Abstract

UK community finance institutions play an important role in deprived neighbourhoods by serving households and businesses unable to access mainstream finance. This paper analyses the short-term effects of the Coronavirus pandemic on the activities and sustainability of the community finance sector by analysing longitudinal survey data for 40 providers and follow-up interviews with 25 organisations. COVID-19 resulted in an acceleration of the shift to online service delivery and temporary and permanent branch closures among community finance institutions. Further, the demand for, and volume and value of lending fell significantly during the first lockdown only recovering by the end of the summer 2020. This resulted in lower income, greater costs and lower regulatory ratios. Smaller providers in a weak financial position with more financially vulnerable customers were worst affected by the pandemic. We argue the pandemic may reduce access to finance for the financially excluded through the intensification of the shift to online services and by increasing the risk of providers serving the poorest folding or being merged with larger providers.

Introduction

The impact of COVID-19 on the UK community finance sector, comprising credit unions and Community Development Finance Institutions (CDFIs), is an important issue for local economic policymakers. This is because these institutions fill an important gap in the market not served by mainstream financial institutions. In the wake of the debt crisis of the early 1990s, the UK financial sector moved credit away from poorer to richer segments of society as form of risk avoidance (Leyshon and Thrift, 1995). The most obvious manifestation of this withdrawal has been the closure of branches. Between 1995 and 2003, UK banks and building societies closed 20% of their branches, disproportionally in more deprived areas (Leyshon et al., 2008). From 2012 to 2018, the number of branches in the UK fell by a further 17% (Bennett, 2020) and to a greater degree in more deprived local authority areas (Nieboer, 2019).

Branch closures may lead to increased costs and inconvenience for households and businesses in accessing cash and transaction services (Leyshon et al., 2008), especially for older customers who experience greater difficulty in using online banking and for small businesses that rely on branches as the main way of banking (Bennett, 2020). There are also concerns that branch closures may send local economies into a downward spiral of decline linked to the loss of employment and consumers starting to shop in other areas with greater banking facilities (Leyshon et al., 2008).

It is also well evidenced that low-income, socially excluded communities are less likely to have access to mainstream credit and financial services (Worton et al., 2018; Financial Conduct Authority, 2019). These consumers instead often resort to commercial high-cost credit (payday loans, home credit and rent-to-own) for which they pay higher interest rates and are at greater risk of customer detriment (Financial Conduct Authority, 2017). Henry et al. (2017) find that levels of lending by the seven largest UK banks are lower in deprived communities, but that the association is weak. They note that the current geographical data on bank lending and activity is insufficient to allow for a robust analysis.

Conversely, credit unions and CDFIs are predominantly community-based institutions that serve relatively small geographical markets (Coen et al., 2019; Dayson et al., 2020). They often have a physical presence in those communities and enable customers to access services through their head office or a branch. They provide a range of services, including loans, budgeting support, savings and banking and transaction services, to excluded and underserved communities. CDFIs were explicitly set up to serve groups unable to access mainstream finance, whilst credit unions often serve communities not well served by mainstream financial institutions, such as rural areas (Coen et al., 2019) as well as financially excluded groups (Jones, 2006). In Canada, for example, credit union’ branches are over-represented in rural and middle-income areas (Maiorano et al., 2017).

There is also research that suggests the presence of credit unions has positive effects on markets by reducing rates on loans and increasing savings interest rate through increased competitive pressures on banks (see Coen et al., 2019). Coen et al. (2019: 209) argue that: ‘Despite playing a smaller role than traditional banking institutions in providing credit and deposit services, U.K. credit unions remain firmly on the radar of prudential supervisors given the important role they play in supporting local economies’. Indeed, Fuller and Jonas (2002: 88) argue that from the late 1990s, the government pursued an explicit policy ‘to encourage these alternative financial institutions to develop alongside the mainstream economy’.

The Coronavirus pandemic caused unprecedented disruption to economic activity in the UK and globally (International Monetary Fund, 2021). To stop or limit the spread of COVID-19, national governments introduced travel restrictions, mandated the closure of non-essential customer-facing businesses, and restricted the movement of households. This led to significant falls in economic output, especially in the retail, travel and leisure industries. In the UK, the ‘magnitude of the recession caused by the pandemic is unprecedented in modern times’ (Harari and Keep, 2021: 6).

Community finance institutions have a potentially critical role in rebuilding deprived communities after the pandemic, but because of their small size and their propensity to serve vulnerable customers, they may also be vulnerable to the economic effects of the virus. To date, there is very little empirical research on how the UK community finance sector has been affected by the pandemic. There have been no peer reviewed outputs on the topic, but some consultancy and research reports. Jones et al. (2020) conducted a survey of 24 credit unions in April 2020 to find out how they had responded to the pandemic. Dabrowska et al. (2020) surveyed the impact on the European microfinance sector, which primarily lend to businesses. There has also been more anecdotal evidence provided in blogs and articles (e.g. McCarthy, Undated).

In this article, we address this dearth in the knowledge by analysing the short-term effects of COVID-19 on the credit union and personal lending CDFI sector drawing on a longitudinal online survey of 40 UK credit unions and CDFIs, and semi-structured interviews with 25 survey respondents. The research was conducted in May and November 2020. Although the sample is small, it covers between 40% and 50% of the lending by the sector. The survey explores the effects of the pandemic on loan demand, lending and income of the sector from April to October 2020. It provides a unique insight into the impact on the sector, as other datasets only contain balance sheet and income statement data (e.g. Bank of England annual and quarterly credit union returns). As such, the paper makes an important contribution to understanding how the community finance sector has been affected by COVID-19.

We find that the demand for, and volume and value of lending by affordable credit providers fell significantly during the first lockdown, only recovering by the end of the summer of 2020. This, in turn, negatively affected the finances of most providers, including through lower income, greater costs and lower regulatory ratios. Smaller providers in a weak financial position pre-pandemic with more financially vulnerable customers were worst affected by the pandemic. The pandemic led providers to change their operating and delivery models, including a shift towards greater online delivery, branch closures and mergers. We argue that the effects of the pandemic may reduce the access to financial services among the most vulnerable, financially excluded communities by intensifying the move to online-only service provision and by increasing the likelihood of small organisations serving the most vulnerable failing.

Since we collected the data, the pandemic has eased, the government restrictions have been lifted and academic research has shed light on long-term societal and economic effects of COVID-19 (Blundell et al., 2022). Yet, understanding the short-term effects of the pandemic on community lenders is important for two reasons. Firstly, the short-term effects documented in this paper have long-term implications for community lenders and the communities they serve. The significant decline in the value of loans disbursed affects future interest income and financial viability of the sector. Some of the changes in practice (shift to online service provision, closure of some branches) resulting from the pandemic were permanent and irreversible. Secondly, evidence on the short-term effects of COVID-19 on the behaviour and resilience of community lenders may inform policies to support the sector and the communities they serve in any future pandemics or other events necessitating the imposition of lockdowns or government restrictions.

