Abstract

Regional resilience is a topic of growing academic and policymaker interest. This article empirically examines this concept by scrutinising the impact of Brexit on Scottish small and medium-sized enterprises (SMEs). Given their crucial importance for the Scottish economy, SMEs are a good ‘unit of analysis’ and a powerful barometer for measuring regional resilience. The research adopted a novel mixed methods approach examining the Longitudinal Small Business Survey together with in-depth interviews with SMEs. It is clear from the survey analysis that certain types of SMEs (i.e. innovators and exporters) were disproportionately fearful of Brexit. This was firmly corroborated by the interview data which found these same firms to be the most detrimentally impacted, manifesting in reductions in employment, exports and innovation. In contrast, the majority of domestically focused, less innovative SMEs were much less concerned and less negatively affected. While a small minority managed to deploy adjustment mechanisms to mitigate these negative effects, overall many firms had major difficulties operationally and strategically coping with this uncertain and turbulent environment. The findings suggest proactive public policies will be needed to help mitigate the difficulties caused by Brexit for certain types of SMEs.

Introduction

In the main, the academic debate on Brexit has strongly centred on the underlying sources of inequality (i.e. the so-called ‘left behind’) which generated the vote to leave the EU (Billing et al., 2019; Lee et al., 2018; Pollard, 2018). By comparison, much less academic scrutiny has centred on the types of businesses most vulnerable to these forms of unforeseen shocks. Prior evidence suggests that small and medium-sized enterprises (SMEs) are disproportionately impacted by chronic uncertainty given their lower resilience to unexpected shocks (Monsson, 2017; Williams and Vorley, 2017), especially those located in peripheral regions (Gherhes et al., 2018). Yet, to date, how different types of regions and firms cope, adjust and adapt to unforeseen shocks such as Brexit and its related uncertainty has been largely under-researched. Therefore, following pleas for more ‘agency’ and ‘firm-centred’ approaches towards analysing regional resilience (Bristow and Healy, 2014; Dawley et al., 2010; Soroka et al., 2020), this article empirically scrutinizes the impact of Brexit on Scottish SMEs.

Regional resilience is a topic of growing academic and policy maker interest (Bristow and Healy, 2014; Martin and Sunley, 2020; Ray et al., 2017), a term invoked by spatial scholars to describe how regions respond to shocks and disequilibrium (Boschma, 2015; Bristow and Healy, 2014; Hassink, 2010). Despite accusations of opacity and conceptual ‘fuzziness’ (Fröhlich and Hassink, 2018; Pendall et al., 2010), regional resilience helps stimulate important new ways of thinking about changes to our economic landscape (Martin, 2018; Pike et al., 2010). Consequently, it has ‘become a fashionable lens for understanding the factors that shape and determine the nature of economic change and performance over time’ (Williams and Vorley, 2017: 1).Indeed, much of the regional economic debate since the onset of the Global Financial Crisis (GFC) has focused on factors which explain the resilience or vulnerability of regions to sudden economic change (Bachtler and Begg, 2018). Consequently, over the last decade the impact of ‘shocks’ has recently become a prominent subject of empirical enquiry in economic geography and regional research (Martin and Gardiner, 2019).

On the whole those examining resilience to Brexit at a firm-level have typically focused on how large firms (often foreign-owned) are likely to be affected by Brexit (Dhingra et al., 2018). Such evidence provides valuable insights; but it fails to provide the necessary information to assess the likely impact of Brexit for SMEs, despite these firms being crucial for peripheral regional economies such as Scotland. While many SMEs have limited resources and managerial capabilities they often have the ability to pivot quickly to adjust to rapid changes in the marketplace caused by unforeseen shocks (Morgan et al., 2020). For others, this may not be the case however. Indeed, some commentators have speculated that Brexit could have ‘dire consequences’ for these small businesses (Cumming and Zahra, 2016: 690). However, to date there has been a paucity of hard empirical evidence on the actual impact of Brexit at a sub-national level (Brown et al., 2019; Los et al., 2017).

There are compelling arguments for examining Brexit-related resiliency within the Scottish context. In March 2018, there were 343,535 SMEs operating in Scotland, accounting for 99.3% of all private sector businesses and 54.9% of private sector employment (Scottish Government, 2018). Scotland is also highly dependent on EU sources of human capital and regional funding which disproportionately benefit Scottish SMEs (McCullough, 2018). 1 Given their crucial importance for the Scottish economy, SMEs are therefore a good ‘unit of analysis’ and a powerful barometer for measuring regional resilience. Indeed, recent research examining the perceived impact of Brexit revealed that Scottish SMEs exhibited greater reservations about Brexit compared to their counterparts elsewhere in the UK (Brown et al., 2019).

In addition to this conceptual focus on regional resilience, this article also has strong implications for both UK and Scottish public policy more generally given the applicability of the resilience construct for policymakers (Healy and Bristow, 2020; Martin and Sunley, 2020). As scholars have noted, institutions acutely matter for regional resilience, especially their role in mitigating ‘the impact of shocks’ such as Brexit (Boschma, 2015: 744). This is important because having significant devolved powers may potentially enable Scotland to mitigate some of the negative Brexit-related impacts on the economy via bespoke policy interventions. Indeed, some scholars have noted how Scotland was one of the first parts of the UK to respond to the impact of Brexit with new support packages designed to assist SMEs (Brown et al., 2019). This may also hold for Wales and Northern Ireland who have similar devolved powers.

