harder and it gets harder to judge trustworthiness and riskiness.

Routine activities: Internet use

Following the Routine Activity Theory (Cohen and Felson, 1979; Felson, 2016), a characteristic that can increase the risk of victimization is the activities that people partake in. Van Wilsem (2013), for instance, found that the more time people spent online shopping and visiting online forums, the more likely they were to be a victim of online consumer fraud. Chen et al. (2017) found that online shopping and opening e-mails from unknown sources are associated with victimization of Internet frauds.

Prior fraud knowledge

Fraud knowledge is another characteristic that may reduce the risk of victimization. Titus and Gover (2001) found that fraud attempts are less likely to succeed if potential victims have heard of the fraud before. A study on social engineering showed that interventions that improve knowledge reduce victimization (Bullee and Junger, 2020). Yet other studies about fraud and phishing found no effect of knowledge (Holt et al., 2018; Leukfeldt et al., 2018; Van ’t Hoff-de Goede et al., 2019); these studies, however, did not take exposure to fraud attempts into account.

Taking the above into account, the current work addresses the following research questions:

In what personal characteristics do victims of fraud differ from non-victims of fraud, for various categories of fraud? (Victimization.)

In what personal characteristics do victims of fraud differ from non-victims of fraud who were exposed to a fraud attempt, for various categories of fraud? (Susceptibility.)

In what personal characteristics do those exposed to fraud attempts differ from those not exposed to fraud attempts, for various categories of fraud? (Exposure.)

Method

For our investigation, we use data from a fraud victimization survey that we conducted in 2021 (Junger et al., 2022), which was largely based on a pilot by DeLiema et al. (2017b). We linked the data from our fraud victimization survey with several background variable surveys that were previously conducted with the same participants, after which we performed the analysis.

Fraud victimization survey

From 11 January to 2 February 2021, this survey was administered with the Longitudinal Internet Studies for the Social Sciences (LISS) panel of CentERdata (Tilburg University, the Netherlands) (see https://www.lissdata.nl/). Approximately 5,000 households, consisting of about 7,500 individuals, are part of the LISS panel. Members are randomly drawn from the population register of Statistics Netherlands. Surveys are administered online; households that do not have a computer or Internet connection are provided with this to still be able to join the panel (CentERdata, 2023). The LISS panel delivers good representativeness for the Dutch population (Brüggen et al., 2016; De Vos, 2010; Eckman, 2016; Scherpenzeel, 2018).

Some 3,623 random LISS panel members were invited to participate in the survey; 2,920 members started the survey and 2,873 completed it; 9 participants were removed after an initial data quality screening, as they gave unreliable answers. This led to a final sample of 2,864 participants and a response rate of 79%.

