Abstract

Recent technological advances both on the farm and in the lab are boosting not only the efficiency of modern farming but have made it also more independent from nature than ever before. Increasingly affordable and accessible new technologies are helping us to better understand and ‘manage’ nature and thus, for first time in history farming is becoming as any other industry – susceptible to specialisation and economies of scale. This in turn, besides increases in productivity and the minimum efficient scale, leads to fundamental organisational change, away from traditional family farms and towards corporate forms with the associated implications for employment and rural livelihoods. Recent evidence from the digitalisation in agriculture suggests that new technologies require developing capabilities in abstract and analytical skills substituting skills in routine tasks. However, this is not the end game for farmers; new partnerships between technology providers and agribusiness players emerge as digitalisation and connectivity become a strategic issue. Thus, while the first Industrial Revolution led to machines replacing ‘muscles’ the new Digital Revolution is leading to machines replacing ‘brains and souls’, and it may eventually end family farming as we know it.

Introduction

In their best-selling book The Second Machine Age, Erik Brynjolfsson and Andrew McAfee (2014) argue that there is a new Digital Revolution unfolding. While as a result of the first Industrial Revolution machines replaced ‘muscles’ the new Digital Revolution is leading to machines replacing ‘brains and souls’. In a related article in The Guardian, Evan Fraser and Sylvain Charlebois (2016) discuss how the latest technology adoption serge in farming is good for food security but they also pose the question to what extent the farming jobs are under treat. A striking evidence of a complete departure from traditional family farming is provided by Lindsay Fortado and Emiko Terazono (2019) in their Financial Times article on the case of AeroFarms highlighting the dramatic technological and organisational change that farming is undergoing.

What is actually happening?

The revolutionising of agriculture is taking off in two distinct areas. Both on-farm and genome-scale increasingly affordable technologies are boosting the efficiency of modern farming. On the farm, satellite driven geo-positioning systems and sensors detect nutrients and water in soil. This technology is enabling tractors, harvesters and planters to make decisions about what to plant, when to fertilise and how much to irrigate. As the technology progresses, equipment will ultimately be able to tailor decisions on a yard-by-yard basis. Robots can already do much of the harvesting of lettuce and tomatoes in greenhouses. In the dairy industry, robotic milking and computer-controlled feeding equipment allow for the careful management of individual animals within a herd. A similarly dramatic technological revolution is happening with the genetics of plants and animals making it much easier to identify individual plants and animals that are particularly robust or productive and less dependent of nature.

It is worth noting that alongside this dramatic technological shift a related and similarly significant trend towards globalization of trade has led to market expansion and rise in the global demand for farm products. This in turn has created strong incentives for further technology adoption in pursuit of ever-increasing productivity.

What are the implications for farming?

Since the onset of the Industrial Revolution developments in technology and other social factors have changed the way we work and the types of work that we do. These processes have led to the shape of the industrial landscape today where services are the dominant industries while manufacturing (and farming) industries account for only a small share of the work force. Nevertheless, the importance of manufacturing (and farming) varies between the urbanised and rural local economies and across counties and regions. Importantly, the changes in industry composition have been accompanied by a general transition of the industrial production organization from family firms towards large, factory-style corporations.

Notably farming has been an exception and remained a last bastion of family production providing livelihood in rural local economies. According to Douglas Allen and Dean Lueck (2003) who published the influential book The Nature of the Farm, the main reason for farming deviating from the trends in industrial organisation restructuring is the sector’s technological specificity associated with strong nature dependence. Production stages in farming tend to be short, infrequent and require few distinct tasks. These characteristics, due to high transaction and information costs, limit the benefits of specialization and make wage labour especially costly to monitor. Notwithstanding the market expansion effects of globalization, providing some opportunities for gaining economies of scale, only when farmers can truly control the effects of nature by mitigating the effects of seasonality and random shocks to output would farm organisation gravitate toward factory-type processes, associated with large-scale corporate forms found elsewhere in the economy.

