Abstract

The ongoing Covid-19 crisis and recession represent one of the biggest shocks to the UK manufacturing ecosystem yet, and comes at a time when the ecosystem was already in a worrying situation after decades of deindustrialisation, a decade of austerity and an impending ‘Brexit’. The effects of this shock will also be unevenly felt due to the geography of the UK manufacturing ecosystem, amplifying the need for a successful response to ensure that places are not left (further) behind. This paper assesses the pre-Covid-19 ecosystem to ascertain the areas and industries likely to be particularly impacted by the crisis, and to understand existing issues. These issues are important to consider due to the implications for choosing strategies moving forward, for which two are appraised here. First, the reshoring of supply chains is considered in light of recent government comments, but difficulties in implementation may arise due to the highly fragmented nature of UK policy frameworks. Second, an acceleration of the ‘grand challenges’ approach is likely but limited by issues of connectivity in the ecosystem and small and medium-sized firm disengagement. We suggest that any strategy moving forward must strike a balance between such strategies

Keywords

Manufacturing in the Covid-19 recession

According to the World Bank (2020), the Covid-19 recession represents the worst global economic crisis since the Great Depression of the early 1930s and will cause a 7% fall in economic activity in the advanced industrialised countries this year. The economic shock and downturn are unique in terms of the breadth and steepness of the decline in activity across many sectors and, in terms of its highly synchronous nature, in local economies around the world. In the UK, the pandemic crisis has already had unprecedented and geographically uneven economic impacts through the direct effects of ill health and excess deaths, drastic contraction or cessation of economic activity during lockdown, reductions in the labour supply and consumption caused by the imposition of social distancing measures, and the ‘second round’ effects of falling incomes, increasing uncertainty and loss of confidence that have the potential to reduce growth in the future (Hughes et al., 2020). The severity of the recession stems from the combined effects of both demand and supply-side shocks. Generating profound disruptions for local economies reliant upon such activities, the sectoral effects of lockdown have been differentiated and felt most strongly by retail, hospitality, wholesale, transport and associated services, and construction. As a result, younger, lower paid, female and black and minority ethnic workers have been disproportionately affected and more likely to be furloughed (McKinsey and Company, 2020). It is also becoming clear that manufacturing industries are being severely impacted by the crisis and the ‘second round’ effects as well as the uncertain, stilted return of demand as governments struggle to re-open economies while managing the continued prevalence of Covid-19. In fact, the UK’s Office of Budget Responsibility (OBR, 2020) has predicted huge falls in manufacturing output and the OECD (2020) has concluded that the UK will be particularly negatively affected by the recession for reasons including the economy’s high dependence on transport, especially motor vehicles, manufacturing.