The article investigates the impact of Brexit on Scottish SMEs by employing a novel mixed methods empirical research design (Molina-Azorín et al., 2012). This dual approach enabled the research to examine ex ante the concerns immediately following the referendum and then explore the actual impacts arising from Brexit-related uncertainty. In order to obtain an overview of how Brexit will impact Scottish SMEs, it draws upon the UK’s main small business survey. To delve deeper into the current and likely future impact of Brexit, the research also involved in-depth interviews with a wide cross-section of Scottish SMEs (n = 21) to gauge the firm-levels effects emanating from the Brexit process. This method provides a novel empirically grounded contribution to literature on regional resilience by answering the following research question: what types of Scottish SMEs are most concerned by Brexit and how they are being impacted.

The remainder of the article is structured as follows. First, we examine the literature on regional resilience uncertainty and how this could impact smaller firms. Second, we outline the methodology adopted. Third, we examine the quantitative data to see the types of Scottish SMEs most likely to be affected by Brexit. Fourth, we outline the results of the qualitative data collected. The article ends with a discussion, conclusions and policy recommendations.

Literature review

This literature review draws upon two overlapping streams of academic research pertinent to the empirical focus of the article. First, we explore the concept of regional resilience and how this manifests itself when areas are faced with unforeseen or ‘exogenous shocks’. Second, it examines the literature on economic uncertainty and firm-level behaviour and outcomes.

Regional resilience

While the resilience metaphor has been deployed disparately across various disciplines it is commonly conceptualised as the capacity for an entity (such as a region or firm) to ‘resist, absorb, adjust to, and recover successfully from shocks or disturbances that disrupt that entity’s or system’s pre-shock state’ (Martin and Gardiner, 2019: 1802). Resilience signifies an organisation’s ability to maintain reliable and effective functioning throughout disruption and adversity (Williams et al., 2017). This in part has stemmed from the increased economic, environmental and political volatility which has constantly shaped and reshaped the world economy over the last twenty years, meaning that disequilibrium is very much the norm. Recent exogenous shocks such as the onset of the GFC, the unexpected Brexit vote and most recently the Covid-19 pandemic all testify to uncertainty becoming the ‘new normal’ (Brown et al., 2020; Wenzel et al., 2020).

Although originally invoked to depict resilience and in fields such as engineering and ecology (Healy and Bristow, 2020), in recent years there has been an upsurge of academic interest in the concept of ‘regional resilience’ (Boschma, 2015; Hassink, 2010). This concept is of critical importance because a key implication from this literature is that differences in resiliency to major shocks can contribute to determining the long-run growth paths of different regions (Bristow and Healy, 2014). Indeed, an expanding empirical literature has revealed how different locations have differing capabilities to deal with exogenous or unforeseen shocks.

A common focus within the literature has been to examine how different locations cope with unexpected shocks such as major recessions and crisis events (Martin, 2018). A number of studies have also examined the impact on regional resilience generated by the shock of the GFC (Dijkstra et al., 2015; Giannakis and Bruggeman, 2017). An interesting recent study assessed credit scores to assess firm resilience during the post-GFC period (Soroka et al., 2020). This showed firm closure was often precipitated by falling credit scores in the years prior to foreclosure. One Spanish study found that the regions least affected by the crash were those specialising in the most dynamic and productive industries (Cuadrado-Roura and Maroto, 2016). In an empirical study of the UK it was found that regional resilience to the GFC was highest in areas where the stock of knowledge intensive service firms was greatest (Bishop, 2019). Similarly, a Canadian study also found that regions with the greatest resilience were those dominated by business services, which act as ‘regional shock absorbers’ (Ray et al., 2017). Blažek et al. (2020) found that major European financial centres such as Frankfurt, Paris and London were those demonstrating the greatest resilience to the GFC.

While this body of evidence shows how aggregate economic performance is affected by cyclical shocks, it fails to properly explain how different types of firms (specifically SMEs) adapt, change and reconfigure themselves to accommodate destabilising unforeseen shocks. Indeed, while overall only a limited body of work has examined resilience in SMEs (Wishart, 2018), some studies have vividly illustrated that entrepreneurship is central to creating more resilient regional economies (Williams and Vorley, 2014). Conversely, regional resilience can be undermined in peripheral economies with low levels of entrepreneurial ambition and dynamism (Gherhes et al., 2018). This latter point is crucially important and shows the path-dependent nature of resilience within some entrepreneurial ecosystems (Roundy et al., 2017).

Consequently, there is now growing awareness of the importance of better understanding firm ‘agency’ to adapt to shocks as a means of better appraising the resilience of the regions in which they are based (Bristow and Healy, 2014). In other words, not all firms are equally resilient when faced by destabilising shocks. Therefore, there seems ‘good reason’ to argue that a fuller conceptualisation of regional resilience must incorporate ‘an understanding of the resilience of individual firms and their specific capacities to cope with, adapt to and reconfigure their technological, network and organizational structures within a constantly evolving economic environment’ (Soroka et al., 2020: 3). Given their crucial importance to modern day economies, SMEs may be a suitable ‘unit of analysis’ and a powerful barometer for measuring regional resilience.

Uncertainty and firm behaviour

We now turn attention to a related micro-level literature to see how different types of SMEs may cope with profound uncertainty caused by events such as Brexit. Research from a wide range of disciplines including economics, entrepreneurship and strategic management have all examined the fundamental role of uncertainty in affecting firm-level decision-making processes (Baker et al., 2016; Bylund and McCaffrey, 2017; Milliken, 1987; Wenzel et al., 2020). Almost a century ago, the US economist Frank Knight (1921) first examined the crucial role of uncertainty in shaping economic behaviour by making the important distinction between risk and uncertainty. For Knight the essential fact is that risk can be measured, but true uncertainty (or Knightian uncertainty) is not readily quantifiable. Rare, so-called ‘black swan events’ (Orlik and Veldkamp, 2014), such as Brexit, the GFC or the Covid-19 pandemic generate such acute uncertainty they have consequences so far-reaching they represent something of an ‘unknowable risk’ for firms (Diebold et al., 2010).