The ongoing technological advances both on the farm and in the lab have made farming more independent from nature than ever before. Arguably, the new and accessible technologies are helping us to better understand and ‘manage’ nature and thus for first time in history farming is becoming as any other industry, truly susceptible to the forces of specialisation and economies of scale. This in turn, besides the increase in productivity, leads to fundamental organisational change, away from family control of agricultural production towards corporate forms with the associated implications for employment and rural livelihoods – the new technologies in farming is likely to replace not only ‘muscles’ but also ‘brains and souls’. This is because the intricate knowledge that farmers have had about the local conditions and operation of their farms is becoming increasingly substitutable by the new intelligent technologies.

What evidence do we have so far?

It has been notoriously difficult to obtain clear evidence on the impact of technological change on agricultural sector production organisation besides the well observed fact of the increasing scale of operation and the resulting continuous reduction in the number of family farms operating. This scarcity of evidence is mostly due to two reasons: (i) production organisation changes usually happen over a long time horizon and (ii) the effect of (endogenous) technological change has been confounded with the effects of other factors, most prominently the state support to the agricultural sector. Historically, family farming has been generally difficult and very brittle sort of activity, susceptible to nature and technology shocks. Sarah Taber (2019) in her Intelligencer article about the unfortunate love of America for family farms argues that family farming only makes a viable livelihood for farmers when land is nearly valueless for sheer lack of people. Otherwise, family farming has always been a low return to assets and unattractive investment proposition. In local economies where family farming has persisted for more than a couple generations it is largely due to extensive, modern technocratic government interventions like grants, guaranteed loans, subsidized crop insurance, free training, tax breaks, suppression of farmworker wages and more. Thus, perhaps, the existence of enduring state interventions in agriculture during the post-Second world War period both in North America and Europe is the most telling evidence so far of the suboptimality of the family farm production organisation, at least during the Second Machine Age.