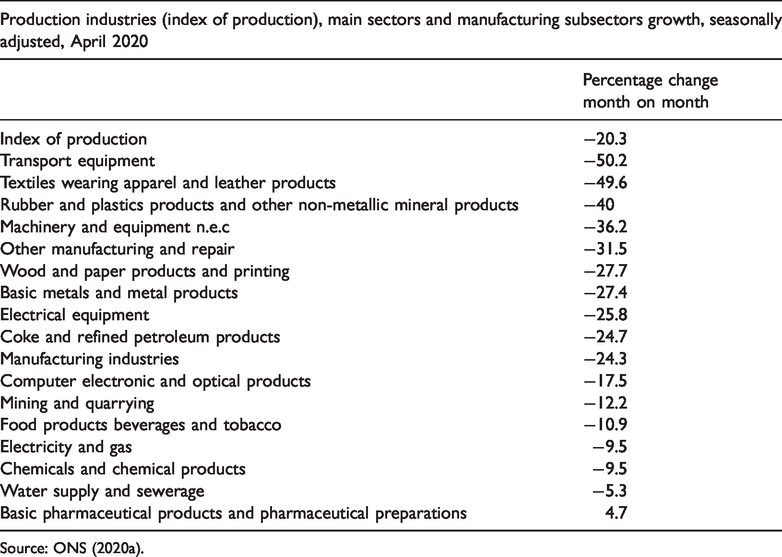

Further studies have begun to confirm these analyses and reveal the scale of the fall in UK manufacturing activity. The manufacturer’s trade association MakeUK’s Monitoring Reports have shown the dire impacts with over 70% of manufacturing firms reporting declines in sales and orders. At the height of the pandemic in April 2020, only 11.7% of manufacturing firms were operating at full capacity and 35.6% were operating at between zero and half capacity (MakeUK, 2020). Moreover, 25% of all manufacturing firms reported that they plan to make employees redundant in the six months between April and September 2020, and some had already done so. According to the UK’s Office for National Statistics (ONS), while services output fell 19% in April, this was exceeded by a 24.3% fall in output in manufacturing – by far the largest monthly fall since the series began over 50 years ago in 1968. The declines in output have been large and ranged across high and medium technology sectors such as computers, electronics and optics and automobiles, and lower technology manufacturing industries such as furniture and leather goods (Table 1). The largest falls were in motor vehicles where output fell by 90.3%, furniture (69.7%) and leather goods (59.2%). Unsurprisingly given the public health emergency, the only industry that went against trend and saw a small increase in output was pharmaceuticals, while the reduction in chemicals output is also smaller than in most sectors.

Changes in UK manufacturing output by sector.

Source: ONS (2020a).

These dramatic falls in production have been caused by a combination of several factors. First, the lockdown and effective closure of large swathes of the economy led to drastically reduced demand and precipitous declines in consumer spending for consumer durables such as automobiles, domestic appliances and furniture that are not readily and easily purchased on-line. The collapse in export sales triggered by severe and broadly simultaneous recessions in many countries, rolling around the world economy from China in early 2020, has compounded the collapse in demand. In addition, the almost total cessation of air travel has meant that many aircraft Original Equipment Manufacturers and tier 1 suppliers have cancelled orders, faced share price collapses, had their creditworthiness and debt downgraded and cut their workforces. The UK based aero-engine producer Rolls-Royce, for example, is reducing its workforce by 9000 this year; 6000 advanced manufacturing jobs will be lost in the UK and many of these will be at sites in Derby in the East Midlands region of England and Inchinnan in Scotland’s Central Belt (Hollinger and Georgiadis, 2020). In addition, many manufacturing production operations rely on physical proximity and fast-paced teamworking which have been severely disrupted by social distancing measures. Complying with this shifting guidance has forced manufacturers to reorganise their processes with negative impacts on their efficiency and productivity. The negative effects of the demand shock and reorganised activities have been compounded by the reliance of many medium and high-technology manufacturing sectors on globalised supply chains. Bottlenecks in these supply networks, especially those based in China, have created shortages, price increases and delays in component supplies. As a result, it appears likely that the most adversely affected manufacturing sectors will be those most exposed to internationalised supply chains and that are labour and export intensive (ONS, 2020b).

The combined negative effects of the drop in output have been visible in automobiles, transport equipment, especially civil aerospace, and in machinery and mechanical equipment. A key problem for the UK economy and for its national and local industrial strategies in particular is that many of the core ‘flagship’ parts of the country’s advanced or high-value manufacturing, including aerospace, transport equipment, computers, electronics and optics, are being severely impacted by the recession. Bailey and Rajic (2020) show that just seven manufacturing subsectors (air and spacecraft; automobiles; pharmaceuticals; computers, electronic and optics; machinery and equipment; and fabricated metal products) accounted for half of total UK manufacturing output in 2018. The recent Confederation of British Industry (2020) business association’s survey of manufacturing firms found that output fell by 57% in the three months to June 2020, driven by falls in the motor vehicles and transport equipment, mechanical engineering and metal products sub-sectors. As the Covid-19 recession unfolds amidst the easing of lockdown restrictions and planning for economic recovery, it is clear that manufacturing is at the centre of the economic storm.

