Abstract

Background:

People living with terminal illness are at higher risk of experiencing financial insecurity. The variance in definitions of financial insecurity, in addition to its impact on the well-being of this population has not yet been systematically analysed.

Aim:

To understand the definition, prevalence and impact of financial insecurity on the physical and psychological well-being of people living with terminal illness.

Design:

A systematic review with a narrative synthesis (prospectively registered; CRD42023404516).

Data sources:

Medline, Embase, CINAHL, AMED, PsycINFO, ProQuest Central and Cochrane Central Register of Controlled Trials, from inception to May 2023. Included studies had to measure or describe the impact of financial insecurity on an aspect of participants’ physical or mental well-being. Study quality was assessed using the Hawker tool.

Results:

A total of 26 studies were included in the review. Financial insecurity was defined using many different definitions and terminology. Out of 4824 participants, 1126 (23%) reported experiencing high levels of financial insecurity. Nine studies reported 21 unique analyses across three domains of physical well-being. Out of those 21 analyses, 10 (48%) reported a negative result (an increase in financial insecurity was reported with a decrease in physical well-being). Twenty-one studies reported 51 unique analyses across nine domains of psychological well-being. Out of these analyses, 35 (69%) reported a negative result (an increase in financial insecurity was reported with a decrease in psychological well-being).

Conclusions:

People living with terminal illness require support with their financial situation to ensure their well-being is not negatively impacted by financial insecurity.

People who are living with a terminal illness are at greater risk of experiencing poverty.

Financial insecurity can significantly impact adherence to treatment plans and can cause undue distress.

It is unclear how financial insecurity impacts the physical and psychological well-being of people living with terminal illness.

Financial insecurity was defined and discussed in no consistent manner.

Where financial insecurity was categorised into levels of insecurity, 23% of people living with terminal illness reported experiencing high levels of financial insecurity.

An increase in financial insecurity was often reported alongside a decrease in the physical and psychological well-being of people living with terminal illness.

Policy makers should ensure that people living with terminal illness have the support they need to address their financial situation, including signposting to available support; so that they are not left to suffer from the ill-effects of financial insecurity, as well as their illness.

Standardised terminology, definition and method of assessing financial insecurity would ensure clarity in the need and prevalence of financial insecurity and allow cross-comparison across studies.

Introduction

Poverty is a complex and nuanced global discussion. Terms, definitions, indicators, measurement and thresholds for identifying and assessing poverty vary between and within countries.1–3 The current cost-of-living crisis fuelled by rising transport, food and energy prices is having a detrimental impact on global health and well-being.4,5 It is estimated that 1 in 10 people in the world live in poverty.3,6 A recent report commissioned by Marie Curie estimated that 90,000 people die each year in poverty, 7 and that people living with a terminal illness are more at risk of poverty; although this data is limited to the UK.

Financial insecurity refers to when an individual encounters objective difficulty or subjective distress when trying to cover necessary financial expenses. 8 Whilst this is the definition adopted within this review, there is no universally agreed term for this concept.9–12 People living with terminal illness (defined as an illness that is not curable and likely to lead to death) are particularly at risk of being impacted by financial insecurity and poverty as they are often forced to give up work due to ill health.13,14 This decrease in income is further compounded by the increase in out-of-pocket expenditures associated with having a terminal illness, such as more travel costs for medical appointments and the energy needed to run medical equipment at home. 15 Additional financial insecurity can arise if family members, who support someone with a terminal illness, need to reduce their working hours in order to fulfil their caregiving role. 16 While welfare benefits may be accessed to supplement or serve as one’s sole income, these payments have been found to be inadequate for people living with terminal illness. 17 To the authors’ knowledge, the extent to which financial insecurity affects people living with terminal illness has not been explored.

The evidence indicates that financial insecurity is a key determinant of poor healthcare experiences.18–21 Among people with curable cancer and survivors of cancer, experiencing financial insecurity has been found to reduce quality of life and increase rates of non-adherence to treatment plans,22,23 as well as depression, anxiety and psychological distress. 24 There is some evidence to suggest that financial insecurity impacts well-being at the end of life although this remains an underexplored area. 25

This review seeks to address the gaps in the current knowledge, through synthesising international evidence on financial insecurity for people living with terminal illness.

Review questions

RQ1: How is financial insecurity defined and measured for people living with terminal illness?

RQ2: What is the prevalence of financial insecurity in this population?

RQ3: What is the impact of financial insecurity on the physical and psychological well-being of people living with terminal illness?

Methods

This systematic review followed the Cochrane Handbook for Systematic Reviews 26 and is reported in accordance with the Preferred Reporting Items for Systematic Reviews and Analyses (PRISMA). 27 The review protocol was registered prospectively in PROSPERO on the 7th of March 2023. (CRD2023404516).

Eligibility criteria

Inclusion

Adults (18 years old and above) living with a terminal illness (synonyms: palliative, advanced, life-limiting, metastatic, non-curable, end-stage or stage 4).

Measured or described participant’s exposure to financial insecurity.

Measured or described the impact of this financial insecurity on an aspect of participants’ physical and/or psychological well-being.

Both qualitative and quantitative studies were included in this review, due to the multi-faceted experience of financial insecurity.28,29

Exclusion

Abstracts (where the full text was not available), editorials, systematic/scoping reviews, research letters, theses.

Paediatric population (<18 years)

Focus solely on carers and not patients.

Not reported in English language.

Information sources

Ovid platform (Medline, Embase, AMED and PsycINFO), CINAHL, ProQuest Central and Cochrane Central Register of Controlled Trials were searched from inception to May 2023. Grey literature was searched for via the OpenGrey website. If only an abstract was identified (i.e. conference abstracts), authors were contacted via email to provide a full text. Additionally, authors of included papers were contacted to check if they had any further relevant published or unpublished work. Forward and backward citation searching was conducted using Google Scholar, to ensure no relevant papers were missed.

Search strategy

The key concepts, taken from the review questions, were ‘terminal illness’ (population), ‘financial insecurity’ (exposure) as well as ‘physical and psychological well-being’ (outcome). A comprehensive list of search terms, both MeSH and textual and their truncated variants were derived from existing literature on terminal illness and financial insecurity.13,25 The key concepts were connected using the Boolean operator ‘AND’, meanwhile search terms within each concept were connected using the Boolean operator ‘OR’ (see Supplemental Material 1 for search strategy). Terms were adapted according to each database functionality.