According to North (1990), institutions exist due to the uncertainties involved in human interaction and the institutional environment determines the formal and informal rules of the game. As such a stable institutional environment is crucial for mediating entrepreneurial activity and firm-level strategic behaviour (Minniti, 2008). Conversely, prior evidence suggests that unforeseen events can hinder the effective operation of institutions (such as banks during the global financial crisis) generating acute levels of uncertainty, which in turn leads to reductions (and delays) in tangible and intangible investments (Doshi et el, 2018; Julio and Yook, 2012).

Extant prior evidence suggests that SMEs may be disproportionately impacted by uncertainty given their lower resiliency to unexpected shocks (Brown et al., 2020; Doshi et al., 2018; Ghosal and Loungani, 2000; Ghosal and Ye, 2015; Lee et al., 2015). Most SMEs are often controlled by resource-constrained entrepreneurs and managers with limited contingency planning or foresight capabilities, making it difficult for such firms to deal with heightened levels of uncertainty (Brown et al., 1998). By contrast, some studies attest to the fact some astute SMEs can overcome adversity through their business acumen and firm-level innovation (Bamiatzi and Kirchmaier, 2014; Morgan et al., 2020). Of course, it should be borne in mind that not all SMEs have the same levels of resources and innovative competences. Very small so-called micro-sized SMEs employing less than 10 people are considerably different to larger medium-sized enterprises. This may manifest itself in more limited risk mitigation capabilities. Heightened uncertainty can also inhibit SMEs investing for the future, thereby preventing firms undertaking riskier growth-related activities such as innovation (Lee et al., 2015).

Overall, therefore the impact of uncertainty when faced with exogenous shocks is likely to vary significantly across different types of SMEs according to their size, strategic orientation and sectoral orientation. As a consequence, an investigation of the types of SMEs likely to be affected by Brexit, and how this is likely to affect future strategic intentions and decisions is a highly relevant exercise from both a conceptual focus on regional resilience and from a policy perspective.

Methodology

In response to calls for more multi-level approaches towards studying regional resilience (Korber and McNaughton, 2018), this research adopted a mixed methods approach involving both quantitative survey analysis and qualitative interviews with SMEs. This approach is recognized to be of significant value, particularly when research needs to be contextualized in wider phenomena (Molina-Azorín et al., 2012) or when there are interaction effects at play. Given longitudinal approaches are often need to monitor resilience over time (Bristow and Healy, 2020), this method enabled the collection of ‘baseline’ views on perceptions on the impact of Brexit via the survey and further exploration and triangulation of these views and emerging impacts two years later via interviews. 2 This complementarity is a key strength of mixed methods work (Molina-Azorín et al., 2012).

In terms of the survey, we utilised the Longitudinal Small Business Survey (LSBS) compiled by the UK Department for Business Energy and Industrial Strategy. The LSBS is one of the largest annual attitudinal surveys of SMEs undertaken in the UK, sampling approximately 10,000 firms. In the immediate aftermath of the referendum result in June 2016, a number of specific questions were added to the LSBS in order to gauge the nature and potential economic impact of Brexit on SMEs. This included specific questions such as whether entrepreneurs and/or small business managers perceived the UK’s exit from the EU as a major obstacle to the success of your business in general.

The data presented in this article are from the 2017 survey – the most recent year for which the complete LSBS data were available. While the data are over two years old, the results provide insights into the performance and challenges of Scotland’s SMEs since the Brexit vote. For the purposes of the present analysis, the larger UK-wide dataset mentioned above was further refined to the Scottish-based SMEs surveyed during 2017. In 2017, 1042 Scottish SMEs took part in the survey, of which 739 had employees. The LSBS data are weighted to ensure that the results are representative of the overall Scottish SME population. A series of statistical tests (informed by previous research on Brexit and uncertainty) were carried out on these largely categorical data in order to discover possible relationships between Brexit-related competitive issues and various firm-level metrics.

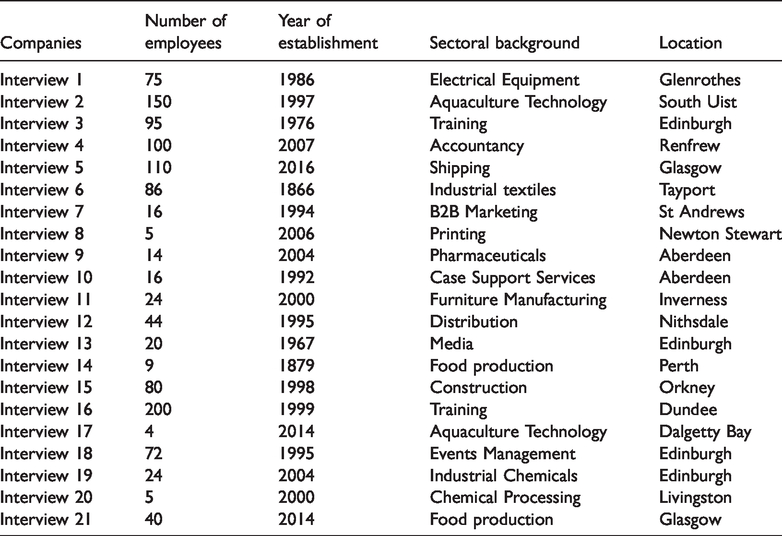

In terms of interviews, the researchers undertook 21 interviews with a wide and diverse cohort of Scottish SMEs (see Table 1). Qualitative interviews are particularly appropriate during times of intense economic and social change (e.g. Schoenberger, 1991), where complex issues require nuanced probing. The firms interviewed were randomly selected from a list of Scottish SMEs obtained from the commercial business database Financial Analysis Made Easy. The inclusion criteria were that participants had to be employers with 1 to 249 employees, registered in Scotland and actively trading in Scotland. In total, 189 firms were approached with 21 agreeing to be interviewed, giving a response rate of 11%. These firms operated in a very diverse range of different sectors and geographic locations, and were of various sizes, ages and varied ownership structures (see Table 1).