Regional and local vulnerability to manufacturing decline

This severe downturn in many manufacturing industries appears to undermine hopes that the UK can use industrial and innovation policies to revitalise manufacturing and sectorally rebalance the economy away from financial services. It also raises profound questions for the national government’s ambition to ‘level up’ the economy geographically by regenerating the so-called ‘left behind’ local economies in cities and towns across the country. The uneven local and regional outcomes of the current recession are, of course, still unclear and in the making. Past recessions suggest that these spatial outcomes are rarely as expected and predicted and, as such, provide poor guides to policy responses in the current circumstances (Martin and Gardiner, 2019; Overman, 2020). What is clear is that lower paid and less skilled groups in already weaker local economies across the UK are likely to prove more vulnerable in the medium and longer term. Such groups suffer more from the enduring scarring effects of economic downturns and the historically embedded structural weaknesses in such places will be exacerbated by this recession (Centre for Progressive Policy, 2020). There are limits to using sectoral composition to predict the outcomes of recession and past experience demonstrates that the growth dynamics, skill levels and occupational and task specialisations have mattered more than sectoral structure (Martin and Gardiner, 2019, 2020; Martin et al., 2016). Given increasingly significant geographical variations and differences on the impacts of the recession within industries and sectors, there are many limits on the degree to which sectoral outcomes can be translated directly into impacts on local and regional economies. Those places that are initially hit hardest may not be those that are most adversely affected over the long run as this depends on their recovery and resilience (Centre for Progressive Policy, 2020; Martin et al., 2016). Nevertheless, as the emergent data reveal, there is growing evidence that certain advanced and other manufacturing industries are being particularly strongly impacted by the recession and some local areas are much more vulnerable to a long-term decline in these sectors. The Centre for Progressive Policy (2020) applied the OBR’s estimates of broad sector declines in output to the composition of local economies. It found that local authorities in the Midlands and North West, such as Pendle, South Derbyshire, Stratford-upon-Avon and Corby, are likely to be most negatively affected as they are highly dependent on manufacturing and also more reliant on wholesale and retail activities. In their analysis, 16 of the 20 worst affected areas are located in the traditional manufacturing heartlands of the North East and Midlands. Other reports have concluded that consumer durables manufacturing is being most negatively affected. Thoung et al. (2020) map the dependence of local authorities on these sectors and reveal that 20 local authority districts have more than 10% of their total Gross Value Added in these sectors. These include many areas in the West Midlands, as well as South Derbyshire, Sunderland, Bridgend, Knowsley, Barking and Dagenham, Crawley and Hastings.

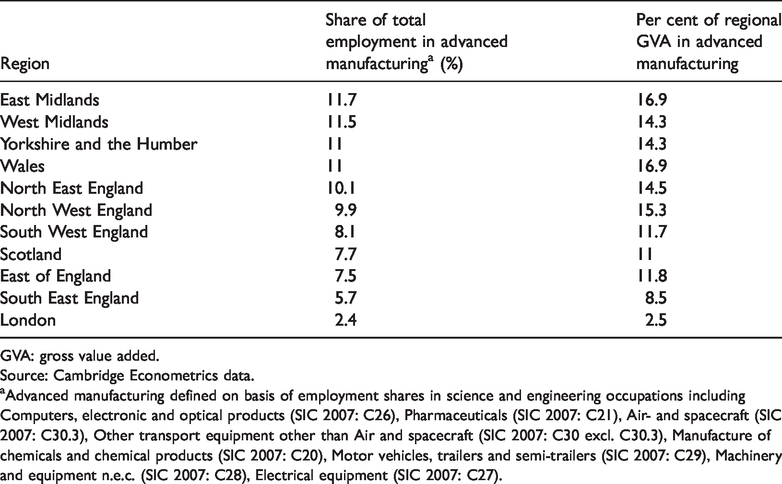

The geographical patterns of dependence on different manufacturing industries support the prediction that local economies in the North and Midlands may be more adversely affected by the pandemic recession, particularly because of the spatial concentration and localised nature of automobile and aerospace manufacturing. Table 2 shows regional employment shares in advanced manufacturing industries and the dependence of regional economies on these sectors. Regional consequences will, at least partly, be shaped by which industries are hardest hit. A severe contraction in automobiles is likely to have its worst outcomes in West and East Midlands. A decline in aerospace will impact strongly on the East Midlands and South West as these are more reliant on civil aerospace than the North West, which is more specialised in defence-related activities. However, contractions in electrical equipment and mechanical sectors will have a more geographically diffuse impact as these are more dispersed across the regions. Our research for an ESRC-funded project on manufacturing renaissance in industrial regions in the UK has found that those parts of advanced manufacturing based on engineering-related knowledge and skills have grown more in traditional industrial regions, such as the North, Midlands and Scotland, than other advanced manufacturing industries that rely more on analytical knowledge and science-based innovation (Sunley et al., 2020). As the analysis here demonstrates, however, these mechanical and engineering-related manufacturing industries look likely to be the most hurt by the Covid-19 recession. Moreover, the small growth in pharmaceuticals may not provide much relief to manufacturing regions in the North and Midlands. Over the past two decades pharmaceutical manufacture has declined strongly in areas in the North and Midlands as production has been outsourced and offshored and R&D has consolidated in a smaller number of innovation systems around life-science and biomedical institutions (Gautam and Pan, 2016). Former production sites have been converted into innovation parks and incubators such as Alderley Park, Nottingham BioCity and Charnwood campus in the North West and East Midlands. Any continued upturn in pharmaceuticals production might well benefit parts of the North West, especially Cheshire, but it is unlikely to make a significant wider contribution to ‘levelling up’ between local and regional economies across the country. While the geographical outcomes of manufacturing contractions cannot be predicted with much certainty, it is clear that the recession in these manufacturing industries is making the challenge of ‘levelling up’ even harder. It would therefore be prudent to try to support these industries in order to promote economic resilience and recovery in the most affected areas. Policy also needs to pay particular attention to the difficulties of lower paid and less skilled groups in those areas where manufacturing contractions prove to be deep and persistent. In the next section, we turn to the issues surrounding whether the UK has an effective local policy and institutional system that can respond to this intensified challenge.