Selection

All references were stored using Rayyan software. 30 Following deduplication, two independent reviewers conducted a title and abstract screen. During this stage, the primary aim for the reviewers was to check the population under study (i.e. people living with terminal illness) and whether financial insecurity was being considered. After this initial screen, two independent reviewers conducted a full-text screen, in accordance with the eligibility criteria. During this stage, reasons for exclusion were recorded. Any discrepancies were resolved via discussion between the two reviewers. If discrepancies remained unresolved following discussion, the opinion of third independent reviewer was sought.

Data collection process and data items

Data extraction tables were developed to address the review questions.

The first table detailed the study characteristics, including: author, publication date, country, setting, design, sample size and participant characteristics (i.e. sex, age, ethnicity, employment status and primary diagnosis).

The second data extraction table detailed how each study defined and measured financial insecurity.

Two tables were developed to extract data which described the impact of financial insecurity on physical or psychological well-being. Participant quotes and author reflections, which described the impact of financial insecurity on well-being, were extracted from qualitative studies and stored in a separate data extraction table.

The data extraction tables were completed by two independent reviewers (RWP and ABr) for the first three studies. Any discrepancies between the reviewers were resolved through discussion with a third independent reviewer (NW). Once the data extraction tables were deemed applicable, data extraction of the remaining studies were then completed by one reviewer (RWP).

Quality appraisal

The quality of included papers was assessed using the Hawker tool. 31 This tool comprises standardised criteria suitable for appraising the quality of research using any study design. 32 Two independent reviewers rated each domain as either very poor (+1), poor (+2), fair (+3) or good (+4). Total scores for each study ranged from 9 to 36. Discrepancies in the total scores awarded were resolved through discussion with a third independent reviewer. Whilst Hawker and colleagues 29 did not indicate how total scores could be interpreted, previous systematic reviews using this tool classified studies with a total score of 18 and below, 18–30 and 31–36 as of poor, fair or good quality, respectively.33,34 Studies were not excluded based on their quality, but they were reported to allow for a comprehensive understanding of the included studies and the data reported. It also helps to identify and pertinent problematic areas for future research.

Data synthesis

Relevant data from included studies were synthesised using a narrative synthesis approach. 35

The terminology, definitions, methods of assessment and extent of financial insecurity were tabulated. Studies were grouped by whether they measured financial insecurity with a continuous score or by grouping the participants (e.g. ‘No financial insecurity’ and ‘High financial insecurity’). A summary of the patient population was provided in relation to their sex, age, employment status and primary diagnosis.

The association between financial insecurity on the physical and psychological well-being of people living with terminal illness was analysed. Due to the substantial level of clinical heterogeneity, a meta-analysis was not completed. Therefore, the findings of quantitative studies, which assessed an impact on the same domain of well-being (e.g. psychological health), were tabulated.

All relevant unique analyses reported in the included studies were extracted, organised by the domain (physical or psychological well-being). Both correlation and predictive analyses were included and documented. To summarise the analyses, the authors extracted the main analysis findings and indicated for each analysis whether the finding was:

(1) No difference (either correlation or association)

(2) Negative (where higher financial insecurity was reported alongside a worsening domain)

(3) Positive (where higher financial insecurity was reported alongside improving domain)

To interpret the correlation analysis, the recommended benchmarks were adopted, 36 in which studies reporting an r value of 0.3 or less were considered as very weak therefore no correlation was noted. Studies reporting an r value between 0.3 and 0.4 were noted as weak, r values between 0.401 and 0.699 were noted as moderate and r values ⩾0.7 were interpreted as strong.

Data extracted from qualitative studies was analysed through reflexive thematic analysis.37,38 Modelling from previous research using this analysis, 39 this method enables the research (RWP) to fully explore and reflect on the data. RWP read each study and extracted all occasions in which financial insecurity was discussed. Through reading each extraction, RWP generated descriptive codes by noting similar experiences. The reflexive element of the thematic analysis was helpful to aid the researcher in getting familiar with the data, engaging and reflecting on the themes generated. The findings were discussed, shared and refined with the research team. The results were tabulated in a hierarchal structure consisting of overall themes and sub-themes, supported by quotes.