The remainder of the article is structured as follows. The second section describes the UK community finance sector. The third section discusses the literature on the impact of COVID-19 on the UK economy and the community finance sector. The fourth presents the methods and data, whilst the fifth details the results of the analysis. The final section concludes.

The UK community finance sector

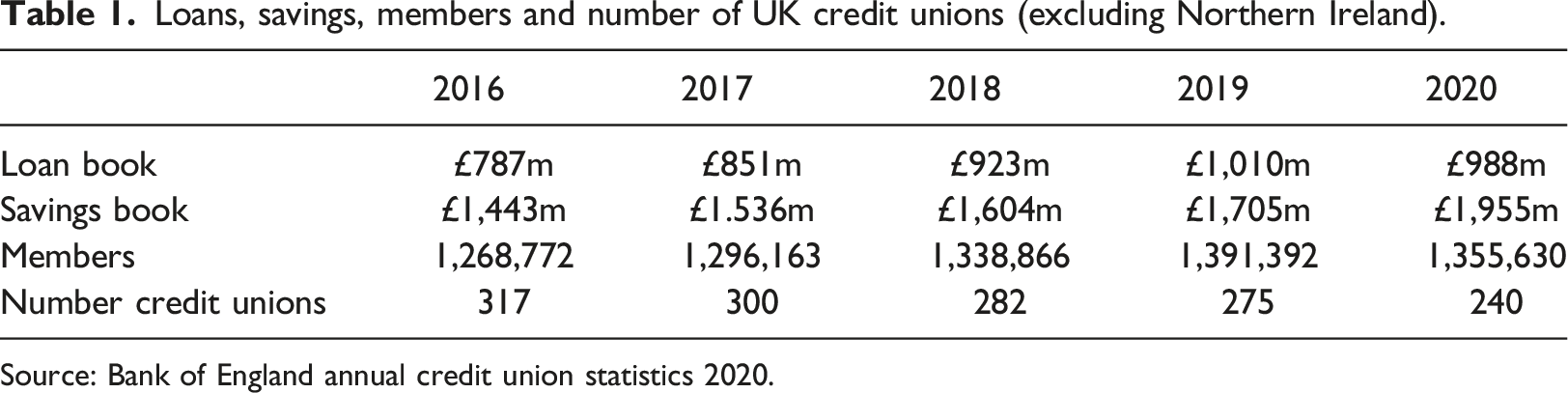

Loans, savings, members and number of UK credit unions (excluding Northern Ireland).

Source: Bank of England annual credit union statistics 2020.

There are around 240 credit unions in the UK. They have an outstanding loan book of around £1bn, a savings book of nearly £2bn and 1.35m members. Apart from the Scottish credit union sector, which has among the highest credit union penetration rates in Europe, the UK credit union sector reaches a small proportion of the population in international comparisons (Tischer et al., 2015). Most credit unions mainly or, in many cases, only provide loans and savings products, partly due to regulation. Less than 5% are allowed to provide residential real estate lending (Coen et al., 2019). Credit unions have historically placed particular emphasis on savings and the building of assets as a means to improve the financial circumstances of individuals in the long run (Jones, 2008). Many, 56% according to Lee and Brierley (2017), still require members to save for a period before getting a loan. Several credit unions also provide financial education and budgeting support to their members.

Although diverse in terms of size, products and customer groups, there are broadly two types of credit unions. Employer-based credit unions, which include some of the largest credit unions in the UK, serve employees and retired employees of private and public sector organisations. Community credit unions serve members living or working in a geographical area. They are often smaller than employer-based credit unions and include the smaller, volunteer-driven organisations, and many of them were set up by community activists, charities and local authorities in the 1980s and 90s to address social and financial exclusion (Jones, 2008).

Overall, UK credit union customers are more likely to be socially and financially excluded than the population as a whole (McKillop et al., 2007; Collard and Smith, 2006; Coen et al., 2019). They tend to have lower incomes and are less likely to be banked (Collard and Smith, 2006; McKillop et al., 2007). This is especially the case for England and Wales, but less so for Scotland (McKillop et al., 2007; Martin, 2018). However, credit unions have a diverse membership, including middle class, less excluded people. Analysis of the Scottish Household Survey commissioned by the Carnegie UK Trust (Martin, 2018), showed that the profile of credit union account holders broadly matched the overall population in terms of household income, home ownership rates and employment status.

The CDFI sector consists mostly of not-for-profit, non-deposit taking institutions, which take numerous institutional and legal forms. The earliest business lending CDFIs emerged in the 1970s, though most were founded in the 1980s and 90s (Appleyard, 2011). The first personal lending CDFIs emerged in the early 2000s (Dayson et al., 2020). In last few years, several profit-with-a-purpose providers have emerged (e.g. Salad Money, Auden). Most organisations are members of the trade body Responsible Finance and provide consumer, housing and business loans and ancillary services (advice, budgeting support and business development support) for individuals, businesses and social enterprises unable to access mainstream finance.

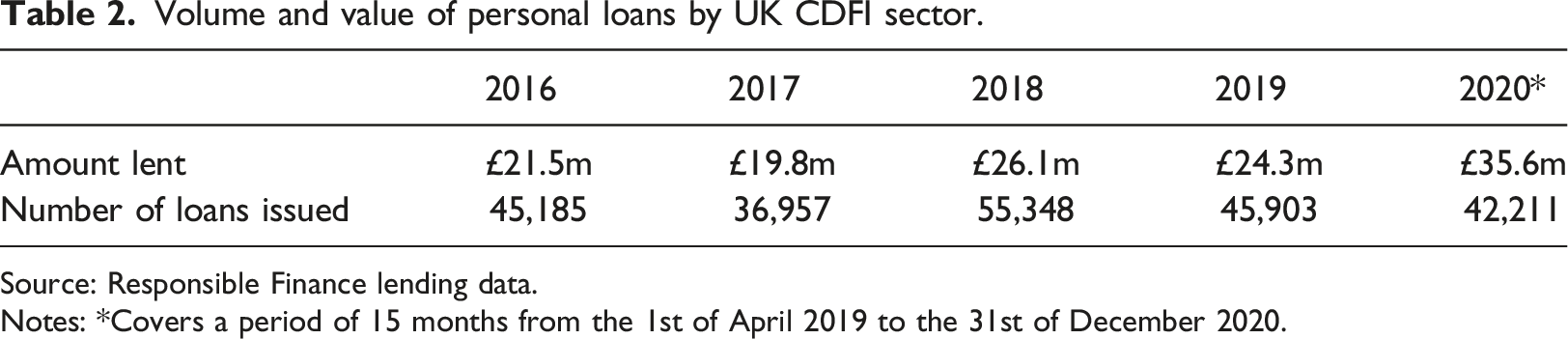

Volume and value of personal loans by UK CDFI sector.

Source: Responsible Finance lending data.

Notes: *Covers a period of 15 months from the 1st of April 2019 to the 31st of December 2020.