The geography of advanced manufacturing by UK region, 2015.

GVA: gross value added.

Source: Cambridge Econometrics data.

aAdvanced manufacturing defined on basis of employment shares in science and engineering occupations including Computers, electronic and optical products (SIC 2007: C26), Pharmaceuticals (SIC 2007: C21), Air- and spacecraft (SIC 2007: C30.3), Other transport equipment other than Air and spacecraft (SIC 2007: C30 excl. C30.3), Manufacture of chemicals and chemical products (SIC 2007: C20), Motor vehicles, trailers and semi-trailers (SIC 2007: C29), Machinery and equipment n.e.c. (SIC 2007: C28), Electrical equipment (SIC 2007: C27).

The UK manufacturing ‘ecosystem’ pre-Covid-19

The previous sections have detailed the uneven geography and performance of the UK manufacturing ecosystem, highlighting its frailty and the uneven effects that the Covid-19 recession is having. However, before considering possible strategies that could help manufacturing recover and build resilience to future disruptive change, it is worth understanding existing characteristics and problems with the UK manufacturing ecosystem and its capacity for such strategies.

With the abolition of the nine regional development agencies (RDAs) in 2012 and the introduction of 38 local enterprise partnerships (LEPs), the economic development policy framework in England has become increasingly localised and fragmented. The aim was to involve business and local public sector partners to identify and resolve local issues to ‘unlock’ local growth. However, a recent progress review noted concerns over both their performance and fundamental capacity to deliver the complex projects required for local economic growth (House of Commons Committee of Public Accounts, 2019). While LEPs offer the potential to resolve particular local issues, several disadvantages can be identified in terms of their support for manufacturing. Local variations in policies and programmes have created a geographically uneven ‘postcode lottery’ in terms of support for firms. The churn of sub-national development organisations and lack of institutional memory has led to new organisations commissioning reports and re-considering strategies and policies that rehearse and repeat earlier efforts, with few problems actually resolved. Fundamentally, in an era of austerity, LEPs have been underfunded; the LEPs in a region typically receive less in total than the prior RDA, and much funding has been provided in disconnected, conditional and temporary initiatives (Industrial Communities Alliance, 2020). In our research, aerospace, electronic and automotive manufacturing firms reminisced about the regional scale activities initiated by RDAs, and expressed the view that their voices were heard to a greater degree by these organisations. Interestingly, these complaints are less frequent in Scotland where a different and more Scotland-wide and regionalised rather than localised structure has been put in place.

This shift towards local economic governance in England has also seen a reduction in national organisations and support, such as the Manufacturing Advisory Service, which was discontinued and withdrawn in 2015. The push towards localised policy intervention has created issues in supporting supply chains, which typically connect and stretch beyond local economies, as the capacity for cross-regional partnerships has been diminished. As a result, regional sectoral bodies have emerged out of the dissolution of RDAs, such as the Northwest Aerospace Alliance or the Midlands Automotive Alliance, in attempts to fill the gaps in strategy, policy and support and to help orchestrate manufacturing supply chains within and between regions. However, there are no attempts at organising supply chains at a UK-wide scale, making tackling gaps and limitations within industry supply chains particularly difficult. Furthermore, these industry alliances are not government funded and have to rely on private backing and the provision of services on a commercial basis, limiting their capacity for change and ability to pursue longer-term, higher risk/higher reward-type innovation-oriented activities.