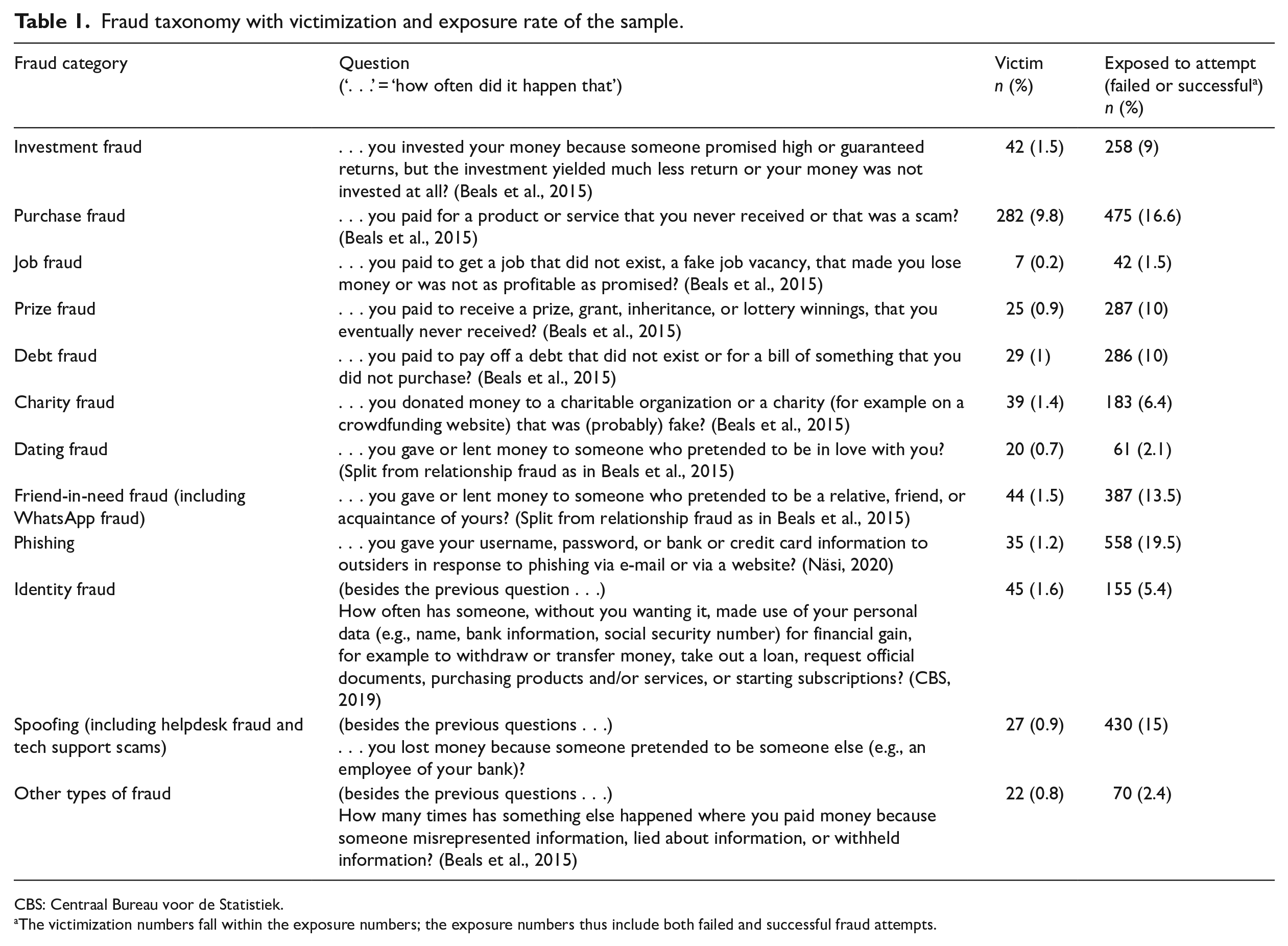

The fraud victimization survey employed the fraud taxonomy developed by Beals et al. (2015). It expanded the fraud taxonomy by splitting relationship fraud into dating fraud and friend-in-need fraud (which includes WhatsApp fraud), as specifically friend-in-need fraud gained much prominence in the Netherlands in the past years (Fraudehelpdesk, 2020). It also added categories for identity fraud (based on a digital safety and crime survey of Statistics Netherlands (CBS, 2019), phishing (based on work by Näsi (2020), and spoofing (which includes bank helpdesk fraud and tech support scams). Table 1 shows the applied fraud taxonomy and the accompanying questions that were asked to participants, which form the category definitions.

Fraud taxonomy with victimization and exposure rate of the sample.

CBS: Centraal Bureau voor de Statistiek.

The victimization numbers fall within the exposure numbers; the exposure numbers thus include both failed and successful fraud attempts.

The survey started with a victimization screening, which delivers the dependent variables of this research: victimization, susceptibility, exposure. Participants indicated for every fraud category (see Table 1) how often they fell victim to it in the year 2020 (victimization). For each category participants also indicated if they had experienced a fraud attempt to which they did not fall victim (exposure, together with those that did fall victim). Susceptibility was assessed by modeling victimization in the subsample of those who were exposed (see ‘Analysis’).

After the victimization screening, various questions were then asked about the events which were reported (these are not analyzed in the current work). At the end, background questions were asked which included a self-control scale (dysfunctional impulsivity scale from Dickman, 1990) and a question on whether participants already knew the fraud categories before encountering them and before filling out the fraud victimization survey.

Data gathered from the fraud survey were extensively inspected for correctness and pre-processed, as reported by Junger et al. (2022). This led to the final victimization and exposure rate of the sample, as shown in Table 1.

Background variable surveys

The LISS panel provides extensive data on all their participants. Basic socio-demographic variables are available for all participants that completed the fraud victimization survey. Additional data from all surveys executed with the LISS panel can be linked using a participant identifier. This includes studies on various background variables which are repeated (bi-)yearly (‘LISS core studies’).

For the current investigation, where available we use participant variables from before 2020 to predict fraud events during 2020. As fraud events may impact participant variables after they have happened, using variables from before the fraud events paints the clearest possible picture of the mechanisms behind these events and aids in eventual causal inference. 4