Unlike credit unions, who serve a broader market, CDFIs target almost exclusively low-income, financially excluded customers. Nearly three quarters of CDFI customers are on low incomes, 60% are in social housing and over 70% are in receipt of welfare benefits (Responsible Finance, 2021). The sector provides small, short-term consumer loans of an average of around £650 typically repayable over 52 weeks or less (Responsible Finance, 2021). Several CDFIs also offer budgeting support and the flexibility in repayment often needed by low-income consumers. Some provide access to linked savings accounts in partnerships with banks or credit unions. The sector aims to contribute to improved financial resilience and wellbeing by reducing customer reliance on commercial high-cost credit and hence the cost of interest rate payments, and by providing budgeting support and linked savings (Dayson et al., 2020).

The impact of COVID-19 on the community finance sector

The Coronavirus pandemic had significant disruptive effects on the UK economy. In response to the spread of the virus, the government imposed numerous lockdowns, which restricted people’s movements and forced non-essential businesses to close. These lockdowns, especially the first lockdown in the spring of 2020, led to sharp falls in consumer spending hitting the hospitality, transport and recreation sectors in particular (Harari and Keep, 2021). The pandemic triggered the steepest fall in economic output – of 9.7% in 2020 – in the UK since consistent records began in 1948 (Harari and Keep, 2021).

The short-term effects on household finances were mixed. Overall, average household income remained broadly unchanged, savings increased and consumer debt declined (Collard et al., 2021; Harari and Keep, 2021). UK households were in a stronger financial position at the start of the pandemic compared with the financial crisis of 2007 (Franklin et al., 2021). The government also introduced various support programmes, which cushioned the effects of the pandemic on households. This included support for employers to retain and pay workers whilst their businesses were closed (the furlough scheme), financial support for the self-employed, a temporary £20 per week uplift in welfare benefits and additional funding for local government hardship funds. There were also restrictions on creditor actions and payment deferrals across mortgages and consumer credit products.

However, 32% of households had a member experiencing job loss or lower pay due to COVID-19 (Collard et al., 2021). People in precarious forms of employment (nonfixed hours, 0 h contracts), in the sectors hardest hit by the pandemic (leisure, hospitality, retail and service sector), and in self-employment were worst affected (Collard et al., 2021). Low-income and socially excluded households were disproportionally affected because they came into the crisis with higher levels of unsecured debt, less savings and lower or unchanged real income (Bank of England, 2020; Collard et al., 2021; Franklin et al., 2021).

The UK financial sector was less affected by the pandemic than other industries (Harari and Keep, 2021). COVID-19 did not trigger large loan losses or forced banks to reduce the supply of credit as happened during the 2007 global financial crisis. Banks continued to provide finance and forbearance to households (Franklin et al., 2021). This is because UK households entered the pandemic in a better financial shape, interest rates were lower and banks were better capitalised than in 2007 (Franklin et al., 2021).

There is limited evidence about the effects of the pandemic on the UK credit union and personal lending CDFI sector. As far as we are aware, there are no peer reviewed outputs that examine the impact of COVID-19 on UK credit unions or the CDFI sector. National statistics and research reports and articles in the grey literature suggest three potential effects of the pandemic.

Firstly, the available data indicates that credit union lending fell, whilst savings increased. Unsecured lending, the main source of income for the sector fell significantly in March to May 2020, November 2020 and January 2021 (Bank of England, 2022). The value of the outstanding loan portfolio of the UK credit union sector fell by £1.58bn or 3.6% in 2020 compared with 2019, though for England it increased by 2.4% (Bank of England, 2021). Conversely, members’ share balances, the main liability of credit unions, increased by £313m or around 11% from 2019 to 2020 (Bank of England, 2021).

Secondly, according to a survey of 24 credit unions in Great Britain, credit unions changed some of their practices in response to COVID-19 (Jones et al., 2020). Several credit unions closed or reduced the opening hours of branches. Some or all staff started working from home, and several credit unions furloughed employees who could not perform their tasks from home. Several introduced or made greater use of remote delivery, such as cashless payments, remote underwriting, online application forms and electronic signature facility. Some had to invest time and resources to encourage and support members to use online or remote services. There was also greater use of technology for collaborative working, including cloud-based telephony and business communication platforms. It should be noted that the survey by Jones et al. (2020) was conducted at the beginning of pandemic – March and April 2020 – and only captured the immediate operational changes caused by COVID-19.

Thirdly, there is evidence to suggest that several credit unions provided additional support to members during the pandemic. Credit unions in Great Britain provided members with emergency loans and enhanced access to their savings, as well as additional forbearance to borrowers (Jones et al., 2020). Beyond this, credit unions proactively communicated with vulnerable members, referred members to mental health services and foodbanks, and provided food and utility vouchers to vulnerable customers (Jones et al., 2020). Several credit unions also reported making donations to local community groups and charities (Jones et al., 2020). Similar examples have been highlighted for the credit union sector in Ireland (McCarthy, 2021). CDFIs too provided additional support for customers, including contacting vulnerable customers, signposting to hardship support, and offering payment holidays to borrowers struggling to repay (Responsible Finance, 2021).

More broadly, there is evidence to suggest that credit unions are better positioned to weather economic downturns and financial crises (Hoyt and Menzani, 2012; Coen et al., 2019; Birchall and Ketilson, 2009). Indeed, many credit unions and sectors emerged or were set up during times of crises (Birchall and Ketilson, 2009). Several studies suggest that they have greater longevity and survival rates, including for start-ups, than other business models (Birchall and Ketilson, 2009; McKillop et al., 2020). It should be noted that there is limited research on credit union failures in the UK, partly because failures are less common outside of the US (Coen et al., 2019). In the UK, struggling credit unions tend to be transferred to other, financially healthier credit unions rather than allowing them to fail (Coen et al., 2019).

There is evidence that there is greater stability and less fluctuation in credit union lending, especially compared with shareholder businesses. In their analysis of US credit union and bank lending and delinquency for 1986–2009, Smith and Woodbury (2010) found that credit union loan portfolios were 25% less susceptible to business cycle fluctuations. The peaks were lower and troughs higher in credit union lending relative to banks. They also found that the lending was not correlated with the national unemployment cycle. Conversely, a study of the determinants of credit union failures in the UK concluded that the national unemployment rate had material effects on the failure rates (Coen et al., 2019).

Credit unions are not only less likely to experience steep declines in lending during crises, but there is also evidence from the US suggesting that credit unions provide additional liquidity when banks are reducing credit supply. Lu and Swisher (2020) found that US credit union lending grew at a faster rate than bank lending during and following the global financial crisis of 2007. A study by Walker (2016), which examined bank and credit union business lending for 2010–14, concluded that credit unions increased their share of business lending following the financial and economic crisis of 2007. Business loans from credit unions increased by 39.2%, while assets increased by 22.7%. Community banks reduced their business lending by 5.6% for the same period (Walker, 2016). Moreover, where their competitors were larger, credit unions supplied more credit to business (Walker, 2016). There is also evidence to suggest that credit union savings increase during downturns suggesting they are seen as safe havens (Rauterkus et al., 2018; cf. McKillop et al., 2020).