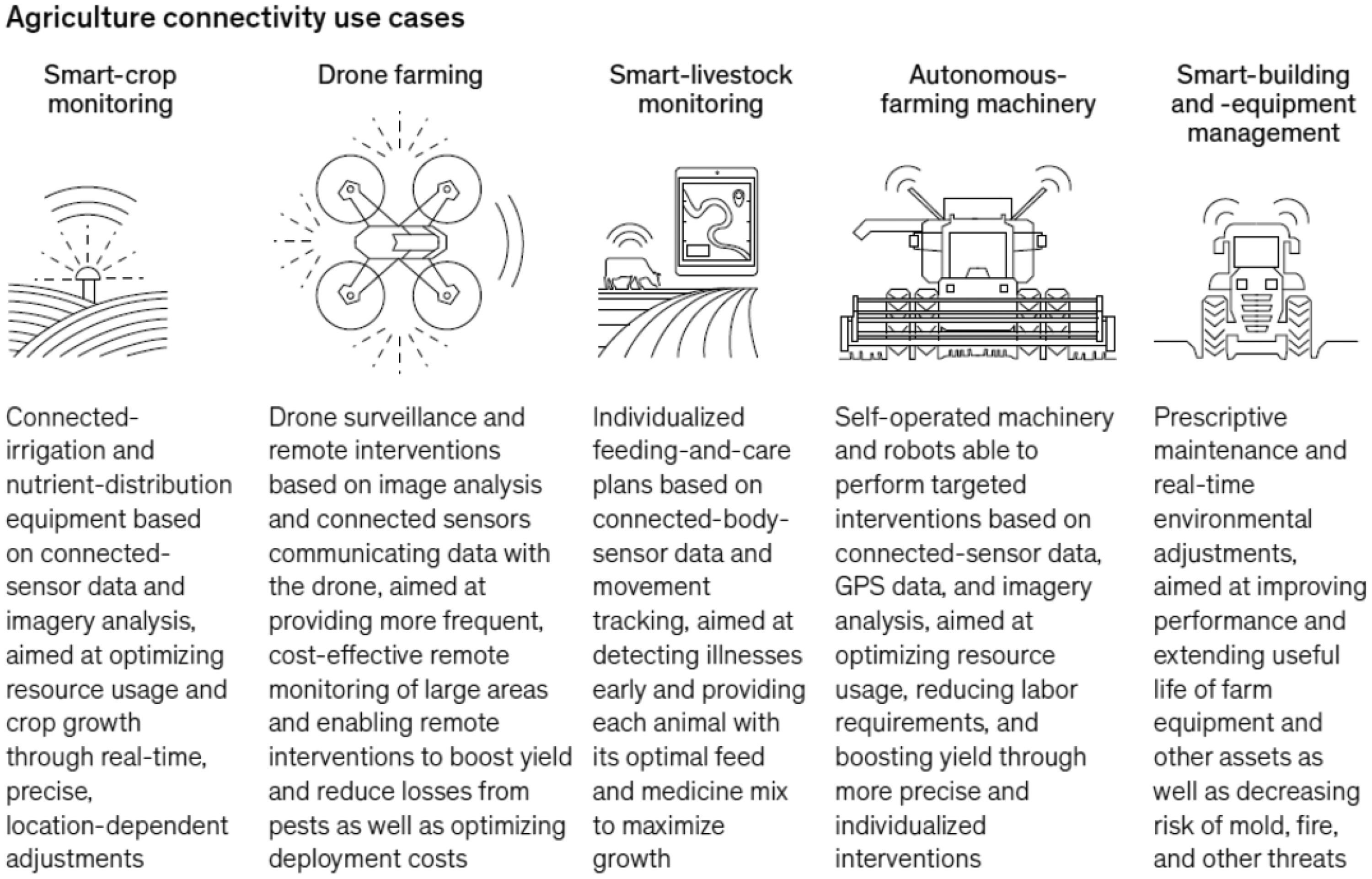

Alongside the preceding arguments, recent, detailed analyses by the McKinsey Centre for Advanced Connectivity and Agriculture Practice on the emerging and expected effects of new digital technologies in agriculture generate very relevant, even though, perhaps some-what speculative, evidence on the future of the agricultural sector production organisation. Lutz Goedde et al. (2020) from McKinsey analyse five connectivity technology use cases – crop monitoring, livestock monitoring, building and equipment management, drone farming, and autonomous farming machinery – where digital technology and enhanced connectivity are already in the early stages of being used and are delivering higher yields, lower costs, and greater resilience and sustainability (Exhibit 1). It is noteworthy that use cases do not apply equally across local economies. For example, monitoring solutions, drones and autonomous machinery deliver more impact to advanced markets, as technology is more readily available there.

▪ Source: McKinsey & Company.

Goedde, Katz, Menard and Revellat observe that as the agricultural industry digitises, new pockets of value are being unlocked. For example, the USA input providers selling seed, nutrients, pesticides and equipment have played a critical role in the data ecosystem because of their close ties with farmers, their own knowledge of agronomy and their track record of innovation. The fertiliser distributors now start offering both fertilising agents and software that analyses field data to help farmers determine where to apply their fertilizers and in what quantity. Similarly, large equipment manufacturers are developing precision controls that make use of satellite imagery and vehicle-to-vehicle connections to improve the efficiency of field equipment.

Goedde, Katz, Menard and Revellat note that advanced connectivity does, however, give new players an opportunity to enter the space and this is the crucial evidence so far for potential shift in the production organisation of the agricultural sector. For example, telecommunication companies and network providers have an essential role to play in installing the connectivity infrastructure needed to enable digital applications on farms. They could partner with public authorities and other agriculture players to develop public or private rural networks, capturing some of the new value in the process.

Agritech companies are another example of the new players coming into the agriculture sphere. They specialise in offering farmers innovative products that make use of technology and data to improve decision making and thereby increase yields and profits. Such agritech enterprises could offer solutions and pricing models that reduce perceived risk for farmers – with, for example, subscription models that remove the initial investment burden and allow farmers to opt out at any time – likely leading to faster adoption of their products. An Italian agritech is doing this by offering to monitor irrigation and crop protection for wineries at a seasonal, per-acre fee inclusive of hardware installation, data collection and analysis, and decision support. Agritech also could partner with farmers to develop complex agribusinesses solutions. Overall, the tendency is though one of reduced autonomy in farmer operating decisions and closer integration in investing.