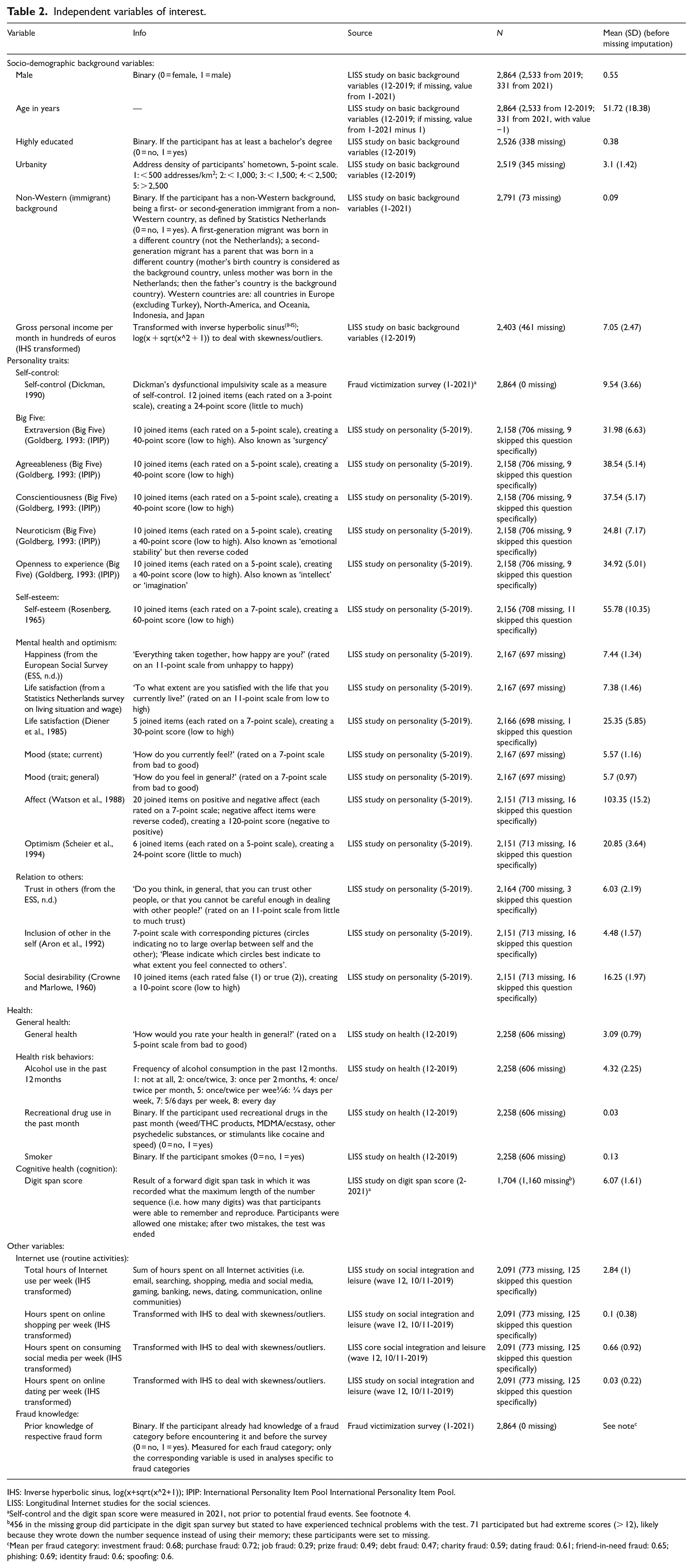

We gathered socio-demographic variables (dated 0–1 month before 2020), personality traits (6–8 months before 2020; except for self-control, which was from the end of the fraud victimization survey, 0–1 month after 2020), health and health risk behaviors (0–1 month before 2020), a digit span task (1–2 months after 2020), and Internet use (1−3 months before 2020). Table 2 provides a description of every independent variable of interest (with also variables from the fraud victimization survey). Socio-demographic background variables include sex, age, education level, urbanity, a non-Western (immigrant) background, and gross personal income. Personality traits include self-control, the Big Five, self-esteem, social desirability, various scales related to mental health, and two scales on relations with others. Health and health risk behaviors include a general subjective health question, questions on drinking, smoking, and recreational drug use, and the digit span task as a measure of cognitive health. Internet use, as an indicator of potentially relevant activities (relating to Routine Activity Theory), includes total hours of Internet use per week, and hours per week spent on online shopping, consuming social media, and online dating. Finally, prior knowledge of every specific fraud category was included from the end of the fraud victimization survey.

Independent variables of interest.

IHS: Inverse hyperbolic sinus, log(x+sqrt(x^2+1)); IPIP: International Personality Item Pool International Personality Item Pool.

LISS: Longitudinal Internet studies for the social sciences.

Self-control and the digit span score were measured in 2021, not prior to potential fraud events. See footnote 4.

456 in the missing group did participate in the digit span survey but stated to have experienced technical problems with the test. 71 participated but had extreme scores (> 12), likely because they wrote down the number sequence instead of using their memory; these participants were set to missing.

Mean per fraud category: investment fraud: 0.68; purchase fraud: 0.72; job fraud: 0.29; prize fraud: 0.49; debt fraud: 0.47; charity fraud: 0.59; dating fraud: 0.61; friend-in-need fraud: 0.65; phishing: 0.69; identity fraud: 0.6; spoofing: 0.6.

Because new members join the panel over time, some participants of the fraud victimization survey are not present in the background variables surveys that we use. 5 Sometimes participants also do not fill out every question. 6 Many statistical techniques cannot handle missing data by default, which results in the listwise deletion of participants with a missing value on any of the variables used. Multiple imputation of these missing data can then help in preserving these participants and the information that was collected on them, so improving the estimates of these analyses (Royston, 2004). With the ‘mice’ package for R (Van Buuren and Groothuis-Oudshoorn, 2011), we therefore created a multiple imputation model with all the independent variables of interest in Table 1, as well as all dependent variables. To further improve the imputations of this model we added the latest basic socio-demographic variables 7 as available for all participants of the fraud victimization survey. We created 50 imputations over a maximum of 50 iterations, respectively double and tenfold of recommend minimums (see Van Buuren, 2018a, 2018c; Von Hippel, 2007); further details are available in the R script (see ‘Availability of materials, data, and code’).

Analysis

To answer research questions 1–3, we used binary logistic regression to model three types of fraud events: ‘victimization’, ‘susceptibility’, and ‘exposure’. ‘Victimization’ encompassed prediction of who fell victim (coded as 1) or not (coded as 0), performed with the whole sample. ‘Susceptibility’ encompassed prediction of who fell victim (1) or not (0), performed with a subsample of everyone who was exposed to at least one fraud attempt in the respective category. ‘Exposure’ encompassed prediction of who was exposed to at least one fraud attempt in the respective category (1) or not (0), performed with the whole sample. Exposure included both failed and successful fraud attempts. As exposure is a condition for victimization, everyone who was a victim of a certain fraud category was also considered to be exposed to it.

Models were made for each fraud category individually. Job fraud was excluded from the analysis as the number of victimized participants was too low (7 victims for job fraud; all other categories had at least 20 victims); the ‘other types of fraud’ category was also excluded as the events in this category were diverse which would hinder finding consistent relationships with the independent variables.

A base model consisting of basic socio-demographic background variables was first specified. Then, subsequent models were made which each consisted of one characteristic together with the base model. This allows for assessment of the effect of the characteristic as only controlled for basic background variables, avoiding the ‘Table 2 fallacy’ (Westreich and Greenland, 2013).

Since we used a range of variables as predictors of victimization, susceptibility, and exposure in multiple fraud categories, many tests are performed (33 predictor variables * 3 fraud event outcomes × 10 fraud categories = 990 tests). This introduces the problem of ‘multiple testing’, meaning that several false positives will almost definitely occur. To account for this, we used the ‘qvalue’ package for R (Dabney et al., 2010) to compute q values from the 990 performed tests, which we assess instead of the respective p values. This procedure ensures that the expected proportion of false positive results remains at the alpha level, while our statistical power to find true positive results is maximized (Storey, 2003).