The main explanation of the resilience of the credit union model is that they are more risk averse in terms of lending and expansion when compared with other types of financial service providers. There are fewer incentives to take risks in cooperatives because of the lack of profit and share options for management (McKillop et al., 2020; Smith and Woodbury, 2010). The link between savings and lending also acts as a constraining influence on credit unions (Birchall and Ketilson, 2009). Unlike banks, credit unions rely on members’ savings rather than capital markets for lending, which lead to focus on retained profits and taking fewer risks (Birchall and Ketilson, 2009). It is also suggested that the credit union model reduces credit risk as the focus on geographically concentrated markets and common identity among members reduces moral hazard and information asymmetries (McKillop et al., 2020). However, the inability to access capital markets and the less diversified nature of credit unions reduces their ability to absorb balance sheet shocks (Fonteyne, 2007).

Larger, better capitalised credit unions with higher levels of earnings are less likely to fail compared with smaller, less well capitalised institutions with lower earnings (Coen et al., 2019). Further, credit unions that serve more vulnerable, financially excluded customers appear more vulnerable to economic fluctuations. Lending to such groups involves making smaller, unsecured loans and greater credit risk (Dayson et al., 2020). Coen et al. (2019) find that a higher proportion of unsecured loans and arrears is positively associated with failures. There is an older study by McKillop et al. (2007) which compared credit union performance in areas of differing levels of financial exclusion in the UK. In England and Wales, credit unions in areas of higher levels of financial exclusion had faster membership growth but lower assets, return, efficiency and reserves compared with credit unions in more affluent areas (McKillop et al., 2007). McKillop et al. (2007: 37) argue that ‘the performance of credit unions may be adversely affected if they are overly focused on areas of high financial exclusion’.

More generally, several authors argue it is difficult if not impossible for community lenders to serve financially excluded communities and, at the same time, be financially sustainable (Fuller and Jonas, 2002; Sinclair, 2014). However, Jones (2008) and others argue that it is possible to serve financially excluded consumers and be financially sustainable by shifting to the so-called new model credit unions. This involves building wide membership (including low-income and middle class), putting particular emphasis on savings and widening the service offering (Jones, 2008).

Based on a review of the literature, we conclude that there is very little research on how CDFIs are affected by crises and shocks, and even less on the CDFIs that engage in personal and consumer lending. CDFIs share some similar characteristics with credit unions. They are not-for-profit providers (that do not provide bonuses or shareholder interests) and they mostly focus on small geographical areas, though some are nominally national (Dayson et al., 2020). Most CDFIs borrow from mainstream financial institutions or social lenders to on-lend (Dayson et al., 2020), but they do not have access to international capital markets. It is possible that this may make them less prone to uneven growth linked to business cycle fluctuations than shareholder-owned firms relying extensively on capital market. During and following the 2007 financial crisis, the UK personal lending CDFI sector grew its lending (see Dayson et al., 2020).

Methods

Sample overview by wave.

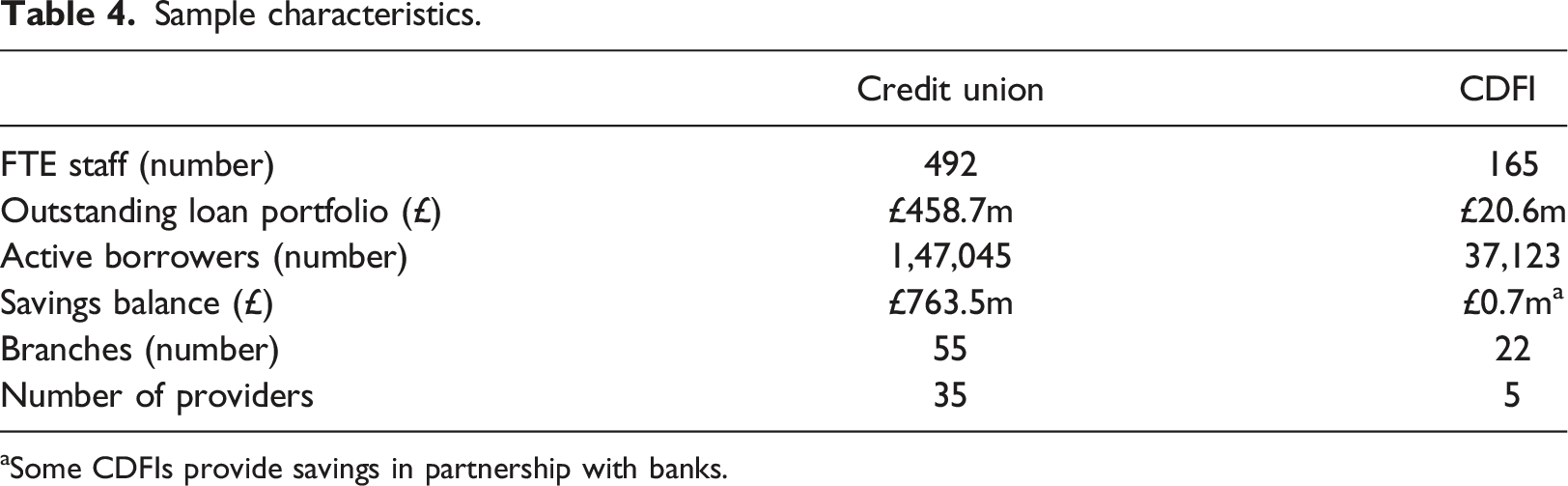

Sample characteristics.

aSome CDFIs provide savings in partnership with banks.

Out of the 64 respondents to the first survey, 24 (all credit unions) did not take part in the second survey. Smaller, volunteer-led credit unions were less likely to respond to both surveys. Eight organisations – two CDFIs and six credit unions – that had not responded to the first survey, took part in the second survey. We only use the data from the 35 credit unions and 5 CDFIs that participated in both surveys.

In terms of the credit unions, 35 or only around 14% out of the 240 credit unions in the UK (excluding Northern Ireland) were represented in the sample. However, the credit unions in the sample make up around 46% of the sector’s outstanding loan portfolio and 40% of the savings. On average, the respondent credit unions were significantly larger than the UK average in terms of loan and savings portfolio. Most of the largest credit unions participated, but few of the smallest volunteer-based credit unions took part. There is no equivalent balance sheet data for the CDFI sector, but most of the largest, well-established providers participated in both surveys. The credit unions are significantly larger than the CDFIs with three times greater outstanding loan portfolios.

We used the Wilcoxon signed-rank test to test for statistically significant differences in the monthly loan application, lending, arrears and income data for February–October 2020 with the previous year to ascertain the impact of COVID-19. This test is suitable for testing associations between an ordinal or continuous dependent variable and independent variable consisting of two categorical, related groups. We used year-on-year growth rates rather than monthly growth because consumer lending by credit unions and CDFIs is often seasonal peaking during Christmas and school holidays.