Results

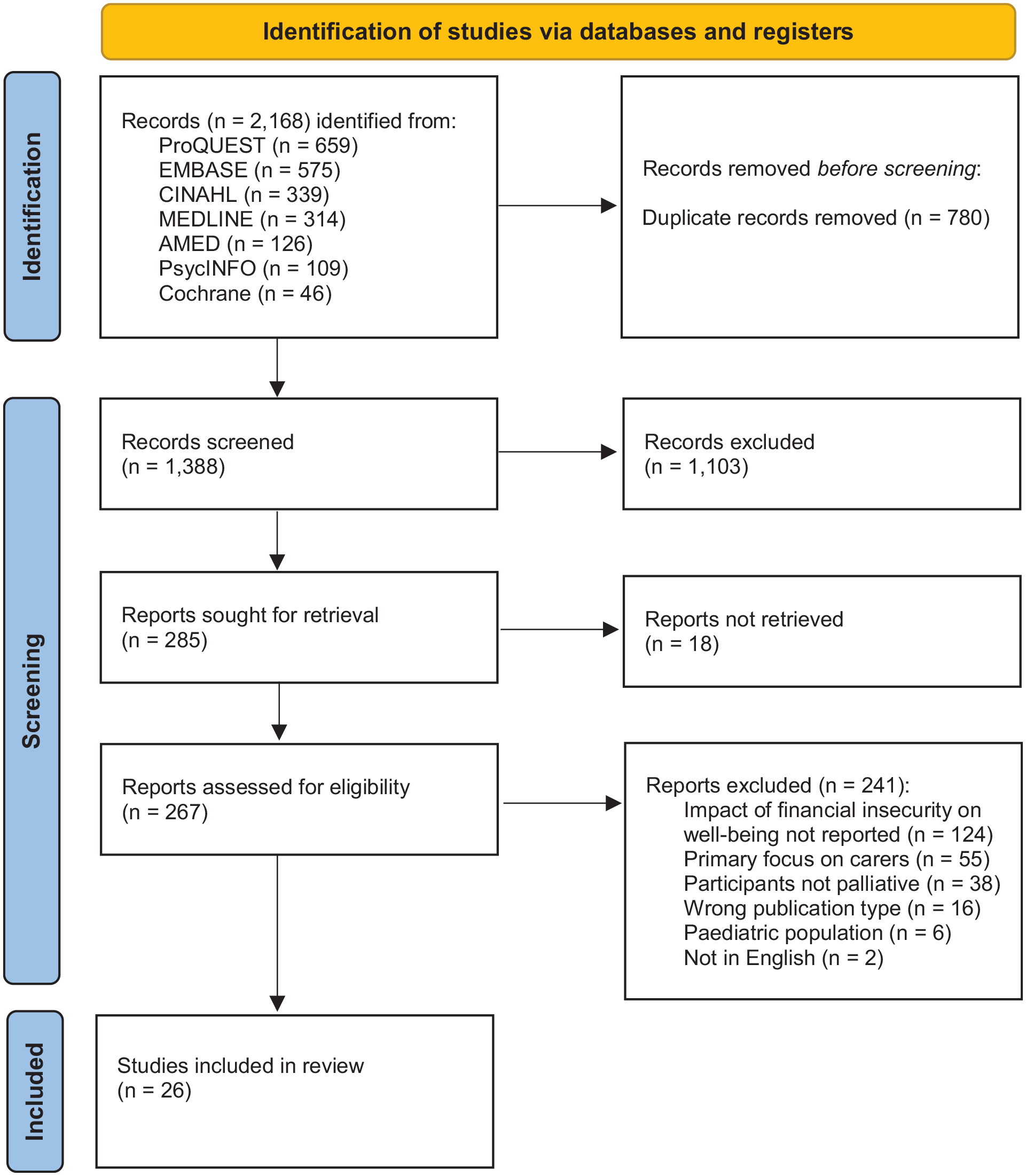

Of the 2168 studies identified in the search; 26 studies were included in the final review.40–64 See Figure 1 for details of the screening process.

PRISMA 2020 flow diagram here.

Study Characteristics

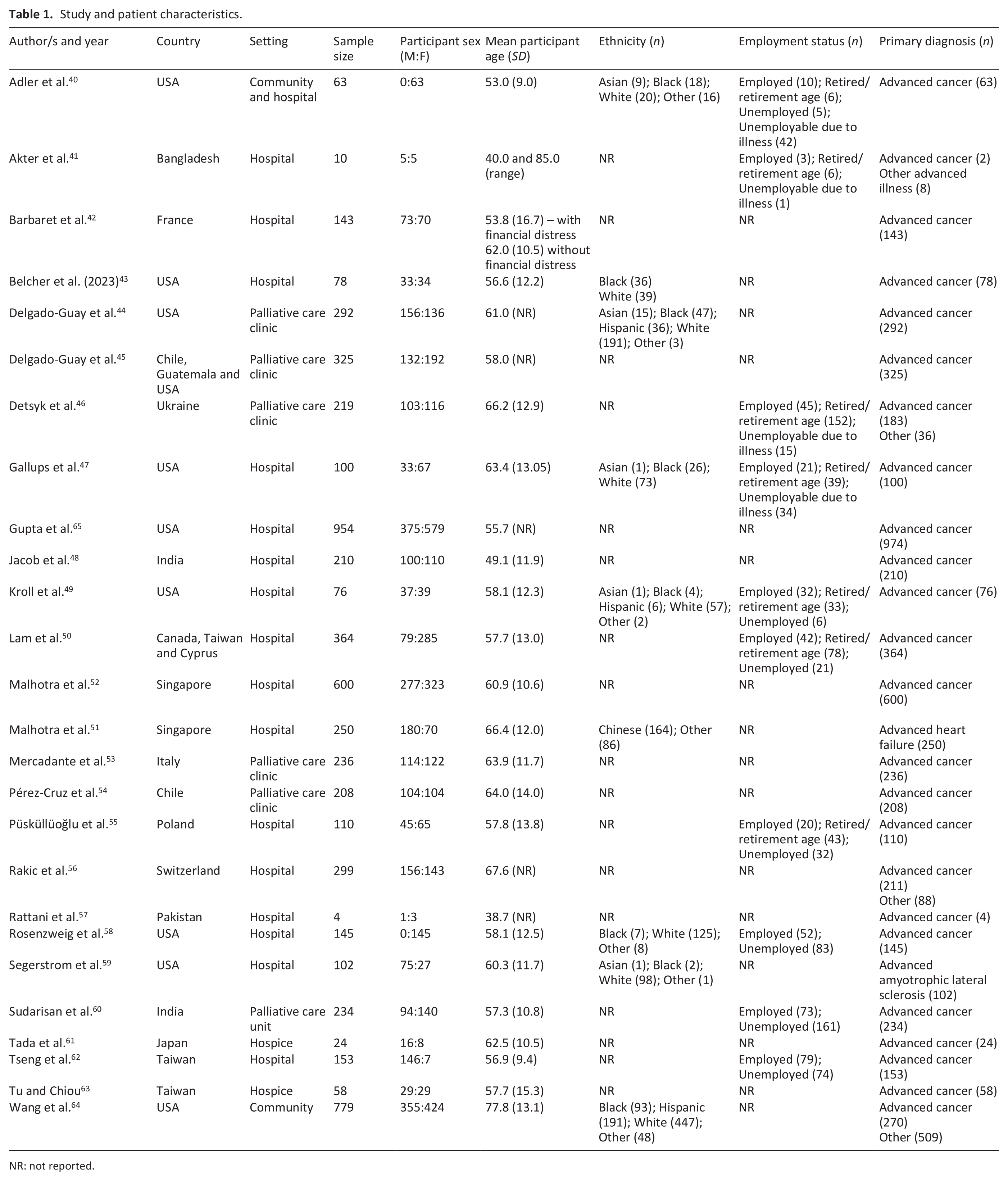

The characteristics of the 26 included studies can be found in Table 1. Whilst studies were conducted internationally, most studies were from the USA (n = 10).40,43–45,47,49,58,59,64,65 and were conducted either in a hospital or a palliative care setting (e.g. hospital ward or hospice). Twenty-one studies employed a quantitative study design,42–55,58–61,63–65 four studies employed a qualitative design,40,41,56,57 and one study employed both quantitative and qualitative methods. 62 All studies were cross-sectional or cohort in nature, apart from five studies which were longitudinal.44,46,59,64,65

Study and patient characteristics.