Results

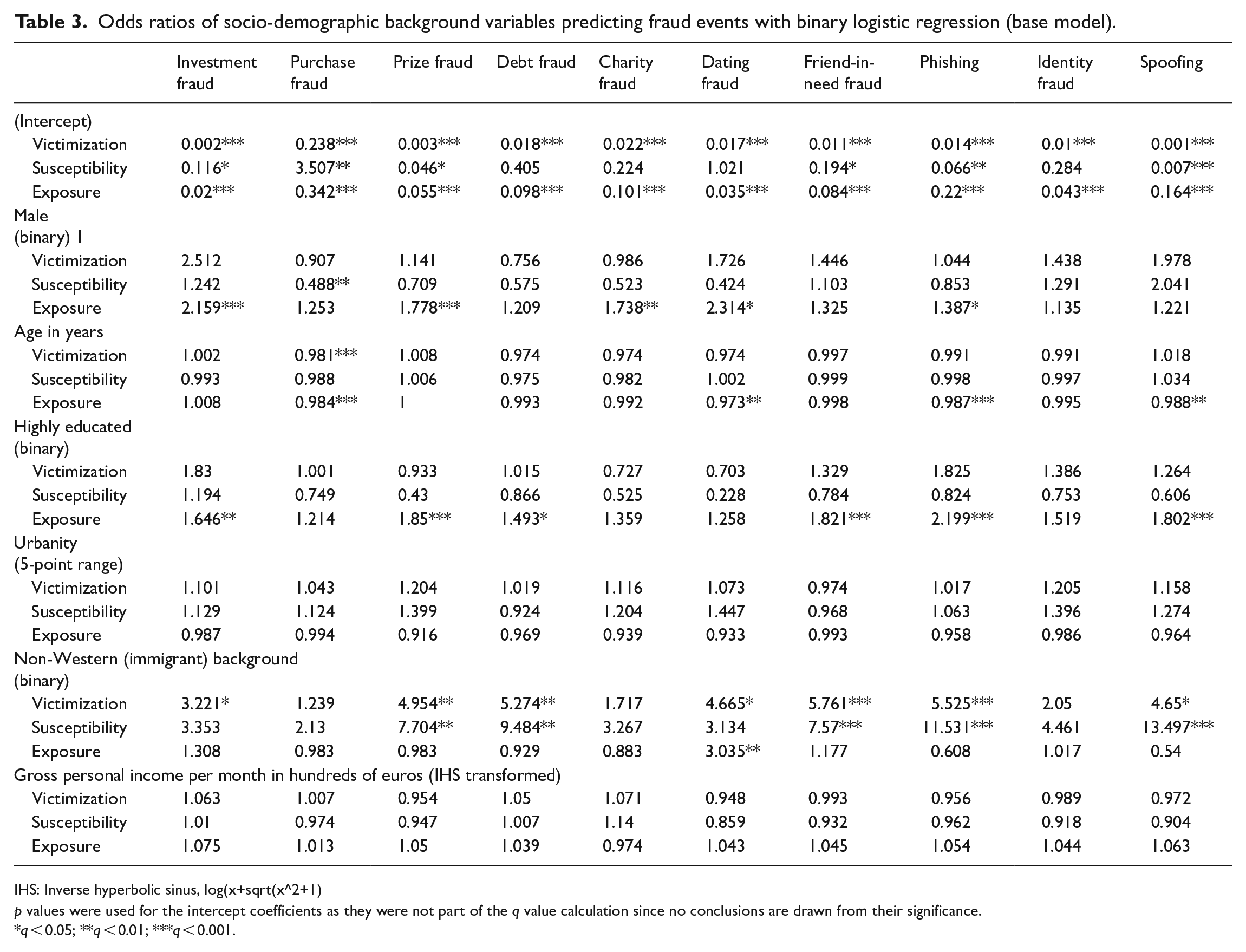

Table 3 presents the results of binary logistic regression predicting fraud victimization, susceptibility, and exposure with socio-demographic background variables only.

Odds ratios of socio-demographic background variables predicting fraud events with binary logistic regression (base model).

IHS: Inverse hyperbolic sinus, log(x+sqrt(x^2+1)

p values were used for the intercept coefficients as they were not part of the q value calculation since no conclusions are drawn from their significance.

q < 0.05; **q < 0.01; ***q < 0.001.

We found:

There were no sex differences in victimization. However, men were significantly less susceptible to purchase fraud. Moreover, men were significantly more exposed to investment fraud, prize fraud, charity fraud, dating fraud, and phishing.

Older age significantly predicted less victimization of purchase fraud. It also significantly predicted less exposure to purchase fraud, dating fraud, phishing, and spoofing.

A higher education level significantly predicted more exposure to investment fraud, prize fraud, debt fraud, friend-in-need fraud, phishing, and spoofing.

A non-Western immigrant background significantly predicted more victimization of investment fraud, prize fraud, debt fraud, dating fraud, friend-in-need fraud, phishing, and spoofing. It significantly predicted more susceptibility to prize fraud, debt fraud, friend-in-need fraud, phishing, and spoofing. It also significantly predicted more exposure to dating fraud.

Urbanity and gross personal income had no significant associations with any of the fraud categories.