Details of SME informant interviewees.

Interviews were conducted from Spring to Autumn 2019, when political uncertainty about the Brexit process was at its peak due to the fraught nature of the negotiation process. The interviews were conducted with owner-managers and entrepreneurs; these typically lasted between 30 and 60 minutes. They were semi-structured to explore commonalities and differences (Patton, 1990) and primarily focused on Brexit-related concerns, the type of impacts detected and the role of policy support for SMEs. The thematic issues explored in the semi-structured interviews probed to see the types of firms most affected, the key concerns expressed by the interviewees and the operational impact on the SMEs examined. A significant amount of the interviews was used to probe their reactions to the increased uncertainty within their operations together with the nature of the adjustment strategies and organizational changes deployed by the SMEs to mitigate the changing environment. All interviews were recorded and transcribed immediately upon completion. The data were analysed based on an a priori coding framework developed from the regional resilience and uncertainty literatures, although a number of themes and codes emerged from the data analysis process (i.e. types of firms most affected). Each transcript was analysed independently by the researchers, before codes were compared and reassessed by the researchers in order to ensure analytical rigour (Miles and Huberman, 1994). While direct quotations are used to ensure transparency of collected data (Healy and Perry, 2000) and to allow the data to ‘let the data speak’ for itself (Easterby-Smith et al., 2006: 119), companies have been anonymised and any identifying information withheld. The direct quotes in the article are taken from a wide variety of the cohort interviewed.

Quantitative analysis

This section examines Scottish SMEs as a whole, utilizing the LSBS data described earlier. As a starting point, it was critical to ascertain how these SMEs viewed Brexit overall. To Scottish-based SMEs, the UK’s departure from the EU ranks only sixth in terms of competitive challenges, well behind other, commonly cited barriers such as market competition, taxation and other issues. We can see from Figure 1, that Brexit was viewed as competitive threat by slightly more Scottish SMEs than their counterparts in the rest of the UK. This may in part owe to the fact that voting patterns strongly diverged between Scotland and the rest of the UK during the Brexit referendum, with the former country much more strongly predisposed towards remaining in the EU (McHarg and Mitchell, 2017). 3 For the most part, Brexit was seen as one of many key competitive issues confronting SMEs.

Percentage of Scottish and rest of the UK SMEs indicating that Brexit was a firm-level competitive issue. Source: Department for Business, Innovation and Skills (2018).

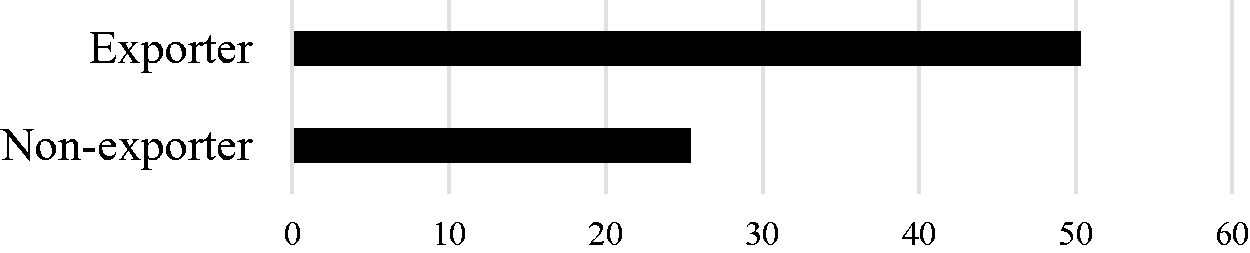

With this in mind, a majority of the ensuing analyses encompass the nearly 30% of Scottish SMEs (311 firms) that cited Brexit as a competitive issue. For this group of Scottish SMEs (and for a particular subset of these firms, to be detailed below), Brexit was a very salient concern. Figure 2 suggests that exporters viewed Brexit differently relative to non-exporters in terms of whether it posed a challenge to their firm, by a statistically significant margin of 50.3% to 25.4%, respectively (chi-square, p < 0.01). Again, this dovetails with the opaqueness about the future, and with a strong reluctance to engage internationally due to uncertainty about the international trade environment. International markets (especially new, untested markets) inevitably provide some degree of uncertainty, particularly when set against domestic customers. Indeed, the Brexit scenario and its incumbent uncertainty seem to pose a relevant threat to exporters. For these SMEs, the very possibility of increased barriers to EU markets increases the amount of perceived administrative or psychic distance between buyer and seller. 4

Is Brexit a competitive issue? Scottish SME exporters versus non-exporters (percentage of surveyed firms selecting). Source: Department for Business, Innovation and Skills (2018).