The range of innovation centres that have emerged across the UK since 2010 with a remit to create more ‘translational infrastructure’ between universities and industry is certainly a strength (Hauser, 2010). Spread across the UK, these centres offer space and resources for firms to experiment with R&D, generally around key emerging technologies. The nine Catapult centres tackle issues such as medicines discovery, offshore renewable energy, satellite applications and energy systems. Some Catapults, such as the High Value Manufacturing Catapult, have specialised further with seven focused centres for Composites, Nuclear or Advanced Forming, among others. There are also other Enterprise Zones across the UK, such as HORIBA-MIRA, which offers a leading site for R&D in the automotive industry. These centres are rooted in local areas, making them key components in the ‘levelling-up’ of such areas, but have national remits and partnerships. However, despite the significant ongoing investment of over £1 billion, the outcomes have been uneven and critiques are rife. Many manufacturing SMEs see the centres as expensive and unwelcoming, even describing them as ‘Tumbleweed centres’ due to their under-utilisation (Academic, authors’ interview, 2020). Some have been found to be ineffectively managed and ‘overwhelmingly reliant on public funding’ (EY, 2017: 12), and our respondents have argued that they are struggling to commercialise research.

Indeed, it is perhaps because of this focus on innovation centres that respondents in our research note the disconnected nature of the UK’s advanced manufacturing ecosystem. The sheer number of these early stage R&D-focused centres means that early Technology Readiness Levels (TRLs) (i.e. research that is not close to market applications) are well catered for, to the extent that these centres are widely considered to have already saturated some research fields despite the planned addition of further centres. However, this imbalanced focus has opened up gaps at other TRL levels where firms lack support. Several key areas lacking in support and poor co-ordination throughout the manufacturing ecosystem mean that the innovation centres often overlap in their service provision. A similar problem is that under-resourced LEPs can often only afford to provide generalised business support and do not provide the specific and specialist support necessary as manufacturing firms develop and grow. University research centres in the UK do not have an especially strong record of supporting manufacturing. Regional ecosystems, therefore, need a better balance between, and combination of, cross-sector, new-technology missions or ‘grand challenges’, with demand-led research focused on innovation that can be diffused and absorbed in specific sectors, places and supply chains. As Brown (forthcoming) argues, the key problem with mission-oriented projects is that they pay inadequate attention to the contexts of local and regional demand, and other types of diffusion-oriented innovation policy are often more appropriate to raising the productivity and competitiveness of SMEs especially in traditional industrial regions.

Such limitations in the current institutional set-up and policy mix for manufacturing mean that many SMEs feel unsupported. They find themselves priced out of innovation centres and often feel overlooked by LEPs. Even more favourable policies like R&D tax credits are inefficient because they still require the SME to cover the up-front costs and claim them back, leading to cash-flow issues. Our research finds that the absorptive capacity of many SMEs is a key constraint so that proximity to innovative firms and centres is not enough to facilitate the diffusion of new practices and technologies (Harris et al., 2019). Pervasive across the UK is a struggle to get SMEs prepared for the fourth industrial revolution – known as ‘Industry 4.0’ – based on ‘smart’ internet-linked factories, autonomous systems and Artificial Intelligence and machine learning, especially since ‘some of the companies we’re dealing with are at 2.0!’ (Policy manager, Scottish government, authors’ interview, 2020). There are bright spots here, however. Scottish Enterprise and the Scottish Manufacturing Advisory Service run programmes that are laying the groundwork for Industry 4.0, LEPs in the Northwest have been piloting the successful Made Smarter programme which has been adopted in other areas, and some individual LEPs like Liverpool City Region have their own successful programmes aimed at upskilling SMEs (LCR 4.0). However, while these success stories are clearly positive, they also reflect the geographically uneven, underdeveloped and patchwork nature of current initiatives to support manufacturing in local economies across the UK.