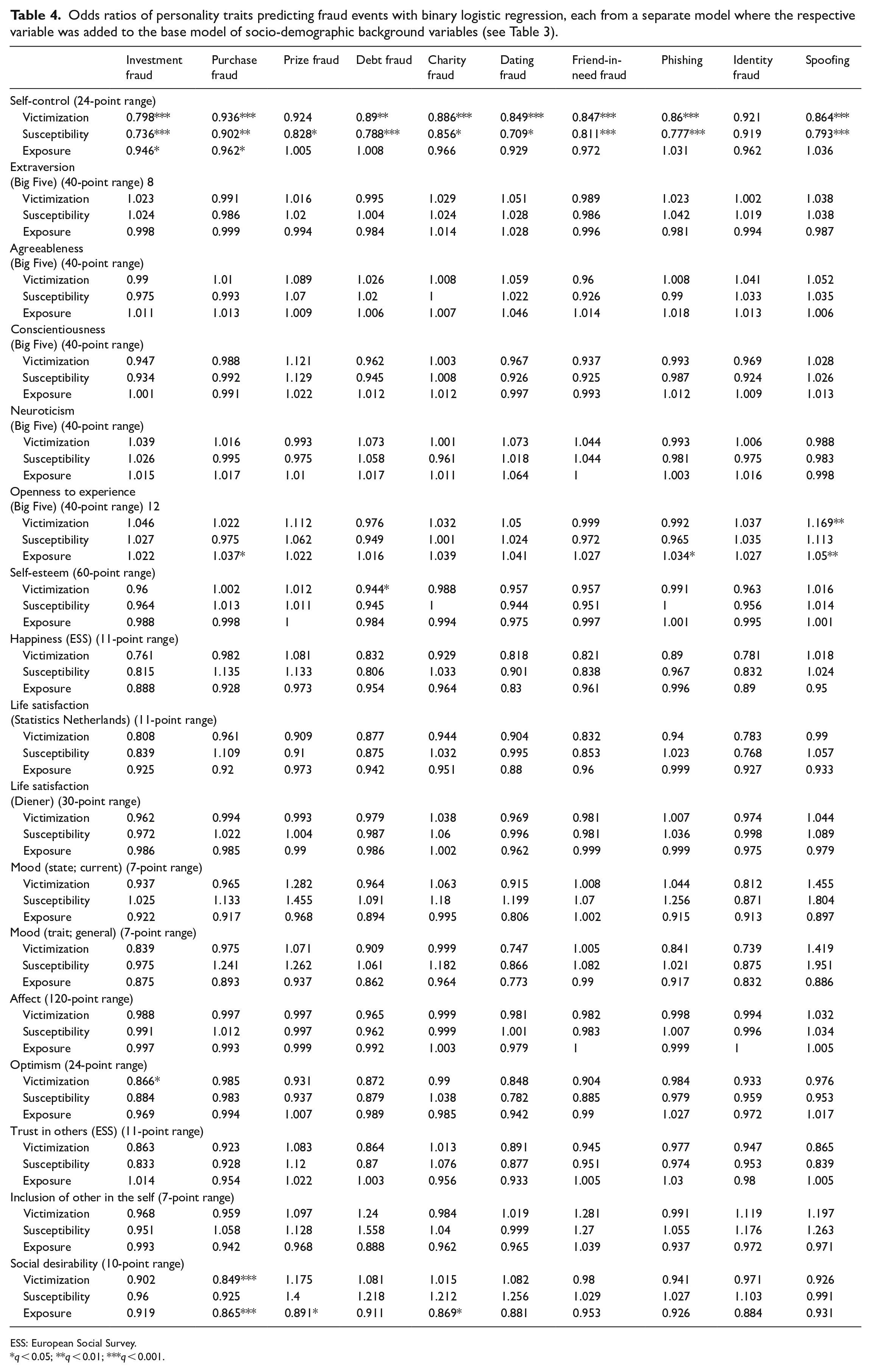

Table 4 presents the results of binary logistic regression predicting fraud victimization, susceptibility, and exposure with personality traits. For each personality trait separately, models were specified with that personality trait and the socio-demographic background variables (see Table 3) as predictors.

Odds ratios of personality traits predicting fraud events with binary logistic regression, each from a separate model where the respective variable was added to the base model of socio-demographic background variables (see Table 3).

ESS: European Social Survey.

q < 0.05; **q < 0.01; ***q < 0.001.

Self-control was associated with significantly less victimization in every fraud category except for prize fraud and identity fraud. It was associated with significantly less susceptibility to every fraud category except identity fraud. It was also associated with significantly less exposure to investment fraud, and purchase fraud.

Looking at the Big Five, extraversion, agreeableness, conscientiousness, and neuroticism had no significant associations with any of the fraud categories. Openness to experience significantly predicted more victimization of spoofing; it also significantly predicted more exposure to purchase fraud, phishing, and spoofing.

Self-esteem significantly predicted less victimization of debt fraud.

All mental health–related traits, namely happiness, both life satisfaction scales, both mood scales, and affect, had no significant associations with any of the fraud categories. Optimism significantly predicted less investment fraud victimization.

Looking at the traits about the relation to others, trust in others and the IOS had no significant associations with any of the fraud categories. Social desirability significantly predicted less victimization of purchase fraud; it also significantly predicted less exposure to purchase fraud, prize fraud, and charity fraud.

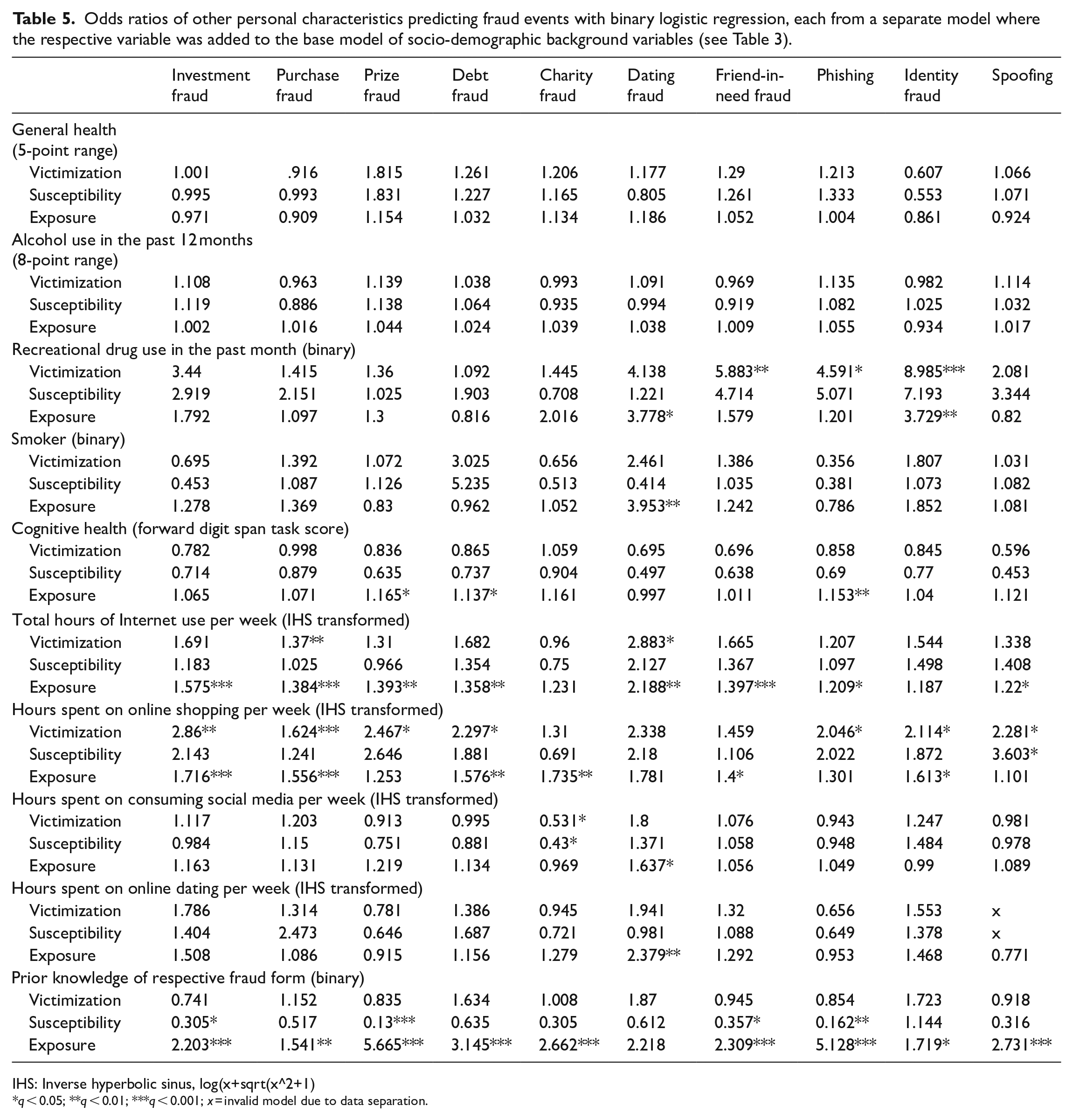

Table 5 presents the results of binary logistic regression predicting fraud victimization, susceptibility, and exposure with other personal characteristics. For each personal characteristic separately, models were specified with that personal characteristic and the socio-demographic background variables (see Table 3) as predictors.