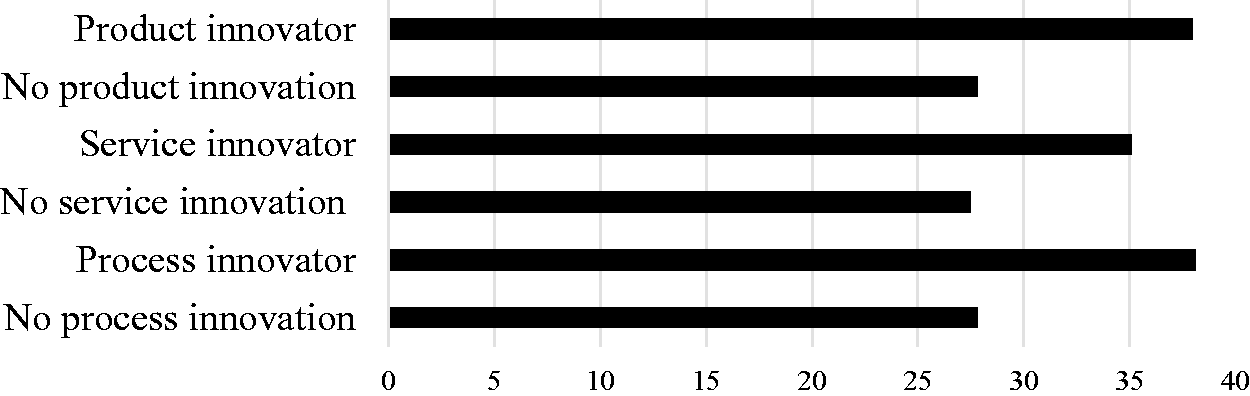

The theme of uncertainty surrounding Brexit follows in Figure 3, which provides a breakdown of three types of innovation (a new product, service, or process developed within the past three years) and whether these groups of firms viewed Brexit as an obstacle to their firm-level operations. In each case, there were significant differences between innovators and non-innovators. In terms of product innovation, the difference was 38.0% to 27.8% (chi-square, p < 0.01). With regard to service-oriented innovation, the difference was 35.1% to 27.5% (chi-square, p = 0.012). Finally, in terms of process innovation, the results were again significant by a margin of 38.1% to 27.8% (chi-square, p < 0.01). As with the case of the exporters, the data suggest Brexit was perceived as a significant competitive challenge for a particular subset of Scottish SMEs, most notably innovative firms. Importantly, these are often the types of ambitious and outward-looking firms that policymakers actively attempt to grow and nurture (Mason and Brown, 2013).

Is Brexit a competitive issue? Scottish SME innovators versus non-innovators* (percentage of surveyed firms citing Brexit as a competitive issue). *Introduced a product, service, or process innovation within the previous three years. Source: Department for Business, Innovation and Skills (2018).

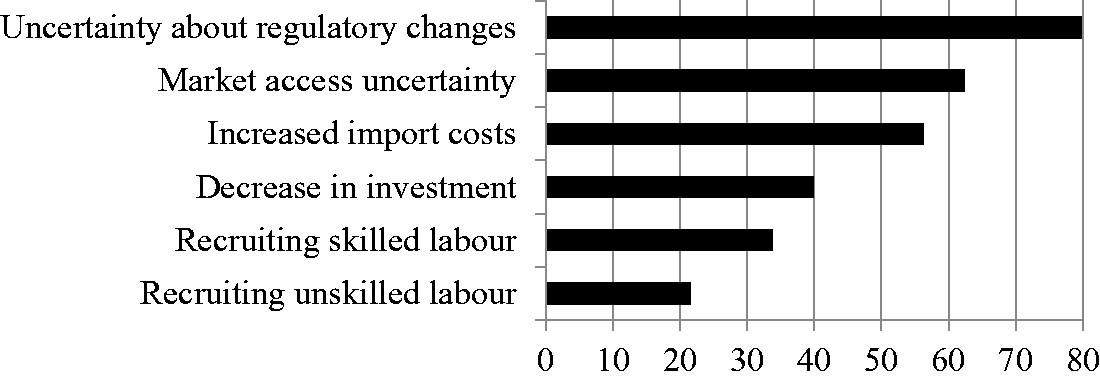

As seen above, Brexit impacts (or is perceived to impact) a certain type of firm. We now probe ‘why’ Brexit is perceived as a competitive concern. As shown in Figure 4, the top two Brexit-related concerns focus on uncertainty. Uncertainty is often cited as a reason firms are reluctant to explore new markets or engage in risk-taking business in general, especially for SMEs with limited resources (Bylund and McCaffrey, 2017). The Brexit referendum has undoubtedly introduced a large degree of uncertainty to firm-level plans and operations. The combination of uncertainty about a new regulatory environment, coupled with market uncertainty (i.e. will firms need to find new export destinations) provides considerable barriers for Scottish SMEs moving forward, potentially impacting strategic decisions and innovation. The possibility of increased import costs caused by new tariffs was also viewed as a concern by nearly 60% of Scottish SMEs.

Brexit-related challenges for Scottish SMEs (percentage of surveyed firms selecting). Source: Department for Business, Innovation and Skills (2018).

The remaining Brexit-related competitive issues concern the movements of goods, services, capital, or labour leading up to the UK’s withdrawal from the EU. But again, even these obstacles encompass some degree of uncertainty. For example, potentially higher input costs provide yet another obstacle for firms operating in cost-competitive environments. Additionally, a potential decrease in investment could have detrimental effects on SMEs, especially in terms of their future competitiveness in the marketplace. And while the labour-related issues (both unskilled and skilled) were selected by comparatively few of the surveyed firms, it remains a salient issue, especially if firms are to remain competitive in comparatively tight labour markets.