The move to localism and decentralisation of powers and resources to combined authorities in England could potentially be particularly useful in tackling skills shortages. Firms are united in their concerns about the ageing of the manufacturing workforce, the lack of upskilling and training programmes, the concentration and falling number of apprenticeships under the UK Apprenticeship Levy, and the massive challenge of changing perceptions about manufacturing and making it attractive as a career option for men and women of the next generation. In tackling such longstanding and difficult issues, however, there has been an absence of local tailoring of policy regarding skills development. The LEPs in England currently have no powers and resources for this and, while the devolution of the adult education budgets is a step in the right direction, it is only to the mayoral combined authorities to date. More promising is the Scotland-wide approach of Skills Development Scotland. Similarly, there are huge disparities in infrastructure that cannot be tackled through more decentralised structures and need more integration and co-ordination with national level investments and networks. While our respondents broadly welcome the new high-speed rail network being planned between London and Birmingham (HS2), they highlight the need for the development of East–West infrastructure as travelling across the Midlands or the North is already slower than reaching London. It is not just transport infrastructure that is lacking; firms also bemoaned the lack of suitable production space built in the last decade, as construction has been preoccupied with unsuitable call centre-style office facilities.

In sum, a decade of austerity and persistent deindustrialisation has generated a fragmented and disconnected manufacturing ecosystem that had performed admirably in spite of infrastructure imbalances, inadequate skills development and funding shortages, but now faces the daunting dual challenge of the unknown disruptions of ‘Brexit’ beyond the current transition period at the end of 2020 and the possibly lasting effects of the Covid-19 recession.

Strategies post-Covid-19

Given the characteristics and issues with the UK manufacturing ecosystem, what can be done to organise a post-Covid-19 response and wider recovery? Of course, the UK’s national Coronavirus Job Retention Scheme and packages of loans have already ameliorated and cushioned the immediate effects of the economic shock on manufacturing firms. Many large manufacturers, such as BASF, Bayer and Nissan, have taken out the largest loans by value under these schemes. However, there is still considerable uncertainty about whether the current government is prepared to embrace a more interventionist and supportive national and local industrial policy, given the administration’s apparent scepticism towards the previous administration’s earlier attempts to develop an industrial strategy (Westwood, 2020). Yet, it appears that the case for such a policy has never been stronger, not only to help manufacturing recover from the recession and support ‘levelling up’ across the country, but also to drive and support the de-carbonisation of industries to hit the Net Carbon Zero 2050 target and accelerate the adoption and adaptation to Industry 4.0 and new digital practices. Successive UK governments have, of course, steered away from ‘picking winners’ and supporting key firms since the 1970s. However, new rationales have been developed for industrial policy, outlining and encouraging changed roles for government in relation to key and strategic firms and industries (Aiginger and Rodrik, 2020). Such thinking will be especially important and more feasible for the UK after the end of the Brexit transition (Coman, 2020). Given the parlous financial condition and high indebtedness of some large manufacturing firms, the UK government has formulated ‘Project Birch’ to enable the state to take equity stakes in strategically important businesses facing acute financial difficulties or provide further major loans to ensure the survival of key firms, especially in economically vulnerable places. Given the need to align interventions to achieve decarbonisation, levelling up and Industry 4.0, it is critical that any such support is conditional on the fulfilment of programmes that respond to these imperatives. As yet, however, much remains unclear about the direction of industrial strategy.

Amidst the USA’s ongoing trade war with China and the problems experienced in the supply of Personal Protective Equipment and medical kit during the pandemic, the idea of reshoring supply chains has understandably gained much popularity. Some have even argued that ‘reshoring’ in medical supply chains could be used as more general model for a post-pandemic industrial strategy (Westwood, 2020). Such interest, of course, has been driven by increasing geopolitical tensions with China. The Foreign secretary Dominic Raab stated in April that there will be no return to ‘business as usual’ with China, and outlined ‘Project Defend’ which seeks to ensure security of critical supply chains. It appears probable, then, that at least some reshoring of medical and pharma supply chains will be attempted. Whether a wider reshoring in other advanced manufacturing industries is desirable and feasible is not clear. There are strong limits to the degree and potential of reshoring in the UK (Bailey and DePropis, 2014). Analyses of supply chain management argue that domestic or shorter supply chains do not necessarily create robustness in moments of crisis (Miroudot, 2020), while there is currently no evidence that complex supply chains have been more impacted by Covid-19. Indeed, some empirical studies have indicated that more centralised supply chains would have fared worse (Bonadio et al., 2020).