Odds ratios of other personal characteristics predicting fraud events with binary logistic regression, each from a separate model where the respective variable was added to the base model of socio-demographic background variables (see Table 3).

IHS: Inverse hyperbolic sinus, log(x+sqrt(x^2+1)

q < 0.05; **q < 0.01; ***q < 0.001; x = invalid model due to data separation.

General health and alcohol use had no significant associations with any of the fraud categories. Recreational drug use significantly predicted more victimization of friend-in-need fraud, phishing, and identity fraud; it also significantly predicted more exposure to dating fraud and identity fraud. Smoking significantly predicted more exposure to dating fraud.

A higher forward digit span score, a measure of cognitive health, was significantly associated with more exposure to prize fraud, debt fraud, and phishing.

Looking at variables related to routine activities, more Internet use significantly predicted more victimization of purchase fraud and dating fraud; it also significantly predicted more exposure to investment fraud, purchase fraud, prize fraud, debt fraud, dating fraud, friend-in-need fraud, phishing, and spoofing. More time spent online shopping significantly predicted more victimization of investment fraud, purchase fraud, prize fraud, debt fraud, phishing, identity fraud, and spoofing; it also significantly predicted more susceptibility to spoofing and more exposure to investment fraud, purchase fraud, debt fraud, charity fraud, friend-in-need fraud, and identity fraud. More time spent consuming social media significantly predicted less victimization of and susceptibility to charity fraud; it also significantly predicted more exposure to dating fraud. More time spent online dating significantly predicted more exposure to dating fraud.

Prior fraud knowledge significantly predicted less susceptibility to investment fraud, prize fraud, friend-in-need fraud, and phishing. It also significantly predicted more exposure to every fraud category except dating fraud.

Discussion

We investigated the influence of socio-demographic variables, personality traits, and other personal characteristics on general fraud victimization, susceptibility to fraud attempts, and exposure to fraud attempts. To this end, we combined data from a Dutch victimization survey on fraud against individuals (n = 2,864) with an extensive set of participant background data, primarily measured before the fraud events occurred, and specified models which predicted the fraud events. Below, we discuss our most important findings and provide a conclusion with policy implications.

Personal characteristics predicting with fraud victimization, susceptibility, and exposure

Socio-demographics

According to our results, the influence of socio-demographic background variables is generally small and specific to fraud categories, as expected based on previous research (FTC, 2022b; Morgan, 2021; ONS, 2022).

First and foremost, our results showed no victimization differences between men and women. We did find that men are significantly less susceptible to purchase fraud and that men experience higher exposure to multiple fraud categories. Younger people experience more victimization of purchase fraud, in line with data from the FTC (2022b); our results indicate that this is driven by increased exposure. In our study, younger people furthermore experienced more exposure to multiple fraud categories. Data from the FTC (2022b) also showed that older people were about five times more likely to report losing money on tech support scams (this falls under spoofing in our fraud taxonomy); our results do not support this. While a higher education level did not affect victimization or susceptibility, it significantly predicted more exposure to several fraud categories. Urbanity and gross personal income had no impact on victimization, unlike what was suggested by previous work (Deevy et al., 2012).

One socio-demographic background variable that did play a large role was a non-Western, immigrant background. This variable significantly predicted more victimization of and susceptibility to multiple fraud categories. This population is thus much more vulnerable to fraud attempts, which may require policymaker attention. Previous research on immigrants as victims of crime is rather limited and troubled by unclear definitions, while immigration status is also conflated with ethnicity; some studies found that immigrants may be less or equally likely to be a victim of crime, except for hate and fear crime, domestic violence, and exploitation, to which they may be more vulnerable (McDonald and Erez, 2007; Makkai and Taylor, 2009).

Personality traits

Our findings indicate that the effect of personality traits on fraud victimization, susceptibility, and exposure is limited. Except for self-control, there were no clear personality traits that are associated with falling victim to and/or being exposed to fraud. Below, we discuss these findings in detail.

Self-control

Self-control was found to be the variable most strongly associated with fraud victimization, which is in line with previous research (Bossler and Holt, 2010; Holtfreter et al., 2008; Louderback and Antonaccio, 2021; Pratt et al., 2014; Schreck, 1999; Van Wilsem, 2013). Self-control was associated with significantly less victimization of and susceptibility to nearly every fraud category, and with significantly less exposure to some fraud categories. That self-control also affects exposure is an interesting finding, as Holtfreter et al. (2008) found that self-control did not affect consumers being targeted for fraud.

A limitation in our investigation of the relation of self-control to fraud victimization is that, unlike the other personality traits in our study, it was not available in the dataset prior to the year over which victimization was measured. Therefore, it was measured at the end of the fraud victimization survey. Due to this lack of temporal ordering, a causal effect of self-control on victimization cannot be determined from only this study’s data. It should be considered that victimization could affect self-control. Agnew et al. (2011) found that after victimization, self-control may be reduced in the short term, which they explain by General Strain Theory: victimization hurts physical and mental well-being and creates anger, whereby it is a strain that temporarily contributes to the traits underlying low self-control. While self-control likely still affects victimization, given the above-mentioned wide range of prior research into self-control and victimization, the impact of self-control might be overstated in the current results.