Whilst uncertainty generates concerns about current activities it equally mediates future-oriented plans. The data note that comparatively few Scottish SMEs see positive effects from the UK exiting the EU – a combined 5.5% of firms see any positive impacts from the referendum. By contrast, a full third of SMEs foresaw some sort of negative impact stemming from the UK’s departure from the EU viewing it as either very (or fairly) detrimental. Just under half of the surveyed SMEs were neutral with regard to Brexit. In essence, a third of the surveyed Scottish SMEs either viewed Brexit very negatively whilst a very small minority viewed it favourably.

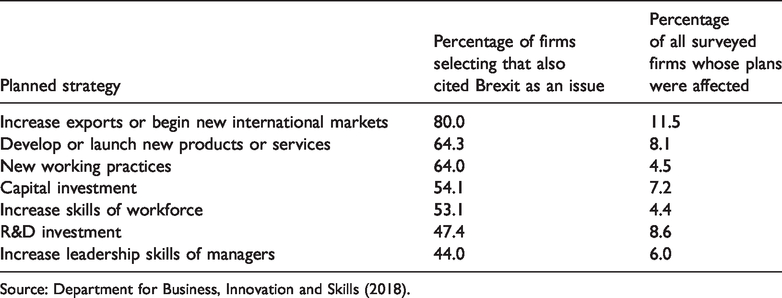

Table 2 provides a look at the ways in which Scottish SMEs perceived their plans to be impacted by Brexit. Note that a rather small percentage of all surveyed Scottish SMEs (typically less than 10%, see Table 2) were impacted in terms of their plans for exports, innovative practices and capital investment and so on. However, these proportions change markedly when one examines the group of Scottish SMEs that originally indicated that Brexit was a critical obstacle that could impact their operations. All of the plans were selected by a comparatively large percentage of firms in this subgroup. For a start, fully 80% of these firms estimated that their export expansion plans were influenced by Brexit. Once more, this ties into the role that uncertainty is playing in firm decision making. Within the Scottish context, this lends further support to earlier concerns over Scottish SMEs finding new (i.e. outside the EU) export markets post-Brexit (see Kalafsky and Brown, 2018). Firms appear to be holding back on export plans until they ascertain what the future trading landscape will entail.

Scottish SME business plans impacted by Brexit.

Source: Department for Business, Innovation and Skills (2018).

The next two plans that were mentioned by these SMEs concerned innovation in terms of products, services, or new processes. Again, the uncertainty surrounding the UK’s departure has caused this group of Scottish firms to hold back on their innovative plans. Importantly, Brexit also appears to have potentially negative effects on plans for capital investment and workforce training. Essentially, SMEs might refrain from longer-term investment strategies if there is a large degree of opaqueness about the trade and overall economic environment moving forward.

When taken together, the findings within this section lend strong support to previous literature (e.g. Ghosal and Ye, 2015) concerning the negative impacts of uncertainty on SME operations and performance. More specifically, the survey data intimates that innovative and export-oriented Scottish SMEs see Brexit as a major impediment to their business plans, corroborating previous evidence (Brown et al., 2019). These analyses in turn provide a context for the next section, which presents results from firm-level interviews providing an in-depth look at the micro-foundations of this endemic uncertainty.

Qualitative findings

The interviews with the 21 SMEs were undertaken to augment, probe and triangulate the aggregate survey analysis outlined above. In this regard the interviews uncovered a number of important aspects concerning the types of firms most affected, key Brexit-related concerns, the type of impacts detected and the role of policy support for SMEs.

Types of firms most affected

In line with the survey analysis, our interviews strongly suggest certain types of companies are more acutely and deleteriously affected by Brexit than others. Of the interviewed SMEs, roughly two-thirds were domestically oriented firms with little or no export or internationalisation activities. These firms are engaged in a wide variety of different service and manufacturing activities such as printing, food and drink production, logistics, training and events management. Overall, this cohort of SMEs was quite stable in terms of their growth, employment levels and export-intensity. In the main, this group of firms was relatively unconcerned with the potential impact of Brexit. While some did detect some potential pitfalls such as regulatory change and the devaluation of the pound, these were deemed as relatively insignificant: ‘at the moment, it is business as normal’. Another common trait across these organisations was a lack of any pre-planning to respond to Brexit or to enhance their resilience to the shock of Brexit. This relative insulation from the entire Brexit process was reflected by a number of participants, as per the following statements: ‘We have not seen any impacts on our organisation.’ ‘I don’t think we thought it [i.e. the referendum] would affect our growth at the stage. And in fact, it has not affected our growth at all.’ ‘We have not been adversely or positively affected by Brexit – but we’re just a bit bored with it.’ ‘The organisation has not done anything to prepare in any department.’ ‘Brexit has slowed us down, having to deal with more [internal] bureaucracy’ ‘The uncertainty is making it difficult to expand and grow in Europe, while at the same time, the company is also hesitant to compete in North America’ ‘Basically, we have all the steps in place, so really until a final decision and path is decided on, we’re at a point where there’s nothing more we can do until we know more’ ‘We had plans, but they did not incorporate the situation whereby a government could not come to any solution. While they were extending the uncertainty, our customers took that Therefore, while acute uncertainty is confronting firms from all sectoral backgrounds, it appears that those who are disproportionately negatively affected were often innovative and export-oriented SMEs. This corroborates our aggregate survey findings reported above. These firms were typically found in more high-tech oriented industries such as aquaculture, technical textiles, pharmaceuticals, biotech and chemicals who often rely more of wider external supply chains and non-domestic markets.