NR: not reported.

Patient characteristics

In total, 6024 individuals with terminal illness were included in the review. The majority (83.5%) of individuals had a primary diagnosis of advanced cancer. Approximately 55% of these individuals were female. The mean patient age, across the studies, ranged between 38.7 to 77.8. Ten studies reported participants’ employment status.40,41,46,47,49,50,55,58,60,62 Of the 1208 individuals with terminal illness, whose employment status was recorded, 377 (31.2%) were employed, 357 (29.6%) were retired or of retirement age and 474 (39.2%) were unemployed.

Quality appraisal

The results of the quality appraisal, using the Hawker tool, can be found in Supplemental Material 2. Seventeen studies40–42,44,46,49,50,52–57,59–62 scored between 18 and 30 and were, therefore, rated as being of fair quality. The other nine studies.43,45,47,48,51,58,63–66 scored between 31 and 36 and were, therefore, rated as being of good quality. No studies were rated as being of poor quality.

One area consistently low across all studies, was the ethics and bias domain; in which 21/26 (81%) studies scored as ‘Poor’. This was often due to very limited (if any) reflection on the relationship between the researcher and the participant.

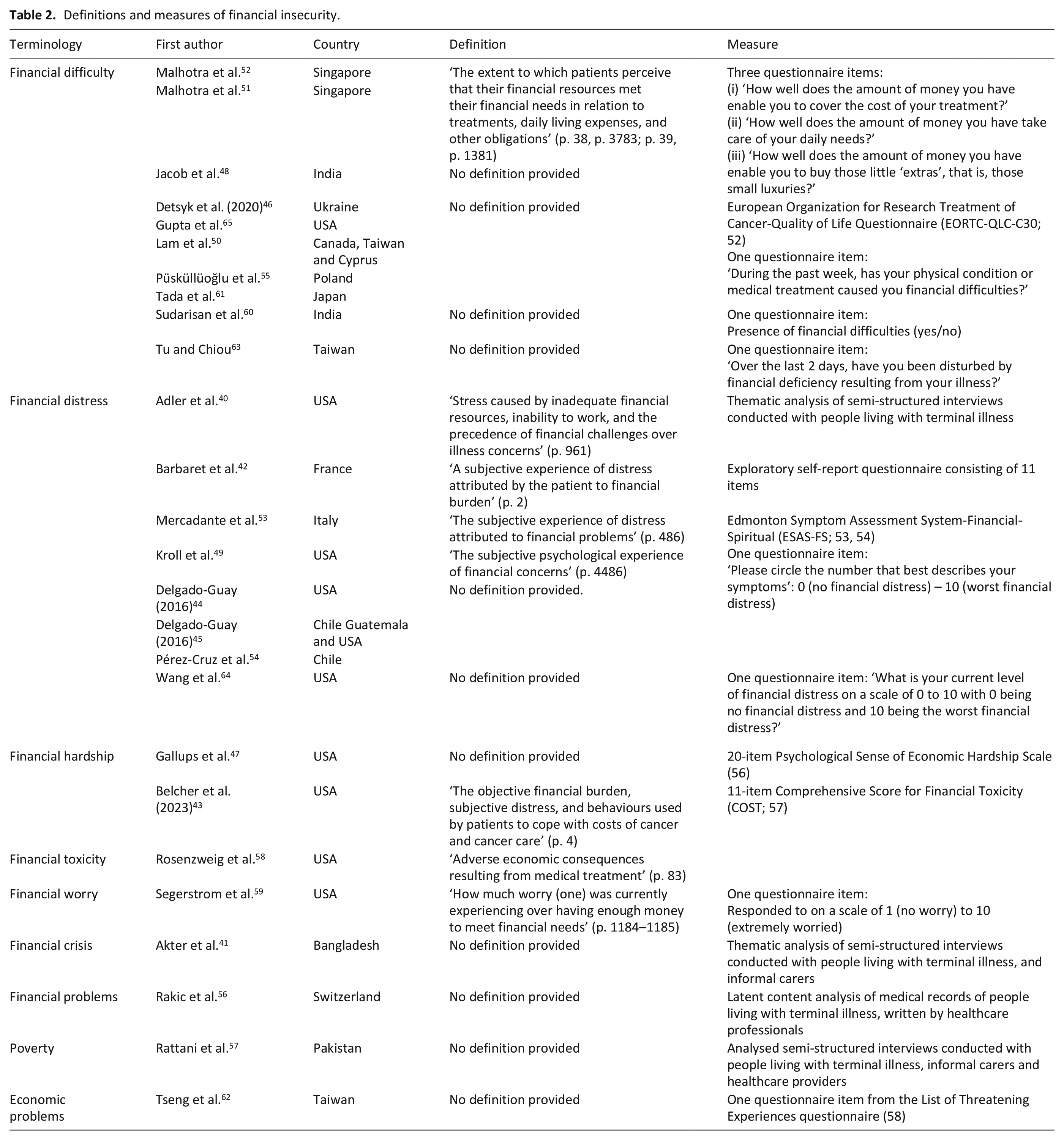

Defining and measuring financial insecurity

The terminology and measures used to describe financial insecurity can be seen in Table 2. Studies varied in their use of terminology including: ‘Financial difficulty’,46,48,50–52,55,60,61,63,65 ‘Financial distress’,40,42,44,45,49,53,54,64. ‘Financial hardship’,43,47 ‘Financial toxicity’, 58 ‘Financial worry’, 59 ‘Financial crisis’, 41 ‘Financial problems’, 56 ‘Poverty’ 57 and ‘Economic problems’. 62 Within studies, the definitions and measures used to define and assess financial insecurity varied.

Definitions and measures of financial insecurity.

There was little relationship between the geography of the study and the terminology used (see Table 2).