Identity fraud was the only fraud category which had no associations with self-control. As Golladay and Holtfreter (2017) write, identity theft distinguishes itself from other consumer-based frauds since it typically entails no contact or relationship between the victim and the offender. Self-control likely is important when there is interaction with fraudsters, or when the victim plays an active role like when visiting websites during online purchase fraud, but besides that it may not have an effect on fraud victimization.

Big Five

From the Big Five personality traits (see Goldberg, 1990, 1993; John and Srivastava, 1999), only openness to experience significantly predicted fraud events, and still only to a very limited degree. That openness to experience is somewhat more important than the other traits is in line with previous research from Van de Weijer and Leukfeldt (2017) and Cawvey et al. (2018), who found openness to experience to be a relatively important predictor of traditional crime and cybercrime victimization; they argued that the heightened curiosity and need for novelty associated with the trait lead to victimization through increased exposure. While this hypothesized mechanism is in line with our results for phishing and spoofing, we find the general effect on fraud to be limited.

Self-esteem

Self-esteem significantly predicted less debt fraud victimization but was not associated at all with other fraud categories. Previous research on the effect of self-esteem on victimization is very limited. Van Geel et al. (2018) found that low self-esteem may lead to peer victimization (children falling victim to other children, e.g. bullying). They explain this finding by hypothesizing that those with lower self-esteem may be easy targets for offenders (Veenstra et al., 2010; Volk et al., 2014) and that those with low self-esteem may fail to defend themselves. Other work has also suggested that self-esteem is associated with reduced susceptibility to persuasion (Kropp et al., 2005; Leary and Baumeister, 2000; Rhodes and Wood, 1992). Our findings suggest that similar mechanisms may apply to debt fraud victimization.

Mental health and optimism

A wide range of scales related to mental health (happiness, two life satisfaction scales, two mood scales, and an affect scale) did not predict any fraud events. Norris and Brookes (2021) hypothesized that people in worse emotional states may be more susceptible to appeals in fraudulent communication as they seek to repair their mood, an idea that is supported by previous research (Ebner et al., 2020; Yu et al., 2021; Yulei et al., 2021). Our findings, however, do not support this idea. Other work suggested that a negative mood may be associated with more vigilant, detail-oriented information processing, as well as with more skepticism and better deception detection (Forgas, 2017); our findings also do not support this idea. Potentially, the improved information processing cancels out negative effects that the desire for mood repairing may cause. Future research should further explore these relations.

Optimism significantly predicted less victimization of investment fraud. Previous work suggested that optimism is connected to many positive life outcomes but may have drawbacks in certain situations where positive expectations are punished, like in gambling (Carver et al., 2010; Gibson and Sanbonmatsu, 2004). In the context of fraud, optimism may be an advantage rather than a drawback.

Relation to others

We found no significant associations between fraud and two scales about the relation with others, namely, about trust in others and the IOS. That trust in others does not affect fraud victimization is in line with recent work (Ebner et al., 2020; Judges et al., 2017); while some have argued that people with more general trust are also better at detecting lies (Anderson, 2003; Carter and Weber, 2010): we found no support for this. Shao et al. (2019) suggested that credulity, rather than general trust, may be a better indicator of fraud vulnerability.

Social desirability, a third scale about the relation to others, significantly predicted less victimization of purchase fraud and less exposure to some other fraud categories. Some research has been done on social desirability and self-reporting victimization. Bell and Naugle (2007) found that social desirability is connected to less self-reported partner abuse, which, they hypothesize, is because of impression management and not because of actual victimization differences, though they note that not all research agrees with this (e.g. Riggs et al., 1989). This is part of a bigger debate regarding whether social desirability scales measure merely a response bias (‘style’) or actual personality traits (‘substance’) (Connelly and Chang, 2016; Lanz et al., 2022; McCrae and Costa, 1983). For now, it is unclear if it is reporting differences or actual exposure differences that explain our findings about social desirability.

Other personal characteristics

Health and health risk behaviors

The results of our study showed no effect of self-reported general health on later fraud victimization, susceptibility, or exposure. This is unlike the work of DeLiema et al. (2017a), who did report such an association, though in a sample of older adults. While Thompson et al. (2008) found that alcohol use can increase the risk of violent victimization, in our study we found no relationship between alcohol use and fraud victimization. Recreational drug use, however, significantly predicted more victimization of and exposure to some fraud categories. These associations of health risk behaviors and fraud are however few and may simply be the result of health risk behaviors being correlated with low self-control (Berkman et al., 2011; Conner et al., 2009; Dvorak et al., 2011; Sussman et al., 2003). Smoking significantly predicted more exposure to dating fraud; a possible explanation for this is that marital status has associations with smoking (Ramsey et al., 2019).

Cognitive health

Our findings showed no support for cognitive health (or ‘cognition’), as measured via a forward digit span task, being associated with victimization or susceptibility. It was however significantly associated with more exposure to phishing and spoofing. It is not clear why this was the case, but it should be considered that those that score better on the digit span task also tend to have a better long-term memory (Cowan, 2008; Nee and Jonides, 2008); Jones and Macken (2015) argue that the digit span task does not measure short-term memory, but long-term associative learning. Therefore, it could be a reporting difference that stems from those scoring higher on the digit span task being better at remembering fraud attempts. Regardless, digit span task score was not associated with victimization or susceptibility. This is contrary to previous work that did find that worse cognition may be associated with increased fraud victimization (Ebner et al., 2020; Judges et al., 2017; Ueno et al., 2021; Yu et al., 2021), though that work did use different measures of cognition, like self-reported cognitive ability via the Multiple Ability Self-Report Questionnaire (Seidenberg et al., 1994) or the Brief Test of Adult Cognition by Telephone (Tun and Lachman, 2006), of which a digit span task is only a part. Since convincing evidence suggests that cognition may be related to fraud victimization through the (dis)ability to make sound financial decisions and to judge trustworthiness and riskiness (Deane, 2018; Walzak and Thornton, 2022), we think the forward digit span task may simply be a too limited measure of cognition. A further limitation is that the digit span task was not conducted prior to the year over which fraud events were measured.