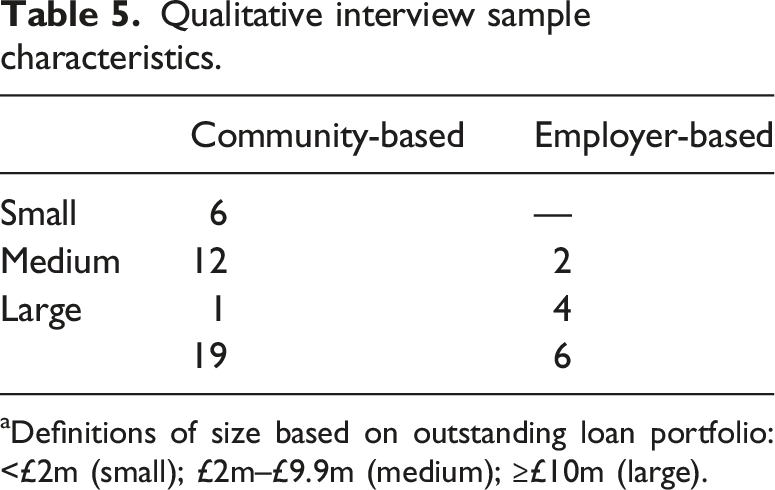

Qualitative interview sample characteristics.

aDefinitions of size based on outstanding loan portfolio: <£2m (small); £2m–£9.9m (medium); ≥£10m (large).

We distinguish between community-based providers, which serve people living or working in a defined geographical area, and employer-based institutions, which provide services for employees from one or multiple employers. All the CDFIs are community-based. The majority of the interviewees were small and medium-sized community-based organisations. Four of the five large organisations were employer-based. Five of the organisations interviewed were based in Scotland. The remaining providers were from England.

Findings

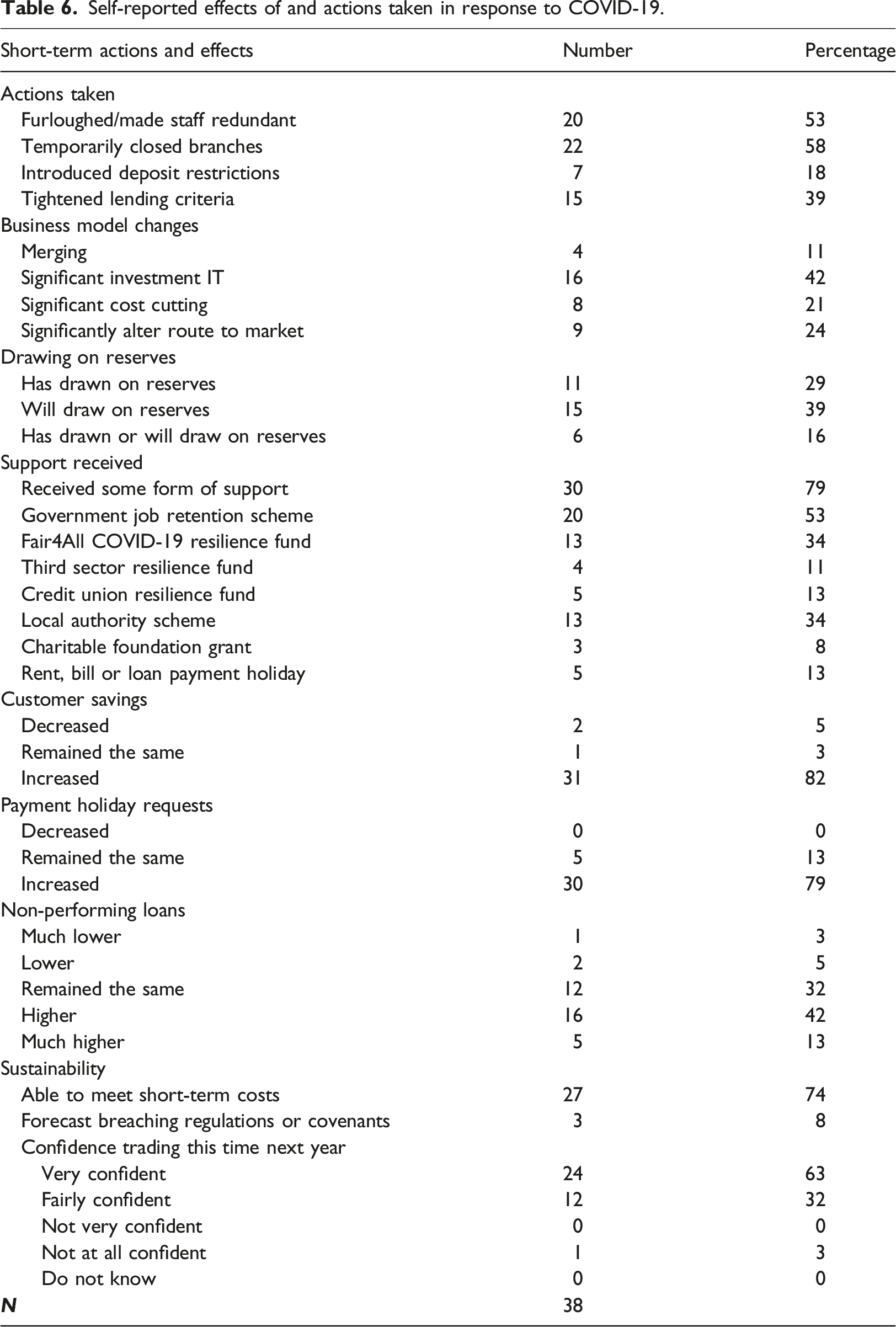

Self-reported effects of and actions taken in response to COVID-19.

The most immediate impact of the pandemic was that it forced around 60% of providers to temporarily close branches in response to government restrictions. Several of the larger providers, especially national, employer-based credit unions, did not have any branches to close, as the vast majority of their customers already accessed services remotely. The customers would use the head office for any services requiring face-to-face interaction (e.g. larger loans requiring wet signature or verification of identity).

Around half of providers furloughed staff. This was often linked to the temporary closure of branches, as branch staff were most commonly among those furloughed. Many also stopped using volunteers, who had often manned collection points. The temporary closure or reduced use of branches and offices required the providers to have systems and processes enabling the provision of services to customers remotely and for all or parts of the workforce to work from home. The changes made to enable staff to work from home included purchasing hardware, setting up cloud computing and transferring telephony capabilities. Providers made a range of changes to be able to serve customers remotely, including introducing e-signature, increasing the loan size that required a wet signature and introducing video conferencing with first time borrowers to verify their identity.