Key concerns

In terms of concerns expressed by the SMEs in relation to Brexit, the main issues identified across the entire population of firms related to the problem of uncertainty, especially in relation to the future regulatory environment. This remained the case for most SMEs irrespective of size, age, sector and level of export-orientation. Given the interviews were conducted almost three years after the Brexit referendum, many firms were deeply concerned about the lack of clarity about the future trade and regulatory environment. In many cases, this had negatively affected the SMEs to varying degrees, especially the longer the negotiations between the UK and the EU had gone on. The nature and opaqueness caused by pervasive uncertainty is reflected in the following statements: ‘Concerned – but concerned because you actually don’t know. We didn’t know what to be concerned about yet.’ ‘The indecisive nature of it and the fact that it is still unclear whether it will happen. I’m not certain it will even happen.’ ‘Fundamentally, nothing has changed. And since nothing has changed legally, the only thing that has changed is our customers thought they couldn’t get products from us, so they sourced elsewhere.’ ‘I suspect we will do less business in the EU than we planned to do. We will probably not seek out European business unless it comes to us. We’ll look for internal business or possibly tackle the US instead of Europe. Europe is no longer the easy option.’ ‘Until we know what the result is, I can’t make any plans.’ ‘At this point, until we know about tariffs and free trade information, there is very little we can do.’ ‘How am I supposed to know? How is anyone supposed to know? I don’t think anyone knows! How am I to prepare for Brexit when I don’t know what I am preparing for? I can’t. It is unknown what is going to happen. So how am I supposed to prepare for that?’ ‘Basically, we have all the steps in place, so really until a final decision and path is decided on, we’re at a point where there’s nothing more we can do until we know more.’

Operational impacts

The research discovered a range of different Brexit-related effects and impacts within the SMEs interviewed that were primarily designed to negate the problems caused by chronic Brexit-induced uncertainty. A number of the firms seemed to be focusing on cost reduction strategies to provide a buffer for any declines in sales caused by the uncertainty and turbulence. This approach was described as ‘battening down the hatches’ by one seasoned entrepreneur so that the firm could withstand the financial shock due to a decline in sales or the loss of key customers. This was very common across the two-thirds who were less internationally exposed. SMEs described themselves as: ‘wary of spending money at the moment, just in case we have to get through as short-term blip, if that makes sense.’ ‘reluctant to invest [into new computers], because I want to have the money available in the bank if it all goes wrong just after Brexit.’ ‘Yes – we have put on hold any product developments for the EU market, such as irrigation and pipe rehabilitation.’ ‘[We were] looking to invest into a capital expenditure specifically designed for products in Europe, but those sales have stalled, so the expense has been put on hold.’ ‘90% of the business is in the UK, but we are getting to the stage where there isn’t enough business in the UK not to expand overseas. And now we don’t know whether to expand into Europe or not.’ ‘In terms of exports, it has completely hampered our planned entry into other EU markets.’

Adjustment strategies

While the above operational impacts had been quite a reactive response to Brexit, some SMEs had been more proactive via various adjustment strategies. These strategies seemed to be firm specific and often pre-determined by the nature of their industry and sector they operated within. In some cases, this was fairly minor in that firms had taken on extra stock from suppliers from the EU. The devaluation of the pound following the referendum had encouraged some firms to consider sourcing more suppliers from the UK rather than overseas. Of greater strategic importance were the changes adopted by some companies which entailed SMEs seeking to break into new and different markets. For example, a conference organising business had started to target the US market to help reduce their reliance on the EU as Brexit had made Scotland a ‘harder sell’ to European customers.

In some SMEs, there had been discernible changes as a result of the experimentation of the founders/entrepreneurs. For example, in one fisheries business this had resulted in the change to their business model. 7 Due to Brexit-related concerns, the business now enables customers to lease rather than buy their products to reduce the sunk costs entailed for their customers. This arose due to uncertainty facing customers because of their dependence on the EU as the core marketplace for Scottish shellfish. In another company, an adjustment strategy deployed by the entrepreneur led them to begin a side-line property-related business to insulate themselves from any further collapse of their core business.

In a very small number of cases, some SMEs had undertaken quite major structural adjustments to help alleviate potential negative effects from Brexit. Despite being quite small companies with less than 50 employees, two of the firms had decided to undertake major organisational changes as a consequence of Brexit. In one instance, a maritime training provider who had become ‘a lot more concerned as time has gone on’ decided to seek out a joint venture (JV) with an Italian counterpart. The company was seeking to tender for a major contract from an Italian ferry provider and they were concerned that a lack of certainty around their accreditation status may undermine their chances of success. Therefore, the JV was seen as a means of mitigating any possible regulatory uncertainty caused by being out with the EU.

In another case, a small Scottish pharmaceutical company focused on the design and development of anti-infective disease treatments had opted to move their head office. According to their CEO ‘Brexit has had a major effect on us. We moved our key office to Dublin, Ireland’. This move was primarily done so that the firm could license their products under the jurisdiction of the EU pharmaceutical authorities. While such a step seems very adept at adjusting to the changing regulatory circumstances, it has nevertheless ‘had direct costs, effort and transfer of responsibilities’. So rather than being an expansive or growth-oriented move, this step taken was more linked to alleviating any turbulence caused by the UK withdrawal from the EU regulatory frameworks.