Routine activities: Internet use

A higher level of total Internet use and more time spent online shopping significantly predicted more victimization of and exposure to several fraud forms. Time spent online dating significantly predicted more exposure to dating fraud, in line with expectations. These findings support Routine Activity Theory (Cohen and Felson, 1979; Felson, 2016), and make sense given that the events reported in the fraud victimization survey took place mostly fully (68.9%) or partly (17.8%) online (Junger et al., 2022). That online shopping significantly predicted not just purchase fraud but also various other fraud forms may need further exploring. One hypothesis is that web shops leaking customer data put people at extra risk for fraud, for instance, because they can be approached by cybercriminals via their leaked e-mail address (see, for example, Fowler, 2022). Interestingly, more hours spent consuming online social media predicted a reduction of charity fraud victimization and susceptibility; further research should explore why this was the case.

Prior fraud knowledge

Prior fraud knowledge was not a predictor of victimization to any fraud category, but it was associated with less susceptibility to some fraud forms. From this, it seems prior fraud knowledge is important for retaliating against fraud attempts, but ultimately it does not decrease general victimization. Some previous studies on crime knowledge did not find an effect on victimization and risky behavior (Holt et al., 2018; Leukfeldt et al., 2018; Van ’t Hoff-de Goede et al., 2019), while others did (Bullee and Junger, 2020; Titus and Gover, 2001). In our findings, fraud knowledge was also associated with increased exposure to every fraud category except dating fraud. One possible explanation is that this concerns a reporting difference, with those with more fraud knowledge being better at recognizing and remembering fraud attempts; then, at least partly, the effect of fraud knowledge on susceptibility may be due to this reporting difference. However, analysis of qualitative answers from the same fraud victimization survey did show that participants primarily rely on fraud knowledge in resisting fraud attempts (Junger et al., 2023), which is in line with the current quantitative findings regarding susceptibility. Further research is needed on the effect of knowledge of victimization.

Conclusion and policy implications

Our study has several strengths and novelties. It used a large, nationally representative sample with a high response rate, which delivers high-quality data (Brüggen et al., 2016; De Vos, 2010; Eckman, 2016; Scherpenzeel, 2018). We used a fraud taxonomy with a wide variety of fraud categories, developed to be exhaustive, mutually exclusive, and futureproof (Beals et al., 2015; DeLiema et al., 2017b). We applied a two-stage approach in measuring fraud victimization, so as to also gain insight into exposure and susceptibility. We systematically analyzed a wide range of variables on socio-demographics, personality traits, mental, general, and cognitive health, activities, and prior fraud knowledge, while correcting for multiple testing, and we used data from the previous year to aid in determining causality.

Limitations of our study also need to be considered. First, despite using a relatively large and strong sample, some fraud categories only had a small number of victims. Such ‘low-event’ data reduces the statistical power of models (Woo et al., 2022). Second, we modeled susceptibility by creating models for the exposed subsample, which means that it is possible the findings regarding susceptibility do not fully apply to the broader sample, should they be exposed to fraud. A two-step model may have solved this issue but was not applicable to our data due to a lack of suitable exclusion restriction variables (Bendig and Hoke, 2022; Bushway et al., 2007). Third, while the use of data from the previous year facilitates the assessment of causal relationships, it also means that some data were already months old and therefore possibly outdated once fraud events potentially occurred (the literature does, however, suggest that personality traits like the Big Five are quite stable (Cobb-Clark and Schurer, 2012); also, causality cannot be determined from our observational data alone (Rohrer and Murayama, 2023). It should also be repeated that specifically the self-control and the digit span score variables were measured after potential fraud events, unlike other independent variables used in our models. Fourth, not all background data were available for each participant. While we used missing imputation to address this problem, it may have reduced our statistical power; 8 unfortunately, it is hard to assess power after missing imputation, since this depends on many variables which determine the quality of the imputation model, and ultimately the true value of the missing variables remains unknown. We do think our imputation model is of high quality, since we included a wide range of auxiliary variables and ran double the recommended number of imputations. Nonetheless, it should be kept in mind that absence of evidence is not evidence of absence. Fifth, fraud victimization was self-reported by participants. This means that participants may have misreported their experiences to some extent: for instance, some victims may have been unaware of their victimization or may have been unwilling to report it (see Deevy et al., 2012: 14–16). Moreover, found associations between background variables and fraud events may have reflected reporting differences instead of actual differences in exposure, susceptibility, and victimization. Sixth, we investigated a wide range of independent variables and multiple dependent variables. While we applied the q value procedure to keep the false positive rate at 5%, the possibility of false positives should still be considered. Furthermore, though the q value procedure was designed to only remove the expected share of false positives which occurs from multiple testing, identical research with less variables may have deemed certain variables significant which were now deemed insignificant.

Despite these limitations, and given the above-mentioned strengths, we think our study is an important contribution to the literature on fraud victimization. It has important implications for policy about the ‘who’ and ‘how’ of fraud victimization prevention. First and foremost, we found few and limited predictors of fraud victimization, which means that almost everyone is vulnerable. However, non-Western immigrants and frequent Internet users are at higher risk; these groups should be considered for targeted interventions, though the general public should not be neglected. Besides self-control, personality is generally of little importance to fraud victimization. While some have tried to train self-control, this seems like an unlikely way to solve the fraud problem (Friese et al., 2017; Nofziger and Rosen, 2017; Tiemeijer, 2022). Our results do point to promoting fraud knowledge as a potentially fruitful way to reduce victimization through reducing susceptibility. Besides this, our study suggests that, on the side of the individual, there is little that can be done to prevent fraud. Thus, other than improving fraud knowledge, the role of preventing fraud may fall primarily on third parties like payment providers, trading and social media platforms, and Internet and service providers, whose services are being abused for fraud.

Footnotes

Acknowledgements

In this paper, the authors made use of the data of the LISS panel, administered by CentERdata (Tilburg University, the Netherlands).

Availability of materials,data,and code

The materials and data for both the fraud victimization survey and background variable surveys and the R scripts for pre-processing and analysis are openly available at the LISS Archive (https://www.dataarchive.lissdata.nl/; materials and data) and the OSF repository (![]() , DOI 10.17605/OSF.IO/9B2Q3; R scripts).

, DOI 10.17605/OSF.IO/9B2Q3; R scripts).