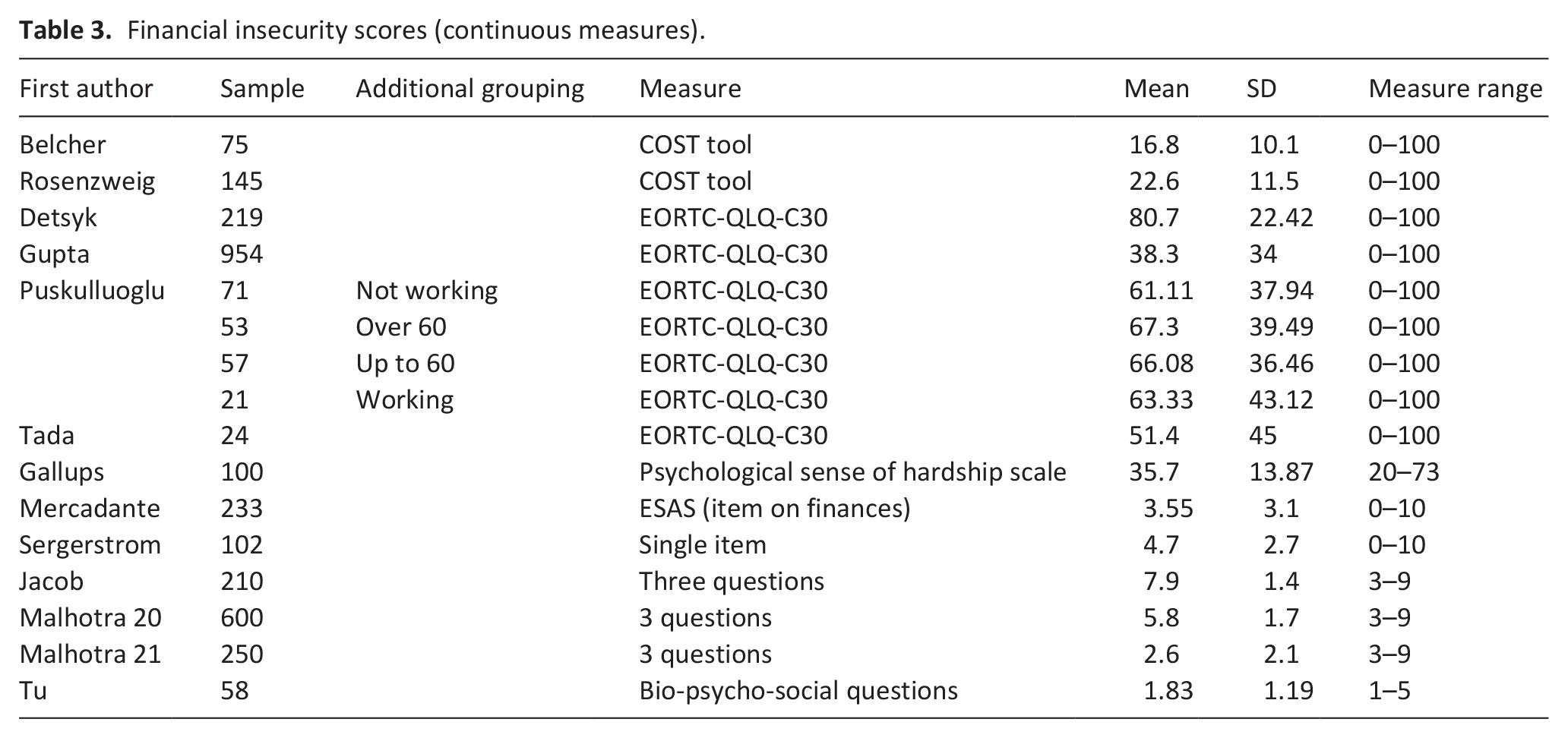

The reported level of financial insecurity

Thirteen studies collected data on financial insecurity through a continuous score.43,46–48,51–53,55,58,59,61,63,65 Table 3 shows the range of scores reported, the measures used for financial insecurity and the interpretation of the score. In all but two studies 39,54 a higher score indicated a higher level of financial insecurity. Four studies all measured financial insecurity using the EORTC-QLQ-C30 tool. 66 In this tool, the question about finances has a Likert scale (1 = ‘Not at all’ up to 4 = ‘Very much’) and the score is reported out of 100 with a higher score indicating a higher level of financial insecurity. The mean scores ranged from 38.3 (SD = 34) up to 80.7 (SD = 22.42).

Financial insecurity scores (continuous measures).

Püsküllüoğlu et al. 55 reported the financial scores by several characteristics, in addition to those reported in Table 3. This includes the financial impact on gender (Female = 59.49, SD = 39.74; Male = 77.04, SD = 32.43), on primary site (Breast, Prostate, Lung, GI tract, Unknown, Other) with financial scores ranging between 53.33 (SD = 50.55) for unknown primary up to 84.85 (SD = 22.92) for Other sites; on chemotherapy usage (No chemotherapy = 52.31, SD = 43.18; Chemotherapy = 75.62, SD = 31.02); surgery history (No surgery = 56.50, SD = 40.71; Surgery = 78.43, SD = 30.42); and on education level (Elementary = 82.54, SD = 29.10; High school = 58.62, SD = 41.09; University = 68.12, SD = 36.90).