The shift to local strategy making and growth policy based on LEP geographies in England and regional partnerships in Scotland also raises questions about coherence and co-ordination in any support for manufacturing supply chains. There are already doubts that LEPs in their current form have the ability to co-ordinate complex activities (EY, 2017; Hauser, 2014), and with each LEP tasked with looking out for their specific locality, competitive and highly selective place-based deals may well inhibit progress and exacerbate geographical inequalities (Tomaney and Pike, 2020). However, there are examples of LEPs and regional industry organisations working with one another effectively in pan-regional alliances. These types of partnerships can bear fruit in the future, particularly if better funded (EY, 2017; Hauser, 2014). The attraction of foreign direct investors, especially highly capable suppliers, and the development of existing supply chains will both require a better co-ordinated and multi-scalar industrial strategy with appropriate measures at local, regional and national scales. Neither only top-down nor bottom-up approaches can achieve the changes required in isolation, a more co-ordinated and integrated approach across the different levels and institutions is required.

A second and more probable direction for national and local industrial strategies will be an acceleration of the current ‘grand challenges’ approach on the grounds that this turbulent period offers the perfect opportunity for disruptive technological advantages and experimentation and risk-taking in public policy. For instance, firms in the automotive industry agree electrification is likely to be accelerated because of the Covid-19 recession, while Rolls-Royce has submitted plans, expected to be fast-tracked by the government, for a fleet of mini-nuclear reactors (GWPF, 2020). In the current context of deep recession and uncertain economic recovery, incentives to gain early mover advantage in such emerging technologies appear even stronger. The UK is already well equipped for a ‘grand-challenges’ acceleration given the investments made into the various research centres, such as the Nuclear Advanced Manufacturing Research Centre in Sheffield, the Energy Innovation Centre in Warwick, and the National Composites Centre or the Advanced Forming Research Centre. However, there is a need to decentralise R&D and innovation investment to make it a meaningful part of the government’s ‘levelling up’ agenda in policy terms (Oxford Economics, 2020). While the aim of these research centres was to provide the translational infrastructure between universities and firms, the issue remains of their connectivity with the rest of the ecosystem, in terms of SMEs and the commercialisation of new technologies. For the UK to gain a competitive advantage in emerging technologies, it needs a nationally and locally integrated and co-ordinated ecosystem that facilitates not just the experimentation between SMEs and universities in innovation centres, but ensures the outputs can be successfully commercialised and supports the growth of these firms until they are financially viable. A practical strategy to deliver on the ‘grand challenges’ would place innovative manufacturing SMEs at its heart, which requires a significant shift away from the current situation where many such SMEs feel somewhat marginal. The Scottish version of a mission-oriented ‘grand challenge’-focused industrial strategy has been criticised for lacking a cogent and detailed blueprint for how a large sum of earmarked money can be appropriately spent (Brown, forthcoming). Such findings suggest that such moves have yet fully to grapple with the difficult issues of building and sustaining start-ups and commercialisation and diffusion of ideas.

The discussion across these possible scenarios highlights not just the difficulty of following either individual strategy, but also the tensions of addressing both horizontal/new technology sectoral/supply chain and challenge issues. While the existing manufacturing ecosystem seems set up to engage with the current horizontal/new technology challenges, especially if Horizon 2020 funding is to be fully replaced in the post-Brexit context, we would argue that this is only half the story. If such a strategy is to bear fruit then it also requires a stronger attempt to support SME innovation, adaptation and capabilities (see also Bailey and Rajic, 2020). It is a pity that this second strategy focused on adaptation and support of existing SMEs has so far been weakly developed because it is precisely adaptation and digitisation in manufacturing SMEs that may be key to their Covid-19 response and future resilience (Meffert et al., 2020). It is unlikely that this second half can be delivered without a stronger set of local and regional institutions with more policy discretion and funding aimed at providing tailored support for manufacturing firms. There have been many policy recommendations for how this could be achieved. Among the most pressing are fuller and locally tailored training and apprenticeship provision; a range of financial schemes targeted at different stages of firm growth; a set of subsidised and long-term loans to encourage digitisation; and a return to digital, technical diffusion and advisory support services through supply chains. All of these initiatives have some merit but will need to embedded in, delivered and co-ordinated by a stronger and more comprehensive local, regional and national institutional framework in order to ensure that the future recovery is also a period of adaptation, upgrading and renewal for manufacturing in the UK.

Footnotes

Acknowledgements

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the ESRC project ‘Manufacturing renaissance in industrial regions? Investigating the potential of advanced manufacturing for sectoral and spatial rebalancing’ (ES/P003923/1).