There are three principal ways partnerships could be formed and the necessary investment for digital technology and connectivity take place:

Farmer-driven deployment. Farm owners, alone or in partnership with network providers or telecommunication companies, could drive investment even though such partnerships are not a common place and the participating farmers are rarely your typical family farmer type. Generally, this requires farmers to develop the knowledge and skills to gather and analyse data locally, rather than through third parties, which is no small hurdle. The ‘advantage’ is that farmers retain more control over data and operations.

Telecommunication company-driven deployment. Though the economic returns to high-bandwidth rural networks have generally been poor, telecommunication companies can benefit from a sharp increase in rural demand for their bandwidth as farmers integrate advanced applications and integrated solutions in their business operations. Clearly, farmers’ dependence on the services provided and the access to and use of data may lead to a loss of full operational and financial control.

Input provider-driven deployment. Input providers, with their existing industry knowledge and relationships, are probably best positioned to take the lead in digital technology and connectivity-related investment. They would usually partner with telecommunication company or network provider to develop rural connectivity networks and then offer farmers business models integrating connected technology and product and decision support. As in the previous scenario, farmers will have to compromise with their operational and financial independence.

Apparently, in the three scenarios above, family farming is likely to evolve into sort of a contractor type arrangement. This is so because developing new capabilities however challenging is not the end game. Agribusiness players able to develop partnerships with telecommunication companies or network providers will gain significant leverage in the new connected-agriculture ecosystem. Not only will they be able to procure connectivity hardware and services more easily and affordably through those partnerships, they will also be better positioned to take over and control farming operations as connectivity becomes a strategic issue.

What might the future of farmers look like?

Notwithstanding the recent evidence from digitalisation of agriculture, a simple economic model of industrial production and historic evidence from the last two centuries since the start of the Industrial Revolution demonstrate that an increase in labour productivity does not necessarily reduce employment in the long run. While inventions in technology may mean that fewer labour hours are needed to make any particular good, labour-saving technology tends to reduce the costs of producing each unit, resulting in lower prices. Lower prices, in turn, lead to higher demand for goods, and, correspondingly, to higher demand for workers, in the same or related up- and down-stream industries.

Would the Digital Revolution be any different? Tyler Cowen (2013) in his book Average Is Over has argued that the rapid advance of machines and computing will create two classes: a highly skilled elite, making up about a tenth of the population, who will profit handsomely by learning to work alongside machines; and everyone else, who will see their wages stagnate or decline. Evidence from the last two decades, from both North America and Western Europe on ‘wage polarisation’ and corresponding ‘job polarisation’ provided by several authors is consistent with the view that technological change during the period tended to complement the abstract (analytical) skills at the high end of the skill and wage distribution, and, in some instances, the non-routine (personalised) tasks performed in a number of lower-wage jobs.

Either of the two (high-wage vs. low-wage) scenarios, described above could apply to farming. To realize the optimistic, employment and income enhancing, scenario, Claudia Goldin and Lawrence Katz (2008) in their book The Race Between Education and Technology have argued, will require a major commitment to increasing education and skill levels as well as fostering business and organization innovation. Regional, national and even international effort and commitment will be required, but arguably, based on political economy arguments, such commitment could be better sustained at a supra-national level. A good example is the provision of infrastructure needed to enhance connectivity through large-scale, cross-country projects. However, the pessimistic scenario – of underemployment and low wages – in the case of farming is quite possible, considering that agricultural land is a finite and limited resource commanding high values and low returns. With the demand for land and its values continuously increasing the viability of family farms is likely to further decline. This makes meeting the challenges posed by technological change even more imperative, if we were to avoid that a substantial portion of the farming population was deprived of their traditional livelihoods. Notwithstanding the importance of education and skills upgrading, if Brynjolfsson, McAfee, and Tyler are right about the implications of the Digital Revolution for jobs and employment, the re-distributive role of the national and supra-national governments will also become increasingly important in supporting those who fall behind.