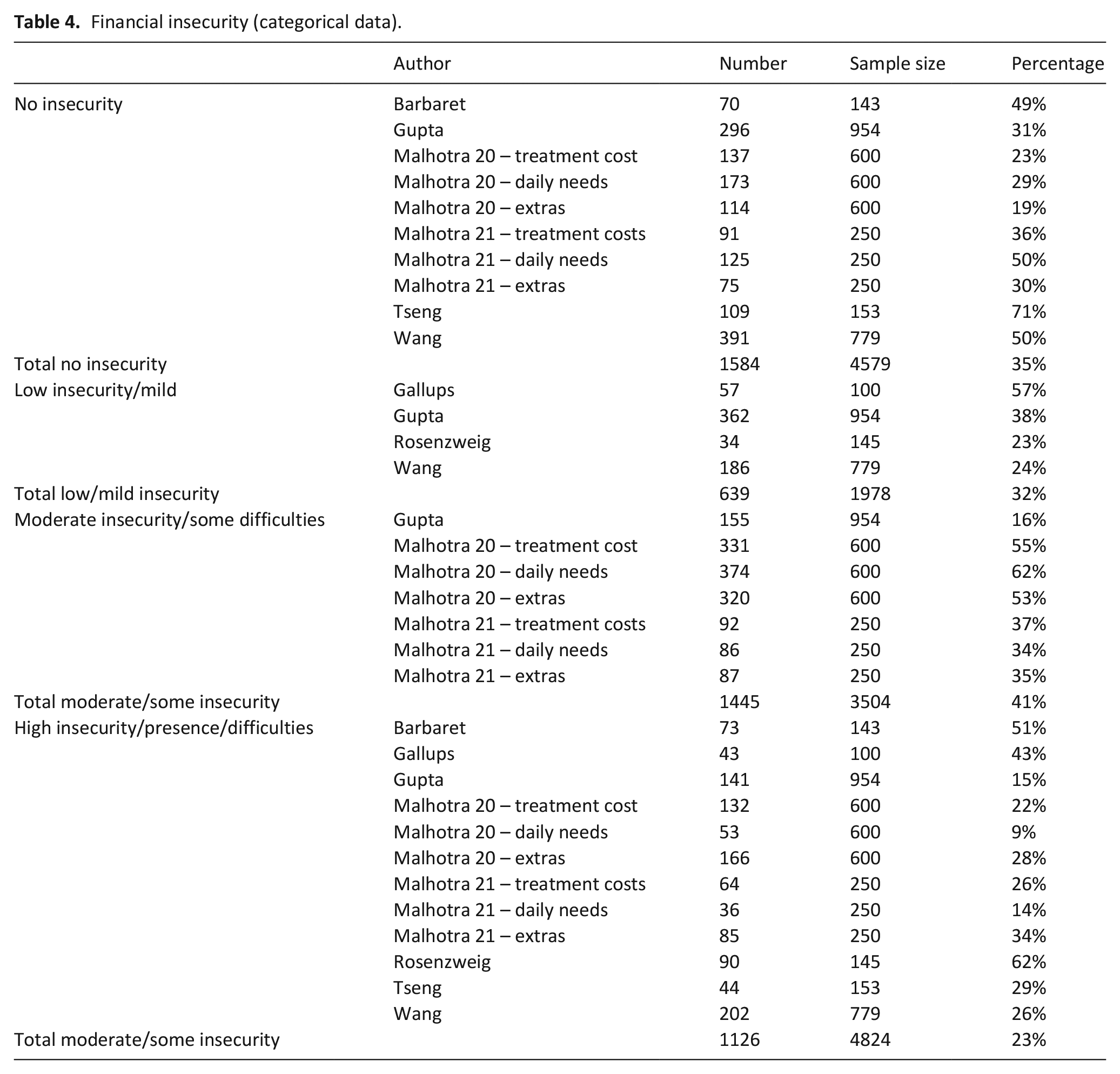

Eight studies42,47,51,52,58,62,64,65 reported financial insecurity in terms of categories (i.e. no insecurity, low or mild insecurity, moderate or some difficulties or high insecurity or difficulties). In two studies,51,52 participants were asked about their perceived financial difficulties regarding three domains: the cover of the cost of treatment, taking care of daily needs and buy little ‘extras’. They were asked to rate each one as either ‘very well’ (reported as No insecurity in Table 4), ‘fairly well’ (reported as Some difficulties in Table 4) or ‘poorly’ (reported as High/present difficulties on Table 3). The results of financial insecurity as categorical data are displayed in Table 4. Percentage estimates of high levels of financial insecurity ranged from 9% to 62%.

Financial insecurity (categorical data).

Six studies presented grouped data on ‘No financial insecurity’.42,51,52,62,64,65 Out of a total sample size of 4579, 35% (n = 1584) said they had no experience of financial insecurity. Four studies presented group data on ‘Low’ or ‘Mild’ financial insecurity.47,58,64–66 Out of a total sample size of 1978, 32% (n = 639) reported experiencing low or mild financial insecurity. Three studies presented a moderate group.51,52,65 Out of a total sample size of 3504, 41% (n = 1445) reported moderate some difficulties. Eight studies reported financial difficulties that were high or present.42,47,51,52,58,62,64,65 Out of a total sample size of 4824, there were 23% (n = 1126) who reported experiencing high levels of financial insecurity.

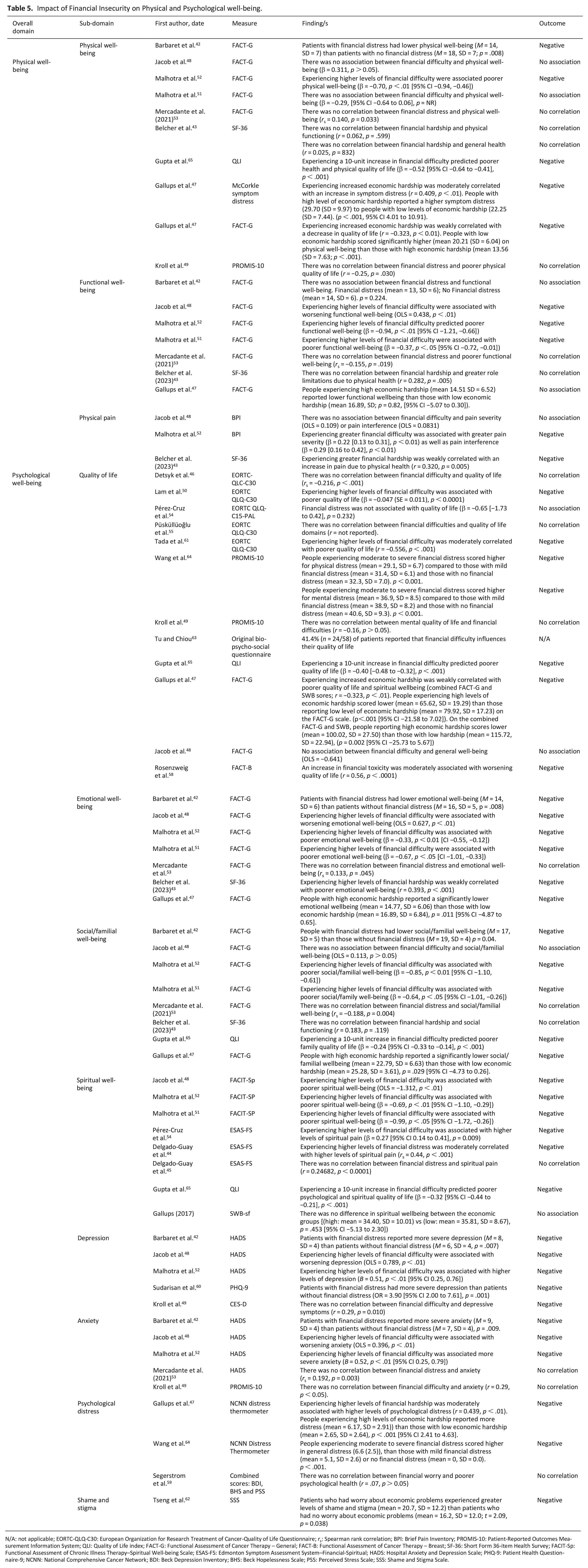

The impact of financial insecurity on physical well-being

Table 5 also presents the data reported on psychological well-being. Twenty-one studies42,44–54,58–65 reported 51 individual analyses across nine domains of psychological well-being. These domains were: quality of life, emotional well-being, social/familial well-being, spiritual well-being, depression, anxiety, psychological distress and shame and stigma.