Policy issues

Linking back to the role of institutions and regional resilience, the final issue examined concerned the usefulness (or otherwise) of support received by the firms from various public and private institutions to help them overcome Brexit-induced uncertainty and upheaval. Across the population of SMEs examined, the vast majority had not proactively sought out advice from external public sector actors or private intermediaries. Most had relied on their own local non-specialist networks for advice (i.e. ‘so far, only our accountants’). The explanation for this was a belief that the problem itself lay with politicians and that ‘lack of clarity from the government’ was the key problem facing the firms. In most instances, firms had ‘not gone looking for help’. While some of the larger better-resourced SMEs had sought advice from various public and private sector intermediaries, the commonplace view was that the types of advice offered were ‘pretty poor’ and provided little in the way of practicable assistance: ‘We are part of the [Fife] Chamber of Commerce, so we have discussed it with them.’ ‘We spoke to our bank and financial institute, not to the trade bodies or lawyers.’ ‘I know the Customs do have a help line just now. They refer you to certain Customs notices that aren’t always effectual. The one document is 300 pages long, so you get a bit lost in them. To have somebody to listen to your questions and answer them would be helpful.’ ‘We are were happy with the advice, but until we know [the situation], there is very limited things we can do.’

Discussion and conclusions

This article makes a novel contribution to the literature on regional resilience by empirically examining the impact of Brexit on Scottish SMEs. While much of the regional resilience literature has traditionally focused on the macro-level nature of change to entire regional economies, this article highlights important firm-level behavioural impacts and changes in light of shocks such as Brexit. Given their crucial importance for the Scottish economy, SMEs therefore act as a powerful barometer and a strong proxy for measuring levels of regional resilience. Like others we strongly view that studying firms is a crucial mechanism for understanding regions and the use of informant interviews in particular enables us to make important connections between firm-level resilience and resilience at a regional-level (Markusen, 1994).

Another innovative aspect of this research was the mixed methods approach deployed. This enabled the research to examine ex ante the types of firms and their concerns identified after the referendum and then compliment this with an in-depth assessment of how the prolonged Brexit process had actually affected SMEs over subsequent years. This mixed-method approach lends itself well to properly understanding complex and contextualized issues (Molina-Azorín et al., 2012) such as Brexit-induced uncertainty which endures over the longer-term. Indeed, in some respects the Brexit referendum turned from an exogenous shock to a ‘slow-moving crisis’ which has still not fully resolved itself from a regulatory perspective, despite the fact that the UK has now formally left the EU. 9 Owing to this, there seems conceptual merit in viewing exogenous shocks such as Brexit as a ‘process’ rather than purely as ‘events’ (Williams et al., 2017).

The research also produced interesting empirical findings to augment our understanding about firm-level resilience. The work clearly shows how protracted uncertainty strongly challenges and undermines the resilience in some SMEs. Whilst two-thirds of the companies interviewed did not perceive Brexit to be a central or strategic problem, it is clear from our findings that certain types of SMEs (i.e. innovators, exporters and growth-oriented) were disproportionately concerned by Brexit, echoing other empirical studies (Brown et al., 2019). Our in-depth interviews strongly confirmed these same firms to be the most detrimentally affected in terms of job losses, reduced exports and lower innovation expenditure. In this sense, then, this work adds to the growing bodies of research about uncertainty and innovative SMEs (Doshi et al., 2018; Williams and Vorley, 2017). These findings are also of crucial importance for policy makers, as innovation is thought to play a key role in sustaining regional resilience in the longer-term (Evenhuis and Dawley, 2017).

In terms of the firm-level ‘agency’ explored during the interviews, while the minority of Scottish SMEs had managed to deploy adjustment mechanisms to mitigate these negative effects, many firms’ encountered major difficulties coping with this uncertain and turbulent environment. In the main, the default strategy was strategic inaction; such ‘wait and see’ approaches being a commonplace strategic response to uncertainty (Clarke and Liesch, 2017). While understandable, this lack of action is likely to make it more difficult for Scottish SMEs to respond to the fast changing regulatory landscape in the longer-term.

A number of SMEs adopted a focus on crude cost reduction strategies to mitigate against innate uncertainty. However, much of this was purely aimed at cutting back growth-enhancing activities like innovation, capital investment and R&D. In contrast to other studies (Bamiatzi and Kirchmaier, 2014), even growth-oriented and innovative Scottish SMEs demonstrated limited resilience in face of adversity, resulting in jobs being lost, expansion plans cut back, reduced exports and less innovation. Interestingly, only a very small minority enacted more radical and innovative structural adjustment strategies (e.g. JVs and headquarter relocation). Clearly, further work involving larger samples is needed to corroborate or refute the veracity of these findings.

Nevertheless, this research thus has clear and important policy implications. First, given that job losses in smaller companies tend be more enduring than from larger enterprises (Nyström, 2018), policymakers will have to make a concerted effort to help alleviate redundancies made by SMEs. This may require a proactive approach given few of the SMEs examined sought advice and support or engaged with relevant institutions. Second, it appears from our analysis that the types of assistance most beneficial to bolster resilience in SMEs are dedicated bespoke financial support packages, such as the Scottish Government’s Brexit Support Grant, enabling SMEs to devise their assistance accordingly. 10 To foster a culture of entrepreneurial adjustment in Scottish SMEs, there seems merit in expanding this programme to a wider range of potential beneficiaries, especially those most affected such as innovative and export-oriented SMEs. This type of proactive policy framework may be particularly relevant in peripheral regions and weaker entrepreneurial ecosystems lacking a strong entrepreneurial culture such as Scotland (Gherhes et al., 2018; Roundy et al., 2017).

Brexit has undoubtedly affected certain regions more than others and the impact of the Covid-19 crisis is likely to further magnify these marked spatial imbalances across the UK in the future (Harris et al., 2020). Echoing others (Billing et al., 2019; Brown et al., 2019), to adequately deal with these potent complex forces generating profound uncertainty, greater devolved responsibility across all UK regions and devolved administrations in policy areas such as immigration and industrial policy will arguably be needed in order to increase firm-level regional resilience in the longer-term.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.