The need to make changes to accommodate remote working and service provision varied considerably across the sample. Providers whose customers were mainly or exclusively accessing services remotely at the start of the pandemic had to make few if any changes. These tended to have a more middle-class customer base as opposed to low-income consumers. Several other lenders brought forward existing plans to digitise and move processes online: “We had a strategy to become more digital, offer more digital services and online access for members. We had that in place anyway, but we have definitely speeded that up… we introduced new things that had been on a timescale for 12 months’ time that were actually implemented straight away” Interviewee 1, small community credit union, England

As government restrictions were eased and providers were allowed to reopen branches, it was challenging to keep branches open due to self-isolation requirements: “Last week we had three people self-isolating, so you know, try running a branch-based operation when you’ve got three people self-isolating and that’s because all of them are from one branch! That’s a big challenge at the moment.” Interviewee 15, medium-sized CDFI

The pandemic led providers to reconsider or accelerate their business plans and approaches. Many abandoned or delayed planned business development activities, including shelving, or scaling back marketing campaigns. In some instances, providers used funds intended for development to bridge gap between income and expenditure or dedicated more time to fundraising (several received funding from local or central government) at the expense of other development work: “We’re running a net deficit of £500 a month. It is not looking like we’ll make up what we’ve lost in lost income and increased costs. So put that into context £500 a month is £6,000 a year, which is around 10% of our income. We were reasonably cushioned because we had some grant funding for development to cover increased staffing over a couple of years while we continued to grow the credit union. I guess that gave us a cushion to absorb the immediate losses but it’s going to create a problem, well it’s creating problems now because for the things we're supposed to be doing I was expecting to have three full-time staff not two.” Interviewee 1, small community credit union, England

There has been, according to the interviewees, an increase in and acceleration of discussions on mergers and acquisitions. Several of the larger credit unions reported being, to a greater degree, approached by smaller providers for take-over discussions: “I think it [mergers and acquisitions] have accelerated. I think Covid-19 has caused issues for credit unions and crystalised the need for mergers. We have actually been approached before Christmas by a credit union that was struggling with its capital asset ratio prior to Covid and that wanted to merge with us. That’s the first time I ever have been approached in the seven years that I’ve been at [name credit union]. I think it has changed the narrative of the credit union.” Interviewee 23, large employer-based credit union, Scotland

According to the managers interviewed, smaller credit unions approached them often in response to operational challenges of moving online rather than due to immediate financial pressures. Some of the smaller credit unions and CDFIs in our sample were looking for larger providers to merge with sooner than planned.

The Coronavirus also encouraged providers to rethink their delivery channels. Some providers decided to permanently close some of the branches they had temporarily closed during the pandemic, by not renewing or cancelling leases: “We closed two branches as a direct result of what happened [Covid]. Whilst branch strategy was something we were talking about, those closures were a direct result of responding to the new environment. The one lease came to an end in that period. Another one we negotiated our way out of.” Interviewee 16, medium-sized CDFI

Others decided to retain the reduced opening hours introduced during the Coronavirus pandemic. More radical proposals providers included were considering becoming wholly online and abandoning office: “…we have to look after ourselves and we are seriously looking at a permanent vacation of office space and moving to become a virtual business.” Interviewee 7, medium-sized community credit union

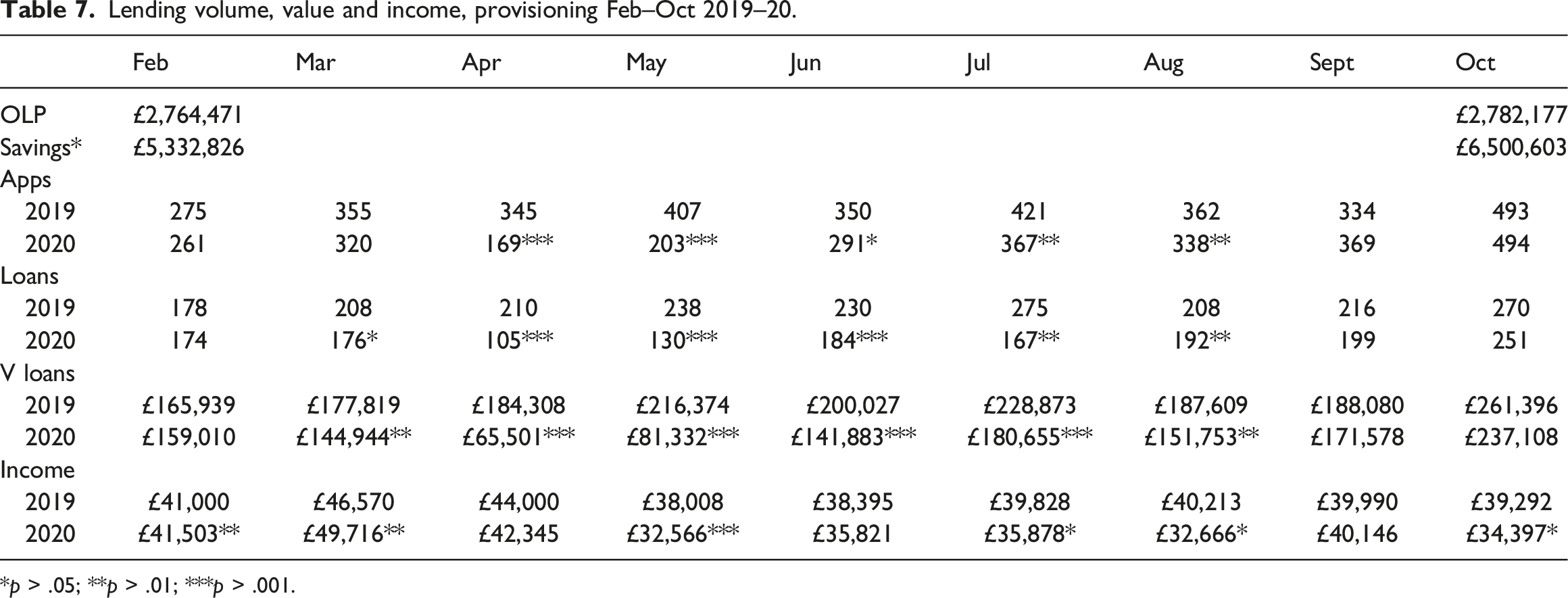

Lending volume, value and income, provisioning Feb–Oct 2019–20.

*p > .05; **p > .01; ***p > .001.

Demand, as measured by the number of loan applications, fell significantly year-on-year between April and August before returning to 2019 levels in September and October. In April and May, the median number of applications fell by over 100%. The volume and value of loans issued was significantly down year-on-year to April–August 2020 before returning to near 2019 levels in September and October. The greatest falls in lending were in April and May.

The evidence suggests that the fall in lending was largely due to a collapse in demand for loans rather than lenders restricting supply. The number of loan applications fell significantly over the same period. In many cases, customers did not borrow simply because they had no opportunity or reason to spend: “When we ask why they’re not taking loans. They say, ‘well what are we going to spend it on.’ We do a lot of loans for cars. They’re always buying a new motor or doing their car up. Holiday is another big thing.” Interviewee 22, large employer-based credit union, England

Travel restrictions, closure of non-essential shops and government advice to work from home meant that customers were not borrowing to go on holidays, buy cars, going out or commuting. Other customers were reportedly not borrowing because their financial situation had been affected by COVID-19. They or someone in their household had been furloughed, made redundant or had their hours or overtime reduced. This group was, according to the managers interviewed, a minority of customers: “There are a small number of people who have been impact because they’ve been made redundant, furloughed on 80% of pay or they’re self-employed… Those have been badly affected and from our point of view we’ve deferred loan payments and we have tried to be as sympathetic as possible.” Interviewee 5, small community-based credit union, England