Impact of Financial Insecurity on Physical and Psychological well-being.

N/A: not applicable; EORTC-QLQ-C30: European Organization for Research Treatment of Cancer-Quality of Life Questionnaire; rs: Spearman rank correlation; BPI: Brief Pain Inventory; PROMIS-10: Patient-Reported Outcomes Measurement Information System; QLI: Quality of Life index; FACT-G: Functional Assessment of Cancer Therapy – General; FACT-B: Functional Assessment of Cancer Therapy – Breast; SF-36: Short Form 36-item Health Survey; FACIT-Sp: Functional Assessment of Chronic Illness Therapy–Spiritual Well-being Scale; ESAS-FS: Edmonton Symptom Assessment System–Financial-Spiritual; HADS: Hospital Anxiety and Depression Scale; PHQ-9: Patient Health Questionnaire-9; NCNN: National Comprehensive Cancer Network; BDI: Beck Depression Inventory; BHS: Beck Hopelessness Scale; PSS: Perceived Stress Scale; SSS: Shame and Stigma Scale.

The impact of financial insecurity on psychological well-being

Table 5 also presents the data reported on psychological well-being. Twenty-one studies42,44–54,58–65 reported 51 individual analyses across nine domains of psychological well-being. These domains were: quality of life, emotional well-being, social/familial well-being, spiritual well-being, depression, anxiety, psychological distress and shame and stigma.

From the 51 analyses completed, 15 (29%) analyses indicated no association or correlation between financial insecurity and psychological well-being. A total of 35 analyses (69%) reported a negative result (in that financial insecurity was either correlated or predictive of a domain of psychological well-being). One study did not complete an analysis but reported prevalence data, that 41% of the participants felt that financial insecurity impacted their quality of life. 63

Of the three studies that adopted a longitudinal design, one reported on the relationship between financial insecurity and mental and physical well-being over time (1 month). Wang et al. 64 reported that participants who were experiencing financial distress had significantly (statistically and clinically) greater reductions in symptom burden (as measured on the Edmonton Symptom Assessment Scale (ESAS), mean score difference −4.39, 95% CI −7.91, −1.17, p < .01). This study was primarily investigating the effectiveness of a home-based palliative care team; to determine if a targeted intervention could reduce symptom burden with a group analysis on financial distress, rather than looking at the impact of financial insecurity over time.

Qualitative findings

Thematic analysis of the four international qualitative studies40,41,56,57 generated three themes relevant to the review aims: psychological distress, physical risk-taking and restricted access to treatment (see Supplemental Material 3).

Psychological Distress

Psychological distress manifested itself in feelings of stress, worry, frustration and helplessness. The stress induced by financial insecurity was described by one individual living with terminal illness: ‘Last year was the worst financial year ever. We were standing in food lines and going to food banks and having to get assistance with the utility bills. It was so stressful for me.’ (

40

, p. 961-962, Bangladesh)

Additionally, the worry attached to financial insecurity was described by Akter et al.,

41

who alluded to how people living with terminal illness worried about how the cost of their medical care may affect their family members: ‘The respondents mentioned that they felt exhausted worrying about their family members without income.’ (

41

, p. 6, Switzerland)

People living with terminal illness also expressed their frustration and discontent in relation to being financially dependent on others: ‘I would have to have my boyfriend pay for some of my meds, especially when I didn’t get a paycheck. I can’t even contribute! I hate depending on people’. (

40

, p. 962, Bangladesh)

Physical risk-taking

Due to financial insecurity, people living with terminal illness were forced to take risks which threatened their physical health. This phenomenon was described by one of the healthcare providers: ‘They [patients] do not have any means of transportation. They come in buses. They come in on top of cars’. (

57

, p. 7, Pakistan)

Restricted access to treatment

Financial insecurity restricted participants’ access to treatment. This was illustrated by one informal carer, who talking about her mother, described how: ‘She kept her illness a secret because she was unwilling to use any of the scarce family resources to seek medical attention’. (

57

, p. 7, Pakistan)

Discussion

Main findings of the study

There are three key findings to highlight from this review. Firstly, there is a lack of clarity and consistency on the terminology of what it means to be ‘financial insecure’ at the end of life. Secondly, approximately 23% of people who have a terminal illness report experiencing high levels of financial insecurity. Finally, an increase in financial insecurity was reported alongside a decrease in physical (48%) and psychological (69%) wellbeing.

What this study adds?

The finding that there was a very high degree of variation of terminology regarding financial insecurity is hugely important. The lack of an agreed definition or terminology for financial insecurity in a palliative care setting could make initiating conversations about the topic very difficult for healthcare professionals, further exacerbating inequities to support. 67 This is particularly important when reflecting upon findings by Marie Curie, that people who have a terminal illness are more likely to experience financial insecurity. 15

The Marie Curie report estimated that in the UK, every year, 90,000 people die in poverty. They also state that people who are living with terminal illness are at greater risk of experiencing poverty. 7 This review is the first to synthesise international data to suggest that 23% of people living with terminal illness, almost 1 in 4 people, experience high levels of financial insecurity. Whilst the precision of this figure is limited by methodological and reporting limitations across the included studies, it does help to provide a global barometer at which people who are living with terminal illness might be impacted by financial insecurity. Alongside the figures reporting the global prevalence of poverty (i.e. 1 in 10 people), and the recent data from Marie Curie, these findings indicate a clear need for frequent assessment and normalising conversations, using agreed terminology, about individual finances.

The majority of studies reported an increase in financial insecurity alongside a decrease in physical and/or psychological wellbeing. These findings complement previous evidence that suggests financial insecurity is associated with worse outcomes,4,5,13 particularly at the end of life.14,15

Strengths and Limitations

This systematic review included international evidence using both qualitative and quantitative data. A comprehensive search strategy was applied. Despite yielding no results, the grey literature search in addition to the manual forward and backward citation searching ensured no relevant papers were missed. The inclusion and integration of qualitative data, allowed for the nuances and complexities of financial insecurity to be understood in greater depth, how the different healthcare systems create or exacerbate financial difficulties. Due to time constraints and resources, studies not available in English were excluded from this review. This may have resulted in the exclusion of studies with relevant data. Most of the included studies employed a cross-sectional design. Not only does this result in there being less scope to assess the impact of financial insecurity on well-being over time, but it also raises an issue with causation. It has been well evidenced that people from lower socioeconomic groups are at greater risk of poor healthcare outcomes (e.g. higher mortality rates). 68 One cannot rule out the opposite direction of causality in which poorer well-being caused an individual with terminal illness to have higher financial insecurity. Financial insecurity was primarily measured, in the quantitative studies, using single self-report items derived from pre-existing questionnaires. It is unlikely that one questionnaire item will be able to accurately capture one’s level of financial insecurity, including fluctuations over time, given the multi-faceted nature of the experience.28,29

Implications for practice, policy and future research

The prevalence of financial insecurity and lack of an agreed definition or terminology for financial insecurity is a major issue for future practice, policy and research. The topics of death and dying and finances are two taboo topics that can be very difficult to discuss openly. If almost 1 in 4 people are experiencing financial insecurity, it is vital that healthcare professionals across the globe receive clear guidance and support when raising potentially both taboos in the same conversation. Agreed terms can help healthcare professionals to communicate effectively and clearly to identify the needs and necessary support for the individual. Reports such as ‘Money matters at the end of life’ from the Dying in the Margins project are extremely helpful to develop the building blocks to such conversations. 69

With clear terminology and definitions, research will be more readily able to make comparisons across studies to investigate the mechanisms which underlie the relationship between financial insecurity and well-being. A better understanding of the impact of financial insecurity on physical and psychological well-being in people who are living with a terminal illness, could enable clinical teams to predict negative consequences more accurately and target interventions more effectively.

This review highlights important global considerations when it comes to wealth and equity in healthcare provision.

In the UK, the National Health Service (NHS) provides health care, free of charge at the point of access. This means that people living with terminal illness are not required to cover the full cost of their care. Interestingly in this review, no studies from the UK were included. Studies were predominately from the USA, where people who are living with terminal illness but do not have appropriate health insurance may be required to pay for all or some of the medical care they receive. 16 In this review, three of the four qualitative studies were conducted in countries where access to medical care relies on out-of-pocket payment (i.e. USA, Bangladesh and Pakistan). These countries are not similar in terms of wealth. Inevitably because of this wealth difference, the financial support at the end of life will vary across countries. In the UK, changes to the Social Security (Special Rules for End of Life) Bill have enabled individuals in the last 12 months of their lives to apply for additional financial support.14,70 In the USA, hospice access through Medicaid or Medicare (the largest USA healthcare insurance providers) is available for individuals who have a predicted survival of 6 months or less. 71

Pickett and Wilkinson 72 bring forward an important discussion about inequity and healthcare access from an international perspective. They argue that it is in unequal societies, not poor societies, where more health and social care problems exist. They note that life expectancy, for example, is lower in unequal societies. In this review, financial insecurity was experienced across countries with different economic structures and resources: suggesting that there is more to this complex phenomenon than global wealth, but rather availability and equitable access to support.

Conclusion

Financial insecurity is associated with reduced physical and psychological well-being among people living with terminal illness. That said, it continues to be poorly defined and inconsistently measured. Future research should seek to provide a uniform definition to aid healthcare professionals in initiating potentially challenging conversations about death and finances. Policy makers should ensure that people living with terminal illness have the support they need to address their financial situation, including signposting to available support. This support would mean that they are not left to suffer from the ill-effects of financial insecurity, as well as their illness.

Supplemental Material

sj-pdf-1-pmj-10.1177_02692163241257583 – Supplemental material for A systematic review on the impact of financial insecurity on the physical and psychological well-being for people living with terminal illness

Supplemental material, sj-pdf-1-pmj-10.1177_02692163241257583 for A systematic review on the impact of financial insecurity on the physical and psychological well-being for people living with terminal illness by Ross Walker-Pow, Andrea Bruun, Nuriye Kupeli, Alessandro Bosco and Nicola White in Palliative Medicine

Supplemental Material

sj-pdf-2-pmj-10.1177_02692163241257583 – Supplemental material for A systematic review on the impact of financial insecurity on the physical and psychological well-being for people living with terminal illness

Supplemental material, sj-pdf-2-pmj-10.1177_02692163241257583 for A systematic review on the impact of financial insecurity on the physical and psychological well-being for people living with terminal illness by Ross Walker-Pow, Andrea Bruun, Nuriye Kupeli, Alessandro Bosco and Nicola White in Palliative Medicine

Supplemental Material

sj-pdf-3-pmj-10.1177_02692163241257583 – Supplemental material for A systematic review on the impact of financial insecurity on the physical and psychological well-being for people living with terminal illness

Supplemental material, sj-pdf-3-pmj-10.1177_02692163241257583 for A systematic review on the impact of financial insecurity on the physical and psychological well-being for people living with terminal illness by Ross Walker-Pow, Andrea Bruun, Nuriye Kupeli, Alessandro Bosco and Nicola White in Palliative Medicine

Footnotes

Acknowledgements

We would like to acknowledge Veronica Parisi (Librarian at UCL) for their support to develop robust search terms. We would like to also acknowledge Dr Victoria Vickerstaff for her input during the analysis of the quantitative data.

Author contributions

NW and NK: concept, review procedures, analysis, interpretation and write up. RWP and ABr: protocol development, review procedures, analysis, interpretation and write up. ABo: analysis, interpretation and write up. All authors approved the final draft.

Data management and sharing

All available data is reported in the manuscript and Supplemental Material.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Marie Curie Core funding (MCCC-FPO-16-U) and Marie Curie Research Grant Scheme 2022 (MCRGS-EOI-56); NK was supported by an Alzheimer’s Society Junior Fellowship, Grant/Award Number: 399 AS-JF-17b-016.

Research ethics and patient consent

Ethical approval and patient consent were not required since the review only involved secondary analysis of published data.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.