15 institutions – 40% of the sample – introduced lending restrictions in response to the pandemic. This had, according to the managers interviewed, only a minor impact on lending. Changes in lending policy mainly restricted access to credit for those in sectors directly affected by the pandemic (e.g. hospitality, travel), who for most lenders made up a small part of their customers: “So, we have kind of tightened depending on what sector they are working in. We have tightened the rules a little bit to identify where they are and whether they’re furloughed and digging a bit deeper into the data and seeing exactly what is happening with them.” Interviewee 17, medium-sized community credit union

Another important observation from the data on lending is that the value of lending fell to a greater extent than the number of loans, indicating that the community lenders made smaller loans during the pandemic. Indeed, the average loan amount fell from £1300 in March 2020 to £970 in April 2020 before returning to 2019 levels in July 2020. The follow-up interviews suggest that credit unions, in particular, made smaller loans than usual to help their customers bridge temporary gaps between income and expenditure: “The other thing we said was that we’ll do £200 emergency loans. We still have to comply with regulation and rules, but where we can, we will help just to make sure people have got access to money. This gave people a bit of reassurance.” Interviewee 25, small community credit union, England

Some providers, as per the above quote, introduced specific small ticket emergency loan facilities to support their customers.

Despite the significant year-on-year falls in the value of lending during the pandemic, the value of the outstanding loans increased slightly between the first and second survey. The aggregate increase in the outstanding loan portfolio masks significant variation in the sample. Many providers – 24 out of 40 – experienced a decrease in the value of the outstanding loan book, some by as much as 25%. All the providers interviewed reported that the level of lending was lower than projected, even if some were experiencing growth in lending. Interviewees also noted that it takes time for the value of loans disbursed to translate into a smaller loan book.

The pandemic negatively affected the finances of most providers in the sample primarily by increasing costs and reducing future income. On the income side, the significant year-on-year fall in the value of loans disbursed will result in lower than projected interest income, as there is a smaller loan book to generate interest income. The lower levels of lending are yet to result in significantly a smaller loan book for most providers. The impact on the loan book and interest income would, according to managers, be cumulative over the coming years: “…it’s had a massive impact on our bottom line […] so double whammy, you know, we took on this cost, we didn’t have the capital to lend, so we couldn’t build the new customers that then become existing customers, which then in subsequent years has a further impact on your income from lending, your future income from lending, and you haven’t had time to build up, even though we’ve got the capital, we get a pandemic for 6 months which means we don’t get time to build up the existing. […] it’s a feeling of almost running with three years of cost, and it is taking time for the income from lending to come through.” Interviewee 20, medium-sized CDFI

As alluded to in the quote, it takes time to build up a loan book as the lower levels of lending delay repeat borrowing. Further, although many were experiencing a recovery in lending, it was noted that the lending that did not take place would be lost business: “…the thing for us to try and get our heads around is that …lost consumption is lost consumption. So, we might achieve a normality, or a restoration of 2019, but the lost business is lost forever,” Interviewee 7, medium-sized community credit union

Three types of costs increased due to the pandemic. Firstly, providers incurred one-off or recurring expenses to operate in compliance with government restrictions. This included adjusting branches to allow for social distancing (e.g. signage), enhanced cleaning routines and staff training. Secondly, bad debt provisioning increased because of higher levels of arrears. Around 60% or 21 providers reported that the proportion of non-performing loans had already increased because of the pandemic. The vast majority experienced higher levels of loan repayment holiday requests from customers after the pandemic. Indeed, many credit unions had not received any such requests prior to the pandemic: “We’ve had around about 30 payment holiday requests and on our loan agreement it does state that we don’t offer payment holidays. So, payment holidays is something that we weren’t regularly asked for. We have had one or two in the past, but they’ve just been told that it is not something we offer. So, our payment holiday requests has pretty much increased by 100% because we don’t grant them.” Interviewee 3, small community credit union, England

The follow-up interviews suggest that this was due to an initial panic among borrowers and proactive communication about the availability of payment holidays. Most were now repaying as normal. However, many of the managers interviewed expected arrears to increase with the phasing out of government support schemes and restrictions on creditor and landlord actions: “What we’re not sure of, and this is the big concern for us because lots of our members are housing association members or private landlords and so they’re not allowed to evict anybody at the moment, until last week or something when they were allowed to start proceedings. That’s one thing, and also bailiffs weren’t allowed to visit homes so there could be an underlying debt, financial rent arrears problem that is going to, you know, surface when things get to normality.” Interviewee 17, medium-sized community credit union

The third cost increase, experienced only by the credit unions in the sample, was associated with the significant rise in savings. 31 out of the 34 credit unions in the sample reported an increase in customer savings. The savings book was significantly larger at time of the second survey (December 2020) than at the beginning of the pandemic (April 2020). This is, according to the interviewees, because customers spent less and saved more. There were fewer opportunities to spend money due to the restrictions on travel, retail and hospitality. Not only did customers save more, but fewer people also withdrew savings: “...members weren’t lifting out their savings that they would normally lift out, which meant our share retention was a lot higher than it would normally have been and we’re still seeing a wee bit of that but not as much as it was.” Interviewee 6, small community credit union, Scotland

The increased size of the savings book meant that providers incurred greater costs to pay members their dividend. Moreover, the combination of a significant increase in savings with the stagnation of the loan portfolio resulted in falling Capital Asset Ratios (CAR) for most of the credit unions. In the follow-up interviews, credit union managers reported falls in the region of 2–4 percentage points: “We have an aspiration to get to 20% capital asset ratio and that’s against a regulatory target of about 10%…Last year [2019] we just hit 20%, but because of the additional savings that are coming in...we are now at 16.8%. The effects of those extra savings coming in has actually increased our capital asset ratio by 3%.” Interviewee 24, large employer-based credit union, England

Aside from being an indication of the financial health of the credit union, it is also used by the financial regulator. Credit unions that fall below a given ratio are subject to greater scrutiny and reporting. For most, the fall was not a major concern as they were well capitalised and had a high starting point. Some of the smaller credit unions that were not yet profitable were concerned about the fall in the ratio: “If that [bad debt] grows and gets out of control that is a bit of an existential crisis for us because we have to meet regulatory targets to continue to trade, and the key target we have to meet is this capital-to-asset ratio and compared to a lot of other credit unions our reserves are quite low. A lot of them had a grant about ten years ago of which [name of credit union] got the first tranche of but didn’t manage it well so a lot of credit unions used that grant to build their reserves. If you’ve got reserves, then you can meet this regulatory ratio ok and you got a buffer. We’ve had very little buffer so far. If the bad debts really go the wrong way that would impact on us.” Interviewee 3, small community credit union, England

In response to the rise in savings and the implications for regulatory ratios, seven credit unions introduced restrictions on the overall amount customers can hold or deposit. Other credit unions planned to reduce the level of dividend paid out to members.

Because of the increasing costs and falling lending, many, especially CDFIs and smaller credit unions targeting low-income consumers, reported they would have made a loss without financial support to cover loan losses and the extra costs associated with complying with government restrictions and regulations. In some cases, lenders drew on funding originally intended for development. Around 80% or 30 of the organisations received some form of support, with the most common source being the Government Job Retention Scheme, local authorities and the government funding body Fair4All Finance.

The providers differed considerably in their perceived ability to cope with the effects of the pandemic. The follow-up interviews and the survey data point to three determinants: financial position at the start of the pandemic, customer characteristics and size. Well capitalised providers with significant reserves and accumulated profits were confident and highly unlikely to breach regulatory ratios due to the pandemic: “…we did see an initial increase in bad debt and payment holidays, but that did settle down, though we do expect bad debt to increase right up next year, but we’re well capitalized, we can manage that […] we’ve got wriggle room if needed” Interviewee 18, medium-sized community credit union, England

The fall in CAR had no regulatory or prudential consequences because of the high starting point. The key step these providers took or would consider, if any, to manage the fallout of the pandemic was to reduce the dividend paid to members. Conversely, providers in transition towards full sustainability and had limited reserves showed greater strains and were more concerned about the future. For some providers, falling regulatory ratios would, if not reversed, impose additional supervision, and pose a threat to their financial viability: “It’s only now becoming an issue. We managed to maintain our capital asset ratios. I think they dropped from 8 to 6.5 [percent] but more recently it’s dropped, we’re seeing about five now and we’re going to have to work out what to do about that. The reason it’s dropped is a combination of strong savings growth, but also increased delinquency.” Interviewee 1, small community credit union, England

These providers were less well positioned to cope with any drops in income and the additional costs, because they were still not fully sustainable or only able to generate very small surpluses. They were more likely to draw on reserves or use development funds to cover deficits.

The characteristics of a provider’s customer base also influenced the immediate effects of the pandemic. Customers that were directly affected by the pandemic through loss of employment or reduced income were, according to interviewees, more likely to experience problems repaying loans and less likely to take out new loans causing problems for providers with many such customers: “a lot of our customers are in precarious employment […] so we had a look to see, you know, where the risks were in our loan book by sector, so hospitality, retail. […] we do have a quite a big proportion of people who are working in those sectors, I think between 30 and 40% of our members who are working are working in those sectors.” Interviewee 4, small CDFI

The repayment capacity of and long-term demand by customers already on benefits pre-pandemic or whose work or pay was unaffected was not seen to be detrimentally affected by the pandemic. Many of the providers, especially credit unions, primarily served consumers whose finances were not significantly affected by the pandemic, such as public sector employees. As a result, they predicted that the pandemic would have limited long-term effects for them: “All of that is manageable. We are well capitalised, and we see this [increase in savings and drop in lending] as a short-term issue until people get more back to normal. There’s lots of research that says when there is economic uncertainty, people tend to stop spending money...so we see this hopefully as a short-term impact.” Interviewee 24, large employer-based credit union, England

The providers serving lower-income, financially excluded consumers were generally in a weaker financial position. This reflects that lending to such groups is a more marginal activity because of the smaller loan amounts and greater risks. Conversely, providers lending to more middle-class customers tended to be in a stronger financial situation, as this customer groups would take out larger loans and involve lower risk.

The smallest providers appeared to be especially vulnerable to the effects of COVID-19. They had fewer staff and resources to meet the additional costs and requirements of social distancing and remote service delivery: “Obviously we have more staff working from home and that’s also an issue because we can’t invest a lot of money into IT development. If there had been funds available to modernise our IT, there are systems and services being made available to credit unions, but it’s the capital costs of those but also the ongoing revenue costs, which when you’ve got income shrinking and potential bad debt costs rising it is not a good time to take on new costs. Those elements have made it particularly challenging.” Interviewee 3, small community credit union, England

Overall, they had limited capacity for working remotely and providing services online at start of pandemic. They were often too small to benefit from various funding sources. Larger institutions often had a greater loan book to generate income and tended to be in a stronger financial position.

Conclusion

The data presented in this article suggests that the demand for, and volume and value of lending by affordable credit providers fell significantly during the first lockdown only recovering by the end of the summer. This is in line with the significant drops in UK consumer lending during the same period (Bank of England, 2022). This trend, in turn, negatively affected the finances of most providers, including through lower income, greater costs and lower regulatory ratios. The ability to cope with these negative effects varied considerably across the sample. Larger providers, those serving less vulnerable customers and providers in a strong financial position at the start of the pandemic were less affected than smaller providers in a weak financial position at the outset serving poorer consumers. Partly in line with Jones et al. (2020), we find that the pandemic led providers to change their operating and delivery models, including a shift towards greater online delivery, branch closures and mergers.

We do not have sufficient evidence to assess the relative resilience of the community-based lending model in the face of economic downturns, which is a key question in the academic literature (Lu and Swisher, 2020; Coen et al., 2019). The long-term impact of COVID-19 on affordable credit sector and access to credit for financially excluded consumers is still uncertain. At the time of collecting the data, the various government support schemes were still being phased out. Moreover, we only have data for the first lockdown and the period up to the second lockdown in October 2020. Lending may have recovered or fallen more during subsequent lockdowns. The sample also does not cover the whole sector, comprising instead of 14% of the number of providers and 46% of the value of outstanding loans.

However, the effects of the pandemic on the affordable credit sector highlighted by the data presented in this article may affect the access to financial services among the most vulnerable, financially excluded communities in two ways. First, the intensification of the move to online service provision and the closure of branches may reduce access to services for the most financially excluded, who often operate in cash. Existing research indicates that providers struggle to serve the most excluded groups more prone to using cash through remote channels (Vik et al., 2021). Compared with face-to-face, manual underwriting, providers using online channels tend to serve more men, more in employment and with higher incomes (Dayson et al., 2020).

Second, the providers targeting more vulnerable, low-income households appeared to be under greater financial pressure due to the pandemic. This may make them more likely to fold or be taken over by a larger provider potentially resulting in reduced or no provision for these consumers. Those providers serving low-income consumers are often less financially sustainable as lending to this group involves smaller loan amounts, greater arrears and forbearance, and at least a degree of manual underwriting. A recent analysis of credit union failures in Great Britain suggests that credit unions in deprived communities are more likely to fail (Coen et al., 2019).

Local and national policymakers need to be aware and monitor these risks to ensure that the fallout of the pandemic does not hollow out the provision to deprived communities. This may involve supporting struggling local providers or working with the larger providers in mergers to make sure the continuation of provision to low-income communities.

Moreover, the findings underline the need for future research on two areas. Firstly, there is a need to empirically test the link between borrower characteristics and financial performance, which our interview data indicate. Using neighbourhood deprivation data (Coen et al., 2019) is not sufficient to demonstrate this link, as community lenders may be located in deprived communities and still serve less vulnerable customers. Secondly, further research is required to determine if and the degree to which the short-term effects of COVID-19 (e.g. sharp fall in value of lending, increased operating costs) documented in this paper influence the long-term financial sustainability of community lenders.

Footnotes

Declaration of conflicting interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: Karl Dayson was a non-executive director of one of the participating community finance providers from 2010 to 2019.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by Fair4All Finance.